∗ Department of Mathematics, Karlsruhe Institute of Technology, D-76128 Karlsruhe, Germany

Extremal Behavior of Long-Term Investors with Power Utility

Abstract.

We consider a Bayesian financial market with one bond and one stock where the aim is to maximize the expected power utility from terminal wealth. The solution of this problem is known, however there are some conjectures in the literature about the long-term behavior of the optimal strategy. In this paper we prove now that for positive coefficient in the power utility the long-term investor is very optimistic and behaves as if the best drift has been realized. In case the coefficient in the power utility is negative the long-term investor is very pessimistic and behaves as if the worst drift has been realized.

- Key words:

-

Bayes Approach, Investment Problem, Stochastic Ordering

1. Introduction

This paper investigates structural properties of the optimal portfolio choice in a financial market with one bond and one stock. The drift rate of the stock price process is modeled as a random variable whose outcome is unknown to the investor. However, the investor is able to observe the stock price process. Thus we face a Bayesian model. The aim is to maximize the expected power utility from terminal wealth.

Portfolio optimization problems with partial observation, in particular with unknown drift process have been studied extensively over the last decade. The solution for the Bayesian case for power utility can be found among others in Karatzas and Zhao (2001), Rieder and Bäuerle (2005), Longo and Mainini (2016). This is a special case of a Hidden Markov model which has been treated in Honda (2003), Sass and Haussmann (2004), Rieder and Bäuerle (2005) and with full information in Bäuerle and Rieder (2004). More general and recent approaches towards these kind of models can be found in Björk et al. (2010), Shen and Tak Kuen (2012), Fouque et al. (2015), Guéanty and Pu (2016) where processes and utility functions differ. In this paper we simply take the solution for the optimal portfolio from the literature and discuss its behavior when the time horizon tends to infinity. There have been some conjectures about this behavior in the literature. In Cvitanić et al. (2006) in the case of a negative coefficient for the power function it is reported that the long-term investor behaves more conservative. In Longo and Mainini (2016), Rieder and Bäuerle (2005) it has been deduced from numerical data that in case , the long-term investor behaves like an investor with known drift and the drift is the largest possible one. Meaning that the investor is quite optimistic. This observation stresses the fact that the behavior of an investor with power utility is rather different to one with logarithmic utility (see also recent findings in Guéanty and Pu (2016), Section 2.3.4), though it is known that the logarithmic utility can be obtained as limiting case from the power utility. In our paper we show that for , indeed the optimal fraction invested in the stock converges for time horizon to infinity to the largest possible Merton ratio and thus investors are very optimistic. For , the point of view changes dramatically. The optimal fraction invested in the stock converges for time horizon to infinity to the smallest possible Merton ratio. In this case investors are very pessimistic. In particular the effect of learning does not play a role for a long-term investor in contrast to a short-term investor. For the influence of learning, see e.g. Xia (2001).

Our paper is organized as follows: In Section 2 we describe our model and recall the optimal portfolio strategy. In Section 3 we state and prove the behavior of a long-term investor which is quite surprising.

2. The Investment Problem and the Optimal Solution

Suppose that is a filtered probability space and is a fixed time horizon. We consider a financial market with one bond and one risky asset. The bond evolves according to

| (2.1) |

with being the interest rate. The stock price process is given by

| (2.2) |

where is an -Brownian motion, and is a random variable with known initial distribution where are the possible values of . We assume that and are independent. The outcome of is not known to the investor, but the investor is able to observe the stock price. Thus we face a Bayesian model. Note that this is a special case of a Hidden Markov Model where the value of the hidden process does not change.

The optimization problem is to find self-financing investment strategies in this market that maximize the expected utility from terminal wealth. As utility function we choose the power utility with . The parameter represents the risk aversion of the investor. Smaller correspond to higher risk aversion.

Let be the filtration generated by the stock price process . In what follows we denote by the fraction of wealth invested in the stock at time . is then the fraction of wealth invested in the bond at time . If , then this means that the stock is sold short and corresponds to a credit. The process is called portfolio strategy. An admissible portfolio strategy has to be an -adapted process. The wealth process under an admissible portfolio strategy is given by the solution of the stochastic differential equation

| (2.3) |

where we assume that is the given initial wealth. The optimization problem is defined by

| (2.4) |

A portfolio strategy is optimal if it attains the supremum. The solution of this problem can e.g. be found in Karatzas and Zhao (2001), Sass and Haussmann (2004), Rieder and Bäuerle (2005), Longo and Mainini (2016). We will only briefly sketch its derivation. Since is not known we have to estimate it by which is the conditional expectation of , given our observation up to time . Define now . It can be shown that is an -Brownian motion (see Lemma 1 in Rieder & Bäuerle 2005). Thus, the process

| (2.5) |

is -adapted and hence observable for the investor. Finally we can represent our wealth process by

| (2.6) |

Note that and the conditional probabilities satisfy and

| (2.7) |

which is a special case of the Wonham filter equation, see e.g. Elliott et al. (1994). The optimization problem is thus reduced to a situation with complete observation and can be solved with standard techniques like e.g. the Hamilton-Jacobi-Bellman equation.

In order to present the optimal portfolio strategy, let us introduce the following abbreviations: Define and

| (2.8) |

for and Further set

| (2.9) |

It is well-known that is a martingale density process with respect to the filtration which is the filtration generated by and . Then we can define a new probability measure by . Under the process is an -Brownian motion. The process is a -martingale with respect to . Note that it can be shown that and are independent under . Then the Bayes formula implies that

| (2.10) |

which yields that

| (2.11) |

The proof of the following theorem can be found in Karatzas and Zhao (2001) (Theorem 3.2 and Example 3.5) and Rieder and Bäuerle (2005) (Theorem 8).

Theorem 2.1.

Note that a similar statement is true when the initial distribution of is more general, see e.g. Karatzas and Zhao (2001), Longo and Mainini (2016). Further it is crucial to remark that in case is known and equal to , then the optimal fraction to invest in the stock is equal to

| (2.13) |

independent of time and wealth. This is the so-called Merton-ratio. The representation of the optimal portfolio strategy in Theorem 2.1 is derived by using a change of measure technique (for more details see the proof of Theorem 8 in Rieder & Bäuerle 2005). An equivalent formulation would be

| (2.14) |

where the first term corresponds to the Merton-ratio where we replace the unknown by its estimate and is the so-called hedging demand. The hedging demand vanishes for and for (the case formally corresponds to the logarithmic utility). For a proof of the latter statements see Theorem 9 in Rieder & Bäuerle (2005).

3. Convergence of the Optimal Investment Strategy as Time Horizon tends to Infinity

3.1. The case

In this section we are going to prove the following result:

Theorem 3.1.

Let , , and . Then

| (3.1) |

This result is quiet interesting because it says that with a very large time horizon, the optimal investment strategy in the Bayesian case with is approximately the same as in a setting with known, maximal possible drift. This result is independent of the prior distribution and the current belief, so the actual probability that the maximal drift has realized could be rather small. This means that the Bayes investor with is pretty optimistic in the long run. Such a behavior has been conjectured in Rieder and Bäuerle (2005) and Longo and Mainini (2016) from the observation of numerical data. It is also remarkable that in the case of a logarithmic utility function, the optimal fraction of wealth invested in the stock is in feedback form given by (see e.g. Rieder & Bäuerle 2005)

| (3.2) |

This expression is independent of the time horizon . And it has been shown in Rieder and Bäuerle (2005) that for , the optimal fraction converges to the optimal fraction of the logarithmic utility function. This is of course no contradiction but shows that there is a significant difference of behavior between an investor with power utility and an investor with logarithmic utility function. In the next subsection we will discuss the case .

For the proof we need the following result, where is the density of a normal distribution with zero mean and variance .

Lemma 3.2.

The function

| (3.3) |

is increasing for .

Proof.

Similar proofs can be found in Rieder and Bäuerle (2005) Theorem 9 and Longo and Mainini (2016) Theorem 6. We start by rewriting this expression as

| (3.4) |

Now denote

| (3.5) |

The derivative of is given by

| (3.6) |

for all and is positive by definition of . Thus, is increasing.

Next consider the density

| (3.7) |

We show that this density is increasing in the likelihood ratio ordering with respect to . For more details about the likelihood ratio ordering consult Müller and Stoyan (2002). In order to do so, we have to show by definition that for , the ratio

| (3.8) |

is increasing. We obtain

| (3.9) |

where is a positive constant independent of . Since is increasing and we have by assumption , the ratio is indeed increasing in . Since the likelihood ratio ordering implies the usual stochastic ordering, the statement follows by definition of the stochastic ordering and the fact that is increasing. ∎

Now we are able to prove Theorem 3.3.

Proof.

It holds that

| (3.10) | |||||

and we have to show that .

First define

| (3.11) |

Note that also depends on . However will be fixed throughout and we do not make the dependence explicit in our notation. Obviously , and

| (3.12) |

Thus, it is enough to show that . Once we have shown this statement for an , it holds for all , since by Lemma 3.2 we have that for all . Now suppose and define . Consider the following lines of inequalities where we use the formula for the moment generating function of a normal distributed random variable in the last equation.

| (3.13) | |||||

Next we obtain with the Jensen inequality (note that is convex for ):

| (3.14) | |||||

Thus we obtain that

| (3.15) |

Since can be chosen arbitrarily close to , the statement follows. ∎

3.2. The case

In this section we are going to prove the following result:

Theorem 3.3.

Let , , and . Then

| (3.16) |

In the case the optimal investment strategy in the Bayesian case for an investor with a very large time horizon is approximately the same as in a setting with known, minimal possible drift. This result is independent of the prior distribution and the current belief. This means that the Bayes investor with is pretty pessimistic in the long run. Obviously there is a significant difference in the long run behavior of investors with , (logarithmic utility) and investors with .

Proof.

We define and as in the previous proof and have to show that . For this it is enough to show that . Similar to Lemma 3.2 it is possible to show that is decreasing in for all (we simply have to replace by ). Thus we have for that and it is enough to prove for an arbitrary close to zero. In order to do so we first rewrite as follows:

| (3.17) | |||||

We used the change of variables in the last equation. Let us now consider the density

| (3.18) |

for fixed and and the function

| (3.19) |

Then we can write . We further use the notation for the density of a normal distribution We obtain:

| (3.20) | |||||

with . Now let

| (3.21) |

Then we can finally write the density as a mixture of normal densities:

| (3.22) |

Next we obtain the following estimate with the Jensen inequality since is concave

| (3.23) | |||||

Next let us choose such that which is possible due to our assumptions and consider the estimate

| (3.24) | |||||

where the second inequality follows form the fact that for all and the last inequality follows since is decreasing which can easily be seen by inspecting its derivative (see also Lemma 3.2). Finally we investigate what happens with these terms when . First we obtain

| (3.25) | |||||

since . Next we obtain

| (3.26) | |||||

since is chosen such that for . Last but not least we obtain by change of variables that

| (3.27) |

since . Finally note that can be made arbitrarily small such that can be made arbitrarily close to which implies the result. ∎

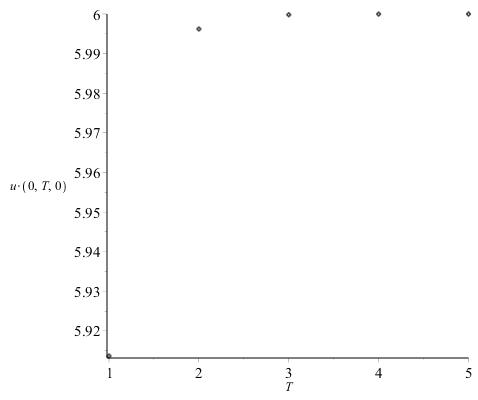

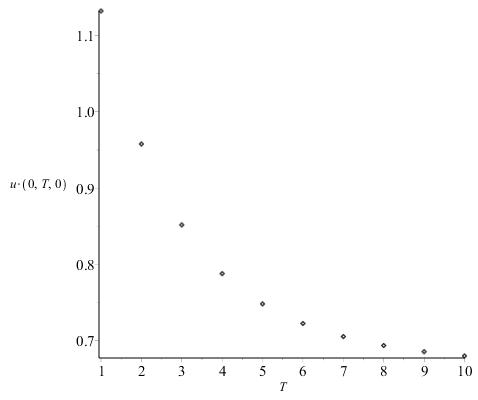

Example 3.4.

Since we have explicit formulas it is easy to compute the optimal fraction of wealth which has to be invested in the stock. To illustrate our theoretical results we have done this calculation for a toy example with , , , , and . For we have chosen and . In this example we have for that and for that We can see the convergence as in the figures. The speed of convergence is rather different, but we have no statement about it.

4. Conclusion

In this paper we have shown that investors with very long time horizon who cannot observe the drift of the stock and use a Bayesian model behave in an extreme way which is rather surprising. In practice the drift may not be constant over a long time horizon and it would be desirable to do the same analysis in e.g. a Hidden Markov Model. But there are no explicit formulas in this case which makes the analysis much harder. From a theoretical point of view the convergence analysis shows that the behavior of investors with power utility for is very sensitive with respect to .

References

- Bäuerle and Rieder [2004] Bäuerle, N., U. Rieder, Portfolio optimization with Markov-modulated stock prices and interest rates. IEEE Transactions on Automatic Control 49(3) (2004), 442-447.

- Björk et al. [2010] Björk, T., M.H.A. Davis, C. Landén, Optimal investment under partial information. Mathematical Methods of Operations Research 71(2) (2010), 371-399.

- Cvitanić et al. [2006] Cvitanić, J., A. Lazrak, L. Martellini, F. Zapatero, Dynamic portfolio choice with parameter uncertainty and the economic value of analysts recommendations. Review of Financial Studies 19(4) (2006), 1113-1156.

- Elliott et al. [1994] Cvitanić, Elliott, R., L. Aggoun, J. Moore, Hidden Markov models: Estimation and control. Springer, New York (1994).

- Fouque et al. [2015] Fouque, J.P., A. Papanicolaou, R. Sircar, Filtering and portfolio optimization with stochastic unobserved drift in asset returns. Communications in Mathematical Sciences 13(4) (2015), 935-953.

- Guéanty and Pu [2016] Guéanty, O., J. Pu, Portfolio choice under drift uncertainty: A Bayesian learning and stochastic optimal control approach. arXiv:1611.07843 (2006).

- Honda [2003] Honda, T., Optimal portfolio choice for unobservable and regime-switching mean returns. J Econ Dyn Control 28 (2006), 45-78.

- Karatzas and Zhao [2001] Karatzas, I., X. Zhao, Bayesian adaptive portfolio optimization. In: Handb. Math. Finance: Option Pricing, Interest Rates and Risk Management, Eds. Cvitani c, J., M. Musiela, E. Jouini, Cambridge University Press (2001), 632 669.

- Longo and Mainini [2016] Longo, M., A. Mainini, Learning and Portfolio Decisions for CRRA Investors. International Journal of Theoretical and Applied Finance 19(3) (2016), 1650018.

- Müller and Stoyan [2002] Müller, A., D. Stoyan, Comparison Methods for Stochastic Models and Risks. John Wiley & Sons (2002).

- Rieder and Bäuerle [2005] Rieder, U., N. Bäuerle, Portfolio optimization with unobservable Markov-modulated drift process. Journal of Applied Probability 42 (2005), 362-378.

- Sass and Haussmann [2004] Sass, J., U.G. Haussmann, Optimizing the terminal wealth under partial information: The drift process as a continuous time Markov chain. Finance and Stochastics 8 (2004), 553-577.

- Shen and Tak Kuen [2012] Shen, Y., T.K. Siu, Asset allocation under stochastic interest rate with regime switching. Economic Modelling 29(4) (2012), 1126-1136.

- Xia [2001] Xia, Y., Learning about predictability: The effects of parameter uncertainty on dynamic asset allocation. The Journal of Finance 56 (2001), 205-246.