Critical link of self-similarity and visualisation for jump-diffusions driven by -stable noise

Abstract

The purpose of this paper is to derive a critical link of parameters for the self-similar trajectories of jump-diffusions which are described as solutions of stochastic differential equations driven by -stable noise. This is done by a multivariate Lagrange interpolation approach. To this end, we utilise computer simulation algorithm in MATLAB to visualise the trajectories of the jump-diffusions for various combinations of parameters arising in the stochastic differential equations.

Key words: Stochastic differential equations, -stable processes, self-similarity, simulation, multivariate Lagrange interpolation.

AMS Subject Classification(2010): 60E07; 60G17; 65C99; 68U20

1 Introduction

With the passage of time, modelling time evolution uncertainty by stochastic differential equations (SDEs) appears in many diverse areas such as studies of dynamical particle systems in physics, biological and medical studies, engineering and industrial studies, as well as most recently micro analytic studies in mathematical finance and social sciences. Beyond modelling uncertainty by Gaussian or normal distributions, there is a large amount of data featured with heavy-tailed distributions. On the other side, it is necessary to admit symmetry for the mean (average) by using Gaussian models while asymmetry and/or skewness are accepted by non-Gaussian models. In some applications, asymmetric or heavy-tailed models are needed or even inevitable, in which a model using stable distributions could be a viable candidate. Another important feature of such non-Gaussian models is the use of probability distributions with infinite moments which turns to be more realistic than Gaussian models from the view point of heavy tail type data (cf. e.g. [15]). The research on modelling uncertainty using stable distributions and stable stochastic processes have been increased dramatically, see e.g. [8], [20], [5] and [7]. The self-similarity property of stable distributions has drawn more and more attention from both theoretical and practical view points, i.e [2, 14] and [19, 10, 18]. We refer the reader to [6] for discussions of utilising -stable distributions to model the mechanism of Collateralised Debt Obligations (CDOs) in mathematical finance.

Historically, probability distributions with infinite moments are also encountered in the study of critical phenomena. For instance, at the critical point one finds clusters of all sizes while the mean of the distribution of clusters sizes diverges. Thus, analysis from the earlier intuition about moments had to be shifted to newer notions involving calculations of exponents, like e.g. Lyapunov, spectral, fractal etc., and topics such as strange kinetics and strange attractors have to be investigated. It was Paul Lévy who first grappled in-depth with probability distributions with infinite moments. Such distributions are now called Lévy distributions. Today, Lévy distributions have been expanded into diverse areas including turbulent diffusion, polymer transport and Hamiltonian chaos, just to mention a few. Although Lévy’s ideas and algebra of random variables with infinite moments appeared in the 1920s and the 1930s (cf. [11, 12]), it is only from the 1990s that the greatness of Lévy’s theory became much more appreciated as a foundation for probabilistic aspects of chaotic dynamics with high entropy in statistical analysis in mathematical modelling (cf. [15, 18], see also [14, 19]). Indeed, in statistical analysis, systems with highly complexity and (nonlinear) chaotic dynamics became a vast area for the application of Lévy processes and the phenomenon of dynamical chaos became a real laboratory for developing generalisations of Lévy processes to create new tools to study nonlinear dynamics and kinetics. Following up this point, SDEs driven by Lévy type processes, in particular -stable noise, and their influence on long time statistical asymptotic will be unavoidably encountered.

The study of SDEs driven by Lévy processes is well presented in the monograph [1]. Numerical solutions and simulations of -stable stochastic processes were carried out in [9]. The motivation of this paper is to obtain a critical link among the parameters in the SDEs driven by -stable noises towards self-similarity property from simulations. This can be further linked to sample data analysis after model identifications. We mainly focus on testing two simple types of SDEs, one class is the SDEs with linear drift coefficient and additive -stable noise and the solutions are called -stable Ornstein-Uhlenbeck processes and the other class is the linear SDEs (i.e., SDEs with linear drift and diffusion coefficients or the linear SDEs with multiplicative -stable noise) and the solutions are called -stable geometric Lévy motion.

2 Preliminaries

Given a probability space endowed with a complete filtration . We are concerned with the following stochastic differential equation (SDE) driven by -stable Lévy motion

where are measurable coefficients, is an -Brownian motion, and is an -stable -Lévy process with the following Lévy-Ito representation

with being the Poisson random (counting) measure on and

the associated compensated martingale measure with density , where is fixed and is a cádlág (i.e., right continuous with left limits) stochastic process.

Under the usual conditions, like linear growth and local Lipschitz conditions, for the coefficients , there is a unique solution to the above SDE with initial data (see, e.g., [1]). In what follows, we introduce two simple ctypes of SDEs fulfilling the usual conditions.

2.1 The -stable Ornstein-Uhlenbeck processes

The -stable Ornstein-Uhlenbeck processes are solutions of the following type SDEs

| (1) |

for , where the -stable noise is formulated as follows

By Itô formula (cf., e.g., [1]), the solution is explicitly given as follows

| (2) |

2.2 The -stable geometric Lévy motion

Consider the following linear SDE

where , . Then by Itô formula, one can derive the following explicit solution

| (3) |

Due to the above expression, the solution is called an -stable geometric Lévy motion.

2.3 Trajectories and self-similarity

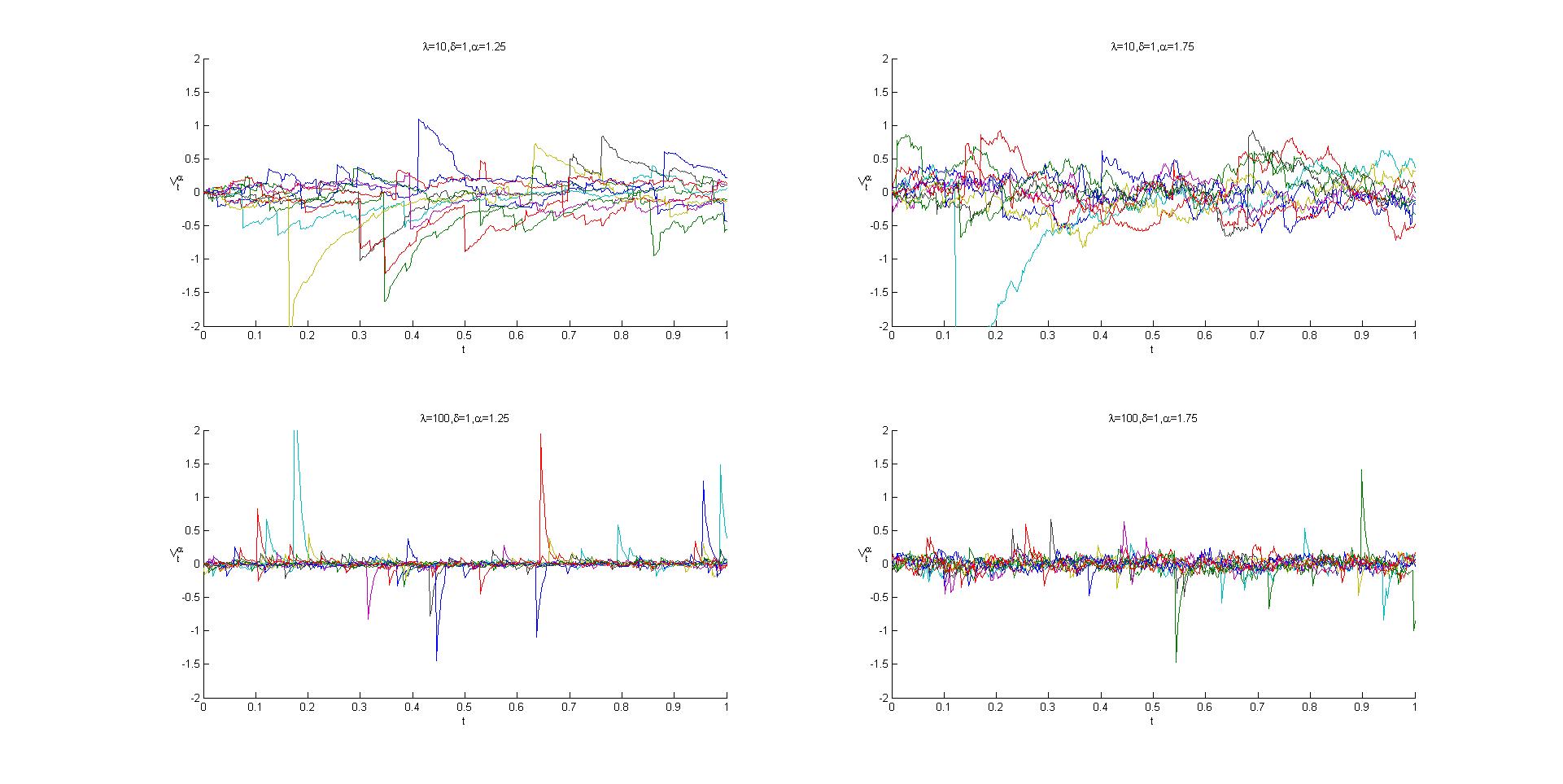

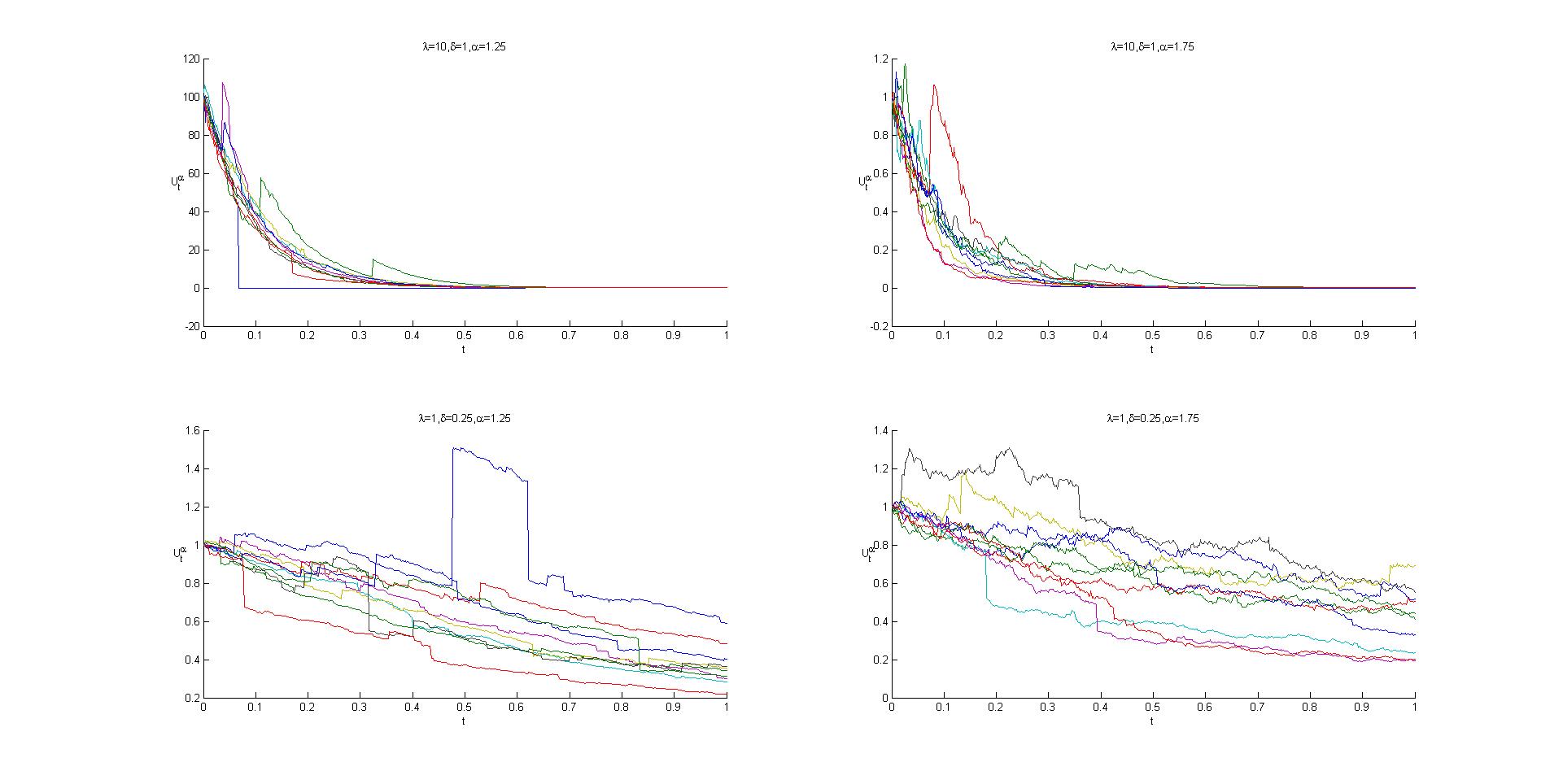

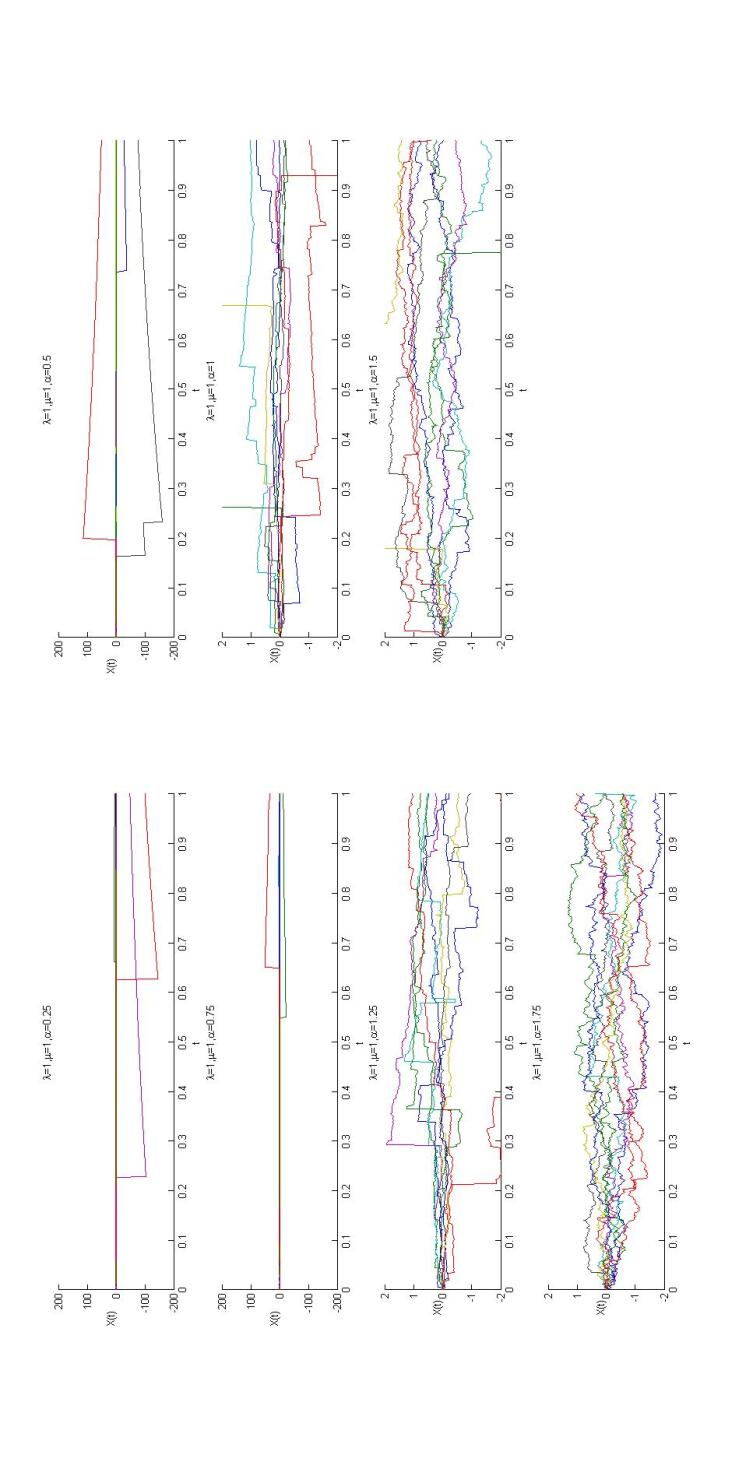

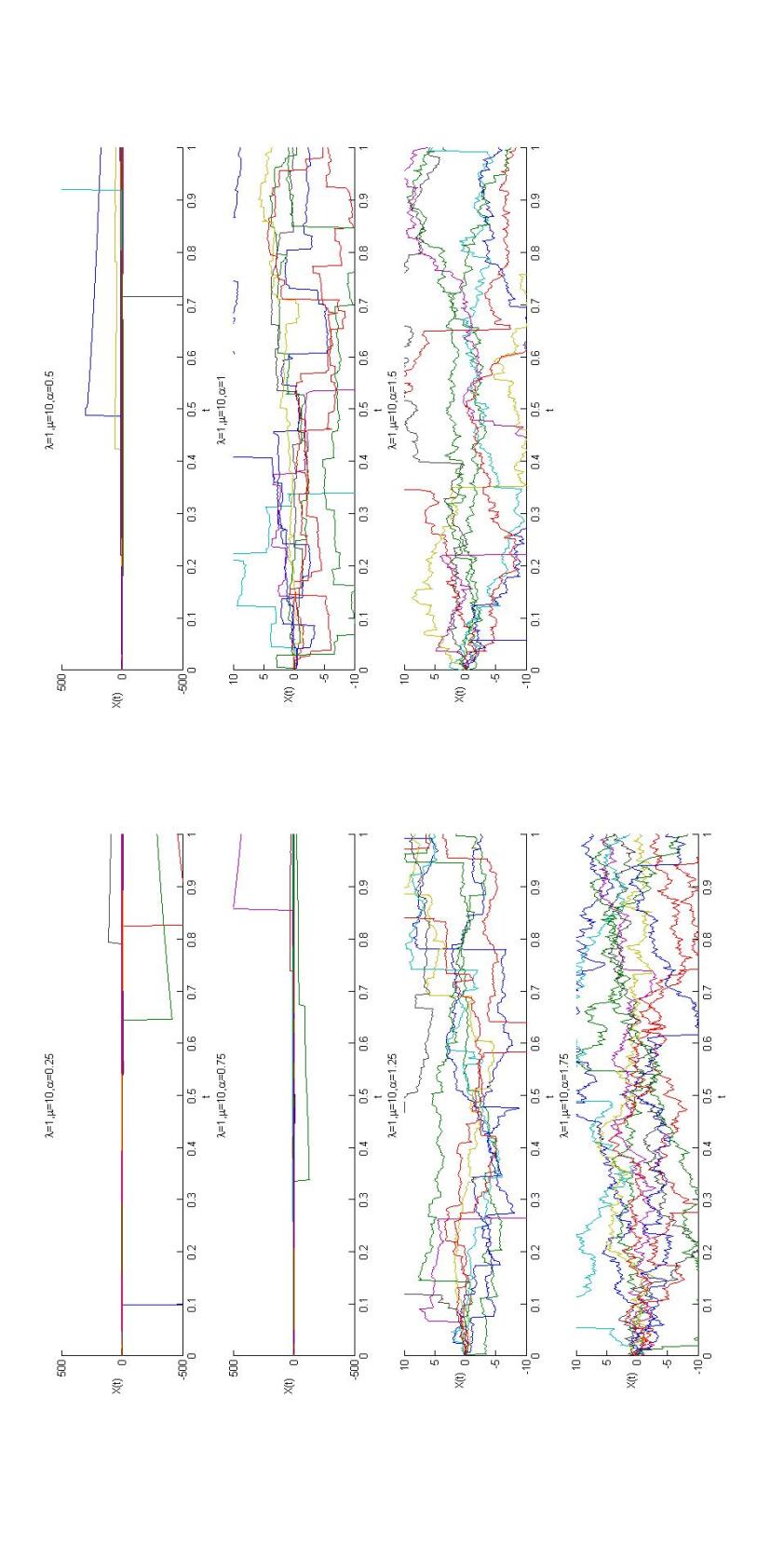

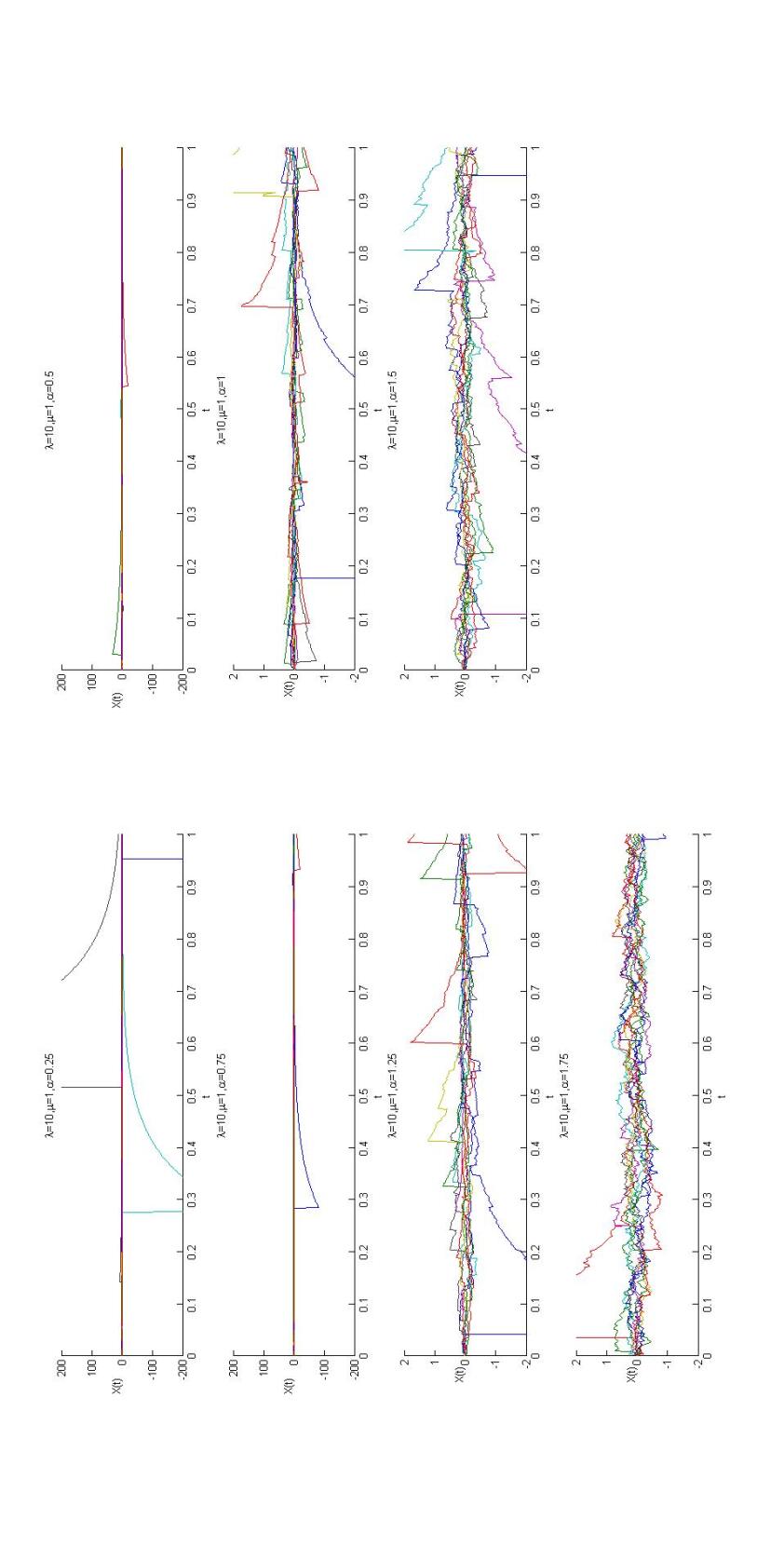

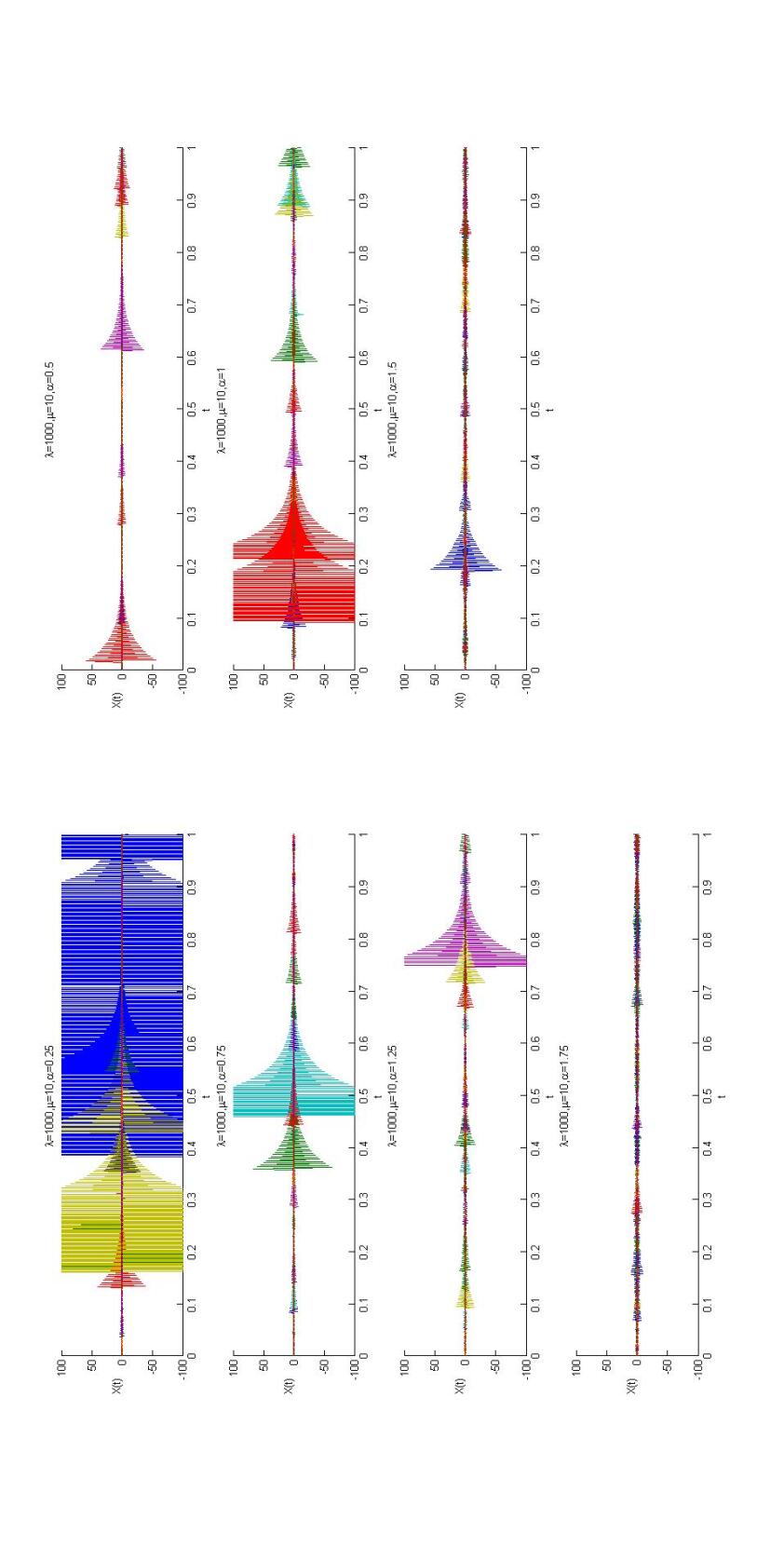

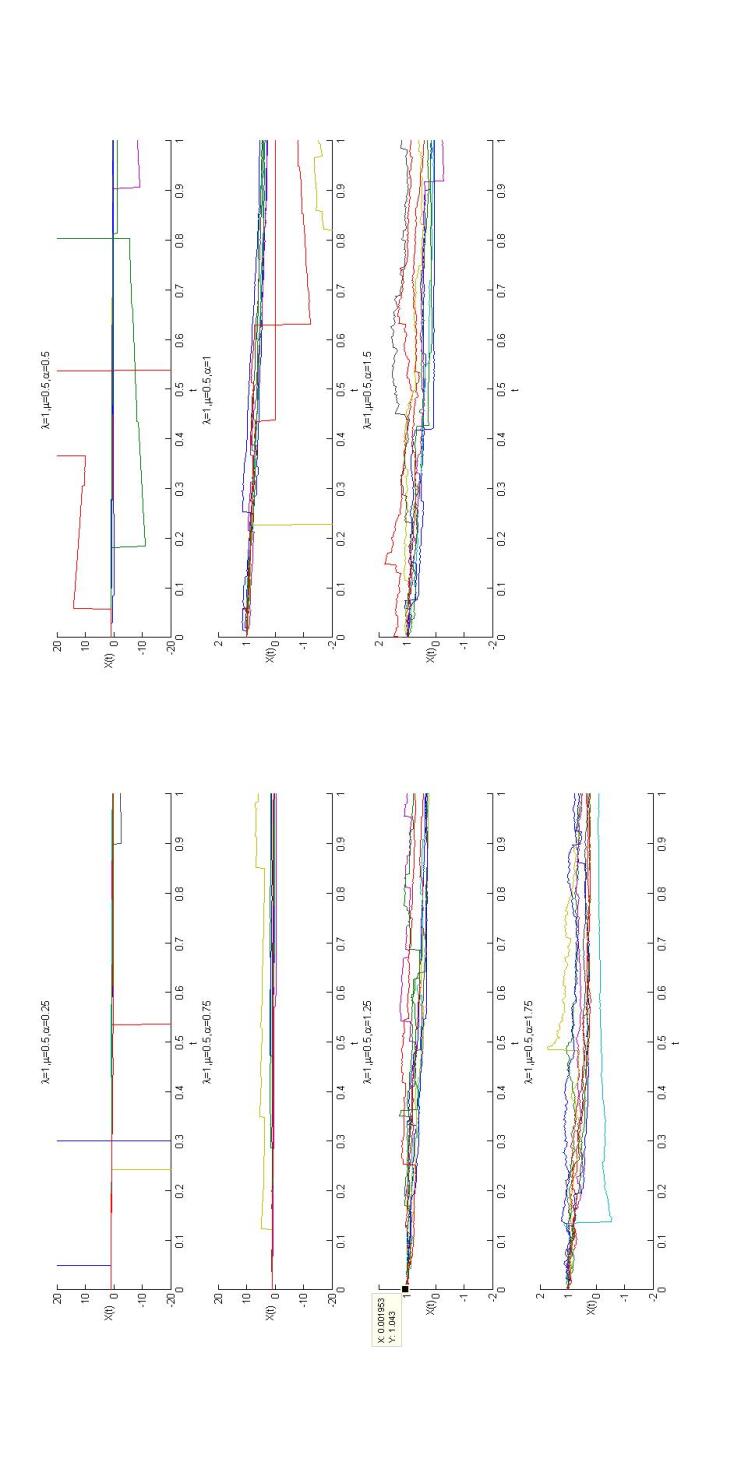

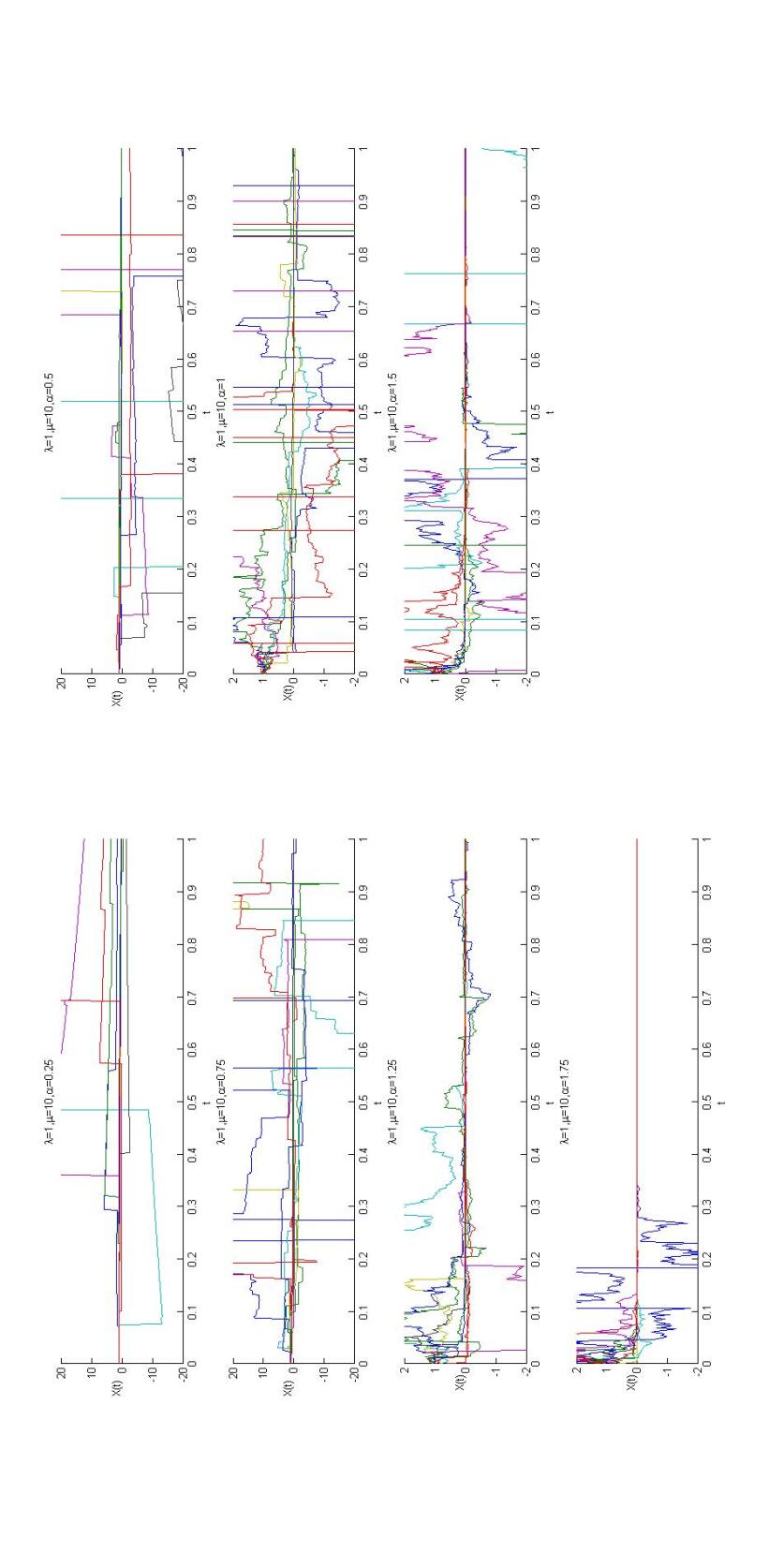

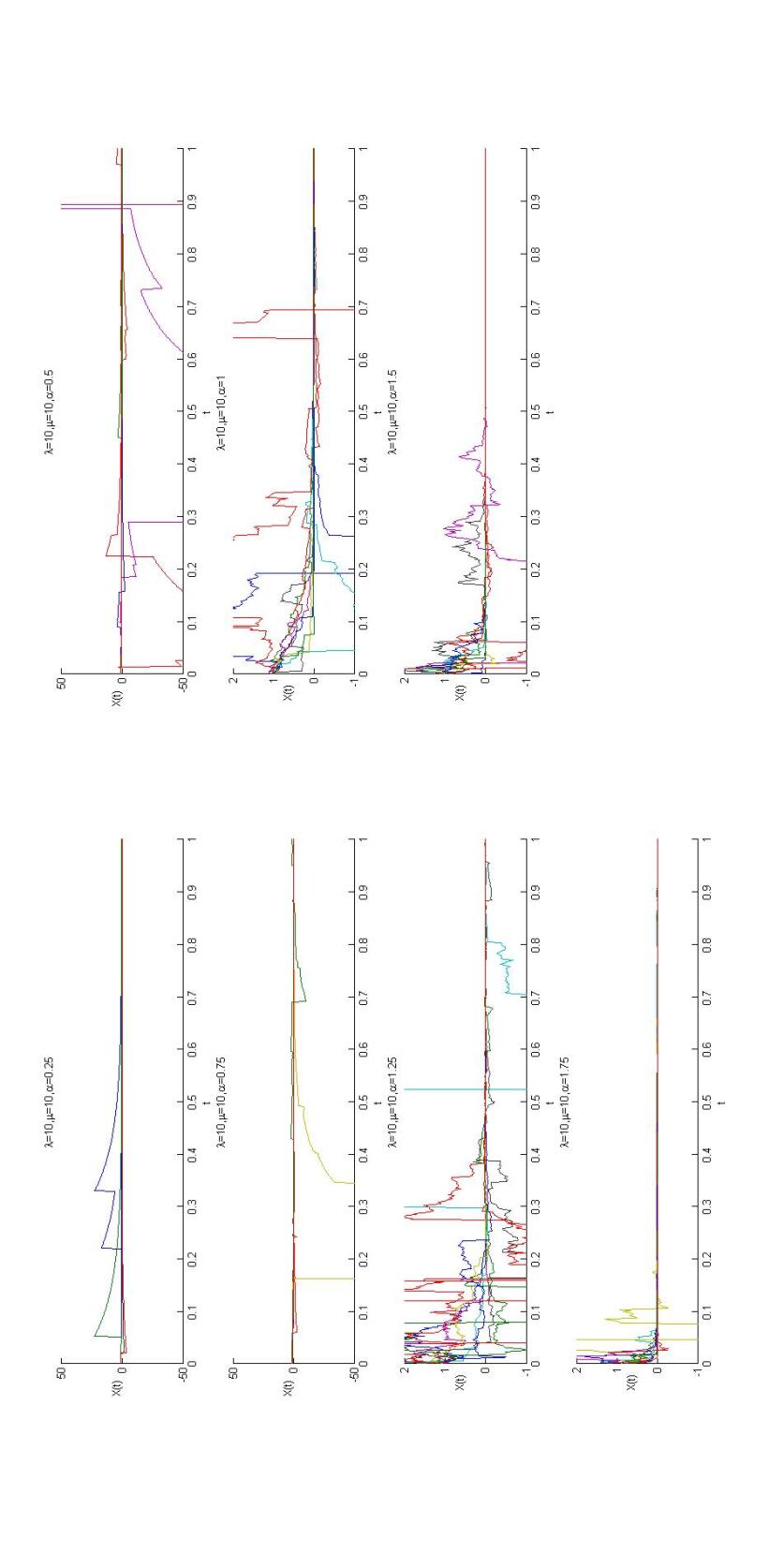

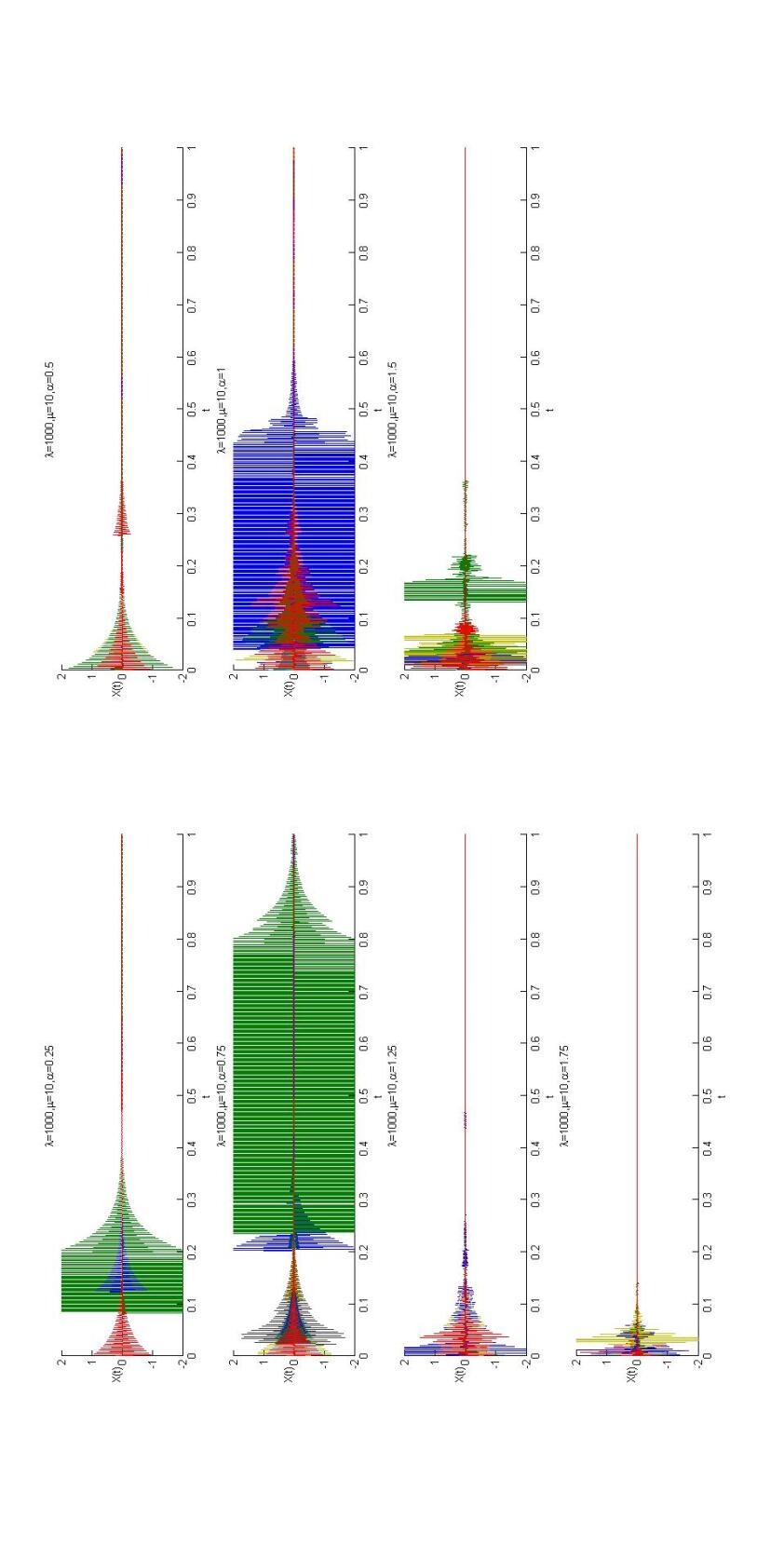

By applying simulation methods in MATLAB, sample trajectories can be generated and codes are listed in Appendix.A. Following graphs show sample trajectories -stable OU processes and -stable geometric L motions respectively with a number of parameters combinations.

From the trajectories, self-similarity can be observed. To define self-similarity,

Definition 2.1.

A stochastic process is said to be ”self-similar” if for any , there exists such that

For an -stable Lvy motion, if we have a real number , then the processes and have the same finite dimensional distributions [15]. Our aim is to obtain a critical link among parameters in SDE towards similarity and it can be used for data fitting purpose in future.

3 Interpolation

According to our research problem, polynomial interpolation approach is needed for determining the links among parameters and coefficients in the -stable driven SDEs. The methodology we use is the n-state polynomial interpolation with multiple variables, [3], [16], [4],[13] and [17].

Let be an -variable multinomial function of degree . In [16], let be the number of terms in , and assume we have at least distinct points , , for to be uniquely defined,

where are the coefficients in , and also is the -tuple of independent variables of . is an exponent vector with nonnegative integer entries which has an ordered partition of an integer in [0, n]. stands for vector dot product and . Similarly, comparing with Lagrange interpolation, is the ideal form we would like to have and is a multinomial function with independent, where X represents the value of data. Let us think about a linear equation system

where , now consider,

| (4) |

as a sample matrix and assume .

Remark 3.1.

We want to determine without solving for its coefficients individually.

The algorithm is to make some substitutions. If we have , we use in M, then we have

| (5) |

Use and in where , then we have

| (6) |

We can easily see that the row appears twice in which results in . Now So

| (7) |

and

| (8) |

4 Simulations and examples

In this section, a critical link will be obtained for -stable Ornstein-Uhlenbeck process and -stable geometric Lvy motion respectively towards self-similarity from simulations by interpolation method introduced in the above section. Trajectories of -stable Ornstein-Uhlenbeck process as Equation.1 with different combinations of parameters in its SDE are included in Appendix.B. And the case for -stable geometric Lvy motion can be found in Appendix.C. We could clarify the model into different perspectives by observations and general characteristics of trajectories are summarized as follows,

-

1.

Fix and , the trajectories become more tempered as the stability index increases, but the jump size becomes smaller and smaller so that the trajectories become less and less volatile. In other words, for smaller stability index , the trajectories of are generally more tough than those of bigger stablility index .

-

2.

Fix and , trajectories look more likely deterministic exponential paths along with the increase of . As for bigger , the trajectories are chaotic more sharply.

-

3.

Fix and , increasing the volatility parameter indicates higher chaoticity.

4.1 -stable Ornstein-Uhlenbeck process

For the triple , there is a critical link of the three parameters , and towards the similarity of trajectories. By simulations, we choose the situations for shows similarity property and keep records of parameters , and when the first jump appears. Especially, the degree 1 linear relationship among these three parameters is useful in data modelling for uncertainty related problems in reality.

| t | ||||

|---|---|---|---|---|

| 1 | 0.25 | 1 | 0.06055 | 0.4198 |

| 1 | 1 | 1.75 | 0.003906 | -0.1551 |

| 1 | 100 | 0.75 | 0.03125 | 18.82 |

| 10 | 0.25 | 0.5 | 0.02148 | 0.4561 |

| 1000 | 0.25 | 1.75 | 0.001952 | 0.0374 |

We have degrees , variables , so terms= If we have which is a degree 1 function with 4 parameters, and

where are coefficients, .

By calculation

Then

If we take the average value of t, we have

and average value of , we have

Therefore

We summarise our deviation as

Proposition 4.1.

The critical link of parameters for self-similarity of the trajectories of -stable Ornstein-Uhlenbeck process is given by the following liner equation

4.2 -stable geometric Lvy motion

Similarly, for the triple , we are working on determining a critical link of the three parameters , and towards the similarity of trajectories. The data and calculations have been processed to obtain the degree 1 linear relationship are as follows.

| t | ||||

|---|---|---|---|---|

| 1 | 0.5 | 1.25 | 0.001952 | 1.043 |

| 1 | 1 | 1 | 0.007813 | 1.372 |

| 100 | 0.5 | 1.75 | 0.001953 | 0.9523 |

| 100 | 10 | 1.25 | 0.005859 | 0.5114 |

| 1000 | 1 | 0.75 | 0.001796 | -0.7903 |

We have degrees , variables , so terms= If we have which is a degree 1 function with 4 parameters, and

where are coefficients, . We have

By calculation

Then

If we take the average value of t, we have

and average value of , we have

Therefore

Proposition 4.2.

The critical link of parameters for self-similarity of the trajectories of -stable geometric Lvy motion is given by the following liner equation

Remark 4.1.

Here we only consider linear Lagrange interpolation. One can extend to higher order polynomial interpolation in which more computation is needed. Our consideration gives a simple yet efficient calculation.

Appendix A -stable random variable generator

Following codes are used to generate sample trajectories [21].

Appendix B Sample trajectories of -stable Ornstein-Uhlenbeck process

Appendix C Sample trajectories of -stable geometric Lvy motion

References

- [1] Applebaum, D. Lévy Processes and Stochastic Calculus. 2nd edn. Cambridge University Press: Cambridge, 2009.

- [2] Campbell, J.Y.; Lo, A.W.C.; MacKinlay, A.C. The Econometrics of Financial Markets. Princeton University Press, Princeton, 1997.

- [3] De Boor, C.; Ron, A. On multivariate polynomial interpolation. Constr. Approx., 1990, 6(3), 287-302.

- [4] De Marchi, S. Lectures on multivariate polynomial interpolation, Göttingen-Padova Erasmus Course, February 2015. [http://www.math.unipd.it/ demarchi/MultInterp/LectureNotesMI.pdf]

- [5] Dror, M.; L’Ecuyer, P.; Szidarovszky, F. (eds) Modeling Uncertainty: An Examination of Stochastic Theory, Methods, and Applications, Springer Science Business Media, 2002.

- [6] Du, H.; Wu, J.-L.; Yang, W. On the mechanism of CDOs behind the current financial crisis and mathematical modeling with Lévy distributions, Intelligent Information Management, 2010, 2, 149-158.

- [7] Fiche, A.; Cexus, J.C.; Martin, A.; Khenchaf, A. Features modeling with an -stable distribution: Application to pattern recognition based on continuous belief functions. Information Fusion 2013, 14(4), 504-520.

- [8] Giacometti, R.; Bertocchi, M.; Rachev, S.T.; Fabozzi, F.J. table distributions in the Black-Litterman approach to asset allocation. Quantitative Finance. 2007, 7(4), 423-433.

- [9] Janicki, A.; Weron, A. Simulation and Chaotic Behavior of -Stable Stochastic Processes. Monographs and Textbooks in Pure and Applied Mathematics, 178. Marcel Dekker, Inc., New York, 1994.

- [10] W. E. Leland, W.E.; Taqqu, M. S.; Willinger, W.; Wilson, D.W. On the self-similar nature of ethernet traffic. In ACM SIGCOMM Computer Communication Review, 1993, 23, 183-193.

- [11] Lévy P. Calcul des probabilités. Gauther-Villars, 1925.

- [12] Lévy, Théorie de l’addition des variables aléatoires. Gauther-Villars, 1937.

- [13] Liang, X.Z.; Zhang, J.L.; Zhang, M.; Cui, L.H. The application of Cayley-Bacharach theorem to bivariate Lagrange interpolation. Journal of Computational and Applied Mathematics.2006,163, 177-187.

- [14] Mandelbrot, B. The Pareto-Lévy las and the distribution of income, International Economic Review, 1960, 1, 79-106.

- [15] Samorodnitsky, G.;Taqqu, M.S. Stable non-Gaussian Random Processes: Stochastic Models with Infinite Variance. CRC Press, 1994.

- [16] Saniee, K. A simple expression for multivariate Lagrange interpolation. Copyright@SIAM, 2008. [https://www.siam.org/students/siuro/vol1issue1/S01002.pdf]

- [17] Sauer, T.; Xu, Y. A case study in multivariate Lagrange interpolation. In Approximation theory, wavelets and applications. Springer, Netherlands, 1995, pp443-452.

- [18] Shlesinger, M.F. ; Zaslavsky, G.M.; Frisch, U. (Eds.) Lévy Flights and Related Topics in Physics. Lecutre Notes in Physics, Vol. 450, Springer-Verlag, Berlin, 1995.

- [19] Zolotarev, V.M. One-Dimensional Stable Distributions. American Mathematical Society, R. I. Province, 1986.

- [20] Zopounidis, C.; Pardalos, P.M. Managing in Uncertainty: Theory and Practice (Vol. 19); Springer Science Business Media, 2013.

- [21] Veillette, M. https://github.com/markveillette/stbl, 2014.