Integral equations, quasi-Monte Carlo methods and risk modelling

Dedicated to the th anniversary of Ian Sloan

Abstract

We survey a QMC approach to integral equations and develop some new applications to risk modeling. In particular, a rigorous error bound derived from Koksma-Hlawka type inequalities is achieved for certain expectations related to the probability of ruin in Markovian models. The method is based on a new concept of isotropic discrepancy and its applications to numerical integration. The theoretical results are complemented by numerical examples and computations.

1 Introduction

During the last two decades quasi-Monte-Carlo methods (QMC-methods) have been applied to various problems in numerical analysis, statistical modeling and mathematical finance. In this paper we will give a brief survey on some of these developments and present new applications to more refined risk models involving discontinuous processes. Let us start with Fredholm integral equations of the second kind:

| (1) |

where the kernel is given by

with

having period in each component of

. As it is quite common in

applications of QMC-methods (see for example [9],

[28], [20]) it is assumed that and belong to a weighted Korobov space. Of course, there

exists a vast literature concerning the numerical solution of

Fredholm equations, see for instance [18], [5] or [31].

In particular, we want to mention the work of I. Sloan in the late 1980’s where he

explored various quadrature rules for solving integral equations

and applications to engineering problems ([27], [26] and [34]), which have also, after some modifications, been applied to Volterra type integral equations (see [32] or [33]).

In [9] the authors approximate using the Nyström method based on QMC

rules.

For points in

the -th approximation of is given by

| (2) |

where the function values are obtained by solving the linear system

| (3) |

Under some mild conditions on and the integration points

it is shown in [9]

that there exists a unique solution of (3). Furthermore, the

authors analyze the worst case error of this, so-called

QMC-Nyström method. In addition, good lattice point sets

are presented, which lead

to a best possible worst case error. A special focus of this

important paper lies on the study of tractability and strong

tractability of the QMC-Nyström method. For tractability theory in

general we refer to the fundamental monograph of

[23].

Using ideas of E. Hlawka [16] the third

author of the present paper worked on iterative methods for solving Fredholm and Volterra equations,

see also Hua-Wang [17].

The idea is to approximate the solution of integral equations by means of iterated (i.e. multi-dimensional) integrals. The convergence of this procedure follows from Banach’s fixed point theorem and error estimates can be established following the proof of the Picard-Lindelöf approximation for ordinary differential equations. To be more precise, let us consider integration points with star discrepancy defined as usual by

| (4) |

where the supremum is taken over all axis-aligned boxes with one vertex in the origin and Lebesgue measure . In [30] the following system of integral equations has been considered for given functions on and on :

| (5) |

where we have used the notations and . Furthermore, we assume that the partial derivatives up to order of the functions and , , are bounded by some constants and , respectively. Then, for a given point set in with discrepancy , the solution of the system (5) can be approximated by the quantities given recursively by

| (6) |

here stands for the inner product , where . In [30] it is shown, that based on the classical Koksma-Hlawka inequality the worst case error, i.e., (sum of componentwise supremum norms) can be estimated in terms of the bounds and and the discrepancy of the integration points. This method was also extended to integral equations with singularities, such as Abel’s integral equation. The main focus of the present paper lies on applications in mathematical finance. In Albrecher & Kainhofer [3] the above method was used for the numerical solution of certain Cramér-Lundberg models in risk theory. However, it turned out that in these models certain discontinuities occur. This means, that one cannot assume bounds for the involved partial derivatives and simply apply the classical Koksma-Hlawka inequality. Moreover, the involved functions are indicator functions of simplices thus not of bounded variation in the sense of Hardy and Krause, see Drmota & Tichy [10] and Kuipers & Niederreiter [19].

Albrecher & Kainhofer [3] considered a risk model with non-linear dividend

barrier and made some assumptions to overcome the difficulties

caused by discontinuities. For such applications it could help to

use a different notion of variation for multivariate functions.

Götz [14] proved a version of the Koksma-Hlawka inequality for

general measures, Aistleitner & Dick [1] considered functions

of bounded variation with respect to signed measures and

Brandolini et al. [7, 6]

replaced the integration domain by an arbitrary

bounded Borel subset of and proved the inequality

for piecewise smooth integrands. Based on fundamental work of

Harman [15], a new concept of variation was developed for a wide

class of functions, see Pausinger & Svane [25] and Aistleitner et al. [2].

In the following we give a brief overview on concepts of

multivariate variation and how they can be applied for error

estimates in numerical integration. Let be a

function on and points

in , where denotes the natural componenwise partial

order. Following the notation of Owen [24] and Aistleitner et al. [2] for a subset

we denote by

the point with th coordinate

equal to if and equal to otherwise. Then

for the box we introduce the

dimensional difference operator

where the summation is extended over all subsets with cardinality and complement . Next we define partitions of as they are used in the theory of multivariate Riemann integrals, which we call here ladder. A ladder in is the cartesian product of one-dimensional partitions (in any dimension ). Define the successor of to be if and . For we define the successor and have

Using the notation

the Vitali variation of over is defined by

| (7) |

Given a subset let

and set . For a ladder there is a corresponding ladder on the -dimensional face of consisting of points of the form . Clearly,

Using the notation

for the variation over the ladder of the restriction of to the face of specified by , the Hardy-Krause variation is defined as

Assuming that is of bounded Hardy-Krause variation, the classical Koksma-Hlawka inequality reads as follows:

| (8) |

where is a finite point set in with star discrepancy . In the case has continuous mixed partial derivatives up to order the Vitali variation (7) is given by

| (9) |

Summing over all non-empty subsets immediately yields an explicit formula for the Hardy-Krause variation in terms of

intergrals of partial derivatives, see Leobacher & Pillichshammer [21, Ch.3, p. 59]. In particluar,

the Hardy-Krause variation can be estimated from above by an absolute constant if we

know global bounds on all partial derivatives up to order .

In the remaining part of the introduction we briefly sketch a more general concept of

multidimensional variation which was recently developed in [25].

Let denote an arbitrary family of measurable subsets

of which contains the empty set and

. Let denote the

vectorspace generated by the system of indicator

functions with .

A set

is called an algebraic sum of sets in

if there exist

such that

and is defined to be the collection of algebraic sums of sets in . As in [25] we define the Harman complexity of a non-empty set as the minimal number such there exist with

for some and or . Moreover, set and for

Furthermore, let denote the collection of all measurable, real-valued functions on which can be uniformly approximated by functions in Then the variation of is defined by

| (10) |

and set if The space of functions of bounded variation is denoted by . Important classes of sets are the class of convex sets and the class of axis aligned boxes containing as a vertex. In Aistleitner et al. [2] it is shown that the Hardy-Krause variation coincides with . For various applications the variation seems to be a more natural and suitable concept. A convincing example concerning an application to computational geometry is due to Pausinger & Edelsbrunner [11]. Pauisnger & Svane [25] considered the variation with respect to the class of convex sets. They proved the following version of the Koksma-Hlawka inequality:

where is the isotropic discrepancy of the point set , which is defined as follows

Pausinger & Svane [25] have shown that twice continuously

differentiable functions admit finite ,

and in addition they gave a bound which will be usefull in our context.

Our paper is structured as follows. In Section 2 we introduce specific Markovian models in risk theory where in a natural

way integral equations occur. These equations are based on arguments from renewal theory

and only in particular cases they can be solved analytically. In Section 3 we develop a QMC method for such equations. We give an

error estimates based on Koksma-Hlawka type inequalities for such models.

In Section 4 we compare our numerical results to exact solutions in specific instances.

2 Discounted penalties in the renewal risk model

2.1 Stochastic modeling of risks

In the following we assume a stochastic basis which is large enough to carry all the subsequently defined random variables. In risk theory the surplus process of an insurance portfolio is modeled by a stochastic process . In the classical risk model, going back to Lundberg [22], takes the form

| (11) |

where the deterministic quantities and represent the initial capital and the premium rate. The stochastic ingredient is the cumulated claims process which is a compound Poisson process. The jump heights - or claim amounts - are for which with . The counting process is a homogeneous Poisson process with intensity . A crucial assumption in the classical model is the independence between and . A major topic in risk theory is the study of the ruin event. We introduce the time of ruin , i.e., the first point in time at which the surplus becomes negative. In this setting is a stopping time with respect to the filtration generated by , with . A first approach for quantifying the risk of , is the study of the associated ruin probability

which is non-degenerate if , and satisfies the integral equation

In Gerber & Shiu [12, 13] so-called discounted penalty functions are introduced. This concept allows for an integral ruin evaluation and is based on a function which links the deficit at ruin and the surplus prior to ruin via the function

The time of ruin is included by means of a discounting factor which gives more weight to an early ruin event. In this setting specific choices of allow for an unified treatment of ruin related quantities.

Remark 2.1

When putting a focus on the study of , the condition is crucial. It says that on average premiums exceed claim payments in one unit of time. Standard results, see Asmussen & Albrecher [4], show that under this condition -a.s. From an economic perspective the accumulation of an infinte surplus is unrealistic and risk models including shareholder participation via dividends are introduced in the literature. We refer to [4] for model extensions in this direction.

2.2 Markovian risk model

In the following we consider an insurance surplus process of the form

The quantity is called the initial capital, the cumulated claims are represented by

and the state-dependend premium rate is . The cumulated claims process is given by a

sequence of positive, independently and identically distributed (iid) random variables and a counting process .

For convenience we assume that the claims distribution admits a continuous density .

In our setup we model the claim counting process as a renewal counting process which is specified by the

inter-jump times which are positive and iid random variables. Then, the time of the th jump

is and if we assume that admits a density ,

the jump intensity of the process is . Here denotes the time since the last jump.

A common assumption we are going to adopt, is the independence between and .

We choose, in contrast to classical models, a non-constant premium rate to model the effect of a so-called dividend barrier in a smooth way.

A barrier at level has the purpose that every excess of surplus of this level is distributed as a dividend to shareholders which allows to include

economic considerations in insurance modeling. Mathematically, this means that the process is reflected at level .

Now instead of directly reflecting the process we use the following construction. Fix and for some , define

| (15) |

with some positive and twice continuously differentiable function which fulfills .

Altogether, we assume with some Lipschitz constant and

, , and bounded derivatives , .

Then and the process always stays below level if started in .

A concrete choice for would be

| (16) |

In the following we do not specify any further.

In this setting we add into the definition of the time of ruin, i.e., .

Remark 2.2

In this model setting ruin can only take place at some jump time and since the process is bounded a.s. we have that . If an approximation to classical reflection of the process at level is implemented, then the process virtually started above is forced to jump down to and continue from this starting value. Consequently, we put the focus on starting values .

In the remainder of this section we will study analytic properties of the discounted value function which in this framework takes the form

| (17) |

with and a continuous penalty function .

To have a well defined function, typically the following integrability condition is used

see [4]. Since our process is kept below level and is supposed to be continuous in both arguments we can naturally replace the above condition by

| (18) |

which we will assume in the following. The condition from equation (18) holds true for example,

if and admits a finite -th moment for some .

Remark 2.3

From the construction of we have that with is a piecewise-deterministic Markov process, see Davis [8]. Since the jump intensity depends on , one needs this additional component for the Markovization of . But on the discrete time skeleton with the process has the Markov property.

2.3 Analytic properties and a fixed point problem

We start with showing some elementary analytical properties of the function defined in (17).

Theorem 2.1

The function is bounded and continuous.

Proof.

The boundedness of follows directly from the assumption made in (18).

For proving continuity we split off the expectation defining into two parts which we separately deal with.

Let and observe

For we fix some and notice the following bound

| (19) |

Before going on we need some estimates on the difference of two paths, one starting in and the other in . For fixed we have that on the surplus fulfills with initial condition , is finite with probability one. Standard arguments on ordinary differential equations, see for instance Stoer & Bulirsch [29, Th. 7.1.1 - 7.1.8], yield that an appropriate solution exists and is continuously differentiable in and continuous in the initial value . We even get the bound for fixed , where denotes the path which starts in and the Lipschitz constant of . From these results we directly obtain for a given path

which by iteration results in

because .

Since ruin takes place at some claim occurrence time we get that on

the quantities and

converge to the corresponding quantities started in , all possible differences are bounded by .

Therefore, sending to in (19) and then sending to infinity, we get that converges to zero

because and bounded convergence. We can repeat the argument for when using in (19).

Now consider part . We first observe that .

Consequently, we need to show that tends to zero if or .

Again, fix for which , this implies

that there is a claim amount , occuring at some point in time , for which

i.e., causing ruin for the path started in , , but not causing ruin for the one started in , . From the construction of the drift , it is decreasing to zero, we have that, surpressing the dependence,

Since we have

which approaches zero whenever and tend to each other since is continuous.∎

Define for functions the operator by

| (20) |

The Markov property of the sequence and the definition of in (17) allow us to derive that , or explicitely written

We can state the following lemma.

Lemma 2.2

If , the operator defined in (20) is a contraction with respect to .

Proof.

Let be bounded by some constant , then

is bounded by . From the integral representation of we get continuity in ,

where is the ODE’s solution up to time with . From Stoer & Bulirsch [29, Th. 7.1.4] we have that is continuous

in its initial value which shows that is continuous in .

Let , then

we have for all that

Since and a.s., is contractive with Lipschitz constant . ∎

For a possible application of quasi-Monte Carlo techniques we need to examine the structure of ,

For the probabilistic interpretation of iterated applications of is . Using and we can write

where and

Here, and represents the time of the -th jump. We see that via the path of the process depends on all integration variables

.

For dealing with the situation , i.e., when the contraction argument fails, we can use a probabilistic argument.

Since and we have that

for .

Using we get

pointwise, even in the case if .

In what follows we put the focus on the determination of .

3 Approximation procedure

For the application of QMC methods we need to transform in a first step the integration domain in

to . This is achieved by use of the following substitutions

Here it has to be taken into account that the values of the reserve process have to be calculated recursively, i.e., depends on and . Since the Jacobian matrix of this transformation has a lower triangular form, the determinant can easily be found as . Alltogether, we arrive at

Consequently, for recovering the Koksma-Hlawka type errorbound we need to examine the variation of the integrand:

| (21) |

Here we denote by the solution to with . Consequently, we can write

Or in terms of , putting and

| (22) |

In the following proposition we show that with a particular choice of model parameters it is possible to apply results from [25] to show that the integrand in (3) is in some sense of finite variation. Its proof shows that probabilistic and deterministic model ingredients are considerably interconnected.

Theorem 3.1

Proof.

The main idea of the proof is the application of [25, Th. 3.12]. For this purpose we need to show that , and are finite, with the implication

Since in this theorem the operator (matrix) norm is arbitrary we use the 2-norm and exploit the relation

We will show that is finite for all . At first we observe that when taking derivatives with respect to and , the structure of (22) implies the appearance of the following terms:

The functions correspond to the first and second derivative of the ODE’s solution with respect to the initial value. They can be derived from the

associated first and second order variational equations (see [36]).

From our assumptions on we have that

is bounded by one () and all other derivatives including are bounded as well. The boundedness of can be derived from the

boundedness of and an analysis of the growth behaviour of .

For the structure of we can derive the following

where and a function . is evaluated at the integration points and and its derivatives which themselves are evaluated in points of the form for . If and its derivatives are considered to be variables, neglecting their dependence on s and s, then is a polynomial of degree . The degree of the polynomial is produced by the recursive structure of the paths and its dependence on all previous jump times and sizes. From this inspection we get that under the conditions and all entries of the Hessian matrix are bounded. Furthermore, the conditions on the parameters ensure that is finite and . ∎

Remark 3.1

We can combine the above result with the convergence rate from Banach’s fixed point theorem and obtain for our specific situation

Here denotes the integrand from (3) in dimension , the

isotropic discrepancy of a pointset with elements in and is the QMC approximation for . For the last term we used that is bounded by some and the fact the follows a Gamma distribution .

From the type of arguments we used for the proof of Theorem 3.1, we expect that the result holds true for -distributed inter-claim times and jump heights and with similar conditions on the parameters. Hence the method is also applicable for this more general situation. A detailed study of this claim is part of future research.

4 Numerical results

In this section, we evaluate the integrals from Section 3 by applying Monte Carlo and quasi-Monte Carlo methods for different choices of the penalty function .

4.1 The discounted time of ruin

Letting , we arrive at which is the discounted time of ruin. Lin et al. [35] found an analytic expression for this discounted time of ruin if both the inter-arrival times of the claims and the claim sizes are exponentially distributed. To have a reference value, we also adopt these assumptions and denote the parameters of the exponential distributions with for the parameter of the inter-arrival times and for the parameter of the claim sizes. The premium rate was chosen as in Section 2.2 with from equation (16), with , and was set to . Note that the results of Lin et al. [35] were proved for a reflected process in the classical sense, which means for and for . Since Theorem 3.1 requires a premium rate satisfying certain smoothness conditions, we cannot use a discontinuous and thus have a methodic error in our simulations. However, we will see that this error is, at least for small , very small.

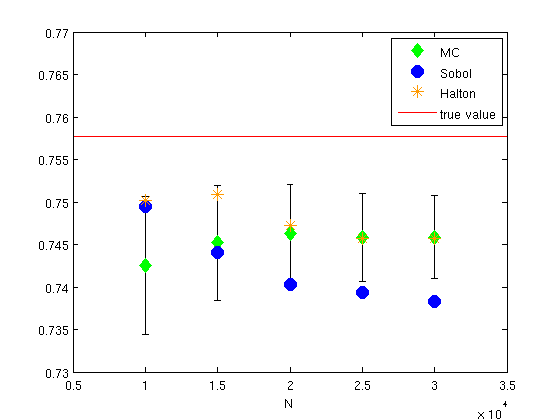

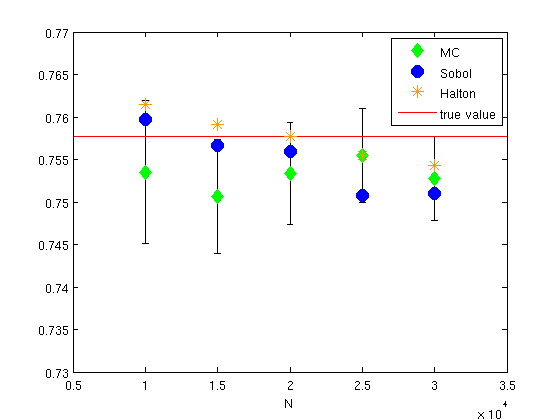

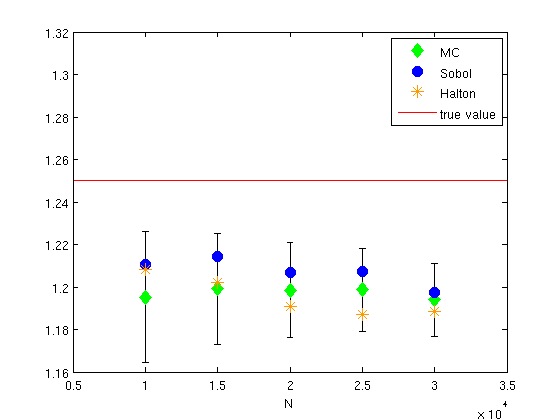

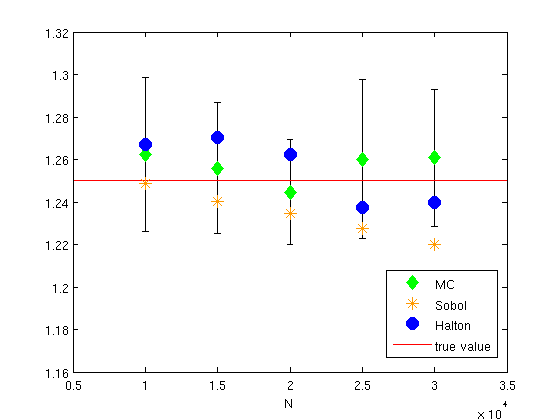

We list the parameters together with the approximation values for increasing numbers of (Q)MC points and iterations of the algorithm in Table 2, whereas Table 2 shows the approximation values for iterations of the algorithm. Figure 2 and Figure 2 show the MC points (green) with confidence intervals, together with QMC points from Sobol sequences (blue) and Halton sequences (orange).

: MC: Sobol: Halton:

: MC: Sobol: Halton:

The red line at height marks the true value. As can be seen in Figure 2, the algorithm has not yet converged for , whereas Figure 2 shows that already yields a very good approximation.

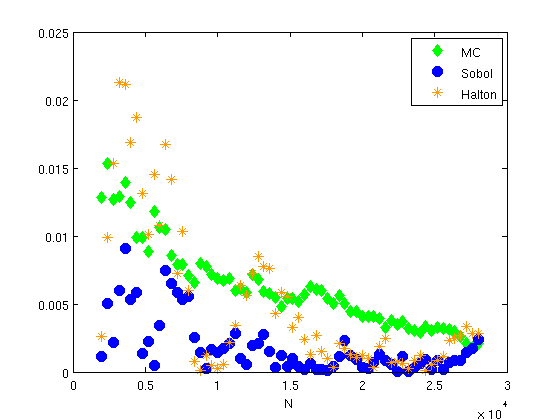

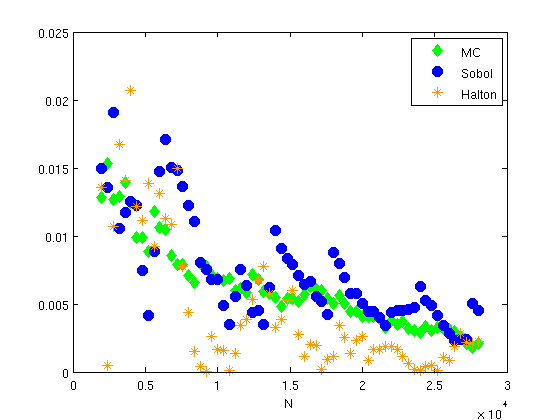

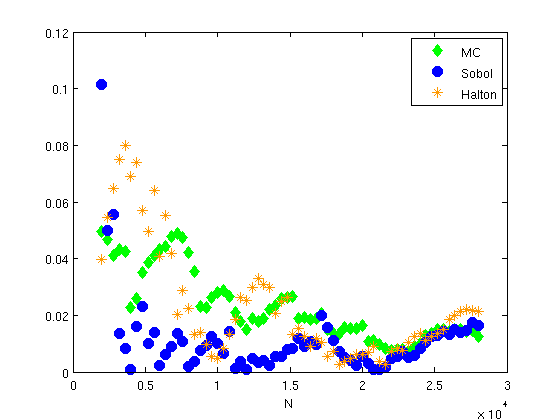

To illustrate the speed of convergence, we also plotted the absolute error, both for the MC approach as well as for QMC points (again taken from Sobol and Halton sequences) for varying numbers of points . Figures 4 and 4 show the values obtained for iterations of the algorithm. Obviously, is also not yet enough to reach the actual value. But notice that the absolute error even for more iterations cannot converge to zero because of the smoothed reflection procedure.

For both of the QMC methods, a scramble improved the results. In the Sobol case however, an “unlucky” choice in the scramble and the skip value (i.e. how many elements are dropped in the beginning) can lead to relatively high variation in the output, whereas the Halton set shows a more stable performance (compare Figures 4 and 4).

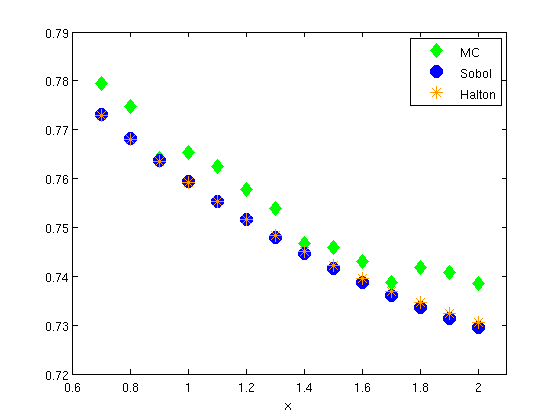

For Figure 5 we evaluated iterations of the algorithm with (Q)MC points for different starting values , ranging from to . As expected, the discounted time of ruin decreases for increasing .

4.2 The deficit at ruin

If we set , and , we have , the expected deficit at ruin. We use the same premium rate as before and again choose exponential distributions for the inter-arrival times and claim sizes with parameters and respectively, since also in this case the true value (for a classically reflected process) can be found in [35]. Figures 7 and 7 show the results for and iterations respectively. The reference value is again shown as a red line, in our case at . The MC points are drawn in green, the Sobol points blue and the Halton points in orange. Table 7 and Table 7 contain the precise values along with the corresponding parameters.

Note again the difference between Figure 7 and Figure 7, resulting from a different number of iterations .

: MC: Sobol: Halton:

: MC: Sobol: Halton:

Again, we plotted the absolute error for iterations of the algorithm and a varying number of (Q)MC points . Figure 8 shows the results using the same colorings as before.

Remark 4.1

We considered in our numerical examples two test cases for which explicit (approximate) reference values are available. Certainly our approach is not restricted to this particular choice of model ingredients - which are , and the penalty function .

References

- [1] C. Aistleitner and J. Dick. Functions of bounded variation, signed measures, and a general Koksma-Hlawka inequality. Acta Arith., 167(2):143–171, 2015.

- [2] C. Aistleitner, F. Pausinger, A. M. Svane, and R. F. Tichy. On functions of bounded variation. Math. Proc. Cambridge Philos. Soc., pages 1–15, to appear.

- [3] H. Albrecher and R. Kainhofer. Risk theory with a nonlinear dividend barrier. Computing, 68(4):289–311, 2002.

- [4] S. Asmussen and H. Albrecher. Ruin probabilities. World Scientific, River Edge, 2nd edition, 2010.

- [5] K. E. Atkinson. The numerical solution of fredholm integral equations of the second kind. SIAM Journal on Numerical Analysis, 4(3):337–348, 1967.

- [6] L. Brandolini, L. Colzani, G. Gigante, and G. Travaglini. A koksma–hlawka inequality for simplices. In Trends in Harmonic Analysis, pages 33–46. Springer, 2013.

- [7] L. Brandolini, L. Colzani, G. Gigante, and G. Travaglini. On the koksma–hlawka inequality. Journal of Complexity, 29(2):158 – 172, 2013.

- [8] M. H. A. Davis. Markov models and optimization. Chapman & Hall, London, 1993.

- [9] J. Dick, P. Kritzer, F. Y. Kuo, and I. H. Sloan. Lattice-nyström method for fredholm integral equations of the second kind with convolution type kernels. Journal of Complexity, 23(4):752–772, 2007.

- [10] M. Drmota and R. F. Tichy. Sequences, discrepancies and applications. 1997.

- [11] H. Edelsbrunner and F. Pausinger. Approximation and convergence of the intrinsic volume. Advances in Mathematics, 287:674–703, 2016.

- [12] H. U. Gerber and E. S. W. Shiu. On the time value of ruin. N. Am. Actuar. J., 2(1):48–78, 1998.

- [13] H. U. Gerber and E. S. W. Shiu. The time value of ruin in a Sparre Andersen model. N. Am. Actuar. J., 9(2):49–84, 2005.

- [14] M. Götz. Discrepancy and the error in integration. Monatshefte für Mathematik, 136(2):99–121, 2002.

- [15] G. Harman. Variations on the Koksma-Hlawka inequality. Unif. Distrib. Theory, 5(1):65–78, 2010.

- [16] E. Hlawka. Funktionen von beschränkter variation in der theorie der gleichverteilung. Annali di Matematica Pura ed Applicata, 54(1):325–333, 1961.

- [17] L. K. Hua and Y. Wang. Applications of number theory to numerical analysis. Springer-Verlag, Berlin-New York; Kexue Chubanshe (Science Press), Beijing, 1981. Translated from the Chinese.

- [18] Y. Ikebe. The galerkin method for the numerical solution of fredholm integral equations of the second kind. Siam Review, 14(3):465–491, 1972.

- [19] L. Kuipers and H. Niederreiter. Uniform distribution of sequences. Courier Corporation, 2012.

- [20] F. Y. Kuo. Component-by-component constructions achieve the optimal rate of convergence for multivariate integration in weighted korobov and sobolev spaces. Journal of Complexity, 19(3):301–320, 2003.

- [21] G. Leobacher and F. Pillichshammer. Introduction to quasi-Monte Carlo integration and applications. Compact Textbook in Mathematics. Birkhäuser/Springer, Cham, 2014.

- [22] F. Lundberg. Approximerad framställning av sannolikhetsfunktionen. Aterförsäkring av kollektivrisker. Akad. Afhandling. Almqvist o. Wiksell, Uppsala, 1903.

- [23] E. Novak and H. Woźniakowski. Tractability of Multivariate Problems: Standard information for functionals, volume 12. European Mathematical Society, 2010.

- [24] A. B. Owen. Multidimensional variation for quasi-Monte Carlo. In Contemporary multivariate analysis and design of experiments, volume 2 of Ser. Biostat., pages 49–74. World Sci. Publ., Hackensack, NJ, 2005.

- [25] F. Pausinger and A. M. Svane. A Koksma-Hlawka inequality for general discrepancy systems. J. Complexity, 31(6):773–797, 2015.

- [26] I. H. Sloan. A quadrature-based approach to improving the collocation method. Numerische Mathematik, 54(1):41–56, 1988.

- [27] I. H. Sloan and J. N. Lyness. The representation of lattice quadrature rules as multiple sums. Mathematics of computation, 52(185):81–94, 1989.

- [28] I. H. Sloan and H. Woźniakowski. Tractability of multivariate integration for weighted korobov classes. Journal of Complexity, 17(4):697–721, 2001.

- [29] J. Stoer and R. Bulirsch. Numerische Mathematik. 2. Springer-Lehrbuch. [Springer Textbook]. Springer-Verlag, Berlin, fourth edition, 2000. Eine Einführung—unter Berücksichtigung von Vorlesungen von F. L. Bauer. [An introduction, with reference to lectures by F. L. Bauer].

- [30] R. F. Tichy. Über eine zahlentheoretische Methode zur numerischen Integration und zur Behandlung von Integralgleichungen. Österreich. Akad. Wiss. Math.-Natur. Kl. Sitzungsber. II, 193(4-7):329–358, 1984.

- [31] S. Twomey. On the numerical solution of fredholm integral equations of the first kind by the inversion of the linear system produced by quadrature. Journal of the ACM (JACM), 10(1):97–101, 1963.

- [32] Brunner, H.: Iterated collocation methods and their discretizations for Volterra integral equations. SIAM J. Numer. Anal. 21(6), 1132–1145 (1984)

- [33] Brunner, H.: Implicitly linear collocation methods for nonlinear Volterra equations. Appl. Numer. Math. 9(3), 235–247 (1992)

- [34] Kumar, S., Sloan, I.H.: A new collocation-type method for Hammerstein integral equations. Math. Comp. pp. 585–593 (1987)

- [35] Lin, X.S., Willmot, G.E., Drekic, S.: The classical risk model with a constant dividend barrier: analysis of the Gerber–Shiu discounted penalty function. Insurance Math. Econom. 33(3), 551–566 (2003)

- [36] Grigorian, A.: Ordinary differential equation. Lecture notes, available at https://www.math.uni-bielefeld.de/~grigor/odelec2009.pdf (2009)

Institute of Analysis and Number Theory, Graz University of Technology, Steyrergasse 30/II, 8010 Graz, Austria

E-mail addresses: preischl@math.tugraz.at, stefan.thonhauser@math.tugraz.at, tichy@tugraz.at