Perpetual integrals convergence and extinctions in population dynamics

Abstract

In this article we use a criterion for the integrability of paths of one-dimensional diffusion processes from which we derive new insights on allelic fixation in several situations. This well known criterion involves a simple necessary and sufficient condition based on scale function and speed measure. We provide a new simple proof for this result and also obtain explicit bounds for the moments of such integrals. We also extend this criterion to non-homogeneous processes by use of Girsanov’s transform. We apply our results to multi-type population dynamics: using the criterion with appropriate time changes, we characterize the behavior of proportions of each type before population extinction in different situations.

Keywords: one-dimensional diffusion processes; path integrability; diffusion absorption; population dynamics; extinction and allelic fixation.

1 Introduction

Our motivations in this paper come from population genetics. The first question concerns the dynamics of an allelic proportion in a variable size population going to extinction. We wonder whether the allelic proportion will attain or (fixation or loss of the allele in the population) before population extinction. The second question concerns the dynamics of the respective proportions of neutral alleles until fixation of one of them. We are asking about simultaneous allele extinctions or not.

In both cases, we need to slow down the dynamics before either population extinction or allele fixation by the use of a time change. That leads us to study quantities of the form (which are referred to as perpetual integrals [15]), for a nonnegative diffusion process and the hitting time of , or , for a diffusion process and the hitting times of and . We need to know whether such integrals are finite or not. In Section 2, we state and prove a general criterion involving a necessary and sufficient condition based on the scale function and speed measure of the nonnegative diffusion process , which ensures that the integral is finite almost surely or infinite almost surely. This 0-1 law criterion was already known and proved using a combination of the local time formula, the Ray-Knight Theorem and Jeulin’s Lemma (see [5, 12]). We provide a simpler proof which also provides explicit bounds for the moments of perpetual integrals and can be easily extended to more general one dimensional Markov processes. Then, we extend this result to a diffusion taking values in a compact subset and finally to non-homogeneous processes by the use of Girsanov’s transform. Applications to standard population models are given.

In Section 3, we apply these general integrability results to several open allele fixation problems. The use of tricky time changes dramatically simplifies these questions. Subsection 3.1 concerns the dynamics of an allele proportion in a population with variable size. We assume that the total population size goes to almost surely. We give a necessary and sufficient condition for the coupled logistic population size dynamics and allelic neutral Wright-Fisher equation (with variable size) to get allelic fixation before extinction almost surely. The condition is satisfied when the population size dynamics is a logistic Feller stochastic differential equation. Nevertheless, we give examples of population size dynamics for which extinction occurs before fixation with positive probability, emphasizing by this way the necessity of taking into account the behavior of the population size, in particular near extinction. We also study a case with allelic selection using a Girsanov’s transform for the coupled system of population size and allelic proportion. In Subsection 3.2, we consider a neutral -type Wright-Fisher diffusion. We show that one of the alleles is fixed almost surely in finite time and that until that time, the population experiences successive (and not simultaneous) allele extinctions. These results are proved by induction on and using a time change based on the fixation time: we slow down time before fixation to observe the successive allele extinctions.

2 Integrability properties for diffusion processes

2.1 General diffusion processes on

Let us consider a general one-dimensional diffusion process (that is a continuous strong Markov process) with values in . We denote by the hitting time of by the process :

if the set is non empty and is infinite otherwise. When the process has to be specified, this time will be denoted .

Let us denote by the law of starting from . We assume that is regular (, ). This implies (see Revuz-Yor [13, VII-Proposition 3.2]) that for any and ,

We may associate with the process a scale function and its locally finite speed measure on (see [13, Chapter VII]). We will assume moreover that, for all ,

| (2.1) |

where is the explosion time.

Lemma 2.1.

Condition (2.1) is equivalent to

| (2.2) |

Note that Condition (2.2) is well known in the case where is solution of a stochastic differential equation (cf. [10] p.348, [8] p.450).

Proof.

Assume first that (2.1) is satisfied. As has scale , is a local martingale on such that a.s.. We deduce that and . The diffusion has a natural scale with speed measure (see [13], Chapter VII). Since it attains in finite time almost surely, we deduce using [14, Theorem 51-2] that . As , we obtain (2.2).

Conversely, assume (2.2). Conditions and imply that the local martingale doesn’t explode a.s.. Since , then and the process attains in finite time a.s., so does the process . That concludes the proof. ∎

Since the function is defined up to a constant, we choose by convention as soon as .

In the following theorem, we prove a law for the finiteness/infiniteness of perpetual integrals of diffusion processes and provide explicit bounds for their moments. This law has been extensively studied and already proved by different ways in the literature. Its first proof goes back to [5] (see also [12]) using a combination of the local time formula, Ray-Knight Theorem and Jeulin’s Lemma. Attempts to simplify this approach are provided in [3] for some stochastic differential equations using an appropriate space change. The almost sure finiteness criterion has also been recovered by simple means in [11], where the existence of a non-explicit exponential moment for perpetual integrals is also proved. Proofs of the 0-1 law in particular settings are given in [4, 7]. In [16], the authors define perpetual integrals as the first hitting times of diffusion processes, and illustrate how the Laplace transform of some perpetual integrals can be found using Feynman-Kac formula.

Theorem 2.2.

Let be a regular diffusion process on with scale function and speed measure on satisfying (2.2). Let also be a non-negative measurable function on which is locally integrable on . Then, for all and all ,

and

Proof.

Because of the non-explosion assumption (2.2), we have and such that . Hence it is sufficient to prove Theorem 2.4 for functions satisfying for all . We make this assumption from now on.

As has scale function and speed measure , the process is on a natural scale with speed measure . Then it is enough to prove the result if the process is on a natural scale (); the general case will follow immediately. In particular, we have the following Green formula (see [Chapter 23] of [9])

One easily checks that, under for any , satisfies a law. Indeed, we have

where the , , are non-negative independent (because of the strong Markov property) random variables which are almost surely finite (in fact with finite expectation, because of our assumptions and the Green’s formula applied under up to time ). Hence the above series is finite with probability zero or one.

Assume first that . Then almost surely and, for all ,

where we used the Markov property. We immediately deduce by induction that

This concludes the proof of the first part of Theorem 2.2 (the inequality is trivial when ).

Assume now that and fix . For all , we set

In particular, for all and hence, using the inequalities established above and then the fact that goes to infinity and the fact that is assumed to be finite on neighborhood of , we deduce that

We deduce that, for large enough,

Indeed, for any random variable such that , we have, setting ,

and hence . Now using the fact that is increasing in , we deduce that, for large enough,

Since is not bounded in , we deduce that

This and the fact that satisfies a law conclude the proof of Theorem 2.2. ∎

The equivalences stated in Theorem 2.2 are particularly useful when is solution of a one-dimensional stochastic differential equation

| (2.3) |

where is a one dimensional Brownian motion, and and are measurable functions such that is locally integrable and such that for all . Here and are the scale function (up to a constant) and speed measure equal to

| (2.4) |

as detailed in Chapter 23 of [9]. In particular, is a regular diffusion.

Corollary 2.3.

Assume that is solution of (2.3) with and . Let us consider a non negative locally bounded measurable function on . Then, under ,

Let us give two examples for population size processes.

Example 1.

Branching process with immigration. Let us consider the solution of the stochastic differential equation

The scale function and except when for which and , cf. (2.4). Then

Applying Corollary 2.3 with , we obtain

| (2.5) |

since . In the particular case , the authors of [7] propose an other approach based on self-similarity properties.

Example 2.

Logistic diffusion process. Let us consider the process

where . Then and and , since . (Note that if , the condition is not satisfied). It is immediate to check that (1) also holds.

2.2 General diffusion processes on

Let us consider a general diffusion process with scale function and locally finite speed measure on , with . Let us denote by and the hitting times of and respectively by the process . We assume that, for all , . This is the case if and only if one of the following properties is satisfied

; and ;

and ; ;

and ; .

Theorem 2.4.

Fix and let be a locally bounded measurable function. Then

A similar result holds at the boundary :

Proof.

As in the proof of Theorem 2.2, it is enough to prove the result in the case where is the identity function.

Without loss of generality, we take . Let us consider , fix and consider a locally finite measure on such that . Let be a diffusion process on natural scale on with speed measure and starting from , built as a time change of the same Brownian motion as . Because of this construction, and coincide up to time on the event .

Now, by Theorem 2.2 applied to and , we deduce that

Since and coincide up to time on the event , we deduce that, up to negligible events,

But on , holds for , so that, up to -negligible events,

The continuity of the paths of implies that

which yields, up to negligible events,

This concludes the proof of the direct implications in Theorem 2.4.

Now, assume for instance that on . Then, a fortiori, on for any . This implies that on . But happens with probability by definition of the natural scale. We deduce from Theorem 2.2 that does not hold and hence, because is non-negative, that . This provides the first implication in Theorem 2.4. The second implication in Theorem 2.4 is proved using similar arguments.

The result at boundary is proved similarly. ∎

Let us illustrate Theorem 2.4 by simple examples from population genetics, which will be used as central arguments in Section 3.

Example 3.

The neutral Wright-Fisher diffusion. Let be the stochastic process solution of

The process is on natural scale on with speed measure . Since it reaches or in finite time a.s..

Therefore, since and for all ,

| (2.6) |

Example 4.

The Wright-Fisher diffusion with selection. Let be the process solution of

Its scale function on is given by and its speed measure is . In particular, we deduce that Hence, the process reaches or in finite time a.s.. Setting as in the previous example , we have and Theorem 2.4 yields

| (2.7) |

2.3 Extension to non-homogeneous processes by use of Girsanov transform

We are interested in generalized one-dimensional stochastic differential equations of the form

| (2.8) |

where is a Brownian motion for some filtration and is predictable with respect to . The process can for example model an environmental heterogeneity. Other examples will be given in Section 3.1.

Assumption : We consider real functions and such that for any Brownian motion on some probability space, the one-dimensional stochastic differential equation satisfies the assumptions of Corollary 2.3.

Theorem 2.5.

Let us consider a solution of (2.8) where and satisfy Assumption . We also assume that almost surely and that the sequence tends almost surely to infinity as tends to infinity.

Next, we assume that for any ,

| (2.9) |

Let be a non negative locally bounded measurable function on . We have

where and are defined in (2.4).

Note that (2.9) holds true as soon as, for all ,

| (2.10) |

Proof.

We use the Girsanov Theorem, as stated for example in Revuz-Yor [13] Chapter 8 Proposition 1.3.

Let us consider the diffusion process on , absorbed when it reaches or , at time . The exponential martingale , where , is uniformly integrable thanks to (2.9) and Novikov’s criterion. Define for any the probability with . Then, the process is a -Brownian motion and, under , is solution to the SDE

Hence restricted to is the scale function of under . Since and are both bounded in a vicinity of , we deduce from Theorem 2.4 that

Note also that, since we assumed that tends almost surely to infinity, we have up to a -negligible event,

and hence

But, by definition of and by Theorem 2.4, we have

| (2.11) | ||||

| (2.12) | ||||

| (2.13) |

Letting tend to infinity concludes the proof. ∎

3 Applications to population genetics

3.1 Wright Fisher equation with variable population size

We are interested in the allelic fixation in a population with variable size that goes almost surely to extinction. The main question is whether one allele has time or not to get fixed before the population goes extinct. We will see that it depends on the behavior of the diffusion coefficient (near extinction) in the equation satisfied by the population size.

3.1.1 Probability of fixation before extinction - Neutral case

Consider the process solution to the system of stochastic differential equations

| (3.1) |

where are independent one-dimensional Brownian motions and are locally Hölder functions. The system is well defined for all time , which is called the extinction time of the system. We set and for all , where is a cemetery point. The stochastic process models the population size dynamics, while represents the dynamics of the proportion of a given allele, or type, in the population. We also denote by . We say that fixation occurs before extinction if and only if (otherwise we have ). The following result provides a necessary and sufficient criterion ensuring this event to happen with probability one.

Theorem 3.1.

Fixation occurs before extinction with probability one if and only if

| (3.2) |

Remark 1.

Note that the counterpart of the above result is: if and only if .

Remark 2.

Proof.

We define the random number

and the time change , for all , as the unique positive real number satisfying

| (3.3) |

In particular, is increasing and . Now, we set for

The time change formula implies that is solution to the stochastic differential equation

where is a standard Brownian motion. We denote by the (possibly infinite) absorption time of .

(i) Assume that . In this case, by Theorem 2.2 and reaches or in finite time almost surely. In particular, almost surely and

As a consequence, with probability one, and hence fixation occurs before extinction almost surely.

(ii) Assume that . In this case with probability one by Theorem 2.2.

Let be a Brownian motion independent from and consider the solution to the SDE . We define for the time changed , so that is solution to the SDE system (3.1) and hence, by uniqueness in law of the solution to this system, and have the same law. Since and can be obtained as the same function of and respectively, we deduce that they share the same law up to time . Then we have

since and are independent and is a Wright-Fisher diffusion. This concludes the proof, since , therefore . ∎

Theorem 3.1 can be extended in a natural way to the case where is not on natural scale. We consider the following classical modeling of Wright-Fisher diffusion with variable population size, which corresponds to .

Proposition 3.2.

Let us consider the two-dimensional stochastic system

with two independent Brownian motions and .

-

(i)

Fixation occurs before extinction with probability one if and only if

-

(ii)

Under this condition,

(3.4)

Proof.

(i) The extension of Theorem 3.1 to with general scale function is immediate, using Corollary 2.3. Condition (3.2) becomes

| (3.5) |

Using (2.4) we note that for the present case, , which allows to conclude.

(ii) Using notations of Theorem 3.1, we get a.s., for all , and is a neutral Wright-Fisher diffusion process. From Equation (2.6) we have

| (3.6) |

Noting that , that , and we get the result. ∎

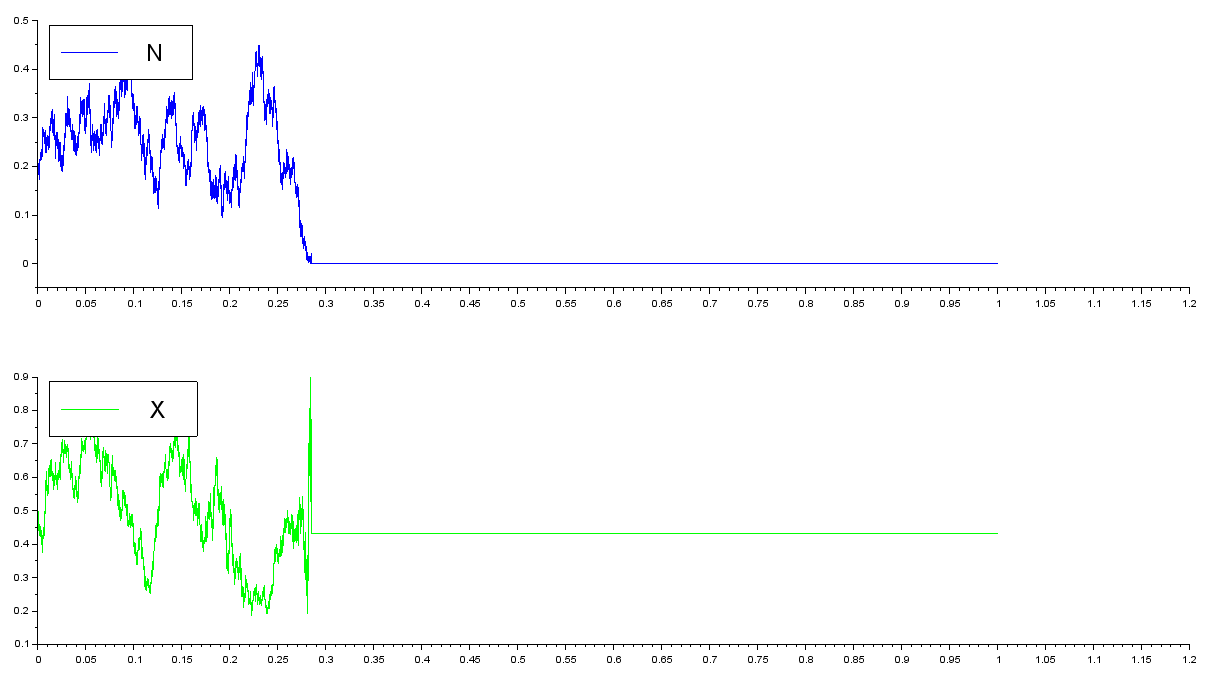

The previous corollary highlights the major effect of the demography on the maintenance of genetic diversity. The behavior of near extinction plays a main role. For the usual demographic term , we have almost sure fixation before extinction, but for a small perturbation of this diffusion term, taking for example , , extinction before fixation occurs with positive probability. An example of extinction before fixation is illustrated in Figure 1 and the effect of on the probability of extinction before fixation is numerically studied in Figure 2

3.1.2 Wright-Fisher equation with selection and variable population size

Let us consider a -types competitive Lotka-Volterra stochastic system as introduced in [1]:

where is a standard Brownian motion, . Setting and leads to

with two independent Brownian motions and . The parameter represents the selective advantage of the type of population .

Proposition 3.3.

-

(i)

Fixation occurs before extinction almost surely.

-

(ii)

We get

Proof.

We use a -dimensional Girsanov theorem: let us consider the exponential martingale , where

For each , the martingale is uniformly integrable. Under the probability such that , the process

is a bi-dimensional Brownian motion, and the process is solution to the stochastic differential equation

3.2 Successive fixations for the multi-allelic Wright-Fisher case

We consider now a neutral -type Wright-Fisher diffusion with types (Ethier-Kurtz [6], pp. ) describing the dynamics of the respective proportions of the alleles. We are interested in the study of the successive extinctions of alleles.

Since , it is enough to study the dynamics of the process . We know (see for example [6, Chap. 10]) that this diffusion admits the following infinitesimal generator.

| (3.8) | ||||

We can represent the diffusion in the following way: let us start by distinguishing types of alleles, the allele and the others. The stochastic process is a neutral Wright-Fisher diffusion and writes

where is a Brownian motion. Next, among the set of alleles that are not allele (this population has size at time ),we can again distinguish types of alleles, the allele and the others. The proportion of allele in this new population satisfies:

where is a Brownian motion independent from . Finally, the diffusion process satisfies the diffusion equation:

| (3.9) |

for all , where is a -dimensional Brownian motion. To check these assertions, it suffices to prove that the diffusion process that satisfies Equation (3.9) admits the following quadratic variation terms: for all ,

These results are easily obtained by using a recursion on .

Our aim is to prove the following theorem:

Theorem 3.4.

-

One of the alleles is fixed almost surely in finite time, i.e. the random variable attains in finite time almost surely.

-

Till that time, the population experiences successive (and non simultaneous) allele extinctions.

The proof of this theorem relies on the following lemma

Lemma 3.5.

Let be a -dimensional Wright-Fisher diffusion process, let for all time , and define the change of time on (from Example 3) such that for all . Now let

The stochastic process is a -dimensional Wright-Fisher diffusion process.

Proof of Lemma 3.5.

Let us denote by the infinitesimal generator of the -dimensional diffusion process . From Equation (3.8), the infinitesimal generator of the -dimensional Wright-Fisher diffusion process satisfies for any bounded real-valued twice differentiable function on :

Now for any bounded real-valued twice differentiable function defined on , we may write

where

and .

Therefore, we obtain that

which gives the result since . ∎

Proof of Theorem 3.4.

We prove both results by induction on . For , we know that the result is true for . Now for alleles, note that the proportion of allele follows a -dimensional Wright-Fisher diffusion. Therefore allele gets fixed or disappears almost surely in finite time. If allele gets fixed then one of the alleles gets fixed almost surely in finite time. If allele gets lost then from its extinction time, the population follows a -type Wright-Fisher diffusion, therefore one of the remaining alleles gets fixed almost surely in finite time, using the induction assumption.

We now prove . We have

from Example 3. We define the time change , for all , as the unique non-negative real number satisfying

Now, for all , let us define the stochastic process such that

From Lemma 3.5, the stochastic process is a dimensional Wright-Fisher diffusion process. By recurrence assumption, this diffusion process experiences successive and non simultaneous extinctions, at times denoted by . Therefore . Under the event , the times , …, and correspond to the extinction times experienced by the population, which gives the result, since from . ∎

Acknowledgements: This work was partially funded by the Chair ”Modélisation Mathématique et Biodiversité” of VEOLIA-Ecole Polytechnique-MNHN-F.X. It was also supported by a public grants as part of the ”Investissement d’avenir” project, reference ANR-11-LABX-0056-LMH,-LabEx LMH, and reference ANR-10-CAMP-0151-02, Fondation Mathématiques Jacques Hadamard, and by the Mission for Interdisciplinarity at the Centre national de la recherche scientifique.

References

- [1] P. Cattiaux, and S. Méléard. Competitive or weak competitive stochastic Lotka-Volterra systems conditioned on non-extinction. J. Math. Biol. 60, 797–829, 2016.

- [2] C. Coron. Slow-fast stochastic diffusion dynamics and quasi-stationarity for diploid populations with varying size. J. Math. Biol. 72 (1-2), 171–202, 2016.

- [3] Z. Cui. A new proof of an Engelbert-Schmidt type zero-one law for time-homogeneous diffusions. Statistics & Probability Letters, 89, 118–123, 2014.

- [4] H.J. Engelbert, T. Senf. On Functionals of a Wiener Process with Drift and Exponential Local Martingales. Stochastic Processes and Related Topics, Series Mathematical Research, pp. 45 - 58, Akademie-Verlag, Berlin, Friedrich-Schiller-Univ., 1991.

- [5] H.J. Engelbert, G. Tittel. Integral functionals of strong Markov continuous local martingale. In Stochastic Processes and Related Topics: Proceedings of the 12th Winter School Siegmundsburg, Germany, edited by R. Buckdahn, H.J. Engelbert and M. Yor. Taylor & Francis, 2002.

- [6] S.N. Ethier, T.G. Kurtz. Markov Processes. Characterization and convergence. Wiley series in statistics and probability. John Wiley Sons, 1986.

- [7] C. Foucart, O. Hénard. Stable continuous stat branching processes with immigration and Beta-Fleming-Viot processes with immigration. Electron. J. Probab.18 (23), 1–21, 2013.

- [8] N. Ikeda, S. Watanabe. Stochastic differential equations and diffusion processes, 2nd edition, North-Holland, 1989.

- [9] O. Kallenberg. Foundations of modern probability, 2nd edition, Springer, 2001.

- [10] I. Karatzas, S.E. Shreve. Brownian motion and stochastic calculus, 2nd edition, Springer, 1991.

- [11] D. Khoshnevisan, P. Salminen and M. Yor A note on a.s. finiteness of perpetual integral functionals of diffusions. Electron. Commun. Probab. 11, 108–117, 2006.

- [12] A. Mijatovic, M. Urusov. Convergence of integral functionals of one-dimensional diffusions. Electron. Commun. Probab. 17, 2012.

- [13] D. Revuz, M. Yor. Continuous martingales and Brownian motion. Third edition, Springer, 1999.

- [14] L.C.G. Rogers, D. Williams. Diffusions, Markov processes and martingales. Vol. 2, 2nd edition, Cambridge University Press, 2000.

- [15] P. Salminen, M. Yor. Properties of perpetual integral functionals of Brownian motion with drift. Ann. Inst. Henri Poincaré Probab. Stat. 41(3), 335–347, 2005.

- [16] P. Salminen, M. Yor. Perpetual Integral Functionals as Hitting and Occupation Times. Electron. J. Probab. 10 371–419, 2005.