Distributed Simultaneous Inference in Generalized Linear Models via Confidence Distribution

Abstract

We propose a distributed method for simultaneous inference for datasets with sample size much larger than the number of covariates, i.e., , in the generalized linear models framework. When such datasets are too big to be analyzed entirely by a single centralized computer, or when datasets are already stored in distributed database systems, the strategy of divide-and-combine has been the method of choice for scalability. Due to partition, the sub-dataset sample sizes may be uneven and some possibly close to , which calls for regularization techniques to improve numerical stability. However, there is a lack of clear theoretical justification and practical guidelines to combine results obtained from separate regularized estimators, especially when the final objective is simultaneous inference for a group of regression parameters. In this paper, we develop a strategy to combine bias-corrected lasso-type estimates by using confidence distributions. We show that the resulting combined estimator achieves the same estimation efficiency as that of the maximum likelihood estimator using the centralized data. As demonstrated by simulated and real data examples, our divide-and-combine method yields nearly identical inference as the centralized benchmark.

keywords:

Bias correction , Confidence distribution , Inference , Lasso , Meta-analysis , Parallel computing.MSC:

[2010] Primary 62H15 , Secondary 62F12This paper is published in Journal of Multivariate Analysis, https://doi.org/10.1016/j.jmva.2019.104567.

For citation, please use

Tang, L., Zhou, L., & Song, P.X.K. (2020). Distributed simultaneous inference in generalized linear models via confidence distribution. Journal of Multivariate Analysis, 176, 104567.

1 Introduction

We consider simultaneous inference for the generalized linear model (GLM) under the situation where data are stored on distributed computer clusters instead of a centralized location. The use of distributed storage can be due to either large data volume or protection of individual-level sensitive data from leaving data-owning entities. Such distributed data presents great challenges in statistical analyses because the entire dataset cannot be loaded once to a single processor for computation [9]. In the advent of cloud storage and computing, the method of divide-and-combine, also known as divide-and-conquer [1], has become the state-of-the-art in big data analytics to effectively improve scalability. Divide-and-combine is a computational procedure that divides the data into relatively independent, smaller and computable batches, processes them in parallel and combines the separate results. However, not all existing statistical methods are directly parallelizable. Some complicated methods require special treatment in order to be adapted to the parallel computing architecture; see for examples, parallel matrix factorization by randomized matrix approximation in [22], scalable bootstrap by bag of little boostraps in [16], divide-and-combine-type kernel ridge regression in [40], and communication efficient lasso regression in [17], among others. In this paper, we consider simultaneous inference for the GLM using divide-and-combine. While both the sample size and the number of covariates may be large in practice, here we focus on the case when , but is not small and can vary from hundreds to thousands. The observations are split into mutually independent sub-datasets.

Meta-analysis is an example of divide-and-combine that combines summary statistics from independent studies, see for examples [29, 28, 14]. The classical fixed-effect meta-analysis uses inverse variance weighted average to combine separate point estimates. Raw data can be processed locally and only summary quantities are communicated between machines to reduce cost of data transfer [17]. In the development of distributed algorithms for statistical inference, one question arises naturally: are the proposed divide-and-combine estimators and the maximum likelihood estimator (MLE) obtained from the centralized data asymptotically equivalent, leading to comparable statistical inferences? Lin and Zeng [19] showed that such a meta-estimator asymptotically achieves the Fisher’s efficiency; in other words, it follows asymptotically the same distribution as the centralized MLE. The Fisher’s efficiency has also been established for a combined estimator by [20] through aggregating estimating equations under a relatively strong condition that is of order where and is the sample size of a sub-dataset. Recently, Battey et al. [2] proposed test statistics and point estimators in the context of the divide-and-combine, where the method of hypothesis testing is only developed for low dimensional parameters, and the combined estimator takes a simple form of an arithmetic average over sub-datasets. Different from [2], we consider simultaneous inference for all parameters and use the inverse of variance-covariance matrices to combine estimates.

Although the overall sample size is large, it is reduced times in the sub-datasets due to data partition. The sample size reduction and potentially unbalanced sample sizes across sub-datasets may cause numerical instability in the search for the MLE, especially in overfitted models when most of covariates are unimportant among all covariates that are included in the analysis. As shown in Section 4, coverage probabilities of confidence intervals obtained by the classical meta-analysis method deviate drastically from the nominal level as increases. This motivates the use of regularized regression to overcome such numerical instability. For regularized estimators, such as lasso [31] and SCAD [10], constructing confidence intervals is analytically challenging because: (i) sparse estimators usually do not have a tractable limiting distribution, and (ii) the oracle property [10] relying on knowledge of the truly non-zero parameters is not applicable to statistical inference since the oracle is unknown in practice.

When penalized regression is applied on each sub-dataset, variable selection procedures will choose different sets of important covariates by different tuning schemes. Such misaligned selection prohibits any weighting approaches from combining the separate results; both dimensionality and meaning of the estimates across sub-datasets may be very different. Chen and Xie [4] proposed a majority-voting method to combine the estimates of the covariates most frequently identified by the lasso across the sub-datasets. Unfortunately, this method does not provide inference for the combined estimator, and it is sensitive to the choice of inclusion criterion. To fill in this gap, we propose a new approach along the lines of the post-selection inference developed for the penalized estimator by [13] and [39], which allows us to combine bias-corrected lasso estimators obtained from sub-datasets.

In this paper, we use the confidence distribution approach [36] to combine results from the separate analyses of sub-datasets. The confidence distribution, originally proposed by Fisher [11] and later formally formulated by Efron [8], has recently attracted renewed attention in the statistical literature; see for examples, [26, 36] and references therein. An advantage of the confidence distribution approach is that it provides a unified framework for combining distributions of estimators, so statistical inference with the combined estimator can be established in a straightforward and mathematically rigorous fashion. Specifically related to divide-and-combine, Xie et al. [37] developed a robust meta-analysis-type approach through confidence distribution, and Liu et al. [21] proposed to combine the confidence distribution functions in the same way as combining likelihood functions for inference, and showed their estimator achieves the Fisher’s efficiency. The step of combining via confidence distribution theory requires well-defined asymptotic joint distributions of all model parameters of interest, which, in the current literature, are only available for less than , the sample size of one sub-dataset under equal data split. Here, we consider the scenarios where and can both diverge to infinity with rates slower than . Our new contribution is two-fold: (i) the combined estimator achieves asymptotically the Fisher’s efficiency; that is, it is asymptotically as efficient as the MLE obtained from the direct analysis on the full data; and (ii) the distributed procedure is scalable and parallelizable to address very large sample sizes through easy and fast parallel algorithmic implementation. The latter presents a desirable numerical recipe to handle the case when the centralized data analysis is time consuming and CPU demanding, or even numerically prohibitive.

This paper is organized as follows. Section 2 focuses on the asymptotics of the bias-corrected lasso estimator in sub-datasets. Section 3 presents the confidence distribution method to combine results from multiple regularized regressions. Section 4 provides extensive simulation results, and Section 5 illustrates our method by a real data. We conclude in Section 6. We provide key technical details in the Appendix and defer complete proofs and supporting information to the Supplementary Material.

2 Distributed Penalized Regressions for Sub-datasets

For GLM, the systematic component is specified by the mean of a response that is related to a -dimensional vector of covariates by a known monotonic canonical link function in the form , for subject . The random component is specified by the conditional density of given . The variance of the response takes the form of where is the dispersion parameter and is the unit variance function [23]. The associated likelihood function is given by where and the canonical parameters have the form , with being the -element vector of regression parameters of interest.

The centralized MLE solution, , in general has no closed-form expression, except for the Gaussian linear model, and is often obtained numerically by certain iterative algorithms such as Newton-Raphson. Thus, it is not trivial to establish exact parallel algorithms that only require a single passing of each sub-dataset, and still achieve the same efficiency as the centralized MLE. Sample partition naturally results in sub-datasets, each with size , and .

This section focuses on deriving the regularized estimator and confidence distribution for a single sub-dataset of sample size for a specific . Since the method in this section is general to all sub-datasets, for ease of exposition, we suppress unless otherwise noted. We start by deriving the asymptotic properties of lasso regularized regression, as our divide-and-combine procedure is dependent on the asymptotic results. The regularization plays an important role in stabilizing numerical performance on the divided datasets, which will be shown in later sections. We use lasso [31] in the development of this paper. With little effort, other types of regularization, such as SCAD [10] or elastic net [42], may be adopted in our proposed procedure.

2.1 Lasso in Generalized Linear Models

The lasso estimator is obtained by maximizing the following penalized log-likelihood function with respect to the regression parameters subject to a normalizing constant,

where is a nonnegative tuning parameter, and is the -norm of the regression coefficient vector . Let be a lasso estimator of at a given tuning parameter . Solution may be obtained by coordinate descent via Donoho and Johnstone [7]’s soft-thresholding approach, with the tuning parameter being determined by, say, cross-validation [25].

2.2 Confidence Distribution for Bias-corrected Lasso Estimator

To combine multiple lasso estimators obtained from separate sub-datasets, we need to overcome the issue of misalignment: the sets of selected covariates with non-zero estimates in the model are different across sub-datasets. Our solution is based on bias-corrected lasso estimators. The bias correction enables us not only to obtain non-zero estimates of all regression coefficients, but also, more importantly, to establish the joint distribution of regularized estimators. The latter is critical for us to utilize the confidence distribution to combine estimators, which will be described in Section 3.

Denote the score function by . It is known that the lasso estimator, , satisfies the following Karush-Kuhn-Tucker (KKT) condition: where subdifferentials satisfy , and if . The first-order Taylor expansion of in the KKT condition at the true value leads to It follows that where is a bias-corrected lasso estimator [13]:

| (1) |

The second equality in (1) follows directly from the KKT condition and the definition of the sensitivity matrix , which is assumed to be a positive-definite Hessian matrix, and is the variance function. For now, let us first consider the case when . We show in Theorem 1 that under some regularity conditions, is asymptotically normally distributed, namely,

| (2) |

where . Based on the joint asymptotic normality in (2), following [36], we form the asymptotic confidence distribution density function of as . Replacing in (1) by the sparse lasso estimator , we obtain

| (3) |

Likewise, replacing by in the asymptotic covariance in (2) leads to a “data-driven” asymptotic confidence density

| (4) |

It is worth pointing out that this bias-corrected estimator in (3) is equivalent to a one-step Newton-Raphson updated estimator of the lasso estimator. In the GLM framework, we have where is the diagonal matrix of the variance functions. When the dispersion parameter is unknown, e.g., in the linear regression setting, we use a root- consistent estimator , where is the number of non-zero entries of vector , , and is the unit deviance function; refer to [27, Chapter 2] for details.

2.3 Examples

Example 1.

Gaussian linear model. Assume follows a normal distribution with mean , variance function , and link function . The score function takes the form . The confidence density function in (4) is obtained by plugging in the bias-corrected estimator . Here

Example 2.

Binomial logistic model. Assume follows a Bernoulli distribution with probability of success , variance function , link function and . Similarly, we obtain its confidence density with where , and .

Example 3.

Poisson log-linear model. Assume follows a Poisson distribution with mean , variance function , link function and . We can obtain with where , and .

2.4 Large Sample Property

From here on, we bring back the subscript to denote a quantity concerning the th sub-dataset as the results will be carried forward to Section 3 where we discuss the combination step. Let and denote the minimum and maximum singular values of a matrix , respectively. Let and be the minimum and maximum across the set of constants , . Denote the signal set by and the non-signal set by , where is the true coefficient. Here we allow and may diverge to infinity. To establish large-sample properties for given in (3) based on the th sub-dataset , and subsequently the combined estimator in Section 3 across all sub-datasets, we postulate the following regularity conditions:

(C1) Assume the score function is unbiased, namely,

(C2) Assume for constants and , and for some , where .

(C3) For some , for all satisfying , it holds that , where is the number of true signals in and . In addition, assume and .

(C4) Assume the same underlying true parameters , . Denote the common signal set, non-signal set, and number of signals as , and , respectively, for all . Further, assume and .

Conditions (C1) and (C2) are two mild regularity conditions widely used in the literature; see for example [21]. It follows from condition (C2) that, with for some positive constants , and . Condition (C3) is the compatibility condition required to ensure the convergence of lasso estimator in terms of both and norm [3]. When with , condition (C3) states that must be of the order of in the GLM, which is slightly stronger than order , a usual condition required in the linear model; see for examples [39] and [13] and detailed discussion therein. Condition (C4) is the model homogeneity assumption as well as the uniformly bounded assumption across sub-datasets, which is required to combine results, as considered in Theorem 2.

Theorem 1.

Under conditions (C1)-(C3), for , , and any fixed integer , let be a matrix of rank with . Then the fixed-length bias-corrected estimator , with given in (3), is consistent and asymptotically normally distributed, namely, as where , and .

Theorem 1 may be viewed as an extension of the covariate-wise asymptotic result in [13] to the joint asymptotic distribution on , a fixed-length sub-vector of . Matrix chosen under a target subset of parameters allows to perform a joint inference, and univariate inference is a special case with . We emphasize the need of a joint asymptotic distribution in order to use the method of confidence distribution in (4) to combine results in Section 3. This is a critical step to yield a combined estimator and related inference. Corollary 1 establishes the validity of the bias-corrected lasso estimator with being selected via the commonly used R-fold cross-validation procedure. It shows that such satisfies a sufficient condition required by Theorem 1, and can be tuned locally within individual sub-datasets. In effect, when the sample sizes are balanced, a single tuning parameter is needed. However, to synchronously tune a common across sub-datasets will introduce additional overhead cost in communication. Thus, we keep parameter tuning separate. More discussion is given in Remark 5 in Section 3. A brief proof of Theorem 1 is given in the Appendix, and the complete proofs of Theorem 1 and Corollary 1 are given in the Supplementary Material.

Corollary 1.

Under the same conditions of Theorem 1, for any finite integer , has the same asymptotic distribution with the tuning parameter being obtained from -fold cross-validation using the th sub-dataset.

Remark 1.

The procedure based on Theorem 1 for the construction of the confidence density remains valid when the adaptive lasso estimator [41] is used to replace in (3) and (4). An adaptive lasso estimator is obtained by where the weights are given by , with an initial root- consistent estimate of and some suitable constant , which is typically set to 1.

Remark 2.

Collinearity is often encountered in high-dimensional data analysis where some of the covariates are highly correlated. One solution is to construct the confidence distribution in (4) by using the KKT condition of the elastic net estimator [42]. Another remedy to improve numerical stability is to use a ridge-type estimator by adding a ridge term , where , to stabilize the matrix inverse of , i.e., .

3 Combined Estimation and Inference

We now consider a full data of size being partitioned into sub-datasets, , each with size , and . Here, both and are allowed to diverge along with . Let be the sample size infimum as and grow. Consider a target parameter set , where is fixed. At a rate , we obtain , where is the log-likelihood function of the th sub-dataset . If there existed a “god-made” computer with unlimited computational capacity to store and process the full data, the centralized MLE could be applied directly to obtain where is the log-likelihood function of the full data . Arguably, is the gold standard for inference. There are many ways to combine estimates obtained from sub-datasets. This paper considers using the confidence distribution due to its generalizability under unified objective functions and its ease in establishing statistical inferences. For each sub-dataset , we first apply Theorem 1 to construct the asymptotic confidence density , . Then, in the same spirit as [21], we may combine the confidence densities to derive a combined estimator of , denoted by , where refers to divide-and-combine, given as follows:

| (5) |

where and is the estimate given in (3) with respect to the th sub-dataset . The key advantage of the approach in (5) is to derive an inference procedure for the combined estimator , as stated in Theorem 2 under diverging .

Theorem 2.

Assume . Under conditions (C1)-(C4), if and , respectively, for all , then the MODAC estimator obtained from (5) is consistent and asymptotically normally distributed, namely, as , with , where the latter is the centralized Fisher information matrix of the full data. That is, the MODAC is asymptotically as efficient as the centralized MLE .

The key result of Theorem 2 is that the combined estimator and the gold standard MLE are asymptotically equally efficient. Although it may be tempting to allocate CPUs to speed up computation, the order of in Theorem 2 guides us to choose a proper number of CPUs to ensure that each CPU has enough samples. It is worth noting that the dispersion parameter is not required to be homogeneous across sub-datasets as it does not affect the estimation; and the divide-and-combine estimator does not require additional conditions than those required by the regularized estimator in each sub-dataset. This is because constructing confidence densities makes the individual asymptotic normal distributions readily available, and the asymptotic distribution of the combined estimator follows. The practical implication of Theorem 2 is that as long as the sample size of each sub-dataset is not too small, the proposed will have little loss of estimation efficiency, while enjoying fast computing in the analysis of big data. The proof of Theorem 2 is given in the Appendix.

For the ease of exposition, without loss of generality, we may take , i.e., . In this way, we can stick on the notation of in the rest of this paper. By simple algebra, the solution to the divide-and-combine estimator (5) can be expressed explicitly as a form of weighted average of , as follows:

| (6) |

where . Note that the inverse matrix in (6) is readily available from the confidence distribution of each sub-dataset. The only matrix inversion required is for the sum of the Fisher information matrices. It follows that the variance-covariance matrix of is estimated by , from which confidence regions for any sub-vector of can be obtained by using standard multivariate analysis methods [15].

Remark 3.

Note that when for all , our proposed estimator in (6) reduces to the classical meta-estimator . Lin and Xi [20] found a similar result as a special case of the aggregated estimating equation estimator. However, the aggregated estimating equation estimator requires a strong assumption of , and it does not consider regularized estimation for variable selection. In addition, regardless of and in (6) taking the same form, they are derived from different criteria with different purposes. Specifically, aims to improve statistical power via weighted average, while is obtained by minimizing the combined confidence densities for the interest of statistical inference theory. The flexibility of the confidence density approach allows incorporating additional features in the combination; for example, the homogeneity may be relaxed by imposing a mixture of normals in (5), which is not feasible in the meta-estimator.

Remark 4.

A majority voting approach [4] to combine sparse estimates from sub-datasets takes the form where is a set of selected signals in terms of a prespecified voting threshold , denotes a corresponding sub-vector of the lasso estimate , and is a subsetting matrix corresponding to set . The majority voting estimator has been shown to have the oracle property, which, however, is not applicable to statistical inference.

Remark 5.

The role of tuning in individual datasets is not to induce sparsity in the final aggregated estimate, but to produce intermediate sparse estimates that give rise to a robust approximation of the covariance in the individual confidence distributions. Since the bias-correction procedure offsets the effect of sparsity tuning, the choice of tuning parameter becomes of little relevance to the means of the derived confidence distributions. The purpose of our integrative inference distinguishes from those estimation methods given in [17, 35] that aim to produce aggregated sparse estimates, in which a common tuning parameter has to be chosen across all sub-datasets. As a result, their estimation methods require one more round of synchronization, whereas in ours, tuning can be done in parallel (from Corollary 1).

The overall computational complexity of centralized MLE based on Fisher’s scoring is of order [32], which is dominated by the cost of matrix inversion. The complexity of divided procedures in MODAC involves coordinate descent (of order when is given [12]) and evaluating Fisher information matrix (of order ), for each sub-dataset. The aggregation step involves summation of order and matrix inversion of order . Therefore, the complexity under the ideal parallel situation is of order . Even in the worst scenario when parallel procedures are run sequentially, the upper bound of overall complexity of MODAC is , which remains comparable to that of the centralized MLE. Similarly, the complexity of the distributed meta-estimator is at order with an upper bound . The value is purely dependent on the choice of a matrix inversion algorithm, and it ranges over for some efficient algorithms.

4 Simulation Studies

In this section, we demonstrate the numerical performance of our method under linear, logistic and Poisson regressions through simulation experiments. Specifically, we compare across three divide-and-combine methods, including the meta-analysis method by inverse variance weighted averaging described in Remark 3, the majority voting method described in Remark 4, and our method. Note that when , under no data partition, meta-analysis is equivalent to the centralized MLE, the majority voting method is equivalent to the centralized lasso regression [31], and our method is equivalent to centralized lasso with post-selection inference from Theorem 1.

All methods are compared thoroughly on the performance of variable selection, statistical inference and computation time. The evaluation metrics for variable selection include the sensitivity and specificity of correctly identifying non-zero coefficients. The evaluation metrics for statistical inference include mean squared error, absolute bias, coverage probability and asymptotic standard error of coefficients in the signal set and the non-signal set , respectively. Coverage probabilities and standard errors are not reported for the majority voting method since it does not provide inference.

We use results from the centralized MLE, , as our gold standard in all comparisons. In order to ensure the best variable selection results of the majority voting method, we carefully select in such that the sum of sensitivity and specificity is maximized.

The computation time of all methods includes the time taken to read data from disks to memory and the time taken by numerical calculations. Under the divide-and-combine setting with , computation time is reported as the sum of the maximum time used among parallelized jobs and the time used to combine results.

All shrinkage estimates are obtained by applying the R package glmnet with tuning parameter selected to yield the smallest average 10-fold cross-validated error.

All simulation experiments are conducted by R software on a standard Linux cluster with 16 GB of random-access memory per CPU.

Table 1 presents the simulation results from a moderate size dataset with and so that methods without data partition can be repeated in multiple rounds of simulations within a reasonable amount of time. Clearly, this is a typical regression data setting with . We consider linear, logistic and Poisson models, with responses generated from the mean model , with covariates generated from the multivariate normal distribution with mean zero and variance one, and with a compound symmetric covariance structure with correlation , a simulation setting similar to that considered by [13]. We report scenarios when the full dataset is randomly divided into and subsets of equal sizes, each with sample size and , respectively. Results for are also reported. We randomly select coefficients from to be set at non-zero. The non-zero coefficients are set to for linear models, for logistic models, and for Poisson models. CMLE, META, MV and MODAC denote the centralized MLE, meta-analysis, majority voting and our method of divide-and-combine (MODAC), respectively. Results are based on 500 replications.

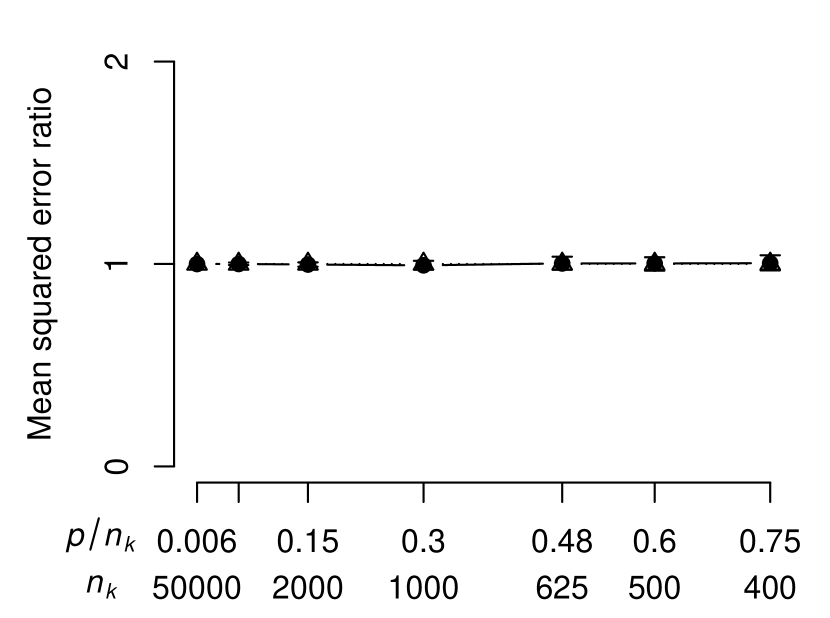

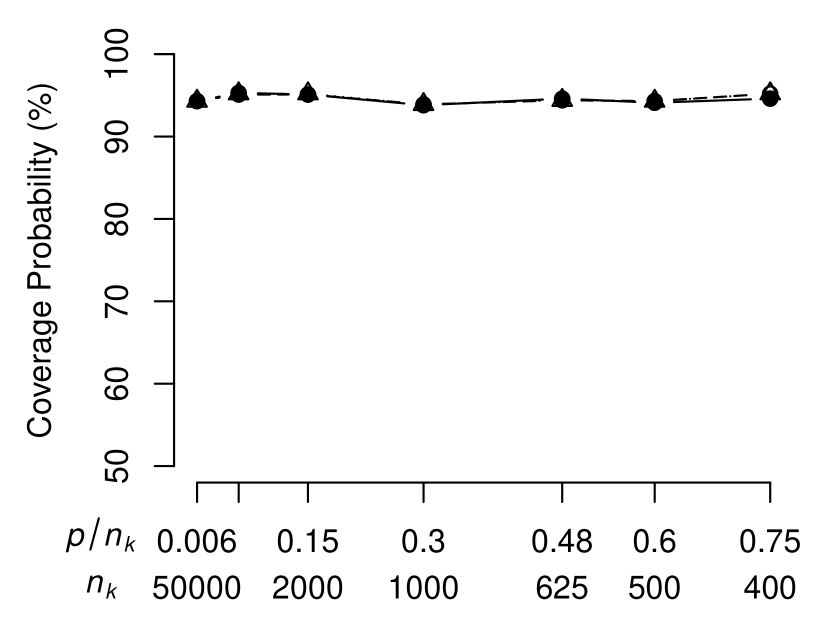

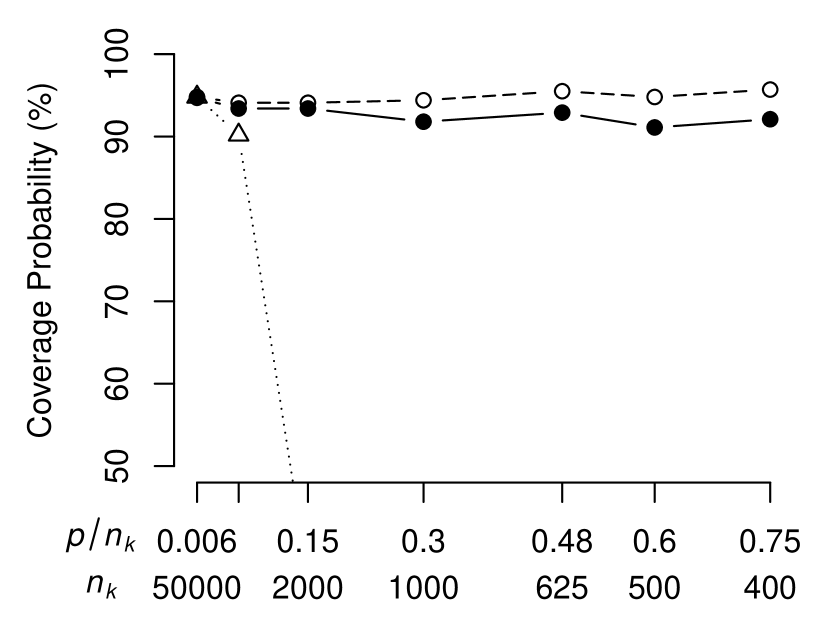

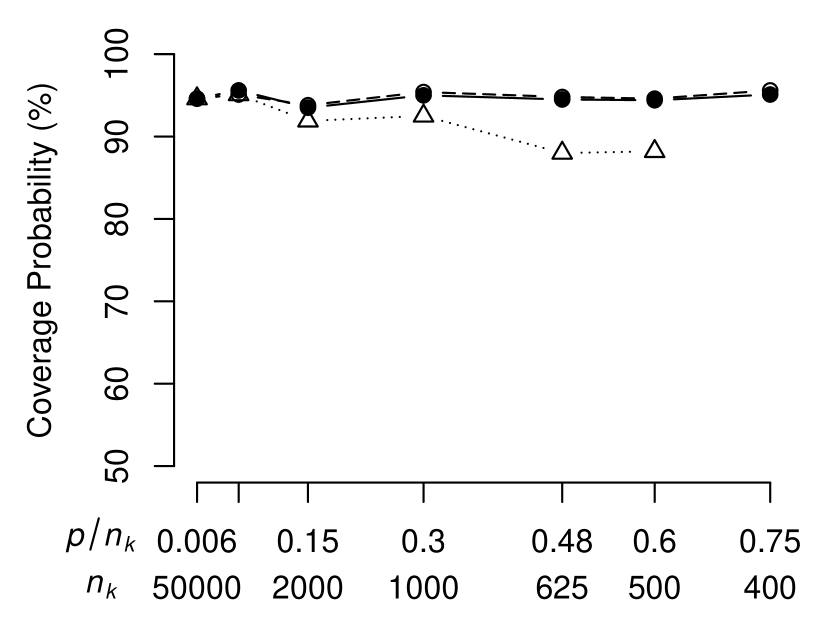

The results of the Gaussian linear model in Table 1 reassuringly show that all methods perform as well as the gold standard. META and MODAC exhibit identical performances as that of CMLE regardless of the choices of . This is because under the linear model, CMLE can be directly parallelized, so META and MODAC solutions are exact and identical to CMLE. Among all methods, MV has the highest sensitivity and specificity when for and for . This shows the improvement of selection consistency by divide-and-combine. Under the same model settings, Figs. 1 and 2 display additional simulation results at varying choices of with fixed at , summarized over 100 replications. Fig. 1 shows the ratio comparison of mean squared error of META and MODAC, respectively, to that of CMLE, for as increases. Fig. 2 compares the coverage probabilities of between CMLE, META and MODAC. Since META and MODAC are identical to CMLE, their mean-squared errors and coverage probabilities are almost identical, as shown in Figs. 1(a) and 2(a).

| Linear Model | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| CMLE | META | META | MV | MV | MV | MODAC | MODAC | MODAC | |

| () | () | () | () | () | () | () | () | () | |

| () | () | ||||||||

| Sensitivity | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Specificity | 0.95 | 0.95 | 0.95 | 0.91 | 1.00 | 1.00 | 0.95 | 0.95 | 0.95 |

| MSE of () | 0.01 | 0.01 | 0.01 | 0.03 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 |

| MSE of () | 0.01 | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.01 |

| Absolute bias of | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 |

| Absolute bias of | 0.01 | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.01 |

| Cov. prob. of | 0.95 | 0.95 | 0.95 | — | — | — | 0.95 | 0.95 | 0.95 |

| Cov. prob. of | 0.95 | 0.95 | 0.95 | — | — | — | 0.95 | 0.95 | 0.95 |

| Asymp. st. err. of | 0.01 | 0.01 | 0.01 | — | — | — | 0.01 | 0.01 | 0.01 |

| Asymp. st. err. of | 0.01 | 0.01 | 0.01 | — | — | — | 0.01 | 0.01 | 0.01 |

| Computation time | 34.85 | 0.62 | 0.20 | 31.50 | 2.16 | 2.08 | 36.61 | 2.28 | 2.14 |

| Logistic Model | |||||||||

| CMLE | META | META | MV | MV | MV | MODAC | MODAC | MODAC | |

| () | () | () | () | () | () | () | () | () | |

| () | () | ||||||||

| Sensitivity | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Specificity | 0.95 | 1.00 | 1.00 | 0.89 | 1.00 | 1.00 | 0.95 | 0.95 | 0.96 |

| MSE of () | 0.08 | 0.57 | 189.38 | 0.23 | 0.20 | 0.29 | 0.08 | 0.09 | 0.10 |

| MSE of () | 0.08 | 0.05 | 4.15 | 0.00 | 0.00 | 0.00 | 0.08 | 0.08 | 0.07 |

| Absolute bias of | 0.02 | 0.07 | 1.36 | 0.04 | 0.04 | 0.05 | 0.02 | 0.02 | 0.02 |

| Absolute bias of | 0.02 | 0.02 | 0.16 | 0.00 | 0.00 | 0.00 | 0.02 | 0.02 | 0.02 |

| Cov. prob. of | 0.95 | 0.36 | 1.00 | — | — | — | 0.95 | 0.94 | 0.92 |

| Cov. prob. of | 0.95 | 1.00 | 1.00 | — | — | — | 0.95 | 0.95 | 0.96 |

| Asymp. st. err. of | 0.03 | 0.03 | 1895.12 | — | — | — | 0.03 | 0.03 | 0.03 |

| Asymp. st. err. of | 0.03 | 0.03 | 1893.23 | — | — | — | 0.03 | 0.03 | 0.03 |

| Computation time | 66.01 | 1.63 | 1.40 | 260.48 | 15.78 | 10.42 | 266.09 | 15.92 | 10.53 |

| Poisson Model | |||||||||

| CMLE | META | META | MV | MV | MV | MODAC | MODAC | MODAC | |

| () | () | () | () | () | () | () | () | () | |

| () | () | ||||||||

| Sensitivity | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Specificity | 0.95 | 0.94 | 0.91 | 0.91 | 1.00 | 1.00 | 0.95 | 0.95 | 0.95 |

| MSE of () | 0.70 | 0.80 | 0.90 | 1.70 | 0.80 | 0.50 | 0.70 | 0.70 | 0.70 |

| MSE of () | 0.70 | 0.70 | 0.80 | 0.00 | 0.10 | 0.00 | 0.70 | 0.70 | 0.70 |

| Absolute bias of | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.00 | 0.01 | 0.01 | 0.01 |

| Absolute bias of | 0.01 | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.01 |

| Cov. prob. of | 0.95 | 0.93 | 0.90 | — | — | — | 0.95 | 0.95 | 0.95 |

| Cov. prob. of | 0.95 | 0.94 | 0.91 | — | — | — | 0.95 | 0.95 | 0.95 |

| Asymp. st. err. of | 0.01 | 0.01 | 0.01 | — | — | — | 0.01 | 0.01 | 0.01 |

| Asymp. st. err. of | 0.01 | 0.01 | 0.01 | — | — | — | 0.01 | 0.01 | 0.01 |

| Computation time | 42.26 | 1.46 | 0.40 | 132.06 | 26.57 | 25.00 | 136.85 | 26.67 | 25.08 |

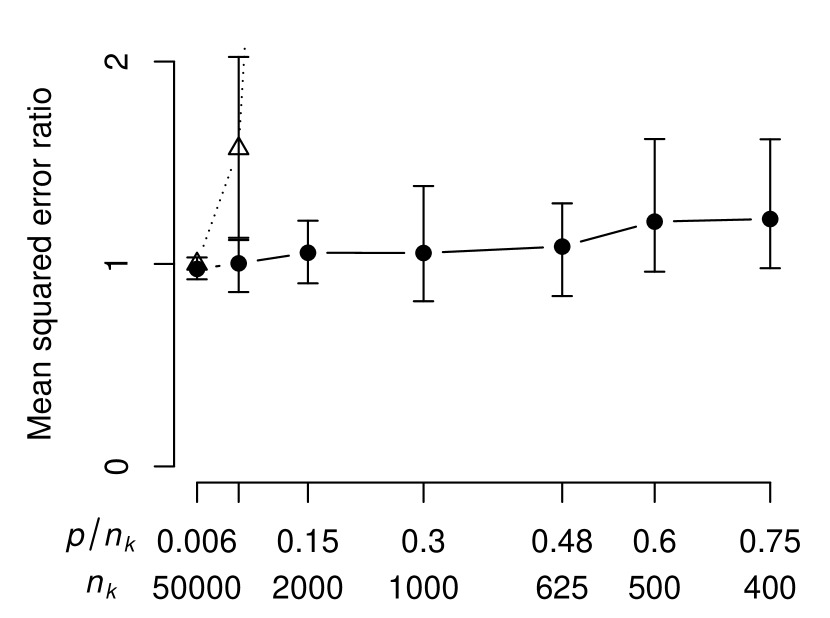

The existence of exact solutions for divide-and-combine methods under the linear model no longer holds in other generalized linear models, where iterative numerical procedures are needed to search for the estimates. For example in the logistic model, the ratio is responsible for numerical stability, as shown in Figs. 1(b) and 2(b). When approaches one, the mean squared errors and coverage probabilities of META quickly deviate from those of CMLE, whereas MODAC remains stable. Although is much smaller than , data partitioning may sometimes result in closer to for some sub-datasets. Regularization is shown in our simulation to be an appealing strategy to reduce the dimension of the optimization to achieve more stable numerical performance. The regularization helps stabilize the Newton-Raphson iterative updating algorithm, in which the Hessian matrix may be otherwise poorly estimated in case of being close to one. The numerical results of META appear to be unstable within each sub-dataset in both cases and . Such poor numerical performance results from the estimated probabilities approaching the boundaries in , causing the variance estimates too close to 0. In short, META gives biased parameter estimates and overestimated standard errors of these parameter estimates, and is very sensitive to the choice of . On the other hand, through the regularized estimation of , the proposed MODAC exhibits stable performance similar to that of CMLE. The bias of MV for is higher than that of CMLE as expected due to the penalty.

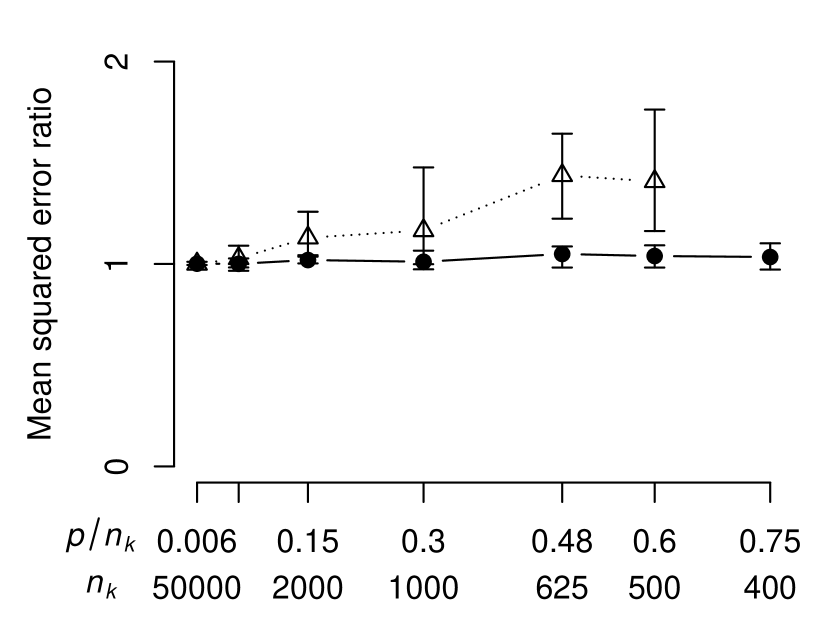

In regard to the Poisson model, Table 1 shows that similar to our findings in the linear and logistic models, MODAC again gives the most stable results among all divide-and-combine methods. On the other hand, META gives improper coverage probabilities in comparison to the nominal 95% level, as well as poorer selection accuracy than CMLE. In Fig. 1(c), we see that the mean squared errors of MODAC is stable against the change of . In contrast, the mean squared errors of META quickly deviates from the mean squared error of CMLE for the Poisson model as increases. In Fig. 2(c), as similar to the logistic model, the 95% confidence interval coverage probabilities of MODAC remains close to the nominal level, whereas the coverage probabilities of META deviates from 95% when gets close to one. MV gives the best variable selection with carefully chosen.

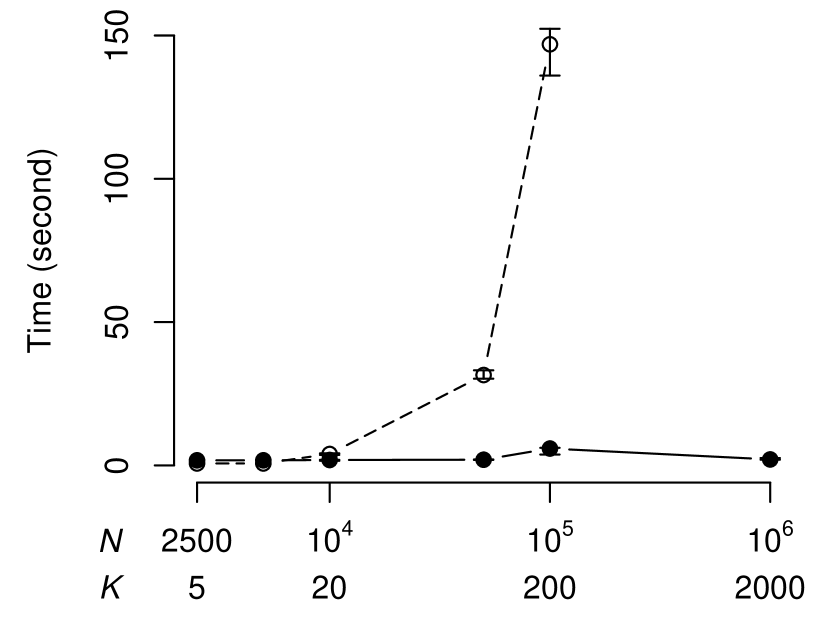

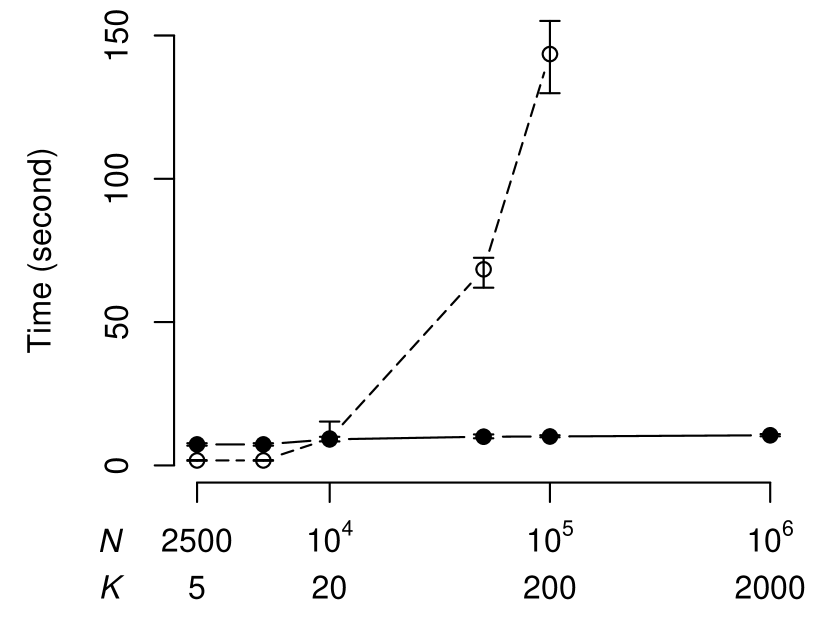

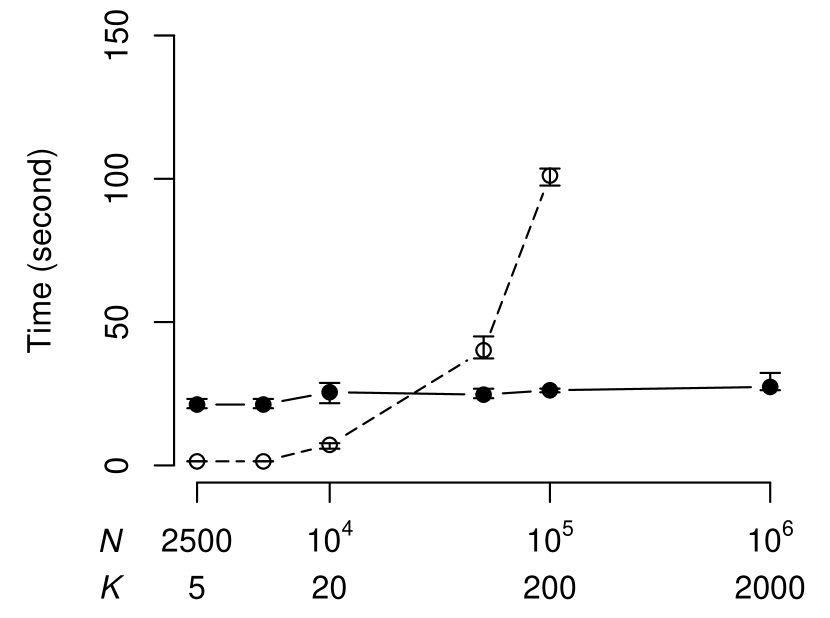

The key message from Table 1 and Figs. 1-2 is that the invocation of regularization greatly helps to achieve consistent and stable mean and variance estimation in the application of divide-and-combine methods. We see that MODAC produces the most comparable results to those of the gold standard, and is virtually unaffected by the partition size . In contrast, the performances of META and MV vary over the partition size . Another noticeable advantage of MODAC is the saving of computation time in comparison to gold standard CMLE due to MODAC’s scalability, as shown in Fig. 3 with increase in and in MODAC, based on 100 replications. We see that the computational burden increases sharply for CMLE as increases, whereas the computation time for MODAC remains almost the same in all three types of models, which clearly demonstrates its scalability. Computation time for CMLE when is not reported because the computation exceeds the maximum memory limit allowed on the Linux cluster. In summary, MODAC achieves significant computation time reduction without sacrificing statistical accuracy. Despite the fact that META is the fastest as it does not involve a tuning parameter selection step, its results are clearly unstable in both the logistic and Poisson models.

We present additional simulations in the Supplementary Material to show (i) sensitivity of MV regarding choices of , (ii) sensitivity of MODAC under different levels of correlation in design matrices, and (iii) comparison with another faster version of CMLE given by R package speedglm.

5 Real Data Application

| CMLE (1.17s) | META (0.03s) | MODAC (0.62s) | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Predictors | Estimate | St. Err. | -value | Estimate | St. Err. | -value | Estimate | St. Err. | -value |

| Age | 0.08 | 0.01 | 0.00 | 0.08 | 0.01 | 0.00 | 0.08 | 0.01 | 0.00 |

| If any other passenger | -0.17 | 0.03 | 0.00 | -0.16 | 0.03 | 0.00 | -0.17 | 0.03 | 0.00 |

| If passenger below 14 | -0.31 | 0.06 | 0.00 | -0.27 | 0.06 | 0.00 | -0.26 | 0.05 | 0.00 |

| If driver female | -0.08 | 0.03 | 0.01 | -0.08 | 0.03 | 0.02 | -0.08 | 0.03 | 0.01 |

| Driver weight | 0.10 | 0.01 | 0.00 | 0.09 | 0.01 | 0.00 | 0.10 | 0.01 | 0.00 |

| Driver height | -0.09 | 0.02 | 0.00 | -0.08 | 0.02 | 0.00 | -0.09 | 0.02 | 0.00 |

| If restraint used | -1.07 | 0.03 | 0.00 | -1.00 | 0.03 | 0.00 | -1.05 | 0.03 | 0.00 |

| Number of lanes | 0.03 | 0.01 | 0.03 | 0.03 | 0.01 | 0.04 | 0.03 | 0.01 | 0.03 |

| Speed limit | 0.01 | 0.01 | 0.65 | 0.00 | 0.01 | 0.81 | 0.00 | 0.01 | 0.72 |

| Vehicle age | 0.01 | 0.01 | 0.43 | 0.01 | 0.01 | 0.40 | 0.01 | 0.01 | 0.40 |

| Vehicle curb weight | -0.02 | 0.02 | 0.30 | -0.01 | 0.02 | 0.48 | -0.02 | 0.02 | 0.34 |

| If truck | -0.05 | 0.04 | 0.19 | -0.05 | 0.04 | 0.21 | -0.05 | 0.04 | 0.18 |

| If vehicle in previous accident | -0.11 | 0.03 | 0.00 | -0.10 | 0.03 | 0.00 | -0.10 | 0.03 | 0.00 |

| If four wheel drive | 0.01 | 0.04 | 0.69 | 0.02 | 0.04 | 0.67 | 0.01 | 0.04 | 0.70 |

| If drinking involved | 0.00 | 0.04 | 0.90 | 0.01 | 0.05 | 0.78 | 0.00 | 0.04 | 0.90 |

| If drug involved | 0.03 | 0.04 | 0.51 | 0.03 | 0.05 | 0.49 | 0.03 | 0.04 | 0.54 |

| If Hispanic | 0.12 | 0.04 | 0.00 | 0.11 | 0.04 | 0.00 | 0.11 | 0.04 | 0.00 |

| If roadway condition bad | 0.00 | 0.05 | 0.98 | 0.03 | 0.05 | 0.60 | 0.00 | 0.05 | 0.98 |

| If inclement weather | -0.02 | 0.06 | 0.77 | -0.03 | 0.06 | 0.58 | -0.02 | 0.06 | 0.77 |

| Driver race - White (baseline) | |||||||||

| Driver race - Black | -0.07 | 0.03 | 0.03 | -0.06 | 0.03 | 0.07 | -0.07 | 0.03 | 0.03 |

| Driver race - Asian | -0.08 | 0.07 | 0.23 | -0.01 | 0.07 | 0.83 | -0.08 | 0.07 | 0.23 |

| Region - West (baseline) | |||||||||

| Region - Mid-Atlantic | -0.16 | 0.04 | 0.00 | -0.15 | 0.04 | 0.00 | -0.15 | 0.04 | 0.00 |

| Region - Northeast | -0.07 | 0.06 | 0.22 | -0.04 | 0.06 | 0.52 | -0.07 | 0.06 | 0.23 |

| Region - Northwest | 0.27 | 0.05 | 0.00 | 0.26 | 0.05 | 0.00 | 0.28 | 0.05 | 0.00 |

| Region - South | -0.29 | 0.05 | 0.00 | -0.26 | 0.05 | 0.00 | -0.27 | 0.04 | 0.00 |

| Region - Southeast | -0.29 | 0.06 | 0.00 | -0.25 | 0.06 | 0.00 | -0.26 | 0.06 | 0.00 |

| Region - Southwest | -0.13 | 0.04 | 0.00 | -0.12 | 0.04 | 0.00 | -0.12 | 0.04 | 0.00 |

| Light condition - daylight (baseline) | |||||||||

| Light condition - dark | 0.05 | 0.05 | 0.24 | 0.07 | 0.05 | 0.16 | 0.05 | 0.04 | 0.26 |

| Light condition - dawn/dusk | -0.02 | 0.06 | 0.76 | 0.03 | 0.07 | 0.71 | -0.02 | 0.06 | 0.76 |

| Light condition - dark/lighted | -0.03 | 0.03 | 0.33 | -0.02 | 0.03 | 0.45 | -0.03 | 0.03 | 0.33 |

| Season - Summer (baseline) | |||||||||

| Season - Spring | 0.12 | 0.03 | 0.00 | 0.11 | 0.04 | 0.00 | 0.11 | 0.03 | 0.00 |

| Season - Fall | 0.01 | 0.04 | 0.83 | 0.00 | 0.04 | 0.93 | 0.00 | 0.03 | 0.88 |

| Season - Winter | 0.03 | 0.04 | 0.34 | 0.03 | 0.04 | 0.46 | 0.03 | 0.04 | 0.37 |

| Trafficway flow - divided with barrier (baseline) | |||||||||

| Trafficway flow - divide without barrier | 0.02 | 0.04 | 0.64 | 0.01 | 0.04 | 0.73 | 0.01 | 0.04 | 0.71 |

| Trafficway flow - not divided | -0.02 | 0.04 | 0.63 | -0.03 | 0.04 | 0.49 | -0.02 | 0.04 | 0.53 |

| Trafficway flow - one way | -0.19 | 0.06 | 0.00 | -0.16 | 0.06 | 0.01 | -0.17 | 0.06 | 0.00 |

| Day of Week - Sun (baseline) | |||||||||

| Day of week - Mon | -0.21 | 0.05 | 0.00 | -0.19 | 0.05 | 0.00 | -0.21 | 0.04 | 0.00 |

| Day of week - Tue | -0.22 | 0.05 | 0.00 | -0.21 | 0.05 | 0.00 | -0.21 | 0.04 | 0.00 |

| Day of week - Wed | -0.09 | 0.04 | 0.03 | -0.09 | 0.05 | 0.06 | -0.09 | 0.04 | 0.03 |

| Day of week - Thu | -0.17 | 0.04 | 0.00 | -0.17 | 0.05 | 0.00 | -0.17 | 0.04 | 0.00 |

| Day of week - Fri | -0.15 | 0.04 | 0.00 | -0.15 | 0.04 | 0.00 | -0.15 | 0.04 | 0.00 |

| Day of week - Sat | -0.19 | 0.04 | 0.00 | -0.18 | 0.04 | 0.00 | -0.18 | 0.04 | 0.00 |

| Year - 2009 (baseline) | |||||||||

| Year - 2010 | -0.06 | 0.04 | 0.15 | -0.05 | 0.04 | 0.26 | -0.05 | 0.04 | 0.18 |

| Year - 2011 | 0.01 | 0.04 | 0.78 | 0.01 | 0.04 | 0.83 | 0.01 | 0.04 | 0.81 |

| Year - 2012 | 0.11 | 0.04 | 0.01 | 0.11 | 0.04 | 0.01 | 0.10 | 0.04 | 0.01 |

| Year - 2013 | 0.08 | 0.04 | 0.08 | 0.07 | 0.04 | 0.09 | 0.07 | 0.04 | 0.09 |

| Year - 2014 | 0.04 | 0.05 | 0.32 | 0.06 | 0.05 | 0.22 | 0.04 | 0.04 | 0.34 |

| Year - 2015 | 0.14 | 0.05 | 0.00 | 0.15 | 0.05 | 0.00 | 0.14 | 0.05 | 0.00 |

We illustrate our method using a publicly available dataset from the National Highway and National Automotive Sampling System Crashworthiness Data System between the years of 2009 and 2015. Details on the access of the data are provided in the Supplementary Material. This national database contains detailed information of about 5,000 crashes each year sampled across the United States. The response variable of interest is a binary outcome of injury severity, where 1 corresponds to a crash leading to moderate or severer injury, and 0 for minor or no injury. Most of the predictors included in this study are categorical, and are transformed into dummy variables before regression. Our logistic regression analysis includes drivers with 48 predictors after the transformation. The full data are randomly partitioned into sub-datasets, each with sample size of about . The logistic regression estimation and inference results are provided in Table 2, which shows the estimated coefficients, standard errors and -values of 48 potential risk factors obtained by CMLE, META and MODAC. Recall that CMLE is the centralized MLE method, which reads in all data batches and fit one logistic regression. CMLE gives the exact solution of maximum likelihood estimate and thus serves as our gold standard for comparisons. In terms of time, MODAC requires 0.66 seconds, one half of that by CMLE, which is 1.17 seconds. MODAC yields the exact same inference result as that of CMLE. Although META is the fastest and finishes in 0.03 seconds, its inference results deviate from those of CMLE and MODAC. For example, as inferred by both CMLE and MODAC, African American is less likely to have moderate to severe injury in a crash than White, and accidents are more likely to result in minor injuries on Wednesday than Sunday; in contrast, META is unable to capture these factors at the same confidence level.

6 Discussion

In this paper, we proposed a scalable regression method in the context of GLM with reliable statistical inference through the seminal work of confidence distribution. Although the divide-and-combine idea has been widely adopted in practice to solve computational challenges arising from the analysis of big data, statistical inference has been little investigated in such setting. We found in this paper that regularized estimation is appealing in the context of the GLM, especially in the logistic regression because regularization can effectively increase the numerical stability of regression analysis where there are many noisy features. In fact, such divide-and-combine inference may adopt other regularized estimators with regular limiting distributions, but we recommend sparse estimators for better numerical stability in estimating the bias terms and approximating the Fisher information matrices.

In practice, heterogeneity in covariate distributions may arise from various forms of distributed data storage over time and/or space. Some careful analyses are required to understand the nature of heterogeneity, which guide us to choose suitable methods in the integrative inference. Our method is essentially applicable to the targeted regression parameters that are the same across the sub-datasets, while both untargeted regression parameters and parameters of the second moments are allowed to differ across sub-datasets. When such targeted parameters are not clearly defined a prior, we may run an additional subgrouping analysis to identify the unknown subpopulations (see examples considered in [30, 34]), and then apply the proposed method to perform a group-based inference. Additionally, extension to allow unbalanced covariates’ distributions and/or missing covariates across sub-datasets is an important direction to account for potential imbalances of data divisions, yet proper inference will require additional conditions similar to those proposed in [18, 33] to handle these complications.

Our method can be readily built in into some of the most popular open source parallel computing platforms, such as MapReduce [5] and Spark [38], to handle massive datasets where sample sizes are in the order of millions. Examples include estimating conversion rates using the Criteo online advertising data that have more than 2 million observations [6] and predicting patient disease status based on 9 million patients’ electronic health records [35]. Although divide-and-combine is not needed for small datasets, our simulation results show that it is still preferable to impose regularization for large using the bias-correction technique. For reproducibility, R code is provided in the Supplementary Material.

Acknowledgments

The authors thank Editor-in-Chief, Associate Editor and two anonymous reviewers for their constructive comments. Zhou’s research was partially supported by the Chinese Fundamental Research Funds for the Central Universities. Song’s research was supported by an National Institutes of Health grant R01 ES024732 and an National Science Foundation grant DMS1811734.

Appendix Proofs

.

Proof of Theorem 1. We present here the key steps in the proof of Theorem 1 and relegate the complete proof to the Supplementary Material (Section LABEL:sec:supp:thm1proof). We explicitly write subscript in the proof because the results will be used in Theorem 1. Denote some positive constants by . For any fixed integer , consider the bias-corrected estimator with , where the lasso estimator satisfies the KKT condition . Let and , where . Under condition (C2), it is easy to show that for any ,

| (7) |

where indicates is positive semi-definite. So is invertible. With , we have

where is a certain value between and . It follows that

According to Corollary 6.2 in [3] and conditions (C1)-(C3), we show that

| (8) |

where .

To show the consistency and asymptotic normality of , we begin with the first-order Taylor expansion on the KKT condition. Under conditions (C1)-(C3), we obtain

| (9) |

where and

Note that from condition (C2) and (7),

| (10) |

Similarly, we have

| (11) |

Furthermore, by the multivariate Lindeberg-Levy central limit theorem [24] and Slutsky’s theorem, the first term in (9) satisfies asymptotically as . Also, under condition (C3) that and , inequalities (8), (10) and (. ‣ Appendix Proofs) guarantee and . Thus, Theorem 1 follows. ∎

.

Proof of Corollary 1. See the Supplementary Material. ∎

.

Proof of Theorem 2. Denote and . It is easy to show . On the other hand,

| (12) | |||||

where the second equality holds under conditions (C1)–(C4). Then, by the law of large numbers, , where the first equation follows from the condition that and the second equation follows from condition that . Furthermore, we have , which is a negative-definite matrix given conditions (C1) and (C2). By combining this with and , the consistency of follows.

By simple algebra, we obtain

and . Applying the condition that with and the central limit theorem, we establish the asymptotic normal distribution of .

References

- Aho and Hopcroft [1974] A. V. Aho, J. E. Hopcroft, Design & Analysis of Computer Algorithms, Pearson Education India, 1974.

- Battey et al. [2018] H. Battey, J. Fan, H. Liu, J. Lu, Z. Zhu, Distributed testing and estimation under sparse high dimensional models, The Annals of Statistics 46 (2018) 1352–1382.

- Bühlmann and van de Geer [2011] P. Bühlmann, S. van de Geer, Statistics for high-dimensional data: methods, theory and applications, Springer Science & Business Media, 2011.

- Chen and Xie [2014] X. Chen, M. Xie, A split-and-conquer approach for analysis of extraordinarily large data, Statistica Sinica 24 (2014) 1655–1684.

- Dean and Ghemawat [2008] J. Dean, S. Ghemawat, Mapreduce: simplified data processing on large clusters, Communications of the ACM 51 (2008) 107–113.

- Diemert Eustache, Meynet Julien et al. [2017] Diemert Eustache, Meynet Julien, P. Galland, D. Lefortier, Attribution modeling increases efficiency of bidding in display advertising, in: Proceedings of the AdKDD and TargetAd Workshop, KDD, Halifax, NS, Canada, August, 14, 2017, ACM, 2017, p. To appear.

- Donoho and Johnstone [1994] D. L. Donoho, J. M. Johnstone, Ideal spatial adaptation by wavelet shrinkage, Biometrika 81 (1994) 425–455.

- Efron [1993] B. Efron, Bayes and likelihood calculations from confidence intervals, Biometrika 80 (1993) 3–26.

- Fan et al. [2014] J. Fan, F. Han, H. Liu, Challenges of big data analysis, National Science Review 1 (2014) 293–314.

- Fan and Li [2001] J. Fan, R. Li, Variable selection via nonconcave penalized likelihood and its oracle properties, Journal of the American statistical Association 96 (2001) 1348–1360.

- Fisher [1956] R. A. Fisher, Statistical methods and scientific inference., Oxford, England: Hafner Publishing Co., 1956.

- Friedman et al. [2010] J. Friedman, T. Hastie, R. Tibshirani, Regularization paths for generalized linear models via coordinate descent, Journal of statistical software 33 (2010) 1.

- van de Geer et al. [2014] S. van de Geer, P. Bühlmann, Y. Ritov, R. Dezeure, On asymptotically optimal confidence regions and tests for high-dimensional models, The Annals of Statistics 42 (2014) 1166–1202.

- Hedges and Olkin [2014] L. V. Hedges, I. Olkin, Statistical methods for meta-analysis, Academic Press, 2014.

- Johnson and Wichern [2002] R. A. Johnson, D. W. Wichern, Applied multivariate statistical analysis, London: Prenticee Hall, 2002.

- Kleiner et al. [2014] A. Kleiner, A. Talwalkar, P. Sarkar, M. I. Jordan, A scalable bootstrap for massive data, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76 (2014) 795–816.

- Lee et al. [2017] J. D. Lee, Q. Liu, Y. Sun, J. E. Taylor, Communication-efficient sparse regression, Journal of Machine Learning Research 18 (2017) 1–30.

- Li et al. [2018] F. Li, K. L. Morgan, A. M. Zaslavsky, Balancing covariates via propensity score weighting, Journal of the American Statistical Association 113 (2018) 390–400.

- Lin and Zeng [2010] D. Lin, D. Zeng, On the relative efficiency of using summary statistics versus individual-level data in meta-analysis, Biometrika 97 (2010) 321–332.

- Lin and Xi [2011] N. Lin, R. Xi, Aggregated estimating equation estimation, Statistics and Its Interface 4 (2011) 73–83.

- Liu et al. [2015] D. Liu, R. Y. Liu, M. Xie, Multivariate meta-analysis of heterogeneous studies using only summary statistics: efficiency and robustness, Journal of the American Statistical Association 110 (2015) 326–340.

- Mackey et al. [2011] L. W. Mackey, M. I. Jordan, A. Talwalkar, Divide-and-conquer matrix factorization, in: Advances in neural information processing systems, pp. 1134–1142.

- McCullagh and Nelder [1989] P. McCullagh, J. A. Nelder, Generalized Linear Models, Chapman & Hall,, 1989.

- Serfling [2009] R. J. Serfling, Approximation theorems of mathematical statistics, volume 162, John Wiley & Sons, 2009.

- Shao and Deng [2012] J. Shao, X. Deng, Estimation in high-dimensional linear models with deterministic design matrices, The Annals of Statistics 40 (2012) 812–831.

- Singh et al. [2005] K. Singh, M. Xie, W. E. Strawderman, Combining information from independent sources through confidence distributions, The Annals of Statistics 33 (2005) 159–183.

- Song [2007] P. X.-K. Song, Correlated data analysis: modeling, analytics, and applications, New York: Springer, 2007.

- Stangl and Berry [2000] D. Stangl, D. A. Berry, Meta-analysis in medicine and health policy, CRC Press, 2000.

- Sutton and Higgins [2008] A. J. Sutton, J. Higgins, Recent developments in meta-analysis, Statistics in Medicine 27 (2008) 625–650.

- Tang and Song [2016] L. Tang, P. X. Song, Fused lasso approach in regression coefficients clustering: learning parameter heterogeneity in data integration, The Journal of Machine Learning Research 17 (2016) 3915–3937.

- Tibshirani [1996] R. Tibshirani, Regression shrinkage and selection via the lasso, Journal of the Royal Statistical Society. Series B (Methodological) (1996) 267–288.

- Toulis and Airoldi [2015] P. Toulis, E. M. Airoldi, Scalable estimation strategies based on stochastic approximations: classical results and new insights, Statistics and computing 25 (2015) 781–795.

- Wang et al. [2015] F. Wang, P. X.-K. Song, L. Wang, Merging multiple longitudinal studies with study-specific missing covariates: A joint estimating function approach, Biometrics 71 (2015) 929–940.

- Wang et al. [2016] F. Wang, L. Wang, P. X.-K. Song, Fused lasso with the adaptation of parameter ordering in combining multiple studies with repeated measurements, Biometrics 72 (2016) 1184–1193.

- Wang et al. [2019] Y. Wang, N. Palmer, Q. Di, J. Schwartz, I. Kohane, T. Cai, A fast divide-and-conquer sparse cox regression, Biostatistics (2019) doi: 10.1093/biostatistics/kxz036.

- Xie and Singh [2013] M. Xie, K. Singh, Confidence distribution, the frequentist distribution estimator of a parameter: a review, International Statistical Review 81 (2013) 3–39.

- Xie et al. [2011] M. Xie, K. Singh, W. E. Strawderman, Confidence distributions and a unifying framework for meta-analysis, Journal of the American Statistical Association 106 (2011) 320–333.

- Zaharia et al. [2010] M. Zaharia, M. Chowdhury, M. J. Franklin, S. Shenker, I. Stoica, Spark: Cluster computing with working sets., HotCloud 10 (2010) 95.

- Zhang and Zhang [2014] C.-H. Zhang, S. S. Zhang, Confidence intervals for low dimensional parameters in high dimensional linear models, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76 (2014) 217–242.

- Zhang et al. [2015] Y. Zhang, J. Duchi, M. Wainwright, Divide and conquer kernel ridge regression: A distributed algorithm with minimax optimal rates, Journal of Machine Learning Research 16 (2015) 3299–3340.

- Zou [2006] H. Zou, The adaptive lasso and its oracle properties, Journal of the American Statistical Association 101 (2006) 1418–1429.

- Zou and Hastie [2005] H. Zou, T. Hastie, Regularization and variable selection via the elastic net, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 67 (2005) 301–320.