Multi-Chart Detection Procedure for Bayesian Quickest Change-Point Detection with Unknown Post-Change Parameters

Abstract

In this paper, the problem of quickly detecting an abrupt change on a stochastic process under Bayesian framework is considered. Different from the classic Bayesian quickest change-point detection problem, this paper considers the case where there is uncertainty about the post-change distribution. Specifically, the observer only knows that the post-change distribution belongs to a parametric distribution family but he does not know the true value of the post-change parameter. In this scenario, we propose two multi-chart detection procedures, termed as M-SR procedure and modified M-SR procedure respectively, and show that these two procedures are asymptotically optimal when the post-change parameter belongs to a finite set and are asymptotically optimal when the post-change parameter belongs to a compact set with finite measure. Both algorithms can be calculated efficiently as their detection statistics can be updated recursively. We then extend the study to consider the multi-source monitoring problem with unknown post-change parameters. When those monitored sources are mutually independent, we propose a window-based modified M-SR detection procedure and show that the proposed detection method is first-order asymptotically optimal when post-change parameters belong to finite sets. We show that both computation and space complexities of the proposed algorithm increase only linearly with respect to the number of sources.

I Introduction

To quickly detect the abrupt or the abnormal change in the observing sequence is of interest in wide range of practical applications. For example, in the cognitive radio system, the secondary user wants to quickly identify the time instant when the primary user accesses or releases the channel to maximize its throughput [2, 3, 4]. As another example, in seismic monitoring, it is crucial to quickly detect the abnormal signal caused by the earth crust movement. In such applications, to minimize the detection delay, which is the difference between the time when the abnormal change occurs and the time when the change is declared, is of interest. Quickest change-point detection (QCD) is a suitable mathematical framework for such applications. In particular, QCD aims to design online algorithms that can identify the abrupt change in the probabilistic distribution of a stochastic process as quickly and accurately as possible. QCD has two main classes of problem formulations: Bayesian formulation [5, 6] and non-Baysian formulation [7, 8]. For the classic Bayesian formulation, one sequentially observes a stochastic process with a random change-point . Before the change-point , the sequence are independent and identically distributed (i.i.d.) with probability density function (pdf) , and after , the sequence are i.i.d. with pdf . In the Bayesian formulation, the change-point is typically modeled as a geometrically distributed random variable. The goal is to find an optimal stopping time , at which we declare the change has happened, that minimizes the average detection delay subjected to a false alarm constraint. The Shiryaev-Robert (SR) procedure is known to be the optimal detection procedure for Bayesian QCD [6, 9]. In the non-Bayesian formulation, the change-point is assumed to be a fixed but unknown constant.

In the classic Bayesian QCD, it assumes that both the pre-change distribution and the post-change distribution are perfectly known by the observer. In most of practical applications, it is reasonable to assume that the pre-change distribution is known, as we typically know the behavior of the system in the normal state. However, one may not know the post-change distribution perfectly, as this represents the system in the abnormal states. Motivated by this fact, in this paper we extend the classic Bayesian QCD problem to the case with incomplete post-change information. In particular, we focus on the case that the post-change distribution belongs to a parametric distribution family, but the true post-change parameter, which belongs to a known compact set , is unknown to the observer. The goal of the observer is to design an effective online algorithm to quickly detect the change-point in the observation sequence for all possible post-change parameter in . In this scenario, we propose two low complexity multi-chart procedures for the purpose of quickest detection. In the first proposed detection algorithm, the observer divides into small disjoint subsets. By selecting one candidate point in each small subset, the observer constructs a finite set . Then, for each elements within , the observer runs a SR detection procedure; the observer declares that the change has occurred when any one of these procedures stops. We note that the observer runs multiple SR procedures simultaneously in each time slot, we term this algorithm as M-SR procedure. The second proposed algorithm is similar to the first one except that it replaces the summation operator within the SR statistic by the maximum operator; hence we term the second proposed multi-chart procedure as the modified M-SR procedure. For both proposed algorithms, we show that they are asymptotically optimal for the post-change parameters within and asymptotically optimal for all parameters within if is properly selected. The definition of asymptotic optimality will be given explicitly in the sequel. Loosely speaking, it indicates that the performance loss of the proposed algorithm is no larger than a small constant as the false alarm probability vanishes. We further point out that both proposed algorithms can be calculated recursively hence they are computationally efficient.

We then further extend the study to the multi-source monitoring problem under Bayesian QCD framework. In particular, the observer monitors mutually independent sources (except the change happens at the same time) and aims to detect the geometrically distributed change-point as quickly as possible. We consider the case that the distributions of all sources change simultaneously at but the post-change distribution of each source contains one unknown parameter. If we directly apply the M-SR or the modified M-SR procedure to the case of multi-variate unknown parameter, the computational complexity will increase exponentially w.r.t. . In this scenario, we propose a window-based modified M-SR procedure. We analyze the complexity and the performance of the proposed algorithm in detail, and show that the computational complexity of this proposed algorithm increases only linearly w.r.t. and the proposed algorithm is asymptotically optimal as the false alarm probability goes to zero.

The problem considered in this paper is related to recent works on the QCD problem that take the unknown post-change parameter into consideration. Due to limited space, we mention a few of them. For Bayesian setups, optimal solutions are likely to be obtained by converting proposed problems into Markovian optimal stopping problems. For example, [10] solves the Poisson disorder problem with unknown post-change arrival rate; [11] solves the Bayesian sequential change diagnosis problem, in which the observer aims not only to quickly detect the change but also to accurately identify the post-change parameter from a finite set; [12] solves a generalized formulation of the sequential change diagnosis problem for a Markov modulated sequence. For non-Bayeisan QCD setups, most of existing works propose modified versions of the CUSUM detection procedure, which is the optimal scheme for the classic non-Bayeisan QCD problem with known parameters [13], and discuss their robustness over the post-change uncertainty. For example, [7, 14, 15] replace the unknown likelihood ratio in the CUSUM statistic by the generalized likelihood ratio (GLR). [16] proposes the mixture-based CUSUM algorithm in which the CUSUM statistic is averaged over a prior distribution of the unknown parameter. [17] further shows the asymptotic optimality of the GLR-based CUSUM and the mixture-based CUSUM detection algorithms. [18] designs a composite stopping time that combines multiple CUSUM procedures to quickly detect the disorder time in the Wiener process with post-change uncertainty. [19] mentions the multi-chart CUSUM detection strategy. One may refer to a recent book [20] and references therein for more detailed results of this topic.

Different from aforementioned literatures, our work is formulated under Bayesian framework and focuses on the performance of low complexity multi-chart detection procedures instead of optimal schemes, which usually have high computational complexities. [21] has studied the asymptotic detection rules for Bayesian sequential diagnosis problem. Our paper focuses on the QCD problem and shows that the multi-chart version of the well-known SR procedure exhibits robustness over unknown parameters. The problem studied in this paper can be also viewed as a special case of the Markov chain tracking problem [22, 23, 24] with several absorbing states. However, those works focus on the optimal solution of generalized formulations while our work focus on the asymptotic optimal algorithms for the QCD problem.

There are also many recent works considering the QCD problem for multi-source monitoring. [25] is one of the most related works. Specifically, [25] considers the QCD problem in a distributed multi-sensor system when the post-change parameters are unknown. Authors also proposed to use multi-chart CUSUM to solve the proposed problem. In addition, [26] proposes the SUM algorithm, which is based on the sum of local CUSUMs, to quickly detect the abrupt change in multiple independent data streams. However, [26] only focuses on the case with known post-change distributions. Both [25] and [26] are formulated under non-Bayesian setting. We consider the multi-source monitoring problem under Bayesian QCD framework and discuss the performance and the implementation complexity of the proposed algorithm in detail.

This paper extends our previous conference publication [1] in several ways. Specifically, [1] only discusses the asymptotic optimality of the M-SR procedure when the post-change parameter belongs to a finite set. In addition to including the contributions made in [1], this paper also proposes the modified M-SR procedure, and studies the performance of both algorithms under a more general setting. Furthermore, we consider the multi-source monitoring problem and analyze the performance of our newly proposed algorithm.

The remainder of this paper is organized as follows. The mathematic model is given in Section II. Section III presents the proposed multi-chart detection algorithms and analyzes their asymptotic performances. Section IV discusses the multi-source monitoring problem and analyzes the performance of the proposed window-based modified M-SR procedure. Technical proofs in this paper are presented in Section V. Numerical examples are given in Section VI to illustrate the theoretic results obtained in this work. Finally, Section VII offers concluding remarks.

II Model

II-A Problem Formulation

We consider a random observation sequence whose distribution changes at an unknown time . In particular, observations obtained before the change-point , namely , are i.i.d. with pdf ; observations obtained after the change-point , namely , are i.i.d. with pdf .

In the classic QCD problem, both the pre-change distribution and the post-change distribution are perfectly known by the observer. In this paper, we consider the case that the observer only knows partial information of the post-change distribution. Specifically, we assume that the pre-change distribution is perfectly known to the observer; hence is a known parameter. However, the post-change distribution contains an unknown parameter . The observer knows that is taken from a compact set but he does not know the true value of . For notation convenience, in the rest of paper, is also denoted as , and is denoted as .

In this paper, we focus on the Bayesian QCD problem. In Bayesian framework, the change-point is modeled as a geometric random variable with known parameter , i.e., for ,

| (1) |

Observations ’s generate the filtration with

and contains the sample space .

To facilitate the presentation, we denote as the conditional probability measure of the observation sequence given . For a measurable event , we define probability measure as

We use and to denote the expectations with respect to probability measures and , respectively.

The observer aims to detect the change-point as quickly and accurately as possible. Let be a set of finite stopping times adapted to . A stopping time indicates the time instant that the observer stops taking observation and declares that the change has occurred. If the observer raises the alarm before the change-point occurs, i.e. , we call the observer makes a false alarm. On the other hand, if , we define as the detection delay. Hence, we use the following two performance metrics to evaluate a detection procedure :

In our setup, the observer aims to minimize the average detection delay (ADD) while keeping the probability of false alarm (PFA) under control regardless of the value of . In other words, the observer wants to solve the following optimization problem:

| (2) |

where is a constant to control the false alarm. We note that (2) aims to minimize ADD and to achieve a small probability of false alarm for all possible post-change parameters simultaneously. In general, it is difficult to find an optimal solution for the above multi-objective optimization problem. In this paper, we aim to design asymptotically optimal or sub-optimal detection algorithms.

II-B Other Related Formulations

We emphasize that, in our formulation stated in (2), the observer requires no prior distribution of . In some existing related literatures, such as [10, 18, 21], the prior distribution of the post-change parameter is assumed to be known by the observer. When the prior distribution of is available, in our context, it is natural to consider the problem formulation with averaged or weighted performance metrics.

Specifically, let be the prior distribution (or a subjective normalized weighting function) of , and

| (3) |

In this case, we can define an averaged PFA as

| (4) |

and define an averaged ADD as

| (5) |

Correspondingly, the observer may want to solve the following optimization problem

| (6) |

We note that the (asymptotically) optimal solution of Formulation (2) is also (asymptotically) optimal for Formulation (6). To see this fact, it is worth to notice that

This is because all observations are generated from on the event (when false alarm happens); hence the false alarm probability is independent of the post-change parameter . As a result, we have

| (7) |

Hence, if the worst case false alarm constraint in (2) is satisfied by detection procedure , the average false alarm constraint in (6) is also satisfied. Furthermore, for the objective function, we note that to minimize for all simultaneously in (2) is stronger than to minimize , the detection delay averaged over , in (5). Hence, Formulation (2) is more stringent than Formulation (6). As a result, the (asymptotically) optimal solution for Formulation (2) is also expected to have a good performance for Formulation (6).

III Multi-Chart Procedures and Their Sub-Optimality

It is well known that the SR procedure is the optimal detection procedure for classic Bayesian QCD problem. In this section, we propose two new detection algorithms, both of which are modified versions of the SR procedure, and analyze their performances.

III-A Multi-chart procedures

For the classic Bayesian QCD problem with pre-change distribution and post-change distribution , the SR procedure is known as

for a properly chosen threshold . For our formation, as the post-change distribution contains an unknown parameter, it is natural to consider replacing the likelihood ratio in the SR procedure with the generalized likelihood ratio. In our context, the GLR-based SR procedure can be written as

Though the GLR-based SR procedure is natural and attractive, it has several shortcomings. Theoretically, it is a challenging task to find the false alarm probability of . Practically, has large computational complexity as the observer needs to solve for the best at each time slot . The computational complexity depends on the specific form of and , which could lead to very challenging optimization problems.

In order to resolve these difficulties, we discretize the feasible set by selecting finitely many candidate points. Specifically, let be a discrete set with different elements, and . For , let

| (8) |

be the detection statistic, we propose the following detection procedure:

| (9) | |||

| (10) |

There are a few comments about the proposed algorithm. Firstly, the proposed algorithm can be viewed as a GLR-based SR detection procedure over the discrete set . As we use to approximate the post-change parameter set, then can be viewed as an approximation of . Secondly, the proposed algorithm is a multi-chart detection procedure. Specifically, in the proposed algorithm, the observer updates statistics , , in a parallel manner at each time slot, and each statistic is compared with its own threshold . The procedure stops when any one of statistics exceeds its corresponding threshold. As is the statistic used in the SR procedure, we term our proposed multi-chart procedure as M-SR procedure. Thirdly, we comment that can be calculated efficiently since can be updated recursively at each time slot. It is easy to see

| (11) |

Hence, the computational complexity of the proposed M-SR procedure is on the order of at each time slot.

Besides the M-SR procedure, we also propose the following modified M-SR procedure:

| (12) | |||

| (13) | |||

| (14) |

We note that the difference between and is that takes summation over to but takes the maximum. It is worth to notice that can also be updated recursively as

| (15) |

Hence, the computational complexity of the proposed modified M-SR procedure is also on the order of at each time slot.

In the rest of this section, we will analyze the performance of and for our proposed Formulation (2) under different assumptions on . Before our further analysis, we first present asymptotic lower bounds of ADDs for the post-change parameters in in the following theorem:

Theorem III.1.

(Lower Bounds) For all , as ,

| (16) |

where is the Kullback-Leibler (KL) divergence between and .

III-B M-SR procedure and posterior probabilities

The statistics in the M-SR procedure can be equivalently expressed in terms of posterior probabilities. Let be the discrete set for implementing the M-SR procedure. Define posterior probabilities as

| (17) |

We emphasize that (17) is defined on a probability measure given being the true post change parameter. By the definition of posterior probability, we have

| (18) |

in which

By direct calculations, it is easy to verify that

| (19) |

(19) reveals an insightful relationship between the M-SR procedure and the posterior probability of the change-point occurrence, it plays an important role in analyzing the false alarm probability of the proposed algorithm. Despite is an uncountable set in general, the proposed M-SR procedure only has finitely many statistics . Since each corresponds to a posterior probability by , it is possible to bound the false alarm probability for each . Then, the overall false alarm probability can be bounded by the union bound inequality. The detailed technical proof is presented in Lemma V.1 in the sequel.

III-C optimality of the proposed multi-chart procedures

Let with be the set for implementing the M-SR procedure and the modified M-SR procedure. Since is a finite set in general but is an uncountable infinite set, and constructed from will not be asymptotically optimal for all points in . To measure the loss of optimality, we define optimality as follows:

Definition III.2.

Let be a detection procedure that satisfies the false alarm constraint. is called (asymptotically) optimal if

| (20) |

for all .

The definition above resembles the idea of optimality for the case of non-Bayesian QCD problem, which is originally proposed in [27, Section 2.3.3]. In particular, given the true post-change parameter being , the numerator of (20) is the infimum of ADD for all qualified detection procedure; hence it presents the lower bound of the detection delay. The denominator of (20) is the ADD of a given detection procedure . As a result, is a measurement of detection efficiency or optimality loss; it is easy to see that and that is asymptotically optimal for post-change parameter when . We note that for a given detection procedure , the detection efficiency also depends on ; hence we call asymptotically optimal if (20) holds for all .

To study the asymptotic performance of and , we need to impose some additional assumptions on and . Specifically, for any given , we define the random variable

| (21) |

in which

| (22) |

and the supremum of an empty set is defined as . We note that when is the true post-change parameter, on the event , we have

| (23) |

Hence, we have almost surely under for all . We make additional assumptions that for any given , satisfies the condition

| (24) |

and

| (25) |

With these assumptions, we have the following conclusion for the M-SR procedure and the modified M-SR procedure:

Theorem III.3.

Proof.

Please see Section V-A. ∎

Remark III.4.

(24) and (25) are modifications of the well known assumptions “-quick convergence” and “average--quick convergence”[9], respectively, in the classic Bayesian QCD when . The “-quick convergence” was originally proposed in [28] and has been used in [29, 30] to show the asymptotic optimality of the sequential multi-hypothesis testing. The “average--quick convergence” was originally introduced in [9] to show asymptotic optimality of the SR procedure in the Bayesian QCD problem.

We discuss the conclusion obtained in Theorem III.3 in the following. First, we note that if the true post-change parameter belongs to , we have ; then the upper bound of ADD meets the lower bound, which indicates that and are asymptotically optimal for the parameters within . As a result, we have the following corollary:

Corollary III.5.

When is a finite set, by choosing and setting , and are first order asymptotically optimal as . In addition

| (26) | |||||

for all .

For the general case , by Theorem III.1 and Theorem III.3, we have

for any . Then, it is straightforward to see that and are asymptotically optimal if we properly select such that

| (27) |

In practice, can be designed offline by using (27) for the implementation of the M-SR procedure and the modified M-SR procedure. If satisfies certain properties, the design procedure could be further simplified. Let be a constant, it is easy to see that

is a stronger condition than (27). If is a Lipschitz continuous function w.r.t. , then we have

| (28) |

where is a real constant. (28) provides a simple method to design : the observer can first divide into a series of disjoint sub-intervals whose length is bounded by , and then constructs by picking one point in each sub-interval. However, we also point out that the cardinality of is in inverse proportion to , a larger will lead to more computation and longer detection delay. The asymptotic result in Theorem III.3 holds when is infinitely smaller than .

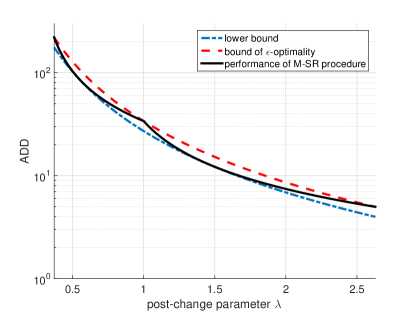

Example III.6.

Assume the pre-change distribution is , the post-change distribution is , and . For and , it is easy to verify that

| (29) |

When and , the observer can control the tolerant loss by setting , which is illustrated in Figure 1. Figure 1 shows that the performance of M-SR procedure (the black solid curve) lies within between the lower bound of ADD (the blue dot-dash line) and the bound of optimality (the red dash line). In addition, the performance of M-SR procedure meets the lower bound at and .

IV Extension: Multi-Source Monitoring Problem

In Section II and Section III, we focus on low complexity algorithms for solving the problem that an abrupt change happens on a single observation sequence. In this section, we extend our study to the multi-source monitoring problem. Particularly, in this section, we assume that there are mutually independent sources and that the observer is capable of monitoring all sources simultaneously; hence the observer obtains a dimensional random vector at each time slot. We denote the observation sequence as , in which is the observation obtained at time slot , and is the sample from the source at time slot . We note that is the source index and is the time index.

Similar to the model presented in Section II, the distribution of the observation sequence changes abruptly at the change-point . The prior distribution of is the same as (1). In this section, we further assume that the distributions of all sources change simultaneously at .

Pre-change distributions of the observed sources are perfectly known by the observer but the post-change distributions contain unknown parameters. For the source, let be the pre-change distribution, in which is a known parameter. Let be the post-change distribution, which contains an unknown parameter . Denote as the feasible set of . Throughout this section, is assumed to be a finite set that can be written as

hence . For the scenario that is an interval, the asymptotic optimality result obtained in Theorem IV.1 in the sequel can be easily generalized to the asymptotic optimality as we have done in Section III-C. Observations from the source are conditionally i.i.d. (conditioned on the change-point and the post-change parameter).

Therefore, the distribution of contains parameters. We denote these parameters in a vector form. Specifically, let be the parametric vector for pre-change distribution. As our assumption, is known by observer. Let , with , be the vector of post-change parameters, which is unknown to the observer. Denote

| (30) |

as the set of all possible post-change parameter vector. Obviously, ; hence for , we have and . We note that sub-index and have a one-to-one relationship, for example, one may set

Using these notations, the problem we aim to solve can be written as:

| (31) |

As a simple extension of the conclusions obtained in Section III, we know that

| (32) | |||

| (33) |

and

| (34) | |||

| (35) |

are asymptotically optimal if we choose . However, and have obvious drawbacks since they need to maintain many detection statistics at each time slot; hence both the computational complexity and the storage complexity increase exponentially w.r.t. ; these shortcomings limit the practical implementation of and when is large. In the rest of this section, we propose a window-based modified M-SR detection procedure, and show that the proposed algorithm is asymptotically optimal and has low computational complexity. In particular, the proposed algorithm can be written as

| (36) | |||

| (37) | |||

| (38) |

We note that the proposed procedure is the same as the modified M-SR procedure except that takes maximum over the latest likelihood ratios instead of all likelihood ratios. The asymptotic optimality of is presented in the following theorem:

Theorem IV.1.

By choosing such that

and setting threshold , then satisfies the false alarm constraint. In addition, as ,

| (39) |

in which

| (40) |

Proof.

Please see Section V-B. ∎

Remark IV.2.

Concise expressions (36) to (38) bring mathematical convenience in showing the asymptotic performance of . In the following, we rewrite the proposed algorithm into another equivalent form for the implementation purpose. We note that (38) can be equivalently written as

| (42) |

As indicated in Theorem IV.1, can be chosen as a constant over to guarantee the asymptotic optimality. In this case, we have

| (43) | |||||

By taking logarithm on both sides, we have

| (44) |

(43) or (44) indicates that the problem of searching best from elements can be decomposed into sub-problems, each of which only needs to find the best from elements. Hence the computational complexity substantially decrease from to . In the following, we discuss in detail about the implementation and the complexity of the above window-based modified M-SR algorithm.

For the proposed algorithm, the main computation lies on the term

| (45) |

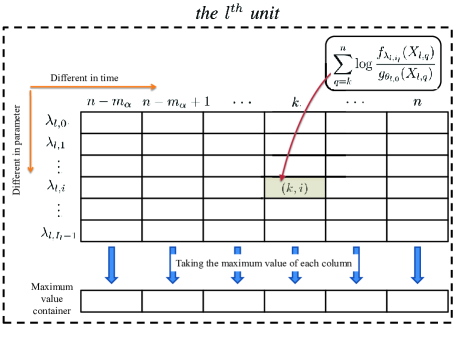

Note that we need to solve (45) for . These problems could be difficult to solve in general since is a discrete set and , could lead to a rather complex log-likelihood formula. To solve (45), the observer can maintain a structure, which is termed as a unit in this section, as illustrated in Figure 2. In particular, the unit, which corresponds to the source, requires two storage spaces: the first space is named as the LLR table with rows and columns. Specifically, the row, , and the column, , stores the value of . The second space with size is named as maximum value container, the cell of which stores the maximum value the column of the LLR table; hence the maximum value container stores the optimal value of (45) for .

The LLR table is updated at each time slot whenever there comes a new observation. Assume the observer newly receives , then he updates the LLR table by following steps: 1) selecting component in and computing the value of for all ; 2) erasing the values in the left-most column in the LLR table, shifting the rest of values one column to the left and then writing zeros in the right-most column; 3) adding to the row of the LLR table. This updating procedure simply uses the recursive relationship

of the statistic in (45). Once the LLR table has been updated, the maximum value container needs to be updated correspondingly. Based on above discussions, it is easy to see that the computational complexity of updating the unit is on the order of since both updating the LLR table and updating the maximum value container require computational amount.

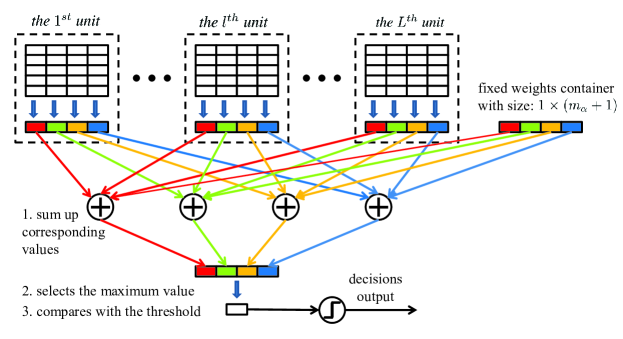

According to (44), Figure 3 illustrates a structure for the implementation of the proposed algorithm. Besides units for monitoring sources described above, we require another storage space with size to store the value of for . We term this space as the fixed weights container, which is illustrated in the upper-right corner in Figure 3. Noting that both the maximum value containers within the units and the fixed weights container have the same size, the detection statistic can be calculated by summing up the values in the cells with the same index and then selects the maximum of them. Finally, the decision rule can be made by comparing the value of with our pre-designed threshold.

Given the values in the maximum value containers within units, it is easy to see that the computational amount of calculating is on the order of . Hence, the main computational burden of implementing the whole algorithm is located in the updates of units, and the total computational amount is then on the order of . However, Figure 3 indicates that the calculation procedure can be speed up by updating units in a parallel manner. This is because the update of the unit only requires in , which is a consequence of the mutual independence between each two sources. The storage requirement, as the structure illustrated in Figure 3, can be easily found to be .

V Proof

V-A Proofs in Section III

In this subsection, we prove the main conclusion, Theorem III.3, in Section III. To proceed, we first present some supporting lemmas.

Lemma V.1.

By setting , the M-SR procedure defined in (10) satisfies the false alarm probability constraint, i.e.,

| (46) |

Proof.

We note that is the compact set of all possible post-change parameter and is the finite set to implement . From (19), we have

| (47) |

As a result setting , defined in (9) can be written as

| (48) | |||||

Hence

We note that

This is because all observations on the event are generated from , which is not related to the post-change parameter. As a result, we have

| (49) |

Using above argument again, we conclude

| (50) |

for all . As a result, we have . ∎

In the sequel, Lemma V.1 will be used in proving the false alarm probability of and , and the following Lemma will be used in bounding the detection delay. To proceed, we define some notations. Let

| (51) |

be the log likelihood ratio, and define a new statistic as

| (52) |

Furthermore, let

| (53) | |||

| (54) |

Then, we have the following lemma.

Proof.

On the event , we can decompose into two parts if :

| (56) |

When is the true post-change parameter, by the strong law of large numbers, we have

| (57) |

in which

By (56), can be written equivalently as

Hence,

| (58) |

Define the random variable

By (57), almost surely under probability measure . In addition, and by Assumption (24) and (25).

On the event , we have

hence

| (59) |

Then we have

Taking the conditional expectation on both sides, since and as , then we have

Therefore,

| (60) |

We note that and are finite. To see this,

where (a) is true because are generated by . Hence, we have

Since

we have

Therefore, is bounded. Since as , then

By (60) we obtain

| (61) |

Since the above equation holds for any , then

∎

Proof of Theorem III.3

Recall the definitions of in (8), in (12) and in (52), we have . Hence for the same threshold , we have , which further indicates . Therefore, it is sufficient for us to bound the false alarm probability of and to bound the average detection delay of .

Specifically, we set threshold . Then, for the false alarm probability, we have

| (62) |

in which the last inequality is because of Lemma V.1. Therefore, both and satisfies the false alarm constraint. Furthermore, for ADD

| (63) | |||||

in which the last inequality is because as and the conclusion obtained in Lemma V.2. Note that (63) holds for all , then we can choose a smallest upper bound as

That ends the proof.

V-B Proofs in Section IV

Proof of Theorem IV.1

We first show that satisfies the false alarm constraint. Recall (32), (34) and (36), we have by definition, therefore and . Following the similar argument presented in Lemma V.1, we can show that by choosing . Hence the false alarm constraint is satisfied.

We then analyze the detection delay. Recall that

By the strong law of large number, when is the true post-change parameter, on the event , we have

| (64) |

As a result, we have , such that

| (65) |

In the following, we set

in which , and is a small constant such that

| (66) |

for any . Recall that

Since , then it is sufficient to present an upper bound for the detection delay of . To this end, we use a technique that is similar to the one adopted in [17]. Let be the true post-change parameter. Then, for any given such that (66) is satisfied, when is small enough, we have

| (67) |

in which (a) is because of (66) for small enough; (b) is because are i.i.d. over and are independent of event ; (c) is because is the smallest integer ; (d) is an application of (65), noting that for a given , when is small enough. With (67), we have

| (68) |

As a result, we have

| (69) | |||||

Then the conclusion is achieved since the above equation holds for any given small .

VI Numerical Simulation

In this section, we provide some numerical examples to illustrate the theoretical results obtained in this paper.

In the first simulation, we illustrate the performance of the M-SR procedure and the modified M-SR procedure for Formulation (2). In this simulation, we set , and we assume that the pre-change distribution is and the post-change distribution is , where takes value in a close interval . We set the true post-change parameter is , but this value is unknown to the observer. To implement the proposed algorithms, the observer needs to select a discrete set . In the simulation, we select two different discrete sets, namely and , and compare the performances of the proposed algorithms on these two sets. The simulation result is shown in Figure 4. The black dot-dash line is the theoretical asymptotic lower bound calculated by (16). The red dash line with stars and the red solid line with squares are the performance of the modified M-SR procedure and that of the M-SR procedure w.r.t. , respectively. The blue dash line with diamonds and the blue solid line with circles are the performance of the M-SR procedure and that of the M-SR procedure w.r.t. , respectively. For both cases, the detection delay of the modified M-SR procedure is larger than that of the M-SR procedure. This is because is larger than as indicated by (8) and (12). However, the gap between the M-SR procedure and the modified M-SR procedure are relatively small w.r.t. the detection delay as . This verifies the result in Theorem III.3 that the M-SR procedure and the modified M-SR procedure have the same asymptotic performance. Furthermore, we note that the lines in blue are almost parallel to the asymptotic lower bound but the lines in red are not. This indicates that the algorithms based on are asymptotic optimal since the constant differences between the blue lines and the black dash line are negligible when the detection delay goes to infinity. For the same reason, the algorithms based on suffer performance loss. This phenomenon is also indicated by the result in Theorem III.3. Since one of the candidate points in is the true post-change parameter, we have , hence blue lines are asymptotically optimal.

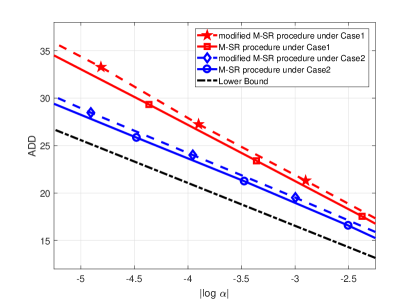

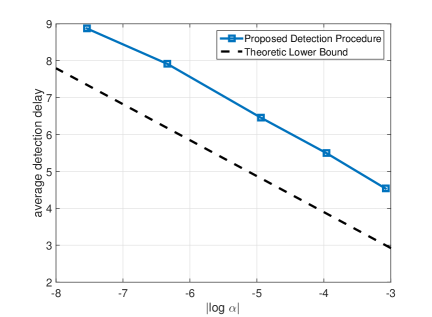

In the second simulation, we examine the asymptotic optimality of the proposed window-based modified M-SR procedure for the multi-source monitoring problem considered in Section IV. In this simulation, we consider three mutually independent sources. For all of these three sources, the pre-change distribution is and the post-change distribution is for . In the simulation, we set with for . However, the true post-change parameter for each source is different: particularly, , and . In addition, we set and the window length . The performance of the proposed window-based modified M-SR procedure is presented in Figure 5. The black dot line is the theoretical asymptotic lower bound calculated by (41) and the blue line with squares is the performances of the proposed algorithm. We can see that the blue line is parallel to the theoretical asymptotic lower bound, hence the proposed modified M-SR procedure is asymptotically optimal.

VII Conclusion

In this paper, we have considered the Bayesian QCD problem with unknown post-change parameters. In this case, we have proposed two low complexity multi-chart detection procedures, namely the M-SR procedure and the modified M-SR procedure, and have shown these two multi-chart detection procedures are asymptotically optimal when , the feasible set of the post-change parameter, is finite and asymptotically optimal when is an interval. We have also considered the multi-source monitoring problem with unknown post-change parameters. In this case, we have proposed a window-based modified M-SR detection procedure and have shown its asymptotic optimality. Both the computational complexity and storage requirement of the proposed algorithm have been shown to be on the order of .

References

- [1] J. Geng and L. Lai, “Bayesian quickest detection with unknown post-change parameter,” in Proc. IEEE Intl. Conf. on Acoustics, Speech, and Signal Processing, (Shanghai, China), Mar. 2016.

- [2] S. J. Kim and G. B. Giannakis, “Sequential and cooperative sensing for multichannel cognitive radios,” IEEE Trans. Signal Processing, vol. 58, pp. 4239–4253, Aug. 2010.

- [3] Q. Zou, S. Zheng, and A. H. Sayed, “Cooperative sensing via sequential detection,” IEEE Trans. Signal Processing, vol. 58, pp. 6266–6283, Dec. 2010.

- [4] L. Lai, Y. Fan, and H. V. Poor, “Quickest detection in cognitive radio: A sequential change detection framework,” in Proc. IEEE Global Telecommunications Conf., (New Orleans, Louisiana, USA), Nov. 2008.

- [5] A. N. Shiryaev, “The problem of the most rapid detection of a disturbance in a stationary process,” Soviet Math. Dokl., no. 2, pp. 795–799, 1961. (translation from Dokl. Akad. Nauk SSSR vol. 138, pp. 1039-1042, 1961).

- [6] A. N. Shiryaev, “On optimal methods in quickest detection problems,” Theory of Probability and Its Applications, vol. 8, pp. 22–46, 1963.

- [7] G. Lorden, “Procedures for reacting to a change in distribution,” Annals of Mathematical Statistics, vol. 42, no. 6, pp. 1897–1908, 1971.

- [8] M. Pollak, “Optimal detection of a change in distribution,” Annals of Statistics, vol. 13, pp. 206–227, Mar. 1985.

- [9] A. G. Tartakovsky and V. V. Veeravalli, “General asymptotic Bayesian theory of quickest change detection,” Theory of Probability and Its Applications, vol. 49, no. 3, pp. 458–497, 2005.

- [10] E. Bayraktar, S. Dayanik, and I. Karatzas, “Adaptive poisson disorder problem,” Annals of Applied Probability, vol. 16, pp. 1190–1261, 2006.

- [11] S. Dayanik, C. Goulding, and H. V. Poor, “Bayesian sequential change diagnosis,” Mathematics of Operations Research, vol. 33, no. 2, pp. 475–496, 2008.

- [12] S. Dayanik and C. Goulding, “Detection and identification of an unobservable change in the distribution of a Markov-modulated random sequence,” IEEE Trans. Inform. Theory, vol. 55, pp. 3323–3345, July 2009.

- [13] G. V. Moustakides, “Optimal stopping times for detecting changes in distribution,” Annals of Statistics, vol. 14, no. 4, pp. 1379–1387, 1986.

- [14] G. Lorden, “Open-ended tests for Koopman-Darmois families,” Annals of Statistics, vol. 1, no. 4, pp. 633–643, 1973.

- [15] T. L. Lai, “Sequential changepoint detection in quality control and dynamical systems,” Journal of the Royal Statistical Society, vol. 57, pp. 613–658, 1995.

- [16] M. Pollak, “Average run lengths of an optimal method of detecting a change in distribution,” Annals of Statistics, vol. 15, pp. 749–779, 1987.

- [17] T. L. Lai, “Information bounds and quickest detection of parameter changes in stochastic systems,” IEEE Trans. Inform. Theory, vol. 44, no. 7, pp. 2917–2929, 1998.

- [18] H. Yang, O. Hadjiliadis, and M. Ludkovski, “Detection and identification in the Wiener disorder problem with post-change drift uncertainty,” Stochastics, vol. 89, no. 3-4, pp. 654–685, 2017.

- [19] T. Banerjee and V. V. Veeravalli, “Data-efficient minimax quickest change detection with composite post-change distribution,” IEEE Trans. Inform. Theory, vol. 61, no. 9, pp. 5172–5184, 2015.

- [20] A. Tartakovsky, I. Nikiforov, and M. Basseville, Sequential Analysis: Hypothesis Testing and Changepoint Detection. New York: CRC Press, 2014.

- [21] S. Dayanik, W. B. Powell, and K. Yamazaki, “Asymptotically optimal Bayesian sequential change detection and identification rules,” Annals of Operations Research, vol. 208, no. 1, pp. 337–370, 2013.

- [22] E. Bayraktar and M. Ludkovski, “Sequential tracking of a hidden Markov chain using point process observations,” Stochastic Processes and their Applications, vol. 119, pp. 1792–1822, June 2009.

- [23] E. Bayraktar and S. Sezer, “Online change detection for a Poisson process with a phase-type change-time prior distribution,” Sequential Analysis: Design Methods and Application, vol. 28, pp. 218–250, 2009.

- [24] E. Bayraktar and M. Ludkovski, “Inventory management with partially observed non-stationary demand,” Annals of Operations Research, vol. 176, pp. 7–39, 2010.

- [25] A. G. Tartakovsky and A. S. Polunchenko, “Quickest changepoint detection in distributed multisensor systems under unknown parameters,” in Proc. Intl. Conf. on Information Fusion, (Cologne, Germany), pp. 878–885, Jul. 2008.

- [26] Y. Mei, “Efficient scalable schemes for monitoring a large number of data streams,” Biometrika, vol. 97, no. 2, pp. 419–433, 2010.

- [27] I. V. Nikiforov, “A simple change detection scheme,” Signal Processing, vol. 81, pp. 149–172, 2001.

- [28] T. L. Lai, “On -quick convergence and a conjecture of Strassen,” Annals of Probability, vol. 4, pp. 612–627, 1976.

- [29] A. G. Tartakovsky, “Asymptotic optimality of certain multihypothesis sequential tests: non-i.i.d. case,” Statistical Inference for Stochastic Processes, vol. 1, no. 3, pp. 265–295, 1998.

- [30] V. P. Dragalin, A. G. Tartakovsky, and V. V. Veeravalli, “Multihypothesis sequential probability ratio tests – Part I: Asymptotic optimality,” IEEE Trans. Inform. Theory, vol. 45, pp. 2448–2461, Nov. 1999.