1920171233776

Lattice paths with catastrophes

Abstract

In queuing theory, it is usual to have some models with a “reset” of the queue. In terms of lattice paths, it is like having the possibility of jumping from any altitude to zero. These objects have the interesting feature that they do not have the same intuitive probabilistic behaviour as classical Dyck paths (the typical properties of which are strongly related to Brownian motion theory), and this article quantifies some relations between these two types of paths. We give a bijection with some other lattice paths and a link with a continued fraction expansion. Furthermore, we prove several formulae for related combinatorial structures conjectured in the On-Line Encyclopedia of Integer Sequences. Thanks to the kernel method and via analytic combinatorics, we provide the enumeration and limit laws of these “lattice paths with catastrophes” for any finite set of jumps. We end with an algorithm to generate such lattice paths uniformly at random.

keywords:

Lattice path, generating function, algebraic function, kernel method, context-free grammar, random generation1 Introduction

Lattice paths are a natural model in queuing theory: indeed, the evolution of a queue can be seen as a sum of jumps, a subject e.g. considered in Feller (1968). In this article we consider jumps restricted to a given finite set of integers J, where each jump is associated with a weight (or probability) . The evolution of a queue naturally corresponds to lattice paths constrained to be non-negative. For example, if , this corresponds to the so-called Dyck paths dear to the heart of combinatorialists. Moreover, we also consider the model where “catastrophes” are allowed.

Definition 1.1.

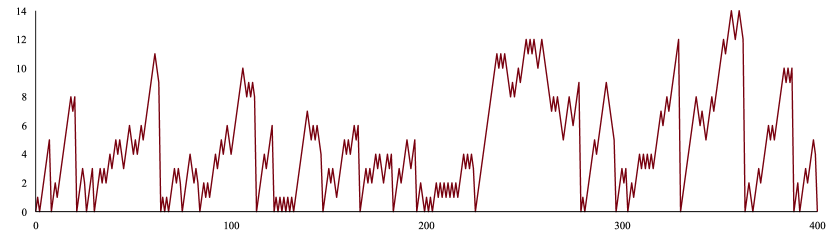

A catastrophe is a jump from an altitude () to altitude , see Figure 1.

Such a jump corresponds to a “reset” of the queue. The model of queues with catastrophes was e.g. considered in Krinik, Rubino, Marcus, Swift, Kasfy, and Lam (2005) and Krinik and Mohanty (2010), which list many other references. In financial mathematics, this also gives a natural, simple model of the evolution of stock markets, allowing bankruptcies at any time with a small probability (for the analysis and the applications of related discrete models, see e.g. Schoutens (2003), Elliott and Kopp (2005)). In probability theory and statistical mechanics, it was also considered under the name “random walks with resetting”, see e.g. Kusmierz, Majumdar, Sabhapandit, and Schehr (2014). It is also related to random population dynamics, see e.g. Ben-Ari, Roitershtein, and Schinazi (2017), to the random the Poland–Scheraga model for DNA denaturation, as analysed by Harris and Touchette (2017), or to Markov chains with restarts, as studied by Janson and Peres (2012).

Link with a continued fraction. We first start with the observation that the generating function of Dyck paths with catastrophes ending at altitude has the following continued fraction expansion:

| (1) |

We give two proofs of this phenomenon in Theorem 3.1. In this article, we also tackle the question of what happens for more general sets of jumps than , and we provide the enumeration and asymptotics of the corresponding number of lattice paths under several constraints.

Link with generating trees. In combinatorics, such lattice paths are related to generating trees, which are a convenient tool to enumerate and generate many combinatorial structures in some incremental way (like e.g. permutations avoiding some pattern), see e.g. West (1996). In such trees, the distribution of the children of each node follows exactly the same dynamics as lattice paths with some “extended” jumps, as was intensively investigated by the Florentine school of combinatorics, e.g. in Barcucci, Del Lungo, Pergola, and Pinzani (1999), Duchi, Fédou, and Rinaldi (2004), Ferrari, Pergola, Pinzani, and Rinaldi (2011). For example, these “extended” jumps can be a continuous set of jumps: from altitude , one can jump to any altitude between and , possibly with some weights, plus a finite set of bounded jumps. This model can be seen as an intermediate model between Dyck paths and our lattice paths with catastrophes; we investigated it in our series of articles Banderier, Bousquet-Mélou, Denise, Flajolet, Gardy, and Gouyou-Beauchamps (2002), Banderier (2002), Banderier and Merlini (2003), Banderier, Fédou, Garcia, and Merlini (2003). In this article, we will, however, see that several statistics of lattice paths with catastrophes behave in a rather different way than these walks with a continuous set of jumps, even if they share the following unusual property: both of them correspond to random walks with an “infinite negative drift” (in fact, a space-dependent drift tending to when the altitude increases). At the same time, they are constrained to remain at non-negative altitudes; this leads to some counter-intuitive behaviour: unlike classical directed lattice paths, the limiting object is no more directly related to Brownian motion theory.

Enumeration and asymptotics: why context-free grammars would be a wrong idea here. One way to analyse our lattice paths could be to use a context-free grammar approach, see Labelle and Yeh (1990): this leads to a system of algebraic equations, and therefore we already know “for free” that the corresponding generating functions are algebraic. However, this system involves nearly equations (where is the largest negative jump and the largest positive jump), so solving it (with resultants or Gröbner bases) leads to computations taking a lot of time and memory (a bit complexity exponential in ): even for , the needed memory to compute the algebraic equation with this method would be more than the expected number of particles in the universe! Another drawback of this method is that it would be a “case-by-case” analysis: for each new set of jumps, one would have to do new computations from scratch. Hence, with this method, there is no way to access “universal” asymptotic results: while it is well known that the coefficients of algebraic functions exhibit an asymptotic behaviour of the type , only the “critical exponent” can be proven to belong to a specific set (see Banderier and Drmota (2015)). What is more, there is no hope to have easy access to and with this context-free grammar approach, in a way which is independent of a case-by-case computation (which, what is more, would be impossible for ).

The solution: kernel method and analytic combinatorics. In this article, we offer an alternative to context-free grammars. Our approach uses methods of analytic combinatorics for directed lattice paths: the kernel method and singularity analysis, as presented in Banderier and Flajolet (2002), Flajolet and Sedgewick (2009). It allows us to get exact enumeration, the typical behaviour of lattice paths with catastrophes, and has the advantage of offering universal results for the asymptotics as well as generic closed forms, whatever the set of jumps is.

Plan of this article. First, in Section 2, we present the model of walks with catastrophes and derive their generating functions. In Section 3, we establish a bijection between two generalizations of Dyck paths. In Section 4, we analyse our model in more detail and first derive the asymptotic number of excursions and meanders. Then we use these results to obtain limit laws for the number of catastrophes, the number of returns to zero, the final altitude, the cumulative size of catastrophes, the average size of a catastrophe, and the waiting time for the first catastrophe (see Figures 2 and 3). In Section 5, we discuss the uniform random generation of such lattice paths. In Section 6, we summarize our results and mention some possible extensions.

2 Generating functions

In this section, we give some explicit formulae for the generating functions of non-negative lattice paths with catastrophes. We consider the set of jumps where a weight is attached to each jump and we associate to this set of jumps the following jump polynomial:

| (2) |

Every catastrophe is also assigned a weight . The weight of a lattice path is the product of the weights of its jumps. The weights and are real and non-negative: in fact, even if they would be taken from , our enumerative formulae would remain valid. The non-negativity of the weights or the fact that and only play a role for establishing the universal asymptotic phenomena presented in Section 4.

The generating functions of directed lattice paths can be expressed in terms of the roots , , of the kernel equation

| (3) |

More precisely, this equation has solutions. The small roots are the solutions with the property for . The remaining solutions are called large roots as they satisfy for . The generating functions of four classical types of lattice paths are shown in Table 1.

| ending anywhere | ending at | |

|---|---|---|

![[Uncaptioned image]](/html/1707.01931/assets/x4.png) |

![[Uncaptioned image]](/html/1707.01931/assets/x5.png) |

|

| unconstrained | ||

| (on ) | ||

| walk/path () | bridge () | |

![[Uncaptioned image]](/html/1707.01931/assets/x6.png) |

![[Uncaptioned image]](/html/1707.01931/assets/x7.png) |

|

| constrained | ||

| (on ) | ||

| meander () | excursion () | |

These results follow from the expression for the bivariate generating function of meanders, see Bousquet-Mélou and Petkovšek (2000) and Banderier and Flajolet (2002) : Let be the number of meanders of length going from altitude to altitude , then

| (4) |

This formula is obtained by the kernel method: Starting from (3), it consists in setting in the functional equation which mimics the recursive definition of a meander. This results in new and simpler equations which lead to the closed form (4). The generating function of excursions is .

Let us now investigate which perturbation is introduced by allowing catastrophes in this model. First, we partition the set of jumps into the set of positive jumps ( iff111“iff” is Paul Halmos’ convenient abbreviation of “if and only if”. ), the set of negative jumps ( iff ), and the possible zero jump ( iff ).

Theorem 2.1 (Generating functions for lattice paths with catastrophes).

Let be the number of meanders with catastrophes of length from altitude to altitude . Then the generating function is algebraic and satisfies

| (5) | ||||

| (6) |

where is the generating function of excursions ending with a catastrophe, , and where, for any set of jumps encoded by , the ’s and the ’s are the small roots and the large roots of the kernel equation (3).

Proof.

Take an arbitrary non-negative path of length . Let be the last time it returns to the -axis with a catastrophe (or if the path contains no catastrophe). This point gives a unique decomposition into an initial excursion which ends with a catastrophe (this might be empty), and a meander without any catastrophes. This directly gives (5).

What remains is to describe the initial part . Consider an arbitrary excursion ending with a catastrophe. We decompose it with respect to its catastrophes, into a sequence of paths having only one catastrophe at their very end and none before, which we count by . Thus,

| (7) |

Because of Definition 1.1 of a catastrophe, is given by the generating function of meanders that are neither excursions nor meanders ending at altitudes () followed by a final catastrophe. This implies the shape of : . ∎

Remark 2.2.

Our results depend on the choice of Definition 1.1 of catastrophes. Some slightly different definitions could be used without changing their structure. For example, one could consider allowing catastrophes from any altitude (in this case, ). In order to ensure an easy adaptation to different models, we will state all our subsequent results in terms of a generic .

Let us now consider a famous class of lattice paths (see e.g. Stanley (2011)), which we call in this article “classical” Dyck paths.

Definition 2.3.

A Dyck meander is a path constructed from the possible jumps and , each with weight , and being constrained to stay weakly above the -axis. A Dyck excursion is additionally constrained to return to the -axis. Accordingly, the polynomial encoding the allowed jumps is .

For these paths, when one also allows catastrophes of weight , one gets the following generating functions.

Corollary 2.4 (Generating functions for Dyck paths with catastrophes).

The generating function of Dyck meanders with catastrophes, , satisfies

where the small root of the kernel is in fact the generating functions of Catalan numbers: . Moreover, is also the number of equivalence classes of Dyck excursions of length for the pattern duu, see OEIS A274115222Such references are links to the web-page dedicated to the corresponding sequence in the On-Line Encyclopedia of Integer Sequences, http://oeis.org..

The generating function of Dyck excursions with catastrophes, , is

This sequence corresponds to OEIS A224747. Moreover, is also the number of Dumont permutations of the first kind of length avoiding the patterns 1423 and 4132, see OEIS A125187.

Proof.

The formulae for and are a direct application of Theorem 2.1. Then one notes that equals the generating function of Dumont permutations of the first kind of length avoiding the patterns 1423 and 4132, see Burstein (2005) for the definition of such permutations, and the derivation of their generating function. In Manes, Sapounakis, Tasoulas, and Tsikouras (2016), two Dyck excursions are said to be equivalent if they have the same length and all occurrences of the pattern duu are at the same places. They derived the generating function for the number of equivalence classes, which appears to be equal to . ∎

In the next section we will analyse Dyck paths with catastrophes in more detail. On the way we solve some conjectures of the On-Line Encyclopedia of Integer Sequences.

3 Bijection for Dyck paths with catastrophes

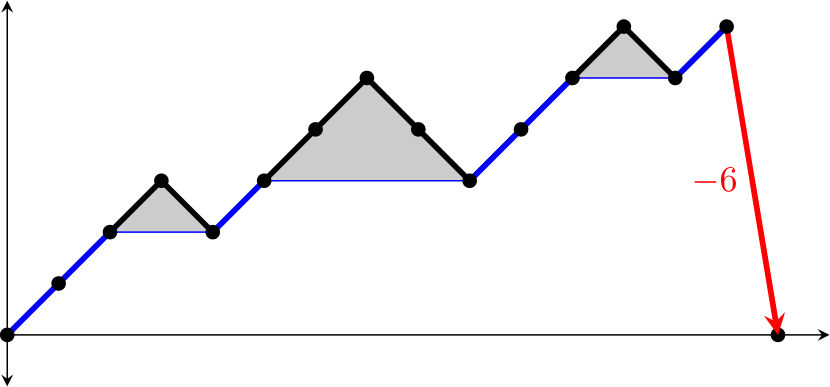

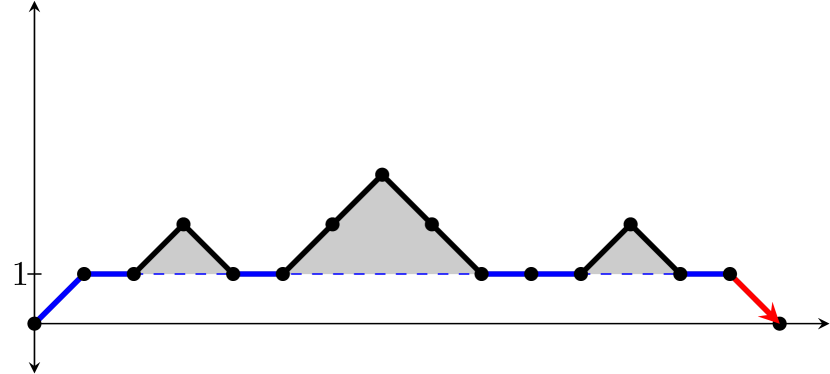

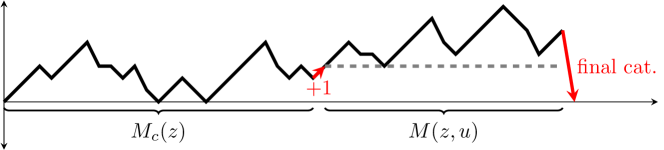

The goal of this section is to establish a bijection between two classes of extensions of Dyck paths333We thus prove several conjectures by Alois P. Heinz, R. J. Mathar, and other contributors in the On-Line Encyclopedia of Integer Sequences, see sequences A224747 and A125187 therein.. We consider two extensions of classical Dyck paths (see Figure 4 for an illustration):

-

1.

Dyck paths with catastrophes are Dyck paths with the additional option of jumping to the -axis from any altitude ; and

-

2.

-horizontal Dyck paths are Dyck paths with the additional allowed horizontal step at altitude .

Theorem 3.1 (Bijection for Dyck paths with catastrophes).

The number of Dyck paths with catastrophes of length is equal to the number of -horizontal Dyck paths of length :

Proof.

A first proof that follows from a continued fraction approach: Each level of the continued fraction encodes the non-negative jumps starting from altitude and the negative jumps going to altitude (see e.g. Flajolet (1980)). The jumps and translate into in Equation (8) below. At altitude , a horizontal jump is also allowed; this translates into the term in the continuous fraction. We thus get the continued fraction of Equation (1). Simplifying its periodic part, we get

| (8) |

where is the generating function of classical Dyck paths, . One then gets that equals the closed form of given in Corollary 2.4. We now give a bijective procedure which transforms every Dyck path with catastrophes into a -horizontal Dyck path, and vice versa.

Every Dyck path with catastrophes can be decomposed into a sequence of arches, see Figure 1. There are two types of arches: arches ending with catastrophes and arches ending with a jump given by . This gives the alternative decomposition to (6) illustrated in Figure 1:

Thus, without loss of generality, we continue our discussion only for arches. The following procedure is visualized in Figure 4.

Let us start with an arbitrary arch of Dyck paths with catastrophes. It is either a classical Dyck path, and therefore also a -horizontal Dyck path, or it ends with a catastrophe of size . First, we associate the catastrophe with up steps . Specifically, we draw horizontal lines to the left until we hit an up step. All but the first one are replaced by horizontal steps. Finally, we replace the catastrophe by a down step . All parts in between stay the same. Note that we replaced up steps, and therefore decreased the altitude by , but we also replaced the catastrophe of size by a down step, which represents a gain of altitude by . Thus, we again return to the -axis. Furthermore, all horizontal steps are at altitude . Thus, we always stay weakly above the -axis, and we got an arch of a -horizontal Dyck path. The inverse mapping is analogous. ∎

The most important building blocks in the previous bijection were arches ending with a catastrophe. Let us note that these can be enumerated by an explicit formula.

Proposition 3.2 (Dyck arches ending with a catastrophe).

Let be the generating function of arches ending with a catastrophe. Then one has the following closed forms

where and are the generating functions of classical Dyck paths for meanders, excursions, and meanders ending at , respectively, see OEIS A037952.

Proof.

Every excursion ending with a catastrophe can be uniquely decomposed into an initial excursion and a final arch with a catastrophe. By Theorem 2.1 we get the generating function of .

In order to compute , additionally drop the initial up-jump which is necessary for all such arches of positive length. The remaining part is a Dyck meander (always staying weakly above the -axis) that does not end on the -axis. Thus,

where denotes the Iverson bracket, which is if the condition is true, and otherwise. ∎

4 Asymptotics and limit laws

The natural model in which all paths of length have the same weight creates a probabilistic model in which the drift of the walk is then space-dependent: it converges to minus infinity when the altitude of the paths is increasing. So, unlike the easier classical Dyck paths (and their generalization via directed lattice paths, having a finite set of given jumps), we are losing the intuition offered by Brownian motion theory. This leads to the natural question of what the asymptotics of the fundamental parameters of our “lattice paths with catastrophes” are. This is the question we are going to answer now.

To this aim, some useful results of Banderier and Flajolet (2002) are the asymptotic enumeration formulae for the four types of paths shown in Table 1. A key result is the fact that the principal small root and the principal large root of the kernel equation (3) are conjugated to each other at their dominant singularity , where is the minimal real positive solution of . In particular, it holds that

with the constant . This singularity of and turns out to be the dominant singularity of the generating functions of directed lattice paths.

We refer to Flajolet and Sedgewick (2009) for the notion of dominant singularity and a clear presentation of its fundamental role in the asymptotics of the coefficients of a generating function. It could be the case that the generating functions have several dominant singularities. This happens when one has a periodicity in the support of the jump polynomial .

Definition 4.1.

We say that a function has periodic support of period or (for short) is -periodic if there exists a function and an integer such that . If this holds only for , the function is said to be aperiodic.

In Banderier and Wallner (2017a, Lemma 8.7 and Theorem 8.8) we show how to deduce the asymptotics of walks having periodic jump polynomials from the results on aperiodic ones. Therefore, without loss of generality we consider only the aperiodic jump polynomials in this article.

4.1 Asymptotic number of lattice paths

Because of its key role in the expression given in Theorem 2.1, we start by analysing the function . In particular, we need to find its singularities, which are given by the behaviour of

Caveat: Even if we already know that the radii of convergence of , it is a priori not granted that does not have a larger radius of convergence (some cancellations could occur). In fact, the results of Banderier and Flajolet (2002) allow us to prove that no such cancellations occur here via the asymptotics of the coefficients of and . Therefore the radius of convergence of is .

We now determine the radius of convergence of .

Lemma 4.2 (Radius of convergence of ).

Let be the set of zeros of of minimal modulus with . This set is either empty or has exactly one real positive element which we call . The sign of the drift of the walk dictates the location of the radius of convergence :

-

•

If , we have .

-

•

If , it also depends on the value :

Proof.

As is a generating function with positive coefficients, Pringsheim’s theorem implies that it has a dominant singularity on the real positive axis, which we call . This singularity is either , the singularity of , or it is the smallest real positive zero of (if it exists, it is denoted by and it is therefore such that ).

What is more, has no other dominant singularity: When this follows from the aperiodicity of , and proven in Banderier and Flajolet (2002). When this follows from the strong triangle inequality. Indeed, as has non-negative coefficients and is aperiodic, one has for any , .

It remains to determine the location of the singularity. The functions and are analytic for , whereas the behaviour of depends on the drift . For it possesses a simple pole at , i.e. . Thus, , and together with this implies that there is a solution .

For we have that is bounded for , and we have . Thus, for a fixed jump polynomial any case can be attained by a variation of . As is monotonically increasing on the real axis, it suffices to compare its value at its maximum . ∎

Note that strongly depends on the weight of the catastrophes . Therefore, for a fixed step set with negative drift one can obtain any of the three possible cases by a proper choice of .

Theorem 4.3 (Asymptotics of excursions ending with a catastrophe).

Let be the number of excursions ending with a catastrophe. The asymptotics of depend on the structural radius and the possible singularity :

where is given by the Puiseux expansion of for . The last two cases occur only when .

Proof.

The critical exponent in the Puiseux expansion of in for or , respectively, satisfies

-

•

if ,

-

•

if ,

-

•

if does not exist.

Indeed, the singularity of arises at the minimum of and , as derived in Lemma 4.2. In the first case , the singularity is a simple pole as the first derivative of the denominator at is strictly positive. We get for

| (9) |

This yields a simple pole at for and singularity analysis then gives the asymptotics of .

If does not exist, or if , we get a square root behaviour for

| (10) |

For the constant term is , and we get for

| (11) |

Yet, if does not exist, the constant term does not vanish. This gives for

| (12) |

Applying singularity analysis yields the result. ∎

With the help of the last result we are able to derive the asymptotic number of lattice paths with catastrophes. Let us state the result for excursions next.

Theorem 4.4 (Asymptotics of excursions with catastrophes).

The number of excursions with catastrophes is asymptotically equal to

Proof.

Next we also state the asymptotic number of meanders. The only difference is the appearance of instead of , and a factor instead of in the first term when does not exist.

Theorem 4.5 (Asymptotics of meanders with catastrophes).

The number of meanders with catastrophes is asymptotically equal to

Proof.

Remark 4.6.

In the previous proofs we needed that is an aperiodic jump set. Otherwise, the generating function does not have a unique singularity on its circle of convergence, but several. In such cases one needs to consider all singularities and sum their contributions; however, this can lead to cancellations, thus extra care is necessary. A systematic approach of the periodic cases is treated in Banderier and Wallner (2017a). These considerations about periodicity are only necessary when the dominant asymptotics come from the singularity , while when , we have a unique dominant simple pole (the possibly periodic functions and do not contribute to the asymptotics). This polar behaviour occurs e.g. for Dyck paths.

Corollary 4.7.

The number of Dyck paths with catastrophes and Dyck meanders with catastrophes are respectively asymptotically equal to

where

is the unique positive root of .

Proof.

Remark 4.8.

It is one of the surprising behaviours of Dyck paths with catastrophes: they involve algebraic quantities of degree ; this was quite counter-intuitive to predict a priori, as Dyck path statistics usually involve by design algebraic quantities of degree .

As a direct consequence of the last two theorems, we observe that our walks with catastrophes have the feature that excursions and meanders have the same order of magnitude: , whereas it is often for other classical models of lattice paths. In probabilistic terms this means that the set of excursions is not a null set with respect to the set of meanders. We quantify more formally this claim in the following corollary.

Corollary 4.9 (Ratio of excursions).

The probability that a meander with catastrophes of length is in fact an excursion is equal to

For Dyck walks, this gives (meander of length is an excursion) .

In the next sections, we will need the following variant of the supercritical composition scheme from Flajolet and Sedgewick (2009, Proposition IX.6), in which we add a perturbation function . In the following, we denote by the radius of convergence of a function .

Proposition 4.10 (Perturbed supercritical composition).

Consider a combinatorial structure constructed from components according to the bivariate composition scheme . Assume that and satisfy the supercriticality condition , that is analytic in for some , with a unique dominant singularity at , which is a simple pole, and that is aperiodic. Furthermore, let be analytic for . Then the number of -components in a random -structure of size , corresponding to the probability distribution has a mean and variance that are asymptotically proportional to ; after standardization, the parameter satisfies a limiting Gaussian distribution, with speed of convergence .

Proof.

As is analytic at the dominant singularity, it contributes only a constant factor to the asymptotics. Then Hwang’s quasi-power theorem, see Flajolet and Sedgewick (2009, Theorem IX.8), gives the claim. ∎

A simple (and useful) application of this result in the context of sequences leads to:

Proposition 4.11 (Perturbed supercritical sequences).

Consider a sequence scheme that is supercritical, i.e., the value of at its dominant positive singularity satisfies . Assume that is aperiodic, , and is analytic for , where is the positive root of . Then the number of -components in a random -structure of size is, after standardization, asymptotically Gaussian with444The formula for the asymptotics of in Flajolet and Sedgewick (2009, Proposition IX.7) contains some typos and misses the -factors in the numerator and one in the denominator.

What is more, the number of components of some fixed size is asymptotically Gaussian with asymptotic mean , where .

Proof.

The proof follows exactly the same lines as Flajolet and Sedgewick (2009, Proposition IX.7). We state it for completeness. The first part is a direct consequence of Proposition 4.10 with and replaced by . The second part results from the bivariate generating function

and from the fact that close to induces a smooth perturbation of the pole of at , corresponding to . ∎

4.2 Average number of catastrophes

In Theorem 2.1 we have seen that excursions consist of two parts: a prefix containing all catastrophes followed by the type of path one is interested in. If we want to count the number of catastrophes, it suffices therefore to analyse this prefix given by . What is more, due to (7) we already know how to count catastrophes: by counting occurrences of . Thus, let be the number of excursions ending with a catastrophe of length with catastrophes. Then we have

Let be the number of excursions with catastrophes, we get

| (13) |

Let be the random variable giving the number of catastrophes in excursions of length drawn uniformly at random:

Theorem 4.12 (Limit law for the number of catastrophes).

The number of catastrophes of a random excursion with catastrophes of length admits a limit distribution, with the limit law being dictated by the relation between the singularities (the structural radius where is the minimal real positive solution of ) and (the minimal real positive root of with ).

-

1.

If , the standardized random variable

with and converges in law to a standard Gaussian variable

-

2.

If , the normalized random variable , with , converges in law to a Rayleigh distributed random variable with density :

In particular, the average number of catastrophes is given by .

-

3.

If does not exist, the limit distribution is a discrete one:

where is defined as in Theorem 4.3, , , and is the unique real positive root of . In particular, converges to the random variable given by the following sum of two negative binomial distributions555The negative binomial distribution of parameters and is defined by .:

Proof.

First, for we see from (13) that we are in the case of a perturbed supercritical composition scheme from Proposition 4.11. It is supercritical because is singular at and . The perturbation is analytic for , and the other conditions are also satisfied. Hence, we get convergence to a normal distribution.

Second, for , we start with the asymptotic expansion of at . Due to Banderier and Flajolet (2002, Theorem 3) we have

| (14) |

This implies by (10) the asymptotic expansion

for and . The shape above is the one necessary for the Drmota–Soria limit scheme in Drmota and Soria (1997, Theorem 1) which implies a Rayleigh distribution. By a variant of the implicit function theorem applied to the small roots, the function satisfies the analytic continuation properties required to apply this theorem.

Third, we know by Theorem 4.3 that possesses a square-root singularity. Thus, combining the expansions (10), (12), and (14) we get the asymptotic expansion of , which is of the same type of a square root as the one from Theorem 4.4. Extracting coefficients with the help of singularity analysis and normalizing by the result of Theorem 4.4 shows the claim. ∎

Let us end this discussion with an application to Dyck paths.

Corollary 4.13.

The number of catastrophes of a random Dyck path with catastrophes of length is normally distributed. Let be the unique real positive root of , and be the unique real positive root of . The standardized version of ,

| with | and |

converges in law to a Gaussian variable .

4.3 Average number of returns to zero

In order to count the number of returns to zero, we decompose into a sequence of arches. Let be the corresponding generating function. (Caveat: this is not the same generating function as in Proposition 3.2.) Then,

Let be the number of excursions with catastrophes of length and returns to zero. Then,

From now on, let be the random variable giving the number of returns to zero in excursions with catastrophes of length drawn uniformly at random:

Applying the same ideas and techniques we used in the proof of Theorem 4.12, we get the following result.

Theorem 4.14 (Limit law for the number of returns to zero).

The number of returns to zero of a random excursion with catastrophes of length admits a limit distribution, with the limit law being dictated by the relation between the singularities and .

-

1.

If , the standardized random variable

with and converges in law to a standard Gaussian variable .

-

2.

If , the normalized random variable

converges in law to a Rayleigh distributed random variable with density . In particular, the average number of returns to zero is given by .

-

3.

If does not exist, the limit distribution is :

with

Again, we give the concrete statement for Dyck paths with catastrophes.

Corollary 4.15.

The number of returns to zero of a random Dyck path with catastrophes of length is normally distributed. Let be the unique real positive root of , and be the unique real positive root of . The standardized version of ,

| with | and |

converges in law to a Gaussian variable .

It is interesting to compare the results of Corollaries 4.13 and 4.15 for Dyck paths: more than of all steps are returns to zero, and more than are catastrophes. This implies that among all returns to zero approximately are catastrophes and are -jumps. Note that the expected number of returns to zero of classical Dyck paths converges to the constant .

4.4 Average final altitude

In this section we want to analyse the final altitude of a path after a certain number of steps. The final altitude of a path is defined as the ordinate of its endpoint. Theorem 2.1 already encodes this parameter using :

where is the bivariate generating function of meanders.

Let be the random variable giving the final altitude of paths with catastrophes of length drawn uniformly at random:

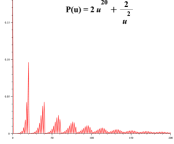

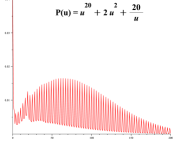

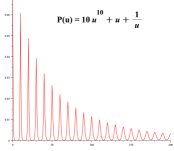

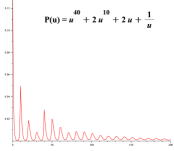

This random variable exhibits an interesting periodic behaviour, as can be observed in Figure 5, and is more formally stated in the following theorem.

Theorem 4.16 (Limit law for the final altitude).

The final altitude of a random lattice path with catastrophes of length admits a discrete limit distribution:

| (15) |

Proof.

Let us distinguish three cases. First, in the case of the function is responsible for the singularity of . Thus, by Pólya and Szegő (1925, Problem ) (see also Flajolet and Sedgewick (2009, Theorem VI.12)) we get the asymptotic expansion

Corollary 4.17.

The final altitude of a random Dyck path with catastrophes of length admits a geometric limit distribution with parameter :

The parameter is the unique real positive root of and is given by

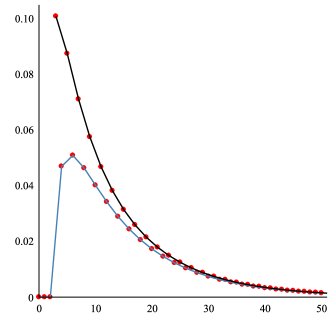

The nature of this result changes to a periodic one for different step polynomials as seen in Figure 5.

The main periodicity observed in these pictures is due to the fact that the limit law is a sum of “geometric limit laws” of complex parameter (as given in Theorem 4.16). The pictures show a combination of a “macroscopic” and a “microscopic” behaviour. On the macroscopic level we see a period of the size of the largest positive jump . On the microscopic level we see smaller fluctuations related to the small jumps (with some additional periodic behaviour if the support of these small jumps is periodic).

We observe that for some values of , is very close to zero, while it is not the case for nearby values of . This noteworthy phenomenon has links with the Skolem–Pisot problem (i.e., deciding if a rational function has a zero term in its Taylor expansion, see e.g. Ouaknine and Worrell (2014) for recent progress). In fact, a partial fraction expansion of from Equation (15) gives a closed-form expression for in terms of powers of the poles of , which dictate how close to zero our limit laws can get.

4.5 Cumulative size of catastrophes

Another interesting parameter is the cumulative size of catastrophes of excursions of length . Thereby we understand the sum of sizes of all catastrophes contained in the path. Let be the number of excursions with catastrophes of length and cumulative size of catastrophes . Then its bivariate generating function is given by

The generating function keeps track of the sizes of used catastrophes. The new parameter does not influence the singular expansion of analysed in Theorem 4.3. We get for and the expansion

| (16) |

where is a non-zero function, and in terms of the previous expansion of we have .

Let be the random variable giving the cumulative size of catastrophes in lattice paths with catastrophes of length drawn uniformly at random:

Theorem 4.18 (Limit law for the cumulative size of catastrophes).

The cumulative size of catastrophes of a random excursion with catastrophes of length admits a limit distribution, with the limit law being dictated by the relation between the singularities and .

-

1.

If , the standardized random variable

converges for in law to a standard Gaussian variable .

-

2.

If , the normalized random variable

converges in law to a Rayleigh distributed random variable with density . In particular, the average cumulative size of catastrophes is here .

-

3.

If does not exist, the limit distribution is discrete and given by:

Proof.

In the first case we will use the meromorphic scheme from Flajolet and Sedgewick (2009, Theorem IX.9), which is a generalization of Hwang’s quasi-power theorem. In order to apply it we need to check three conditions. First, the meromorphic perturbation condition: We know already from the proof of Theorem 4.3 that is a simple pole. What remains is to show that in a domain the function admits the following representation

where and are analytic for . There exists a such that . For this value the representation holds, as and are only singular for or .

Next, the non-degeneracy is easily checked. It ensures the existence of a non-constant analytic at , such that .

Finally, the variability condition for is also satisfied due to

This implies the claimed normal distribution.

In the second case we apply again the Drmota–Soria limit theorem Drmota and Soria (1997, Theorem 1) which leads to a Rayleigh distribution. As , like in (9), we have a cancellation of the constant term in the Puiseux expansion (for and ). Thus, using the asymptotic expansions (14) and (16) leads to

Note that the analyticity and the other technical conditions required to apply this theorem follow from the respective properties of the generating functions and . This implies the claimed Rayleigh distribution with the normalizing constant .

Corollary 4.19.

The cumulative size of catastrophes of a random Dyck path with catastrophes of length is normally distributed. Let be the unique real positive root of , and be the unique real positive root of . The standardized version of ,

| with | and |

converges in law to a Gaussian variable .

4.6 Size of an average catastrophe

As one of the last parameters of our lattice paths with catastrophes, we want to determine the law behind the size of a random catastrophe among all lattice paths of length . In other words, one draws uniformly at random a catastrophe among all possible catastrophes of all lattice paths of length . Note that this is also the law behind the size of the first (or last) catastrophe, as cyclic shifts of excursions ending with a catastrophe transform any catastrophe into the first (or last) one.

We can construct it from the generating function counting the number of catastrophes. It is given in (13) where each catastrophe is marked by a variable .

Lemma 4.20.

The bivariate generating function marking the size of a random catastrophe among all excursions with catastrophes is given by

Proof.

A random excursion with catastrophes either contains no catastrophes and is counted by , or it contains at least one catastrophe. In the latter we choose one of its catastrophes and its associated excursion ending with this catastrophe. Then we replace it with an excursion ending with a catastrophe whose size has been marked. This corresponds to

Computing this expression proves the claim. ∎

As before we define a random variable for our parameter as

Due to the factor the situation is similar to final altitude in Section 4.4.

Theorem 4.21 (Limit law for the size of a random catastrophe).

The size of a random catastrophe of a lattice path of length admits a discrete limit distribution:

Proof.

The proof is similar to the one of Theorem 4.16. First, for it holds that only is singular at , where all other terms are analytic. Thus, by Pólya and Szegő (1925, Problem ) the claim holds. It is then possible to extract a closed-form expression for the coefficients of an algebraic function, via the Flajolet–Soria formula which is discussed in Banderier and Drmota (2015), but this expression of in terms of nested sums of binomials is here too big to be useful.

Second, in the case we combine the singular expansions (11), (14), and (16) to get

In other words, the polar singularity of dominates, and the situation is similar to the one before.

In the final case when does not exist, we again combine the singular expansions. This time the expansion of is given by (12). This implies a contribution of all terms, as all of them are singular at once and all of them have the same type of singularity. ∎

Corollary 4.22.

Let be the unique real positive root of and given by

The size of a random catastrophe among all Dyck paths with catastrophes of length admits a (shifted) geometric limit distribution with parameter :

Comparing this result to the one for the final altitude of meanders in Corollary 4.17, we see that the type of the law is of the same nature (yet shifted for the size of catastrophes), and that the parameter is the same. The following lemma explains this connection.

Lemma 4.23.

Let , i.e., be the jump polynomial. Then, the generating function of excursions of length (marked by ) ending with a catastrophe of size (marked by ) admits the decomposition

Proof.

The idea is a last passage decomposition with respect to reaching level . First, assume that . Then the smallest catastrophe is of size . We decompose the excursion with respect to the last jump from altitude to altitude , see Figure 6. Left of it, there is a meander ending at altitude , and right of it there is a meander starting at altitude and always staying above altitude . The size of the ending catastrophe is then given by the final altitude plus , this gives the factor . This proves the first part.

For the second part, note that if one of the is equal to , then catastrophes of the respective size are allowed. These are given by meanders ending at this altitude and a jump to . ∎

This lemma shows that the probability generating function of the final altitude and of the size of an average catastrophe are connected. In particular, for and we have

We see the shift by of the probability generating function. It is now obvious how these laws are related: the parameters are the same, there is just a shift in the parameter and a subtraction of certain, initial values.

The results of Lemma 4.23 can be generalized to , but the explicit results are more complicated. For example, for there are different cases in the last passage decomposition: a -jump from to , a -jump from to , a -jump from altitude to , all followed by a meander, and a -jump from to followed by a path always staying above .

However, in all cases there is a factor in if .

4.7 Waiting time for the first catastrophe

We end the discussion on limit laws with a parameter that might be of the biggest interest in applications: the waiting time for the first catastrophe. Let be the number of excursions with catastrophes of length such that the first catastrophe appears at the -th steps for . Let be the number of such paths without a catastrophe. Then its bivariate generating function is given by

This is easily derived from Theorem 2.1 as the prefix is a sequence of excursions with only one catastrophe at the very end. Thus, marking the length of the first of such excursions marks the position of the first catastrophe.

As done repeatedly we define a random variable for our parameter as

Theorem 4.24 (Waiting time of the first catastrophe).

The waiting time for the first catastrophe in a lattice path with catastrophes of length admits a discrete limit distribution:

Proof.

In the case of Dyck paths we have

The corresponding limit law, which consists of the sum of two discrete distributions for the odd and even waiting times, is shown in Figure 7. We see a periodic behaviour with a distribution for the even and odd steps. This arises from the fact that catastrophes are not allowed at altitudes and . Starting from the origin this effects only the odd numbered steps. The probabilities for catastrophes at an odd step are lower than the ones at the following even step, because we can reach altitude from below and from above, whereas the only restriction for the even steps is at altitude which can only be reached from above. It was also interesting (and a priori not expected) to discover that the occurrence of the first catastrophe has a higher probability at step than at step .

5 Uniform random generation

In order to generate our lattice paths with catastrophes, it is for sure possible to use a dynamic programming approach; this would require bits in memory. Via some key methods from the last twenty years, our next theorem shows that it is possible to do much better.

Theorem 5.1 (Uniform random generation).

-

•

Dyck paths with catastrophes can be generated uniformly at random in linear time.

-

•

Lattice paths (with any fixed set of jumps) with catastrophes of length can be generated

-

–

in time with memory,

-

–

or in time with memory (if output is given as a stream).

-

–

Proof.

First, via the bijection of Theorem 3.1, the linear-time approach of Bacher, Bodini, and Jacquot (2013) for Motzkin trees can be applied to Dyck paths with catastrophes. The other cases can be tackled via two approaches. A first approach is to see that classical Dyck paths (and generalized Dyck paths) can be generated by pushdown automata, or equivalently, by a context-free grammar. The same holds trivially for generalized lattice paths with catastrophes. Then, using the recursive method of Flajolet, Zimmerman, and Van Cutsem (1994) (which can be seen as a wide generalization to combinatorial structures of what Hickey and Cohen (1983) did for context-free grammars), such paths of length can be generated in average time. Goldwurm (1995) proved that this can be done with the same time complexity, with only memory. The Boltzmann method introduced by Duchon, Flajolet, Louchard, and Schaeffer (2004) is also a way to get a linear average time random generator for paths of length within .

A second approach relies on a generating tree approach Banderier, Bousquet-Mélou, Denise, Flajolet, Gardy, and Gouyou-Beauchamps (2002), where each transition is computed via

where is the number of paths with catastrophes of length , starting at altitude and ending at altitude . Then, for fixed and each , the theory of D-finite functions applied to the algebraic functions derived similarly to Theorem 2.1 allows us to get the recurrence for the corresponding (see the discussion on this in Banderier and Drmota (2015)). In order to get the -th term of such recursive sequences, there is a algorithm due to Chudnovsky and Chudnovsky (1986). It is possible to win space and bit complexity by computing the ’s in floating point arithmetic, instead of rational numbers (although all the are integers, it is often the case that the leading term of such recurrences is not 1, and thus it then implies rational number computations, and time loss in gcd computations). All of this leads to a cost , moreover, a memory is enough to output the jumps of the lattice path, step after step, as a stream. ∎

Note that this complexity is hiding a dependency in in its constant. The cost of getting each D-finite recurrence indeed depends on the largest upward and downward jumps and . Some computer algebra methods for getting these recurrences (via the Platypus algorithm from Banderier and Flajolet (2002), or via integral contour representation) are analysed in Dumont (2016).

6 Conclusion

In this article, motivated by a natural model in queuing theory where one allows a “reset” of the queue, we analysed the corresponding combinatorial model: lattice paths with catastrophes. We showed how to enumerate them, how to get closed forms for their generating functions.

En passant, we gave a bijection (Theorem 3.1) which extends directly to lattice paths with a -jump and an arbitrary set of positive jumps (they are sometimes called Łukasiewiecz paths). Łukasiewiecz paths with catastrophes could be considered as a kind of Galton–Watson process with catastrophes, in which some pandemic suddenly kills the full population. Our results quantify the probability of such a pandemic over long periods.

It is known that the limiting objects associated to classical Dyck paths behave like Brownian excursions or Brownian meanders (see Marchal (2003)). For our walks, Theorem 4.14 gives some bounds on the length of the longest arch, which, in return, proves that excursions with catastrophes (if one divides their length by the length of the longest arch) have a non-trivial continuous limiting object. Moreover, it was interesting to see what type of behaviour these lattice paths with catastrophes exhibit. This is illustrated by our results on the asymptotics and on the limit laws of several parameters. We note that it is unusual to see that this leads to “periodic” limit laws (see Figure 5). In fact, all these phenomena are well explained by our analytic combinatorics approach, which also gives the speed of convergence towards these limit laws.

Naturally, it could be also possible to derive some of these results with other tools. One convenient way would be the following. To any set of jumps, one can associate a probabilistic model with drift ; this is done by Cramér’s trick of shifting the mean, see Cramér (1938, p. 11): It is using for a real such that . A trivial computation shows that this implies that is then exactly equal to , the unique real positive saddle point of . This often leads to a rescaled model which is analysable by the tools of Brownian motion theory. This trick would work for the first two cases in the trichotomy of behaviours mentioned in our theorems, and would fail for the third case, as the process is then trivially killed by any Brownian motion renormalization. In this last case, other approaches are needed to access to the discrete limit laws. Analytic combinatorics seems the right tool here and it is pleasant to rephrase some of its results in terms of some probabilistic intuition. Indeed, our analytic quantities have thus a probabilistic interpretation: could be seen as a “variance”, (from the Puiseux expansion in Theorem 4.3) could be seen as “the multiplicative constant in the tail estimate of having an arch of length ” (this tail behaves like ). However, if one uses this natural probabilistic approach, the details needed for the proofs are technical, and we think that analytic combinatorics is here a more suitable way to directly establish rigorous asymptotics.

One advantage of probability theory is to offer more flexibility in the model: the limit laws will remain the same for small perturbations of the model. So it is natural to ask which type of flexibility analytic combinatorics can also offer. Like we sketched in Remark 2.2, our results can indeed include many variations on the model. E.g. if catastrophes are allowed everywhere, except at some given altitudes belonging to a set , one has . A natural combinatorial model would be for example lattice paths with catastrophes allowed only at even altitude , or at even time. They can be analysed with the approach presented in this article. Another interesting variant would be lattice paths where catastrophes are allowed at any altitude , with a probability to have a catastrophe and a probability to have one of the jumps encoded by . This leads to functional equations involving a partial derivative, which are, however, possible to solve. Some other models are walks involving catastrophes and windfalls (a direct jump to some high altitude), as considered by Hunter, Krinik, Nguyen, Switkes, and Von Bremen (2008), or walks with a direct jump to their last maximal (or minimal) altitude (see Majumdar, Sabhapandit, and Schehr (2015)). For all these models, further limit laws like the height, the area, the size of largest arch or the waiting time for the last catastrophe, are interesting non-trivial parameters which can in fact be tackled via our approach. Let us know if you intend to have a look on some of these models!

In conclusion, we have here one more application of the motto emerging from Flajolet and Sedgewick (2009) about problems which

can be expressed by a combinatorial specification:

“If you can specify it, you can analyse it!”

Indeed, it is pleasant that the tools of analytic combinatorics and the kernel method allowed us to solve a variant of lattice path problems, giving their exact enumeration and the corresponding asymptotic expansions, and, additionally, offered efficient algorithms for uniform random generation.

Remark on this version. This article is the long-extended version of the article with the same title which appeared in the volume dedicated to the GASCom’2016 conference (see Banderier and Wallner (2017b)). In this long version, we included more details, we gave the proofs for the asymptotic results, and we also added the analysis of three new parameters: Subsections 4.5 (cumulative size of catastrophes), 4.6 (average size of a catastrophe), 4.7 (waiting time for the first catastrophe). We also added the Section 5 dedicated to uniform random generation issues.

Acknowledgments. The authors thank Alan Krinik and Gerardo Rubino

who suggested considering this model of walks with catastrophes

during the Lattice Paths Conference’15, which was held in August 2015 in California in Pomona.

We also thank Jean-Marc Fédou and the organizers of the GASCom 2016 Conference, which was held in Corsica in June 2016,

where we presented the first short version of this work.

We are also pleased to thank Grégory Schehr and Rosemary J. Harris for the interesting links

with the notion of “resetting” which they pinpointed to us,

and Philippe Marchal for his friendly probabilistic feedback on this work.

Last but not least, we thank our efficient hawk-eye referee!

The second author was partially supported by the Austrian Science Fund (FWF) grant SFB F50-03.

References

- Bacher et al. (2013) Axel Bacher, Olivier Bodini, and Alice Jacquot. Exact-size Sampling for Motzkin Trees in Linear Time via Boltzmann Samplers and Holonomic Specification. In SIAM Workshop on Analytic Algorithmics and Combinatorics (ANALCO’13), 2013.

- Banderier (2002) Cyril Banderier. Limit laws for basic parameters of lattice paths with unbounded jumps. In Mathematics and computer science, II, Trends Math., pages 33–47. Birkhäuser, 2002.

- Banderier and Drmota (2015) Cyril Banderier and Michael Drmota. Formulae and asymptotics for coefficients of algebraic functions. Combinatorics, Probability and Computing, 24(1):1–53, 2015.

- Banderier and Flajolet (2002) Cyril Banderier and Philippe Flajolet. Basic analytic combinatorics of directed lattice paths. Theoretical Computer Science, 281(1-2):37–80, 2002.

- Banderier and Merlini (2003) Cyril Banderier and Donatella Merlini. Algebraic succession rules and Lattice paths with an infinite set of jumps. In Proceedings of Formal Power Series and Algebraic Combibatorics (Melbourne, 2002), pages 1–10, 2003.

- Banderier and Wallner (2017a) Cyril Banderier and Michael Wallner. The kernel method for lattice paths below a rational slope. In Lattice paths combinatorics and applications, Developments in Mathematics Series. Springer, 2017a. To appear.

- Banderier and Wallner (2017b) Cyril Banderier and Michael Wallner. Lattice paths with catastrophes. Electronic Notes in Discrete Mathematics, 59:131–146, 2017b. Random Generation of Combinatorial Structures (GASCom 2016).

- Banderier et al. (2002) Cyril Banderier, Mireille Bousquet-Mélou, Alain Denise, Philippe Flajolet, Danièle Gardy, and Dominique Gouyou-Beauchamps. Generating functions for generating trees. Discrete Mathematics, 246(1-3):29–55, 2002. Formal power series and algebraic combinatorics (Barcelona, 1999).

- Banderier et al. (2003) Cyril Banderier, Jean-Marc Fédou, Christine Garcia, and Donatella Merlini. Algebraic succession rules and Lattice paths with an infinite set of jumps. Preprint, pages 1–32, 2003.

- Barcucci et al. (1999) Elena Barcucci, Alberto Del Lungo, Elisa Pergola, and Renzo Pinzani. ECO: a methodology for the Enumeration of Combinatorial Objects. Journal of Difference Equations and Applications, 5:435–490, 1999.

- Ben-Ari et al. (2017) Iddo Ben-Ari, Alexander Roitershtein, and Rinaldo B. Schinazi. A random walk with catastrophes. arXiv, 1709.04780:1–23, 2017.

- Bousquet-Mélou and Petkovšek (2000) Mireille Bousquet-Mélou and Marko Petkovšek. Linear recurrences with constant coefficients: the multivariate case. Discrete Mathematics, 225(1-3):51–75, 2000. Formal power series and algebraic combinatorics (Toronto, 1998).

- Burstein (2005) Alexander Burstein. Restricted Dumont permutations. Annals of Combinatorics, 9(3):269–280, 2005.

- Chudnovsky and Chudnovsky (1986) David V. Chudnovsky and Gregory V. Chudnovsky. On expansion of algebraic functions in power and Puiseux series. I. Journal of Complexity, 2(4):271–294, 1986.

- Cramér (1938) Harald Cramér. Sur un nouveau théorème-limite de la théorie de probabilités. Actualités Scientifiques et Industrielles, 736:5–23, 1938.

- Drmota and Soria (1997) Michael Drmota and Michèle Soria. Images and preimages in random mappings. SIAM Journal on Discrete Mathematics, 10(2):246–269, 1997.

- Duchi et al. (2004) Enrica Duchi, Jean-Marc Fédou, and Simone Rinaldi. From object grammars to ECO systems. Theoretical Computer Science, 314(1-2):57–95, 2004.

- Duchon et al. (2004) Philippe Duchon, Philippe Flajolet, Guy Louchard, and Gilles Schaeffer. Boltzmann samplers for the random generation of combinatorial structures. Combinatorics, Probability and Computing, 13(4-5):577–625, 2004.

- Dumont (2016) Louis Dumont. Algorithmes rapides pour le calcul symbolique de certaines intégrales de contour à paramètre. PhD thesis, École polytechnique, Université de Paris-Saclay, 2016.

- Elliott and Kopp (2005) Robert J. Elliott and P. Ekkehard Kopp. Mathematics of Financial Markets. Springer Finance, 2nd edition, 2005.

- Feller (1968) William Feller. An introduction to probability theory and its applications. Vol. I. John Wiley & Sons, 3rd edition, 1968.

- Ferrari et al. (2011) Luca Ferrari, Elisa Pergola, Renzo Pinzani, and Simone Rinaldi. Some applications arising from the interactions between the theory of Catalan-like numbers and the ECO method. Ars Combinatoria, 99:109–128, 2011.

- Flajolet (1980) Philippe Flajolet. Combinatorial aspects of continued fractions. Discrete Mathematics, 32(2):125–161, 1980.

- Flajolet and Sedgewick (2009) Philippe Flajolet and Robert Sedgewick. Analytic Combinatorics. Cambridge University Press, 2009.

- Flajolet et al. (1994) Philippe Flajolet, Paul Zimmerman, and Bernard Van Cutsem. A calculus for the random generation of labelled combinatorial structures. Theoretical Computer Science, 132(1-2):1–35, 1994.

- Goldwurm (1995) Massimiliano Goldwurm. Random generation of words in an algebraic language in linear binary space. Information Processing Letters, 54(4):229–233, 1995.

- Harris and Touchette (2017) Rosemary J. Harris and Hugo Touchette. Phase transitions in large deviations of reset processes. Journal of Physics. A. Mathematical and Theoretical, 50(10):10LT01, 13, 2017.

- Hickey and Cohen (1983) Timothy Hickey and Jacques Cohen. Uniform random generation of strings in a context-free language. SIAM Journal on Computing, 12(4):645–655, 1983.

- Hunter et al. (2008) Blake Hunter, Alan Krinik, Chau Nguyen, Jennifer M. Switkes, and Hubertus F. Von Bremen. Gambler’s ruin with catastrophes and windfalls. Journal of Statistical Theory and Practice, 2008.

- Janson and Peres (2012) Svante Janson and Yuval Peres. Hitting times for random walks with restarts. SIAM Journal on Discrete Mathematics, 26(2):537–547, 2012.

- Krinik and Mohanty (2010) Alan Krinik and Sri Gopal Mohanty. On batch queueing systems: a combinatorial approach. Journal of Statistical Planning and Inference, 140(8):2271–2284, 2010.

- Krinik et al. (2005) Alan Krinik, Gerardo Rubino, Daniel Marcus, Randall J. Swift, Hassan Kasfy, and Holly Lam. Dual processes to solve single server systems. Journal of Statistical Planning and Inference, 135(1):121–147, 2005.

- Kusmierz et al. (2014) Lukasz Kusmierz, Satya N. Majumdar, Sanjib Sabhapandit, and Grégory Schehr. First order transition for the optimal search time of Lévy flights with resetting. Physical Review Letters, 113:220602, 2014.

- Labelle and Yeh (1990) Jacques Labelle and Yeong Nan Yeh. Generalized Dyck paths. Discrete Mathematics, 82(1):1–6, 1990.

- Majumdar et al. (2015) Satya N. Majumdar, Sanjib Sabhapandit, and Grégory Schehr. Random walk with random resetting to the maximum position. Physical Review E. Statistical, Nonlinear, and Soft Matter Physics, 92(5):052126, 13, 2015.

- Manes et al. (2016) Kostas Manes, Aristidis Sapounakis, Ioannis Tasoulas, and Panagiotis Tsikouras. Equivalence classes of ballot paths modulo strings of length 2 and 3. Discrete Mathematics, 339(10):2557–2572, 2016.

- Marchal (2003) Philippe Marchal. Constructing a sequence of random walks strongly converging to Brownian motion. In Cyril Banderier and Christrian Krattenthaler, editors, Discrete random walks (Paris, 2003), Discrete Math. Theor. Comput. Sci. Proc., AC, pages 181–190, 2003.

- Ouaknine and Worrell (2014) Joël Ouaknine and James Worrell. Positivity problems for low-order linear recurrence sequences. In Proceedings of the Twenty-Fifth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 366–379. ACM, New York, 2014.

- Pólya and Szegő (1925) George Pólya and Gábor Szegő. Aufgaben und Lehrsätze aus der Analysis. Erster Band: Reihen, Integralrechnung Funktionentheorie. Springer, 1st edition, 1925.

- Schoutens (2003) Wim Schoutens. Lévy Processes in Finance: Pricing Financial Derivatives. John Wiley & Sons, 2003.

- Stanley (2011) Richard P. Stanley. Enumerative combinatorics. Volume 1, volume 49 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, 2nd edition, 2011.

- West (1996) Julian West. Generating trees and forbidden subsequences. Discrete Mathematics, 157:363–374, 1996.