When does inequality freeze an economy?

Abstract

Inequality and its consequences are the subject of intense recent debate. Using a simplified model of the economy, we address the relation between inequality and liquidity, the latter understood as the frequency of economic exchanges. Assuming a Pareto distribution of wealth for the agents, that is consistent with empirical findings, we find an inverse relation between wealth inequality and overall liquidity. We show that an increase in the inequality of wealth results in an even sharper concentration of the liquid financial resources. This leads to a congestion of the flow of goods and the arrest of the economy when the Pareto exponent reaches one.

1 Introduction

Today’s global economy is more interconnected and complex than ever, and seems out of any particular institution’s control. The diversity of markets and traded products, the complexity of their structure and regulation, make it a daunting challenge to understand behaviours, predict trends or prevent systemic crises. The neo-classical approach, that aimed at explaining global behaviour in terms of perfectly rational actors, has largely failed [1, 2, 4]. Yet, persistent statistical regularities in empirical data suggest that a less ambitious goal of explaining economic phenomena as emergent statistical properties of a large interacting system may be possible, without requiring much from agents’ rationality (see e.g. [6, 7]). One of the most robust empirical stylised fact, since the work of Pareto, is the observation of a broad distribution of wealth which approximately follows a power law. Such a power law distribution of wealth does not require sophisticated assumptions on the rationality of players, but it can be reproduced by a plethora of simple models (see e.g. [14, 15, 16, 17]), in which it emerges as a typical behaviour – i.e. as the behaviour that the system exhibits with very high probability – within quite generic settings.

The debate on inequality has a long history, dating back at least to the work of Kutznets [8] on the u-shaped relationship of inequality on development. Much research has focused on the relation between inequality and growth (see e.g. [9]). Inequality has also been suggested to be positively correlated with a number of indicators of social disfunction, from infant mortality and health to social mobility and crime [10].

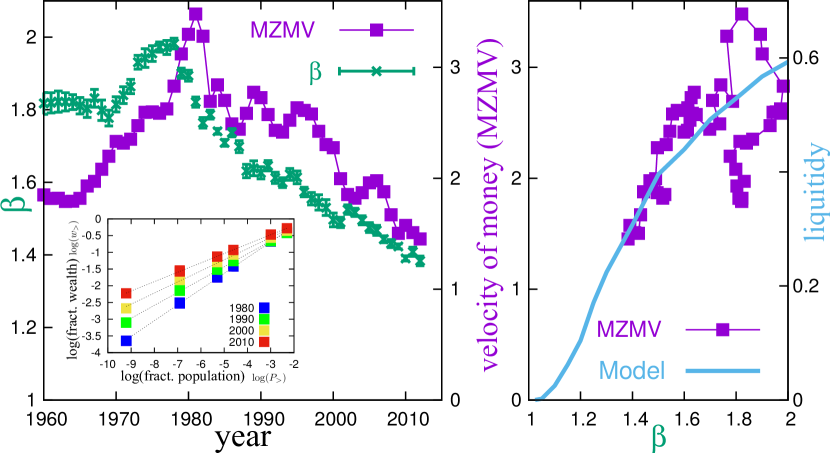

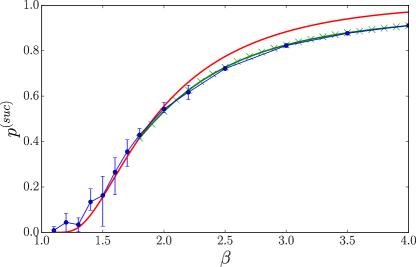

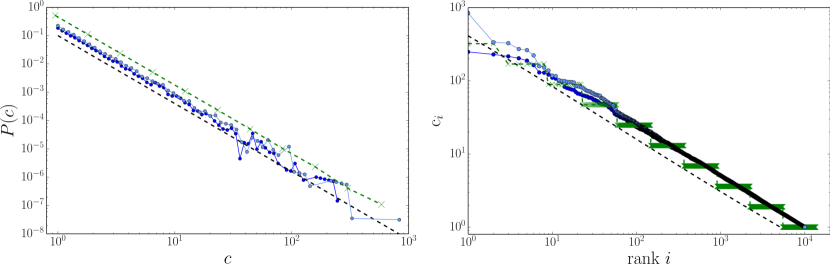

The subject has regained much interest recently, in view of the claim that levels of inequality have reached the same levels as in the beginning of the 20th century [11]. Saez and Zucman [13] corroborate these findings, studying the evolution of the distribution of wealth in the US economy over the last century, and they find an increasing concentration of wealth in the hands of the 0.01% of the richest. Figure 1 shows that the data in Saez and Zucman [13] is consistent with a power law distribution , with a good agreement down to the 10% of the richest (see caption111 Ref. [13] reports the fraction of wealth in the hands of the and richest individuals. If the fraction of individuals with wealth larger than is proportional to , the wealth share in the hands of the richest percent of the population satisfies (for ). Hence is estimated from the slope of the relation between and , shown in the inset of Fig. 1 (left) for a few representative years. The error on is computed as three standard deviations in the least square fit. ). The exponent has been steadily decreasing in the last 30 years, reaching the same levels it attained at the beginning of the 20th century ( in 1917).

Rather than focusing on the determinants of inequality, here we focus on a specific consequence of inequality, i.e. on its impact on liquidity. There are a number of reasons why this is relevant. First of all, the efficiency of a market economy essentially resides on its ability to allow agents to exchange goods. A direct measure of the efficiency is the number of possible exchanges that can be realised or equivalently the probability that a random exchange can take place. This probability quantifies the “fluidity” of exchanges and we shall call it liquidity in what follows. This is the primary measure of efficiency that we shall focus on. Secondly, liquidity, as intended here, has been the primary concern of monetary polices such as Quantitative Easing aimed at contrasting deflation and the slowing down of the economy, in the aftermath of the 2008 financial crisis. A quantitative measure of liquidity is provided by the velocity of money [3], measured as the ratio between the nominal Gross Domestic Product and the money stock222We report data on the MZM (money with zero maturity), the broadest definition of money stock that includes all money market funds. We refer to [5] for further details. and it quantifies how often a unit of currency changes hand within the economy. As Figure 1 shows, the velocity of money has been steadily declining in the last decades. This paper suggests that this decline and the increasing level of inequality are not a coincidence. Rather the former is a consequence of the latter.

Without clear yardsticks marking levels of inequality that seriously hamper the functioning of an economy, the debate on inequality runs the risk of remaining at a qualitative or ideological level. Our main finding is that, in the simplified setting of our model, there is a sharp threshold beyond which inequality becomes intolerable. More precisely, when the power law exponent of the wealth distribution approaches one from above, liquidity vanishes and the economy halts because all available (liquid) financial resources concentrate in the hands of few agents. This provides a precise, quantitative measure of when inequality becomes too much.

Our main goal in the present work is thus to isolate the relation between inequality and liquidity in the simplest possible model that allows us to draw sharp and robust conclusions. Specifically, the model is based on a simplified trading dynamics in which agents with a Pareto distributed wealth randomly trade goods of different prices. Agents receive offers to buy goods and each such transaction is executed if it is compatible with the budget constraint of the buying agent. This reflects a situation where, at those prices, agents are indifferent between all feasible allocations. The model is in the spirit of random exchange models (see e.g. [18, 19]), but our emphasis is not on whether the equilibrium can be reached or not. In fact we show that the dynamics converges to a steady state, which corresponds to a maximally entropic state where all feasible allocations occur with the same probability. Rather we focus on the allocation of cash in the resulting stationary state and on the liquidity of the economy, defined as the fraction of attempted exchanges that are successful. We remark that since the wealth distribution is fixed, the causal link between inequality and liquidity is clear in the simplified setting we consider.

Within our model, the freezing of the economy occurs because when inequality in the wealth distribution increases, financial resources (i.e. cash) concentrate more and more in the hands of few agents (the wealthiest), leaving the vast majority without the financial means to trade. This ultimately suppresses the probability of successful exchanges, i.e. liquidity (see Figure 1, right).

This paper is organised as follows: we start by describing the model and its basic characteristics in Section 2, providing a quick overview of the main results and features of the model in Section 3. In Section 4 we explain in more detail how these features can be understood by an approximated solution of the Master Equation governing the trading dynamics. Details on the analytical derivations and Monte Carlo simulations are thoroughly presented in the appendices. We conclude with some remarks in Section 5.

2 The model

The model consists of agents, each with wealth with . Agents are allowed to trade among themselves objects. Each object has a price . A given allocation of goods among the agents is described by an allocation matrix with entries if agent owns good and zero otherwise. Agents can only own baskets of goods that they can afford, i.e. whose total value does not exceed their wealth. The wealth not invested in goods

| (1) |

corresponds to the cash (liquid capital) that agent has available for trading. The inequality for all indicate that lending is not allowed. Therefore the set of feasible allocations – those for which for all – is only a small fraction of the conceivable allocation matrices .

Starting from a feasible allocation matrix , we introduce a random trading dynamics in which a good is picked uniformly at random among all goods. Its owner then attempts to sell it to another agent drawn uniformly at random among the other agents. If agent has enough cash to buy the product , that is if , the transaction is successful and his/her cash decreases by while the cash of the seller increases by . We do not allow objects to be divided. Notice that the total capital of agents does not change over time, so and the prices are parameters of the model. The entries of the allocation matrix, and consequently the cash, are dynamical variables, which evolve over time according to this dynamics. This model belongs to the class of zero-intelligent agent-based models, in the sense that agents do not try to maximize any utility function.

An interesting property of our dynamics is that the stochastic transition matrix is symmetric between any two feasible configurations and : . We note that any feasible allocation can be reached from any other feasible allocation by a sequence of trades. This implies that the dynamics satisfies the detailed balance condition, with a stationary distribution over the space of feasible configurations that is uniform: . Alternative choices of dynamics which also fulfil these conditions are explored in appendix A.1.

In particular, we focus on realisations where the wealth is drawn from a Pareto distribution , for for each agent . We let vary to explore different levels of inequality, and compare different economies in which the ratio between the total wealth and the total value of all objects is kept fixed. We use so as to have feasible allocations. We consider cases where the objects are divided into a small number of classes with objects per class (); objects belonging to class have the same price . If is the number of object of class that agent owns, then (1) takes the form .

3 Main results

The main result of this model is that the flow of goods among agents becomes more and more congested as inequality increases until it halts completely when the Pareto exponent tends to one from above.

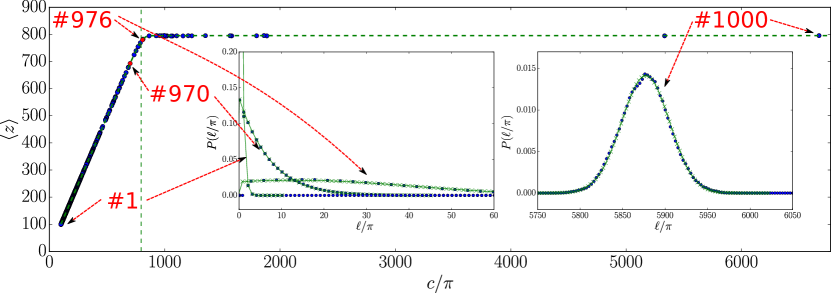

The origin of this behaviour can be understood in the simplest setting where , i.e. all goods have the same price (we are going to omit the subscript in this case). Figure 2 shows the capital composition for all agents in the stationary state, where is the average number of goods owned by agent . The population of agents separates into two distinct classes: a class of cash-poor agents, who own an average number of goods that is very close to the maximum allowed by their wealth, and a cash-rich class, where agents have on average the same number of goods. These two classes are separated by a sharp crossover region. The inset of Figure 2 shows the cash distribution (where represents the number of goods they are able to buy) for some representative agents. While cash-poor agents have a cash distribution peaked at , the wealthiest agents have cash in abundance.

These two observations allow us to trace the origin of the arrest in the economy back to the shrinkage of the cash-rich class to a vanishingly small fraction of the population, as . As we’ll see in the next section, when is smaller than the fraction of agents belonging to this class vanishes as . In this regime, not only the wealthiest few individuals own a finite fraction of the whole economy’s wealth, as observed in Ref. [14], but they also drain all the financial resources in the economy.

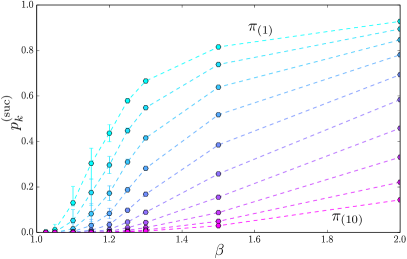

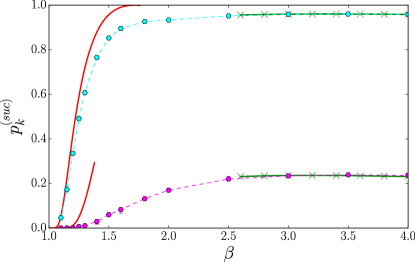

These findings extend to more complex settings. Figure 3 illustrates this for an economy with classes of goods (see figure caption for details) and different values of . In order to visualise the freezing of the flow of goods we introduce the success rate of transactions for goods belonging to class , denoted as . Figure 3 shows that, as expected, for a fixed value of the Pareto exponent the success rate increases as the goods become cheaper, as they are easier to trade. Secondly it shows that trades of all classes of goods halt as tends to unity, that is when wealth inequality becomes too large, independently of their price.

|

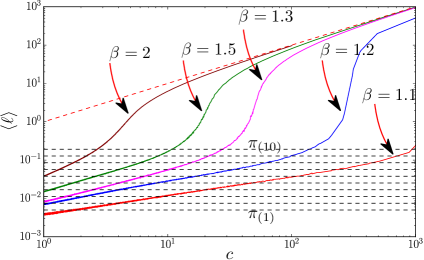

The decrease of when inequality increases (i.e. as decreases) is a consequence of the concentration of cash in the hands of the wealthiest agents. This can be observed in the right panel of Figure 3, which shows the average cash of agents with a given wealth, for different values of . The freezing of the economy when decreases occurs because fewer and fewer agents can dispose of enough cash (i.e. have ) to buy the different goods (prices correspond to the dashed lines).

Note finally that quantifies liquidity in terms of goods. In order to have an equivalent measure in terms of cash that can be compared to the velocity of money, we average over all goods

| (2) |

This quantifies the frequency with which a unit of cash changes hand in our model economy, as a result of a successful transaction. It’s behaviour as a function of for the same parameters of the economy in Figure 3 is shown in the right panel of Figure 1.

4 The analytical approach to the stationary state

In order to shed light on the findings described above, in this section we describe how to derive them within an analytic approach. We start by dealing with the simpler case where all the goods in the system have the same price , (i.e. ).

A formal approach to this problem consists in writing the complete Master Equation that describes the evolution of the probability to find the economy in a state where each agent has a definite number of goods. Taking the sum over all values of for , one can derive the Master Equation for a single agent with wealth . The corresponding marginal distribution in the stationary state can be derived from the detailed balance condition

| (3) |

where is the maximum number of goods which agent can buy with wealth and is the probability that a transaction where agent sells one good (i.e. ) is successful. Eq. (3) says that, in the stationary state, the probability that agent has objects and buys a new object is equal to the probability to find agent with objects, selling successfully one of them. The factor enforces the condition that agent can afford at most goods and it implies that for . Exchanges are successful if the buyer does not already have a saturated budget . So the probability is also given by

| (4) | |||||

| (5) |

where the last relation holds because when the dependence on becomes negligible. This is important, because it implies that for large the variables can be considered as independent, i.e. , and the problem can be reduced to that of computing the marginals self-consistently.

The solution of Eq. (3) can be written as a truncated Poissonian with parameter

| (6) |

with is a normalization factor that can be fixed by . Finally, the value of – or equivalently of – can be found self-consistently, by solving Eq. (5).

Notice that the most likely value of for an agent with is given by

| (7) |

This provides a natural distinction between cash-poor agents – those with – that often cannot afford to buy further objects, and cash-rich ones – those with – who typically have enough cash to buy further objects.

This separation into two classes of agents was already pointed out in Figure 2. In terms of wealth, the poor are defined as those with whereas the rich ones have , where the threshold wealth is given by . Notice that when , a condition that occurs when the economy is nearly frozen (), the distribution is sharply peaked around so that its average is . Then the separation between the two classes becomes rather sharp, as in Figure 2.

In this regime, we can also derive an estimate of in the limit , for . Indeed, we have for , so a rough estimate of is given by . Taking the average over agents, as in Eq. (5), and assuming a distribution density of wealth for and for , one finds (see Appendix A.2.1)

| (8) | ||||

| (9) |

Here is the expected value of the wealth. Notice that diverges as , but also that within this approximation the threshold wealth diverges much faster, with an essential singularity. More precisely, we note that , so that is a number smaller than 1 (yet positive). From Eq. (8), we have . Therefore the liquidity vanishes as .

For finite , this approximation breaks down when gets too close to or smaller than one. Also, is ill-defined and in Eq. (9) it should be replaced with , which strongly fluctuates between realizations and depends on . An estimate of for finite and can be obtained by observing that the wealth marking the separation between the two classes cannot be larger than the wealth of the wealthiest agent. By extreme value theory, the latter is given by , with . Therefore the solution is characterised by . Furthermore, for the average wealth is dominated by the wealthiest few, i.e. and therefore . In other words, in this limit the cash-rich class is composed of a finite number of agents, who hold almost all the cash of the economy. Figure 4 (left) shows that the rough analytical estimate of Eq. (9) is in good agreement with Monte Carlo simulations.

The analysis carries forward to the general case in which classes of goods are considered, starting from the full Master Equation for the joint probability of the ownership vectors for all agents . For the same reasons as before, the problem can be reduced to that of computing the marginal distribution of a single agent. The main complication is that the maximum number of goods of class that agent can get now depends on how many of the other goods agent owns, i.e. , where . The detailed balance condition

| (10) |

again yields the stationary state distribution (for ). On the left we have the probability that one of the objects of type of agent is picked for a successful sale (here is the vector with all zero components and with a component equal to one, and is the probability that a sale of an object of type is successful). This must balance the probability (on the r.h.s.) that agent is selected as the buyer of an object of type , which requires that agent has less than objects of type , for the transaction to occur (here is the probability that an object of type is picked at random, and is the probability that agent is selected as the buyer). It can easily be checked that the solution to this set of equations is given by a product of Poisson laws with parameters , with the constraint Eq. (1),

| (11) |

with a normalization factor obeying . Here the corresponds to the acceptance rates of transactions of goods of class and are given by

| (12) |

As in the case with , the values of the need to be found self-consistently, which can be complicated when and are large.

When the total number of objects per agent is large for any class , we expect that , and then the values of are close to their expected values. This implies that the population of agents splits into classes, where agents with wealth have their budget saturated with goods of class and cannot afford more expensive objects (here , and ). An estimate for the thresholds can be derived following the same arguments as for , by observing that when analysing the dynamics of goods of type , all agents in class are effectively frozen and can be neglected. Combining this with the conservation of the total number of objects of each kind, we obtain a recurrence relation for . We refer the interested reader to the Appendix A.2.2 for details on the derivation, and report here the result in the case of goods with , large enough, with and in the limit :

| (13) | ||||

| (14) |

In the limit of large inequality, close inspection333Note that the term in square brackets is smaller than one, when . of Eq. (13) shows that , which implies that all agents become cash-starved except for the wealthiest few. Since , this implies that all markets freeze: . The arrest of the flow of goods appears to be extremely robust against all choices of the parameter , as is an upper bound for the other success rates of transactions . These conclusions are fully consistent with the results of extensive numerical simulations (see Figure 4 in appendix A.2).

5 Summary and conclusions

In this paper we have introduced a zero-intelligence trading dynamics in which agents have a Pareto distributed wealth and randomly trade goods with different prices. We have shown that this dynamics leads to a uniform distribution in the space of the allocations that are compatible with the budget constraints. We have also shown that when the inequality in the distribution of wealth increases, the economy converges to an equilibrium where typically (i.e. with probability very close to one) the less wealthy agents have less and less cash available, as their budget becomes saturated by objects of the cheapest type. At the same time this class of cash-starved agents takes up a larger and larger fraction of the economy, thereby leading to a complete halt of the economy when the distribution of wealth becomes so broad that its expected average diverges (i.e. when ). In these cases, a finite number of the wealthiest agents own almost all the cash of the economy.

The model presented in this paper is intentionally simple, so as to highlight a simple, robust and quantifiable link between inequality and liquidity. In particular, the model neglects important aspects such as i) agents’ incentives and preferential trading, ii) endogenous price dynamics and iii) credit. It is worth discussing each of these issues in order to address whether the inclusion of some of these factors would revert our finding that inequality and liquidity are negatively related.

First, our model assumes that all exchanges that are compatible with budget constraints will take place, but in more realistic setting only exchanges that increase each party’s utility should take place. Yet if the economy freezes in the case where agents would accept all exchanges that are compatible with their budget, it should also freeze when only a subset of these exchanges are feasible. Also the model assumes that all agents trade with the same frequency whereas one might expect that rich agents trade more frequently than poorer ones. Could liquidity be restored if trading patterns exhibit some level of homophily, with rich people trading more often and preferentially with rich people?

First we note that both these effects are already present in our simple setting. Agents with higher wealth are selected more frequently as sellers as they own a larger share of the objects. In spite of the fact that buyers are chosen at random, successful trades occur more frequently when the buyer is wealthy. So, in the trades actually observed the wealthier do trade more frequently than the less wealthy, and preferentially with other wealthy agents. Furthermore, if agents are allowed to trade only with agents having a similar wealth (e.g. with the agents immediately wealthier or less wealthy) it is easy to show that detailed balance still holds with the same uniform distribution on allocations. As long as all the states are accessible, the stationary probability distribution remains the same444 The dynamics changes and thus changes, in particular for goods more expensive than , the seller is typically cash-rich and thus its neighbours are too. This can induce to have a liquidity of expensive goods higher than that of cheaper ones. However in the limit , it is still true that cash concentrates in the hands of a vanishing fraction of agents, and there is still a freeze of the economy.. Therefore, our conclusions are robust with respect to a wide range of changes in our basic setting that would account for more realistic trading patterns.

Secondly, it is reasonable to expect that prices will adjust – i.e. deflate – as a result of a diminished demand caused by the lack of liquidity. Within our model, the inclusion of price adjustment, occurring on a slower time-scale than trading activity, would reduce the ratio (between total value of goods and total wealth), but it would also change the wealth distribution. Since the freezing phase transition occurs irrespective of the ratio , the first effect, though it might alleviate the problem, would not change our main conclusion. The second would make it more compelling, because cash would not depreciate as prices do, so deflation would leave wealthy agents – who hold most of the cash – even richer compared to the cash deprived agents, that would suffer the most from deflation. So while price adjustment apparently increases liquidity, this may promote further inequality, that would curtail liquidity further.

Finally, can the liquidity freeze be avoided by allowing agents to borrow? Access to credit, we believe, will hardly improve the situation555Allowing agents to borrow using goods as collaterals is equivalent to doubling the wealth of cash-starved agents, provided that any good can be used only once as a collateral, and that goods bought with credit cannot themselves be used as collaterals. This would at most blur the crossover between cash-rich agents and cash-starved ones, as intermediate agents would sometimes use credit. This does not change our main conclusion that inequality and liquidity are inversely related and that the economy would halt when ., in line with the results of Ref. [15] and for similar reasons. Credit may mitigate illiquidity in the short term, but cash deprived agents should borrow from wealthier ones. With positive interest rates, this would make inequality even larger in the long run. So credit is likely to make things worse, in line with the arguments666Piketty [12] observes that when the rate of return on capital exceeds the growth rate of the economy (which is zero in our setting), wealth concentrates more in the hands of the rich. in [12].

Therefore, even though the model presented here can be enriched in many ways, we don’t see a way in which the relation between inequality and liquidity could be reversed.

Corroborating the present model with empirical data goes beyond the scope of the present paper, yet we remark that our findings are consistent with the recent economic trends, as shown in Figure 1. For example, it is worth observing that, alongside with increasing levels of inequality, trade has slowed down after the 2008 crisis777The U.S. Trade Overview, 2013 of the International Trade Administration observes that “Historically, exports have grown as a share of U.S. GDP. However, in 2013 exports contributed to 13.5% of U.S. GDP, a slight drop from 2012’” (see http://trade.gov/mas/ian/tradestatistics/index.asp#P11). A similar slowing down can be observed at the global level, in the UNCTAD Trade and Development Report, 2015, page 7 (see http://unctad.org/en/pages/PublicationWebflyer.aspx?publicationid=1358).. More generally, avoiding deflation -or promoting inflation- has been a major target of monetary policies after 2008, which one could take as an indirect evidence of the slowing down of the economy. Furthermore, the fact that inequality hampers liquidity and hence promotes demand for credit suggests that the boom in credit market before 2008 and the increasing levels of inequality might not have been a coincidence.

An interesting side note is that the concentration of capital in the top agents goes hand in hand with a flow of cash to the top. Indeed, in our model an injection of extra capital in the lower part of the wealth pyramid –the so-called helicopter money policy– is necessarily followed by a flow of this extra cash to the top, via many intermediate agents, thus generating many transactions on the way. This trickle up dynamics should be contrasted with the usual idea of the trickle down policy, which advocates injections of money to the top in order to boost investment. In this respect, it is tempting to relate our findings to the recent debate on Quantitative Easing measures, and in particular to the proposal that the (European) central bank should finance households (or small businesses) rather than financial institutions in order to stimulate the economy and raise inflation [20, 21]. Clearly, our results support the helicopter money policy, because injecting cash at the top does not disengages the economy from a liquidity stall.

Extending our minimal model to take into account the endogenous dynamics of the wealth distribution and of prices, accounting for investment and credit, is an interesting avenue of future research, for which the present work sets the stage. In particular, this could shed light on understanding the conditions under which the positive feedback between returns on investment and inequality, that lies at the very core of the dynamics which has produced ever increasing levels of inequality according to [11, 12, 13], sets in.

6 Acknowledgments

JPJ thanks FAPESP process number 2014/16045-6 for the financial support and the Abdus Salam ICTP for the hospitality. IPC thanks the Abdus Salam ICTP for the hospitality and also thanks Javier Toledo Marín for the work done during some stages of the research presented here. MM thanks Arnab Chatterjee for discussions at an earlier stage of this project and Davide Fiaschi for interesting discussions and comments.

References

- [1] S. Abu Turab Rizvi. The sonnenschein-mantel-debreu results after thirty years. History of Political Economics, 38:228–245, 2006.

- [2] Jean-Philippe Bouchaud. Economics need a scientific revolution. Nature, 455:1181, 2008.

- [3] Irving Fisher. The Purchasing Power of Money: Its Determination and Relation to Credit, Interest, and Crises. Library of Economics and Liberty, 1922

- [4] Alan P Kirman. Complex economics: individual and collective rationality. Routledge, 2010.

- [5] Federal Reserve Bank of St. Louis, Velocity of MZM Money Stock [MZMV], retrieved from https://research.stlouisfed.org/fred2/series/MZMV April 13, 2016.

- [6] Dhananjay K Gode and Shyam Sunder. Allocative efficiency of markets with zero-intelligence traders: Market as a partial substitute for individual rationality. Journal of political economy, pages 119–137, 1993.

- [7] Eric Smith, J Doyne Farmer, László Gillemot, and Supriya Krishnamurthy. Statistical theory of the continuous double auction. Quantitative finance, 3(6):481–514, 2003.

- [8] Simon Kuznets. Economic growth and income inequality. The American Economic Review, 45(1):1–28, 1955.

- [9] Torsten Persson and Guido Tabellini. Is inequality harmful for growth? The American Economic Review, 84(3):600–621, 1994.

- [10] Richard G Wilkinson and Kate Pickett, The Spirit Level: Why More Equal Societies Almost Always Do Better, Allen Lane. 2009.

- [11] Thomas Piketty and Emmanuel Saez. Income inequality in the united states, 1913-1998. Technical report, National bureau of economic research, 2001.

- [12] Thomas Piketty Capital in the Twenty-First Century. Harward Univ. Press, 2014.

- [13] Emmanuel Saez and Gabriel Zucman. Wealth inequality in the united states since 1913: Evidence from capitalized income tax data. Quarterly Journal of Economics, 2016. http://gabriel-zucman.eu/uswealth/

- [14] Jean-Philippe Bouchaud and Marc Mézard. Wealth condensation in a simple model of economy. Physica A: Statistical Mechanics and its Applications, 282(3):536–545, 2000.

- [15] Victor M Yakovenko and J Barkley Rosser Jr. Colloquium: Statistical mechanics of money, wealth, and income. Reviews of Modern Physics, 81(4):1703, 2009.

- [16] Xavier Gabaix. Power laws in economics and finance. Annual Review of Economics, 1:255–293, 2009.

- [17] Aleksandr Saičev, Yannick Malevergne, and Didier Sornette. Zipf’s law and maximum sustainable growth. J. Econ. Dyn. and Control, 37:1195–1212, 2013.

- [18] Duncan K Foley A statistical equilibrium theory of markets. Journal of Economic Theory, 62(2): 321-345, 1994.

- [19] Sjur Didrik Flam and Kjetil Gramstad. Direct exchange in linear economies. International Game Theory Review, 14(04):1240006, 2012.

- [20] John Muellbauer. Quantitative Easing: Evolution of economic thinking as it happened on Vox, chapter Combatting Eurozone deflation: QE for the people. CEPR Press, London, 2003.

- [21] Victoria Chick, Frances Coppola, Nigel Dodd, and et. al. Better ways to boost eurozone economy and employment. Financial Times, March 26, 2015.

- [22] Git Repository: (2015) https://bitbucket.org/flandes/ineqfreezeseconomy_montecarlo_mastereq/.

Appendix A Appendix

A.1 About the Rules Providing Detailed Balance

The detailed balance condition is a useful criterium to find the stationary state in stochastic processes. Given a dynamics formulated in terms of the transition rates between configurations and , If one can find a measure over configurations that satisfies the detailed balance condition

| (15) |

and if the system is ergodic888Meaning that for each pair of configurations and there is a path of a finite number of intermediate configurations with non-zero rate ,, then is the unique stationary distribution. The detailed balance property corresponds to a local balance of the flux between any pair of configurations.

The simplest way to have detailed balance property is to use symmetrical transfer rates: . In that case, one automatically gets a uniform distribution over the space of configurations: . The flux is then also uniform. It is clear that the dynamics defined in this paper has this property, because for any two configurations that differs by the ownership of one object, the rate of the process linking them is equal to in both directions.

What about the rules providing detailed balance, but without symmetry of the rates? In that case, one would need to explicitly find the probability density over the configurations. Since the resulting density would be non-uniform, it would be more difficult to link dynamical observables (rate of money transfer, etc.) to static variables (number of neighbouring configuration to a given configuration). We do not explore these cases.

What are the rules that give symmetrical transfer rates? We define time such that at each time step, a single object is picked and there is a single attempt at selling it to another agent (not the current owner). In this paper, we consider the simplest case where objects are picked independently of their price999One could pick an object with a rate proportional to its value. This kind of choice would still give the same phase space and thus the same probability distribution over microstates, but the dynamics could become very different in terms of the speed of transactions, in particular it could fluctuate much more.. This still leaves us several choices. There are rules which yield symmeteric rates (and thus respect detailed balance). The generic case is the following, with :

-

•

rule : The integer is fixed. Select distinct agents at random. Select one object among the set of all the objects they (collectively) own. This object will be sold (if possible) by the owner to a randomly selected agent among the remaining agents in the set of selected agents.

This generic rule is a bit cryptic, but has two particular cases that are clearer:

-

•

rule : Select two distinct agents at random. Select one object among the set of all the objects they (collectively) own. This object is sold (if possible) by the owner to the other agent.

-

•

rule : Pick an object at random. The owner is then the seller. Select a buyer at random amongst the remaining agents.

Note that the rule does not make sense, so that there are indeed different rules. In this paper, we always use the rule , i.e. simply pick the object at random. As all these rules produce an ergodic dynamics, and since the probability distribution of configurations is the same for all rules (it is ), it does not matter at all which of these dynamical rules we picked.

We do not claim that these rules are the only ones providing symmetric rates, or even that this property is necessary for interesting dynamics. We simply point out that the detail of the choice of the dynamical rule is not crucial, as long as we as we have a simple zero-intelligent dynamics which generates symmetric transition rates. We now give a few examples of rules that are either identical to those above, or do not yield symmetrical probabilities of transfer:

-

•

Select one seller among the N agents by using weighted probabilities: each agent is affected a weight where is the number of objects owned by agent . Pick an object from this agent at random. It will be sold to an agent picked uniformly among the remaining agents. This rule is actually exactly the rule .

-

•

The following rule does not yield symmetrical probabilities of transfer: select a buyer at random. Select any object not already owned by him at random. The owner of that object sells it to the buyer. The problem is that if the buyer has more objects than the seller, the inverse transaction has smaller probability to occur than the direct one.

-

•

The following rule very clearly breaks symmetry: select one seller at random. Select an object in his set at random. Select a buyer among the remaining agents at random. Naively, this rule could be named , but it clearly breaks symmetry. (The transaction from a hoarder to an agent with few objects has much smaller probability to occur than the inverse transaction.)

A.2 Computation of in the large limit

A.2.1 Derivation of and in the large limit for 1 type of good.

As discussed in the main text, we can compute using

| (16) |

approximating the probability to be on a threshold by

| (17) |

The first case can be understood by noting that

| (18) |

where the approximation is valid in the limit . Assuming this approximation to be valid in all the range is clearly a bad assumption for all agents with close to . However the wealth is power law distributed, and so the weight of agents with is negligible in the sum over all agents, Eq. (16). The accuracy of this approximation increases when the exponent of the power law decreases.

Then can be computed using

| (19) |

This is an implicit expression for , since it appears on the l.h.s. of the equation and also on the r.h.s. (because ).

When this expression can be expressed to be realization-independent, using

| (20) |

where is the expected value of the wealth per agent. We also use the fact that we fill in the system a number of goods in such a way to have a fixed ratio . Performing the integral on the r.h.s of Eq. (19) gives an equation for :

| (21) |

that simplifies into:

| (22) |

A.2.2 Derivation of and in the large limit for several types of good.

An analytic derivation for the and can be obtained also for the cases of several goods, but only in the limit in which prices are well separated (i.e. ) and the total values of good of any class is approximately constant (we use ). In this limit we expect to find a sharp separation of the population of agents into classes. This is because implies that the market is flooded with objects of the class , which constantly change hands and essentially follow the laws found in the single type of object case. On top of this dense gas of objects of class , we can consider objects of class as a perturbation (they are picked times less often!). On the time scale of the dynamics of objects of type , the distribution of cash is such that all agents with a wealth less than have their budget saturated by objects of type and typically do not have enough cash to buy objects of type nor more expensive ones. Likewise, there is a class of agents with that will manage to afford goods of types and , but will hardly ever hold goods more expensive that .

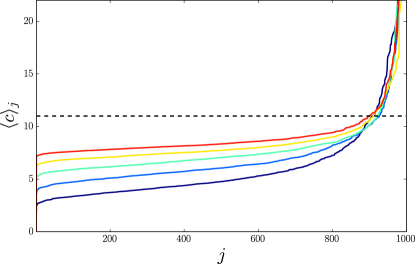

In brief, the economy is segmented into classes, with class composed of all agents with who can afford objects of class up to , but who are excluded from markets for more expensive goods, because they rarely have enough cash to buy goods more expensive than . This structure into classes can be read off from Figure 3, where we present the average cash of agents, given their cash in a specific case (see caption). The horizontal lines denote the prices of the different objects, and the intersections with the horizontal lines define the thresholds . Agents that have just above are cash-filled in terms of object of class , but are cash-starved in terms of objects .

The liquidities can be given by the following expression

| (23) |

According to the previous discussion of segmentation of the system into classes, and using the same approximation for this threshold probability discussed in the case of 1 type of good, we assume

| (24) |

Then

| (25) |

In this case now we have

| (26) |

With similar calculations to the ones showed for the previous case, one can easily get to the recurrence relation:

| (27) |

Iterating, we explicit this into:

| (28) |

A comparison between the analytical estimate and numerical simulations, presented in Figure 4, shows that this approximation provides an accurate description of the collective behaviour of the model.

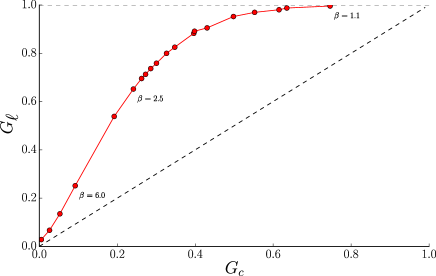

See also in Fig. 5 how the liquidity over-concentrates (with respect to capital concentration). There, we compare the liquid and capital concentrations, measured via their Gini coefficients, for various values of in the system of Fig. 3 ().

In particular, note that the limit is singular, as reaches one around , with smaller yielding also . This is an alternative way to see how the concentration of capital generates an over-concentration of liquidities.

A.3 Details on the numerical methods

A.3.1 Monte-Carlo Simulations

We perform our Monte Carlo simulations of the trading market for agents. Prices generally start from and increase by a factor between each good class. The minimal wealth is . The ratio is fixed as indicated in captions, and most importantly is kept constant between different realizations. As the total wealth fluctuates, so does the total number of goods.

There are no peculiar difficulties with the numerical method (apart from the large fluctuations in the average wealth, addressed below). The only thing one has to be careful with is to ensure that the stationary state has been reached, i.e. that all observables have a stationary value, an indication that the (peculiar) initial condition has been completely forgotten. The codes for this Monte Carlo simulation are available online [22].

Adjusted Pareto Wealth Distribution

For we have predictions for the regime, in which the average wealth is particularly fluctuating from realization to realization. Because the value of controls the number of objects introduced in the market, this in turns produces large fluctuations in the values of the which can make it difficult to have robust results.

More importantly, the typical value of the (empirical) average wealth is usually quite different from its expectation value . This effect is well known and well documented for power laws, but we present a concrete example of it in Figure 6 to emphasize its intensity.

For the sample size that is typically manageable in our simulations, i.e. , the typical value for the average value of the wealth (using e.g. ) is of the order of the half of its expected value: . This indicates that is (by far) an insufficient size to correctly sample a power-law with exponent .

To circumvent this problem, we introduce the “adjusted” Pareto distribution. The idea is to draw numbers from a power law distribution as usual, and then to adjust the value of a few of them so that the empirical average matches the expected one. The algorithm is the following: Start from a true random Pareto distribution.

-

•

if , we select an agent at random and increase its wealth until we have exactly .

-

•

if , we select the wealthiest agent and decrease its wealth until we have exactly , or until its wealth becomes . If we reach the latter case (it is quite unlikely), then we perform the same operation on the second-wealthiest agent, and so on until .

As can be seen in Figure 6, the most common case is the first one. The corresponding adjustment is equivalent to re-drawing the wealth of a single agent until it is such that . This is a weak deviation from a true Pareto distribution. The second case is more rare, and mostly consists also in a correction on the wealth of a single agent.

This change in the wealth distribution is very efficient at reducing the variability between different realizations of the same value. Furthermore it ensures that we can compare our numerical results at finite with the predictions that implicitly assume , since we now have . It is quite crucial to use this “adjusted” Pareto law for the small ’s (i.e. for ). See Figure 7 to have an idea of what this modified distribution means: the only changes in the two sample shown would be in the values of the wealthiest agent.

A.3.2 Algorithm computing self-consistent solution

Here we describe the algorithm used to converge to a self-consistent set of values for , i.e. solving Eq. (12) for (or more simply Eq. (5) in the case of a single type of goods). It can be generalized straightforwardly to , although it may become numerically extremely expensive (see also our code, [22]). The results (green crosses) presented in Figure 4 were obtained using the method described here.

For each agent there is a constant to be determined self-consistently. This presents a technical difficulty, as for a true power-law distribution, each agent gets a different wealth and thus the number of constants to compute is .

Staircase-like distribution of wealth (with exponent )

A way to tackle this difficulty is to consider a staircase-like distribution of wealth, where agents are distributed in groups with homogeneous wealth and where the number of agents per group is , so that individual agents approximately follow a power law with exponent . See Figure 7 (green crosses) to have an idea of what this modified distribution means concretely. This kind of staircase distribution is not a true power-law, in particular because its maximum is always deterministic and finite. However, as we now have , we can numerically solve the equations and thus find the exact value of . Of course, the value of found in this way perfectly matches with Monte Carlo results if and only if we use the exact same distribution of wealth and goods in the simulation. This is not surprising at all, and merely validates our iterative scheme.

However, we note that staircase-like wealth distributions turn out to be very good approximations of true power laws, when the wealth levels are sufficiently refined and the number of classes sufficiently large. In particular, using with a base , it can be seen that for large enough , the average wealth converges to a value very close to the expected one (and no longer depends on ). For large , typically , convergence is reached rather fast ( is enough), and the iterative method can be used (see for instance Figure 8a). Under these conditions, the observables (e.g. ) have the same values for a true power law and the corresponding staircase-distribution (see Figure 8b). However for smaller values of , convergence is very slow and one needs at least to converge (see Figure 8c). The maximum wealth is then very large, which makes the iterative method useless for practical purposes (overflow errors arise, and the number of terms in the sums to be computed explodes exponentially, along with the computational cost).

(b): Dependence on of the computed from the iterative method, using a staircase-like distribution of wealth (green crosses). As soon as , it approaches its “true” value, i.e. the value obtained for a true power-law with exponent (dashed blue line). We used .

(c): Average wealth dependence on for a staircase distribution, using and . Black dots: average computed (exactly) for the staircase distribution. Dashed black: expectation value for the corresponding true power law. It takes very large to converge.

The algorithm

See also our Mathematica code, [22]. The idea is the following. We define “old” and “new” values for each of the variables and for . For , we define only the “current” values, and have “target” values. We start with an initial guess, e.g. that all the and (which is not consistent, of course). Then we use the new values of the to compute the new normalization factors. These are used to compute the “target” , i.e. to know if the should be increased or decreased. New values of are again used to recompute the normalizations, and so forth.

To be more precise, here is the pseudo code we used. We start with some guess values for the , e.g. . Let the variables be set to . The function uses as normalization factor, and the current values of the (since the term is ubiquitous in the expression of ).

-

•

Compute the new using the :

-

•

Compute .

-

•

Set .

-

•

Compute the target values of the :

(29) and symmetrically for .

-

•

For each , compute .

-

•

For each , If , set to .

-

•

For each , set to .

-

•

If the obtained is smaller than , set it to and divide by .

-

•

If the obtained is larger than , set it to .

-

•

Loop until all the are smaller than the predefined allowed error and/or the is close enough to .

This algorithm converges to the true value of the for large enough .

Typically, the that is sufficient to achieve a reasonable approximated convergence can be estimated by taking a quick look at how much the is close to the . Running this algorithm at different values of , one can directly probe the convergence: when increasing does not change the values of the more than the errorbar allowed, then one considers the method to have converged. In practice, it is fairly fast to converge for large ’s, and the number of operations exponentially explodes as is decreased towards .