New approximation for GARCH parameters estimate Yakoub BOULAROUK1 , Nasr-eddine HAMRI1 1 Institute of Science and Technology, Melilab laboratory, University Center of Mila, Algeria

Abstract: This paper presents a new approach for the optimization of GARCH parameters estimation. Firstly, we propose a method for the localization of the maximum. Thereafter, using the methods of least squares, we make a local approximation for the projection of the likelihood function curve on two dimensional planes by a polynomial of order two which will be used to calculate an estimation of the maximum.

Keyword GARCH Process, Likelihood function, Least squares.

1 Introduction

The modeling of time series is applied today in fields as diverse (econometrics, medicine or demographics….). As it is a crucial step in the study of time series, it has undergone a great evolution during the last fifty years and several models of representation have been proposed.

In 1982, Engle [4] proposed the conditionally heteroskedastic autoregressive (ARCH) model, which allowed the conditional variance to change as a function of past errors over time, while leaving the variance unconditional constant. This model has already proved useful in the modeling of several phenomenas. In Engle [4, 5] and Engle and Kraft [6], models for the inflation rate are constructed recognizing that the uncertainty of inflation tends to change over time. In 1984, Weiss [14] considered the ARMA models with ARCH errors. He used these models for the modeling of sixteen US microeconomic time series.

In 1986, Bollerslev [1] proposed a generalization of these ARCH models to the Generalized AutoRegressive Conditional Heteroskedasticity (GARCH) models, whose the variance in the present depends on its past and the process past. As it studied the conditions of

stationarity and the structure of the autocorrelations for this class of models.

The GARCH family contains a number of parameters which must be estimated on actual data for empirical applications. The estimation of the parameters returns to calculate the maximum of the log-likelihood function which is non-linear, this leads to the use of non-linear optimization methods. Several optimization methods are used, including The Nelder-Mead method, BGFS method and others :

-

•

Nelder and Mead [11] introduced their method using only

the likelihood function values. Altough their method is relatively slow, it’s robust and leads to results for the non differentiable functions. In their turn Fletcher and Reeves [9] have introduced the method of the conjugate gradient which does not store matrix.

- •

-

•

In 1990 David M. Gay [7] have published a technical report in which he proposed a method intitiled optimization using PORT routines (noted OPR).

It is common knowledge among practitioners that the GARCH parameters are numerically difficult to estimate in empirical applications. The existant numerical algorithm can easily fail, or converge to erratic solutions. Therefore, the resulting fitted parameters must be examined with a healthy dose of scepticism. In this work, we propose a new algorithm in which we exploit the asymptotic convexity of the likelihood function. We will develop a method to locate the maximum value instead of using the confidence intervals resulting from asymptotic normality of the estimated parameters thereafter and as in [2], we approach the likelihood function by a quadratic form that we use to calculate an approximation of the maximum.

2 The GARCH model and its likelihood function

The GARCH process was introduced by Bollerslev [1] as solution for the system of equations:

| (2.1) |

Let’s note the vector of unknown parameters, with , for , for , strictly positive. The is a sequence of normal random independent and identically distributed satisfying the standard assumptions and . The ARCH is an GARCH

The conditional likelihood of expresses as, up to an additional constant,

| with |

The quasi-likelihood is obtained by plugging in the approximations , where is different of zero only for finitely many ,

| with |

Remark that unobserved values have to be fixed a priori equal to in the quasi-likelihood . In the next proposition, we give a necessary and sufficient condition for the process stationarity.

Proposition 2.1.

The GARCH( ) process as defined in (2.1) is wide-sense stationary with , and for if and only if

| (2.2) |

Proof 1.

This result is proved by Bollerslev in [1].

The condition (2.2) implies that and . Else, we define the stationarity set

| (2.3) |

3 Necessary tools

3.1 Convexity

W.C. Ip and al. [13] have proved the convexity of the negative likelihood function in the asymptotic sense for GARCH models. This property allows us the local approximation of this function in the Neighborhood of its minimum by a polynomial of degree two.

Proposition 3.1.

Suppose is an arbitrary compact, convex subset of and the second derivative of . Then there exist a constant and a set with satisfying that for each and , there is a positive integer such that

| (3.1) |

3.2 Localisation method

In this part, we propose a method to search for a block of the form containing the maximum sought-after. The method is based on the principle of dichotomy applied for projections of the likelihood function on a plane with dimension two, we follow the steps

-

1.

We search a point that verifie , where is the order derivative of the likelihood function with respect to .

-

2.

We put and

-

3.

-

•

if then we replace by

-

•

else if we replace by

-

•

We repeat the step until .

4 Calculation procedure

To calculate the maximum likelihood, one passes by the following steps

-

1.

Calculate confidence intervals for the unknown parameters using the localisation method.

-

2.

Make a subdivision of elements for all the confidence intervals .

-

3.

Calculate the function values where , Which is a cut for the curve of the likelihood function on the diagonal plane of the confidence region.

-

4.

Numerical approximation for the orthogonal projection of the log likelihood function cut by polynomials of order two taking the form : we use the least squares method.

-

5.

Calculate these maximum.

5 Example of application ARCH(1)

The process is presented as solution of the system

| (5.1) |

where and .

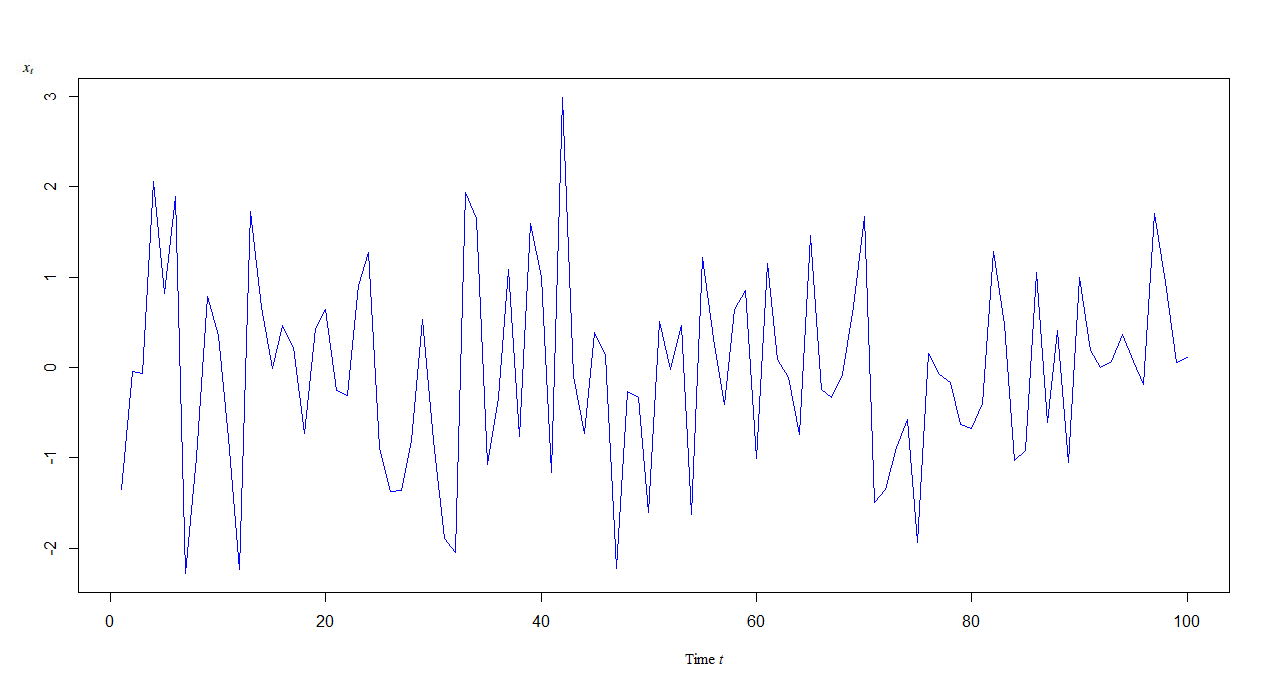

Let be the simulated first order conditionally heteroskedastic autoregressive time series with ( and ) presented by the table 3.

| Time | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| -1.348 | -0.05 | -0.063 | 2.055 | 0.815 | 1.893 | -2.277 | -1 | 0.782 | 0.351 | |

| Time | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 |

| -0.791 | -2.24 | 1.723 | 0.667 | -0.015 | 0.464 | 0.22 | -0.737 | 0.434 | 0.643 | |

| Time | 21 | 22 | 23 | 24 | 25 | 26 | 27 | 28 | 29 | 30 |

| -0.259 | -0.313 | 0.907 | 1.268 | -0.888 | -1.376 | -1.367 | -0.805 | 0.528 | -0.813 | |

| Time | 31 | 32 | 33 | 34 | 35 | 36 | 37 | 38 | 39 | 40 |

| -1.89 | -2.051 | 1.94 | 1.643 | -1.071 | -0.336 | 1.085 | -0.766 | 1.59 | 0.993 | |

| Time | 41 | 42 | 43 | 44 | 45 | 46 | 47 | 48 | 49 | 50 |

| -1.162 | 2.985 | -0.1 | -0.732 | 0.391 | 0.132 | -2.224 | -0.271 | -0.336 | -1.606 | |

| Time | 51 | 52 | 53 | 54 | 55 | 56 | 57 | 58 | 59 | 60 |

| 0.509 | -0.026 | 0.468 | -1.626 | 1.219 | 0.315 | -0.416 | 0.636 | 0.848 | -1.011 | |

| Time | 61 | 62 | 63 | 64 | 65 | 66 | 67 | 68 | 69 | 70 |

| 1.152 | 0.085 | -0.114 | -0.744 | 1.456 | -0.243 | -0.332 | -0.078 | 0.678 | 1.668 | |

| Time | 71 | 72 | 73 | 74 | 75 | 76 | 77 | 78 | 79 | 80 |

| -1.499 | -1.347 | -0.886 | -0.578 | -1.94 | 0.156 | -0.082 | -0.173 | -0.63 | -0.677 | |

| Time | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 |

| -0.397 | 1.283 | 0.479 | -1.035 | -0.917 | 1.054 | -0.605 | 0.412 | -1.055 | 0.994 | |

| Time | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 100 |

| -0.259 | -0.313 | 0.907 | 1.268 | -0.888 | -1.376 | -1.367 | -0.805 | 0.528 | -0.813 |

We plot this time series as function of time

The log likelihood of an process is given by

to obtain we replace by zero.

Now, we proceed to the calculation of the maximum likelihood using our method

-

1.

We remark that , therefore .

0.0001 0.2001 0.4001 0.6001 0.8001 -7613853 -455.4789 -93.72643 -19.2947 5.967303 Table 2: Table of the derivative values. -

2.

Using the localisation procedure, we find that the region contains the maximum.

-

3.

We calculate the function values on the diagonal plane of the confidence region, which give the table 3.

0.7751 0.7759 0.7766 0.7774 0.7781 0.7789 0.7796 0.7804 0.7812 0.7819 0.2813 0.2821 0.283 0.2838 0.2846 0.2854 0.2862 0.2871 0.2879 0.2887 109.257 109.251 109.245 109.239 109.233 109.227 109.222 109.217 109.212 109.207 0.7827 0.7834 0.7842 0.7849 0.7857 0.7865 0.7872 0.788 0.7887 0.7895 0.2895 0.2903 0.2912 0.292 0.2928 0.2936 0.2945 0.2953 0.2961 0.2969 109.202 109.198 109.194 109.19 109.186 109.182 109.179 109.176 109.173 109.17 0.7903 0.791 0.7918 0.7925 0.7933 0.794 0.7948 0.7956 0.7963 0.7971 0.2977 0.2986 0.2994 0.3002 0.301 0.3018 0.3027 0.3035 0.3043 0.3051 109.168 109.165 109.163 109.161 109.159 109.158 109.156 109.155 109.154 109.153 0.7978 0.7986 0.7993 0.8001 0.8009 0.8016 0.8024 0.8031 0.8039 0.8046 0.3059 0.3068 0.3076 0.3084 0.3092 0.3100 0.3109 0.3117 0.3125 0.3133 109.153 109.152 109.152 109.152 109.152 109.152 109.153 109.153 109.154 109.155 0.8054 0.8062 0.8069 0.8077 0.8084 0.8092 0.8099 0.8107 0.8115 0.8122 0.3141 0.315 0.3158 0.3166 0.3174 0.3183 0.3191 0.3199 0.3207 0.3215 109.156 109.157 109.159 109.161 109.162 109.164 109.167 109.169 109.171 109.174 0.813 0.8137 0.8145 0.8153 0.816 0.8168 0.8175 0.8183 0.819 0.8198 0.3224 0.3232 0.324 0.3248 0.3256 0.3265 0.3273 0.3281 0.3289 0.3297 109.177 109.18 109.183 109.186 109.19 109.193 109.197 109.201 109.205 109.21 0.8206 0.8213 0.8221 0.8228 0.8236 0.8243 0.8251 0.8259 0.8266 0.8274 0.3306 0.3314 0.3322 0.333 0.3338 0.3347 0.3355 0.3363 0.3371 0.3379 109.214 109.218 109.223 109.228 109.233 109.238 109.244 109.249 109.255 109.26 0.8281 0.8289 0.8296 0.8304 0.8312 0.8319 0.8327 0.8334 0.8342 0.8349 0.3388 0.3396 0.3404 0.3412 0.3421 0.3429 0.3437 0.3445 0.3453 0.3462 109.266 109.272 109.279 109.285 109.291 109.298 109.305 109.312 109.319 109.326 0.8357 0.8365 0.8372 0.838 0.8387 0.8395 0.8403 0.841 0.8418 0.8425 0.347 0.3478 0.3486 0.3494 0.3503 0.3511 0.3519 0.3527 0.3535 0.3544 109.333 109.341 109.349 109.356 109.364 109.372 109.38 109.389 109.397 109.406 0.8433 0.844 0.8448 0.8456 0.8463 0.8471 0.8478 0.8486 0.8493 0.8501 0.3552 0.356 0.3568 0.3576 0.3585 0.3593 0.3601 0.3609 0.3617 0.3626 109.414 109.423 109.432 109.441 109.45 109.46 109.469 109.479 109.488 109.498 Table 3: Table of . -

4.

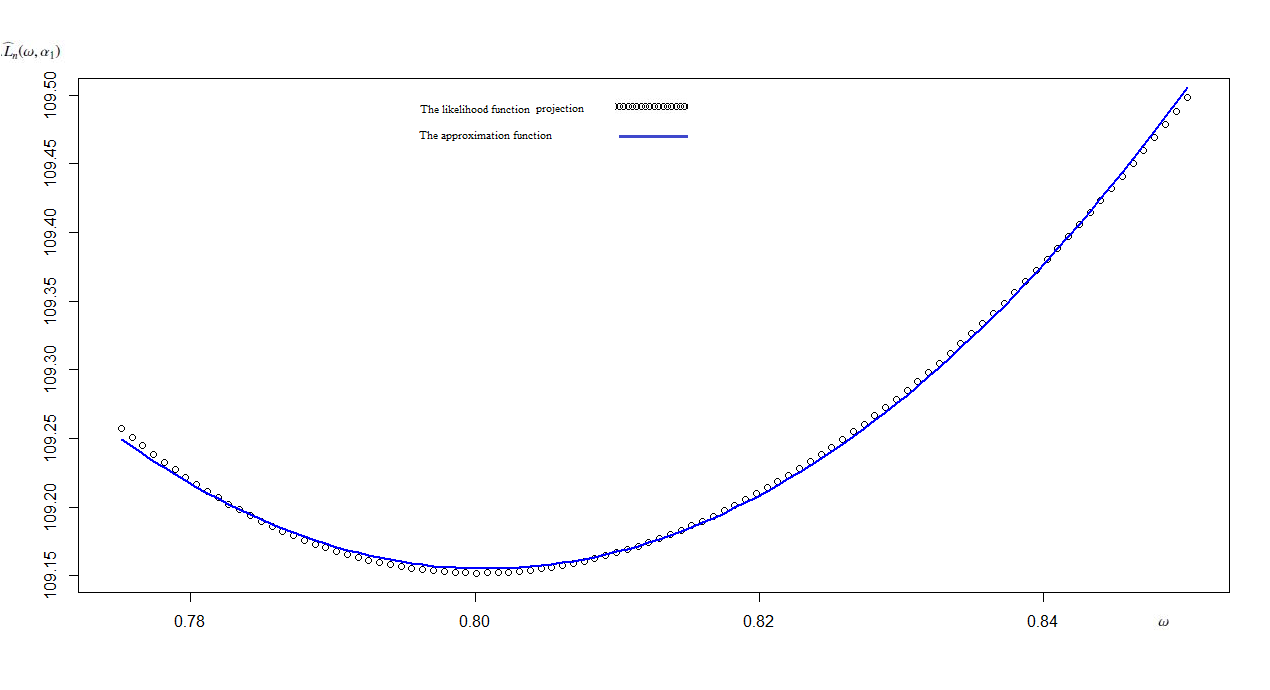

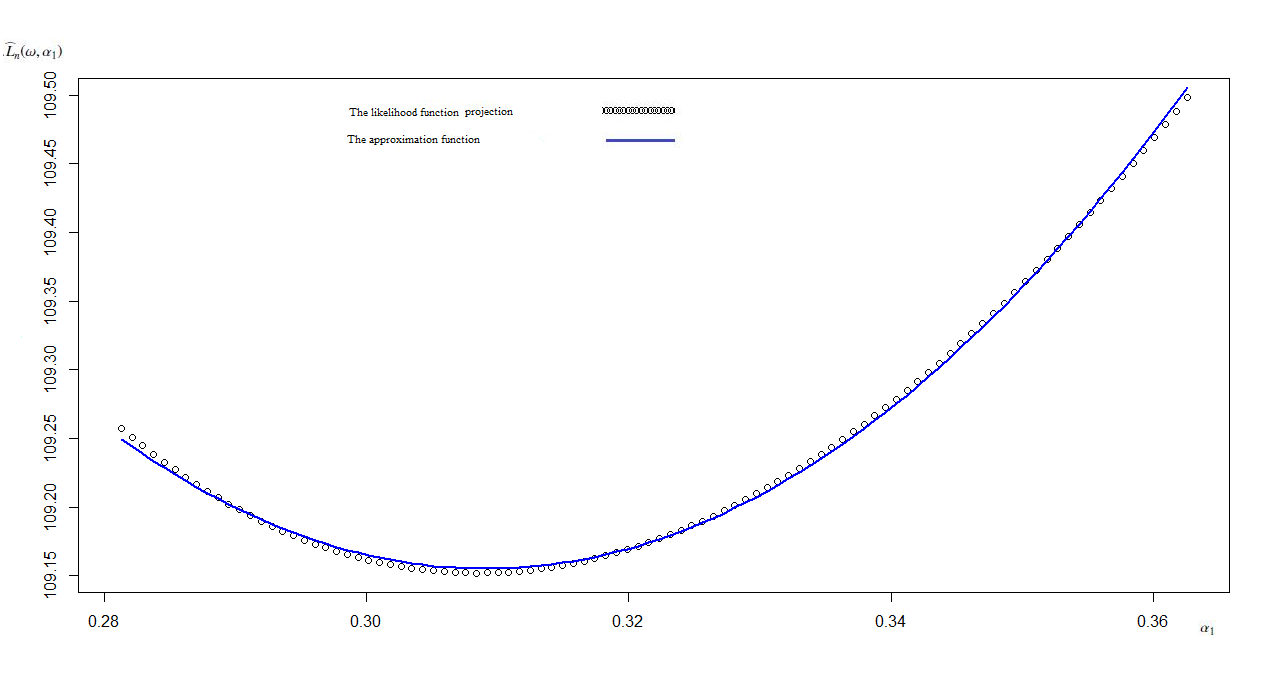

Using the least squares method, we calculate approximations of and the orthogonal projections of the likelihood function curve cut on the planes , respectively.

-

•

The approximation function for the likelihood function Curve cut projection on the plane is

;

the maximum of this function is .

In the Figure 2, we represent the projection of the cut of the likelihood function on the plane and its approximation

Figure 2: The projection of the cut of the likelihood function on the plane and its approximation -

•

The approximation function for the likelihood function curve cut projection on the plane is

;

the maximum value of this function is .

The Figure 3 illustrates the projection of the cut of the likelihood function on the plane and its approximation

Figure 3: The projection of the cut of the likelihood function on the plane and its approximation

-

•

6 Numerical comparaison study

To illustrate the performance of the proposed method, we compare it with some popular methods (BGFS, Simplex and OPR) usually used in the Time series parameters calculation. We applied these methods to independent replications of two ARCH process (one with , end the other with , for different sample size , and , thereafter we compute the root-mean-square error (RMSE) of the resulting estimation, the results are presented in Table 4.

| Sample size | Our Method | BGFS | Simplex | OPR | Our Method | BGFS | Simplex | OPR | |

|---|---|---|---|---|---|---|---|---|---|

| 100 | 0.485 | 0.607 | 0.609 | 0.609 | 0.798 | 0.804 | 0.807 | 0.807 | |

| 200 | 0.345 | 0.368 | 0.368 | 0.368 | 0.747 | 0.752 | 0.752 | 0.752 | |

| 300 | 0.292 | 0.300 | 0.300 | 0.300 | 0.742 | 0.743 | 0.743 | 0.743 | |

Conclusion of the numerical comparaison results: On the one hand, it is clear that the RMSE decreases as the sample size increases, which validates the theoretical results (consistency of the estimators). On the other hand, Table 4 show that our method provides more accurate estimation than the BGFS, Simplex and OPR methods.

References

- [1] Bollerslev, T. (1986), Generalised autoregressive conditional heteroscedasticity, Journal of Econometrics, 31, 307-327.

- [2] Y. Boularouk and K. Djeddour (2015), New approximation for ARMA parameters estimate, Mathematics and Computers in Simulation, 118,116-122.

- [3] Broyden, C. G. (1970), The convergence of a class of double-rank minimization algorithms, Journal of the Institute of Mathematics and Its Applications, 6, 76-90.

- [4] Engle, R.F. (1982), Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation, Econometrica 50, 987-1008.

- [5] Engle, R.F. (1983), Estimates of the variance of U.S. inflation based on the ARCH model, Journal of Money Credit and Banking 15, 286-301.

- [6] Engle, R.F. and D. Kraft (1983), Multiperiod forecast error variances of inflation estimated from ARCH models, in: A. ZeUner, ed., Applied time series analysis of economic data (Bureau of the Census, Washington, DC) 293-302.

- [7] David M. Gay (1990), Usage summary for selected optimization routines. Computing Science Technical Report 153, AT and T Bell Laboratories, Murray Hill.

- [8] Fletcher, R. (1970), A New Approach to Variable Metric Algorithms, Computer Journal, 13, 3, 317-322

- [9] Fletcher, R. Reeves, C. M. (1964), Function minimization by conjugate gradients, The Computer Journal, Vol. 7, 2, 149-154.

- [10] Goldfarb, D. (1970),A Family of Variable Metric Methods Derived by Variational Means Maths. Comput., 24, 23-26.

- [11] Nelder, J. A. Mead, R. (1965), A Simplex Method for Function Minimization. Comput. J. 7, 308-313.

- [12] Shanno, David, F. Kettler, Paul C. (1970), Optimal conditioning of quasi-Newton methods, Math. Comput. 24, 111, 657-664.

- [13] W.C. Ipa, Heung Wonga, J.Z. Panb, , , D.F. Lic (2006), The asymptotic convexity of the negative likelihood function of GARCH models. Computational Statistics and Data Analysis, Volume 50, Issue 2, 30 January 2006, 311-331.

- [14] Weiss, A.A. (1984), ARMA models with ARCH errors. J. Time Ser. Anal., 5, 2, 129-143.