Further Results on Size and Power of Heteroskedasticity and Autocorrelation Robust Tests, with an Application to Trend Testing††thanks: We thank the referees for helpful comments on a previous version of the paper. Financial support of the second author by the Danish National Research Foundation (Grant DNRF 78, CREATES) and by the Program of Concerted Research Actions (ARC) of the Université libre de Bruxelles is gratefully acknowledged. Address correspondence to Benedikt Pötscher, Department of Statistics, University of Vienna, A-1090 Oskar-Morgenstern Platz 1. E-Mail: benedikt.poetscher@univie.ac.at.

Second version: January 2018

Third version: April 2019)

Abstract

We complement the theory developed in Preinerstorfer and Pötscher (2016) with further finite sample results on size and power of heteroskedasticity and autocorrelation robust tests. These allow us, in particular, to show that the sufficient conditions for the existence of size-controlling critical values recently obtained in Pötscher and Preinerstorfer (2018) are often also necessary. We furthermore apply the results obtained to tests for hypotheses on deterministic trends in stationary time series regressions, and find that many tests currently used are strongly size-distorted.

1 Introduction

Heteroskedasticity and autocorrelation robust tests in regression models suggested in the literature (e.g., tests based on the covariance estimators in Newey and West (1987, 1994), Andrews (1991), and Andrews and Monahan (1992), or tests in Kiefer et al. (2000), Kiefer and Vogelsang (2002a, b, 2005)) often suffer from substantial size distortions or power deficiencies. This has been repeatedly documented in simulation studies, and has been explained analytically by the theory developed in Preinerstorfer and Pötscher (2016) to a large extent. Given a test for an affine restriction on the regression coefficient vector, the results in Preinerstorfer and Pötscher (2016) provide several sufficient conditions that imply size equal to one, or severe biasedness of the test (resulting in low power in certain regions of the alternative). The central object in that theory is the set of possible covariance matrices of the regression errors, i.e., the covariance model, and, in particular, its set of concentration spaces. Concentration spaces are defined as the column spaces of all singular matrices belonging to the boundary of the covariance model (cf. Definition 2.1 in Preinerstorfer and Pötscher (2016)). In Preinerstorfer and Pötscher (2016) it was shown that the position of the concentration spaces relative to the rejection region of the test often lets one deduce whether size distortions or power problems occur. Loosely speaking, if a concentration space lies in the “interior” of the rejection region, the test has size equal to one, whereas if a concentration space lies in the “exterior” (the “interior” of the complement) of the rejection region, the test is biased and has nuisance-minimal power equal to zero.111The situation is a bit more complex. For example, sometimes a modification of the rejection region, which leaves the rejection probabilities unchanged, is required in order to enforce the interiority (exteriority) condition; see Theorem 5.7 in Preinerstorfer and Pötscher (2016). These interiority (exteriority) conditions can be formulated in terms of test statistics and critical values, can be easily checked in practice, and have been made explicit in Preinerstorfer and Pötscher (2016) at different levels of generality concerning the test statistic and the covariance model (cf. their Corollary 5.17, Theorem 3.3, Theorem 3.12, Theorem 3.15, and Theorem 4.2 for more details).

Given a test statistic, the results of Preinerstorfer and Pötscher (2016) just mentioned – if applicable – all lead to implications of the following type: (i) size equals one for any choice of critical value (e.g., testing a zero restriction on the mean of a stationary AR(1) time series falls under this case); or (ii) all critical values smaller than a certain real number (depending on observable quantities only) lead to a test with size one. While implication (i) certainly rules out the existence of a size-controlling critical value, implication (ii) does not, because it only makes a statement about a certain range of critical values. Hence, the question when a size-controlling critical value actually exists has not sufficiently been answered in Preinerstorfer and Pötscher (2016). Focusing exclusively on size control, Pötscher and Preinerstorfer (2018) recently developed conditions under which size can be controlled at any level.222We note that, apart from the results mentioned before, Preinerstorfer and Pötscher (2016) also contains results that ensure size control (and positive infimal power). The scope of these results is, however, substantially more narrow than the scope of the results in Pötscher and Preinerstorfer (2018). It turns out that these conditions can, in general, not be formulated in terms of concentration spaces of the covariance model alone. Rather, they are conditions involving a different, but related, set , say, of linear spaces obtained from the covariance model. This set consists of nontrivial projections of concentration spaces as well as of spaces which might be regarded as “higher-order” concentration spaces (cf. Section 5 and Appendix B.1 of Pötscher and Preinerstorfer (2018) for a detailed discussion). Again, the conditions in Pötscher and Preinerstorfer (2018) do not depend on unobservable quantities, and hence can be checked by the practitioner. Pötscher and Preinerstorfer (2018) also provide algorithms for the computation of size-controlling critical values, which are implemented in the R-package acrt (Preinerstorfer (2016)).

Summarizing we arrive at the following situation: Preinerstorfer and Pötscher (2016) provide – inter alia – sufficient conditions for non-existence of size-controlling critical values in terms of the set of concentration spaces of a covariance model, whereas Pötscher and Preinerstorfer (2018) provide sufficient conditions for the existence of size-controlling critical values formulated in terms of a different set of linear spaces derived from the covariance model. Combining the results in Preinerstorfer and Pötscher (2016) and Pötscher and Preinerstorfer (2018) does in general not result in necessary and sufficient conditions for the existence of size-controlling critical values. [This is partly due to the fact that different sets of linear spaces associated with the covariance model are used in these two papers.] Rather, there remains a range of problems for which the existence of size-controlling critical values can be neither disproved by the results in Preinerstorfer and Pötscher (2016) nor proved by the results in Pötscher and Preinerstorfer (2018).

In the present paper we close the “gap” between the negative results in Preinerstorfer and Pötscher (2016) on the one hand, and the positive results in Pötscher and Preinerstorfer (2018) on the other hand. We achieve this by obtaining new negative results that are typically more general than the ones in Preinerstorfer and Pötscher (2016). Instead of directly working with concentration spaces of a given covariance model (as in Preinerstorfer and Pötscher (2016)) our main strategy is essentially as follows: We first show that size properties of (invariant) tests are preserved when passing from the given covariance model to a suitably constructed auxiliary covariance model which has the property that the concentration spaces of this auxiliary covariance model coincide with the set of linear spaces derived from the initial covariance model (as used in the results of Pötscher and Preinerstorfer (2018)). Then we apply results in Preinerstorfer and Pötscher (2016) to the concentration spaces of the auxiliary covariance model to obtain a necessary condition for the existence of size-controlling critical values. [This result is first formulated for arbitrary covariance models, and is then further specialized to the case of stationary autocorrelated errors.] The so-obtained new result now allows us to prove that the conditions developed in Pötscher and Preinerstorfer (2018) for the possibility of size control are not only sufficient, but are – under certain (weak) conditions on the test statistic – also necessary. Additionally, we also study power properties and provide conditions under which a critical value leading to size control will lead to low power in certain regions of the alternative; we also discuss conditions under which this is not so.

Obtaining results for the class of problems inaccessible by the results of Preinerstorfer and Pötscher (2016) and Pötscher and Preinerstorfer (2018) is not only theoretically satisfying. It is also practically important as this class contains empirically relevant testing problems: As a further contribution we thus apply our results to the important problem of testing hypotheses on polynomial or cyclical trends in stationary time series, the former being our main focus. Testing for trends certainly is an important problem (not only) in economics, and has received a great amount of attention in the literature. Using our new results we can prove that many tests currently in use (e.g., conventional tests based on long-run-variance estimators, or more specialized tests as suggested in Vogelsang (1998) and Bunzel and Vogelsang (2005)) suffer from severe size problems whenever the covariance model is not extremely small (that is, is large enough to contain all covariance matrices of stationary autoregressive processes of order two or a slight enlargement of that set, a weak condition that is satisfied by the covariance models used in Vogelsang (1998) or Bunzel and Vogelsang (2005); cf. also the last paragraph preceding Section 5.1.1). Furthermore, our results show that this problem can not be resolved by increasing the critical values used (as it is established that no size-controlling critical value exists).

The structure of the article is as follows: Section 2 introduces the framework and some notation. In Section 3 we present results concerning size properties of nonsphericity-corrected F-type tests. This is done on two levels of generality: In Subsection 3.1 we present results for general covariance models, whereas in Subsection 3.2 we present results for covariance models obtained from stationary autocorrelated errors. In these two sections it is also shown that the conditions for size control obtained in Theorems 3.2, 3.8, 6.5, 6.6 and in Corollary 5.6 of Pötscher and Preinerstorfer (2018) are not only sufficient but are also necessary in important scenarios. In Section 4 we present results concerning the power of tests based on size-controlling critical values. Finally, in Section 5 we discuss consequences of our results for testing restrictions on coefficients of polynomial and cyclical regressors. All proofs as well as some auxiliary results are given in the appendices.

2 Framework

2.1 The model and basic notation

Consider the linear regression model

| (1) |

where is a (real) nonstochastic regressor (design) matrix of dimension and where denotes the unknown regression parameter vector. We always assume and . We furthermore assume that the disturbance vector is normally distributed with mean zero and unknown covariance matrix , where varies in a prescribed (nonempty) set of symmetric and positive definite matrices and where holds ( always denoting the positive square root).333Since we are concerned with finite-sample results only, the elements of , , and (and even the probability space supporting and ) may depend on sample size , but this will not be expressed in the notation. Furthermore, the obvious dependence of on will also not be shown in the notation. The set will be referred to as the covariance model. We shall always assume that allows and to be uniquely determined from .444That is, has the property that implies for every . [This entails virtually no loss of generality and can always be achieved, e.g., by imposing some normalization assumption on the elements of such as normalizing the first diagonal element of or the norm of to one, etc.] The leading case will concern the situation where results from the assumption that the elements of the disturbance vector are distributed like consecutive elements of a zero mean weakly stationary Gaussian process with an unknown spectral density, but allowing for more general covariance models is useful.

The linear model described in (1) together with the Gaussianity assumption on induces a collection of distributions on the Borel-sets of , the sample space of . Denoting a Gaussian probability measure with mean and (possibly singular) covariance matrix by , the induced collection of distributions is then given by

| (2) |

Since every is positive definite by assumption, each element of the set in the previous display is absolutely continuous with respect to (w.r.t.) Lebesgue measure on .

We shall consider the problem of testing a linear (better: affine) hypothesis on the parameter vector , i.e., the problem of testing the null against the alternative , where is a matrix always of rank and . Set . Define the affine space

and let

Adopting these definitions, the above testing problem can then be written more precisely as

| (3) |

We also define as the linear space parallel to , i.e., for some . Obviously, does not depend on the choice of . The previously introduced concepts and notation will be used throughout the paper.

The assumption of Gaussianity is made mainly in order not to obscure the structure of the problem by technicalities. Substantial generalizations away from Gaussianity are possible exactly in the same way as the extensions discussed in Section 5.5 of Preinerstorfer and Pötscher (2016); see also Appendix E of Pötscher and Preinerstorfer (2018). The assumption of nonstochastic regressors can be relaxed somewhat: If is random and, e.g., independent of , the results of the paper apply after one conditions on . For arguments supporting conditional inference see, e.g., Robinson (1979).

We next collect some further terminology and notation used throughout the paper. A (nonrandomized) test is the indicator function of a Borel-set in , with called the corresponding rejection region. The size of such a test (rejection region) is the supremum over all rejection probabilities under the null hypothesis , i.e.,

Throughout the paper we let , where is the design matrix appearing in (1) and . The corresponding ordinary least squares (OLS) residual vector is denoted by . If it is clear from the context which design matrix is being used, we shall drop the subscript from and and shall simply write and . We use as a generic symbol for a probability measure. Lebesgue measure on the Borel-sets of will be denoted by , whereas Lebesgue measure on an affine subspace of (but viewed as a measure on the Borel-sets of ) will be denoted by , with zero-dimensional Lebesgue measure being interpreted as point mass. The set of real matrices of dimension is denoted by (all matrices in the paper will be real matrices). Let denote the transpose of a matrix and let denote the subspace in spanned by its columns. For a symmetric and nonnegative definite matrix we denote the unique symmetric and nonnegative definite square root by . For a linear subspace of we let denote its orthogonal complement and we let denote the orthogonal projection onto . For an affine subspace of we denote by the group of all affine transformations on of the form where and as well as belong to . [If is a linear space, consists precisely of all transformations of the form with and .] The -th standard basis vector in is written as . Furthermore, we let denote the set of all positive integers. A sum (product, respectively) over an empty index set is to be interpreted as (, respectively). Finally, for a subset of a topological space we denote by the closure of (w.r.t. the ambient space).

2.2 Classes of test statistics

The rejection regions we consider will be of the form , where the critical value satisfies and the test statistic is a Borel-measurable function from to . With the exception of Section 4, the results in the present paper will concern the class of nonsphericity-corrected F-type test statistics as defined in (28) of Section 5.4 in Preinerstorfer and Pötscher (2016) that satisfy Assumption 5 in that reference. For the convenience of the reader we recall the definition of this class of test statistics. We start with the following assumption, which is Assumption 5 in Preinerstorfer and Pötscher (2016):

Assumption 1.

(i) Suppose we have estimators and that are well-defined and continuous on , where is a closed -null set. Furthermore, is symmetric for every . (ii) The set is assumed to be invariant under the group , i.e., implies for every and every . (iii) The estimators satisfy the equivariance properties and for every , for every , and for every . (iv) is -almost everywhere nonsingular on .

Nonsphericity-corrected F-type test statistics are now of the form

| (4) |

where , , and satisfy Assumption 1 and where . We recall from Lemmata 5.15 and F.1 in Preinerstorfer and Pötscher (2016) that is then a closed -null set that is invariant under , and that is continuous on (and is obviously Borel-measurable on ). Furthermore, is -invariant, i.e., holds for every , every , every , and for every .

Remark 2.1.

(Important subclasses) (i) Classical autocorrelation robust test statistics (e.g., those considered in Newey and West (1987), Andrews (1991) Sections 3-5, or in Kiefer et al. (2000), Kiefer and Vogelsang (2002a, b, 2005)) fall into this class: More precisely, denoting such a test statistic by as in Pötscher and Preinerstorfer (2018), it follows that is a nonsphericity-corrected F-type test statistic with Assumption 1 above being satisfied, provided only Assumptions 1 and 2 of Pötscher and Preinerstorfer (2018) hold. Here is given by the ordinary least squares estimator , is given by defined in Section 3 of Pötscher and Preinerstorfer (2018), and holds (see Remark 5.17 in Pötscher and Preinerstorfer (2018)). Furthermore, is then nonnegative definite on all of (see Section 3.2 of Preinerstorfer and Pötscher (2016) or Section 3 of Pötscher and Preinerstorfer (2018)). We also recall from Section 5.3 of Pötscher and Preinerstorfer (2018) that in this case the set can be shown to be a finite union of proper linear subspaces of .

(ii) Classical autocorrelation robust test statistics like , but where the weights are now allowed to depend on the data (e.g., through data-driven bandwidth choice or through prewithening, etc.) as considered, e.g., in Andrews (1991), Andrews and Monahan (1992), and Newey and West (1994), also fall into the class of nonsphericity-corrected F-type tests under appropriate conditions (with the set now typically being nonempty), see Preinerstorfer (2017) for details. The same is typically true for test statistics based on parametric long-run variance estimators or test statistics based on feasible generalized least squares (cf. Section 3.3 of Preinerstorfer and Pötscher (2016)).

(iii) A statement completely analogous to (i) above applies to the more general class of test statistics discussed in Section 3.4B of Pötscher and Preinerstorfer (2018), provided Assumption 1 of Pötscher and Preinerstorfer (2018) is traded for the assumption that the weighting matrix appearing in the definition of is positive definite (and is of course now as discussed in Section 3.4B of Pötscher and Preinerstorfer (2018)); see Remark 5.17 in Pötscher and Preinerstorfer (2018). Again, is then nonnegative definite on all of (see Section 3.2.1 of Preinerstorfer and Pötscher (2016)), holds, and is a finite union of proper linear subspaces of (see Section 5.3 of Pötscher and Preinerstorfer (2018)).

(iv) The (weighted) Eicker-test statistic (cf. Eicker (1967)) as defined on pp.410-411 of Pötscher and Preinerstorfer (2018) is also a nonsphericity-corrected F-type test statistic with Assumption 1 above being satisfied, where , defined on p.411 of Pötscher and Preinerstorfer (2018), and holds. Again, is nonnegative definite on all of , and holds (see Sections 3 and 5.3 of Pötscher and Preinerstorfer (2018)). We note that the classical (i.e., uncorrected) F-test statistic also falls into this class as it coincides (up to a known constant) with in case is the identity matrix.

(v) Under the assumptions of Section 4 of Preinerstorfer and Pötscher (2016) (including Assumption 3 in that reference), usual heteroskedasticity-robust test statistics considered in the literature (see Long and Ervin (2000) for an overview) also fall into the class of nonsphericity-corrected F-type test statistics with Assumption 1 being satisfied. Again, the matrix is then nonnegative definite everywhere, holds, and is a finite union of proper linear subspaces of (the latter following from Lemma 4.1 in Preinerstorfer and Pötscher (2016) combined with Lemma 5.18 of Pötscher and Preinerstorfer (2018)).

We shall also encounter cases where may not be nonnegative definite for some values of . For these cases the following assumption, which is Assumption 7 in Preinerstorfer and Pötscher (2016), will turn out to be useful. For a discussion of this assumption see p. 314 of that reference.

Assumption 2.

For every with we have .

3 Results on the size of nonsphericity-corrected F-type test statistics

3.1 A result for general covariance models

In this subsection we start with a negative result concerning the size of a class of nonsphericity-corrected F-type test statistics that is central to many of the results in the present paper. In particular, it allows us to show that the sufficient conditions for size control obtained in Pötscher and Preinerstorfer (2018) are often also necessary. The result complements negative results in Preinerstorfer and Pötscher (2016) and is obtained by combining Lemmata A.1 and A.3 in Appendix A with Corollary 5.17 of Preinerstorfer and Pötscher (2016). Its relationship to negative results in Preinerstorfer and Pötscher (2016) is further discussed in Appendix A.1. We recall the following definition from Pötscher and Preinerstorfer (2018).

Definition 3.1.

Given a linear subspace of with and a covariance model , we let , where . Furthermore, we define

where the closure is here understood w.r.t. . [The symbol here denotes a norm on . Note that does not depend on which norm is chosen.]

The space figuring in this definition will always be an appropriately chosen subspace related to invariance properties of the tests under consideration. A leading case is when . Loosely speaking, the linear spaces belonging to are either (nontrivial) projections of concentration spaces of the covariance model (in the sense of Preinerstorfer and Pötscher (2016)) on , or are what one could call “higher-order” concentration spaces. For a more detailed discussion see Appendix B.1 of Pötscher and Preinerstorfer (2018).

Theorem 3.1.

Remark 3.2.

(Extensions) (i) As noted in Section 2.2, any as in the theorem is -invariant. In some cases and its associated set are additionally invariant w.r.t. addition of elements from a linear space . In such a case necessarily has dimension less than , and the variant of Theorem 3.1 where is replaced by also holds.555That must hold is seen as follows: Suppose . Then is -almost everywhere constant (this is trivial if and follows from Remark 5.14(i) in Pötscher and Preinerstorfer (2018) in case ). However, this contradicts Part 2 of Lemma 5.16 of Pötscher and Preinerstorfer (2018).

The preceding theorem can now be used to show that the conditions for size control obtained in Corollary 5.6 (and Remark 5.8) of Pötscher and Preinerstorfer (2018) are not only sufficient, but are actually necessary, in some important scenarios. This is formulated in the subsequent corollary; see also Remark 3.4 below. [We note that in this corollary satisfies the assumptions of Corollary 5.6 of Pötscher and Preinerstorfer (2018) (with and ) in view of Lemma 5.16 in the same reference.]

Corollary 3.3.

Let be a covariance model. Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1 with . Furthermore, assume that is nonnegative definite for every , and that . Then for every is necessary and sufficient for size-controllability (at any significance level ), i.e., is necessary and sufficient for the fact that for every there exists a real number such that

| (6) |

holds.666For conditions under which a smallest size-controlling critical value exists and when equality can be achieved in (6) see Pötscher and Preinerstorfer (2018), Section 5.2.

Remark 3.4.

(Special cases) (i) Corollary 3.3 applies, in particular, to the (weighted) Eicker-test statistic in view of Remark 2.1(iv) above. Note that is here always satisfied. By Remark 2.1(iv), Corollary 3.3 also applies to the classical F-test statistic.

(ii) Next consider the classical autocorrelation robust test statistic with Assumptions 1 and 2 of Pötscher and Preinerstorfer (2018) being satisfied. Then Corollary 3.3 also applies to in view of Remark 2.1(i) above, provided holds. While the relation need not always hold for (see the discussion in Section 5.3 of Pötscher and Preinerstorfer (2018)), it holds for many combinations of restriction matrix and design matrix (in fact, it holds generically in many universes of design matrices as a consequence of Lemma A.3 in Appendix A of Pötscher and Preinerstorfer (2018)). Hence, for such combinations of and , Corollary 3.3 applies to .

Remark 3.5.

While Theorem 3.1 applies to any combination of test statistic and covariance model as long as they satisfy the assumptions of the theorem, in a typical application the choice of the test statistic used will certainly be dictated by properties of the covariance model one maintains. For example, in case models stationary autocorrelated errors different test statistics will be employed than in the case where models heteroskedasticity.

3.2 Results for covariance models obtained from stationary autocorrelated errors

We next specialize the results of the preceding section to the case of stationary autocorrelated errors. i.e., to the case where the elements of the disturbance vector in model (1) are distributed like consecutive elements of a zero mean weakly stationary Gaussian process with an unknown spectral density, which is not almost everywhere equal to zero. Consequently, the covariance matrix of the disturbance vector is positive definite and can be written as where

with varying in , a prescribed (nonempty) family of normalized (i.e., ) spectral densities, and where holds. Here denotes the imaginary unit. We define the associated covariance model via . Examples for the set are (i) , the set of all normalized spectral densities, or (ii) , the set of all normalized spectral densities corresponding to stationary autoregressive moving average models of order at most , or (iii) the set of normalized spectral densities corresponding to (stationary) fractional autoregressive moving average models, etc. We shall write for .

We need to recall some more concepts and notation from Pötscher and Preinerstorfer (2018); for background see this reference. Let and let be an integer. Define as the -dimensional matrix with -th row equal to . Given a linear subspace of with , define for every

| (7) |

As discussed in Section 3.1 of Pötscher and Preinerstorfer (2018), the set on the r.h.s. of (7) is nonempty for every . Thus is well-defined and takes values in . Furthermore, holds at most for finitely many as shown in the same reference. We now define as the vector obtained by ordering the elements of from smallest to largest, provided this set is nonempty, and we denote by the dimension of this vector; furthermore, we set for every , where denotes the -the coordinate of , and we write for the vector with -th coordinate equal to . If the set is empty, we take as well as as the -tuple and set . As in Pötscher and Preinerstorfer (2018), for a natural number we define for and for . Furthermore, we set where the sum extends over , with the convention that this sum is zero if . For ease of notation we shall often simply write for .

The subsequent theorem specializes Theorem 3.1 to the case where . For a definition of the collection of certain subsets of figuring in this theorem see Definition 6.4 of Pötscher and Preinerstorfer (2018).

Theorem 3.6.

Let be a nonempty set of normalized spectral densities, i.e., . Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1 with . Furthermore, assume that is nonnegative definite for every . Suppose there exists a linear subspace of that can be written as

| (8) |

where the ’s denote the elements of and , such that satisfies (or, equivalently, ). Then holds. Furthermore,

holds for every critical value , , for every , and for every .

Remark 3.7.

This theorem is applicable to any nonempty set of normalized spectral densities. In case more is known about the richness of , the sufficient condition in the preceding result can sometimes be simplified substantially. Below we present such a result making use of the subsequent lemma.

Lemma 3.8.

Let satisfy and let be a linear subspace of with . Let . Then if and only if . And holds for every if and only if . Furthermore, if and only if .

Remark 3.9.

(i) A sufficient condition for (, respectively) is given by (, respectively). This follows from established in Lemma D.1 in Appendix D of Pötscher and Preinerstorfer (2018).

(ii) In the case the latter two conditions become and , respectively. Note that the condition is always satisfied for or (as then ). For this condition coincides with , and is always satisfied except if and .

Armed with the preceding lemma we can now establish the following consequence of Theorem 3.6 provided is rich enough to encompass , which clearly is a very weak condition in the context of autocorrelation robust testing.777Recall that a premise of autocorrelation robust testing is agnosticism about the correlation structure of the error process.

Theorem 3.10.

Let satisfy . Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1 with . Furthermore, assume that is nonnegative definite for every . Suppose there exists a such that . Then holds, and we have

| (9) |

for every critical value , , for every , and for every .

Remark 3.11.

(Further comments on the necessity of the sufficient conditions for size control in Pötscher and Preinerstorfer (2018)) (i) Suppose is as in Theorem 3.6, additionally satisfying . Theorem 3.6 then shows that the sufficient conditions for size control given in Part 1 of Theorem 6.5 in Pötscher and Preinerstorfer (2018) (or the equivalent formulation given in Part 2 of that theorem) is also necessary.

(ii) Suppose is as in (i) and assume furthermore that is as in Remark 3.7. Then also the sufficient condition for size control “ for every ” mentioned in Part 2 of Theorem 6.5 of Pötscher and Preinerstorfer (2018) is necessary. [This is seen as follows: Suppose not, i.e., holds for some . Now apply Theorem 3.6 with , which is possible because of Remark 3.7, resulting in size being equal to one, a contradiction.]

(iii) Suppose is as in (i) and assume that satisfies . Then satisfies the property in Remark 3.7 in view of Lemma 3.8, and thus (ii) above applies. In this situation even more is true in view of Theorem 3.10: The further sufficient condition for size control “ for every ” given in Part 2 of Theorem 6.5 of Pötscher and Preinerstorfer (2018) is in fact also necessary.

(iv) The discussion in (i)-(iii) covers (weighted) Eicker-test statistics (including the classical F-test statistic) as well as classical autocorrelation robust test statistics (the latter under Assumptions 1 and 2 of Pötscher and Preinerstorfer (2018) and if holds); it also covers the test statistics (provided the weighting matrix is positive definite and holds). In particular, the discussion in (i)-(iii) thus applies to the sufficient conditions given in Theorem 6.6 in Pötscher and Preinerstorfer (2018) and its variants outlined in Remark 6.8 of that reference. Furthermore, it transpires from this discussion that the sufficient conditions for size control provided in Theorem 3.8 of Pötscher and Preinerstorfer (2018) are actually necessary; and the same is true for Theorem 3.2 in that reference (provided the set given there coincides with ).888Note that in those two theorems.

The results so far have only concerned the size of nonsphericity-corrected F-type test statistics for which the exceptional set is empty and is nonnegative definite everywhere. We now provide a result also for the case where this condition is not met.999Theorem A.4 in Appendix A also allows for , but requires to be nonnegative definite for every (implying that is nonnegative definite -a.e.). This result also contains further assumptions such as .

Definition 3.2.

Let denote the set of all normalized spectral densities of the form with and , , .

Obviously, holds. While the preceding result maintained that contains , the next result maintains the slightly stronger condition that .

Theorem 3.12.

Let satisfy . Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1. Furthermore, assume that also satisfies Assumption 2. Suppose there exists a such that . Then for every critical value , , for every , and for every it holds that

| (10) |

where is defined by

with the random variable given by

on the event where and by otherwise. Here is a standard normal -vector, if and denotes the first column of otherwise. [Recall that .]

The significance of the preceding theorem is that it provides a lower bound for the size of a large class of nonsphericity-corrected F-type tests, including those with or with not necessarily nonnegative definite. In particular, it shows that size can not be controlled at a given desired significance level , if is below the threshold given by the lower bound in (10). Observe that this threshold will typically be close to , at least if is sufficiently large, since (possibly after rescaling) will often approach a positive definite matrix as .

Remark 3.13.

(i) There are at most finitely many satisfying the assumption in the preceding theorem. To see this note that any such must coincide with a coordinate of (since trivially in case by this assumption, and since in case ), and that the dimension of the vector is finite since can hold at most for finitely many ’s as discussed subsequent to (7).

(ii) If denotes the (finite) set of ’s satisfying the assumption in the theorem, relation (10) in fact implies

Remark 3.14.

Remark 3.15.

Some results in this section are formulated for sets of spectral densities satisfying or , and thus for covariance models satisfying or , respectively. Trivially, these results also hold for any covariance model (not necessarily of the form ) that satisfies or , respectively. This observation also applies to other results in this paper further below and will not be repeated.

4 Results concerning power

We now show for a large class of test statistics, even larger than the class of nonsphericity-corrected F-type test statistics, that – under certain conditions – a choice of critical value leading to size less than one necessarily implies that the test is severely biased and thus has bad power properties in certain regions of the alternative hypothesis (cf. Part 3 of Theorem 5.7 and Remark 5.5(iii) in Preinerstorfer and Pötscher (2016)). The relevant conditions essentially say that a collection as in the subsequent lemma can be found that is nonempty. It should be noted, however, that there are important instances where (i) the relevant conditions are not satisfied (that is, a nonempty satisfying the properties required in the lemma does not exist) and (ii) small size and good power properties coexist. For results in that direction see Theorems 3.7, 5.10, 5.12, and 5.21 in Preinerstorfer and Pötscher (2016) as well as Proposition 5.2 and Theorem 5.4 in Preinerstorfer (2017).

The subsequent lemma is a variant of Lemma 5.11 in Pötscher and Preinerstorfer (2018). Recall that , defined in that lemma, certainly contains all one-dimensional (provided such elements exist).

Lemma 4.1.

Let be a covariance model. Assume that the test statistic is Borel-measurable and is continuous on the complement of a closed set . Assume that and are -invariant, and are also invariant w.r.t. addition of elements of a linear subspace of . Define and assume that . Let and be defined as in Lemma 5.11 of Pötscher and Preinerstorfer (2018). Let be a subset of and define and , with the convention that and if is empty. Suppose that has the property that for every the set is a -null set for some (and hence for all . Then the following holds:

-

1.

For every , every , and every we have

-

2.

For every , every , and every we have

Part 1 of the lemma implies that the size of the test equals if . Part 2 shows that the test is severely biased for , which – in view of the invariance properties of (cf. Part 3 of Theorem 5.7 and Remark 5.5(iii) in Preinerstorfer and Pötscher (2016)) – implies bad power properties such as (13) and (14) below. In particular, Part 2 implies that infimal power is zero for such choices of . [Needless to say, the lemma neither implies that is less than for nor that is positive for . For conditions implying that size is less than for appropriate choices of see Pötscher and Preinerstorfer (2018).] The computation of the constants and can sometimes be simplified, see Lemma C.1 in Appendix C. Before proceeding, we want to note that the preceding lemma also provides a negative size result (namely that the test based on has size equal to for every ), if holds for a collection satisfying the assumptions of that lemma.

The announced theorem is now as follows and builds on the preceding lemma.

Theorem 4.2.

Let be a covariance model. Assume that the test statistic is Borel-measurable and is continuous on the complement of a closed set . Assume that and are -invariant, and are also invariant w.r.t. addition of elements of a linear subspace of . Define and assume that . Then the following hold:

-

1.

Suppose there exist two elements and of such that . Suppose further that for the set is a -null set for some (and hence for all . Then for any critical value , , satisfying101010Because of -invariance (cf. Remark 5.5(iii) in Preinerstorfer and Pötscher (2016)), the left-hand side of (11) coincides with for any and any Similarly, the left-hand side of (12) coincides with for any and any

(11) we have

(12) - 2.

- 3.

In the important special case where , the assumptions on and the associated set in the second and third sentence of the preceding theorem are satisfied, e.g., for nonsphericity-corrected F-type test statistics (under Assumption 1), including the test statistics , , and given in Section 2.2 above; see also Section 5.3 in Pötscher and Preinerstorfer (2018). Furthermore, for the class of test statistics such that Theorem 3.1 applies (and for which holds), it can be shown that is a -null set for any (in fact, for any ) provided (11) holds. These observations lead to the following corollary.

Corollary 4.3.

Let be a covariance model and let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1 with . Furthermore, assume that is nonnegative definite for every and that .

- 1.

- 2.

Theorem 4.2 as well as the preceding corollary maintain conditions that, in particular, require to be nonempty. In view of Lemma 5.11 in Pötscher and Preinerstorfer (2018), is certainly nonempty if a one-dimensional exists. The following lemma shows that for with this is indeed the case; in fact, for such typically at least two such spaces exist.111111While the one-dimensional spaces given in the lemma typically will be different, it is not established in the lemma that this is necessarily always the case.

Lemma 4.4.

Let satisfy . Let be a linear subspace of satisfying . Then, for , belongs to and is one-dimensional.

The preceding lemma continues to hold for any covariance model in a trivial way, since then certainly holds. Also note that the condition is always satisfied in the important special case where , since .

5 Consequences for testing hypotheses on deterministic trends

In this section we discuss important consequences of the results obtained so far for testing restrictions on coefficients of polynomial and cyclical regressors when the errors are stationary, more precisely, have a covariance model of the form . Such testing problems have, for obvious reasons, received a great deal of attention in econometrics, and are relevant in many other fields such as, e.g., climate or ecological research.121212See, e.g., Bence (1995), who finds substantial undercoverage of confidence intervals derived from several tests corrected for autocorrelation. In particular, we show that a large class of nonsphericity-corrected F-type test statistics leads to unsatisfactory test procedures in this context. In Subsection 5.1 we present results concerning hypotheses on the coefficients of polynomial regressors. Results concerning tests for hypotheses on the coefficients of cyclical regressors are briefly discussed in Subsection 5.2.

5.1 Polynomial regressors

We consider here the case where one tests hypotheses that involve the coefficient of a polynomial regressor as expressed in the subsequent assumption:

Assumption 3.

Suppose that , where is an -dimensional matrix ), the -th column being given by , and where is an -dimensional matrix such that has rank (here is the empty matrix if ). Furthermore, suppose that the restriction matrix has a nonzero column for some , i.e., the hypothesis involves coefficients of the polynomial trend.

Under this assumption one obtains the subsequent theorem as a consequence of Theorem 3.10.

Theorem 5.1.

The previous theorem relies in particular on the assumption that and that is nonnegative definite everywhere. While these two assumptions may appear fairly natural and are widely satisfied, e.g., for the test statistics , , and as discussed in Remark 2.1, we shall see in Subsections 5.1.1 and 5.1.2 below that they are not satisfied by some tests suggested in the literature. To obtain results also for tests that are not covered by the previous theorem we can apply Theorem 3.12. The following result is then obtained.

Theorem 5.2.

Let satisfy . Suppose that Assumption 3 holds. Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1. Furthermore, assume that also satisfies Assumption 2. Then for every critical value , , for every , and for every it holds that

| (15) |

where denotes the first nonzero column of . [Note that is -almost everywhere nonsingular in view of Assumption 1.]

Theorem 5.2 shows that under Assumption 3 a large class of nonsphericity-corrected F-type tests, including cases with or with but where is not necessarily nonnegative definite everywhere, typically have large size. In particular, size can not be controlled at a given desired significance level , if is below the lower bound in (15). Observe that this lower bound will typically be close to , at least if is sufficiently large.

Remark 5.3.

(i) In the special case where Assumption 3 is satisfied with , Theorem 5.1 continues to hold even under the weaker assumption that only holds.131313In fact, it holds more generally for any covariance model that has as a concentration space in the sense of Preinerstorfer and Pötscher (2016). This follows from Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016) upon noting that is a concentration space of by Lemma G.1 in the same reference, that vanishes on as a consequence of the assumption (see the discussion following (27) in Preinerstorfer and Pötscher (2016)), and that for all .141414To see that , note that is of the form with , since is the first column of . The equivariance property of in Assumption 1 gives as well as for every . This implies , and hence . Here denotes the vector of ones.

(ii) In the special case where Assumption 3 is satisfied with , also Theorem 5.2 continues to hold under the weaker assumption that holds, provided the identity matrix appearing in (15) is replaced by the nonsingular matrix , where is the matrix given in Part 3 of Lemma G.1 in Preinerstorfer and Pötscher (2016). This follows from Remark 5.14(iii) further below, upon noting that the situation considered here can be viewed as a special case of the situation described in Remark 5.14(iii) with .

To illustrate the scope and applicability of Theorems 5.1 and 5.2 above (beyond the test statistics such as , , and mentioned before), we shall now apply them to some commonly used test statistics that have been designed for testing polynomial trends. First, in Subsection 5.1.1, we shall derive properties of conventional tests for polynomial trends. Such tests are based on long-run-variance estimators and classical results due to Grenander (1954). In Subsection 5.1.2 we shall discuss properties of tests that have been introduced more recently by Vogelsang (1998) and Bunzel and Vogelsang (2005). While our discussion of methods is certainly not exhaustive (for example, we do not discuss tests in Harvey et al. (2007) or Perron and Yabu (2009), which have been suggested only for the special case of testing a restriction on the slope in a “linear trend plus noise model”), it should also serve the purpose of presenting a general pattern how one can check the reliability of polynomial trend tests. It might also help to avoid pitfalls in the construction of novel tests for polynomial trends.

Before we proceed to a discussion of properties of specific tests, we would like to emphasize the following: in the present section we provide, for some commonly used tests, results on their maximal rejection probability over

for every and every . We establish these results under the weak assumption that contains at least or the slight enlargement . The recent trend testing literature, cf. in particular Section 3.1 in Vogelsang (1998) and Assumption 1 in Bunzel and Vogelsang (2005), studies tests for models induced by all regression errors satisfying

Here is an additional unknown parameter and is a weakly stationary linear process with martingale difference innovations that have uniformly bounded fourth moments and conditional variance , and with coefficients for satisfying and the summability condition . Also the coefficients are unknown parameters. Obviously, the assumptions on the innovations are satisfied for an i.i.d. sequence of standard normal random variables. Hence, setting in the previous displayed equation, we see that the model considered in Vogelsang (1998) or Bunzel and Vogelsang (2005) contains, in particular,

As a consequence, any lower bound for size obtained in our context for sets required only to satisfy (or ) a fortiori provides a lower bound for the size in the setting considered in Vogelsang (1998) and Bunzel and Vogelsang (2005) (since ).

5.1.1 Properties of conventional tests for hypotheses on polynomial trends

The structure of tests that have traditionally been used for testing restrictions on coefficients of polynomial trends (i.e., when the design matrix satisfies Assumption 3, and in particular if ) is motivated by results concerning the asymptotic covariance matrix of the OLS estimator (and its efficiency) in regression models with stationary error processes and deterministic polynomial time trends by Grenander (1954) (cf. also the discussion in Bunzel and Vogelsang (2005) on p. 383). The corresponding test statistics are nonsphericity-corrected F-type test statistics as in (4). They are based on the OLS estimator and a covariance matrix estimator

| (16) |

Here the “long-run-variance estimator” is of the form

| (17) |

where is a symmetric, possibly data-dependent, -dimensional matrix that may not be well-defined on all of .151515The matrix may depend on , a dependence not shown in the notation. Furthermore, assuming symmetry of entails no loss of generality, since given a long-run-variance-estimator as in (17) and based on a non-symmetric weights matrix , one can always pass to an equivalent long-run-variance estimator by replacing with the symmetric matrix . In many cases, however, is constant, i.e., does not depend on , and is also positive definite. For example, this is so in the leading case where the -th element of is of the form for some (deterministic) (typically depending on ) and a kernel function such as the Bartlett, Parzen, Quadratic-Spectral, or Daniell kernel (positive definiteness does not hold, e.g., for the rectangular kernel with ). Note that in case is given by a kernel the estimator in the previous display can be written in the more familiar form

where for . For trend tests based on the OLS estimator and a covariance estimator as in (16) we shall first obtain two corollaries from Theorems 5.1 and 5.2 that cover the case where is constant.161616The slightly more general case, where is not constant in (and is defined on all of ) but is so, can immediately be subsumed under the present discussion, if one observes that coincides with and is constant. Further below we shall then address the case where is allowed to depend on . Note that the assumptions on in the subsequent corollary are certainly met if is constant, symmetric, and positive definite, and hence are satisfied in the leading case mentioned before (provided is deterministic).

Corollary 5.4.

We next consider the case where the matrix is nonzero, but not (necessarily) nonnegative definite, and thus the previous corollary is not applicable. The subsequent corollary covers this case and is obtained under the slightly stronger assumption that . [Note also that the case where is constant but is equal to zero is of no interest as it leads to a long-run-variance estimator that vanishes identically.]

Corollary 5.5.

Let satisfy and suppose that Assumption 3 holds. Suppose further that is constant and symmetric, and that is nonzero. Then and satisfy Assumption 1 with . Let be of the form (4) with , , and . Then

| (18) |

holds for every critical value , , for every , and for every . Furthermore, for every the lower bound in the previous display is an upper bound for the maximal power of the test under i.i.d. errors, i.e.,

| (19) |

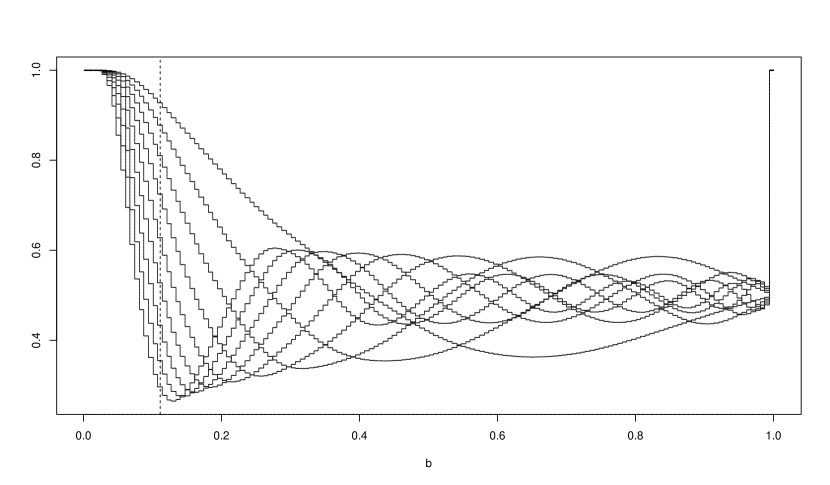

The previous corollary shows that the size of the test is bounded from below by the probability that the long-run-variance estimator used in the construction of the test statistic is nonnegative, where the probability is taken under -distributed errors. For consistent long-run-variance estimators this probability approaches as sample size increases, and hence the size of tests based on such estimators will exceed any prescribed nominal significance level eventually. Additionally, it is shown in that corollary that for nonnegative critical values (the standard in applications) the probability also provides an upper bound on the maximal power of the test under i.i.d. errors. Thus, if the lower bound in (18) is small, and hence (18) does not tell us much about size, the inequality in (19) shows that power must then be small over a substantial subset of the parameter space (unless perhaps one chooses a negative critical value). To get an idea of the magnitude of the lower (upper) bound in (18) ((19)) in a special case, we computed numerically for the rectangular kernel, i.e., for , for the cases when Assumption 3 is satisfied with , respectively, sample size , and bandwidth parameter for .171717For the matrix has all entries equal to one, implying that and thus are identically zero. This is an uninteresting case and falls outside the scope of Corollary 5.5. [If one insists on using the corresponding test statistic as defined in (4), is then identically zero, leading to a useless testing procedure.] Of course, for such values of the probability equals one, explaining the sharp increase of the graph in Figure 1 for close to . The results are presented in Figure 1.181818The corresponding figure in the previous versions of this paper was incorrect due to a coding error. Furthermore, to emphasize that the functions shown in the figure are step functions, we now use a finer grid for in the computation; and the vertical connecting lines were added to facilitate readability. For all values of and the probability is quite large, in particular is larger than , and thus exceeds commonly used significance levels. Thus, as a consequence of (18), one has strong size distortions regardless of the values of and chosen if one decides to use a test based on the rectangular kernel. Together with (19), Figure 1 also shows that for a large range of ’s the power of the corresponding tests (with nonnegative critical value ) can nowhere exceed , no matter how strong the deviation from the null hypothesis might be. Note also that the probability can be easily obtained numerically in any other case, as it is the probability that a quadratic form in a standard Gaussian random vector is nonnegative (for the actual computation we used the algorithm by Davies (1980)).

The assumption of being data-independent, i.e., constant as a function of , in the previous two corollaries is not satisfied for the important class of long-run-variance estimators that incorporate prewhitening or data-dependent bandwidth parameters (e.g., Andrews (1991), Andrews and Monahan (1992), and Newey and West (1994)). An additional complication for such estimators is that the corresponding weights matrix , and thus also , are in general not well-defined for every . Nevertheless, after a careful structural analysis of such estimators (similar to the results obtained in Section 3.3 of Preinerstorfer (2017)), one can typically show that the resulting test statistic satisfies the assumptions of Theorem 5.2 above and thus one can obtain suitable versions of the above corollaries tailored towards test statistics based on specific classes of prewhitened long-run-variance estimators with data-dependent bandwidth parameters. To make this more compelling, we provide in the following such a result for a widely used procedure in that class. We consider a version of the AR(1)-prewhitened long-run-variance estimator based on auxiliary AR(1) models for bandwidth selection and the Quadratic-Spectral kernel as discussed in Andrews and Monahan (1992). This is a long-run-variance estimator as in (17), where the weights matrix is obtained as follows (the set where all involved quantities are well-defined is given in (21) further below): Let

| (20) |

and define for , which one can write in an obvious way as with a continuous function on . Define the data-dependent bandwidth parameter via

The long-run-variance estimator is now obtained (granted the involved expressions are well-defined) by choosing in (17) equal to

where is defined as in case holds (cf., e.g., p. 821 in Andrews (1991) for a definition of the Quadratic-Spectral kernel ). The corresponding covariance matrix estimator is then given by plugging into (16). The set where (and hence ) is well-defined is easily seen to coincide with the set of all such that and are both well-defined and are not equal to , i.e., with the set

| (21) |

Define as the complement of the set (21) in . A result concerning size properties of polynomial trend tests based on the long-run-variance estimator is now obtained by combining Theorem 5.2 above with results obtained in Lemma D.3 in Appendix D, showing, in particular, that and satisfy Assumptions 1 with , provided holds. Note that (i) the condition only depends on properties of the design matrix and hence can be checked, and that (ii) in case , the matrix is nowhere well-defined, and tests based on this estimator hence break down in a trivial way.

Corollary 5.6.

Remark 5.7.

5.1.2 Properties of some recently suggested tests for hypotheses on polynomial trends

In this subsection we discuss finite sample properties of classes of tests for polynomial trends that have been suggested in Vogelsang (1998) and Bunzel and Vogelsang (2005). We start with a discussion of the tests introduced in the former article. Vogelsang (1998) introduces two classes of tests for testing hypotheses on trends, in particular polynomial trends. From Section 3.2 of Vogelsang (1998) it is not difficult to see that these classes of test statistics (i.e., the classes referred to as and in that reference) are (possibly up to a constant positive multiplicative factor that can be absorbed into the critical value) of the form (4). More specifically, the test statistics in Vogelsang (1998) are based on a combination of one of the two estimators

| (22) |

with a corresponding covariance estimator of the form

| (23) |

for and where if and if . Here is the -dimensional matrix that has above the main diagonal and on and below the main diagonal, is a real number191919We here also allow for the value in the formulation of the covariance estimators because this turns out to be convenient in the proofs., is an -dimensional matrix (with ) such that is of full column-rank . [In Vogelsang (1998) the column vectors of correspond to polynomial trends of an order exceeding the polynomial trends already contained in .] Furthermore,

| (24) |

and

with , where we use the notation

for nonsingular and for of rank . It is obvious from the above expressions that the covariance estimator is not well-defined on all of . However, it is also not difficult to see that the set where such an estimator is well-defined coincides with , see the proof of Lemma D.4 in Appendix D. We stress once more that the matrix used in the construction above is chosen in a particular way in Vogelsang (1998). We do not impose such a restriction here, because it would unnecessarily complicate the presentation of the result below, and because this restrictions is actually not necessary for establishing the result. The following result now shows, in particular, that the tests suggested in Vogelsang (1998) suffer from substantial size distortions in case .

Corollary 5.8.

Next we turn to the tests introduced in Bunzel and Vogelsang (2005). We first discuss tests introduced in that article with data-independent tuning parameters and data-independent critical values: These tests are based on the OLS estimator and two classes of covariance matrix estimators, both of which incorporate a tuning parameter , and which are defined as

| (25) |

where is an -dimensional matrix with such that is of full column-rank (note that and have been defined in (17) and (24) above), and

| (26) |

where has been defined below (23). The subsequent result applies, in particular, if where is a (fixed) real number and is a kernel function such that is positive definite, including the recommendation in Bunzel and Vogelsang (2005) to use the Daniell kernel. In that case, and more generally whenever is nonzero and nonnegative definite (with constant202020Cf. Footnote 16 and symmetric), the subsequent corollary shows that the above mentioned tests in Bunzel and Vogelsang (2005) have size equal to one if ; in case is nonzero but not nonnegative definite, a lower bound on the size is obtained, which also provides an upper bound for the power in the case of i.i.d. errors. A discussion similar to the discussion following Corollary 5.5 also applies here (cf. also Figure 1).

Corollary 5.9.

Let satisfy and suppose Assumption 3 holds. Suppose that is constant and symmetric, that is nonzero, and that . Furthermore, for the statements that involve , suppose is an -dimensional matrix with such that is of full column-rank . Then, and ( and , respectively) satisfy Assumption 1 with (, respectively). Let be of the form (4) with , , and , or with , , and . Then

holds for every critical value , , for every , and for every . The lower bound equals in case is nonnegative definite. Furthermore, for every the lower bound in the previous display is an upper bound for the maximal power of the test under i.i.d. errors, i.e.,

| (27) |

We shall now turn to the approach Bunzel and Vogelsang (2005) suggest for practical applications. This approach is based on a data-driven selection of the weights matrix and of the tuning parameter , and on a data-driven selection of the critical value . Their approach is as follows: Bunzel and Vogelsang (2005) focus on based on the Daniell kernel. More specifically, they set (cf. Bunzel and Vogelsang (2005), Appendix B, for a definition of the Daniell kernel). Recall that, regardless of the value of , the matrix with elements based on the Daniell kernel is positive definite. The authors recommend to choose as a positive piecewise constant function of (which has been defined in (20) above), more precisely, for constants , (), and , , they suggest to use

For a recommendation concerning the choice of these constants see Bunzel and Vogelsang (2005), p. 388. Furthermore, Bunzel and Vogelsang (2005) suggest to choose their data-driven critical value and a data-driven tuning parameter as a polynomial function of , respectively. More precisely, for constants (, ) and (, ) they suggest to use

Then they set

and define, in correspondence with (25) and (26), the covariance estimators

and

The vectors of (constant) tuning parameters , , , and this approach is based on are tabulated in Bunzel and Vogelsang (2005) for certain cases, and need to be obtained numerically, following the rationale in Bunzel and Vogelsang (2005), for the cases not tabulated in that paper. Furthermore, the data-driven tuning parameters and as well as the data-driven critical value are well-defined for a given if and only if is well-defined, i.e., these quantities are well-defined on the complement of the closed set

| (28) |

Clearly, is contained in . Hence, it is not difficult to see that the estimator is well-defined on and that the estimator is well-defined on . In fact, under Assumption 3 we have that (see the proof of the subsequent corollary). Consequently, under Assumption 3, the estimator is well defined on and is well-defined on . [In order that the data-driven critical value is also defined for every , we set equal to an arbitrary value (, say) on the null-set . Of course, the choice of assignment on this null-set is inconsequential for the result below.]

The following corollary shows that the tests for hypotheses concerning polynomial trends based on data-driven tuning parameters and a data-driven critical value as suggested in Bunzel and Vogelsang (2005) have size one in case . The proof of this is based on a similar approach as used in the proof of Corollary 5.9 above, but has to deal with the fact that the choice of the tuning parameters and the critical value is data-driven, and hence is more involved. In particular, it turns out that in order for Assumption 1 to be satisfied for the covariance estimators used here, one has to work with null-sets and that are larger than and , respectively.

Corollary 5.10.

Let satisfy and suppose Assumption 3 holds. Let for (), for , for with and , and for with and . Furthermore, for the statements that involve , suppose is an -dimensional matrix with such that is of full column-rank . Then, and satisfy Assumption 1 with (defined in Lemma D.6 in Appendix D), and and satisfy Assumption 1 with (defined in Lemma D.6). Let be of the form (4) with , , and , or with , , and . Then

holds for every and for every .

Remark 5.11.

Alternatively one can consider , where

for all such that is nonsingular, and where else, (and we can similarly define a test statistic with and in place of and , respectively). While and are well-defined test statistics, we are not guaranteed that and ( and , respectively) satisfy Assumption 1 with (, respectively). However, as well as differ from the corresponding test statistics considered in the preceding corollary at most on a null-set, hence the conclusions of the corollary carry over to and .

5.2 Cyclical trends

We here consider briefly the case when one tests hypotheses concerning a cyclical trend, i.e., when the following assumption is satisfied:

Assumption 4.

Suppose that for some where is an -dimensional matrix such that has rank (here is the empty matrix if ). Furthermore, suppose that the restriction matrix has a nonzero column for some , i.e., the hypothesis involves coefficients of the cyclical component.

Under this assumption we obtain the subsequent theorem from Theorem 3.10.

Theorem 5.12.

Under a slightly stronger condition on , the following theorem is applicable in case the assumption that or the nonnegative definiteness assumption on in the previous theorem are violated.

Theorem 5.13.

Let satisfy . Suppose Assumption 4 holds. Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1. Furthermore, assume that also satisfies Assumption 2. Then for every critical value , , for every , and for every it holds that

where is defined in Theorem 3.12.

Using these results, one can now obtain similar results as in Subsection 5.1.2 concerning the tests developed in Vogelsang (1998) and Bunzel and Vogelsang (2005) under Assumption 4. Due to space constraints, however, we do not spell out the details.

Remark 5.14.

(The cases or ) (i) In case (or ) consider Assumption 4 with the understanding that , that is now -dimensional, and that , where denotes the first column of . Then Theorems 5.12 and 5.13 continue to hold with this interpretation of Assumption 4. Also note that the case can be subsumed under the results of Subsection 5.1 by setting .

(ii) In case (or ), Theorem 5.12 (with the before mentioned interpretation of Assumption 4) in fact continues to hold under the weaker assumption that .212121In fact, it holds even more generally for any covariance model that has as a concentration space. This follows from Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016) upon noting that is a concentration space of the covariance model , that vanishes on as a consequence of the assumption (see the discussion following (27) in Preinerstorfer and Pötscher (2016)), and that for every with .222222This is proved similarly as in Footnote 14.

(iii) In case (or ), Theorem 5.13 (with the before mentioned interpretation of Assumption 4) also continues to hold under the weaker assumption that if in the definition of is now replaced by defined as

on the event where and by otherwise, and if the distribution appearing in the lower bound is replaced by where is nonsingular. Note that then reduces to . Here is the matrix given in Part 3 and is the matrix given in Part 4 of Lemma G.1 in Preinerstorfer and Pötscher (2016). This can be proved by making use of Theorem 5.19 and Lemma G.1 in Preinerstorfer and Pötscher (2016).

Appendix A Appendix: Proofs and auxiliary results for Section 3.1

Lemma A.1.

Let be a covariance model and let be a linear subspace of with . Let and , where and where ; here denotes the -th eigenvalue of counting (with multiplicity) from smallest to largest. Then and are covariance models. Furthermore, the collection of concentration spaces of coincides with , and the collection of concentration spaces of coincides with the collection .

Proof: 1. That and are covariance models is obvious since the elements of these two collections are clearly symmetric and positive definite matrices (as by construction).

2. Suppose . Then for some with . In particular, is the limit of for a sequence . But then belongs to and converges to for , since converges to , which equals zero as a consequence of . This shows that , and hence , is a concentration space of . Conversely, suppose is a concentration space of . Then for some singular matrix that is the limit of some sequence . In particular, holds for some sequence . Since the matrices reside in the unit sphere in , we have convergence of to a limit along an appropriate subsequence ; in particular, follows. Furthermore, we conclude that converges to , and hence obtain the equality . Since is certainly symmetric and nonnegative definite, we have that . Note that for every by construction of . Hence must hold. If would hold we would have , implying that is nonsingular, contradicting singularity of . Consequently, and must hold, implying that belongs to and that holds. But this shows .

3. Suppose . Then for some with . In particular, is the limit of for a sequence . But then belongs to and converges to for . Now is singular since . Hence, is a concentration space of and clearly holds. This proves one direction. Conversely, suppose is a concentration space of . Then for some singular matrix that is the limit of some sequence , where for some . By the same compactness argument as before, we have implying that . Furthermore, we immediately arrive at . As before it follows that must hold and hence that . But then holds, implying the result.

Remark A.2.

(i) By construction . Furthermore, all three collections coincide with the collection of all concentration spaces of (the union over which is in the notation of Preinerstorfer and Pötscher (2016)).

(ii) The sum is an orthogonal sum and hence is uniquely determined.

(iii) The map is surjective from to by definition, and the analogous statement holds for the map . But these maps need not be injective.

Lemma A.3.

Let be a covariance model and let be a linear subspace of with . Furthermore, let be a rejection region of a test, which is -invariant for some . Then for every , , and every we have

Furthermore, these probabilities do not depend on and they are unaffected if is replaced by an arbitrary element of .

Proof: The first claim is essentially proved by the argument establishing (B.1) in Appendix B of Pötscher and Preinerstorfer (2018). The second claim is an immediate consequence of the assumed invariance (cf. also Proposition 5.4 in Preinerstorfer and Pötscher (2016)).

Proof of Theorem 3.1: By monotonicity w.r.t. we may assume . Note that by our general model assumptions. Since is -invariant by Lemma 5.16 in Preinerstorfer and Pötscher (2016), the preceding Lemma A.3, applied with and , hence shows that it suffices to prove the theorem with replaced by . By Lemma A.1, also applied with , the space appearing in the formulation of the theorem is a concentration space of . We now apply Part 3 of Corollary 5.17 of Preinerstorfer and Pötscher (2016) to the linear model (1) considered in the present paper, but with replaced by . All assumptions of that result, except for the assumption that and simultaneously hold -almost everywhere, are easily seen to be satisfied. We verify the remaining assumption now as follows: The discussion following (27) in Section 5.4 of Preinerstorfer and Pötscher (2016) shows that in case (which is assumed here) holds for every , and thus for every (since has been assumed). Hence, -almost everywhere follows (note that trivially holds). Furthermore, Assumption 1 together with imply that for every and every , which of course implies for every . Since we have assumed , it follows on the one hand that for every we have if and only if . On the other hand, by construction holds, showing that must hold for all nonzero in view of the fact that has been assumed. Since can not be zero-dimensional in view of its definition (cf. the discussion in Pötscher and Preinerstorfer (2018) following Definition 5.1), follows, which completes the proof (since trivially holds).

Proof of Corollary 3.3: Necessity follows immediately from Theorem 3.1. For sufficiency we apply Corollary 5.6 in Pötscher and Preinerstorfer (2018) with , i.e., with : Observe that holds, and that and satisfy the assumptions of this corollary in view of Lemma 5.16 in the same reference. Since is assumed, the condition for every implies for every (as is obviously invariant under addition of elements ) and for every . An application of Corollary 5.6 in Pötscher and Preinerstorfer (2018) now delivers (6).

Theorem A.4.

Let be a covariance model. Let be a nonsphericity-corrected F-type test statistic of the form (4) based on and satisfying Assumption 1. Assume further that , that , and that is nonnegative definite for every . Suppose there exists an with the property that and hold for -almost all . Furthermore, assume that is not orthogonal to . Then (5) holds for every critical value , , for every , and for every .

Proof: The proof proceeds as the proof of Theorem 3.1 up to the point where Part 3 of Corollary 5.17 of Preinerstorfer and Pötscher (2016) is applied to the linear model (1), but with replaced by . Here now all assumptions of this result in Preinerstorfer and Pötscher (2016) are easily seen to be satisfied, except for (i) -almost everywhere, and (ii) -almost everywhere. Since hold for -almost all by assumption, we have that is singular for -almost all . But this implies for -almost all since has been assumed. Since trivially , this verifies (i). We turn to (ii): Let . Note that then by construction of . But then

belongs to since . Now,

Hence, if and only if , which in turn is equivalent to (since ). But since also belongs to as shown before, we conclude that holds if and only if . As a consequence,

This is a proper linear subspace of except in case , which, however, is impossible by the assumption that is not orthogonal to . Hence, only occurs on a proper linear subspace of , and hence on a subset of that has -measure zero. Since trivially , this proves (ii) and completes the proof.

A.1 Some comments on Lemmata A.1 and A.3

Lemmata A.1 and A.3 allow one to derive results regarding the rejection probabilities under a covariance model by working with a different, though related, covariance model . [By Lemma A.1 this related covariance model has the property that its concentration spaces in the sense of Preinerstorfer and Pötscher (2016) are precisely given by the elements of .] A case in point is Theorem 3.1 in Section 3.1, which provides a “size one” result for the covariance model , and which has been derived by applying Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016) to the covariance model , after an appeal to the aforementioned lemmata. In a similar vein, one can combine other results of Preinerstorfer and Pötscher (2016) with these lemmata, but we do not spell this out here. Often this will lead to improvements over what one obtains from a direct application of the respective result of Preinerstorfer and Pötscher (2016) to the covariance model . We illustrate this in the following by comparing the result in Theorem 3.1 with what one gets if instead one works with the originally given and directly applies Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016) to .

Suppose and are as in Theorem 3.1 (again with and nonnegative definiteness of for every ). Applying Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016) to the originally given covariance model allows one to obtain the following result: If a concentration space of exists that satisfies and , then (5) holds (for every , every , and every ). [To see this note that by Corollary 5.17 in Preinerstorfer and Pötscher (2016) one only has to verify that and hold -almost everywhere. The argument for -a.e. is identical to the corresponding argument given in the proof of Theorem 3.1. For the second claim a similar argument as in the proof of Theorem 3.1 shows that for we have if and only if . In other words, for only occurs when , which is a -null set, since .]

We now show that Theorem 3.1 is indeed at least as good a result as the result obtained in the preceding paragraph. For this it suffices to show that a concentration space of satisfying and gives rise to an element satisfying the assumptions of Theorem 3.1: To see this, set and observe that by Part 1 of Lemma B.3 in Appendix B.1 of Pötscher and Preinerstorfer (2018) (since in view of , and since in view of, , and ). Furthermore, observe that must also hold, since and .

Theorem 3.1 will sometimes actually give a strictly better result for the following reason (at least for covariance models that are bounded, an essentially costfree assumption in view of Remark 5.1(ii) in Pötscher and Preinerstorfer (2018)): Concentration spaces of , that satisfy but also , can not be used in a direct application of Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016) since such spaces do not satisfy the relevant assumptions (note that for all holds for such spaces ); hence they do not help in establishing a result of the form (5) via a direct application of Part 3 of Corollary 5.17 in Preinerstorfer and Pötscher (2016). Nevertheless, such concentration spaces can have associated with them spaces in the way as described in Part 2 of Lemma B.3 in Appendix B.1 of Pötscher and Preinerstorfer (2018), that then may allow one to establish (5) via an application of Theorem 3.1 (provided the condition can be shown to hold).

Appendix B Appendix: Proofs and auxiliary results for Section 3.2

Proof of Theorem 3.6: First, that is equivalent to where is obvious since any element of is the sum of an element of and an element of . Second, , , and the fact that is certainly orthogonal to imply . Since we always maintain we can conclude that must hold. This together with Proposition 6.1 of Pötscher and Preinerstorfer (2018) now shows that the linear subspace figuring in the theorem belongs to as clearly holds. An application of Theorem 3.1 with then completes the proof.

Proof of Lemma 3.8: If holds, the definition of (Definition 6.4 in Pötscher and Preinerstorfer (2018)) immediately implies that must hold. To prove the converse, we first claim that there exists a sequence of spectral densities in so that the sequence of spectral measures defined by their spectral densities

converges weakly to a spectral measure that satisfies . Here is a certain differencing operator given in Definition 6.3 of Pötscher and Preinerstorfer (2018) and denotes the support of . To prove this claim, let converge to as , and let for be a sequence in , where , that converges to as . Now for every fixed the sequence of spectral measures with spectral density