Mellin-Meijer-kernel density estimation on

Abstract

Nonparametric kernel density estimation is a very natural procedure which simply makes use of the smoothing power of the convolution operation. Yet, it performs poorly when the density of a positive variable is to be estimated (boundary issues, spurious bumps in the tail). So various extensions of the basic kernel estimator allegedly suitable for -supported densities, such as those using Gamma or other asymmetric kernels, abound in the literature. Those, however, are not based on any valid smoothing operation analogous to the convolution, which typically leads to inconsistencies. By contrast, in this paper a kernel estimator for -supported densities is defined by making use of the Mellin convolution, the natural analogue of the usual convolution on . From there, a very transparent theory flows and leads to new type of asymmetric kernels strongly related to Meijer’s -functions. The numerous pleasant properties of this ‘Mellin-Meijer-kernel density estimator’ are demonstrated in the paper. Its pointwise and -consistency (with optimal rate of convergence) is established for a large class of densities, including densities unbounded at 0 and showing power-law decay in their right tail. Its practical behaviour is investigated further through simulations and some real data analyses.

1 Introduction

Kernel density estimation is a very popular nonparametric method which enables estimation of an unknown probability density function without making any assumption on its functional shape. Its main ingredients are a kernel function , typically a unit-variance probability density symmetric around 0, and a smoothing parameter fixed by the analyst, which controls the smoothness of the resulting estimate. One usually defines , the rescaled version of which has standard deviation . A common choice for is the standard normal density . Then, the estimator simply makes use of the well-known smoothing power of the convolution operation. Specifically, consider a sample drawn from a distribution admitting a density , and define its empirical measure , where and is the usual Dirac delta. The conventional kernel density estimator of is just

| (1.1) |

Expanding this convolution yields the familiar expression:

| (1.2) |

The statistical properties of are well understood (Wand and Jones, 1995, Härdle et al, 2004), and its merit is widely recognised when the support of is the whole real line . Unfortunately, when the support of admits boundaries, the good properties of (1.2) are usually lost.

A case of bounded support of major importance is when is the distribution of a positive random variable , with density supported on . Typically, those distributions are skewed, with showing a maximum at or near the boundary 0 and a long tail on the right side. Sometimes, the behaviour of the density close to 0 is what mostly matters for the analyst; in other cases, it is rather the tail behaviour which is the main focus, for instance when high quantiles (e.g., Value-at-Risk) are of interest. Yet, (1.2) fails to correctly estimate both the behaviour of close to 0 and in the tail. Close to 0, the estimator suffers from boundary bias: the terms corresponding to ’s close to 0 typically overflow beyond the boundary and place positive probability mass in the forbidden area, generally preventing consistency of the estimator there (Wand and Jones, 1995, Section 2.11). In the tail region, where data are usually sparse, it produces ‘spurious bumps’ (Hall et al, 2004), i.e. artificial local maxima at each observed value, thus performing poorly as well.

Hence modifications and extensions of (1.2), attempting to make it suitable for -supported densities, abound in the literature. Early attempts at curing boundary effects looked for correcting close to 0. Those include the ‘cut-and-normalised’ method and its variants based on ‘boundary kernels’ (Gasser and Müller, 1979, Müller, 1991, Jones, 1993, Jones and Foster, 1996, Cheng et al, 1997, Zhang et al, 1999, Dai and Sperlich, 2010), the reflection method (Schuster, 1985, Karunamuni and Alberts, 2005), and other types of local data alteration (Cowling and Hall, 1996, Hall and Park, 2002, Park et al, 2003). These methods are essentially ad hoc manual surgeries on (1.2) close to 0, and have shown their limitations. In addition, as they leave the tail area untouched, they do not address the ‘spurious bumps’ at all.

Later, the problem was approached from a more global perspective and (1.2) was generalised as

| (1.3) |

where is an asymmetric -supported density whose parameters are functions of and a smoothing parameter . Using asymmetric kernels supposedly enables the estimator to take the constrained nature of the support of into account. In his pioneering work, Chen (2000) took to be the Gamma density with shape parameter and rate , defining the ‘first’ Gamma kernel density estimator, viz.

| (1.4) |

(we use instead of Chen’s original for the smoothing parameter, for consistency with standard notation). Although more types of asymmetric kernels were investigated in the subsequent literature (Log-Normal, Jin and Kawczak (2003), Igarashi (2016); Birnbaum-Saunders, Jin and Kawczak (2003), Marchant et al (2013), Igarashi and Kakizawa (2014); Inverse Gaussian and reciprocal Inverse Gaussian distributions, Scaillet (2004), Igarashi and Kakizawa (2014)), none really outperformed Chen’s Gamma kernel density estimator which remains some sort of ‘gold standard’ in the field. Its properties were further investigated in Bouezmarni and Scaillet (2005), Hagmann and Scaillet (2007), Zhang (2010) and Malec and Schienle (2014). Asymmetric kernel density estimation remains an area of very active research, as the number of recent papers in the area evidences (Kuruwita et al, 2010, Jeon and Kim, 2013, Dobrovidov and Markovich, 2014, Igarashi and Kakizawa, 2014, Hirukawa and Sakudo, 2014, Funke and Kawka, 2015, Markovich, 2015, Hoffmann and Jones, 2015, Funke and Hirukawa, 2016, Igarashi, 2016, Markovich, 2016, Rosa and Nogueira, 2016, Balakrishna and Koul, 2017). Hirukawa and Sakudo (2015) describe a family of ‘generalised Gamma kernels’ which includes a variety of similar asymmetric kernels in an attempt to standardise those results.

‘Ironically’, as Jones and Henderson (2007, Section 2) put it, such asymmetric kernel estimators do not really address boundary problems. Indeed, generally nothing prevents (1.3) from taking positive values for . For instance, (1.4) is defined and positive for as long as . This explains why those estimators need a further correction near the boundary (‘second’ Gamma kernel estimator in Chen (2000), also known as ‘modified’ Gamma kernel estimator; see also Conditions 1 and 2 in Hirukawa and Sakudo (2015)), performing yet another ‘manual surgery’ on an initially unsuitable estimator around 0. Worse, even the modified version of the Gamma kernel estimator was somewhat picked apart in Zhang (2010) and Malec and Schienle (2014).

Actually, those problems arise from the fact that estimators like (1.3) are, in general, not induced by any valid smoothing operation analogous to (1.1) on . Beyond questioning the mere validity of the construction, this has some unpleasant consequences. Those include that (1.3) does not automatically integrate to one, hence is not a bona fide density (and manually rescaling the estimate usually produces some extra bias). Also, in contrast to the obvious visible in (1.2), it is not clear how (1.3) actually appreciates the proximity between and the observations ’s relative to . The local nature of (1.3) is only induced by making the parameters of the kernel heuristically depend on and in a way barely driven by any intuition: see for instance (1.4) or Hirukawa and Sakudo (2015, Section 2.3.1) for more general expressions. This spoils the intuitive simplicity of the initial kernel density estimation scheme.

These observations demonstrate the need for an asymmetric kernel density estimator based on a simple, natural and transparent methodology, and with good theoretical and practical properties. This paper precisely suggests and studies such a methodology, finding its inspiration from yet another popular approach for kernel estimation of -supported densities: support transformation (Copas and Fryer, 1980, Silverman, 1986, Wand et al, 1991, Marron and Ruppert, 1994, Ruppert and Cline, 1994, Geenens, 2014, Geenens and Wang, 2016). Define . Kernel estimation of the density of should be free from boundary issues, as is supported on . From standard arguments, one has , which suggests, upon estimation of by some estimator , the estimator for . If one uses a basic kernel estimator like (1.2) for estimating , one obtains the closed form

| (1.5) |

With the Gaussian kernel in (1.5), one gets

| (1.6) |

Interestingly, this can be written

| (1.7) |

where is the log-Normal density with parameters and . It seems, therefore, fair to call this estimator (1.6) the log-Normal kernel density estimator – remarkably, it is different to Jin and Kawczak (2003)’s and Igarashi (2016)’s homonymous estimators. It can be shown (Geenens and Wang, 2016) that, under suitable conditions,

| (1.8) | ||||

| (1.9) |

as , and . However, and despite being simple and natural, (1.5)-(1.6) shows very disappointing performance in practice, see for instance Figure 2.13 in Silverman (1986) or Figure 2.1 in Geenens and Wang (2016). This estimator as-is has consequently been given little support in the literature.

There are, however, two important observations to make. The first is that this ‘log-Normal kernel density estimator’ as (1.7) is an asymmetric kernel density estimator but of a different nature to (1.3). Here is an asymmetric -supported density whose parameters are functions of and a smoothing parameter , that is, the roles of and have been swapped around compared to (1.3). Surprisingly, estimators of type (1.7) have not been investigated much in the literature, two notable exceptions being Jeon and Kim (2013) and the discusssion in Hoffmann and Jones (2015). Yet, (1.7) is as valid a generalisation of (1.2) as (1.3): being symmetric in (1.2), and can be switched imperceptibly. For instance, in the case , it is actually irrelevant whether is or (where is the -density). In the asymmetric case, though, the respective roles of and are of import.

Working with a proper density in is more natural, though. Clearly, automatically, and for . Hence (1.7) cannot assign probability weight to the negative values, which attacks the above-described boundary problem at the source. Also, typically shares the same right-skewness as the density to be estimated, and this is usually beneficial to the estimator in the tail area (no more ‘spurious bumps’). It is not clear why estimators of type (1.7) have remained so inconspicuous in the literature so far.

The second important observation is how (1.5) really addresses the boundary isssue. This will be discussed in detail in Section 2.1, and will suggest a simple redefinition of (1.1) suitable for -supported densities. From there, a very natural methodology will flow and will lead to a new asymmetric kernel density estimator of type (1.7), based on a valid and intuitive smoothing operation on . As it will be seen, the new estimator shares some similarities with the ‘convolution power kernel density estimator’ of Comte and Genon-Catalot (2012) and with the ‘varying kernel density estimator’ of Mnatsakanov and Sarkisian (2012). The latter estimator actually arose as a by-product from those authors’ previous work on recovering a probability distribution from its moments (Mnatsakanov and Ruymgaart, 2003, Mnatsakanov, 2008). The appropriate tool for solving that so-called Stieltjes moment problem was seen to be the Mellin transform (Mellin, 1896), and our estimator also has a strong ‘Mellin flavour’. The kernel functions that fit naturally in this framework belong to a family of -supported distributions strongly related to Meijer’s -functions (Meijer, 1936, Bateman and Erdélyi, 1953) – the duality between the Mellin transform and Meijer’s -functions was elucidated in Marichev (1982). Hence we call the whole methodology Mellin-Meijer-kernel density estimation on . The numerous pleasant properties of the estimator will be exhibited throughout the paper: it relies on a natural smoothing operation on , whereby it avoids any inconsistency; it has a closed form expression easy-to-understand intuitively; it always produce a bona fide density; the smoothness of its estimates is controlled by a natural smoothing parameter; it is consistent for densities potentially unbounded at the boundary and admitting power-law decay in the right tail; it reaches optimal MISE-rate of convergence over under mild assumptions; etc. In addition, its theoretical properties are derived directly through the Mellin transform theory, which make all the proofs very transparent. Properties of the estimator ‘in the Mellin world’ also suggest an easy way of selecting the always crucial smoothing parameter in practice.

The paper is structured as follows: Section 2 motivates the ‘Mellin-Meijer’ construction and revise the main properties of the Mellin transform and the Meijer -functions. Section 3 defines the estimator, while in Section 4 its theoretical properties are derived. Section 5 suggests an easy way to select the smoothing parameter. Section 6 and Section 7 investigate the performance of the estimator in practice, through simulations and real data examples, respectively. Section 8 summarises the main ideas of the paper and offers some perpectives for continuing this line of research. Futher properties, proofs and technical lemmas are provided in Appendix.

2 Preliminaries

2.1 Motivation

The very origin of the boundary issues of (1.2) is easy to understand. The convolution of two probability densities is known to be the density of the sum of two independent random variables having respective densities and . Hence, smoothing is achieved in (1.1) through ‘diluting’ each observation by adding to it some continuous random noise with density . This does not cause any inconsistency if is -supported, but it does if is -supported. Indeed, may take on negative values, and will surely do so for the small ’s. This produces an estimated density that ‘spills over’. In response to that, (1.5) first sends the observations onto the whole through the log-transformation, adds to them some random disturbance of mean 0 and variance , and moves everything back to by exponentiation. So, in terms of what happens on , (1.5) realises smoothing by multiplying each observation by a positive random disturbance . In the particular case of (1.6), has a certain log-Normal distribution.

In algebraic terms, the conventional estimator (1.1)-(1.2) is justified on because is a group. By contrast is not, which causes issues for -supported densities. Now, is a group. Naturally, it is isomorphic to through the transformation, and this is what theoretically validates estimator (1.5). However, the benefits of distorting to forcibly move back to are not clear – the presence of and in the bias expression (1.8) is precisely caused by that distortion (the bias of the conventional estimator (1.2) only involves ). It seems more natural to define a kernel estimator directly in , which would address in a forthright manner the particular challenges arising in that environment.

The estimator suggested in this paper will thus realise smoothing by multiplying each observation by a random disturbance whose density is supported on , generalising by a large extent the log-Normal kernel density estimator (1.6). It will heavily rely on properties of the Mellin transform, the “natural analytical tool to use in studying the distribution of products and quotients of independent random variables”, as Epstein (1948) described it. The next section briefly reviews the properties of that transform which will be useful in this paper.

2.2 Mellin transform and Mellin convolution

The Mellin transform of any locally integrable -supported function is the function defined on the complex plane as

| (2.1) |

when the integral converges. The change of variable shows that the Mellin transform is directly related to the Laplace and Fourier transforms and suggests that it is, in some sense, equivalent to them. This is only partly true, as Butzer et al (2014) noted. There are many situations where it appears more convenient to stick to the Mellin form, and the problem studied here is surely one of those. If, for some and ,

| (2.2) |

then (2.1) converges absolutely on the vertical strip of the complex plane . It can be shown that is holomorphic on – therefore known as the strip of holomorphy of – and uniformly bounded on any closed vertical strip of finite width entirely contained in . There is a one-to-one correspondence between the function and the couple , in the sense that two different functions may have the same Mellin transform, but defined on two non-overlapping vertical strips of the complex plane. For instance, the function has, by definition, Euler’s Gamma function as Mellin transform for , but for any real nonnegative integer , the restriction of to is actually the Mellin transform of

| (2.3) |

by the Cauchy-Saalschütz representation of (Temme, 1996, Section 3.2.2). It is thus equivalent to know or in a given vertical strip of . In particular, can be recovered from by the inverse Mellin transform: for all ,

| (2.4) |

for any real . From Cauchy’s residue theorem, the integration path can be displaced sideways inside without affecting the result of integration, so the value of (2.4) is independent of the particular constant , and the integral is absolutely convergent. See Sneddon (1974, Chapter 4), Wong (1989, Chapter 3), Paris and Kaminski (2001, Chapter 3), Graf (2010, Chapter 6) or Godement (2015, Section VIII.13) for comprehensive treatments of the Mellin transform. A exhaustive table of Mellin transforms and inverse Mellin transforms is provided in Bateman (1954, Chapters VI and VII).

Now, if is the probability density of a positive random variable , then

| (2.5) |

Hence the line always belongs to the strip of holomorphy of Mellin transforms of all probability density functions supported on . So there will never be any ambiguity about the strip of holomorphy here, which will allow to be unequivocally represented by its Mellin transform , and vice-versa. In the above example, is the only probability density with Mellin transform , as that is the only such that and . This also makes clear the essential role of the value in this framework.

From (2.1), one clearly has

| (2.6) |

thus actually defines all real, complex, integral and fractional moments of . Hence, for a probability density, the strip of holomorphy of is actually determined by the existence (finiteness) of the real moments of :

| (2.7) |

In view of (2.2), for light-tailed densities whose all positive moments exist, while is bounded from the right () for fat-tailed densities with only a certain number of finite positive moments.111The qualifiers ‘fat’, ‘heavy’ or ‘long’ have sometimes found different meanings in the literature when describing the tails of a distribution. In this paper, by ‘fat-tailed’ distribution we mean explicitly this: a distribution whose not all positive power moments are finite. Hence here we consider the log-Normal as ‘light-tailed’, although it is is generally regarded as ‘heavy-tailed’ in many other references. Similarly, for densities whose all negative moments exist – let us call such densities ‘light-headed’, while is bounded from the left () for ‘fat-headed’ densities, for which some negative moments are infinite.

From (2.6), and given that moments of products of independent random variables are the products of the individual moments, the density of the product of two independent positive random variables with respective densities and , has Mellin transform

| (2.8) |

From standard arguments, one also knows that

| (2.9) |

This operation, that we will denote , is called Mellin convolution, owing to the equivalence

| (2.10) |

Clearly, Mellin transform/Mellin convolution play the same role for products of independent random variables as Fourier transform/convolution for sums of independent random variables.

Some important operational properties of the Mellin transform can be found in Appendix A. Those are useful for easily obtaining the Mellin transform of common -supported probability densities.

Example 2.1.

Gamma density: Consider the Gamma-density, i.e.,

| (2.11) |

By definition, (). By (A.2), it follows (), and by (A.4), (). Finally, by (A.1), we obtain

| (2.12) |

The strip of holomorphy is bounded from the left, but not from the right: the Gamma density is fat-headed and light-tailed, it has all its positive moments but only those negative moments for .

Example 2.2.

Inverse Gamma density: Consider the Inverse Gamma-density , i.e. the density of the random variable if has the above Gamma-distribution. Standard results on functions of random variables show that

| (2.13) |

that is,

| (2.14) |

Combining (A.3) and (A.4), it follows directly from (2.13) that . The Mellin transform of (2.14) is thus

| (2.15) |

Its strip of holomorphy is bounded from the right, but not from the left. The Inverse Gamma distribution is light-headed and fat-tailed, as expected from its definition and Example 2.1.

The Gamma and Inverse Gamma densities are just two very particular cases of a huge class of -supported densities which have Mellin transforms of similar tractable form, viz. (rescaled) ratios of Gamma functions. Given that the whole kernel density estimation methodology proposed in this paper will rely on Mellin-convolution ideas, those densities are the natural candidates for acting as ‘kernel’ in our framework. We define such densities, called Meijer densities, in Section 2.4, after a brief review of Meijer’s -functions.

2.3 Meijer’s -functions

Meijer (1936) introduced the -functions as generalisations of the hypergeometric functions. There are three types of -functions, one of them being the following Barnes integral: for ,

for and ( are natural numbers), and for some constant ensuring the existence of the integral. Through the change of variable , this is also

| (2.16) |

with , which shows by (2.4) that has Mellin transform

| (2.17) |

on some strip of the complex plane containing . In particular, the -function has Mellin transform

| (2.18) |

on the strip (provided ). The -functions are very general functions whose particular cases cover most of the common, useful or special functions defined on . See Bateman and Erdélyi (1953, Section 5.3) or Mathai and Saxena (1973) for more details, or Beals and Szmigielski (2013) for a recent short review.

2.4 Meijer densities

For some and , consider the -supported function whose Mellin transform is

| (2.19) |

on the strip of holomorphy

| (2.20) |

Clearly, for all and , , hence , by (2.5). In fact, the following result shows that is always a valid probability density.

Proposition 2.1.

Proof.

See Appendix. ∎

The proof uses the representation of an -distributed random variable as a (rescaled) product of two independent Gamma and Inverse Gamma random variables. This allows us to extend (2.19) to the cases and as well. Set

| (2.21) | ||||

| (2.22) |

Lemma A.1 in Appendix, (2.12) and (2.15) make the density of for and the density of for , in agreement with the usual interpretation of the -distribution with infinite (either numerator or denominator) degrees of freedom.

The strip of holomorphy (2.20) clarifies how the parameters , and act on the lightness/fatness of the head and the tail of the density . The ratio fixes the ‘overall fatness’ of : the higher the value of , the fatter both its head and its tail. How exactly that overall fatness is shared between the head and the tail of is specified by : produces a density with as light a tail and as fat a head as can be (given the other parameters), while produces a density with as fat a tail and as light a head as can be (given the other parameters). The balanced case is, of course, for . Thus, by playing with the values of , and , one can produce a wide variety of different head and tail behaviours for . Those include exponential behaviours ( or , or ), and positiveness/unboundedness at , for (see that then, , meaning that and cannot be as ).

We call a probability density whose Mellin transform can be written under the form (2.19) (or its simplified versions (2.21) and (2.22)) for some and , a Meijer density. Indeed, all densities defined through (2.19), having for Mellin transform a rescaled product of two Gamma functions as in (2.18), are rescaled versions of a -Meijer function. Specifically, for , it can be checked that

| (2.23) |

giving explicit forms for those densities in terms of . Similar, appropriately simplified expressions in terms of and are valid for as well. Most of the -supported probability distributions of practical interest are actually Meijer distributions. These include, but are not limited to, the Amoroso/Stacy (i.e., Generalised Gamma), Beta prime, Burr, Chi, Chi-squared, Dagum, Erlang, Fisher-Snedecor, Fréchet, Gamma, Generalised Pareto, Lévy, Log-logistic, Maxwell, Nakagami, Rayleigh, Singh-Maddala and Weibull distributions; see Table A.1 in Appendix A.2. All the ‘inverse’ distributions of these, such as the Inverse Gamma, are also Meijer distributions, as it appears clearly from (2.19) and Corollary A.1 that the class of Meijer distributions is closed under the ‘inverse’ operation. Finally, they admit the log-Normal distribution as limiting case as . In fact, being essentially the density of a certain power of an -distributed random variable, it has strong links to what has sometimes been called the Generalised -distribution in the literature (Prentice, 1975, McDonald, 1984, Cox, 2008).

Remark 2.1.

It is possible to define probability densities as appropriate rescaled versions of general -functions (2.16) for as well. Their Mellin transform would involve a ratio of Gamma factors, as in the full form (2.17). Given the richness of the class of densities defined through , though, the form (2.19) seems sufficient for many purposes.

From (2.19), the basic properties of densities (2.23) are actually easy to obtain. In particular, the coefficient of variation of will be of interest in the next sections.

Proposition 2.2.

If and , the density has coefficient of variation equal to

| (2.24) |

Proof.

See Appendix. ∎

According to the above observations, if (resp. ) then the factors containing (resp. ) would not appear in (2.24). Also, the parameter does not affect the value of , which was expected given the purely multiplicative nature of its role as described by Proposition 2.1. For , (2.24) can be simplified using the recursion formula (). For instance, for one finds

| (2.25) |

Clearly, in this case, as . In fact, this asymptotic equivalence holds true in general.

Proposition 2.3.

Let and be fixed, and let . Then, the coefficient of variation of is asymptotically equivalent to : , as .

Proof.

See Appendix. ∎

The following asymptotic expansion of (2.19) as will also be of importance in the next sections.

Proposition 2.4.

Consider the Meijer density as described above. Fix and . Let and for some real constant . Then, the Mellin transform of (2.19) admits the following expansion:

| (2.26) |

where , provided .

Proof.

See Appendix. ∎

Remark 2.2.

The choice yields the simple form

| (2.27) |

which only involves explicitly.

Finally, the Mellin transform of , described by the following result, will also be used.

Proposition 2.5.

Consider the Meijer density as described above. The Mellin transform of is

| (2.28) |

where is the Beta function, on the strip of holomorphy

| (2.29) |

Fix and . Let and for some real constant . Then we have the asymptotic expansion

| (2.30) |

where , provided .

Proof.

See Appendix. ∎

3 Mellin-Meijer kernel density estimation

3.1 Basic idea

Following the idea introduced in Section 2.1, we define a ‘Mellin’ version of the kernel estimator of a density supported on as

| (3.1) |

where is again the sample empirical measure and is an -supported density whose ‘spread’ (to make precise later) is driven by a parameter playing the role of smoothing parameter. Obviously, (3.1) is just the multiplicative analog of (1.1). From (2.9), we have , that is

| (3.2) |

Estimator (3.2) assesses which observations are local to through the ratios , which is natural on . Similarities and differences between (3.2) and expression (2) in Comte and Genon-Catalot (2012) and expression (2.4) in Mnatsakanov and Sarkisian (2012), are easy to identify. In particular, neither of those two estimators integrates to one, whereas always defines a bona fide density: given that is a density, it is obvious that and . In addition, in contrast to estimators of type (1.3), estimator (3.2) is constructed as a sum of ‘bumps’ , which makes it easy to understand visually – see Härdle et al (2004, Section 3.1.5) for related comments in the case of the conventional kernel density estimator (1.2). Figure 3.1 (left panel) illustrates this for an artificial sample of size .

Unlike in the conventional case, though, here the ‘bumps’ do not have the same width. By definition, is the density of the random variable , where has density and is fixed. If and are the mean and standard deviation of , then has standard deviation , obviously different for each . Hence, to an extent driven by , the bumps corresponding to the ’s close to the boundary 0 are high and narrow, while those in the right tail are wide and flat (Figure 3.1, left). More smoothing is thus automatically applied in the tail than close to the boundary (‘adaptive behaviour’), and this is essentially how both boundary issues and the ‘spurious bumps’ problem are addressed by (3.1)-(3.2).

Given that has mean , what is common to all the ’s is actually their coefficient of variation . Note that this is also the coefficient of variation of , the ‘canonical’ bump for . This points out the natural role of the coefficient of variation of the kernel in this framework, suggesting to defining it as the global smoothing parameter .

3.2 Boundary undersmoothing, tail oversmoothing and smoothing transfer

Unfortunately, this idea has to be slightly amended. The reason is that the seemingly desirable ‘adaptive behaviour’ described in the previous section actually occurs in excess. Given that for , the effective amount of smoothing applied in the boundary area is virtually nil. As a result, the basic estimator (3.2) severely undersmooths close to 0 (regardless of the value of ), and typically shows a very rough and erratic behaviour there (Figure 3.1, left). On the other hand, the effective amount of smoothing applied in the tail area is very high, as gets huge as does. Visually less disturbing, this severe oversmoothing effect usually goes unnoticed, but it exists nonetheless.

Theoretically, this ‘boundary undersmoothing/tail oversmoothing’ behaviour materialises through a factor in the asymptotic variance expression – see e.g. (1.9), recalling that the log-Normal kernel density estimator (1.6) is a particular case of (3.2) with being a Log-Normal density.222The same factor appears in variance expressions of many other estimators, including Comte and Genon-Catalot (2012)’s, Jin and Kawczak (2003)’s, Marchant et al (2013)’s and Mnatsakanov and Sarkisian (2012)’s. In fact, this arises because the Haar measure on is . It has thus a mere topological origin, and cannot really be thought of as a deficiency of the idea: the estimator does exactly what it is supposed to do in . It remains, though, that the so-produced estimates are visually unsatisfactory, which calls for some adjustment. What is suggested here is a very natural (as opposed to an ad-hoc correction) smoothing transfer operation: given that the basic estimator smooths too much in the tail and not enough at the boundary, make it use some of the amount of smoothing in excess in the tail for filling the shortage of smoothing at the boundary.

This transfer is easily achieved by making the coefficient of variation of a decreasing function of , instead of keeping it constant for all . One can think of setting , with some smoothing parameter. This enforces for all , i.e., all the ‘bumps’ have the same width (same standard deviation). Of course, means that one exactly adapts to the ‘Haar geometry’ of . As a result, the whole extra amount of smoothing initially applied in the tail is transferred back to the boundary area, and the exact same level of smoothing is applied all over . This means, however, that the adaptive behaviour of the initial estimator has been destroyed entirely, which typically implies the resurgence of boundary issues (bias) and spurious bumps in the tail. This is not desirable.

A natural trade-off between ‘full adaptation’ and ‘no adaptation’ to the Haar geometry is achieved by setting or

| (3.3) |

for some smoothing parameter . Both choices produce equivalent estimators asymptotically ( as , see Assumption 4.4 below), however (3.3) typically produces more stable estimates in practice, as stays bounded for . Hence (3.3) will be the preferred option throughout the rest of the paper. In any case, now , and the bumps remain wider in the tail than at the boundary. The estimator keeps adapting to the boundary and tail areas, but not as excessively as previously. This is illustrated in Figure 3.1 (right panel) for the same sample and with the same smoothing parameter as in the left panel: the ‘bumps’ at the boundary are no more as narrow, and the bumps in the tail no more as flat, as in the initial case. The final estimate of seems rightly smooth all over .

Figure 3.1 highlights another major benefit of allowing to depend on : now the bumps vary in shape as well. In the basic case (3.2), all the bumps are just rescaled versions of , hence have the same shape. In particular, if is such that , then the basic estimator automatically, no matter what the data show in the boundary area (Figure 3.1, left).333This problem of ‘’ is shared by many other kernel estimators of -supported densities, including Jin and Kawczak (2003)’s, Scaillet (2004)’s, Marchant et al (2013)’s and Mnatsakanov and Sarkisian (2012)’s. This is no more the case when may have different coefficients of variation. For instance, in Figure 3.1 (right), the bumps associated to the data close to 0 are no more tied down to 0: as their coefficient of variation increases, they are forced to climb along the -axis. This enables the final estimator to take a positive and even infinite value at .

This justifies to define a ‘refined’ version of estimator (3.1) as

| (3.4) |

where each is an -supported density whose coefficient of variation depends on both an overall smoothing parameter and on through (3.3). Explicitly, this is

| (3.5) |

The observations made about (3.2) obviously remain valid: is always a valid probability density, it assesses the proximity between and through their ratio , etc. Actually, (3.5) is just another version of (3.2) which allows a better allocation of the total amount of smoothing applied, but without affecting the intuitive simplicity of the basic estimator.

Remark 3.1.

Estimator (3.5) may be thought of as a ‘sample-smoothing’ kernel estimator (Terrell and Scott, 1992), in the sense that the smoothing parameter associated with a particular ‘bump’, here , varies with . However, conventional ‘sample-smoothing’ aims to produce adaptive estimators by using a large bandwidth where data are sparse, i.e. when the density is low, and a small bandwidth where data are abundant, i.e. where is high, see e.g. Abramson (1982)’s square-root law. As a result, it typically requires pilot estimation of , which is not without causing further issues (Terrell and Scott, 1992, Hall et al, 1995). Here, ‘sample-smoothing’ is deterministically articulated around (3.3) – obviously, no pilot estimation is necessary – and just aims to adjust to the particular ‘Haar geometry’ of .

3.3 Meijer kernels

Owing to the connection between Mellin transforms and Meijer densities expounded in Section 2, using kernels of Meijer type seems natural here. Hence, consider taking for in (3.4)-(3.5) a Meijer density as described in Section 2.4. Fix the parameters and and keep them constant for all . Those essentially determine the type of kernels that will be used. E.g., if we take and , then the ’s are Gamma densities; with and , then the ’s are Inverse Gamma densities; with and , the ’s are Nakagami densities, etc.; refer to Table A.1 in Appendix A.2. In some sense, chosing and is akin to chosing which kernel (e.g. Epanechnikov or Gaussian) to work with in the conventional case (1.2). Here, though, this choice should be made more carefully, as and drive the head and tail behaviour of the kernels (Section 2.4). If it is anticipated that has a fat tail and/or head, then it seems intuitively clear that working with kernels with fat tails and/or heads should be beneficial to the estimator, and and should be picked accordingly. This will be confirmed by theoretical considerations in Section 4 (in particular, see Assumption 4.3).

Now, for some smoothing parameter, set

| (3.6) |

This is motivated by (3.3) and Proposition 2.3, stating that asymptotically the coefficient of variation of is equivalent to . Finally, motivated by Remark 2.2, set

| (3.7) |

This choice ensures that the expectation of is asymptotically equivalent to for all values of and (take in (2.27)). Intuitively, given that is the density of the multiplicative noise used to dilute (see Section 2.1), it is understood that should have expectation (close to) 1 for all and . The reason why it should not be exactly 1, is again that expectations are slightly distorted in the multiplicative environment. For instance, the expectation of the log-Normal distribution is not , but as . The parameter as in (3.7) exactly accounts for that distortion.

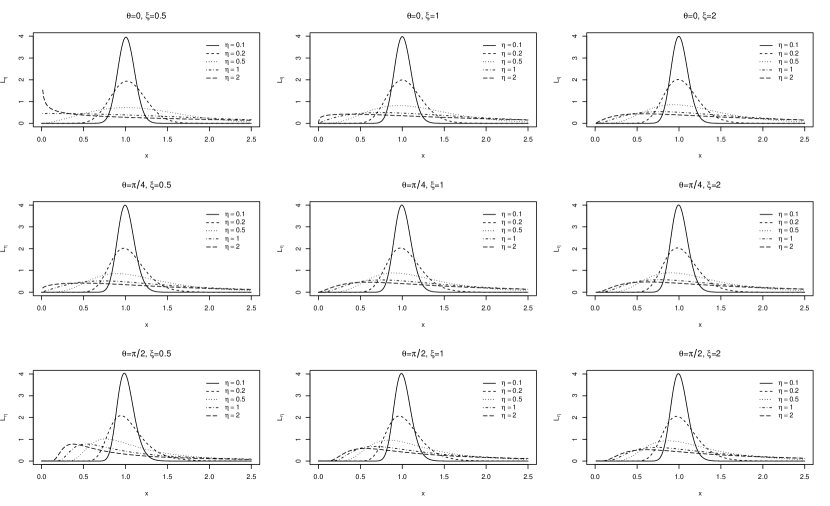

We call kernels with this parameterisation (3.6)-(3.7), Meijer kernels. Figure 3.2 shows examples of such Meijer kernels for and , for (canonical kernel ) and several values of the smoothing parameter . As approaches 0, the kernels concentrate around 1 with a fading effect of the values of and on their shape, as suggested by expansion (2.27).

Remark 3.2.

As mentioned above, setting and as parameters of the Meijer kernels amounts to using Gamma densities for in (3.5). However, the so-defined estimator is obviously not, and is not even related to, Chen (2000)’s ‘Gamma kernel estimator’ (in any of its forms). Indeed, with and , (2.21) tells that is the density of , where , that is, with (3.6)-(3.7), is the density of the -distribution. This gives for the final estimator the explicit form

| (3.8) |

This cannot be compared to (1.4). The slightly more complicated nature of expression (3.8) should not be repelling as it is given here just for illustration. Exactly as all the properties of the conventional estimator are obtained from the generic expression (1.2) only, without the need to write explicitly the kernel function , the behaviour of the Mellin-Meijer kernel density estimator is to be comprehended exclusively through (3.5) and the general properties of Meijer kernels.

4 Asymptotic properties

In this section we obtain the asymptotic properties of the Mellin kernel density estimator (3.5) with Meijer kernels parameterised as described in Section 3.3, under the following assumptions.

Assumption 4.1.

The sample consists of i.i.d. replications of a positive random variable whose distribution admits a density twice continuously differentiable on ;

Assumption 4.2.

There exist , with , such that and ;

Assumption 4.3.

For any smoothing parameter and for each , the kernel is a Meijer kernel as described in Section 3.3, with and such that and ;

Assumption 4.4.

The smoothing parameter is such that and as .

Assumption 4.1 fixes the setup. The requirement that has two continuous derivatives is classical in kernel estimation. Assumption 4.2 is a condition on the existence of some negative and positive moments of , and excludes densities with both ‘very’ fat head and tail, but it is actually a very mild requirement. In particular, is allowed to be positive and even unbounded at the boundary (), and/or to have power law decay in its tail (), provided that it does not show extreme versions of those behaviours simultaneously ( and cannot be both very small at the same time). Assumption 4.3 essentially requires that the parameters and of the Meijer kernels enable the estimator to properly reconstruct the head and tail behaviour of . For instance, for ( has a very fat head), it would not work to take ‘small’ and (lightest head for the kernel, see Figure 3.2). The imposed conditions leave much freedom about the choice of and , though, and are restrictive only in extreme cases. For instance, only for (extremely fat tail for ) would the condition not be trivially satisfied. Finally, Assumption 4.4 is the classical condition on the smoothing parameter in kernel estimation. Under these assumptions, we have the following result.

Theorem 4.1.

Proof.

See Appendix. ∎

Note that, under Assumptions 4.2 and 4.3, (4.2) defines a nonempty interval. Theorem 4.1 establishes the convergence to 0 of a weighted Mean Integrated Squared Error (MISE) of the estimator, where the set of values defining weights assuring convergence essentially depends on the assumed negative and positive moments of . The consistency of the estimator in the usual MISE- (-)sense follows.

Corollary 4.1.

Proof.

If and , then belongs to (4.2). ∎

Of course, the optimal rate of convergence is achieved for , which gives

the usual optimal rate of convergence for nonparametric estimation of a univariate probability density under Assumption 4.1. Note that Corollary 4.1 establishes this result for , that is, . This requires as , and in particular, . This is restrictive: for instance, Chen (2000) showed that his ‘modified’ Gamma kernel estimator has pointwise (i.e., at some fixed ) bias proportional to , and pointwise variance proportional to , hence deduced its MISE-consistency under the assumptions that and . If is obviously equivalent to in our framework, does not tell much about the moments of . If implies as , there exist distributions with but with . Those include the Exponential distribution, to cite only one simple example.

The results presented thus far naturally followed from the properties of the Mellin transform of inside its strip of holomorphy. As such, (4.1)-(4.3) have been proved under proper conditions on the existence of moments of only, as those define . However, those assumptions can actually be relaxed to conditions similar to Chen (2000)’s. The condition in (4.2), which requires if one wants , comes from resorting to the general identity

| (4.4) |

in the proof of Theorem 4.1. The point is that ‘’ is a sufficient condition for (4.4) to be true, but is not necessary. The simple case of the Exponential density heuristically illustrates the claim. Indeed has Mellin transform on . Inverting (4.4) through (2.4) one has

| (4.5) |

for , that is, for . However, from (2.3) we know that, for , is the Mellin transform of , which allows to write for . As evidently , it follows that (4.5) holds true for , and actually, for , as as well.

What theoretically validates this argument is that , initially defined as for only, can be analytically continued on the negative half of the real axis by making repeated use of the identity (). This implies that in (4.4) is well defined even for . So, more generally, assuming that the analytical continuation of to the left of is well-behaved in some sense, the proof of Theorem 4.1 carries over when relaxing the condition , and (4.1) remains valid. Actually, the analytic continuation of a Mellin transform outside its strip of holomorphy gives a much more complete picture of the behaviour of at 0 or at , see Paris and Kaminski (2001, p.86 ff.) or Wong (1989, Theorem 5) for details. Thorough discussion of this aspect is beyond the scope of this paper, nevertheless we can state the following result.

Proposition 4.1.

Proof.

See Appendix. ∎

Further support for Proposition 4.1 is brought by analysing the pointwise properties of the Mellin-Meijer kernel density estimator.

Theorem 4.2.

Proof.

See Appendix. ∎

Theorem 4.2 allows one to write the Asymptotic (i.e., only dominant terms) Mean Integrated Squared Error (AMISE) of estimator (3.5) as

| (4.9) |

which is indeed provided that (i.e., ) and . Interestingly, (4.7) and (4.8) are the same as the asymptotic expressions for the ‘away-from-the-boundary’ bias and variance of Chen (2000)’s modified Gamma kernel estimator (which admits a different behaviour in the boundary area as it is manually modified there). The (asymptotic) bias (4.7) only depends on (not on or ), as opposed to (1.8) or the bias of Chen (2000)’s original Gamma estimator and modified Gamma estimator at the boundary. The (asymptotic) variance (4.8) is proportional to . This factor obviously remains unbounded as in theory, but tends to much slower than the factor in (1.9). Note that, if we exactly adapted to the ‘Haar geometry’ of by taking for the Meijer kernels as briefly contemplated in Section 3.2, we would produce an estimator such that and , the usual pointwise bias and variance asymptotic expressions for the conventional estimation (1.2). For the reasons expounded in Section 3.2, this might not be desirable in this framework, though.

5 Smoothing parameter selection

The choice of the smoothing parameter for acurate nonparametric estimation is always crucial, and estimator (3.5) is no exception. Hence a data-driven way of selecting a reasonable value of is desirable. Although the classical idea of cross-validation can be easily adapted to this case, Mellin transform ideas again provide a natural framework for deriving an easy plug-in selector.

From (4.1), (4.7) and (4.8), one can write the asymptotic WMISE of the estimator as

| (5.1) |

for any in (4.2). Balancing the two terms, one easily obtains the asymptotically optimal value of :

| (5.2) |

Plug-in methods attempt to estimate the unknown factors in (5.2) in order to produce an approximation of . If estimating by is straightforward, estimating the denominator involving is less obvious. For conventional kernel estimation, this step usually requires estimating higher derivatives of , which in turn requires the selection of pilot smoothing parameters and/or resorting to a ‘reference distribution’, see e.g. Sheather and Jones (1991).

Here, combining (4.4) and (A.9) yields

| (5.3) |

for . Of course, can be naturally estimated by . Now, if , , and

This suggests to approximate (5.3) by

for some value . Note that the antiderivative of is available in closed form, which makes evaluating the integral very easy. The only stumbling stone is that the integral actually diverges for , which is not surprising here given that it would essentially reflect the integrated squared ‘second derivative’ of . It is, therefore, paramount to select an appropriate value of .

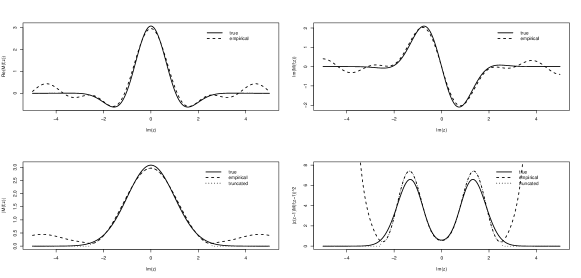

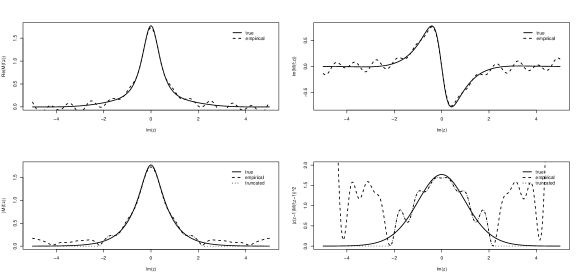

A thoughtful choice can be made by noting from the definition (2.1) that, for a fixed , is symmetric around , i.e. the real axis, and always reaches its maximum at . In addition, typically tends to 0 quickly as one moves away from the real axis. In particular, is known to be as (Paris and Kaminski, 2001, Lemma 3.2), and most of the common densities on , being essentially Meijer densities as observed in Section 2.4, show similar Gamma factors in their Mellin transform. It turns out that is remarkably accurate at reconstructing over a substantial set of values of around the real axis, that is, where it matters. The approximation badly deteriorates as grows, but there we know that anyway. This is illustrated in Figures 5.1 and 5.2 for the case of the log-Normal distribution and the Exponential distribution.

A reasonable choice for seems, therefore, the location, say , of the first local minimum in away from . Typically, this is where the ‘empirical’ oscillations which heavily affect further approximations, start. It also occurs where the true is already ‘small’, hence neglecting any contribution to (5.3) made for is unlikely to change the outcome dramatically; see Figures 5.1 and 5.2. This suggests to take, finally,

| (5.4) |

The value of should, of course, be chosen in (4.2), to guarantee that all involved quantities are finite. Taking seems to be a reasonable default value, as it always belongs to (4.2) under the mild moment conditions and (and ). If the behaviour of at 0 allows it, one can also take , which would approximate the usual MISE-optimal bandwidth. In any case, (5.4) is shown to consistently produce reliable estimates in the simulation study in the next section.

6 Simulation study

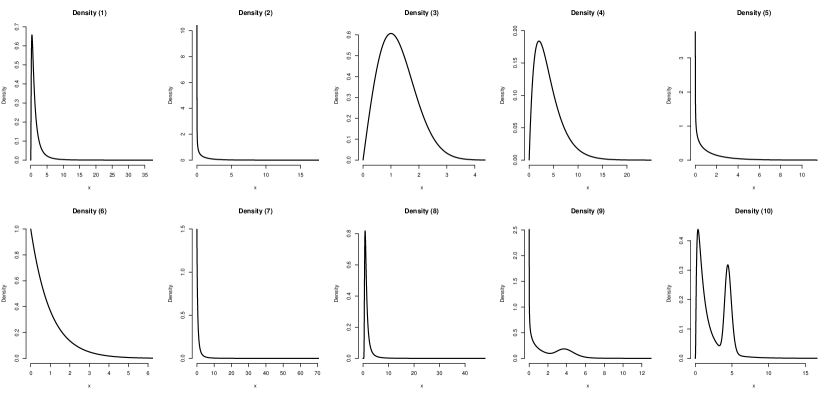

In this section the practical performance of the Mellin-Meijer kernel density estimator (3.5) is analysed through simulations. Inspired by Bouezmarni and Scaillet (2005), we consider the following 10 test densities (refer to Table A.1 for parameterisation), shown in Figure 6.1:

-

(1)

the standard log-Normal density;

-

(2)

the Chi-squared density with degree of freedom;

-

(3)

the Nakagami density with and ;

-

(4)

the Gamma density with and ;

-

(5)

the Gamma density with and ;

-

(6)

the standard Exponential density;

-

(7)

the Generalised Pareto density with and ;

-

(8)

the inverse Weibull density with and ;

-

(9)

a mixture of Gamma densities: ;

-

(10)

a mixture of log-Normal densities: .

These 10 densities exhibit various behaviours at 0 (light head: (1), (8), (10); fat head (): (3), (4); very fat head (): (6), (7) (bounded), (2), (5), (9) unbounded) and in the tail (light tail: (1), (2), (3), (4), (5), (6), (9), (10); fat tail: (7), (8)). From each of these distributions, independent samples of size and were generated, with Monte Carlo replications for each sample size. On each of them, the density was estimated by the estimator (3.5), where the basic parameters of the Meijer kernel were set to , and (‘MM-1’, ‘MM-2’ and ‘MM-3’ in Table 6.1). For each case, the smoothing parameter was selected according to (5.4), where three values were tested: , and (MM-x-12, MM-x-22 and MM-x-32) in Table 6.1).

For comparison, we have also included in the study Chen (2000)’s ‘modified’ Gamma kernel estimator (‘Gamma’ in Table 6.1), whose bandwidth was chosen following the reference rule prescribed in Hirukawa and Sakudo (2014). This estimator was computed using the dbckden function in the R package evmix.

The densities were estimated on a fine grid of points between and , where is the quantile of level 0.9999 of the relevant density. The Mean Integrated Squared Error (MISE) of a given estimator was then approximated by

where is the number of Monte Carlo replications. The results are reported in Table 6.1 for . The results for show a very similar pattern and are omitted here. For ease of reading and interpretation, all the values in Table 6.1 are relative to the (approximated) MISE of the Gamma kernel estimator, which is taken as benchmark owing to its central and reference role within the asymmetric kernel density estimators. For reference, its effective MISE () is reported in italics in the second row of the table (which are, therefore, not on the same scale as the other values).

| Dens 1 | Dens 2 | Dens 3 | Dens 4 | Dens 5 | Dens 6 | Dens 7 | Dens 8 | Dens 9 | Dens 10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Gamma | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| 2.52 | 15.04 | 27.89 | 1.59 | 5.37 | 9.39 | 0.02 | 3.08 | 6.70 | 8.04 | |

| \hdashlineMM-1-12 | 1.1423 | 60.5327 | 0.8151 | 0.8668 | 16.3165 | 7.1636 | 7.1307 | 0.5167 | 10.5386 | 0.7328 |

| MM-1-22 | 0.9929 | 6.0001 | 0.9142 | 0.8704 | 3.0499 | 1.7499 | 1.8415 | 0.4838 | 1.7679 | 1.0435 |

| MM-1-32 | 1.0267 | 0.4933 | 0.8263 | 0.8310 | 0.9904 | 1.4479 | 1.1517 | 0.5052 | 1.0581 | 1.5039 |

| MM-2-12 | 1.1365 | 60.5346 | 0.8712 | 0.8507 | 16.2919 | 7.0522 | 7.1313 | 0.5144 | 10.5138 | 0.7334 |

| MM-2-22 | 1.0608 | 5.9855 | 1.0394 | 0.9920 | 2.9871 | 1.6653 | 1.8440 | 0.4851 | 1.7170 | 1.1043 |

| MM-2-32 | 1.1962 | 0.5274 | 0.8116 | 0.8611 | 1.1069 | 1.5037 | 1.0181 | 0.5304 | 1.1575 | 1.6735 |

| MM-3-12 | 1.1459 | 60.5320 | 0.8235 | 0.8812 | 16.3201 | 7.1824 | 7.1304 | 0.5178 | 10.5421 | 0.7335 |

| MM-3-22 | 0.9865 | 6.0018 | 0.9144 | 0.8738 | 3.0635 | 1.7788 | 1.8405 | 0.4848 | 1.7790 | 1.0352 |

| MM-3-32 | 1.0057 | 0.4975 | 0.8402 | 0.8466 | 0.9898 | 1.4613 | 1.1706 | 0.5034 | 1.0502 | 1.4776 |

Table 6.1 confirms the aptitude of Mellin-Meijer kernel estimation. Specifically, there is a MM-estimator which outperforms (Densities 2, 3, 4, 8, 10), sometimes by a large extent (half MISE for Densities 2 and 8), or is on par with (Densities 1, 5, 7, 9) the Gamma kernel estimator. A notable exception is Density 6 (Exponential), for which the Gamma estimator does better. The ‘modified’ Gamma kernel estimator is actually so designed for staying bounded at (Chen, 2000, p. 473). So it is especially good at estimating densities such as the Exponential. This may sometimes be counterproductive, though, see next Section. The MM-kde is not doing bad either, in any case (for , its MISE is less than 1.5 the MISE of the Gamma estimator).

The results also show that the choice of the parameters and has little influence on the MISE of the estimator, although it may have a more important effect on a particular estimate as individual inspection reveals. As a guideline, it seems better to use and/or when is suspected to be positive or unbounded at , and when is expected to have a fat tail. If both, the ‘default’ choice works fine with ‘small’, for instance .

The parameter which does have a great impact on the final estimate is, as usual, the smoothing parameter . The results show that the selector (5.4) is good at picking a right value of if used with an appropriate value of . In particular, we get huge MISE’s for Densities 2, 5, 6, 7 and 9 if (5.4) is computed with . Those are the densities such that . As (5.3) involves along the line , the empirical is huge for , which obviously produces a heavily undersmoothed bandwidth . For those densities, the selector is doing very good with . For the other densities, the value of is less important. Usually works well in most situations.

7 Real data analyses

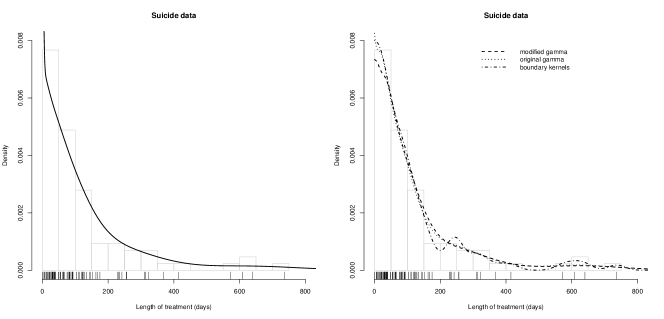

This section illustrates the performance of the Mellin-Meijer kernel estimator (3.5) when estimating two -supported densities from real data. The first data set is the ‘suicide’ data set,444This data set is directly available from the R package bde, among others. which gives the lengths (in days) of spells of psychiatric treatment undergone by patients used as controls in a study of suicide risks. Originally reported by Copas and Fryer (1980), it was studied among others in Silverman (1986) and Chen (2000) in relation to boundary issues: indeed, visual inspection (raw data at the bottom of the graph, histogram) reveals that the density should be positive, if not unbounded, at , making the conventional estimator (1.2) clearly unsuitable. The anticipated ‘fat head’ suggests the choice and for the Meijer kernels. The smoothing parameter returned by (5.4) with is . Figure 7.1 (left panel) shows the estimated density. The estimate shows a spike at the 0 boundary, which is easily understood. There are 3 observations exactly equal to 1 in the data set, and at this scale, this is pretty much ‘on the boundary’. Hence the estimator attempts to put a positive probability mass atom at 0, producing the spike. Away from the boundary, the estimate decays readily and smoothly.

For comparison, the two Gamma kernel estimators (‘original’ (1.4) and ‘modified’), with bandwidths chosen by reference rule (Hirukawa and Sakudo, 2014), as well as the ‘boundary-corrected’ conventional estimator (Jones and Foster, 1996) with Sheather and Jones (1991)’s bandwidth, are shown in the right panel. While the Gamma kernel estimators behave very similarly to the Mellin-Meijer kernel estimator in the tail, their behaviour at the boundary is not satisfactory. The original Gamma shows an inelegant kink, whereas the modified Gamma seems to underestimate there, compared to the other estimates and the histogram. This is typical of the modified Gamma estimator, as discussed in Malec and Schienle (2014). The boundary-corrected kernel estimate fails to show a real peak at , and exhibits numerous ‘spurious bumps’ in the right tail for .

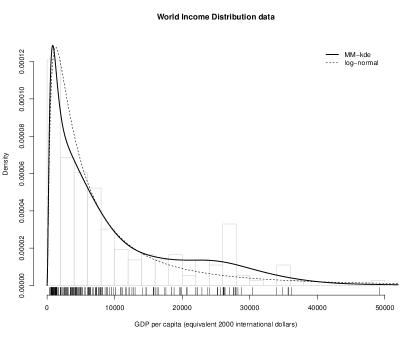

In the second example we estimate the World Distribution of Income. Estimating such distribution is important as various measures of growth, poverty rates, poverty counts, income inequality or welfare at the scale of the world are based on it (Pinkovskiy and Sala-i-Martin, 2009). We obtained data555Data available on request. about the GDP per capita (in constant 2000 international dollars) of countries in 2003 from the World Bank Database. Raw data are shown in Figure 7.2 along with an histogram and the estimated density by the MM-kernel estimator. We set and (‘default’ choice), and the value returned by (5.4) with was .

A log-Normal parametric density, fitted by Maximum Likelihood (, ), is also shown in Figure 7.2. Pinkovskiy and Sala-i-Martin (2009) strongly advocated in favour of the log-Normal distribution for modelling these data. However, the nonparametric, (mostly) unconstrained MM-estimate reveals that the peak close to 0 is actually narrower than the ‘log-Normal peak’, whereas there are much more countries with GDP per capita in the range 15,000 - 40,000 than what the log-Normal distribution prescribes. In other words, analysis through the log-Normal model is likely to underestimate poverty and income inequality at the world level. See further discussion in Dai and Sperlich (2010, Section 4).

8 Concluding remarks and perspectives

Within his seminal works on compositional data, i.e., data living on the simplex, Aitchison (2003, Section 1.8.1) already noted: “For every sample space there are basic group operations which, when recognized, dominate clear thinking about data analysis.” He continued: “In , the two operations, translation and scalar multiplication, are so familiar that their fundamental role is often overlooked”, implying that, when not in (in his case: in the simplex), there is no reason to blindly stick to those operations. The methodology developed in this paper perfectly aligns with this stance. It has apparently been largely overlooked in earlier literature that the ‘boundary issues’ of the conventional kernel density estimator find their very origin in that equipped with the addition is not a group. Noting that the natural group operation on is the multiplication , we have investigated a new kind of kernel estimation for -supported probability densities which achieves smoothing through ‘multiplicative dilution’, as opposed to ‘additive dilution’ for the conventional kernel estimator.

The construction gives rise to an estimator which makes use of asymmetric kernels, although in a different way to most of other estimators known under that name, such as the Gamma kernel estimator (Chen, 2000). Unlike those competitors, our estimator is based on a valid smoothing operation on , namely the Mellin convolution, which avoids any inconsistency in the definition and the behaviour of the estimator. Owing to the strong connection between the Mellin convolution and Meijer’s -functions, we have proposed to use so-called Meijer densities as kernels. Meijer distributions form a huge class of distributions supported on which includes most of the classical distributions of interest, and have tractable Mellin transforms given as a product of Gamma functions. This produces an integrated theory for such ‘Mellin-Meijer kernel density estimation’, with general features no more specific to a particular choice of kernel. The numerous pleasant properties of the estimator have been expounded in the paper.

The idea can be extended to more general settings in a straightforward way. Suppose that the density of a random variable living on a given domain is to be estimated from a sample. If can be equipped with an operation making a group, then a natural kernel estimator can easily be constructed by diluting any observation through -convoluting it with a random disturbance in . For instance, Aitchison (1986, Section 2.8) defined the perturbation operator as the fundamental group operation on the simplex. Thus, proper kernel density estimation on the simplex (and that includes univariate density estimation on ) should be performed by ‘-dilution’ of each observation. This will be investigated in more details in a follow-up paper.

Interestingly, Aitchison (2003, Section 2.4.2) already introduced the Mellin transform as the suitable analytical tool for simplicial distributions. More generally, the Mellin transform of a probability density ought to be a fundamental function in statistics. In some sense, it is more natural than the characteristic function (the Fourier transform of ) itself, as it just explicitly returns the moments of (real, complex, integral and fractional) – Nair (1939) initially called it the “moment function”. It is, therefore, rather surprising that Mellin-inspired procedures have stayed this inconspicuous in the statistical literature so far. Historically, one can find papers investigating statistical applications of the Mellin transform only intermittently over decades (Epstein, 1948, Lévy, 1959, Dolan, 1964, Springer and Thompson, 1966, 1970, Lomnicki, 1967, Subrahmaniam, 1970) or Gray and Zhang (1988). Only recently has the Mellin transform made a (discreet) resurgence in the statistical literature, e.g. in Tagliani (2001), Nicolas and Anfinsen (2002), Cottone et al (2010), Balakrishnan and Stepanov (2014) or Belomestny and Schoenmakers (2015, 2016). Those papers testify of the appropriateness of the Mellin transform and Mellin convolution in any multiplicative framework, such as problems of multiplicative censoring for instance. We hope that the present paper will humbly contribute to that resurgence.

Appendix

Appendix A Further properties of Mellin transforms

A.1 Operational properties

Further properties of the Mellin transform include:

| (A.1) | |||||

| (A.2) | |||||

| (A.3) | |||||

| (A.4) | |||||

| (A.5) | |||||

| (A.6) | |||||

| (A.7) | |||||

| (A.8) |

where is the differential operator. Proofs of these results can be found in the above-mentioned references. In addition, the Mellin version of Parseval’s identity (Paris and Kaminski, 2001, Equation (3.1.15)) reads

| (A.9) |

for any .

The following useful result about Mellin transforms of probability densities easily follows from these properties.

Lemma A.1.

Let be a continuous positive random variable with density whose Mellin transform is on the strip of holomorphy , for some . Then, the random variable , where and , has a density whose Mellin transform is on () or ().

Proof.

Corollary A.1.

Let be a continuous positive random variable with density whose Mellin transform is on the strip of holomorphy , for some . Then the inverse random variable has density whose Mellin transform is on .

Proof.

Take and in Lemma A.1. ∎

A.2 Meijer parameterisation

| Common name | Density | Parameters | ||||

|---|---|---|---|---|---|---|

| Beta prime | ||||||

| Burr | ||||||

| Chi | ||||||

| Chi-squared | ||||||

| Dagum | ||||||

| Erlang | 1 | |||||

| Fisher-Snedecor | 1 | 1 | ||||

| Fréchet | ||||||

| Gamma | 1 | 0 | ||||

| Generalised Pareto | ||||||

| Inverse Gamma | 1 | |||||

| Lévy | 1 | |||||

| Log-logistic | ||||||

| Maxwell | 0 | |||||

| Nakagami | 0 | |||||

| Rayleigh | 0 | |||||

| Singh-Maddala | ||||||

| Stacy | 0 | |||||

| Weibull | 0 |

Appendix B Proofs

Preliminary lemma

First we state a technical lemma that will be used repeatedly in the proofs below. Tricomi and Erdélyi (1951) gave the following asymptotic expansion for the ratio of two Gamma functions. Let . Then, as ,

| (B.1) |

where , provided that are bounded and . Here are the generalised Bernoulli polynomials, which are polynomials in and of degree , see Temme (1996, Section 1.1). The first such polynomials are , and . The following result, proved in Fields (1970), essentially gives a uniform version of (B.1) which allows and to become ‘large’ as well, if more slowly than .

Lemma B.1.

Let . Then, for all , one has, as ,

| (B.2) |

where , provided that and .

Proof of Proposition 2.1

For any two parameters and , the Fisher-Snedecor distribution has density

| (B.3) |

where is the Beta function. One of its characterisations is that, if and for some arbitrary positive and ( and independent), then

see Johnson et al (1994, Section 27.8). Hence the -distribution is the distribution of the product of a Gamma r.v. and an Inverse Gamma r.v., rescaled by the constant . Lemma A.1, (2.8), (2.12) and (2.15) then yield the Mellin transform of (B.3):

| (B.4) |

Proof of Proposition 2.2

If , then . Then, by (2.6), the mean of is , that is,

| (B.5) |

Also, as , the standard deviation of is

which is

The announced result follows from .

Proof of Proposition 2.3

Proof of Proposition 2.4

The proof is given for the case only. As , Lemma B.1 ascertains that

where , provided . Similarly,

where , provided . Also, the binomial series expands as

where , provided as . Multiplying these factors yields

where , provided .

Proof of Proposition 2.5

Proof of Theorem 4.1

Proof.

Lemma B.2 ascertains that (B.6) is valid for any . In particular, it is true for satisfying (4.2), as and .

Now, because is holomorphic on and is real-valued, , where denotes complex conjugation. Hence, . By (A.1), . Hence (B.6) is

and

| (B.10) |

From (B.8), we have

whence

| (B.11) |

Given that , it holds for all

from (A.9) back and forth. Hence the first term in (B.11), say -1, is

| (B.12) |

The second term in (B.11), say -2, has expectation

for a generic . Interchanging expectation and integral is justified as belongs to both and (for all ), making the corresponding integrals both absolutely convergent. Likewise,

It is easily seen that

| (B.13) |

which is clearly the integrated squared bias term, say , in the Weighted Mean Integrated Square Error expression (B.10). The remaining thus forms the integrated variance, say IV. Below, we show that and as , under our assumptions.

Integrated squared bias term: Under condition (4.2), , hence . Let as , such that for

| (B.14) |

Note thas this implies as . Write

| (B.15) |

where is the indicator function, equal to 1 if the condition is satisfied and 0 otherwise. See that , hence one can make use of the asymptotic expansion (2.26)-(2.27) with (3.6)-(3.7) to write, as ,

where for some constant . From this and (B.15) we have

that is,

Hence the integrated squared bias (B.13) is such that

| (B.16) |

As , . By combining (A.4) and (A.7), it is seen that if , which is the case here by (B.9) and because by (4.2). With (A.9), , hence

| (B.17) |

Given that , for some constant and

Now,

Clearly the strip of holomorphy of is contained in that of any of its restriction on , so by (A.9) again,

By Assumpion 4.2, , which implies as . Hence

following Example 4 in Paris and Kaminski (2001, Section 1.1.1). With and condition (B.14), it can be checked that this is

| (B.18) |

Finally,

and it follows

The integral may be seen to be bounded by (A.8), as for under condition (4.2), hence

| (B.19) |

It follows from (B.16), (B.17), (B.18) and (B.19) that

Integrated variance term: Consider again with as . Then write (B.12) as

| -1 | (B.20) | |||

Seeing again that , one can write the expansion (2.30) for in -1-a, that is, making use of (3.6)-(3.7),

where . Also, , for large enough. This means that, as ,

where for some constant , yielding

Assumption 4.2 ensures that as , whence

It follows

This is if , which is the case under condition (4.2).

Now, because , each is finite and , for some constant. Hence

| (B.21) |

Similarly to above,

making use again of as . Taking expectations in (B.21) yields

It can be checked that, for , . Hence, , leading to

| (B.22) |

The dominant term in can be understood to be . Yet,

which is bounded for any . Hence , which shows

∎

Proof of Proposition 4.1

Proof of Theorem 4.2

The proof is very similar to the proof of Theorem 4.1, hence only a sketch is given. Using the inverse Mellin transform expression (2.4), we can write

where is given by (B.8) and is any value in , from Lemma B.2. Expanding the square, working out the terms and taking expectations yield, after lengthy derivations,

Clearly the first term is the square of the inverse Mellin transform of , hence is the squared pointwise bias term, say , in the usual expansion of the MSE of . The term in is thus the pointwise variance, .

Acting essentially as in the proof of Theorem 4.1, in particular making use of expansion (2.26)-(2.27) again, one obtains that the dominant term asymptotically in the squared bias term is

from (A.4) and (A.7), provided , that is, . It follows that

| (B.23) |

Making use of expansion (2.30), one finds that, asymptotically,

which, plugged in the expression of , yields the following dominant term for the pointwise variance:

| (B.24) |

provided .

References

- Abramson (1982) Abramson, I. (1982), On bandwidth variation in kernel estimates: a square-root law, Ann. Statist., 10, 1217-1223.

- Aitchison (1986) Aitchison, J., The Statistical Analysis of Compositional Data, Monographs on Statistics and Applied Probability, Chapman & Hall, London, 1986.

- Aitchison (2003) Aitchison, J. (2003), A concise guide to compositional data analysis. In: 2nd Compositional Data Analysis Workshop, Girona, Italy, 134 pp.

- Balakrishna and Koul (2017) Balakrishna, N. and Koul, H.L. (2017), Varying kernel marginal density estimator for a positive time series, J. Nonparametr. Stat., to appear.

- Balakrishnan and Stepanov (2014) Balakrishnan, N. and Stepanov, A. (2014), On the use of bivariate Mellin transform in bivariate random scaling and some applications, Methodology and Computing in Applied Probability, 16, 235-244.

- Bateman (1954) Bateman, H., Table of integral transforms, Vol. 1, McGraw-Hill, New York, 1954.

- Bateman and Erdélyi (1953) Bateman, H. and Erdélyi, A., Higher transcendental functions, Vol. 1, McGraw-Hill, New York, 1953.

- Beals and Szmigielski (2013) Beals, R. and Szmigielski, J. (2013), Meijer -functions: a gentle introduction, Notices of the AMS, 60, 866-872.

- Belomestny and Schoenmakers (2015) Belomestny, D. and Schoenmakers, J. (2015), Statistical Skorohod embedding problem: Optimality and asymptotic normality, Statist. Probab. Lett., 104, 169-180.

- Belomestny and Schoenmakers (2016) Belomestny, D. and Schoenmakers, J. (2016), Statistical inference for time-changed Lévy processes via Mellin transform approach, Stochastic Process. Appl., 126, 2092-2122.

- Bouezmarni and Scaillet (2005) Bouezmarni, T. and Scaillet, O. (2005), Consistency of asymmetric kernel density estimators and smoothed histograms with application to income data, Econometric Theory, 21, 390-412.

- Butzer et al (2014) Butzer, P.L., Bardaro, C. and Mantellini, I. (2014), The foundations of fractional Mellin transform analysis, Manuscript, arXiv:1406.6202.

- Chen (2000) Chen, S.X., (2000), Probability Density Function Estimation Using Gamma Kernels, Annals of the Institute of Statistical Mathematics, 52, 471 - 480.

- Cheng et al (1997) Cheng, M.Y., Fan, J. and Marron, J.S. (1997), On automatic boundary corrections, Ann. Statist., 25, 1691-1708.

- Comte and Genon-Catalot (2012) Comte, F. and Genon-Catalot, V., (2012), Convolution power kernels for density estimation. J. Statist. Plan. Inference 142, 1698-1715.

- Copas and Fryer (1980) Copas, J.B. and Fryer, M.J. (1980), Density estimation and suicide risks in psychiatric treatment. J. Roy. Statist. Soc. Ser. A, 143, 167-176.

- Cottone et al (2010) Cottone, G., Di Paola, M. and Metzler, R. (2010), Fractional calculus approach to the statistical characterization of random variables and vectors, Phys. A, 389, 909-920.

- Cowling and Hall (1996) Cowling, A. and Hall, P. (1996), On pseudodata methods for removing boundary effects in kernel density estimation, J. R. Stat. Soc. Ser. B Stat. Methodol., 58, 551-563.

- Cox (2008) Cox, C. (2008), The generalized F distribution: An umbrella for parametric survival analysis, Stat. Med., 27,4301-4312.

- Dai and Sperlich (2010) Dai, J. and Sperlich, S. (2010), Simple and effective boundary correction for kernel densities and regression with an application to the world income and Engel curve estimation, Comput. Statist. Data Anal., 54, 2487-2497.

- Devroye and Györfi (1985) Devroye, L. and Györfi, L., Nonparametric Density Estimation: the L1 View, Wiley, 1985.

- Dobrovidov and Markovich (2014) Dobrovidov, A.V. and Markovich, L.A. (2014), Data-driven bandwidth choice for gamma kernel estimates of density derivatives on the positive semi-axis, Manuscript, arXiv.

- Dolan (1964) Dolan, B.A. (1964), The Mellin transform for moment-generation and for the probability density of products and quotients of random variables, Proc. IEEE, 52, 1745-1746.

- Epstein (1948) Epstein, B. (1948), Some applications of the Mellin transform in statistics, Ann. Math. Statist., 19, 370-379.

- Fields (1970) Fields, J.L. (1970), The uniform asymptotic expansion of a ratio of Gamma functions, In: Proc. Int. Conf. on Constructive Function Theory, Varna, May 1970, 171-176.

- Funke and Kawka (2015) Funke, B. and Kawka, R. (2015), Nonparametric density estimation for multivariate bounded data using two non-negative multiplicative bias correction methods, Comput. Statist. Data Anal., 92, 148-162.

- Funke and Hirukawa (2016) Funke, B. and Hirukawa, M. (2016), Nonparametric estimation and testing on discontinuity of positive supported densities: a kernel truncation approach, Manuscript, arXiv.

- Gasser and Müller (1979) Gasser, T. and Müller, H.-G. (1979), Kernel estimation of regression functions. In: Gasser, T., Rosenblatt, M. (Eds.), Lecture Notes in Mathematics, vol. 757. Springer, Heidelberg, pp. 23-68.

- Geenens (2014) Geenens, G. (2014), Probit transformation for kernel density estimation on the unit interval, J. Amer. Statist. Assoc., 109, 346–358.

- Geenens and Wang (2016) Geenens, G. and Wang, C. (2016), Local-likelihood transformation kernel density estimation for positive random variables, Manuscript, arXiv:1602.04862.

- Godement (2015) Godement, R. (2015), Analysis III - Analytic and Differential Functions, Manifolds and Riemann Surfaces, Springer.

- Graf (2010) Graf, U., Introduction to Hyperfunctions and their Integral Transforms, Birkhauser-Springer, Basel, 2010.

- Gray and Zhang (1988) Gray, H.L. and Zhang, N.F. (1988), On a class of non-stationary processes, Journal of Time Series Analysis, 9, 133-154.

- Gustafsson et al (2009) Gustafsson, J., Hagmann, M., Nielsen, J.P. and Scaillet, O. (2009), Local transformation kernel density estimation of loss distributions, J. Bus. Econom. Statist., 27, 161-175.

- Hall et al (1995) Hall, P., Hu, T. and Marron J.S. (1995), Improved variable window kernel estimates of probability densities, Ann. Statist., 23, 1-10.

- Hall and Park (2002) Hall, P. and Park, B.Y. (2002), New methods for bias correction at endpoints and boundaries, Ann. Statist., 30, 1460-1479.

- Hall et al (2004) Hall, P., Minnotte, C. and Zhang, C. (2004), Bump hunting with non-gaussian kernels, Ann. Statist., 32, 2124-2141.

- Hagmann and Scaillet (2007) Hagmann, M. and Scaillet, O. (2007), Local multiplicative bias correction for asymmetric kernel density estimators, J. Econometrics, 141, 213-249.

- Härdle et al (2004) Härdle, W., Müller, M., Sperlich, S. and Werwatz, A., Nonparametric and semiparametric models: an introduction, Springer, 2004.

- Hirukawa and Sakudo (2014) Hirukawa, M. and Sakudo, M. (2014), Nonnegative bias reduction methods for density estimation using asymmetric kernels, Comput. Statist. Data Anal., 75, 112-123.

- Hirukawa and Sakudo (2015) Hirukawa, M. and Sakudo, M. (2015), Family of generalised gamma kernels: a generator of asymmetric kernels for nonnegative data, J. Nonparametr. Stat., 27, 41-63.

- Hoffmann and Jones (2015) Hoffmann, T. and Jones, N. (2015), Unified treatment of the asymptotics of asymmetric kernel density estimators, Manuscript, arXiv.

- Hossjer and Ruppert (1995) Hossjer, O. and Ruppert, D. (1995), Asymptotics for the Transformation Kernel Density Estimator, Ann. Statist., 23, 1198-1222.

- Igarashi and Kakizawa (2014) Igarashi, G. and Kakizawa, Y. (2014), Re-formulation of inverse Gaussian, reciprocal inverse Gaussian, and Birnbaum-Sauders kernel estimators, Statist. Probab. Lett., 84, 235-246.

- Igarashi (2016) Igarashi, G. (2016), Weighted log-Normal kernel density estimation, Comm. Statist. Theory Methods, to appear.

- Jeon and Kim (2013) Jeon, Y. and Kim J.H.T. (2013), A gamma kernel density estimation for insurance loss data, Insurance: Mathematics and Economics, 53, 569-579.