A Primal-Dual Parallel Method with Convergence for Constrained Composite Convex Programs††thanks: This paper extends our conference paper [17] by considering composite convex programs and proposing new algorithm parameter rules that are irrelevant to the optimal Lagrange multipliers.

Abstract

This paper considers large scale constrained convex (possibly composite and non-separable) programs, which are usually difficult to solve by interior point methods or other Newton-type methods due to the non-smoothness or the prohibitive computation and storage complexity for Hessians and matrix inversions. Instead, they are often solved by first order gradient based methods or decomposition based methods. The conventional primal-dual subgradient method, also known as the Arrow-Hurwicz-Uzawa subgradient method, is a low complexity algorithm with an convergence time. Recently, a new Lagrangian dual type algorithm with a faster convergence time is proposed in Yu and Neely (2017). However, if the objective or constraint functions are not separable, each iteration of the Lagrangian dual type method in Yu and Neely (2017) requires to solve a unconstrained convex program, which can have huge complexity. This paper proposes a new primal-dual type algorithm with convergence for general constrained convex programs. Each iteration of the new algorithm can be implemented in parallel with low complexity even when the original problem is composite and non-separable.

keywords:

constrained convex programs, composite convex programs, parallel methods, convergence time90C25, 90C30

1 Introduction

Recall that a function is said to be separable (with respect to its vector variable ) if it can be written as the summation of multiple smaller functions, each of which only involves disjoint components or blocks of , e.g, . Fix positive integers and , which are typically large. Consider the following constrained convex program:

| (1) | min | |||

| (2) | s.t. | |||

| (3) |

where set is a closed convex set; function is convex and smooth (but possibly non-separable) on ; function is convex and separable (but possibly non-smooth) on ; functions are convex, Lipschitz continuous and smooth (but possibly non-separable) on , and functions are convex, Lipschitz continuous and separable (but possibly non-smooth) on . The convex program (1)-(3) is called a constrained composite convex program since either its objective function or each of its constraint functions is in general the sum of a smooth function and a non-smooth function.

Denote the stacked vector of functions via ; and . The Lipschitz continuity of each and implies that is Lipschitz continuous on . Throughout this paper, we use to denote the Euclidean norm of vector , also known as the norm, and have the following assumptions on convex program (1)-(3):

Assumption 1 (Basic Assumptions).

Assumption 2 (Existence of Lagrange multipliers).

Under 1 and 2, this paper proposes a new primal dual type algorithm which can solve convex program (1)-(3) with convergence. That is, the new algorithm only requires iterations to achieve an -approximate solution. Furthermore, each iteration of this new algorithm can be decomposed into multiple smaller independent subproblems and hence can be implemented in parallel with low complexity even though the original convex program (1)-(3) involves non-separable and .

1.1 Example Problems

The general convex program (1)-(3) considered in this paper includes many difficult convex programs as special cases.

1.1.1 Large Scale Constrained Smooth Convex Programs

If and , then problem (1)-(3) is a constrained smooth convex program. In general, constrained smooth convex program (1)-(3) can be solved via interior point methods (or other Newton type methods) which involve the computation of Hessians and matrix inversions at each iteration. The associated computation complexity and memory space complexity at each iteration is between and ), which is prohibitive when is extremely large. For example, if and each floating point number uses bytes, then Gbytes of memory space is required even to save the Hessian at each iteration. Thus, large scale convex programs are usually solved by first order gradient based methods or decomposition based methods. The primal-dual subgradient algorithm, also known as the Arrow-Hurwicz-Uzawa subgradient method, is a first order method with a slow convergence time for large scale convex programs [12].

1.1.2 Constrained Composite Convex Programs

If and/or , then problem (1)-(3) is a constrained composite convex program. Due to the non-differentiability, interior points methods (or other Netwon type methods) are usually not applicable. Such a non-smooth convex program can be solved by a mirror descent based method in [1] with a slow convergence time. In the special case when there is only one single smooth constraint given by , i.e., , work [16] proposes a dual method with an convergence time. In the special case when is linear and , work [6] proposes a random primal-dual method that can converges to a solution whose expected error is with an convergence time.

One representative example of constrained composite convex programs is the constrained LASSO problem from machine learning applications [9] and financial portfolio optimization [4] as follows:

| s.t. | |||

where denotes the norm of vector . The constrained LASSO problem is a special case of convex program (1)-(3) with , , and . In fact, many constrained optimization problems from machine learning, compressed sensing and financial portfolio optimization involve a non-smooth but separable norm term in the objective or constraint functions and can hence can be cast as a special case of convex program (1)-(3).

1.2 The Primal-Dual Subgradient Method

The primal-dual subgradient method, also known as Arrow-Hurwicz-Uzawa subgradient method, with primal averaging is a first order method that can be applied to solve convex program (1)-(3) as described in Algorithm 1. In this paper, we use to denote either the gradient (when is differentiable) or a subgradient (when is non-differentiable) of function at point .

The primal-dual subgradient method can solve constrained non-smooth convex programs. The updates of and only involve the computation of subgradients and simple projection operations. For large scale constrained smooth convex programs with large value, the computation of subgradients is much simpler than the computation of Hessians and matrix inversions and hence the primal dual subgradient has lower complexity computations at each iteration and is more suitable when compared with the interior point method. However, Algorithm 1 is known to have a slow convergence time [12]. Another drawback of Algorithm 1 is that its implementation requires , which are upper bounds of each component of the Lagrange multiplier vector that attains the strong duality. In practice, is usually unavailable.

Let be a constant step size. Choose any . Initialize Lagrangian multipliers . At each iteration , observe and and do the following:

-

•

Choose via

where is the projection onto convex set .

-

•

Update Lagrangian multipliers via

where and is the projection onto interval .

-

•

Update the running averages via

1.3 The Dual Subgradient Method and Its Variations

The classical dual subgradient algorithm is a Lagrangian dual type iterative method that can solve constrained strictly convex programs [3]. By averaging the resulting primal estimates from the classical dual subgradient algorithm, we can solve general constrained convex programs (possibly without strict convexity) with an convergence time [13, 11, 14]. The dual subgradient algorithm with primal averaging is more suitable to separable convex programs because the updates of each component are independent and parallel if both the objective function and the constraint function are separable .

Recently, a new Lagrangian dual type algorithm with convergence for general convex programs is proposed in [18]. This algorithm can solve convex program (1)-(3) following the steps described in Algorithm 2. Similar to the dual subgradient algorithm with primal averaging, Algorithm 2 can decompose the updates of into smaller independent subproblems if functions and are separable. Moreover, Algorithm 2 has faster convergence when compared with the primal-dual subgradient algorithm or the dual subgradient algorithm with primal averaging.

Let be a constant parameter. Choose any . Initialize virtual queues . At each iteration , observe and and do the following:

-

•

Choose as

-

•

Update virtual queue vector via

-

•

Update the running averages via

In this paper, however, objective function involves possibly non-separable and each constraint function involves possibly non-separable . As a result, the update of is not decomposable and requires to solve a set constrained non-smooth strongly convex program which is typically solved via a subgradient based method. However, the subgradient based method for set constrained convex programs is an iterative technique and involves at least one projection operation at each iteration. To obtain an -approximate solution to the set constrained convex program, the projected subgradient method in general requires iterations and can be improved to only require or iterations for certain special problems [15, 2].

1.4 New Algorithm

In this paper, we propose a new primal-dual type algorithm to solve convex program (1)-(3) as described in Algorithm 3. The new algorithm uses the same virtual queue update as in Algorithm 2, however, the update of is fundamentally different. The modification enable us to update each component of in parallel even if or each is non-separable. Later, we will further show that the convergence of Algorithm 2 is preserved in the new algorithm.

Let be a sequence of positive algorithm parameters (defined in Section 3). Choose any . Initialize virtual queues . At each iteration , observe and and do the following:

-

•

Choose to solve .

-

•

Update virtual queue vector via

-

•

Update the running averages via

At each iteration , are given constants. Note that is a linear function and hence is separable; is separable by assumption; and is also separable. Thus, the update of requires to minimize a separable convex function. It follows that each component of can be updated independently by solving a scalar convex program. Thus, each iteration of Algorithm 3 is parallel and has low complexity.

The next lemma shows that if and each are norms, then the update in Algorithm 3 has a closed-form update equation for each coordinate.

Lemma 1.

If , and , then the following holds:

-

1.

The update of in Algorithm 3 can be decomposed into scalar convex programs and each is the solution to a scalar convex program given by

(4) where , and are constants. Note that we use to denote the partial gradient of with respect to the -th component at point .

-

2.

Scalar convex program (4) has a closed-form solution given by

where is the projection onto the interval .

Proof.

-

1.

The first part follows trivially by combining terms of each component in the convex program with vector variable .

-

2.

The second part follows by recalling that the subgradient of is when ; is when ; and is the interval when . The closed-form solution is obtained by considering different ranges of parameters.

The next lemma summarizes that if and , i.e., problem (1)-(3) is a constrained smooth convex program, then update in Algorithm 3 follows a simple projected gradient update, which is parallel for each component as long as is a Cartesian product.

Lemma 2.

If and , then the update of in Algorithm 3 is given by

where and is the projection onto convex set .

Proof.

The projection operator can be reinterpreted as an optimization problem as follows:

| (5) |

where (a) follows from the definition of the projection onto a convex set; and (b) follows from the fact the minimizing solution does not change when we remove constant term and multiply positive constant in the objective function.

Recall that . This lemma follows because (5) is identical to the update of in Algorithm 3 when and .

For constrained smooth convex programs, 2 suggests that Algorithm 3 has a similar per-iteration complexity when compared with Algorithm 1. However, Algorithm 3 can be more easily implemented since it does not require any upper bound of as required by Algorithm 1. Moreover, we shall show that Algorithm 2 has faster convergence in comparison with the slow convergence of Algorithm 1.

2 Preliminaries and Basis Analysis

This section presents useful preliminaries on convex analysis and important facts of Algorithm 3.

2.1 Preliminaries

Definition 1 (Lipschitz Continuity).

Let be a convex set. Function is said to be Lipschitz continuous on with modulus if there exists such that for all .

Definition 2 (Smooth Functions).

Let and function be continuously differentiable on . Function is said to be smooth on with modulus if is Lipschitz continuous on with modulus .

Note that linear function is smooth with modulus . If a function is smooth with modulus , then is smooth with modulus for any .

Lemma 3 (Descent Lemma, Proposition A.24 in [3]).

If is smooth on with modulus , then for all .

Definition 3 (Strongly Convex Functions).

Let be a convex set. Function is said to be strongly convex on with modulus if there exists a constant such that is convex on .

By the definition of strongly convex functions, it is easy to show that if is convex and , then is strongly convex with modulus for any constant .

Lemma 4 (Corollary 1 in [18]).

Let be a convex set. Let function be strongly convex on with modulus and be a global minimum of on . Then, for all .

2.2 Properties of the Virtual Queue Vector and the Drift

The following preliminary results (Lemmas 5-6) on virtual queue vector and its drift are proven for Algorithm 2 in [18] and hold regardless of the update of . Since Algorithm 3 has the same update equation of , these results also hold for Algorithm 3.

Lemma 5 (Lemma 3 in [18]).

In Algorithm 3, we have

-

1.

At each iteration , for all .

-

2.

At each iteration , for all .

-

3.

At iteration , . At each iteration , .

Lemma 6 (Lemma 7 in [18]).

Let be the vector of virtual queue backlogs. Define . The function shall be called a Lyapunov function. Define the Lyapunov drift as

| (6) |

Lemma 7 (Lemma 4 in [18]).

2.3 Properties from Strong Duality

Lemma 8.

Let be an optimal solution of problem (1)-(3) and be a Lagrange multiplier vector satisfying 2. Let be sequences generated by Algorithm 3. Then,

2.4 An Upper Bound of the Drift-Plus-Penalty Expression

Lemma 9.

Let be an optimal solution of problem (1)-(3). For all in Algorithm 3, we have

where and are defined in 1.

Proof.

Fix . By part (2) in 5, . Thus, is convex with respect to . Since is strongly convex with respect to with modulus , it follows that is strongly convex with respect to with modulus .

Since is chosen to minimize the above strongly convex function, by 4, we have

Adding constant on both sides and rearranging terms yields

| (8) |

where (a) follows from the convexity of and each , and the fact that (i.e., part (2) in 5); and (b) follows because , , which further follows from the feasibility of , and (i.e., part (2) in 5).

Recall that is smooth on with modulus by 1. By 3, we have

Adding on both sides, recalling and rearranging terms yields

| (9) |

Recall that each is smooth on with modulus by 1. Thus, each is smooth with modulus . By 3, we have

| (10) |

Summing (10) over yields

Adding on both sides, recalling and rearranging terms yields

| (11) |

Note that the right side of (12) is identical to the left side of (8). Thus, by combining (8) and (12); and rearranging terms, we have

| (13) |

Note that for any . Thus, we have

| (14) |

Substituting (14) into (13) and rearranging terms yields

where (a) follows from the fact that , which further follows from the assumption that is Lipschitz continuous with modulus .

The next corollary follows directly by noting that when each is a linear function.

Corollary 1.

Let be an optimal solution of problem (1)-(3) where each is a linear function. If in Algorithm 3, then for all , we have

where and are defined in 1.

Proof.

Note that if each is a linear function, then we have . Fix . By 9 with and , we have

where (a) follows from .

3 Convergence Time Analysis of Algorithm 3

This section analyzes the convergence time of Algorithm 3 for convex program (1)-(3). In particular, the following two rules for choosing in Algorithm 3 are considered.

-

•

Constant : Choose algorithm parameters via

(15) -

•

Non-decreasing : Choose algorithm parameters via

(18) Note that part (2) of 5 implies , and hence since is a nondecreasing sequence.

3.1 Convex Programs with Linear

This subsection proves that if each is a linear function, then it suffices to choose constant parameters in Algorithm 3 to solve convex program (1)-(3) with an convergence time.

Theorem 1.

Consider convex program (1)-(3) under 1 and 2 where each is a linear function. Let be an optimal solution. Let be a Lagrange multiplier vector satisfying 2. If we choose constant in Algorithm 3 according to (15), then for all , we have

-

1.

.

-

2.

.

where and are defined in 1. That is, Algorithm 3 ensures error decays like and provides an -approximate solution with convergence time .

Proof.

- 1.

-

2.

Fix . Note that (19) can be written as

(20) where (a) follows from the Cauchy-Schwarz inequality; (b) follows from Lipschitz continuity of in 1; and (c) follows from .

3.2 Convex Programs with Possibly Non-linear

Assumption 3.

-

•

There exists such that for all .

-

•

There exists such that for all .

Note that 3 holds when is a compact set.

This subsection proves that if convex program (1)-(3) with possibly nonlinear satisfies Assumptions 1-3, then it suffices to choose non-decreasing parameters according to (18) in Algorithm 3 to solve convex program (1)-(3) with an convergence time.

Lemma 10.

Proof.

- 1.

-

2.

Summing over and rearranging terms yields

where (a) follows from part (1) of this lemma and by recalling that ; and (b) follows because by part (3) in 5.

- 3.

Lemma 11.

Proof.

This lemma can be proven by induction as follows. Note that by (18), we have

where (a) follows from the Cauchy-Schwarz inequality; and (b) follows from where the second inequality follows from part (3) of 5 and the third inequality follows from 3. Thus, we have .

Now assume holds for and consider . By (18), is given by

Since by induction hypothesis, to prove , it remains to prove

By part (3) of 10, we have

| (27) |

where (a) follows the hypothesis in the induction. Thus, we have

where (a) follows from the Cauchy-Schwarz inequality; (b) follows from triangle inequality; (c) follows from (27) and by 3; (d) follows by substituting ; and (e) follow from the basic inequality for any .

Thus, we have . This lemma follows by induction.

The next theorem summarizes the convergence time of Algorithm 3 for convex program (1)-(3) with possibly nonlinear .

Theorem 2.

Consider convex program (1)-(3) under Assumptions 1- 3 with possibly nonlinear . Let be an optimal solution and be a Lagrange multiplier vector satisfying 2. If we choose non-decreasing in Algorithm 3 according to (18), then for all , we have

-

1.

.

-

2.

.

where is defined in 11; and and are defined in 3. That is, Algorithm 3 ensures error decays like and provides an -approximate solution with convergence time .

Proof.

-

1.

Dividing both sides by and using Jensen’s inequality for convex function yields .

- 2.

4 Numerical Experiment: Minimum Variance Portfolio with Norm Constraints

4.1 Minimum Variance Portfolio with the Norm Constraint

Consider the following constrained smooth optimization

| s.t. | |||

where is the weight vector of assets and is the correlation matrix of all assets. This problem is known as global minimum variance portfolio under flexible norm constraints (GMV-N) and the -norm constraint is imposed to avoid a solution that concentrates in low volatility assets. For example, in the special case maximum decorrelation portfolio, we choose in the -norm constraint [10].

Without loss of optimality, we can replace the equality constraint with an inequality constraint in the above formulation to obtain an equivalent reformulation. 111This is because if we relax by , the optimal solution to the relaxed problem must satisfy . This equivalent reformulation is a special case of problem (1)-(3) with and . In general, for any convex programs with a linear equality constraint , we can always replace the equality constraint with two convex inequality constraints and ; and reformulate the convex programs into the general form (1)-(3). In fact, if the convex program has a linear equality constraint , we can modify the corresponding virtual queue in Algorithm 3 as at each iteration to solve it directly. (This is also a property owned by Algorithm 2 to solve convex programs with linear equality constraints, see e.g., footnote 2 in [18].)

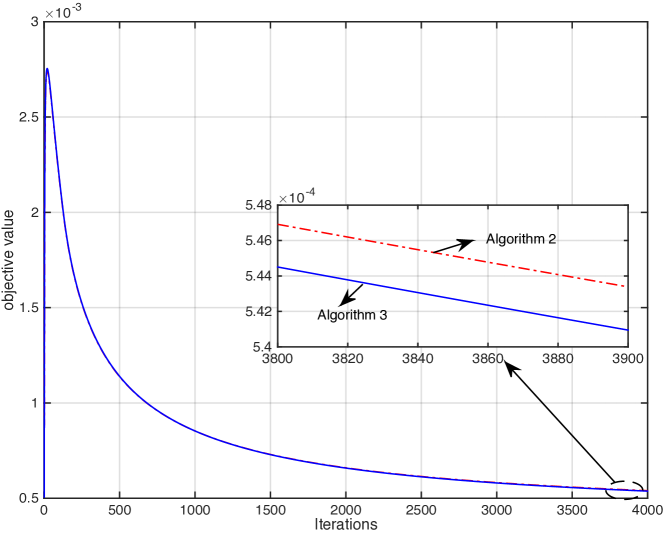

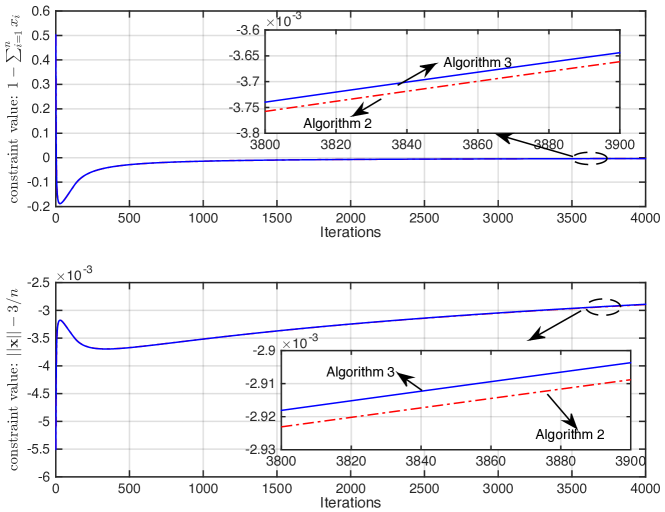

Since is not diagonal, the objective function is not separable and hence at each iteration the update of in Algorithm 2 requires to solve an -dimensional set constrained quadratic program, which can have huge complexity when is large. In contrast, the update of in Algorithm 3 has a closed form update for each coordinate by 2.

In the numerical experiment, we take , and generate correlation matrix where is an matrix follows the standard Gaussian distribution. We run both Algorithm 2 and Algorithm 3 with the same initial point . Fig. 1 and Fig. 2 show that both algorithms have quite similar convergence performance as observed in the zoom-in subfigures. However, when implementing both algorithms using MATLAB in a PC with a 4 core 2.7GHz Intel i7 CPU and 16GB Memory, each iteration of Algorithm 3 only takes around milliseconds while each iteration of Algorithm 2 takes around milliseconds. (Note that our implementation uses quadprog in MATLAB to solve the box constrained quadratic program involved in each iteration of Algorithm 2.) Thus, Algorithm 3 is times faster than Algorithm 2 in this example.

4.2 Minimum Variance Portfolio with the Norm Constraint

Consider the following constrained non-smooth optimization

| s.t. | |||

where is the weight vector of assets and is the correlation matrix of all assets. Note that each component can be possibly negative by assuming that we can sell short the considered assets. The norm constraint is imposed to promote sparsity and other desired properties. For example, the minimum variance portfolio with the shortsale constraint considered in [8] is corresponding to the special case in the norm constraint [5].

Similarly to the minimum variance portfolio with the norm constraint, we can replace the equality constraint with an inequality constraint in the above formulation to obtain an equivalent reformulation that is special case of problem (1)-(3) with , and .

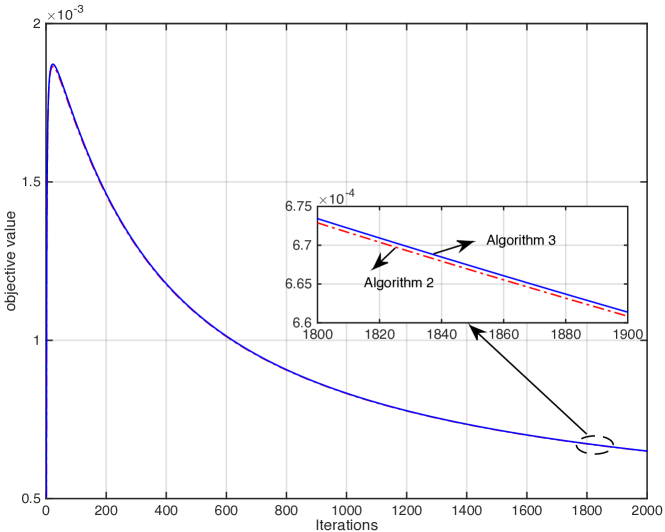

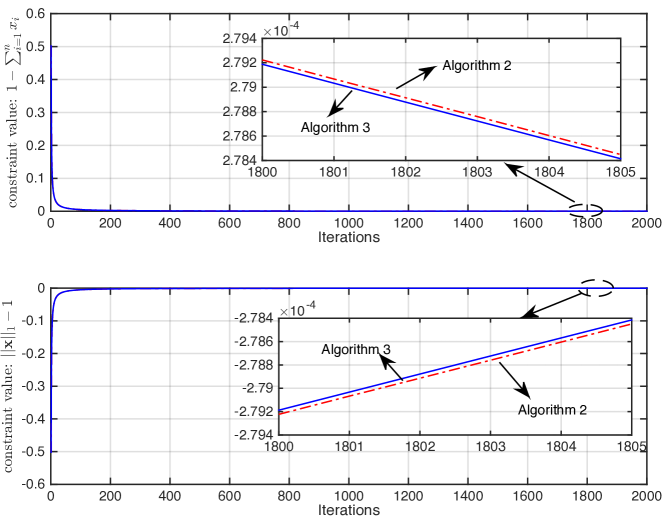

Since is not diagonal, the objective function is not separable and hence at each iteration the update of in Algorithm 2 requires to solve an -dimensional unconstrained composite minimization, which can have huge complexity when is large. In contrast, each iteration of Algorithm 3 has a closed form update for each coordinate by 1.

In the numerical experiment, we take , and generate correlation matrix where is an matrix follows the standard Gaussian distribution. We run both Algorithm 2 and Algorithm 3 with the same initial point . Fig. 3 and Fig. 4 show that both algorithms have quite similar convergence performance as observed in the zoom-in subfigures. However, when implementing both algorithms using MATLAB in a PC with a 4 core 2.7GHz Intel i7 CPU and 16GB memory, each iteration of Algorithm 3 only takes around milliseconds while each iteration of Algorithm 2 takes around seconds. (Note that our implementation uses CVX [7] to solve the unconstrained composite minimization involved in each iteration of Algorithm 2.) Thus, Algorithm 3 is times faster than Algorithm 2 in this example.

5 Conclusion

This paper proposes a new primal-dual type algorithm with convergence for constrained composite convex programs. The new algorithm is faster than the classical primal-dual subgradient algorithm and the dual subgradient algorithm, both of which have an convergence time. The new algorithm has the same convergence time as that of a parallel algorithm recently proposed in [18] for convex programs with separable objective and constraint functions. However, if the objective or constraint function is not separable, the algorithm in [18] is no longer parallel and each iteration requires to solve a set constrained convex program. In contrast, the algorithm proposed in this paper is still parallel when the convex program is smooth or the non-smooth part is separable. In these cases, the new algorithm has much smaller per-iteration complexity than the algorithm in [18].

References

- [1] A. Beck, A. Ben-Tal, N. Guttmann-Beck, and L. Tetruashvili, The CoMirror algorithm for solving nonsmooth constrained convex problems, Operations Research Letters, 38 (2010), pp. 493–498.

- [2] A. Beck and M. Teboulle, A fast iterative shrinkage-thresholding algorithm for linear inverse problems, SIAM journal on imaging sciences, 2 (2009), pp. 183–202.

- [3] D. P. Bertsekas, Nonlinear Programming, Athena Scientific, second ed., 1999.

- [4] J. Brodie, I. Daubechies, C. De Mol, D. Giannone, and I. Loris, Sparse and stable markowitz portfolios, Proceedings of the National Academy of Sciences, (2009).

- [5] V. DeMiguel, L. Garlappi, F. J. Nogales, and R. Uppal, A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms, Management Science, 55 (2009), pp. 798–812.

- [6] X. Gao, Y. Xu, and S. Zhang, Randomized primal-dual proximal block coordinate updates, arXiv:1605.05969, (2016).

- [7] M. Grant and S. Boyd, CVX: Matlab software for disciplined convex programming, version 2.0 beta, http://cvxr.com/cvx, (2013).

- [8] R. Jagannathan and T. Ma, Risk reduction in large portfolios: Why imposing the wrong constraints helps, The Journal of Finance, 58 (2003), pp. 1651–1684.

- [9] G. M. James, C. Paulson, and P. Rusmevichientong, The constrained LASSO, Technical report, University of Southern California, (2012).

- [10] P. J. Kremer, A. Talmaciu, and S. Paterlini, Risk minimization in multi-factor portfolios: What is the best strategy?, Annals of Operations Research, 1–37 (2017).

- [11] A. Nedić and A. Ozdaglar, Approximate primal solutions and rate analysis for dual subgradient methods, SIAM Journal on Optimization, 19 (2009), pp. 1757–1780.

- [12] A. Nedić and A. Ozdaglar, Subgradient methods for saddle-point problems, Journal of Optimization Theory and Applications, 142 (2009), pp. 205–228.

- [13] M. J. Neely, Distributed and secure computation of convex programs over a network of connected processors, in DCDIS International Conference on Engineering Applications and Computational Algorithms, Guelph, Canada, 2005.

- [14] M. J. Neely, A simple convergence time analysis of drift-plus-penalty for stochastic optimization and convex programs, arXiv:1412.0791, (2014).

- [15] Y. Nesterov, Introductory Lectures on Convex Optimization: A Basic Course, Springer Science & Business Media, 2004.

- [16] R. Shefi and M. Teboulle, A dual method for minimizing a nonsmooth objective over one smooth inequality constraint, Mathematical Programming, (2016), pp. 137–164.

- [17] H. Yu and M. J. Neely, A primal-dual type algorithm with the convergence rate for large scale constrained convex programs, in Proceedings of IEEE Conference on Decision and Control (CDC), 2016.

- [18] H. Yu and M. J. Neely, A simple parallel algorithm with an convergence rate for general convex programs, SIAM Journal on Optimization, 27 (2017), pp. 759–783.