[2]footnote

Sampling of probability measures in the convex order by Wasserstein projection

Abstract.

In this paper, for and two probability measures on with finite moments of order , we define the respective projections for the -Wasserstein distance of and on the sets of probability measures dominated by and of probability measures larger than in the convex order. The -projection of can be easily computed when and have finite support by solving a quadratic optimization problem with linear constraints. In dimension , Gozlan et al. [14] have shown that the projections do not depend on . We explicit their quantile functions in terms of those of and . The motivation is the design of sampling techniques preserving the convex order in order to approximate Martingale Optimal Transport problems by using linear programming solvers. We prove convergence of the Wasserstein projection based sampling methods as the sample sizes tend to infinity and illustrate them by numerical experiments.

e-mails : aurelien.alfonsi@enpc.fr, j.corbetta@zeliade.com, benjamin.jourdain@enpc.fr.

This research benefited from the support of the “Chaire Risques Financiers”, Fondation du Risque, the French National Research Agency under the program ANR-12-BS01-0019 (STAB) and was completed after the hiring of Jacopo Corbetta by Zeliade Systems

Keywords: Convex order, Martingale Optimal Transport, Wasserstein distance, Sampling techniques, Linear Programming

AMS Subject Classification (2010): 91G60, 90C08, 60G42, 60E15.

1. Introduction

For in the set of probability measures on , we say that is smaller than for the convex order and denote if for each convex function non-negative or integrable with respect to . Up to our knowledge, few studies consider the problem of preserving the convex order while approximating two such probability measures. We can mention the one-dimensional method based on the quantile functions proposed by David Baker in his PhD thesis [6] (see the beginning of Section 2.2 for more details). The dual quantization introduced by Pagès and Wilbertz [23] gives another way to preserve the convex order in dimension one (see the remark after Proposition 10 in [23]). This is unfortunately no longer true for higher dimensions. Take for example the case of the probability laws and the distribution on with uniform on . We have . We calculate their dual quantizers and on the two triangles and with vertices and . We easily obtain , . Thus, we have , , which proves that the convex order is not preserved. However, the quantization and the dual quantization give a possible way to approximate and in the convex order. Precisely, the quantization of gives a probability measure with finite support such that while the dual quantization of gives a probability measure with finite support such that . We therefore have . Though being general, this construction has several drawbacks. First, to define the dual quantization, and therefore must have a compact support. This is a very restrictive assumption. Second, the calculation of the quantization of and of the dual quantization of is in general not obvious in dimension and may require an important computation time. This is why one usually pre-calculates the quantization for standard distributions, see [22] for the Gaussian case. Third, this method only works for two measures and does not generalize to design approximations of preserving the convex order when .

To avoid the curse of dimension, it is natural to look at the Monte-Carlo method and to consider the empirical measures and , where (resp. ) are i.i.d. random variables with distribution (resp. ). Clearly, there is no reason to have (a necessary condition for the convex order from the choices with ) and even more to have . In dimension , according to Kertz and Rösler [19, 20], the set of probability measures with a finite first moment is a complete lattice for the increasing and decreasing convex orders. The present paper stems from our preprint [1] (Sections 3 and 4), where, in Section 2 devoted to the one-dimensional case, we also investigate the approximation of by (resp by ) defined as the infimum of and for the decreasing convex order when and for the increasing convex order otherwise so that (resp. ). Unfortunately, this approach does not generalize to dimension , where, according to Proposition 4.5 [21], even the set of probability measures with a constant expectation is no longer a lattice for the convex order. In the present paper, still looking for modifications of smaller than in the convex order, we introduce the following minimization problem where

| (1.1) |

For , this is a quadratic optimization problem with linear constraints which can be solved efficiently numerically (see Section 5). In general, this is the minimization of a continuous function on a compact set and there exists a minimizer . We then define

By construction, we have . In the next section, we generalize this problem by considering, in place of the point measures and , general elements of with denoted (with a slight abuse of notation) by and . This leads us to define the projection of on the set of probability measures dominated by in the convex order for the Wasserstein distance with index :

where the set of probability measures on with marginal laws and , i.e. and for any Borel set . We show that this projection is well defined for and study some of its properties. Notice that after our preprint [1], Gozlan and Juillet [13] and Backhoff-Varaguas et al. [5] have recently considered the projection for . In dimension , according to Gozlan et al. [14] Theorem 1.5, the projection does not depend on . We explicit its quantile function in terms of the quantile functions of and so that it can be computed by efficient algorithms when and have finite supports. In Section 3, we prove that, when , then and deduce that converges weakly to as . Moreover, we extend the construction to the sampling of several probability measures ranked in the convex order. Section 4 is devoted to the projection of on the set of probability measures larger than in the convex order for the Wasserstein distance with index . Last, in Section 5, we illustrate by numerical experiments the Wasserstein projection based sampling methods and their application to approximate Martingale Optimal Transport problems. One important motivation of this paper is indeed to tackle numerically the Martingale Optimal Transport (MOT) problem introduced in [7], which has received a recent and great attention in finance to get model-free bounds on option prices. A family of probability measures on is called a Markov kernel on if for any Borel set , is measurable. We define where denotes a Markov kernel such that , the set of martingale couplings. Theorem 8 in Strassen [27] ensures that, when , . For a measurable payoff function , the MOT problem consists in finding an optimal coupling that minimizes (or maximizes)

| (1.2) |

among all couplings . In finance, this problem arises naturally if one considers the prices of assets at dates . We assume zero interest rates and suppose that we can observe the marginal laws (resp. ) of (resp. ) from option prices on the market and that we want to price an option that pays at date . Any martingale coupling is an arbitrage free pricing model: the supremum and the infimum of over all these couplings give model free bounds on the option price. From the dual formulation of the problem, Beiglböck, Penkner and Henry-Labordère [7] have proved that the upper (resp. lower) bound is the cheapest (resp. most expensive) initial value among superhedging (resp. subhedging) strategies. To compute the model free bounds on the option price, one may consider approximating the probability measures and by probability measures with finite supports (typically the empirical measures of i.i.d. samples) and , with , for any and and solve the approximate MOT problem: to minimize (or maximize)

| (1.3) |

over under the constraints

This problem falls into the realm of linear programming: powerful algorithms have been developed to solve it numerically. The key issue to run these algorithms is the existence of such matrices , that amounts to the existence of a martingale coupling between and . By Strassen’s theorem, this is equivalent to have , which motivates the interest of preserving the convex order when sampling both the probability measures and . It is very natural in the financial application to consider empirical measures with : once a stochastic model is calibrated to European option market prices, one basically samples it at different times to price exotic options, which gives the empirical measures at those times.

2. Wasserstein projection of on the set of probability measures dominated by in the convex order

2.1. Definition, existence and uniqueness

For a Markov kernel on , we set

It is well known (see [11] pages 78–80 or [24] page 117) that if , there exists a -a.e. unique Markov kernel such that . This kernel satisfies obviously , which we note later on. Conversely, if is a kernel satisfying then defines a probability measure in . We define the set of probability measures on and, for ,

the set of probability measures with finite moment of order .

Suppose that and is a Markov kernel such that . Then

so that is defined -a.e.. Moreover for each convex function such that , by Jensen’s inequality,

Despite the restriction on the growth of the convex function , by Lemma A.1 below, this ensures that .

For and , we consider the following generalization of the minimization problem (1.1) :

Note that this problem is a particular case of the general transport costs considered by Gozlan et al. [15] and Alibert et al. [3], who are interested in duality results and by Backhoff-Veraguas et al. [5] who deal with existence of optimal transport plans and necessary and sufficient optimality conditions in the spirit of cyclical monotonicity. Gozlan and Juillet [13] characterize optimal transport plans between and for the cost . When the are distinct, (1.1) is recovered by setting

At optimality in (1.1), by Jensen’s inequality when for and the problem (1.1) modified with the additional constraint when is recovered by setting

According to the next theorem the generalized problem is equivalent to the computation of the projection of on the set of probability measures dominated by in the convex order for the -Wasserstein distance.

Theorem 2.1.

Let , . One has where both infima are attained. If , then the functions are a.e. equal, is the unique minimizing and the unique optimal transport plan such that .

When , is the projection of on the set of probability measures dominated by in the convex order and .

Proof.

For ,

where the right-hand side is finite if since . By the Markov inequality and the Prokhorov theorem, this last bound implies that is relatively compact for the weak convergence topology. For and , denoting by a martingale kernel such that , we have

For a sequence in weakly converging to , this implies uniform integrability ensuring that for continuous and such that , . With Lemma A.1 below and the continuity of real valued convex functions on , we deduce that . Hence is compact for the weak convergence topology.

Since is lower-semicontinuous for this topology, there exists such that . Let be a martingale Markov kernel such that and a Markov kernel such that and . One has and, by martingality of ,

With Jensen’s inequality, we deduce that

| (2.1) |

On the other hand, for any Markov kernel such that , and . Hence

so that both infima are equal and . Moreover, the inequality in (2.1) is an equality. If , by strict convexity of , this implies that a.e. so that .

For , the uniqueness of is also obtained from the strict convexity of . Namely, for any optimal kernel we have

Since , we necessarily have and then , -a.e.. ∎

Remark 2.2.

When , let us give an example of non-uniqueness for the optimal functions and the probability measures such that . Let (resp. ) be the uniform law on (resp. ). We have

For , is such that , and is the uniform law on . Using that for for the first equality, we have

Thus all the kernels and pushforward measures are optimal.

Example 2.3.

Let and . We assume that , which implies that . For , let be the image of by . Then, for any kernel such that ,

This lower bound is attained for , where is any martingale kernel such that , since for this choice. Therefore, for , .

Let us observe that if with , then we have for any . In general, as in the next example, is different from .

Example 2.4.

Let , with and . For , since, by Theorem 2.1, is the image of by some transport map and , one has for some . For , since the distances between and and between and are equal whereas is closer to than , one has . Since the unique minimizer of on is , one has and . Since the unique minimizer of on is , for , one has and .

Nevertheless, the situation is strikingly different in dimension where, according to Gozlan et al. [14] Theorem 1.5, the projection does not depend on . We are going to explicit this projection by characterizing its quantile function in terms of the quantile functions of and .

2.2. Dimension

Let and be the cumulative distribution functions and for , and their left-continuous and non-decreasing generalized inverses also called quantile functions. The convex order is characterized as follows in terms of the quantile functions (see Theorem 3.A.5 [26]) : for ,

| (2.2) |

Notice that, as a consequence of this characterization, if , then for , , as stated by Baker in Theorem 2.4.11 [6].

Theorem 2.5.

For , let denote the convex hull (largest convex function bounded from above by) of the function . There exists a probability measure such that , . Moreover, and for each such that , . Last, is non-decreasing and is an optimal transport map : and for all , .

For probability measures (resp. ) on the real line with and (resp. and ), the continuous and piecewise affine function changes slope at with a change equal to (which can be equal to zero if and ). Clearly, is piecewise affine and changes slope at most at points with changes not greater than so that with . The convex hull can be computed by Andrew’s monotone chain algorithm and the points are easily deduced.

The proof of Theorem 2.5 relies on the following lemma and is postponed after its proof.

Lemma 2.6.

Let and . Then is non-increasing.

Proof.

It is enough to check that if is not non-increasing for some , one can find such that where, according to Proposition 2.17 [25], . With the left-continuity of , the lack of monotonicity of this function is equivalent to

Let , where one easily checks that the denominator does not vanish on and that . For ,

so that by strict convexity,

With Jensen’s inequality, we deduce that

The right-hand side is not smaller than where denotes the image of the Lebesgue measure on by . For convex and such that , by Jensen’s inequality,

Since the right-hand side is equal to , by Lemma A.1 below, one has .

∎

Proof of Theorem 2.5.

Let be uniformly distributed on .

Since for all , where the right-hand side is a convex function of , one has and . By Lemma A.2 below, the convexity of both and implies that is convex. Let denote the left-hand derivative of this function and the probability distribution of . By Lemma A.3 below, is equal to so that , .

Let . Since with equality when , one has with equality when so that by (2.2), . By concavity of , the left-continuous function is non-increasing.

The set

is not empty since . Let denote the distribution of for . For all , and . By Lemma A.4 below, the set admits an infimum for the convex order and for all , . For , since is non-decreasing, by Lemma A.3, and coincide away from the at most countable set of their common discontinuities, with the former left-continuous and the latter right-continuous. Hence for ,

where the right-hand side is not greater than since . Since iff is non-decreasing, , and for all , (see (2.2)), the definition of implies that for all , . Hence for all which ensures that is the distribution of . Therefore, if is such that ,

where we used the definition of and the convexity of for the inequality and Lemma 2.6 for the final equality. Since, by Theorem 2.1, is the unique minimizer of on , we conclude that .

From the left-continuity of the quantile functions, we get for , and this function is non-decreasing. Thus, is nondecreasing. To conclude the proof, it is now sufficient to check that for a.e. . Indeed, combined with the inverse transform sampling and Proposition 2.17 [25], this ensures that and

By definition of the quantile function , for all , and by right-continuity of , for all , . With the monotonicity of we deduce that for all such that , . Therefore, if is such that for some , then . Otherwise, for some such that . We observe that and are constant on since is concave on this interval. For , we have and we get . Therefore the equality holds for outside the countable set . ∎

3. Approximations in the convex order

The next proposition is the key result to construct approximations of probability measures that preserve the convex order.

Proposition 3.1.

Let , such that . Then, we have

where, for , by a slight abuse of notation, denotes any such that .

Let be such that . From Proposition 3.1, if we have approximations and that satisfy and , then also approximates since we have . In particular, if we take i.i.d. samples (resp. ) distributed according to (resp. ), the empirical measure (resp. ) satisfy (resp. ) almost surely. Indeed, the law of large numbers gives the almost sure weak convergence of towards as well as the almost sure convergence of to . By Proposition 7.1.5 of [4], we get almost surely. Under more restrictive assumptions on the measures and , we can have almost sure estimates on the rate of convergence. Let us assume that is such that for some and . Then, by Theorem 2 of Fournier and Guillin [12], there are constants depending on such that

Therefore we have , which gives that almost surely, there exists such that . Since is convex, , in which case we have both and and thus

Theorem 2 of [12] also gives upper bounds of under different weaker assumptions on . We can repeat the same argument in those cases and get a weaker rate of convergence of towards .

We now briefly consider the multi-marginal case. Let , , be positive integers and be probability measures on such that and . We consider for , the empirical measure of an i.i.d. sample distributed according to . Let us set and define (using for the abuse of notation made in Proposition 3.1) by backward induction for , the projection of on the set for the -Wasserstein distance. Then, by Proposition 3.1, we have for ,

Therefore, we deduce by induction that

We eventually get the following result.

Proposition 3.2.

Let , be probability measures on such that and . Then, as , converges almost surely to . Besides, if for some and , we have a.s. .

Proof of Proposition 3.1.

We consider . Let (resp. ) be a Markov kernel such that (resp. ) is an optimal transport plan for (resp. ). Let be a martingale kernel such that . We observe that is a Markov kernel such that . By Theorem 2.1, then using the martingale property of , the Jensen and Minkowski inequalities, we get

The claim follows since . ∎

4. Wasserstein projection of on the set of probability measures larger than in the convex order

Let . We have just presented a construction of a measure such that . Then, a natural question is: can we construct similarly a measure such that ? Let us start again with two empirical measures and . A natural construction would be to take , where minimizes under the constraint (this constraint can always be satisfied when by taking for or when by taking as the images of the vertices of the canonical simplex by some similarity transformation). The analogous construction for would be then to take , where is a measurable map that minimizes , under the constraint . More generally, we define

Let us now assume that . The latter problem coincides with the former one when is absolutely continuous with respect to the Lebesgue measure (i.e. for any Borel set with zero Lebesgue measure), since we know in this case that the optimal coupling for the Wasserstein distance is given by a transport map, see e.g. Theorem 6.2.4 in [4]. We now check that it is well defined. Let be such that and . Let denote an optimal transport plan between and for . We have : the boundedness of the moments ensures that there is a subsequence such that and weakly converges to and . This gives for any . By monotone convergence, we deduce that . Clearly, is a coupling between et . Besides, from the uniform integrability given by the bounds on the -th moment, we get that for any convex function such that , . Therefore, by Lemma A.1 below, , which shows the existence of a minimum. When is absolutely continuous with respect to the Lebesgue measure, we can show that this minimum is unique. Let us consider such that . One has , and, by Lemma A.5 below, we get and since the inequality is necessarily an equality. In dimension , uniqueness still holds without any assumption on . Indeed, by (2.2), the probability measure defined by is such that . Again by Lemma A.5, and since the inequality is necessarily an equality. In dimension , if , let

Let denote the concave hull (smallest concave function larger than) of the function . There is a probability measure such that . Moreover, . For , let denote the distribution of for uniformly distributed on . By Lemma A.4 below, the set admits an infimum for the convex order and for all , . For , one has by Lemma A.3 below. With the fact that if and only if for all with equality for and is concave, one deduces that for ,

Hence . If for some , then

By Lemma A.6 below, . Therefore and .

For probability measures (resp. ) on the real line with and (resp. and ), is equal to minus the convex hull of which has already been discussed after Theorem 2.5 and can be computed by Andrew’s monotone chain algorithm. One then may compute the probability measure which writes with , and denoting the differences between the successive elements of the increasing reordering of .

Let such that and be arbitrary approximations of and . The probability measure (or any minimizing probability measure when uniqueness is not shown) satisfies

| (4.1) |

We proceed like in the proof of Proposition 3.1. Let (resp. ) be a Markov kernel such that (resp. ) is an optimal transport plan for (resp. ) and be a martingale kernel such that . We obviously have . By Jensen inequality and using the martingale property of , we have , so that

We get (4.1) using Minkowski’s inequality and the triangle inequality . In the multi-marginal case, defining inductively and for , as the projection of on , we deduce that for ,

Despite all these interesting properties that we summarize in the next proposition, the measure(s) do(es) not seem easy to be calculated numerically, even for . In fact, the constraint of the convex order is not simple to handle in a minimization program. More precisely, in the case of empirical measures, one would have to minimize under the constraint . Even in dimension 1, this constraint is not linear since it is equivalent to , , , and for any , see e.g. Corollary 2.2 in [1]. This is why we mostly focus on that leads to a clear implementation of a quadratic problem with linear constraints.

Theorem 4.1.

For , if , then is attained by some probability measure which is unique when is absolutely continuous with respect to the Lebesgue measure or . If , then there is a probability such that for all , where denotes the concave hull of the function . Moreover, for each such that . Last, if and , then

Comparing and leads to interesting properties.

Corollary 4.2.

For , , we have

and there is a measurable transport map such that the only optimal transport plan between and is . Moreover, for any martingale kernel such that , a.e., . Last, in dimension , when , we also have for all , where is the left-hand derivative of the convex hull of the function .

Proof.

Since , we may replace by in Proposition 3.1 to get . Using that to replace by in Theorem 4.1, we obtain the converse inequality.

Now, let , denote a martingale kernel such that and a Markov kernel such that is an optimal transport plan for . Repeating the arguments of Proposition 3.1 (replacing again by ), we get

The equality in the last inequality ensures that a.e., where . Moreover, the equality in the second inequality implies that a.e., .

If is another Markov kernel such that is an optimal transport plan for , then is also an optimal transport plan and a.e., is a Dirac mass so that .

In dimension , we observe that

| (4.2) |

Thus, we have and for , which gives the claim. ∎

The property , a.e., in Corollary 4.2 indicates that in dimension 1, an optimal transport map between and should be piecewise affine with slope 1 on the irreducible components of introduced in Theorem A.4 [8], provided that we can find a martingale kernel that spans the whole components. This is indeed the case according to the following proposition which moreover exhibits a common optimal transport map for and .

Proposition 4.3.

Let , . Let , , (resp. , ) be the irreducible components of (resp. ). Then, we have and , up to a renumbering of .

Let be the convex hull of the function . Then, the function defined by

is an optimal transport map for and .

Proof.

We set and . From (4.2) and Lemma A.8 below which characterizes the irreducible components in terms of the quantile functions, we get

which gives the first claim. From the second equality and since is the convex hull of , we get

| (4.3) |

and for . From (4.2), this gives

| (4.4) |

Any point in is the limit of an increasing sequence of points in . Since, by (4.2) and (4.3), and , the left-continuity of the quantile functions implies that and . We deduce that

| (4.5) |

By Corollary 4.2, there exists an optimal transport map between and . By Proposition 2.17 in [25], we have -a.e. . For such that , since is constant (equal to ) on , we deduce that the left-continuous function is also constant on this interval. Let now . By definition of the irreducible components, we have

| (4.6) |

If , is constant and equal to on the interval and, by definition of , and are equal on this interval.

We are now going to prove that a.e., , which, by Proposition 2.17 in [25], ensures that is an optimal transport map between and .

If then and with the right-hand side equal to by (4.4) since, by (4.6),

By the above reasoning for , the equality between and still holds on .

If , then or . We deduce that for , and . The right-hand side is equal to when since then and otherwise when since, then, the interval on which is constant contains .

In conclusion for outside the at most countable set and therefore a.e..

5. Numerical experiments

5.1. Wasserstein distance

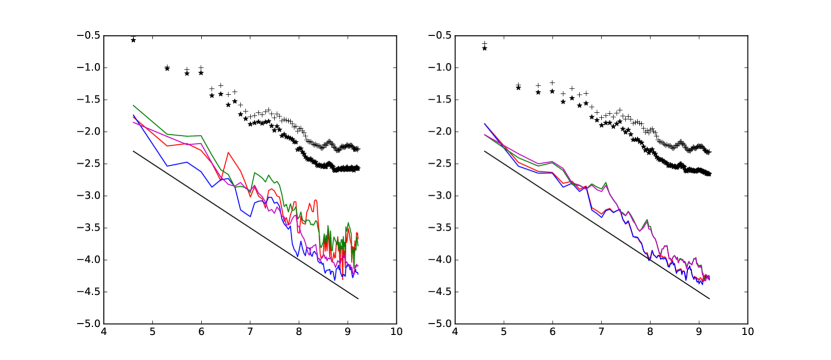

We start by illustrating numerically the convergences obtained in Proposition 3.2, and deduced from Theorem 4.1. We present on an example the convergence of the Wasserstein projection (resp. ) toward (resp. ) for the Wasserstein distance when and are the respective empirical measures of and with . To do so we consider an example in dimension one with , so that the projections can be calculated explicitly according to Theorems 2.5 and 4.1. We take and . For , we consider independent samples and distributed respectively according to and . Then, we set , , , , and . Notice that, to define and , we took advantage of the knowledge of the common mean of and . This situation is usual in financial applications : discounted asset prices are martingales and their means are given by the present values. We calculate the Wasserstein projections and (resp. and ) and the -Wasserstein distance between each of these measures and (resp. ), as explained below.

As a comparison to these projections, we consider the respective approximations of and by and , where and are respectively defined as the infimum and the supremum of and for the decreasing convex order when and for the increasing convex order otherwise so that and . We also consider the approximations by and . These approximations can be calculated explicitly for probability measures with finite support (see [2] or [1]) and are natural alternatives to the Wasserstein projections in dimension 1.

The graph at left (resp. right) of Figure 1 illustrates the convergence of , , and (resp. , , and ) toward zero as . The corresponding curves are respectively in red, blue, green and magenta. The star (resp. cross) points indicate the upper bound for (left) and (right) (resp. (left) and (right)) given by Proposition 3.1 (resp.Theorem 4.1). As expected, the curves in blue and magenta are below these points. Let us mention that all these Wasserstein distances are calculated exactly by using the quantile function of the standard normal variable. For instance, if with , and for ,

Asymptotically, the measure (resp. ) seems to slightly better approximate (resp. ) than (resp. ). Nonetheless, all these measures seem to converge for the Wasserstein distance at a rate close to as indicated by the line in black with equation . This rate is better than the theoretical one stated in Proposition 3.2. In the right figure, we first observe that equalizing the means improves the approximations and reduces the Wasserstein distances (see the distances to the black lines). However, the rate of convergence is still roughly in . We also observe that there are only very small differences between using or (resp. or ).

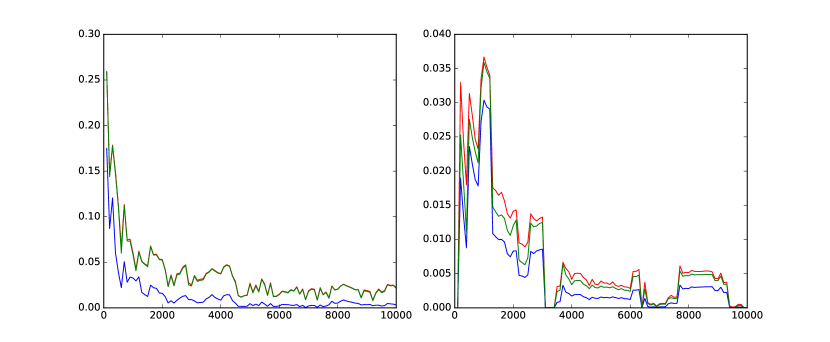

In Figure 2 are plotted at left (resp. right) the values of , , (resp. , , ) in function of . The corresponding curves are in red, blue and green. We observe that the values of and are very close. As expected, the blue curve is below the two other ones. At right, we observe that all the Wasserstein distances are equal to on our sample for , but take again positive values for larger values of . This shows that the value of from which we have , if it exists, depends on the sample and may be large.

Now, we conclude this section by checking the accuracy of the solver COIN-OR***https://www.coin-or.org/ for the quadratic optimization problem (1.1) with . In fact, in dimension 1, we know that can be calculated explicitly as described below Theorem 2.5. In Table 1, we calculate the Wasserstein distance between and the measure obtained by solving numerically (1.1) with COIN-OR for different sample sizes .

| 10 | 50 | 100 | 200 | 300 | |

|---|---|---|---|---|---|

| -Wasserstein distance |

As expected, the difference is very small. This validates numerically our theoretical results. More importantly, this indicates that the solver is reliable for finding the optimal solution with the values of that we have considered in this paper.

5.2. MOT problems in dimension 2 with two marginal laws.

An explicit example

Let and be respectively the uniform distributions on and . For and , we consider the minimization of the cost function , with . For any , we have . Jensen’s inequality gives

The equality condition in Jensen’s equality gives that , -almost surely. Now, let us consider be distributed according to and a couple of independent Rademacher random variables which is independent of . Then is distributed according to and satisfies . The probability distribution of is the unique martingale optimal coupling that minimizes . Indeed, if is distributed according to an optimal coupling, then and follow the Rademacher distribution, and both these random variables are necessarily independent of in order to satisfy the martingale property. Last, and are necessarily independent, otherwise would not follow .

We now illustrate the MOT and consider independent samples and respectively distributed according to and . We set and , with and . We work with and rather than with the empirical measures and since we have noticed on our experiments that they better approximate and (see Figure 1) and give better results for the approximation of MOT problems (see [2]). Let us mention here that in financial applications, it is generally possible to calculate and from the empirical measures and since the mean of and is given by the current price of the underlying assets. To calculate , we have to solve the quadratic optimization problem with linear constraints described in equation (1.1) for . The dimension of the problem is thus equal to . We have used the COIN-OR solver in our numerical experiments, which enables us to solve (1.1) for up to . Once is calculated, we can then solve the discrete MOT problem between and .

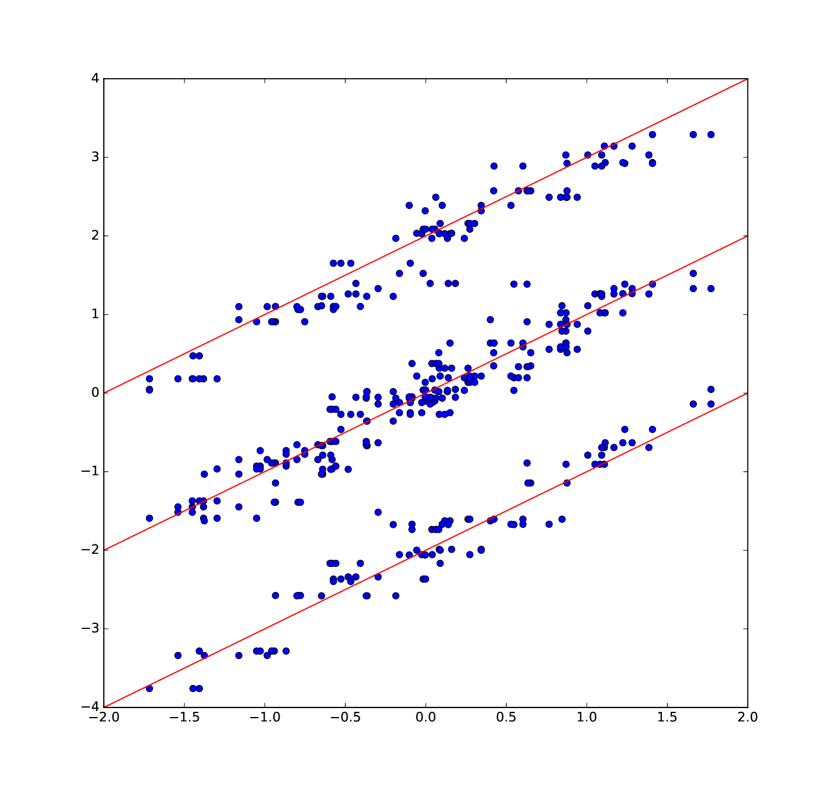

In Figure 3, for , we have plotted in function of for the points with positive probability in the MOT for . We recall that the optimal coupling for the continuous MOT is given by with and , being a couple of independent Rademacher random variables. Since and takes values in , we expect to observe that the points are gathered around the lines , and , which is the case on Figure 3. This checks our implementation of the algorithm. Besides, we have calculated on independent runs the value of the discrete MOT for with : the average is equal to and the standard deviation is equal to , which gives as confidence interval, which approximates well the value of the continuous MOT.

Model-free bounds on a best-of option

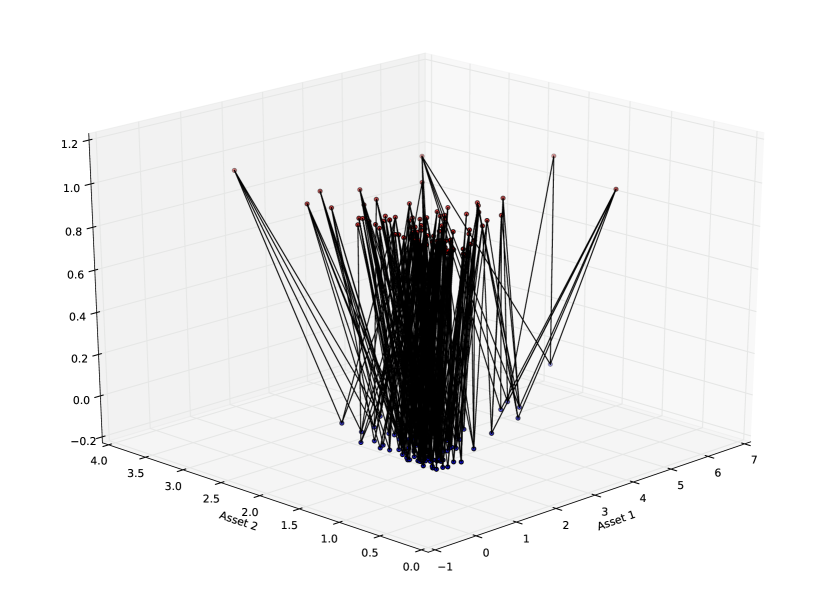

Let be a centered Gaussian vector with covariance matrix . We denote by the law of with for , and by the law of with . In the financial context, this choice of marginal laws is usual and corresponds to a two-dimensional Black-Scholes model: is the price of two assets at time and is the price of these assets at time . We are interested in an option that pays , i.e. the best arithmetic performance of the two assets, if positive. The price of this option in the Black-Scholes model can easily be calculated by using a Monte-Carlo algorithm.

Let and denote independent samples respectively distributed according to and . We set and , with , , and . We calculate numerically by using again the quadratic optimization solver COIN-OR, and then solve the discrete MOT problem between and .

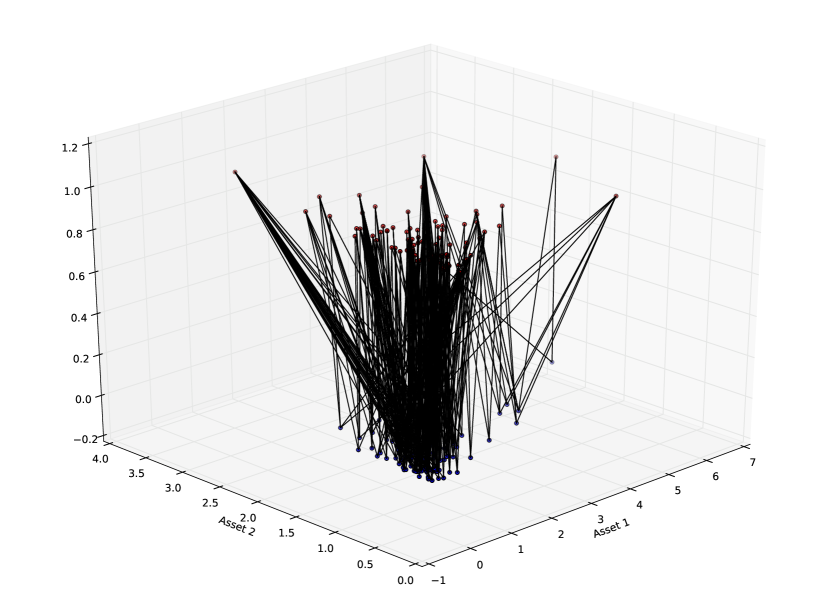

We now turn to our example illustrated in Figure 4. We have considered the following covariance matrix . With this choice, the Black-Scholes price of the option is approximately equal to . With , we have calculated on independent runs the value of the minimization and the maximization programs, and then computed the mean values. We have thus obtained for the lower bound price and for the upper bound price. The corresponding standard variations are respectively and , which makes 95% confidence intervals with half lengths and . In Figure 4, we have plotted the discrete MOT on the same sample for the minimization and the maximization problem. Precisely, we have plotted the points , in the hyperplane and the points in the hyperplane . The edges between the points and indicate that the optimal coupling gives a positive weight to the corresponding transitions. The difference between the two optimal couplings is clear. We can heuristically explain the graphs as follows. The cost function will anyway be positive for a large increase of one of the two assets. Therefore, to minimize the cost, one has to gather the large increases of Asset and Asset . Instead, to maximize the cost, it is better to gather an increase of one asset with a decrease of the other one.

The CPU time needed for the computation of the Wasserstein projection and for the linear programming problem is reported in Table 2. The dimension rows of the table correspond to the MOT problem between the laws of and for the cost function . What mainly influences the computation time is the dimension in which the optimal matrix has to be found. The dimension of the underlying space of the probability measures has a low impact on the computation time for the quadratic problem (1.1), since the number of equality constraints does not change with . Instead, it has some impact on the linear programming problem (1.3), since the number of equality constraints increases with . Nonetheless, since the resolution of the linear problem is much less time consuming than the resolution of the quadratic problem, the impact of the dimension on the overall computation time is rather mild.

5.3. Further directions

In view of Propositions 3.1 and 3.2, it would be nice to prove the stability of

with respect to and in for the weak convergence topology or the Wasserstein distance. On our numerical example of Figure 3 where the continuous MOT is explicit, the convergence of the discrete optimal cost towards the continuous one seems to hold. We plan to investigate this property in a future work. Note that for cost functions satisfying the so-called Spence-Mirrlees condition (see [17]), the stability of left-curtain couplings obtained by Juillet [18] is an important step in that direction.

To overcome the sample size limitation for the linear programming solvers to compute the solution of problem (1.3), one can contemplate introducing an entropic regularization of this problem similar to the one proposed by Benamou et al. [9] for discrete optimal transport. For and , the regularized problem is the minimization of

under the constraints and for . Since the constraints are affine, this problem can be solved by the iterative Bregman projections presented in [9]. In particular the solution is obtained by iterating successive entropic projections on the first marginal law constraints, on the second marginal law constraints and on the martingale constraints. The two first projections are explicit (see for instance Proposition 1 [9]). The entropic projection on the martingale constraints can be computed using the generalized iterative scaling algorithm introduced by Darroch and Ratcliff [10]. Such an approach combined with a relaxation of the martingale constraint has been recently investigated by Guo and Oblòj [16].

Appendix A Technical lemmas

Lemma A.1.

Let . Then, we have if, and only if,

Proof.

Let be a convex function. We define the Legendre-Fenchel transform of and have

The function is a convex lower semicontinuous function. Therefore, for any , there exists with Euclidean norm and . There exists such that for , otherwise we would have and then . We set and have for

Thus, is with affine growth and therefore . By the monotone convergence theorem the integrals (resp. ) converge to (resp. ) as . We conclude that . ∎

Lemma A.2.

Let be two convex functions and denote the convex hull of . Then is convex.

Proof.

Let and . If , then, using the convexity of , then the fact that is bounded from above by for the two inequalities, we obtain that

| (A.1) |

Otherwise, is affine on some interval with , and . If , then replacing by in (A.1), we get so that . In a symmetric way, . Hence,

By convexity of and the affine property of on the interval containing , the left-hand side is not smaller than . ∎

Lemma A.3.

Let be a non-decreasing function and denote the probability distribution of for uniformly distributed on . Then and the quantile function coincide away from the at most countable set of their common discontinuities and even everywhere on if is moreover left-continuous.

Proof.

The random variables and are both distributed according to . Hence for , so that . By symmetry, with the supremum equal to by left-continuity and monotonicity of . Hence with the supremum equal to when is left-continuous. ∎

Lemma A.4.

For , any non empty subset of has an infimum for the convex order. Moreover for all , .

Proof.

The existence of the infimum is given by Kertz and Rösler [20] p162. These authors work with the characterization of the convex order in terms of the cumulative distribution functions. By the more convenient characterization in terms of the quantile functions recalled in (2.2), it is enough to check that for all , for some probability measure such that . For , and for all , . Therefore for all , , and . The function being concave on as the infimum of concave functions it is continuous on . Since for , , is continuous at and and therefore on . Denoting its left-hand derivative by , one has and for all , with non-decreasing. One concludes by defining as the image of the Lebesgue measure on by . ∎

Lemma A.5.

Let and . Then

| (A.2) |

Besides, when is absolutely continuous with respect to the Lebesgue measure or and has no atom, equality holds if and only if . Last, when , the statements remain valid with replaced by the distribution of with uniformly distributed on .

Proof.

Let . For , there exists an optimal probability measure that satisfies . Since , we have

| (A.3) |

We now suppose that is absolutely continuous with respect to the Lebesgue measure. We know by Theorem 6.2.4 in [4] that the probability measure satisfying is unique, and writes for some Borel map . If (A.2) is an equality, then the inequality in (A.3) is also an equality and, by uniqueness, . Hence , which gives , -a.e., and implies .

Lemma A.6.

Let and . The function is non-decreasing.

Proof.

It is enough to check that for such that is not non-decreasing then (indeed is non-decreasing and ). By Proposition 2.17 [25] and the definition of ,

where denotes the left-hand derivative of the concave hull of . Since , where the right-hand side is a concave function of , and . Now either and coincide on and is non-decreasing or the open set is non empty and writes as the at most countable union of disjoint intervals with , , and affine on . For each in the non empty set , for all , so that, by Jensen’s inequality,

| (A.4) |

For , either is equal to on a left-hand neighbourhood of or there is an accumulation of intervals at the left of with a sequence of distinct elements of , for all and . For in the left-hand neighbourhood of in the first case and in in the second one, . By the left-continuity of and the definition of , one concludes that . Therefore which combined with (A.4) and Proposition 2.17 [25] leads to when and do not coincide on . ∎

Remark A.7.

Lemma 2.6 can be proved by similar arguments. But to exhibit with and non-increasing when is such that is not non-increasing, we chose a more elementary transformation exploiting directly the lack of monotonicity in place of .

Lemma A.8.

Let be two distinct probability measures such that and , be the irreducible components of . Then, we have

Proof.

For , let for , for and for . One has for all and , is the countable family of disjoint intervals such that

| (A.5) |

Since and are the antiderivatives of two reciprocal non-decreasing functions, it is well known they are the Legendre-Fenchel transforms of each other i.e. . In fact, for , if then for , if then for and if then for . We deduce that and

| (A.6) |

Therefore, we have

Hence

| (A.7) |

Now, we observe that and, for such that , is affine for . Using the convexity of , we get

If , we have by using that is the Legendre transform of . Similarly, , and we get

By (A.6), if , . Since and the Legendre transform of is not greater than , we deduce that . In the same way, if , then so that

| (A.8) |

Now, (A.5) implies that . If , we necessarily have , and for , we have and since is right-continuous. Therefore, we have and thus for . Similarly, we show that for , which, with (A.7) and (A.8), gives the claim. ∎

References

- [1] Aurélien Alfonsi, Jacopo Corbetta, and Benjamin Jourdain. Sampling of probability measures in the convex order and approximation of Martingale Optimal Transport problems. ArXiv eprint 1709.05287, 2017.

- [2] Aurélien Alfonsi, Jacopo Corbetta, and Benjamin Jourdain. Sampling of one-dimensional probability measures in the convex order and computation of robust option price bounds probability measures in the convex order and computation of robust option prices bounds. To be published in the International Journal of Theoretical and Applied Finance, 22, 2019.

- [3] Jean-Jacques Alibert, Guy Bouchitté, and Thierry Champion. A new class of cost for optimal transport planning. Preprint hal-01741688, March 2018.

- [4] Luigi Ambrosio, Nicola Gigli, and Giuseppe Savaré. Gradient flows in metric spaces and in the space of probability measures. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2005.

- [5] Julio Backhoff Veraguas, Mathias Beiglböck, and Gudmun Pammer. Existence and Cyclical monotonicity for weak transport costs. ArXiv e-print 1809.05893, September 2018.

- [6] David Baker. Martingales with specified marginals. Theses, Université Pierre et Marie Curie - Paris VI, December 2012.

- [7] Mathias Beiglböck, Pierre Henry-Labordère, and Friedrich Penkner. Model-independent bounds for option prices—a mass transport approach. Finance Stoch., 17(3):477–501, 2013.

- [8] Mathias Beiglböck and Nicolas Juillet. On a problem of optimal transport under marginal martingale constraints. Ann. Probab., 44(1):42–106, 2016.

- [9] Jean-David Benamou, Guillaume Carlier, Marco Cuturi, Luca Nenna, and Gabriel Peyré. Iterative Bregman projections for regularized transportation problems. SIAM J. Sci. Comput., 37(2):A1111–A1138, 2015.

- [10] J. N. Darroch and D. Ratcliff. Generalized iterative scaling for log-linear models. Ann. Math. Statist., 43:1470–1480, 1972.

- [11] Claude Dellacherie and Paul-André Meyer. Probabilities and potential, volume 29 of North-Holland Mathematics Studies. North-Holland Publishing Co., Amsterdam-New York; North-Holland Publishing Co., Amsterdam-New York, 1978.

- [12] Nicolas Fournier and Arnaud Guillin. On the rate of convergence in Wasserstein distance of the empirical measure. Probab. Theory Related Fields, 162(3-4):707–738, 2015.

- [13] Nathael Gozlan and Nicolas Juillet. On a mixture of Brenier and Strassen theorems. ArXiv e-print 1808.02681, August 2018.

- [14] Nathael Gozlan, Cyril Roberto, Paul-Marie Samson, Yan Shu, and Prasad Tetali. Characterization of a class of weak transport-entropy inequalities on the line. Ann. Inst. Henri Poincaré Probab. Stat., 54(3):1667–1693, 2018.

- [15] Nathael Gozlan, Cyril Roberto, Paul-Marie Samson, and Prasad Tetali. Kantorovich duality for general transport costs and applications. Arxiv, 1412.7480v4, 2015.

- [16] Gaoyue Guo and Jan Oblòj. Computational Methods for Martingale Optimal Transport problems. arXiv e-prints, page arXiv:1710.07911, October 2017.

- [17] Pierre Henry-Labordère and Nizar Touzi. An explicit martingale version of the one-dimensional Brenier theorem. Finance Stoch., 20(3):635–668, 2016.

- [18] Nicolas Juillet. Stability of the shadow projection and the left-curtain coupling. Ann. Inst. Henri Poincaré Probab. Stat., 52(4):1823–1843, 2016.

- [19] Robert P. Kertz and Uwe Rösler. Stochastic and convex orders and lattices of probability measures, with a martingale interpretation. Israel J. Math., 77(1-2):129–164, 1992.

- [20] Robert P. Kertz and Uwe Rösler. Complete lattices of probability measures with applications to martingale theory. In Game theory, optimal stopping, probability and statistics, volume 35 of IMS Lecture Notes Monogr. Ser., pages 153–177. Inst. Math. Statist., Beachwood, OH, 2000.

- [21] Alfred Müller and Marco Scarsini. Stochastic order relations and lattices of probability measures. SIAM J. Optim., 16(4):1024–1043, 2006.

- [22] Gilles Pagès and Jacques Printems. Optimal quadratic quantization for numerics: the Gaussian case. Monte Carlo Methods Appl., 9(2):135–165, 2003.

- [23] Gilles Pagès and Benedikt Wilbertz. Intrinsic stationarity for vector quantization: foundation of dual quantization. SIAM J. Numer. Anal., 50(2):747–780, 2012.

- [24] David Pollard. A user’s guide to measure theoretic probability, volume 8 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2002.

- [25] Filippo Santambrogio. Optimal transport for applied mathematicians. Progress in Nonlinear Differential Equations and their Applications, 87. Birkhäuser/Springer, 2015.

- [26] Moshe Shaked and J. George Shanthikumar. Stochastic orders. Springer Series in Statistics. Springer, New York, 2007.

- [27] Volker Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36:423–439, 1965.