Attraction properties for general urn processes and applications to a class of interacting reinforced particle systems.

Jiro Akahori***Department of Mathematical Sciences, Ritsumeikan University Email: akahori@se.ritsumei.ac.jp, Andrea Collevecchio†††School of Mathematical Sciences, Monash University Email: andrea.collevecchio@monash.edu, Timothy Garoni‡‡‡ARC Centre of Excellence for Mathematical and Statistical Frontiers (ACEMS) and School of Mathematical Sciences, Monash University Email: tim.garoni@monash.edu and Kais Hamza§§§School of Mathematical Sciences, Monash University Email: kais.hamza@monash.edu

()

Abstract. We study a system of interacting reinforced random walks defined on polygons. At each stage, each particle chooses an edge to traverse which is incident to its position. We allow the probability of choosing a given edge to depend on the sum of, the number of times that particle traversed that edge, a quantity which depends on the behaviour of the other particles, and possibly external factors. We study localization properties of this system and our main tool is a new result we establish for a very general class of urn models. More specifically, we study attraction properties of urns composed of balls with two distinct colors which evolve as follows. At each stage a ball is extracted. The probability of picking a ball of a certain color evolves in time. This evolution may depend not only on the composition of the urn but also on external factors or internal ones depending on the history of the urn. A particular example of the latter is when the reinforcement is a function of the composition of the urn and the biggest run of consecutive picks with the same color. The model that we introduce and study is very general, and we prove that under mild conditions, one of the colors in the urn is picked only finitely often.

AMS 2000 subject classification: 60K35

Keywords: urn processes, strong reinforcement, system of reinforced random walks.

1 Introduction

1.1 Description of the main models and results

This paper contains two main results concerning an interacting particle system and a general urn model. The results are connected, as the latter concerns the main tool we use in our study of the former. We do however emphasize that the main result on the class of general urns is also of independent interest.

For the first result, we study a system of interacting particles defined on a polygon. Each particle reinforces an edge when passing through it, and can be affected by the behaviour of all other particles as well. More precisely, given that a particle is located on a given vertex, its next transition would be towards a neighbor of that vertex. The probability that it traverses a given edge is proportional to a quantity which depends on how many times that particle has previously traversed that edge, how many other particles traversed that edge, and other factors. In order to study this system we need to keep track not only of the position of the particles but also of the transition probabilities which evolve randomly in time. We are able to understand the main features of the behaviour of each single particle by keeping track of its position and an auxiliary Markov chain on a larger space. Under general assumptions we infer that if the reinforcement is strong enough, each of the particles gets ‘stuck’ on exactly one edge. To understand the impact on applications of this model see, for example, [16]. In fact, many biological systems can be modeled by random walkers that deposit a non-diffusible signal that modifies the local environment for succeeding passages. The response to the environment frequently involves movement toward or away from an external stimulus (see [16]). In these systems, one example of which is the motion of myxobacteria, the question arises as to whether aggregation happens.

Our results are, to the best of our knowledge, the first involving interacting random walks with strong reinforcement. We focus on the case when the underlying graph is a polygon. A lot of effort has been devoted to the study of single strongly reinforced particles on polygons, resulting in a long-standing open problem to establish localization (see [22], [15], [5], and Section 1.5 for a literature review). Moreover, we believe that our method can, in principle, be pushed to describe the behaviour of many reinforced interacting particles on more general graphs.

For our second main result we consider a very general urn model where the probability to pick a ball of a given colour depends on intrinsic features of the colour, the past behavior of the urn process as well as external factors. In particular, at each stage the composition of the urn changes by adding exactly one ball and the probability to pick a ball of a particular colour is determined by an underlying Markov process defined on a general space. This is a significant generalization of Pólya urns, as the transition probabilities not only may depend on the actual composition of the urn but also on the whole past and even other external factors.

Urn models have been used successfully to describe the evolution of systems composed of elements which interact among each other. Such systems are of great interest in several areas of application: in medicine, clinical trials and the evolution of a system of interacting cells, in the social sciences, networks and preferential attachment (see for example [3]), in physics and chemistry, the evolution over time of the concentration of certain molecules within cells (see for example [19]).

For a literature review on reinforced random walks and urns see Section 1.5. In the next section we introduce a toy model that will shed some light on the general structure we are considering in this paper.

1.2 Example of a reinforced random walks system on a triangle with two particles

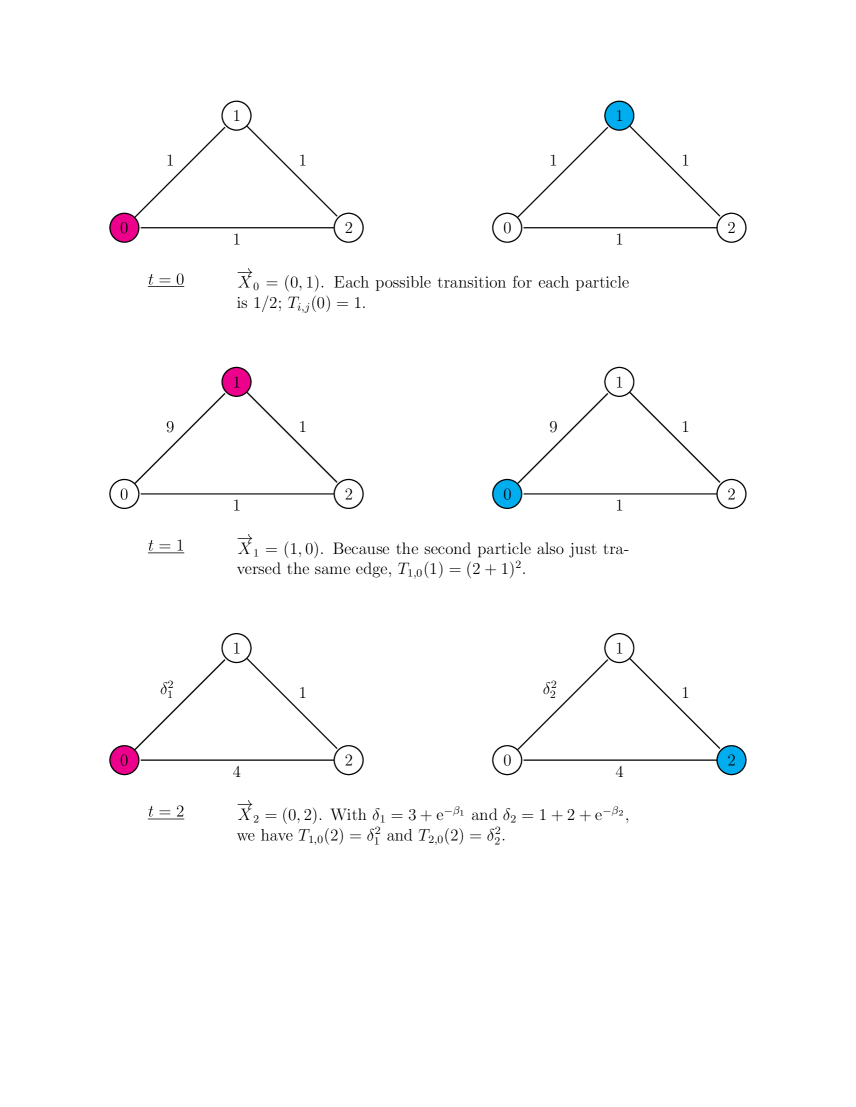

Consider a system of reinforced random walks defined as follows. The system consists of exactly two particles that take values on the vertices of a triangle labeled 0, 1 and 2. Each particle jumps at each stage to one of the other two vertices (the two nearest neighbors). We label the edges using the same set , where edge is the one connecting to . All labels are understood modulo 3 so that a label of 3 equates to a label of 0. Initially, each particle assigns a weight of one to each edge. These weights will change in time.

Starting from an initial configuration , we recursively define the stochastic process in the following way. Let

be the number of times particle traverses edge in either direction (plus one), and

represents the reinforcement function for particle on edge . It takes into account the times the other particle traversed edge , discounted in time with rate .

Conditional on the “present”, together with , the probability that particle jumps to vertex is given by

where is mod 3.

In this system of particles, each particle remembers its past, and detects the chemicals, e.g. slime for myxobacteria or pheromones for ants, that the other particles leave in their trails. We suppose that this chemical evaporates in time, and this explains the discount factor included in the reinforcement functions.

A particular evolution of this system up to time two is depicted in Figure 1 where the two particles were decoupled and their movements represented on separate triangles.

We anticipate that each particle will visit one of the vertices only finitely often. In other words, each of the particle gets stuck on one of the edges, possibly different edges for different particles.

A more general example, one with particles on a general polygon, will be described in Example 1.3. It forms part of a more general setting which is introduced in the next Section.

1.3 Interacting reinforced random walks on finite polygons.

Consider a polygon with exactly vertices, and label them using the set of integers . We assume that is connected exactly to and . Here and are understood modulo and we shall simply write and .

We denote this graph by , where is the set of vertices and is the set of edges. We call the edge connecting vertex to . By this labelling, we can identify with .

We consider, on a filtered probability space , a system of reinforced random walks that interact through reinforcement. More specifically, with , denote the -th random walk by , for and set

Reinforcement occurs through the number of traverses of a particular edge, augmented by an initial weight, but can also be affected by other factors, be it environmental or path-dependent. To this end, we suppose that, for each edge and each process index , we are given a -measurable random variable , the initial weight, as well as a -adapted process , representing the other factors. Together, they form the reinforcement functions

| (1.1) |

for some , where

| (1.2) |

Finally, each walk takes values on the vertices of and jumps, at each step, to one of two neighbors according to the rule

Further, we assume that given , the transitions of the particles at time are conditionally independent.

It is natural, and mathematical convenient, to restrict the choices of processes as to ensure that the process

| (1.3) |

evolves as a strong Markov chain on a countable subset of .

The quantities appearing in (1.3) are defined as follows. For each and let

Given , we denote by the probability measure on that sets the initial states of the chain to : .

Definition 1.1.

With a slight abuse of notation, set , which is the system of particles just described with starting point . We denote by .

Theorem 1.2.

Consider with a fixed . Assume that , a.s., for some constant . Then each , with , will localize on one edge, i.e. for each , there exists a vertex such that for all large we have that .

Notice that the model is only well defined for a finite number of particles. This circumvents the difficulty of dealing with infinite products.

Example 1.3.

Define as follows.

for a fixed , , and . In this case, the process is influenced by the number of times the other particles passed a given edge, discounted in time. To see why is a Markov chain in this case, notice that

Moreover,

In the case of , we can allow different discount factors , as described in the Section 1.2. In fact, the markovian structure is preserved.

In this example, particles enjoy a support system with diminishing memory. Each time a particle traverses an edge, the likelihood that it is traversed by other particles is increased. However, this effect diminishes (exponentially) over time. An example of such behaviour could be found in ants. As they travel along a path, they deposit pheromone, a behaviour-altering chemical agent that encourages other ants to take the same path. This chemical evaporates over time reducing its ability to reinforces the path. The system reinforces recently visited edges.

Example 1.4.

For , and , set on the event and

| (1.4) |

otherwise. Set

1.4 Definition of Generalized Urn Processes (GUP).

Before we introduce the definition of Generalized Urn Processes (GUP), we analyze a key example, where the transition probabilities of the urn depend not only on its actual composition but also on other factors.

Example 1.5.

Consider an urn which initially contains exactly two balls, one white and one red. At each stage, a ball is added according to a certain random rule described below. Fix an increasing function with the following properties. Either

-

•

, or

-

•

is twice continuosly differentiable, , , exists in , and

Let be a homogeneous Markov chain taking values in a countable state space and adapted to a given filtration . Denote the composition of the urn at time as follows. Set (resp. ) the number of white (resp. red) balls in the urn at time , with . Then, conditional on , the probability to pick a white ball at stage is

where and are two given positive functions. Note that is possibly larger than the natural filtration of the urn process. We assume that , a.s. for all large , for , and some positive increasing function satisfying

| (1.5) |

We prove (see Theorem 1.10 below) that, under the above assumptions the urn localizes on one of the two colours. More precisely one of the colors will be picked only finitely often. This a by-product of a more general result, i.e. Theorem 1.9. Examples of functions which satisfy the properties above are , with , for , and , for some . For these choices of , we can choose for any

Define a generalized urn process, called GUP, as follows. Informally, the key in this definition is that there is a driving Markov process, defined on a larger abstract space, which carries the information about the transition probabilities and the composition of the urn.

Formally, consider an urn which initially contains a fixed number of balls, white and red, where . Suppose that at each step a ball is picked, its colour observed, and returned to the urn together with another ball of the same colour. Given the history of the process up to time , the probability of picking a white ball is

| (1.6) |

where and are positive, random and depend on the history of the process up to time . We set , for . Denote by , the composition of the urn at time ; white balls and red balls. We assume that the urn process satisfies the following properties.

-

A)

There exists a countable space , such that for each there exists a probability space and a homogeneous Markov chain on , which satisfies the following. For each , we have . Moreover and for some functions and , with .

-

B)

There exists such that for all , and .

The process GUP, described above, is a strong generalization of Pólya urns. Our aim is to understand the behaviour of the urn based on the behaviour of each of the , with , . The processes are called the reinforcement functions associated to the GUP. We emphasize that our results below only assume the existence of general quantities such as the process and not their knowledge.

In what follows denotes a sequence, whereas denote a set. The difference is that the sequence allows repetitions. We denote by the minimum between and and by the maximum between and . For any countable set define with the usual convention that the sum over the empy set is zero. For each , define the sequence of random times where we pick the ‘-th colour’, as follows. For , let . Suppose we defined , then let . Let

and set Recall that can list the same element more than once. Note that the quantities and , with , and , are deterministic.

Assumption I. There exists such that , for all .

Remark 1.6.

Assumption I becomes a familiar condition in reinforced random walks and generalized Pólya urns when the reinforcement functions only depend on the actual composition of the urn; more specifically when (1.6) holds for , with , for a pair of deterministic functions . In this case, (as ) and Assumption I is necessary and sufficient, according to the celebrated Rubin’s Theorem (see [7]), for one colour to be picked finitely often, a.s..

Denote by the event that . For and , set . The following Proposition is a corollary of Proposition 4.1 which can be found in the Appendix.

Proposition 1.7.

.

Definition 1.8.

For any fixed sequence , with , consider independent GUP(), where (, with ) denotes a sequence of independent copies of with different starting points. The process starts from . Let be the corresponding product measure. For fixed , define (resp. ), to be the sequence of reinforcement functions determined by (resp. the sequence of composition of the -th urn by time ). Let be the event that . Set

| (1.7) |

Let

The sequences , with , can be finite.

Assumption II. Suppose and there exists a sequence that satisfies the following conditions

-

i)

;

-

ii)

Either , a.s., or

(1.8) where .

-

iii)

There exist two families of random sequences and which satisfy the following.

-

–

For , is measurable with respect to , , , and

-

–

Define , and . For all larger than an a.s. finite random time (not necessarily stopping time), we have

(1.9)

-

–

Our main result is the following.

Theorem 1.9.

Consider GUP(, for some . Assumptions I and II cannot simultaneously hold.

Theorem 1.10.

The urn described in Example 1.5 is GUP and one of the colours is picked only finitely often.

Theorem 1.9 is a very general and powerful tool to decide whether for urns where the reinforcement depends not only on the composition of the urn but also on external factors (e.g. interacting urns) or internal ones depending on the history of the urn. A very particular example is when the reinforcement is a function of the composition of the urn and the biggest run of consecutive picks with same colour. To the authors’ knowledge very little is found in the literature about urns with strong dependence on the past. In general the reinforcement only depends on the composition of the urn at a given stage, revealing still a Markovian structure. This is of course quite a constraint for the applications. Think of a consumer that has to choose between two products. He will not only observe how many times in the past one of the products has been chosen over the other by other consumers, but also the actual trend. In fact it is possible that one of the products might have been chosen less times than the other but was quite successful in recent times, attracting the preference of the consumer.

Urn processes have a variety of applications and are very important tools in statistics, medicine and network theory (see preferential attachment models). We emphasize that we cannot recover these results from the standard general techniques already available for generalized Pólya urns. In particular we were not able to apply the decoupling method introduced by Rubin (see [7]) in our setting to prove attraction properties of one colour over the other. A review of the existing results and applications of urn models is given in Section 1.5.

1.5 Literature review

Reinforced random walks were introduced by D. Coppersmith and P. Diaconis in an unpublished manuscript ([4]). The case of a single particle which moves to nearest neighbors vertices of a graph is considered. The probability to traverse a given edge incidental to the actual position is proportional to the weight of that edge, which in turn evolves in time as follows. Each time is traversed the edge’s weight is increased by a fixed constant . This is the linear case. A more general case was studied by B. Davis [7]. He studied the case where the probability to pass an edge is proportional to a reinforcement function of the times that edge has been traversed in the past. T. Sellke (see [17]) conjectured that if the reinforcement function is strong, i.e. satisfies , then RRW on the triangle visits exactly two adjacent vertices infinitely often; that is oscillates on one edge at all large times. V. Limic proved the result when for . Limic and P. Tarrés (see [14]) extended this result on general graphs for a large class of reinforcement functions, including all the monotone increasing functions. C. Cotar and D. Thacker have recently announced (see [5]) a complete solution of the problem on any bounded degree graph. They also include in their paper complete results for the superlinear vertex reinforced random walk. As for the latter properties, it is curious that it shows localization even in the linear case, where each vertex is reinforced by one each time it is visited. It was proved by Tárres (see [20]) that when defined on it localizes on exactly 5 consecutive vertices. See also [23] for the study of this process on general graph. For a survey on reinforcement, including discussion on linear and sublinear reinforced random walk see [19] and [12]. The results listed above only describe the behaviour of a single particle. In [11] it is considered a system of two particles with linear reinforcement, defined on . In that paper Y. Kovchegov proved that the two particles meet infinitely often. Yilei Hu studied the case with particles in his Phd thesis (see [9]).

To the best of our knowledge, the result contained in our paper is the first concerning a system of particles which interact through strong reinforcement. We also emphasize the fact that our results on urn and system of reinforced particles go beyond the simple composition of the urn or the number of times an edge has been visited. It actually covers more sophisticated transition probabilities.

1.6 Brief description of the proof of Theorem 1.9

We reason by contradiction. We suppose that both Assumptions I and II hold. From now on is used to denote a sequence which satisfies Assumption II. Later, we will work with subsequences of this sequence. We embed infinitely many urns using the same Brownian motion, sequentially. Each embedding can be briefly described as follows. Suppose we defined , then the composition of the urn at time , i.e. is determined by the Brownian motion. We then use an external randomization to get using the fact that given and the support of is countable and conditionally independent of the past with . Recall that we denoted by the Markov processes associated to the -th urn. The -th urn has initial condition . Time , properly defined later, will denote the time when the first urns are embedded. We prove that a.s.. In fact, this stopping time is smaller than the hitting time of a the set for some finite . Hence the process , with , is a martingale. We prove that there exists a random time such that for all . We also prove that under Assumptions I and II the stopping time has infinite first moment. At this point we distinguish two cases.

-

•

If , using the Kolmogorov three series Theorem and Burkholder-Davis-Gundy (BDG) inequality, we prove that which yields a contradiction with the above statement.

-

•

then we use BDG inequality to argue that the martingale , with , is bounded in . This contradicts, using the Doob martingale convergence Theorem, its convergence to .

Throughout the embedding, we make use of the following fact.

Remark 1.11.

For any function , and any positive constant , denote by the function which maps . Fix . It is immediate to realize that GUP(), where is a positive constant, has the same distribution as GUP(). In fact, the transition probabilities described in (1.6) remain unchanged.

1.7 Embedding of the GUP into Brownian motion

Let be a sequence in satisfying the conditions in Assumption II. We embed GUP() into Brownian motion. Recall that we denote the reinforcement processes for this urn using , with . To simplify the notation, we drop the index 1 in the remaining part of this subsection. Fix . Set , i.e. the initial configuration of the urn, which is determined by . Recall that the reinforcement functions at time 1, i.e., and are also determined by . Set and . Recall the definition of the sequences and , with , from Assumption II. Let the process be a standard Brownian motion, which starts at . Denote by the natural filtration of this Brownian motion. We use this process to generate GUP( ). Set , a.s.. Let

| (1.10) |

If then set , otherwise set . Given , with , we define by generating a random variable independent of , with distribution

and setting . Suppose we defined and . Set to be the -th coordinate of , with . Set

If then set , otherwise set . Next, given the events , with , we define by generating a random variable , independent from both and , and with distribution

and setting . We assume that Brownian motion and the random variables , , are defined on the same probability space .

By the ruin problem for Brownian motion, we have that

which is exactly the urn transition probability.

Remark 1.12.

It is convenient for us to embed the process into the Brownian motion, because we use the well known results regarding this process to get a contradiction.

Define

| (1.11) |

This limit exists because the sequence of stopping times is increasing. For this reason is itself a stopping time, possibly infinite.

1.8 Proof of Theorem 1.9 in the case , for infinitely many .

We reason by contradiction and assume that both Assumptions I and II hold. We further assume in this part of the proof that for infinitely many . By taking a subsequence, we assume that holds for all . In virtue of Proposition 1.7, we have that . Recall the definition of from Section 1.1. Set

| (1.12) |

The sequence is deterministic, this will play a major role in what follows. Notice that we are going to repeat the procedure of taking subsequences few more times in the remaining part of the proof. Consider the infinite sequence of independent copies of , say with starting points . Set . Next, we use the process to embed GUP(, , , ) defining the hitting times and to be times when the -th ball is generated (similarly to what we have described above) and let to be its ending stopping time, i.e. . We repeat this procedure, to define the stopping times , each time using a new reinforcement scheme, as follows. For . we have that time is the ending time of the embedding of GUP(, , ) and all the GUP(, , ), with .

Remark 1.13.

The GUPs embedded are independent of each other. As before, we assume that the Brownian motion and the variables used in the embedding are defined on the same probability space . Finally, notice that by the fact that is a deterministic sequence, combined with remark 1.11, we have that GUP(, has same distribution as GUP(, . We use because it changes the time needed to embed. In this way the total time needed to embed all the GUP’s has infinite expectation, as we prove below.

Definition 1.14.

Set to be the event that infinitely many balls of each colour are picked in the GUP().

Proposition 1.15.

There exists an a.s. finite random time such that for all , we have

Proof.

Recall the definitions of and from the introduction.

As and form a partition of , we have that

eventually, The last inequality is due to Assumption II.

The next Proposition is a well known result from Brownian motion. For completeness, we include its proof in the Appendix of this paper. Denote by the hitting time of the point by the one dimensional Brownian motion.

Proposition 1.16.

Denote by the probability measure associated to a Brownian motion which starts from . Denote by the corresponding expectation. For , we have

| (1.13) | |||||

| (1.14) |

Remark 1.17.

Notice that if both and are non-negative then

| (1.17) |

Recall that denotes the composition at time in the GUP(, , , ) embedded into Brownian motion. Notice that ‘time’ for the GUP(, , , ) translates into time for the Brownian motion.

Definition 1.18.

Let be the index such that . Let We define to be the -th element of , which was defined in (1.7). More precisely, let , and let

Define .

Lemma 1.19.

Denote by the expected value associated to the measure . For , we have that for all ,

| (1.18) |

Proof.

Given the variable is independent of

-

i)

where recall that is the natural filtration of Brownian motion ;

-

ii)

, with , as this process is a Brownian motion independent of ;

-

iii)

. This is a consequence of points i) and ii) above.

This together with (1.13), (1.14) and the structure of our embedding scheme proves (1.18).

Remark 1.20.

Using (1.17), we have

| (1.19) |

Lemma 1.21.

We have

Proof.

Definition 1.22.

Let By Assumption II i), combined with Borel-Cantelli Lemma, , a.s.. Define where was defined in the statement of Proposition 1.15. By taking a subsequence of we may and do assume that

Proposition 1.23.

If Assumptions I and II hold then

Proof.

Notice that Assumption II can be rewritten as

This implies that no matter which subsequence of the we are considering, we have

This implies, using Lemma 1.21,

Lemma 1.24.

We have

| (1.21) |

Proof.

Recall the definition of given in Assumption II and from (1.12). In order to prove (1.21) it is enough to prove

The latter is proved once we prove that

| (1.22) |

where the random sequence was introduced in definition 1.18. The first inequality in (1.22) comes from the fact that , for all , due to the definition of . The last inequality is a consequence of the definition of , because the -th term in is larger than We used the convention , and .

Definition 1.25.

Recall and from definition 1.18. For , set

Lemma 1.26.

a.s..

Proof.

As exactly one of the two quantities and equals one while the other is zero, we have

where we used again the fact that , for all .

Lemma 1.27.

Let . We have

| (1.23) |

Proof.

Notice that for any positive function , we have that for any ,

| (1.24) |

For , using , for all , we have

| (1.25) |

where in the second inequality we used (1.24) with and the definition of . (1.25) proves the Lemma for the case . The remaining case, i.e. is dealt as follows.

where in the last step we used both

and

Proposition 1.28.

There exists a constant such that for all , we have

| (1.26) |

Proof.

It is a consequence of (1.13) and the following reasoning. Using conditional independence (see proof of Lemma 1.19), we have that for ,

| (1.27) | ||||

We have

First we prove that I is -a.s. bounded by a constant. Using (1.27), (1.18), (1.13), (1.16), and the non-negativity of , we have

In virtue of Lemmas 1.24 and 1.26, each of the terms appearing in the previous equation are bounded by a constant which is independent of . Next we prove that II is a.s. bounded by a constant. Notice that from corollary 1.20 with , we have

where , , and . Hence, using corollary 1.20, we have

| (1.28) |

In virtue of Lemma 1.27, each of the terms appearing in the previous equation are bounded by a constant which is independent of , ending the proof.

Lemma 1.29.

Proof.

Using Jensen’s inequality, and setting , we have

where in the last step we used Lemma 1.27. Notice that using Burkholder-Davis-Gundy (BDG) inequality, we have

for some constant . Hence

Define . The random variable can be seen as an infinite sum of independent random variables . Moreover, in virtue of Proposition 1.15, we have that is non-increasing for . This implies that . Hence, by Kolmogorov 0-1 law, is either a.s. finite or it equals a.s..

We distinguish the two cases.

Case I. In this case, we assume that

| (1.29) |

Lemma 1.30.

If we assume (1.29) then we can choose a subsequence , with , such that

Proof.

As can be represented as the sum of independent variables we have, using the Kolmogorov Three Series Theorem (see for example page 115 of [18]), that

| (1.30) |

On the other hand

| (1.31) | ||||

The inequality before the last one is an application of BDG inequality, and the last inequality is a consequence of Proposition 1.28. By the three-series Theorem, we have that

The latter implies that . Hence we can choose a subsequence of such that

| (1.32) |

Notice that the embedding times obtained using satisfy (1.29). Next we work with the embedding obtained using the sequence . Combining (1.32) with (1.31), we have that

| (1.33) |

Using the trivial inequality , we have

Combining this with (1.30) and (1.33), we get

Recall that is a zero-mean random variable. Hence . Using Fatou’s Lemma, we have

This implies our result.

Recall that from Lemma 1.29 we have Notice that for any sequence which has the property that there exists an integer such that for all , we have

| (1.34) |

where . In fact, the inequality is trivial for . For notice that the sequence is non-decreasing in . Hence . Hence, for we have

proving (1.34). Using , we have

| (1.35) |

By the Optional Sampling Theorem, we have that , for all . Hence, for ,

| (1.36) | ||||

where we used Lemmas 1.29 and 1.30 to establish that the latter quantity is finite.

Equation (1.36) yields, by sending and using monotone convergence Theorem, that which contradicts Proposition 1.23.

Case II.

Assume that

a.s..

The process , with , is a martingale. In this case we have that

| (1.37) |

For we have This implies that for all , we have

| (1.38) |

where in the last step we used Lemma 1.29. Notice that, as is a zero mean martingale, we have

Hence, the martingale convergence theorem implies that exists and is integrable. This contradicts (1.37).

1.9 Proof of Theorem 1.9 in the case , eventually.

Recall that we are assuming that both Assumption I and II hold and again reason by contradiction. In this case, to complete the proof of Theorem 1.9 we suppose that for all but finitely many , where is the sequence described in Assumption II. By taking a subsequence, we assume that for all . Hence, in virtue of Assumption 1, there exists an index such that for all . Without loss of generality, we suppose that for all while for all . In order for Assumption II to hold, we have

| (1.39) |

for all . Fix such that (1.39) holds and . This implies that

where the sequence was introduced in definition 1.18. We embed the GUP( into Brownian motion starting at 0, in the way we described in Section 2.3. Notice that we embed just one GUP. In this embedding we choose and for all . In this case, on , the Brownian motion would hit before hitting , which gives a contradiction, as the Brownian motion is recurrent in one dimension.

2 Proof of Theorem 1.2

From now on we fix and assume that the assumptions of Theorem 1.2 hold. Recall the Markov process , with , which takes values in the space defined in Section 1.3.

The next result establishes that the jumps from each vertex of the -process can be modelled using a suitable GUP. In order to simplify the notation, as is fixed, we remove it from most of the notation used throughout this section, with the exception of the process itself.

Lemma 2.1.

Fix . Consider . Suppose that each time the process jumps from to (resp. to ) we add one white ball (resp. one red ball) to a given urn. This urn evolves like a GUP(), for some choice of reinforcement processes , and Markov process on . This representation is true up to the random time, possibly infinite, of the last visit of the process to vertex .

Proof.

Set Throughout this paper, the infimum over an empty set is . Define recursively, for ,

In the remaining part of the proof of this lemma, we simplify the notation into , removing the reference to the vertex , which is fixed. Set Define the processes

Next we show that these processes satisfy the conditions listed in the definition of GUP. In fact, referring to the definition of GUP, given in Section 1.11, we have the following.

-

A)

It is satisfied. The processes and (the latter is the composition of the urn described above, at time ), with , are determined by .

-

B)

is countable. This is a consequence of our assumption on the family of random variables .

The resulting GUP models the jumps of from vertex to its neighbors, up to the last visit of this process to .

Definition 2.2.

We denote the GUP described in Lemma 2.1 by GUP(), where is the initial configuration of . Define to be the event that GUP() picks infinitely many balls of each colour. We emphasize the fact that these objects depend on . However, in our reasoning below, we decouple the behaviour of from the other processes.

For and , under the measure is deterministic. We denote using the value of under . Define the event

Notice that implies that . As jumps to nearest neighbors, we can assume that is a connected set. Our aim is to prove that holds with probability 1, no matter what is the initial configuration in . More precisely we prove that can be taken as the set of two adjacent vertices. Of course this pair of vertices is random.

Set to be the smallest even number larger than both and . Define the set as follows.

Lemma 2.3.

Consider , for . We have

| (2.1) |

Proof.

Consider . Throughout this proof, the constant stands for a generic positive constant which depends on but does not depend on the initial state of the Markov chain , with .

Next, for each configuration , we distinguish two main cases.

-

1.

Suppose satisfies

(2.2) We prove, for this case, that

(2.3) where recall that is a constant independent of . Our strategy to prove (2.3) is to prove the existence of a path of length , with probability at least , which makes . We describe the path as follows. Consider the largest between and . Suppose the latter is the largest. It is easy to adapt the following argument to the other case. Define the event

Notice, that as is even, on the event we have that . Define . Finally let

Notice that on we have that , and that we use in the definition of in such a way that the condition , appearing in the definition of , is satisfied. Next, we bound from below when satisfies (2.2). As we already pointed out, the event depends on the first consecutive jumps of . During the first steps, the difference between adjacent weights can be at most , which is a rough upper bound. This is because satisfies (2.2). Hence, each path of length has a probability of at least

(2.4) It follows from the fact that the function

is monotone increasing, for .

-

2.

Suppose that satisfies

(2.5) Notice that (2.5), together with and the fact the underlying graph is a polygon, implies that

(2.6) To prove (2.6), it is enough to reason by contradiction. If (2.6) does not hold, then the minimizer of would satisfy , which contradicts .

Consider to be one among the largest non-empty set of consecutive edges with the following property. If , then

In virtue of (2.5), we have . Denote by the second largest subset of consecutive edges, disjoint from , with the properties described above. Notice that could be an empty set. On the opposite, could have the same size as .

Suppose that consists of exactly edges, with , say . To simplify the notation, we assume that and leave to the reader the simple task to adapt the following reasoning to the general . Notice that in what follows, to simplify the reasoning, we ignore the second condition appearing in the definition of , i.e. . This would affect the path by just one step (stop either one step earlier or one step later).

First, suppose that . We first deal with the case where the probability of the event(2.7) Set Recall that is the hitting time of vertex by the process . We have

(2.8) yielding the result for this case. In fact, on the event appearing in the probability in the right-hand side of (2.8), we have

for . As for the requirement , as discussed above, it holds for at least one element of the set .

When (2.7) does not hold, replace with in the left-hand side of (2.8).

Next, suppose that . We distinguish two further subcases. The number of edges in can be either or . First consider the case when has exactly one edge, which we denote by . Assume that under the initial configuration we have . We can adapt easily the following argument to the other case. Let . Let . Define recursively . Set . Notice that(2.9) Notice that on the event inside the previous probability, we have that either holds or hits .

Finally consider the case when is empty, and consists of exactly one edge . SetAgain, we distinguish two cases. Define

(2.10) where the constant is chosen to be large enough, as specified later. Suppose that . Suppose that . Then,

(2.11) If the event appearing inside the probability in (2.11) holds, either holds or the process hits . A similar result holds when .

Next, we consider the case when the initial state . We show that either holds, or there exists an a.s. finite time , under , such that . It means that either holds or we can use results from other cases to infer that hits . We reason by contradiction. For each , define the following eventWe have that Suppose for some . Consider the following urn. Suppose that each time that jumps from vertex to or from to we add one red ball and each time it jumps either from vertex to or from to we add one white ball. We show that this urn evolves like a GUP(), for some choice of reinforcement processes , and Markov process on . To see this, define

Define recursively, for ,

Define the stochastic processes

where . Let , for . It is trivial to check that A) and B) from the definition of GUP are both satisfied. For to hold, either must hold or infinitely many balls of each color must be picked. Suppose that , where, as before, is the event that infinitely many balls of each color are picked in this urn. In virtue of the proof of Proposition 4.1, we can find a sequence of configurations in , such that

(2.12) and . Next we prove that this GUP would satisfy both Assumption I and II, yielding a contraddiction. As for Assumption I), it is simple to check, using (1.1), that

for .

As for Assumption II) i), we can definitely choose (by considering subsequences) in such a way that it satisfiesThere exists random time such that if then holds -a.s.. We turn to Assumption II ii). We have

Whenever a red ball is picked from GUP, the following happens. The process either jumps from to or from to . Before returning to vertex or , it must cross again either edge or edge . In the evaluation of and we don’t count the transition weights used to jump from to and the ones used to jump from to . In the evaluation of and we don’t count the transition weights used to jump from either to or from to . Recall that for this GUP we have that the initial state satisfies , due to (2.12). Recall that . We have

notice that on ,

Finally Hence Assumption II ii) is satisfied on . We turn to Assumption II iii). Denote by , with , the reinforcement process for this GUP with initial condition . We associate to the edges and , while is associated to edges and . For , we have

whereas

where the last inequality holds for large enough. Hence, Assumption II iii) holds with the choice for all . Using Theorem 1.9, we infer that only finite many red or white balls are picked. This contradicts .

Next we combine the two cases described above, to get our result. Notice that in each of the cases we considered, there is a positive probability that either hits a configuration in within an a.s. finite time on or the event I holds. Denote by the hitting time by the process . In the reasoning above, we sometimes simplified the notation and fixed to be a particular set of edges. For this reason time appeared in one of the estimates. More generally, is an apper bound for each of the times listed above, with the exception of the case when the initial configuration is in . Set and

where is the hitting time of after the first hitting time of which happens by time on. Notice that . Finally, notice that as in our reasoning above was arbitrary, we have

where . Using the strong Markov property and the Borel Cantelli Lemma, we have our result.

For , define one of the indices , chosen uniformly at random among the ones which satisfy

| (2.13) |

If , set . Let the event

Lemma 2.4.

Proof.

Lemma 2.5.

For any we have .

Proof.

For any vector , define the following shift operator, which means that we change the labels of the vertices mapping . More formally, we denote the shift operator by , where under we have , and finally . For , define and recursively We have

| (2.14) |

This is because the event does not depend on the actual label of the index chosen uniformly at random from the set of indices satisfying (2.13). It is enough to prove that for . In virtue of (2.14), for each , we can set, using a proper rotation, . Consider . Suppose that each time that jumps from to or to we add one red ball and each time it jumps either from to or from to we add one white ball. We show that this urn evolves like a GUP(), for some choice of reinforcement processes , and Markov process on . To see this, define

Define recursively, for ,

Define the stochastic processes

where recall that . Let , for . It is trivial to check that A) and B) from the definition of GUP are both satisfied. In this context is a subset of the event, that in the urn described above, both white and red balls are picked infinitely often. Suppose that

and reason by contraddiction. Recall that we can find a sequence such that

Consider GUP, as defined in the proof of Lemma 2.4. By taking subsequences, we assume that . Next we prove that this GUP, if , would satisfy both Assumption I and II, yielding a contraddiction. As for Assumption I), it is simple to check, using (1.1), that

for .

As for Assumption II) i), we can definitely choose, by considering subsequences, satisfying

We turn to Assumption II ii). We have

Whenever a red ball is picked from GUP, the following happens. The process either jumps from 1 to 0 or from 2 to 3. Before returning to vertex 1 or 2, it must cross again either edge 0 or edge 2. In the evaluation of and we don’t count the transition weights used to jump from 3 to 2 or the ones used to jump from 0 to 1. Recall that for this GUP we have that the initial state is in . Hence , and , and this implies

notice that on ,

Finally Hence Assumption II ii) is satisfied. We turn to Assumption II iii). Denote by , with , the reinforcement process for this GUP with initial condition . We associate to the edge 1. As on we have that this implies that

where in the last inequality, we used

On the other hand, we have that

Then, as , we have

| (2.15) |

Hence, Assumption II iii) holds with the choice for all ,.

Hence, if

we have that

Assumption I and II hold for this particular GUP. In virtue of Theorem 1.9 and Lemma 2.4, we have a contradiction.

We denote by the minimum time satisfying the following. For , the condition , implies that

In words, the process after each visit to either or made after time , it steps always in the same direction. If the direction taken is from to and from to , then I holds, as either the process visits only two vertices at all large times or the set is visited only finitely often. The alternative, in virtue of Lemma 2.5, is that from it always jumps to and from it always jumps to . Notice that is not stopping time, and that can be infinite. On the other hand, if , on , due to Lemma 2.5.

For , denote by

Lemma 2.6.

Fix , and . We have

| (2.16) |

Proof.

To prove (2.16) we reason as follows. Recall that is the -th visit to vertex . Define as the maximiser of , with . In case of equality, we pick edge . Define

Our goal is to prove that

| (2.17) |

In fact, if then for all . The probability, that after time , , the process will traverse the edge , conditionally to the past, is at least

This is because edge has an advantage at time , in terms of transition probabilities. This, together with Borel-Cantelli Lemma, proves (2.17). The extra appearing in the definition of is due to the gap between and .

Lemma 2.7.

Fix and . Set . Then

| (2.18) |

Proof.

Denote by the event appearing in the left-hand side of (2.18). Suppose that . This implies that there exists a sequence , such that

| (2.19) |

By the proof of Proposition 4.1, we can choose in such a way that the state communicates with , i.e. there exists such that . This implies that . Consider a sequence of independent , where satisfies (2.19). Denote by , where . In order to model the jumps from vertex we have to consider an independent sequence of GUP.

We check that this sequence of GUP satisfies Assumptions I and II on . Assumption I is quite simple. As for Assumption II, choose any sequence which satisfies Assumption II i). Next we use the fact that on the event we have that each time the process jumps from vertex it goes back to that vertex using the same edge, on . We have, on ,

whereas

This is due to the fact that after time , roughly speaking, the cycle structure is broken, as explained above. Moreover,

Hence Assumption II ii) holds.

As for Assumption II iii), we

pick as follows. It equals if and equals otherwise. Recall that is associated to white balls (move to the left) white with red ones (move to the right). In fact, if , we have

Similar reasoning, applies for the case .

Hence if we reason by contradiction and assume that both colours (directions) are picked infinitely often with positive probability, then GUP satisfies both Assumption I and II and Theorem 1.9 yields a contradiction.

Proof of Theorem 1.2. Suppose that is a configuration such that . Lemma 2.3 implies that on the process hits a configuration in . Moreover on , holds (via Lemma (2.5)) and the process hits a configuration in after , in virtue of 2.6. In virtue of Lemma 2.7, for each there exists a random time and a vertex such that for all finite . This proves that

| (2.20) |

where

Next, we prove that

| (2.21) |

Denote by . Notice that there exist such that . We have

for all large , such that . This implies that for all sufficiently large , we have

| (2.22) |

for all , and . By sending , (2.22) implies that . With a very similar argument we infer . Hence, (2.20) combined with (2.21) implies that . This gives a contraddiction, as and we assumed .

Hence, we proved that , for all . Next, we prove that can be taken to contain exactly two adjacent vertices. We reason again by contradiction. Fix a vertex such that .

| (2.23) |

Consider GUP(). We proved that after a random time, each time the process makes a jump from , if it returns to it does it through the same edge used in the jump. Hence after a random time, the GUP behaves like an urn. Using the similar estimates appearing in the proof of Lemma 2.7 we obtain that After a certain random time, each jump from would either always go towards or always towards . In the former case, is visited finitely often, which yields a contradiction. In the other case, the walk we have that the event

holds, yielding another contradiction. The particular choice of the set does not affect the generality of the result. We just use a relabelling of the vertices and a union bound to get a contradiction. We conclude that the process oscillates between exactly two vertices at all large times.

3 Proof of Theorem 1.10

We consider the urn defined in Example 1.5, but with general initial conditions. Denote by the initial composition of the urn, i.e. (resp. ) white (resp. red) balls. In Example 1.5 the initial composition was assumed to be . The evolution of the urn is the same as described in the Example, and the constraint on and becomes

a.s., for all large , , where the properties of are described in Example 1.5.

Notice that in virtue of (1.5), combined with the monotonicity of , we have for all large .

The process evolves as an homogeneous markov chain on a countable state space. Set

, for . Both and are functions of . With this representation, it is trivial to see that the urn in Example 1.5 evolves as GUP().

Proposition 3.1.

Consider an urn with arbitrary initial conditions. The event

holds a.s..

Proof.

Let the index which maximizes . In case of equality we choose an index uniformly at random. Define

Notice that

Using for all large combined with the second Borel Cantelli lemma, over disjoint and hence independent blocks, we have

On the other hand,

as , for all large , ending the proof.

Proof of Theorem 1.10. As satisfies it is immediate to see that the GUP associated to the urn satisfies Assumption I. Next, we reason by contradiction and suppose that for this GUP, we have that there exists such that . Then we prove that also Assumption II hold, yielding a contradiction (via Theorem(1.9)). Using the proof of Proposition 4.1, we can argue the existence of a sequence of comunicating states in , i.e. for all ,

which satisfies Assumption II i). We consider a sequence of independent urns. The urns have different initial conditions. The Markov chain associated with the -th urn is denoted by and satisfies . Denote by the initial composition of the urn when . Using Proposition 3.1, we can assume that the initial composition of the urn satisfies

| (3.1) |

In fact, for any initial state , in virtue of Proposition 3.1, there exists an a.s. finite stopping time when

Define one of the elements in the support of , such that The existence of such is a consequence of the markov property and law of total probability. We use instead of , so we drop ′ and assume (3.1) to hold. Moreover, we can assume that both sequences , are strictly increasing in . Using Proposition 4.2, we can easily argue that Assumption II ii) holds. Set

We have and . Notice that using (3.1), we have

whereas

In virtue of Proposition 4.3 we conclude that Assumption II iii) holds by choosing constantly equal to the index in corresponding to the color corresponding to the maximizer .

4 Appendix

Proposition 4.1.

Consider a Markov chain on a countable state space . Let the measure under which , a.s.. For any event , we have

Proof.

Suppose that there exists such that . Under this assumption we prove that . Let . There exists a sequence of events , such that , . For any fixed , choose large enough that and . Choose , such that

where the supremum in the right-hand side is taken over the integers such that . Recall that is a Markov chain, and the future of the GUP given is independent of . Hence as , we have

Moreover,

where was defined above. Fix . By our choice of , we have

if we choose small enough. In the inequality before the last one, we used the fact that .

Proof of Proposition 1.16 We first compute

| (4.1) |

We start with

| (4.2) |

A reference for the previous formula is, for example, Karatzas-Shreve (second edition) page 100 formula 8.28. By taking the derivative of the right-hand side of (4.3) we obtain

| (4.3) | ||||

Use the fact that the expression in the first parenthesis approaches 0 as and apply De L’Hopital to evaluate the limit in the second parenthesis, which turns out to be the right-hand side of (4.1). By taking a second derivative, we get (1.14).

Proposition 4.2.

Suppose that the function is increasing and either

-

a)

, or

-

b)

is twice continuously differentiable, with , , exists in , and

(4.4)

We have

| (4.5) |

Proof.

We distinguish the two cases. First assume that In this case, we prove that

| (4.6) |

The first step to prove (4.6) is to prove that

| (4.7) |

To this end, notice that

| (4.8) |

Hence, (4.7) is a consequence of De L’Hopital applied to the right hand side of (4.8) (with a continuous variable instead of the discrete ) and the assumption , which yield

Hence

proving (4.6). Finally

Next, we move to case b). Our assumptions imply that

| (4.9) |

exists in . Notice that

Hence, using (4.9), we infer that a sufficient condition for (4.5) to hold, is that

| (4.10) |

for some , which is specified below, and for all . A sufficient condition for (4.10) to hold is that

| (4.11) |

Using De L’Hopital in (4.11) we require that

| (4.12) |

(4.12) holds if and only if

Using the De L’Hopital one more time,

which is a consequence of (4.4).

Proposition 4.3.

Suppose that the function is differentiable, with for all . If is a positive increasing function for which there exists such that

| (4.13) |

then

Proof.

It is enough to prove

| (4.14) |

In order to prove (4.14), we apply a suitable change of variable. Let , where is smooth and one-to-one on . Since by definition , a simple change of variables yields

| (4.15) |

Hence, a sufficient condition for (4.14) to hold is

| (4.16) |

or equivalently

To this end we show that for all large we have, for ,

| (4.17) |

or equivalently that

or that

which is clearly true for large enough.

In the same way we have that, for large enough,

Acknowledgements. This research was supported under Australian Research Council’s Discovery Projects funding scheme (project numbers DP140100559, DP120102728 and DP150103588), by JSPS KAKENHI (grants number 23330109, 24340022, 23654056, 25285102) and the project RARE-318984 (an FP7 Marie Curie IRSES).

References

- [1] L. Basdevant, B. Schapira and A. Singh. (2014) Localization on 4 sites for Vertex-reinforced random walks on . Ann. Probab. 42, 2, 527-558.

- [2] M. Benaim, O. Raimond and B. Schapira (2013). Strongly Reinforced Vertex-Reinforced Random Walks on the Complete Graph. ALEA Lat. Am.. J. Probab Math. Stat. , 10, 2, 767-782.

- [3] A. Collevecchio, C. Cotar, and M. LiCalzi. On a preferential attachment and generalized Polya’s urn model. Ann. Appl. Probab. , 23, 3, 1219-1253, 2013.

- [4] D. Coppersmith and P. Diaconis Unpublished Manuscript.

- [5] C. Cotar and D. Thacker (2015) Edge- and vertex-reinforced random walks with super-linear reinforcement on infinite graphs. arXiv:1509.00807

- [6] C. Cotar and V. Limic. Attraction time for strongly reinforced walks. Ann. Appl. Probab., 19, 5, 1972-2007, 2009.

- [7] B. Davis (1990), Reinforced random walk, Prob. Theory and rel. fields Vol 84, N 2, 203-229.

- [8] M.P. Holmes, A. Sakai. (2007) Senile reinforced random walks. Stochastic Processes and their Applications Vol. 117 pp. 1519-1539

- [9] Y. Hu (2010) Essays on Random Processes with Reinforcement PhD Thesis, Oxford University.

- [10] Kious D. (2016) Stuck Walks: a conjecture of Erschler, Tóth and Werner. To Appear Annals of Probability

- [11] Y. Kovchegov (2008) Multi-particle processes with reinforcements Journal of Theoretical Probability, Vol.21 pp.437-448

- [12] G. Kozma (2012) Reinforced Random Walk. http://arxiv.org/abs/1208.0364

- [13] V. Limic (2003) Attracting edge property for a class of reinforced random walks. Ann. Probab., Vol. 31, 1615–1654.

- [14] V. Limic and P. Tarrès (2008). What is the difference between a square and a triangle? In and out of equilibrium 2. Series: Progress in Probability, Birkhäuser, 60, 481-496.

- [15] V. Limic and P. Tarrès (2007). Attracting edge and strongly reinforced random walks. Ann. Probab., 35, 5, 1783-1806.

- [16] H.G. Othmer, A. Stevens (1997), Aggregation, blowup, and collapse: the ABC’s of taxis in reinforced random walks, SIAM J. Appl. Math. Vol 57, N. 4, 1044-1081.

- [17] T. Sellke (1994). Reinforced random walks on the − dimensional integer lattice. Technical report 94-26, Purdue University.

- [18] D. Williams (1990), Probability with martingales, Cambridge University Press.

- [19] R. Pemantle (2007), A survey of random proceses with reinforcement, Probab. Surv., N 4, 1-79.

- [20] P. Tarrès. (2004) VRRW on eventually gets stuck at a set of five points. Ann. Probab., 32, 2650–2701.

- [21] A. Erschler, B. Tóth and W. Werner (2012) Stuck walks Probability Theory and Related Fields Vol. 154 pp.149-163

- [22] Sellke, T. (2008). Reinforced random walks on the d-dimensional integer lattice, Markov Process. Related Fields, 14, 291-308.

- [23] S. Volkov. (2001) Vertex-reinforced random walk on arbitrary graphs. Ann. Probab., 29, 1, 66-91.