Fundamental properties of solutions to utility maximization problems in wireless networks

Abstract

We introduce a unified framework for the study of the utility and the energy efficiency of solutions to a large class of weighted max-min utility maximization problems in interference-coupled wireless networks. In more detail, given a network utility maximization problem parameterized by a maximum power budget available to network elements, we define two functions that map the power budget to the energy efficiency and to the utility achieved by the solution. Among many interesting properties, we prove that these functions are continuous and monotonic. In addition, we derive bounds revealing that the solutions to utility maximization problems are characterized by a low and a high power regime. In the low power regime, the energy efficiency of the solution can decrease slowly as the power budget increases, and the network utility grows linearly at best. In contrast, in the high power regime, the energy efficiency typically scales as as , and the network utility scales as . We apply the theoretical findings to a novel weighted rate maximization problem involving the joint optimization of the uplink power and the base station assignment.

I Introduction

To cope with the ever increasing rate demand of wireless networks in a cost effective way, system engineers need to improve the energy efficiency, which often translates to increasing the rates for a given power budget. This fact has motivated many studies on trade-offs between achievable rates and energy efficiency for many years [1, 2, 3]. In particular, the field of information theory has been fundamental to reveal bounds that cannot be exceeded irrespective of the available computational power [1, 2]. Unfortunately, extending existing information theoretic results to general wireless networks, while capturing limitations of practical hardware and communication strategies, has been proven notoriously difficult. However, as we show in this study, useful and surprisingly simple performance bounds for a large class of communication strategies in wireless networks are available if we depart from the formal setting of information theory.

In practical wireless systems, the parameters of a network configuration are often obtained by solving optimization problems [4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15]. In particular, it is well-known that many weighted max-min rate or signal-to-interference-plus-noise ratio (SINR) maximization problems can be posed as conditional eigenvalue problems involving nonlinear mappings [4, 8, 9, 10, 11, 12, 13, 14]. The practical implication of this observation is that these maximization problems can be solved with simple iterative fixed point algorithms similar to the standard power method in linear algebra [16, 17]. One of the first studies to establish the connection between nonlinear conditional eigenvalue problems and utility maximization in wireless networks is shown in [4]. Later results appeared in, to cite a few, [8, 9, 10, 11, 12, 13], which considered utility optimization problems assuming different interference models.

Building upon the findings in [4], we start by explicitly stating a canonical problem that is solved in many of the applications addressed in [8, 9, 10, 11, 12, 13, 4]. Unlike these previous studies, which mostly focus on developing efficient numerical solvers or on posing the utility maximization problems as conditional eigenvalue problems, the objective of this study is to derive properties of the solutions to the canonical problem. Particular emphasis is devoted to properties that provide us with highly valuable insights into the energy efficiency and the utility of networks.

In more detail, given the large class of transmission strategies covered by the canonical problem, we can only evaluate the energy efficiency or the utility achieved by the solution after solving the canonical problem with iterative algorithms. This process can be time consuming, so we exploit properties of the solution to conditional eigenvalue problems and results on asymptotic or recession functions in convex analysis [18] to derive simple and useful bounds on the network utility. These bounds are then used to derive novel bounds on the energy efficiency.

The above results reveal interesting phenomena (some already observed in particular interference models [19]) that are common to all network utility maximization problems that can be written in the canonical form shown here. More specifically, the solutions are typically characterized by two power regimes: a low power regime and a high power regime. In both regimes, the network utility and the energy efficiency are always monotonically increasing and non-increasing, respectively, as a function of the power budget available to the transmitters. However, in the low power regime, the energy efficiency is bounded by a constant, and it can decrease slowly as we increase the power budget. In contrast, the network utility is upper bounded by a linear function. In the high power regime, the energy efficiency shows a fast decay because it typically scales as as , whereas gains in network utility saturate because the network utility scales as as (see Sect. II for the definition of ). The bounds derived here do not depend on any unknown constants, so the power budget characterizing the boundary of the power regions is precisely known. In addition, we show that the spectral radius of lower bounding matrices (a concept introduced in [20]) provides us with a formal means of identifying interference limited networks, which we define as networks for which the utility cannot grow unboundedly as the power budget diverges to infinity. We also use the concept of recession functions in convex analysis to characterize networks for which the utility can grow unboundedly with increasing power budget, and we call these networks noise limited networks.

We illustrate the above theoretical findings in a novel joint uplink power control and base station assignment problem for weighted rate maximization. This application is related to that in [12], but here we use results shown in [21], which have been independently obtained in [22, 23] in the context of load coupled interference models, to pose the optimization problem in terms of achievable rates instead of the SINR. As a result, we work directly with the variables of interest to system designers (in contrast, note that maximizing the SINR is only an indirect approach to the problem of improving the rates). We emphasize that solving weighted rate maximization problems by choosing appropriate coefficients for weighted SINR maximization problems may not be straightforward because the bijective relation between rate and SINR used in many studies is not affine. One interesting consequence of our novel formulation is that the simple solver based on the fixed point algorithm in [16, 17] becomes readily available. Furthermore, this application exemplifies the validity of the theoretical findings with interference models based on concave mappings that are neither affine nor differentiable.

This study is structured as follows. In Sect. II we review definitions and known mathematical tools that are extensively used to prove the main results in this study. In Sect. III we introduce a new framework for the study of the energy efficiency and the achievable utility of solutions to a large class of network utility maximization problems. The general results obtained in Sect. III are illustrated with a concrete application in Sect. IV.

II Preliminaries

The intention of this section is twofold. First, we try to make this study as self-contained as possible by presenting many standard definitions and results that are essential for the proofs in the next sections. Second, we clarify much of the notation used throughout this study. We note that much of the background material collected here has been taken directly from [20, 8]. In this section, we also show the first (minor) technical result (Proposition 1).

In more detail, for given , the inequality should be understood as a entry-wise inequality. The transpose of vectors or matrices is denoted by . The sets and are the sets of non-negative reals and positive reals, respectively. The spectral radius of a matrix is denoted by . The effective domain of a function is . Given two functions and we say that scales as when (or, in set notation, as ) if

If is a constant function, then we use the convention .

We use the notation to indicate the convex hull of ; i.e., the smallest convex subset of containing [24, p. 43]. The interior of is the set given by [24, p. 90], where is the closed ball centered at with radius and is the standard Euclidean norm. A set is said to be downward comprehensible on if [7, p. 30]. A convex set is symmetric if implies , and it is called a convex body if it is a compact convex set with nonempty interior [25, Ch. 1].

We say that a mapping is concave if

As shown below, positive concave mappings are instances of standard interference functions, which are functions with many applications in wireless networks [26]. A simple proof of the following fact can be seen in [20], among other studies.

Fact 1

Let be a concave mapping. Then each of the following holds:

-

1.

(Scalability) () .

-

2.

(Monotonicity) .

In the next section, we extensively exploit the close connection between a large class of utility maximization problems in wireless networks and conditional eigenvalues of concave mappings. Before stating the conditional eigenvalue problem, we introduce the definition of monotone norms used in [17, 16], and we refer the reader to [27] for nonequivalent notions of monotonicity that are also common in the literature.

Definition 1

(Monotone norm) A norm on is said to be monotone if

Note that the widely used norms, , are monotone in the sense of Definition 1.

Fact 2

([28, Ch. 13.5] Equivalence of norms in finite dimensional spaces) Let and be arbitrary norms defined on . Then .

Recall that a sequence is said to converge to if the sequence converges to zero (by Fact 2, the convergence holds for any choice of the norm ). In this case, we write . We can now formally introduce the conditional eigenvalue problem and a simple iterative solver:

Fact 3

([16, 17]) Let be a concave mapping and a monotone norm. Then each of the following holds:

-

1.

There exists a unique solution to the conditional eigenvalue problem

Problem 1

Find such that and .

For reference, the scalar is said to be the conditional eigenvalue of for the norm .

-

2.

The sequence generated by

(1) converges geometrically to the uniquely existing vector , which is also the vector of the tuple that solves Problem 1. Furthermore, the sequence satisfies .

To find a simple lower bound for the conditional eigenvalue of a concave mapping for any monotone norm, we can use the concept of lower bounding matrices introduced in [20].

Definition 2

([20] Lower bounding matrices) Let be a continuous concave mapping, and denote by the continuous concave functions such that for every . The lower bounding matrix of the mapping is the matrix with its th row and th column given by111See [20, Example 1] for an alternative and equivalent construction method based on supergradients.

| (2) |

where the limit can be shown to exist and () is the unit vector with all components being zero, except for the th component, which is equal to one.

Lower bounding matrices are at the heart of many of the results in this study because of the next result:

Fact 4

By considering Definition 3 below, we can observe the strong connection between (2) and the concept of recession or asymptotic functions in convex analysis, which we use to study the behavior of networks in the high power regime.

Definition 3

(Recession or asymptotic functions [18, Ch. 2.5]) Let be upper semicontinuous, proper, and concave. We define its recession or asymptotic function at the function given by

The above limit can be more conveniently calculated by using [18, Corollary 2.5.3]

| (3) |

and the equality in (3) is valid for every if . We also recall that asymptotic functions are positively homogeneous [18, Proposition 2.5.1(a)].

We end this section with a simple result that is later used for the analysis of the energy efficiency.

Proposition 1

Let be an arbitrary norm and an arbitrary continuous concave mapping. Then the following holds:

Proof.

Fix arbitrarily. Denote by the continuous concave functions such that for every , and note that, for each , the function is also concave. Now choose arbitrarily. By [24, Corollary 16.15], we know that , where is the superdifferential of the concave function at . For each , choose an arbitrary tuple satisfying , and define . The definition of the superdifferential and the fact that (because is positive and concave; see, e.g., [20, Lemma 1.1]) for every shows that

| (4) |

Let satisfy and , where , , and is an arbitrary monotone norm. By (4), the monotonicity of the norm , and the triangle inequality, we deduce

Since norms are equivalent in finite dimensional spaces (Fact 2), we obtain

which completes the proof as is arbitrary. ∎

III Proposed framework

III-A The canonical utility maximization problem

In this study, we are interested in utility maximization problems that can be posed in the following canonical form:

Problem 2

(Canonical form of the network utility maximization problem)

| (9) |

where is a design parameter hereafter called power budget, is an arbitrary monotone norm, and is an arbitrary continuous concave mapping called interference mapping in this study.

Following standard terminology, we say that a tuple is feasible to Problem 2 if it satisfies all constraints in (9). The set of all feasible tuples is defined to be the feasible set. If a feasible tuple is also a solution to Problem 2, then we say that this tuple is optimal.

Problem 2 can be seen as a particular instance of that addressed in [4] (see [21, 29, 30] for other notable extensions). However, Problem 2 already covers a large array of network utility optimization problems, and, as we show below, its solution has a rich structure that, to the best of our knowledge, we explore for the first time here. Particular instances of Problem 2 include max-min rate optimization in load coupled networks [8], the joint optimization of the uplink power and the cell assignment [12], the optimization of the uplink receive beamforming [7, Sect. 1.4.2], and many of the applications described in [21, 29, 30]. Later in Sect. IV we show a novel weighted rate maximization problem that is also an instance of Problem 2.

Typically, in network utility maximization problems written in the canonical form shown above, the optimization variable corresponds to the transmit power of network elements (e.g., base stations or user equipment); the optimization variable , hereafter called utility, is the common desired rate, or, depending on the problem formulation, the common SINR of all users; the norm is chosen based on the energy source of the network elements (e.g., we can use the norm if all networks elements share the same source, or the norm if the network elements have independent sources); and is a known mapping that captures the interference coupling among network elements. In particular, the mapping is constructed with information about many environmental and control parameters such as the pathgains, MIMO beamforming techniques, the user-base station assignment mechanisms, and the system bandwidth, to name a few. For concreteness, in the next sections we use the above interpretation of the optimization variables to explain in words the implications of the main results in this study.

In the next proposition, we show that the seemingly simple power constraints in Problem 2 are equivalent to a rich class of constraints commonly found in applications in wireless networks. The next result is also useful to identify utility optimization problems that cannot be addressed with the formulation in Problem 2, in which case approaches such as those described in [30] should be considered.

Proposition 2

Let be a compact convex set with nonempty interior. Assume that is also downward comprehensible, and define , where . Then the gauge function or Minkowski functional of [25, Ch. 2][18, Corollary 2.5.6], denoted by

| (10) |

for all , is a monotone norm. Furthermore, we have

| (11) |

Conversely, given an arbitrary monotone norm , the set is a compact convex set that is downward comprehensible on . Furthermore, has nonempty interior.

Proof.

First note that the set is compact with nonempty interior because it is the convex hull of a compact set with nonempty interior in a finite dimensional space. It is also symmetric by construction, so is a symmetric convex body. Therefore, by [25, Proposition 2.1], the function in (10) defines a norm on , and can be equivalently expressed as the unit ball (see also [18, Corollary 2.5.6]). We now proceed to show that this norm is monotone and that ; i.e., given , the operation does not remove or add any vectors to the nonnegative orthant.

It is clear that implies . We now prove that implies . As a consequence of [24, Proposition 3.4], any vector can be written as

where , , , , , , and . Since is a non-negative vector and , we deduce

Therefore, is a convex combination of points in and . Since is a convex and downward comprehensible set, we have both and . Combining everything, we verify that if and only if . Since we have already proved that is the unity ball with the norm , the result also implies (11). Moreover, by (10), we can write

| (12) |

The monotonicity of the norm in (10) follows from (12) and the fact that, if satisfies for some , then we have by downward comprehensibility of .

We now proceed to prove the converse. Let be a monotone norm. By using standard arguments in convex analysis, we know that is a compact convex set with nonempty interior. We omit the details for brevity. Furthermore, by monotonicity of the norm, we have , which implies and concludes the proof that is downward comprehensible on .

∎

A practical implication of Proposition 2 is that, if we are given power constraints of the form for possibly nonlinear and nondifferentiable convex functions , …, , and if satisfies the assumptions of the proposition, then we can equivalently represent these constraints by a monotone norm that can be computed as in (10). If the norm in (10) is not easy to obtain in closed form, but we can easily verify whether a given point satisfies , then the norm can be evaluated numerically by using the simple techniques described in [30, Algorithm 2,Algorithm 3] (e.g., the bisection algorithm). Therefore, we can construct the sequence described in (1), and, as we show below, the simple fixed point algorithm in (1) with the monotone norm , where , solves Problem 2: 222As already mentioned in the Introduction, the focus of this study is on obtaining a deep understanding of properties of the solution to Problem 2, and not on the development of algorithmic solutions, which has been the focus of previous work.

Fact 5

For reference, we call the functions and in Fact 5.2 the utility and power functions, respectively. Uniqueness of the solution to Problem 2 also enables us to define a notion of energy efficiency (utility over power) as follows:

Definition 4

(-energy efficiency function) Let and be, respectively, the utility and power functions. By assuming that is a monotone norm, the -energy efficiency function is given by , or, equivalently, , which is an immediate consequence of Fact 5.1.

Example 1

If the monotone norm is selected as the norm for a utility maximization problem in which is a vector of transmit power of base stations (in Watts) and the utility is the common rate achieved by users (in bits/second), then shows how many bits each user receives for each Joule spent by a network optimized for the power budget . See [8] for an example of a network utility maximization problem with variables having this interpretation.

With the above definitions, we now proceed to study properties of the functions , , and . The results in the following sections establish the main contribution of this study.

III-B Monotonicity and continuity of the power, utility, and energy efficiency functions

Fact 5 shows that the utility and power functions are (coordinate-wise) increasing. However, as we show below, the transmit power always grows faster than the utility.

Lemma 1

The -energy efficiency function in Definition 4 is non-increasing; i.e.,

Proof.

The following proposition establishes the continuity of the power, utility, and energy efficiency functions.

Proposition 3

Let be an arbitrary sequence of power budgets converging to an arbitrary scalar . Then the power function , the utility function , and the -energy efficiency function satisfy the following:

-

(i)

;

-

(ii)

; and

-

(iii)

.

Proof.

To simplify the notation in the proof, we define for every and .

(i) The sequence is bounded because it converges, so is also bounded because for every (see Fact 5). Therefore, by [24, Lemma 2.38] and [24, Lemma 2.41(ii)] (see also [18, Sect. 2.1]), follows if we show that is the only accumulation point of the bounded sequence .

By the equivalence of norms in finite dimensional spaces, there exists a constant such that for every . Let be an arbitrary accumulation point of . As a consequence of [28, Theorem 6.7.2], we can extract from a subsequence , , converging to . By Fact 5, the definition of the scalar , and monotonicity of concave mappings (Fact 1.2), we have

| (13) |

Therefore, (13) and monotonicity of the norms and yield

| (14) |

The above inequalities show that the sequence is bounded, so we can use the Bolzano-Weierstrass theorem to conclude that there is a subsequence , , converging to a scalar . From (14), we also know that . As a result, from the continuity of the mapping , , and (13),

| (15) |

and, from continuity of norms and (13),

| (16) |

By (15) and (16) the tuple is a solution to the conditional eigenvalue problem associated with the mapping . Hence, by Fact 5.1, is the unique solution to Problem 2 with the power budget . As a result, we have , which by uniqueness of shows that converges to .

(ii) By Fact 1.2 and monotonicity of , the inequalities hold for every . Since and by Fact 5.1, we use (i) and continuity of to obtain .

(iii) As shown above, we have for every , so for every . Therefore, (i) and continuity of the mapping yield

which completes the proof. ∎

III-C Bounds on the utility

Fact 5.2 shows that the utility (e.g., rates) increases by increasing the power budget available to transmitters. However, in the next proposition we verify that the possible gain in utility is limited in general.333One of the inequalities in Proposition 4 has already appeared in [8]. However, that study considered only the norm and a very particular max-min utility maximization problem in load coupled networks. The next proposition also derives a conservative lower bound for the utility function. The bounds shown below are useful for a quick evaluation of the network performance for different values of the power budget .

Proposition 4

Consider the assumptions and definitions in Problem 2, and denote by the lower bounding matrix of the interference mapping . Let be the utility function in Definition 4. Then each of the following holds:

-

(i)

(Upper bound)

Furthermore, if , then we also have

-

(ii)

(Combined upper bound) Assume that , then

where .

-

(iii)

(Lower bound) Let be an arbitrary scalar satisfying for every (see Fact 2). Then

(17) -

(iv)

(Asymptotic lower bound) Denote by the concave function given by th component of the interference mapping ; i.e., for every . Let be as in part (iii) of the proposition, and define , where is the asymptotic function of for (see Definition 3). Then we have

(18)

Proof.

In this proof, we use the standard notation for the power function in Definition 4.

(i) Define by the monotone norm for a given power budget . By Fact 5.1, we have

| (19) |

Now, monotonicity of both the norm and the mapping (Fact 1.2) yields

Hence . Now assume that , in which case immediately follows from (19) and Fact 4.

(ii) Immediate from the two inequalities in (i).

A possible application of Proposition 4 is to identify noise limited networks and interference limited networks with a precise mathematical statement. More specifically, assume that we have a max-min fairness problem that can be posed in the canonical form in (9). For this problem, if in Proposition 4(iii) is infinity, then any utility (e.g., rate) is achievable if the power budget is sufficiently large. In contrast, if the lower bounding matrix of the interference mapping satisfies , then Proposition 4(i) shows that the utility cannot grow unboundedly. In other words, interference cannot be overcome by increasing the power budget. As expected, the assumption is typically satisfied in network optimization problems with links directly or indirectly coupled by interference; i.e., changes in the power of any link has influence on the interference received by any other link in the network. If links are not coupled, then we usually have (which also implies ), and in this case the utility can be as large as desired by using a sufficiently large power budget.

III-D Bounds on the energy efficiency

We now proceed to derive bounds on the energy efficiency as a function of the power budget .

Proposition 5

Let be the -energy efficiency function in Definition 4. Then we have the following.

-

(i)

(Lower bound) Let be an arbitrary scalar satisfying for every , and an arbitrary scalar satisfying for every (see Fact 2). Then

(21) -

(ii)

(Upper bound) Assume that , where is the lower bounding matrix of the interference mapping . Then

(22) where is an arbitrary scalar satisfying for every .

-

(iii)

(Maximum energy efficiency)

(23) -

(iv)

(Combined upper bound) Let be as in (ii). Then

where .

Proof.

(i) Divide both sides of (17) by and use to obtain the sought lower bound

(ii) Recall that by Fact 5.1 for every . Since by assumption, it follows from Proposition 4(i) that . Therefore,

which concludes the proof of the upper bound.

(iii) Existence of the limit and the equality is immediate from non-negativity of and Lemma 1. To obtain the value of the limit, denote by and the utility and power functions, respectively. Let be an arbitrary sequence satisfying , and let the sequence of tuples be given by for every . Since , we have . Recalling that is continuous by assumption and that norms are continuous, we obtain:

which implies (23).

(iv) Immediate from (ii) and (iii). ∎

III-E Asymptotic behavior of the utility and the energy efficiency functions

With the results obtained in the previous subsections, we have all the ingredients necessary to study the behavior of the utility and energy efficiency functions as . We start by studying the utility function.

Corollary 1

Assume that the lower bounding matrix of the concave mapping in Problem 2 satisfies . Then as .

Proof.

The next example shows that known results in the literature [6, Ch. 5] are particular cases of the upper bound in Proposition 4(ii). In addition, this example proves that the upper bound for the utility (assuming ) is asymptotically sharp for an important class of interference mappings that are common in max-min fairness problems in wireless networks [6].

Example 2

Let be arbitrary and assume that is a matrix satisfying . Now consider Problem 2 with the affine interference mapping , and note that the lower bounding matrix of is the matrix . The results in [6, Theorems A.16 and A.51] show that, for any , the vector is strictly positive, where we define . Therefore, given the power budget , we have . Fact 5.1 now shows that the tuple is the solution to Problem 2 with the power budget . This result proves that any utility strictly smaller than can be achieved for the affine interference mappings considered in this example, provided that the power budget is large enough. More precisely, Fact 5.2 shows that

| (24) |

where is the utility function in Definition 4.

Scaling properties of the energy efficiency function are shown in the next corollary.

Corollary 2

Let be the lower bounding matrix of the interference mapping in Problem 2. The -energy efficiency function has the following properties:

-

(i)

The limit exists and . Furthermore, if , then .

-

(ii)

Assume that , then

-

(iii)

With the assumption in (ii), we also have as .

Proof.

We can also show that the upper bound in Proposition 5(ii) is as sharp as possible, in the sense that, if we consider all positive concave mappings , there are mappings for which the upper bound is achieved asymptotically as the power budget diverges to infinity:

Example 3

Consider the model and definitions in Example 2. Recalling that for every by Fact 5.1, where is the power function in Definition 4, we deduce from (24):

where is the -energy efficiency function in Definition 4. In words, the above proves that the -energy efficiency function can be made arbitrarily close to the upper bound in Proposition 5(ii) with the choice for a sufficiently large power budget .

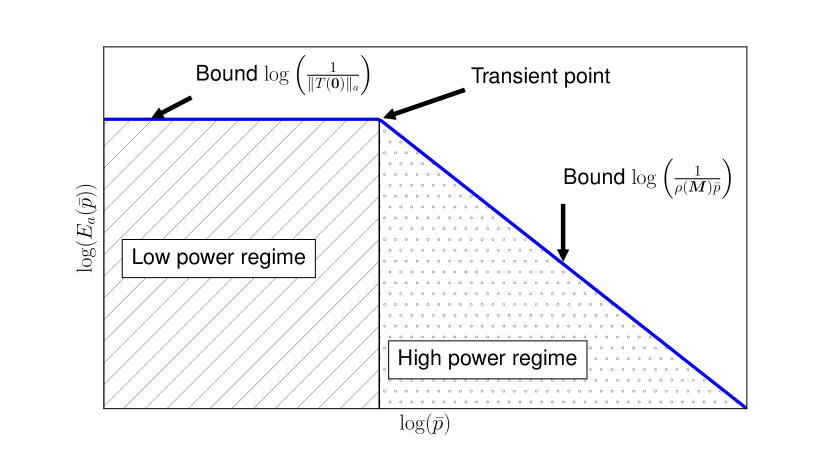

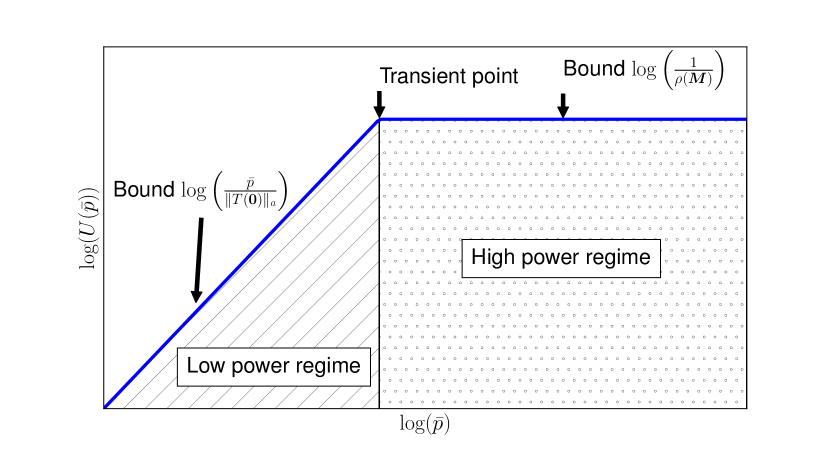

III-F Discussion - Power regimes in network utility maximization problems

The upper bound in Proposition 4(ii) motivates the definition of two power regimes: a low power regime (), where the linear bound in Proposition 4(ii) is effective, and a high power regime (), where the constant bound in Proposition 4(ii) is effective. The transition between these two regimes happens at the transient point . For convenience, let us focus for the moment on the -energy efficiency function in Definition 4, which we denote by . In the low power regime, by (23), we verify that as , hence the decay in energy efficiency as increases can be small. In contrast, the utility increases at best linearly in this power regime (see Proposition 4(ii)). These observations show that we should transmit with low power and low utility (e.g., rates) if high transmit energy efficiency is desired, and we emphasize that we have proved this expected result by using a very general model that unifies, within a single framework, the behavior of a large array of transmission technologies in wireless networks.

In the high power regime, the energy efficiency eventually decays quickly as the power budget diverges to infinity because as , while gains in utility eventually saturate because of the uniform bound . The above observations are illustrated in Fig. 1. Note that the -energy efficiency function is continuous, converges to the upper bound as the power budget decreases to zero, and decreases within the hatched areas corresponding to the power regimes. Furthermore, the utility function is also continuous, converges to zero as the power budget decreases to zero, and increases within the hatched areas corresponding to the power regimes.

Interestingly, the above properties of the energy efficiency and the utility hold for all network utility maximization problems that can be posed in the canonical form in (9). Equipping the network with advanced communication technologies such as massive multi-antenna transmission schemes, transmitter and receiver beamforming techniques, intelligent user-base station assignment mechanisms, or a combination of all these technologies can only change the position of the transient point and move upwards the bounds on the energy efficiency and the utility. However, if , these two power regimes are always present.

IV Exemplary application

We now illustrate the results obtained in the previous section with a concrete application; namely, a novel joint power control and base station allocation problem for weighted rate maximization.

IV-A System model and the proposed algorithm

Denote by and by the set of base stations and the set of users, respectively, in a network. The pathloss between base station and user is indicated by the variable . Let be the uplink power vector, where is the uplink transmit power of user . The SINR of user if connected to base station for a given power allocation is given by

We assume that users connect to their best serving base stations and that each user is equipped with a single-user decoder that treats interference as noise. With these assumptions, the achievable rate of user for a given power allocation under Gaussian noise is commonly approximated by , where is the system bandwidth.

The utility maximization problem we solve in this section, which we refer to as the weighted rate allocation problem, is formally stated as:

Problem 4

(The weighted rate allocation problem)

| (29) |

where is the weight or priority assigned to the rate of user .

To gain intuition on the weights , we now relate two particular choices to traditional network utility maximization problems. The simplest choice is the use of uniform weights for every , in which case the solution to Problem 4 can be shown to maximize the minimum observed rate in the network (max-min fairness). As a second example of a weighting scheme related to that used later in the simulations, for a fixed power , we can use for every . With this choice, is simply the best rate that each user can achieve if alone in the system and transmitting at full power . In particular, if , then the solution to Problem 4 allocates to each user the fraction of its best individual achievable rate . The number is the largest fraction common to all users that the network can support.

We now proceed to state Problem 4 in the canonical form in (9). For any , , and satisfying the first constraint in (29), we have

which shows that the first constraint in Problem 4 can be equivalently written as

| (30) |

where and

for every .

For fixed , we know by [21, 22][23, Lemma 2] that as a function of is concave444After the submission of the first version of the manuscript, one of the reviewers pointed out that [21] is possibly the first study to show that this function is concave. The studies in [22, 23] show all formal details of the continuous extension of this function to the boundary of the domain. This continuous extension is crucial to the bounds we derive because the mapping in Problem 2 is assumed to be continuous. It is also worth mentioning that the function is known to be log-log concave [31], a property that has already been exploited for many years to solve utility maximization problems without using common simplifications such as those based on the high SINR assumption considered in [32], for example. for every , hence is also concave for every because it is the minimum of concave functions [24, Proposition 8.14]. Therefore, by replacing the rate constraint in Problem 4 by the constraint in (30), we have Problem 4 in the canonical form in (9), except that the domain of the mapping must be extended to include the boundary . By [33, Theorem 10.3], we know that each function , , has one and only one continuous extension to , and by following similar arguments to those used in the proof of [23, Lemma 3], the continuous extension of the mapping is given by

| (31) |

where

for every .

The above discussion shows that the weighted rate allocation problem is equivalent to the following problem in the canonical form:

Problem 5

where in the application under consideration the mapping is given by (31), and we assume that . In light of Fact 5.1, we can now use the simple iterative scheme in (1) with the monotone norm to solve Problem 4. Furthermore, all bounds derived in Sect. III are available because the continuous mapping is defined at . Once a solution is obtained, we recover an optimal user-base station assignment by connecting each user to any base station providing the best SINR .

Note that the component of the th column and th row of the lower bounding matrix of the interference mapping in (31) is given by

With the assumption for every and , we observe that is irreducible [6, Sect. A.4.1] because only the diagonal terms of the non-negative matrix are zero. Therefore, we conclude that because the spectral radius of an arbitrary irreducible matrix is positive [34, p. 673]. The practical implication of this fact is that, by Proposition 4, the network considered here is interference limited because the rates cannot grow unboundedly by increasing the power budget.

The bounds in Proposition 4 and Proposition 5 can also provide us with intuition on optimal assignment strategies in the low power regime. For example, Proposition 5 shows that the energy efficiency function, which is continuous, converges to as the power budget decreases to zero. The th component of the vector is by definition, which shows that, as the power budget decreases to zero, each user selects the base station with the smallest ratio . If the noise power is the same at every base station , then we obtain the intuitive result that each user selects the base station with the best propagation condition, which is the expected result in a regime where noise dominates interference. Note that this result is valid for any choice of positive weights .

IV-B Simulations

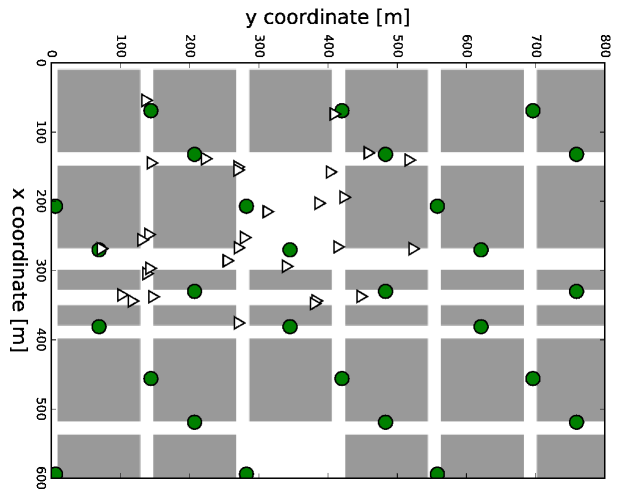

The simulations in this section are based on the “dense urban information society” scenario provided by the METIS project [35, Sect. 4.2][36], which is depicted in Fig. 2. For simplicity, we only use the microcells of that scenario. The pathloss between users and microcells are obtained from the lookup tables available at [36]. For the simulation, we place 30 users uniformly at random on the streets or the park within the box region and of the network in Fig. 2. Users are free to connect to any microcell in the whole region. The noise power spectral density at every base station is dBm/Hz, and the total system bandwidth is MHz.

The user priorities to build the concave mapping in (31) are assigned as follows. We first compute the interference-free rate of each user when transmitting at W; i.e., . We then use the weight vector , where . With this normalization, the solution to Problem 5 has the following interpretation. The utility is the highest rate observed in the network, and the weight is the fraction of this maximum rate that is assigned to user . As described above, for , all users transmit with the same fraction of the rates they could achieve if alone in the system.

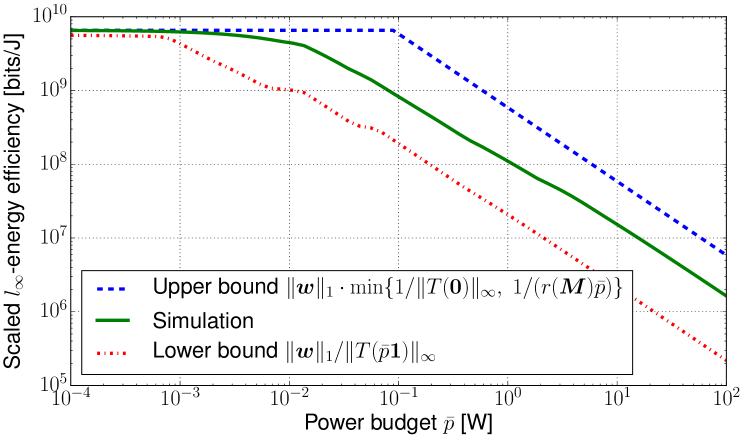

The above discussion shows that the sum throughput of the network is . To evaluate the energy efficiency of the solution to Problem 5 with these settings, for given power budget , we use the -energy function scaled by ; i.e., we use , where is the -energy efficiency function. This scaled version of the -energy efficiency, which has dimension bits/Joule, shows the ratio between the sum throughput in the network and the maximum observed transmit power of a user. (We could use also the -energy efficiency, in which case the energy efficiency is the rate achieved by a user for given total transmit power in the network.)

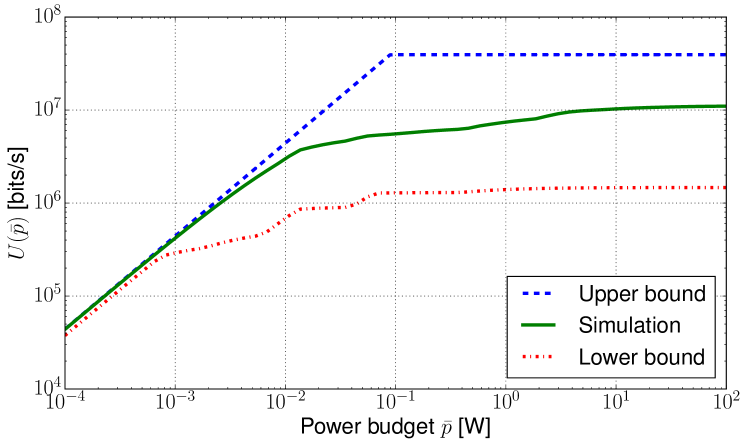

We approximate the solution to Problem 5 by applying 5,000 iterations of the fixed point algorithm in (1) with the mapping in (31). The starting power allocation of the iterations is . Fig. 3 and Fig. 4 show the energy efficiency and the utility (i.e., the rates) obtained with the simulation. For the bounds in Proposition 5, we use . We can see that the results are consistent with the analysis in Sect. III. Even with a nonlinear mapping such as that in (31), we can clearly identify the two power regimes described in Sect. III-F. In particular, with a power budget above , which characterizes the high power regime, we note that increasing the power budget by orders of magnitude improves the achievable rates only marginally. We also observe a gap in the rate and energy efficiency bounds in the high SINR regime, which is expected because in this regime the bounds derived here are not necessarily asymptotically sharp for utility maximization problems with arbitrary interference mappings.

V Summary and conclusions

We have proved that the energy efficiency and the utility (e.g., rates or SINR) of solutions to a large class of network utility maximization problems are continuous and monotonic as a function of the power budget available to the network. Furthermore, we used the concept of lower bounding matrices introduced in [20], or, more generally, the concept of asymptotic or recession functions in convex analysis [18], to derive simple upper and lower bounds for the energy efficiency and for the network utility. In particular, the upper bounds reveal that the solutions are characterized by a low power regime and a high power regime, and the transition point is precisely known. In the low power regime, the upper bounds are asymptotically sharp (i.e., as the power budget tends to zero). The energy efficiency can decrease slowly as the power budget increases, whereas the utility grows linearly at best as a function of the power budget. In the high power regime, the typical behavior of interference-limited networks is that there are marginal gains in network utility and a fast decrease in energy efficiency as the power budget tends to infinity. In addition, the upper bounds we derived here are asymptotically sharp as the power budget diverges to infinity for the important family of network utility maximization problems constructed with affine interference mappings.

The general theory developed here was illustrated with a novel joint uplink power control and base station assignment problem for weighted rate allocation. One of the main advantages of the formulation is that it works directly with the rate of users, which is the parameter that network engineers are typically interested in maximizing. We showed that this problem can be solved optimally with an existing iterative method that, from a mathematical perspective, is nothing but a fixed point algorithm that solves a conditional eigenvalue problem. In this application, simulations show that the bounds are particularly good in the low power regime, and they are within the same order of magnitude of the optimal values in the high power regime. Therefore, the bounds derived here can serve as a simple estimate of the limits of a given network configuration. This fact can be especially useful in planning tasks that require the evaluation of multiple candidate configurations. With the bounds derived here, many inefficient configurations can be quickly ruled out without solving optimization problems.

References

- [1] R. G. Gallager, “Energy limited channels: Coding, multi-access and spread spectrum,” in Proc. Conference on Information Sciences and Systems (CISS), Mar 1988, p. 372.

- [2] S. Verdu, “Recent results on the capacity of wideband channels in the low-power regime,” IEEE Wireless Commun. Mag., vol. 9, pp. 40–45, August 2002.

- [3] R. L. G. Cavalcante, S. Stańczak, M. Schubert, A. Eisenbläter, and U. Türke, “Toward energy-efficient 5G wireless communication technologies,” IEEE Signal Processing Mag., vol. 31, no. 6, pp. 24–34, Nov. 2014.

- [4] C. J. Nuzman, “Contraction approach to power control, with non-monotonic applications,” in IEEE GLOBECOM 2007-IEEE Global Telecommunications Conference. IEEE, 2007, pp. 5283–5287.

- [5] M. Chiang, P. Hande, T. Lan, and C. W. Tan, “Power control in wireless cellular networks,” Foundations and Trends® in Networking, vol. 2, no. 4, pp. 381–533, 2008.

- [6] S. Stańczak, M. Wiczanowski, and H. Boche, Fundamentals of Resource Allocation in Wireless Networks, 2nd ed., ser. Foundations in Signal Processing, Communications and Networking, W. Utschick, H. Boche, and R. Mathar, Eds. Berlin Heidelberg: Springer, 2009.

- [7] M. Schubert and H. Boche, Interference Calculus - A General Framework for Interference Management and Network Utility Optimization. Berlin: Springer, 2011.

- [8] R. L. G. Cavalcante, M. Kasparick, and S. Stańczak, “Max-min utility optimization in load coupled interference networks,” IEEE Trans. Wireless Commun., vol. 16, no. 2, pp. 705–716, Feb. 2017.

- [9] D. W. Cai, T. Q. Quek, and C. W. Tan, “A unified analysis of max-min weighted SINR for MIMO downlink system,” IEEE Trans. Signal Processing, vol. 59, no. 8, pp. 3850–3862, 2011.

- [10] D. W. Cai, T. Q. Quek, C. W. Tan, and S. H. Low, “Max-min SINR coordinated multipoint downlink transmission - duality and algorithms,” IEEE Trans. Signal Processing, vol. 60, no. 10, pp. 5384–5395, 2012.

- [11] Y. Huang, C. W. Tan, and B. Rao, “Joint beamforming and power control in coordinated multicell: Max-min duality, effective network and large system transition,” IEEE Trans. Wireless Commun., vol. 12, no. 6, pp. 2730–2742, 2013.

- [12] R. Sun and Z.-Q. Luo, “Globally optimal joint uplink base station association and power control for max-min fairness,” in IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), 2014, pp. 454–458.

- [13] Y.-W. P. Hong, C. W. Tan, L. Zheng, C.-L. Hsieh, and C.-H. Lee, “A unified framework for wireless max-min utility optimization with general monotonic constraints,” in IEEE INFOCOM, 2014, pp. 2076–2084.

- [14] C. W. Tan, “Optimal power control in rayleigh-fading heterogeneous wireless networks,” IEEE/ACM Transactions on Networking, vol. 24, no. 2, pp. 940–953, 2016.

- [15] G. J. Foschini and Z. Miljanic, “A simple distributed autonomous power control algorithm and its convergence,” IEEE transactions on vehicular Technology, vol. 42, no. 4, pp. 641–646, 1993.

- [16] U. Krause, “Perron’s stability theorem for non-linear mappings,” Journal of Mathematical Economics, vol. 15, no. 3, pp. 275–282, 1986.

- [17] ——, “Concave Perron–Frobenius theory and applications,” Nonlinear Analysis: Theory, Methods & Applications, vol. 47, no. 3, pp. 1457–1466, 2001.

- [18] A. Auslender and M. Teboulle, Asymptotic Cones and Functions in Optimization and Variational Inequalities. New York: Springer, 2003.

- [19] B. Song, R. L. Cruz, and B. D. Rao, “Network duality for multiuser MIMO beamforming networks and applications,” IEEE Transactions on Communications, vol. 55, no. 3, pp. 618–630, 2007.

- [20] R. L. G. Cavalcante, Y. Shen, and S. Stańczak, “Elementary properties of positive concave mappings with applications to network planning and optimization,” IEEE Trans. Signal Processing, vol. 64, no. 7, pp. 1774–1873, April 2016.

- [21] D. W. Cai, C. W. Tan, and S. H. Low, “Optimal max-min fairness rate control in wireless networks: Perron-frobenius characterization and algorithms,” in INFOCOM, 2012 Proceedings IEEE. IEEE, 2012, pp. 648–656.

- [22] R. L. G. Cavalcante, E. Pollakis, and S. Stanczak, “Power estimation in LTE systems with the general framework of standard interference mappings,” in IEEE Global Conference on Signal and Information Processing (GlobalSIP’ 14), Dec. 2014.

- [23] R. L. G. Cavalcante, S. Stańczak, J. Zhang, and H. Zhuang, “Low complexity iterative algorithms for power estimation in ultra-dense load coupled networks,” IEEE Trans. Signal Processing, vol. 7, no. 22, pp. 6058–6070, Nov. 2016.

- [24] H. H. Bauschke and P. L. Combettes, Convex Analysis and Monotone Operator Theory in Hilbert Spaces. Springer, 2011.

- [25] R. Vershynin, “Lectures in geometric functional analysis,” unpublished manuscript, available at http: // www-personal. umich. edu/ romanv/papers/GFA-book/GFA-book.pdf, 2011.

- [26] R. D. Yates, “A framework for uplink power control in cellular radio systems,” IEEE J. Select. Areas Commun., vol. 13, no. 7, pp. pp. 1341–1348, Sept. 1995.

- [27] C. R. Johnson and P. Nylen, “Monotonicity properties of norms,” Linear Algebra and its Applications, vol. 148, pp. 43–58, 1991.

- [28] M. Searcoíd, Metric Spaces. London: Springer, 2007.

- [29] C. W. Tan, “Wireless network optimization by perron-frobenius theory.” Now Publishers Inc, 2015.

- [30] L. Zheng, Y.-W. P. Hong, C. W. Tan, C.-L. Hsieh, and C.-H. Lee, “Wireless max–min utility fairness with general monotonic constraints by perron–frobenius theory,” IEEE Transactions on Information Theory, vol. 62, no. 12, pp. 7283–7298, 2016.

- [31] J. Papandriopoulos, S. Dey, and J. Evans, “Optimal and distributed protocols for cross-layer design of physical and transport layers in MANETs,” IEEE/ACM Transactions on Networking (TON), vol. 16, no. 6, pp. 1392–1405, 2008.

- [32] M. Chiang, “Balancing transport and physical layers in wireless multihop networks: Jointly optimal congestion control and power control,” Selected Areas in Communications, IEEE Journal on, vol. 23, no. 1, pp. 104–116, 2005.

- [33] R. T. Rockafellar, Convex analysis. Princeton university press, 1970.

- [34] C. D. Meyer, Matrix Analysis and Applied Linear Algebra. USA: SIAM, 2000.

- [35] P. Agyapong, V. Braun, M. Fallgren, A. Gouraud, M. Hessler, S. Jeux, A. Klein, J. Lianghai, D. Martín-Sacristán, M. Maternia, M. Moisio, J. F. Monserrat, K. Pawlak, H. Tullberg, and A. Weber, “Deliverable D6.1 - simulation guidelines,” Mobile and wireless communications Enablers for the Twenty-twenty Information Society (METIS), Tech. Rep., Oct. 2013.

- [36] “METIS ray tracing files,” accessed on 20.03.2015. [Online]. Available: https://www.metis2020.com/documents/simulations/