Extremal Quantile Regression: An Overview

Abstract.

Extremal quantile regression, i.e. quantile regression applied to the tails of the conditional distribution, counts with an increasing number of economic and financial applications such as value-at-risk, production frontiers, determinants of low infant birth weights, and auction models. This chapter provides an overview of recent developments in the theory and empirics of extremal quantile regression. The advances in the theory have relied on the use of extreme value approximations to the law of the Koenker and Bassett (1978) quantile regression estimator. Extreme value laws not only have been shown to provide more accurate approximations than Gaussian laws at the tails, but also have served as the basis to develop bias corrected estimators and inference methods using simulation and suitable variations of bootstrap and subsampling. The applicability of these methods is illustrated with two empirical examples on conditional value-at-risk and financial contagion.

1. Introduction

In 1895, the Italian econometrician Vilfredo Pareto discovered that the power law describes well the tails of income and wealth data. This simple observation stimulated further applications of the power law to economic data including Zipf (1949), Mandelbrot (1963), Fama (1965), Praetz (1972), Sen (1973), and Longin (1996), among many others. It also opened up a theory to analyze the properties of the tails of the distributions so-called Extreme Value (EV) theory, which was developed by Gnedenko (1943) and de Haan (1970). Jansen and de Vries (1991) applied this theory to analyze the tail properties of US financial returns and concluded that the 1987 market crash was not an outlier; rather, it was a rare event whose magnitude could have been predicted by prior data. This work stimulated numerous other studies that rigorously documented the tail properties of economic data (Embrechts et al., 1997).

Chernozhukov (2005) extended the EV theory to develop extreme quantile regression models in the tails, and analyze the properties of the Koenker and Bassett (1978) quantile regression estimator, called extremal quantile regression. This work builds especially upon Feigin and Resnick (1994) and Knight (2001), which studied the most extreme, frontier regression case in the location model. Related results for the frontier case – the regression frontier estimators – were developed by Smith (1994), Chernozhukov (1998), Jurečková (1999), and Portnoy and Jurec̆ková (1999). Portnoy and Koenker (1989) and Gutenbrunner et al. (1993) implicitly contained some results on extending the normal approximations to intermediate order regression quantiles (moderately extreme quantiles) in location models. The complete theory for intermediate order regression quantiles was developed in Chernozhukov (2005). Jurečková (2016) recently characterized properties of averaged extreme regression quantiles.

In this chapter we review the theory of extremal quantile regression. We start by introducing the general setup that will be used throughout the chapter. Let be a continuous response variable of interest with distribution function . The marginal -quantile of is the left-inverse of at , that is for some Let be a -dimensional vector of covariates related to , be the distribution function of , and be the conditional distribution function of given . The conditional -quantile of given is the left-inverse of at , that is for some We refer to as the -quantile regression function. This function measures the effect of on , both at the center and at the tails of the outcome distribution. A marginal or conditional -quantile is extremal whenever the probability index is either close to zero or close to one. Without loss of generality, we focus the discussion on close to zero.

The analysis of the properties of the estimators of extremal quantiles relies on EV theory. This theory uses sequences of quantile indexes that change with the sample size . Let be the order of the -quantile. A sequence of quantile index and sample size pairs is said to be an extreme order sequence if and as ; an intermediate order sequence if and as ; and a central order sequence if is fixed as . In this chapter we show that each of these sequences produce different asymptotic approximations to the distribution of the quantile regression estimators. The extreme order sequence leads to an EV law in large samples, whereas the intermediate and central sequences lead to normal laws. The EV law provides a better approximation to the extremal quantile regression estimators.

We conclude this introductory section with a review of some applications of extremal quantile regression to economics and finance.

Example 1 (Conditional Value-at-Risk).

The Value-at-Risk (VaR) analysis seeks to forecast or explain low quantiles of future portfolio returns of an institution, , using current information, (Chernozhukov and Umantsev, 2001; Engle and Manganelli, 2004). Typically, the extremal -quantile regression functions with and are of interest. The VaR is a risk measure commonly used in real-life financial management, insurance, and actuarial science (Embrechts et al., 1997). We provide an empirical example of VaR in Section 4.

Example 2 (Determinants of Birthweights).

In health economics, we may be interested in how smoking, absence of prenatal care, and other maternal behavior during pregnancy, , affect infant birthweights, (Abrevaya, 2001). Very low birthweights are connected with subsequent health problems and therefore extremal quantile regression can help identify factors to improve adult health outcomes. Chernozhukov and Fernández-Val (2011) provide an empirical study of the determinants of extreme birthweights.

Example 3 (Probabilistic Production Frontiers).

An important application to industrial organization is the determination of efficiency or production frontiers, pioneered by Aigner and fan Chu (1968), Timmer (1971), and Aigner et al. (1976). Given the cost of production and possibly other factors, , we are interested in the highest production levels, , that only a small fraction of firms, the most efficient firms, can attain. These (nearly) efficient production levels can be formally described by the extremal -quantile regression function for and ; so that only a -fraction of firms produce or more.

Example 4 (Approximate Reservation Rules).

In labor economics, Flinn and Heckman (1982) proposed a job search model with approximate reservation rules. The reservation rule measures the wage level, , below which a worker with characteristics, , accepts a job with small probability , and can by described by the extremal -quantile regression for .

Example 5 (Approximate -Rules).

The -adjustment models arise as an optimal policy in many economic models (Arrow et al., 1951). For example, the capital stock, , of a firm with characteristics is adjusted sharply up to the level once it has depreciated below some low level with probability close to one, . This conditional -rule can be described by the extremal -quantile regression functions and for .

Example 6 (Structural Auction Models).

Consider a first-price procurement auction where bidders hold independent valuations. Donald and Paarsch (2002) modelled the winning bid, , as , where is the efficient cost function that depends on the bid characteristics, , is a mark-up that approaches 1 as the number of bidders approaches infinity, and the disturbance captures small bidding mistakes independent of and . By construction, the structural function corresponds to the extremal quantile regression function for and .

Example 7 (Other Recent Applications).

Following the pioneering work of Powell (1984), Altonji et al. (2012) applied extremal quantile regression to estimate extensive margins of demand functions with corner solutions. D’Haultfœuille et al. (2015) used extremal quantile regression to deal with endogenous sample selection under the assumption that there is no selection at very high quantiles of the response variable conditional on covariates . They applied this approach to the estimation of the black wage gap for young males in the US. Zhang (2015) employed extremal quantile regression methods to estimate tail quantile treatment effects under a selection on observables assumption.

Notation: The symbol denotes convergence in law. For two real numbers , means that is much less than . More notation will be introduced when it is first used.

Outline: The rest of the chapter is organized as follows. Section 2 reviews models for marginal and conditional extreme quantiles. Section 3 describes estimation and inference methods for extreme quantile models. Section 4 presents two empirical applications of extremal quantile regression to conditional value-at-risk and financial contagion.

2. Extreme Quantile Models

This section reviews typical modeling assumptions in extremal quantile regression. They embody Pareto conditions on the tails of the distribution of the response variable and linear specifications for the -quantile regression function .

2.1. Pareto-Type and Regularly Varying Tails

The theory for extremal quantiles often assumes that the tails of the distribution of have Pareto-type behavior, meaning that the tails decay approximately as a power function, or more formally, a regularly varying function. The Pareto-type tails encompass a rich variety of tail behaviors, from thick to thin tailed distributions, and from bounded to unbounded support distributions.

: Define the variable by if the lower end-point of the support of is and by if the lower end-point of the support of is finite. In words, is a shifted copy of whose support ends at either or . The assumption that the random variable exhibits a Pareto-type tail is stated by the following two equivalent conditions:111 means that with an appropriate notion of limit.

| as | (2.1) | ||||||

| as | (2.2) |

for some , where is a non-parametric slowly-varying function at , and is a non-parametric slowly-varying function at .222A function is said to be slowly-varying at if for every The leading examples of slowly-varying functions are the constant function and the logarithmic function. The number as defined in (2.1) or (2.2) is called the extreme value (EV) index or the tail index.

The absolute value of measures the heavy-tailedness of the distribution. The support of a Pareto-type tailed distribution necessarily has a finite lower bound if and an infinite lower bound if . Distributions with include stable, Pareto, Student’s , and many others. For example, the -distribution with degrees of freedom has and exhibits a wide range of tail behaviors. In particular, setting yields the Cauchy distribution which has heavy tails with , while setting gives a distribution that has light tails with and is very close to the normal distribution. On the other hand, distributions with include the uniform, exponential, Weibull, and many others.

The assumption of Pareto-type tails can be equivalently cast in terms of a regular variation assumption, as is commonly done in the EV theory. A distribution function is said to be regularly varying at with index of regular variation if

This condition is equivalent to the regular variation of the quantile function at with index ,

The case of corresponds to the class of rapidly varying distribution functions. Such distribution functions have exponentially light tails, with the normal and exponential distributions being the chief examples. For the sake of simplicity, we omit this case from our discussion. Note, however, that since the limit distribution of the main statistics is continuous in , the inference theory for is included by taking .

2.2. Extremal Quantile Regression Models

The most common model for the quantile regression (QR) function is the linear in parameters specification

| (2.3) |

and for every , the support of . This linear functional form not only provides computational convenience but also has good approximation properties. Thus, the set can include transformations of such as polynomials, splines, indicators or interactions such that is close to . In what follows, without loss of generality we lighten the notation by using instead of . We also assume that the -dimensional vector contains a constant as the first element, has a compact support , and satisfies the regularity conditions stated in Assumption 3 of Chernozhukov and Fernández-Val (2011). Compactness is needed to ensure the continuity and robustness of the mapping from extreme events in to the extremal QR statistics. Even if is not compact, we can select the data for which belongs to a compact region.

The main additional assumption for extremal quantile regression is that , transformed by some auxiliary regression line , has Pareto-type tails. More precisely, together with (2.3), it assumes that there exists an auxiliary regression parameter such that the disturbance has lower end point or a.s., and its conditional quantile function satisfies the tail equivalence relationship:

| (2.4) |

for some quantile function that exhibits a Pareto-type tail (2.1) with EV index , and some vector parameter such that and a.s.

Condition (2.4) imposes a location-scale shift model. This model is more general than the standard location shift model that replaces by a constant, because it permits conditional heteroskedasticity that is common in economic applications. Moreover, condition (2.4) only affects the far tails, and therefore allows covariates to affect extremal and central quantiles very differently. Even at the tails, the local effect of the covariates is approximately given by , which can be heterogenous across extremal quantiles.

Existence and Pareto-type behavior of the conditional quantile density function is also often imposed as a technical assumption that facilitates the derivation of inference results. Accordingly, we will assume that the conditional quantile density function exists and satisfies the tail equivalence relationship

uniformly in where exhibits Pareto-type tails as with EV index .

3. Estimation and Inference Methods

This section reviews estimation and inference methods for extremal quantile regression. Estimation is based on the Koenker and Bassett (1978) quantile regression estimator. We consider both analytical and resampling methods. These methods are introduced in the univariate case of marginal quantiles and then extended to the multivariate or regression case of conditional quantiles. We start by imposing some general sampling conditions.

3.1. Sampling Conditions

We assume that we have a sample of of size that is either independent and identically distributed (i.i.d.) or stationary and weakly-dependent, with extreme events satisfying a non-clustering condition. In particular, the sequence is assumed to form a stationary, strongly mixing process with geometric mixing rate, that satisfies the condition that curbs clustering of extreme events (Chernozhukov and Fernández-Val, 2011). The assumption of mixing dependence is standard in econometrics (White, 2001). The non-clustering condition is of the Meyer (1973) type and states that the probability of two extreme events co-occurring at nearby dates is much lower than the probability of just one extreme event. For example, it assumes that a large market crash is not likely to be immediately followed by another large crash. This assumption is convenient because it leads to limit distributions of extremal quantile regression estimators as if independent sampling had taken place. The plausibility of the non-clustering assumption is an empirical matter.

3.2. Univariave Case: Marginal Quantiles

The analog estimator of the marginal -quantile is the sample -quantile,

where is the order statistic of , and denotes the integer part of . The sample -quantile can also be computed as a solution to an optimization program,

where is the asymmetric absolute deviation function of Fox and Rubin (1964).

We review the asymptotic behavior of the sample quantiles under extreme and intermediate order sequences, and describe inference methods for extremal marginal quantiles.

3.2.1. Extreme Order Approximation

Recall the following classical result from EV theory on the limit distribution of extremal order statistics: as , for any integer such that ,

| (3.1) |

where

| (3.2) |

The variable is defined in Section 2.1 and is an i.i.d. sequence of standard exponential variables. We call the canonically-normalized quantile (CN-Q) statistic because it depends on the canonical scaling constant . The result (3.1) was obtained by Gnedenko (1943) for i.i.d. sequences of random variables. It continues to hold for stationary weakly-dependent series, provided the probability of extreme events occurring in clusters is negligible relative to the probability of a single extreme event (Meyer, 1973). Leadbetter et al. (1983) extended the result to more general time series processes.

The limit in (3.1) provides an EV distribution as an approximation to the finite-sample distribution of , given the scaling constant . The limit distribution is characterized by the EV index and the variables . The index is usually unknown but can be estimated by one of the methods described below. The variables are gamma random variables. The limit variable is therefore a transformation of gamma variables, which has finite mean if and has finite moments of up to order if . Moreover, the limit EV distribution is not symmetric, predicting significant median asymptotic bias in with respect to that motivates the use of the median-bias correction techniques discussed below.

The classical result (3.1) is often not feasible for inference on because the constant is unknown and generally cannot be estimated consistently (Bertail et al., 2004). One way to deal with this problem is to add strong parametric assumptions on the non-parametric, slowly varying function in Equation (2.1) in order to estimate consistently. This approach is discussed in Section 3.2.3. An alternative is to consider the self-normalized quantile (SN-Q) statistic

| (3.3) |

for such that is an integer. For example, for some spacing parameter (e.g. ). The scaling factor is completely a function of data and therefore feasible, avoiding the need for the consistent estimation of . Chernozhukov and Fernández-Val (2011) shows that as , for any integer such that ,

| (3.4) |

The limit distribution in (3.4) only depends on the EV index , and its quantiles can be easily obtained by the resampling methods described in Section 3.2.5.

3.2.2. Intermediate Order Approximation

Dekkers and de Haan (1989) show that as and , and under further regularity conditions,

| (3.5) |

where is defined as in (3.3). This result yields a normal approximation to the finite-sample distribution of . Note this normal approximation holds only when , while the EV approximation (3.4) holds not only when but also when because the EV distribution converges to the normal distribution as . In finite samples, we may interpret the condition as requiring that .

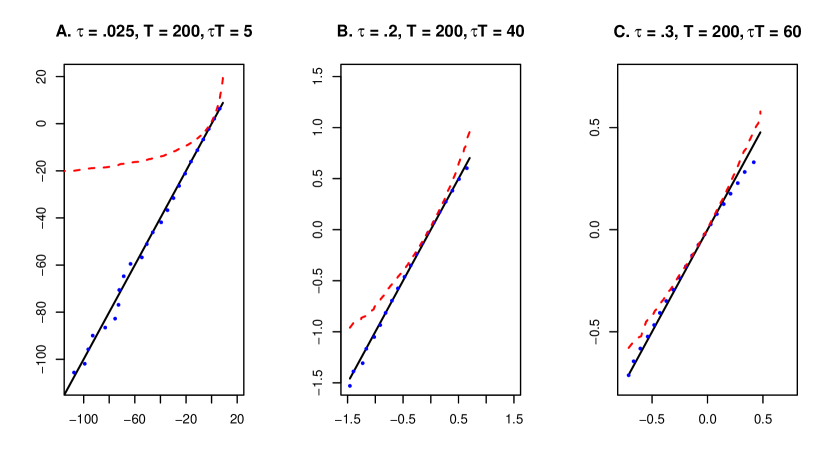

Figure 1, taken from Chernozhukov and Fernández-Val (2011), shows that the EV distribution provides a better approximation to the distribution of extremal sample quantiles than the normal distribution when . It plots the quantiles of these distributions against the quantiles of the finite-sample distribution of the sample -quantile for and . If either the EV or the normal distributions were to coincide with the exact distribution, then their quantiles would fall on the 45 degree line shown by the solid line. When the order is or , the quantiles of the EV distribution are very close to the 45 degree line, and in fact are much closer to this line than the quantiles of the normal distribution. Only for the case when the order becomes , do the quantiles of the EV and normal distributions become comparably close to the 45 degree line.

3.2.3. Estimation of

Some inference methods for extremal marginal quantiles require a consistent estimator of the EV index . We describe two well-known estimators of . The first estimator, due to Pickands (1975), relies on the ratio of sample quantile spacings:

| (3.6) |

Under further regularity conditions, for and as ,

The second estimator, developed by Hill (1975), is the moment estimator:

| (3.7) |

which is applicable when and . This estimator is motivated by the maximum likelihood method that fits an exact power law to the tail data. Under further regularity conditions, for and as ,

The previous limit results can be used to construct the confidence intervals and median-bias corrections for . We give an example of these confidence intervals and corrections in Section 4.

Embrechts et al. (1997) provide methods for choosing . There is a variance-bias trade-off, as the variance of the estimator decreases, but the bias increases, as increases. Another view on the choice of is that the statistical models are approximations, but not literal descriptions of the data. In practice, the dependence of on the threshold reflects that power laws with different values of would fit some tail regions better than others. Therefore, if the interest lies in making the inference on for a particular , it seems reasonable to use constructed using or the closest to subject to . This condition ensures to have a sufficient number of observations to estimate .

3.2.4. Estimation of

To use the CN-Q statistic for inference, we need to estimate the scaling constant defined in (3.2). This requires additional strong restrictions on the underlying model. For instance, assume that the slowly varying function is just a constant , i.e., as ,

| (3.8) |

Then, we can estimate by

| (3.9) |

where is either the Pickands or Hill estimator given in (3.6) and (3.7), and can be chosen using the same methods as in the estimation of . Then, the estimator of is

| (3.10) |

3.2.5. Computing Quantiles of the Limit EV Distributions

The inference and bias corrections for extremal quantiles are based on the EV approximations given in (3.1) and (3.4), with an estimator in place of the EV index if needed. In practice, it is convenient to compute the quantiles of the EV distributions using simulation or resampling methods, instead of an analytical method. Here we illustrate two of such methods: extremal bootstrap and extremal subsampling. The bootstrap method relies on simulation, whereas the subsampling method relies on drawing subsamples from the original sample. Subsampling has the advantages that it does not require the estimation of and is consistent under general conditions (e.g. subsampling does not require i.i.d. data). Nevertheless, bootstrap is more accurate than subsampling when a stronger set of assumptions holds. It should be noted here that the empirical or nonparametric bootstrap is not consistent for extremal quantiles (Bickel and Freedman, 1981).

The extremal bootstrap is based on simulating samples from a random variable with the same tail behavior as . Consider the random variable,333The variable follows the generalized extreme value distribution, which nests the Frechet, Weibull, and Gumbell distributions. There are other possibilities, for example, the standard exponential distribution can be replaced by the standard uniform distribution, in which case would follow the generalized Pareto distribution.

| (3.11) |

This variable has the quantile function

| (3.12) |

which satisfies Condition (2.2) because . The extremal bootstrap estimates the distribution of by the distribution of obtained by simulation. This approximation reproduces both the EV limit (3.4) under extreme order sequences and the normal limit (3.5) under intermediate order sequences. Algorithm 1 describes the implementation of this method.

Algorithm 1 (Extremal Bootstrap).

(1) Choose the quantile index of interest and the number of simulations (e.g., ). (2) For each , draw an i.i.d. sequence from the random variable defined in (3.11), replacing by the estimator (3.6) or (3.7). (3) For each , compute the statistic , where is the sample -quantile in the bootstrap sample and is defined as in (3.12) replacing by the same estimator as in step (2). (4) Estimate the quantiles of by the sample quantiles of .

Extremal bootstrap can be also applied to estimate the distribution of other statistics, including the estimators of the EV index in (3.6) or (3.7) and the extrapolation estimators of Section 3.2.7.

We now describe an extremal subsampling method to estimate the distributions of and developed by Chernozhukov and Fernández-Val (2011). It is based on drawing subsamples of size from such that and as , and computing the subsampling version of the SN-statistic as

| (3.13) |

where is the sample -quantile in the subsample of size , and . Similarly, the subsampling version of the CN-Q statistic is

| (3.14) |

where is a consistent estimator of . For example, under the parametric restrictions specified in (3.8), we can set for as in (3.9) and one of the estimators in (3.6) or (3.7).

The distributions of and over all the subsamples estimate the distributions of and , respectively. The number of possible subsamples depends on the structure of serial dependence in the data, but it can be very large. In practice, the distributions over all subsamples are approximated by the distributions over a smaller number of randomly chosen subsamples, such that as (Politis et al., 1999, Chap. 2.5) . Politis et al. (1999) and Bertail et al. (2004) provide methods for choosing the subsample size . Algorithm 2 describes the implementation of the extremal subsampling.

Algorithm 2 (Extremal Subsampling).

(1) Choose the quantile index of interest , the subsample size (e.g., ), and the number of subsamples (e.g., ).444Chernozhukov and Fernández-Val (2005) suggest the choice with and , to guarantee that the minimal subsample size is . (2) If the data have serial dependence, draw subsamples from of size of the form where . If the data are independent, can be drawn as a random subsample of size from without replacement. (3) For each , compute or applying (3.13) or (3.14) to the subsample . (4) Estimate the quantiles of or by the sample quantiles of or .

Extremal subsampling differs from conventional subsampling, which is inconsistent for extremal quantiles. This difference can be more clearly appreciated in the case of . Here, conventional subsampling would recenter the subsampling version of the statistic by the estimator in the full sample . Recentering in this way requires for consistency (see Theorem 2.2.1 in Politis et al. (1999)), but when . Thus, when the extremal sample quantiles diverge rendering conventional subsampling to be inconsistent. In contrast, extremal subsampling uses for recentering. This sample quantile may diverge, but because it is an intermediate order quantile if , the speed of its divergence is strictly slower than that of . Hence, extremal subsampling exploits the special structure of the order statistics to do the recentering.

3.2.6. Median Bias Correction and Confidence Intervals

Chernozhukov and Fernández-Val (2011) construct asymptotically median-unbiased estimators and -confidence intervals (CI) for based on the SN-Q statistic as

where is a consistent estimator of the -quantile of that can be obtained using Algorithms 1 or 2. Chernozhukov and Fernández-Val (2011) also construct asymptotically median-unbiased estimators and -CIs for based on the CN-Q statistic as

where is a consistent estimator of the -quantile of that can be obtained using Algorithm 2, and is a consistent estimator of such as (3.10).

3.2.7. Extrapolation Estimator for Very Extremes

Sample -quantiles can be very inaccurate estimators of marginal -quantiles when is very small, say . For such very extremal cases we can construct more precise estimators using the assumptions on the behavior of the tails. In particular, we can estimate less extreme quantiles reliably, and extrapolate them to the quantile of interest using the tail assumptions.

Dekkers and de Haan (1989) develop the following extrapolation estimator:

| (3.15) |

where and is a consistent estimator of such as (3.6) or (3.7). Then, for and with ,

where and are independent, has a standard gamma distribution with shape parameter , and with i.i.d. standard exponential. He et al. (2016) proposed the closely related estimator

| (3.16) |

Under some regularity conditions, they show that for as this estimator converges to a normal distribution jointly with the EV index estimator .

3.3. Multivariate Case: Conditional Quantiles

The -quantile regression (-QR) estimator of the conditional -quantile is:

| (3.17) |

This estimator was introduced by Laplace (1818) for the median case, and extended by Koenker and Bassett (1978) to include other quantiles and regressors.

In this section, we review the asymptotic behavior of the QR estimator under extreme and intermediate order sequences, and describe inference methods for extremal quantile regression. The analysis for the multivariate case parallels the analysis for the univariate case in Section 3.2.

3.3.1. Extreme Order Approximation

Consider the canonically-normalized quantile regression (CN-QR) statistic

| (3.18) |

and the self-normalized quantile regression (SN-QR) statistic

| (3.19) |

where and is a real number such that for . For example, where is a spacing parameter (e.g. ). The CN-QR statistic is generally infeasible for inference because it depends on the unknown canonical normalization constant . This constant can only be estimated consistently under strong parametric assumptions, which will be discussed in Section 3.3.4. The SN-QR statistic is always feasible because it uses a normalization that only depends on the data.

Chernozhukov and Fernández-Val (2011) show that for as ,

| (3.20) |

where for if and if ,

| (3.21) |

where is an i.i.d. sequence with distribution ; ; is an i.i.d. sequence of standard exponential variables that is independent of ; and . Furthermore,

| (3.22) |

The limit EV distributions are more complicated than in the univariate case, but they share some common features. First, they depend crucially on the gamma variables , are not necessarily centered at zero, and can have a significant first-order asymptotic median bias. Second, as mentioned above, the limit distribution of the CN-QR statistic in Equation (3.21) is generally infeasible for inference due to the difficulty in consistently estimating the scaling constant .

Remark 1 (Very Extreme Order Quantiles).

3.3.2. Intermediate Order Approximation

Chernozhukov (2005) shows that for and as ,

| (3.23) |

where is defined as in (3.19). As in the univariate case, this normal approximation provides a less accurate approximation to the distribution of the extremal quantile regression than the EV approximation when . The condition can be interpreted in finite samples as requiring that , where is a dimension-adjusted order of the quantile explained in Section 3.4.

3.3.3. Estimation of and

Some inference methods for extremal quantile regression require consistent estimators of the EV index and the scale parameter . The regression analog of the Pickands estimator is

| (3.24) |

This estimator is consistent if and as . Under additional regularity conditions, for and as ,

| (3.25) |

The regression analog of the Hill estimator is

| (3.26) |

which is applicable when and . Under further regularity conditions, for and ,

| (3.27) |

These limit results can be used to construct confidence intervals for . The scale parameter can be estimated by

| (3.28) |

which is consistent if and as .

The choice of is similar to the univariate case in Section 3.2.3. This time, however, one needs to take into account the multivariate nature of the problem. For example, if the interest lies in making the inference on for a particular , it is reasonable to set equal to the closest value to such that . We refer again the reader to Section 3.4 for a discussion on the difference in the choice of between the univariate and multivariate cases.

3.3.4. Estimation of

To use the CN-QR statistic for inference, we need to estimate the scaling constant defined in (3.18). This requires strong restrictions and an additional estimation procedure. For example, assume that the non-parametric slowly varying component of is replaced by a constant , i.e., as

| (3.29) |

Then we can estimate the constant by

| (3.30) |

where is either the Pickands or Hill estimator given in (3.24) or (3.26). Thus, the scaling constant is estimated by

3.3.5. Computing Quantiles of the Limit EV Distributions

We consider inference and asymptotically median unbiased estimation for linear functions of the coefficient vector , for some nonzero vector , based on the EV approximations from (3.22) and from (3.22). We describe three methods to compute critical values of the limit EV distributions: analytical computation, extremal bootstrap, and extremal subsampling. The analytical and bootstrap methods require estimation of the EV index and the scale parameter . Subsampling applies under more general conditions than the other methods, and hence we would recommend the use of it. However, the analytical and bootstrap methods can be more accurate than subsampling if the data satisfy a stronger set of assumptions.

The analytical computation method is based directly on the limit distributions (3.20) and (3.22) replacing and by consistent estimators. Define the -dimensional random vector:

| (3.31) |

where if and if , is an estimator of such as (3.24) or (3.26), is an estimator of such as (3.28), , is an i.i.d. sequence of standard exponential variables, and is an i.i.d. sequence independent of with distribution function , where is any smooth consistent estimator of , e.g., a smoothed empirical distribution function of the sample . Also, let

The quantiles of and are estimated by the corresponding quantiles of the and , respectively. In practice, these quantiles can only be evaluated numerically via the following algorithm.

Algorithm 3 (QR Analytical Computation).

(1) Choose the quantile index of interest and the number of simulations (e.g., ). (2) For each , draw an i.i.d. sequence from the random vector defined in (3.31) with and the infinite summation truncated at some finite value (e.g. ). (3) For each , compute . (4) Estimate the quantiles of and by the sample quantiles of and .

The extremal bootstrap is computationally less demanding than the analytical methods. It is based on simulating samples from a random variable with the same tail behavior as . Consider the bootstrap sample , where

| (3.32) |

and is a fixed set of observed regressors from the data. The variable has the conditional quantile function

| (3.33) |

The extremal bootstrap approximates the distribution of by the distribution of where is the -QR estimator in the bootstrap sample. This approximation reproduces both the EV limit (3.22) under extreme value sequences, and the normal limit (3.23) under intermediate order sequences. The distribution of can be obtained by simulation using the algorithm:

Algorithm 4 (QR Extremal Bootstrap).

(1) Choose the quantile index of interest and the number of simulations (e.g., ). (2) For each , draw a bootstrap sample from the random vector defined in (3.32), replacing by the estimator (3.24) or (3.26) and by the estimator (3.28). (3) For each , compute the statistic , where is the -QR in the bootstrap sample and is defined as in (3.33) replacing and by the same estimators as in step (2). (4) Estimate the quantiles of by the sample quantiles of .

Chernozhukov and Fernández-Val (2011) developed an extremal subsampling method to estimate the distributions of and . It is based on drawing subsamples of size from such that and as , and computing the subsampling version of the SN-QR statistic as

| (3.34) |

where for some spacing parameter (e.g. ), is the -QR estimator in the subsample of size , is the sample mean of the regressors in the subsample, and .555In practice, it is reasonable to use the following finite-sample adjustment to : if , and if . The idea is that is adjusted to be non-extremal if , and the subsampling procedure reverts to central order inference. The truncation of by is a finite-sample adjustment that restricts the key statistics to be extremal in subsamples. These finite-sample adjustments do not affect the asymptotic arguments. Similarly, the subsampling version of the CN-QR statistic is

| (3.35) |

where is a consistent estimator for . For example, for given by (3.30) and is the estimator of given in (3.24) or (3.26).

As in the univariate case, the distributions of and over all the possible subsamples estimate the distributions of and , respectively. These distributions can be obtained by simulation using the algorithm:

Algorithm 5 (QR Extremal Subsampling).

(1) Choose the quantile index of interest , the subsample size (e.g., ), and the number of subsamples (e.g., ). (2) If the data have serial dependence, draw subsamples from of size , , of the form where . If the data are independent, can be drawn as a random subsample of size from without replacement. (3) For each , compute or applying (3.34) or (3.35) to the subsample . (4) Estimate the quantiles of or by the sample quantiles of or .

The comments of Section 3.2.5 on the choice of subsample size, number of simulations, and differences with conventional subsampling also apply to the regression case.

3.3.6. Median Bias Correction and Confidence Intervals

Chernozhukov and Fernández-Val (2011) construct asymptotically median-unbiased estimators and -CIs for based on the SN-QR statistic as

where is a consistent estimator of the -quantile of that can be obtained using Algorithms 3, 4, or 5. Chernozhukov and Fernández-Val (2011) also construct asymptotically median-unbiased estimators and -CIs for based on the CN-QR statistic as

where is a consistent estimator of the -quantile of that can be obtained using Algorithms 3 or 5.

3.3.7. Extrapolation Estimator for Very Extremes

The -QR estimators can be very inaccurate when is very small, say . We can construct extrapolation estimators for these cases that use the assumptions on the behavior of the tails. By analogy with the univariate case,

| (3.36) |

or

| (3.37) |

where , and is the Pickands or Hill estimator of in (3.24) or (3.26). He et al. (2016) derived the joint asymptotic distribution of . Wang et al. (2012) developed other extrapolation estimators for heavy-tailed distributions with .

The estimators in (3.36) and (3.37) have good properties provided that the quantities on the right-hand side are well estimated, which in turn requires that be large, and that the Pareto-type tail model be a good approximation. To construct the confidence interval for based on extrapolation, we can apply the extremal subsampling to the statistic

For the estimator (3.37), we can also use analytical methods based on the asymptotic distribution given in Corollary 3.4 of He et al. (2016).

3.4. EV Versus Normal Inference

Chernozhukov and Fernández-Val (2011) provided a simple rule of thumb for the application of EV inference. Recall that the order of a sample -quantile from a sample of size is (rounded to the next integer). This order plays a crucial role in determining the quality of the EV or normal approximations. Indeed, the former requires , whereas the latter requires . In the regression case, in addition to the order of the quantile, we need to take into account , the dimension of . As an example, consider the case where all covariates are indicators that divide equally the sample into subsamples of size . Then, each of the components of the -QR estimator will correspond to a sample quantile of order . We may therefore think of as a dimension-adjusted order for quantile regression.

A common simple rule for the application of the normal is that the sample size is greater than 30. This suggests that we should use extremal inference whenever . This simple rule may or may not be conservative. For example, when regressors are continuous, the computational experiments in Chernozhukov and Fernández-Val (2011) show that the normal inference performs as well as the EV inference provided that to , which suggests using EV inference when to for this case. On the other hand, if we have an indicator in equal to one only for 2% of the sample, then the coefficient of this indicator behaves as a sample quantile of order , which would motivate using EV inference when to in this case. This rule is far more conservative than the original simple rule when . Overall, it seems prudent to use both EV and normal inference methods in most cases, with the idea that the discrepancies between the two can indicate extreme situations.

4. Empirical Applications

We consider two applications of extremal quantile regression to conditional value-at-risk and financial contagion. We implement the empirical analysis in R language with Koenker (2016) quantreg package and the code from Chernozhukov and Du (2008) and Chernozhukov and Fernández-Val (2011).

The data are obtained from Yahoo! Finance.666The dataset and the code are available online at Fernández-Val’s website: http://sites.bu.edu/ivanf/research/.

4.1. Value-at-Risk Prediction

We revisit the problem of forecasting the conditional value-at-risk of a financial institution posed by Chernozhukov and Umantsev (2001) with more recent methodology. The response variable is the daily return of the Citigroup stock, and the covariates , , and are the lagged daily returns of the Citigroup stock (C), the Dow Jones Industrial Index (DJI), and the Dow Jones US Financial Index (DJUSFN), respectively. The lagged own return captures dynamics, DJI is a measure of overall market return, and the DJUSFN is a measure of market return in the financial sector. We estimate quantiles of conditional on with and . There are 1,738 daily observations in the sample covering the period from January 1, 2009 to November 30, 2015.

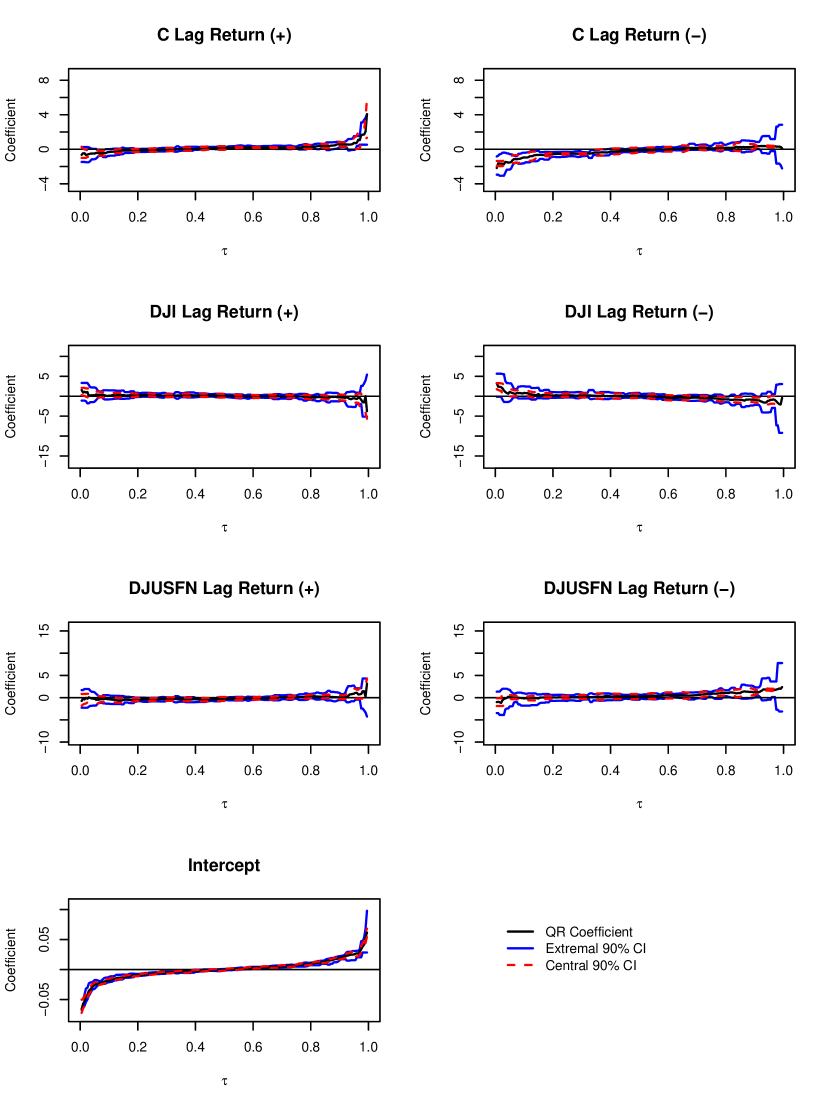

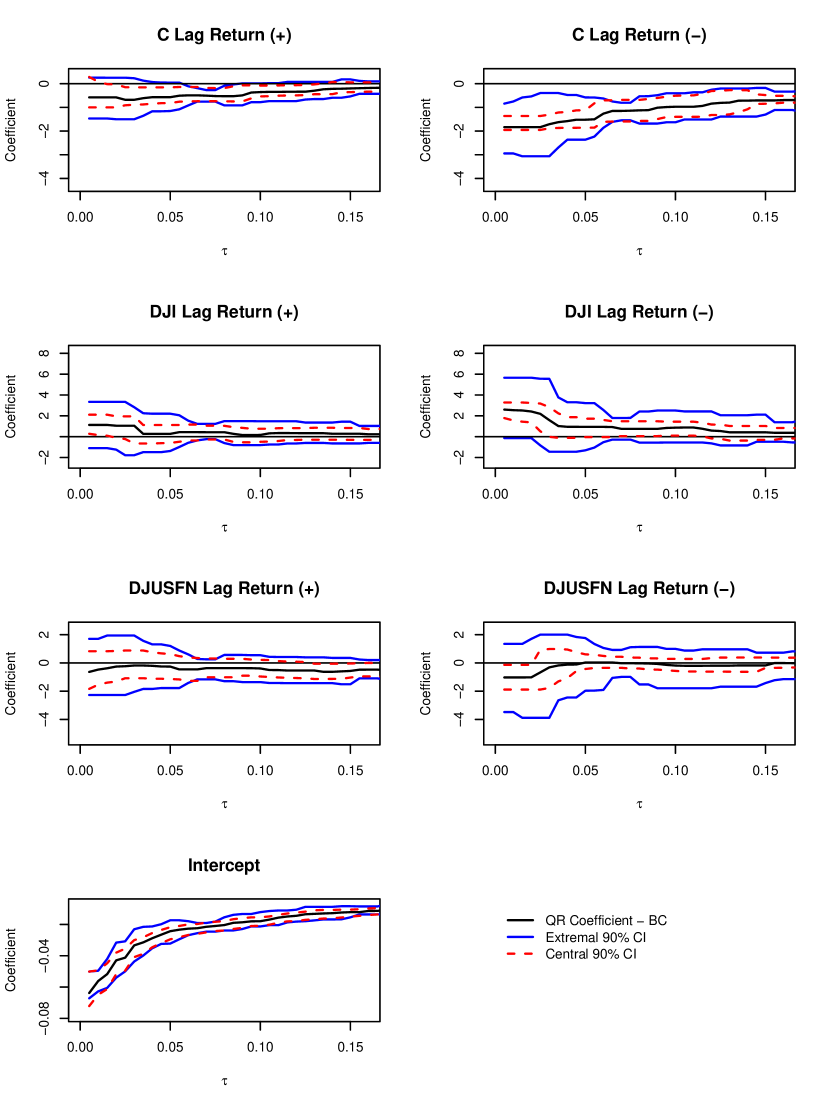

Figure 2 plots the QR estimates along with 90% pointwise CIs. The solid lines represent the extremal CIs and the dashed lines the normal CIs. The extremal CIs are computed by the extremal subsampling method described in Algorithm 5 with the subsample size and the number of simulations . We use the SN-QR statistic with spacing parameter . The normal CIs are based on the normal approximation with the standard errors computed with the method proposed by Powell (1991).777We used the command summary.rq with the option ker in the quantreg package to compute the standard errors. Figure 3 plots the median bias-corrected QR estimates along with 90% pointwise CIs for the lower tail (note that due to the median bias-correction, the coefficient estimates are slightly different from Figure 2). The bias correction is also implemented using extremal subsampling with the same specifications.

We focus the discussion on the impact of downward movements of the explanatory variables (the C lag , the DJI lag , and the DJUSFN lag ) on the extreme risk, that is, on the low conditional quantiles of the Citigroup stock return. To interpret the results, it is helpful to keep in mind that if the covariates were completely irrelevant (i.e. independent from the response), then their coefficients would be equal to zero uniformly over , except for the constant term. The intercept would coincide with the unconditional quantile of Citigroup daily return. Another general remark is that we would expect the estimates and CIs to be more volatile at the tails than at the center due to data sparsity. Figures 2 and 3 show that most of the coefficients are insignificant throughout the distribution, what confirms the expected unpredictability of the stock returns. However, we do find that the coefficient on the Citigroup’s lagged return is significantly different from zero in the extreme low quantiles (see the upper right figure in Figure 3). This suggests that from 2009 to 2015, a past drop in the stock price of Citigroup has significantly pushed down the extreme low quantiles of the current stock price. Informally speaking, the negative return on the stock price induced the risk of a further negative outcome in the near future.

Comparing the CIs produced by the extremal inference and the normal inference, Figure 2 shows that they closely match in the central region, while Figures 3 reveals that the normal CIs are often narrower than the extremal CIs in the tails, especially for . As briefly mentioned in Section 3.2.2, the extremal CIs coincide with the normal CIs when the situation is non-extremal. Therefore, this discrepancy indicates that the normal CIs on the tails substantially underestimates the sampling variation and hence it might lead to a substantial undercoverages in the CIs.

We next characterize the tail properties of the model. Table 1 reports the estimates of the EV index obtained by the Hill estimator in (3.26), together with bias corrected estimates and 90% CIs based on (3.27), which were obtained using the QR extremal bootstrap of Algorithm 4 with applied to the Hill estimator. The bias-corrected estimates of are relatively stable even at the extreme tails. They are greater than zero, confirming that the distribution of stock returns has a much thicker lower tail than the normal distribution. It is noteworthy that none of these estimates were used to produce the fig. 2 and 3 because they were obtained from extremal subsampling method applied to the SN-QR statistic.

| Estimate | Bias-Corrected | 90% Confidence | |

|---|---|---|---|

| Estimate | Interval | ||

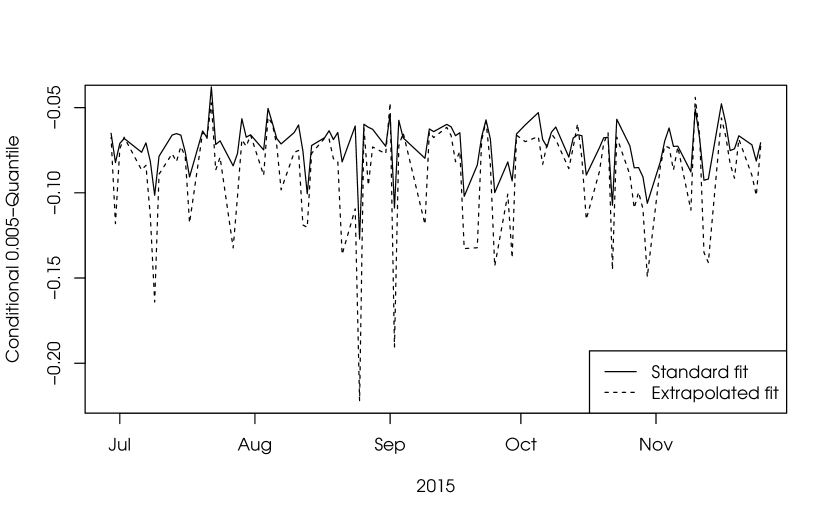

Having characterized the EV index, we can now estimate the very extreme quantiles using extrapolation methods. We set to be the estimate with , and compute the extrapolation estimator (3.36) for , , and in Table 2. For comparison purposes, the first column reports the -QR estimates for obtained from (3.17). This estimator cannot be calculated for the other quantile indexes considered. We find some discrepancies between the two estimators especially for the coefficients of the negative lags at . Figure 4 plots the predicted values for the conditional -quantiles in the second half of 2015 obtained from the QR and extrapolation estimators. The standard QR fit uses sample data that contains few observations on the extreme events, while the extrapolated fit uses the tail model and a reliably estimated conditional -quantile coefficients to predict the magnitude of such events. The quality of this prediction clearly depends on whether the tails model is accurate.

| Regression | Extrapolation | ||||

|---|---|---|---|---|---|

| Variable | estimate | estimate | |||

| Intercept | |||||

| C lag return () | |||||

| C lag return () | |||||

| DJI lag return () | |||||

| DJI lag return () | |||||

| DJUSFN lag return () | |||||

| DJUSFN lag return () | |||||

4.2. Application 2: Contagion of Financial Risk

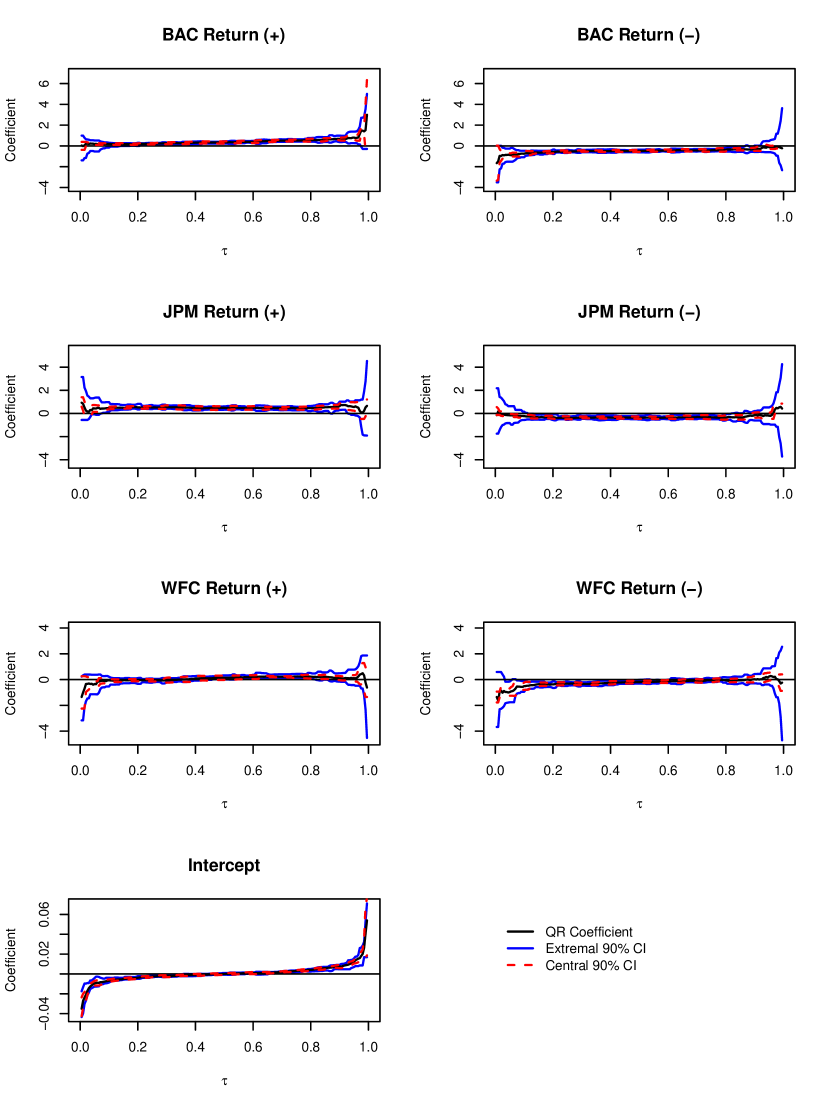

We consider an application to contagion of financial risk between commercial banks. The response variable is the daily return of the Citigroup stock (C), and the covariates , , and are the contemporaneous daily returns of the stocks of other banks, namely, Bank of America (BAC), JPMorgan Chase & Co. (JPM), and Wells Fargo & Co. (WFC). As in the previous section, we estimate the quantiles of conditional on using 1,738 daily observations covering the period from January 1, 2009 to November 30, 2015.

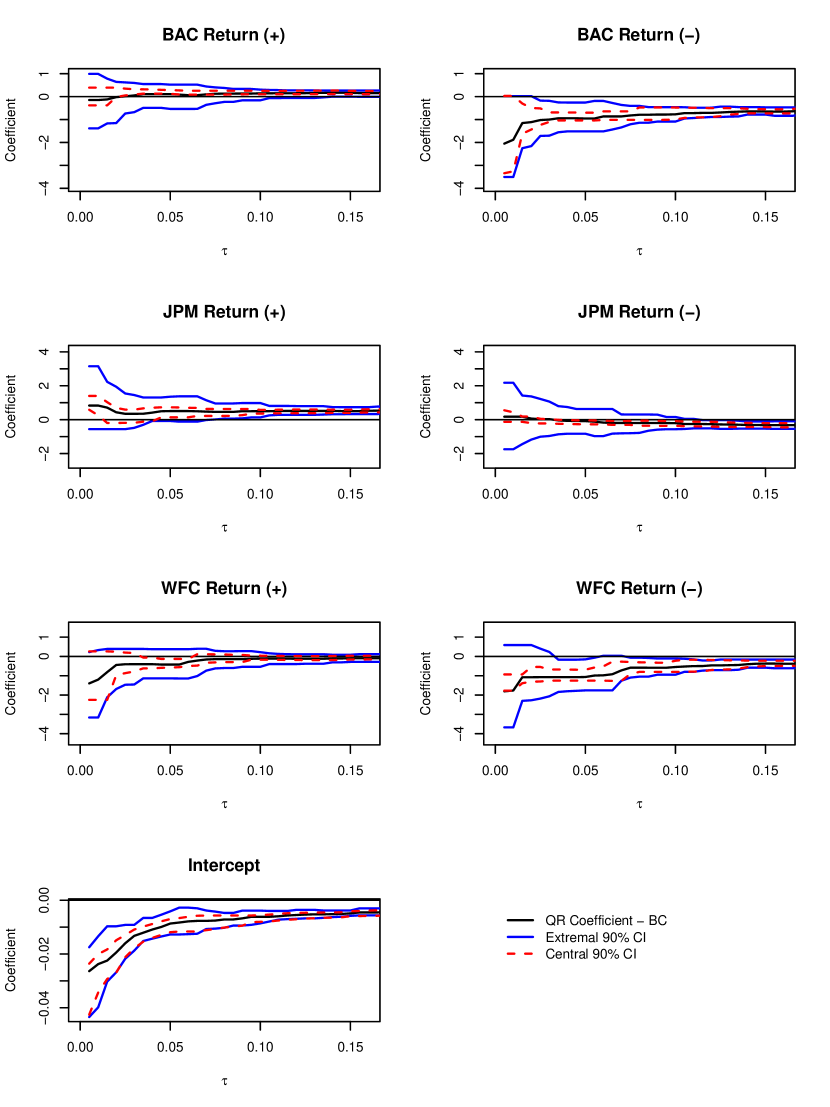

Figure 5 plots the QR estimates along with 90% pointwise CIs. The solid lines represent the extremal CIs and the dashed lines the normal CIs. The extremal CIs are computed by the extremal subsampling method described in Algorithm 5 with the subsample size and the number of simulations . We use the SN-QR statistic with spacing parameter . The normal CIs are based on the normal approximation with the standard errors computed with the method proposed by Powell (1991). Figure 6 plots the median bias-corrected QR estimates along with 90% pointwise CIs for the lower tail. The bias correction is also implemented using extremal subsampling with the same specifications.

We find a significant effect of Bank of America’s risk on Citigroup’s risk. Observe that the coefficient of BAC () is positive and that of BAC () is negative across most of the quantiles. This tells that BAC and C hold similar portfolios and that there might be a direct contagion of BAC’s risk to C’s risk (negative return of BAC is likely to cause negative return of C). Similar observation holds for JPM’s risk onto C’s risk. However, there are no such contagion effect of WFC’s risk onto C’s. In fig. 6 we see that the negative return of Bank of America’s stock has a large effect on the extreme low quantile of C’s return, while its positive return has no significant effect. This indicates that Bank of America’s risk has an asymmetric and large impact on its competitor. As in the value at risk application, we find that the normal and extremal CIs are similar in the central region, while the normal CIs are narrower than the extremal CI in the tails, especially for .

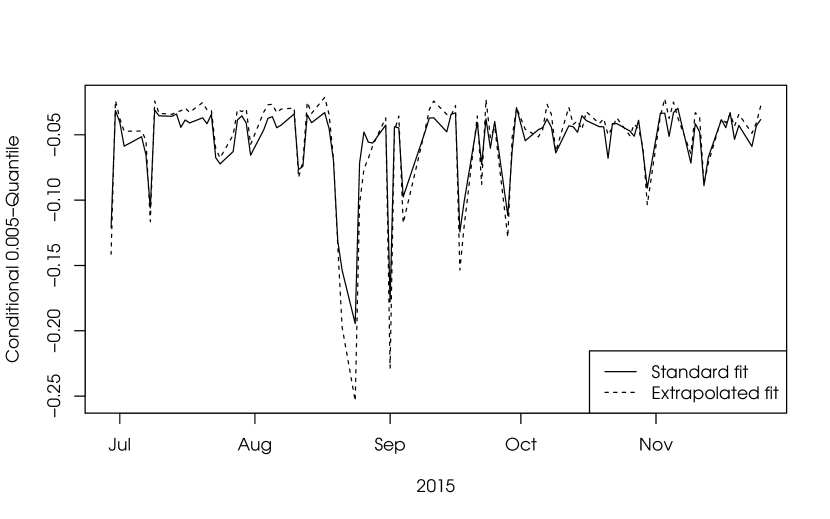

Table 3 reports the estimates of the EV index obtained by the Hill estimator (3.26), together with bias corrected estimates and 90% CIs based on (3.27), which were obtained using the QR extremal bootstrap of Algorithm 4 with applied to the Hill estimator. Again we find estimates significantly greater than zero confirming that stock returns have thick lower tails relative to the normal distribution. Table 4 shows the estimates of the QR coefficients for very low quantiles obtained from QR and the extrapolation estimator (3.36) with the estimate from table 3 for . The largest difference between the regression and extrapolation estimates occur for the WFC’s return. Here we find a large negative coefficient for the return (-) that indicates that there might be contagion of financial risk from WFC to C at very low quantiles. Figure 7 contrasts the predicted values for the conditional -quantiles in the second half of 2015 obtained from the QR and extrapolation estimators. Overall, the two methods produce similar estimates, although the extrapolated estimator predicts deeper troughs in the quantiles.

| Estimate | Bias-Corrected | 90% Confidence | |

|---|---|---|---|

| Estimate | Interval | ||

| Regression | Extrapolation | ||||

|---|---|---|---|---|---|

| Variable | estimate | estimate | |||

| Intercept | |||||

| BAC return () | |||||

| BAC return () | |||||

| JPM return () | |||||

| JPM return () | |||||

| WFC return () | |||||

| WFC return () | |||||

References

- Abrevaya (2001) Abrevaya, J., 2001. The effect of demographics and maternal behavior on the distribution of birth outcomes. Empirical Economics 26 (1), 247–259.

- Aigner et al. (1976) Aigner, D. J., Amemiya, T., Poirier, D. J., 1976. On the estimation of production frontiers: maximum likelihood estimation of the parameters of a discontinuous density function. International Economic Review 17 (2), 377–396.

- Aigner and fan Chu (1968) Aigner, D. J., fan Chu, S., 1968. On estimating the industry production function. American Economic Review 58, 826–839.

- Altonji et al. (2012) Altonji, J. G., Ichimura, H., Otsu, T., 2012. Estimating derivatives in nonseparable models with limited dependent variables. Econometrica 80 (4), 1701–1719.

- Arrow et al. (1951) Arrow, K. J., Harris, T., Marschak, J., 1951. Optimal inventory policy. Econometrica 19 (3), 205–272.

- Bertail et al. (2004) Bertail, P., Haefke, C., Politis, D. N., White, H., 2004. A subsampling approach to estimating the distribution of diverging extreme statistics with applications to assessing financial market risks. Journal of Econometrics 120 (2), 295–326.

- Bickel and Freedman (1981) Bickel, P., Freedman, D., 1981. Some asymptotic theory for the bootstrap. Annals of Statistics 9, 1196–1217.

- Chernozhukov (1998) Chernozhukov, V., 1998. Nonparametric extreme regression quantiles, working paper, Standord Univ. Presented at Princeton Econometrics Seminar, December 1998.

- Chernozhukov (2005) Chernozhukov, V., 2005. Extremal quantile regression. Ann. Statist. 33 (2), 806–839.

- Chernozhukov and Du (2008) Chernozhukov, V., Du, S., 2008. extremal quantiles and value-at-risk. In: Durlauf, S. N., Blume, L. E. (Eds.), The New Palgrave Dictionary of Economics. Palgrave Macmillan, Basingstoke.

- Chernozhukov and Fernández-Val (2005) Chernozhukov, V., Fernández-Val, I., 2005. Subsampling inference on quantile regression processes. Indian Journal of Statistics 67, 253–276.

- Chernozhukov and Fernández-Val (2011) Chernozhukov, V., Fernández-Val, I., 2011. Inference for extremal conditional quantile models, with an application to market and birthweight risks. Review of Economic Studies 78, 559–589.

- Chernozhukov and Umantsev (2001) Chernozhukov, V., Umantsev, L., 2001. Conditional value-at-risk: Aspects of modeling and estimation. Empirical Economics 26 (1), 271–293.

- de Haan (1970) de Haan, L., 1970. On Regular Variation and Its Applications to the Weak Convergence. Mathematical Centre Tract 32, Mathematical Centre, Amsterdam, Holland.

- Dekkers and de Haan (1989) Dekkers, A., de Haan, L., 1989. On the estimation of the extreme-value index and large quantile estimation. Annals of Statistics 17 (4), 1795–1832.

- D’Haultfœuille et al. (2015) D’Haultfœuille, X., Maurel, A., Zhang, Y., 2015. Extremal quantile regressions for selection models and the black-white wage gap, working Paper.

- Donald and Paarsch (2002) Donald, S. G., Paarsch, H. J., 2002. Superconsistent estimation and inference in structural econometric models using extreme order statistics. Journal of Econometrics 109 (2), 305–340.

- Embrechts et al. (1997) Embrechts, P., Klüppelberg, C., Mikosch, T., 1997. Modelling extremal events 33.

- Engle and Manganelli (2004) Engle, R. F., Manganelli, S., 2004. Cariar: Conditional autoregressive value at risk by regression quantiles. Journal of Business and Economic Statistics 22 (4), 367–381.

- Fama (1965) Fama, E. F., 1965. The behavior of stock market prices. Journal of Business 38, 34–105.

- Feigin and Resnick (1994) Feigin, P. D., Resnick, S. I., 1994. Limit distributions for linear programming time series estimators. Stochastic Processes and their Applications 51, 135–165.

- Flinn and Heckman (1982) Flinn, C. J., Heckman, J. J., 1982. New methods for analyzing structural models of labor force dynamics. Journal of Econometrics 18 (1), 115–168.

- Fox and Rubin (1964) Fox, M., Rubin, H., 1964. Admissibility of quantile estimates of a single location parameter. Annals of Mathematical Statistics 35, 1019–1030.

- Gnedenko (1943) Gnedenko, B., 1943. Sur la distribution limité du terme d’ une série alétoire. Annals of Mathematics 44, 423–453.

-

Gutenbrunner et al. (1993)

Gutenbrunner, C., Jurečková, J., Koenker, R., Portnoy, S., 1993.

Tests of linear hypotheses based on regression rank scores. J. Nonparametr.

Statist. 2 (4), 307–331.

URL http://dx.doi.org/10.1080/10485259308832561 - He et al. (2016) He, F., Cheng, Y., Tong, T., 2016. Estimation of extreme conditional quantiles through an extrapolation of intermediate regression quantiles. Statistics and Probability Letters 113, 30–37.

- Hill (1975) Hill, B. M., 1975. A simple general approach to inference about the tail of a distribution. Annals of Statistics 3 (5), 1163–1174.

- Jansen and de Vries (1991) Jansen, D. W., de Vries, C. G., 1991. On the frequency of large stock returns: Putting booms and busts into perspective. Review of Economics and Statistics 73, 18–24.

-

Jurečková (1999)

Jurečková, J., 1999. Regression rank-scores tests against

heavy-tailed alternatives. Bernoulli 5 (4), 659–676.

URL http://dx.doi.org/10.2307/3318695 -

Jurečková (2016)

Jurečková, J., 2016. Averaged extreme regression quantile. Extremes

19 (1), 41–49.

URL http://dx.doi.org/10.1007/s10687-015-0232-2 - Knight (2001) Knight, K., 2001. Limiting distributions of linear programming estimators. Extremes 4 (2), 87–103.

-

Koenker (2016)

Koenker, R., 2016. quantreg: Quantile Regression. R package version 5.21.

URL https://CRAN.R-project.org/package=quantreg - Koenker and Bassett (1978) Koenker, R., Bassett, G. S., 1978. Regression quantiles. Econometrica 46, 33–50.

- Laplace (1818) Laplace, P.-S., 1818. Théorie analytique des probabilités. Éditions Jacques Gabay (1995), Paris.

- Leadbetter et al. (1983) Leadbetter, M. R., Lindgren, G., Rootzén, H., 1983. Extremes and related properties of random sequences and processes. Springer-Verlag, New York-Berlin.

- Longin (1996) Longin, F. M., 1996. The asymptotic distribution of extreme stock market returns. Journal of Business 69 (3), 383–408.

- Mandelbrot (1963) Mandelbrot, M., 1963. The variation of certain speculative prices. Journal of Business 36, 394–419.

- Meyer (1973) Meyer, R. M., 1973. A poisson-type limit theorem for mixing sequences of dependent “rare” events. Annals of Probability 1, 480–483.

- Pickands (1975) Pickands, III, J., 1975. Statistical inference using extreme order statistics. Annals of Statistics 3, 119–131.

- Politis et al. (1999) Politis, D. N., Romano, J. P., Wolf, M., 1999. Subsampling. New York: Springer-Verlag.

- Portnoy and Jurec̆ková (1999) Portnoy, S., Jurec̆ková, J., 1999. On extreme regression quantiles. Extremes 2 (3), 227–243.

-

Portnoy and Koenker (1989)

Portnoy, S., Koenker, R., 1989. Adaptive -estimation for linear models.

Ann. Statist. 17 (1), 362–381.

URL http://dx.doi.org/10.1214/aos/1176347022 - Powell (1984) Powell, J. L., 1984. Least absolute deviations estimation for the censored regression model. Journal of Econometrics 25, 303–325.

- Powell (1991) Powell, J. L., 1991. Estimation of monotonic regression models under quantile restrictions. Nonparametric and semiparametric methods in Econometrics,(Cambridge University Press, New York, NY), 357–384.

- Praetz (1972) Praetz, V., 1972. The distribution of share price changes. Journal of Business 45 (1), 49–55.

- Sen (1973) Sen, A., 1973. On economic inequality.

-

Smith (1994)

Smith, R. L., 1994. Nonregular regression. Biometrika 81 (1), 173–183.

URL http://dx.doi.org/10.1093/biomet/81.1.173 - Timmer (1971) Timmer, C. P., 1971. Using a probabilistic frontier production function to measure technical efficiency. Journal of Political Economy 79, 776–794.

- Wang et al. (2012) Wang, H., Li, D., He, X., 2012. Estimation of high conditional quantiles for heavy-tailed distributions. Journal of the American Statistical Association 107, 1453–1464.

- White (2001) White, H., 2001. Asymptotic Theory for Econometricians, revised Edition. New York: Academic Press.

- Zhang (2015) Zhang, Y., 2015. Extremal quantile treatment effects, job Market Paper.

- Zipf (1949) Zipf, G., 1949. Human Behavior and the Principle of Last Effort. Cambridge, MA: Addison-Wesley.