A probabilistic max-plus numerical method for

solving stochastic control problems

Marianne Akian1 and Eric Fodjo21Marianne Akian is with

INRIA and CMAP, École polytechnique CNRS. Address:

CMAP, École Polytechnique,

Route de Saclay,

91128 Palaiseau Cedex, France.

marianne.akian@inria.fr2Eric Fodjo is with

I-Fihn Consulting and

INRIA and CMAP, École polytechnique CNRS. Address:

CMAP, École Polytechnique,

Route de Saclay,

91128 Palaiseau Cedex, France.

eric.fodjo@polytechnique.edu

Abstract

We consider fully nonlinear Hamilton-Jacobi-Bellman equations

associated to diffusion control problems involving

a finite set-valued (or switching) control and possibly

a continuum-valued control.

We construct a lower complexity probabilistic numerical algorithm

by combining the idempotent expansion properties obtained by

McEneaney, Kaise and Han (2011) for solving such problems

with a numerical probabilistic method such as the one

proposed by Fahim, Touzi and Warin (2011)

for solving some fully nonlinear parabolic partial differential

equations.

Numerical tests on a small example of pricing and hedging an option

are presented.

I Introduction

We consider a finite horizon diffusion control problem on involving

at the same time a “discrete” control taking its values in a finite set ,

and a “continuum” control taking its values in some subset

of a finite dimensional space (for instance a

convex set with nonempty interior), which we next describe.

Let be the horizon.

The state at time

satisfies the stochastic differential equation

(1)

where is a -dimensional

Brownian motion on a filtered probability space

.

The control processes and

take their values in the

sets and respectively and they are admissible if

they are progressively measurable with respect to

the filtration .

We assume that, for all ,

the maps and

are continuous

and satisfy properties implying the existence of the process

for any admissible control processes and .

Given an initial time , the control problem consists in maximizing

the following payoff:

where, for all , ,

(the set of positive reals),

and are given continuous maps.

We then define the value function of the problem as the optimal payoff:

where the maximization holds over all admissible control processes

and .

Let denotes the set of symmetric matrices.

The Hamiltonian

of the above control problem is defined as:

with

Under suitable assumptions, the value function

is the unique

(continuous) viscosity solution of

the following Hamilton-Jacobi-Bellman equation

(2)

satisfying also some growth condition at infinity (in space).

In [1], Fahim, Touzi and Warin proposed a probabilistic numerical

method to solve such fully nonlinear partial

differential equations (2), inspired by their backward stochastic

differential equation interpretation

given by Cheridito, Soner, Touzi and Victoir

in [2].

However this method only works when

the diffusion matrices are

at the same time bounded from below (with respect to the Loewner order)

by a symmetrix positive definite matrix and

bounded from above by .

Such a constraint can be restrictive, in particular it may not hold

even when the matrices do not depend on and but take

different values for . Also some regularity conditions

may be needed for , which are not fulfilled

when is a finite set.

McEneaney, Kaise and Han

proposed in [3, 4]

an idempotent numerical method which works at least when

the hamiltonian corresponds to linear quadratic control problems.

This method is based on the distributivity of the (usual) addition operation

over the supremum (or infimum) operation, and on a property

of invariance of the set of quadratic forms.

It computes in a backward manner the value function

at time as a supremum of quadratic forms.

However, as decreases, the number of quadratic forms generated

by the method increases exponentially (and even become infinite

if the Brownian is not discretized in space) and some pruning

is necessary to reduce the complexity of the algorithm.

Here, we combine the two above methods to construct a

new algorithm.

The method is using in particular the simulation of a small number of

uncontrolled stochastic processes as in [1].

We show that

even without pruning, the complexity of the algorithm

is bounded polynomially in the number of discretization time steps

and in the size of the sample of the uncontrolled stochastic processes.

Numerical tests of our algorithm

on an example of pricing and hedging an option in dimension 2

considered in [5] are presented.

II The algorithm of Fahim, Touzi and Warin

Let be a time discretization step such that is an integer.

We denote by the set of discretization times

of .

For each , we shall assume that we can apply

the algorithm of [1] to the equation:

(3)

For this purpose, we decompose as the sum of the (linear) generator

of a diffusion (with no control) and of

a nonlinear elliptic Hamiltonian , that is

with

and such that

is positive semidefinite, for all .

We also assume that

.

The time discretization of (3) proposed in [1]

can be written in the following form:

where, under some conditions, is a monotone operator

over the set of Lipschitz continuous functions from to :

(4)

Moreover, the operator is constructed by using a

probabilistic scheme.

Denote by

the Euler discretization of the diffusion with generator :

(5)

Then,

(6)

with, for ,

being the approximation of the th derivative of

obtained as follows:

where, for all , is

a polynomial of degree

with values in an appropriate finite dimensional space,

and in particular .

Although the operator

does not depend on , since both the law of

and the Hamiltonian do not depend on ,

we keep the index since it will become

important when applying a regression approximation (see below).

In [1], the convergence of such a time discretization is

proved under the above assumptions and some other technical assumptions.

Note that these conditions include the boundedness of the coefficients

of the Hamiltonians and , and the boundedness of

the value function of the corresponding control problem.

However, a change of variable on the value and on the state

allows one to obtain the same type of result for

unbounded coefficients and value function satisfying some suitable

growth conditions at infinity.

Such a change of variables may induce a deformation on the

discretizations (5) and (6) and so on the algorithm, but we shall

not discuss this here.

A greater difficulty is that the above assumptions do not allow

in general to handle directly

the case where is replaced by .

However, in the case of as above one can simply consider the

following scheme:

(7)

The difference with the usual scheme of [1] is that

one needs to construct several operators and so several

processes , one for each .

The solution of this time discretization will converge to the

value function of our problem, that is the solution

of the Hamilton-Jacobi-Bellman equation with hamiltonian ,

as soon as the convergence

is proved for the time discretization of the equations

with hamiltonians .

Although the above scheme can be compared to a standard numerical

approximation if one develops the expression

of each , with ,

one may compute given by (7) as in [1],

that is using a regression estimator.

One just simulates the process and

do at each time a regression estimation to find the value

of at the points by using

the values of and .

Although this variation of the method of [1], based

on (7),

is appealing and may work in practice,

several difficulties remain.

First, theoretically, the sample size to obtain

the convergence of the estimator is at least

in the order of [6].

Hence, it is exponential in the dimension of the system

showing the persistence of the curse of dimensionality,

although in some practical examples, a much smaller sample size

may be sufficient.

Next, one possible regression estimation is to

approximate the conditional expectation of a random map

by projecting it orthogonally into a finite dimensional

linear space of functions. Then, to obtain a good estimation,

the dimension of this space need to be exponential in the dimension .

In the sequel, we shall rather use a

small dimensional regression space and use a distributivity property as in

the work of McEneaney, Kaise and Han [3, 4]

to find a good approximation of living in the max-plus linear space

of finite suprema of quadratic forms.

III The algorithm of McEneaney, Kaise and Han

In [3, 4], the following time

discretization is used.

Denote by

the Euler discretization of the process defined in the introduction,

when the controls and are fixed:

Then, a time discretization of the solution of (2)

is given by:

(8)

where

(9)

Under appropriate assumptions,

this scheme converges to the solution of (2)

(see [4] for ).

Note that the processes of the

previous section are not related to the processes

and so the above discretization is different from the one

of the previous section.

Assume that the final reward of the control problem

can be written as the supremum of a finite number

of concave quadratic forms.

Denote , where

is the set of negative definite symmetric

matrices, and let

(10)

be the quadratic form with parameter applied to the vector .

Then for , we have

where is a finite subset of .

Then, in [4], the following property is deduced from

a max-plus distributivity property, in the more general

case where the Brownian motion does not have the same

dimension as the state space.

Assume that , that does not depend on and ,

that is affine with respect to , that

is concave quadratic with respect to , and that is

the supremum of a finite number of concave quadratic forms.

Consider the time discretization of (8) with (9).

Then, for all , there exists a set

and a map such that

for all , is a concave quadratic form and

Moreover, the sets satisfy

where is the space of values of the Brownian process.

Note that the sets are infinite as soon as .

However, if the Brownian process is discretized in space,

the set can be replaced by a finite subset,

and the sets become finite.

Nevertheless, their cardinality increases exponentially as decreases:

where is the cardinality of

the discretization of . Then,

McEneaney, Kaise and Han proposed in [4] a pruning method

to reduce at each time step the cardinality of .

IV Combining max-plus approximations and probabilistic schemes

Here, we assume that the assumptions of the two previous sections

hold, and consider a time discretization scheme similar to the one

of Section II.

The application of the operator of (6) to a function can be written, for each

, as

(11a)

where is an operator from to ,

where is the set of measurable functions from to

with at most exponential growth rate, and

Let us say that an operator is monotone

if it satisfies:

(13a)

and that it is additively -subhomogeneous, for some

constant , if it satisfies:

(13b)

where is the map .

The above properties imply that the restriction of to

the set of bounded measurable functions is Lipschitz continuous with constant

.

Using the same kind of proof as in [1]

for (4), one can obtain the stronger property

that all the operators belong to the

class of monotone additively -subhomogeneous operators

from to , for some constant with .

This implies that sends the set of bounded measurable functions

to itself and is Lipschitz continuous with constant on it.

Since we shall consider approximations of the value function

by suprema of concave quadratic forms, we shall need to apply the

operators to quadratic forms, which are unbounded maps.

Therefore, in order

to apply the above properties, we shall rather

assume that the operators can also be written as

(14)

where is given by

with beeing the Euclidian norm,

and where are also of the above form (11)

with some operators instead of belonging again to the

class of monotone additively -subhomogeneous operators

from to , for some constant

with .

Under these conditions, We obtain

a result similar to [4, Theorem 5.1].

Theorem 2

Consider the control problem of Section I.

Assume that and are constant, that

is affine with respect to , that

is concave quadratic with respect to , and that

is the supremum of a finite number of concave quadratic forms.

Consider the time discretization (7)

with ,

and affine.

Assume that the operators satisfy (14)

for some operators of the form (11),

with some operators instead of belonging to the

class of monotone additively -subhomogeneous operators

from to , for some constant

with , see (13).

Assume also that the discretized value function of (7)

is such that is bounded and Lipschitz continuous

with respect to .

Then, for all , there exists a set

and a map such that

for all , is a concave quadratic form and

Moreover, the sets satisfy

This result uses the following properties, the

second one being a generalization of [4, Theorem 3.1].

Lemma 3

Let be a measurable function from to

. Let us consider the notations and assumptions

of Theorem 2 and let be related to

by (12).

Let be the map

, with as in (10).

Then, the function is a concave quadratic form, that is it can be written as for some .

Theorem 4

Let and be a monotone additively -subhomogeneous operator

from to , for some constant , see (13).

Let be a mesurable space, and let be endowed with its

Borel -algebra.

Let be mesurable map such that for all , is bounded and continuous. Let be such that

. Assume that v is continuous and

bounded. Then,

where ,

and

Proof:

Since is bounded and continuous, it belongs to , so that

is well defined. Similarly,

by definition, for all ,

is measurable and bounded, so it belongs to , so that is well defined.

Let .

By definition of , for all , there exists such that .

Then, since and are

continuous maps , there exists such that

for all (the open ball centered at with radius

), and . Then, for , we have

As is the countable union of compact metric spaces,

there exists a sequence of such that

.

Let us denote, for all , and .

Define the function such that,

for all , , for .

Since is a countable partition of

composed of Borel sets, the map is well defined on and

measurable.

Moreover, by the above properties and the definition of , we have

Since is bounded, this implies that is bounded,

which implies that belongs to .

Since is monotone and additively -subhomogeneous from to ,

and , we get that

Then

and since this property holds for all , we

obtain the equality, which shows the assertion of the theorem.

∎

Using Theorem 2, we get that is

the supremum of concave quadratic maps,

but as in [4, Theorem 5.1],

the sets are infinite for .

Here, we shall compute the expression of

the maps by approximating the operators

as in the same spirit as in [1], that is using

the simulation of the processes .

The main difference with the method of [1]

is that the egression estimations are done on quadratic forms and

not on the value functions directly.

Because of the simulations,

we should only need to compute the values .

This means that if is the number of samples of the

Brownian process, then the number of quadratic forms

that are essentials in the computation

of as a supremum of quadratic forms

is less or equal to , where is the cardinality of .

Then, for any random quadratic form

which is optimal for a particular ,

we need to compute its image by .

In [4], this image is obtained by hand. Here, we shall

rather use a regression estimation.

The result of Lemma 3 implies that taking

for the linear regression space, the space of quadratic forms

gives an exact result at least when the sample size is large

(to ensure that the solution of the estimation problem is unique).

With all these properties in mind, we construct the following algorithm.

Let us denote by the following operator

which sends into

:

Since is constant and

is affine, the map is affine for all

.

Algorithm 1

Input: A constant giving the precision,

and a -uple of integers giving the numbers of samples

and the “method of sampling” described below.

A finite subset of such that

, for all ,

and ,

and the operators and as in Theorem 2.

Output:

The subsets of , for ,

and the approximate value function

.

Initialization:

Let be random and independent of the Brownian process.

Consider a sample of

of size indexed by ,

and denote, for each and

, the value

of induced by this sample and satisfying (5).

Define ,

for , with as in (10).

For apply the following 3 steps:

(1) For each and ,

construct a sample

of elements of ,

using the method and possibly

the constants and .

Induce the sample (resp. )

for

of (resp. ).

Denote by

the set of for .

(2) For each and ,

construct depending on and as follows:

Let

be such that,

for all we have

Extend as a measurable map on .

Let be as in Lemma 3,

that is be the map .

Compute an approximation of

by a regression

estimation on the set of quadratic forms using the sample

, with .

We obtain such that

.

(3) Denote by the set of all the obtained in this way,

and define

Let us precise now the different choices of the “method of sampling”

used in the algorithm:

Method 1:

Assume and take for

, which means that we take the initial sampling.

Method 2:

Assume , and choose

once for all and in the algorithm:

a random sampling

among the elements of

and independently a random sampling

among the elements of ,

then take the product of samplings, leading to

for and . Reindexing the sampling,

we obtain for .

Method 3:

Do as in Method 2, but choose different samplings

for each and in the algorithm,

independently.

Method 4:

Assume and and do as in Method 2, but

take the fixed sampling instead of random sampling.

Method 5:

Assume and do as in Method 2, but

take the fixed samplings and

instead of random samplings.

It is easy to see that the sets

of the above algorithm satisfy

for all .

Then, the number of computations at each time step for the optimization

(computation of the )

will be at most in the order of

and at most in the order of

when using methods 2,3,4.

Moreover, the number of computations at each time step for the

regression estimation will be at most in the order of

so will be negligeable with respect to

the optimization step.

Note that in the above algorithm, the regression estimation depends

only on the value of on the simulations

, with . That is

the extension of to a measurable function on

was only needed for the definition of

and .

From Lemma 3,

is a quadratic form.

Hence, when is large, the regression estimation of

as a quadratic form using the given sample is a good approximation.

Under these conditions, we have

for all ,

with holding

for all with .

This implies that, when the regression approximations converge,

is a good approximation of .

Then, under the assumptions of Theorem 2,

one may expect a convergence result comparable to

the one of [1],

showing the existence of some 5-uples such that

converges towards the value

function of the control problem when goes to .

We present numerical tests to confirm this convergence in the next section,

at least in the case of some of the sampling methods proposed above.

The precise convergence study is left for further work.

V Numerical tests

To test our algorithm,

we consider the problem of pricing and hedging an option

with uncertain volatility and two underlying processes,

studied as an example in Section 3.2 of [5].

There, the method proposed is based on a regression on

a process involving not only the state but also the (discrete) control.

With the notations of the introduction, we consider the case where

, with , and there is no continuum control, so is ommited.

The dynamics of the processes are given,

for all , by

, and for ,

with .

The parameters of the reward satisfy , ,

and, for ,

with , .

The two coordinates of the controlled process stay in ,

the set of positive reals.

To be in the conditions of Theorem 2, we approximate the function with a supremum of a finite number of concave quadratic forms on a large subset of , typically on the set of such that .

Note that since the second derivative of is in some points,

it is not -semiconvex for any and bounded domain, so

the approximation need to use some quadratic forms with a large negative

curvature, and so the algorithm proposed in [4] may not work.

The maps for are not constant but they are linear, so one can show that the result of Theorem 2 still holds.

We take the same constants as in [5]:

,

.

We fix the time discretization step to .

We first tested our algorithm in the case where is the singleton

or , which means that there is no action

on the process, so that the true value function can be computed

analytically, and compared with the solution obtained by our algorithm.

The method gives very bad results even at time .

The method need too much space and time even for .

In Table I, we present for different

values of , with ,

the norm of the error

on the value function at time and states

and .

We see that the best method is the second one,

and that Method 3 gives very bad results.

This may be explained by the introduction of

a biais due to the maximization of independent random variables.

Note also that the errors for Method 2 are comparable

to the standard deviations obtained

in [7] by Gobet, Lemor and Warin in the case of

similar option problems with a usual regression estimation of

the value function.

-0.8

1000

10000

10

1000

2

0.521

0.173

0.8

1000

10000

10

1000

2

0.157

0.074

-0.8

1000

1000

10

100

2

0.75

0.41

0.8

1000

1000

10

100

2

0.36

0.11

-0.8

1000

1000

10

100

3

3.48

1.92

0.8

1000

1000

10

100

3

3.05

0.81

-0.8

100

1000

10

100

2

1.95

0.46

0.8

100

1000

10

100

2

1.81

0.33

-0.8

100

10000

10

1000

2

2.09

0.53

0.8

100

10000

10

1000

2

1.79

0.36

-0.8

100

1000

10

100

4

2.15

0.55

0.8

100

1000

10

100

4

1.80

0.39

TABLE I: Sup-norm and normalized norm of the error,

on the value function with constant ,

at time , and states and ,

denoted and resp.

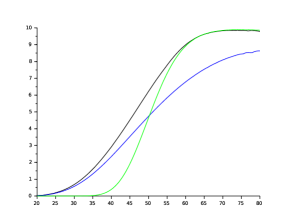

In view of these results, we present in Figure 1 the result obtained for

the control problem tested in [5], that is

with ,

and , , ,

and .

The result is very similar to the one presented in [5].

Figure 1:

Value function obtained at , and as a function

of .

Here , , ,

and .

In blue, is constant equal to , in green is constant

equal to , and in black .

References

[1]

A. Fahim, N. Touzi, and X. Warin, “A probabilistic numerical method for fully

nonlinear parabolic PDEs,” Ann. Appl. Probab., vol. 21, no. 4, pp.

1322–1364, 2011. [Online]. Available:

http://dx.doi.org/10.1214/10-AAP723

[2]

P. Cheridito, H. M. Soner, N. Touzi, and N. Victoir, “Second-order backward

stochastic differential equations and fully nonlinear parabolic PDEs,”

Comm. Pure Appl. Math., vol. 60, no. 7, pp. 1081–1110, 2007.

[Online]. Available: http://dx.doi.org/10.1002/cpa.20168

[3]

H. Kaise and W. M. McEneaney, “Idempotent expansions for continuous-time

stochastic control: compact control space,” in Proceedings of the 49th

IEEE Conference on Decision and Control, Atlanta, Dec. 2010.

[4]

W. M. McEneaney, H. Kaise, and S. H. Han, “Idempotent method for

continuous-time stochastic control and complexity attenuation,” in

Proceedings of the 18th IFAC World Congress, 2011, Milano, Italie,

2011, pp. 3216–3221.

[5]

I. Kharroubi, N. Langrené, and H. Pham, “A numerical algorithm for fully

nonlinear HJB equations: an approach by control randomization,”

Monte Carlo Methods Appl., vol. 20, no. 2, pp. 145–165, 2014.

[Online]. Available: http://dx.doi.org/10.1515/mcma-2013-0024

[6]

B. Bouchard and N. Touzi, “Discrete-time approximation and Monte-Carlo

simulation of backward stochastic differential equations,” Stochastic

Process. Appl., vol. 111, no. 2, pp. 175–206, 2004. [Online]. Available:

http://dx.doi.org/10.1016/j.spa.2004.01.001

[7]

E. Gobet, J.-P. Lemor, and X. Warin, “A regression-based monte carlo method to

solve backward stochastic differential equations,” The Annals of

Applied Probability, vol. 15, no. 3, p. 2172–2202, 2005.