Portfolio Choice with Small Temporary and Transient Price Impact

Ibrahim Ekren†

Florida State University

Johannes Muhle-Karbe‡

Carnegie Mellon University

We study portfolio selection in a model with both temporary and transient price impact introduced by Garleanu and Pedersen (2016). In the large-liquidity limit where both frictions are small, we derive explicit formulas for the asymptotically optimal trading rate and the corresponding minimal leading-order performance loss. We find that the losses are governed by the volatility of the frictionless target strategy, like in models with only temporary price impact. In contrast, the corresponding optimal portfolio not only tracks the frictionless optimizer, but also exploits the displacement of the market price from its unaffected level.

Keywords: portfolio choice; temporary price impact; transient price impact; asymptotics.

Mathematics Subject Classification (2010): 91G10, 91G80, 35K55.

JEL Classification: G11, G12, G23, C61.

1. Introduction

When rebalancing large portfolios, the adverse price impact of each trade is a key concern. Indeed, large transactions deplete the liquidity available in the market and lead to less favorable execution prices. After the completion of a large trade liquidity recovers, but only gradually. Whence, it is of crucial importance for portfolio managers to schedule their order flow in an appropriate manner, so as to trade off the gains and costs of rebalancing in an optimal manner.

Accordingly, there is a large and growing literature on price impact models. Following the survey paper of Gatheral and Schied (2013), these models can be broadly classified into two categories. The first distinguishes between temporary trading costs, that only affect each trade separately, and permanent price impact that affects the current and all future trades in the same manner (cf., e.g., Bertsimas and Lo (1998); Almgren and Chriss (2001) and many more recent studies). The second takes into account the transient nature of price impact, which is caused by large trades but gradually wears off once these are completed, cf., e.g., Bouchaud et al. (2004, 2006); Obizhaeva and Wang (2013); Gatheral (2010); Alfonsi et al. (2010); Predoiu et al. (2011); Gatheral and Schied (2013).

These models were originally developed for optimal execution problems, where the goal is to split up a single, exogenously given order in an optimal manner. More recently, dynamic portfolio choice and hedging problems with price impact have also received increasing attention (Garleanu and Pedersen, 2013, 2016; Collin-Dufresne et al., 2012; Guasoni and Weber, 2017; Moreau et al., 2017; Guéant and Pu, 2017; Almgren and Li, 2016; Bank et al., 2017). This means that the target orders to be executed are no longer assumed to be given, but are instead derived endogenously from a dynamic optimization problem. This allows to explicitly model the tradeoff between gains from reacting to new information and costs of trading. However, the complexity of the optimization problem increases considerably. Whence, attention has almost exclusively focused on first-generation price impact models with only temporary trading costs so far.

The only exception is the recent work of Garleanu and Pedersen (2016). They study portfolio choice for agents that try to exploit partially predictable returns in the presence of linear temporary and transient price impact. Using dynamic programming arguments, they describe the value function of the problem at hand and the corresponding optimal trading rate via the solution of a coupled system of nonlinear equations.111The coupled nature of these optimality equations complicates the analysis of even the simplest concrete models, unlike for models with purely temporary costs, where linear-quadratic problems can be solved explicitly in essentially full generality (Garleanu and Pedersen, 2013, 2016; Cartea and Jaimungal, 2016; Bank et al., 2017; Bank and Voß, 2018). This analysis identifies the current deviation of the market price from its “unaffected” value as an important new state variable. However, the involved nonlinear nature of the optimality conditions makes it difficult to draw further qualitative and quantitative conclusions beyond a benchmark model with a linear factor process.

To overcome this lack of tractability and analyze models with more general dynamics, small-cost asymptotics have proven to be very useful in models with temporary trading costs only. This means that one views the trading friction at hand as a perturbation of the frictionless benchmark model, and looks for corrections of the frictionless optimizer that take it into account in an asymptotically optimal manner. As succinctly summarized by Whalley and Wilmott (1997), the goal is to “reveal the salient features of the problem while remaining a good approximation to the full but more complicated model”. For example, in the context of linear temporary price impact, Moreau, Muhle-Karbe and Soner (2017) have shown that both the optimal trading rate and the leading-order loss due to transaction costs admit explicit asymptotic expressions.222Related work on other small transaction costs includes Shreve and Soner (1994); Whalley and Wilmott (1997); Korn (1998); Janeček and Shreve (2004); Bichuch (2014); Soner and Touzi (2013); Possamaï et al. (2015); Martin (2014); Kallsen and Muhle-Karbe (2017); Kallsen and Li (2015); Altarovici et al. (2015); Cai et al. (2017a, b); Feodoria (2016); Melnyk and Seifried (2018); Herdegen and Muhle-Karbe (2018). The trading rate turns out to be proportional to the distortion relative to the frictionless target and a universal constant – the square-root of risk aversion, times market variance, divided by trading costs.333The same statistic also plays a key role in optimal execution problems Almgren and Chriss (2001); Schied and Schöneborn (2009) and models with asymmetric information Muhle-Karbe and Webster (2018). In contrast, the volatility of the target strategy does not feature in this formula, so that the optimal relative trading speed is the same for a broad class of optimization problems. In contrast the volatility of the frictionless target is a crucial input for the leading-order effect of the trading costs, which are equal to a suitably weighted average of this quantity, weighted with a term explicitly determined by risk aversion, market volatility, and trading costs.

The present study brings similar asymptotic methods to bear on the model of Garleanu and Pedersen (2016). As this model includes two frictions – temporary and transient price impact – we consider the joint limit where both of these become small. In order to understand the contribution of both frictions, we focus on the “critical regime”, where both are rescaled so as to feature nontrivially in the limit.

In a general Markovian setting, this enables us to obtain tractable formulas for the asymptotically optimal trading rate and the leading-order performance loss due to illiquidity due to both temporary and transient price impact. These results show that the volatility of the frictionless target portfolio is still the key statistic for its sensitivity with respect to small trading frictions. Indeed, the representation of the first-oder loss from Moreau et al. (2017) remains valid in the present context after updating the scaling weight to account for the additional model parameters. In contrast, the optimal trading rate is more complex. To wit, with only temporary transaction costs, the asymptotically optimal policy simply tracks the frictionless target. The transient price distortion in the present model provides an additional predictor for future price changes. Accordingly, the optimal trading rate now trades off tracking the frictionless target against the exploitation of this trading signal.

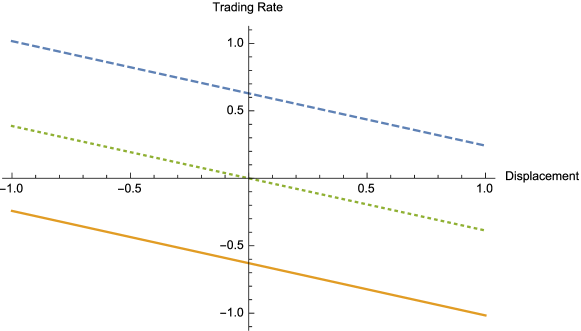

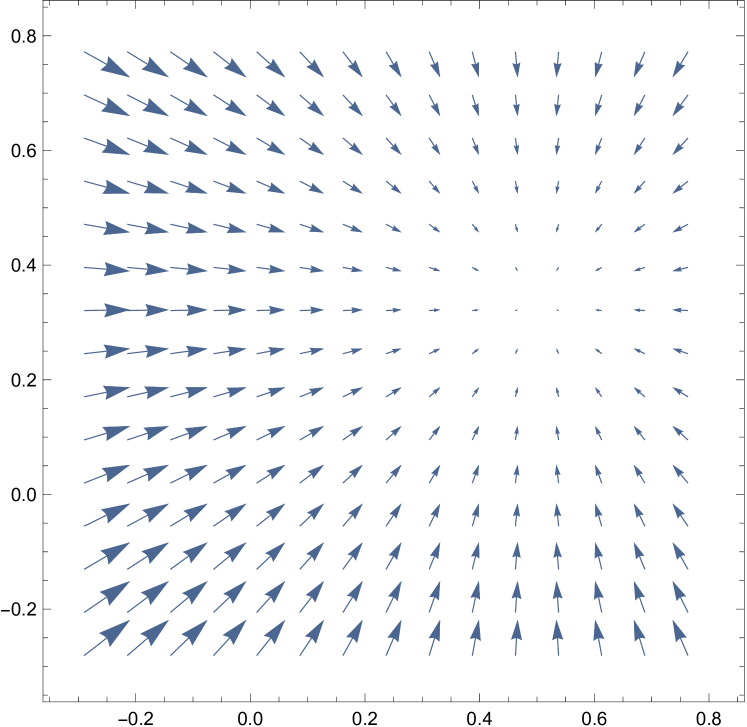

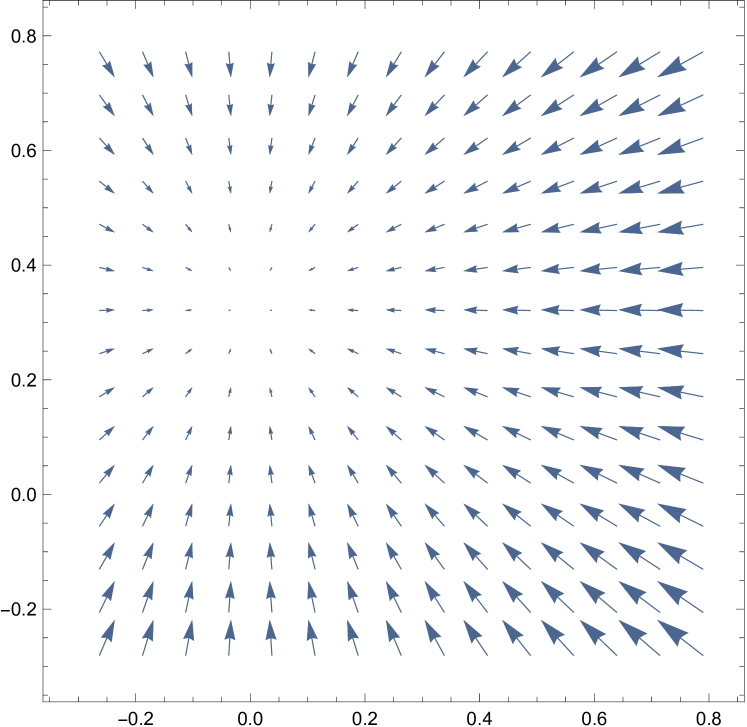

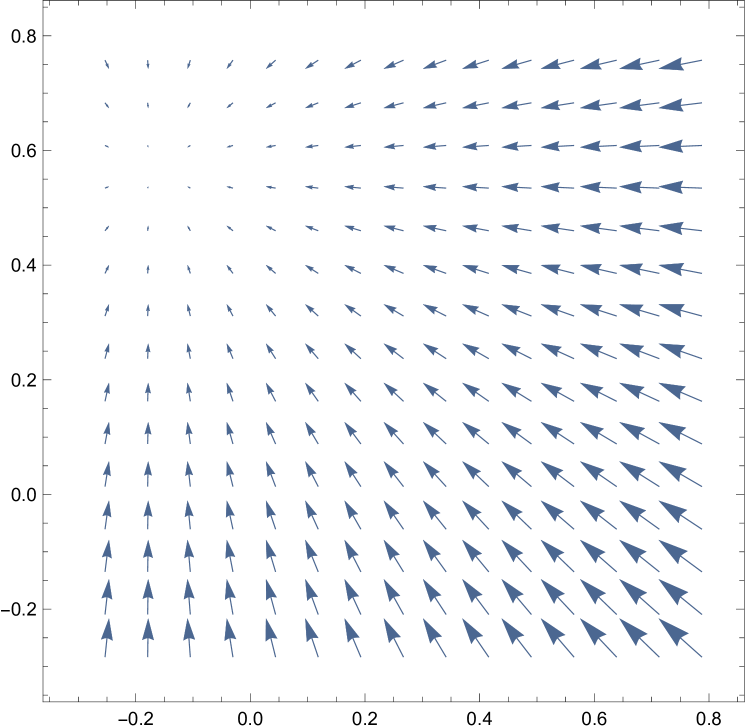

This is displayed in Figure 1 for a model with one risky asset and constant optimal trading speed. As a positive distortion predicts negative future price changes, the corresponding trading rate is reduced and vice versa. The more involved comparative statics for several risky assets are illustrated in Figures 2 and 3. There, we plot the vector field of asymptotically optimal trading speeds for two assets and display the effect a price distortion in one of the assets has on these. In Figure 2, the two assets are uncorrelated. Accordingly, a positive price distortion in asset one only affects the optimal trading speed in the latter, whereas the turnover in asset two remains unchanged.444This decoupling between uncorrelated assets is typical for agents with constant absolute risk aversions (Liu, 2004), but only holds true approximately in the high risk-aversion limit for constant relative risk aversions (Guasoni and Muhle-Karbe, 2015). The comparative statics of a multidimensional model with temporary price impact and constant relative risk aversion are discussed in detail by Guasoni and Weber (2018). In Figure 3, the two assets have substantial positive correlation. Then, a positive price distortion in the first asset still is a negative indicator for its future returns, so that the corresponding target position is reduced. However, to compensate for this change of the portfolio composition, the target position in the positively correlated second asset now is increased.

These effects depicted in these figures are clearly visible in our simple asymptotic formulas. More generally, these show that the tracking speed for the frictionless target turns out to be the same as for purely temporary costs. In contrast, the weight placed on the current distortion depends on the tradeoff between all price impact parameters. If temporary price impact is substantially larger than its transient counterpart, this dependence reduces to the simple ratio of price distortion over temporary trading cost, cf. Section 3.5.

To prove these results, we follow Soner and Touzi (2013); Altarovici et al. (2015); Moreau et al. (2017) and use stability results for viscosity solutions. However, substantial new difficulties arise here due to the presence of an additional state variable, the price distortion caused by trading. Its presence leads to a substantially more complicated limiting control problem. Moreover, with only temporary costs, the frictional value is always dominated by its frictionless counterpart and the partial differential equations involved have some non-degeneracy that is crucial for establishing their expansions. This is no longer the case in the present context. To overcome these difficulties, we therefore study a suitably renormalized version of the value function and develop new methods to obtain locally uniform bounds for its scaled deviation from the frictionless value.

The remainder of this article is organized as follows. In Section 2 we introduce the model, its frictionless solution, and the dynamic programming characterization of the version with temporary and transient price impact. Our main results, a first-order expansion of the frictional value function in the large liquidity limit and a corresponding asymptotically optimal policy, are presented in Section 3. In Section 4, we give estimates that enable us in Section 5 to define the upper and lower semilimits of the rescaled deviation of the value functions from the frictionless value. We in turn characterize these semilimits as viscosity semisolutions of the second corrector equation in Section 6. The dependence of these semilimits on the initial states is subsequently studied in Section 7. Finally, the asymptotic optimality of our candidate policy is established in Section 8. To ease readability, some technical proofs are delegated to Appendix A.

Notation

We write for the identity matrix on and denote by the cone of -valued, symmetric, positive definite matrices. Inequalities between symmetric matrices are understood in the sense that the difference is symmetric positive semidefinite. denotes the transpose of a matrix , its trace, and its Frobenius norm. For a function , we write for the gradient of . For a locally bounded function , the corresponding upper and lower semicontinuous envelopes are denoted by and , respectively. To simplify notation in the technical estimates, is used to denote a generic, sufficiently large positive constant that may vary from line to line.

2. Model

2.1. Financial Market

Fix a filtered probability space , endowed with an -valued Brownian motion . We consider a financial market with assets. The first one is safe; its price is normalized to one. The other assets are risky; their prices are given by the first components of a -valued Markovian state process with dynamics

| (2.1) |

where or . The deterministic functions and are twice continuously differentiable and Lipschitz, so that this stochastic differential equation has a unique strong solution for any initial condition .

To ease notation, we write

| (2.2) |

and set

when there is no ambiguity about the initial condition of . To rule out degenerate cases, we assume throughout that the infinitesimal covariance matrix is invertible with inverse .

For all smooth functions , the infinitesimal generator of the diffusion applied to is denoted by

Example 2.1.

Throughout the paper, we will illustrate our results for a nonlinear extension of the arithmetic model with mean-reverting returns from De Lataillade et al. (2012); Martin (2014); Garleanu and Pedersen (2013, 2016). This means that the second component of the factor process is an autonomous Ornstein-Uhlenbeck process with dynamics

for . The corresponding risky asset has dynamics

for constants and , as well as a function with bounded derivatives of order one, two, and three.

2.2. Trading and Optimizations without Frictions

Without frictions, self-financing trading strategies are modeled by predictable, -valued processes , where denotes the number of shares of risky asset held at time . The corresponding portfolio returns then are described by the stochastic integral as usual. As in Kallsen (2002); Grinold (2006); Martin and Schöneborn (2011); Martin (2014); Garleanu and Pedersen (2013, 2016); Guasoni and Mayerhofer (2016), we consider an investor with infinite planning horizon who maximizes her expected returns penalized for the corresponding variances. In the continuous-time limit this leads to the following local mean-variance functional,

| (2.3) |

Here, and are the investor’s risk aversion and time-discount rate, respectively. Pointwise maximization of the integrand in (2.3) readily yields that the optimizer is the (myopic) Merton portfolio,

| (2.4) |

Hence, the value function

has the following probabilistic representation,

| (2.5) |

For our PDE analysis of the corresponding problems with frictions, we focus on the case where this value function is finite and smooth enough in the initial data to satisfy the corresponding dynamic programming equation in the classical sense.

Assumption 2.2.

The frictionless value function (2.5) is finite and a classical solution of the dynamic programming equation,

| (2.6) |

Example 2.3.

For the model with mean-reverting returns from Example 2.1, the optimal strategy is also a (possibly nonlinear) function of the Ornstein-Uhlenbeck state process,

The corresponding value function can be computed as

| (2.7) |

where with is Gaussian with mean and variance . Given the boundedness of the first two derivatives of , one can easily show by differentiating under the integral that is twice continuously differentiable.

2.3. Trading and Optimization with Frictions

Following Garleanu and Pedersen (2016), we now introduce two trading frictions into the above model.555This is a special case of the general framework for transient price impact studied in Gatheral (2010). The first one is purely temporary in that it only affects each trade separately through a quadratic cost666Put differently, each trade has a linear temporary price impact proportional to both trade size and speed, compare Guasoni and Weber (2015); Moreau et al. (2017) for more details.

| (2.8) |

levied on the turnover rate

This friction is parametrized by the symmetric definite positive matrix ,777Symmetry can be assumed without loss of generality, compare Garleanu and Pedersen (2013); Guasoni and Weber (2015); positive-definiteness means that each trade incurs a nontrivial cost. This is evidently satisfied in the most common specifications or for a scalar , for example. and naturally constrains trading strategies to be absolutely continuous. As pointed out by Garleanu and Pedersen (2016), this “resembles the method used by many real-world traders in electronic markets, namely to continuously post limit orders close to the best bid or ask. The trading speed is the limit orders’ “fill rate” […]”.

In addition to the temporary trading cost, trades also have a longer-lasting impact on market prices denoted by . To wit, trading at an (adapted) rate shifts the unaffected market quote by for a symmetric positive definite matrix , i.e., purchases create an additional positive drift, etc. However, this price impact is not permanent as in Almgren and Chriss (2001); Almgren and Li (2016) but decays gradually over time with an exponential rate .888Related models with transient price impact have been studied intensively in the optimal execution literature, compare, e.g., Obizhaeva and Wang (2013); Gatheral (2010); Alfonsi et al. (2010); Predoiu et al. (2011). In summary, for an initial state

the “transient” distortion of the actual price from its unaffected version thus has the following Ornstein-Uhlenbeck-type dynamics,

| (2.9) |

and the risky positions evolve as

| (2.10) |

With temporary and transient price impact, maximizing the risk-adjusted returns of a trading strategy then boils down to

| (2.11) |

As in Garleanu and Pedersen (2016), this objective function means that the investor has mean-variance preferences over the changes in wealth in each time period. The first term on the right-hand side of (2.11) collects the expected returns due to i) changes in the unaffected price process (2.2) and ii) changes in the price distortion (2.9).999The safe position pinned down by the self-financing condition does not appear explicitly because the safe asset is normalized to one. The second term is the usual risk penalty, and the third accounts for the temporary transaction costs. Unlike for the frictionless problem (2.3), the risky positions can no longer be adjusted immediately and for free. Instead, they become additional state variables that can only be adjusted gradually by applying the controls . In particular, the problem is no longer myopic and therefore needs to be attacked by dynamic programming methods. With additional transient price impact, the distortion of the current price relative to its unaffected value enters as an additional crucial statistic.

To make sure that this infinite-horizon problem (2.11) is well posed, we focus on admissible strategies that satisfy a suitable (mild) transversality condition,101010Garleanu and Pedersen (2016) mention that a condition of this type is needed, but do not provide it. If the price impact parameters are constant, our notion (2.12) encompasses all uniformly bounded trading rates, for example.

| (2.12) |

(The dependence of on the initial data will be omitted when there is no ambiguity.)

2.4. Viscosity Characterization

We now want to characterize the frictional value function

| (2.13) |

If it is locally bounded, then weak dynamic programming arguments as in Bouchard and Touzi (2011) show that this value function is a (possibly discontinuous, compare (Fleming and Soner, 2006, Definition 4.2)) viscosity solution of the frictional dynamic programming equation:

Proposition 2.4.

Suppose the frictional value function is locally bounded. Then it is a (possibly discontinuous) viscosity solution of the following frictional dynamic programming equation,

| (2.14) |

for all .

Proof.

See Appendix A. ∎

Using our transversality conditions (2.12), Lemma A.2 in the appendix shows that the value function is indeed locally bounded under a condition on the model parameters, which sharpens (Garleanu and Pedersen, 2016, Lemma 1, Equation (A.27)). For constant covariance matrices , this condition is satisfied in particular if the discount rate is sufficiently small, compare Remark A.3. It also holds automatically if the transient price impact is sufficiently small or the resilience parameter is sufficiently large. This applies, in particular, in the large-liquidity regime that we turn to now.

3. Main results

3.1. Large-Liquidity Regime

Beyond linear state dynamics, the frictional dynamic programming equation (2.4) only allows to characterize the corresponding value function and optimal policy through the solution of a coupled system of nonlinear equations Garleanu and Pedersen (2016). To shed more light on the qualitative and quantitative properties of the optimal policy and its performance, we therefore perform a large-liquidity expansion around the frictionless case. To wit, we assume that i) the temporary quadratic trading cost is small, ii) the permanent price impact is small, and iii) the mean-reversion speed towards the unaffected prices is large.

To study how all three of these liquidity parameters influence the solution, we study the following “critical regime”,111111This scaling is chosen so that neither of the frictions dominates the other in the limit. If one of them would be sent to zero faster, then only the effects of the other would remain visible asymptotically. Similar “matched asymptotics” for small transaction costs and large risk aversion are studied in Barles and Soner (1998). where none of them scales out as the asymptotic parameter becomes small,121212This slight abuse of notation is made to emphasize that the matrices , , are replaced by their rescaled versions (3.1) from now on. The scaling of the permanent impact parameter and the resilience speed are reminiscent of the high-resilience asymptotics in Roch and Soner (2013); Kallsen and Muhle-Karbe (2014) which suggest that – in related models with purely transient price impact – should have an effect of the same order as .

| (3.1) |

In the large-liquidity limit , we obtain a first-order expansion of the corresponding frictional value function (Theorem 3.6) and a corresponding asymptotically optimal policy (Theorem 3.9). Before stating these results, we first introduce the regularity conditions we require for our rigorous convergence proofs as well as the quantities that appear in the leading-order approximations.

3.2. Inputs for the Expansion

Our asymptotic expansion requires the following integrability and smoothness assumptions on the market and cost parameters, which are evidently verified for the model with mean-reverting returns from Example 2.3, for example.

Assumption 3.1.

-

(i)

There exists such that for all we have

(3.2) -

(ii)

The following functions are locally bounded on ,

Similarly to Moreau et al. (2017) and Soner and Touzi (2013), the dependence of our expansion on the deviation from the Merton portfolio is described by the solution of the so-called “first corrector equation”, cf. (6.6). With our quadratic costs, this equation can be solved using an algebraic Riccati equation.131313Its explicit solution in the one-dimensional case is discussed in Section 3.5. Note that this solution and in turn our leading-order expansions do not depend on the discount rate . This time-preference parameter therefore becomes negligible for the asymptotically optimal trading rates in Theorem 3.6 and only appears as a scaling parameter in the value expansion from Theorem 3.9, compare Lemma 3.4.

Lemma 3.2.

Suppose Assumption 3.1 is satisfied and define the -valued matrices

| (3.7) |

Then, there exists such that for each the matrix-valued Riccati equation

| (3.10) |

has a maximal solution

for which the corresponding quadratic form

| (3.11) |

satisfies the following upper and lower bounds,

| (3.12) |

Proof.

See Appendix A. ∎

The last assumption for our value expansion in Theorem 3.6 is a comparison principle for a linear PDE.

Assumption 3.3.

Comparison holds for the second corrector equation

| (3.13) |

among viscosity semisolutions satisfying,

| (3.14) |

Here, the source term is:141414The linear PDE (3.13) corresponds to the “second corrector equation” of Soner and Touzi Soner and Touzi (2013); accordingly, the source term is the principal component of the value expansion (3.6).

| (3.15) |

is the (infinitesimal) quadratic variation of the Merton portfolio.

In view of the positivity of (cf. Lemma 3.2), the following probabilistic representation of the function immediately shows that it is nonnegative.

Lemma 3.4.

Proof.

See Appendix A. ∎

3.3. Value Expansion

For all , denote by and the mean-variance criterion and the value function corresponding to the asymptotic regime (3.1). We are now ready to state our first main result, the large-liquidity expansion of the frictional value function.

Theorem 3.6.

Proof.

The value expansion (3.6) has two components, one stemming from dynamic trading over time and the other one from the initial conditions of the system.

The “dynamic component” described by the function is similar to the corresponding expansions for models with only temporary trading costs. Indeed, the probabilistic representation (3.16) and (3.15) show that the frictionless target strategy only enters through its (infinitesimal) quadratic variation here, just as for models with quadratic, proportional, or fixed costs, cf. Moreau et al. (2017) and the references therein. Whence, this “portfolio gamma” or “activity rate” is the crucial sensitivity of trading strategies with respect to small frictions also in the present setting where part of their effect only wears off gradually. The quadratic variation of the Merton portfolio is multiplied by the positive-definite matrix determined from the Riccati equation (3.10). If the resilience becomes large compared to the price impact parameters and , one readily verifies that converges to the solution of the matrix equation , that is

| (3.19) |

Whence, as resilience grows, temporary trading costs become the dominant friction and recovers the factor for purely temporary quadratic costs (Moreau et al., 2017, Remarks 4.5 and 4.6).151515The same quantity also appears in a model with constant relative risk aversion, see (Guasoni and Weber, 2018, Theorem 5). The other comparative statics of this term are discussed in more detail in Section 3.5 for the one-dimensional case, where the Riccati equation (3.10) can be solved explicitly.

In addition to the dynamic component discussed so far, the value expansion (3.6) also includes several terms that depend on the initial conditions. The quadratic form is similar to its counterpart for purely temporary costs (Moreau et al., 2017, Theorem 4.3), in that it penalizes squared deviations of the initial portfolio from the frictionless optimum. Here, however, the initial distortion of the prices relative to their unaffected values also comes into play. In particular, the terms depending on the initial positions and displacements may have either a positive or a negative sign, unlike for purely temporary costs. The intuition is that a very large initial risky position may become favorable if the initial displacement is negative enough. Indeed, the mean reversion of the affected price to its unaffected value then leads to substantial extra positive returns, that may dominate the performance of the frictionless optimizer. However, these anomalies disappear if the initial price distortion is small enough.161616The initial conditions would also disappear in the long-run limit if the discounted infinite-horizon criterion (2.11) would be replaced by an ergodic goal functional as in Dumas and Luciano (1991); Gerhold et al. (2014); Guasoni and Mayerhofer (2016).

3.4. Almost-Optimal Policy

As our second main result, we now provide a family of “almost-optimal” policies that achieves the leading-order optimal performance in the value expansion (3.6). To guarantee the admissibility of these policies, the following additional assumption is required.

Assumption 3.7.

There exists such that the solution of the matrix Riccati equation (3.10) satisfies

Example 3.8.

Using the solution to the Riccati equation 3.10, we can now identify the asymptotically optimal trading speeds that track the frictionless Merton portfolio and exploit the distortion of the asset prices relative to their unaffected values.

Theorem 3.9.

Suppose the prerequisites of Theorem 3.6 and Assumption 3.7 are satisfied and the function from Lemma 3.4 is twice continuously differentiable. Define

| (3.20) |

and the feedback controls

| (3.21) |

Assume that for some ,

| (3.22) | |||

| (3.23) | |||

| (3.24) |

and the local martingale in the Itô decomposition of the approximate value function

| (3.25) |

is a true martingale for all . Then the controls are admissible and asymptotically optimal in that, locally uniformly in ,

Proof.

See Section 8. ∎

Example 3.10.

As already observed in Garleanu and Pedersen (2016), the asymptotically optimal trading rates with temporary and transient price impact strike a balance between the following two objectives. On the one hand, they track the Merton portfolio, so as to remain near the optimal risk-return tradeoff in the frictionless model. On the other hand, they exploit the distortion of the asset prices relative to their unaffected values as an additional trading signal.

The asymptotic formulas from Theorem 3.9 indentify the respective trading speeds through the matrix Riccati equation (3.10). As the resilience parameter becomes large, one readily verifies that becomes negligible, , and is given by (3.19). As a consequence, the asymptotically optimal (relative) trading speeds in this “high-resilience regime” are

as . The second formula shows that as the resilience grows, we recover the asymptotically optimal trading rate for the model with purely temporary trading costs (Moreau et al., 2017, Theorem 4.7). In particular, this tracking speed only depends on the market, preference, and cost parameters, but not the optimal trading strategy at hand.

The corresponding coefficient of the price distortion has an even simpler form in the large-resilience limit. Indeed, it is independent of permanent impact, risk aversion, and price volatility. Instead, the exploitation of the displacement only trades off its size against the temporary trading cost.171717Even though this coefficient does not vanish for , the effect of the distortion disappears in the high-resilience limit, because price distortions then disappear almost immediately.

3.5. Explicit Formulas for One Risky Asset

For a single risky asset (, the Riccati equation (3.10) can be solved explicitly. With the notation from (3.20), we obtain

As a consequence,

The last equation has one positive and one negative solution; the correct one is the positive one,

| (3.26) |

Indeed, the corresponding matrix

then is positive as required for Lemma 3.2, because both its trace and determinant are positive.

Let us first discuss the lower-right entry of this matrix, which multiplies the quadratic variation of the Merton portfolio in the leading-order term (3.16) of the value expansion (3.6). Its first summand is the corresponding term for the model with only temporary costs (Moreau et al., 2017, Formula (1.2)); whence, the second summand accounts for the additional effects of the transient price impact. Differentiation shows that this term is increasing in the permanent price impact parameter. For large resilience , the first-order expansion is

This shows that the relative adjustment compared to the model with only temporary trading costs is substantial if the ratio of permanent price impact and resilence is large compared to the temporary price impact parameter .

Next, note that the tracking speed for the frictionless Merton portfolio is always the same universal quantity

that already appears in the work of Almgren and Chriss (2001) on optimal liquidation and is also asymptotically optimal in the model without transient price impact Moreau et al. (2017).181818The same parameter also appears in more general liquidation problems Schied and Schöneborn (2009) and in linear-quadratic models with small information asymmetries, cf. Muhle-Karbe and Webster (2018). Whence, this tracking speed is not only independent of the specific application for which the frictionless target strategy is designed, but is also the same with and without transient price impact. Note that for a single risky asset, this quantity obtains for any size of the transient impact parameters.

With transient price impact, the distortion of the price relative to its unaffected value is used as an additional trading signal. The corresponding weight is , which has the second-order expansion

The first term in this expansion is the universal high-resilience limit already identified in the multi-asset case above. The second-order term in turn shows it becomes more difficult to exploit price distortions if i) permanent price impact is large (so that initial distortions are offset quickly), ii) market risk is high relative to temporary trading costs (so that the Merton portfolio is tracked closely), or iii) resilience is low (so that the distortion only decays slowly and therefore can be exploited gradually).

4. Outline of the Proof and Initial Estimates

4.1. Outline of the Proof

The proof of Theorem 3.6 is based on stability results for viscosity solutions as in Soner and Touzi (2013); Moreau et al. (2017). However, due to the presence of the price distortion, these arguments cannot be applied directly to the value function at hand here. Instead, we first study a “rescaled” version of the value function, defined in Section 4.2. We then establish an expansion for and in turn use it to derive the expansion of the actual value function .

To obtain the expansion of the rescaled value function, we first establish locally uniform bounds for in Section 4. This allows us to show in Section 5 that – the deviation of from the frictionless value scaled with an appropriate power of – admits locally bounded upper and lower semilimits and which are upper and lower semicontinuous, respectively.

In Section 6 we then establish that and (i.e, the semilimits evaluated along the frictionless versions of their state variables) are viscosity sub- and supersolutions, respectively, of the second corrector equation (3.13). Together with our estimates on , the comparison principle for (3.13) from Assumption 3.3 in turn yields for all .

4.2. The Rescaled Value Function

As liquidity becomes large in our critical regime (3.1), we expect that the price distortion tends to zero. To charaterize its limit behavior, therefore needs to be rescaled appropriately. In Lemma 4.3, we show that the natural scaling of is of order . In order to expand the value function for small , it is therefore natural to study its rescaling . However, it turns out that the asymptotic analysis of this function is severely complicated by the fact that it is not uniformly bounded from above by the frictionless value function for all arguments, e.g., if the agent starts with a large positive risky position and the initial price distortion is sufficiently negative. As a way out, we study the asymptotic expansion of the following shifted version of instead,

| (4.1) |

In Lemma 4.3, we are then able to show that is bounded from above by the frictionless value function for small . After deriving the limiting results for this function, we can then in turn deduce the expansion of the actual value function and a corresponding asymptotically optimal policy.

The viscosity property of the value function (cf. Proposition 2.4) and a direct calculation show that the rescaled value function is a (possibly discontinuous, compare (Fleming and Soner, 2006, Definition 4.2)) viscosity solution of

| (4.2) |

where

| (4.3) | ||||

| (4.4) | ||||

Here, for all and , the source term and the convex Hamiltonian are

| (4.5) | ||||

| (4.6) |

with .

Remark 4.1.

Note that as a symmetric matrix of dimension , is degenerate. One of the main technical challenges of this paper is the consequence that the Hamiltonian is degenerate in . This is not the case in Moreau et al. (2017) where the problem remains dimensional and the non-degeneracy of is a sufficient assumption to establish the viscosity property of the semilimits defined below. Here, we show that the non-degeneracy assumption of the Hamiltonian can be replaced by the existence of positive solutions for a matrix-valued Riccati equation, cf. (3.10).

4.3. A Uniform bound

In this section, we derive some elementary moment estimates for Ornstein-Uhlenbeck-type processes. These will be used to derive bounds for the semilimits introduced in Section 5 below.

Lemma 4.2.

Let , be twice continuously differentiable functions. Define the semimartingales

and the corresponding Ornstein-Uhlenbeck-type processes

and set . Then, there exists a (sufficiently large) constant such that for all and ,

| (4.7) | ||||

and

| (4.8) | ||||

Proof.

Step 1: Itô’s formula applied to and the -Young inequality show that there exists such that

for and .

Step 2: Apply Itô’s formula to and solve the ODE for , obtaining

Together with the inequality from Step 1, it follows that, for some ,

This establishes the first part of the assertion.

Step 3: As in Step 2, Itô’s formula applied to gives

Combined with the estimate from Step 1, this identity shows that, for some ,

as claimed. ∎

4.4. Expansion Along a Class of Policies

Note that the value function uses the state variable which, for , satisfies

To simplify notation, we pass to , which satisfies

| (4.9) |

We now apply Lemma A.2 in the present large-liquidity context to derive the following uniform upper bound, valid for any admissible strategy.

Lemma 4.3.

Proof.

It suffices to verify that the prerequisites of Lemma A.2 are satisfied. Whence, we need to show that the family

is bounded from below by a symmetric negative matrix for sufficiently small . Let be a matrix in this family and . Then,

Note that is constant and by Assumption 3.1(i). Hence there exists such that for all we have and

establishing the required uniform lower bound for the above family. ∎

To control the semilimits studied in Section 5 below, we define the following class of suboptimal but simple feedback controls,

| (4.10) |

For this parametric class, we have the following estimate.

Proposition 4.4.

Suppose Assumption 3.1 is satisfied and fix . Then there exists constants such that, for all and ,

| (4.11) |

Proof.

Fix a control as in (4.10) and set

Then, in matrix-vector notation, the corresponding state dynamics are

In view of (Silvester, 2000, Theorem 3), the matrix is symmetric positive definite. Thus, it is diagonalisable and can be written as

where is the diagonal matrix with entries and , The rescaled state variable

in turn has dynamics or, equivalently,

Whence, after these transformations the components of satisfy the assumptions of Lemma 4.2, so that the estimates provided there can be used to bound moments involving . To bring this to bear, we now use Lemma 4.3 to express the quantity we want to bound in terms of as follows,

| (4.13) | ||||

| (4.16) | ||||

| (4.19) |

We first use (4.7) to obtain the following bound (for a generic constant depending on ),

Similarly, using (4.8), we can control the absolute value of the last two terms of the right-hand side of (4.4) as follows ( is again a generic constant depending on ):

Together, these two estimates show that there exists a constant such that, for all sufficiently small :

Whence, the bound (4.4) is indeed satisfied. ∎

5. Semilimits

As discussed in Section 4.2, to establish the value expansion in Theorem 3.6 we study the rescaled function

| (5.1) |

As this object has no a-priori regularity, we follow Soner and Touzi (2013); Moreau et al. (2017) and consider its upper and lower semicontinuous envelopes,

and the corresponding upper and lower “semilimits”,

| (5.2) |

By definition, . In the following sections, we use viscosity techniques to establish the converse inequality. Then, the two semilimits coincide and – again by definition – also equal the actual limit (5.1) we are interested in.

The first step to carry out this program is to show that the ratio (5.1) is locally bounded, so that its upper and lower envelopes are indeed finite, upper and lower semicontinuous functions.

Proposition 5.1.

Suppose Assumption 3.1 is satisfied. Then there exists such that is locally bounded on . Hence and are upper and lower semicontinuous functions, respectively, and there exists a constant such that

Proof.

Step 1: lower bound. By Lemma 4.3, for ,

As shown in the proof of Lemma 4.3 the following matrix is positive for sufficiently small ,

Whence, the following lower bound is valid for all sufficiently small ,

By Lemma 4.2 the following convergence holds locally uniformly in as , which shows that (5.1) is indeed bounded from below:

Step 2: upper bound. We now derive an upper bound for . By definition of it is sufficient to find a family of control and such that is bounded from above by an appropriate function for all .

6. Corrector Equations

In this and the subsequent section, we show that for all we have

| (6.1) |

where is the solution of the second corrector equation from Lemma 3.4. As a consequence, the limit of (5.1) indeed exists and is given by this expression in line with the expansion from Theorem 3.6. To this end, we first establish that the semilimits, evaluated along the frictionless state variables,

| (6.2) | |||

| (6.3) |

are viscosity sub- and supersolutions, respectively, of the second corrector equation (3.13). The comparison principle for the second corrector equation (cf. Assumption 3.3) in turn implies

We then show in Section 7 that, as a function of , and are viscosity sub- and supersolutions of a first-order PDE. The equality and a comparison result for this first-order equation in turn imply that the dependence of both functions in is given by (6.1).

6.1. Notations for the Proof of the Viscosity Property

Set

| (6.4) | ||||

and define the following differential operator acting on smooth functions,

| (6.5) |

where is the dimensional Hessian matrix of corresponding to . Similarly to (Moreau et al., 2017, Definition 3.6) and (Soner and Touzi, 2013, Definition 3.1), we now define the “first corrector equation” for our expansion.

Definition 6.1.

Fix . The first corrector equation is the differential equation

| (6.6) |

where the unknown quantity is the couple and .

A direct computation shows that

for the quadratic form from (3.11). By definition of in (3.15), it in turn follows that the couple is a solution of the first corrector equation (6.6).

Also note that due to our regularity assumptions on and , the following function is locally bounded on ,

| (6.7) |

6.2. Expansion of the Generator

We now expand the generator of the PDE (4.2). To simplify notation, we set

| (6.10) |

(Generally, for vectors in or , the left superscript as in refers to the scaling factor of , whereas right superscripts indicate initial conditions .) We also define the function

| (6.11) | ||||

where denote the Jacobian matrix.

The first step of our proof is to derive an expansion of the action of the operator from (4.3) on a class of smooth functions.

Proposition 6.2.

Suppose Assumption 3.1 is satisfied and define

for smooth functions and . Then,

| (6.12) | ||||

(Here, all functions of are evaluated at and is the gradient of in .) Moreover, there exists a (sufficiently large) constant such that if the function satisfies

| (6.13) |

for some function , then

| (6.14) |

Note that the inequality (6.2) is a quantitative version of the remainder estimate in (Moreau et al., 2017, Lemma 6.1, (Ri)). It implies that from (6.2) is bounded on bounded sets of . Moreover, it shows that this remainder term converges to zero on sets of for which is bounded.

Proof of Proposition 6.2.

We first compute the required derivatives,

As a consequence,

We now prove the inequality (6.2) under the additional assumption (6.13) by dominating each of the terms in the definition (6.2) of . Here, the upper bound for follows from (6.13) and the definition of . For the remaining terms, we can dominate all terms that only depend on but not on or its derivatives by a constant multiple of . Whence it remains to estimate the following upper bound,

Taking into account the condition on , this in turn yields the desired upper bound. ∎

6.3. Viscosity Subsolution Property

The proof of viscosity properties in this section and the following requires to construct local minima or maxima. Then, we use the viscosity property of at these extrema. The construction of the extrema is classical in homogenisation theory and is similar to the proofs of (Moreau et al., 2017, Proposition 6.3 and Proposition 6.4). We therefore only outline this construction. In contrast, we give more details on how to use the viscosity property of , because the quantities that need to be controlled are more involved here. For example, the linear part of the Hamiltonian is new here and its sign needs to be controlled separately. To ease comparison to the corresponding arguments in (Moreau et al., 2017, Proposition 6.3 and Proposition 6.4), the proofs are broken up into the same steps are there.

Proposition 6.3.

Proof.

We adapt the proof of (Moreau et al., 2017, Proposition 6.3) to the present setting and keep the same steps for simplicity of reading. Let .

Consider a smooth function such that, for all ,

| (6.15) |

By the continuity of , for all there exists , such that

Recall the constant from Lemma 3.2. Similarly to (Moreau et al., 2017, Proposition 6.3), taking smaller if needed, due to the continuity of and the definition of , there exists such that with

we have

for all . (Note that the term , which is not present in (Moreau et al., 2017, Proof of Proposition 6.3), corrects a minor error in that proof.)

Step 2: Construction of a test function. Now define, for ,

and set

On and for all and ,

Indeed, if then the estimate in Lemma 3.2 gives

If , then and in turn . Moreover,

Thus there exists a local minimum of on the compact set . This is equivalent to the fact that is a local minimum of the function

where for all and ,

Denoting this minimum by .

Step 3: Boundedness of and Step 4: Control of signs. Using the viscosity supersolution property of (this is precisely the discontinuous viscosity supersolution property of ), it follows that

| (6.16) |

with and where the function is evaluated at and is evaluated at . Note that, due to the boundedness of , the fact that the second derivative of is locally bounded and Proposition 6.2, the term

is bounded. By the first corrector equation (6.6),

We also compute

As a consequence,

| (6.17) |

Note that by definition of ,

which implies that

Thus, together with (3.2), it follows that

so that the family is bounded.

Step 5: Conclude. Let be an accumulation point of this family (which might depend on ). The strict inequality (6.3) implies . In addition, the boundedness of combined with (6.3) and Proposition 6.2 gives

as . We finally use (6.3) to obtain that, for all ,

(Here, might depend on .) Using the first corrector equation (6.6) and sending to , we obtain

This establishes the claimed viscosity subsolution property. ∎

6.4. Viscosity Supersolution Property

Proposition 6.4.

Proof.

As mentioned in Remark 4.1 our Hamiltonian is degenerate and does not satisfy the non-degeneracy condition (Moreau et al., 2017, Equation 6.27) that plays a crucial role in the asymptotic analysis of the model with only temporary trading costs. We therefore outline how to modify the proof of the supersolution property in (Moreau et al., 2017, Proposition 6.4) to be able to use the non-degeneracy of our source term rather than of .

We start similarly to the subsolution property. By Proposition 5.1, is lower semicontinuous, non-negative and locally bounded. Let and smooth such that for all we have

| (6.18) |

By the continuity of , for all there exists such that

Similarly to Moreau et al. (2017), we can take small enough such that, for all ,

| (6.19) |

Step 1: Penalize . Set

By the choice of , we have

and

| (6.20) |

Similarly as in Moreau et al. (2017), define

For all , pick a function and such that

for some . We write, for all ,

and

Step 2 and 3: Construct two test functions. Now define

and – similarly to (Moreau et al., 2017, Proof of Proposition 6.4) – fix an even, smooth function satisfying

Then, for all there exist with satisying the following two properties: i) there are such that

and ii) the function

has a local minimum at .

Step 4: Boundedness of for suitable . Defining and, similarly to Moreau et al. (2017), using the discontinuous viscosity subsolution property of , it follows that the family is bounded and, up to taking a subsequence, we have the convergence as .

Step 5: Boundedness of for suitable . Using this boundedness and Proposition 6.2 similarly as in (Moreau et al., 2017, Proof of Proposition 6.4), we obtain

The definitions of and imply

As a consequence,

We can expand the left-hand side of this estimate as follows,

where is evaluated at and is evaluated at . Due to the non-degeneracy of the source term , this can be bounded from below by

The conditions on and the definition of in turn yield

Therefore, we obtain the following bound,

Note that the last term on the right-hand side goes to as . This implies that for all there exists such that, for all ,

We can now proceed as in (Moreau et al., 2017, Step 6, Proof of Proposition 6.4) to show that

which is the desired supersolution property. ∎

By combining Propositions 6.3 and 6.4 with the comparison principle from Assumption 3.3 and the upper bound for the semilimits at Proposition 5.1, we obtain the main result of this section.

Theorem 6.5.

Suppose the assumptions of Theorem 3.6 are satisfied. Then,

| (6.21) |

7. Dependence of and on

Recall the source term and the Hamiltonian from (4.5), and define

| (7.1) |

As is a second order polynomial in , the function is a smooth solution of the following first-order PDE,

| (7.2) |

The goal of this section is to prove the following result.

Proposition 7.1.

The upper and lower semilimits and from (5.2) satisfy

| (7.3) |

The converse inequality evidently holds by definition of and . Whence, Proposition 7.1 shows that all three functions are equal and depend on the initial conditions of the price distortion and the risky positions through the function . We will establish this result by first showing that the semilimits and are viscosity sub- and supersolutions, respectively, of the first-order PDE (7.2). We then conclude by proving that, under the condition (which we have already verified, cf. Theorem 6.5), this PDE admits a comparison result among non-negative semisolutions.

7.1. A First-Order Equation

We first prove that the semilimits and are viscosity sub- and supersolution of (7.2):

Lemma 7.2.

For all , the function is a viscosity subsolution of

| (7.4) |

Likewise, is a viscosity supersolution of

| (7.5) |

Proof.

We only prove the subsolution property; the supersolution property can be verified along the same lines. Consider a smooth function and such that the following strict local maximality holds,

There exists a family satisfying the following properties,

Similarly to (Moreau et al., 2017, Lemma 6.7) there are and such that the function

| (7.6) |

has a local minimum at .

For the rest of the section, we fix and omit the dependence on to ease notation. Note that the first-order equation (7.2) lacks “properness” in the sense of (Crandall et al., 1992, Page 2). To restore properness and prove a comparison result, we define the following auxiliary functions,

as well as

| (7.7) |

We also introduce the generator

| (7.8) |

Using the viscosity properties from Lemma 7.2, direct computations show that and are viscosity sub- and supersolutions of the PDE corresponding to ,

| (7.9) | |||

| (7.10) |

and is smooth solutions of the same PDE,

| (7.11) |

Moreover,

The next step is to obtain a result enabling us to compare the semisolutions and of the PDE (7.11). Note that our task here is simpler than establishing a general comparison result because the PDE admits a smooth solution . Therefore it is sufficient to obtain the following “partial comparison result” inspired by (Ekren et al., 2016, Proposition 5.3), (Ekren et al., 2014, Lemma 5.7) and (Moreau et al., 2017, Proof of Lemma 6.10):

Lemma 7.3.

There exists a partial comparison result for bounded, nonpositive viscosity semisolutions of (7.11) in the following sense. Let a bounded, lower semicontinuous, nonpositive viscosity supersolution of (7.10) and a bounded, upper semicontinuous, nonpositive viscosity subsolution of (7.9) satisfying

| (7.12) |

If either one of or is continuously differentiable with bounded derivatives then

Proof.

We focus on the case where is continuously differentiable with bounded derivatives. The other case can be treated similarly. Assume that the comparison does not hold and

Set . We proceed similarly as in (Moreau et al., 2017, Proof of Lemma 6.10) and fix , satisfying , , , and for . We can also ensure that satisfies the following non-degeneracy and monotonicity conditions,

For , define

Note that and for all . Thus, there exists such that

Note that this implies

| (7.13) |

As , up to taking a subsequence, we have

By monotonicity of in , for all we have . Hence,

and in turn

We now use the function

as a test function for at to obtain

As is a smooth subsolution of (7.9) we have

which implies

Note that one can find and such that the last two lines are bounded by

Additionally, using again the viscosity subsolution property of and its sign we find that

Combining this with (7.13) we obtain

Together with (7.13), it follows that

Hence, as . Using one more time (7.13) and the lower semicontinuity of finally yields

which is a contradiction to (7.12). Whence, comparison holds for (7.11) under this assumption as asserted. ∎

8. Asymptotically Optimal Portfolios

We now turn to the proof of our second main result, Theorem 3.9, which provides a family of asymptotically optimal policies. We first prove a general sufficient criterion for the admissibility of a certain class of trading strategies. It implies admissibility of our asymptotic optimizers and also guarantees the admissibility of the constant coefficient portfolios used to establish a lower bound for the value function in Proposition 5.1. To cover both of these applications, we consider the following class of feedback trading rates,

| (8.1) |

where is the frictionless Merton portfolio for the problem without illiquidity and are -valued functions.

Proposition 8.1.

Proof.

Recall the rescaled price distortion from (4.9) and note that, for fixed , checking the transversality conditions (2.12) for or is equivalent. Define and

With this notation,

Itô’s formula yields

| (8.8) | ||||

up to local martingale, where can be explicitly written using and whose moments can be bounded using the terms in (8.7). Taking into account the elementary estimate , it follows that

is a local supermartingale. In view of (8.7), this proces is bounded from below by an integrable process, so that it is a true supermartingale and therefore converges to a finite limit almost surely and in as . As the process is increasing and integrable by (8.7), it follows that admits a finite limit as well. Therefore,

so that the control is admissible as claimed.

To apply this result to the policies from Theorem 3.9, let

We now show that the conditions of the present proposition are satisfied for . As satisfies the Riccati equation (3.10), we have

| (8.13) | ||||

| (8.14) |

Under Assumption 3.7 and the other conditions of Theorem 3.9 and by Lemma 3.2, the matrix is positive, and satisfies as well as (8.7). Whence, the controls (3.21) are admissible by the first part of the present proposition. ∎

We now turn to the proof of the asymptotic optimality of the policies proposed in Theorem 3.9:

Proof of Theorem 3.9.

Recall the approximate value function defined in (3.18). As in Section 4.4, starting from we denote by the state controlled with the feedback strategy from (3.21). Define and

With this notation, . Itô’s formula, applied to , , and (3.25) in turn yield

Here, is defined as in (8.8) and we have used the second corrector equation (3.13) satisfied by , the Riccati equation (3.10) for , the frictionless dynamic programming equation (2.6) for , as well as Assumption 3.7. Set

which satisfies

for some constant . By Assumption (3.23), the right-hand side of this inequality tends to as , so that as .

As a consequence:

Recalling that and in turn

we finally obtain

In view of the value expansion in Theorem 3.6, the trading rates therefore indeed are asymptotically optimal as claimed. ∎

Appendix A Appendix: Additional Proofs

A.1. Additional Proofs for Section 2

The following result shows that the comparison Assumption 3.3 for the second corrector equation is satisfied for the model with mean-reverting returns from Example 2.1.

Proposition A.1.

Fix a constant . Comparison holds for the PDE

| (A.1) |

among semisolutions satisfying the following growth condition,

| (A.2) |

Proof.

The first step is to exhibit a supersolution of the equation that dominates the semisolutions satisfying the growth condition for sufficiently large arguments. To this end, let

Note that for all function satisfying (A.2), there exists a compact set such that on the complement of , holds. A computation shows

By choosing sufficiently large , we can control the terms coming from the second derivatives by and obtain

We now use the boundedness of the derivative of and take large enough to obtain

By choosing sufficiently large we can therefore guarantee that the right-hand side dominates and therefore indeed is a supersolution of (A.1).

To use this supersolution to establish comparison, argue by contradiction. If comparison does not hold, there is a subsolution and supersolution of the equation such that . One can then find small enough such that (with the supersolution constructed above) is also a supersolution of the equation satisfying .

By the growth conditions for , and , there exists a compact such that

The “doubling-of-variable method” and (Crandall et al., 1992, Theorem 3.2) (applied on ) can now be used to obtain a contradiction. ∎

Next, we sketch how the weak-dynamic programming approach of Bouchard and Touzi (2011) enables us to derive the viscosity property of the frictional value function.

Proof of Proposition 2.4.

The proof is a minor modification of (Bouchard and Touzi, 2011, Corollary 5.6), also compare (Altarovici et al., 2015, Proof of Theorem 2.1). By (Bouchard and Touzi, 2011, Remark 3.11), for all families of uniformly bounded stopping times and upper semicontinuous minorants of , the function satisfies the following weak dynamic programming principles,

| (A.3) | |||

| (A.4) | |||

As the generator of (2.14) is continuous, one can now modify the proof of (Bouchard and Touzi, 2011, Corollary 5.6) to establish that (resp. ) is a viscosity subsolution (resp. supersolution) of the frictional dynamic programming equation (2.14). This is the definition of discontinuous viscosity property for . ∎

Next, we turn to the sufficient conditions for the finiteness of the frictional value function.

Lemma A.2.

Proof.

Fix an admissible control . Note that due to our admissibility condition, the right-hand side of (A.2) is well defined; we denote it by Our objective is to use the admissibility condition to show that this quantity is equal to

We differentiate and use (2.9) and the transversality condition (2.12), obtaining

Similarly we differentiate to derive

| (A.6) |

Another application of (2.9) gives

| (A.7) | |||

| (A.8) |

Note that by definition of we have

| (A.9) |

which implies finally that

| (A.10) | |||

| (A.11) | |||

| (A.12) |

Now, take the expectation of both sides and use (2.5) to obtain

This shows that is well defined for all and (A.2) holds. We now rewrite the right-hand side of (A.2) as

Note that the last two lines in this expression correspond to the action of the matrices in on the vector . By assumption, these are bounded from above by

| (A.13) |

Moreover, together with the admissibility of , the -Young inequality yields

Notice that (A.13) allows us to bound the last term above because

This finally gives

Moreover, we obtain the upper bound

by taking the supremum over admissible controls. This concludes the proof because is finite by Assumption (2.2). ∎

Remark A.3.

The mappings and are affine and under the assumptions of Lemma A.2 the mapping is concave for all . In order to compare our result with (Garleanu and Pedersen, 2016, Lemma 1), assume that is constant. Then, Lemma A.2 provides a sufficient condition for the concavity of , which in turn yields that the frictional optimizer is unique. This sufficient condition is the positivity of the symmetric matrix

This is satisfied in particular if

| (A.14) |

which is a sharper sufficient condition than the one from (Garleanu and Pedersen, 2016, Lemma 1). In particular, (A.14) holds for sufficiently small discount rates . Note also that if goes to or goes to infinity, then this condition is satisfied.

A.2. Additional Proofs for Section 3

We first establish the properties of the solution of the Riccati equation (3.10):

Proof of Lemma 3.2.

The matrix only has strictly negative eigenvalues; thus by (Klamka, 2016, Definition 5), is stabilizable. As, moreover, is symmetric positive definite, (Ran and Vreugdenhil, 1988, Theorem 2.1) shows that there exists a maximal solution of the Riccati equation (3.10) such that all eigenvalues of are nonpositive. In addition, by (Ran and Vreugdenhil, 1988, Theorem 2.2), is symmetric positive definite.

For , define

Then, for sufficiently small and sufficiently large ,

| (A.17) |

Denote the maximal solution of the Riccati equation

(Ran and Vreugdenhil, 1988, Theorem 2.2(i)) and the inequality (A.17) imply

In view of Assumption 3.1(i), the choice of can be made uniformly for so that the lower bound in (3.12) also holds uniformly on . ∎

Next, we show that the probabilistic representation (3.16) indeed provides the unique solution of the second corrector equation under suitable assumptions:

Proof of Lemma 3.4.

We first note that the continuity of , and implies that the upper and lower semicontinuous envelopes of the generator of (3.13) coincide. Thus, the (discontinuous) viscosity property of , i.e., that is a viscosity subsolution and is a viscosity supersolution, can be established similarly as in the proof of Proposition 2.4. The comparison result from Assumption 3.3 in turn yields . Hence is indeed the unique continuous solution of (3.13) as claimed. ∎

Finally, we establish that the model with mean-reverting returns from Example 2.3 satisfies all regularity condition required for the application of Theorem 3.9. First, we consider Assumptions 3.1 and 3.3

Proof of Example 3.5.

For the model with mean-reverting returns from Example 2.3, and are constants. A direct computation shows that thanks to the boundedness of the derivatives of , there exists such that . Together with the mean reversion of , this implies for some . Thus, (3.14) becomes , for some . A comparison result for (3.13) under this growth condition is estsablished in Proposition A.1. Note that it is obvious here that the function

| (A.18) |

is a smooth solution of this PDE. Nevertheless, a comparison result for semicontinuous semisolutions of the second corrector equation as in Proposition A.1 is necessary because the upper and lower semilimits defined in Section 5 can a priori only be chracterized as viscosity semisolutions satisfying the growth condition (3.14). Hence, the comparison result from Proposition A.1 is crucial to obtain a full characterisation of these semilimits and deduce that they in fact coincide. ∎

To conclude, we discuss the other regularity conditions from Theorem 3.9:

Proof of Example 3.10.

For the model with mean-reverting returns from Example 2.3, the first integrability condition (3.22) is clearly satisfied because is constant and the squared diffusion coefficient of the frictionless Merton portfolio is bounded in this case. The limit (3.23) posits that the optimally controlled states converge to their frictionless counterparts as the frictions vanish for . This can be verified as in the proofs of Lemma 4.2 and Proposition 4.4 for any model where is constant as in Example 2.3.

In order to check (3.24) one can explicitly compute each term in the definition of and obtain that a sufficient condition for (3.24) is that, for all ,

| (A.19) |

In the context of Example 2.3, the function is bounded. Set

| (A.22) |

which satisfies by (3.10). Then, in matrix-vector notation, the corresponding state dynamics are

Itô’s formula applied to shows

A direct computation using the Riccati equation (3.10) shows that . The -Young inequality in turn yields that, for some constant ,

As a consequence, , so that has at most linear growth in ; in particular, due to the uniform lower bound (3.12) for , (3.24) holds.

To verify the martingale property in (3.25), recall that the frictionless value function is given by (2.7) and its derivative in

has at most linear growth in , and the components of are constant. Recall also the function defined in (A.18) whose derivative in can be proven to be bounded. The local martingale part in the Itô decomposition of the approximate frictional value function from (3.6) therefore is

Whence, the required square integrability of the integrands is a special case of (3.23) combined with the estimates in the second moment of . ∎

References

- (1)

- Alfonsi et al. (2010) Alfonsi, A., Fruth, A. and Schied, A. (2010), ‘Optimal execution strategies in limit order books with general shape functions’, Quant. Finance 10(2), 143–157.

- Almgren and Chriss (2001) Almgren, R. F. and Chriss, N. (2001), ‘Optimal execution of portfolio transactions’, J. Risk 3, 5–40.

- Almgren and Li (2016) Almgren, R. F. and Li, T. M. (2016), ‘Option hedging with smooth market impact’, Market Microstucture Liq. 2(1), 1650002.

- Altarovici et al. (2015) Altarovici, A., Muhle-Karbe, J. and Soner, H. M. (2015), ‘Asymptotics for fixed transaction costs’, Finance Stoch. 19(2), 363–414.

- Bank et al. (2017) Bank, P., Soner, H. M. and Voß, M. (2017), ‘Hedging with temporary price impact’, Math. Finan. Econ. 11(2), 215–239.

- Bank and Voß (2018) Bank, P. and Voß, M. (2018), ‘Linear quadratic stochastic control problems with singular stochastic terminal constraint’, SIAM J. Control Optim. 56(2), 672–699.

- Barles and Soner (1998) Barles, G. and Soner, H. M. (1998), ‘Option pricing with transaction costs and a nonlinear black-scholes equation’, Finance Stoch. 2(4), 369–397.

- Bertsimas and Lo (1998) Bertsimas, D. and Lo, A. W. (1998), ‘Optimal control of execution costs’, J. Finan. Markets 1(1), 1–50.

- Bichuch (2014) Bichuch, M. (2014), ‘Pricing a contingent claim liability using asymptotic analysis for optimal investment in finite time with transaction costs’, Finance Stoch. 18(3), 651–694.

- Bouchard and Touzi (2011) Bouchard, B. and Touzi, N. (2011), ‘Weak dynamic programming principle for viscosity solutions’, SIAM J. Control Optim. 49(3), 948–962.

- Bouchaud et al. (2004) Bouchaud, J.-P., Gefen, Y., Potters, M. and Wyart, M. (2004), ‘Fluctuations and response in financial markets: the subtle nature of ‘random’ price changes’, Quant. Finance 4(2), 176–190.

- Bouchaud et al. (2006) Bouchaud, J.-P., Kockelkoren, J. and Potters, M. (2006), ‘Random walks, liquidity molasses and critical response in financial markets’, Quant. Finance 6(2), 115–123.

- Cai et al. (2017a) Cai, J., Rosenbaum, M. and Tankov, P. (2017a), ‘Asymptotic lower bounds for optimal tracking: a linear programming approach’, Ann. Appl. Probab. 27(4), 2455–2514.

- Cai et al. (2017b) Cai, J., Rosenbaum, M. and Tankov, P. (2017b), ‘Asymptotic optimal tracking: feedback strategies’, Stochastics 89(6-7), 943–966.

- Cartea and Jaimungal (2016) Cartea, Á. and Jaimungal, S. (2016), ‘A closed-form execution strategy to target volume weighted average price’, SIAM J. Finan. Math. 7(1), 760–785.

- Collin-Dufresne et al. (2012) Collin-Dufresne, P., Daniel, K., Moallemi, C. and Saglam, M. (2012), Strategic asset allocation in the presence of transaction costs. Preprint.

- Crandall et al. (1992) Crandall, M., Ishii, H. and Lions, P. (1992), ‘User’s guide to viscosity solutions of second order partial differential equations’, Bull. Amer. Math. Soc. (N.S.) 27(1), 1–67.

- De Lataillade et al. (2012) De Lataillade, J., Deremble, C., Potters, M. and Bouchaud, J.-P. (2012), ‘Optimal trading with linear costs’, J. Investment Strat. 1(3), 91–115.

- Dumas and Luciano (1991) Dumas, B. and Luciano, E. (1991), ‘An exact solution to a dynamic portfolio choice problem under transactions costs’, J. Finance 46(2), 577–595.

- Ekren et al. (2014) Ekren, I., Keller, C., Touzi, N. and Zhang, J. (2014), ‘On viscosity solutions of path dependent PDEs’, Ann. Probab. 42(1), 204–236.

- Ekren et al. (2016) Ekren, I., Touzi, N. and Zhang, J. (2016), ‘Viscosity solutions of fully nonlinear parabolic path dependent PDEs: Part I’, Ann. Probab. 44(2), 1212–1253.

- Feodoria (2016) Feodoria, M. R. (2016), Optimal investment and utility indifference pricing in the presence of small fixed transaction costs, PhD thesis, Christian-Albrechts-Universität zu Kiel.

- Fleming and Soner (2006) Fleming, W. H. and Soner, H. M. (2006), Controlled Markov processes and viscosity solutions, second edn, Springer, New York.

- Garleanu and Pedersen (2013) Garleanu, N. and Pedersen, L. H. (2013), ‘Dynamic trading with predictable returns and transaction costs’, J. Finance 68(6), 2309–2340.

- Garleanu and Pedersen (2016) Garleanu, N. and Pedersen, L. H. (2016), ‘Dynamic portfolio choice with frictions’, J. Econ. Theory 165, 487–516.

- Gatheral (2010) Gatheral, J. (2010), ‘No-dynamic-arbitrage and market impact’, Quant. Finance 10(7), 749–759.

- Gatheral and Schied (2013) Gatheral, J. and Schied, A. (2013), Dynamical models of market impact and algorithms for order execution, in J.-P. Fouque and J. A. Langsam, eds, ‘Handbook of systemic risk’, Cambridge University Press, Barcelona, pp. 579–599.

- Gerhold et al. (2014) Gerhold, S., Guasoni, P., Muhle-Karbe, J. and Schachermayer, W. (2014), ‘Transaction costs, trading volume, and the liquidity premium’, Finance. Stoch. 18(1), 1–37.

- Grinold (2006) Grinold, R. (2006), ‘A dynamic model of portfolio management’, J. Invest. Manag. 4(2), 5–22.

- Guasoni and Mayerhofer (2016) Guasoni, P. and Mayerhofer, E. (2016), The limits of leverage. Math. Finance, to appear.

- Guasoni and Muhle-Karbe (2015) Guasoni, P. and Muhle-Karbe, J. (2015), ‘Long horizons, high risk aversion, and endogenous spreads’, Math. Finance 25(4), 724–753.

- Guasoni and Weber (2015) Guasoni, P. and Weber, M. (2015), Nonlinear price impact and portfolio choice. Preprint.

- Guasoni and Weber (2017) Guasoni, P. and Weber, M. (2017), ‘Dynamic trading volume’, Math. Finance 27(2), 313–349.

- Guasoni and Weber (2018) Guasoni, P. and Weber, M. (2018), ‘Rebalancing multiple assets with mutual price impact’, J. Optimiz. Theory Appl. 179(2), 618–653.

- Guéant and Pu (2017) Guéant, O. and Pu, J. (2017), ‘Option pricing and hedging with execution costs and market impact’, Math. Finance 27(3), 803–831.

- Herdegen and Muhle-Karbe (2018) Herdegen, M. and Muhle-Karbe, J. (2018), ‘Stability of Radner equilibria with respect to small frictions’, Finance Stoch. 22(2), 443–502.

- Janeček and Shreve (2004) Janeček, K. and Shreve, S. E. (2004), ‘Asymptotic analysis for optimal investment and consumption with transaction costs’, Finance. Stoch. 8(2), 181–206.

- Kallsen (2002) Kallsen, J. (2002), ‘Derivative pricing based on local utility maximization’, Finance Stoch. 6(1), 115–140.

- Kallsen and Li (2015) Kallsen, J. and Li, S. (2015), Portfolio optimization under small transaction costs: a convex duality approach. Preprint.

- Kallsen and Muhle-Karbe (2014) Kallsen, J. and Muhle-Karbe, J. (2014), High-resilience limits for block-shaped order books. Preprint.

- Kallsen and Muhle-Karbe (2017) Kallsen, J. and Muhle-Karbe, J. (2017), ‘The general structure of optimal investment and consumption with small transaction costs’, Math. Finance 27(3), 659–703.

- Klamka (2016) Klamka, J. (2016), ‘Controllability of dynamical systems’, Mathematica Applicanda 36(50/09), 57–75.

- Korn (1998) Korn, R. (1998), ‘Portfolio optimisation with strictly positive transaction costs and impulse control’, Finance. Stoch. 2(2), 85–114.

- Liu (2004) Liu, H. (2004), ‘Optimal consumption and investment with transaction costs and multiple risky assets’, J. Finance 59(1), 289–338.

- Martin (2014) Martin, R. (2014), ‘Optimal trading under proportional transaction costs’, RISK August, 54–59.

- Martin and Schöneborn (2011) Martin, R. and Schöneborn, T. (2011), ‘Mean reversion pays, but costs’, RISK February, 96–101.

- Melnyk and Seifried (2018) Melnyk, Y. and Seifried, F. T. (2018), ‘Small-cost asymptotics for long-term growth rates in incomplete markets’, Math. Finance 28(2), 668–711.

- Moreau et al. (2017) Moreau, L., Muhle-Karbe, J. and Soner, H. M. (2017), ‘Trading with small price impact’, Math. Finance 27(2), 350–400.

- Muhle-Karbe and Webster (2018) Muhle-Karbe, J. and Webster, K. (2018), ‘Information and inventories in high-frequency trading’, Market Microstructure Liq. 3(2), 1750010.

- Obizhaeva and Wang (2013) Obizhaeva, A. A. and Wang, J. (2013), ‘Optimal trading strategy and supply/demand dynamics’, J. Finan. Markets 16(1), 1–32.

- Possamaï et al. (2015) Possamaï, D., Soner, H. M. and Touzi, N. (2015), ‘Homogenization and asymptotics for small transaction costs: the multidimensional case’, Comm. Part. Diff. Eq. 40(11), 2005–2046.

- Predoiu et al. (2011) Predoiu, S., Shaikhet, G. and Shreve, S. E. (2011), ‘Optimal execution in a general one-sided limit-order book’, SIAM J. Finan. Math. 2(1), 183–212.

- Ran and Vreugdenhil (1988) Ran, A. and Vreugdenhil, R. (1988), ‘Existence and comparison theorems for algebraic riccati equations for continuous-and discrete-time systems’, Linear Algebra Appl. 99, 63–83.

- Roch and Soner (2013) Roch, A. and Soner, H. M. (2013), ‘Resilient price impact of trading and the cost of illiquidity’, Int. J. Theor. Appl. Finance 16(6), 1350037.

- Schied and Schöneborn (2009) Schied, A. and Schöneborn, T. (2009), ‘Risk aversion and the dynamics of optimal liquidation strategies in illiquid markets’, Finance. Stoch. 13(2), 181–204.

- Shreve and Soner (1994) Shreve, S. E. and Soner, H. M. (1994), ‘Optimal investment and consumption with transaction costs’, Ann. Appl. Probab. 4(3), 609–692.

- Silvester (2000) Silvester, J. R. (2000), ‘Determinants of block matrices’, Math. Gazette 84(501), 460–467.

- Soner and Touzi (2013) Soner, H. M. and Touzi, N. (2013), ‘Homogenization and asymptotics for small transaction costs’, SIAM J. Control Optim. 51(4), 2893–2921.

- Whalley and Wilmott (1997) Whalley, A. E. and Wilmott, P. (1997), ‘An asymptotic analysis of an optimal hedging model for option pricing with transaction costs’, Math. Finance 7(3), 307–324.