Bootstrapping Empirical Processes of Cluster Functionals with Application to Extremograms

Holger Drees111University of Hamburg, Department of Mathematics,

SPST, Bundesstr. 55, 20146 Hamburg, Germany;

email: drees@math.uni-hamburg.de

Abstract

In the extreme value analysis of time series, not only the tail behavior is of interest, but also the serial dependence plays a crucial role. Drees and Rootzén (2010) established limit theorems for a general class of empirical processes of so-called cluster functionals which can be used to analyse various aspects of the extreme value behavior of mixing time series. However, usually the limit distribution is too complex to enable a direct construction of confidence regions. Therefore, we suggest a multiplier block bootstrap analog to the empirical processes of cluster functionals. It is shown that under virtually the same conditions as used by Drees and Rootzén (2010), conditionally on the data, the bootstrap processes converge to the same limit distribution. These general results are applied to construct confidence regions for the empirical extremogram introduced by Davis and Mikosch (2009). In a simulation study, the confidence intervals constructed by our multiplier block bootstrap approach compare favorably to the stationary bootstrap proposed by Davis et al. (2012).

222Keywords and phrases: bootstrap, cluster

functionals, clustering

of extremes, confidence regions, extremogram, serial dependence, uniform central limit theorem.

AMS 2010 Classification: Primary 62G32; Secondary 60G70, 60F17.

1 Introduction

Time series of observations in environmetrics, (financial) risk

management and other fields often exhibit a non-negligible serial

dependence between extremes. For example, stable areas of low (or

high) pressure may lead to consecutive days of high precipitation

(or high temperature). Likewise, large losses to a financial

investment tend to occur in clusters.

The statistical analysis of the serial dependence structure between

extreme observations is still a challenging task. Yet even if one is

only interested in marginal parameters, like extreme quantiles, it

is crucial to take into account the serial dependence when

assessing the estimation error; see, e.g., Drees (2003) for a

simulation study which demonstrates how misleading confidence

intervals may be if the serial dependence is ignored.

In most applications, no parametric time series model for the

extremal behavior suggests itself. Hence, one should resort to

non-parametric procedures to avoid the risk of an unquantifiable,

but potentially large modeling error. In this context, a general

class of empirical processes that can capture a wide range of

different aspects of the extremal behavior of time series prove a

powerful tool.

To be more concrete, assume that a stationary time series

with values in is observed, from

which we construct blocks

(1.1)

of “standardized extreme observations” , . A

typical choice for univariate time series is

(1.2)

for suitable normalizing constants and .

Later on, we will use a different notion of extreme

observation in our application to the analysis of the extremogram, for

a multivariate time series.

Denote by the set of vectors of

arbitrary length with components in , which is equipped with the

-field induced by

the Borel--fields on , . Let be a

family of so-called cluster functionals, i.e. functions

such that and

for all

where the numbers of coordinates equal

to 0 in the beginning and in the end of the argument on the

right-hand side can be arbitrary. Thus the value of the cluster

functional depends only on the core of the argument, which is

the smallest subvector of consecutive coordinates that contains all

non-zero values (resp. it equals 0 if the argument only consists of

zeros). Then, the pertaining empirical process of cluster

functionals is defined by

(1.3)

with . Drees and Rootzén (2010) established

sufficient conditions for to converge to a Gaussian process in

the space of bounded functions on . The

following theorem summarizes their main results; the conditions are

recalled in the appendix.

1.1 Theorem

(i)

If the conditions (B1), (B2) and (C1)–(C3) are fulfilled,

the finite-dimensional marginal distributions (fidis) of the

empirical process converge to the pertaining fidis of a

Gaussian process with covariance function (defined in

(C3)).

(ii)

Under the conditions (B1), (B2) and (D1)–(D4) the

empirical process is asymptotically tight in

. If, in addition, the conditions (C1)–(C3)

are met, then weakly converges to .

(iii)

If the assumptions (B1), (B2), (D1), (D2’), (D3) and (D5)

are satisfied and, in addition, (D6) (or the more restrictive

condition (D6’)) holds, then is asymptotically

equicontinuous. Hence, weakly converges to in

if also the conditions (C1)–(C3) hold.

For certain types of families of cluster functionals, Drees and

Rootzén (2010) also gave sets of conditions that are sufficient for

to converge and easier to verify than the

abstract conditions listed in the appendix.

We will demonstrate their usefulness by improving on limit results

on an empirical version of the so-called extremogram introduced by

Davis and Mikosch (2009) in the framework of time series with

regularly varying marginals. To be more precise, assume that

is a stationary -valued time series such that

for all the vector is regularly

varying. Recall that a random vector is regularly varying

if there exists a non-null measure on

such that

for all -continuity sets that are bounded away from

the origin 0. Note that, while this definition of regular variation

does not depend on the choice of the norm , the specific

form of the limiting measure does. In any case, the limiting measure is homogeneous of order for some , the so-called index of regular variation.

Then, with denoting the quantile function of

and , to each

lag there exists a measure on

such that

(1.4)

for all -continuity sets bounded away from the origin.

In particular, for all bounded away from 0 such that

and

one has

Davis and Mikosch (2009) called (as a function of )

the extremogram of (pertaining to ). It

is worth mentioning that the extremogram is closely related to the

concept of tail processes introduced by Basrak and Segers (2008).

Based on the observations , they proposed the

following empirical counterpart as an estimator of :

(1.5)

Here is a sequence that tends to at a slower rate

than so that at a slower rate than , and

thus the number of extreme observations used for estimation tends to

. Under suitable conditions, is asymptotically normal (see

Davis and Mikosch, 2009, Corollary 3.4).

This result has two serious drawbacks. First, usually, the

normalizing constants are unknown and must hence be replaced

with an empirical counterpart, like, e.g., the

largest observed norm:

(1.6)

It is not obvious whether this modification influences the

asymptotic behavior of the empirical extremogram.

Secondly, the extremogram for a fixed pair of sets and

conveys limited information on the extremal dependence structure, in

particular in a multivariate setting, i.e. if . To get a

fuller picture, one should consider the extremogram for a whole

family of sets simultaneously. For example, in the case , Drees et al. (2015) considered rays and for all simultaneously. However, the techniques used by Davis

and Mikosch (2009) are not applicable to infinite families of sets.

We will show that both problems can be neatly solved using the

theory of empirical processes of cluster functionals. Indeed, if the

families of sets and are suitably chosen and the bias of

is asymptotically negligible, then the

asymptotic normality of the empirical extremogram with estimated

normalizing sequence follows immediately.

If one wants to construct confidence regions using this limit

theorem, then estimators of the limiting covariance structure are

needed. Since the direct estimation does not look promising, Davis

et al. (2012) proposed to use a so-called stationary bootstrap

instead. Here we follow a somewhat different approach. First, in the

general setting considered by Drees and Rootzén (2010), it is shown

that the convergence of a multiplier block bootstrap version of the

empirical process of cluster functional conditionally given the data

follows under the same conditions as the convergence of

itself. From this powerful result it is easily concluded that a

multiplier block bootstrap version can be used to construct

confidence regions for the extremogram.

Though in the present paper we focus on the extremogram as one

possible measure for the extremal dependence structure of the time

series, the same approach using empirical processes of cluster

functionals can be used in a much wider context. For example, Drees

(2011) analyzed block estimators of the so-called extremal index of

absolutely regular time series using empirical processes of cluster

functionals and suggested a bias corrected version thereof.

The paper is organized as follows. In Section 2 we introduce

multiplier block bootstrap versions of the empirical process .

Moreover, we give sufficient conditions under which, in probability

conditional on the data, this bootstrap processes weakly converge to

the same limiting process as . In Section 3, it is demonstrated

that the theory developed by Drees and Rootzén (2010) yields limit theorems for the empirical extremogram with

estimated normalizing sequence uniformly over suitable families of

sets. In the same setup, a bootstrap result easily follows from the

general theory developed in Section 2. The results of a small simulation study are reported in Section 3. All proofs are postponed to

Section 5.

Throughout the paper, we will use the notation for the

vector made up by the first components in

the vector , if has at least components, and otherwise

. The maximum norm of a vector for some

is denoted by . We omit indices of random variables

to denote a generic random variable with the same distribution; for

example, is a generic random variable with the same

distribution as and is a generic random vector with

the same distribution as .

2 Multiplier processes

In what follows, is a row-wise

stationary triangular scheme of -valued random vectors.

Usually these vectors are derived from some fixed stationary time

series by a transformation which depends on the

stage and which sets all but the “extreme” observations to 0

in such a way that the probability that a transformed observation is

non-zero tends to 0 as . For univariate time series,

often definition (1.2) is used. In our application

to the empirical extremogram instead we define

(2.1)

for some and .

According to Theorem 1.1, under suitable conditions,

the empirical process of cluster functionals converge to a

Gaussian process with covariance function , which is defined

in (C3) as the limit of the covariance function of the cluster

functionals applied to a block of consecutive

“standardized extremes” . One may try to estimate this

covariance function by an empirical covariance, but since most of

the blocks defined in (1.1) equal 0, a

bootstrap approach seems more promising.

Because the processes are defined via functionals applied to whole

blocks of “standardized extremes”, it suggests itself to

use some block bootstrap. More precisely, we consider the following

two versions of multiplier block bootstrap processes:

(2.2)

(2.3)

where

and , are i.i.d. random variables with

and independent of .

Note that in the definition of the multiplier process

expectations are used which are usually unknown to the

statistician. Hence, in some applications, it may be useful to

replace them with the estimators , which leads to

the bootstrap processes .

Our main goal is to prove weak convergence of and

to in probability, conditionally on the data. To

this end, as usual, we metrize weak convergence in

using the bounded Lipschitz metric on the space

of probability measures on . That is, for two

probability measures and we define

where

Likewise, for the convergence of the fidis, we use the distance

between two probability measures and on , where

By (resp. ) we denote the (outer) expectation with

respect to , i.e. is the expectation of

the function conditionally on the observations. Likewise, we denote by the

probability measure w.r.t. . (Cf. Kosorok, 2003,

for a precise definition using a special construction of probability

spaces.)

Our first result shows that the asymptotic behavior of the fidis of

, conditionally on the data, is the same as the

(unconditional) behavior of the fidis of .

2.1 Theorem

Under the conditions (B1), (B2) and (C1)–(C3) one has for all

(2.4)

in probability.

Since the supremum in (2.4) is bounded by 2, it readily follows that

that is, the (unconditional) weak convergence of the fidis of

to the corresponding fidis of

.

Following the ideas developed by Kosorok (2003), the following

result establishes the asymptotic tightness of under a

bracketing entropy condition, and thus also the weak convergence of

under the same conditions as the convergence of the

original empirical process in Theorem 1.1(ii).

2.2 Proposition

Suppose that the conditions (B1), (B2), (D1), (D3) and (D4) hold

and

(i)

(D2) holds and is bounded, or

(ii)

(D2’) holds and .

Then is asymptotically tight in . Hence

it converges to if, in addition, the conditions (C1)–(C3) are

met.

Now a modification of the arguments given in the proof of Theorem 2

of Kosorok (2003) yields the desired convergence result for the

multiplier process conditionally on the data.

2.3 Theorem

If condition (D3) and convergence (2.4) hold and

weakly converges to , then

(2.5)

in outer probability.

A combination of this result with Theorem 2.1 and

Proposition 2.2 leads to

2.4 Corollary

If the conditions (B1), (B2), (C1)-(C3) and (D1)-(D4) are

satisfied and is bounded, then convergence (2.5) holds.

According to Theorem 2.3, under (D3) the weak

convergence of the multiplier process to

conditionally on the data follows from the weak convergence of the

fidis conditionally on the data and the (unconditional) convergence

of to . The latter assertion may also be derived by

establishing the asymptotic equicontinuity of using a

metric entropy condition (instead of verifying tightness using a

bracketing entropy condition as in Proposition

2.2).

2.5 Proposition

Suppose that the conditions (B1), (B2), (D1), (D2’), (D3)

and

(D5’)For all and the

map

is measurable

are fulfilled and

(i)

(D6) holds and is bounded, or

(ii)

(D6’) holds.

Then is asymptotically equicontinuous. Hence,

it converges to if, in addition, the conditions (C1)–(C3) are

met.

Using Theorem 2.3 and Corollary 2.6.12 of van der

Vaart and Wellner (1996), we obtain as an immediate consequence

2.6 Corollary

If the conditions (B1), (B2), (C1)-(C3), (D1), (D2’), (D3) and

(D5’) are met, if is measurable with and is a VC-hull

class, then convergence (2.5) holds.

To sum up, we have shown that, roughly under the same conditions as

used in Theorem 1.1, the multiplier process

shows the same asymptotic behavior conditionally on the

data as the empirical process unconditionally. The following

result gives conditions under which the convergence of

implies the convergence of the bootstrap process

conditionally on the data.

2.7 Corollary

If convergence (2.4) of the fidis of

holds conditionally on the data, condition (D3) is satisfied and

and weakly, then

(2.6)

in outer probability, weakly and

(2.7)

in outer probability. In particular, these assertions hold under

the conditions of Corollary 2.4 and under the

assumptions of Corollary 2.6.

2.8 Remark

Note that also the normalizing factor in the

definition of may be unknown. In most

applications of multiplier processes, though, this is not

problematic, because this factor is not needed to construct

confidence regions. Nevertheless, it is noteworthy that assertion

(2.7) remains valid if is replaced with some

estimator that is consistent in the sense that in probability.

For specific types of cluster functionals, Drees and Rootzén (2010)

gave simpler sufficient conditions for the convergence of the

corresponding empirical process which carry over to the multiplier

processes considered here. In the next section we will use the

conditions of Corollary 3.6 of that paper, which deals with

so-called generalized tail array sums, i.e. empirical processes

with functionals of the form for functions such that

.

3 Processes of Extremograms

In this section we employ the general theory to analyze the

asymptotic behavior of the empirical extremogram ,

a version with empirical normalization and a bootstrap version

thereof, uniformly over suitable families of sets and and

over lags for some fixed .

Throughout this section we are only interested in the behavior for

vectors with at least one large component. We thus consider families

of pairs of measurable subsets of such that

i.e. for all

. However, the results below can be generalized to

families of sets that are uniformly bounded away from 0 so that

. For

the sake of notational simplicity, we assume that (instead

of ) -valued random vectors are

observed.

3.1 Remark

To keep the presentation simple, we will assume that is

regularly varying on the full cone

with a limiting measure

which is not concentrated on ; see Theorem

3.2 below. This assumption could be weakened to

the regular variation on the cone

defined in the spirit of Das et al. (2013), i.e. there exists a

normalizing sequence and a measure such that

for all -continuity sets bounded away from

, where the limit has to be finite. Here one may

choose as the -quantile of . Under the slightly more restrictive assumption used

in the results below, one has

as , and hence and

,

where is the degree of homogeneity of , i.e. .

For some intermediate sequence (i.e. ,

), we define the empirical extremogram to the sets

and and lag as

Note that this is a slight modification of the definition given by

Davis and Mikosch (2009) in that we do not use the maximal number of

summands in the denominator. However, it is easily seen that all

results given below carry over to the original definition.

The uniform asymptotic behavior of the empirical extremogram will

easily follow from that of the stochastic process

with

This process, in turn, can be analyzed using the theory for

empirical processes of cluster functionals developed by Drees and

Rootzén (2010). In order to use conditions on the joint distribution

of the as weak as possible, it is useful to consider such

processes indexed by and just two lags . Let

Note that, for , we have and ; under the conditions of Theorem 3.2

the difference between these processes is asymptotically negligible

even if .

Using Corollary 3.6 of Drees and Rootzén (2010) and Drees and Rootzén (2015), we

obtain the following set of sufficient conditions for the

convergence of .

3.2 Theorem

Suppose that all four-dimensional marginal distributions of the

stationary time series are regularly varying, i.e. for all index vectors of dimension there exists a measure such that

(3.1)

for all Borel sets bounded away from , and that .

In addition, assume that

the conditions (B1), (B2) and () are fulfilled, and

. Finally, assume that there exists a bounded semi-metric

on such that is totally bounded w.r.t. , and a function such that

and

(3.2)

for all , ,

and that the conditions (D5) and (D6) hold for

if , , or , ,

and else for some

sufficiently large constant .

(Here denotes the

symmetric difference of the two sets and .)

Then

converges weakly to

a Gaussian process with covariance function

Observe that in (3.1) necessarily the following

consistency condition holds: for vectors

and of indices and -continuity

sets bounded away from the origin one has

.

Usually the moment condition (3.2) and the

entropy condition (D6) are most difficult to verify. The proof

of Theorem 3.2 shows that the process

indexed by is asymptotically tight if and only if the empirical

processes indexed by resp. are asymptotically tight for all . Thus we may replace condition (D6) by the

assumption that these families are VC-subgraph class of functions,

which in turn is equivalent to the assumption that

(3.3)

is a VC-subgraph class of

functions. Likewise, one may divide the family into a finite

number of subfamilies and check that is a VC-subgraph class of

functions.

For applications to the asymptotic analysis of empirical

extremograms, we shall consider families such that for

also belongs to . The following simple

example exhibits another closedness property of which is

important to prove convergence of the empirical extremogram with

estimated normalizing constant.

3.3 Example

Fix some and measurable sets

bounded away from 0 such that implies

for all and likewise for . (In particular, one

may choose a set such

that and imply .) Then, for

, the family

is a VC-subgraph class of functions. To see this, note

that if , i.e. the functions are linearly ordered. Hence no set of size 2 can be

shattered by the subgraphs of . Likewise, the family

pertaining to is a VC-subgraph class of functions.

Condition (3.2) can be reformulated as follows.

There exists a semi-metric on

such that is totally bounded w.r.t. and and hold for all

and all .

The families of sets and most widely discussed in the

literature are sets of upper right orthants and

complements of lower left orthants.

3.4 Example

Consider the family of pairs of upper right

orthants bounded away from the origin. Then condition (D6) holds for

if condition (B1) is satisfied and

By the same arguments one can show that condition (D6) is

fulfilled for the family .

From Theorem 3.2 one may easily conclude the uniform

asymptotic normality of the empirical extremogram centered at the

pre-asymptotic extremogram

3.5 Corollary

Suppose that the conditions of Theorem 3.2 are met, that

for all and

, and that . Then

(3.5)

weakly.

Hence if, in addition,

(3.6)

then

weakly.

We have already mentioned in the introduction that the empirical

extremogram is not a valid estimator if the

normalizing constants are unknown. In this case we replace

them by some estimator which is consistent in the sense

that in probability. Noting that

the asymptotic normality of is an easy

consequence of Corollary 3.5, provided that

is a sufficiently regular function of .

3.6 Corollary

Assume that the conditions of Corollary 3.5

(except (3.6)) are fulfilled and, in addition,

in probability, that implies

for all in a neighborhood of 1 and that as

. Then

weakly. Hence, if the following second order condition holds

(3.7)

uniformly for , , and some extended

regularly varying function (see Bingham et al., 1987,

Section 2.0) satisfying as and some

functions such that , then

weakly, provided . If , then this

convergence holds with instead of

.

3.7 Remark

(i)

If satisfies the second order condition

(3.8)

uniformly for all with , then under the conditions of

Corollary 3.6 direct calculations show that

satisfies condition (3.7) with

(ii)

If the conditions of Theorem 3.2 hold

when (3.2) is replaced with

for all , , and some function

satisfying as , then the same arguments

as used in the proof of Theorem 3.2 show that

converges weakly to a continuous Gaussian process. From

and

one can easily conclude that in

probability, i.e. is consistent for

.

Indeed, a refined analysis shows that under the second order

condition (3.8) one even has

if

.

As the distribution of the limit process arising in Corollary 3.6

is difficult to estimate, we use the bootstrap approach discussed in

Section 2 to approximate the distribution of the

empirical extremogram. Let

3.8 Theorem

Suppose that all conditions of Corollary 3.6 are

fulfilled and that , , are i.i.d. random variables

with and independent of . Then,

(3.9)

(3.10)

Let . In view of Theorem

3.8, approximate confidence regions for the

extremogram can be obtained

from Monte Carlo simulations of . To

this end, suppose is a family of subsets of

such that as , where

denotes the open -neighborhood of a set w.r.t. the

supremum norm on .

Then all indicator functions , , can be uniformly well

approximated from above and from below by functions of the form

with . Since the functions belong to

, it is easily seen that

(3.9) and (3.10) imply

and as , respectively.

In particular, if for sufficiently large , is a

subset of such that

(3.11)

then under the conditions of Corollary 3.6 with

, for sufficiently large , we have

(3.12)

To find such a set (or rather an approximation to it), one may

simulate independent realizations

, , of the bootstrap version of the empirical extremogram. For

some fixed set let

with denoting the

smallest such that

Here ought to be star-shaped, i.e. implies for all . The shape of determines the

emphasis which is laid on particular features of the extremogram.

See Section 4 for an example.

4 Finite sample performance of bootstrapped extremograms

In this section we investigate the finite sample performance of confidence intervals which are constructed using the multiplier block bootstrap approach, the stationary bootstrap proposed by Davis et al. (2012) and a modified version of the latter.

Davis et al. (2012) suggested to construct bootstrap samples from an observed time series as follows. Let , , be iid random variables uniformly distributed on , and , , iid random block lengths with a geometric distribution with expectation , independent of . Define , , , and for and . For , , let , where for is interpreted as . This means that blocks of length starting from the observation at are glued together until one obtains a new time series of length ; in this process one repeats the original time series after the last observation as often as necessary.

Now denote by the bootstrap estimator of calculated from .

Davis et al. (2012) proved that under suitable conditions, conditionally on the data, the limit distribution of is the same as the one of , so that bootstrap confidence intervals can be constructed.

One disadvantage of this approach is that for indices near the end of a block such that for some the indicator has a completely different behavior than , because does not correspond to a pair of observations with lag in the original time series.

To overcome this drawback, we suggest the following modification of the stationary bootstrap estimator. For simplicity, we assume that the time series has been observed at time points (in other words, we redefine ). Then we define

which has the same asymptotic behavior as , but only observations are compared which are lagged by . In essence, this mean that we apply the stationary bootstrap technique to the bivariate time series .

In addition to these two version of stationary bootstrap estimators, we consider the multiplier bootstrap. Here we have drawn multipliers from a Student -distribution with 5 degrees of freedom and scale parameter such that . However, this particular choice is not crucial as in further simulations we have obtained a similar performance of the multiplier block bootstrap for other distributions which are symmetric about 1 with an unbounded support (e.g., for normally distributed multiplier).

Here we report the results for three different models:

(i)

a GARCH model , with and -distributed innovations with 8 degrees of freedom, independent of

(ii)

an autoregressive model of order 1: with and symmetrized Fréchet distribution of the innovations, i.e., for all

(iii)

a moving average time series of order 3, namely with as in (ii).

For each model we simulated time series of length .

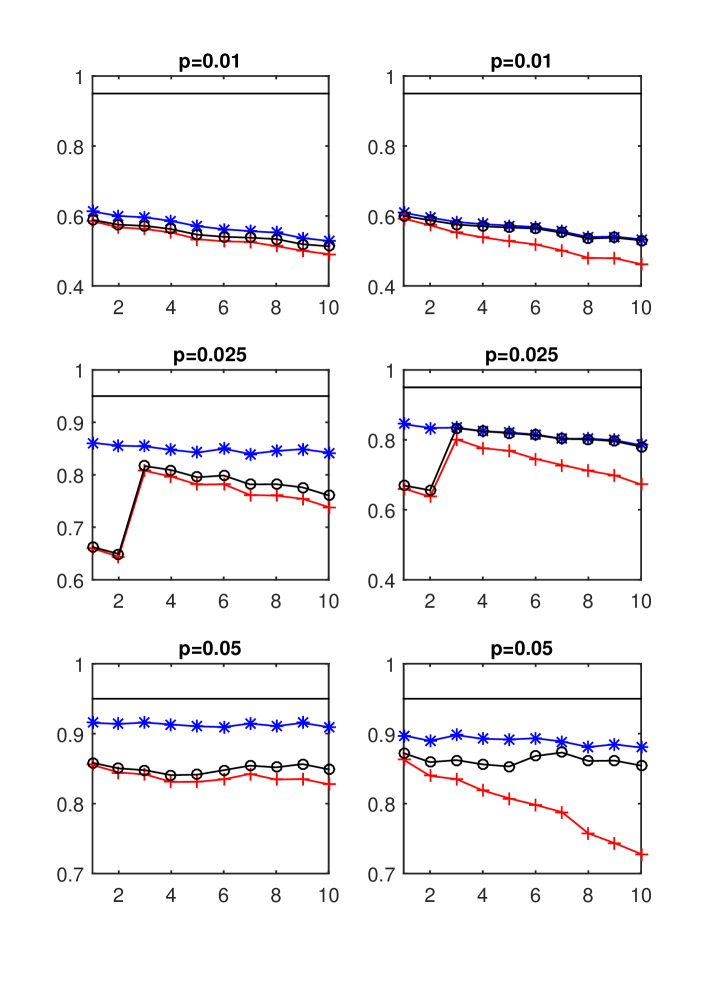

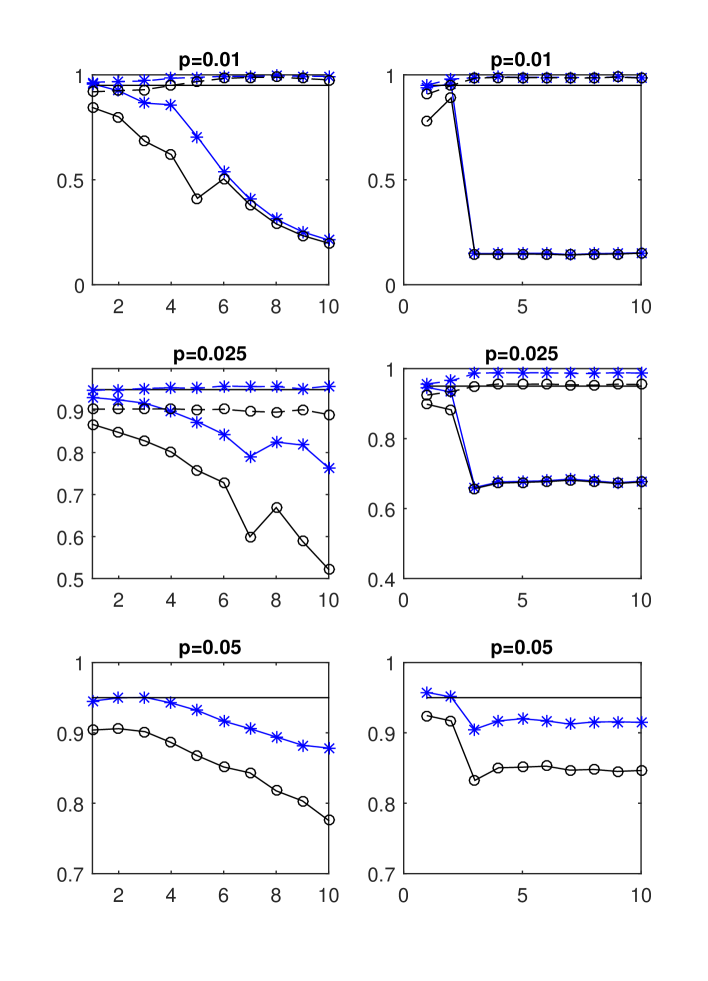

Figure 1: Empirical coverage probability of confidence intervals (4.1) for as a function of , constructed using multiplier block bootstrap (blue ), stationary bootstrap suggested by Davis et al. (red ) and the modification thereof (black ) with (average) block length (left) and (right) for the -GARCH model (i), different thresholds with exceedance probability are used in the three rows; the nominal coverage probability 0.95 is indicated by the horizontal line.

We consider the extremogram for , i.e., , which is often also called tail dependence coefficient, and lags . As normalizing constants (thresholds) we have chosen the -quantile of the stationary distribution for which have been estimated by the corresponding empirical quantiles. The true pre-asymptotic extremograms have been determined by simulation (based on 1000 time series of length ). Analytic expression for the (asymptotic) extremograms are known for the linear models (ii) and (iii) (see e.g., Meinguet and Segers, 2010, Example 9.2). For the GARCH model, they were determined using a simulation algorithm suggested by Ehlert et al. (2015).

In each simulation we have drawn bootstrap replicas according to each of the three bootstrap procedures. If, for fixed , the upper and lower empirical -quantile of the resulting bootstrap estimates of the extremogram are denoted by and then, according to (3.11) and (3.12),

(4.1)

is a confidence interval for the (pre-asymptotic) extremogram with nominal coverage probability .

We first discuss the results for the -GARCH model in detail, before we show the results for the linear time series in abbreviated form. For this model,

Figure 1 shows the empirical coverage probabilities of all three bootstrap procedures as a function of for the pre-asymptotic extremogram. The three rows correspond to the three thresholds with ascending exceedance probabilities. The left column shows the results for (average) block length , the right column for . For all bootstrap procedures, the actual coverage probabilities are much smaller than the nominal value 0.95 if the threshold is chosen too high. For the estimator based on the largest 5% of the observations and blocks of length , the coverage probability of the multiplier block bootstrap is reasonably close to the nominal size while both versions of the stationary bootstrap have a considerably lower coverage probability. In all simulations, the multiplier block bootstrap yields the highest coverage probability, while the stationary bootstrap proposed by Davis et al. (2012) performs worst. Moreover, in most cases the performance is better for larger block sizes. In particular, the stationary bootstrap proposed by Davis et al. is sensitive to too small a block size, as was to be expected from the above discussion.

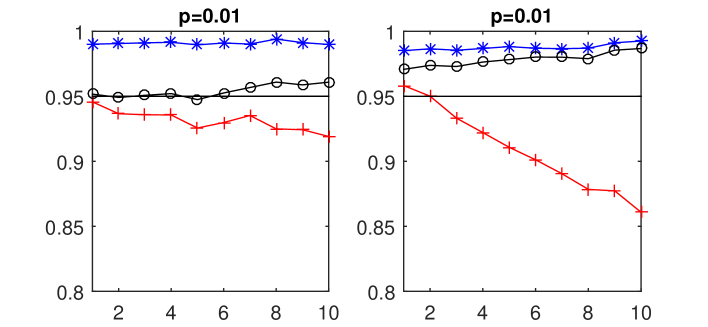

The main reason for the disappointing performance for high thresholds is that then for very few or even none time instants both and exceed the threshold. If there are no joint exceedances in the original time series (leading to an estimate 0 for the extremogram) then also the bootstrap estimate equals 0 if one uses the multiplier block bootstrap or the modified stationary bootstrap (and it equals 0 for the original stationary bootstrap with very high probability). Hence the confidence intervals do not cover the true value if this is not exactly equal to 0, which is neither the case for the pre-asymptotic nor the asymptotic extremogram, leading to a high non-coverage probability. Indeed, for , Figure 2 shows that if one considers only those simulations when the estimated extremogram does not equal 0, then the empirical coverage probability is rather close to the nominal value.

Figure 2: Empirical coverage probability of confidence intervals (4.1) for the pre-asymptotic extremogram as a function of , constructed using multiplier block bootstrap (blue ), stationary bootstrap suggested by Davis et al. (red ) and the modification thereof (black ) with (average) block length (left) and (right) for the -GARCH model (i), based only on those simulations in which for some both and exceed the threshold .

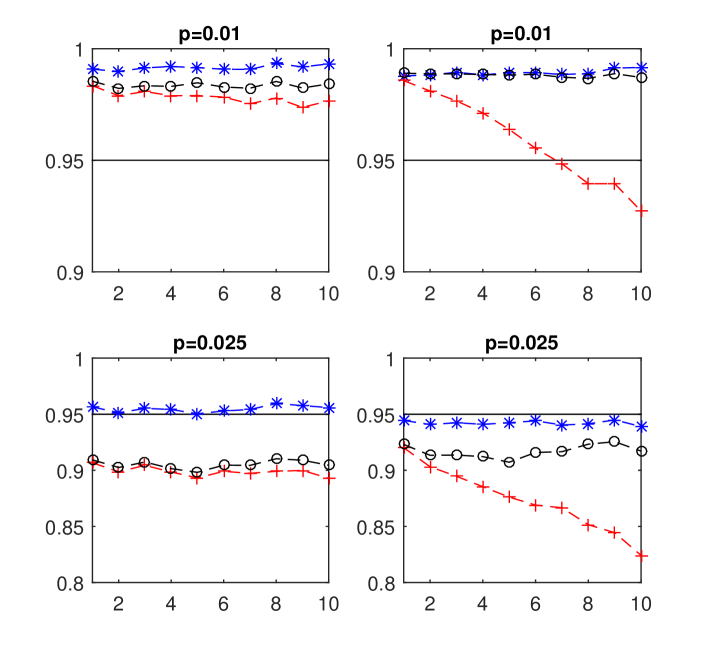

To overcome this weakness, we suggest to estimate the error distribution using a bootstrap based on a lower threshold if one wants to construct confidence intervals for the pre-asymptotic extremogram for a high threshold (or even the extremogram). Denote by the empirical extremogram based on the exceedances over the threshold with exceedance probability , and by some bootstrap version thereof. Then, according to Theorem 3.8, conditional on the data, for , the bootstrap error has approximately the same distribution as . So if and denote the empirical bootstrap quantiles as defined above, calculated from the bootstrap for the threshold with the higher exceedance probability , then

(4.2)

is a confidence interval with nominal coverage probability .

Figure 3: Empirical coverage probability of confidence intervals (4.2) for as a function of , constructed using multiplier block bootstrap (blue ), stationary bootstrap suggested by Davis et al. (red ) and the modification thereof (black ) with (average) block length (left) and (right) for the -GARCH model (i).

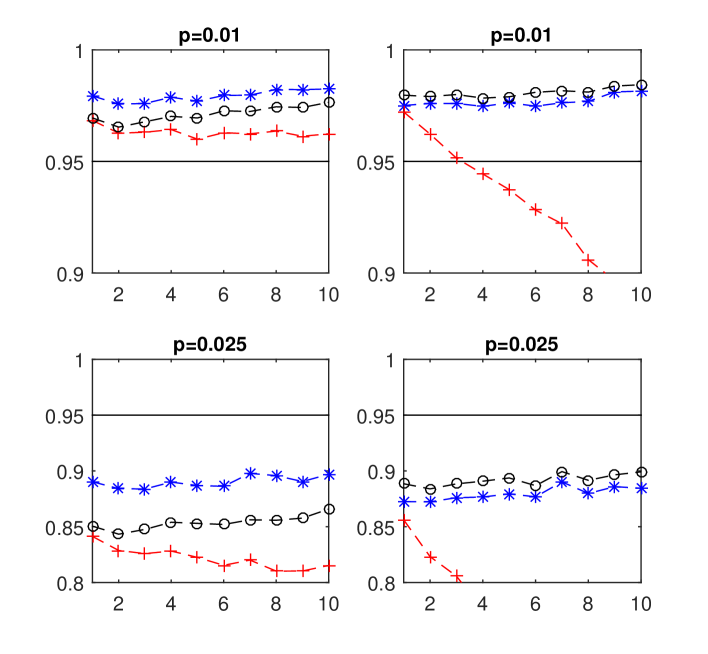

Figure 3 displays the empirical coverage probabilities of this confidence interval for the pre-asymptotic extremogram, and , which are now much closer to the nominal size 0.95. (Indeed, for the new confidence intervals are a bit too conservative.) As for small the pre-asymptotic extremograms are closer to the limit extremograms, for these thresholds one may also be interested in the coverage probability for the latter, which are shown in Figure 4. The confidence intervals based on the threshold with exceedance probabilities are still a bit conservative, while for , when the bias is larger and the confidence intervals more narrow, the actual coverage probabilities are too low.

Figure 4: Empirical coverage probability of confidence intervals (4.2) (4.1) for the exremogram as a function of , constructed using multiplier block bootstrap (blue ), stationary bootstrap suggested by Davis et al. (red ) and the modification thereof (black ) with (average) block length (left) and (right) for the -GARCH model (i).

Figure 5: Empirical coverage probability of confidence intervals (4.1) (solid lines) and (4.2) (dashed lines) constructed using multiplier block bootstrap (blue ) and modified stationary bootstrap (black ) with block length for the AR(1) model (ii) (left) and MA(3) model (iii) (right) and different thresholds with exceedance probability ; the nominal coverage probability 0.95 is indicated by the horizontal line.

Finally, we briefly discuss the linear time series models. As overall the conclusions are similar, we present just the most important findings for block size . Figure 5 shows the coverage probabilities for the autoregressive model (ii) in the left column and for the moving average (iii) in the right column, both for the confidence intervals (4.1) (solid lines) and (4.2) (dashed lines). In order to not overload the plot, the results for the original stationary bootstrap (which again performed worst) are not shown. Again the multiplier block bootstrap gives the highest coverage probabilities, which are nevertheless not satisfactory if one uses the direct bootstrap interval

(4.1) for a high threshold for the extremogram at lags not close to 0. This is particularly true, if the true value is small (e.g., for large lags in the autoregressive model). In these cases, it helps a lot to borrow strength from the bootstrap for a lower threshold as in (4.2).

5 Proofs

Proof of Theorem 2.1. We combine ideas from the proofs of Theorem 2.3 of Drees and

Rootzén (2010) and of Theorem 2 by Kosorok (2003). Denote by

, , independent copies of that

are independent of . As in Drees and

Rootzén (2010), we define , . (Recall that for

with .)

We first analyze the asymptotic behavior of

conditionally given . Note that . Moreover, because of

(5.1)

Now by condition (C1)

(5.2)

and

(5.3)

Combining (5.1)–(5.3), we see that the

left-hand side of (5.1) tends to 0 in probability.

Next check that from (5.2) and (5.3) we may conclude

(5.4)

in probability. Therefore, to each subsequence there exists a subsubsequence

such that the convergence of the left-hand side of (5.1) and the convergence

of the left-hand side of

(5.4) hold almost surely. By Theorem 4.10 of Petrov (1995), on the corresponding set of probability

1, for all ,

(5.5)

We can argue the same way to obtain convergence (5.5)

uniformly for a finite number of cluster functionals and

for the analogous sum over the odd numbered blocks.

By Lemma 3 of Kosorok (2003) and the conditions (C2) and (C3), the subsubsequence can be

chosen such that on a set with probability 1

Because of the aforementioned generalizations of (5.5) it follows that

Since, by (B2),

(see Drees and Rootzén, 2010, proof of Lemma 5.1), the last convergence in turn implies

(5.6)

in probability. Hence, along a further subsequence of , the convergence

holds almost surely and w.l.o.g. we may

assume almost sure convergence along .

By the above arguments, one easily sees that the analog to (5.5)

also holds for instead of . Together with the same

argument for the odd numbered blocks it follows that can be chosen such that on a set with probability

1, for all ,

Thus from (5.6) we can conclude that for all subsequences

there exists a subsubsequence such that almost surely

which is equivalent to the assertion.

Proof of Proposition 2.2. The asymptotic tightness of follows if we can prove

asymptotic tightness of and the analogous assertion for the

sum over the odd numbered blocks. Similarly as in the proof of

Theorem 2.8 of Drees and Rootzén (2010), it suffices to prove

tightness of with and denoting

independent copies of , because the total variation

distance between the distribution of the processes with dependent

blocks (which are separated in time)

resp. with independent blocks tends to 0.

To this end, we verify that the conditions of van der Vaart and

Wellner (1996), Theorem 2.11.9, are fulfilled for

which

are centered random variables because of the independence of

and .

The second displayed formula of this theorem is an immediate

consequence of condition (D3), since implies

. Likewise, the bracketing number for the

multiplier process considered here is the same as the bracketing

number for the original process so that the bracketing entropy

condition (i.e. the third displayed formula in Theorem 2.11.9)

follows from (D4).

It remains to verify that

(5.7)

If is bounded, then this convergence is obvious from (D2).

Under the conditions of part (ii), one has for all

By condition (D2’) one can find a sequence such that

Moreover, also the first term is of smaller order than ,

because and, by assumption,

. Now, by the Cauchy-Schwarz inequality and

the Chebyshev inequality, the left-hand side of

(5.7) can be bounded by

Proof of Theorem 2.3. By (D3) the family is totally bounded w.r.t. the metric

. Hence there exists a sequence of finite -nets

of , i.e. finite sets such that to every

there exists whose

-distance to is less than . Because has

continuous sample paths w.r.t. and is bounded and Lipschitz-continuous with

Lipschitz-constant 1, we may conclude

(5.8)

For fixed , denote by the

cardinality of the -net. Theorem 2.1 gives

(5.9)

in outer probability (cf. van der Vaart and Wellner, 1996, p. 182).

Next note that by the definition of

Since weakly converges to , it is asymptotically

equicontinuous, that is, for all and all sequences

Hence

and thus by Fubini’s theorem (van der Vaart and Wellner, 1996,

Lemma 1.2.6)

This in turn implies

(5.10)

in outer probability for all .

By (5.8), for all and all

, one has for sufficiently large that . Therefore, in view of

(5.9) and (5.10), for all

and sufficiently large

which proves the assertion.

Proof of Proposition 2.5. For define , and . We are going to apply Theorem 2.11.1 of van der Vaart and

Wellner (1996) to the processes

with and denoting

independent copies of . The assertion then follows by

the same arguments as used in the proof of Drees and Rootzén

(2010), Theorem 2.10 (cf. also the proof of Proposition

2.2 of the present paper).

Because is an envelope function of and

the first condition of Theorem 2.11.1 is obviously fulfilled if

is bounded and (D2’) holds, while it follows from the

arguments given at the end of the proof of Proposition

2.2 if holds.

The second condition of Theorem 2.11.1 is equivalent to our

condition (D3), because and the independence of

and imply

.

It remains to verify the metric entropy condition (2.11.2) of van der Vaart and

Wellner (1996), which is equivalent to

for all where

If , then

so that and the entropy condition readily

follows from (D6).

If is not necessarily bounded, but the uniform entropy

condition (D6’) holds, then one may proceed similarly as in the

proof of Theorem 2.10 of Drees and Rootzén (2010). Let

with denoting the Dirac measure with mass 1 at ,

and check that

Hence . Moreover, for all

Since , this probability can be made

arbitrarily small for all by choosing sufficiently

large.

Thus, for all , there exists such that with outer

probability of at least

as by (D6’).

Hence, under both sets of conditions, the asymptotic

equicontinuity follows from Theorem 2.11.1 of van der Vaart and

Wellner (1996).

which implies (2.6).

Hence the weak convergence follows from the analogous

convergence of .

Finally, by (2.6), the definition of

and Theorem 2.3

in outer probability uniformly for all .

Proof of Theorem 3.2. The convergence of follows from Corollary 3.6(ii) and Remark 3.7(i) of Drees and Rootzén (2010); see also Drees and Rootzén (2015). To see this, check that

Condition (D3) is fulfilled since for

Since, by (), for

satisfies the analog to () if is replaced with

Moreover,

(3.1) ensures that convergence (3.8) of Drees and Rootzén (2010) holds, because

and likewise

Hence, by Drees and Rootzén (2015), condition (C3) holds and converges to a Gaussian process

with the covariance function specified in formula (3.10) of Drees and Rootzén (2010) in terms of the functions .

Since

the convergence of to a Gaussian process with covariance function

follows from the approximation (3.6) of Drees and

Rootzén (2010). Now the assertion is obvious.

Proof of condition (D6) in Example 3.4.

For fixed define

functions , with . The

subgraph of equals

Consider some fixed set of points in . If

for the symmetric difference

does not contain any of the

, , , then the intersections

and are identical. Since the

hyperplanes , , , , divide into at most

hypercubes and for belonging

to the same hypercube does not contain any of the ,

the family can pick out at most

different subsets of . Hence it cannot shatter

if , which is fulfilled if

and

is sufficiently large.

To sum up, so far we have shown that, for some and all , the VC-index of is less than .

By Theorem 2.6.7 of van der Vaart and Wellner (1996), we conclude

that

(5.11)

for all , all probability measures on

, and suitable universal constants , and

with denoting the envelope function of .

Next let for

, for and define

independent copies of , . Consider

the non-zero values of the of

these blocks with at most non-zero ’s; if

necessary, these are completed by zeros to obtain vectors ,

i.e. for and for . Let

and consider the squared random -distance

for all . In particular,

with

so that a ball with radius w.r.t. is contained in a ball with radius w.r.t. .

Note that

Hence, in view of (5.11), (defined in (3.3)) can be covered by

with denoting the multiplier process

pertaining to (cf. (2.2)).

By Proposition 2.5, Theorem 2.3

and the proof of Theorem 3.2 (in particular, the

convergence of )

(cf. also Corollary 3.6 of Drees and Rootzén, 2010).

Thus

Note that

where according to the central limit theorem and the regular variation of

the second term is of the order .

Hence

uniformly for . In the

last step we have used that by the regular variation of and

the definition of

where, by assumption, is bounded away from 0. Now we

can conclude (3.9) from

(5.13) and (3.5).

Finally, notice that in outer probability for all , because and is asymptotically

equicontinuous w.r.t. . Therefore,

(3.10) is an immediate consequence of

(3.9).

Appendix

The following conditions were used by Drees and Rootzén (2010, 2015). For

the ease of reference, we use the same numbering as in these papers.

(B1)The rows are stationary, , (B2) ()For all and all there exists such that exists and .

Recall that for and we define

.

(C1)For for all . (C2) (C3) (D1)The index set consists of

cluster functionals such that is finite for all

and such that the envelope functionis finite for all . (D2)

(D2’)

(D3)There exists a semi-metric on

such that is totally bounded (i.e., for all the

set can be covered by finitely many balls with radius

w.r.t. ) such that

Finally, we consider different entropy conditions, which measure the

complexity of the family . The bracketing number

is defined as the smallest number

such that for each there exists a partition

of such that

(5.14)

For a given semi-metric on , the (metric) covering number

is the minimum number of balls with radius

w.r.t. needed to cover . The condition (D6) bounds the rate of increase of

as tends to 0 for the random semi-metric

that is the -semi-metric w.r.t. to empirical measure

,

where , , are i.i.d. copies of .

In (D6’) we instead use the supremum of all covering numbers

where

and

ranges over the set of discrete probability measures

on .

(D4) (D5)For all , , and the

map

is measurable.

(D6)

(D6’)The envelope function is

measurable with and

Acknowledgement: I thank Anja Janßen for helpful

discussions about regular variation on general cones and for providing R-code to calculate the extremogram for -GARCH time series. The financial

support by the German Research foundation DFG via the grant JA

2160/1 is gratefully acknowledged.

References

Basrak, B., and Segers, J. (2008). Regularly varying multivariate time series. Université Catholique de Louvain,

Institut de Statistique discussion paper 0717.

Bingham, N.H., Goldie, C.M., and Teugels, J.L. (1987). Regular

Variation. Cambridge University Press.

Das, B., Mitra, A., and Resnick S. (2013). Living on the

multi-dimensional edge: seeking hidden risks using regular

variation. Adv. Appl. Probab.45, 139–163.

Davis, R., and Mikosch, T. (2009). The extremogram: A correlogram for

extreme events. Bernoulli15, 977- 1009.

Davis, R., Mikosch, T., and Cribben, I. (2012). Towards estimating extremal serial dependence via the

bootstrapped extremogram. J. Econometr.170, 142–152.

Drees, H. (2003). Extreme quantile estimation for dependent data with applications to

finance. Bernoulli9, 617–657.

Drees, H. (2011). Bias correction for estimators of the extremal index. Preprint, arXiv:1107.0935v1

Drees, H., and Rootzén, H. (2010). Limit Theorems for Empirical Processes of Cluster Functionals.

Ann. Statist.38, 2145–2186.

Drees, H., and Rootzén, H. (2015). Correction note to “Limit Theorems for Empirical Processes of Cluster Functionals”. Preprint, arXiv:1510.09090v1.

Drees, H., Segers, J., and Warchoł, M. (2015). Statistics for Tail Processes of Markov Chains. Extremes18, 369–402.

Ehlert, A., Fiebig, U.-R., Janßen, A., and Schlather, M. (2015). Joint extremal behavior of hidden and observable time series with applications to GARCH processes. Extremes18, 109–140.

Kosorok, M.R. (2003). Bootstraps of sums of independent but not identically distributed stochastic processes.

J. Multiv. Analysis84, 299–318.

Meinguet, T., and Segers, J. (2010). Regularly varying time series in Banach spaces. Preprint, arXiv:1001.3262v1.

Petrov, V.V. (1995). Limit Theorems of Probability Theory. Oxford Science Publication.