Approximate pricing of European and Barrier claims in a local-stochastic volatility setting

Abstract

We derive asymptotic expansions for the prices of a variety of European and barrier-style claims in a general local-stochastic volatility setting. Our method combines Taylor series expansions of the diffusion coefficients with an expansion in the correlation parameter between the underlying asset and volatility process. Rigorous accuracy results are provided for European-style claims. For barrier-style claims, we include several numerical examples to illustrate the accuracy and versatility of our approximations.

1 Introduction

Barrier-style claims are among the most liquid path-dependent claims. As barrier-style claims are generally cheaper than their European counterparts, the former are popular among speculators who wish to bet on market movements while taking advantage of the lower prices barrier-style claims entail. Yet, despite their widespread use, barrier-style claims remain challenging to price.

In his landmark work, Merton (1973) was the first to value a down-and-out call in closed form when the underlying stock follows geometric Brownian motion (GBM). There exists a variety of static hedging results for barrier claims in GBM or GBM-like settings. For example, in a GBM framework, Bowie and Carr (1994) show that the payoff of a down-and-out call with barrier can be replicated by buying a European call on the same underlying futures price with the same maturity and strike and also selling puts with strike . Carr et al. (1998) prove that this static hedge works in any model with local volatility, provided that the volatility function is symmetric in the log of the futures price relative to the barrier. Carr and Lee (2009) make clear that symmetry condition is merely sufficient, but not necessary. The hedge described above for a down-and-out call works provided that there are no jumps over the barrier and the call and put have the same implied volatility at the first passage time to the barrier, a condition referred to as Put Call Symmetry (PCS), which was introduced to finance by Bates (1988) as a way to measure skewness. More recently, Carr and Nadtochiy (2011) show how to statically hedge barrier options for a general class of local volatility models. And Carr and Lorig (2015) develop semi-static hedges for barrier-style claims on price and volatility.

Unfortunately, the restrictive symmetry conditions described above prohibit static hedging results from being applied when the underlying is described by any of the models that are most frequently used to price European options: CEV Cox (1975), Heston Heston (1993) and SABR Hagan et al. (2002). For these models, a number of closed-form pricing formulas have been developed and the associated hedging strategies are dynamic. Davydov and Linetsky (2001) price barrier-style claims in a CEV setting using eigenfunctions expansions. Assuming zero correlation between the price and volatility-driving process, it is known that the underlying in a stochastic volatility model can be expressed as a time-changed GBM. As a result, in the zero correlation setting, barrier options can be priced via Fourier Sine series (for double barrier options) or via Fourier Sine transforms (for single barrier options) so long as the Laplace transform of the time integral of the stochastic variance process is known in closed form. This has been done in Faulhaber (2002) for the Heston model and presumably could be carried out in the SABR model using the results of Antonov and Spector (2012), though, a detailed literature search did not reveal any paper in which the zero-correlation SABR computation has been carried out.

Zero correlation stochastic volatility models induce symmetric implied volatility smiles and are not consistent with empirical evidence from equity markets, where smiles exhibit strong at-the-money skews. It is therefore important to allow the underlying to be correlated with the volatility-driving process. When correlation is non-zero, closed-form formulas for barrier option prices are not available and perturbation methods are often employed. Lipton et al. (2014), for example, finds approximate barrier options prices by expanding prices in a small parameter, which is equal to the correlation times the vol-of-vol. Fouque et al. (2011) price barrier options in a fast mean-reverting volatility setting. And Lorig (2014) values barrier options and other claims for a class of multiscale stochastic volatility models (see Fouque et al. (2011) for a review of these models). Yet the methods of Lipton et al. (2014) and Fouque et al. (2011) cannot be applied in the CEV or SABR settings, and the results in Lorig (2014) require a separation of time scales between the price process and the corresponding fast and slow factors of volatility, which may not be realistic in certain markets.

In this paper we consider a very general class of local-stochastic volatility models which naturally include the CEV, Heston and SABR models. We find approximate prices of barrier-style claims by expanding the coefficients of infinitesimal generator of the underlying as a Taylor series about a fixed point. The Taylor series expansion method was initially developed for European-style claims in scalar diffusion setting in Pagliarani and Pascucci (2012) and later extended to -dimensional diffusions in Lorig et al. (2015b) and Lorig et al. (2015a).

A significant mathematical challenge arises when extending the methods developed in Lorig et al. (2015a) for diffusions in to diffusions in strict subsets of . In particular, in , the zeroth order approximate transition density of a diffusion is given by a Gaussian kernel. The Gaussian kernel is a function of the difference of the forward and backward variables. This symmetry between forward and backward variables greatly simplifies the computations required to obtain higher order corrections to the transition density. For a diffusion in a strict subset of however, the zeroth order transition density approximation will no longer be a function of the difference of the forward and backward variables. As a result, the computations needed to obtain higher order corrections to the transition density are significantly more involved.

The rest of this paper proceeds as follows. In Section 2, we introduce a general local-stochastic volatility model and describe the option-pricing problems we wish to solve. In Section 3, we develop an asymptotic expansion for options prices. This expansion leads to a sequence of nested PDE problems, which we solve explicitly in Section 4. In Section 5, we establish the asymptotic accuracy of our approximation for European options. Finally, in Section 6, we provide several numerical illustrations of our pricing approximation for barrier-style claims and compare our results to prices obtained via Monte Carlo simulation. Some concluding remarks are offered in Section 7.

2 Market model

We consider a market defined on a complete, filtered probability space . Here, the measure represents the market’s chosen pricing measure. Let be the value of a risky asset. We suppose the dynamics of are given by

| (2.1) | ||||

| (2.2) | ||||

| (2.3) | ||||

| (2.4) |

where the function must be positive, strictly increasing and . The processes and are driftless -Brownian motions with constant correlation . We assume the dynamics of are such that has a unique strong solution, at least up until the first exit time of of some interval .

For simplicity, we take the risk-free rate of interest to be zero. Thus, in order to preclude the possibility of arbitrage, the risky asset must be a martingale. As a result, the function , which controls the drift of , must satisfy

| (2.5) |

The condition on can be easily derived by computing and setting the -term to zero. Typical choices for are , in which case , or , in which case .

We are interested in computing the price of a barrier-style claim, whose payoff at the maturity date is given by

| (2.6) |

where is an interval in . For a single-barrier claim with a barrier we have . For a double-barrier claim, we have where . We also allow for the possibility that , which corresponds to a European claim on .

Remark 2.1.

When , payoffs of the form (2.6) are knock-out style payoffs. A knock-in style payoff is a payoff of the form

| (2.7) |

It is known that the value of a knock-in claim with payoff (2.7) is equal to the value of a European claim with payoff minus the value of a knock-out claim with payoff (2.6). Thus, by pricing both knock-out and European style claims we can also price knock-in style claims.

The value of the claim with payoff (2.6) at time is given by

| (2.8) |

Under mild conditions, the function , defined in (2.8), is the unique classical solution of the Kolmogorov Backward equation

| (2.9) |

where , the generator of , is given explicitly by

| (2.10) |

and is defined to act on functions that are twice differentiable and satisfy certain boundary conditions

| (2.11) |

Here we use the notation to indicate a finite endpoint of . So, for example, if , then acts on functions that satisfy . Throughout this paper, we assume a unique classical solution to (2.9) exists. Our goal is to find the solution of PDE (2.9). As no explicit solution of (2.9) exists for general coefficients , we shall seek instead an explicit approximation for .

3 Formal asymptotic expansion

In this section, we will present a formal asymptotic expansion for . To begin, let us introduce some notation. For any coefficient of we define

| (3.1) |

where is a fixed point and . Next, we introduce an operator , which is given explicitly by

| (3.2) |

where . Consider, now, a family of PDE problems, indexed by

| (3.3) |

Noting that it follows from (2.9) and (3.3) that . Thus, rather than seek an approximation solution to PDE problem (2.9) directly, we shall instead seek an approximation solution to PDE problem (3.3) by expanding in powers of and as follows

| (3.4) |

where the functions are (at present) unknown. Once we obtain an approximation for , our approximation for will be obtained by setting .

Assume for the moment that the coefficients in are analytic. We shall see later that the approximation we obtain for does not require this assumption. However, making this assumption simplifies the presentation considerably so we will temporarily proceed with it. As the coefficients of are analytic, we have

| (3.5) | ||||

| (3.6) | ||||

| (3.7) |

where and have introduced the notation

| (3.8) |

for . Observe that is the th order term in the Taylor series expansion of about the point .

Inserting expansions (3.4) and (3.5) into PDE problem (3.3) and collecting terms with like powers of and , we obtain

| (3.9) | |||||||

| (3.10) |

For clarity, we present the lowest order terms explicitly here

| (3.11) | |||||||

| (3.12) | |||||||

| (3.13) | |||||||

| (3.14) | |||||||

| (3.15) |

The above computation motivates the following definition.

Definition 3.1.

Remark 3.2.

Remark 3.3.

Note that we have set in (3.16). This is often a point of confusion, and we wish to clarify how this should be handled. First, one should solve the sequence of nested PDE problems (3.9)–(3.10) with fixed. To be explicit, let us denote the solution of the PDE as . If one is then interested in the approximate value of at the point , one should then compute in the sum (3.16). The reason for choosing is as follows. The small-time behavior of a diffusion is predominantly determined by the geometry of the diffusion coefficients near the starting point of the diffusion . In turn, the most accurate Taylor series expansion of any function near the point is the Taylor series expansion centered at .

Remark 3.4.

As previously mentioned, analyticity of the coefficients of is not required. Indeed, to construct the th order approximation one requires only the operators for . Thus, the th order approximation of requires only that the coefficients of be .

4 Explicit expressions

In this section, we provide explicit expressions for the functions required to compute , the th order approximation of . We begin with a review of Duhamel’s principle. Let be the fundamental solution of parabolic operator . That is,

| (4.1) |

Duhamel’s principle states that the the unique classical solution to

| (4.2) |

is given by

| (4.3) |

where we have introduced the semigroup generated by , which is defined as follows

| (4.4) |

where .

Proposition 4.1.

Proof.

See Appendix A. ∎

For clarity, we present the lowest order terms here

| (4.9) | ||||

| (4.10) | ||||

| (4.11) | ||||

| (4.12) | ||||

| (4.13) | ||||

| (4.14) | ||||

| (4.15) | ||||

| (4.16) | ||||

| (4.17) |

To proceed further, we must specify explicitly the action of the semigroup . We will consider three separate cases: European claims, single-barrier claims, and double-barrier claims.

4.1 European claims

In this section, we consider the case . As when , we see from (2.6) that this case corresponds to a European claim written on . We begin with the following lemma.

Lemma 4.2.

Let be the following linear operator

| (4.18) |

The following holds

| (4.19) | ||||||

| (4.20) |

Moreover, we have

| (4.21) |

where is a Dirac delta function and denotes the complex conjugate of .

Proof.

The lemma can easily be checked by direct computation. ∎

Proposition 4.3.

Let be the semigroup generated by with . Then we have

| (4.22) | ||||

| (4.23) |

where and are given by

| (4.24) | ||||||

| (4.25) |

with and as defined in (4.20).

Proof.

Now, from Proposition 4.1, we see that the are a sum of terms of the form

| (4.28) |

Using (4.22), we can write these terms as

| (4.29) | ||||

| (4.30) |

Although the multiple integral may seem unwieldy, we shall see that all but a single integral collapses when we compute the elements

| (4.31) |

which appear in (4.30)

Lemma 4.4.

Proof.

The proof is a straightforward computation. Recalling that , we have

| (4.34) | ||||

| (4.35) | ||||

| (4.36) | ||||

| (4.37) |

where, in the last step, we have used (4.21). ∎

Remark 4.5.

The derivative of a Dirac delta function is defined as follows:

| (4.38) |

where we have integrated by parts.

Note from (3.6), (3.7) and (3.8) that the operators are sums of operators of the form (4.32). Thus, in light of Lemma 4.4 and Remark 4.5, we see that the integrals in (4.30) with respect to and , for collapse due to the Dirac delta functions. The integral with respect to also collapses, due to the fact that the payoff function does not depend on . And the iterated integrals with respect to for involve only exponentials and can always be computed explicitly. Thus, what remains is the integral with respect to , which, in general, must be computed numerically (if for some and , then the integral with respect to can be evaluated analytically).

4.2 Single-barrier claims

In this section, we consider the case , which corresponds to a single-barrier knock-out claim written on with a barrier . The case with can be handled analogously. We begin with the following lemma.

Lemma 4.6.

Let be the following linear operator

| (4.39) |

The following holds

| (4.40) | ||||||

| (4.41) |

Moreover, we have

| (4.42) |

Here, is a Dirac delta function.

Proof.

The lemma can be checked by direct computation. ∎

Proposition 4.7.

Proof.

Once again, to compute the , we must examine terms of the form (4.28). Using (4.44), we write these terms as

| (4.49) | ||||

| (4.50) |

where and are as in Proposition 4.7. Noting that each can be expressed as a sum of operators with the form of , which is defined in (4.32), we must compute inner products of the form

| (4.51) |

This motivates the following lemma.

Lemma 4.8.

Proof.

Note from (3.6), (3.7) and (3.8), the operators are sums of operators of the form (4.32). We see from (4.52) that the integrals with respect to , in (4.50) collapse due to the Dirac delta functions. As is independent of , the integral with respect to also collapses. Furthermore, the iterated integrals with respect to , in (4.50) involve only exponentials in and can therefore be evaluated explicitly. We are left only with integrals with respect to , , which can be evaluated numerically.

4.3 Double-barrier claims

In this section, we consider the case , which corresponds to a double-barrier knock-out claim written on with a barriers and satisfying . We begin with the following lemma.

Lemma 4.9.

Let be the following linear operator

| (4.63) |

The following holds

| (4.64) | ||||||

| (4.65) |

Moreover, we have

| (4.66) |

Here, is a Kronecker delta function and is given by (4.42).

Proof.

The lemma can be checked by direct computation. ∎

Proposition 4.10.

Proof.

As with the European and single-barrier cases, to compute the functions we must evaluate terms of the form (4.28). Using (4.68) we write these terms as

| (4.73) | ||||

| (4.74) |

As each is a sum of operators with the form of , which is defined in (4.32), we must compute terms of the form .

Lemma 4.11.

Proof.

Remark 4.12.

The functions and , which appear in the expression for , arise from computing integrals of the form and . For any , these integrals are equal to finite sums of terms containing powers of , sines and cosines (as can be seen by integrating by parts). Thus, the functions and can be evaluated with minimal computational effort.

Note from (3.6), (3.7) and (3.8), the operators are sums of operators of the form (4.32). We see from (4.75) that the integrals with respect to , in (4.74) collapse due to the Dirac delta functions. Since is independent of , the integral with respect to also collapses. Furthermore, the iterated integrals with respect to , in (4.50) involve only exponentials in and can therefore be evaluated explicitly. Thus, (4.74) is an explicit sum and does not require any numerical integration.

Remark 4.13.

The fundamental solution corresponding to the parabolic operator can be obtained explicitly in all three of the cases we have considered (European, single barrier and double barrier). As such, one might wonder why we expand the operator in powers of and as well as in powers (as opposed to expanding in powers of and only). The reason we expand in powers of is that, without this expansion, the integrals in (4.6) with respect to cannot be computed explicitly in the single or double-barrier cases. Thus, by expanding in avoid having to evaluate multidimensional numerical integrals.

5 Accuracy results

In this section, we establish the accuracy of our formal pricing approximation for European options. Before stating our accuracy result, let us introduce some additional notation. For a set , denote by the class of bounded functions on with globally Lipschitz continuous derivatives of order less than or equal to . Let denote the sum of the -norms of the derivatives of up to order . We also denote by and we set . The following theorem describes the accuracy of the th order approximation of the price of a European option written on an asset described by local-stochastic volatility dynamics.

Theorem 5.1.

Proof.

See Appendix B. ∎

Establishing asymptotic accuracy for barrier-style claims remains an open problem for the following reason. The proof of Theorem 5.1 exploits Gaussian symmetry present in the pricing kernel of the zeroth order European problem. This symmetry is absent in both the single-barrier and double-barrier cases, and hence the same techniques for proving accuracy cannot be applied. In the following section we explore the accuracy of our approximations for barrier-style claims in several numerical examples.

6 Numerical examples

6.1 Heston model

In this section, we implement our pricing approximation for an underlying that has Heston dynamics Heston (1993). Specifically, we suppose that satisfies

| (6.1) |

where so that the process remains strictly positive. In our numerical experiments, we consider double-barrier knock-out calls and puts with the following parameters fixed

| 0.62 | 0.04 | .62 | 0.083 | -0.4 | 1.15 | 0.04 | 0.2 |

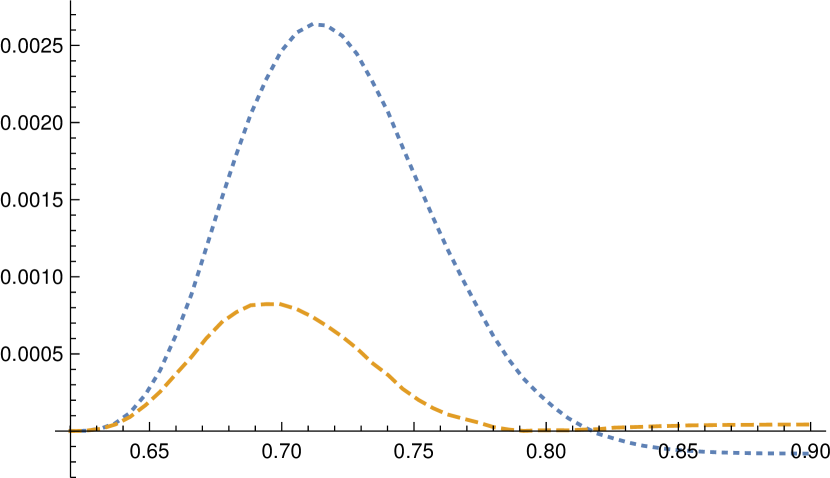

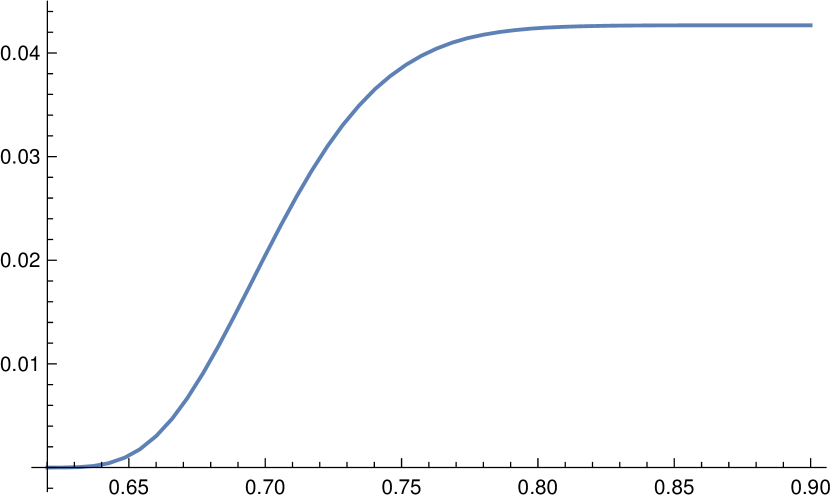

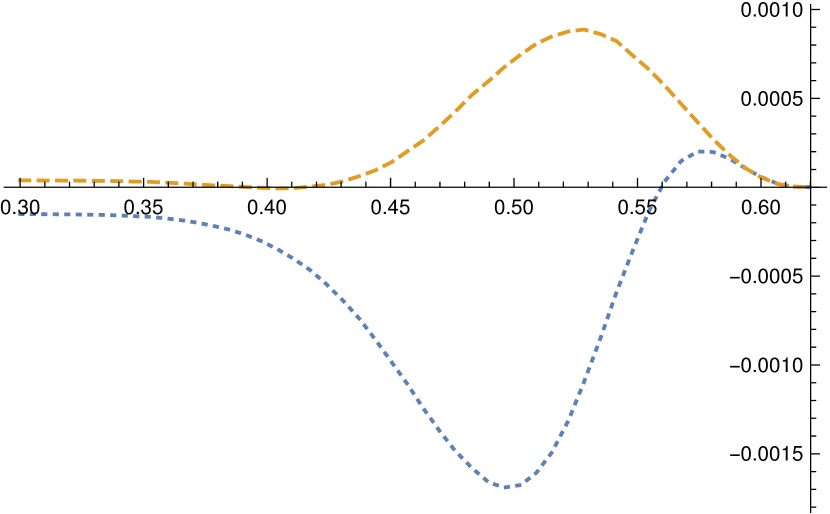

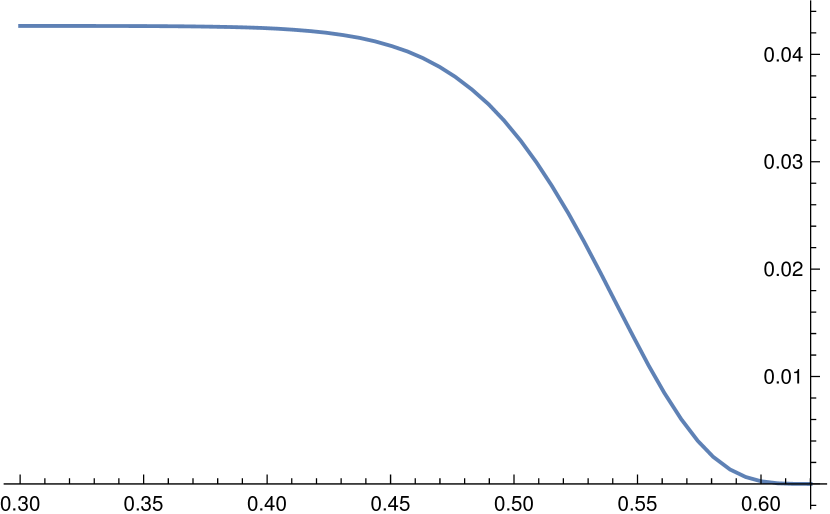

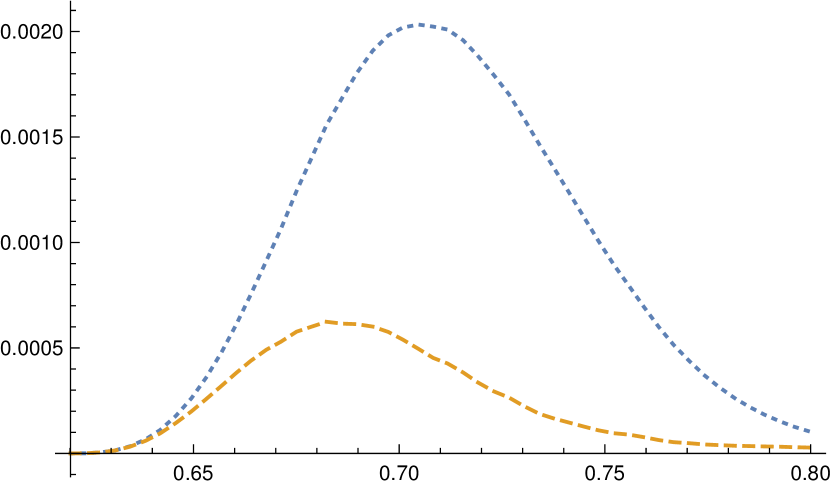

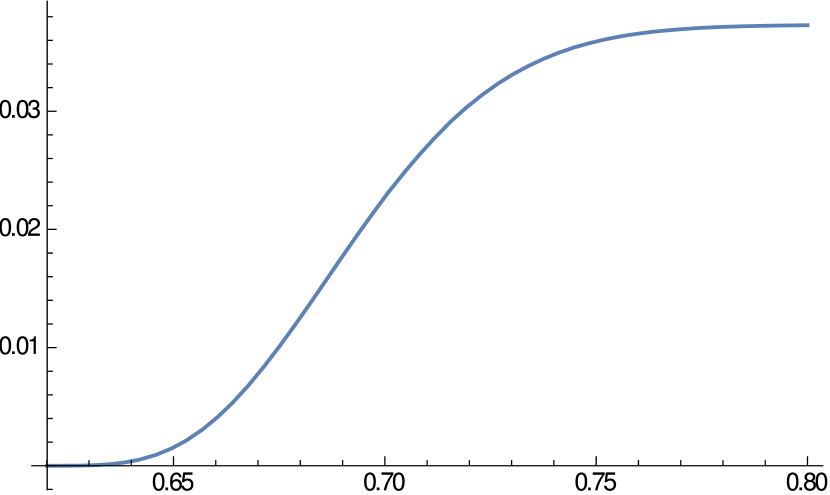

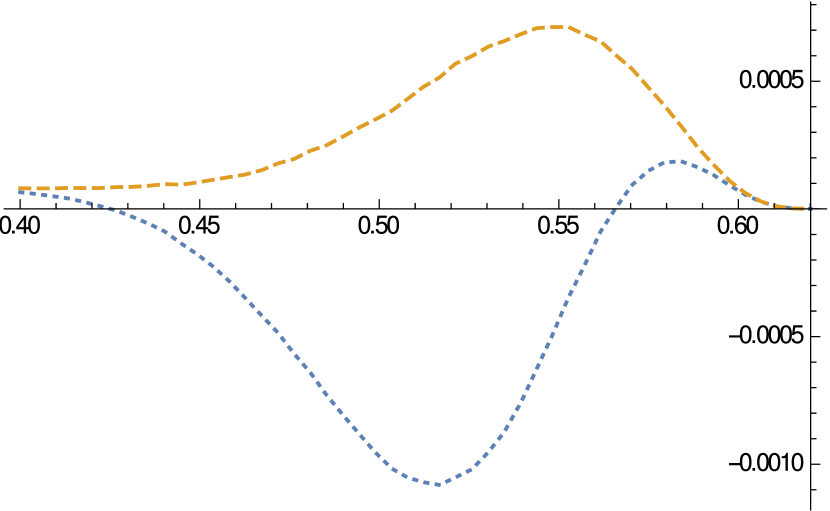

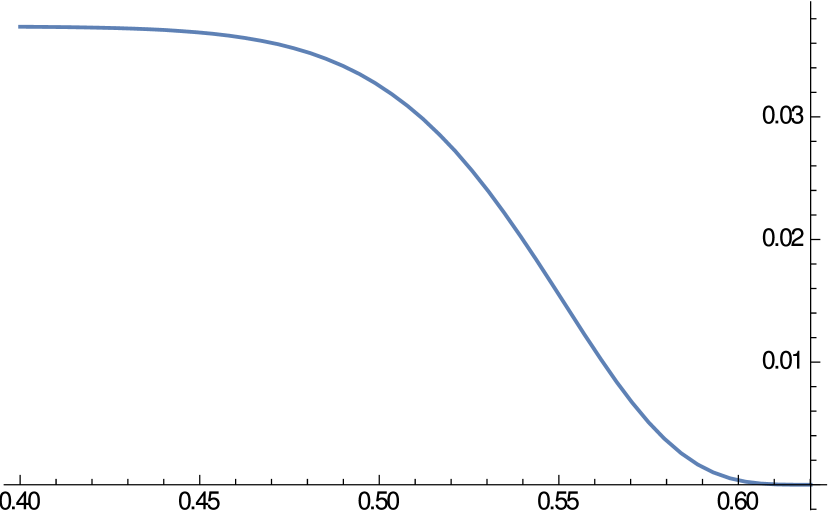

where represents the strike and represents the maturity date. We first consider call payoffs with the lower barrier fixed and the upper barrier varying. We compute both our zeroth and second order price approximation and as well as “exact” price , which we obtain via Monte Carlo simulation. In Figure 2, we plot the error and of our zeroth and second order approximations as a function of the upper barrier . To get a sense of the scale of the error, we also plot in Figure 2 the exact price as a function of . In Figures 4 and 4, we provide analogous plots for put payoffs with the upper barrier fixed while varying the lower barrier . We see from Figures 2 and 4 that provides a more accurate approximation of than for both puts and calls at nearly all levels of and .

Remark 6.1.

We omit the first order approximation in Figures 2 and 4 for the following reason. The difference is small compared to because, when the payoff function depends only on (as is the case for call and put payoffs), we have . Therefore, the first correlation correction term in our approximation appears at the second order in . The effect of including the first correlation correction is large compared to the first correction due to -dependence in the coefficients of .

6.2 CEV Model

In this section, we implement our pricing approximation for an underlying that has Constant Elasticity of Variance (CEV) dynamics Cox (1975). Specifically, we suppose that satisfies

| (6.2) |

where and . We consider double-barrier knock-out calls and puts with the following parameters fixed

| 0.62 | 0.62 | 0.083 | 0.32 | 0.019 |

where represents the strike and represents the maturity date. We first consider call payoffs with the lower barrier fixed and the upper barrier varying. We compute the zeroth and second order price approximation and , respectively, as well as “exact” price , which we obtain via Monte Carlo simulation. Note that we omit the superscript from and as correlation plays no role in a local volatility setting. In Figure 6, we plot the error and of our zeroth and second order approximations as functions of the upper barrier . To get a sense of the scale of the error, we also plot in Figure 6 the exact price as a function of . In Figures 8 and 8, we provide analogous plots for put payoffs with the upper barrier fixed while varying the lower barrier . We see from Figures 6 and 8 that in both the call and put cases the second order approximation outperforms the zeroth order approximation.

7 Conclusion

In this paper we have presented a formal pricing approximation for European and barrier-style claims in a local-stochastic volatility setting. We have provided rigorous accuracy results for European-style claims. And we have provided several numerical examples illustrating the accuracy and versatility of our approximation for barrier-style claims. Future research will focus on extending our techniques to other path-dependent derivatives, such as lookback and variance-style claims.

Acknowledgments

The authors are grateful to Stefano Pagliarani and Andrea Pascucci for helpful feedback on this manuscript.

Appendix A Proof of Proposition 4.1

In this section, we present the proof of Proposition 4.1.

Proof of Proposition 4.1.

We first note that formula (4.6) holds for and by applying Duhamel’s principle to (3.11) and (3.12). Next, assume as an inductive hypothesis that for non-negative integers and such that formula (4.6) holds for pairs of non-negative integers such that . Define

| (A.1) |

Applying Duhamel’s principle to (3.10), we see that

| (A.2) | ||||

| (A.3) | ||||

| (A.4) | ||||

| (A.5) |

where (A.5) follows from our inductive hypothesis. Reordering the sums in (A.5) we obtain

| (A.6) | ||||

| (A.7) |

Next, note that

| (A.8) |

Therefore, combining (A.8) with (A.7) we obtain

| (A.9) | ||||

| (A.10) |

Relabeling and reindexing and gives

| (A.11) | ||||

| (A.12) | ||||

| (A.13) | ||||

| (A.14) |

which is (4.6) for the case . The proof for the case is analogous. ∎

Appendix B Proof of Theorem 5.1

In this section, we prove Theorem 5.1. Our strategy is to adapt the proof of asymptotic accuracy in Lorig et al. (2015a) to our present situation. As such, many of the propositions and lemmas needed for the proof of Theorem 5.1 follow from analogous propositions and lemmas contained in Lorig et al. (2015a).

Throughout this section, we let , and be elements of . It will also be convenient to introduce multi-index notation for the operators and . We have

| (B.1) | ||||||

| (B.2) |

where

| (B.3) |

Before proving Theorem 5.1, we require some preliminary results. In what follows, we denote by the fundamental solution corresponding to the parabolic operator .

Lemma B.1.

For any , and with , we have

| (B.4) |

and

| (B.5) |

where is the fundamental solution of the operator , and is a positive constant dependent only on and .

Proof.

The following fact will also be helpful. Let and be constants such that . Then, for

| (B.6) |

where is the Euler gamma function.

Proposition B.2.

Proof.

The proof is analogous to the proof of (Lorig et al., 2015a, Lemma 6.24). ∎

Proposition B.3.

Define for

| (B.9) | |||||

| (B.10) | |||||

with the convention that . Then for , we have

| (B.11) |

Proof.

We will show that

| (B.12) |

from which (B.11) follows by an application of Duhamel’s principal. Note that (B.12) follows if we show

| (B.13) |

because and . From equations (3.9), (3.10), (B.9) and (B.10), we deduce

| (B.14) |

We now proceed to show (B.13) by induction. When , since , we have

| (B.15) |

Assume now that (B.13) holds for . Then we have by (B.14) that

| (B.16) | ||||

| (B.17) | ||||

| (B.18) | ||||

| (B.19) |

Therefore, (B.13) holds for all . ∎

We are now in a postition to prove Theorem 5.1.

Proof of Theorem 5.1.

| (B.20) |

Let be the -th Taylor polynomial approximation of with the convention that . We rewrite (B.20) as

| (B.21) | ||||

| (B.22) | ||||

| (B.23) |

where

| (B.24) | |||

| (B.25) | |||

| (B.26) |

We first consider . We note that since by convention. For , we perform integration by parts to obtain for ,

| (B.27) |

By the product rule and (B.5), evaluating at gives

| (B.28) | ||||

| (B.29) |

Applying (B.4) and (B.8) gives

| (B.30) | |||||

| (B.31) | |||||

| (B.32) | |||||

Similar arguments show

| (B.33) |

for . When , , so by (B.23) we have

| (B.34) |

When , by (B.23) we have

| (B.35) | ||||

| (B.36) | ||||

| (B.37) | ||||

| (B.38) |

which proves Theorem 5.1. ∎

References

- Antonov and Spector (2012) Antonov, A. and M. Spector (2012, march). Advanced analytics for the sabr model. SSRN.

- Bates (1988) Bates, D. (1988). The crash premium: Option pricing under asymmetric processes, with applications to options on deutschemark futures. Working Paper, University of Pennsylvania.

- Bowie and Carr (1994) Bowie, J. and P. Carr (1994, 8). Static simplicity. Risk.

- Carr et al. (1998) Carr, P., K. Ellis, and V. Gupta (1998). Static hedging of exotic options. The Journal of Finance 53(3), 1165–1190.

- Carr and Lee (2009) Carr, P. and R. Lee (2009). Put-call symmetry: Extensions and applications. Mathematical Finance 19(4), 523–560.

- Carr and Lorig (2015) Carr, P. and M. Lorig (2015, August). Robust replication of barrier-style claims on price and volatility. ArXiv e-prints.

- Carr and Nadtochiy (2011) Carr, P. and S. Nadtochiy (2011). Static hedging under time-homogeneous diffusions. SIAM Journal on Financial Mathematics 2(1), 794–838.

- Cox (1975) Cox, J. (1975). Notes on option pricing I: Constant elasticity of diffusions. Unpublished draft, Stanford University. A revised version of the paper was published by the Journal of Portfolio Management in 1996.

- Davydov and Linetsky (2001) Davydov, D. and V. Linetsky (2001). Pricing and hedging path-dependent options under the cev process. Management science 47(7), 949–965.

- Faulhaber (2002) Faulhaber, O. (2002). Analytic methods for pricing double barrier options in the presence of stochastic volatility. Ph. D. thesis, Technische Universität Kaiserslautern.

- Fouque et al. (2011) Fouque, J.-P., S. Jaimungal, and M. Lorig (2011). Spectral decomposition of option prices in fast mean-reverting stochastic volatility models. SIAM Journal on Financial Mathematics 2(1).

- Fouque et al. (2011) Fouque, J.-P., G. Papanicolaou, R. Sircar, and K. Solna (2011). Multiscale stochastic volatility for equity, interest rate, and credit derivatives. Cambridge: Cambridge University Press.

- Hagan et al. (2002) Hagan, P., D. Kumar, A. Lesniewski, and D. Woodward (2002). Managing smile risk. Wilmott Magazine 1000, 84–108.

- Heston (1993) Heston, S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343.

- Lipton et al. (2014) Lipton, A., A. Gal, and A. Lasis (2014). Pricing of vanilla and first-generation exotic options in the local stochastic volatility framework: survey and new results. Quantitative Finance 14(11), 1899–1922.

- Lorig (2014) Lorig, M. (2014). Pricing derivatives on multiscale diffusions: An eigenfunction expansion approach. Mathematical Finance 24(2), 331–363.

- Lorig et al. (2015a) Lorig, M., S. Pagliarani, and A. Pascucci (2015a). Analytical expansions for parabolic equations. To appear: SIAM Journal on Applied Mathematics.

- Lorig et al. (2015b) Lorig, M., S. Pagliarani, and A. Pascucci (2015b). Explicit implied volatilities for multifactor local-stochastic volatility models. To appear: Mathematical Finance.

- Merton (1973) Merton, R. (1973). Theory of rational option pricing. The Bell Journal of Economics and Management Science 4(1), 141–183.

- Pagliarani and Pascucci (2012) Pagliarani, S. and A. Pascucci (2012). Analytical approximation of the transition density in a local volatility model. Cent. Eur. J. Math. 10(1), 250–270.