remarkRemark \newsiamremarkexampleExample \newsiamthmassumptionAssumption \headersError Rate of CQMC for Discontinuous FunctionsZ. He

On the Error Rate of Conditional Quasi-Monte Carlo for Discontinuous Functions††thanks: Submitted to the editors DATE: April, 2018. \fundingThis work was supported by the National Science Foundation of China under grant 71601189.

Abstract

This paper studies the rate of convergence for conditional quasi-Monte Carlo (QMC), which is a counterpart of conditional Monte Carlo. We focus on discontinuous integrands defined on the whole of , which can be unbounded. Under suitable conditions, we show that conditional QMC not only has the smoothing effect (up to infinitely times differentiable), but also can bring orders of magnitude reduction in integration error compared to plain QMC. Particularly, for some typical problems in options pricing and Greeks estimation, conditional randomized QMC that uses samples yields a mean error of for arbitrarily small . As a by-product, we find that this rate also applies to randomized QMC integration with all terms of the ANOVA decomposition of the discontinuous integrand, except the one of highest order.

keywords:

Conditional quasi-Monte Carlo, Smoothing, ANOVA decomposition, Singularities, Discontinuities41A63, 65D30, 97N40

1 Introduction

Conditional Monte Carlo (CMC) is widely used in stochastic simulation (see [1, 4]), which is also called conditioning. Suppose that our goal is to estimate an expectation (integral)

where is the dimension of the problem, and is the probability density function (PDF) of the random vector . The basic idea of CMC is to use conditional expectation of as an estimator. CMC enjoys a good effect of reducing the variance, compared to plain Monte Carlo (MC). On the other hand, thanks to another effect of smoothing, CMC is widely used in sensitivity estimation when the problem involves discontinuities (see [3, 4]). In practice, there are two major concerns in using CMC:

-

•

the choice of conditioning variables (say, ), and

-

•

the tractability of the resulting conditional expectation .

In this paper, we restrict our attention to the case of choosing some components of as the conditioning variables and assume that the components of are independent identically distributed (IID). We focus on investigating the smoothness property of the resulting conditional expectation rather than inspecting the tractability of .

Quasi-Monte Carlo (QMC) is usually applied to integration problems over the unit cube, which yields an asymptotic error rate of when the integrand has bounded variation in the sense of Hardy and Krause [18]. Conditional QMC (CQMC) is a counterpart of CMC by replacing the random points with QMC points. We consider a setting that the integrand is discontinuous, under which plain QMC may lose its power because QMC favors smooth integrands. He and Wang [13] and He [11] gave convergence rates of randomized QMC (RQMC) for certain classes of discontinuous functions. The rates decline quickly as the dimension goes up. CQMC has the potential to improve the efficiency of QMC as conditioning could smooth the integrand more or less. Our main interest is to provide theoretical guarantees for using CQMC.

A necessary first step in applying QMC methods to an integral over is to transform the integral into an integral over the unit cube . That transformation may introduce singularities at the boundary of . In general, conditioning cannot remove such singularities, but it brings a smoothing effect [7, 8, 9]. Griebel et al. [8, 9] studied kink functions of the form , where is a smooth function on , and showed that under suitable conditions, integrating out some components of (this process is actually the conditioning method in our terminology) leads to a function with unlimited smoothness. Griebel et al. [7] considered the setting of integration problems over the domain . More recently, Griewank et al. [10] considered a smoothing method called “preintegration”. In the preintegration method, one of the variables is integrated out for non-smooth integrands with kinks or discontinuities. By extending the work in [8, 9], Griewank et al. [10] proved that the presmoothed integrand belongs to an appropriate mixed derivative function space. However, these papers do not give error analysis for the smoothed function. Particularly, Griebel et al. [8] commented that

“These results are expected to lay the foundation for a future rigorous error analysis of direct numerical methods for option pricing integrals over , methods that do not involve mapping to the unit cube.”

Motivated by a sequence of papers by Griebel et al. [7, 8, 9] and Griewank et al. [10], we first study the smoothness property of conditioning for certain discontinuous functions, which often arise in the pricing and hedging of financial derivatives. We then give conditions such that the resulting function satisfies the so-called boundary growth condition studied in Owen [20]. The error analysis for CQMC is thus carried out by applying the results in Owen [20]. In particular, we show that conditional RQMC yields a mean error rate of for arbitrarily small under some conditions. As illustrative examples, we show that the rate is attainable for arithmetic Asian options with their Greeks and binary options, when using proper constructions of the Brownian motion and conditioning variables. It is known that using dimension reduction methods in QMC can enhance the efficiency of QMC [14, 22]. The rate also holds if one uses some dimension reduction methods to combine with CQMC. As a by-product, we give error rates for RQMC integration with all terms of the ANOVA decomposition of the discontinuous integrand. Under some conditions, RQMC can achieve a mean error rate of for all ANOVA terms, except the one of highest order. While for the highest order term which is non-smooth, the rate may be just , as found in He [11].

To summarize, we make the following contributions in this paper.

- •

-

•

More importantly, we give rates of convergence for CQMC. Our analysis does not rely on the concrete form of the resulting conditional expectation. Additionally, the required conditions are very easy to check for our applications.

We find that the choice of conditioning variables is very important in CQMC as it has an impact on the smoothness of the resulting estimate and hence on the QMC accuracy. The theoretical underpinnings in this paper are expected to predict the benefits of using CQMC in real-world applications.

The remainder of the paper is organized as follows. We formulate the problem in Section 2. Section 3 studies the smoothing effect of conditioning. Section 4 establishes rigorous error analysis for CQMC sampling. Section 5 studies the error rate of QMC integration with all terms of ANOVA decomposition. Several examples from financial engineering are studied in Section 6 to exemplify the value of our theoretical underpinnings, followed by concluding remarks in Section 7.

2 Problem Formulation

Consider an expectation (or equivalently an integral over )

| (1) |

where the components of are IID with PDF and cumulative distribution function (CDF) . For simplicity, we use the same notation for random variable and the integration variable. Throughout this paper, assume that . To estimate the integral (1) by QMC, one may transform (1) into an integral over

where the inverse function applies to each component of . We then take the following quadrature rule as an estimate of ,

| (2) |

where . In this paper, we are interested in discontinuous integrands over of the form

| (3) |

where are smooth functions of all variables. See Section 6 for examples of this form.

Denote as the components of apart from . Integrating (3) with respect to (i.e., taking as the conditioning variables) gives

We should note that . RQMC integration with renders unbiased estimate, as the CMC sampling; see [16] for a survey on RQMC.

Prior to studying the smoothness property of the function , we specify some notations. Denote and . For , denotes the derivative taken with respect to each once for all . For any multi-index whose components are nonnegative integers,

where . If for all and otherwise, then .

3 The Smoothing Effect of Conditioning

In this section, we study the smoothness property of . A key condition we require below is the uniform convergence for improper integrals with parameters. That condition ensures the interchange of differentiation and integration.

Definition 3.1.

Let . An integral converges uniformly on a set if for any , there exists a constant depending on such that

for all and all .

Theorem 3.2.

Let be an open set of , and let be a function defined over . Suppose that

-

•

and are continuous functions over , where ;

-

•

exists for any ; and

-

•

for any , there exists a set with such that the integral converges uniformly on the set .

Then

| (4) |

which is continuous on . If , then

| (5) | ||||

| (6) |

which are both continuous on .

Proof 3.3.

Let be fixed. Assume that

Theorem 3.4 (Implicit Function Theorem).

Let be a positive integer. Denote . If and Assumption 3 is satisfied, then is open, and there exists a unique function such that

and for all , we have

for all .

Proof 3.5.

See the proof of Theorem 2.3 in [8].

Theorem 3.6.

Let be a positive integer. Suppose that is given by (3) with and , , and Assumption 3 is satisfied. Denote . Let

Then is open, and there exists a unique function such that for all . Assume that for any , there exists a set with such that converges uniformly on for any multi-index satisfying and . Assume also that every function over of the form

| (7) |

where is a constant, are integers, and are multi-indices with the constraints , , , , satisfies

| (8) |

Then , and for every multi-index with and ,

| (9) |

where is a nonnegative integer depending only on , and for and , has the form (7) with parameters satisfying , , , , otherwise .

Proof 3.7.

This proof benefits largely from the proof of Theorem 1 in [9]. The implicit function theorem guarantees the existence of the solution of for any . Without loss of generality, we suppose that in Assumption 3. This implies that is an increasing function with respect to for given . We then have

where . So the function can be rewritten as

Let us consider the partial derivative of for . For , applying the Leibniz rule (6) gives

| (10) |

which is continuous on . The implicit function theorem admits

Thus (10) turns out to be

Similarly, for , we have

where

In general, for every multi-index with and , one can conclude by induction on that

where is a nonnegative integer depending on , and each function has the form (7) with integers and multi-indices satisfying , , , . Also, is continuous on .

When , it reduces to the smooth scheme, i.e., or . When , . For the two extreme cases, the condition (8) is satisfied automatically. We should note that Assumption 3 is critical to ensure a good smoothing effect of conditioning. As we will see in Section 6, if Assumption 3 is violated, is just continuous, but not differentiable. The uniform convergence is also critical in establishing Theorem 3.6. The simplest standard test of the uniform convergence of an improper integral with parameters is the Weierstrass test (see, e.g., [2]), which will be used for the CQMC error analysis.

Theorem 3.8 (Weierstrass Test).

Let be a function defined on . If there exists a function defined on such that for all and , then converges uniformly on .

Proof 3.9.

Since is integrable, for any , there exists a constant such that

holds for any . As a result,

The uniform convergence immediately stands because depends on but not .

4 Error Analysis for CQMC

Under the transformation , given by (3) is then changed to

where

| (11) |

The function may have singularities along boundary of the unit cube . He [11] showed that under certain conditions, RQMC integration with the function yields a mean error of for arbitrarily small . The rate for discontinuous functions deteriorates quickly as the dimension goes up. As we will see, smoothing the integrand is a promising way to improve QMC accuracy.

Let . Although conditioning leads to a smooth effect, the smoothed function may also have singularities along boundary of the unit cube . For functions satisfying the boundary growth condition (defined below), Owen [20] found a mean error rate for RQMC and a similar error rate for Halton sequence. We are going to give conditions on and such that the function satisfies the boundary growth condition. The convergence rates in Owen [20] can therefore be applied to the CQMC estimate.

In this paper, we focus on RQMC integration using scrambled -sequences in base proposed by Owen [19] as inputs. Here we do not restrict that because sometimes refers to the dimension of the CQMC estimate. In what follows, we assume that the points in the quadrature rule defined by (2) are the first points of a scrambled -sequence in base . The error analysis for deterministic QMC integration with Halton sequence is similar.

Definition 4.1.

A function defined on is said to satisfy the boundary growth condition if

| (12) |

holds for some , and all .

Proposition 4.2.

Let be a function defined over , and let be the first points of a scrambled -sequence in base . If satisfies the boundary growth condition (12) with , then

| (13) |

for arbitrarily small .

Proof 4.3.

See Theorem 5.7 of [20].

Remark 4.4.

Remark 4.5.

If all the growth rates are arbitrarily small, we arrive at the optimal rate . The constant in (13) is used for hiding the logarithmic term , which depends on the dimension of the problem. As a result, the dimension may has an important impact on the QMC efficiency, even for the optimal case of the growth rates.

The boundary growth condition is critical in establishing the error rate for smooth integrands with singularities at the boundary of the unit cube. It actually requires the existence of the mixed partial derivatives of the integrands. By the chain rule, we have

where . We next give conditions such that the mixed partial derivatives exist for any and then the boundary growth condition for holds.

Suppose that the integers and are fixed. There exist constants and such that

| (14) | ||||

| (15) | ||||

| (16) |

hold for and any multi-index satisfying .

The parameter can be viewed as a measure of the smoothness. Condition (14) ensures that because all . We show in Section 6 that Assumption 4 is satisfied with arbitrarily small for several typical examples from financial engineering.

Let be a strictly positive PDF, and let be the associated CDF. Assume that there exits constants such that

| (17) |

Assume also that for any nonnegative integer and any ,

| (18) |

| (19) |

The next lemma shows that Assumption 4 is satisfied with arbitrarily small for the standard normal distribution.

Lemma 4.6.

If is the density of the standard normal distribution, i.e.,

then Assumption 4 is satisfied with arbitrarily small and any .

Proof 4.7.

It is easy to see that and for all . Let be the CDF of the standard normal distribution. Note that

| (20) |

as (see Chapter 3.9 of [21]). We fine that

For any , we have

and similarly,

This gives

for any . Gordon [6] showed that for . For and any nonnegative integer , we have

Note that is a linear combination of some terms of the form with . We therefore obtain (18). The equality (19) can be obtained by replacing with in (18).

Theorem 4.8.

Proof 4.9.

Let . We first prove that for any , there exists a set with such that converges uniformly on the ball for any multi-index with and . For any , from (14), we have

where is a constant depending on . Together with

Weierstrass test admits that converges uniformly on .

For the function given by (7), by Assumption 4, we find that

| (22) |

where

Again as approaches a boundary point of lying in and , respectively. Since , it follows (18) and (19) that as , leading to (8). Therefore, by Theorem 3.6, we have .

Using (14) again gives

where we used . Since is continuous over , is bounded. According to (22) (replacing with ),

for finite . By (9), we have

| (23) |

where is a constant.

Now assume , and let . Let be a multi-index with entries for and otherwise. Then and . Let . Using (17) and (23), we obtain

As a result, satisfies the boundary growth condition with rates

for all . Note that . Applying Proposition 4.2 then gives (21). Finally, letting all and be arbitrarily small, the last part holds immediately.

The rate in (21) suggests that if there is a list of candidates to be integrated out, we prefer to choose the one with largest because it delivers the best rate.

5 ANOVA Decomposition

Griebel et al. [8] investigated the smoothness property for the terms of the ANOVA decomposition of functions with kink. In this section, we study the convergence rate for the RQMC integration with the ANOVA terms of discontinuous functions. The ANOVA decomposition of is given by

where depends only on the variables with indices , and satisfies for all .

For , denotes the components of with indices in . Let and let be the cardinality of the set . Generally, one can integrate (3) with respect to with , that is,

We may write that . Fubini’s theorem allows us to take any order within the product. The ANOVA terms are defined through the recurrence relation

where by convention. Kuo et al. [15] showed that the ANOVA terms can expressed explicitly by

| (24) |

We next pay particular attention to RQMC integration with for general . The study of below paves the way to understand the QMC error of ANOVA components of the integrand, although the projection cannot be calculated analytically in practice. Note that .

Theorem 5.1.

Proof 5.2.

From Theorem 4.8, we have . Now suppose that there is satisfying . Let be any multi-index with and for all . For any and any , it follows from (23) that

where is a constant depending on . Applying Weierstrass test again gives that

converges uniformly on the ball . By Theorem 3.2, we have and hence . By (23),

where we used .

Performing the same procedure recursively on all other elements in the set , one can easily show that and

| (26) |

where is a multi-index with and for all . Moreover, .

We now prove the second part. For any , by (26), we find that

Let . By (17), we obtain

for some constant . As a result, satisfies the boundary growth condition with rates for . Note that . Applying Proposition 4.2 then gives (25). Letting all and be arbitrarily small, the last part holds immediately.

Theorem 5.1 shows that inherits the full smoothness of and . An interesting point behind (25) is that integrating more variables out does not decrease the error rate of RQMC.

Theorem 5.3.

Consider the setup in Theorem 4.8. Let be the ANOVA term (24) for the function given by (3).

-

•

Suppose that . If , then . If , and

then

for arbitrarily small .

-

•

Suppose that Assumptions 3 and 4 are satisfied with all . Then the results above hold for any . Suppose that is given by (11), whose boundary admits a -dimensional Minkowski content111See [11] for the formal definition. In the terminology of geometry, the Minkowski content is known as the surface area of the set . Clearly, the convex sets in satisfy this condition as their surface areas are bounded by the surface area of the unit cube, which is .. If , and are arbitrarily small, then

(27)

Proof 5.4.

For any , by Theorem 5.1, we have and

since . The first part immediately follows from (24) and . If Assumptions 3 and 4 are satisfied with all , then the results in the first part hold for any . We now assume that all and are arbitrarily small. The first two cases in (27) are straightforward. For the case , . Note that , where viewed as a function over satisfies the boundary growth condition with rates . By Corollary 3.5 of [11], we obtain that

Using the triangle inequality, we finally have

which completes the proof.

Theorem 5.3 suggests that QMC can still be very effective for non-smooth integrands if they have low effective dimension. For these cases, QMC integration with all the ANOVA terms of the non-smooth integrand, expect the one of highest order, can enjoy the best possible rate . The highest non-smooth term contributes little to the integration error as its variance is negligible compared to the total variance. This finding can explain the success of dimension reduction techniques used in improving the accuracy of QMC, such as the linear transform (LT) method proposed by Imai and Tan [14], and the gradient principal component analysis (GPCA) method proposed by Xiao and Wang [25].

6 Examples from Option Pricing and Greeks Estimation

6.1 Model Setting

Let denote the underlying price dynamics at time under the risk-neutral measure. In a simulation framework, it is common that the prices are simulated at discrete times satisfying , where is the maturity of the financial derivative of interest. Without loss of generality, we assume that the discrete times are evenly spaced, i.e., , where . Denote . We assume that under the risk-neutral measure the asset follows the geometric Brownian motion

| (28) |

where is the riskfree interest rate, is the volatility and is the standard Brownian motion. Under this framework, the solution of (28) is analytically available

| (29) |

where is the initial price of the asset. Let . We have , where is a positive definite matrix with entries .

Let be a matrix satisfying . Using the transformation , where , it follows from (29) that

| (30) |

The matrix is called the generating matrix as it determines the way of simulation. Under the risk-neutral measure, the price and the sensitivities of the financial derivative can be expressed as an expectation for a real-valued function over . It is known that the choice of the matrix may have an impact on the efficiency of QMC (see, e.g., [12, 14]), but it does not affect the variance of plain MC estimate.

Many functions in the pricing and hedging of financial derivatives are discontinuous or unbounded, which can be expressed in the form (3). We next consider some representative examples of this form. Examples 6.1–6.6 below are the arithmetic Asian option and its Greeks, which were also studied in [11, 24]. Example 6.7 is the binary option, which was considered in [10]. The Greeks of the binary option can be treated as those of the arithmetic Asian option in a similar way, so we omit these cases. In this section, and denote the PDF and the CDF of the standard normal distribution, respectively.

Example 6.1.

The discounted payoff of an arithmetic average Asian option is

| (31) |

where and is the strike price.

Example 6.2.

The pathwise estimate of the delta of the Asian option is

| (32) |

The delta of an option is the sensitivity with respect to the initial price of the underlying asset.

Example 6.3.

An estimate of the gamma of the Asian option is

| (33) |

which results from applying the pathwise method first and then the likelihood ration method (see [5]). The gamma is the second derivative with respect to the initial price of the underlying asset.

Example 6.4.

The pathwise estimate of the rho of the Asian option is

| (34) |

where

The rho of an option is the sensitivity with respect to the risk-free interest rate .

Example 6.5.

The pathwise estimate of the theta of the Asian option is

| (35) |

where

The theta of an option is the sensitivity with respect to the maturity of the option .

Example 6.6.

The pathwise estimate of the vega of the Asian option is

| (36) |

in which

The vega of an option is the sensitivity with respect to the volatility .

Example 6.7.

The discounted payoff of a binary Asian option is

| (37) |

6.2 CQMC Error Rates

All the examples above fit into the form (3) with and depending on the examples. It is easy to see that . Lemma 4.6 guarantees the validation of Assumption 4. From (30), we find that

| (38) |

Thanks to all , Assumption 3 is satisfied if there exists an index such that

| (39) |

This condition is not void for commonly used constructions of the Brownian motion. For the standard construction and the Brownian bridge construction, all elements so that Assumption 3 is satisfied with all . For the principal component analysis (PCA) construction, the elements have the same sign so that Assumption 3 is satisfied with , but for , the elements can have both signs. See [5, 7] for details on these commonly used constructions.

It remains to verify Assumption 4. For simplicity, we assume that for all . For any multi-index (including ), it follows from (30) that

| (40) |

where

| (41) |

and . For any and any , it follows from (20) that

Similarly,

As a result, This implies that

| (42) |

for arbitrarily small . It then follows from (30) and (40)–(42) that the condition (15) holds for arbitrarily small and arbitrary multi-index . Since is nonsingular, there exists an index such that . For any , by (38) and (42), we find that

So the condition (16) holds for arbitrarily small and all . He [11] showed that the boundary growth condition for is satisfied with arbitrarily small for Examples 6.1–6.6. By the same way, it is easy to check that the condition (14) for the function is satisfied with arbitrarily small and arbitrary . For Example 6.7, the condition (14) is straightforward since is a constant. As a result, Assumption 4 is satisfied with arbitrarily small and all . Based on the analysis above, we conclude the following theorem for our examples as consequences of Theorems 5.1 and 5.3.

Theorem 6.8.

Note that for the standard construction and the Brownian bridge construction, the condition (39) is satisfied with all . For these cases, it is not surprising that the ANOVA terms can have unlimited smoothness, except the one of highest order, because Griebel et al. [8, 9] have shown such a smoothness property for the arithmetic Asian option (Example 6.1). We extend their results to discontinuous functions so that the smoothing effect of conditioning can be examined for the Greeks of the arithmetic Asian option (Examples 6.2–6.6) and the binary option (Example 6.7). More importantly, we show additionally that QMC can achieve the best possible error rate of for these smooth terms with singularities. For the highest order term which is non-smooth, the rate may be just , as claimed in Theorem 5.3.

We now consider the case in which the condition (39) (or equivalently Assumption 3) does not hold. In other words, there exist such that . For our examples, we find that

implying that is strictly convex over . Since , by the implicit function theorem again, there exists a unique function such that for all . Therefore, for a given , is decreasing with respect to for , while it is increasing for . This gives

Denote

It is easy to see that and for any and any . By the implicit function theorem, there exist two unique functions such that and for all . The function can then be rewritten as

Note that and as approaches a boundary point of lying in (i.e., the set ). This implies that is continuous over . However, for , may be no longer continuous over . Notice that for ,

Let be a boundary point of of lying in . Then . If

| (43) |

then

because

and

We claim that there exists an index such that . Otherwise, if for all , we then have all by (38). That leads to a contradiction. So the condition (43) reduces to . For Examples 6.2–6.6 and 6.7, it is easy to see that there exists (at least) a point such that . This implies that for Examples 6.2–6.6 and 6.7 because the derivative does not exist.

Now let us consider Example 6.1. For any , since

reduces to

which converges to as . So we have . However, the higher order mixed partial derivative with does not exist for some point in , because for any the derivative includes some terms like (7) (replacing with or ), which converges to infinity as approaches a boundary point of lying in . This implies that for Example 6.1.

We conclude that if the condition (39) is violated, cannot have unlimited smoothness for our examples. It is only guaranteed that is continuous. The mixed partial derivatives of may have additional singularities beyond those at the boundary of the unit cube . So, in this case, we may not obtain the mean error rate for the RQMC estimate as in Theorem 6.8, except the case of Example 6.1 with . This suggests that under the PCA construction, integrating out for may not gain as much as integrating out in improving the efficiency of QMC.

Although conditioning can result in smooth integrands, the resulting integrands may have large effective dimension. To circumvent this, a good strategy in practice is to employ some dimension reduction techniques after the conditioning process, such as the LT method proposed by Imai and Tan [14] and the GPCA method proposed by Xiao and Wang [25]. Weng et al. [24] called this strategy the two-step procedure. In the first step (called the smoothing step), they used the variables push-out smoothing method to remove the discontinuities in the target functions. In the second step (called the dimension reduction step), they used a so-call CQR method to reduce the effective dimension of the smoothed function. In the the smoothing step, one can use the conditioning technique instead. In principle, the dimension reduction techniques transform the smooth function to the form , where is a well-chosen orthogonal matrix. The transformation does not affect the unbiasedness of the estimate, since

holds for arbitrary orthogonal matrix . The next theorem shows that using dimension reduction techniques after conditioning does not change the smoothness property and the mean error rate.

Theorem 6.9.

Proof 6.10.

Note that depends on the generating matrix satisfying . For an arbitrary orthogonal matrix , can be expressed as by replacing the matrix with another generating matrix satisfying . Since the th columns of and are the same, the condition (39) still holds for . Applying Theorem 6.8, we obtain the desired results.

6.3 Using CQMC in Practice

A practical aspect of using CQMC is to calculate analytically . Indeed, if we choose the standard construction of the Brownian motion, it is easy to obtain the closed form of with for the examples above. Under the standard construction, we have

which is a lower triangular matrix. This gives

where . It is easy to see that for all ,

This implies that , . Therefore,

Since in the examples is a linear combination of components and , , it reduces to calculate integrals of the form

where do not depend on . By the change of variables, we have

Therefore, is available for the examples considered in this section.

Similarly, one can also obtain the closed form of with , for which do not depend on . For this case,

where . Also, and .

However, for , cannot be computed analytically under the standard construction. This is the case for the Brownian bridge construction (except the case ) and the PCA construction with . One thus may resort to some root-finding algorithms (such as Newtons’ method) to solve the equation for given .

In our numerical experiments, we examine the mean error rate of CQMC for Example 6.2 with the standard construction and . From the analysis above, is available. We also investigate the combination of the CQMC method with the GPCA method proposed by [25]. The combined method is called CQMC+GPCA. Theorem 6.9 shows that both the CQMC method and the CQMC+GPCA method have a mean error of . The purpose of using GPCA is to reduce the effective dimension of . We thus expect that the CQMC+GPCA method can further enhance the efficiency of the plain CQMC method. One can, of course, use other dimension reduction methods instead of GPCA. Here we only focus on the GPCA method because Xiao and Wang [25] found numerically that the GPCA performs consistently better than some common dimension reduction methods in the literature, such as the LT method.

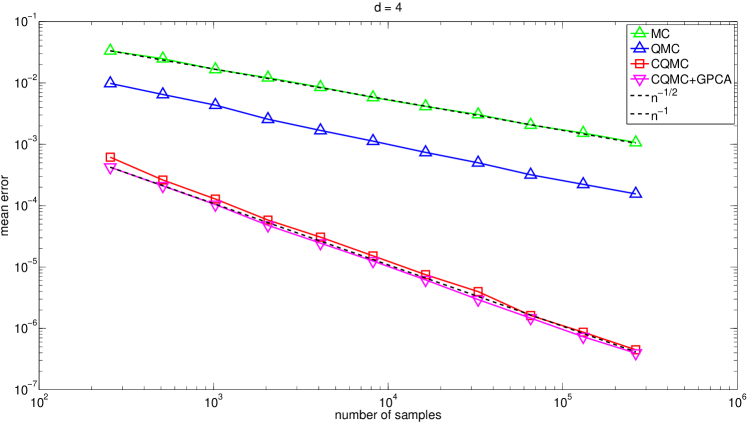

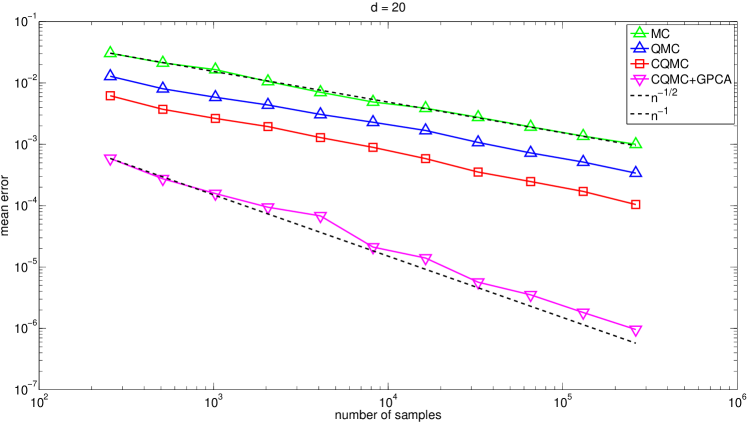

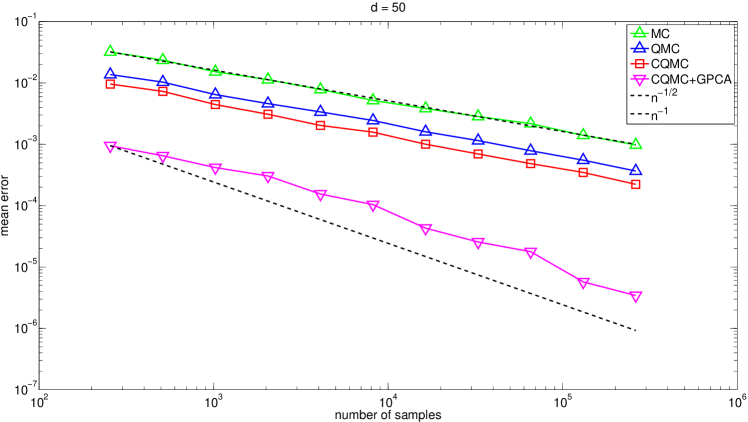

We carry out numerical experiments using MATLAB R2013a on a 2.6 GHz CPU. The RQMC points are the linear scrambled Sobol’ points proposed by [17]. We set parameters in our experiments to , , , , , and . The mean errors are estimated based on repetitions222Estimation of the mean errors requires knowing the true value of the quantity being estimated. Here we use the CQMC+GPCA method with a very large sample size to obtain an accurate estimate of and treat it as the true value.. Figure 1 shows the mean errors of the plain MC, the plain QMC, the CQMC, and the CQMC+GPCA methods for the sample sizes . When , the two CQMC methods (i.e., CQMC and CQMC+GPCA) improve the mean error rate to close to the best possible rate . Their mean error rates deteriorate as the dimension goes up. This is because the mean error of the CQMC methods depends on the dimension , as discussed in Remark 4.5. Combining the GPCA method with the CQMC method reduces the error satisfactorily. The error rate of the combined method (CQMC+GPCA) declines moderately as the dimension increases. This highlights the necessity of reducing the effective dimension in QMC. We also observe a similar pattern (not shown here) for the root mean square errors.

7 Conclusion

In this paper we found convergence rates of CQMC integration with discontinuous functions, which typically arise in the pricing and hedging of financial derivatives. The theoretical results show that conditioning not only has the smoothing effect, but also can bring orders of magnitude reduction in integration error compared to plain QMC. Under the well-known Black-Scholes framework, we showed that conditioning combined with RQMC yields a mean error of for pricing and hedging Asian options. This rate also applies to RQMC integration with all the ANOVA terms of discontinuous functions, except the one of the highest order. From this point of view, plain QMC (without conditioning) may be still successful for high-dimensional discontinuous functions with low effective dimension, as observed frequently in option pricing problems (see, e.g., [12, 22, 23]).

The rate established in this paper also apply to the case of using deterministic Halton sequence as input, thanks to Corollary 5.6 of [20]. It would be interesting to know how generally this rate holds for other branches of models, beyond the Black-Scholes model.

Acknowledgments

The author thanks Professor Ian Sloan for sharing his work [10] and his slides presented in MCQMC 2016 conference. The author also thanks Chaojun Zhang for the helpful discussion.

References

- [1] S. Asmussen and P. W. Glynn, Stochastic Simulation: Algorithms and Analysis, vol. 57, Springer, New York, 2007.

- [2] R. C. Buck, Advanced Calculus, McGraw-Hill, New York, 1978.

- [3] M. C. Fu, L. J. Hong, and J.-Q. Hu, Conditional Monte Carlo estimation of quantile sensitivities, Manage. Sci., 55 (2009), pp. 2019–2027.

- [4] M. C. Fu and J.-Q. Hu, Conditional Monte Carlo: Gradient Estimation and Optimization Applications, Kluwer Academic Publishers, Boston, MA., 1997.

- [5] P. Glasserman, Monte Carlo Methods in Financial Engineering, Springer, 2004.

- [6] R. D. Gordon, Values of mills’ ratio of area to bounding ordinate and of the normal probability integral for large values of the argument, Ann. Math. Statist., 12 (1941), pp. 364–366.

- [7] M. Griebel, F. Y. Kuo, and I. H. Sloan, The smoothing effect of the ANOVA decomposition, J. Complexity, 26 (2010), pp. 523–551.

- [8] M. Griebel, F. Y. Kuo, and I. H. Sloan, The smoothing effect of integration in and the ANOVA decomposition, Math. Comp., 82 (2013), pp. 383–400.

- [9] M. Griebel, F. Y. Kuo, and I. H. Sloan, Note on “The smoothing effect of integration in and the ANOVA decomposition”, Math. Comp., 86 (2017), pp. 1847–1854.

- [10] A. Griewank, F. Y. Kuo, H. Leövey, and I. H. Sloan, High dimensional integration of kinks and jumps – smoothing by preintegration, Preprint, arXiv:1712.00920, (2017).

- [11] Z. He, Quasi-Monte Carlo for discontinuous integrands with singularities along the boundary of the unit cube, Math. Comp., (2018). Appeared online, DOI: https://doi.org/10.1090/mcom/3324.

- [12] Z. He and X. Wang, Good path generation methods in quasi-Monte Carlo for pricing financial derivatives, SIAM J. Sci. Comput., 36 (2014), pp. B171–B197.

- [13] Z. He and X. Wang, On the convergence rate of randomized quasi–Monte Carlo for discontinuous functions, SIAM J. Numer. Anal., 53 (2015), pp. 2488–2503.

- [14] J. Imai and K. S. Tan, A general dimension reduction technique for derivative pricing, J. Comput. Finance, 10 (2006), pp. 129–155.

- [15] F. Kuo, I. Sloan, G. Wasilkowski, and H. Woźniakowski, On decompositions of multivariate functions, Math. Comp., 79 (2010), pp. 953–966.

- [16] P. L’Ecuyer and C. Lemieux, Recent advances in randomized quasi-Monte Carlo methods, in Modeling Uncertainty: An Examination of Stochastic Theory, Methods, and Applications, M. Dror, P. L’Ecuyer, and F. Szidarovszky, eds., Kluwer Academic Publishers, New York, 2005, pp. 419–474.

- [17] J. Matoušek, On the -discrepancy for anchored boxes, J. Complexity, 14 (1998), pp. 527–556.

- [18] H. Niederreiter, Random Number Generation and Quasi-Monte Carlo Methods, SIAM, Philadelphia, 1992.

- [19] A. B. Owen, Randomly permuted (t, m, s)-nets and (t, s)-sequences, in Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing, H. Niederreiter and P. J.-S. Shiue, eds., Springer, 1995, pp. 299–317.

- [20] A. B. Owen, Halton sequences avoid the origin, SIAM Rev., 48 (2006), pp. 487–503.

- [21] J. K. Patel and C. B. Read, Handbook of the Normal Distribution, vol. 150, Marcel Dekker, New York, 1996.

- [22] X. Wang and I. H. Sloan, Quasi-Monte Carlo methods in financial engineering: An equivalence principle and dimension reduction, Oper. Res., 59 (2011), pp. 80–95.

- [23] X. Wang and K. S. Tan, Pricing and hedging with discontinuous functions: Quasi–Monte Carlo methods and dimension reduction, Manage. Sci., 59 (2013), pp. 376–389.

- [24] C. Weng, X. Wang, and Z. He, Efficient computation of option prices and Greeks by quasi-Monte Carlo method with smoothing and dimension reduction, SIAM J. Sci. Comput., 39 (2017), pp. B298–B322.

- [25] Y. Xiao and X. Wang, Enhancing quasi-Monte Carlo simulation by minimizing effective dimension for derivative pricing, Comp. Econ., (2017), pp. 1–24.