Sequential Bayesian Learning for Merton’s Jump Model with Stochastic Volatility

Eric Jacquier

Boston University, Questrom School of BusinessBoston University, Questrom School of Business, email: jacquier@bu.eduNicholas Polson

The University of Chicago Booth School of BusinessThe University of Chicago Booth School of Business, email:nicholas.polson@chicagobooth.eduVadim Sokolov

George Mason University, Volgenau School of EngineeringGeorge Mason University, Volgenau School of Engineering, email: vsokolov@gmu.edu

(First Draft: August 2014

This Draft: October 2016

)

Abstract

Jump stochastic volatility models are central to

financial econometrics for volatility forecasting, portfolio risk management,

and derivatives pricing. Markov Chain Monte Carlo (MCMC) algorithms are computationally unfeasible for the sequential learning of volatility state variables and parameters,

whereby the investor must update all posterior and predictive densities as new information arrives. We develop a particle filtering and learning algorithm to sample posterior distribution in Merton’s jump stochastic volatility. This allows to filter spot volatilities and jump times, together with sequentially updating (learning) of jump and volatility parameters. We illustrate our methodology on Google’s stock return. We conclude with directions for future research.

Jump stochastic volatility models are central to many questions in finance such as pricing, or debt-and-credit risk assessment. Merton (1976); Duffie et al. (2000) provide theoretical treatments of derivatives pricing and Merton (1974); Korteweg and

Polson (2008) provide applications to debt and credit risk assessment. Most theoretical treatments in the literature assume the availability of efficient estimates of volatility, jumps and parameters. Efficient estimates of the current volatility state and jump parameters are available from Markov Chain Monte Carlo (MCMC) algorithms, see Johannes and Polson (2010); Jacquier et al. (2004). A number of

authors have analyzed jump diffusion models by MCMC, see Eraker et al. (2003); Li et al. (2008); Fulop et al. (2012). One caveat is that MCMC algorithms are computationally demanding, and are not feasible for sequential learning. Essentially, MCMC algorithm needs to be run every time new information is available.

Particle filtering (PF) and learning (PL) algorithms, on the other hand, efficiently incorporate new information into the parameter learning process. Early PL algorithms where plagued by degeneracy problem which hampered their performance. Particle learning (Carvalho et al. (2010); Warty et al. (2016)) algorithms deliver posterior

and predictive densities of parameters and latent variable as new information arrives. Sequential parameter learning is obtained by

tracking a state vector of conditional sufficient statistics.

An important goal of an investor, for example, is to characterize the density of current and future

returns to draw inference on the riskiness of a portfolio, probability of shortfall, or value-at-risk.

The distribution of future volatility is an input in the computation of derivative prices or their

hedge ratios. We provide a versatile model of access returns that combines Merton’s pure jump formulation with stochastic

volatility. Within this model, the investor needs to learn about the state variables, namely, volatility,

jump times and jump sizes, and the model parameters from the observed returns. PL methods are particularly well-suited for empirical finance

applications for several reasons.

1.

They are designed to be sequential, updating the relevant posterior distribution as new information

(data) is obtained, with minimal computing resources. Bayesian inference tools directly apply to these

PF algorithms as they produce posterior or predictive densities relevant to the models used.

2.

Akin to MCMC algorithms, particle filtering and learning can be extended to simultaneously estimate both structural

parameters and latent variables. For example, one can separate out the effects of jumps and

stochastic volatility in equity returns.

3.

As conditional simulation methods, they avoid optimization. From a practical perspective,

PF and PL methods are therefore extremely fast in terms of computing time. This has many advantages,

particularly for higher-dimensional multivariate models.

One can also included option price information into the inference problem, see for example Polson and Stroud (2003); Johannes and Polson (2009); Yun (2014). Whilst we only account for stochastic jumps, it is

easy to add deterministic jump components to account for example, for earnings announcement effects, see Dubinsky and Johannes (2005).

The rest of the paper is as follows. Section 2 provides a review of particle filtering methods.

Section 3 provides the main contribution of our paper and an algorithm for sequential filtering states

and performing parameter learning for Merton Jump model together with stochastic volatility (Jacquier et al. (1995, 2004)). Section 4 provide a application to Google’s stock return. Finally, Section 5

concludes with directions for future research.

2 Particle Filtering for Merton’s Jump Model

Merton’s Jump Stochastic volatility model has a discrete time version for log-returns, , with jump times, , jump sizes, , and

spot stochastic volatility, , given by the dynamics

where . The errors

are possibly correlated bivariate normals.

The investor must obtain optimal filters for , and learn the posterior densities

of the parameters . These estimates will be

conditional on the information available at each time.

2.1 Pure Jump Merton model

Let denote a stock or asset price. We have historical log-returns

defined by . Log-returns have a jump component as per

with the probability of jump and

is the jump size. The Merton model involves the following hierarchical conditional

distributions:

where denotes the standard conditionally conjugate Normal-Inverse-Gamma distribution. The parameters are fixed to guarantee identification.

The goal of underlying dynamics is to provide sequential learning plot for states

and the unknown parameters .

To construct a particle filtering and learning algorithm that samples from the set of Bayesian joint posterior distributions , for . We track a particle vector that tracks the

hidden states and the conditional sufficient statistics

for any static parameters that need to be learned. Then attach them in one vector for .

Our Particle learning algorithm has four steps:

1.

Determine the conditional sufficient statistics for the parameters .

We write where with the following distributional assumptions

This leads to a current posterior distribution, that is proportional to

The conditional likelihood

proportional to

Combining these two terms, leads to an updated conditional posterior, with is again a

distribution with updated hyperparameters

where , and and .

2.

Calculate the marginal predictive distribution, denoted by of the next asset return given the states .

This a mixture distribution of the form

We marginalise out the states and the parameters , as follows. First, marginalizing and , we obtain

where with hyperparameter updates are given by

Therefore, we have a marginal joint posterior

Finally, marginalizing over the jump times leads to the require predictive for resampling

where is the current conditional sufficient statistic.

Given the next observation , we then use it to resample particles

3.

Propagate a new state using

the conditional posterior

This is a mixture distribution where we can

use an intermediate parameter vector draw from . In this manner, we obtian a new draw

of the filtered distribution on states given the current return history.

To summarize, we can do this as follows:

(a)

Generate .

(b)

Generate .

(c)

Sample .

4.

Finally, use the update rule for sufficient statistics .

Here we have used the resampled in the update and the sampled from the previous step.

2.2 Extension to Jumps with Stochastic Volatility

We now assume that the log-returns not only have a jump component but also a

stochastic volatility component, with dynamics given by

The relevant conditional distributions are now given by hierarchical structure of conditional distributions, given by

where denotes a truncated normal distribution.

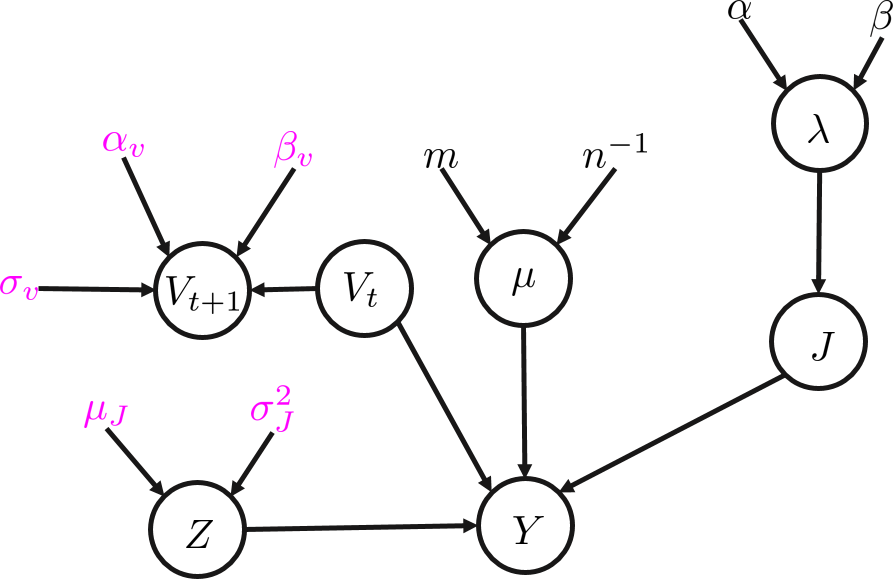

The hierarchical conditional independences structure can also be represented as a graphical model as shown in Figure 1

Figure 1: Jusm Stochastic Volatility Model as a Graphical model

We see, that the jump sizes depend on the magnitude of the current volatility . Thus, the state variables are defined by two parameters . At the same time the distribution of is defined by the hyperparameters that have sufficient statistics , which we denote by . We now construct the conditional posterior distribution of the parameter . Under a sufficient statistic structure, we have

Thus each particle is defined by , for . Let denote joint variable .

The first step is to find the posterior distributions for and . Given , the posterior is given by

with an update value for hyper parameters

Now we look at . Note, that and independent of . Thus we can easily marginalize using sum of normal variables formula, and obtain

We denote the precision parameter by and .

Now, the joint distribution for and is given by

and

On the other hand

To calculate mean and standard deviation of the predictive likelihood and posterior for mean , we use the identity

We apply this identity with correspondence , , , , , , and .

From this we can calculate the updates for the hyper parameters as follows

The predictive distribution is given by

The likelihood precision is , and by normalizing, we obtain

The predictive likelihood is determined by summing out as

(1)

where

Finally, we need to find formulas for propagating the state vector , given the latest observation . Note, that is conditionally independent of , given . Thus, we can propagate the volatility variable by draying from the truncated normal .

The odds ratio for , is given by

If we sample , then size of the jump is irrelevant, otherwise we have

Thus, the posteriors is

This leads to the following algorithm

1.

Resample index , so that

2.

Propagate and , using equations (2.2) and (2.2) correspondingly

3.

Update sufficient statistics , using equations (2.2) and 2.2.

4.

Propagate volatilities by drawing

3 Application: Google stock returns

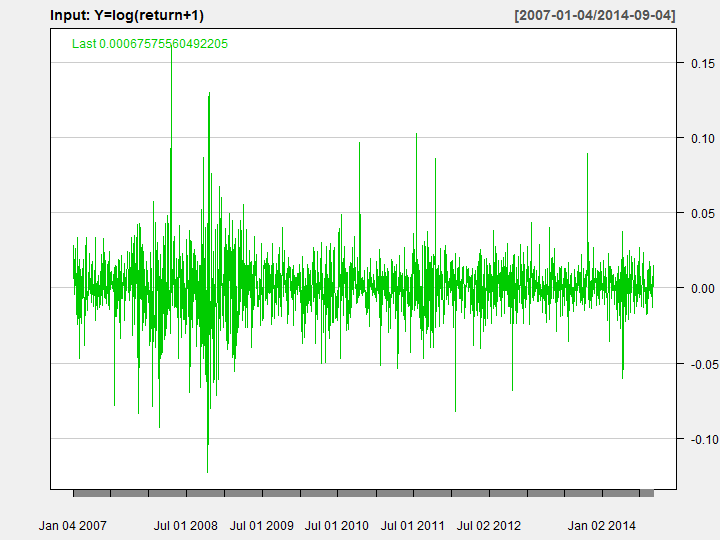

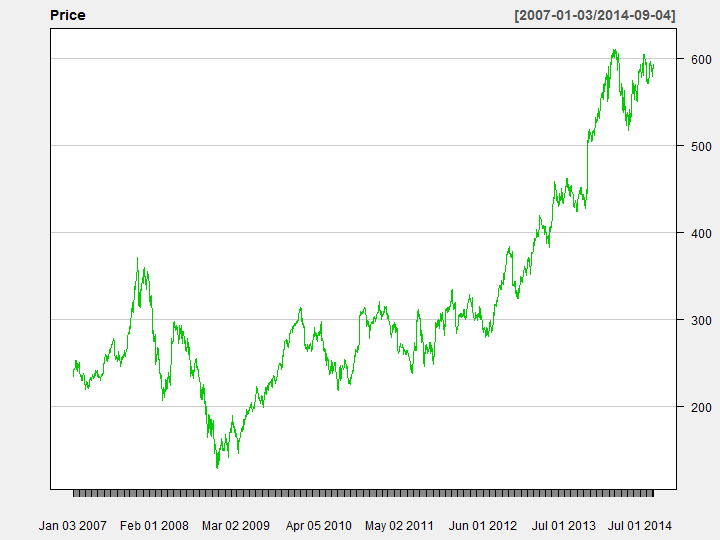

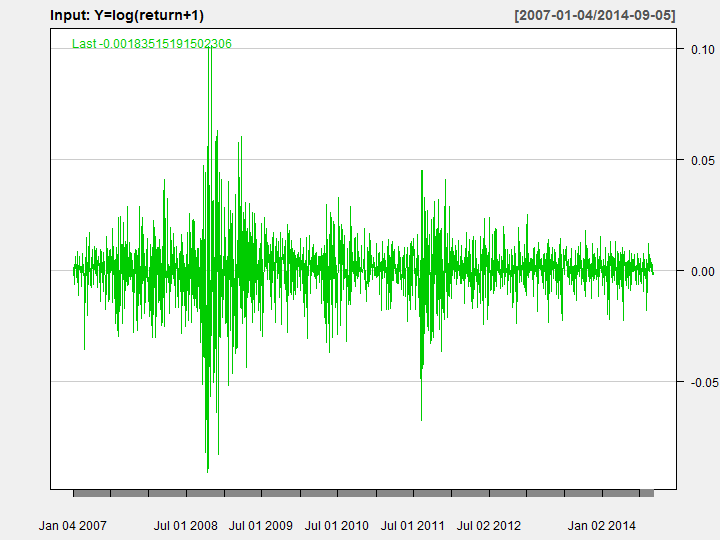

We now implement our particle filtering and learning algorithm. Namely, we applied the algorithm to the 1929 Google and S&P500 daily stock returns from January 3 2007 to August 29, 2014.

Table 1 provides summary statistics for the returns.

Mean

Std. Deviation

Skewness

Kurtosis

Min

Max

Google

4.84e-04

0.0193

0.21

8.7

-0.123

0.161

S&P500

1.78e-04

0.0135

-0.383

9.35

-0.0911

0.101

Table 1: Summary statistics for the daily log-returns

As expected, the daily returns exhibit a large amount of kurtosis consistent with time varying

second moments, as in stochastic volatility or jumps. Figure 2 below shows the price and return data for the selected period, confirming the time variation in volatility.

(a) GOOGLE Daily Log-returns

(b) GOOGLE Daily Price

(c) S&P500 Daily Log-returns

(d) S&P500 Daily Price

Figure 2: Price and return data for Google stock

Tables 2 and 3 provides posterior means and standard deviation of the parameters and state variables for the models estimated, as well as prior values.

The second and fourth columns provide parameter posterior means, and standard deviations in parentheses, for the Merton and Merton-SV models.

Prior (Merton)

Posterior (Merton)

Prior (Merton-SV)

Posterior (Merton-SV)

-0.04

-0.04

1

0.003

3.86e-03 (9.52e-04)

0.003

1.57e-03 (2.96e-03)

0.001

1.49e-04 (3.97e-05)

0.01

1.35e-04 (7.94e-04)

0.09

0.086(0.219)

0.5

7.15e-03 (0.0266)

-0.0399 (8.62e-03)

-0.0397 (0.0413)

0.0016

0.99

0.3

0.237 (0.0336)

Table 2: Parameter Estimates and Priors fro Google

Prior (Merton)

Posterior (Merton)

Prior (Merton-SV)

Posterior (Merton-SV)

-0.04

-0.04

1

0.003

2.77e-03(7.8e-04)

0.003

3.62e-04 (1.98e-03)

0.001

7.05e-05 (2.62e-05)

0.01

1.3e-04 (7.4e-04)

0.09

0.0627 (0.213)

0.5

0.011 (0.0542)

-0.0398 (1.93e-03)

-0.0417 (0.0395)

0.0016

0.99

0.3

0.216 (0.0374)

Table 3: Parameter Estimates and Priors fro S&P 500

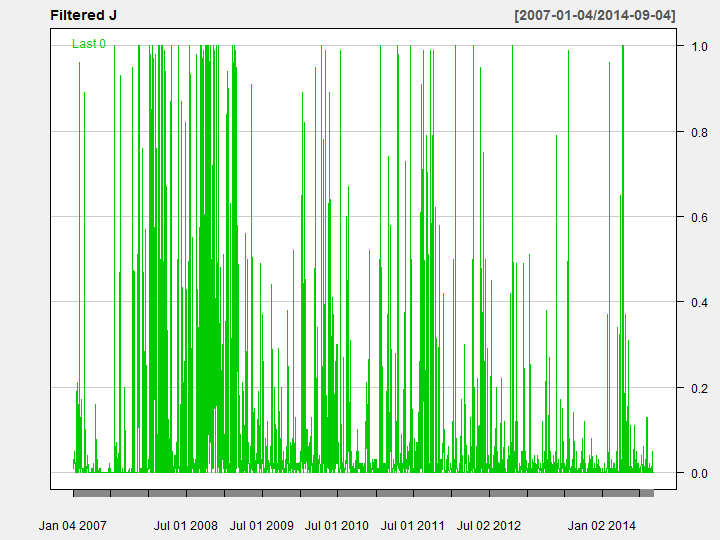

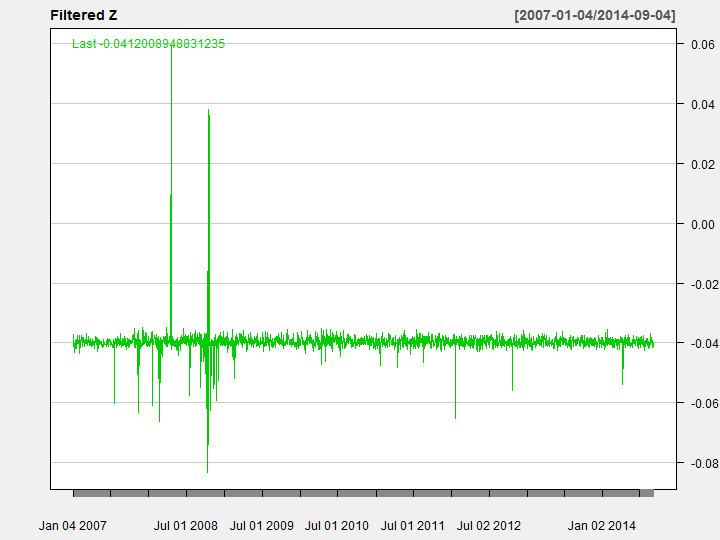

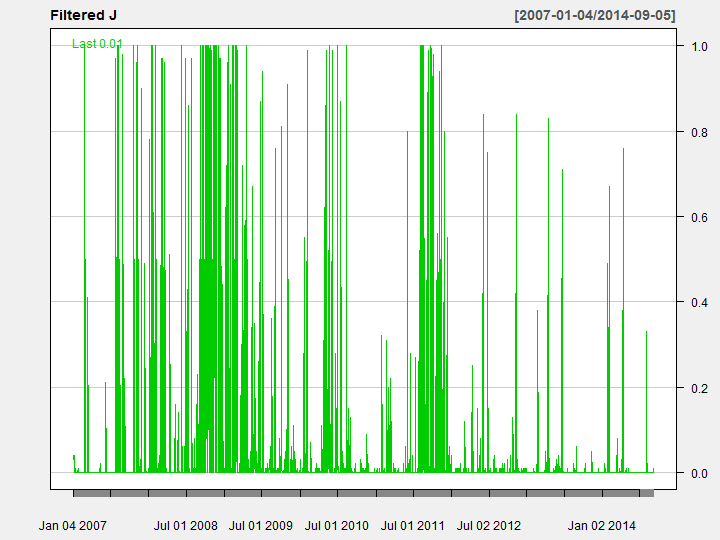

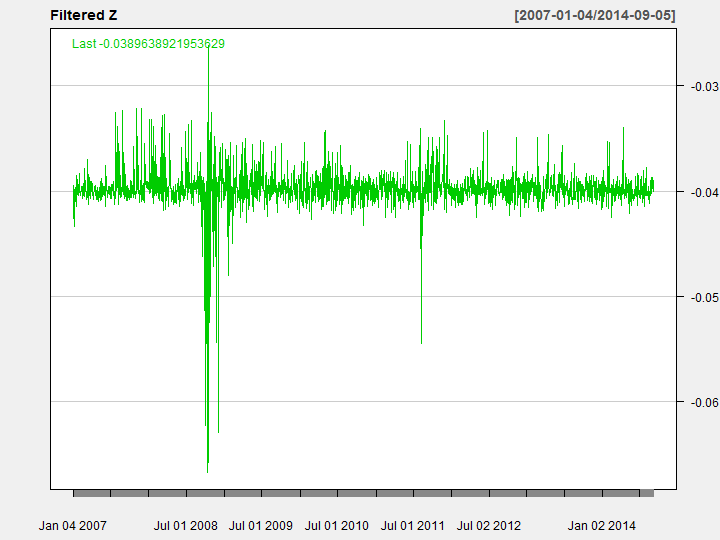

Consider the pure Merton model without stochastic volatility. Figure 3 shows the filtered state parameters ans estimated using the Merton jump model. We can see that the cluster of jumps in July 2008. Such a clustering indicates that the model may be misspecified. One reason for that is that the volatility is fixed in the model and thus, all of the large moves on returns are attributed to jumps. However, the clustering of jumps is extremely unlikely in reality due to the i.i.d assumption on the jump time and size specification and infrequent nature of jumps.

(a) Filtered J for GOOGLE

(b) Filtered Z for GOOGLE

(a) Filtered J for S&P500

(b) Filtered Z for S&P500

Figure 3: Value of the filtered state variables for Merton model

These clustered jumps of 2008 in fact reflect higher volatility of returns.

The fourth column of Tables 2 and 3 provides the parameters estimates for the Merton-SV model. Adding stochastic volatility to the jump model has the expected effect of reducing the amount of jumps in the returns. Virtually, all of the changes on returns are explained by the stochastic volatility

4 Discussion

Particle filtering methods are flexible and fast to compute. They provide a simple solution to the sequential inference problem where Markov Chain Monte Carlo (MCMC) are computationally expensive as they have to be re-run every time a new data point arrives.

We develop and implement a particle filtering and learning algorithm that provides full inference for Merton’s jump stochastic volatility model.

To perform sequential parameter learning we exploit a conditional sufficient statistic state variable that we filter with particle methods and then we draw parameters in an off line fashion. This provides an efficient approach to parameter inference.

There are a number of possible extensions of our work. On the finance side, there are many models with a similar nature to Merton’s original specification such as the Leland and Toft (1996) model of corporate credit. These models are state space-models and are amenable to particle filtering methods. On the econometrics side, extensions to continuous-time jump diffusions (Johannes et al. (2009) with

infinite activity jumps (Li et al. (2008)) or to self-exciting jump processes (Fulop et al. (2012); Aït-Sahalia and

Jacod (2009, 2012)) is an avenue for future study. Incorporating a leverage effect (or correlated errors) together with multivariate models is another area of interest (Jacquier et al. (1995, 2004)). We leave these as avenues for future study.

We intent to extend our analysis to currencies (FX) and security portfolios (e.g. market indexes). Furthermore, we will demonstrate both computational accuracy of estimation differences between particle filters and MCMC based methods.

References

Aït-Sahalia and

Jacod (2009)

Aït-Sahalia, Y. and J. Jacod

2009.

Estimating the degree of activity of jumps in high frequency data.

The Annals of Statistics, Pp. 2202–2244.

Aït-Sahalia and

Jacod (2012)

Aït-Sahalia, Y. and J. Jacod

2012.

Analyzing the spectrum of asset returns: Jump and volatility

components in high frequency data.

Journal of Economic Literature, 50(4):1007–1050.

Carlin et al. (1992)

Carlin, B. P., N. G. Polson, and D. S. Stoffer

1992.

A Monte Carlo approach to nonnormal and nonlinear state-space

modeling.

Journal of the American Statistical Association,

87(418):493–500.

Carpenter et al. (1999)

Carpenter, J., P. Clifford, and P. Fearnhead

1999.

Improved particle filter for nonlinear problems.

IEE Proceedings-Radar, Sonar and Navigation, 146(1):2–7.

Carvalho et al. (2010)

Carvalho, C., M. S. Johannes, H. F. Lopes, and

N. Polson

2010.

Particle learning and smoothing.

Statistical Science, 25(1):88–106.

Dubinsky and Johannes (2005)

Dubinsky, A. and M. Johannes

2005.

Earnings announcements and equity options.

Working Paper.

Duffie (1996)

Duffie, D.

1996.

State-space models of the term structure of interest rates.

In Stochastic Analysis and Related Topics V, Pp.

41–67.

Springer.

Duffie et al. (2000)

Duffie, D., J. Pan, and K. Singleton

2000.

Transform analysis and asset pricing for affine jump-diffusions.

Econometrica, 68(6):1343–1376.

Eraker et al. (2003)

Eraker, B., M. Johannes, and N. Polson

2003.

The impact of jumps in volatility and returns.

The Journal of Finance, 58(3):1269–1300.

Fulop et al. (2012)

Fulop, A., J. Li, and J. Yu

2012.

Bayesian learning of impacts of self-exciting jumps in returns and

volatility.

Working Paper.

Gordon et al. (1993)

Gordon, N. J., D. J. Salmond, and A. F. Smith

1993.

Novel approach to nonlinear/non-Gaussian Bayesian state

estimation.

In IEE Proceedings F-Radar and Signal Processing,

volume 140, Pp. 107–113. IET.

Jacquier et al. (2004)

Jacquier, E., N. Polson, and P. Rossi

2004.

Bayesian Inference for SV models with Correlated Errors.

Journal of Econometrics.

Jacquier et al. (1995)

Jacquier, E., N. G. Polson, and P. E. Rossi

1995.

Models and priors for multivariate stochastic volatility.

Working paper, University of Chicago.

Johannes and Polson (2009)

Johannes, M. and N. Polson

2009.

Particle filtering.

In Handbook of Financial Time Series, Pp. 1015–1029.

Springer.

Johannes and Polson (2010)

Johannes, M. and N. Polson

2010.

MCMC Methods for Continuous-Time Financial Econometrics.

In Handbook of Financial Econometrics: Applications,

L. P. HANSEN and Y. AÏT-SAHALIA, eds., volume 2 of Handbooks in

Finance, Pp. 1–72.

San Diego: Elsevier.

Johannes et al. (2009)

Johannes, M. S., N. G. Polson, and J. R. Stroud

2009.

Optimal filtering of jump diffusions: Extracting latent states

from asset prices.

Review of Financial Studies, 22(7):2759–2799.

Korteweg and

Polson (2008)

Korteweg, A. and N. Polson

2008.

Volatility, Liquidity, Credit Spreads and Bankruptcy

Prediction.

Technical report, Stanford University, Working Paper.

Leland and Toft (1996)

Leland, H. E. and K. B. Toft

1996.

Optimal capital structure, endogenous bankruptcy, and the term

structure of credit spreads.

The Journal of Finance, 51(3):987–1019.

Li et al. (2008)

Li, H., M. T. Wells, and L. Y. Cindy

2008.

A Bayesian analysis of return dynamics with Lévy jumps.

Review of Financial Studies, 21(5):2345–2378.

Merton (1974)

Merton, R. C.

1974.

On the pricing of corporate debt: The risk structure of interest

rates.

The Journal of finance, 29(2):449–470.

Merton (1976)

Merton, R. C.

1976.

Option pricing when underlying stock returns are discontinuous.

Journal of financial economics, 3(1-2):125–144.

Pitt and Shephard (1999)

Pitt, M. K. and N. Shephard

1999.

Filtering via simulation: Auxiliary particle filters.

Journal of the American statistical association,

94(446):590–599.

Polson and Stroud (2003)

Polson, N. and J. Stroud

2003.

Bayesian Inference for Derivative Prices.

In Bayesian Statistics 7, Pp. 641–650.

Oxford University Press.

Storvik (2002)

Storvik, G.

2002.

Particle filters for state-space models with the presence of unknown

static parameters.

IEEE Transactions on signal Processing, 50(2):281–289.

Warty et al. (2016)

Warty, S., H. Lopes, and N. Polson

2016.

Sequential Bayesian learning for stochastic volatility with

variance-gamma jumps in returns (with discussion).

Applied Stochastic Models in Business and Industry, to appear.

Yun (2014)

Yun, J.

2014.

Out-of-sample density forecasts with affine jump diffusion models.

Journal of Banking & Finance, 47:74–87.

Appendix A: Particle Filtering Methods

State space models (Carlin et al. (1992); Duffie (1996); Johannes and Polson (2010)) are central

to inference in financial econometrics. Particle filtering methods are designed to provide state

inference (Gordon et al. (1993); Carpenter et al. (1999); Pitt and Shephard (1999); Storvik (2002); Carvalho et al. (2010)).

Let denote the data, and the state variable. For example, in Merton’s jump stochastic

volatility model, the state variable is , corresponding to the jump times and sizes

and stochastic volatility. Let denote the unknown parameters relating to the dynamics of the

underlying jump and stochastic volatility distributions. For the moment, we suppress the conditioning

on the parameters . We now show how a PF algorithm updates state variables.

We can factorize the joint posterior distribution of the data and state variables both ways as

The goal is to obtain the new filtering distribution from the current

. A particle representation of the previous filtering distribution is a

random histogram of draws. We denote this by

where is a Dirac measure. As the number of particles increases the law of large numbers guarantees that this distribution converges to the true filtered distribution .

In order to provide random draws of the next distribution, we first resample ’s using the smoothing distribution obtained by Bayes rule.

Thus, we draw via an

index from a multinomial with weights

We set and “propagate” to the next time using

Given a particle approximation to

, we can use Bayes rule to write

where the particle weights are given by

This mixture distribution representation leads to a simple simulation approach for propagating particles to the next filtering distribution.

The algorithm consists of two steps:

To implement this algorithm, we need the predictive likelihood for the next observation, ,

given the current state variable . It is defined by

We also need the conditional posterior for the next states given , given by

Our algorithm has several practical advantages. First, it does not suffer from the problem of particle

degeneracy which plagues the standard sample-importance resample filtering algorithms. This effect is

heightened when is an outlier. Second, it can easily be extended to incorporate sequential

parameter learning. It is common to also require learning about other unknown static parameters, denoted by

. To do this, we assume that there exists a conditional sufficient statistic for

at time, namely

where .

Moreover, we can propagate these sufficient statistics by the deterministic recursion

In the next section we develop the sufficient statistics and appropriate recursions for Merton’s jump stochastic volatility model.

This will lead to efficient inference for all model parameters.

Given particles . First, we

resample with weights

proportional to . Then we propagate to the next

filtering distribution

by drawing from

. We next

update the sufficient statistic for ,

This represents a deterministic propagation. Parameter learning is

completed by drawing using for

. We now gives specifics of the algorithm for two models, the Merton model

with constant and stochastic volatility.

We now track the state, , and conditional sufficient statistics, , which will be used to perform off-line learning for .