Ordering-Free Inference from Locally Dependent Data

Kyungchul Song

Vancouver School of Economics, University of British Columbia

Abstract.

This paper focuses on a data-rich environment where the data set has a very large cross-sectional dimension, is likely to exhibit local dependence, and yet is hard to determine the dependence ordering. Such a situation arises, for example, when the data set is collected from the Internet, through a method of web crawling. This paper proposes an approach of randomized subsampling inference, where one constructs a test statistic by aggregating many randomized test statistics using random draws of subsamples, and uses for inference the conditional distribution of the test statistic given data. This paper explores two approaches of such inference: one based on an M-type statistic constructed from randomized mean statistics and the other based on a U-type statistic constructed from randomized U-statistics. This paper provides conditions for local dependence, the number of the random draws, and the subsample size, under which randomized subsampling inference is asymptotically valid. From the Monte Carlo simulation studies, this paper finds that the randomized subsampling inference based on the U-type statistics performs better than that based on the M-type statistics.

Key words. Randomized Subsampling Inference; Local Dependence; Cross-Sectional Dependence; Ordering-Free Inference; Randomized Tests

JEL Classification: C01, C12, C13

At Google, for example, I have found that random samples on the order of 0.1 percent work fine for analysis of business data.

Varian (2014)

1. Introduction

Collecting data from the Internet has recently been among the common practices in empirical research. Typically, such data sets have a huge cross-sectional dimension, and are collected using a sampling scheme that is far from random sampling. The sampling often relies on various methods of web crawling where a computer code automatically searches through numerous websites following a set of protocols. In this set-up, if one simply assumes that the observations are i.i.d., the inference may give nearly zero standard errors, making it irrelevant to perform statistical inference. (See Granger (1988).) On the other hand, incorporating a dependence structure in statistical inference is far from trivial due to the use of a non-random sampling scheme often consisting of complex, and ad hoc protocols.

The issue with unknown dependence ordering is not confined to such online data. For example, if the cross-sectional units are people in a social network, their observed actions are likely to be correlated, but it is hard for the researcher to determine the very network which shapes the cross-sectional dependence ordering of the observations. Another example is a situation where the cross-sectional units are differentiated products and observations are their sales in the market. Due to substitutability among the products, the sales should be correlated, and yet, the precise substitution pattern of the products is notoriously hard to determine from data.

To the best of the author’s knowledge, there does not exist a method of formal statistical inference that is generally available in such a situation. The existing methods of asymptotic inference based on normal approximation do not apply, because it is not possible to make the test statistic asymptotically pivotal without knowing the pattern of local dependence ordering. Inference based on various existing bootstrap methods such as nonparametric bootstrap, residual-based bootstrap or multiplier bootstrap does not apply here.111Nonparametric bootstrap and multiplier bootstrap do not apply due to the local dependence (and potentially distributional heterogeneity) of the cross-sectional observations. Residual bootstrap does not either unless one has a way to recover dependence ordering from data. The method of subsampling does not apply either, because without properly incorporating the dependence pattern in the subsamples, there is no way the distribution of subsamples can imitate the distribution of the whole sample.

In such a situation, this paper proposes using what this paper calls randomized subsampling inference. The main idea is to construct a randomized test statistic by aggregating random subsamples. Randomized subsampling inference is a general idea which is easy to use. It is ordering-free inference in the sense that it enables one to perform statistical inference without committing oneself to a particular model of the way cross-sectional dependence ordering arises among the sample units. For example, suppose that the cross-sectional observations have the same mean and we are interested in testing whether the mean is zero or not. For each randomly drawn subsample, we construct a two-sided t-test statistic. To enhance the power of the test, we build a randomized test statistic by aggregating such t-test statistics. Finally, one constructs many such randomized test statistics and uses their empirical distribution to construct critical values.

The intuition behind this approach is straightforward. As long as the cross-sectional dimension is high and the dependence is local (in the sense that each cross-sectional unit has only a small set of other units that it is strongly correlated with), the observations in each subsample will be likely to be nearly independent, and under proper conditions, this independence will be maintained even after a certain level of aggregation of those subsamples, regardless of what dependence ordering the local dependence of the original observations follows. Hence the distribution of the randomized test statistic may be approximated by a distribution in a way that does not invoke knowledge of the local dependence ordering.

The main goal of this paper is to formally study the method of randomized subsampling inference, focusing on the simple task of testing for the population mean, though the results can be directly extended to more general set-ups. As a first step, this paper formalizes the notion of local dependence in a way that is proper to this type of study. This paper introduces a local dependence measure that is ordering-free in the sense that the set of observations has the same local dependence measure as any permutation of the observations. Roughly speaking, the local dependence measure is based on the likelihood that any randomly chosen small subset of observations turn out to be strongly dependent with one another. When the observations are dependent only locally, this likelihood should be small, yielding a low measure of local dependence. As shown in this paper, a bound for the ordering-free measure of local dependence can be derived from various notions of temporal and spatial weak dependence such as strong mixing time series or random fields, -dependent series, observations with a dependency graph, and observations with a group-dependence structure such that within-group dependence is permitted but between-group dependence is not.

This paper studies two approaches of constructing a test statistic. The first approach uses an M-type statistic which is based on the sample mean of randomized subsamples. The second approach uses a U-type statistic which is based on the U-statistic of randomized subsamples. The main results of this paper are two-fold. First, we establish conditions for local dependence, the number of the randomly drawn subsamples, and the subsample sizes such that the test statistics constructed without knowledge of local dependence ordering are asymptotically pivotal. Second, we introduce the notion of rate-dominance with size control to compare the two approaches. The comparison is not trivial because their size properties are potentially different. This rate-dominance result compares the two approaches in terms of power after the size is controlled up to a higher order term. This paper shows that the U-type statistic approach rate-dominates the M-type statistic approach when permutation-based critical values are used.

This paper studies the performance of the two types of the test statistics through Monte Carlo simulations. The Monte Carlo study considers two types of local dependence; dependency graph and approximate dependency graphs. The study finds the superior performance of randomized subsampling inference based on the U-type statistic approach. In particular, as compared to the normal approximation, it performs more stably across a wide range of local dependence configurations. When the finite sample size is controlled, using the U-type statistic shows higher power than using the M-type statistic.

There are two potential drawbacks of the randomized subsampling inference approach. First, the randomness of the test statistic in the use of inference is primarily from the randomness of the randomized subsamples, which means that given the same sample, the method can yield two different results though with a small probability. To overcome this issue, one may perform randomized inference many times and report the distribution of such results. More specifically, this paper follows Geyer and Meeden (2005) and proposes what it calls a randomized confidence function which traces out the average non-rejection probabilities of many randomized tests across different parameter values. Another potential limitation comes from the fact that the convergence rate of the randomized subsampling inference is slower than the convergence rate of the estimation (e.g. the convergence rate of the sample mean). This paper regards the slower rate as a price to pay for performing inference that is robust to any form of local dependence ordering. When the cross-sectional dimension is high, some loss of power in statistical inference to gain more robustness may not be so detrimental.

Literature Review: The early literature of robust inference under weak dependence and heteroskedasticity has focused on consistent estimation of asymptotic covariance matrix (White (1980), Newey and West (1987) and Andrews (1991)). A more recent strand of literature uses inconsistent scale normalizer that uses a fixed smoothing parameter (Kiefer, Vogelsang, and Bunzel (2000) and Kiefer and Vogelsang (2002)). For example, Phillips, Sun, and Jin (2007) and Sun, Phillips, and Jin (2011) considered power kernels. Jansson (2004) and Sun, Phillips, and Jin (2008) explored higher order accuracy of fixed smoothing asymptotics over increasing smoothing asymptotics. Sun (2014) established related results in a more general context of two-step GMM estimation. In the meanwhile, Müller (2007) showed non-robustness of HAC estimators to local perturbations of the DGP and proposed a class of quadratic long-run variance estimators. Sun and Kim (2015) proposed asymptotic F tests based on fixed smoothing asymptotics in the GMM framework with weakly dependent random fields. Also apart from this econometrics literature, it is worth noting that Shao and Politis (2013) applied the fixed smoothing approach to subsampling inference that uses a calibration method.

Robust estimation of asymptotic covariance matrix has received a great deal of attention in the literature of linear panel models and spatial models as well. Arellano (1987) proposed HAC estimation in linear panel models with fixed effects. Driscoll and Kraay (1998) suggested a simple approach of HAC estimation in linear panel models based on cross-sectional averages of moment functions. Vogelsang (2012) compares the two approaches using fixed smoothing asymptotics. See also Kelejian and Prucha (2007) and Kim and Sun (2011) for HAC estimation in spatial models.

A closely related approach in dealing with cross-sectional dependence is linear or nonlinear modeling of spatial autoregressive models and the approach of clustered errors. (See Lee (2004), and Lee, Liu, and Lin (2010) for contributions to the literature of spatial autoregressive models, among many others, and references therein.) As for models with clustered errors, Cameron, Gelbach, and Miller (2008) proposed and studied bootstrap approaches to deal with clustered errors. This literature typically assumes many independent clusters in a linear set-up. Ibragimov and Müller (2010) proposed a novel approach based on t-statistics where the observations are divided into multiple clusters that are (approximately) independent from each other and the inference is based on within-cluster estimators that are asymptotically normal. Bester, Conley, and Hansen (2011) elaborated this multiple-cluster approach in linear panel models and provided conditions that are more primitive than those of Ibragimov and Müller (2010). The t-statistic approach of Ibragimov and Müller (2010) allows for the clusters to be few and to be heterogeneous on various dimensions such as size or within-cluster dependence strength. However, the approach requires knowledge of this group structure of (at least approximately) independent clusters.

A strand of literature has focused on developing tests for cross-sectional dependence using mainly cross-sectional variations. Pesaran (2004) developed a general test for cross-sectional dependence in linear panel models with a short time series dimension. See also Hsiao, Pesaran, and Pick (2012) for an extension to limited dependent models. Robinson (2008) proposed a correlation test that can be applied for testing cross-sectional dependence in a spatial model. Kuersteiner and Prucha (2013) considered a linear panel model with a large cross-sectional dimension which does not require a long time series. Adopting a sequential exogeneity condition, and assuming conditional moment type restrictions, they obtained a limit theory for GMM estimators that accommodate unknown common shocks and various latent cross-sectional dependence structures. (See also Kuersteiner and Prucha (2015) for a more general framework which includes linear quadratic moment restrictions in dynamic panel models which accommodate social interactions and networks models.)

The use of permutations and subsamples in this paper is different from permutation tests and subsampling-based inference in the literature. Most importantly, the main use of permutations or subsamples in this paper is for constructing test statistics rather than for finding critical values. It is more like a Monte Carlo test than a standard permutation test. Also, randomized subsampling inference is fundamentally different from the subsampling inference of Politis and Romano (1994). Here, subsamples are used primarily to construct a test statistic rather than critical values.

Using randomly drawn subsamples for data analysis is a common practice in empirical research when the data set size is huge. (See Varian (2014).) A closely related approach is bootstrap aggregating (or bagging) proposed by Breiman (1996) which is used to obtain stable predictions using many bootstrap samples. Recently Kleiner, Talwalker, Sarkar, and Jordan (2014) proposed using random subsamples to measure the quality of the estimates adn showed the measure is consistent as the subsample size increases to infinity. The main motivation for their proposal is to reduce the computational costs when the sample size is large. Unlike their approach, the focus here is on inference with observations that are locally dependent but the dependence ordering is not known to the researcher. It does not seem to have received attention in the literature that using randomly drawn subsamples one may obtain inference that is robust to a wide range of configurations of local dependence ordering.

Organization of the Paper: Section 2 introduces the main idea of randomized subsampling inference, ordering-free local dependence measure, and illustrates its meaning through examples. The section also establishes conditions for asymptotic validity, and provide results that compare the M-type statistic and the U-type statistic approaches through the notion of rate-dominance with size control. In Section 3, this paper presents and discusses results from a Monte Carlo simulation study. Technical proofs of part of the main results are found in the appendix. Supplemental Note to this paper contains extension to inference from moment-based restrictions and proofs of the other results in the paper.

2. Randomized Subsampling Inference on the Mean

2.1. The Basic Set-Up

Consider the simple set-up of estimating the population mean from locally dependent data. Suppose that we are given observed random vectors and a (potentially latent) common shock such that

for all . Thus we assume that is conditionally mean independent of the common shock . Let us assume that ’s have the same mean:

The main goal here is to develop a procedure to yield an asymptotically valid confidence set for as the sample size goes to infinity. For this, consider the following testing problem of null and alternative hypotheses.

for a given vector .

Without knowing the local dependence ordering, it is not possible to use the usual t-statistic. The t-statistic (in the case of ) takes the following form:

where and is a consistent estimator of such that

The difficulty here is that without knowing which observations are strongly correlated with for each , it is hard to find a consistent estimator of . In fact, we can write

where

Under local dependence, one can consistently estimate the leading term in the definition of without knowledge of dependence ordering. The problem is the second term for which, to the best of the author’s knowledge, there is no existing method to consistently estimate it without knowing which set of ’s are nearly uncorrelated with for each . Thus performing statistical inference without knowing local dependence ordering is fundamentally a nontrivial task, even for this simple testing problem for a population mean.

2.2. Two Approaches of Randomized Subsampling Inference

2.2.1. The M-Type Statistic Approach

Let be the set of permutations on and be i.i.d. draws from the uniform distribution on . Given each , , and , we define

where

| (2.1) |

and . We call a randomized subsample and the number the subsample size. A randomized subsample is obtained by first permuting the sample using a permutation randomly drawn from and by taking the first observations from the permuted sample. The normalization by the covariance matrix controls only for the “short-run” covariance among the entries of the random vector , not the cross-sectional dependence. Then we define

where and for a vector . We introduce the test statistic as follows:

The additive term is a bias adjustment term which we will explain later.

Let us consider the following method of constructing a critical value. For given , we draw , , i.i.d., where and ’s are i.i.d. draws from the uniform distribution on . Define for ,

In other words, the critical values are read from the percentile of the empirical distribution of . Note that we use the sample mean in place of to ensure that the test may have power when .

2.2.2. The U-Type Statistic Approach

As before, let be the space of permutations on and be i.i.d. draws from the uniform distribution on . Given and , we define

where is as defined in (2.1), and let

We introduce the test statistic as follows:

Again, the term is a bias adjustment term.

For given , we draw , , i.i.d., similarly as before, where and ’s are i.i.d. draws from the uniform distribution on . Define for ,

2.3. Ordering-Free Local Dependence Measure

We first formulate the notion of “locality” in local dependence without invoking dependence ordering. The main idea in this paper is to measure the locality by quantifying the likelihood that a random selection of a small subset of gives a set that is partitioned into two nearly independent subsets. If the likelihood is large, the underlying dependence is deemed local. This notion of locality does not invoke any underlying dependence ordering.

To formalize this intuition, suppose that for any subset , measures the strength of the joint conditional dependence of given a common shock . We will introduce one definition of later. Then, the ordering-free local dependence measure of the triangular array is defined as follows: for each ,

| (2.2) |

The local dependence of a large set of observations is measured by the convergence rate of (with each fixed ) to zero as the sample size goes to infinity. We call the -coefficient of (with respect to a given common shock ). The -coefficient is ordering-free. Indeed, two triangular arrays and have the same -coefficient if for all , for some .

Let us introduce . First, let for each

i.e., the collection of the sets of two nonempty subsets of which constitute a partition of . Let be the union of ’s over , where is a given class of real measurable functions on . (For this paper’s proposal, it suffices to take the class of functions as a finite set of eighth-order polynomials. See a remark prior to Assumption 2.1 below.) For each , we take

where

and represents the conditional (Pearson) correlation coefficient between and given if and zero otherwise. (The minimum over an empty set in the above expression is taken to be one.) For example, when there exists such that is conditionally independent of given , we have . Hence when ’s are conditionally independent, , for any .

The notion of -coefficient here is inspired by -weak dependence notion proposed by Doukhan and Louhichi (1999) for time series. The major distinction is that the dependence measure is made invariant to the permutations of the observations, making unnecessary any reference to the underlying dependence ordering.

Example 1: Triangular Arrays with a Dependency Graph Let a graph over be given, where denotes the collection of pairs , with representing an edge (or a link) between vertices (or nodes) and . We exclude loops, i.e., for all , . Let us assume that the graph is undirected so that whenever , . Let be a given triangular array of random variables. Let us say that is a conditional dependency graph for given a -field , if for any two subsets and of such that , and are conditionally independent given . (See e.g. Penrose (2003), p.22.)

The case of a triangular array with a dependency graph having a bounded maximum degree includes -dependent time series as a special case.222A degree of a node , denoted by , is the size of its neighborhood, i.e., . The maximum degree is , i.e., the maximum of over . Also dependence with clusters, where there is a partition of the observations into clusters and dependence is restricted to within-cluster observations, not between clusters, is a special case of local dependence with a dependency graph.

A simple combinatoric argument gives a bound for the -coefficient of the triangular array . (The proof is found in Supplemental Note.)

Lemma 2.1.

Suppose that is a triangular array of random variables having as a conditional dependency graph given .

Then for each integer , there exist and depending only on such that for all ,

where denotes the maximum degree of .

Suppose that is bounded. Then at any fixed , the -coefficient converges to zero as at the rate of . The bound in Lemma 2.1 is conveniently simple, as it depends on the graph through only its maximum degree. It is possible to obtain a more sophicated bound that involves other features of the network.

Example 2: Weakly Dependent Random Fields Suppose that a random field is given, where is a subset of such that and is a lattice as a subset of . For each pair , we define distance , where and are the -th entry of and respectively. We assume that the lattice is infinite countable having such that for all , we have . Hence as in Conley (1999) and Jenish and Prucha (2009a), we exclude the infill asymptotics where the sampling points become dense in a given domain as the sample size increases.

To map the random field to a triangular array, let be a one-to-one map, so that we let , , and define for simplicity. Also, for given subsets of , let

For simplicity, let us assume that there is no common shock. Define for ,

Hence measures stochastic dependence among ’s with , when there exists a partition of such that . The following lemma characterizes a bound for the -coefficient of in terms of . (The proof is found in Supplemental Note.)

Lemma 2.2.

Suppose that is a random field and let , Suppose further that for some , and for each integer , there exists such that

| (2.3) |

Then, for each integer , there exist and such that

where and are constants depending only on and .

When the random field is a strong-mixing random field, the condition (2.3) can be verified in terms of the strong-mixing coefficient. To see this, define

| (2.4) |

where denotes the strong mixing coefficient between the two -fields generated by and , i.e.,

with the supremum being that over all the Borel sets and . Let for

| (2.5) |

Suppose that for some and , for all . Then by covariance inequality (e.g. Corollary A.2 of Hall and Heyde (1980), p.278), for any disjoint subsets and of such that , we have for some constant ,

The condition (2.3) is reduced to the requirement of the existence of a constant such that for all ,

where

2.4. Asymptotic Theory

2.4.1. Asymptotic Validity

We take the class of functions to be the union of over , where is the collection of real maps on of the form: , where with , , , and . Define

We introduce two pairs of conditions in the assumption below, one for the M-type statistic approach and the other for the U-type statistic approach.

Assumption 2.1.

For a sequence and a constant which do not depend on the joint distribution of , it is satisfied that for all ,

M-(i) , and

M-(ii) , for each .

Assumption 2.2.

For a sequence and a constant which do not depend on the joint distribution of , it is satisfied that for all ,

U-(i) , and

U-(ii) , for each .

Assumptions 2.1 and 2.2 specify the requirement on the local dependence of the triangular array . For example in the case of a dependency graph with a bounded maximum degree, Assumption 2.1 requires that

For Assumption 2.1, it suffices to take and such that as . On the other hand, Assumption 2.2 requires that

It suffices to take and such that as . Assumptions 2.1 and 2.2 do not require that . In fact can be chosen to be a fixed constant as .

Assumption 2.3.

There exist constants which do not depend on the joint distribution of and satisfy the following conditions for all .

(i) .

(ii) The minimum eigenvalue of is greater than , where

In Assumption 2.3, we require bounded moments and nondegenerate variances. The following theorem is the main result of this paper. Let

i.e., the -field generated by and .

Theorem 2.1.

Furthermore, for each , we have as ,

Furthermore, for each , we have as ,

Both tests are asymptotically pivotal under the stated conditions, despite that they were constructed without knowledge about the underlying dependence ordering.

2.4.2. Heuristics and Discussions

Let us give heuristics on the asymptotic validity of the randomized subsampling approach. We show how the statistics and which are used to generate critical values is linked to the test statistics and . In doing so, we will see how the bias adjustment term arises. For simplicity, we assume that there is no common shock and we know .

First, let us consider the M-type statistic approach. Let and write

where and

| (2.7) |

As for the last term in the definition of , note that

where One can show that the conditional expectation of given is . Thus,

We conclude that

where

| (2.8) |

Since , by Assumption 2.1 M-(i), it follows that

| (2.9) |

Since is a sum of i.i.d. random variables conditional on (due to the i.i.d. property of random permutations), we can apply the central limit theorem to establish the asymptotic distribution of .

Using as a test statistic is not feasible, because the last term in (2.8) is not consistently estimable without knowledge of the dependence ordering. Thus we take the case of ’s being independent as a benchmark in which case , and replace by zero. We obtain the following form of a test statistic:

| (2.10) |

Under Assumption 2.1, the bias adjustment term is asymptotically negligible, as . However, including it stablizes the finite sample size properties of the test. The relation (2.9) shows why using the conditional distribution of given data is an alternative way of obtaining the critical values, i.e., permutation-based ones .

Now let us turn to the U-type statistic approach. Similarly as before, we write

where

| (2.11) |

As for the last term in the definition of , note that

where

One can show that the conditional expectation of given is . Thus,

Therefore, if we define

| (2.12) |

we can write

By Assumptions 2.2, it follows that

| (2.13) |

Again, since is a sum of i.i.d. random variables conditional on , we can apply the central limit theorem to establish its asymptotic normality of .

Similarly as before, we replace by zero and use the following as our test statistic:

| (2.14) |

Under Assumption 2.2, the bias adjustment term is asymptotically negligible, as .

2.4.3. Local Power Analysis

One might wonder whether the use of randomized subsampling inference leads to a test that achieves the convergence rate, i.e., the same convergence rate that can be achieved with knowledge of local dependence ordering. Here we show that the answer is negative. Consider the following Pitman local alternatives:

where is a constant vector,

We maintain the assumption that .

Theorem 2.2.

Suppose that Assumption 2.3 holds and for some positive definite matrix .

(i) Suppose further that Assumption 2.1 holds. Then under ,

where is the conditional CDF of , given , and .

(ii) Suppose further that Assumption 2.2 holds. Then under ,

The local power function for the U-type statistic depends on the quadratic form of the drift term , showing that the test is for two-sided testing. The rate of convergence of the test is which is slower than by Assumption 2.2(i). A similar remark applies to the M-type statistic approach.

2.4.4. Rate-Dominance with Size Control

In this section, we compare the M-type test and the U-type test. Since the tests have different finite sample size distortions depending on the choice of and , we cannot directly compare them solely based on the rate of convergence of Pitman drifts for which the tests have nontrivial power. For proper comparison, we introduce the notion of rate-dominance with size control.

Let be the collection of the joint distributions of the random vector . Let be the parameter of interest, which is a map from to . We are interested in testing

Corresponding to the hypothesis testing problem, we partition , where

For each sequence , we define

Thus a sequence of probabilities constitutes Pitman local alternatives at the rate . Let us introduce the following definitions.

Definition 2.1.

A sequence of tests is said to be asymptotically exact at the rate , if

as , and the sequence is not .

Definition 2.2.

The rate of a sequence of tests is defined to be a nonstochastic sequence such that for any sequence such that as ,

and for any sequence such that as ,

It is not hard to see that the rate of tests is unique in the equivalence class of sequences where two sequences and are defined to be equivalent if and . Similarly the rate at which the tests are asymptotically exact is unique in the equivalence class of sequences.

Finally, we introduce the notion of rate-dominance of one sequence of test statistics over another.

Definition 2.3.

Given two sequences of tests and , we say that rate-dominates with size control at , if and are asymptotically exact at the rate , and

where and are the rates of and .

When rate-dominates with size control at , it means that using the test , one can detect a deviation from the null hypothesis more sensitively than the test , given that both tests control the size asymptotically up to . Since the rate at which the tests are asymptotically exact is unique in the equivalence class of sequences, the rate dominance relation among the sequences of tests is transitive.

We introduce a theorem which shows U-type statistic-based tests rate-dominates M-type statistic-based tests when permutation-based critical values are used. Suppose that is a continuous random vector, and let

| (2.15) | |||

| (2.16) |

where . Define

We make the following assumptions.

Assumption 2.4.

The joint distributions of and are absolutely continuous with respect to Lebesgue measure.

Assumption 2.5.

There exist , , , and such that for all and all , the following conditions hold.

(i) The minimum eigenvalues of and are larger than .

(ii) .

(iii) for all .

(iv) and .

Our rate-dominance result uses a modulus of continuity for the empirical measures of the sets in (2.15) up to a higher order. One can use an Edgeworth expansion for the empirical measure, but the classical Edgeworth expansion is not applicable here, because the classical Cramér condition for the empirical measure does not apply. To overcome this, we use Angst and Poly (2017) and Song (2018). Assumptions 2.4 and 2.5 are used primarily for this. The following theorem gives a result of rate-dominance with size control between the M-type statistic and the U-type statistic approaches. (The proof is found in Supplemental Note.)

Theorem 2.3.

Let be in the definition of the test , and be in the definition of the test . Suppose that Assumption 2.1 is satisfied with and Assumption 2.2 with , and that Assumptions 2.3 - 2.5 hold.

Then, for each , rate-dominates with size control at , if we choose such that

Let us give a heuristic for Theorem 2.3. Using the Edgeworth expansion of the conditional distribution of given , we find that

(In fact, the last rate comes from , and is sharp under the regularity conditions, and the error in the Edgeworth expansion is dominated by this rate.) Similarly, we also obtain that

We normalize the rate by choosing and such that

for some sequence . From the local power result in Theorem 2.2 and using Assumption 2.5(iv), we find that

as , where , by Assumption 2.2. Thus rate-dominates with size control.

2.5. Non-randomized Inference

The tests based on and are randomized tests, where there is randomness of the test statistic apart from that of the samples. Hence different researchers may have different results using the same data and the same model though with a small probability. To address this issue, this paper proposes the following approach of constructing confidence intervals. For a given large positive integer , for each , we let , where ’s are i.i.d. draws from the uniform distribution on . Then we define for

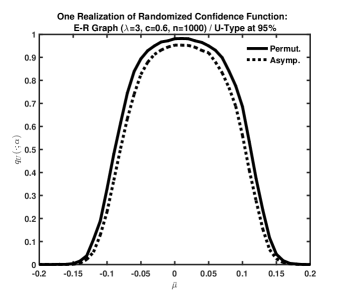

We call the randomized confidence function.

Corollary 2.1.

Suppose that Assumption 2.3 holds. Then for each , the following statements hold as jointly.

(i) Under Assumption 2.1, if , and otherwise.

(ii) Under Assumption 2.2, if , and otherwise.

The convergence of or to 0 at reflects the consistency property of the randomized test. The result of Corollary 2.1 can be shown by slightly modifying the proof of Theorem 2.1.

The randomized confidence function is not a familiar concept in econometrics.333The notion of the randomized confidence function in this paper coincides with what Geyer and Meeden (2005) referred to as the membership function of fuzzy confidence intervals. The way randomized tests arise in this paper is different. They do here because the asymptotic pivotalness of the test (thus permitting ordering-free inference) prevents us from drawing an arbitrarily large number of random permutations. Instead, one may use a nonrandomized confidence set of the following form. Take and define for

| (2.17) |

Then it is not hard to see from Corollary 2.1 that

as . For example, we may take , which is used in simulation studies in this paper. (In simulation studies unreported in this paper, the choice of was also used, and the results were not very different.)

3. Simulation Studies

3.1. Data Generating Process

This section presents and discusses a Monte Carlo simulation study which investigates the finite sample properties of the randomized subsampling approach in various situations with local dependence. As for local dependence, this study considered three kinds of data generating processes: (i) i.i.d. variables, (ii) variables having a dependency graph, (iii) network dependent variables. Both asymptotic and permutation critical values are considered.

As for the dependency graph case, we use two kinds of graphs. One is based on Erdös-Rényi graphs, and the other is based on Barabási-Albert graphs of preferential attachment. In an Erdös-Rényi random graph, each pair of the vertices form an edge with equal probability . The simulation study here chose from . Thus each vertex from this random graph has degree on average, and the degree distribution is approximately a Poisson distribution with parameter when the graph is large. For a Barabási-Albert random graph of preferential attachment, we first began with an Erdös-Rényi random graph of size with . Then we let the graph grow by adding each vertex sequentially and let the vertex form edges with other existing vertices. (We chose from for this study.) The probability of a new vertex forming an edge with an existing vertex is proportional to the number of the neighbors of the existing vertex. We keep adding new vertices until the size of the graph becomes .

As for the generation of the random variables, we follow the design in Song (2015). We first generate i.i.d. from . Let be the set of edges in the graph with redundant edges removed from (i.e., remove with ) and let be two-column matrix whose entries are of the form for . Let be sorted on the first column so that .

Step 1: For , such that , we draw and set

where is a parameter that determines the strength of graph dependence. We replace by , and redefine the series .

Step : For such that , we draw and set

We replace by , and redefine the series .

Turning now to the third data generation design involving network dependent observations, they are drawn from a jointly normal random vector with mean zero and a covariance matrix such that the correlation between two random variables at the distance is set to be , where is a parameter that determines the strength of the correlation. The parameter was taken from . (Note that is roughly 0.3674 and is roughly 0.1353.) For the graph underlying the network-dependent observations, the simulation study considered a realization of a Erdös-Reényi random graph with .

The size of the networks was taken from . As for and , we chose and for the M-type statistic and and for the U-type statistic. The Monte Carlo simulation number and the permutation number (i.e., ) were set to be 1000, and the tuning parameter 0.005.

U-Type Statistics

| Asymp. | Permut. | |||||

|---|---|---|---|---|---|---|

| 0.968 | 0.919 | 0.875 | 0.990 | 0.946 | 0.895 | |

| 0.967 | 0.914 | 0.868 | 0.991 | 0.947 | 0.896 | |

| 0.963 | 0.909 | 0.861 | 0.991 | 0.945 | 0.894 |

M-Type Statistics

| Asymp. | Permut. | |||||

|---|---|---|---|---|---|---|

| 0.980 | 0.928 | 0.874 | 0.986 | 0.931 | 0.876 | |

| 0.981 | 0.929 | 0.876 | 0.987 | 0.933 | 0.878 | |

| 0.980 | 0.928 | 0.875 | 0.987 | 0.933 | 0.878 |

U-Type Statistics

| E-R | B-A | |||||||

|---|---|---|---|---|---|---|---|---|

| 0.919 | 0.916 | 0.915 | 0.914 | 0.913 | 0.914 | |||

| 0.911 | 0.916 | 0.914 | 0.912 | 0.917 | 0.914 | |||

| 0.908 | 0.911 | 0.909 | 0.907 | 0.909 | 0.912 | |||

| Asymp. | ||||||||

| 0.917 | 0.919 | 0.919 | 0.916 | 0.917 | 0.916 | |||

| 0.916 | 0.912 | 0.910 | 0.917 | 0.915 | 0.914 | |||

| 0.910 | 0.913 | 0.912 | 0.908 | 0.913 | 0.911 | |||

| 0.946 | 0.944 | 0.942 | 0.942 | 0.941 | 0.942 | |||

| 0.945 | 0.948 | 0.947 | 0.945 | 0.949 | 0.947 | |||

| 0.945 | 0.947 | 0.946 | 0.945 | 0.945 | 0.948 | |||

| Permut. | ||||||||

| 0.944 | 0.946 | 0.946 | 0.944 | 0.944 | 0.943 | |||

| 0.948 | 0.945 | 0.943 | 0.949 | 0.947 | 0.946 | |||

| 0.946 | 0.949 | 0.949 | 0.945 | 0.949 | 0.947 |

M-Type Statistics

| E-R | B-A | |||||||

|---|---|---|---|---|---|---|---|---|

| 0.928 | 0.926 | 0.925 | 0.923 | 0.923 | 0.924 | |||

| 0.926 | 0.930 | 0.929 | 0.926 | 0.930 | 0.929 | |||

| 0.927 | 0.929 | 0.927 | 0.926 | 0.928 | 0.930 | |||

| Asymp. | ||||||||

| 0.927 | 0.928 | 0.927 | 0.925 | 0.926 | 0.925 | |||

| 0.929 | 0.927 | 0.926 | 0.931 | 0.930 | 0.928 | |||

| 0.928 | 0.931 | 0.931 | 0.927 | 0.931 | 0.929 | |||

| 0.932 | 0.929 | 0.929 | 0.927 | 0.927 | 0.927 | |||

| 0.930 | 0.934 | 0.932 | 0.930 | 0.934 | 0.932 | |||

| 0.931 | 0.933 | 0.931 | 0.931 | 0.932 | 0.935 | |||

| Permut. | ||||||||

| 0.930 | 0.931 | 0.930 | 0.928 | 0.929 | 0.928 | |||

| 0.933 | 0.931 | 0.930 | 0.934 | 0.933 | 0.932 | |||

| 0.932 | 0.935 | 0.935 | 0.932 | 0.935 | 0.933 |

Notes: The E-R represents Erdös-Rényi Random Graph with probability equal to , and chosen from , and the B-A represents Barabási-Albert random graph of preferential attachment, with refering to the number of links each new node forms with other existing nodes. A larger parameter represents a stronger correlation between two linked observations.

U-Type Statistics

| Asymp. | Permut. | ||||||

|---|---|---|---|---|---|---|---|

| 0.912 | 0.904 | 0.889 | 0.940 | 0.934 | 0.921 | ||

| 0.908 | 0.901 | 0.883 | 0.942 | 0.935 | 0.921 | ||

| 0.902 | 0.897 | 0.884 | 0.941 | 0.936 | 0.926 | ||

| 0.900 | 0.881 | 0.817 | 0.930 | 0.914 | 0.854 | ||

| 0.904 | 0.877 | 0.811 | 0.939 | 0.914 | 0.857 | ||

| 0.893 | 0.873 | 0.805 | 0.934 | 0.918 | 0.857 |

M-Type Statistics

| Asymp. | Permut. | ||||||

|---|---|---|---|---|---|---|---|

| 0.922 | 0.917 | 0.907 | 0.926 | 0.920 | 0.911 | ||

| 0.924 | 0.919 | 0.908 | 0.929 | 0.923 | 0.913 | ||

| 0.923 | 0.920 | 0.911 | 0.928 | 0.925 | 0.915 | ||

| 0.915 | 0.902 | 0.860 | 0.918 | 0.906 | 0.865 | ||

| 0.921 | 0.904 | 0.862 | 0.925 | 0.909 | 0.867 | ||

| 0.917 | 0.904 | 0.862 | 0.921 | 0.909 | 0.869 |

Notes: The Erdös-Rényi Random Graph

with probability equal to was used.

The correlation between linked observations is set to be where represents the length of the shortest path between the two indices of the observations on the graph.

Independent Observations

| U-Type | M-Type | ||||||

|---|---|---|---|---|---|---|---|

| 0.829 | 0.526 | 0.174 | 0.864 | 0.680 | 0.425 | ||

| Asymp. | 0.745 | 0.244 | 0.015 | 0.815 | 0.506 | 0.190 | |

| 0.554 | 0.032 | 0.000 | 0.716 | 0.257 | 0.030 | ||

| 0.870 | 0.585 | 0.212 | 0.868 | 0.688 | 0.434 | ||

| Permut. | 0.797 | 0.301 | 0.022 | 0.822 | 0.518 | 0.199 | |

| 0.634 | 0.046 | 0.000 | 0.726 | 0.267 | 0.032 |

Dependency Graphs

| U-Type | M-Type | ||||||

|---|---|---|---|---|---|---|---|

| 0.833 | 0.542 | 0.190 | 0.867 | 0.689 | 0.437 | ||

| Asymp. | 0.744 | 0.248 | 0.014 | 0.819 | 0.513 | 0.194 | |

| 0.558 | 0.032 | 0.000 | 0.719 | 0.260 | 0.030 | ||

| 0.874 | 0.602 | 0.229 | 0.872 | 0.697 | 0.446 | ||

| Permut. | 0.805 | 0.305 | 0.021 | 0.827 | 0.524 | 0.202 | |

| 0.637 | 0.046 | 0.000 | 0.728 | 0.269 | 0.033 |

Notes: We chose for the Erdös-Rényi (ER) Random Graph with .

3.2. Results

3.2.1. Finite Sample Size Properties

First, let us report results on finite sample size properties. The results are shown in Tables 1 - 3. Table 1 presents the results from i.i.d. observations as a benchmark case. Table 2 uses simulated observations with dependency graphs where graphs are chosen to be from a single realization from two random graphs: Erdös-Reényi random graph and Barabási-Albert random graph. Finally, Table 3 shows the results from using network dependent observations.

First, for the U-type statistic approach, the permutation critical values perform conspicuously better than asymptotic critical values. Asymptotic critical values do not perform very well even in the case of independent observations. (See Table 1.) However, the contrast is much less stark for the M-type statistic approach.

Second, the U-type statistic approach exhibits more stable size properties than the M-type statistic approach. Interestingly, the performance does not seem to worsen much as the graph gets denser and the correlation stronger. This is perhaps because as one observation has more neighbors, the correlation between the observation and each neighbor tends to be weaker by the design of the data generating process.

Third, the randomized subsampling approach tends to over-reject the null hypothesis in the case of network dependence case (Table 3), where the overjection becomes severe as the correlation between linked observations gets stronger.

Throughout the simulation study, the increase in the sample size does not necessarily show better size properties. This may be because the graph tends to have more nodes with more neighbors as the sample size becomes larger, and this may offset the improvement in size properties partially.

3.2.2. Power Properties

Let us turn to the power properties of the randomized tests. The results are shown in Table 4. The false coverage probabilities using asymptotic critical values are lower than those using permutation critical values. This is not surprising given that the asymptotic critical values exhibit lower coverage probabilities at the true value of than permutation critical values.

Interestingly, the case of independent observations show only very slightly lower false coverage probabilities than the case of dependency graphs show similar results. This demonstrates the robustness properties of the randomized subsampling approach. However, in the case of network dependent observations, the false coverage probabilities are higher. The performance of randomized subsampling approach in the simulation designs and the choice of , , and does not seem stable for network dependent observations.

Finally, the M-type statistic approach exhibits larger false coverage probability than the U-type statistic approach, despite its worse size distortion. This may reflect the inferior performance of the M-type statistic approach as theoretically shown in terms of rate-dominance with size control.

4. Conclusion

This paper proposes a randomized subsampling approach to perform inference with locally dependent data when the dependence ordering is not known. This paper first introduces the notion of local dependence that does not invoke any reference to the underlying dependence ordering, and pursues ordering-free inference based on M-type statistic and U-type statistic approaches. The main results include establishing conditions for the local dependence which ensure the asymptotic validity of the approaches, and introducing the notion of rate dominance with size control to formally compare the two approaches, and show that U-type statistic approach rate-dominates the M-type statistic approach when permutation-based critical values are used. In general, there is a tradeoff between size and power in the randomized subsampling approach. Of course, when we have a huge number of observations, choosing and much smaller than can improve the small sample size property without hurting much its power. Some theoretical results suggesting a good combination of and in general would be desirable.

5. Appendix: Mathematical Proofs

Recall the definition of . We begin by providing a moment bound. The proof uses the recursive approach of a Doukhan-Portal type inequality (due to Doukhan and Portal (1983)) which is derived for our set-up. (See e.g. Lemma 3 of Andrews and Pollard (1994) and Lemma 14 of Doukhan and Louhichi (1999).)

Lemma 5.1.

Suppose that for some positive integer , and any positive sequence , there exist such that , for all and for each .

Then there exists a constant that depends only on , and such that

for all .

The poof of Lemma 5.1 is found in Supplemental Note. Let us define

| (5.1) | |||||

| (5.2) |

and let for each ,

We focus on the asymptotic properties of . For this, write (with )

| (5.3) |

where

The following lemma gives the convergence rates of for each .

Lemma 5.2.

Suppose that Assumption 2.3 holds. Then

Proof: For notational brevity, denote

| (5.4) |

Since we draw ’s i.i.d. from the uniform distribution on , we can rewrite

Hence for some constant ,

Let us now turn to the second statement. We write

Note that

where

| (5.5) |

and the sum over includes 4-tuples of positive integers from to such that , , and . The leading term in the decomposition above is by the moment conditions in Assumption 2.3.

Let us analyze which we write

where

where the sum over is over all 3-tuples of distinct integers in and the sum over is over all 4-tuples of distinct integers in . The factor 4 in front of appears because for each 4-tuple, say , there are four ways to form a pair with one from and the other from .

We write

By Assumption 2.3(i), the last term is bounded by , for some constant that does not depend on .

We turn to the leading term on the right hand side of (5). Note that

The trace in the leading sum in (5) is bounded by . As we can also write (using the fact that )

the trace in the leading sum of (5) is bounded by

for some constant , where is due to . Similarly, the same trace is also bounded by . Therefore, the leading sum on the right hand side of (5) is bounded by , so that

Let us turn to . By the definition of , we have

for some . We conclude that

completing the proof.

Proof: (i) Write

As for the leading term,

The right hand side of the above equality is equal to . In the same way,

| (5.8) |

Therefore, , and

(ii) Let us consider

because, as we saw in the proof of Lemma 5.2,

Now we write

| (5.9) |

where

Rewrite the leading term on the right hand side of (5.9) as

The last term is bouned by .

We turn to . Write

where the sum over is over all the 4-tuples of positive integers from such that 4-tuples of positive integers from to such that , , and . Again, we write

where

and

As in the proof of Lemma 5.2, the sum over is over all 3-tuples of distinct integers in and the sum over is over all 4-tuples of distinct integers in . By Assumption 2.3, and by counting the number of all 3-tuples of distinct integers in , we have

As for , we write

We conclude that

Recall the definitions of and in (5.1).

Lemma 5.4.

Suppose that the conditions of Lemma 5.1 hold. Then for any ,

As for the second statement, similarly as before, we bound for some ,

Note that

We bound the last term by

By Lemma 5.1, we have for some , . As for , we use Jensen’s inequality and bound

for some , completing the proof.

Lemma 5.5.

Suppose that Assumption 2.3 holds, and that as . Then

| (5.10) |

Proof: Let and write

The desired result follows because .

Lemma 5.6.

Suppose that Assumption 2.3 holds. Then

Proof: We write

We write the last term as , where

As for the first term, we write

The last term is and by (5.8),

| (5.11) |

As for the leading term,

The leading term is bounded by . Hence

Let us turn to which we write as

where

using the same argument as in (5.11).

The second term in (5) is bounded by . As for the leading term in (5), we can follow the same arguments in the proof of Lemma 5.2 and show that it is equal to . Therefore, .

Proof of Theorem 2.1: (i) Let us consider the first statement. Recall the definition of prior to Lemma 5.2. By Lemma 5.3, we find that

Combining this with (5.10) and using (5.3) and Lemma 5.2, we obtain that

We focus on . Since is a triangular array that is rowwise i.i.d. conditional on , we deduce that by Berry-Esseen lemma (e.g. Theorem 3 of Chow and Teicher (1988), p.304), for some ,

where . By Lemma 5.4, the expected value of the last bound has a rate . In view of Lemma 5.5, this completes the proof of the first statement.

Let us turn to the second statement. From (2.4.2), we write

where is due to the estimation error in , and is as defined in (2.7). By Lemma 5.6 and in view of the heuristics in Section 2.4.2, we find that

Therefore,

where is the same as except that is replaced by .

Hence the conditional distribution of given is the same as that of up to a term. From the proof of the first statement, we find that the conditional CDF of given converges (uniformly over the evaluation points) in probability to , which completes the proof.

(ii) The proof is almost the same as that of (i).

Proof of Theorem 2.2: (i) Write , where

Note that

The last term is by Assumption 2.1 M-(i). Thus we obtain the desired result from the proof of Theorem 2.1 and the continuous mapping theorem.

(ii) We write , where

We write , where

We rewrite

By Lemma 5.5, and as we are under the local alternatives, the leading term is equal to and the last term is

by Assumption 2.2 U-(i). As for , we write it as

by (5.10). Hence we conclude that

Using the same arguments in the proof of Theorem 2.1, we obtain the desired result.

References

- (1)

- Andrews (1991) Andrews, D. W. K. (1991): “Heteroskedasticity and autocorrelation consistent matrix estimation,” Econometrica, 59, 817–858.

- Andrews and Pollard (1994) Andrews, D. W. K., and D. Pollard (1994): “An introduction to functional central limit theorems for dependent stochastic processes,” International Statistical Review, 62, 119–132.

- Angst and Poly (2017) Angst, J., and G. Poly (2017): “A Weak Cramér Condition and Application to Edgeworth Expansions,” Electronic Journal of Probability, pp. 1–24.

- Arellano (1987) Arellano, M. (1987): “Computing standard errors for within-group estimators,” Oxford Bulletin of Economics and Statistics, 49, 431–434.

- Bester, Conley, and Hansen (2011) Bester, C. A., T. G. Conley, and C. G. Hansen (2011): “Inference with dependent data using cluster covariance estimator,” Journal of Econometrics, 165, 137–151.

- Breiman (1996) Breiman, L. (1996): “Bagging Predictors,” Machine Learning, 24, 123–140.

- Cameron, Gelbach, and Miller (2008) Cameron, A. C., J. B. Gelbach, and D. L. Miller (2008): “Bootstrap-based improvements for inference with clustered errors,” Review of Economics and Statistics, 90, 414–427.

- Chow and Teicher (1988) Chow, Y. S., and H. Teicher (1988): Probability Theory: Independence, Interchangeability, Martingales. Springer-Verlag, New York, USA.

- Conley (1999) Conley, T. G. (1999): “GMM estimation with cross sectional dependence,” Journal of Econometrics, 92, 1–45.

- Doukhan and Louhichi (1999) Doukhan, P., and S. Louhichi (1999): “A new weak dependence condition and applications to moment inequalities,” Stochastic Processes and Their Applications, 84, 313–342.

- Doukhan and Portal (1983) Doukhan, P., and F. Portal (1983): “Moments de Variables Aléatoires Mélangeantes,” C.R. Acad. Sc. Paris., 297, 129–132.

- Driscoll and Kraay (1998) Driscoll, J. C., and A. C. Kraay (1998): “Consistent covariance martrix estimation with spatially dependent panel data,” Review of Economics and Statistics, 80, 549–560.

- Geyer and Meeden (2005) Geyer, C. J., and G. D. Meeden (2005): “Fuzzy and randomized confidence intervals and P-values,” Statistical Science, 20, 358–366.

- Granger (1988) Granger, C. W. J. (1988): “Extracting Information from Mega-Panels and High-Frequency Data,” Statistica Neerlandica, 52, 258–272.

- Hall and Heyde (1980) Hall, P., and C. C. Heyde (1980): Martingale Limit Theory and Its Application. Academic Press, New York, USA.

- Hsiao, Pesaran, and Pick (2012) Hsiao, C., M. H. Pesaran, and A. Pick (2012): “Diagnostic Tests of Cross-Section Independence for Limited Dependent Variable Panel Models,” Oxford Bulletin of Economics and Statistics, 74, 253–277.

- Ibragimov and Müller (2010) Ibragimov, R., and U. K. Müller (2010): “t-statistic based correlation and heterogeneity robust inference,” Journal of Business and Economic Statistics, 28, 453–468.

- Jansson (2004) Jansson, M. (2004): “The error in rejection probability of simple autocorrelation robust tests,” Econometrica, 72, 937–946.

- Jenish and Prucha (2009a) Jenish, N., and I. R. Prucha (2009a): “Central limit theorems and uniform laws of large numbers for arrays of random fields,” Journal of Econometrics, 150, 86–98.

- Jenish and Prucha (2009b) (2009b): “Central limit theorems and uniform laws of large numbers for arrays of random fields,” Working Paper.

- Kelejian and Prucha (2007) Kelejian, H. H., and I. R. Prucha (2007): “HAC esitmation in a spatial framework,” Journal of Econometrics, 140, 131–154.

- Kiefer and Vogelsang (2002) Kiefer, N. M., and T. J. Vogelsang (2002): “Heteroskedasticity-autocorrelation robust standard errors using the Bartlett kernel without truncation,” Econometrica, 70, 2093–2095.

- Kiefer, Vogelsang, and Bunzel (2000) Kiefer, N. M., T. J. Vogelsang, and H. Bunzel (2000): “Simple robust testing of regression hypotheses,” Econometrica, 55, 703–708.

- Kim and Sun (2011) Kim, M. S., and Y. Sun (2011): “Spatial heteroskedasticity and autocorrelation consistent estimation of covariance matrix,” Journal of Econometrics, 160, 349–371.

- Kleiner, Talwalker, Sarkar, and Jordan (2014) Kleiner, A., A. Talwalker, P. Sarkar, and M. I. Jordan (2014): “A scalable bootstrap for massive data,” Journal of the Royal Statistical Society, B., 76, 795–816.

- Kuersteiner and Prucha (2013) Kuersteiner, G. M., and I. R. Prucha (2013): “Limit theory for panel data models with cross sectional dependence and sequential exogeneity,” Journal of Econometrics, 174, 107–126.

- Kuersteiner and Prucha (2015) (2015): “Dynamic spatial panel models: networks, common shocks, and sequential exogeneity,” Working Paper.

- Lee (2004) Lee, L.-F. (2004): “Asymptotic Distributions of Quasi-Maximum Likelihood Estimators for Spatial Autoregressive Models,” Econometrica, 72, 1899–1925.

- Lee, Liu, and Lin (2010) Lee, L.-F., X. Liu, and X. Lin (2010): “Specification and Estimation of Social Interaction Models with Network Structures,” Econometrics Journal, 13, 145–176.

- Müller (2007) Müller, U. K. (2007): “A theory of robust long-run variance estimation,” Journal of Econometrics, 141, 1331–1352.

- Newey and West (1987) Newey, W., and K. West (1987): “A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix,” Econometrica, 55, 703–708.

- Penrose (2003) Penrose, M. (2003): Random Geometric Graphs. Oxford University Press, Oxford, UK.

- Pesaran (2004) Pesaran, M. H. (2004): “General Diagnostic Tests for Cross Section Dependence in Panels,” CESifo Working Papers, No. 1229.

- Phillips, Sun, and Jin (2007) Phillips, P., Y. Sun, and S. Jin (2007): “Long run variance estimation and robust regression testing using sharp origin kernels with no truncation,” Journal of Statistical Planning and Inference, 137, 985–1023.

- Politis and Romano (1994) Politis, D. N., and J. P. Romano (1994): “Large Sample Confidence Regions Based on Subsamples Under Minimal Assumptions,” Annals of Statistics, 22, 2031–2050.

- Robinson (2008) Robinson, P. M. (2008): “Correlation Testing in Time Series, Spatial and Cross-Sectional Data,” Journal of Econometrics, 147, 5–16.

- Shao and Politis (2013) Shao, X., and D. N. Politis (2013): “Fixed b subsampling and the block bootstrap: improved confidence sets based on b-value calibration,” Journal of the Royal Statistical Society, B, 75, 161–184.

- Song (2015) Song, K. (2015): “Measuring the graph concordance of locally dependent observations,” arXiv:1504.03712v2 [stat.ME].

- Song (2018) (2018): “A Uniform-in- Edgeworth Expansion with a Weak Cramér Condition,” Working Paper.

- Sun (2014) Sun, Y. (2014): “Fixed-smoothing asymptotics in a two-step generalized method of moments framework,” Econometrica, 82, 2327–2370.

- Sun and Kim (2015) Sun, Y., and M. S. Kim (2015): “Asymptotic F-test in a GMM framework with cross-sectional dependence,” Review of Economics and Statistics, 97, 210–223.

- Sun, Phillips, and Jin (2008) Sun, Y., P. C. B. Phillips, and S. Jin (2008): “Optimal bandwidth selection in heroskedasticity-autocorrelation robust testing,” Econometrica, 76, 175–194.

- Sun, Phillips, and Jin (2011) (2011): “Power maximization and size control in heteroskedasticity and autocorrelation robust tests with exponentiated kernels,” Econometric Theory, 27, 1320–1368.

- Varian (2014) Varian, H. R. (2014): “Big data: new tricks for econometrics,” Journal of Economic Perspectives, 28, 3–28.

- Vogelsang (2012) Vogelsang, T. J. (2012): “Heteroskedasticity, autocorrelation, and spatial correlation robust inference in linear panel models with fixed-effects,” Journal of Econometrics, 166, 303–316.

- White (1980) White, H. (1980): “A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity,” Econometrica, 48, 817–838.

Supplemental Note for “Ordering-Free Inference from Locally Dependent Data”

Kyungchul Song

Vancouver School of Economics, University of British Columbia

Supplemental Note consists of four parts. The first part (Appendix A) explains extension of randomized subsampling inference to models with moment restrictions. The second part (Appendix B) is devoted to the proof of Lemmas 2.1 and 2.2. The third part (Appendix C) proves the moment inequality result in Lemma 5.1. The fourth part (Appendix D) provides the proof of Theorem 2.3.

Appendix A Inference from Moment Restrictions

Suppose that we have a locally dependent triangular array of random vectors , with , and that there is a true parameter such that

for all , where is a given moment function. Here we do not assume that the moment restriction point-identifies .

The development of randomized subsampling inference is built on the previous results on the testing on the population mean. For brevity, we focus only on the approach based on a U-type statistic.

The randomized subsampling approach developed for inference on the population mean applies in this set-up straightforwardly, by inverting the U-type statistic. First, define

where and . Let be given as before. Define

where refers to the number of the moment restrictions. Then, we define

The normalization by eliminates asymptotically the dependence among the moment restrictions in the limiting distribution. Again the construction of the test statistic and the critical values do not require knowledge of the dependence ordering of the triangular array

As for the permutation critical values, we draw , , i.i.d., similarly as before, and define

Then we construct

Let us turn to the randomized confidence function. For a given integer , for each , we let as before. Define

We make the following assumption which is used to ensure that we can consistently estimate for each and each .

Assumption A.1.

For each , is identical a.s. across .

Let us study the asymptotic validity of the test. Define for each ,

When ’s are i.i.d. (conditional on ), the set is an identified set for with respect to the conditional distribution of given . The set is the collection of ’s that are away from the identified set.

We make the following assumptions regarding the cross-sectional local dependence of ’s across .

Assumption A.2.

(i) Assumption 2.2 holds when we replace by for each such that .

(ii) Assumption 2.3 holds when we replace by for each .

We are prepared to present the asymptotic result for the randomized confidence function for . The proof of this result can be obtained again by slightly modifying the proof of Theorem 2.1.

Using this, we can construct confidence sets as in (A.2). More specfically, take and define

| (A.2) |

This is the confidence set for .

When the dimension of is high, computing the function can be cumbersome for permutation critical values , because one needs to compute the critical value for each . Then we may consider the following profiling method. Suppose that we are interested in which is a subvector of . Let be such that . Define

where is defined as

The use of this profiling method in general gives conservative inference.

Appendix B Proof of Lemmas 2.1 and 2.2

Proof of Lemma 2.1: Whenever does not constitute a connected component in the graph , we have . Hence for any permutation such that , we have where is chosen from , and is from the neighborhood of , and from the neighborhood of , and so on. After placing this way, we place in the remaining places. In fact, any permutation such that can be obtained in this way, except with a different ordering of in this process.

Thus, we have

where is a constant depending only on . Thus,

which gives the desired result.

Proof of Lemma 2.2 is a bit more involved. Let us introduce notation and an auxiliary lemma. For each nonnegative integer and , let us define

and let for ,

| (B.1) |

Also we set . The sets , constitute a partition of . Fix any integer and define

where when , and let

Lemma B.1.

For each , and , there exist and an integer such that and for each integer , and for each integer , .

Proof: For each , there exists a partition of such that

but there exists no partition of such that . First note that by the definition of , for each , there exist such that . Certainly, we cannot have for infinite ’s, because . Let be the smallest integer such that for all , . Let be the largest integer such that for all , . Then it must be that . For the lemma, it suffices to show that .

To the contrary, assume that . We show that it contradicts that . First, by the definition of and , we have and , and there must exist such that and . We take a partition of such that

(by the choice of ) and

Since , both and are not empty. Furthermore, by the definition of , for all such that for some and for some , we have . Hence . This contradicts that .

Proof of Lemma 2.2: Fix . For each , let us first compute a bound for . Let and be such that . Let be the smallest integer such that for all , . Then by Lemma B.1, for each integer , . We find a bound for by counting the number of ’s which satisfy this latter condition. By our setting of , we have

We consider two cases.

First, suppose that

| (B.2) |

By the way is defined in (B.1), each set , , excludes and . Hence we must have , and there exist such that , and

A bound for the number of such permutations is computed as follows. First we place in one of places, and then place so that . The total number of fixing and this way is bounded by for some constant . (See Lemma A.1 of Jenish and Prucha (2009b).) Now, we choose from and the number of choosing this way is bounded by , and choose from and the number of choosing this way is bounded by . We keep choosing ,…, this way. Then we choose the remaining . Hence the total number of the permutations which satisfy (B.2) is bounded by

| (B.3) | |||

for some that does not depend on .

Second, suppose that

| (B.4) |

Then it is not hard to show that the number of ’s with this property is bounded by the bound in (B.3), because we can choose a bound for the number of choosing both and , say, from the same in a way that the bound is smaller than the previous bound that comes from choosing from and from . Thus the total number of the permutations which satisfy (B.4) has the same bound in (B.3).

Appendix C Proof of Lemma 5.1

First, we introduce a basic inequality that involves permutations. For each and , we write .

Lemma C.1.

For some positive integers , , let and be given nonnegative maps. Then for any disjoint nonempty subsets such that and ,

| (C.1) | |||

Proof: Let be the set of -tuples such that are from and all are distinct. We write the left hand side of (C.1) by (letting )

Since and are nonnegative, we bound the last term by

Note that

where the last bound is obtained by replacing by . Exchanging the roles of and , and noting that , we obtain the upper bound.

Let us introduce some notation. Let be a given triangular array of random variables. For any and , we let

The following lemma is obtained by using a Doukhan-Portal type inequality (Doukhan and Portal (1983)).

Lemma C.2.

Let be a triangular array of random variables having as its -coefficient for some -field , and define for integers ,

Then for any integers , there exists constant such that depends only on and , and for any with ,

| (C.2) |

where , and the product is taken to be 1 if is empty.

Proof: Suppose that . Then the inequality of the lemma trivially holds. Suppose that . For any vector of distinct integers, we let

For each , we let be the collection of ’s such that

i.e., the collection of ’s such that is a minimizer of over all . Using the fact , we bound

where , , and

We prove the inequality (C.2) by induction. Define

| (C.4) |

As we saw before, the inequality (C.2) holds for . Suppose that it holds for . Take arbitrary such that . By (C),

By the hypothesis of induction, we have

| (C.5) |

for some constant that depends only on . For each and , let denote the -th entry of . As for the last bound in (C.5), note that

for some constant that depends only on . Thus the proof is complete.

Proof of Lemma 5.1: For brevity, we assume that . The proof for the general case of is similar. Define for positive integers and ,

| (C.6) |

Let us write

For each having consisting of uniquely distinct integers in , with each appearing in times, we let be with such ’s. Using Lemma C.2 and recalling the definition (C.4) (with replacing there), we bound the term on the right hand side of (C) by

| (C.8) |

for some constant that depends only on and . Note that

where denotes the -th entry of . The restriction in the sum over follows because for each with , we have . This because for such , there exists such that , i.e., there exists an integer, say, , in which appears only once in the vector , and for such , because for all . Hence

where is a constant that depends only on and . The first inequality uses the fact that .

Appendix D Proof of Theorem 2.3

Lemma D.1.

Suppose that and are positive definite matrices such that , for some , where denotes the Frobenius norm, i.e, . Then,

Proof: Since , we obtain that

because .

Lemma D.2.

Suppose that there exist constants , , and and integers and such that and for all , and all .

Then for any and such that

for all , there exists a constant such that

Proof: Note that

By Markov’s inequality, the last probability is bounded by

by Lemma 5.1 (taking and there), where depends only on and .

Lemma D.3.

Suppose that there exist constants and such that

and for all .

Then there exists such that for all and all ,

Lemma D.4.

Under the conditions of Theorem 2.3, the statements below hold.

(i) There exist and such that for all ,

| (D.1) |

(ii) There exist and such that for all ,

Proof: (i) We bound the probability on the right hand side of (D.1) by

where

We bound by

where is a constant that depends only on and . This probability is bounded by by Lemma D.2 (with ), if we choose large enough so that

Now, let us turn to . We bound for any constant such that ,

for some constant by Lemma D.2 again, where . By choosing small enough and using Lemmas D.1 amd D.3, we can bound the last probability by for some constant .

(ii) First, we observe that

We bound

where

We can show that both and are bounded by using the same arguments as in the proof of (i).

Let us define

Lemma D.5.

Proof: Note that for any ,

for some constant by taking sufficiently small , by Lemma D.4(i). We can deal with the second statement similarly.

Lemma D.6.

Suppose that the conditions of Theorem 2.3 hold. Then,

as , where and are random function such that for each , and are -measurable, and there exist and such that for each and ,

Proof: There exists such that the complement of the event that

and

has probability vanishing to zero at the rate of uniformly over , by Lemmas D.4 and D.5. The result then follows from Theorem 3.2 and Corollary 3.1 of Song (2018). (We take , there.)

Lemma D.7.

Suppose that the conditions of Theorem 2.3 hold. Then

as . Furthermore, the terms and on the right hand side of the equations are not and .

Proof: As for the first result, we write as

by Lemma D.6. Note that

As for , we note that

Using the same arguments in the proof of Lemma 5.2, we find that there exists a constant such that for all ,

and . By the assumptions of the lemma,

Since ,

As for the second result, similarly as before, we write as

by Lemma D.6. We write

where

Using similar arguments as before, we find that

and obtain the first result of the lemma. Given the arguments in the proof of Theorem 2.1, it is not hard to show that the terms and in the lemma are not and . Details are omitted.