Classification methods applied to credit scoring: A systematic review and overall comparison

Abstract

The need for controlling and effectively managing credit risk has led financial institutions to excel in improving techniques designed for this purpose, resulting in the development of various quantitative models by financial institutions and consulting companies. Hence, the growing number of academic studies about credit scoring shows a variety of classification methods applied to discriminate good and bad borrowers. This paper, therefore, aims to present a systematic literature review relating theory and application of binary classification techniques for credit scoring financial analysis. The general results show the use and importance of the main techniques for credit rating, as well as some of the scientific paradigm changes throughout the years.

keywords:

Credit Scoring, Binary Classification Techniques, Literature Review, Basel Accords.1 Introduction

The need for credit analysis was born in the beginnings of commerce in conjunction with the borrowing and lending of money, and the purchasing authorisation to pay any debt in future. However, the modern concepts and ideas of credit scoring analysis emerged about 70 years ago with Durand (1941). Since then, traders have begun to gather information on the applicants for credit and catalog them to decide between lend or not certain amount of money (Banasik et al., 1999; Marron, 2007; Louzada et al., 2012b).

According to Thomas et al. (2002) credit scoring is ”a set of decision models and their underlying techniques that aid credit lenders in the granting of credit”. A broader definition is considered in the present work: credit scoring is a numerical expression based on a level analysis of customer credit worthiness, a helpful tool for assessment and prevention of default risk, an important method in credit risk evaluation, and an active research area in financial risk management.

At the same time, the modern statistical and data mining techniques have given a significant contribution to the field of information science and are capable of building models to measure the risk level of a single customer conditioned to his characteristics, and then classify him as a good or a bad payer according to his risk level. Thus, the main idea of credit scoring models is to identify the features that influence the payment or the non-payment behaviour of the costumer as well as his default risk, occurring the classification into two distinct groups characterised by the decision on the acceptance or rejection of the credit application (Han et al., 2006).

Since the Basel Committee on Banking Supervision released the Basel Accords, specially the second accord from 2004, the use of credit scoring has grown considerably, not only for credit granting decisions but also for risk management purposes. The internal rating based approaches allows the institutions to use internal ratings to determine the risk parameters and therefore, to calculate the economic capital of a portfolio Basel III, released in 2013, renders more accurate calculations of default risk, especially in the consideration of external rating agencies, which should have periodic, rigorous and formal comments that are independent of the business lines under review and that reevaluates its methodologies and models and any significant changes made to them (Rohit et al., 2013; RBNZ, 2013).

Hence, the need for an effective risk management has meant that financial institutions began to seek a continuous improvement of the techniques used for credit analysis, a fact that resulted in the development and application of numerous quantitative models in this scenario. However, the chosen technique is often related to the subjectivity of the analyst or state of the art methods. There are also other properties that usually differ, such as the number of datasets applied to verify the quality of performance capability or even other validation and misclassification cost procedures. These are natural events, since credit scoring has been widely used in different fields, including propositions of new methods or comparisons between different techniques used for prediction purposes and classification.

A remarkable, large and essential literature review was presented in the paper by Hand and Henley (1997), which discuss important issues of classification methods applied to credit scoring. Other literature reviews were also conducted but only focused on some types of classification methods and discussion of the methodologies, namely Xu et al. (2009), Shi (2010), Lahsasna et al. (2010a) and Nurlybayeva and Balakayeva (2013). Also, Garcia et al. (2014) performed a systematic literature review, but limiting the study to papers published between 2000 and 2013, these authors provided a short experimental framework comparing only four credit scoring methods. Lessmann et al. (2015) in their review considered 50 papers published between 2000 and 2014 and provided a comparison of several classifications methods in credit scoring. However, it is known that there are several different methods that may be applied for binary classification and they may be encompassed by their general methodological nature and can be seem as modifications of others usual existing methods. For instance, linear discriminant analysis has the same general methodological nature of quadratic discriminant analysis. In this sense, even though Lessmann et al. (2015) considered several classification methods they did not consider general methodologies as genetic and fuzzy methods.

This paper, therefore, we aim to present a more general systematic literature review over the application of binary classification techniques for credit scoring, which features a better understanding of the practical applications of credit rating and its changes over time. In the present literature review, we aim to cover more than 20 years of researching (1992-2015) including 187 papers, more than any literature review already carried out so far, completely covering this partially documented period in different papers. Furthermore, we present a primary experimental simulation study under nine general methodologies, namely, neural networks, support vector machine, linear regression, decision trees, logistic regression, fuzzy logic, genetic programming, discriminant analysis and Bayesian networks, considering balanced and unbalanced databases based on three retail credit scoring datasets. We intent to summarise researching findings and obtain useful guidance for researchers interested in applying binary classification techniques for credit scoring.

The remainder of this paper is structured as follows. In Section 2 we present the conceptual classification scheme for the systematic literature review, displaying some important practical aspects of the credit scoring techniques. The main credit scoring techniques are briefly presented in Section 3. In Section 4 we present the results of the systematic review under the eligible reviewed papers, as well as the systematic review over four different time periods based on a historical economic context. In Section 5 we compare all presented methods on a replication based study. Final comments in Section 6 end the paper.

2 Survey methodology

Systematic review, also known as systematic review, is an adequate alternative for identifying and classifying key scientific contributions to a field on a systematic, qualitative and quantitative description of the content in the literature. Interested readers can refer to Hachicha and Ghorbel (2012) for more details on systematic literature review. It consists on an observational research method used to systematically evaluate the content of a recorded communication (Kolbe and Brunette, 1991).

Overall, the procedure for conducting a systematic review is based on the definition of sources and procedures for the search of papers to be analysed, as well as on the definition of instrumental categories for the classification of the selected papers, here based on four categories to understand the historical application of the credit scoring techniques: year of publication, title of the journal where the paper was published, name of the co-authors, and conceptual scheme based on 12 questions to be answered under each published paper. For this purpose, there is a need for defining the criteria to select credit scoring papers in the research scope. Thus, two selection criteria are used in this paper to select papers related to the credit scoring area to be included in the study:

-

1.

The study is limited to the published literature available on the following databases: Sciencedirect, Engineering Information, Reaxys and Scopus, covering 20,500 titles from 5,000 publishers worldwide.

-

2.

The systematic review restricts the study eligibility to journal papers in English, especially considering ’credit scoring’ as a keyword related to ’machine learning’, ’data mining’, ’classification’ or ’statistic’ topics. Other publication forms such as unpublished working papers, master and doctoral dissertations, books, conference in proceedings, white papers and others are not included in the review. The survey horizon covers a period of almost two decades: from January 1992 to December 2015.

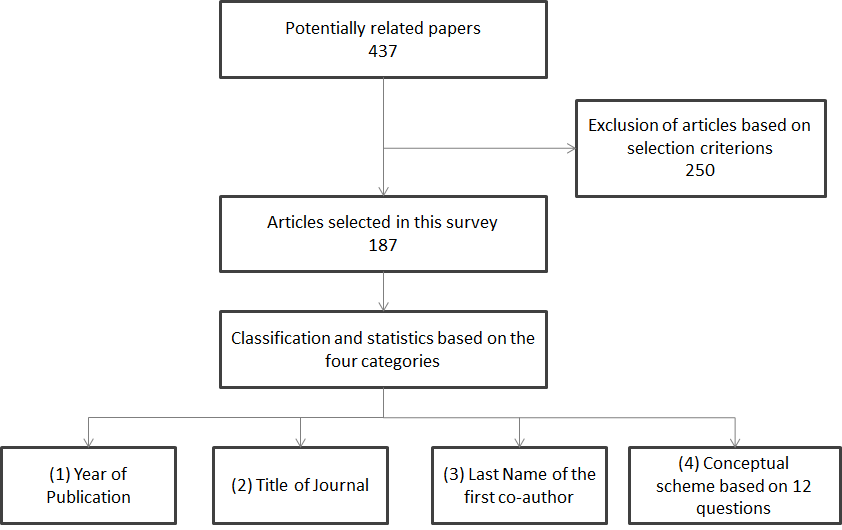

The papers were selected according to the procedure shown in Figure 1. From 437 papers eligible as potentially related to credit scoring, 250 were discarded due to not meeting the second selection criterion. The 187 papers included in the study were subjected to the systematic review, according to 12 questions on the conceptual scenario over the techniques: What is the main objective of the paper? What is the type of the main classification method? Which type the datasets used? Which is the type of the explanatory variables? Does the paper perform variable selection methods? Was missing values imputation performed? What is the number of datasets used in the paper? Was performed exhaustive simulation study? What is the type of validation of the approach? What is the type of misclassification cost criterion? Does the paper use the Australian or the German datasets? Which is the principal classification method used in comparison study? The 12 questions and possible answers are shown in Table A.1 in the Appendix.

2.1 The main objective of the papers

Although a series of papers is focused on the same area, they have different specific objectives. One can separate them in general similar aims. In the present work, we consider seven types of main objectives: proposing a new method for rating, comparing traditional techniques, conceptual discussions, feature selection, literature review, performance measures studies and, at last, other issues. Conceptual discussions account for papers that deal with problems or details of the credit rating analysis. In other issues, were included papers that presented low frequency objectives.

In the proposition of new methods, Lee et al. (2002) introduce a discriminant neural model to perform credit rating, Gestel et al. (2006) propose a support vector machine model within a Bayesian evidence framework. Hoffmann et al. (2007) propose a boosted genetic fuzzy model, Hsieh and Hung (2010) using a combined method that covers neural networks, support vector machine and bayesian networks.

Shi (2010) performed a systematic literature review that covers multiple criteria linear programming models applied to credit scoring from 1969 to 2010. Other literature reviews were performed by Hand and Henley (1997); Gemela (2001); Xu et al. (2009); Shi (2010); Lahsasna et al. (2010a); Van Gool et al. (2012).

Among the papers that perform a conceptual discussion, Bardos (1998) presents tools used by the Banque de France, Banasik et al. (1999) discusses how hazard models could be considered in order to investigate when the borrowers will default, Hand (2001a) discusses the applications and challenges in credit scoring analysis. Martens et al. (2010) performs an application in credit scoring and discusses how their tool fits into a global Basel II credit risk management system. Other examples about conceptual discussion may be seen in Chen and Huang (2003), Marron (2007) and Thomas (2010).

In comparison of traditional techniques, West (2000) compared five neural network model with traditional techniques. The results indicated that neural network can improve the credit scoring accuracy and also that logistic regression is a good alternative to the neural networks. Baesens et al. (2003) performed a comparison involving discriminant analysis, logistic regression, logic programing, support vector machines, neural networks, bayesian networks, decision trees and k-nearest neighbor. The authors concluded that many classification techniques yield performances which are quite competitive with each other. Other important comparisons may be seen in Adams et al. (2001); Hoffmann et al. (2002); Ong et al. (2005); Baesens et al. (2005); Wang et al. (2005); Lee et al. (2006); Huang et al. (2006b); Xiao et al. (2006); Van Gestel et al. (2007); Martens et al. (2007); Hu and Ansell (2007); Tsai (2008); Abdou et al. (2008); Sinha and Zhao (2008); Luo et al. (2009); Finlay (2009); Abdou (2009); Hu and Ansell (2009); Finlay (2010); Wang et al. (2011). Also, Liu and Schumann (2005); Somol et al. (2005); Tsai (2009); Falangis and Glen (2010); Chen and Li (2010); Yu and Li (2011); McDonald et al. (2012); Wang et al. (2012b) handled features selection. Hand and Henley (1997); Gemela (2001); Xu et al. (2009); Shi (2010); Lahsasna et al. (2010a); Van Gool et al. (2012) produced their work in literature review. Yang et al. (2004); Hand (2005a); Lan et al. (2006); Dryver and Sukkasem (2009) worked in performance measures. There are other papers covering model selection (Ziari et al., 1997), sample impact (Verstraeten and Van Den Poel, 2005), interval credit (Rezac, 2011), segmentation and accuracy (Bijak and Thomas, 2012).

2.2 The main peculiarities of the credit scoring papers

Overall the main classification methods in credit scoring are neural networks (NN) (Ripley, 1996), support vector machine (SVM) (Vapnik, 1998), linear regression (LR) (Hand and Kelly, 2002), decision trees (TREES) (Breiman et al., 1984), logistic regression (LG) (Berkson, 1944), fuzzy logic (FUZZY) (Zadeh, 1965), genetic programming (Koza, 1992), discriminant analysis (DA) (Fisher, 1986), Bayesian networks (BN) (Friedman et al., 1997), hybrid methods (HYBRID) (Lee et al., 2002), and ensemble methods (COMBINED), such as bagging (Breiman, 1996), boosting (Schapire, 1990), and stacking (Wolpert, 1992).

In comparison studies, the principal classification methods involve traditional techniques considered by the authors to contrast the predictive capability of their proposed methodologies. However, hybrid and ensemble methods are seldom used in comparison studies because they involve a combination of other traditional methods.

The main classification methods in credit scoring are briefly presented in the Section 3 as well as other issues related to credit scoring modeling, such as, types of the datasets used in the papers (public or not public),the use of the so called Australian or German datasets, type of the explanatory variables, feature selection methods, missing values imputation (Little and Rubin, 2002) number of datasets used, exhaustive simulations, validation approach, such as holdout sample, K-fold, leave one out, trainng/validation/test, misclassification cost criterions, such as Receiver Operating Characteristic (ROC) curve, metrics based on confusion matrix, accuracy (ACC), sensitivity (SEN), specificity (SPE), precision (PRE), false Positive Rate (FPR), and other traditional measures used in credit scoring analysis are F-Measure and two-sample K-S value.

3 The main classification methods in credit scoring

In this section, the main techniques used in credit scoring and their applications are briefly explained and discussed.

Neural networks (NN). A neural network (Ripley, 1996) is a system based on input variables, also known as explanatory variables, combined by linear and non-linear interactions through one or more hidden layers, resulting in the output variables, also called response variables. Neural networks were created in an attempt to simulate the human brain, since it is based on sending electronic signals between a huge number of neurons. The NN structure have elements which receive an amount of stimuli (the input variables), create synapses in several neurons (activation of neurons in hidden layers), and results in responses (output variables). Neural networks differ according to their basic structure. In general, they differ in the number of hidden layers and the activation functions applied to them. West (2000) shows the mixture-of-experts and radial basis function neural network models must consider for credit scoring models. Lee et al. (2002) proposed a two-stage hybrid modeling procedure to integrate the discriminant analysis approach with artificial neural networks technique. More recently, different artificial neural networks have been suggested to tackle the credit scoring problem: probabilistic neural network (Pang, 2005), partial logistic artificial neural network (Lisboa et al., 2009), artificial metaplasticity neural network (Marcano-Cedeno et al., 2011) and hybrid neural networks (Chuang and Huang, 2011). In some datasets, the neural networks have the highest average correct classification rate when compared with other traditional techniques, such as discriminant analysis and logistic regression, taking into account the fact that results were very close (Abdou et al., 2008). Possible particular methods of neural networks are feedforward neural network, multi-layer perceptron, modular neural networks, radial basis function neural networks and self-organizing network.

Support vector machine (SVM). This technique is a statistical classification method and introduced by Vapnik (1998). Given a training set , with , where is the explanatory variable vector, and represents the binary category of interest, and denotes the number of dimensions of input vectors. SVM attempts to find an optimal hyper-plane, making it a non-probabilistic binary linear classifier. The optimal hyper-plane could be written as follows:

where is the normal of the hyper-plane, and is a scalar threshold. Considering the hyper-plane separable with respect to and with geometric distance , the procedure maximizes this distance, subject to the constraint . Commonly, this maximization may be done through the Lagrange multipliers and using linear, polynomial, Gaussian or sigmoidal separations. Just recently support vector machine was considered a credit scoring model (Chen et al., 2009). Li et al. (2006); Gestel et al. (2006); Xiao and Fei (2006); Yang (2007); Chuang and Lin (2009); Zhou et al. (2009, 2010); Feng et al. (2010); Hens and Tiwari (2012); Ling et al. (2012) used support vector machine as main technique for their new method. Possible particular methods of SVM are radial basis function least squares support vector machine, linear least-squares support vector machine, radial basis function, support vector machine and linear support vector machine.

Linear regression (LR). The linear regression analysis has been used in credit scoring applications even though the response variable is a two class problem. The technique sets a linear relationship between the characteristics of borrowers and the target variable , as follows,

where is the random error and independent of . Ordinary least squares is the traditional procedure to estimate , being the estimated vector. Once is a binary variable, the conditional expectation may be used to segregate good borrowers and bad borrowers. Since , the output of the model cannot be interpreted as a probability. Hand and Kelly (2002) built a superscorecard model based on linear regression. Karlis and Rahmouni (2007) propose the Poisson mixture models for analyzing the credit-scoring behaviour for individual loans. Other authors have been working with linear regression models or its generalizations in credit scoring (Hand and Kelly, 2002; Banasik et al., 2003; Karlis and Rahmouni, 2007; Efromovich, 2010).

Decision trees (TREES). Classification and Regression Trees (Breiman et al., 1984) is a classification method which uses historical data to construct so-called decision rules organized into tree-like architectures. In general, the purpose of this method is to determine a set of if-then logical conditions that permit prediction or classification of cases. There are three usual tree’s algorithms: chi-square automatic interaction detector (CHAID), classification and regression tree (CART) and C5, which differ by the criterion of tree construction, CART uses gini as the splitting criterion, C5 uses entropy, while CHAID uses the chi-square test (Yap et al., 2011). John et al. (1996) exhibit a rule based model implementation in a stock selection. Bijak and Thomas (2012) used CHAID and CART to verify the segmentation value in the performance capability. Kao et al. (2012) proposes a combination of a Bayesian behavior scoring model and a CART-based credit scoring model. Other possible and particular methods of decision trees are C4.5 decision trees algorithm and J4.8 decision trees algorithm.

Logistic regression (LG). Proposed by Berkson (1944), the logit model considers a group of explanatory variables and a response variable with two categories , the technique of logistic regression consists in the estimation of a linear combination between and the logit transformation of . Thus, if we consider as the category of interest for analysis, the model can be represented as , where and is the vector containing the model’s coefficients. Alternatively, the model can be represented by,

| (1) |

where is the probability of the individual to belong to category , conditioned to . The logistic regression model is a traditional method, often compared with other techniques (Li and Hand, 2002; Hand, 2005a; Lee and Chen, 2005; Abdou et al., 2008; Yap et al., 2011; Pavlidis et al., 2012) or it is used in technique combinations (Louzada et al., 2011). Other possible and particular methods of logistc regression are regularized logistic regression and limited logistic regression.

Fuzzy logic (FUZZY). Zadeh (1965) introduced the Fuzzy Logic as a mathematical system which deals with modeling imprecise information in the form of linguistic terms, providing an approximate answer to a matter based on knowledge that is inaccurate, incomplete or not completely reliable. Unlike the binary logic, fuzzy logic uses the notion of membership to handle the imprecise information. A fuzzy set is uniquely determined by its membership function, which can be triangular, trapezoidal, Gaussian, polynomial or sigmoidal function. Hoffmann et al. (2002) performed an evaluation of two fuzzy classifiers for credit scoring. Laha (2007) proposes a method of building credit scoring models using fuzzy rule based classifiers. Lahsasna et al. (2010b) investigated the usage of Takagi-Sugeno (TS) and Mamdani fuzzy models in credit scoring. Possible methods in fuzzy logic are regularized adaptive network based Fuzzy inference systems and fuzzy Adaptive Resonance.

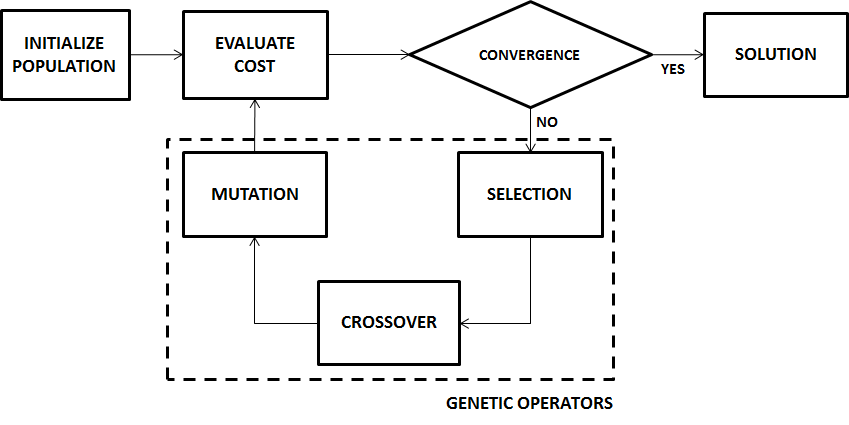

Genetic programming (GENETIC). Genetic Programming (Koza, 1992) is based on mathematical global optimization as adaptive heuristic search algorithms, its formulation is inspired by mechanisms of natural selection and genetics. Basically, the main goal of a genetic algorithm is to create a population of possible answers to the problem and then submit it to the process of evolution, applying genetic operations such as crossover, mutation and reproduction. The crossover is responsible for exchanging bit strings to generate new observations. Figure 2 shows the optimization process of a genetic algorithm. Ong et al. (2005) propose a genetic credit scoring model and compares this with traditional techniques. Huang et al. (2006a) introduce a two-stage genetic programming. Many other authors have investigated genetic models in application of credit scoring (Chen and Huang, 2003; Mues et al., 2004; Abdou, 2009; Won et al., 2012). Other possible methods in genetic programming are the two stages genetic programming and genetic algorithm knowledge refinement.

Discriminant analysis (DA). Introduced by Fisher (1986), the discriminant analysis is based on the construction of one or more linear functions involving the explanatory variables. Consequently, the general model is given by

where represents the discrimination score, the intercept, represents the coefficient responsible for the linear contribution of the explanatory variable , where .

This technique has the following assumptions: (1) the covariance matrices of each classification subset are equal. (2) Each classification group follows a multivariate normal distribution. Frequently, the linear discriminant analysis is compared with other credit scoring techniques (West, 2000; Gestel et al., 2006; Akkoc, 2012) or is subject of studies of new procedures to improve its accuracy (Yang, 2007; Falangis and Glen, 2010). Other possible method in discriminant analysis is quadratic discriminant analysis.

Bayesian networks (BN). A Bayesian classifier (Friedman et al., 1997) is based on calculating a posterior probability of each observation belongs to a specific class. In other words, it finds the posterior probability distribution , where is a random variable to be classified featuring categories, and is a set of explanatory variables. A Bayesian classifier may be seen as a Bayesian network (BNs): a directed acyclic graph (DAG) represented by the triplet (, , ), where are the nodes, are the edges and is a set of probability distributions and its parameters. In this case, the nodes represent the domain variables and edges the relations between these variables. Giudici (2001) presents a conditional Bayesian independence graph to extract insightful information on the variables association structure in credit scoring applications. Gemela (2001) applied bayesian networks in a credit database of annual reports of Czech engineering enterprises. Other authors that have investigated Bayesian nets in credit scoring models are Zhu et al. (2002); Antonakis and Sfakianakis (2009); Wu (2011). Possible methods in Bayesian networks are naive Bayes, tree augmented naive Bayes and gaussian naive Bayes.

Hybrid methods (HYBRID). Hybrid methods combine different techniques to improve the performance capability. In general, this combination can be accomplished in several ways during the credit scoring process. Lee et al. (2002) proposed a hybrid method that integrates the backpropagation neural networks with traditional discriminant analysis to evaluate credit scoring. Huang et al. (2007) proposed a hybrid method that integrates genetic algorithm and support vector machine to perform feature selection and model parameters optimisation simultaneously, as well as Lee et al. (2002); Lee and Chen (2005); Hsieh (2005); Huysmans et al. (2006); Shi (2009); Chen et al. (2009); Liu et al. (2010); Ping and Yongheng (2011); Capotorti and Barbanera (2012); Vukovic et al. (2012); Akkoc (2012); Pavlidis et al. (2012) also work with hybrid methods.

Ensemble methods (COMBINED). The ensemble procedure refers to methods of combining classifiers, thereby multiple techniques are applied to solve the same problem in order to boost credit scoring performance. There are three popular ensemble methods: bagging (Breiman, 1996), boosting (Schapire, 1990), and stacking (Wolpert, 1992). The Hybrid methods can be regarded as a particular case of stacking, but in this paper we consider as stacking only the methods which use this terminology. Wang et al. (2012a) proposed a combined bagging decision tree to reduce the influences of the noise data and the redundant attributes of data. Many other authors have chosen to deal with combined methods Hoffmann et al. (2007); Hsieh and Hung (2010); Paleologo et al. (2010); Zhang et al. (2010); Finlay (2011); Louzada et al. (2011); Xiao et al. (2012); Marques et al. (2012b) in credit scoring problems.

3.1 Other issues related to credit scoring modeling

Types of the datasets used. As much as nowadays the information is considered easy to access, mainly because of the modernization of the web and large data storage centers, the availability of data on the credit history of customers and businesses is still difficult to access. Datasets which contain confidential information on applicants cannot be released to third parties without careful safeguards (Hand, 2001b). Not rarely, public data sets are used for the investigation of techniques and methodologies of credit rating. In this sense, the type of dataset used (public or not public) in the papers is an important issue.

Type of the explanatory variables. The explanatory variables, often known as covariates, predictor attributes, features, predictor variables or independent variables, usually guide the choice and use of a classification method. In general, the type of each explanatory variable may be continuous (interval or ratio) or categorical (nominal, dichotomous or ordinal). A common practice is to discretize a continuous attribute as done by Gemela (2001); Mues et al. (2004); Ong et al. (2005); Wu (2011). In this paper, we consider a continuous dataset to be the one that contains only interval or ratio explanatory variables - independent if a discretization method is applied or not, and a categorical dataset presents only categorical explanatory variables. A mixed dataset is composed by both types of variable.

Feature selection methods. When we use data to try to provide a credit rating, we use the number of variables that, in short, explain and predict the credit risk. Some methods provide a more accurate classification, discarding irrelevant features. Thus, it is a common practice to apply such methods when one proposes a rating model. Some authors used a variable selection procedure in their papers such as Lee et al. (2002); Verstraeten and Van Den Poel (2005); Abdou et al. (2008); Chen and Li (2010); Marques et al. (2012b). Authors, who did not cite or discuss feature selection methods in their papers, were regarded as nonusers.

Missing values imputation. The presence of missing values in datasets is a recurrent statistical problem in several application areas. In credit analysis, internal records may be incomplete for many reasons: a registration poorly conducted, the customers can fail to answer to questions, or the database or recording mechanisms can malfunction. One possible approach is to drop the missing values from the original dataset, as done by Adams et al. (2001); Berger et al. (2005); Won et al. (2012) or perform a preprocessing to replace the missing values, as done by Banasik et al. (2003); Baesens et al. (2005); Paleologo et al. (2010). These procedures are known as missing data imputation (Little and Rubin, 2002).

Number of datasets used. In general, authors must prove the efficiency of their rating methods on either real or simulated datasets. However, due to the difficulty of obtaining data in the credit area, many times the number of datasets used can be small, or even engage the use of other real datasets that prove the efficiency of the rating method. Lan et al. (2006) used 16 popular datasets in the experiments that testify performance measures and which was applied in a credit card application.

Exhaustive simulations. The exhaustive simulations study are based on monte carlo sample replications and the statistical comparisons to assess the performance of the estimation procedure. In this sense, artificial samples with specific properties are randomly generated. Ziari et al. (1997); Hardle et al. (1998); Banasik et al. (2003); Louzada et al. (2012b, a) are some examples of authors who performed exhaustive simulations in credit scoring analysis.

Validation approach. Amongst the various validation procedures we point out:

-

Holdout sample. This validation method involves a random partition of the dataset into two subsets: the first, called training set is designed to be used in the model estimation phase. The second, called test set, is used to perform the evaluation of the respective model. Therefore, the model is fitted based on the training set aimed to predict the cases in the test set. A good performance in the second dataset indicates that the model is able to generalize the data, in other words, there is no overfitting on the training set.

-

K-fold. This method is a generalization of the hold out method, meanwhile the data set is randomly partitioned into K subsets. Each subset is used as a test set for the model fit considering the other K-1 subsets as training set. In this approach, the entire dataset is used for both training and testing the model. Typically, a value of K=10 is used in the literature (Mitchell, 1997).

-

Leave One Out. This method is an instance of K-fold where K is equal to the size of the dataset. Each case is used as a test set for the model fit considering the other cases as training set. In this approach, the entire dataset is used for both training and testing models. It is worth to mention that on large datasets a computational difficulty may arise.

-

Train/validation/test. This validation approach is an alternative of the holdout case for large datasets, the purpose is to avoid some overfitting into the validation set. The training samples are used to develop models, the validation samples are used to estimate the prediction error for the model selection, the test set is used to evaluate the generalization error of the final model chosen. For this, the performance of the selected model should be confirmed through the measuring of the performance on a third independent dataset denominated test set (Bishop, 1995). A common split is 50% for training, 25% each for validation and test.

Misclassification cost criterions. Amongst the various misclassification criterions we point out:

-

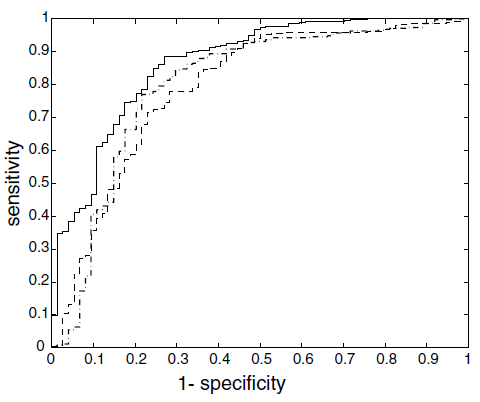

ROC curve. The Receiver Operating Characteristic curve was introduced by Zweig and Campbell (1993) and may be geometrically defined as a graph for visualizing the performance of a binary classifier technique. The ROC curve is obtained by measuring the 1?specificity on the first axis and measured the sensitivity on the second axis, creating a plane. Therefore, the more the curve distances from the main diagonal, the better is the model performance. Figure 3 shows an example of ROC Curve.

Figure 3: The Receiver operating characteristic curves used by Gestel et al. (2006) to compare support vector machine (solid line), logistic regression (dashed-dotted line) and linear discriminant analysis (dashed line). -

Metrics based on confusion matrix. Its aim is to compare the model’s predictive outcome with the true response values in the dataset. A misclassification takes place when the modeling procedure fails to correctly allocate an individual into the correct category. A traditional procedure is to build a confusion matrix, as shown in Table 1, where is the model prediction, is the real values in data set, the number of true positives, F P the number of false positives, the number of false negatives and the number of true negatives. Naturally, , where is the number of observations.

Table 1: Confusion matrix. {1} {0} {1} {0} Through the confusion matrix, some measures are employed to evaluate the performance on test samples.

Accuracy (ACC): the ratio of correct predictions of a model, when classifying cases into class or . ACC is defined as

Sensitivity (SEN): also known as Recall or True Positive Rate is the fraction of the cases that the technique correctly classified to the class among all cases belonging to the class . SEN is defined as

Specificity (SPE): also known as True Negative Rate is the ratio of observations correctly classified by the model into the class among all cases belonging to the class . SPE is defined as

Precision (PRE): is the fraction obtained as the number of true positives divided by the total number of instances labeled as positive. It is measured as False Negative Rate (FNR) also known as Type I Error is the fraction of cases misclassified as belonging to the class. It is measured as

False Positive Rate (FPR) also known as Type II Error is the fraction of cases misclassified as belonging to the class. It is measured as

Other traditional measures used in credit scoring analysis are F-Measure and two-sample K-S value. The F-Measure combines both Precision and Recall, while the K-S value is used to measure the maximum distance between the distribution functions of the scores of the ’good payers’ and ’bad payers’.

Using the Australian and German dataset. The Australian and German datasets are two public UCI (Bache and Lichman, 2013) datasets concerning approved or rejected credit card applications. The first has 690 cases, with 6 continuous explanatory variables and 8 categorical explanatory variables. The second has 1000 instances, with 7 continuous explanatory, 13 categorical attributes. All the explanatory variables’ names and values are encrypted by symbols. The use of these benchmark datasets is frequent in credit rating papers and the comparison of the overall classification performance in both cases is a common practice for the solidification of a proposed method. Ling et al. (2012) shows an accuracy comparison of different authors and techniques for Austrian and German datasets.

Principal methods for comparison. The principal classification methods in comparison studies involve traditional techniques considered by the authors to contrast the predictive capability of their proposed methodologies. However, hybrid and ensemble techniques are rarely used in comparison studies because they involve a combination of other traditional methods.

4 Results and discussion

In this section we present the general results of the reviewed papers. We discuss the classification of papers according to the year of publication, scientific journal, author and conceptual scenery. Moreover, we present a more detailed analysis and discussion of the systematic review for each time period, I, II, III and IV.

4.1 General results

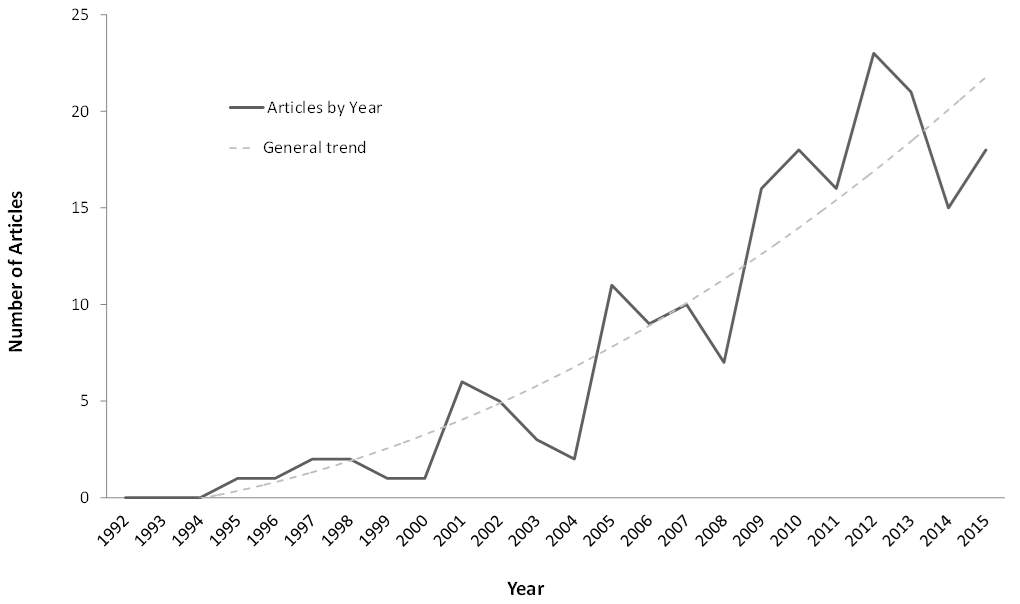

On the classification of papers according to the year of publication. As indicated in Figure 4, the number of papers published in each year from January 1992 to December 2015 ranges on 0 to 25 papers, with a evident growth in all the range and a fast increment after 2000, with an average of 7.8 and standard deviation of 7.6 papers by year.

In order to input in the analysis the historical occurrence we divide the studied period of time in four parts. The historical economic context expressed by Basel I, II and III encounters - 1988, 2004 and 2013, respectively - may have had an increase the number of papers with possible time lag in reviewing and revising the submitted manuscripts. Thus, we consider the following four time period sceneries. The first scenery is obtained by considering papers published before 2006 (Year ), hereafter ’I’; the second scenery is obtained by the papers published between 2006 and 2010 (Year), hereafter ’II’; the third scenery is obtained by the papers published between 2010 and 2010 (Year), hereafter ’III’; and the last time scenery is for papers published after 2012 (Year) referred to ’IV’. The respective number of papers in each time period scenery equals to 45, 51, 39 and 54 papers.

On the classification of papers according to the scientific journal. The reviewed papers were published by 73 journals and the frequencies are shown in Table 2. Most of these papers are related to scientific journals of computer science, decision sciences, engineering and mathematics. As shown in Table 2, the largest number of papers were published by ’Expert Systems with Applications’ and ’Journal of the Operational Research Society’ which account for 27.81% and 10.70% of the 187 reviewed paper, respectively. In the four time periods, the journal ’Expert Systems with Applications’ exhibits moderately an increasing number of papers in credit scoring, while the ’Journal of the Operational Research Society’ exhibits a decreasing number of papers in the same context. ’Knowledge-Based Systems’ amounts to an exponential increase of these papers.

| Journal | I | II | III | IV | Total | % | |

| Expert Systems with Applications | 9 | 16 | 14 | 13 | 52 | 27.81 | |

| Journal of the Operational Research Society | 11 | 5 | 1 | 3 | 20 | 10.70 | |

| European Journal of Operational Research | 1 | 6 | 3 | 6 | 16 | 8.56 | |

| Knowledge-Based Systems | 0 | 1 | 2 | 4 | 7 | 3.74 | |

| Applied Stochastic Models in Business and Industry | 4 | 0 | 0 | 0 | 4 | 2.14 | |

| Computational Statistics and Data Analysis | 1 | 0 | 1 | 1 | 3 | 1.60 | |

| IMA Journal Management Mathematics | 2 | 1 | 0 | 0 | 3 | 1.60 | |

| International Journal of Neural Systems | 0 | 0 | 3 | 0 | 3 | 1.60 | |

| Others | 15 | 22 | 15 | 27 | 79 | 42.25 | |

| Total | 43 | 51 | 39 | 54 | 187 | 100 | |

| † These include papers from ACM Trans. on Knowledge Discovery from Data, Decision Support Systems, Journal of the Royal Stat. Society, | |||||||

| Inter. Journal of Comp. Intelligence & Applications, Applied Math. & Comp., Applied Soft Computing, Comm. in Statistics, Comp. Statistics, | |||||||

| Credit and Banking and others. | |||||||

On the classification of papers according to the authors. In the 187 reviewed papers, there are 525 different co-authors. The frequency of appearance of those is presented in Table 3, where only co-authors with over 4 appearances are shown. Baesens B., Vanthienen J., Hand D.J. and Thomas L.C. are the researchers who published the largest number of papers, which represented 3.0%, 1.9%, 1.5% and 1.5%, respectively. As may be seen in Table 3 these researchers are mostly from Belgium, United Kingdom, Taiwan, US, Chile and Brazil.

| AUTOR | Affliation,Country | I | II | III | IV | Total | % |

|---|---|---|---|---|---|---|---|

| Baesens, B. | Katholieke Univ. Leuven, Belgium | 7 | 5 | 2 | 2 | 16 | 3.0 |

| Vanthienen, J. | Katholieke Univ. Leuven, Belgium | 6 | 4 | 0 | 0 | 10 | 1.9 |

| Hand, D.J. | Imperial College London, UK | 7 | 0 | 1 | 0 | 8 | 1.5 |

| Thomas, L.C. | University of Southampton,UK | 1 | 2 | 2 | 3 | 8 | 1.5 |

| Mues, C. | University of Southampton,UK | 1 | 2 | 3 | 1 | 7 | 1.3 |

| Van Gestel, T. | Katholieke Univ. Leuven, Belgium | 3 | 4 | 0 | 0 | 7 | 1.3 |

| Tsai, C.-F. | Nat. Chung Cheng University, Taiwan | 0 | 3 | 0 | 3 | 6 | 1.1 |

| Bravo, C. | Universidad de Chile, Chile | 0 | 0 | 0 | 4 | 4 | 0.8 |

| Louzada, F. | Universidade de Sao Paulo, Brazil | 0 | 0 | 3 | 1 | 4 | 0.8 |

| Shi, Y. | University of Nebraska Omaha, US | 0 | 3 | 0 | 1 | 4 | 0.8 |

| Others | 95 | 107 | 101 | 148 | 451 | 85.9 | |

| Total | 120 | 130 | 112 | 163 | 525 | 100.0 |

On the classification of papers according to conceptual scene. The twelve questions applied in the systematic review for all 187 reviewed papers are shown in the Table A.2 of the Appendix. In the next section, the analysis and discussion of these results are performed, they allow us to understand the methodological progress occurred in credit scoring analysis on the past two decades.

4.2 Results for different time periods

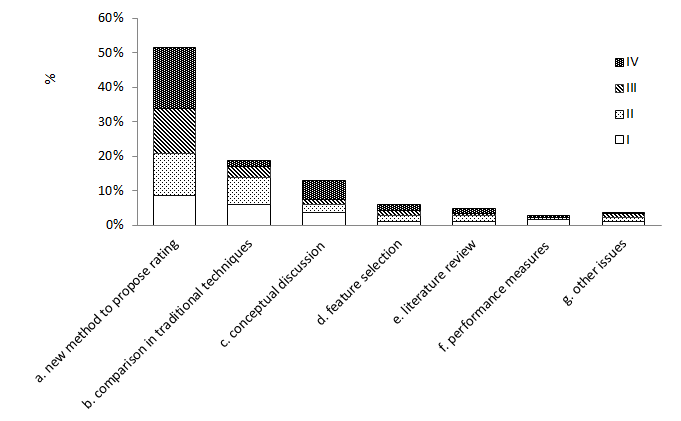

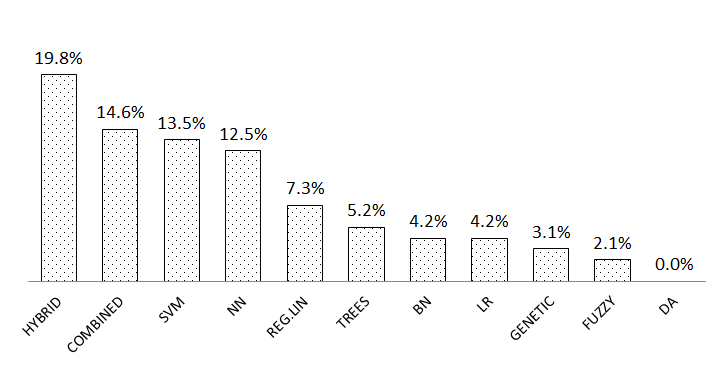

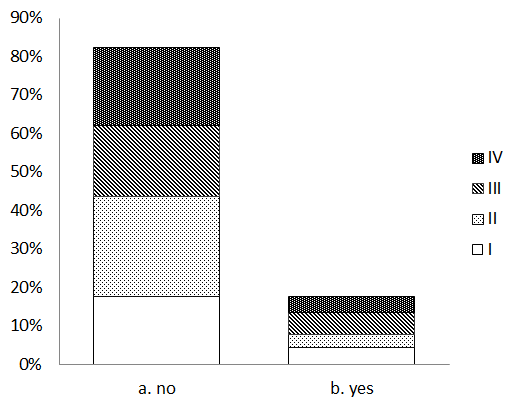

On the main objectives in credit scoring analysis. As shown in Figure 5 the most common goal of the papers is the proposition of new methods in credit scoring, representing 51.3% of all 187 reviewed papers. This preference is maintained for the four time periods. Figure 6 shows the frequencies of general techniques used as new methods in credit scoring. The hybrid is the most common method with almost 20%, followed by combined methods with almost 15% and support vector machine along with neural networks with around 13%. Due to the sheer number of methods involved and different kinds of behavior in each dataset, the second most popular main objective is the comparison of traditional techniques. However, it is becoming less common in the latest years (III and IV). The third most usual main objective is the conceptual discussion, which is most common in IV time period. Other main objectives do not reach 10% of the total of papers reviewed. The performance measures studies are more common in past years (I time period). Also, there is stability in the four time periods of literature review and other issues.

The research evolution of a new field, such as credit scoring, starts with the discovery that it is poorly investigated by researchers. Moreover, the academic and professional interest in a particular research area is usually boosted by new environmental changes. In the case of credit scoring, the main environmental changes are the rapid increase of storage information and the processing capacity, combined with the creation of the Basel accords, which means a change in why and how to control credit risk. The conceptual discussion set definitions, ideas and problems to be faced. The increasing number of researchers interested in credit scoring culminated in the development and adaptation of techniques for tackling the main questions. After the techniques were developed, methods for comparing those are proposed. At last, a field of research will eventually reaches a state-of-the-art phase, followed by new researchers questioning the paradigm, ideas and disrupting the status quo of the credit scoring area. Currently, credit scoring is going through the process of tools development, as shown in Figure 4.

| General |

|

| I | II |

|

|

| III | IV |

|

|

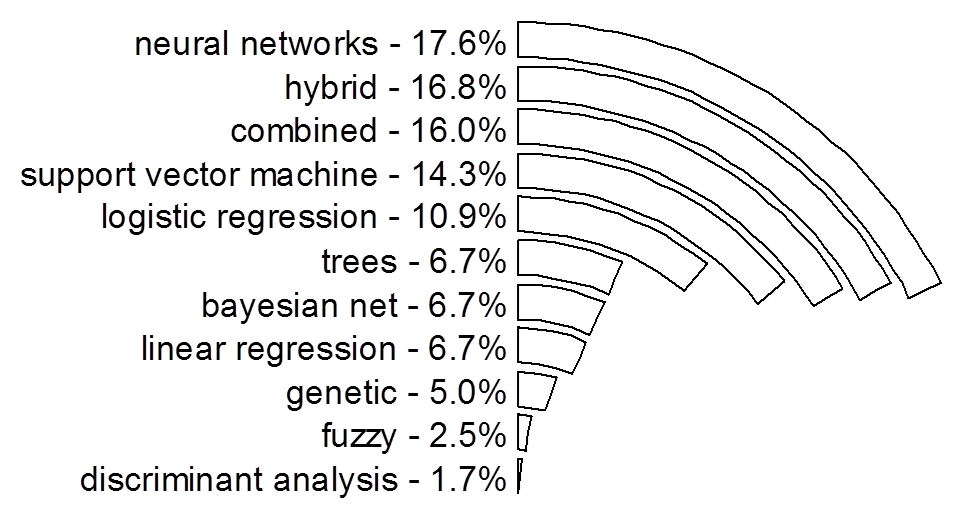

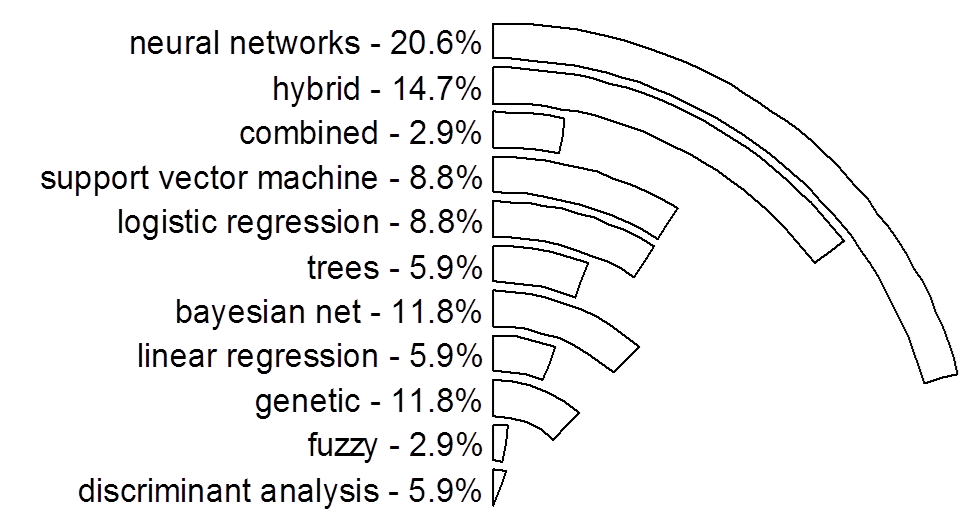

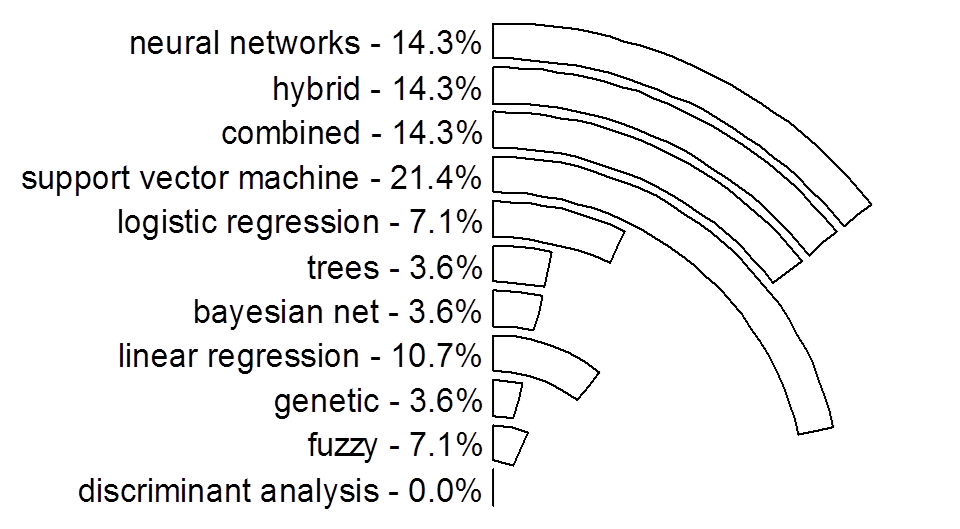

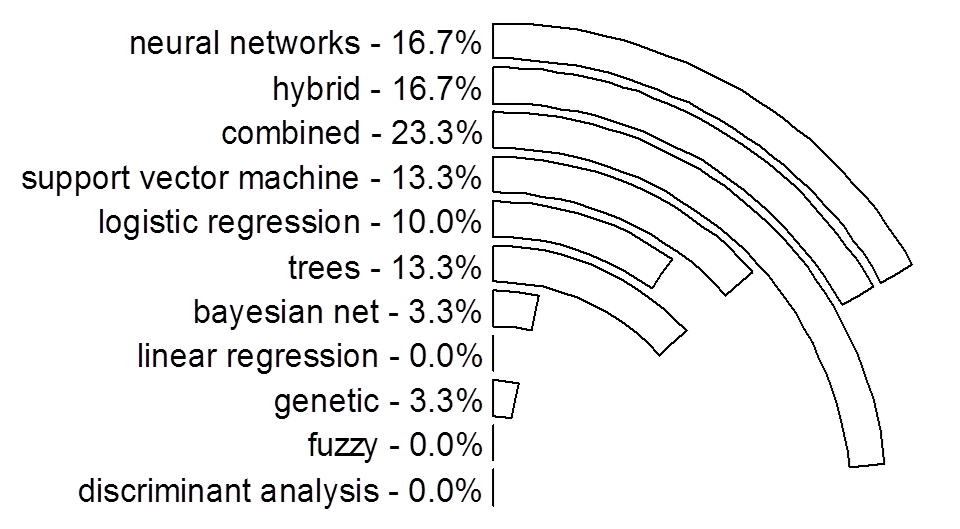

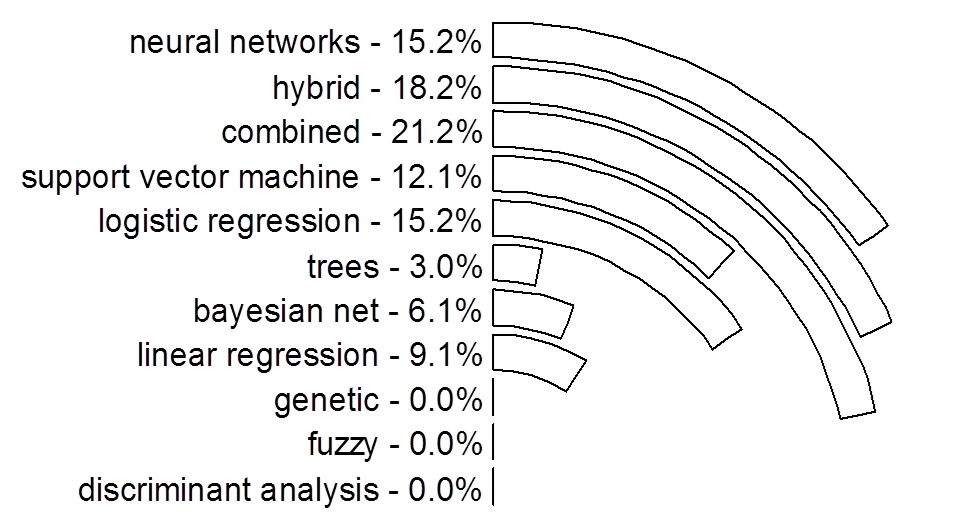

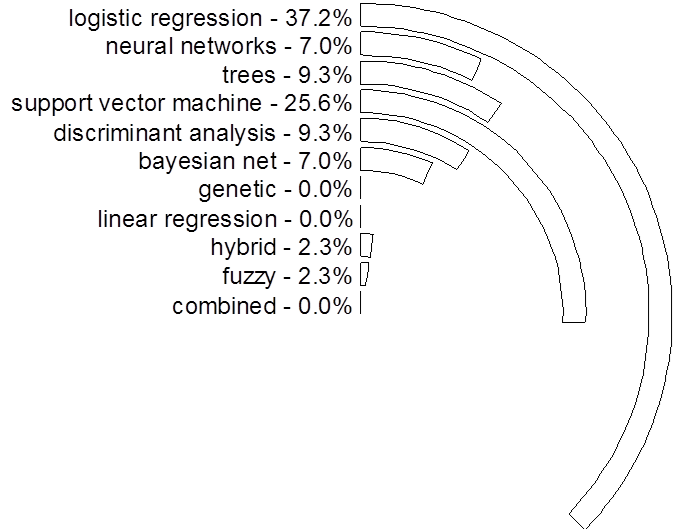

On the main classification techniques. As a classification technique is applied as a credit scoring model, the choice of technique is often related to the subjectivity of the analyst or to state-of-the-art methods. Ideally, a precise prediction indicates whether a credit extended to an applicant will probably result in profit for the lending institution. Figure 7 shows the circular bar plots concerning the main classification techniques applied in all considered periods as well as their utilization over time, this Figure only considers the techniques indicated in Section 2.2. In general, the neural networks and support vector machine are the most common used techniques in credit scoring (17.6%), the discriminant analysis remained as a rarely used technique (1.7%). In the first time period analyzed, the most common technique is the neural network (20.6%).

However, neural networks and hybrid methods remained at constant use in all following periods considered with a higher frequency. Support vector machine was most used between 2006 and 2010 II time period (21.4%), this method is the fourth most commonly used in general, although with a fast increasing in past and decreasing its participation over recent years. The trees, bayesian net, linear regression and logistic regression techniques had this same percentage in this period. However, logistic regression was most used (15.2%) in recent years and matching the use of neural networks in IV time period. In addition, there is a strong decrease in the use of the genetic, fuzzy and discriminant analysis methods and a remarkable growth of combined techniques which are the most used method in recent years, IV time period, with 21.2%. Hybrid methods have always been highly used, but were not the highlights in any time period. In comparison with Figure 6, the hybrid and combined methods are mostly used in new methods to propose rating in credit scoring, followed by support vector machine and neural networks.

|

|

| (a) | (b) |

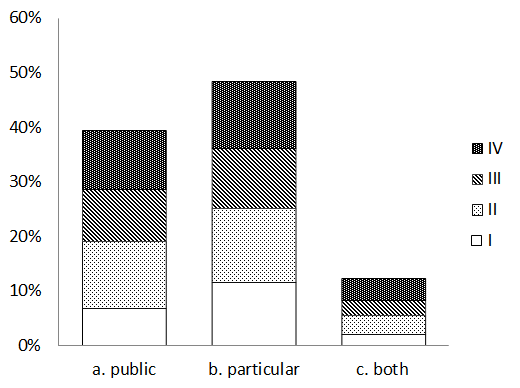

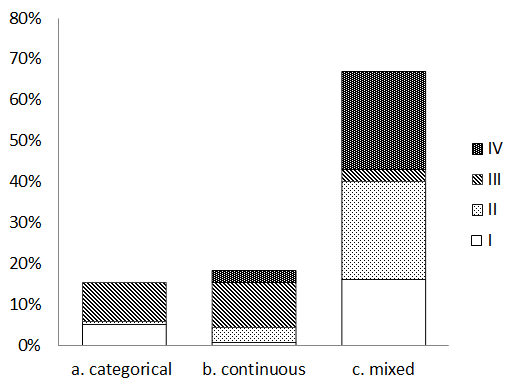

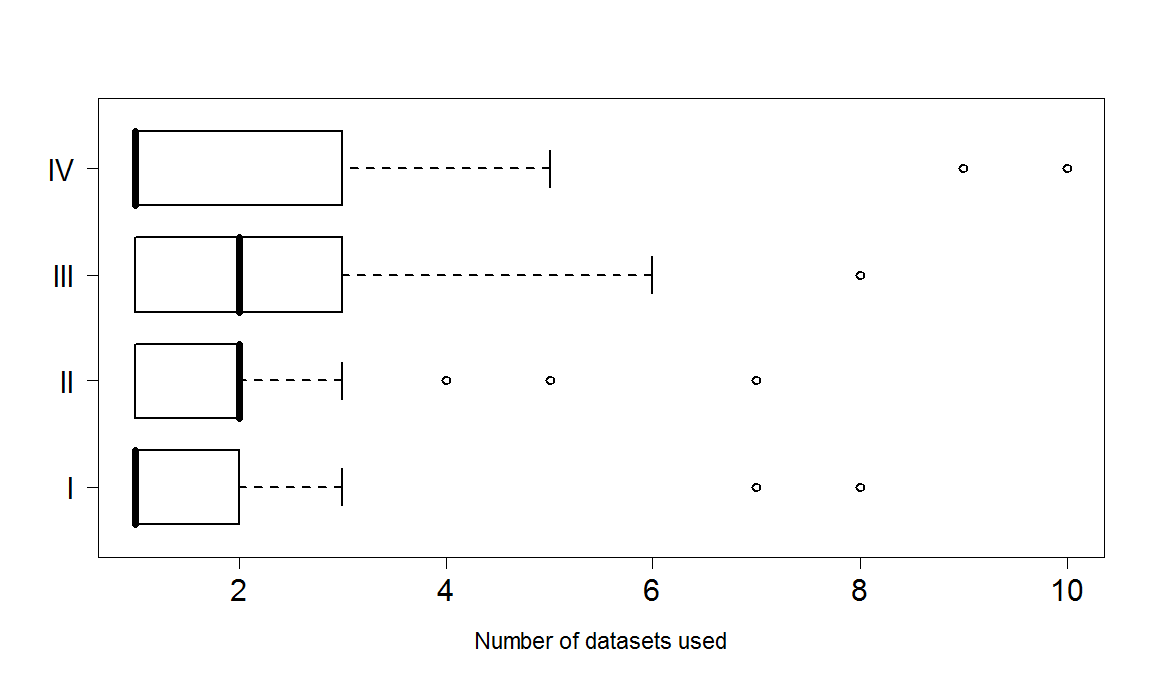

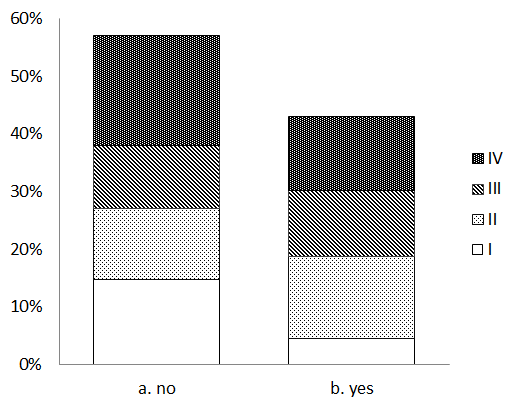

On the datasets used in credit scoring. Figures 8 (a) and 8 (b) show information about the datasets used in credit scoring reviewed papers. As Indicated by 8 (a), the most common type of datasets is private in all time periods, followed by public dataset and lastly the use of both types. In other words, the authors usually employ only private datasets in their credit scoring applications. This fact seems to be independent of the time period. As indicated by 8 (b), authors prefer to use datasets that have continuous and discrete variables. However, in I the datasets with only discrete variables were more common than those with only continuous variables. Discarding Lan et al. (2006), which used 16 datasets in their work, Table 4 shows the basic statistics of the number of datasets used in reviewed papers. In general, the papers consider an average of 2.18 datasets in their content. Figure 9 shows the behaviour of the number of datasets in the four times periods, and indicates a growth in the number of datasets used in the period I, II and III and an average decrease in IV with a growth in the standard deviation.

| Time period | Min. | 1st Qu. | Median | Mean | 3rd Qu. | Max. | Sdv |

|---|---|---|---|---|---|---|---|

| I | 1.00 | 1.00 | 1.00 | 1.80 | 2.00 | 8.00 | 1.69 |

| II | 1.00 | 1.00 | 2.00 | 2.05 | 2.00 | 7.00 | 1.40 |

| III | 1.00 | 1.00 | 2.00 | 2.55 | 3.00 | 8.00 | 1.85 |

| IV | 1.00 | 1.00 | 1.00 | 2.31 | 3.00 | 10.00 | 2.32 |

| General | 1.00 | 1.00 | 1.00 | 2.18 | 3.00 | 10.00 | 1.84 |

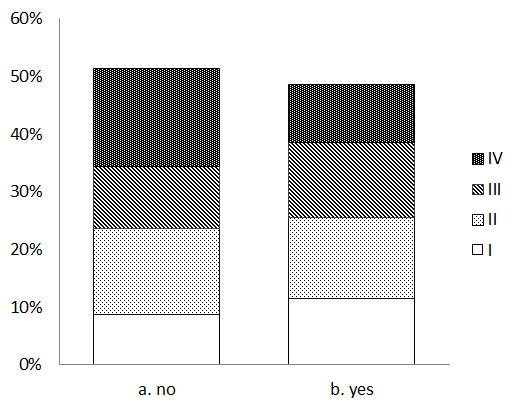

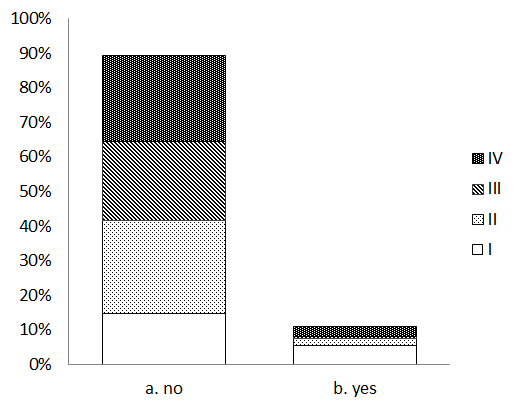

On the preprocessing data methods in credit scoring. In regards to preprocessing methods in credit scoring, this review covers two relevant aspects: the feature (variable) selection and missing data procedures. Figure 10 (a) shows that, independently of the time period, the feature selection is performed in most studies. However, in about 49% of the papers this procedure is not used. Figure 10 (b) shows that the missing data imputation it is a procedure often not used in credit scoring analysis (90%).

|

|

| (a) | (b) |

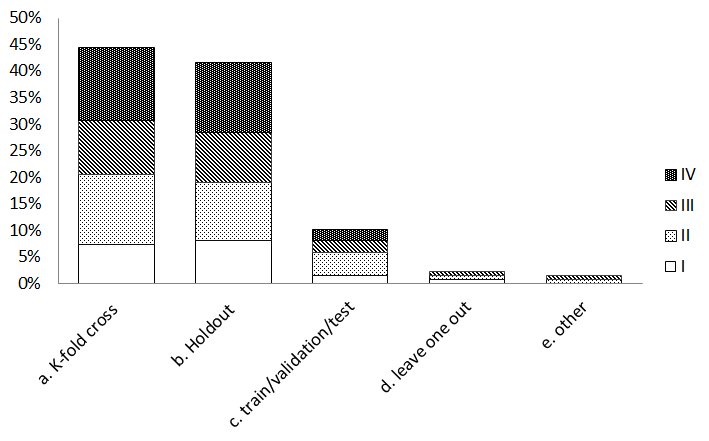

On the validation of the approaches. The validation of the approaches are a part of the procedures that ensures the authors of the examination of the performance and comparability of their methods. In general, as indicated by Figure 11 (a), more than 80% of the papers do not consider exhaustive simulations in their procedures. Likewise, as indicated in Figure 11 (b), almost 45% of all reviewed papers consider the Australian or German credit dataset, and during the II time period it became an even more common practice. Table 5 shows the overall classification performance on Australian and German credit datasets for 30 reviewed papers. Concerning the splitting of the datasets, Figure 12 shows that K-Fold cross validation and holdout methods were more common in general, and in more recent time periods, the K-fold cross validation became the most widely used method. The splitting of the dataset in three parts (train/validation/test) is more used than the leave-one-out procedure.

|

|

| (a) | (b) |

| Paper | AUS | GER | Paper | AUS | GER | |

|---|---|---|---|---|---|---|

| Baesens et al. (2003) | 90.40 | 74.60 | Nieddu et al. (2011) | 87.30 | 79.20 | |

| Hsieh (2005) | 98.00 | 98.50 | Marcano-Cedeno et al. (2011) | 92.75 | 84.67 | |

| Somol et al. (2005) | 92.60 | 83.80 | Ping and Yongheng (2011) | 87.52 | 76.60 | |

| Lan et al. (2006) | 86.96 | 74.40 | Yu and Li (2011) | 85.65 | 72.60 | |

| Hoffmann et al. (2007) | 85.80 | 73.40 | Chang and Yeh (2012) | 85.36 | 77.10 | |

| Huang et al. (2007) | 87.00 | 78.10 | Wang et al. (2012a) | 88.17 | 78.52 | |

| Tsai and Wu (2008) | 97.32 | 78.97 | Hens and Tiwari (2012) | 85.98 | 75.08 | |

| Tsai (2008) | 90.20 | 79.11 | Vukovic et al. (2012) | 88.55 | 77.40 | |

| Tsai (2009) | 81.93 | 74.28 | Marques et al. (2012a) | 86.81 | 76.60 | |

| Luo et al. (2009) | 86.52 | 84.80 | Ling et al. (2012) | 87.85 | 79.55 | |

| Lahsasna et al. (2010b) | 88.60 | 75.00 | Sadatrasoul et al. (2015) | 84.83 | 73.51 | |

| Chen and Li (2010) | 86.52 | 76.70 | Zhang et al. (2014) | 88.84 | 73.20 | |

| Zhang et al. (2010) | 91.97 | 81.64 | Liang et al. (2014) | 86.09 | 74.16 | |

| Liu et al. (2010) | 86.84 | 75.75 | Tsai et al. (2014) | 87.23 | 76.48 | |

| Wang et al. (2011) | 86.57 | 76.30 | Zhu et al. (2013) | 86.78 | 76.62 |

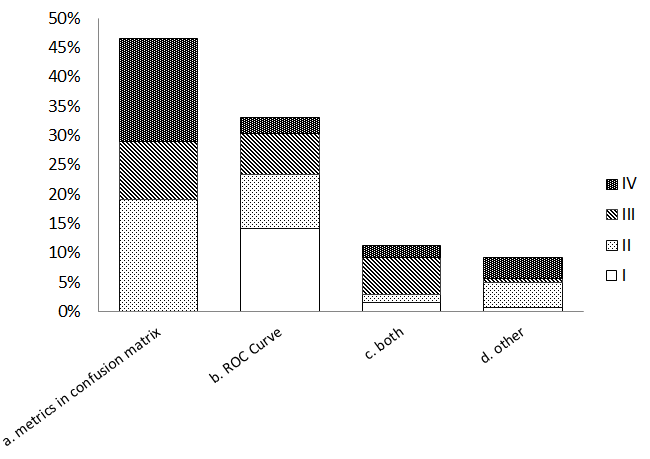

On the misclassification cost criterion. Figure 13 shows that to measure the misclassification cost, the most common criteria used in the reviewed papers are the metrics based on confusion matrix (45%). Although this criterion was not in use solely in the I time period, it was widely used in others. The utilization of the ROC Curve was more common in the past period and about 10% of all the reviewed papers used both or other criteria.

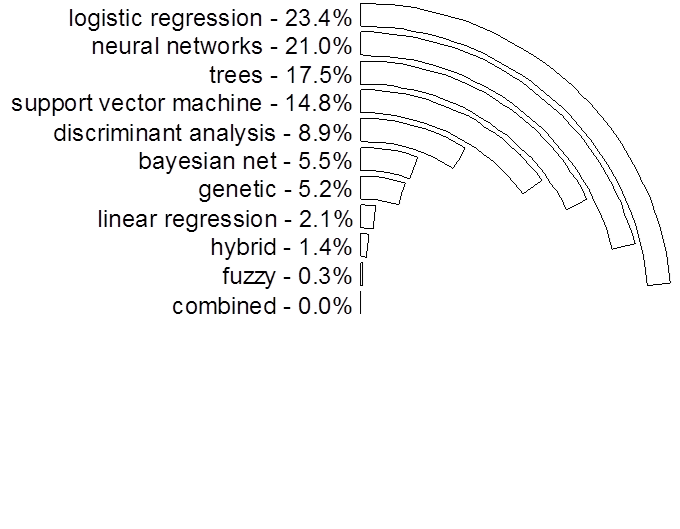

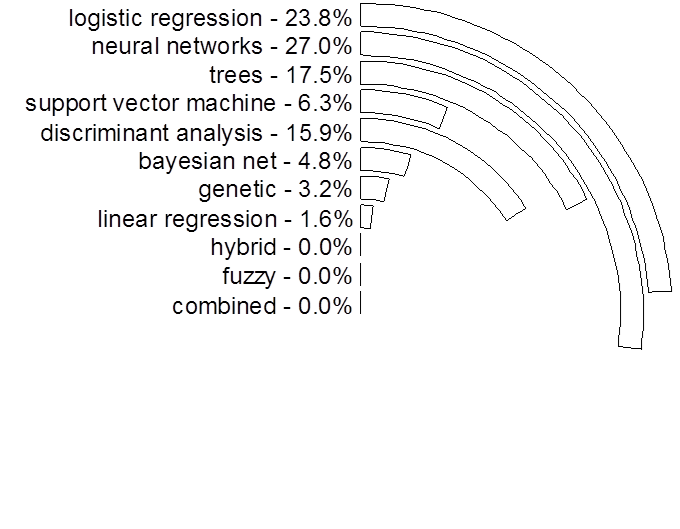

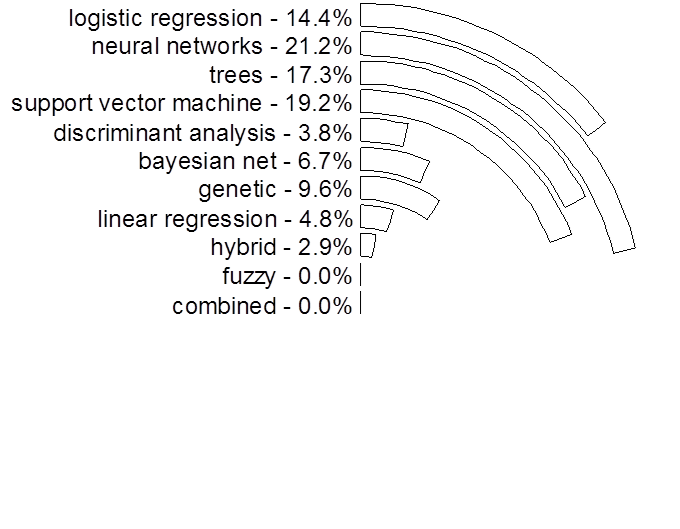

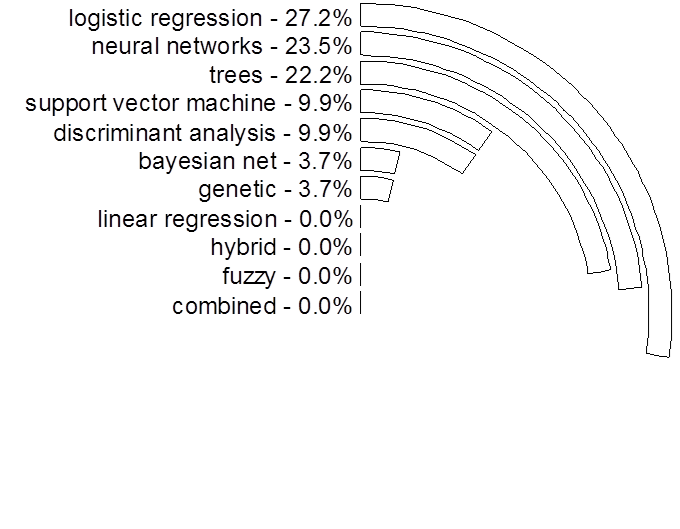

On the classification methods used in comparison studies. Regarding the traditional techniques used in comparison studies, Figure 14 shows the circular bar plots concerning techniques applied in all considered periods. The most used technique in comparison studies is logistic regression (23.14%) which has always had a high frequency of use in all considered periods. The neural networks is the second most used technique (21.0%) with a high usage in II time period. The support vector machine was widely and recently used in comparison studies, but in general it is the fourth most frequently used technique (14.8%). The trees remained as the third most used technique in all periods. In the reviewed papers, no study performs comparisons using combined techniques.

| General |

|

| I | II |

|

|

| III | IV |

|

|

5 Is there a better method? A comparison study

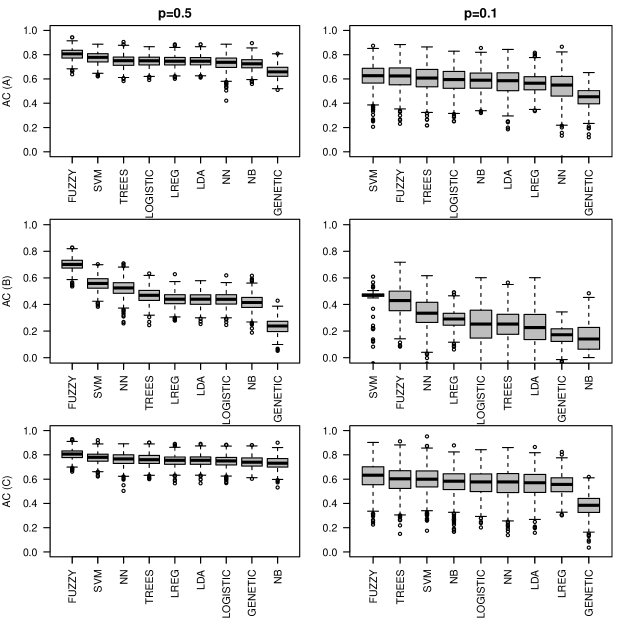

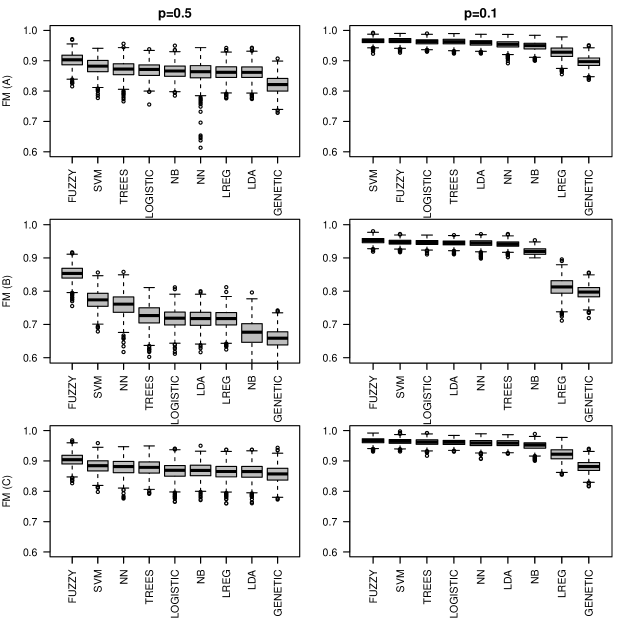

In this section, all presented methods are compared using two frameworks, marked out by two predictive performance measures, AC (Approximate Correlation) and FM (F1-score Measure) for three different benchmark datasets: (A) Australian Credit, (B) Credit German and (C) Japanese Credit, available in UCI Machine Learning Repository (http://archive.ics.uci.edu/ml/). For each dataset we performed 1000 replications in a handout validation approach (70% training sample and 30% test sample) under a balanced base (, 50% of bad payers) and a unbalanced base (, 10% of bad payers). The methods were implemented in Sofware R 3.0.2 through RBase with the packages: , , , , and on a HP Pavilion PC i7-3610QM 2.30GHz CPU, RAM 8.GB, Windows 7 64-bit.

Taking into account the all comparisons, Figures 15 and 16, we noticed the highlight of two methods, SVM and FUZZY, that permeate this comparison study as the two best techniques of greater predictive performance for both measures evaluated, this fact is confirmed by the Kruskal-Wallis test at a significance level of 5% ().

However we noticed that in most cases there is a shift of the predictive performance of both when occurs unbalance in the number of bad payers. For FUZZY is given as the method with greater predictive performance, with SVM as the second method. For SVM is given as the method with greater predictive performance, with FUZZY as the second method. Alternatively, TREES often the third best method and its independent of the unbalance. In addition, we noticed most often that NN lost the predictive performance when there is imbalance. The LOGISTIC, NB and LDA methods do not seem present any standard, with predictive performance behavior between the median methods. GENETIC and LREG are considered as the smaller predictive performance when there is imbalance.

| Dataset | GENETIC | FUZZY | NN | LOGISTIC | SVM | NB | TREES | LDA | LREG |

|---|---|---|---|---|---|---|---|---|---|

| (A) | 41.69 | 39.69 | 0.66 | 0.24 | 0.34 | 0.34 | 0.25 | 0.30 | 0.23 |

| (B) | 42.58 | 24.31 | 0.41 | 0.23 | 0.31 | 0.33 | 0.27 | 0.23 | 0.23 |

| (C) | 146.35 | 82.77 | 1.38 | 0.74 | 0.47 | 0.45 | 0.28 | 0.25 | 0.24 |

| AVERAGE | 76.87 | 48.92 | 0.82 | 0.40 | 0.37 | 0.37 | 0.27 | 0.26 | 0.23 |

Table 6 displays computational time (in seconds) for the implementation of methods for each replication. Among the methods with greater predictive performance, SVM (0.37s) has a much lower computational effort than FUZZY (48.92s). GENETIC and FUZZY are the methods with higher computational effort. In summary among the analysed methods, SVM stands out as a method of high predictive performance and low computational effort than others.

6 Final comments

We present in this paper a methodologically structured systematic literature review of binary classification techniques for credit scoring financial analysis. An amount of 187 papers on credit scoring published in scientific journals during the two last decades (1992-2015) were analysed and classified. Based on the survey, we observed an increasing number of papers in this area and noticed that credit scoring analysis is a current and significant financial area. A plenteous area for the application of statistical and data mining tools.

Although, regardless of the time period, the most common main objective of the revised papers is to propose a new method for rating in credit scoring, especially with hybrid techniques, it is observed a similarity between the predictive performance of the methods. This result is corroborated by Hand (2006). Moreover, comparison with traditional techniques was rarely performed in recent time periods. This fact show that, though the researchers are giving up to compare techniques, the pursuit of a general method with a high predictive performance continues. On the other hand, other types of researches in credit scoring are required as conceptual discussions based on data quality, database enrichment, time dependence, classes type and so on.

While knowing these mishaps, for the moment, neural networks, support vector machine, hybrid and combined techniques appear as the most common main tools. The logistic regression, trees and also neural networks are mostly used in comparisons of techniques as standards that must be overcome. In general, support vector machine appears as a method of high predictive performance and low computational effort than other methods. Regarding datasets for credit scoring, the number has been increasing as well as the presence of a mixture of continuous and discrete variables. The majority of datasets however are private and there is a wide usage of the well known German and Australian datasets. This fact shows how difficult is to obtaining datasets on the credit scoring scenario, since there are issues related to maintenance of confidentiality of credit scoring databases.

The K-fold cross validation and holdout are the most common validation methods. Care should be taken when interpreting the results of both methods, because they are different methods and subject to subjectivity of the random distribution of the database. The use of ROC Curve as unique misclassification criterion has decreased significantly in the articles over the years. More recently it is most common the use of metrics based on confusion matrix. Also, there is a small number of papers that handles with missing data in credit scoring analysis and a high frequency of papers that applied feature selection procedures as pre-proceeding method.

Although our systematic literature review is exhaustive, some limitations still persist. First, the findings were based on papers published in English and in scientific journals inside the following databases: Sciencedirect, Engineering Information, Reaxys and Scopus. Although such databases covers more than 20,000 journal titles, other databases may be hereafter included in the survey. Secondly, as pointed out in Section 2, we did not include in the survey other forms of publication such as unpublished working papers, master and doctoral dissertations, books, conference in proceedings, white papers and others. Moreover, high quality research is eventually published in scientific journals, other forms of publication may be included in this list in future investigations. Notwithstanding these limitations, our systematic review review provides important insights into the research literature on classification techniques applied to credit scoring and how this area has been moving over time.

Acknowledgments: This research was sponsored by the Brazilian organizations CNPq and FAPESP and by Serasa Experian, through their research grant programs.

References

- Abdou (2009) Abdou, H., 2009. Genetic programming for credit scoring: The case of egyptian public sector banks. Expert Systems with Applications 36 (9), 11402–11417.

- Abdou et al. (2008) Abdou, H., Pointon, J., El-Masry, A., 2008. Neural nets versus conventional techniques in credit scoring in egyptian banking. Expert Systems with Applications 35 (3), 1275–1292.

- Abdoun and Abouchabaka (2011) Abdoun, O., Abouchabaka, J., 2011. A comparative study of adaptive crossover operators for genetic algorithms to resolve the traveling salesman problem. International Journal of Computer Applications 31 (11), 49–57.

- Abellàn and Mantas (2014) Abellàn, J.n, J., Mantas, C., 2014. Improving experimental studies about ensembles of classifiers for bankruptcy prediction and credit scoring. Expert Systems with Applications 41 (8), 3825–3830.

- Adams et al. (2001) Adams, N., Hand, D., Till, R., 2001. Mining for classes and patterns in behavioural data. Journal of the Operational Research Society 52 (9), 1017–1024.

- Akkoc (2012) Akkoc, S., 2012. An empirical comparison of conventional techniques, neural networks and the three stage hybrid adaptive neuro fuzzy inference system (anfis) model for credit scoring analysis: The case of turkish credit card data. European Journal of Operational Research 222 (1), 168–178.

- Antonakis and Sfakianakis (2009) Antonakis, A., Sfakianakis, M., 2009. Assessing naivee bayes as a method for screening credit applicants. Journal of Applied Statistics 36 (5), 537–545.

- Aryuni and Madyatmadja (2015) Aryuni, M., Madyatmadja, E., 2015. Feature selection in credit scoring model for credit card applicants in xyz bank: A comparative study. International Journal of Multimedia and Ubiquitous Engineering 10 (5), 17–24.

-

Bache and Lichman (2013)

Bache, K., Lichman, M., 2013. UCI machine learning repository.

URL http://archive.ics.uci.edu/ml - Baesens et al. (2005) Baesens, B., Van Gestel, T., Stepanova, M., Van Den Poel, D., Vanthienen, J., 2005. Neural network survival analysis for personal loan data. Journal of the Operational Research Society 56 (9), 1089–1098.

- Baesens et al. (2003) Baesens, B., Van Gestel, T., Viaene, S., Stepanova, M., Suykens, J., Vanthienen, J., 2003. Benchmarking state-of-the-art classification algorithms for credit scoring. Journal of the Operational Research Society 54 (6), 627–635.

- Bahnsen et al. (2015) Bahnsen, A., Aouada, D., Ottersten, B., 2015. Example-dependent cost-sensitive decision trees. Expert Systems with Applications 42 (19), 6609–6619.

- Banasik et al. (1999) Banasik, J., Crook, J., Thomas, L., 1999. Not if but when will borrowers default. Journal of the Operational Research Society 50 (12), 1185–1190.

- Banasik et al. (2003) Banasik, J., Crook, J., Thomas, L., 2003. Sample selection bias in credit scoring models. Journal of the Operational Research Society 54 (8), 822–832.

- Bardos (1998) Bardos, M., 1998. Detecting the risk of company failure at the banque de france. Journal of Banking and Finance 22 (10-11), 1405–1419.

- Baxter et al. (2007) Baxter, R., Gawler, M., Ang, R., 2007. Predictive model of insolvency risk for australian corporations. Conferences in Research and Practice in Information Technology Series 70, 21–28.

- Bekhet and Eletter (2014) Bekhet, H., Eletter, S., 2014. Credit risk assessment model for jordanian commercial banks: Neural scoring approach. Review of Development Finance 4 (1), 20–28.

- Ben-David and Frank (2009) Ben-David, A., Frank, E., 2009. Accuracy of machine learning models versus hand craft. Expert Systems with Applications 36 (3 PART 1), 5264–5271.

- Berger et al. (2005) Berger, A., Frame, W., Miller, N., 2005. Credit scoring and the availability, price, and risk of small business credit. Journal of Money, Credit and Banking 37 (2), 191–222.

- Berkson (1944) Berkson, J., 1944. Application of the logistic function to bio-assay. Journal of the American Statistical Association 39 (227), 357–365.

- Bijak and Thomas (2012) Bijak, K., Thomas, L., 2012. Does segmentation always improve model performance in credit scoring? Expert Systems with Applications 39 (3), 2433–2442.

- Bishop (1995) Bishop, C. M., 1995. Neural networks for pattern recognition. Oxford university press.

- Blanco et al. (2013) Blanco, A., Pino-Mejías, R., Lara, J., Rayo, S., 2013. Credit scoring models for the microfinance industry using neural networks: Evidence from peru. Expert Systems with Applications 40 (1), 356–364.

- Bravo and Maldonado (2015) Bravo, C., Maldonado, S., 2015. Fieller stability measure: A novel model-dependent backtesting approach. Journal of the Operational Research Society 66 (11), 1895–1905.

- Bravo et al. (2013) Bravo, C., Maldonado, S., Weber, R., 2013. Granting and managing loans for micro-entrepreneurs: New developments and practical experiences. European Journal of Operational Research 227 (2), 358–366.

- Bravo et al. (2015) Bravo, C., Thomas, L., Weber, R., 2015. Improving credit scoring by differentiating defaulter behaviour. Journal of the Operational Research Society 66 (5), 771–781.

- Breiman (1996) Breiman, L., 1996. Bagging predictors. Machine learning 24 (2), 123–140.

- Breiman et al. (1984) Breiman, L., Friedman, J. H., Olshen, R. A., Stone, C. J., 1984. Classification and regression trees. wadsworth & brooks. Monterey, CA.

- Brown and Mues (2012) Brown, I., Mues, C., 2012. An experimental comparison of classification algorithms for imbalanced credit scoring data sets. Expert Systems with Applications 39 (3), 3446–3453.

- Burton (2012) Burton, D., 2012. Credit scoring, risk, and consumer lendingscapes in emerging markets. Environment and Planning A 44 (1), 111–124.

- Capotorti and Barbanera (2012) Capotorti, A., Barbanera, E., 2012. Credit scoring analysis using a fuzzy probabilistic rough set model. Computational Statistics and Data Analysis 56 (4), 981–994.

- Chang and Yeh (2012) Chang, S.-Y., Yeh, T.-Y., 2012. An artificial immune classifier for credit scoring analysis. Applied Soft Computing Journal 12 (2), 611–618.

- Chen and Li (2010) Chen, F.-L., Li, F.-C., 2010. Combination of feature selection approaches with svm in credit scoring. Expert Systems with Applications 37 (7), 4902–4909.

- Chen and Huang (2003) Chen, M.-C., Huang, S.-H., 2003. Credit scoring and rejected instances reassigning through evolutionary computation techniques. Expert Systems with Applications 24 (4), 433–441.

- Chen et al. (2009) Chen, W., Ma, C., Ma, L., 2009. Mining the customer credit using hybrid support vector machine technique. Expert Systems with Applications 36 (4), 7611–7616.

- Chrzanowska et al. (2009) Chrzanowska, M., Alfaro, E., Witkowska, D., 2009. The individual borrowers recognition: Single and ensemble trees. Expert Systems with Applications 36 (3 PART 2), 6409–6414.

- Chuang and Huang (2011) Chuang, C.-L., Huang, S.-T., 2011. A hybrid neural network approach for credit scoring. Expert Systems 28 (2), 185–196.

- Chuang and Lin (2009) Chuang, C.-L., Lin, R.-H., 2009. Constructing a reassigning credit scoring model. Expert Systems with Applications 36 (2 PART 1), 1685–1694.

- Cubiles-De-La-Vega et al. (2013) Cubiles-De-La-Vega, M.-D., Blanco-Oliver, A., Pino-Mejías, R., Lara-Rubio, J., 2013. Improving the management of microfinance institutions by using credit scoring models based on statistical learning techniques. Expert Systems with Applications 40 (17), 6910–6917.

- Deng et al. (2015) Deng, Z., Huye, B., He, P., Li, Y., Li, P., 2015. An artificial immune network classification algorithm for credit scoring. Journal of Information and Computational Science 12 (11), 4263–4270.

- DeYoung et al. (2011) DeYoung, R., Frame, W., Glennon, D., Nigro, P., 2011. The information revolution and small business lending: The missing evidence. Journal of Financial Services Research 39 (41306), 19–33.

- Dong et al. (2011) Dong, Y., Hao, X., Yu, C., 2011. Comparison of statistical and artificial intelligence methodologies in small-businesses’ credit assessment based on daily transaction data. ICIC Express Letters 5 (5), 1725–1730.

- Dryver and Sukkasem (2009) Dryver, A., Sukkasem, J., 2009. Validating risk models with a focus on credit scoring models. Journal of Statistical Computation and Simulation 79 (2), 181–193.

- Durand (1941) Durand, D., 1941. Risk elements in consumer instalment financing. In: National Bureau of Economics. New York.

- Efromovich (2010) Efromovich, S., 2010. Oracle inequality for conditional density estimation and an actuarial example. Annals of the Institute of Statistical Mathematics 62 (2), 249–275.

- Einav et al. (2013) Einav, L., Jenkins, M., Levin, J., 2013. The impact of credit scoring on consumer lending. RAND Journal of Economics 44 (2), 249–274.

- Falangis and Glen (2010) Falangis, K., Glen, J., 2010. Heuristics for feature selection in mathematical programming discriminant analysis models. Journal of the Operational Research Society 61 (5), 804–812.

- Feng et al. (2010) Feng, L., Yao, Y., Jin, B., 2010. Research on credit scoring model with svm for network management. Journal of Computational Information Systems 6 (11), 3567–3574.

- Ferreira et al. (2015) Ferreira, P., Louzada, F., Diniz, C., 2015. Credit scoring modeling with state-dependent sample selection: A comparison study with the usual logistic modeling. Pesquisa Operacional 35 (1), 39–56.

- Figini and Uberti (2010) Figini, S., Uberti, P., 2010. Model assessment for predictive classification models. Communications in Statistics - Theory and Methods 39 (18), 3238–3244.

- Finlay (2008) Finlay, S., 2008. Towards profitability: A utility approach to the credit scoring problem. Journal of the Operational Research Society 59 (7), 921–931.

- Finlay (2009) Finlay, S., 2009. Are we modelling the right thing? the impact of incorrect problem specification in credit scoring. Expert Systems with Applications 36 (5), 9065–9071.

- Finlay (2010) Finlay, S., 2010. Credit scoring for profitability objectives. European Journal of Operational Research 202 (2), 528–537.

- Finlay (2011) Finlay, S., 2011. Multiple classifier architectures and their application to credit risk assessment. European Journal of Operational Research 210 (2), 368–378.

- Fisher (1986) Fisher, R. A., 1986. The use of multiple measurements in taxonomic problems. Annals of Eugenics 7, 179–188.

- Florez-Lopez and Ramon-Jeronimo (2015) Florez-Lopez, R., Ramon-Jeronimo, J., 2015. Enhancing accuracy and interpretability of ensemble strategies in credit risk assessment. a correlated-adjusted decision forest proposal. Expert Systems with Applications 42 (13), 5737–5753.

- Friedman et al. (1997) Friedman, N., Geiger, D., Goldszmidt, M., 1997. Bayesian network classifiers. Machine Learning 29(2-3), 131–163.

- Garcia et al. (2014) Garcia, V., Marques, A., Sanchez, J., 2014. An insight into the experimental design for credit risk and corporate bankruptcy prediction systems. Journal of Intelligent Information Systems 44 (1), 159–189.

- Gemela (2001) Gemela, J., 2001. Financial analysis using bayesian networks. Applied Stochastic Models in Business and Industry 17 (1), 57–67.

- Gestel et al. (2006) Gestel, T., Baesens, B., Suykens, J., Van den Poel, D., Baestaens, D.-E., Willekens, M., 2006. Bayesian kernel based classification for financial distress detection. European Journal of Operational Research 172 (3), 979–1003.

- Giudici (2001) Giudici, P., 2001. Bayesian data mining, with application to benchmarking and credit scoring. Applied Stochastic Models in Business and Industry 17 (1), 69–81.

- Gzyl et al. (2015) Gzyl, H., Ter Horst, E., Molina, G., 2015. Application of the method of maximum entropy in the mean to classification problems. Physica A: Statistical Mechanics and its Applications 437, 101–108.

- Hachicha and Ghorbel (2012) Hachicha, W., Ghorbel, A., 2012. A survey of control-chart pattern-recognition literature (1991–2010) based on a new conceptual classification scheme. Computers & Industrial Engineering 63 (1), 204–222.

- Han et al. (2006) Han, J., Kamber, M., Pei, J., 2006. Data mining: concepts and techniques. Morgan kaufmann.

- Hand (2001a) Hand, D., 2001a. Modelling consumer credit risk. IMA Journal Management Mathematics 12 (2), 139–155.

- Hand (2001b) Hand, D., 2001b. Modelling consumer credit risk. IMA Journal Management Mathematics 12 (2), 139–155.

- Hand (2005a) Hand, D., 2005a. Good practice in retail credit scorecard assessment. Journal of the Operational Research Society 56 (9), 1109–1117.

- Hand (2005b) Hand, D., 2005b. Supervised classification and tunnel vision. Applied Stochastic Models in Business and Industry 21 (2), 97–109.

- Hand (2006) Hand, D., 2006. Classifier technology and the illusion of progress. Statistical Science 21 (9), 1–14.

- Hand and Henley (1997) Hand, D., Henley, W., 1997. Statistical classification methods in consumer credit scoring: A review. Journal of the Royal Statistical Society. Series A: Statistics in Society 160 (3), 523–541.

- Hand and Kelly (2002) Hand, D., Kelly, M., 2002. Superscorecards. IMA Journal Management Mathematics 13 (4), 273–281.

- Hardle et al. (1998) Hardle, W., Mammen, E., Muller, M., 1998. Testing parametric versus semiparametric modeling in generalized linear models. Journal of the American Statistical Association 93 (444), 1461–1474.

- Harris (2015) Harris, T., 2015. Credit scoring using the clustered support vector machine. Expert Systems with Applications 42 (2), 741–750.

- He et al. (2010) He, J., Zhang, Y., Shi, Y., Huang, G., 2010. Domain-driven classification based on multiple criteria and multiple constraint-level programming for intelligent credit scoring. IEEE Transactions on Knowledge and Data Engineering 22 (6), 826–838.

- Hens and Tiwari (2012) Hens, A., Tiwari, M., 2012. Computational time reduction for credit scoring: An integrated approach based on support vector machine and stratified sampling method. Expert Systems with Applications 39 (8), 6774–6781.

- Hofer (2015) Hofer, V., 2015. Adapting a classification rule to local and global shift when only unlabelled data are available. European Journal of Operational Research 243 (1), 177–189.

- Hofer and Krempl (2013) Hofer, V., Krempl, G., 2013. Drift mining in data: A framework for addressing drift in classification. Computational Statistics and Data Analysis 57 (1), 377–391.

- Hoffmann et al. (2002) Hoffmann, F., Baesens, B., Martens, J., Put, F., Vanthienen, J., 2002. Comparing a genetic fuzzy and a neurofuzzy classifier for credit scoring. International Journal of Intelligent Systems 17 (11), 1067–1083.

- Hoffmann et al. (2007) Hoffmann, F., Baesens, B., Mues, C., Van, Gestel, T., Vanthienen, J., 2007. Inferring descriptive and approximate fuzzy rules for credit scoring using evolutionary algorithms. European Journal of Operational Research 177 (1), 540–555.

- Hsieh (2005) Hsieh, N.-C., 2005. Hybrid mining approach in the design of credit scoring models. Expert Systems with Applications 28 (4), 655–665.

- Hsieh and Hung (2010) Hsieh, N.-C., Hung, L.-P., 2010. A data driven ensemble classifier for credit scoring analysis. Expert Systems with Applications 37 (1), 534–545.

- Hu and Ansell (2007) Hu, Y.-C., Ansell, J., 2007. Measuring retail company performance using credit scoring techniques. European Journal of Operational Research 183 (3), 1595–1606.

- Hu and Ansell (2009) Hu, Y.-C., Ansell, J., 2009. Retail default prediction by using sequential minimal optimization technique. Journal of Forecasting 28 (8), 651–666.

- Huang et al. (2007) Huang, C.-L., Chen, M.-C., Wang, C.-J., 2007. Credit scoring with a data mining approach based on support vector machines. Expert Systems with Applications 33 (4), 847–856.

- Huang et al. (2006a) Huang, J.-J., Tzeng, G.-H., Ong, C.-S., 2006a. Two-stage genetic programming (2SGP) for the credit scoring model. Applied Mathematics and Computation 174 (2), 1039–1053.

- Huang et al. (2006b) Huang, Y.-M., Hung, C.-M., Jiau, H., 2006b. Evaluation of neural networks and data mining methods on a credit assessment task for class imbalance problem. Nonlinear Analysis: Real World Applications 7 (4), 720–747.

- Huysmans et al. (2006) Huysmans, J., Baesens, B., Vanthienen, J., Van Gestel, T., 2006. Failure prediction with self organizing maps. Expert Systems with Applications 30 (3), 479–487.

- John et al. (1996) John, G., Miller, P., Kerber, R., 1996. Stock selection using rule induction. IEEE Expert-Intelligent Systems and their Applications 11 (5), 52–58.

- Jung and Thomas (2008) Jung, K., Thomas, L., 2008. A note on coarse classifying in acceptance scorecards. Journal of the Operational Research Society 59 (5), 714–718.

- Kao et al. (2012) Kao, L.-J., Chiu, C.-C., Chiu, F.-Y., 2012. A bayesian latent variable model with classification and regression tree approach for behavior and credit scoring. Knowledge-Based Systems 36, 245–252.

- Karlis and Rahmouni (2007) Karlis, D., Rahmouni, M., 2007. Analysis of defaulters’ behaviour using the poisson-mixture approach. IMA Journal Management Mathematics 18 (3), 297–311.

- Kennedy et al. (2013a) Kennedy, K., Mac Namee, B., Delany, S., O’Sullivan, M., Watson, N., 2013a. A window of opportunity: Assessing behavioural scoring. Expert Systems with Applications 40 (4), 1372–1380.

- Kennedy et al. (2013b) Kennedy, K., Namee, B., Delany, S., 2013b. Using semi-supervised classifiers for credit scoring. Journal of the Operational Research Society 64 (4), 513–529.

- Khashei et al. (2013) Khashei, M., Rezvan, M., Hamadani, A., Bijari, M., 2013. A bi-level neural-based fuzzy classification approach for credit scoring problems. Complexity 18 (6), 46–57.

- Kocenda and Vojtek (2011) Kocenda, E., Vojtek, M., 2011. Default predictors in retail credit scoring: Evidence from czech banking data. Emerging Markets Finance and Trade 47 (6), 80–98.

- Kolbe and Brunette (1991) Kolbe, R., Brunette, M., 1991. Content analysis research: An examination of applications with directives for improving research, reliability and objectivity. Journal of Consumer Research 18 (2), 243–250.

- Koutanaei et al. (2015) Koutanaei, F., Sajedi, H., Khanbabaei, M., 2015. A hybrid data mining model of feature selection algorithms and ensemble learning classifiers for credit scoring. Journal of Retailing and Consumer Services 27, 11–23.