A fixed-point approach to barycenters in Wasserstein space111Research partially supported by the

Spanish Ministerio de Economía y Competitividad, grants

MTM2014-56235-C2-1-P and MTM2014-56235-C2-2, and by Consejería de Educación de la Junta de Castilla y León, grant VA212U13.

Pedro C. Álvarez-Esteban1, E. del Barrio1, J.A. Cuesta-Albertos2 and C. Matrán1 1Departamento de Estadística e Investigación Operativa and IMUVA,

Universidad de Valladolid 2Departamento de

Matemáticas, Estadística y Computación,

Universidad de Cantabria

Abstract

Let be the set of Borel probabilities on with finite second moment and absolutely continuous

with respect to Lebesgue measure.

We consider the problem of finding the barycenter (or Fréchet mean) of a finite set of probabilities

with respect to the Wasserstein metric. For this task we introduce an operator on related to the optimal transport

maps pushing forward any to . Under very general conditions we prove that the barycenter

must be a fixed point for this operator and introduce an iterative procedure which consistently approximates

the barycenter. The procedure allows effective computation of barycenters in any location-scatter

family, including the Gaussian case. In such cases the barycenter must belong to the family, thus it is characterized

by its mean and covariance matrix. While its mean is just the weighted mean of the means of the probabilities,

the covariance matrix is characterized in terms of their covariance matrices through

a nonlinear matrix equation. The performance of the iterative procedure in this case is illustrated through

numerical simulations, which show fast convergence towards the barycenter.

Let us consider a set of elements in a certain space and associated weights, ,

satisfying , , interpretable as a quantification of the relative importance or presence of these elements.

The suitable choice of an element in the space to represent that set is an old problem present in

many different settings. The weighted mean being the best known choice, it enjoys many nice properties that allow us to

consider it a very good representation of elements in an Euclidean space. Yet, it can be highly undesirable

for representing shaped objects like functions or matrices with some particular structure. The Fréchet mean or barycenter is a

natural extension arising from the consideration of minimum dispersion character of the mean, when the space has a

metric structure which, in some cases, may overcome these difficulties. Like the mean, if is a distance in the reference space , a barycenter is determined by the relation

In the last years Wasserstein spaces have focused the interest of researchers from very different

fields (see, e.g., the monographs [4], [27] or [28]), leading in

particular to the natural consideration of Wasserstein barycenters beginning with [1].

This appealing concept shows a high potential for application, already considered in Artificial Intelligence

or in Statistics (see, e.g., [16], [5], [10], [20], [7]

or [3]). The main drawback being the difficulties for its effective computation,

several of these papers ([16], [5], [10]) are mainly devoted to this

hard goal. In fact, the ()Wasserstein distance between probabilities, which is the framework

of this paper, is easily characterized and computed for probabilities on the real line, but

there is not a similar, simple closed expression for its computation in higher dimension.

A notable exception arises from Gelbrich’s bound and some extensions (see [19],

[13], [15]) that allow the computation of the distances between

normal distributions or between probabilities in some parametric (location-scatter) families.

For multivariate Gaussian distributions in particular, in [1], the barycenter has been characterized in

terms of a fixed point equation involving the covariance matrices in a nonlinear way

(see (6) below) but, to the best of our knowledge, feasible consistent algorithms to

approximate the solution have not been proposed yet.

The approach in [1] for the characterization of the barycenter in the Gaussian setting resorted

to duality arguments and to Brouwer’s fixed-point theorem. Here we take a different approach which is not constrained

to the Gaussian setup. We introduce an operator associated to the transformation of a probability measure

through weighted averages of optimal transportations to the set of target distributions.

This operator is the real core of our approach. We show (see Theorem 3.1 and Proposition 3.3 below)

that, in very general situations, barycenters must be fixed points of the above mentioned operator. We also show (Theorem 3.6)

how this operator can be used to define a consistent iterative scheme for the approximate computation of barycenters.

Of course, the practical usefulness of the iteration will depend on the difficulties arising from the computation of the optimal transportation maps

involved in the iteration. The case of Gaussian probabilities is a particularly convenient setup for our iteration.

We provide a self-contained approach to barycenters in this Gaussian framework based on first principles of

optimal transportation and some elementary matrix analysis. This leads also to the characterization (6) and,

furthermore, it yields sharp bounds on the covariance matrix of the barycenter which are of independent interest.

We prove (Theorem 4.2) that our iteration provides a consistent approximation to barycenters in this

Gaussian setup.

We also notice that all the results given for the Gaussian

family are automatically extended to location-scatter families (see Definition 2.1 below).

Finally, we illustrate the performance of the iteration through numerical simulations. These show fast convergence towards the barycenter,

even in problems involving a large number of distributions or high-dimensional spaces.

The remaining sections of this paper are organized as follows. Section 2 gives a succint account of some basic facts about optimal transportation and

Wasserstein metrics and introduces the barycenter problem with respect to these metrics. The section contains pointers to the most relevant references

on the topic. Section 3 contains the core of the paper, introducing the operator in (7), showing the connection

between barycenters and fixed points of and presenting the iterative scheme for approximate computation of

barycenters. The Gaussian and location-scatter cases are analyzed in Section 4, while Section 5 presents some numerical simulations.

We conclude this Introduction with some words on notation. Throughout the paper our space

of reference is the Euclidean space . With we

denote the usual norm and with the inner product. For a matrix , will

denote the corresponding transpose matrix, the determinant and

the trace. will be indistinctly used as the identity map and as the identity

matrix, while will denote the set of (symmetric) positive definite matrices The space where we consider the Wasserstein distance is , the set of Borel probabilities on with finite

second moment. The related set will denote

the subset of containing the probabilities that are absolutely continuous

with respect to Lebesgue measure. The probability law of a random vector will be represented

by .

2 Wasserstein spaces and barycenters.

Given , the ()Wasserstein distance

between them is defined as

(1)

It is well known that this distance metrizes weak convergence of probabilities plus convergence of second moments, that is,

(2)

We refer to [27] for details. In the one-dimensional case is simply

the distance between the quantile functions of and , allowing computation. In

the multivariate case there exist just a few general results that

can be used to simplify problems. An important example, which allows to deal with certain problems

by considering only the case of centered probabilities is the following,

(3)

where and are arbitrary probabilities in , with

respective means , and are the corresponding centered in mean probabilities.

In any case, it is well known that the infimum in (1) is attained. A distribution with marginals and attaining that infimum is called an optimal coupling of and . Moreover, if vanishes

on sets of dimension , in particular if , then

there exists an optimal transport map, , transporting (pushing forward) to .

This important result is the final product of partial results and successive improvements obtained in several papers including Knott and Smith [21], Brenier [8],

[9], Cuesta-Albertos and

Matrán [11], Rüschendorf and Rachev [25] and McCann [23]. We include

for the ease of reference a convenient version (see Theorem 2.12 in Villani’s book [27])

and also refer to [28] for the general theory on Wasserstein distances

and the transport problem. We recall that for a lower semicontinuous convex function

, the conjugate function is defined as .

Theorem 2.1

Let and let be the joint distribution of a pair of valued random vectors with probability laws and .

a) The probability distribution is an optimal coupling of and if and only if there exists a convex lower semi-continuous function such that a.s.

b) If we assume that does not give mass to sets of

dimension at most , then there is a unique optimal coupling

of and , that can be characterized as the unique solution to the Monge transportation

problem –an optimal transport map– , i.e.: (or a.s.), and

Such a map is characterized as - a.s., the -a.s. unique function that maps to and that is the gradient of a lower semicontinuous, convex function .

Moreover, if also does not give mass to sets of dimension at most , then for -a.e. and -a.e. ,

and is the (-a.s.) unique optimal transport map from to

and the unique function that maps to and that is the gradient of a convex, lower semicontinuous function.

Remark 2.2

Concerning optimal couplings, from a) it easily follows that if are optimal couplings of and , for positive weights satisfying , the probability is an optimal coupling for and .

Another remarkable consequence of the theorem is that optimality of a map is a

characteristic that does not depend on the transported measures. In

other words, if is an optimal map for transporting to and are such that and the support of is

contained in that of , then is also an optimal transport map from to

: This fact allows the computation

of the distance between some probabilities when we know that they can be related through optimal

maps. It must be also noted that composition

of optimal maps does not generally preserve optimality, but positive linear combinations and

point-wise limits of optimal maps keep optimality.

Special mention among the class of optimal maps must be given to the class of positive definite affine

transformations. This is done in the following theorem,

a version of Theorem 2.1 in Cuesta-Albertos et al. [13], that suffices

for our purposes here, giving an additional perspective to Gelbrich’s bound (4)

(see [19]).

Theorem 2.3

Let and be probabilities in with means and covariance matrices . If is assumed nonsingular, then

(4)

Moreover, equality holds if and only if the map transports to , where is the positive semidefinite

matrix given by

This theorem allows an easy generalization of the results involving optimal transportation

results between Gaussian probabilities to a wider setting of probability families that we introduce now.

Recall that is the set of (symmetric) positive definite matrices.

Definition 2.1

Let be a random vector with probability law .

The family

of probability laws induced by positive definite affine transformations from will be

called a location-scatter family.

Of course a location-scatter family can be parameterized through the

parameters and that appear in the definition. Note, however, that, if and

are the mean and covariance matrix of , the family can be also defined from

, with mean and covariance

matrix . This allows to parameterize the family through the mean and the covariance

matrix of the laws in the family, a fact that will be assumed throughout without additional

mention. With this assumption, a probability law in the

family will be denoted in terms of its mean, , and its covariance matrix, , by , and, as a consequence of Theorem 2.3, we have

The central problem of this work involves probabilities

and fixed weights that are positive

real numbers such that . For an arbitrary ,

we will consider the functional

Definition 2.2

If is such that

then we say that is a barycenter (with respect to Wasserstein distance)

of .

Through the paper we will maintain the notation for the barycenter. Existence and

uniqueness of barycenters have been considered

in [1]. For the sake of completeness, we give here a succinct argument to

prove these existence and uniqueness. Note first that given probabilities on

and joint probabilities on with marginals and we can always find

a joint probability on such that the marginal of

over factors and equals , (this fact is often invoked as “gluing lemma”, see e.g. [28]). Hence, we have that

where denotes the set of probabilities on

whose last marginals are . Of course, for fixed

we have with

. This means that among all with the same

(joint) marginal distribution over the last factors the functional

is minimized when

is concentrated on the set . This means that

(5)

with denoting the set of probabilities on

with marginals equal to , and a barycenter is the law induced by the map

from , a minimizer for the right-hand side in

(5), provided it exists. Now, write for the minimal value in

(5) and assume that is a minimizing sequence, that is, that

as . The fact that the marginals of are fixed implies that is a tight sequence.

Hence, by taking subsequences if necessary, we can assume that converges weakly, say to . A standard uniform integrability argument (see, e.g., the proof of Theorem 3.1 below)

shows that

hence, a minimizer exists for the multimarginal problem and, as a consequence,

with , is a barycenter, that is, a minimizer of . Strict convexity of the

map when has a density (see Corollary 2.10 in [2])

implies that is strictly convex if at least one of has a density and yields uniqueness of

the barycenter. As we said, this existence and uniqueness results for the barycenter are contained in [1] but

this approach is, arguably, more elementary and shorter.

Beyond the existence and uniqueness results and apart from the case of probability distributions

on the real line, the computation of barycenters is a hard problem. The following theorem

(Theorem 6.1 in [1]) could be an

exception because it characterizes the barycenter for nonsingular multivariate Gaussian distributions and, then,

for distributions in the same location-scatter family.

Theorem 2.4

Let be Gaussian distributions with respective means and nonsingular

covariance matrices . The barycenter of with

weights is the Gaussian distribution with mean and covariance matrix defined as the only positive definite matrix

satisfying the equation

(6)

Parts of this result were already outlined in Knott and Smith [22] and further developed

in Rüschendorf and Uckelmann [26].

However, by itself it is far from allowing an effective computational method for the

barycenter.

In the next section we introduce an iterative procedure that, under some general assumptions, produces

convergent approximations to .

3 A fixed-point approach to Wasserstein barycenters.

We introduce in this section a map whose

fixed points are, under mild assumptions, the barycenters of

with weights in the sense of Definition 2.2. With this goal,

consider now an additional . From Theorem 2.1 there exist

(-a.s. unique) optimal transportation maps such that

, where is a random vector such that , and

, .

Then, we define

(7)

We will show the connection between barycenters and fixed points of and also how we can use the

transform to define a consistent, iterative procedure for the approximate

computation of . First, we prove some basic properties of .

Theorem 3.1

If has a density, , then

maps into and it is continuous for the metric.

Proof. From Theorem 2.1 we know that where is a convex,

lower semicontinuous function. Moreover, since , denoting by the conjugate function, it holds

-a.s. (in particular, is injective in a set of total -measure).

By Alexandrov’s Theorem (see, e.g., Theorem 3.11.2 in [24] or Theorem 1 in Section 6.4 in [18]) we have that for -almost every there is a symmetric,

positive semidefinite matrix, which we denote such that for every

there exists such that implies

But then, the fact that has a density and Lemma 5.5.3 in [4] imply that is a.s. nonsingular, hence

positive definite. Thus, writing we have that

and for -a.e. we have that

that for every

there exists such that implies

(8)

where is symmetric,

positive definite, hence, nonsingular. We claim that is injective outside a -negligible set. To see this, choose satisfying (8) and such that is differentiable at

and consider the convex function . Observe that

and that for we have

(this follows, for instance, from Lemma 3.7.2, p 129 in [24]). Now from

positive definiteness of we know that, for some ,

for every . Take and small enough to ensure, using (8),

that for , . But then

which entails

As a consequence, .

This implies that , that is, is injective in a set of total -measure.

We can apply now Lemma 5.5.3 in [4] with the fact that is -a.s. nonsingular to conclude

that has a density. The fact that with

having law implies that has finite second moment, which completes the proof of the first claim.

Turning to continuity, assume that

satisfy . Write (resp. ) for the optimal

transportation map from (resp. ) to , . According to Skorohod’s representation theorem (see e.g. Theorem 11.7.2 in [17]), we can consider random vectors such that a.s., where has law and having law

. Then, by Theorem 3.4 in [14], also a.s. for , hence a.s., that implies the convergence

Now, the fact that the families are uniformly integrable (indeed the law of is , fixed)

entails the uniform integrability of and shows that thus, by characterization (2),

finishing the proof.

Remark 3.2

Let us additionally assume the following:

(9)

Under these assumptions there is a unique barycenter which has a (bounded) density,

see Theorem 5.1 in [1], and the first conclusion in the Proposition above can be improved.

If, for instance, has a bounded density, say , then has a bounded

density, , which satisfies

To check this note that for almost every the Alexandrov Hessian

can be expressed as

, .

But since and are (a.s.) positive definite and, therefore,

On the other hand, writing for the density of , by the Monge-Ampère equation (see Theorem 4.8 in [27]) we have that a.s.

As a consequence, a.s., as claimed.

Our next result provides a link between the transform and the barycenter problem.

Proposition 3.3

If then

(10)

As a consequence, , with strict inequality if .

In particular, if is a barycenter then .

Proof. We simply note that for any , writing ,

we have .

As a consequence, writing as above for the optimal transportation map from to

and , then

Also note that, from Remark 2.2, is an optimal transportation map from to and

(12)

Finally, writing for the probability induced from by the map

we see that is a coupling of and and, as a consequence

(13)

Combining (3), (12) and (13) we get (10).

Obviously, this implies that

, with strict inequality unless . In particular, if

is a barycenter then the

inequality cannot be strict and, consequently, we must have .

Remark 3.4

We notice that Proposition 3.3 remains true under a more general setting. Assume just that and belong to and let be optimal couplings of and . By the gluing lemma, we can assume that for random valued vectors defined in some probability space. Note that, in general, there exist multiple joint distributions of compatible with this construction. Nevertheless, for each of them, we can consider and the distribution that, as noted in Remark 2.2, will be an optimal coupling of and . Therefore, setting (observe that, however, is not uniquely defined), we can replicate the argument in the proof above to obtain with strict inequality if

We include now a simple but important consequence of Proposition 3.3, which follows after observing that, as noted in Remark 3.2, under (9) the unique barycenter has a density.

We observe that Corollary 3.5 can be obtained as a consequence of the duality results in [1] (see, in particular, Remark 3.9 there) but deducing it from (10) is simpler. Furthermore, Proposition 3.3 and Corollary 3.5 are the basis for considering the following iterative procedure.

We start from and consider the sequence

(14)

By Theorem 3.1 the iteration is well defined. We provide now the consistency framework

of the sequence .

Theorem 3.6

The sequence defined in (14) is tight. Under (9) every weakly convergent subsequence

of must converge in distance to a probability in

which is a fixed point of . In particular, under (9), if has a unique fixed point, , then

is the barycenter of and

.

Proof. We consider a random vector with law and write

for the optimal transportation map from to and

, . The sequence has

fixed marginals, hence it is tight. By continuity,

is also a tight sequence. But .

Arguing as in the proof of Theorem 3.1 we see that is uniformly

-integrable. Hence, any weakly convergent subsequence of

converges also in , as claimed.

Assume now that (9) holds. Without loss of generality we assume that has a bounded density, .

From Remark 3.2 we have that for every Borel . Hence, if

is a weak limit of a subsequence then for every

open and, as a consequence, has a density (upper bounded by ).

Since we have

as , by the continuity result in Theorem

3.1 we have as well.

Now, is continuous in metric (this follows, for instance,

from the fact that ).

As a consequence, and

. But by Proposition 3.3

is a nonnegative and nonincreasing sequence, hence, it is convergent. Therefore,

Using again Theorem 3.1 we see that must satisfy .

Under assumption (9) the (unique) barycenter, , is a fixed point

for . If has a unique fixed point then every subsequence of

has a further subsequence that converges to in . Hence,

.

In some special cases we can guarantee uniqueness of the fixed point and the above result can be sharpened as we show in the next section. Observe that the fixed point condition is equivalent to a.s. If this equality holds for every then is a barycenter (see Remark 3.9 in [1]). However, this is not always the case as the following example shows. Providing sufficient conditions on to guarantee that has a unique fixed point is a goal for future work.

Example 3.1

Consider the set , where , , , and . Given , let be the uniform distribution on the three points , and let be the uniform discrete distribution, supported on 12 points uniformly scattered on the four sides of the unit square excluding the vertices:

It is very easy to prove that the maps , described in Table 1, are the only optimal transport maps between and the probabilities respectively.

Map

A

B

C

D

-

, , , ,

, , ,

, , ,

, , ,

-

, , ,

, , ,

, , ,

, , ,

-

, , ,

, , ,

, , ,

, , ,

-

Table 1: Points going to each point in for the four optimal transports between and the ’s

Given , let us consider the distributions which are uniform on the union of the three balls with radius and centers in , and uniform on the union of the twelve balls with centers at and radius . Let denote the optimal transport map between and . If we take small enough,

then it is obvious that for every and

also that we can choose in such a way that, for every , the ball contains the square with side and center at .

Now, let us consider the map

Assume, for instance, that . Then, according to Table 1, we have that and , for every , hence,

we have that

Therefore belongs to the square with side and center at , and, consequently,

Obviously, the same happens for every point in the support of and we can conclude that . Moreover, we can iterate the procedure and define to be a limit point (through some convergent subsequence) of the process , where is the operator associated to the family with uniform weights. According to Theorem 3.6 and it is a fixed point of that, by the previous argument, satisfies , for every .

To get a second fixed point of , let us consider the probability supported by the points , where are as before and . Let and

and define

It can be checked that , thus is a probability distribution. As in the previous case, the optimal transportation maps, , between and the probabilities are described in Table 2.

Map

A

B

C

D

-

, , , ,

, , , ,

, , ,

, , ,

-

, , ,

, , , ,

, , , ,

, , ,

-

, , ,

, , ,

, , , ,

, , ,

-

Table 2: Points going to each point in for the four optimal transports between and the ’s

From this point on, it is possible to repeat the construction, leading to , to obtain from and suitable values an absolutely continuous (verifying ) which is also a fixed point of . If we take the smaller values obtained for and both constructions work and, then, we have obtained two different fixed points for since .

4 Barycenters in location-scatter families.

We focus now on the barycenter problem in the special

case in which are probabilities in the same location-scatter

family

where, as before, denotes the set of positive definite matrices

and is a random vector with probability law . Also, as in Section 2, and

without loss of generality, we will assume that is centered and has the identity as covariance matrix.

We will provide a consistent iterative method for the computation of the barycenter of .

We remark that this covers the case when

are Gaussian or belong to the same elliptical family (but it is not constrained

to these cases: if we take in the probability whose marginals are independent

standard uniform laws, or even standard normal and exponential, then the family is not elliptical).

In particular, our approach will give a self-contained proof of the fact that equation (6)

has a unique symmetric, positive definite solution.

Let us focus first in the case when are (nondegenerate) centered Gaussians, say , .

We know that there exists a unique barycenter. On the other hand,

since , we see that a minimizer in the

multimarginal formulation (recall the discussion about existence and uniqueness of barycenters after Definition 2.2) is the

law of a random vector with that maximizes

.

From this last expression we see that depends only on the covariance structure

of the -dimensional vector . Given any covariance structure we can find a centered Gaussian random vector with that covariance structure.

Hence, a centered Gaussian minimizer exists for the multimarginal problem and, by linearity of , a centered Gaussian barycenter

exists for . By uniqueness of the barycenter, this shows that the barycenter of nondegenerate centered

Gaussian distributions is a nondegenerate centered Gaussian distribution.

With this fact in mind, and abusing notation, we write for and consider the problem of minimizing

. Note that

(15)

We also write

for the map .

With this notation we have the following upper and lower bounds.

Proposition 4.1

With the above notation, if :

(16)

(17)

where .

Proof. We note first that (16) is just the particular form of (10)

in the present setup. For the other bound, denoting by the matrix associated to the optimal transportation map from to

, namely, , from

the fact that for any we have

for every , with equality if and only if ,

we see that for any -valued random vector such that and ,

(18)

From this we conclude that

In the case , if and then (18)

becomes an equality and we get

Observe now that for any , (16) shows that

is a necessary condition for to be a barycenter, while (17) shows that

the condition is sufficient as well. Thus, recalling the discussion before Proposition 4.1,

if we knew that the barycenter of nondegenerate centered

Gaussian distributions is a centered, nondegenerate Gaussian distribution, then, we could conclude

that it must be , with the unique solution to the matrix equation (6), which, of course, is equivalent

to the condition . Through the consideration of the iteration introduced in Section 3 we will show next that, indeed,

there exists such that

. This will yield an alternative proof of Theorem 2.4. Furthermore, it will provide

a consistent iterative method for the approximation of Gaussian barycenters.

Theorem 4.2

Assume are symmetric positive semidefinite matrices, with at least one of them positive definite.

Consider some and define

(19)

If

is the barycenter of , then

as . Moreover, the covariance matrix

of the barycenter satisfies

(20)

In particular, it is positive definite and it is the unique positive definite solution to

(6). Furthermore,

(21)

with equality in last inequality if and only if .

Proof. Let us begin proving that for ,

(22)

which, in particular, gives that all the are nonsingular and the sequence is well defined.

To this just note that by

the Minkowski determinant inequality (see, e.g., Corollary II.3.21 in [6]) we get

from which (22) follows.

Tightness of the sequence

(which follows from Theorem 3.6) implies boundedness of .

We take a convergent subsequence . By continuity we have

, which shows that .

The map is continuous on the set and, therefore, . Continuity of the map implies that

. Finally, the fact that

is a nonnegative, nonincreasing sequence implies that it is convergent. Hence, we have

In view of (16), this can only happen if . Since

this can happen only if . Hence, we have proved that equation (6) has a unique positive definite

solution which corresponds to the covariance matrix of the barycenter of . Thus .

Using again Theorem 3.6 we conclude that as .

By continuity, (20) follows.

For the first inequality in (21) we write for the matrix of the optimal transportation map from

, to , namely, .

Note that and, as a consequence, , from

which we conclude that

(23)

On the other hand,

which shows that

(24)

Now combining the lower bound (10) with (23) and (24) we obtain

which entails and, therefore,

(25)

Moreover, since

we must have

This and (25) prove the first inequality in (21). To show that , note that

and, therefore,

Last inequality in (21) follows by continuity. Alternatively, using that

together with (15) we see that

which allows us to conclude (21)

with equality if and only if .

Remark 4.3

The already noted fact that convergence in is equivalent to

weak convergence plus convergence of second moments shows that

if and only if

for some (hence, for any) matrix norm.

Remark 4.4

In some cases iterations converge in just one step

to the barycenter. This is the case in dimension , where

(note that in this case the lower bound (20) becomes an equality). More generally,

if we have for all , then ,

for some orthogonal and diagonal . It is easy to check that in this case

If we start the iteration from , then and, again, we achieve convergence in just one step.

As noted before, Theorem 4.2 yields an alternative proof of the already known fact (see

Theorem 6.1 in [1]) that, given there exists a unique

such that

(26)

While this matrix equation is deeply connected to the barycenter problem, we could

read Theorem 4.2 just in terms of approximating the unique solution

of (26). The conclusion becomes that if, starting from any

, we define a sequence of matrices as in (19),

then

Hence, we have provided a consistent iterative method for approximating

the solution of (6).

With this in mind, let us consider now probabilities in a general location-scatter family,

, , and recall that we are assuming

that has a density and it is centered, with as covariance matrix. We focus on the case

(from (3) we see that the barycenter in the general case equals the barycenter

corresponding to the centered probabilities shifted by ).

Now, the discussion at the beginning of this section applies. The minimizer in the

multimarginal formulation is the

law of a random vector with that maximizes

and this depends only on the covariance structure

of . Furthermore, we have seen that among all possible joint covariance matrices, the one that maximizes

is the covariance of the random vector

where ,

and is the unique positive definite solution to the matrix equation (26).

Hence, the barycenter of is the law of

, that is, . Thus we have proved the following

consequence of Theorem 4.2.

Corollary 4.5

If , , where

is has a density and is centered, with as covariance matrix, then the barycenter of

is with and the unique

positive solution of (6). Furthermore, if starting from some positive definite we define as in

(19) then and the bounds (22) to (21)

hold.

To conclude this section we observe that Corollary 4.5 applies, for instance,

to the case of uniform distribution over ellipsoids.

This corresponds to the case where is the uniform distribution over the ball centered at the origin with radius

in (a simple computation shows that is then centered with

as covariance matrix). Now, is the uniform distribution over the ellipsoid

and Corollary 4.5

admits the following interpretation.

On the family of compact convex subsets of with nonvoid interior we could consider the metric

where denotes the uniform distribution on . Given

in that family we could consider the barycenter, namely, the compact convex set that minimizes

provided it exists. In this setup, Corollary 4.5 implies that

the barycenter of a finite collection of ellipsoids is also an ellipsoid.

More precisely, the barycenter of the ellipsoids

is the ellipsoid

with and the unique positive definite solution to

(6). Furthermore, Corollary 4.5 provides an iterative method for the computation

of this barycentric ellipsoid.

Some results in this line, appear in [12] when the sets are required to be convex.

5 Numerical results.

To illustrate the performance of the iteration (19) we have considered the computation

of the Wasserstein barycenters in several different setups. We have applied the iterative procedure

until the difference becomes smaller than a fixed tolerance ( in all the numerical experiments

below). We recall that

is an upper bound for the squared Wasserstein distance .

We have included a comparison to the alternative

iterative procedure considered in [26], which can be summarized as follows. As in Theorem

4.2, we

assume that are symmetric positive semidefinite matrices, with at least one of them positive definite.

We consider and compute, for

(27)

While there is no theoretical consistency result for iteration (27), in [26]

it is noted that the procedure seems to work reasonably well in the case of for bivariate Gaussian distributions. However “for dimension d=3 only for favorable initial matrices convergence is observed and one has to use specific methods of numerical analysis for the solution of this nonlinear equation” (sic).

Figure 1 shows results for the case of centered, bivariate

Gaussian distributions. We have considered three different setups. In the top row we have considered

, and . In the middle row we consider and as before,

and , while the bottom row deals with the same ,

and plus

and

and weights , .

The ellipses are shown

in blue, while in black we see the iterants .

The number of iterations needed to reach the prespecified tolerance is written on top of each graph.

The graphs on the left column correspond to the proposal in this paper, iteration (19), while

the right column shows the performance of iteration (27). In all cases we have taken .

In the top right graph and in agreement with Remark 4.4 (note that and conmute),

we see that iteration (19) has found the barycenter after just

one step (the displayed value comes from the fact that the iterative procedure computes a further

approximation before checking that the decrease in the target function is below the tolerance and stopping). In contrast, it takes 14 iterations

to (27) to reach convergence. Moving away from this particular case of common principal axis,

in the middle and bottom row we see that our method converges fast (5 iterations) to the barycenter, again

with somewhat slower convergence for the iteration (27).

For a more complete evaluation of the performance of iteration (19), as well as comparison

to (27), we have considered a simulation setup with several choices of dimension,

and number of Gaussian distributions, . For each combination of and we have considered

randomly generated, positive definite matrices . Each is generated from a Wishart distribution,

independently of the others. We have used the iteration until convergence (again with tolerance ) and have recorded the required number

of iterations. The whole procedure has been replicated 1000 times. In Table 3 we report the average number of iterations needed for convergence

for each combination of and . The left table corresponds to our proposal (19) and the right table to (27).

We see that, while the number of iterations grows with dimension, in the case of iteration (19) this number remains moderate, even more so for large values of . We also see that the number of iterations tends to be smaller for larger (of course,

the computational cost of each step is higher as both and increase). In contrast, iteration (27) is worse affected

by an increase in dimensionality and its performance is uniformly worse than that of (19).

2

3

5

10

20

2

6.8

7.7

7.8

7.7

7.5

3

9.3

10.1

10.0

9.3

8.6

5

12.2

13.1

12.6

11.2

9.9

10

17.5

18.3

16.4

13.3

11.3

20

22.7

24.1

20.4

15.3

12.3

50

31.8

33.6

25.7

17.3

13.5

2

3

5

10

20

2

20.6

19.1

17.6

16.4

15.7

3

29.1

24.0

21.3

18.8

17.5

5

41.0

31.3

25.6

21.6

19.4

10

66.9

44.2

32.0

25.2

21.9

20

106.9

58.9

38.6

28.4

23.9

50

185.5

82.4

47.7

32.1

26.5

Table 3: Average iteration numbers for convergence. Left: iteration (19); right: (27)

Finally, we would like to remark that our numerical experiments show a fast rate of convergence of iteration (19)

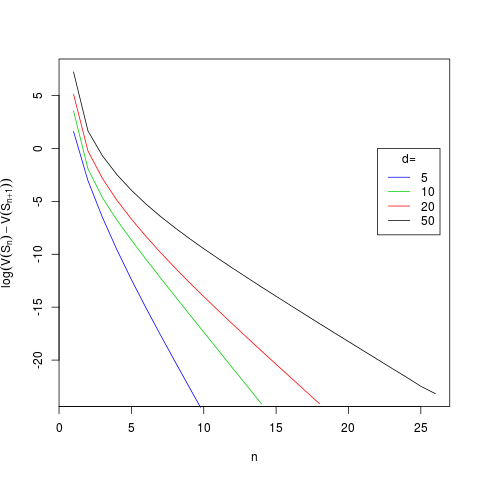

to the Wasserstein barycenter. To illustrate this we have included Figure 2. For this graph we

have considered dimensions . For each of these dimensions we have randomly generated (again from a Wishart distribution)

five positive definite matrices and have used iteration (19). We show the decrease of

with the number of iterations, . We see that in al cases shows a linear decrease with . Since

is an upper bound for , this indicates an exponential decrease

of and, consequently, exponentially fast convergence of towards

the barycenter . We believe that this fast convergence of the iterative procedure in this paper deserves further

research that will be reported elsewhere.

Acknowledgements

We want to express our sincere acknowledgements to a referee by his/her constructive and right remarks on our manuscript, leading to a notable improvement of the paper.

Figure 2: log-decrease of target function for iteration (19), different dimensions

References

[1] Agueh, M. and Carlier, G. (2011). Barycenters in the Wasserstein space. SIAM J. Math Anal.

43, 904–924.

[2] Álvarez-Esteban, P.C., del Barrio, E. Cuesta-Albertos, J.A. and Matrán, C. (2011).

Uniqueness and approximate computation of optimal incomplete transportation plans. Ann. Institut Henri Poincaré

- P & S, 47, 358–375.

[3] Álvarez-Esteban, P.C., del Barrio, E. Cuesta-Albertos, J.A. and Matrán, C. (2015). Wide consensus for parallelized inference. Submitted.

[4] Ambrosio, L., Gigli, N. and Savaré, G. (2008). Gradient Flows in Metric Spaces and in the Space of Probability

Measures, 2nd ed. Birkhäuser.

[5] Benamou, J. D., Carlier, G., Cuturi, M., Nenna, L., and Peyre, G. (2015). Iterative Bregman projections

for regularized transportation problems. SIAM J. Sci. Comput., 37(2), 1111–1138.

[6] Bhatia, R. (1997). Matrix Analysis. Springer.

[7] Bishop, A. N., and Doucet, A. (2014). Distributed nonlinear consensus in the space of probability measures. arXiv Preprint arXiv:1404.0145.

[8] Brenier, Y. (1987) Polar decomposition and increasing rearrangement of vector

fields. C. R. Acad. Sci. Paris Ser. I Math., 305, 805–808.

[9] Brenier, Y. (1991). Polar factorization and monotone rearrangement of vector-

valued functions. Comm. Pure Appl. Math., 44, 375–417.

[10]

Carlier, G., Oberman, A., and Oudet, E. (2015). Numerical methods for matching for teams and Wasserstein barycenters. ESAIM Math. Model. Numer. Anal., to appear.

[11] Cuesta-Albertos, J. A. and Matrán, C. (1989). Notes on the Wasserstein metric in Hilbert spaces. Ann. Probab., 17, 1264–1276.

[12]

Cuesta-Albertos, J. A., Matrán, C., and Rodríguez-Rodríguez, J. (2003).

Approximation to probabilities through uniform laws on convex sets.

J. Theoretical Probab., 16, 363-376.

[13]Cuesta-Albertos, J. A., Matrán, C., and Tuero-Díaz, A. (1996). On lower bounds for the Wasserstein metric in a Hilbert space. J. Theoretical Probab., 9(2), 263–283.

[14]

Cuesta-Albertos, J. A., Matrán, C. and

Tuero-Díaz,, A. (1997). Optimal transportation plans and convergence in distribution. J. Multivariate Anal., 60, 72–83.

[15]

Cuesta-Albertos, J. A., Rüschendorf, L., and Tuero-Díaz, A. (1993). Optimal coupling of multivariate distributions and stochastic processes. J. Multivariate Anal., 46, 335–361.

[16]

Cuturi, M. and Doucet, A. (2013). Fast Computation of Wasserstein Barycenters, in Proceedings of the 31st International Conference on Machine Learning, 2014.

[17] Dudley, R. M. (1989). Real Analysis and Probability. Wadsworth & Brooks.

[18]

Evans, L.C. and Gariepy, R.F. (1992). Measure Theory and Fine Properties of Functions. Studies in Advanced Mathematics. CRC Press, Boca Raton,

FL.

[19]

Gelbrich, M. (1990). On a formula on the Wasserstein metric between measures on Euclidean and Hilbert spaces. Math. Nachr. 147, 185–203.

[20]

Le Gouic, T. and Loubes, J.M. (2015). Existence and consistency of Wasserstein barycenters. hal-01163262

[21]

Knott, M. and Smith, C. S. (1987). Note on the optimal transportation of distributions. J. Optimization Theory and Appl. 52, 323–329.

[22]

Knott, M. and Smith, C. S. (1994). On a generalization of cyclic-monotonicity

and distances among random vectors, Linear Algebra Appl.,199, 36–371.

[23]

McCann, R. J. (1995). Existence and uniqueness of monotone measure-preserving maps. Duke Mathematical Journal 80, 309–323.

[24] Niculescu, P. N. and Persson, L. E. (2006). Convex Functions and

their Applications: A Contemporary Approach. Springer.

[25] Rüschendorf, L. and Rachev, S. T. (1990). A characterization of random variables with minimum -distance. J. Multivariate Anal., 32, 48–54.

[26]

Rüschendorf, L., and Uckelmann, L. (2002). On the -coupling problem. J. Multivariate Anal., 81(2), 242–258. doi:10.1006/jmva.2001.2005

[27] Villani, C. (2003). Topics in Optimal Transportation. American Mathematical Society.

[28] Villani, C. (2008). Optimal transport: Old and New, Vol. 338. Springer Science &

Business Media.