A probabilistic scheme for joint parameter estimation and state prediction in complex dynamical systems

Abstract

Many problems in physics demand the ability to calibrate the parameters and predict the time evolution of complex dynamical models using sequentially-collected data. Here we introduce a general methodology for the joint estimation of the static parameters and the forecasting of the state variables of nonlinear stochastic dynamical models. The proposed scheme is essentially probabilistic. It aims at recursively computing the sequence of joint posterior probability distributions of the unknown model parameters and its (time varying) state variables conditional on the available observations. The new framework combines two layers of inference: in the first layer, a grid-based scheme is used to approximate the posterior probability distribution of the fixed parameters; in the second layer, filtering (or data assimilation) techniques are employed to track and predict different conditional probability distributions of the state variables. Various types of procedures (deterministic grids, Monte Carlo, Gaussian filters, etc.) can be plugged into both layers, leading to a wealth of algorithms. For this reason, we refer to the proposed methodology as nested hybrid filtering. In this paper we specifically explore the combination of Monte Carlo and quasi Monte Carlo (deterministic) approximations in the first layer with Gaussian filtering methods in the second layer, but other approaches fit naturally within the new framework. We prove a general convergence result for a class of procedures that use sequential Monte Carlo in the first layer. Then, we turn to an illustrative numerical example. In particular, we apply and compare different implementations of the methodology to the tracking of the state, and the estimation of the fixed parameters, of a stochastic two-scale Lorenz 96 system. This model is commonly used to assess data assimilation procedures in meteorology. We show estimation and forecasting results, obtained with a desktop computer, for up to 5,000 dynamic state variables.

I Introduction

A common feature to many problems in some of the most active fields of science is the need to calibrate (i.e., estimate the parameters) and then forecast the time evolution of high-dimensional dynamical systems using sequentially-collected observations. One can find obvious examples in meteorology, where current models for global weather forecasting involve the tracking of millions of time-varying state variables Clayton13 , as well as in oceanography VanLeeuwen03 or in climate modelling Dee11 . This problem is not constrained to geophysics, though. In biochemistry and ecology it is often necessary to forecast the evolution of populations of interacting species (typically animal and/or vegetal species in ecology and different types of reacting molecules in biochemistry), which usually involves the estimation of the parameters that govern the interaction as well Golightly11 .

I.1 State of the art

Traditionally, model calibration (i.e., the estimation of the model static parameters) and the tracking and forecasting of the time-varying state variables have been addressed separately. The problem of tracking the state of the system using sequentially-collected observations is often termed data assimilation in geophysics, while it is referred to as stochastic or Bayesian filtering by researchers in computational statistics and applied probability. Carrying out both tasks jointly, parameter estimation and state forecasting, is a hard problem posing several practical and theoretical difficulties.

Many procedures have been suggested over the years (see, e.g., Liu01b ; Aksoy06 ; Evensen09 ; Carvalho10 , as well as Kantas15 for a survey), however they are subject to problems related to observability (i.e., ambiguities), lack of performance guarantees or prohibitive computational demands. Some of the most relevant techniques can be classified in one or more of the categories below.

-

•

State augmentation methods with artificial dynamics: the state vector, which contains the dynamical variables that describe the physical system, is extended with any static unknown parameters (commonly reinterpreted as “slowly changing” dynamical variables) in the model Andrieu04 ; Kitagawa98 ; Liu01b ; zhang2016joint . Standard filtering (or data assimilation) techniques are then used in order to track and forecast the extended state vector.

-

•

Particle learning techniques: for some models, the posterior probability distribution of the static parameters, conditional on the system state, can be computed in closed form and it depends only on a set of finite-dimensional statistics Storvik02 ; Djuric02 ; Carvalho10 . In a Monte Carlo setting, e.g., for particle filters, this means that the static parameters can be efficiently represented by sampling. Unfortunately, this approach is restricted to very specific models (an attempt to extend this idea to a more general setting can be found in Djuric04 ). The term particle learning was coined in Carvalho10 , although the fundamental ideas were introduced earlier Storvik02 ; Djuric02 .

-

•

Classical importance resampling methods: several authors have studied the performance of classical sequential importance sampling for static parameters Papavasiliou05 ; Papavasiliou06 ; Olsson08 . Unfortunately, such algorithms tend to degenerate quickly over time unless certain conditions are met by the prior and posterior distributions Papavasiliou05 ; Papavasiliou06 or computationally-heavy interpolation schemes are adopted for the static parameters Olsson08 .

Only in the last few years there have been advances leading to well-principled probabilistic methods that solve the joint problem numerically and supported by rigorous performance analyses Andrieu10 ; Chopin12 ; Crisan18bernoulli . They aim at calculating the posterior probability distribution of all the unknown variables and parameters of the model. From the viewpoint of Bayesian analysis, these conditional, or posterior, distributions contain all the information relevant for the estimation task. From them, one can compute point estimates of the parameters and states but also quantify the estimation error. However, state-of-the-art methods for Bayesian parameter estimation and stochastic filtering are batch techniques, i.e., they process the whole set of available observations repeatedly in order to produce numerical solutions. For this reason, they are not well suited to problems where observations are collected sequentially and have to be processed as they arrive (or, simply, when the sequence of observations is too long). The popular particle Markov chain Monte Carlo (pMCMC) Andrieu10 and the sequential Monte Carlo square (SMC2) Chopin12 schemes are examples of such batch methods. The nested particle filter (NPF) of Crisan18bernoulli is a purely recursive Monte Carlo method, more suitable than pMCMC and SMC2 when long sequences of observations have to be processed. However, this technique is still computationally prohibitive in high dimensional settings as it relies on two layers of intertwined Monte Carlo approximations.

While the schemes in Andrieu10 ; Chopin12 ; Crisan18bernoulli fully rely on Monte Carlo approximations in order to approximate the posterior probability distribution of the parameters and the states, there is an alternative class of schemes, often coined recursive maximum likelihood (RML) methods Andrieu04 ; Andrieu12 ; Kantas15 ; Tadic10 , that enable the sequential processing of the observed data as they are collected but do not yield full posterior distributions of the unknowns. They only output point estimates instead. Therefore, it is not possible to quantify the uncertainty of the estimates or forecasts. Moreover, they are subject to various convergence (and complexity) issues, e.g., when the posterior probability distribution is multimodal, when it contains singularities or when the parameter likelihoods cannot be computed exactly.

In the physics literature, approximation schemes have been proposed that exploit the conditional dependences between the static parameters and the dynamic state variables, in a way that resembles the SMC2 or NPF schemes. The authors of santitissadeekorn2015two introduce a two-stage filter that alternates the estimation of static parameters (conditional on a fixed state estimate) and the tracking of the dynamic variables (conditional on a fixed estimate of the static parameters). Another alternating scheme, that combines Monte Carlos estimators with ensemble Kalman filters in order to handle the static parameters and dynamic states, can be found in frei2012sequential .

In Ashley15 , an expectation-maximization (EM) algorithm is used to track a particle whose dynamics are governed by a hidden Markov model. The expectation step involves a (Monte Carlo based) forward-filtering, backward-smoothing step that is computationally heavy and prevents the online application of the method. The authors of Ye15 investigate a variational scheme (based in the Laplace integral approximation) for data assimilation (including state and parameter estimation) and illustrate it with applications to the Lorenz 63 and Lorenz 96 models in a low dimensional setting. The same task of data assimilation with parameter estimation is tackled in Ito16 . In this case, the estimation of the states and parameter is reduced to an optimization problem that can be solved via an adjoint method for the estimation of a Hessian matrix. The schemes in Ashley15 , Ye15 and Ito16 require to process the data in batches, rather than recursively, and hence they are not well suited for online implementations. A sequential method, based on variational Bayes techniques, that admits an online (recursive) implementation can be found in Vrettas15 . However, the latter contribution is limited to the estimation of the time-varying states and does not deal with unkown static parameters.

I.2 Contribution

In this paper we propose a general probabilistic scheme to perform the joint task of parameter estimation and state tracking and forecasting. The methodology is Bayesian, i.e., it aims at the computation of the posterior probability distribution of the unknowns given the available data. It involves two layers of estimators, one for the static parameters and another one for the time-varying state variables. It can be interpreted that the state estimators and predictors are nested, or inserted, within a main algorithm that tackles the estimation of the parameters. The estimation of the static parameters and the dynamic variables is carried out in a purely sequential and recursive manner. This property makes the proposed method well-suited for problems where long time series of data have to be handled.

It can be shown that a particular case of the proposed scheme is the NPF of Crisan18bernoulli , which relies on a sequential Monte Carlo sampler in the parameter space and bank of particle filters Gordon93 ; Doucet00 in the space of the dynamic variables. However, the key feature and advantage of the general scheme that we advocate here is the ability to combine different types of algorithms in the two layers of inference (parameters and dynamic variables). Any grid-based method (where the probability distribution of the static parameters is represented by a set of points in the parameter space) can be employed in the first layer, while the computationally-heavy particle filters in the second layer of the NPF can be replaced by simpler algorithms, easier to apply in practical problems.

We have investigated the use of sequential Monte Carlo and quasi-Monte Carlo Gerber15 techniques in the parameter estimation layer. We note that the quasi-Monte Carlo scheme is a deterministic technique, although it formally resembles the Monte Carlo approach (hence the name). In the same vein, an unscented Kalman filter (UKF) can be utilized in the parameter estimation layer, although we have left this for future research. For the second layer, we have assessed two Gaussian filters, namely the extended Kalman filter (EKF) and the ensemble Kalman filter (EnKF). These two types of Gaussian filters have been well-studied in the geophysics literature and there are a number of numerical techniques to ease their practical implementation for large-scale systems (e.g., covariance inflation Anderson09 ; Lihong09 or localization Ott04 ; Houtekamer01 ; vossepoel2007parameter ).

Because the flexibility to combine estimation techniques of different types within the same overall scheme is a key advantage of the proposed methodology, we refer to the resulting algorithms in general as nested hybrid filters (NHFs). Besides the numerical example described below, we provide a theoretical result on the asymptotic convergence of NHFs that use a sequential Monte Carlo scheme in the first layer (for the static parameters) and finite-variance estimators of the state variables in the second layer. Our analysis shows that the NHF can be biased if the filters in the second layer are (as it is the case in general with approximate Gaussian filters). However, it also ensures that the approximate posterior distribution of the parameters generated by the NHF, consisting of samples in the parameter space, converges to a well-defined limit distribution with rate under mild assumptions.

To illustrate the performance of the methodology, we present the results of computer simulations with a stochastic two-scale Lorenz 96 model Arnold13 with underlying chaotic dynamics. In meteorology, the two-scale Lorenz 96 model is commonly used as a benchmark system for data assimilation VanLeeuwen10 and parameter estimation techniques Hakkarainen11 because it displays the basic physical features of atmospheric dynamics Arnold13 (e.g., convection and sensitivity to perturbations). We have implemented, and compared numerically, four NHFs that combine Monte Carlo, quasi-Monte Carlo, EKF and EnKF schemes in different ways. All the combinations that we have tried yield significant reductions of running times in comparison with the NPF for this model, without a significant loss of accuracy. We report simulation results for systems with up to 5,000 dynamical variables to track and forecast.

I.3 Organization of the paper

The rest of the paper is organized as follows. After a brief comment on notation, we describe in Section II the class of (stochastic) dynamical systems of interest. NHFs are introduced and explained in Section III. The asymptotic convergence theorem is stated and discussed in Section IV. In Section V, the stochastic Lorenz 96 model which is used in the simulations is described and then, some illustrative numerical results are presented in Section VI. Finally, Section VII is devoted to the conclusions.

I.4 Notation

We denote vectors and matrices by bold-face letters, either lower-case (for vectors) or upper-case (for matrices). Scalar magnitudes are denoted using regular-face letters. For example, and are scalars, is a vector and is a matrix.

Most of the magnitudes of interest in this paper are random vectors (r.v.’s). If is a -dimensional r.v. taking values in , we use the generic notation for its probability density function (pdf). This is an argument-wise notation. If we have two r.v.’s, and , we write and for their respective pdf’s, which are possibly different. In a similar vein, denotes the joint pdf of the two r.v.’s and denotes the conditional pdf of given . We find this simple notation convenient for the presentation of the model and methods and introduce a more specific terminology only for the analysis of convergence. We assume, for simplicity, that all random magnitudes can be described by pdf’s with respect to the Lebesgue measure. Notation is read as “the r.v. is distributed according to the pdf ”.

II Dynamical model and problem statement

II.1 State space models

We are interested in systems that can be described by a multidimensional stochastic differential equation (SDE) of the form

| (1) |

where denotes continuous time, is the -dimensional system state, is a nonlinear function parametrized by a fixed vector of unknown parameters, , is a scale parameter that controls the intensity of the stochastic perturbation and is a vector of independent standard Wiener processes. Very often, the underlying ordinary differential equation (ODE) describes some peculiar dynamics inherent to the system of interest (e.g., many of the systems of interest in geophysics are chaotic) and the addition of the perturbation accounts for model errors or other sources of uncertainty.

Equation (1) does not have a closed-form solution for a general nonlinear function and, therefore, it has to be discretized for its numerical integration. A discretization scheme with fixed step-size yields, in general, a discrete-time stochastic dynamical system of the form

| (2) |

where denotes discrete time, is the system state at time and is a r.v. of dimension that results from the integration of independent Wiener processes. Since the integral of a Wiener process over an interval of length is a Gaussian random variable with zero mean and variance , the r.v. is also Gaussian, with mean and covariance matrix , where is the identity matrix. This was denoted as . The function depends on the choice of discretization scheme. The simplest one is the Euler-Maruyama method, which yields Gard88

| (3) |

i.e., the noise is additive, with , and . For a Runge-Kutta method of order , as a more sophisticated example, and the function results from applying times, with a Gaussian perturbation passing through the nonlinearity at each of these intermediate steps. See Gard88 for details on various integration methods for SDEs. In the sequel, we work with the general Eq. (2).

We assume that the system of Eq. (2) can be observed every discrete-time steps (i.e., every continuous-time units). The -th observation is a r.v. of dimension that we model as

| (4) |

, where is the system state at the time of the -th observation (continuous time ), is a transformation that maps the state into the observation space and is a -mean observational-noise vector with covariance matrix .

II.2 Probabilistic representation and problem statement

The state equation (5) together with the observation equation (4) describe a (stochastic) state space model. The goal is to design methods for the recursive estimation of both the static parameters and the states , . Note that the latter implies the estimation of the sequence , , i.e., the states between observations instants have to be estimated as well.

We adopt a Bayesian approach to this task. From this point of view, both the parameters and the sequence of states are random and we aim at computing their respective probability distributions conditional on the available data, i.e., the sequence of observations . The problem is best described if we replace the functional representation of the state space model in Eqs. (5) and (4) by an equivalent one in terms of pdf’s 111The pdf’s in model (6)–(9) always exist if the functions and are differentiable. There are problems for which the conditional probability distribution of conditional on , which we may denote as , may not have a density with respect to the Lebesgue measure and model (6)–(9) would not be well defined the way it is written. Even in that case, however, the proposed methodology could be applied using approximation filters in the second layer which do not depend on the differentiability of , such as particle filters or EnKF’s.. To be specific, the probabilistic representation consists of the following elements

| (6) | |||||

| (7) | |||||

| (8) | |||||

| (9) |

where and are, respectively, the a priori pdf’s of the system state and the parameter vector at time ( as well), is the conditional pdf of given the state and the parameters in , and is the conditional pdf of the observation given the state and the parameters.

We note that:

-

•

The priors and can be understood as a probabilistic characterization of uncertainty regarding the system initial condition. If the initial condition were known, could be replaced by a Dirac delta allocating probability 1 at that point.

-

•

The pdf does not have, in general, a closed-form expression because of the nonlinearity . However, it is usually straightforward to simulate given and using Eq. (5) and this is sufficient for many methods to work.

-

•

The observations are conditionally independent given the states and the parameters. If the observational noise is Gaussian, then .

From a Bayesian perspective, all the information relevant for the characterization of and at discrete time (corresponding to ) is contained in the joint posterior pdf , where . The latter density cannot be computed exactly in general and the goal of this paper is to describe a class of flexible and efficient recursive methods for its approximation.

We will show that one way to attain this goal is to tackle the approximation of the sequence of posterior pdf’s of the parameters, , . This yields, in a natural way, approximations for and for each , as well as predictions for the densities of the intermediate states, , for .

III Nested Hybrid Filtering

III.1 Importance sampling for parameter estimation

In order to introduce the proposed scheme of nested hybrid filters, let us consider the approximation of the -th posterior probability distribution of the parameters, with pdf , using classical importance sampling Robert04 . In particular, let be an arbitrary proposal pdf for the parameter vector and assume that whenever .

Assume that the posterior at time , , is available. Then the posterior pdf at time can be expressed, via Bayes’ theorem, as

| (10) |

where the proportionality constant, , is independent of . Expression (10) enables the application of the importance sampling method to approximate integrals w.r.t. the posterior pdf (i.e., to approximate the statistics of this probability distribution). Specifically, if we

-

•

draw independent and identically distributed (i.i.d.) samples from , denoted , ,

-

•

compute importance weights of the form

and normalize them to obtain

then it can be proved Robert04 that

| (11) |

for any integrable function under mild regularity assumptions. In this way one could estimate the value of , e.g.,

where denotes the expected value of conditional on the observations . We could also estimate the mean square error (MSE) of this estimator, as

| (12) |

The choice of is, of course, key to the complexity and the performance of importance sampling schemes. One particularly simple choice is , which reduces the importance sampling algorithm to

-

1.

drawing i.i.d. samples , , from , and

-

2.

computing normalized importance weights

Unfortunately, this method is not practical because

-

•

it is not possible to draw exactly from , since this pdf is unknown, and

-

•

the likelihood function cannot be evaluated exactly either.

In the sequel we tackle the two issues above and, in doing so, obtain a general scheme for the approximation of the posterior distribution of the parameter vector and the state vector , i.e., the distribution with pdf .

III.2 Sequential Monte Carlo hybrid filter

It is well known that the likelihood can be approximated using filtering algorithms Andrieu10 ; Koblents15 . To be specific, function can be written as the integral

| (13) |

where, in turn, the predictive density is

| (14) |

and

| (15) |

Given a fixed parameter vector and a prior pdf , the sequence of likelihoods can be computed by recursively applying Eqs. (13), (14) and (15) for .

Let us now assume that we are given a sequence of parameter vectors and we are interested in computing the likelihood of the last vector, . Following Crisan18bernoulli , one can compute a sequence of approximate likelihoods , , using the recursion

| (16) | |||||

| (17) | |||||

| (18) |

which starts with the initial density . It can be proved, using the same type of continuity arguments in Crisan18bernoulli , that the approximation error

| (19) |

can be kept bounded, for any , provided some simple assumptions on the state space model and the sequence are satisfied. Note that, in expression (19), is the actual likelihood calculated by iterating (13), (14) and (15) for , while is the approximation computed using the sequence and recursion (16)–(18).

The recursive approximation scheme for can be combined with the “naive” IS procedure of Section III.1 to yield a general (and practical) method for the approximation of the sequence of a posteriori probability distributions of the parameter vector , hereafter denoted as

We refer to the proposed scheme as a nested hybrid filter (NHF) and provide a detailed outline in Algorithm 1.

Algorithm 1

Nested hybrid filter (NHF).

Inputs:

-

-

Number of Monte Carlo samples, .

-

-

A priori pdf’s and .

-

-

A Markov kernel which, given , generates jittered parameters .

Procedure:

-

1.

Initialization

Draw , i.i.d. samples from .

-

2.

Recursive step

-

(a)

For :

-

i.

Draw from .

-

ii.

Approximate using a filtering algorithm.

-

iii.

Use this approximation to compute the estimate

(20) and let be the normalized weight of .

-

i.

-

(b)

Resample the discrete distribution

(21) times with replacement in order to obtain the particle set and the approximate probability measure .

-

(a)

Outputs: A set of particles and a probability measure .

Algorithm 1 is essentially a sequential Monte Carlo (SMC) method, often known as a particle filter Gordon93 ; Liu98 ; DelMoral04 . At each time step , the output of the algorithm is an estimate of the posterior probability distribution . Specifically we construct the discrete and random probability measure

| (22) |

that can be used to approximate any integrals w.r.t. the true probability measure . For example, one can estimate any posterior expectations of the parameter vector given the observations , namely

| (23) |

Since we have constructed a complete distribution, statistical errors can be estimated as well. The a posteriori covariance matrix of vector can be approximated as

| (24) |

As a byproduct, Algorithm 1 also yields an approximate predictive pdf for , namely

If one computes the approximate filter, as well, then the joint probability distribution of and conditioned on (denoted ) can be approximated as

The scheme of Algorithm 1 is referred to as nested because the SMC algorithm generates, at each time step , a set of samples and, for each sample , we embed a filter in the state space in order to compute the pdf and the approximate likelihood . The term hybrid is used because the embedded filters need not be Monte Carlo methods –a variety of techniques can be used and in this paper we focus on Gaussian filters, which are attractive because of their (relative) computational simplicity. A scheme with nested particle filters was thoroughly studied in Crisan18bernoulli ; Crisan17 .

Let us finally remark that the NHF scheme relies on two approximations:

-

•

Jittering of the parameters: The difficulty of drawing samples from can be circumvented if we content ourselves with an approximate sampling step. In particular, if we have computed a Monte Carlo approximation at time (with some of the samples replicated because of the resampling step) then we can generate new particles , , where is a Markov kernel, i.e., a probability distribution for conditional on . See Section IV for guidelines on the selection of this kernel. Intuitively, we can either jitter a few particles with arbitrary variance (while leaving most of them unperturbed) or jitter all particles with a controlled variance that decreases as increases.

-

•

Estimation of likelihoods: The sequential approximation of Eqs. (16)–(18) yields biased estimates of the likelihoods Crisan18bernoulli . This is discussed in Section IV. In Appendix A we provide details on the computation of the estimates and using an ensemble Kalman Filter (EnKF). Other techniques (e.g., particle filters as in Crisan18bernoulli or sigma-point Kalman filters Ambadan09 ; Arasaratnam09 ) can be used as well.

III.3 Sequential quasi Monte Carlo hybrid filter

The SMC method in the first layer of Algorithm 1 can be replaced by other schemes that rely on the point-mass representation of the posterior probability distribution . It is possible to devise procedures based, for instance, on an unscented Kalman filter Julier04 or other sigma-point Kalman methods Ambadan09 ; Arasaratnam09 to obtain a Gaussian approximation of . Such Gaussian approximations, however, can be misleading when the posterior distribution is multimodal.

In this subsection, we describe a NHF method (hence, of the same class as Algorithm 1) where the SMC scheme is replaced by a sequential quasi-Monte Carlo (SQMC) procedure of the type introduced in Gerber15 . The term quasi-Monte Carlo (QMC) refers to a class of deterministic methods for numerical integration Niederreiter92 that employ low-discrepancy point sets (e.g., Halton sequences Halton64 or Sobol sequences Bratley88 ), instead of random sample sets, for the approximation of multidimensional integrals. In the context of QMC, discrepancy is defined to quantify how uniformly the points in a sequence are distributed into an arbitrary set . Hence, the lowest discrepancy is attained when these points are equi-distributed. The main advantage of (deterministic) QMC methods over (random) Monte Carlo schemes is that they can attain a faster rate of convergence relative to the number of points in the grid, . The main disadvantage is that the generation of low-discrepancy points in high-dimensional spaces can be computationally very costly compared to the generation of random Monte Carlo samples Martino18 . Within a NHF, the use of QMC should lead to a better performance/complexity trade-off as long as the parameter dimension, , is relatively small. This is illustrated numerically for a stochastic two-scale Lorenz 96 model in Section VI.

The NHF based on the SQMC methodology of Gerber15 can be obtained from Algorithm 1 if we replace the sampling and resampling steps typical of the SMC schemes by the generation of low-discrepancy point sets. Let be a Halton sequence of low-discrepancy (deterministic) uniform samples Halton64 . These uniform samples can be used to generate low-discrepancy variates from other distributions via a number of methods 222One can use a number of techniques used to produce random samples from a given uniform source. See Martino18 for a comprehensive description of the field, both for single and multivariate distributions.. For example, the Box-Muller transformation BoxMuller can be used to generate pairs of independent, standard, normally distributed pseudo-random numbers. We explicitly indicate the use of low-discrepancy uniform numbers, , in the generation of samples with general distributions by conditioning on . Hence, drawing the -th sample from the prior parameter pdf, , is now replaced by . In order to propagate the -th sample at time , , into time , we draw from the kernel . If sampling is needed in the second layer of filters (in order to compute the estimates and ) we use additional Halton sequences in a similar way.

In order to keep the low-discrepancy property across the resampling step, we additionally introduce the following functions (see Gerber15 for details).

-

•

A discrepancy-preserving bijective map . Several choices are possible for this function. Following Gerber15 , here we assume

(25) where and are the -dimensional vectors whose -th components are, respectively,

whereas and , , are component-wise means and variances.

-

•

The inverse Hilbert curve, , which is a continuous fractal space-filling curve that provides a locality-preserving map between a 1-dimensional and a -dimensional space Moon01 .

The SQMC-based NHF is outlined in Algorithm 2.

Algorithm 2

Sequential quasi Monte Carlo nested hybrid filter (SQMC-NHF).

Inputs:

-

-

Number of Monte Carlo samples, .

-

-

A priori pdf’s and .

-

-

A Markov kernel which, given , generates jittered parameters .

Procedure:

-

1.

Initialization

-

(a)

Generate QMC uniform samples in . Draw , .

-

(a)

-

2.

Recursive step, .

-

(a)

For :

-

i.

If , then draw , else draw , for .

-

ii.

Approximate .

-

iii.

Use this approximation to compute the estimate

(26) and let be the normalized weight of .

-

i.

-

(b)

Generate a QMC point set in ; let .

-

(c)

Hilbert sort: find a permutation such that

-

(d)

Resampling: find a permutation such that . For , set if, and only if,

-

(a)

Outputs: A set of particles and a probability measure .

IV Convergence analysis

The nested filtering schemes of Section III admit various implementations depending on how we choose to approximate the conditional pdf which, in turn, is needed to estimate the likelihood function and compute the importance weights , .

For each choice of approximation method, the estimate may behave differently and yield different convergence properties. Here we assume that is a random variable with finite mean and finite moments up to some prescribed order . Specifically, we make following assumption.

A. 1

Given , the estimator is random and can be written as

| (27) |

where is a zero-mean r.v. satisfying for some prescribed . Furthermore, the mean has the form

| (28) |

where is a deterministic and absolutely bounded bias function.

In the sequel, we use to denote the support set of the parameter vector . Given a real function , its absolute supremum is indicated as . The set of absolutely bounded real functions on is denoted , i.e., . For our analysis we assume that and, since we have also assumed the bias function to be bounded, it follows that , i.e., . To be precise, we impose the following assumption.

A. 2

Given a fixed sequence of observations , the family of functions satisfies the following inequalities for each :

-

1.

, and

-

2.

for any .

Since , A.2.1 follows from assumption A.1. Similarly, if for all then A.2.2 is a natural assumption (since is an estimator of a positive magnitude).

We shall prove that, because of the bias , the approximation converges to the perturbed probability measure induced by the mean function , instead of the true posterior probability measure induced by the true likelihood function .

To be specific, the sequence of posterior measures , , can be constructed recursively, starting from a prior , by means of the projective product operation Bain08 , denoted . When is a positive and bounded function and is a probability measure, the new measure is defined in terms of its integrals. In particular, if then

For conciseness, hereafter we use the shorthand

for the integral of a function w.r.t. a measure . With this notation, we can write

| (29) |

If, instead of the true likelihood , we use the biased function to update the posterior probability measure associated to the parameter vector at each time then we obtain the new sequence of measures

where, according to the definition of the projective product,

for any integrable function . Note that the two sequences, and , start from the same prior . Obviously, we recover the original sequence, i.e, , when the bias vanishes, .

In this section we prove that the approximation generated by a generic nested filter that satisfies A.1 and A.2 converges to in , for each , under additional regularity assumption on the jittering kernel .

A. 3

The kernel used in the jittering step satisfies the inequality

| (30) |

for every and some constant independent of .

A simple kernel that satisfies A.3 is Crisan18bernoulli

where and is an arbitrary Markov kernel with mean and finite variance, for example , where and is the identity matrix. Intuitively, this kind of kernel changes each particle with probability and leaves it unmodified with probability .

Finally, we can state a general result on the convergence of Algorithm 1. For a real random variable and , let denote the norm, i.e. .

Theorem 1

Proof: See Appendix B.

We remark that Theorem 1 does not state that the approximate posterior probability measure output by Algorithm 1, , converges to the true posterior measure , but to the biased version . Moreover, the latter depends on the choice of filters used in the second layer of Algorithm 1 (i.e., on the estimator of the likelihood, ). The value of this theorem is that it guarantees the numerical consistency of the the nested hybrid filter: as we increase the computational effort (by increasing ), the random probability measure converges to a well defined limit (and so do any point estimators that we may derive from it, e.g., the posterior mean estimator ). The connection between this limit measure, , and the true posterior measure is given by assumption A.1 and the projective product operation, namely,

with both sequences starting with a common prior measure . The practical performance of the proposed schemes (with finite ) is explored numerically in the sequel.

V A stochastic Lorenz 96 model

In order to assess the proposed methods numerically, we have applied them to a stochastic, discrete-time version of the two-scale Lorenz 96 model Arnold13 ; Hakkarainen11 ; Hirata14 . The latter is a deterministic system of nonlinear differential equations that displays some key features of atmosphere dynamics (including chaotic behavior) in a relatively simple model of arbitrary dimension (the number of dynamic variables can be scaled as needed). The model consists of two sets of dynamic variables, and . The system of stochastic differential equations takes the form

| (32) |

where and represent the slow and fast variables, respectively, and are Wiener processes, are known scale parameters and is a parameter vector of dimension . Let us assume there are slow variables, , , and fast variables per slow variable, i.e., , , overall. The maps and are and functions, respectively, that can be written (skipping the time index ) as

| (33) |

where contains the parameters ,, and . The forcing parameter controls the turbulence of the chaotic flow, determines the time scale of the fast variables , controls the strength of the coupling between the fast and slow variables and determines the amplitude of the fast variables Arnold13 . The dynamic variables are assumed to be arranged on a circular structure, hence the operations on the indices are modulo and operations on the indices are modulo . This means that for any integer , and . Notation indicates the truncation of a positive real number to the closest integer smaller than .

We apply the 4th order Runge-Kutta (RK4) method Gard88 to obtain a discrete-time version of the two-scale Lorenz 96 model. To be specific, we numerically integrate Eq. (32) by means of the stochastic difference equations

| (34) |

where is the integration step-size, and and are sequences of i.i.d. standard Gaussian r.v.’s.

We assume that the observations are linear but can only be collected from this system once every discrete-time steps. Moreover, only 1 out of slow variables can be observed. Therefore, the observation process has the form

| (35) |

where and is a sequence of i.i.d. r.v.’s with common pdf .

In our computer experiments, system (33) is often employed to generate both ground-truth values for the slow variables and synthetic observations, . As a forecast model for the slow variables it is common Hakkarainen11 to use the SDE

| (36) |

where is a (constant) parameter vector, contains all the parameters, function is a polynomial ansatz for the coupling term in (33) and is a standard Wiener process. In this paper we assume that is a polynomial in of degree , characterized by the coefficients and as

Then, the system (34) can be replaced by

| (37) |

where is the RK4 approximation of the function in Eq. (36).

Assuming is Gaussian distributed and is a sequence of independent and identically distributed noise terms with Gaussian probability distribution, , then

| (38) |

which denotes a -dimensional Gaussian density with zero mean and covariance matrix , where is the identity matrix.

VI Numerical results

We have conducted computer simulations to illustrate the performance of the proposed NHF methods. In particular, we have carried out computer experiments for six different schemes: the NPF of Crisan18bernoulli , the two-stage filter of Santitissadeekorn15 and four NHFs that rely on the SQMC and the SMC, both in combination with EKFs or EnKFs. Then, two different versions of Algorithm 1 (SMC-EKF, SMC-EnKF) and Algorithm 2 (SQMC-EKF, SQMC-EnKF) are simulated. The simulation setup is described below, followed by the discussion of our numerical results in Section VI.2.

VI.1 Simulation setup

For our computer experiments we have used the two-scale Lorenz 96 model of Eq. (32), in order to generate

-

•

reference signals , , used as ground truth for the assessment of the estimators, and

-

•

sequences of observations, , as in Eq. 25.

The model is integrated using the RK4 method with Gaussian perturbations Gard88 (as outlined in Eq. (34)). The integration step is set to continuous-time units through all experiments and the fixed model parameters are , , and . For all experiments, we assume that there are fast variables per slow variable, hence the total dimension of the model is (with different values of for different experiments). The noise scaling factors are and , both assumed known. We assume that half of the slow variables are observed in Gaussian noise, i.e., .

We assess the accuracy of the estimation algorithms in terms of the mean square error (MSE) of the predictors of the dynamic variables. For the NHFs, these estimators take the form

| (39) |

where is the posterior-mean estimate obtained from the approximate filter , that can be expressed as , since the approximation is Gaussian. In the plots, however, we show the empirical MSE per dimension resulting directly from the simulations,

| (40) |

averaged over 100 independent simulation runs, being all of them of 40 continuous-time units of duration.

The simulations presented below include running times for the different methods. They have been coded in Matlab R2016a and run on a computer with 64 GB of DRAM and equipped with two Intel Xeon E5-2680 processors (running at 2.80GHz) with 10 cores each and HyperThreading as well as an Intel Xeon Phi co-processor.

VI.2 Results

Table 1 shows a comparison of the performance of the NPF, the two-stage filter and the four NHFs, based on the use of SMC, SQMC, EKF and EnKF schemes as described in Section III, in terms of their running times and the MSE of the state estimators (averaged over time and dimensions). We have carried out this computer simulation for a model with dimension and a gap between observations of continuous-time units. All NHFs algorithms work with particles for the approximation of the posterior distributions of the fixed parameters, using samples per each EnKF in the second-layer. It can be seen that the highest error is achieved by the NPF, followed by the two-stage filter method. The NPF is also the algorithm that takes the longest running time. Both NHFs using EKF attain the least MSE with the smallest running time. In order to improve the performance of the NPF, the numbers of particles and would have to be considerably increased, but this would increase the running times correspondingly (the complexity of the NPF is Crisan18bernoulli ).

| Algorithm | Running time (minutes) | MSE |

|---|---|---|

| NHF: SQMC-EKF | 2.16 | 0.46 |

| NHF: SMC-EKF | 2.27 | 0.49 |

| NHF: SQMC-EnKF | 6.83 | 0.62 |

| NHF: SMC-EnKF | 7.12 | 0.95 |

| Two-Stage Filter | 6.85 | 4.59 |

| NPF | 17.96 | 11.91 |

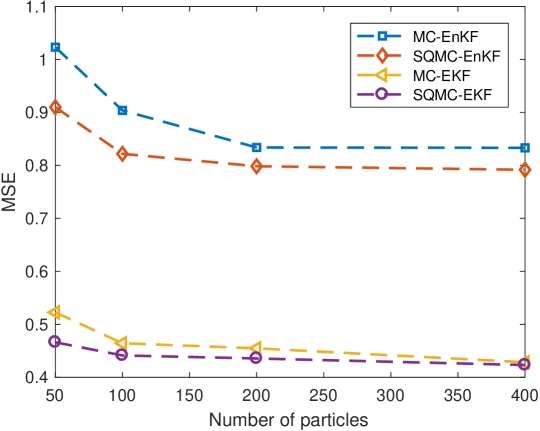

In the next experiment we assess the performance of the different NHFs depending on the number of particles used in the first-layer of the filter, in order to choose appropriately this number to carry out the following computer experiments. For this purpose, we consider a model with dimension , a gap between observations of continuous-time units and a number of particles that ranges from to . Figure 1 shows the numerical results for this experiment. We observe that the MSE for the four algorithms stabilizes quickly. At the sight of these results, we set for all remaining experiments. Additionally, Figure 1 also shows the difference between the NHFs. Specifically, we see that using SQMC in the first-layer we can slightly improve slightly the performance. For this reason, in the next experiments we only simulate NHFs that rely on SQMC. Moreover, it is easy to observe that the filters that use EKFs in the second-layer obtain better results.

In the next set of computer experiments we compare the SQMC-EKF and the SQMC-EnKF methods in terms of their average MSE and their running times for different values of the state dimension and the gap between consecutive observations (in discrete time steps). For each combination of and we have carried out 100 independent simulation runs. The number of particles in the parameter space is fixed, , for all simulations, but the size of the ensemble in the EnKFs is adjusted to the dimension, in particular, we set .

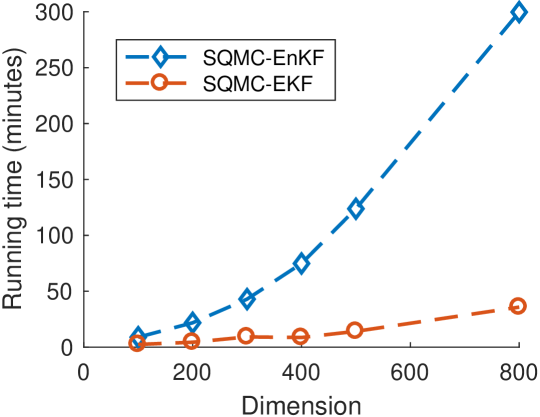

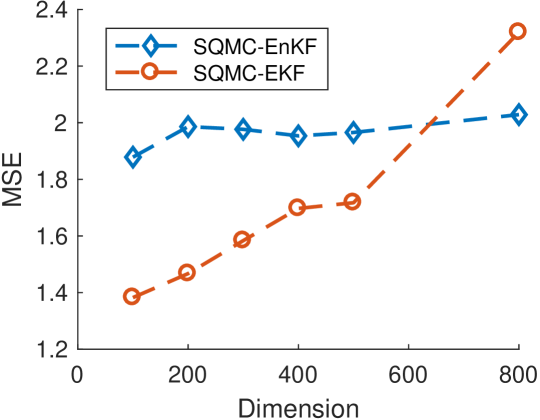

Figure 2 shows (a) the running times and (b) the average MSE attained by the two SQMC NHFs when the state dimension ranges from to . The gap between observations is fixed to (i.e., time units versus in Figure 1). We observe that the SQMC-EKF method attains significantly lower running times compared to the SQMC-EnKF, since the former increases linearly with dimension while the latter increases its cost exponentially. However, the SQMC-EKF obtains an MSE which increase with the dimension , while the values of MSE for the SQMC-EnKF method are steady w.r.t. .

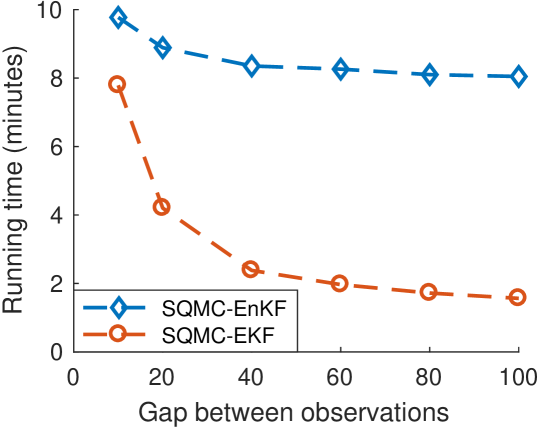

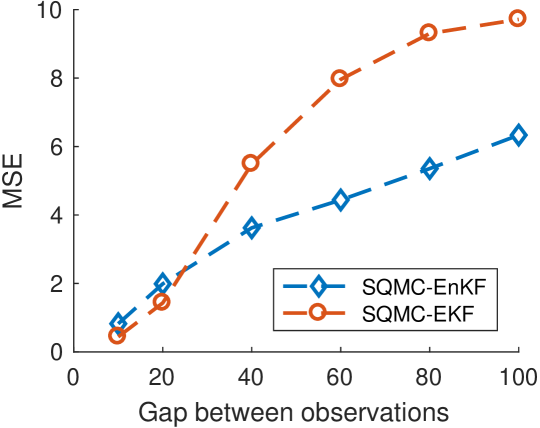

Next, Figure 3 displays the running times and the average MSEs attained by the two NHFs as we increase the gap between observations from to (hence, from to continuous time units). The dimension of the state for this experiment is fixed to . Note that, as the gap increases, less data points are effectively available for the estimation of both the parameters and the states. We observe, again, that the SQMC-EnKF is computationally more costly than the SQMC-EKF, however it attains a consistently smaller MSE when the gap between observations increases, suggesting that it may be a more efficient algorithm in data-poor scenarios.

Finally, we show results for a computer experiment in which we have used the SQMC-EnKF method to estimate the parameters and and track the state variables of the two-scale Lorenz system with dimension and a gap between consecutive observations of continuous-time units. As in the rest of computer simulations, the number of particles used to approximate the sequence of parameter posterior distributions is .

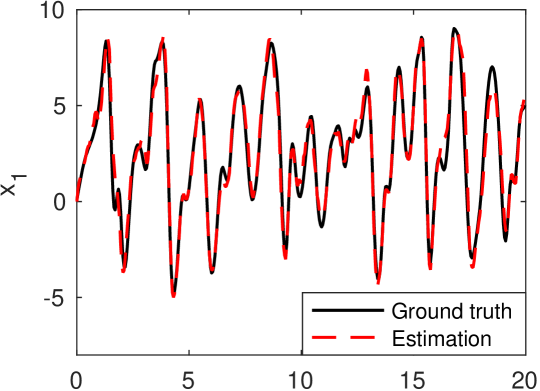

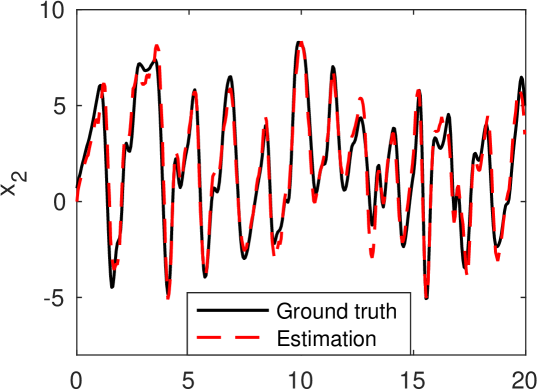

Figure 4 shows the true state trajectories, together with their estimates, for the first two slow state variables of the two-scale Lorenz 96 model. We note that the first variable, , is observed in Gaussian noise (with ) while the second variable, , is not observed. The accuracy of the estimation is similar, though, over the 20 continuous-time units of the simulation run (corresponding to discrete time steps), achieving and . Taking into account the steadiness of MSE w.r.t. dimension of SQMC-EnKF in Figure 2(b) and the values of MSE shown in Figure 3(b) for the gap selected in this experiment (), the results obtained are within the expected range.

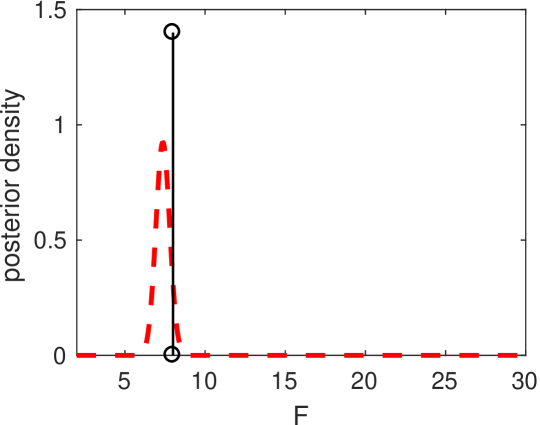

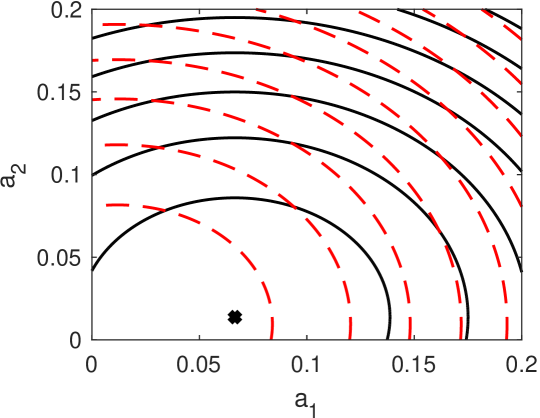

In Figure 5 we observe the estimated posterior pdf’s of the fixed parameters , and , together with the reference values. Note that the value is ground truth, but the values of and are genie-aided least-squares estimates obtained by observing directly the fast variables of the two-scale model. Figure 5(a) displays the true value (vertical line) together with the approximate posterior pdf generated by the same Euler algorithm. We observe that nearly all probability mass is allocated close to the true value. In Fig. 5(b) we compare the approximate pdf of the coefficients produced by the NHF with a kernel density estimator computed from the least-squares genie-aided estimates computed over 100 independent simulations with the same setting. The modes of the two pdf’s are slightly shifted but the two functions are otherwise similar. The genie-aided estimate of is located in a light probability region of the density function computed by the NHF.

VII Conclusions

We have introduced a nested filtering methodology to recursively estimate the static parameters and the dynamic variables of nonlinear dynamical systems. The proposed framework combines a recursive Monte Carlo approximation method to compute the posterior probability distribution of the static parameters with a variety of filtering techniques to estimate the posterior distribution of the state variables of the system. In particular, we have investigated the use of Gaussian filters, as they admit fast implementations that can be well suited to high dimensional systems. As a result, we have proposed a class of nested hybrid filters that combine Monte Carlo and quasi Monte Carlo schemes for the (moderate dimensional) unknown static parameters of the dynamical system with either extended Kalman filtering or ensemble Kalman filtering for the (higher dimensional) time-varying states. Additionally, when sequential MC is applied in the first layer of the NHF scheme, we have proved that the algorithm converges with rate to a well defined limit distribution. We have presented numerical results for a two-scale stochastic Lorenz 96 system, a model commonly used for the assessment of data assimilation methods in the Geophysics. We illustrate the average performance of the methods in terms of estimation errors and running times, and show numerical results for a 5,000-dimensional system. This has been achieved with a relatively inefficient implementation of the method running on a desktop computer, hence we expect that the method can be applied to much larger scale systems using adequate hardware and software.

Acknowledgments

This research has been partially supported by the Spanish Ministry of Economy and Competitiveness (projects TEC2015-69868-C2-1-R ADVENTURE and TEC2017-86921-C2-1-R CAIMAN) and the Office of Naval Research (ONR) Global (Grant Award no. N62909-15-1-2011).

Appendix A Nested hybrid filter implementation using a bank of ensemble Kalman filters

In this appendix we outline a version of the NHF that employs the ensemble Kalman filter (EnKF) Evensen03 in order to compute the posterior (approximate) pdf’s and , which are needed to evaluate the importance weights . In the EnKF, the approximate filter is represented by an ensemble of Monte Carlo particles , which can be combined to yield an empirical covariance matrix .

Each ensemble can be stored in a matrix . The -th mean and the -th covariance matrix can be computed as

respectively, where is an -dimensional column vector and is an ensemble of deviations from . We hence write as a shorthand for the pdf .

We assume that the prior pdf of the state is Gaussian with known mean and covariance matrix, namely

| (41) |

The noise terms in the state space model are also assumed Gaussian, with zero mean and known covariance matrices,

| (42) |

The NHF constructed around a bank of EnKFs is outlined in Algorithm 3 below.

Algorithm 3

NHF via EnKF.

-

1.

Initialization: draw N i.i.d. particles and , . Let , .

-

2.

Recursive step: at time , we have obtained and, for each , .

-

(a)

Prediction step:

-

i.

Draw , .

-

ii.

For each compute

(43) where , , is a matrix of Gaussian perturbations ( denotes the order of the underlying RK integrator).

-

iii.

Set .

-

i.

-

(b)

Update step:

-

i.

For , compute

(44) (45) (46) (47) where is the measurement noise covariance, and , with and a matrix of Gaussian perturbations. and are calculated as

(48) (49) -

ii.

Compute and obtain the normalized weights,

(50) -

iii.

Set the filter approximation

(51)

-

i.

-

(c)

Resampling: draw indices from the multinomial distribution with probabilities , then set

(52) for . Hence

-

(a)

Appendix B Proof of Theorem 1

B.1 Outline of the proof

We need to prove that the approximation generated by a generic nested filter that satisfies assumptions A.1, A.2 and A.3 converges to in , for each . We split the analysis of the nested filter in three steps: jittering, weight computation and resampling. The approximation of is available at the beginning of the -th time step. After jittering, we obtain a new approximation,

| (53) |

that can be proved to converge to using an auxiliary result from Crisan18bernoulli . After the computation of the weights, the measure

| (54) |

is obtained and its convergence towards has to be established. Finally, after the resampling step, a standard piece of analysis proves the convergence of

| (55) |

to . Below, we provide three lemmas for the conditional convergence of , and , respectively. Then we combine them in order to prove Theorem 1 by an induction argument.

B.2 Jittering

In the jittering step, a new cloud of particles is generated by propagating the existing samples across the kernels , . This step has been analyzed in Crisan18bernoulli in the context of the NPF. Several types of kernels can be used. In general, there is a trade-off between the number of particles that are changed using this kernel and the “amount of perturbation” that can be applied to each particle. For this reason, we let the jittering kernel depend explicitly on . For our analysis, assumption A.3 is sufficient.

The convergence results to be given in this appendix are presented in terms of upper bounds for the norms of the approximation errors. For a random variable , its norm is . The approximate measures generated by the nested filter, e.g., , are measured-valued random variables. Therefore, integrals of the form , for some , are real random variables and it makes sense to evaluate the norm of the random error . We start with the approximation produced after the jittering step at time .

Lemma 1

Let the sequence of observations be arbitrary but fixed. If , A.3 holds and

| (56) |

for some and a constant independent of , then

| (57) |

where the constant is also independent of .

Proof: The proof of this Lemma is identical to the proof of (Crisan18bernoulli, , Lemma 3).

B.3 Computation of the weights

In order to analyze the errors at the weight computation step we rely on assumption A.2. An upper bound for the error in the weight computation step is established next.

Lemma 2

Proof: We address the characterization of the weights and, therefore, of the approximate measure . From the definition of the projective product in (29), the integrals of w.r.t. and can be written as

| (60) |

respectively. From (60) one can write the difference as

which readily yields the inequality

| (61) |

by simply noting that , since is a probability measure. From (61) and Minkowski’s inequality we easily obtain the bound

| (62) | |||||

where from assumption A.2.2.

We need to find upper bounds for the two terms on the right hand side of (62). Consider first the term . A simple triangle inequality yields

| (63) |

On one hand, since (see A.2.1), it follows from the assumption in Eq. (58) that

| (64) |

where is a constant independent of .

On the other hand, we may note that

| (65) |

Let be the -algebra generated by the random particles and assume that is even. Then we can apply conditional expectations on both sides of (65) to obtain

where the expression on the right hand side has been simplified by using the assumption in A.1. Also from assumption A.1, the random variables are conditionally independent (given ), have zero mean and finite moments of order , . If we realise that

and bear in mind the conditional independence of the ’s, then it is an exercise in combinatorics to show that the number of non-zero terms in

is at most , for some constant independent of and . Since each of the non-zero terms is upper bounded by (using A.1 again), then it follows that

| (66) |

for even . Given (66), it is straightforward to show that the same result holds for every using Jensen’s inequality. Finally, since the bound on the right hand side of (66) is independent of , we can take expectations on both sides of the inequality and obtain that

| (67) |

Substituting (67) and (64) into (63) yields

| (68) |

where is a constant independent of .

The same argument leading to the bound in (68) can be repeated, step by step, on the norm (simply taking ), to arrive at

| (69) |

B.4 Resampling

The quantification of the error in the resampling step of the nested filter is a standard piece of analysis, well known from the particle filtering literature (see, e.g., Bain08 ). We can state the following result.

Lemma 3

Let the sequence of observations be arbitrary but fixed. If and

| (70) |

for a constant independent of , then

where the constant is independent of as well.

Proof: See, e.g., the proof of (Miguez13b, , Lemma 1).

B.5 An induction proof for Theorem 1

Appendix C Simplification of the inverse

The predictive covariance of the observation vector is a matrix . Inverting has a cost , which can become intractable. Assuming that variables located “far away” in the circumference of the Lorenz 96 model have small correlation we can approximate as a block diagonal matrix, namely, , where denotes element-wise product,

| (71) |

is a mask matrix and and are, respectively, matrices of zeros and ones of dimension . There are blocks in the diagonal of , hence . The original matrix could contain some non-zero values where the zero blocks of are placed, however their values are assumed close to zero. The resulting matrix,

with a computational cost .

References

- [1] A. Aksoy, F. Zhang, and J. W. Nielsen-Gammon. Ensemble-based simultaneous state and parameter estimation in a two-dimensional sea-breeze model. Monthly Weather Review, 134(10):2951–2970, 2006.

- [2] Jaison Thomas Ambadan and Youmin Tang. Sigma-point kalman filter data assimilation methods for strongly nonlinear systems. Journal of the Atmospheric Sciences, 66(2):261–285, 2009.

- [3] Jeffrey L Anderson. Spatially and temporally varying adaptive covariance inflation for ensemble filters. Tellus A, 61(1):72–83, 2009.

- [4] C. Andrieu, A. Doucet, and R. Holenstein. Particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society B, 72:269–342, 2010.

- [5] C. Andrieu, A. Doucet, S. S. Singh, and V. B. Tadić. Particle methods for change detection, system identification and control. Proceedings of the IEEE, 92(3):423–438, March 2004.

- [6] Christophe Andrieu, Arnaud Doucet, and Vladislav B Tadić. One-line parameter estimation in general state-space models using a pseudo-likelihood approach. IFAC Proceedings Volumes, 45(16):500–505, 2012.

- [7] I. Arasaratnam and S. Haykin. Cubature kalman filters. IEEE Transactions on Automatic Control, 54(6):1254–1269, 2009.

- [8] H. M. Arnold. Stochastic parametrisation and model uncertainty. PhD thesis, University of Oxford, 2013.

- [9] Trevor T Ashley and Sean B Andersson. Method for simultaneous localization and parameter estimation in particle tracking experiments. Physical Review E, 92(5):052707, 2015.

- [10] A. Bain and D. Crisan. Fundamentals of Stochastic Filtering. Springer, 2008.

- [11] George EP Box, Mervin E Muller, et al. A note on the generation of random normal deviates. The annals of mathematical statistics, 29(2):610–611, 1958.

- [12] Paul Bratley and Bennett L Fox. Algorithm 659: Implementing sobol’s quasirandom sequence generator. ACM Transactions on Mathematical Software (TOMS), 14(1):88–100, 1988.

- [13] C. M. Carvalho, M. S. Johannes, H. F. Lopes, and N. G. Polson. Particle learning and smoothing. Statistical Science, 25(1):88–106, 2010.

- [14] Nicolas Chopin, Pierre E Jacob, and Omiros Papaspiliopoulos. SMC2: an efficient algorithm for sequential analysis of state space models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(3):397–426, 2013.

- [15] A. M. Clayton, A. Lorenc, and D. M. Barker. Operational implementation of a hybrid ensemble/4D-Var global data assimilation system at the Met Office. Quarterly Journal of the Royal Meteorological Society, 139(675):1445–1461, 2013.

- [16] D. Crisan and J. Miguez. Uniform convergence over time of a nested particle filtering scheme for recursive parameter estimation in state–space Markov models. Advances in Applied Probability, 49(4):1170–1200, 2017.

- [17] Dan Crisan, Joaquin Miguez, et al. Nested particle filters for online parameter estimation in discrete-time state-space markov models. Bernoulli, 24(4A):3039–3086, 2018.

- [18] D. P. Dee, S. M. Uppala, A. J. Simmons, P. Berrisford, P. Poli, S. Kobayashi, U. Andrae, M. A. Balmaseda, G. Balsamo, and P. Bauer. The ERA-interim reanalysis: Configuration and performance of the data assimilation system. Quarterly Journal of the royal meteorological society, 137(656):553–597, 2011.

- [19] P. Del Moral. Feynman-Kac Formulae: Genealogical and Interacting Particle Systems with Applications. Springer, 2004.

- [20] P. M. Djurić, M. F. Bugallo, and J. Míguez. Density assisted particle filters for state and parameter estimation. In Proceedings of the 29th IEEE ICASSP, May 2004.

- [21] P. M. Djurić and J. Míguez. Sequential particle filtering in the presence of additive Gaussian noise with unknown parameters. In Proceedings of ICASSP, May 2002.

- [22] A. Doucet, S. Godsill, and C. Andrieu. On sequential Monte Carlo Sampling methods for Bayesian filtering. Statistics and Computing, 10(3):197–208, 2000.

- [23] G. Evensen. The ensemble Kalman filter: Theoretical formulation and practical implementation. Ocean dynamics, 53(4):343–367, 2003.

- [24] G. Evensen. The ensemble Kalman filter for combined state and parameter estimation. IEEE Control Systems, 29(3), 2009.

- [25] Marco Frei and Hans R Künsch. Sequential state and observation noise covariance estimation using combined ensemble kalman and particle filters. Monthly Weather Review, 140(5):1476–1495, 2012.

- [26] Thomas C Gard. Introduction to stochastic differential equations. M. Dekker, 1988.

- [27] M. Gerber and N. Chopin. Sequential quasi Monte Carlo. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77(3):509–579, 2015.

- [28] A. Golightly and D. J. Wilkinson. Bayesian parameter inference for stochastic biochemical network models using particle Markov chain Monte Carlo. Interface Focus, 1(6):807–820, 2011.

- [29] N. Gordon, D. Salmond, and A. F. M. Smith. Novel approach to nonlinear and non-Gaussian Bayesian state estimation. IEE Proceedings-F, 140(2):107–113, 1993.

- [30] J. Hakkarainen, A. Ilin, A. Solonen, M. Laine, H. Haario, J. Tamminen, E. Oja, and H. Järvinen. On closure parameter estimation in chaotic systems. Nonlinear Proc. Geoph., 19(1):127–143, 2012.

- [31] John H Halton. Algorithm 247: Radical-inverse quasi-random point sequence. Communications of the ACM, 7(12):701–702, 1964.

- [32] Yoshito Hirata. Fast time-series prediction using high-dimensional data: Evaluating confidence interval credibility. Physical Review E, 89(5):052916, 2014.

- [33] Peter L Houtekamer and Herschel L Mitchell. A sequential ensemble kalman filter for atmospheric data assimilation. Monthly Weather Review, 129(1):123–137, 2001.

- [34] Shin-ichi Ito, Hiromichi Nagao, Akinori Yamanaka, Yuhki Tsukada, Toshiyuki Koyama, Masayuki Kano, and Junya Inoue. Data assimilation for massive autonomous systems based on a second-order adjoint method. Physical Review E, 94(4):043307, 2016.

- [35] S. J. Julier and J. Uhlmann. Unscented filtering and nonlinear estimation. Proceedings of the IEEE, 92(2):401–422, March 2004.

- [36] N. Kantas, A. Doucet, S. S. Singh, J. M. Maciejowski, and N. Chopin. On particle methods for parameter estimation in state-space models. Statistical Science, 30:328–351, August 2015.

- [37] G. Kitagawa. A self-organizing state-space model. Journal of the American Statistical Association, pages 1203–1215, 1998.

- [38] E. Koblents and J. Míguez. A population monte carlo scheme with transformed weights and its application to stochastic kinetic models. Statistics and Computing, 25(2):407–425, 2015.

- [39] P. J. Van Leeuwen. A variance-minimizing filter for large-scale applications. Monthly Weather Review, 131(9):2071–2084, 2003.

- [40] P. J. Van Leeuwen. Nonlinear data assimilation in geosciences: an extremely efficient particle filter. Quarterly Journal of the Royal Meteorological Society, 136(653):1991–1999, 2010.

- [41] Hong Li, Eugenia Kalnay, and Takemasa Miyoshi. Simultaneous estimation of covariance inflation and observation errors within an ensemble kalman filter. Quarterly Journal of the Royal Meteorological Society, 135(639):523–533, 2009.

- [42] J. Liu and M. West. Combined parameter and state estimation in simulation-based filtering. In A. Doucet, N. de Freitas, and N. Gordon, editors, Sequential Monte Carlo Methods in Practice, chapter 10, pages 197–223. Springer, 2001.

- [43] J. S. Liu and R. Chen. Sequential Monte Carlo methods for dynamic systems. Journal of the American Statistical Association, 93(443):1032–1044, September 1998.

- [44] Luca Martino, David Luengo, and Joaquín Míguez. Independent Random Sampling Methods. Springer, 2018.

- [45] J. Míguez, D. Crisan, and P. M. Djurić. On the convergence of two sequential Monte Carlo methods for maximum a posteriori sequence estimation and stochastic global optimization. Statistics and Computing, 23(1):91–107, 2013.

- [46] Bongki Moon, Hosagrahar V Jagadish, Christos Faloutsos, and Joel H. Saltz. Analysis of the clustering properties of the hilbert space-filling curve. IEEE Transactions on Knowledge and Data Engineering, 13(1):124–141, 2001.

- [47] Harald Niederreiter. Random number generation and quasi-Monte Carlo methods, volume 63. SIAM, 1992.

- [48] J. Olsson, O. Cappé, R. Douc, and E. Moulines. Sequential monte carlo smoothing with application to parameter estimation in nonlinear state space models. Bernoulli, 14(1):155–179, 2008.

- [49] Edward Ott, Brian R Hunt, Istvan Szunyogh, Aleksey V Zimin, Eric J Kostelich, Matteo Corazza, Eugenia Kalnay, DJ Patil, and James A Yorke. A local ensemble kalman filter for atmospheric data assimilation. Tellus A, 56(5):415–428, 2004.

- [50] A. Papavasiliou. A uniformly convergent adaptive particle filter. Journal of Applied Probability, 42(4):1053–1068, 2005.

- [51] A. Papavasiliou. Parameter estimation and asymptotic stability in stochastic filtering. Stochastic Processes and Their Applications, 116:1048–1065, 2006.

- [52] C. P. Robert and G. Casella. Monte Carlo Statistical Methods. Springer, 2004.

- [53] Naratip Santitissadeekorn and Christopher Jones. Two-stage filtering for joint state-parameter estimation. Monthly Weather Review, 143(6):2028–2042, 2015.

- [54] Naratip Santitissadeekorn and Christopher Jones. Two-stage filtering for joint state-parameter estimation. Monthly Weather Review, 143(6):2028–2042, 2015.

- [55] G. Storvik. Particle filters for state-space models with the presence of unknown static parameters. IEEE Transactions Signal Processing, 50(2):281–289, February 2002.

- [56] Vladislav B Tadic. Analyticity, convergence, and convergence rate of recursive maximum-likelihood estimation in hidden markov models. IEEE Transactions on Information Theory, 56(12):6406–6432, 2010.

- [57] Femke C Vossepoel and Peter Jan van Leeuwen. Parameter estimation using a particle method: Inferring mixing coefficients from sea level observations. Monthly weather review, 135(3):1006–1020, 2007.

- [58] Michail D Vrettas, Manfred Opper, and Dan Cornford. Variational mean-field algorithm for efficient inference in large systems of stochastic differential equations. Physical Review E, 91(1):012148, 2015.

- [59] Jingxin Ye, Daniel Rey, Nirag Kadakia, Michael Eldridge, Uriel I Morone, Paul Rozdeba, Henry DI Abarbanel, and John C Quinn. Systematic variational method for statistical nonlinear state and parameter estimation. Physical Review E, 92(5):052901, 2015.

- [60] Hongjuan Zhang, Harrie-Jan Hendricks-Franssen, Xujun Han, Jasper Vrugt, and Harry Vereecken. Joint state and parameter estimation of two land surface models using the ensemble kalman filter and particle filter. Hydrol. Earth Syst. Sci. Discuss, pages 1–39, 2016.