The Jacobi Stochastic Volatility Model111We thank the participants at the 2014 Stochastic Analysis in Finance and Insurance Conference in Oberwolfach, the 2015 AMaMeF and Swissquote Conference in Lausanne, the 2016 ICMS Workshop in Edinburgh, and the seminar at Mannheim Mathematics Department, as well as Stefano De Marco, Julien Hugonnier, Wahid Khosrawi-Sardroudi, Martin Larsson, and Peter Tankov for their comments. We thank an anonymous referee, an anonymous associate editor, and Chris Rogers (co-editor) for their careful reading of the manuscript and suggestions. The research leading to these results has received funding from the European Research Council under the European Union’s Seventh Framework Programme (FP/2007-2013) ERC Grant Agreement n. 307465-POLYTE. The research of Sergio Pulido benefited from the support of the Chair Markets in Transition (Fédération Bancaire Française) and the project ANR 11-LABX-0019.

Abstract

We introduce a novel stochastic volatility model where the squared volatility of the asset return follows a Jacobi process. It contains the Heston model as a limit case. We show that the joint density of any finite sequence of log returns admits a Gram–Charlier A expansion with closed-form coefficients. We derive closed-form series representations for option prices whose discounted payoffs are functions of the asset price trajectory at finitely many time points. This includes European call, put, and digital options, forward start options, and can be applied to discretely monitored Asian options. In a numerical analysis we show that option prices can be accurately and efficiently approximated by truncating their series representations.

forthcoming in Finance and Stochastics

Keywords: Jacobi process, option pricing, polynomial model, stochastic volatility

MSC (2010): 91B25, 91B70, 91G20, 91G60

JEL Classification: C32, G12, G13

1 Introduction

Stochastic volatility models for asset returns are popular among practitioners and academics because they can generate implied volatility surfaces that match option price data to a great extent. They resolve the shortcomings of the Black–Scholes model [12], where the return has constant volatility. Among the the most widely used stochastic volatility models is the Heston model [33], where the squared volatility of the return follows an affine square-root diffusion. European call and put option prices in the Heston model can be computed using Fourier transform techniques, which have their numerical strengths and limitations; see for instance Carr and Madan [15], Bakshi and Madan [9], Duffie et al. [23], Fang and Oosterlee [28], and Chen and Joslin [16].

In this paper we introduce a novel stochastic volatility model, henceforth the Jacobi model, where the squared volatility of the log price follows a Jacobi process with values in some compact interval . As a consequence, Black–Scholes implied volatilities are bounded from below and above by and . The Jacobi model belongs to the class of polynomial diffusions studied in Eriksson and Pistorius [26], Cuchiero et al. [19], and Filipović and Larsson [30]. It includes the Black–Scholes model as a special case and converges weakly in the path space to the Heston model for and .

We show that the log price has a density that admits a Gram–Charlier A series expansion with respect to any Gaussian density with sufficiently large variance. More specifically, the likelihood ratio function lies in the weighted space of square-integrable functions with respect to . Hence it can be expanded as a generalized Fourier series with respect to the corresponding orthonormal basis of Hermite polynomials . Boundedness of is essential, as the Gram–Charlier A series of does not converge for the Heston model.

The Fourier coefficients of are given by the Hermite moments of , . Due to the polynomial property of the Hermite moments admit easy to compute closed-form expressions. This renders the Jacobi model extremely useful for option pricing. Indeed, the price of a European option with discounted payoff for some function in is given by the -scalar product . The Fourier coefficients of are given in closed-form for many important examples, including European call, put, and digital options. We approximate by truncating the price series at some finite order and derive truncation error bounds.

We extend our approach to price exotic options whose discounted payoff depends on a finite sequence of log returns . As in the univariate case we derive the Gram–Charlier A series expansion of the density of with respect to a properly chosen multivariate Gaussian density . Assuming that lies in the option price is obtained as a series representation of the -scalar product in terms of the Fourier coefficients of and of the likelihood ratio function given by the corresponding Hermite moments of . Due to the polynomial property of the Hermite moments admit closed-form expressions, which can be efficiently computed. The Fourier coefficients of are given in closed-form for various examples, including forward start options and forward start options on the underlying return.

Consequently, the pricing of these options is extremely efficient and does not require any numerical integration. Even when the Fourier coefficients of the discounted payoff function are not available in closed-form, e.g. for Asian options, prices can be approximated by integrating with respect to the Gram–Charlier A density approximation of . This boils down to a numerically feasible integration with respect to the underlying Gaussian density . In a numerical analysis we find that the price approximations become accurate within short CPU time. This is in contrast to the Heston model, for which the pricing of exotic options using Fourier transform techniques is cumbersome and creates numerical difficulties as reported in Kruse and Nögel [42], Kahl and Jäckel [39], and Albrecher et al. [6]. In view of this, the Jacobi model also provides a viable alternative to approximate option prices in the Heston model.

The Jacobi process, also known as Wright–Fisher diffusion, was originally used to model gene frequencies; see for instance Karlin and Taylor [41] and Ethier and Kurtz [27]. More recently, the Jacobi process has also been used to model financial factors. For example, Delbaen and Shirakawa [20] model interest rates by the Jacobi process and study moment-based techniques for pricing bonds. In their framework, bond prices admit a series representation in terms of Jacobi polynomials. These polynomials constitute an orthonormal basis of eigenfunctions of the infinitesimal generator and the stationary beta distribution of the Jacobi process; additional properties of the Jacobi process can be found in Mazet [47] and Demni and Zani [21]. The multivariate Jacobi process has been studied in Gourieroux and Jasiak [32] where the authors suggest it to model smooth regime shifts and give an example of stochastic volatility model without leverage effect. The Jacobi process has been also applied recently to model stochastic correlation matrices in Ahdida and Alfonsi [3] and credit default swap indexes in Bernis and Scotti [10].

Density series expansion approaches to option pricing were pioneered by Jarrow and Rudd [38]. They propose expansions of option prices that can be interpreted as corrections to the pricing biases of the Black–Scholes formula. They study density expansions for the law of underlying prices, not the log returns, and express them in terms of cumulants. Evidently, since convergence cannot be guaranteed in general, their study is based on strong assumptions that imply convergence. In subsequent work, Corrado and Su [17] and Corrado and Su [18] study Gram–Charlier A expansions of 4 order for options on the S&P 500 index. These expansions contain skewness and kurtosis adjustments to option prices and implied volatility with respect to the Black–Scholes formula. The skewness and kurtosis correction terms, which depend on the cumulants of and order, are estimated from data. Due to the instability of the estimation procedure, higher order expansions are not studied. Similar studies on the biases of the Black–Scholes formula using Gram–Charlier A expansions include Backus et al. [8] and Li and Melnikov [44]. More recently, Drimus et al. [22] and Necula et al. [48] study related expansions with Hermite polynomials. In order to guarantee the convergence of the Gram–Charlier A expansion for a general class of diffusions, Ait-Sahalia [4] develop a technique based on a suitable change of measure. As pointed out in Filipović et al. [31], in the affine and polynomial settings this change of measure usually destroys the polynomial property and the ability to calculate moments efficiently. More recently a similar study has been carried out by Xiu [53]. Gram–Charlier A expansions, under a change of measure, are also mentioned in the work of Madan and Milne [46], and the subsequent studies of Longstaff [45], Abken et al. [1] and Brenner and Eom [13], where they use these moment expansions to test the martingale property with financial data and hence the validity of a given model.

Our paper is similar to Filipović et al. [31] in that it provides a generic framework to perform density expansions using orthonormal polynomial basis in weighted spaces for affine models. They show that a bilateral Gamma density weight works for the Heston model. However, that expansion is numerically more cumbersome than the Gram–Charlier A expansion because the orthonormal basis of polynomials has to be constructed using Gram–Schmidt orthogonalization. In a related paper Heston and Rossi [34] study polynomial expansions of prices in the Heston, Hull-White and Variance Gamma models using logistic weight functions.

The remainder of the paper is as follows. In Section 2 we introduce the Jacobi stochastic volatility model. In Section 3 we derive European option prices based on the Gram–Charlier A series expansion. In Section 4 we extend this to the multivariate case, which forms the basis for exotic option pricing and contains the European options as special case. In Section 5 we give some numerical examples. In Section 6 we conclude. In Appendix A we explain how to efficiently compute the Hermite moments. All proofs are collected in Appendix B.

2 Model specification

We study a stochastic volatility model where the squared volatility follows a Jacobi process. Fix some real parameters , and define the quadratic function

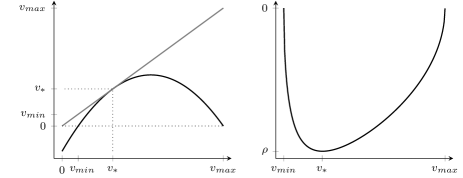

Inspection shows that , with equality if and only if , and for all , see Figure 1 for an illustration.

We consider the diffusion process given by

| (1) | ||||

for real parameters , , , interest rate , dividend yield , and , and where and are independent standard Brownian motions on some filtered probability space . The following theorem shows that is well defined.

Theorem 2.1.

For any deterministic initial state there exists a unique solution of (1) taking values in and satisfying

| (2) |

Moreover, takes values in if and only if and

| (3) |

Remark 2.2.

Property (2) implies that no state is absorbing. It also implies that conditional on , the increments are non-degenerate Gaussian for any as will be shown in the proof of Theorem 4.1. Taking and the limit as , condition (3) coincides with the known condition that precludes the zero lower bound for the CIR process, .

We specify the price of a traded asset by . Then is the stochastic volatility of the asset return, . The cumulative dividend discounted price process is a martingale. In other words, is a risk-neutral measure. The parameter tunes the instantaneous correlation between the asset return and the squared volatility,

This correlation is equal to if , see Figure 1. In general, we have . Empirical evidences suggest that is negative when is a stock price or index. This is commonly referred as the leverage effect, that is, an increase in volatility often goes along with a decrease in asset value.

Since the instantaneous squared volatility follows a bounded Jacobi process on the interval , we refer to (1) as the Jacobi model. For we have constant volatility for all and we obtain the Black–Scholes model

| (4) |

For and the limit we have , and we formally obtain the Heston model as limit case of (1),

| (5) | ||||

In fact, the Jacobi model (1) is robust with respect to perturbations, or mis-specifications, of the model parameters , and initial state . Specifically, the following theorem shows that the diffusion (1) is weakly continuous in the space of continuous paths with respect to , and . In particular, the Heston model (5) is indeed a limit case of our model (1).

Consider a sequence of parameters and deterministic initial states converging to and as , respectively. We denote by and the respective solutions of (1), or (5) if . Here is our main convergence result.

Theorem 2.3.

The sequence of diffusions converges weakly in the path space to as .

As the discounted put option payoff function is bounded and continuous on , it follows from the weak continuity stated in Theorem 2.3 that the put option prices based on converge to the put option price based on the limiting model as . The put-call parity, , then implies that also call option prices converge as . This carries over to more complex path-dependent options with bounded continuous payoff functional.

Polynomial property

Moments in the Jacobi model (1) are given in closed-form. Indeed, let

denote the generator of with drift vector and the diffusion matrix given by

| (6) |

Observe that is continuous in the parameters , , so that for and we obtain

which corresponds to the generator of the Heston model (5). Let be the vector space of polynomials in of degree less than or equal to . It then follows by inspection that the components of and lie in and , respectively. As a consequence, maps any polynomial of degree onto a polynomial of degree or less, , so that is a polynomial diffusion, see Filipović and Larsson [30, Lemma 2.2]. From this we can easily calculate the conditional moments of as follows. For , let denote the dimension of . Let be a basis of polynomials of and denote by the matrix representation of the linear map restricted to with respect to this basis.

Theorem 2.4.

For any polynomial and we have

where is the coordinate representation of the polynomial with respect to the basis .

Proof.

See Filipović and Larsson [30, Theorem 3.1]. ∎

The moment formula in Theorem 2.4 is crucial in order to efficiently implement the numerical schemes described below.

3 European option pricing

Henceforth we assume that is a deterministic initial state and fix a finite time horizon . We first establish some key properties of the distribution of . Denote the quadratic variation of the second martingale component of in (1) by

| (7) |

The following theorem is a special case of Theorem 4.1 below.

Theorem 3.1.

Let . The distribution of admits a density on that satisfies

| (8) |

If

| (9) |

for some then and are uniformly bounded and is -times continuously differentiable on . A sufficient condition for (9) to hold for any is

| (10) |

The condition that is sharp for (8) to hold. Indeed, consider the Black–Scholes model (4) where for all . Then is Gaussian with variance . Hence the integral in (8) is infinite for any .

Since any uniformly bounded and integrable function on is square integrable on , as an immediate consequence of Theorem 3.1 we have the following corollary.

Corollary 3.2.

Remark 3.3.

It follows from the proof that the statements of Theorem 3.1 also hold for the Heston model (5) with and . However, the Heston model does not satisfy (8) for any . Indeed, otherwise its moment generating function

| (13) |

would extend to an entire function in . But it is well known that becomes infinite for large enough , see Andersen and Piterbarg [7]. As a consequence, the Heston model does not satisfy (11) for any finite . Indeed, by the Cauchy-Schwarz inequality, (11) implies (8) for any .

We now compute the price at time of a European claim with discounted payoff at expiry date . We henceforth assume that (9) holds with , and we let be a Gaussian density with mean and variance satisfying (12). We define the weighted Lebesgue space

which is a Hilbert space with scalar product

The space admits the orthonormal basis of generalized Hermite polynomials , , given by

| (14) |

where are the standard Hermite polynomials defined by

| (15) |

see Feller [29, Section XVI.1]. In particular, the degree of is , and if and zero otherwise.

Corollary 3.2 implies that the likelihood ratio function of the density of the log price with respect to belongs to . We henceforth assume that also the discounted payoff function is in . This hypothesis is satisfied for instance in the case of European call and put options. It implies that the price, denoted by , is well defined and equals

| (16) |

for the Fourier coefficients of

| (17) |

and the Fourier coefficients of that we refer to as Hermite moments

| (18) |

We approximate the price by truncating the series in (16) at some order and write

| (19) |

so that as . Due to the polynomial property of the Jacobi model, (19) induces an efficient price approximation scheme because the Hermite moments are linear combinations of moments of and thus given in closed-form, see Theorem 2.4. In particular, since , we have . More details on the computation of are given in Appendix A.

With the Hermite moments available, the computation of the approximation (19) boils down to a numerical integration,

| (20) |

of with respect to the Gaussian distribution , where the polynomial is in closed-form. The integral (20) can be computed by quadrature or Monte-Carlo simulation. In specific cases, we find closed-form formulas for the Fourier coefficients and no numerical integration is needed. This includes European call, put, and digital options, as shown below.

Remark 3.4.

Formula (20) shows that serves as an approximation for the density . In fact, we readily see that integrates to one and converges to in as . Hence, we have convergence of the Gram–Charlier A series expansion of the density of the log price in .666A Gram–Charlier A series expansion of a density function is formally defined as for some real numbers , . In view of Remark 3.3, this does not hold for the Heston model.

Matching the first moment or the first two moments of and , we further obtain

and similarly,

| (21) |

Matching the first moment or the first two moments of and can improve the convergence of the approximation (19). Note however that (12) and (21) imply , so that second moment matching is not always feasible in empirical applications.

Remark 3.5.

If , then is the Black–Scholes option price with volatility parameter . Because , this holds in particular if the first two moments of and match, see (21). In this case, the higher order terms in can be thought of as corrections to the corresponding Black–Scholes price due to stochastic volatility.

The following result, which is a special case of Theorem 4.4 below, provides universal upper and lower bounds on the implied volatility of a European option with discounted payoff at and price . The implied volatility is defined as the volatility parameter that renders the corresponding Black–Scholes option price equal to .

Theorem 3.6.

Assume that the discounted payoff function is convex in . Then the implied volatility satisfies .

Examples

We now present examples of discounted payoff functions for which closed-form formulas for the Fourier coefficients exist. The first example is a call option.777Similar recursive relations of the Fourier coefficients for the physicist Hermite polynomial basis can be found in Drimus et al. [22]. The physicist Hermite polynomial basis is the orthogonal polynomial basis of the space equipped with the weight function so that .

Theorem 3.7.

Consider the discounted payoff function for a call option with log strike ,

| (22) |

Its Fourier coefficients in (17) are given by

| (23) |

The functions are defined recursively by

| (24) | ||||

where denotes the standard Gaussian distribution function and its density.

The Fourier coefficients of a put option can be obtained from the put-call parity. For digital options, the Fourier coefficients are as follows.

Theorem 3.8.

Consider the discounted payoff function for a digital option of the form

Its Fourier coefficients are given by

| (25) |

where denotes the standard Gaussian distribution function and its density.

For a digital option with generic payoff the Fourier coefficients can be derived using Theorem 3.8 and

Error bounds and asymptotics

We first discuss an error bound of the price approximation scheme (19). The error of the approximation is for a fixed order . The Cauchy–Schwarz inequality implies the following error bound

| (26) |

The -norm of has an explicit expression, , that can be computed by quadrature or Monte–Carlo simulation. The Fourier coefficients can be computed similarly. The Hermite moments are given in closed-form. It remains to compute the -norm of . For further use we define

| (27) |

so that, in view of (1), the log price . Recall also given in (7).

Lemma 3.9.

The -norm of is given by

| (28) |

where is the normal density function in with mean and variance , and the pair of random variables is independent from and has the same distribution as .

In applications, we compute the right hand side of (28) by Monte–Carlo simulation of and thus obtain the error bound (26).

We next show that the Hermite moments decay at an exponential rate under some technical assumptions.

Lemma 3.10.

Suppose that (10) holds and . Then there exist finite constants and such that for all .

Comparison to Fourier transform

An alternative dual expression of the price in (16) is given by the Fourier integral

| (29) |

where and denote the moment generating functions given by (13), respectively. Here is some appropriate dampening parameter such that and are Lebesgue integrable and square integrable on . Indeed, Lebesgue integrability implies that and are well defined for through (13). Square integrability and the Plancherel Theorem then yield the representation (29). For example, for the European call option (22) we have for

Option pricing via (29) is the approach taken in the Heston model (5), for which there exists a closed-form expression for . It is given in terms of the solution of a Riccati equation. The computation of boils down to the numerical integration of (29) along with the numerical solution of a Riccati equation for every argument that is needed for the integration. The Heston model (which entails ) does not adhere to the series representation (16) that is based on condition (11), see Remark 3.3.

The Jacobi model, on the other hand, does not admit a closed-form expression for . But the Hermite moments are readily available in closed-form. In conjunction with Theorem 3.7, the (truncated) series representation (16) thus provides a valuable alternative to the (numerical) Fourier integral approach (29) for option pricing. Moreover, the approximation (20) can be applied to any discounted payoff function . This includes functions that do not necessarily admit closed-form moment generating function as is required in the Heston model approach. In Section 4, we further develop our approach to price path dependent options, which could be a cumbersome task using Fourier transform techniques in the Heston model.

4 Exotic option pricing

Pricing exotic options with stochastic volatility models is a challenging task. We show that the price of an exotic option whose payoff is a function of a finite sequence of log returns admits a polynomial series representation in the Jacobi model.

Henceforth we assume that is a deterministic initial state. Consider time points and denote the log returns for . The following theorem contains Theorem 3.1 as special case where .

Theorem 4.1.

Since any uniformly bounded and integrable function on is square integrable on , as an immediate consequence of Theorem 4.1 we have the following corollary.

Corollary 4.2.

Remark 4.3.

There is a one-to-one correspondence between the vector of log returns and the vector of log prices . Indeed,

Hence, a crucial consequence of Theorem 4.1 is that the finite-dimensional distributions of the process admit densities with nice decay properties. More precisely, the density of is .

Suppose that the discounted payoff of an exotic option is of the form . Assume that (30) holds with . Set the weight function , where is a Gaussian density with mean and variance satisfying (31). Define

Then by similar arguments as in Section 3 the price of the option is

where the Fourier coefficients and the Hermite moments are given by

and

| (32) |

with , where is the generalized Hermite polynomial of degree associated to parameters and , see (14). The price approximation at truncation order is given, in analogy to (19), by

| (33) |

so that as .

We now derive universal upper and lower bounds on the implied volatility for the exotic option with discounted payoff function and price . We denote by

| (34) |

the Black–Scholes price process with volatility where is some Brownian motion. The Black–Scholes price is defined by

The implied volatility is the volatility parameter that renders the Black–Scholes option price . The following theorem provides bounds on the values that may take.

Theorem 4.4.

Assume that the payoff function is convex in the prices . Then the implied volatility satisfies .

Examples

We provide some examples of exotic options on the asset with price for which our method applies.

The payoff of a forward start call option on the underlying return between dates and , and with strike is and its discounted payoff function is given by

with the times and . Note that only depends on , so that this example reduces to the univariate case. In particular, the Fourier coefficients coincide with those of a call option and, as we shall see in Theroem A.3, the forward Hermite moments can be computed efficiently. Theorem 4.4 applies in particular to the forward start call option on the underlying return, so that its implied volatility is uniformly bounded for all maturities . On the other hand, we know from Jacquier and Roome [37] that in the Heston model the same implied volatility explodes (except at the money) when .

The payoff of a forward start call option with maturity , strike fixing date and proportional strike is and its discounted payoff function is given by

with the times and . In this case the Fourier coefficients have the form

where denotes the Fourier coefficient of a call option for interest rate and log strike as in (23). Here we have used (23)–(24) to deduce that . In particular no numerical integration is needed. Additionally, the Hermite moments

can be calculated efficiently as explained in Theorem A.3. The pricing of forward start call options (on the underlying return) in the Black–Scholes model is straightforward. Analytical expressions for forward start call options (on the underlying return) have been provided in the Heston model by Kruse and Nögel [42]. However, these integral expressions involve the Bessel function of first kind and are therefore rather difficult to implement numerically.

The payoff of an Asian call option with maturity , discrete monitoring dates , and fixed strike is and its discounted payoff function is given by

The payoff of an Asian call option with floating strike is and its discounted payoff function is given by

The valuation of Asian options with continuously monitoring in the Black–Scholes model has been studied in Rogers and Shi [51] and Yor [55] among others.

Remark 4.5.

The Fourier coefficients may not be available in closed-form for some exotic options, such as the Asian options. In this case, we compute the multi-dimensional version of the approximation (19) via numerical integration of (20) with respect to a Gaussian density in . This can be efficiently implemented using Gauss-Hermite quadrature, see for example Jäckel [36]. Specifically, denote and the -th point and weight of an -dimensional standard Gaussian cubature rule with points. The price approximation can then be computed as follows

| (35) | ||||

where , , , and denotes the standard Hermite polynomial (15). We emphasize that many elements in the above expression can be precomputed. A numerical example is given for the Asian option in Section 5.2 below.

5 Numerical analysis

We analyse the performance of the price approximation (19) with closed-form Fourier coefficients and numerical integration of (20) for European call options, forward start and Asian options. This includes price approximation error, model implied volatility, and computational time. The model parameters are fixed as: , , , , , , and . The parameter values are in line with what could be obtained from a calibration to market prices, such as S&P500 option prices, with the exception of that is set smaller than the typical fitted value. The choice permits to match the first two moments of and as in (21), which improves the convergence of the approximation (19). We refer to Ackerer and Filipović [2] for an extension of the polynomial option pricing method, which works well for arbitrary parameter values.

5.1 European call option

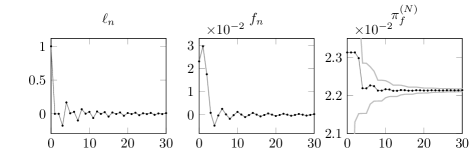

Figure 2 displays Hermite moments , Fourier coefficients , and approximation option prices for a European call option with maturity and log strike (ATM) as functions of the truncation order . The first two moments of the Gaussian density match the first two moments of , see (21).888In practice, depending on the model parameters, this may not always be feasible, in which case the truncation order should be increased. We observe that the and sequences oscillate and converge toward zero. The amplitudes of these oscillations negatively impact the speed at which the approximation price sequence converges. The gray lines surrounding the price sequence are the upper and lower price error bounds computed as in (26) and Lemma 3.9, using Monte-Carlo samples. The price approximation converges rapidly.

Table 1 reports the implied volatility values and absolute errors in percentage points for the log strikes and for various truncation orders. The reference option prices have been computed at truncation order . For all strikes the truncation order is sufficient to be within 10 basis points of the reference implied volatility.

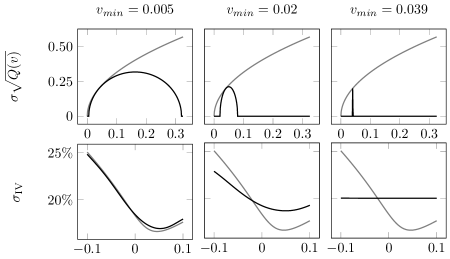

Figure 3 displays the implied volatility smile for various and such that , and for the Heston model (5). We observe that the smile of the Jacobi model approaches the Heston smile when is small and is large. Somewhat surprisingly, a relatively small value for seems to be sufficient for the two smiles to coincide for options around the money. Indeed, although the variance process has an unbounded support in the Heston model, the probability that it will visit values beyond some large threshold can be extremely small. Figure 3 also illustrates how the implied volatility smile flattens when the variance support shrinks, . In the limit , we obtain the flat implied volatility smile of the Black–Scholes model. This shows that the Jacobi model lies between the Black–Scholes model and the Heston model and that the parameters and offer additional degrees of flexibility to model the volatility surface.

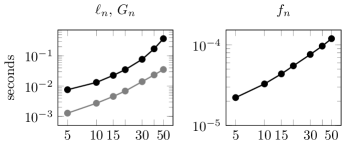

As reported in Figure 4, the Fourier coefficients can be computed in less than a millisecond thanks to the recursive scheme (23)-(24). Computing the Hermite moments is more costly, however they can be used to price all options with the same maturity. The most expensive task appears to be the construction of the matrix , which however is a one-off. The Hermite moment in turn derives from the vector which can be used for any initial state . Note that specific numerical methods have been developed to compute the action of the matrix exponential on the basis vector , see for example Al-Mohy and Higham [5], Hochbruck and Lubich [35], and references therein. The running times were realized with a standard desktop computer using a single 3.5 Ghz 64 bits CPU and the R programming language.

5.2 Forward start and Asian options

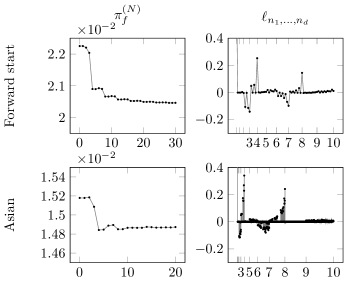

The left panels of Figure 5 display the approximation prices of a forward start call option with strike fixing time and maturity , so that , and of an Asian call option with weekly discrete monitoring and maturity four weeks, for . Both options have log strike . The price approximations at order have been computed using (33). For the forward start call option, we match the first two moments of and . For the Asian call option, we chose and , which is in line with (31) but does not match the first two moments of . The Fourier coefficients are not available in closed-form for the Asian call option, therefore we integrated its payoff function with respect to the density approximation using Gaussian cubature as described in Remark 4.5. We observe that with exotic payoffs the price approximation sequence may require a larger order before stabilizing. For example, for the forward start price approximation it seems necessary to truncate beyond in order to obtain a accurate price approximation.

The Asian option price is approximated by (35) whose computational cost depends on the number of elements in the double summation. Therefore, in order to efficiently approximate the price, we used a truncation of the 4-dimensional product of the one-dimensional Gaussian quadrature with 20 points. More precisely, we selected the quadrature points having a weight larger than the quantile of all the weights. This means that, out of the initial points, points were selected and their weights normalized. Note that the removed points had a total weight of percent which is extremely small. Hence, the selected points cover most of the non-negligible part of the multivariate Gaussian density support. An alternative approach would be to use optimal Gaussian quantizers, see Pagès and Printems [49].

The right panels of Figure 5 display the multi-index Hermite moments with multi-orders . Note that there are Hermite moments of total order . In practice, we observe that a significant proportion of the Hermite moments is negligible so that they may simply be set to zero if they are smaller than a certain threshold to be computed online. As for the quadrature points, doing so reduces the computational cost of approximating the option price. Therefore, when approximating the Asian option price, we removed the Hermite moments having an absolute value smaller than the correspondning quantile. For example, when , this implies removing all the Hermite moments with an absolute value smaller than .

6 Conclusion

The Jacobi model is a highly tractable and versatile stochastic volatility model. It contains the Heston stochastic volatility model as a limit case. The moments of the finite dimensional distributions of the log prices can be calculated explicitly thanks to the polynomial property of the model. As a result, the series approximation techniques based on the Gram–Charlier A expansions of the joint distributions of finite sequences of log returns allow us to efficiently compute prices of options whose payoff depends on the underlying asset price at finitely many time points. Compared to the Heston model, the Jacobi model offers additional flexibility to fit a large range of Black–Scholes implied volatility surfaces. Our numerical analysis shows that the series approximations of European call, put and digital option prices in the Jacobi model are computationally comparable to the widely used Fourier transform techniques for option pricing in the Heston model. The truncated series of prices, whose computations do not require any numerical integration, can be implemented efficiently and reliably up to orders that guarantee accurate approximations as shown by our numerical analysis. The pricing of forward start options, which does not involve any numerical integration, is significantly simpler and faster than the iterative numerical integration method used in the Heston model. The minimal and maximal volatility parameters are universal bounds for Black–Scholes implied volatilities and provide additional stability to the model. In particular, Black–Scholes implied volatilities of forward start options in the Jacobi model do not experience the explosions observed in the Heston model. Furthermore, our density approximation technique in the Jacobi model circumvents some limitations of the Fourier transform techniques in affine models and allows us to price discretely monitored Asian options.

Appendix A Hermite moments

We apply Theorem 2.4 to describe more explicitly how the Hermite moments in (18) can be efficiently computed for any fixed truncation order . We let and be an enumeration of the set of exponents

The polynomials

| (36) |

then form a basis of . In view of the elementary property

we obtain that the –matrix representing on has at most 7 nonzero elements in column with given by

Theorem 2.4 now implies the following result.

Theorem A.1.

The coefficients are given by

| (37) |

where is the –th standard basis vector in .

Remark A.2.

The choice of the basis polynomials in (36) is convenient for our purposes because: 1) each column of the -matrix has at most seven nonzero entries. 2) The coefficients in the expansion of prices (16), can be obtained directly from the action of on as specified in (37). In practice, it is more efficient to compute directly this action, rather than computing the matrix exponential and then selecting the -column.

We now extend Theorem A.1 to a multi-dimensional setting. The following theorem provides an efficient way to compute the multi-dimensional Hermite moments defined in (32). Before stating the theorem we fix some notation. Set and . Let be the matrix representation of the linear map restricted to with respect to the basis, in row vector form,

with as in (36) where is the generalized Hermite polynomial of degree associated to the parameters and , see (14). Define the -matrix by

Theorem A.3.

Proof.

By an inductive argument it is sufficient to illustrate the case . Applying the law of iterated expectation we obtain

Since the increment does not depend on we can rewrite, using Theorem 2.4,

where . Note that this last expression is a polynomial solely in

Theorem 2.4 now implies that the Hermite coefficient is given by

where is the vector representation in the basis of the polynomial

We conclude by observing that the coordinates of the vector are given by if for some integer and equal to zero otherwise, which in turn shows that . ∎

Appendix B Proofs

This appendix contains the proofs of all theorems and propositions in the main text.

Proof of Theorem 2.1

For strong existence and uniqueness of (1), it is enough to show strong existence and uniqueness for the SDE for ,

| (38) |

Since the interval is an affine transformation of the unit ball in , weak existence of a -valued solution can be deduced from Larsson and Pulido [43, Theorem 2.1]. Path-wise uniqueness of solutions follows from Yamada and Watanabe [54, Theorem 1]. Strong existence of solutions for the SDE (38) is a consequence of path-wise uniqueness and weak existence of solutions, see for instance Yamada and Watanabe [54, Corollary 1].

Proof of Theorem 2.3

The proof of Theorem 2.3 builds on the following four lemmas.

Lemma B.1.

Suppose that and , , are random variables in for which all moments exist. Assume further that

| (39) |

for any polynomial and that the distribution of is determined by its moments. Then the sequence converges weakly to as .

Proof.

Theorem 30.2 in Billingsley [11] proves this result for the case . Inspection shows that the proof is still valid for the general case. ∎

Lemma B.2.

The moments of the finite-dimensional distributions of the diffusions converge to the respective moments of the finite-dimensional distributions of . That is, for any and for any polynomials we have

| (40) |

Proof.

Let . Throughout the proof we fix a basis of , where , and for any polynomial we denote by its coordinates with respect to this basis. We denote by and the respective -matrix representations of the generators restricted to of and , respectively. We then define recursively the polynomials and for by

As in the proof of Theorem A.3, a successive application of Theorem 2.4 and the law of iterated expectation implies that

and similarly,

Lemma B.3.

The finite-dimensional distributions of are determined by their moments.

Proof.

The proof of this result is contained in the proof of Filipović and Larsson [30, Lemma 4.1]. ∎

Lemma B.4.

The family of diffusions is tight.

Proof.

Fix a time horizon . We first observe that by Karatzas and Shreve [40, Problem V.3.15] there is a constant independent of such that

| (42) |

Now fix any positive . Kolmogorov’s continuity theorem (see Revuz and Yor [50, Theorem I.2.1]) implies that

for a finite constant that is independent of . The modulus of continuity

thus satisfies

Using Chebyshev’s inequality we conclude that, for every ,

and thus as . This together with the property that the initial states converge to as proves the lemma, see Rogers and Williams [52, Theorem II.85.3].999The derivation of the tightness of from (42) is also stated without proof in Rogers and Williams [52, Theorem II.85.5]. For the sake of completeness we give a short self-contained argument here. ∎

Remark B.5.

Proof of Theorem 3.7

Proof of Theorem 3.8

Proof of Lemma 3.9

Proof of Lemma 3.10

We first recall that by Cramér’s inequality (see for instance Erdélyi et al. [25, Section 10.18]) there exists a constant such that for all

| (46) |

Additionally, as in the proof Theorem 4.1, since ,

where is given in (45). This implies

We can therefore use Fubini’s theorem to deduce

| (47) |

We now analyze the term inside the expectation in (47). A change of variables shows

where we define and . We recall that

| (48) |

The inequalities in (48) together with the fact that is a bounded process yield the following uniform bounds for ,

| (49) |

with constants and . Define

so that

An integration by parts argument using (44) and the identity

shows the following recursion formula

with and . This recursion formula is closely related to the recursion formula of the Hermite polynomials which helps us deduce the following explicit expression

| (50) |

Recall that

| (51) |

and

Cauchy-Schwarz inequality and (46) yield

| (52) |

Inequalities (49) and (52) imply the existence of constants and such that .

Proof of Theorem 4.1

In order to shorten the notation we write for any process . From (1) we infer that the log price where is defined in (27). In particular the log returns have the form

In view of property (2) we infer that for . Motivated by Broadie and Kaya [14], we notice that, conditional on , the random variable is Gaussian with mean vector and covariance matrix . Its density has the form

Fubini’s theorem implies that is measurable and satisfies, for any bounded measurable function ,

Hence the distribution of admits the density on . Dominated convergence implies that is uniformly bounded and –times continuously differentiable on if (30) holds. The arguments so far do not depended on and also apply to the Heston model, which proves Remark 3.3.

For the rest of the proof we assume, without loss of generality, that for . Observe that the mean vector and covariance matrix of admit the uniform bounds

for some finite constant . Define and . Then and . Completing the square implies

| (53) |

Integration of (53) then gives

Hence (8) follows by Fubini’s theorem after taking expectation on both sides. We also derive from (53) that

Hence is uniformly bounded and continuous on if (30) holds. In fact, for this to hold it is enough suppose that (30) holds with . Moreover, (10) implies that and (30) follows.

Proof of Theorem 4.4

We assume the Brownian motions and in (34) and (1) are independent. We denote by the time- price of the exotic option in the Jacobi model.

For any and given a realization , the time- Black–Scholes price of the option is a function of and the spot price defined by

where we write

By assumption, we infer that is convex in . Moreover, satisfies the following PDE

| (54) |

and has terminal value satisfying . Write

and for the martingale driving the asset return in (1) such that, using (54),

Consider the self-financing portfolio with zero initial value, long one unit of the exotic option, and short units of the underlying asset. Let denote the time- value of this portfolio. Its discounted price dynamics then satisfies

Integrating in gives

| (55) |

as .

We now claim that the time- option price lies between the Black–Scholes option prices for and ,

| (56) |

Indeed, let . Because by assumption, it follows from (55) that . Absence of arbitrage implies that must not be bounded away from zero, hence . This proves the left inequality in (56). The right inequality follows similarly, whence the claim (56) is proved.

A similar argument shows that the Black–Scholes price is non-decreasing in , whence , and the theorem is proved.

| IV | error | IV | error | IV | error | |

|---|---|---|---|---|---|---|

| 0–2 | 20.13 | 2.62 | 20.09 | 0.86 | 20.08 | 0.83 |

| 3 | 22.12 | 0.63 | 19.96 | 0.73 | 16.60 | 2.65 |

| 4 | 23.02 | 0.27 | 19.27 | 0.04 | 18.88 | 0.37 |

| 5 | 23.03 | 0.28 | 19.27 | 0.04 | 18.88 | 0.37 |

| 6 | 22.93 | 0.18 | 19.33 | 0.10 | 18.72 | 0.53 |

| 7 | 22.76 | 0.01 | 19.32 | 0.09 | 19.11 | 0.14 |

| 8 | 22.83 | 0.08 | 19.22 | 0.01 | 19.18 | 0.07 |

| 9 | 22.82 | 0.07 | 19.22 | 0.01 | 19.19 | 0.06 |

| 10 | 22.83 | 0.08 | 19.25 | 0.02 | 19.22 | 0.03 |

| 15 | 22.74 | 0.01 | 19.23 | 0.00 | 19.32 | 0.07 |

| 20 | 22.75 | 0.00 | 19.23 | 0.00 | 19.28 | 0.03 |

| 30 | 22.75 | 0.00 | 19.23 | 0.00 | 19.25 | 0.00 |

The quadratic variation of the Jacobi model (black line) and of the Heston model (gray line) are displayed in the left panel as a function of the instantaneous variance. The right panel displays the instantaneous correlation between the processes and as a function of the instantaneous variance. We denote and assumed that .

Hermite moments , Fourier coefficients , and approximation prices with error bounds as functions of the order (truncation order ).

The first row displays the variance process’ diffusion function in the Jacobi model (black line) and in the Heston model (gray line). The second row displays the implied volatility as a function of the log strike in the Jacobi model (black line) and in the Heston model (gray line).

The left panel displays the computing time to derive the Hermite moments (black line) and the matrix (gray line) as functions of the order . The right panel displays the same relation for the Fourier coefficients (black line).

The left panels display the approximation prices as functions of the truncation order . The right panels display the corresponding Hermite moments for multi-orders .

References

- Abken et al. [1996] Peter A. Abken, Dilip B. Madan, and Buddhavarapu Sailesh Ramamurtie. Estimation of risk-neutral and statistical densities by Hermite polynomial approximation: with an application to Eurodollar futures options. Working Paper 96-5, Federal Reserve Bank of Atlanta. Available online at https://www.researchgate.net/profile/Dilip_Madan, 1996.

- Ackerer and Filipović [2017] Damien Ackerer and Damir Filipović. Option pricing with orthogonal polynomial expansions. Swiss Finance Institute Research Paper No. 17-41. Available online at https://ssrn.com/abstract=3076519, 2017.

- Ahdida and Alfonsi [2013] Abdelkoddousse Ahdida and Aurélien Alfonsi. A mean-reverting SDE on correlation matrices. Stochastic Processes and their Applications, 123(4):1472–1520, 2013.

- Ait-Sahalia [2002] Yacine Ait-Sahalia. Maximum likelihood estimation of discretely sampled diffusions: A closed-form approximation approach. Econometrica, 70(1):223–262, 2002.

- Al-Mohy and Higham [2011] Awad H Al-Mohy and Nicholas J Higham. Computing the action of the matrix exponential, with an application to exponential integrators. SIAM journal on scientific computing, 33(2):488–511, 2011.

- Albrecher et al. [2007] Hansjörg Albrecher, Philipp Mayer, Wim Schoutens, and Jurgen Tistaert. The little Heston trap. Wilmott Magazine, January:83–92, 2007.

- Andersen and Piterbarg [2007] Leif BG Andersen and Vladimir V Piterbarg. Moment explosions in stochastic volatility models. Finance and Stochastics, 11(1):29–50, 2007.

- Backus et al. [2004] David K. Backus, Silverio Foresi, and Liuren Wu. Accounting for biases in Black-Scholes. Available online at https://ssrn.com/abstract=585623, 2004.

- Bakshi and Madan [2000] Gurdip Bakshi and Dilip Madan. Spanning and derivative-security valuation. Journal of Financial Economics, 55(2):205–238, 2000.

- Bernis and Scotti [2017] Guillaume Bernis and Simone Scotti. Alternative to beta coefficients in the context of diffusions. Quantitative Finance, 17(2):275–288, 2017.

- Billingsley [1995] P. Billingsley. Probability and Measure. Wiley Series in Probability and Statistics. Wiley, 1995.

- Black and Scholes [1973] Fisher Black and Myron S. Scholes. The pricing of options and corporate liabilities. Journal of political economy, 81(3):637–654, 1973.

- Brenner and Eom [1997] M Brenner and Y Eom. No-arbitrage option pricing: New evidence on the validity of the martingale property. NYU Working Paper No. FIN-98-009. Available online at https://ssrn.com/abstract=1296404, 1997.

- Broadie and Kaya [2006] Mark Broadie and zgr Kaya. Exact simulation of stochastic volatility and other affine jump diffusion processes. Operations Research, 54(2):217–231, 2006.

- Carr and Madan [1999] Peter Carr and Dilip Madan. Option valuation using the fast Fourier transform. Journal of computational finance, 2(4):61–73, 1999.

- Chen and Joslin [2012] Hui Chen and Scott Joslin. Generalized transform analysis of affine processes and applications in finance. Review of Financial Studies, 25(7):2225–2256, 2012.

- Corrado and Su [1996] Charles J Corrado and Tie Su. Skewness and kurtosis in S&P 500 index returns implied by option prices. Journal of Financial research, 19(2):175–192, 1996.

- Corrado and Su [1997] Charles J Corrado and Tie Su. Implied volatility skews and stock index skewness and kurtosis implied by S&P 500 index option prices. Journal of Derivatives, 4(4):8–19, 1997.

- Cuchiero et al. [2012] Christa Cuchiero, Martin Keller-Ressel, and Josef Teichmann. Polynomial processes and their applications to mathematical finance. Finance and Stochastics, 16(4):711–740, 2012.

- Delbaen and Shirakawa [2002] Freddy Delbaen and Hiroshi Shirakawa. An interest rate model with upper and lower bounds. Asia-Pacific Financial Markets, 9(3-4):191–209, 2002.

- Demni and Zani [2009] Nizar Demni and Marguerite Zani. Large deviations for statistics of the Jacobi process. Stochastic Processes and their Applications, 119(2):518–533, 2009.

- Drimus et al. [2013] Gabriel G Drimus, Ciprian Necula, and Walter Farkas. Closed form option pricing under generalized Hermite expansions. Working Paper. Available online at https://ssrn.com/abstract=2349868, 2013.

- Duffie et al. [2003] D. Duffie, D. Filipović, and W. Schachermayer. Affine processes and applications in finance. Annals of Applied Probabability, 13(3):984–1053, 2003.

- Dufresne [2001] Daniel Dufresne. The integrated square-root process. Working Paper No. 90, Centre for Actuarial Studies, University of Melbourne. Available online at https://hdl.handle.net/11343/33693, 2001.

- Erdélyi et al. [1953] Arthur Erdélyi, Wilhelm Magnus, Fritz Oberhettinger, and Francesco G. Tricomi. Higher transcendental functions. Vols. I, II. McGraw-Hill Book Company, Inc., New York-Toronto-London, 1953. Based, in part, on notes left by Harry Bateman.

- Eriksson and Pistorius [2011] Bjorn Eriksson and Martijn Pistorius. Method of moments approach to pricing double barrier contracts in polynomial jump-diffusion models. International Journal of Theoretical and Applied Finance, 14(7):1139–1158, 2011.

- Ethier and Kurtz [1986] Stewart N. Ethier and Thomas G. Kurtz. Markov processes : characterization and convergence. Wiley series in probability and mathematical statistics. J. Wiley & Sons, New York, Chichester, 1986.

- Fang and Oosterlee [2009] F. Fang and C. W. Oosterlee. A novel pricing method for European options based on Fourier-cosine series expansions. SIAM Journal on Scientific Computing, 31(2):826–848, 2009.

- Feller [1960] Vilim Feller. An Introduction to Probability Theory and Its Applications: Volume 1. J. Wiley & sons, 1960.

- Filipović and Larsson [2016] D. Filipović and M. Larsson. Polynomial diffusions and applications in finance. Finance and Stochastics, 20:931–972, 2016.

- Filipović et al. [2013] Damir Filipović, Eberhard Mayerhofer, and Paul Schneider. Density approximations for multivariate affine jump-diffusion processes. Journal of Econometrics, 176(2):93–111, 2013.

- Gourieroux and Jasiak [2006] Christian Gourieroux and Joann Jasiak. Multivariate Jacobi process with application to smooth transitions. Journal of Econometrics, 131(1):475–505, 2006.

- Heston [1993] Steven L Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6(2):327–343, 1993.

- Heston and Rossi [2016] Steven L Heston and Alberto G Rossi. A spanning series approach to options. The Review of Asset Pricing Studies, 7(1):2–42, 2016.

- Hochbruck and Lubich [1997] Marlis Hochbruck and Christian Lubich. On Krylov subspace approximations to the matrix exponential operator. SIAM Journal on Numerical Analysis, 34(5):1911–1925, 1997.

- Jäckel [2005] Peter Jäckel. A note on multivariate Gauss-Hermite quadrature. Technical report. Available online at http://www.jaeckel.org, 2005.

- Jacquier and Roome [2015] Antoine Jacquier and Patrick Roome. Asymptotics of forward implied volatility. SIAM Journal on Financial Mathematics, 6(1):307–351, 2015.

- Jarrow and Rudd [1982] Robert Jarrow and Andrew Rudd. Approximate option valuation for arbitrary stochastic processes. Journal of Financial Economics, 10(3):347–369, 1982.

- Kahl and Jäckel [2005] Christian Kahl and Peter Jäckel. Not-so-complex logarithms in the Heston model. Wilmott magazine, 19(9):94–103, 2005.

- Karatzas and Shreve [1991] Ioannis Karatzas and Steven E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer New York, 1991.

- Karlin and Taylor [1981] S. Karlin and H.M. Taylor. A Second Course in Stochastic Processes. Academic Press, 1981.

- Kruse and Nögel [2005] Susanne Kruse and Ulrich Nögel. On the pricing of forward starting options in Heston’s model on stochastic volatility. Finance and Stochastics, 9(2):233–250, 2005.

- Larsson and Pulido [2017] M. Larsson and S. Pulido. Polynomial preserving diffusions on compact quadric sets. Stochastic Processes and their Applications, 127(3):901–926, 2017.

- Li and Melnikov [2012] Hao Li and Alexander Melnikov. On Polynomial-Normal model and option pricing. In Stochastic Processes, Finance and Control: A Festschrift in Honor of Robert J Elliott, Advances in Statistics, Probability and Actuarial Science, chapter 12, pages 285–302. World Scientific Publishing Company, Singapore, 2012.

- Longstaff [1995] Francis Longstaff. Option pricing and the martingale restriction. Review of Financial Studies, 8(4):1091–1124, 1995.

- Madan and Milne [1994] Dilip B. Madan and Frank Milne. Contingent claims valued and hedged by pricing and investing in a basis. Mathematical Finance, 4(3):223–245, 1994.

- Mazet [1997] O. Mazet. Classification des semi-groupes de diffusion sur associés à une famille de polynômes orthogonaux. In Séminaire de Probabilités XXXI, volume 1655 of Lecture Notes in Mathematics, pages 40–53. Springer, Berlin, 1997.

- Necula et al. [2015] Ciprian Necula, Gabriel Drimus, and Walter Farkas. A general closed form option pricing formula. Swiss Finance Institute Research Paper No. 15-53. Available online at https://ssrn.com/abstract=2210359, 2015.

- Pagès and Printems [2003] Gilles Pagès and Jacques Printems. Optimal quadratic quantization for numerics: The Gaussian case. Monte Carlo Methods and Applications, 9(2):135–165, 2003.

- Revuz and Yor [1999] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion. Grundlehren der mathematischen Wissenchaften A series of comprehensive studies in mathematics. Springer, 1999.

- Rogers and Shi [1995] L Chris G Rogers and Zo Shi. The value of an Asian option. Journal of Applied Probability, 32(4):1077–1088, 1995.

- Rogers and Williams [2000] L.C.G. Rogers and D. Williams. Diffusions, Markov Processes, and Martingales: Volume 1, Foundations. Cambridge Mathematical Library. Cambridge University Press, 2000.

- Xiu [2014] Dacheng Xiu. Hermite polynomial based expansion of european option prices. Journal of Econometrics, 179(2):158–177, 2014.

- Yamada and Watanabe [1971] Toshio Yamada and Shinzo Watanabe. On the uniqueness of solutions of stochastic differential equations. Journal of Mathematics of Kyoto University, 11(1):155–167, 1971.

- Yor [2001] Marc Yor. Bessel processes, Asian options, and perpetuities. In Exponential Functionals of Brownian Motion and Related Processes, pages 63–92. Springer, 2001.