Simultaneous multiple change-point and factor analysis for high-dimensional time series

Abstract

We propose the first comprehensive treatment of high-dimensional time series factor models

with multiple change-points in their second-order structure.

We operate under the most flexible definition of piecewise stationarity,

and estimate the number and locations of change-points consistently

as well as identifying whether they originate in the common or idiosyncratic components.

Through the use of wavelets, we transform the problem of change-point detection in the second-order structure

of a high-dimensional time series, into the (relatively easier) problem of change-point detection

in the means of high-dimensional panel data.

Also, our methodology circumvents the difficult issue of the accurate estimation of

the true number of factors in the presence of multiple change-points by adopting a screening procedure.

We further show that consistent factor analysis is achieved over each segment

defined by the change-points estimated by the proposed methodology.

In extensive simulation studies, we observe that factor analysis

prior to change-point detection improves the detectability of change-points,

and identify and describe an interesting ‘spillover’ effect in which

substantial breaks in the idiosyncratic components get,

naturally enough, identified as change-points in the common components, which prompts us to regard

the corresponding change-points as also acting as a form of ‘factors’.

Our methodology is implemented in the R package factorcpt, available from CRAN.

Key words: piecewise stationary factor model, change-point detection, principal component analysis,

wavelet transformation, Double CUSUM Binary Segmentation.

Email: m.barigozzi@lse.ac.uk.22footnotetext: School of Mathematics, University of Bristol, University Walk, Bristol, BS8 1TW, UK.

Email: haeran.cho@bristol.ac.uk.33footnotetext: Department of Statistics, London School of Economics, Houghton Street, London WC2A 2AE, UK.

Email: p.fryzlewicz@lse.ac.uk.

1 Introduction

High-dimensional time series data abound in modern data science, including finance (e.g., simultaneously measured returns on a large number of assets (Fan et al., 2011b; Barigozzi and Hallin, 2017)), economics (e.g., country-level macroeconomic data (Stock and Watson, 2009) or retail price index data (Groen et al., 2013)), neuroimaging (e.g., measurements of brain activity (Schröder and Ombao, 2016; Barnett and Onnela, 2016)) and biology (e.g., transcriptomics data (Omranian et al., 2015) or Hi-C data matrices (Brault et al., 2016)).

Factor modelling, in which the individual elements of a high-dimensional time series are modelled as sums of a common component (a linear combination of a small number of possibly unknown factors), plus each individual element’s own idiosyncratic noise, is a well-established technique for dimension reduction in time series. Time series factor models are classified, in relation to the effect of factors on the observed time series, into ‘static’ (only a contemporaneous effect, see e.g., Stock and Watson (2002); Bai and Ng (2002); Bai (2003)) or ‘dynamic’ (lagged factors may also have an effect, see e.g., Forni and Lippi (2001); Hallin and Lippi (2013)) factor models.

It is increasingly recognised that in several important application areas, such as those mentioned at the beginning of this section, nonstationary time series data are commonly observed. Arguably the simplest realistic departure from stationarity, which also leads to sparse and interpretable time series modelling, is piecewise-stationarity, in which the time series is modelled as approximately stationary between neighbouring change-points, and changing its distribution (e.g., the mean or covariance structure) at each change-point.

The main aim of this work is to provide the first comprehensive framework for the estimation of time series factor models with multiple change-points in their second-order structure. The existing literature on time series factor modelling has only partially embraced nonstationarity. One way in which a change-point is typically handled in the literature is via the assumption that the structural break in the loadings is ‘moderate’ and it affects only a limited number of series, so that it does not adversely impact the quality of traditional stationary principal component analysis (PCA)-type estimation (Stock and Watson, 2002, 2009; Bates et al., 2013).

However, opinions diverge on the empirically relevant degrees of temporal instability in the factor loadings, and several authors observe that ‘large’ changes in the stochastic data-generating mechanism have the potential to severely distort the estimation of the factor structure. Investigations into the effect of a single break in the loadings or the number of factors on the factor structure, with accompanying change-point tests and estimators for its location, can be found in Breitung and Eickmeier (2011), Chen et al. (2014), Han and Inoue (2014), Corradi and Swanson (2014), Yamamoto and Tanaka (2015), Baltagi et al. (2017), Bai et al. (2017) and Massacci (2017). Lasso-type estimation is considered for change-point analysis under factor modelling in Cheng et al. (2016) and Ma and Su (2016): the former concerns single change-point detection in the loadings and the number of factors, while the latter considers multiple change-point detection in loadings only. Note that the -penalty of the Lasso is not optimal for change-point detection, as investigated in Brodsky and Darkhovsky (1993) and Cho and Fryzlewicz (2011). In summary, apart from Ma and Su (2016) and Sun et al. (2016) (the latter considers factor models with multiple change-points but for a small number of time series only), the existing change-point methods proposed for factor models focus on detecting a single break of a particular type, namely a break in the loadings or the number of factors.

We now describe in detail the contribution and findings of this work, at the same time giving an overview of the organisation of the paper.

-

(a)

We propose a comprehensive methodology for the consistent estimation of multiple change-points in the second-order structure of a high-dimensional time series governed by a factor model. This is in contrast to the substantial time series factor model literature, which is overwhelmingly concerned with testing for a single change-point. In practice, the possibility of the presence of multiple change-points cannot be ruled out from a dataset consisting of observations over a long stretch of time, as illustrated in our applications to financial and macroeconomic time series data in Section 8. Our estimators are ‘interpretable’ in the sense that they enable the identification of whether each change-point originates from the common or idiosyncratic components. Through simulation studies (Section 7), it is demonstrated that in high-dimensional time series segmentation, factor analysis prior to change-point detection improves the detectability of change-points that appear only in either of the common or the idiosyncratic components.

-

(b)

We operate under the most flexible definition of piecewise-stationarity, embracing all possible structural instabilities under factor modelling: it allows factors and idiosyncratic components to have unrestricted piecewise-stationary second-order structures, including changes in their autocorrelation structures (Section 2).

-

(c)

We derive a uniform convergence rate for the PCA-based estimator of the common components under the factor model with multiple change-points in Theorems 1 and 2 (Section 3.1). A key to the derivation of the theoretical results is the introduction of the ‘capped’ PCA estimator of the common components, which controls for the possible contribution of spurious factors to individual common components even when the number of factors is over-specified.

-

(d)

Through the use of wavelets, we transform the problem of change-point detection in the second-order structure of a high-dimensional time series, into the (relatively easier) problem of change-point detection in the means of high-dimensional panel data. More specifically, in the first stage of the proposed methodology, we decompose the observed time series into common and idiosyncratic components, and we compute wavelet transforms for each component (separately), see e.g., Nason et al. (2000), Fryzlewicz and Nason (2006) and Van Bellegem and von Sachs (2008) for the use of locally stationary wavelet models for time series data. In this way, any change-point in the second-order structure of common or idiosyncratic components is detectable as a change-point in the means of the wavelet-transformed series (Sections 3.2 and 3.3).

-

(e)

Each of the panels of transformed common and idiosyncratic components serves as an input to the second stage of our methodology, which requires an algorithm for multiple change-point detection in the means of high-dimensional panel data. For this, a number of methodologies have been investigated in the literature, such as Horváth and Hušková (2012), Enikeeva and Harchaoui (2015), Jirak (2015), Cho and Fryzlewicz (2015) and Wang and Samworth (2018). In Section 4.1, we adopt the Double CUSUM Binary Segmentation procedure proposed in Cho (2016), which achieves consistency in estimating the total number and locations of the multiple change-points while permitting both within-series and cross-sectional correlations. In Section 4.2, we prove that this consistency result carries over to the consistency in multiple change-point detection in the common and idiosyncratic components, as the dimensions of the data, and , diverge (Theorem 3).

-

(f)

Motivated by the theoretical finding noted in (c), our methodology is equipped with a step that screens the results of change-point analysis over a range of factor numbers employed for the estimation of common components (Section 4.3). It enables us to circumvent the challenging problem of accurately estimating the true number of factors in contrast to much of the existing literature, and plays the key role for the proposed methodology to achieve consistent change-point estimation.

-

(g)

Once all the change-points are estimated, we show that the common components are consistently estimated via PCA on each estimated segment (Section 5). Such result is new to the literature on factor models with structural breaks.

-

(h)

We identify and describe an interesting ‘spillover’ effect in which change-points attributed to large breaks in the second-order structure of the idiosyncratic components get (seemingly falsely) identified as change-points in the common components (Section 7). We argue that this phenomenon is only too natural and expected, and can be ascribed to the prominent change-points playing the role of ‘common factors’, regardless of whether they originate in the common or idiosyncratic components. We refer to this new point of view as regarding change-points as factors.

-

(i)

We provide an R package named factorcpt, which implements our methodology. The package is available from CRAN (Cho et al., 2016).

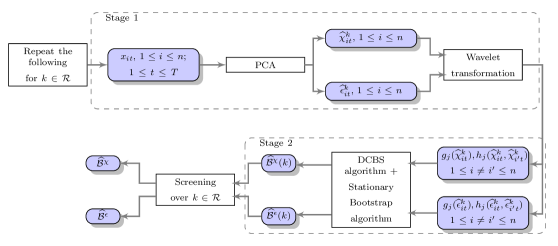

An overview of the proposed methodology

We provide an overview of the change-point detection methodology with an accompanying flowchart in Figure 1. For each step, we provide a reference to the relevant section in the paper.

- Input:

-

time series and a set of factor number candidates .

- Iteration:

-

repeat Stages 1–2 for all .

- Stage 1: Factor analysis and wavelet transformation.

- Stage 2: High-dimensional panel data segmentation.

- Screening over :

-

the sets are screened to obtain the final estimates and (Section 4.3).

Notation

For a given matrix with denoting its element, its spectral norm is defined as , where denotes the th largest eigenvalue of , and its Frobenius norm as . For a given set , we denote its cardinality by . The indicator function is denoted by . Also, we use the notations and . Besides, indicates that is of the order of , and that . We denote an -matrix of zeros by .

2 Piecewise stationary factor model

In this section, we define a piecewise stationary factor model which provides a framework for developing our change-point detection methodology. Throughout, we assume that we observe an -dimensional vector of time series , following a factor model and undergoing an unknown number of change-points in its second-order structure. The location of the change-points is also unknown. Each of element can be written as:

| (1) |

where and denote the common and the idiosyncratic components of , with for all . We refer to as the number of factors in model (1). Then the common components are driven by the factors with , and denotes the -dimensional vector of loadings. We denote the matrix of factor loadings by . The change-points in the second-order structure of are classified into , those in the common components, and , those in the idiosyncratic components.

Remark 1.

In the factor model (1), both the loadings and the factor number are time-invariant. However, it is well established in the literature on factor models with structural breaks, that any change in the number of factors or loadings can be represented by a factor model with stable loadings and time-varying factors. In doing so, , the dimension of the factor space under (1), satisfies , where denotes the minimum number of factors of each segment , , over which the common components remain stationary. We provide a comprehensive example illustrating this point in Appendix A. Many tests and estimation methods for changes in the loadings rely on this equivalence between the two representations of time-varying factor models, see e.g., Han and Inoue (2014) and Chen et al. (2014). Therefore, we work with the representation in (1), where all change-points in the common components are imposed on the second-order structure of as detailed in Assumption 1 below. At the same time, we occasionally speak of changes in the loadings or the number of factors, referring to those changes in that can be ascribed back to such changes.

We denote by the index of the change-point in that is nearest to, and strictly to the left of , and by the latest change-point in strictly before , with the notational convention and . Similarly, is defined with respect to , and denotes the index of the change-point in that is nearest to while being strictly to its left. Then, we impose the following conditions on and .

Assumption 1.

-

(i)

There exist weakly stationary processes associated with the intervals for such that for all , and

for some fixed .

-

(ii)

Let and denote the (auto)covariance matrix of by . Then, there exists fixed such that for any , we have for some .

-

(iii)

There exist weakly stationary processes associated with the intervals for such that for all , and

for some fixed .

-

(iv)

Denote the (auto)covariance matrix of by . Then, there exists fixed such that for any , we have for some .

Assumption 1 (i)–(ii) indicates that for each , the common component is ‘close’ to a stationary process over the segment such that the effect of transition from one segment to another diminishes at a geometric rate as moves away from , and any coincides with a change-point in the autocovariance or cross-covariance matrices of . The same arguments apply to under Assumption 1 (iii)–(iv). The treatment of such approximately piecewise stationary and is similar to that in Fryzlewicz and Subba Rao (2014).

Note that the literature on factor models with structural breaks have primarily focused on the case of a single change-point in the loadings or factor number see e.g., Breitung and Eickmeier (2011), Chen et al. (2014) and Han and Inoue (2014). We emphasise that to the best of our knowledge, the model (1) equipped with Assumption 1 is the first one to offer a comprehensive framework that allows for multiple change-points that are not confined to breaks in the loadings or the emergence of a new factor, but also includes breaks in the second-order structure of the factors and idiosyncratic components.

We now list and motivate the assumptions imposed on the piecewise stationary factor model; see e.g., Stock and Watson (2002), Bai and Ng (2002), Bai (2003), Forni et al. (2009) and Fan et al. (2013) for similar conditions on stationary factor models.

Assumption 2.

-

(i)

.

-

(ii)

There exists some fixed such that, for any and ,

Assumption 3.

-

(i)

There exists a positive definite matrix with distinct eigenvalues, such that as .

-

(ii)

There exists such that for all .

Assumption 4.

-

(i)

There exists such that

for any sequence of coefficients satisfying .

-

(ii)

are normally distributed.

Assumption 5.

-

(i)

and are independent.

-

(ii)

Denoting the -algebra generated by by , let

Then, there exists some fixed satisfying , such that, for all , we have .

We adopt the normalisation given in Assumption 2 (i) for the purpose of identification; in general, factors and loadings are recoverable up to a linear invertible transformation only. Similar assumptions are found in the factor model literature, see e.g., equation (2.1) of Fan et al. (2013). In order to motivate Assumptions 2 (i), 3 and 4 (i), we introduce the notations

We denote the eigenvalues (in non-increasing order) of , , , and by , , , and , respectively. Then, Assumptions 2 (i) and 3 imply that are diverging as and, in particular, are of order for all . Assumption 3 implicitly rules out change-points which are due to weak changes in the loadings, in the sense that the magnitudes of the changes in the loadings are small, or only a small fraction of undergoes the change. A similar requirement can be found in e.g., Assumption 1 of Chen et al. (2014) and Assumption 10 of Han and Inoue (2014). We note that Bai et al. (2017) studies the consistency of a least squares estimator for a single change-point attributed to a possibly weak break in the loadings in the above sense. In Section 7, we provide numerical results on the effect of the size of the break on our proposed methodology.

Assumption 4 (i) guarantees that, when is a normalised eigenvector of , then the largest eigenvalue of is bounded for all and , that is . This is the same assumption as those made in Chamberlain and Rothschild (1983) and Forni et al. (2009) and comparable to Assumption C.4 of Bai (2003) and Assumption 2.1 of Fan et al. (2011a) in the stationary case. Note that Assumption 4 (i) is sufficient in guaranteeing the commonness of and the idiosyncrasy of according to Definitions 2.1 and 2.2 of Hallin and Lippi (2013). Assumption 4 (ii) may be relaxed to allow for of exponential-type tails, provided that the tail behaviour carries over to the cross-sectional sums of . Note that the normality of the idiosyncratic component does not necessarily imply the normality of the data since the factors are allowed to be non-normal.

Assumption 5 is commonly found in the factor model literature (see e.g., Assumptions 3.1–3.2 of Fan et al. (2011a)). In particular, the exponential-type tail conditions in Assumptions 2 (ii) and 4 (ii), along with the mixing condition in Assumption 5 (ii), allow us to control the deviation of sample covariance estimates from their population counterparts, via Bernstein-type inequality (see e.g., Theorem 1.4 of Bosq (1998) and Theorem 1 of Merlevède et al. (2011)).

We also assume the following on the minimum distance between two adjacent change-points.

Assumption 6.

There exists a fixed such that

Under Assumptions 2–6, the eigenvalues of and satisfy:

-

(C1)

there exist some fixed such that for ,

and for ;

-

(C2)

, for any .

Moreover, by Weyl’s inequality, we have the following asymptotic behaviour of the eigenvalues of :

-

(C3)

the largest eigenvalues, , are diverging linearly in as ;

-

(C4)

the th largest eigenvalue, , stays bounded for any .

From (C1)–(C4) above, it is clear that for identification of the common and idiosyncratic components, factor models need to be studied in the asymptotic limit where and . This requirement, in practice, recommends the use of large cross-sections to apply PCA for factor analysis. In particular, we require

Assumption 7.

as , with for some .

Under Assumption 7, we are able to establish the consistency in estimation of the common components as well as that of the change-points in high-dimensional settings where , even when the factor number is unknown.

Remark 2.

The multiple change-point detection algorithm adopted in Stage 2 of our methodology still achieves consistency when Assumption 6 is relaxed to allow for some fixed and , with increasing in such that . However, under these relaxed conditions, it is no longer guaranteed that and, consequently, have diverging eigenvalues. Therefore, in this paper we limit the scope of our theoretical results to the more restricted setting of Assumption 6.

3 Factor analysis and wavelet transformation

3.1 Estimation of the common and idiosyncratic components

Decomposing into common and idiosyncratic components is an essential step for the separate treatment of the change-points in and , such that we can identify the origins of detected change-points. Therefore, in this section, we establish the asymptotic bounds on the estimation error of the common and idiosyncratic components, when using PCA under the piecewise stationary factor model in (1).

Let denote the -dimensional normalised eigenvector corresponding to the th largest eigenvalue of the sample covariance matrix, , with its entries , . When the number of factors is known, the PCA estimator of is defined as , for which the following theorem holds.

Proofs of Theorem 1 and all other theoretical results are provided in the Appendix.

Despite the presence of multiple change-points, allowed both in the variance and autocorrelations of , the rate of convergence for is almost as fast as the one derived for the stationary case, e.g., Theorem 3 of Bai (2003), and Theorem 1 of Pelger (2015) and Theorem 5 of Aït-Sahalia and Xiu (2017) in the context of factor modelling high-frequency data. We highlight that Theorem 1 derives a uniform bound on the estimation error over and ; similar results are found in Theorem 4 of Fan et al. (2013).

However, the true number of factors is typically unknown and, since the seminal paper by Bai and Ng (2002), estimation of the number of factors has been one of the most researched problems in the factor model literature; see also Alessi et al. (2010), Onatski (2010) and Ahn and Horenstein (2013). Although, Han and Inoue (2014) (in their Proposition 1) and Chen et al. (2014) (in their Proposition 2) showed that the information criteria of Bai and Ng (2002) achieve asymptotic consistency in estimating in the presence of a single break in the loadings, it has been observed that such an approach tends to exhibit poor finite sample performance when the idiosyncratic components are both serially and cross-sectionally correlated, or when is large compared to . Also, it was noted that the factor number estimates heavily depend on the relative magnitude of and and the choice of penalty terms as demonstrated in the numerical studies of Bai and Ng (2002) and Ahn and Horenstein (2013). While the majority of change-point methods for factor models rely on the consistent estimation of the number of factors (Breitung and Eickmeier, 2011; Han and Inoue, 2014; Chen et al., 2014; Corradi and Swanson, 2014), our empirical study on simulated data, available in the supplementary document, indicates that this dependence on a single estimate may lead to failure in change-point detection.

To remedy this, we propose to consider a range of factor number candidates in our change-point analysis, in particular, allowing for the over-specification of the number of factors. In high dimensions, the estimated eigenvectors for are in general not consistent, as implied by Theorem 2 of Yu et al. (2015). Thus, estimates of common components based on more than principal components may be subject to a non-negligible overestimation error. In order to control the effect of over-specifying the number of factors, we propose a modified PCA estimator of defined as , where each element of is ‘capped’ according to the rule

for some fixed . The estimated loadings are then given by and the factors by . A practical way of choosing is discussed in Section 6.2.

Note that, thanks to the result in (C3) and Lemmas 2 and 3 in the Appendix, we have . In other words, asymptotically, the capping does not alter the contribution from the leading eigenvectors of to , even when the capping is applied without the knowledge of . On the other hand, by means of this capping, we control the contribution from the ‘spurious’ eigenvectors when , which allows us to establish the following bound on the partial sums of the estimation errors even when the factor number is over-specified.

Theorem 2.

The bound in (2) concerns the case in which we correctly specify the number of factors and is in agreement with Theorem 1. Turning to when the factor number is over-specified, Forni et al. (2000) (in their Corollary 2) and Onatski (2015) (in his Proposition 1) reported similar results for the stationary case. However, the uniform consistency of , in the presence of multiple change-points, has not been spelled out before in the factor model literature to the best of our knowledge; we achieve this via the proposed capping. On the other hand, it is possible to show that with , the estimation error in is non-negligible. Lastly, thanks to Lemma 4 in Appendix, it is straightforward to show that analogous bounds hold for the idiosyncratic component .

Although the over-specification of brings the bound in (2) to increase by , we can still guarantee that all change-points in () are detectable from () provided that , as shown in Proposition 1 and Theorem 3 below. In what follows, we continue describing our methodology by supposing that is given, and we refer to Section 4.3 for the complete description of the proposed ‘screening’ procedure that considers a range of values for .

3.2 Wavelet periodograms and cross-periodograms

As the first stage of the proposed methodology, we construct a wavelet-based transformation (WT) of the estimated common and idiosyncratic components and from Section 3.1, which serves as an input to the algorithm for high-dimensional change-point analysis in Stage 2. In order to motivate the WT, which will be formally introduced in Section 3.3, we limit our discussion in this section to the (unobservable) common component ; the same arguments hold verbatim for the idiosyncratic one. In practice, the WT is performed on the estimated common component, , and the effect of considering estimated quantities rather than the true ones is studied in Section 3.3.

Nason et al. (2000) have proposed the use of wavelets as building blocks in nonstationary time series analogous to Fourier exponentials in the classical Cramér representation for stationary processes. The simplest example of a wavelet system, Haar wavelets, are defined as

with denoting the wavelet scale, and denoting the location. Small negative values of the scale parameter denote fine scales where the wavelet vectors are more localised and oscillatory, while large negative values denote coarser scales with longer, less oscillatory wavelet vectors.

Recall the notation . Wavelet coefficients of (introduced in Assumption 1) are defined as , with respect to , a vector of discrete wavelets at scale . Note that the support of is of length for a fixed (which depends on the choice of wavelet family), so that we have access to wavelet coefficients from at most scales for a time series of length . In other words, wavelet coefficients are obtained by filtering with respect to wavelet vectors of finite lengths.

Wavelet periodogram and cross-periodogram sequences of are defined as and . It has been shown that the expectations of these sequences have a one-to-one correspondence with the second-order structure of the input time series, see Cho and Fryzlewicz (2012) for the case of univariate time series and Cho and Fryzlewicz (2015) for the high-dimensional case. To illustrate, suppose that . Then,

| (4) | |||||

where (with unless ) denotes the autocorrelation wavelets (Nason et al., 2000) and . That is, provided that is sufficiently distanced (by ) from any change-points to its left, is a wavelet transformation of the (auto)covariances . Similar arguments hold between wavelet cross-periodograms and cross-covariances of . Following Cho and Fryzlewicz (2015), we conclude that under Assumption 1 (ii), any jump in the autocovariance and cross-covariance structures of is translated to a jump in the means of its wavelet periodogram and cross-periodogram sequences at some wavelet scale , in the following sense: are ‘almost’ piecewise constant with their change-points coinciding with those in , apart from intervals of length around the change-points.

It is reasonable to limit our consideration to wavelets at the first finest scales (with ), in order to control the possible bias in change-point estimation that arises from the transition intervals of length . On the other hand, due to the compactness of the support of , a change in that appears only at some large lags (), is not detectable as a change-point in the wavelet periodogram and cross-periodogram sequences at the few finest scales (), see (4). To strike a balance between the above quantities related to the choice of , we set for some and some fixed . We refer to Section 6.2 for the choice of . Then,

-

(a)

any change in that occurs at (at least) one out of an increasing number of lags (), is registered as a change-point in the expectations of the wavelet (cross-)periodograms of ;

-

(b)

the possible bias in the registered locations of the change-points is controlled to be at most .

3.3 Wavelet-based transformation for change-point analysis

In this section, we propose the WT of estimated common and idiosyncratic components, and show that the change-points in the complex (autocovariance and cross-covariance) structure of (unobservable) and , are made detectable as the change-points in the relatively simple structure (means) of the panel of the wavelet transformed and . This panel then serves as an input to Stage 2 of our methodology, as described in Section 4. As in Section 3.2, we limit the discussion of the WT and its properties when applied to the change-point analysis of the common components; the same arguments are applicable to that of the idiosyncratic components.

Let denote the wavelet coefficients of . Then, for each , we propose the following transformation which takes and produces a panel of -dimensional sequences with elements:

where . For example, with Haar wavelets at scale ,

Remark 3.

Notice that is simply the squared root of the wavelet periodogram of at scale . Arguments supporting the choice of in place of wavelet cross-periodogram sequences can be found in Section 3.1.2 of Cho and Fryzlewicz (2015), where it is guaranteed that any change detectable from can also be detected from with either of . As per the recommendation made therein, we select , where denotes the sample correlation between and over . This is in an empirical effort to select that better brings out any change in for the given data.

As with wavelet periodograms and cross-periodograms discussed in Section 3.2, the transformed series and contain the change-points in the second-order structure of as change-points in their ’signals’. This is formalised in the following proposition.

Proposition 1.

Suppose that all the conditions in Theorem 2 hold. For some fixed and , consider the -dimensional panel

| (5) |

and denote as a generic element of (5). Then, we have the following decomposition:

| (6) |

-

(i)

are piecewise constant as the corresponding elements of

(7) That is, all change-points in belong to and for each , there exists at least a single index for which .

-

(ii)

.

Therefore, the panel data in (5) contains all change-points in the second-order structure of as the change-points in its piecewise constant signals represented by .

Let us denote by an element of the panel obtained by transforming in place of in (5). Then, the proof of Proposition 1 is based on the following decomposition

Then, accounts for the discrepancy between and and is controlled by Assumption 1 (i), and follows from the weak dependence structure and the tail behaviour of assumed in Assumptions 2 (ii) and 5. Term arises from the estimation error in which can be bounded as shown in Theorem 2, which further motivates the WT of via and rather than using its wavelet (cross-)periodograms.

To conclude, note that the WT of are collected into the -dimensional panel

| (8) |

for change-point analysis, where the elements of (8) are also decomposed into piecewise constant signals

| (9) |

and error terms of bounded partial sums; see Appendix C where we present the result analogous to Proposition 1 for the idiosyncratic components.

4 High-dimensional panel data segmentation

4.1 Double CUSUM Binary Segmentation

Cumulative sum (CUSUM) statistics have been widely adopted for change-point detection in both univariate and multivariate data. In order to detect change-points in the -dimensional additive panel data in (5), we compute univariate CUSUM series and aggregate the high-dimensional CUSUM series via the Double CUSUM statistic proposed by Cho (2016), which achieves this through point-wise, data-driven partitioning of the panel data When dealing with multiple change-point detection, the Double CUSUM statistic is used jointly with binary segmentation in an algorithm, which we refer to as the Double CUSUM Binary Segmentation (DCBS) algorithm. The DCBS algorithm guarantees the consistency in multiple change-point detection in high-dimensional settings, as shown in Theorem 3, while allowing for the cross-sectional size of change to decrease with increasing sample size (see Assumption 9 below). Further, it admits both serial- and cross-correlations in the data, which is a case highly relevant for the time series factor model considered in this paper.

Consider the -dimensional input panel , computed from or for the change-point analysis in either the common or the idiosyncratic components via WT; see (5) and (8) for their definitions. We define the CUSUM series of over a generic segment for some , as

for , where denotes a scaling constant for treating all rows of the panel data on equal footing; see Remark 4 below for its choice. We note that if in (6) were i.i.d. Gaussian random variables, the maximum likelihood estimator of the change-point location for would coincide with .

Proposed in Cho (2016), the Double CUSUM (DC) operator aggregates the series of CUSUM statistics from and returns a two-dimensional array of DC statistics:

for and , where denotes the CUSUM statistics at ordered according to their moduli, i.e., . Notice that takes the contrast between the largest CUSUM values and the rest at each , and thus partitions the coordinates into the that are the most likely to contain a change-point and those which are not in a point-wise manner. Then, the test statistic is derived by maximising the two-dimensional array of DC statistics over both time and cross-sectional indices, as

| (10) |

which is compared against a threshold for determining the presence of a change-point over the interval . If , the location of the change-point is identified as

Remark 4 (Choice of .).

Cho (2016) assumes second-order stationarity on the error term in (6), which enables the use of its long-run variance estimator as the scaling term . However, it is not trivial to define a similar quantity in the problem considered here, particularly due to the possible nonstationarities in . Following Cho and Fryzlewicz (2015), in order for the CUSUM series computed on not to depend on the level of , we also adopt the choice of . Note that the asymptotic consistency of the DCBS algorithm in Theorem 3 below does not depend on the choice of , provided that it is bounded away from zero and from the above for all with probability tending to one (see Assumption (A6) of Cho (2016)). By adopting arguments similar to those in the proof of Lemma 6 in Cho and Fryzlewicz (2012), it can be shown that our choice of satisfies these properties.

We now formulate the DCBS algorithm which is equipped with the threshold . The index is used to denote the level (indicating the progression of the segmentation procedure) and to denote the location of the node at each level.

- The Double CUSUM Binary Segmentation (DCBS) algorithm

- Step 0:

-

Set , , and .

- Step 1:

-

At the current level , repeat the following for all .

- Step 1.1:

-

Letting and , obtain the series of CUSUMs for and , on which is computed over all and .

- Step 1.2:

-

Obtain the test statistic .

- Step 1.3:

-

If , quit searching for change-points on the interval . On the other hand, if , locate , add it to the set of estimated change-points , and proceed to Step 1.4.

- Step 1.4:

-

Divide the interval into two sub-intervals and , where , , and .

- Step 2:

-

Once for all are examined at level , set and go to Step 1.

Step 1.3 provides a stopping rule to the DCBS algorithm, by which the search for further change-points is terminated once on every segment defined by two adjacent estimated change-points in . Depending on the choice of the input panel data as in (5) or (8), the DCBS algorithm returns or , the sets of change-points detected from and , respectively.

4.2 Consistency in multiple change-point detection

In this section, we show the consistency of change-points estimated for the common and idiosyncratic components by the DCBS algorithm, in terms of their total number and locations. Consider the panel that represents the WTs of and as in (5) and (8), respectively. In either case, let denote the change-points in the piecewise constant signals underlying (see (7) and (9) for the precise definitions of ), so that we have either with , or with . We impose the following assumptions on the signals and the change-point structure therein.

Assumption 8.

There exists a fixed constant such that .

Assumption 9.

At each , define , the index set of those that undergo a break at , and denote its cardinality by . Further, let , the average size of jumps in at . Then satisfies as .

Assumption 8 requires the expectations of the WTs of and defined in Assumption 1 to be bounded, which in fact holds trivially as for all .

Assumption 9 imposes a condition on the minimal cross-sectional size of the changes in , represented by . Under Assumption 3, the change-points which are due to breaks in the loadings or (dis)appearance of new factors (see Remark 1), are implicitly required to be ‘dense’, in the sense that the number of coordinates in affected by the changes is of order . Consequently, such changes appear in a large number (of order ) of elements of and, therefore, that of the WT of the second-order structure, . Similarly, noting that , a break in the autocovariance functions of results in a dense change-point that affects a large number of . In other words, for change-point analysis in the common components, Assumption 9 is reduced to requiring , as , allowing for the average jump size in individual coordinates to tend to zero at a rate slower than , and is no longer dependent on . On the other hand, our model in (1) does not impose any assumption on the ‘denseness’ of , and sparse change-points (with ) in the idiosyncratic components are detectable provided that their sparsity is compensated by the size of jumps, .

Let denote the change-points detected from by the DCBS algorithm, i.e., or , depending on whether is the WT of or for some fixed . Accordingly, we have either with , or with . Then the following theorem establishes that the DCBS algorithm performs consistent change-point analysis for both the common and the idiosyncratic components.

Theorem 3.

Theorem 3 shows both the total number and the locations of the change-points in and are consistently estimated; in the rescaled time , the bound on the bias in estimated change-point locations satisfies as under Assumption 9. The optimality in change-point detection may be defined as when the true and estimated change-points are within the distance of (Korostelev, 1987). With our approach, near-optimality in change-point estimation is achieved up to a logarithmic factor when the change-points are cross-sectionally dense () with average size bounded away from zero, so that .

4.3 Screening over a range of factor number candidates

In this section, we detail a screening procedure motivated by Theorem 2, which enables us to bypass the challenging task of estimating the number of factors in the presence of (possibly) multiple change-points in the factor structure.

The performance of most methods proposed for change-point analysis under factor modelling, such as those listed in Introduction, relies heavily on accurate estimation of the factor number. Thanks to Theorem 2, however, mis-specifying the factor number in our methodology does not influence the theoretical consistency as reported in Theorem 3, provided that we choose sufficiently large to satisfy . Based on this observation, we propose to screen , the set of change-points detected from , for a range of factor number candidates denoted as . Specifically, we select the with the largest cardinality over and, if there is a tie, we select with the largest . Denoting , change-points in the idiosyncratic components are detected from , where .

As noted below Theorem 2, using factors leads to with non-negligible estimation error which may not contain all the change-points in as change-points in its second-order structure. Moreover, with such , some ’s may appear as change-points in , which we refer to as the spillage of change-points in the common components over to the idiosyncratic components. This justifies the proposed screening procedure and the choice of .

For , we use the number of factors estimated by minimising the information criterion of Bai and Ng (2002) using as penalty ; in principle, any other procedure for factor number estimation may be adopted to select . The range also involves the choice of the maximum number of factors, . In the factor modelling literature, this choice is a commonly faced problem, e.g., when estimating the number of factors using an information criterion-type estimator. In the literature on stationary factor models, the maximum number of factors is usually fixed at a small number ( is used in Bai and Ng (2002)) for practical purposes. However, the presence of change-points tends to increase the number of factors, as shown with an example in Appendix A. Therefore, we set , where the second term dominates the first when and are large.

5 Factor analysis after change-point detection

Once the change-points are detected, we can estimate the factor space over each segment , defined by two consecutive change-points estimated from the common components. Denoting the sample covariance matrix over by , let denote the eigenvector of corresponding to its -th largest eigenvalue. Then, for a fixed number of factors , the segment-specific estimator of is obtained via PCA as .

The number of factors in the -th segment can be estimated by means of the information criterion proposed in Bai and Ng (2002):

| (11) |

where denotes the maximum allowable factor number, and the penalty function satisfies as well as . Motivated by the formulation of penalties in Bai and Ng (2002), we may use for some .

Let be the matrix of loadings for the -th segment. In order to discuss the theoretical properties of segment-wise factor analysis, we require the following assumption that extends Assumption 3 (i) to each segment .

Assumption 10.

There exists a positive definite matrix such that as .

Then, we obtain the asymptotic results in Propositions 2–3 for the segment-wise estimators of the factor number and the common components.

Proposition 2.

From Propositions 2 and 3, we have the guarantee that the factor space is consistently estimated by PCA over each estimated segment. We may further refine the post change-point analysis by first determining whether can be associated with (a) a break in the loadings or factor number, or (b) that in the autocorrelation structure of the factors only. This can be accomplished by comparing and against the factor number estimated from the pooled segment : a break in the loadings or factor number necessarily brings in a change in the number of factors from the pooled segment. However, if (b) is the case, the segments before and after as well as the pooled one return the identical number of factors, and we can perform the joint factor analysis of the two segments.

6 Computational aspects

6.1 Bootstrap procedure for threshold selection

The range of theoretical rates supplied for in Theorem 3, involves typically unattainable knowledge of the minimum cross-sectional size of the changes. Hence, we propose a bootstrap procedure for the selection of and , the thresholds for change-point analysis of and , respectively. We omit and from their subscripts for notational convenience when there is no confusion. Although a formal proof on the validity of the proposed bootstrap algorithm is beyond the scope of the current paper, simulation studies reported in Section 7 demonstrate its good performance when applied jointly with our proposed methodology. We refer to Trapani (2013), Corradi and Swanson (2014) and Gonçalves and Perron (2014, 2016) for alternative bootstrap methods under factor models and Jentsch and Politis (2015) for the linear process bootstrap for multivariate time series in general.

We propose a new bootstrap procedure which is specifically motivated by the separate treatment of common and idiosyncratic components in our change-point detection methodology. Namely, the resampling method produces bootstrap samples from the common and idiosyncratic components independently, relying on the consistency of the estimated components with an over-specified factor number as reported in Theorem 2.

Let and denote the test statistics computed on the interval for the panel data obtained from the WT of and , respectively. The proposed resampling procedure aims at approximating the distributions of and under the null hypothesis of no change-point, which then can be used for the selection of and , the corresponding, interval-specific test criteria for and over , an interval which is considered at some iteration of the DCBS algorithm.

Among the many block bootstrap procedures proposed in the literature for bootstrapping time series (see Politis and White (2004) for an overview), stationary bootstrap (SB) proposed in Politis and Romano (1994) generates bootstrap samples which are stationary conditional on the observed data (see Appendix D.4 for details). Based on the SB, our procedure derives and . Recall that and denote the loadings and factors estimated via the capped PCA for , see Section 3.1.

- Stationary bootstrap algorithm for factor models.

- Step 1

-

- For the common components:

-

For each , produce the SB sample of as . Compute .

- For the idiosyncratic components:

-

Produce the SB sample of as .

- Step 2:

-

Generate through transforming or using and as described in Section 3.3.

- Step 3:

-

Compute on and generate the test statistic according to (10).

- Step 4:

-

Repeat Steps 1–3 times. The critical value or for the segment is selected as the -quantile of the bootstrap test statistics at given .

The bootstrap algorithm is designed to produce and that mimic the second-order structure of and , respectively, when there is no change-point present, and thus approximates the distributions of the test statistics under the null hypothesis. In the algorithm, the treatment of the common and idiosyncratic components differs only in the application of SB in Step 1: since the factors estimated from the PCA are uncorrelated by construction, we generate the SB samples of for each separately, while the elements of are resampled jointly in an attempt to preserve the cross-sectional dependence therein. We discuss the choice of the bootstrap size and the level of quantile in Section 6.2.

6.2 Selection of tuning parameters

The proposed methodology involves the choice of tuning parameters for the capped PCA, WT, DCBS algorithm and the bootstrap procedure. We here list the values used for the simulation studies (Section 7) and real data analysis (Section 8). We provide further guidance on the implementation of the proposed methodology in Appendix D.

In the examples considered in Section 7, we have not observed unreasonably large contributions to from spurious factors. As noticed in Section 3.1, selecting a sufficiently large constant as effectively disables the capping for the (unknown) leading principal components to . For this reason, in the current implementation, we disable the capping. However, this does not necessarily mean that capping will always be of no practical use. Therefore, we recommend the data-driven choice of . With such , the capping is enabled for only those with , where and denote the smallest and largest number of factors considered in Section 4.3.

For the WT, we propose to use number of finest Haar wavelets for some and , in order to control for any bias in change-point estimation arising from WT. Noting that the bias increases at the rate with increasing , we recommend the choice of in practice.

Although omitted from the description of the DCBS algorithm, we select a parameter controlling the minimum distance between two estimated change-points. In light of Remark 2 and Theorem 3, we choose to use . Note that we can avoid using this parameter by replacing the binary segmentation procedure with wild binary segmentation (Fryzlewicz, 2014), such that the Double CUSUM is applied over randomly drawn intervals to derive the test statistic. It is conjectured that such a procedure will place a tighter bound on the bias in estimated change-point locations, as well as bypassing the need for the parameter . We leave the investigation in this direction for the future research.

Finally, for the proposed bootstrap procedure, we use the bootstrap sample size for the simulation studies and for the real data analysis. As for the level of quantile, we select ; note that this choice does not indicate the significance level in hypothesis testing.

7 Simulation studies

In this section, we apply the proposed change-point detection methodology to both single and multiple change-point scenarios under factor modelling. While our methodology is designed for multiple change-point detection, Section 7.1 gives us insight into its performance in the presence of a single change-point, which is of the type, size and denseness that vary in a systematic manner. Multiple change-point scenarios are considered in Section 7.2.

7.1 Single change-point scenarios

The following stationary -factor model allows for serial correlations in and both serial and cross-sectional correlations in :

| (12) | |||

| (13) | |||

| (14) |

and . The stationary factor model in (12) has been frequently adopted for empirical studies in the factor model literature including Bai and Ng (2002). Throughout we set . T he parameters with , and with , determine the autocorrelations in the factors and idiosyncratic components, while and (randomly drawn from with ), determine the cross-sectional correlations in . The parameter , or its inverse , is chosen from depending on the change-point scenario, in order to investigate the impact of the ratio between the variance of the common and idiosyncratic components, on the performance of the change-point detection methodology. We fix the number of observations at and vary the dimensionality as .

A single change-point is introduced to either or at as follows.

- (S1) Change in the loadings.

-

For a randomly chosen index set , the loadings are shifted by , where .

- (S2) Change in .

-

The signs of the AR parameters in (13) are switched such that the autocorrelations of change while their variance remains the same.

- (S3) A new factor.

-

For a randomly chosen , a new factor is introduced to : with and , where .

- (S4) Change in .

-

For a randomly chosen , the corresponding in (14) have their signs switched so that the autocorrelations of such change while their variance remains the same.

- (S5) Change in the covariance of .

-

For a randomly chosen , the bandwidth in (14) doubles.

In (S1) and (S3)–(S5), the size of the index set is controlled by the parameter , as .

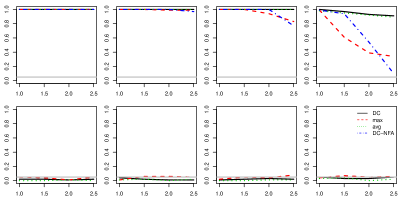

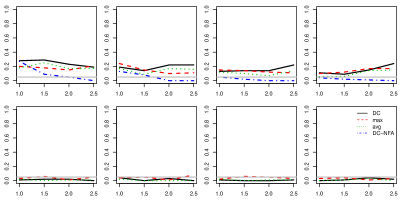

For each simulated dataset, we consider the range of possible factor numbers selected as described in Section 4.3. For any given , we estimate the common and idiosyncratic components and proceed with WT of Stage 1, to which only the first iteration of the DCBS algorithm is applied. In this way, we test for the existence of at most a single change-point in the common and idiosyncratic components separately and, if its presence is detected, we identify its location in time. With a slight abuse of notation, we refer to the simultaneous testing and locating procedure as the DC test, and report its detection power and accuracy in change-point estimation.

As noted in Introduction, existing methods for change-point analysis under factor modelling are not applicable to the scenarios other than (S1) and (S3). Hence, we compare the performance of the DC test to change-point tests based on two other high-dimensional CUSUM aggregation approaches, which are referred to as the MAX and AVG tests: after Stage 1, the -dimensional CUSUMs of the WT series are aggregated via taking their point-wise maximum or average, respectively, which replaces the Double CUSUM statistics in Stage 2. In addition, we report the detection power of a variant of the DC test, where the first iteration of the DCBS algorithm is applied to the panel data consisting of the WT of , and compare its performance against DC, MAX and AVG tests applied to the WT of under (S1)–(S3), and that of under (S4)–(S5). We include this approach, termed the DC-NFA (no factor analysis) test, in order to demonstrate the advantage in linking the factor modelling and change-point detection as proposed in our methodology.

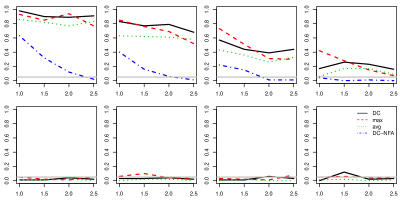

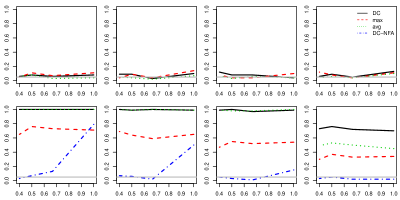

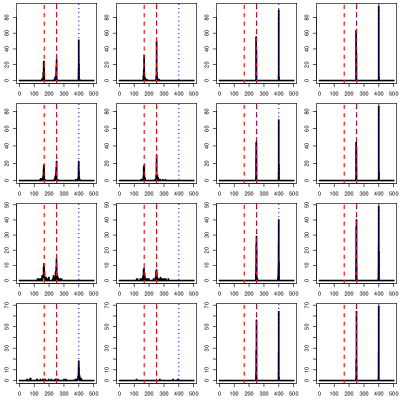

Figures 2–7 plot the detection power of our change-point test as well as that of MAX, AVG and DC-NFA tests under different scenarios over realisations when (we only present the results from (S1) when ). Since () do not contain any change under (S4)–(S5) ((S1)–(S3)), testing for a change-point in () in these scenarios offers insights into the size behaviour of DC, MAX and AVG tests.

Overall, change-point detection becomes more challenging as (the size of changes) or (the proportion of the coordinates with the change) decreases, and also as decreases (with increasing ) under (S1)–(S3) and increases (with increasing ) under (S4)–(S5). In all scenarios, the DC test shows superior performance to the DC-NFA test. This confirms that the factor analysis prior to change-point analysis is an essential step in markedly improving the detection power, as well as in identifying the origins of the change-points; without a factor analysis, a change-point that appears in either of or may be ‘masked’ by the presence of the other component and thus escape detection.

The DC and AVG tests generally attain similar powers, while the MAX test tends to have considerably lower power in scenarios such as (S2), (S4) and (S5). An exception is under (S3), where the MAX test attains larger power than the others in some settings with decreasing (Figure 5). It may be explained by the fact that the smaller is, the sparser the change-point becomes cross-sectionally, which is a setting that favours the approach taken in MAX in aggregating the high-dimensional CUSUM series (see the discussions in Section 2.1 of Cho and Fryzlewicz (2015)). Between the DC and AVG tests, the former outperforms the latter in the more challenging settings when the change is sparse cross-sectionally (with small ), particularly when the change is attributed to the introduction of a single factor to the existing five as in (S3).

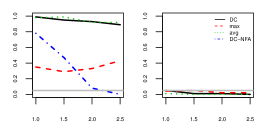

Apart from (S5), the origin of the change-point is correctly identified in the sense that it is detected only from under (S1)–(S3) or under (S4) with power strictly above . In (S5), we observe spillage of the change-point in : the change-point is detected from both and , particularly when a large proportion of undergoes the change of an increase in the bandwidth in (14), and when is small (with large ), see Figure 7. This supports the notion of a pervasive change-point being a factor, i.e., a significant break that affects the majority of the idiosyncratic components in their second-order structure, may be viewed as a common feature. We also note that due to the relatively large variance of common component, the detection power of the DC-NFA test behaves as that of the DC test applied to rather than in this scenario.

We present in a supplementary document the results on other data generating processes taken from the literature on testing for a single change-point under factor models, as well as tables and figures summarising the simulation results for (S1)–(S5) with , along with box plots of the estimated change-points . The performance of all tests under consideration generally improve when .

7.2 Multiple change-point scenarios

7.2.1 Model (M1)

This model is intended to mimic the behaviour of the Standard and Poor’s 100 log-return data, analysed in Section 8.1. The information criterion of Bai and Ng (2002) returned factors for these data and, imposing stability on the loadings, common factors four and idiosyncratic components were estimated by means of PCA as and . Estimated factors exhibit little serial correlations, show the evidence of multiple change-points in their variance and heavy tails. The same evidence holds for the estimated idiosyncratic components. Based on these observations, we adopt the following data generating model:

| (17) | |||

| (20) |

where denotes the sample variance operator, and for even and otherwise. We use the loadings estimated from the S&P100 data without capping, denoted by , and () is chosen from the same dataset by contrasting pairs of intervals with visibly different (). The change-points in the common components are introduced to at and , and those in the idiosyncratic components to at and . The magnitude of each change is controlled by , while determines the ratio between the variance of the common and idiosyncratic components (the larger , the smaller is). We fix and vary .

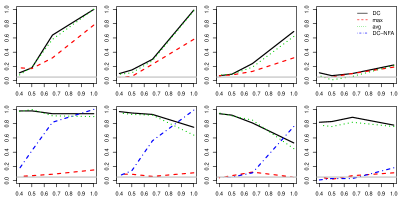

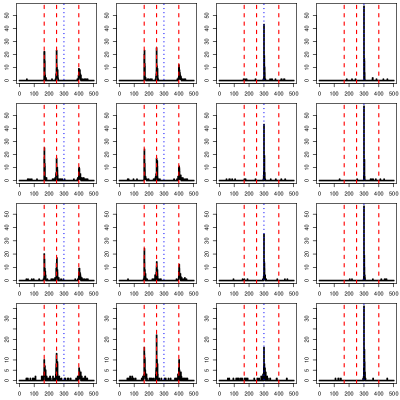

We report the performance of our methodology over realisations when in Figures 8–9 for the two extreme cases with . We also apply the DCBS algorithm to the WT of true common and idiosyncratic components generated under (M1) and report the corresponding results, which serve as a benchmark against which the efficacy of the PCA-based factor analysis of the proposed methodology is assessed. Additional simulation results with varying and are reported in the supplementary document.

The DCBS algorithm detects the two change-points in the idiosyncratic components equally well from and , regardless of the values of and . On the other hand, detection of is highly variable with respect to these parameters. When the size of the change is large (), the panel data generated from transforming serves as as good an input to the DCBS algorithm as that generated from transforming in terms of translating the presence and locations of both change-points.

With decreasing , the change-point , which appears only in the idiosyncratic components, is detected with increasing frequency as a change-point in the common components from , when (a) (the change in is large and thus all three change-points are detected from ), or (b) (the changes in are ignored and a single change-point is detected at from ). This phenomenon is in line with the observation made for the model (S5) in Section 7.1, on the spillage of change-points in the idiosyncratic components over to the common components: a significant co-movement in the dependence structure of may be regarded as being pervasive and common, and hence is captured as a change in the dependence structure of the common components by our proposed methodology.

Lastly, we note that although we impose normality on the idiosyncratic components for the theoretical development, these results show that our methodology works well even when the data exhibits some deviations of normality, such as heavy-tails.

7.2.2 Model (M2)

In this model, change-points are introduced as in (S1)–(S4) of Section 7.1. More specifically,

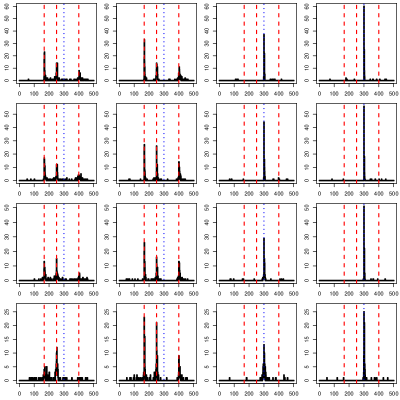

with and . The parameters , , , and are chosen identically as in Section 7.1. In summary, three change-points in the common components are introduced to the loadings (), autocorrelations of the factors () and the number of factors (), while a single change-point in the idiosyncratic components is introduced to their serial correlations (). The cardinality of the index sets , and determines the sparsity of the change-points , and , respectively. We randomly draw each index set from with its cardinality set at , where . Also, in the case of , the size of the shifts in the loadings is controlled by the parameter , as . Finally, we set , a parameter that features in , in order to investigate the impact of on the performance of the change-point detection methodology. We fix the number of observations at and the dimensionality at .

We report the performance of our methodology over realisations in Figures 10–11 for the two extreme cases when with . Also, we include the results from applying the DCBS algorithm to the WT of true common and idiosyncratic components generated under (M2) as a benchmark case. Additional simulation results with varying and are reported in the supplementary document.

In accordance with the observations made under single change-point scenarios (Section 7.1), detecting change-points in the common components, and in particular, becomes more challenging as they grow sparse cross-sectionally (with decreasing ) and as decreases (with increasing ). For the settings considered here, the DCBS algorithm applied to WT of performs as well as that applied to the WT of the true , regardless of the model parameters and . Not surprisingly, as the break in the loadings grows weaker with decreasing , the detection rate of deteriorates, especially when . Comparing the performance of the DCBS algorithm applied to and , the gap is not so striking in the detection of the change-point in the autocorrelations of the factors. As for and , provided that the breaks in the loadings and the number of factors are moderately dense (), and the magnitude of the former reasonably large (), we can expect the common components estimated via PCA to recover the both change-points as those in their second-order structure, for a range of .

8 Real data analysis

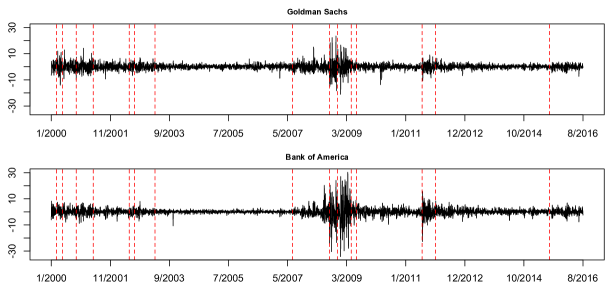

8.1 S&P100 stock returns

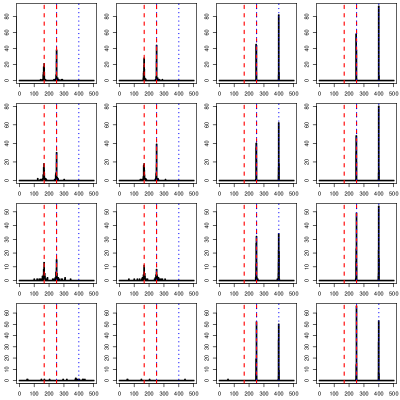

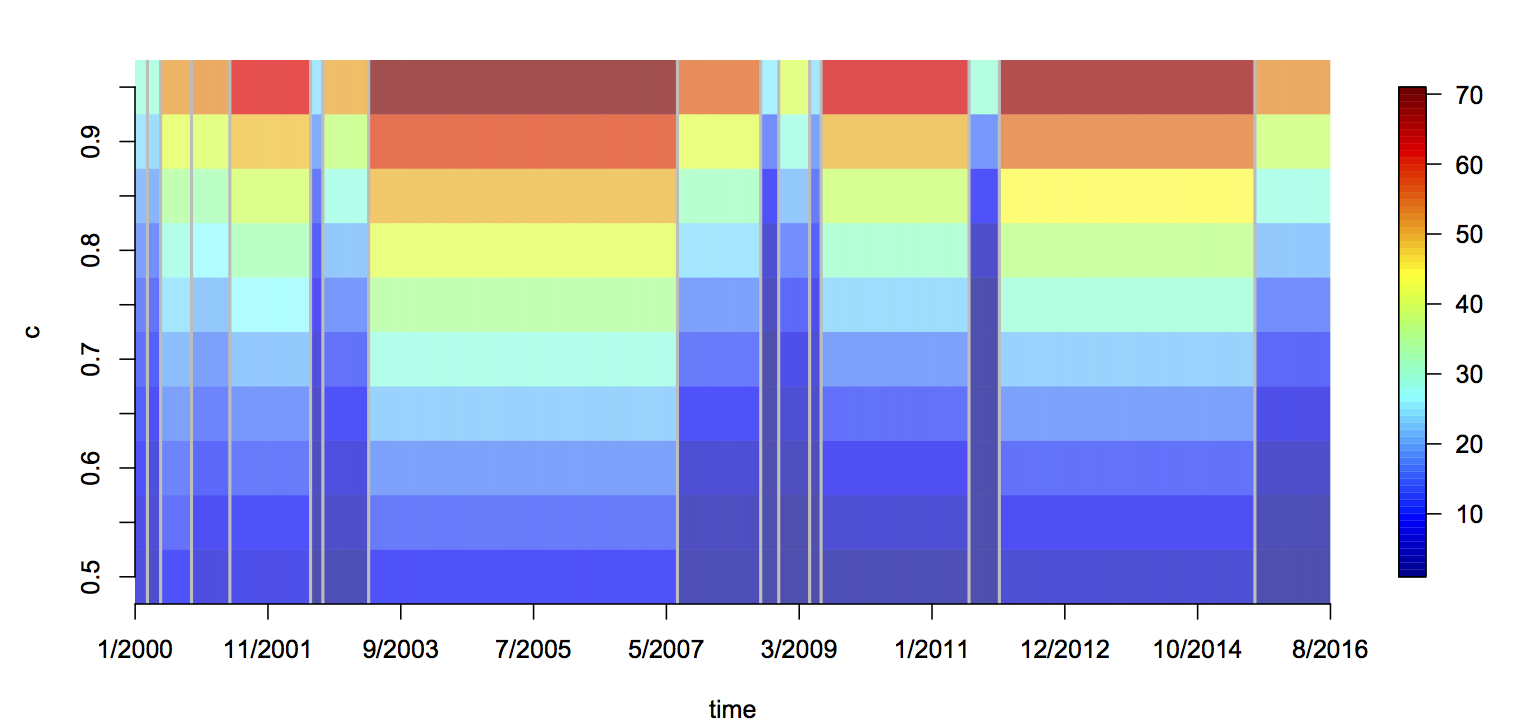

In this section, we perform change-point analysis on log returns of the daily closing values of the stocks composing the Standard and Poor’s 100 (S&P100) index, observed between January and August ( and ). The dataset is available from Yahoo Finance. With returned by the criterion in (11), the set of factor number candidates is chosen as . Also, a constraint is imposed so that no two change-points are detected within the period of working days. The maximum number of change-points for the common components is attained with (), and we obtain for all . Table 1 reports the change-points estimated from and , as well as their order of detection (represented by the level index of the nodes corresponding to the estimated change-points in the DCBS algorithm), and Figure 12 plots two representative daily log return series from the dataset along with .

Most of the change-points we find are in a neighbourhood of the events that characterise the financial market (some of which are not exactly dated). In particular:

-

1.

the burst of the dot-com bubble which took place between March 2000 to October 2002;

-

2.

the start of the second Iraq war in late March 2003;

-

3.

Lehman Brothers bankruptcy in September 2008;

-

4.

the first and second stages of the Greek and EU sovereign debt crisis in the summers of 2011 and 2015, respectively.

| 43 | 89 | 197 | 331 | 613 | 656 | 816 | 1895 | |

| 06/03/2000 | 10/05/2000 | 12/10/2000 | 26/04/2001 | 14/06/2002 | 15/08/2002 | 04/04/2003 | 19/07/2007 | |

| order | 3 | 2 | 5 | 4 | 3 | 4 | 1 | 2 |

| 2186 | 2249 | 2357 | 2397 | 2914 | 3020 | 3913 | ||

| 12/09/2008 | 11/12/2008 | 19/05/2009 | 16/07/2009 | 03/08/2011 | 04/01/2012 | 24/07/2015 | ||

| order | 4 | 5 | 6 | 3 | 5 | 4 | 5 | |

| 85 | 181 | 206 | 268 | 336 | 631 | 652 | 735 | |

| 04/05/2000 | 20/09/2000 | 25/10/2000 | 25/01/2001 | 03/05/2001 | 11/07/2002 | 09/08/2002 | 06/12/2002 | |

| order | 3 | 4 | 5 | 2 | 4 | 3 | 4 | 1 |

| 914 | 1957 | 2184 | 2210 | 2253 | 2354 | 2537 | 3911 | |

| 25/08/2003 | 16/10/2007 | 10/09/2008 | 16/10/2008 | 17/12/2008 | 14/05/2009 | 04/02/2010 | 22/07/2015 | |

| order | 4 | 5 | 3 | 5 | 6 | 4 | 2 | 3 |

By way of investigating the validity of , we computed the following quantities over each segment defined by two neighbouring change-points, :

where denotes the th largest eigenvalue of , and . In short, is the minimum number of eigenvalues required so that the proportion of the variance of accounted for by exceeds a given . Varying , we plot over the segments in Figure 13. We observe that over long stretches of stationarity, greater numbers of eigenvalues are required to account for the same proportion of variance, compared to shorter intervals which all tend to be characterised by high volatility. This finding is in accordance with the observation made in Li et al. (2017), that a small number of factors drive the majority of the cross-sectional correlations during the periods of high volatility.

8.2 US macroeconomic data

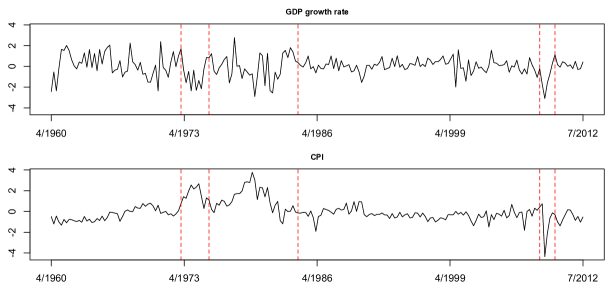

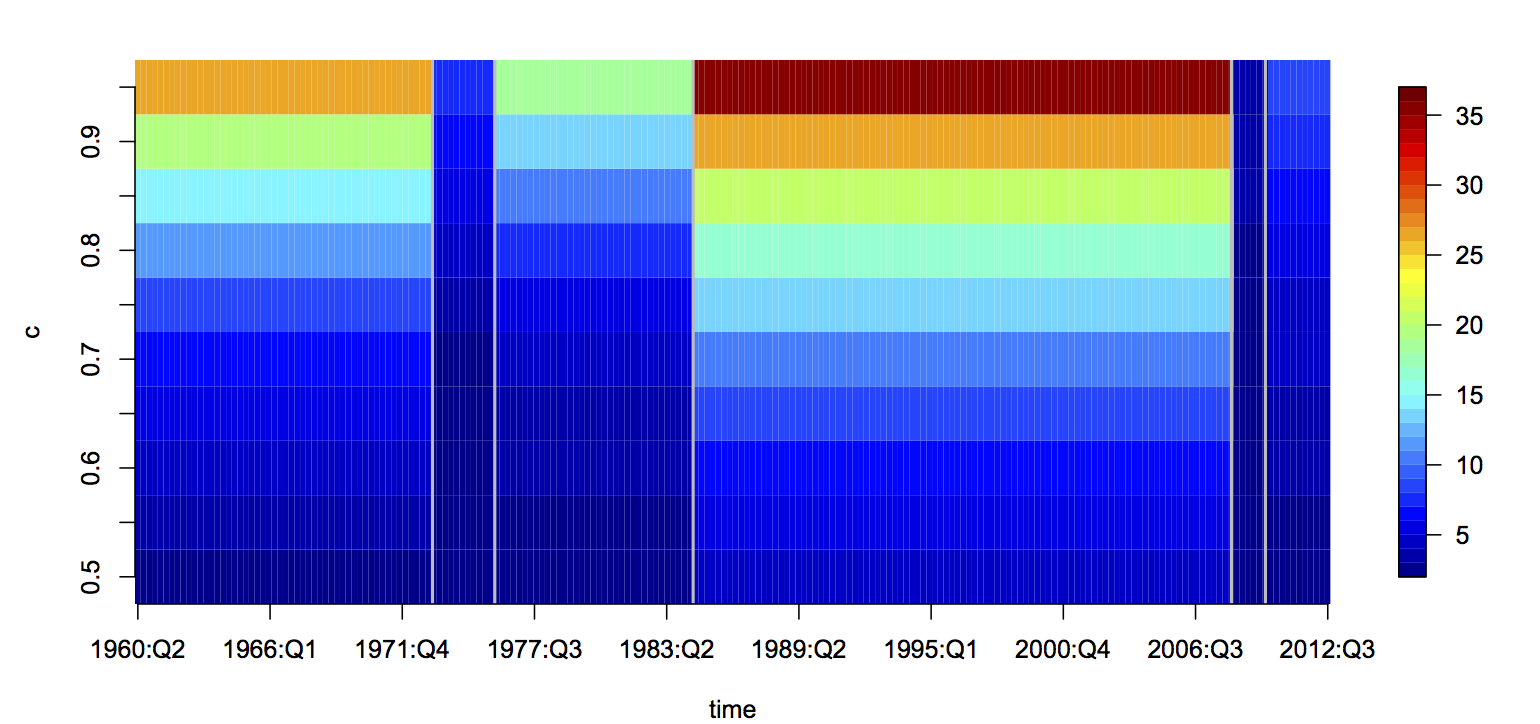

We analyse the US representative macroeconomic dataset of time series, collected quarterly between :Q2 and :Q3 (), for change-points. Similar datasets have been analysed frequently in the factor model literature, for example, in Stock and Watson (2002). The dataset is available from the St. Louis Federal Reserve Bank website (https://fred.stlouisfed.org/). We impose a restriction in applying the DCBS algorithm so that no two change-points are detected within three quarters in analysing the quarterly observations. Applying the information criterion of Bai and Ng (2002), is returned so we choose . All lead to the identical change-point estimates for the common component with so that we select . We also obtain for all . Table 2 reports the change-points estimated from and , and we plot two representative series from the dataset, gross domestic product (GDP) growth rate and consumer price inflation (CPI), along with in Figure 14.

According to the change-points detected, the observations are divided into periods corresponding to different economic regimes characterised by high or low volatility. In particular, we highlight the following regimes (recessions are dated by the National Bureau of Economic Research, http://www.nber.org/cycles.html):

-

1.

early 1970s to early 1980s marked by two major economic recessions, which were characterised by high inflation due to the oil crisis and the level of interest rates;

-

2.

the so-called Great Moderation period which, according to our analysis, started in late 1983 and was characterised by low volatility of most economic indicators as a result of the implementation of new monetary policies, see also Stock and Watson (2003);

-

3.

the period of the financial crisis that took place between 2007 and 2009 and corresponds to the most recent (as of 2018) economic recession, with record low levels of GDP growth and inflation and associated high volatility;

-

4.

the post-2009 years corresponding to the slow recovery of the US economy.

| 48 | 60 | 95 | 190 | 196 | ||

|---|---|---|---|---|---|---|

| 1972:Q1 | 1975:Q1 | 1983:Q4 | 2007:Q3 | 2009:Q1 | ||

| order | 2 | 3 | 1 | 2 | 3 | |

| 49 | 58 | 92 | 189 | 194 | 200 | |

| 1972:Q2 | 1974:Q3 | 1983:Q1 | 2007:Q2 | 2008:Q3 | 2010:Q4 | |

| order | 2 | 3 | 1 | 2 | 3 | 4 |

Cheng et al. (2016) performed change-point analysis on a similar set of macroeconomic and financial indicators, observed monthly rather than quarterly, over a shorter span of period between January and January . Their focus was on verifying the existence of a structural break corresponding to the beginning of the financial crisis, which they estimated to be in December , a date which is close to our (considering that we analyse quarterly observations). As in Section 8.1, we perform a post-change-point analysis by plotting computed on each segment defined by , see Figure 15, where we make similar observations about t he contrast between the number of factors required over long stretches of stationarity and short intervals of volatility.

9 Conclusions

We have provided the first comprehensive treatment of high-dimensional time series factor models with multiple change-points in their second-order structure. We have proposed an estimation approach based on the capped PCA and wavelet transformations, first separating common and idiosyncratic components and then performing multiple change-point analysis on the levels of the transformed data. The number and locations of change-points are estimated consistently as for both the common and idiosyncratic components. Our methodology is robust to the over-specification of the number of factors which, in the presence of multiple change-points, may not be accurately estimated by standard methods. Post change-point detection, we have proved the consistency of the common components estimated via PCA on each stationary segment.

An extensive numerical study has shown the good practical performance of our method and demonstrated that factor analysis prior to change-point detection improves the detectability of change-points. Two applications involving economic data have shown that we are able to pick up most of the structural changes in the economy, such as the recent financial crisis (2008–2009), economic recessions (mid 1970s and late 2000s) or changes in the monetary policy regime (the start of the so-called Great Moderation in early 1908s). Our method is implemented in the R package factorcpt, available from CRAN.

Acknowledgements

Haeran Cho’s work was supported by the Engineering and Physical Sciences Research Council grant no. EP/N024435/1. Piotr Fryzlewicz’s work was supported by the Engineering and Physical Sciences Research Council grant no. EP/L014246/1. We thank the Editor, Associate Editor and two referees for very helpful comments which led to a substantial improvement of this paper.

References

- Ahn and Horenstein (2013) Ahn, S. C. and Horenstein, A. R. (2013), “Eigenvalue ratio test for the number of factors,” Econometrica, 81, 1203–1227.

- Aït-Sahalia and Xiu (2017) Aït-Sahalia, Y. and Xiu, D. (2017), “Using principal component analysis to estimate a high dimensional factor model with high-frequency data,” Journal of Econometrics (In press).

- Alessi et al. (2010) Alessi, L., Barigozzi, M., and Capasso, M. (2010), “Improved penalization for determining the number of factors in approximate static factor models,” Statistics and Probability Letters, 80, 1806–1813.

- Bai (2003) Bai, J. (2003), “Inferential theory for factor models of large dimensions,” Econometrica, 71, 135–171.

- Bai et al. (2017) Bai, J., Han, X., and Shi, Y. (2017), “Estimation and inference of structural changes in high dimensional factor models,” Tech. rep., https://ssrn.com/abstract=2875193.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002), “Determining the number of factors in approximate factor models,” Econometrica, 70, 191–221.

- Baltagi et al. (2017) Baltagi, B. H., Kao, C., and Wang, F. (2017), “Identification and estimation of a large factor model with structural instability,” Journal of Econometrics, 197, 87–100.

- Barigozzi and Hallin (2017) Barigozzi, M. and Hallin, M. (2017), “A network analysis of the volatility of high dimensional financial series,” Journal of the Royal Statistical Society: Series C, 581–605.

- Barnett and Onnela (2016) Barnett, I. and Onnela, J.-P. (2016), “Change point detection in correlation networks,” Scientific Reports, 6.

- Bates et al. (2013) Bates, B. J., Plagborg-Møller, M., Stock, J. H., and Watson, M. W. (2013), “Consistent factor estimation in dynamic factor models with structural instability,” Journal of Econometrics, 177, 289–304.

- Bosq (1998) Bosq, D. (1998), Nonparametric Statistics for Stochastic Process: Estimation and Prediction, Springer.

- Brault et al. (2016) Brault, V., Ouadah, S., Sansonnet, L., and Lévy-Leduc, C. (2016), “Nonparametric homogeneity tests and multiple change-point estimation for analyzing large Hi-C data matrices,” arXiv preprint arXiv:1605.03751.

- Breitung and Eickmeier (2011) Breitung, J. and Eickmeier, S. (2011), “Testing for structural breaks in dynamic factor models,” Journal of Econometrics, 163, 71–84.

- Brodsky and Darkhovsky (1993) Brodsky, B. E. and Darkhovsky, B. S. (1993), Nonparametric Methods in Change-point Problems, Springer.

- Chamberlain and Rothschild (1983) Chamberlain, G. and Rothschild, M. (1983), “Arbitrage, factor structure, and mean–variance analysis on large asset markets,” Econometrica, 51, 1281–1304.

- Chen et al. (2014) Chen, L., Dolado, J. J., and Gonzalo, J. (2014), “Detecting big structural breaks in large factor models,” Journal of Econometrics, 180, 30–48.

- Cheng et al. (2016) Cheng, X., Liao, Z., and Schorfheide, F. (2016), “Shrinkage estimation of high-dimensional factor models with structural instabilities,” The Review of Economic Studies, 83, 1511–1543.

- Cho (2016) Cho, H. (2016), “Change-point detection in panel data via double CUSUM statistic,” Electronic Journal of Statistics, 10, 2000–2038.

- Cho et al. (2016) Cho, H., Barigozzi, M., and Fryzlewicz, P. (2016), factorcpt: Simultaneous change-point and factor analysis, R package version 0.1.2.

- Cho and Fryzlewicz (2011) Cho, H. and Fryzlewicz, P. (2011), “Multiscale interpretation of taut string estimation and its connection to Unbalanced Haar wavelets,” Statistics and Computing, 21, 671–681.

- Cho and Fryzlewicz (2012) — (2012), “Multiscale and multilevel technique for consistent segmentation of nonstationary time series,” Statistica Sinica, 22, 207–229.

- Cho and Fryzlewicz (2015) — (2015), “Multiple change-point detection for high-dimensional time series via Sparsified Binary Segmentation,” Journal of the Royal Statistical Society: Series B, 77, 475–507.

- Corradi and Swanson (2014) Corradi, V. and Swanson, N. R. (2014), “Testing for structural stability of factor augmented forecasting models,” Journal of Econometrics, 182, 100–118.

- Davis and Kahan (1970) Davis, C. and Kahan, W. M. (1970), “The rotation of eigenvectors by a perturbation. III,” SIAM Journal on Numerical Analysis, 7, 1–46.

- Enikeeva and Harchaoui (2015) Enikeeva, F. and Harchaoui, Z. (2015), “High-dimensional change-point detection with sparse alternatives,” arXiv preprint, arXiv:1312.1900.

- Fan et al. (2011a) Fan, J., Liao, Y., and Mincheva, M. (2011a), “High dimensional covariance matrix estimation in approximate factor models,” The Annals of Statistics, 39, 3320–3356.

- Fan et al. (2013) — (2013), “Large covariance estimation by thresholding principal orthogonal complements,” Journal of the Royal Statistical Society: Series B, 75, 603–680.

- Fan et al. (2011b) Fan, J., Lv, J., and Qi, L. (2011b), “Sparse high dimensional models in economics,” Annual Review of Economics, 3, 291–317.

- Forni et al. (2009) Forni, M., Giannone, D., Lippi, M., and Reichlin, L. (2009), “Opening the black box: structural factor models versus structural VARs,” Econometric Theory, 25, 1319–1347.

- Forni et al. (2000) Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2000), “The Generalized Dynamic Factor Model: identification and estimation,” The Review of Economics and Statistics, 82, 540–554.

- Forni and Lippi (2001) Forni, M. and Lippi, M. (2001), “The Generalized Dynamic Factor Model: representation theory,” Econometric Theory, 17, 1113–1141.

- Fryzlewicz (2014) Fryzlewicz, P. (2014), “Wild Binary Segmentation for multiple change-point detection,” The Annals of Statistics, 42, 2243–2281.

- Fryzlewicz and Nason (2006) Fryzlewicz, P. and Nason, G. P. (2006), “Haar–Fisz estimation of evolutionary wavelet spectra,” Journal of the Royal Statistical Society: Series B, 68, 611–634.

- Fryzlewicz and Subba Rao (2014) Fryzlewicz, P. and Subba Rao, S. (2014), “Multiple-change-point detection for auto-regressive conditional heteroscedastic processes,” Journal of the Royal Statistical Society: Series B, 76, 903–924.

- Gonçalves and Perron (2014) Gonçalves, S. and Perron, B. (2014), “Bootstrapping factor-augmented regression models,” Journal of Econometrics, 182, 156–173.

- Gonçalves and Perron (2016) — (2016), “Bootstrapping factor models with cross sectional dependence,” Preprint.

- Groen et al. (2013) Groen, J. J., Kapetanios, G., and Price, S. (2013), “Multivariate methods for monitoring structural change,” Journal of Applied Econometrics, 28, 250–274.