Nonnegative matrix factorization with side information for time series recovery and prediction

Abstract

Motivated by the reconstruction and the prediction of electricity consumption, we extend Nonnegative Matrix Factorization (NMF) to take into account side information (column or row features). We consider general linear measurement settings, and propose a framework which models non-linear relationships between features and the response variables. We extend previous theoretical results to obtain a sufficient condition on the identifiability of the NMF in this setting. Based the classical Hierarchical Alternating Least Squares (HALS) algorithm, we propose a new algorithm (HALSX, or Hierarchical Alternating Least Squares with eXogeneous variables) which estimates the factorization model. The algorithm is validated on both simulated and real electricity consumption datasets as well as a recommendation dataset, to show its performance in matrix recovery and prediction for new rows and columns.

1 Introduction

In recent years, a large number of methods have been developed to improve matrix completion methods using side information [1, 2, 3]. By including features linked to the row and/or columns of a matrix, also called “side information”, these methods have a better performance at estimating the missing entries.

In this work, we generalize this idea to nonnegative matrix factorization (NMF, [4]). Although more difficult to identify, NMF often has a better empirical performance, and provides factors that are more interpretable in an appropriate context. We propose an NMF method that takes into account side information. Given some observations of a matrix, this method jointly estimates the nonnegative factors of the matrix, and regression models of these factors on the side information. This allows us to improve the matrix recovery performance of NMF. Moreover, using the regression models, we can predict the value of interest for new rows and columns that are previously unseen. We develop this method in the general matrix recovery context, where linear measurements are observed instead of matrix entries.

This choice is especially motivated by applications in electricity consumption. We are interested in estimating and predicting the electricity load from temporal aggregates. In the context of load balancing in the power market, electric transmission system operators (TSO) of the electricity network are typically legally bound to estimate the electricity consumption and production at a small temporal scale (half-hourly or hourly), for market participants within their perimeter, i.e. utility providers, traders, large consumers, groups of consumers, etc. [5]. Most traditional electricity meters do not provide information at such a fine temporal scale. Although smart meters can record consumption locally every minute, the usage of such data can be extremely constrained for TSOs, because of the high cost of data transmission and processing and/or privacy issues. Nowadays, TSOs often use regulator-approved proportional consumption profiles to estimate market participants’ load. In a previous work by the authors [5], we proposed to solve the estimation problem by NMF using temporal aggregate data.

Using the method developed in this article, we put in parallel temporal aggregate data with features that are known to have a correlation with electricity consumption, such as the temperature, the day of the week, or the type of client. This not only improves the performance of load estimation, but also allows us to predict future load for users in the dataset, and estimate and predict the consumption of new users previously unseen. In electrical power networks, load prediction for new periods is useful for balancing offer-demand on the network, and prediction for new individuals is useful for network planning.

In the rest of this section, we introduce the general framework of this method, and the related literature. In Section 2, we deduce a sufficient condition on the side information for the NMF to be unique. In Section 3, we present HALSX, an algorithm which solves the NMF with side information problem, that we prove to converge to stationary points. In Section 4, we present experimental results, applying HALSX on simulated and real datasets, both for the electricity consumption application, and for a standard task in collaborative filtering.

1.1 General model definition

We are interested in reconstructing a nonnegative matrix , from linear measurements,

| (1) |

where is a linear operator. Formally, can be represented by , …, , design matrices of dimension , and each linear measurement can be represented by

| (2) |

The design matrices , …, are called masks.

Moreover, we suppose that the matrix of interest, , stems from a generative low-rank nonnegative model, in the following sense:

-

1.

The matrix is of nonnegative rank , with . This means, is the smallest number so that we can find two nonnegative matrices and satisfying

Note that this implies that is of rank at most , and therefore is of low rank.

-

2.

There are some row features and column features connected to each row and column of . We note by the -th row of , and by the -th row of . There are two link functions and , so that

where is the matrix obtained by stacking row vectors , for (idem for ), and is the ramp function which corresponds to thresholding operation at 0 for any matrix or vector.

In this general setting, the features and , the measurement operator , and the measurements are observed. The objective is to estimate the true matrix as well as the factor matrices and , by estimating the link functions and .

To obtain a solution to this matrix recovery problem, we minimize the quadratic error of the matrix factorization. In Section 3, we will propose an algorithm for the following optimization problem:

| (3) | ||||

| s.t. |

where and are some functional spaces in which the row and column link functions are to be searched.

By specializing , , and , or restricting the search space of and , this general model includes a number of interesting applications, old and new.

The masks , …,

-

•

Complete observation: , where is the -th canonical vector. This means every entry of is observed.

-

•

Matrix completion: the set of masks is a subset of complete observation masks, with .

-

•

Matrix sensing: the design matrices are random matrices, sampled from a certain probability distribution. Typically, the probability distribution needs to verify certain conditions, so that with a large probability, verifies the Restricted Isometry Property [6].

-

•

Rank-one projections [7, 8]: the design matrices are random rank-one matrices, that is , where and are respectively random vectors of dimension and . The main advantage to this setting is that much less memory is needed to store the masks, since we can store the vectors and (dimension-) instead of (dimension-). In [7, 8], theoretical properties are proved for the case where and are vectors with independent Gaussian entries and/or drawn uniformly from the vectors of the canonical basis.

-

•

Temporal aggregate measurements: in this case, the matrix is composed of time series concerning individuals, and each measure is a temporal aggregate of the time series of an individual. The design matrices are defined as , where is the individual concerned by the -th measure, the first period covered by the measure, and the number of periods covered by the measure.

The features and

-

•

Individual features: . Basically, no side information is available. The row individuals and column individuals are each different.

-

•

General numeric features: and . This includes all numeric features.

-

•

Features generated from a kernel: certain information about the row and column individuals may not be in the form of a numeric vector. For example, if the row individuals are vertices of a graph, their connection to each other is interesting information for the problem, but it is difficult to encode as real vectors. In this case, features can be generated through a transformation, or by defining a kernel function.

The link functions and

-

•

Linear: , and . In this case, we need to estimate and to fit the model. With identity matrices as row and column features, this case is reduced to the traditional matrix factorization model with

When the features are generated from a kernel function, even a linear link function permits non-linear relationship between the features and the factor matrices.

-

•

General regression models: when the relationship between the features and the variable of interest is not linear, any off-the-shelf regression methods can be plugged in to search for a non-linear link function.

The choice of the optimization problem (3)

Notice that with individual row and column features, linear link functions and complete observations, (3) becomes

| (4) |

This is equivalent to the classical NMF problem,

| (5) | ||||

| s.t. |

in the sense that for any solution to (4), is a solution to (5).

A more immediate generalization of (5) to include exogenous variables would be in the form

| (6) | ||||

| s.t. | ||||

Solving (6) would involve identifying the subset of and that only produce nonnegative value on the row and column features, which could be difficult.

| Link function | Linear | Other regression methods | |||

|---|---|---|---|---|---|

| Features | Identity | General numeric features | Kernel features | General numeric features | |

| Mask | Identity | Matrix factorization | Reduced-regression rank [9, 10, 11] | Multiple kernel learning [12] | Nonparametric RRR [13] |

| Matrix completion | Matrix completion [14] | IMC[15, 1, 16, 17] | GRMF [18, 2, 3] | ||

| Rank-one projections | [7, 8] | ||||

| Temporal aggregates | [5] | ||||

| General masks | Matrix recovery [19, 6] | ||||

By using (3), we actually shifted the search space and to and which consists of composing all functions of and with the ramp function (thresholding at 0). In a word, (3) is equivalent to

| (7) | ||||

| s.t. |

Problem (7) also helps us to reason on the identifiability of (3). In a sense, (3) is not well-identified: two distinct elements in have the same evaluation value of the objective function, if they only differ on their negative parts. In fact, this does not affect the interpretation of the model, because these distinct elements correspond to the same element in . Since we are only going to use the positive parts of the function both in recovery and prediction, this becomes a parameterization choice which has no consequence on the applications.

As a comparison, we also propose an algorithm for the following optimization problem in Section 3:

| (8) |

Instead of minimizing the low-rank approximation error for a matrix that matches the data as a linear matrix equation in (3), (8) minimizes the sampling error of an exactly low-rank matrix. Both have been studied in the literature. For example, objective functions similar to (3) have been considered in [6], and ones similar to (8) in [20]. We will see in both Sections 3 and 4 that (3) has a better performance than (8).

1.2 Prior works

Table 1 shows a taxonomy of matrix factorization models with side information, by the mask, the link function and the features used as side information. A number of problems in this taxonomy has been addressed in established literature.

There is an abundant literature that studies the general matrix factorization problem under various measurement operators, when no additional information is provided (see [21, 14, 6, 8] for various masks considered, and [22] for a recent global convergence result with RIP measurements). The NMF with general linear measurements is studied in various applications [20, 23, 5].

On the other hand, with complete observations, the multiple regression problem taking into account the low-rank structure of the (multi-dimensional) variable of interest is known as reduced-rank regression. This approach was first developed very early (see [9] for a review). Recent developments on rank selection [10], adaptive estimation procedures [24], using non-parametric link function [13], often draw the parallel between reduced-rank regression and the matrix completion problem. However, measurement operators other than complete observations or matrix completion are rarely considered in this community.

Building on theoretical boundaries on matrix completion, the authors of [1, 16, 17] showed that by providing side information (the matrix ), the number of measurements needed for exact matrix completion can be reduced. Moreover, the number of measurements necessary for successful matrix completion can be quantified by measuring the quality of the side information [17].

Collaborative filtering with side information has received much attention from practitioners and academic researchers alike, for its huge impact in e-commerce and web applications [15, 1, 16, 17, 2, 3]. One of the first methods for including side information in collaborative filtering systems (matrix completion masks) was proposed by [18]. The authors generalized collaborative filtering into a operator estimation problem. This method allows more general feature spaces than a numerical matrix, by applying a kernel function to side information. [3] proposed choosing the kernel function based on the goal of the application. [12] applied the kernel-based collaborative filtering framework to electricity price forecasting. Their kernel choice is determined by multi-kernel learning methods.

To the best of our knowledge, matrix factorization (nonnegative or not) with side information, from general linear measurements has rarely been considered, nor is general non-linear functions other than with features obtained from kernels. This article aims at proposing a general approach which fills this gap.

2 Identifiability of nonnegative matrix factorization with side information

Matrix factorization is not a well-identified problem: for one pair of factors , with , any invertible matrix produces another pair of factors, , with . In order to address this identifiability problem, one has to introduce extra constraints on the factors.

When the nonnegativity constraint is imposed on and , however, it has been shown that sometimes the only invertible matrices that verify and are the composition of a permutation matrix and a diagonal matrix with strictly positive diagonal elements. A nonnegative matrix factorization is said to be “identified” if the factors are unique up to permutation and scaling. The identifiability conditions for NMF are a hard problem, because it turns out that NMF identifiability is equivalent to conditions that are computationally difficult to check. In this section, we review some known necessary and sufficient conditions for NMF identifiability in the literature, and develop a sufficient condition for NMF identifiability in the context of linear numerical features.

In order to simplify our theoretical analysis, we focus on the complete observation case in this section (every entry in is observed). Without loss of generality, we derive the sufficient condition for row features. That is, we will derive conditions on and , so that the nonnegative matrix factorization , with , is unique. A generalization to column features can be easily obtained. In this section, we assume that in addition to be of nonnegative rank , matrix is also exactly of rank .

2.1 Identifiability of NMF

The authors of [4] and [25] proposed two necessary and sufficient conditions for the factorization to be unique. Both conditions use the following geometric interpretation of NMF introduced by [4].

Since , the columns of are conical combinations of the columns in . Formally, , the conical hull of the columns of , is a polyhedral cone contained in the first orthant of . As is of rank , the rank of is also . This implies that the extreme rays (also called generators) of are exactly the columns of , which are linearly independent. is therefore

-

•

a simplicial cone of generators,

-

•

contained in ,

-

•

containing all columns of .

Inversely, if we take any cone verifying these three conditions, and define a matrix whose columns are the generators of , there will be a nonnegative matrix , so that . The uniqueness of NMF is therefore equivalent to the uniqueness of simplicial cones of generators contained in the first orthant of and containing all columns .

In [25], an equivalent geometric interpretation in is given in the following theorem:

Theorem 1.

[25] A -dimensional NMF of a rank- nonnegative matrix is unique if and only if the nonnegative orthant is the only simplicial cone with extreme rays satisfying

Despite the apparent simplicity of the theorem, the necessary and sufficient conditions are very difficult to check. Based on the theorem above, several sufficient conditions have been proposed. The most widely used condition is called the separability condition. Before introducing this condition (in its least restrictive version presented by [25]), we need the following two definitions.

Definition 1 (Separability).

Suppose . A nonnegative matrix is said to be separable if there is a -by- permutation matrix which verifies

where is a -by- diagonal matrix with only strictly positive coefficients on the diagonal and zeros everywhere else, and the -by- matrix is a collection of the other rows of .

Definition 2 (Strongly Boundary Closeness).

A nonnegative matrix is said to be strongly boundary close if the following conditions are satisfied.

-

1.

is boundary close: for all , there is a row in which satisfies ;

-

2.

There is a permutation of such that for all , there are rows in which satisfy

-

(a)

for all ;

-

(b)

the square matrix is of full rank .

-

(a)

Strongly boundary closeness demands, modulo a permutation in , that for each , there are rows of that have the following form,

| (9) | ||||

These row vectors, , all have 0 on the -th element, and its lower square matrix of is of full rank. There are therefore enough linearly independent points on each -dimensional facet , which shows that is somewhat maximal in .

The following was proved in [25]:

Theorem 2.

[25] If is strongly boundary close, then the only simplicial cone with generators in containing is . Moreover, if is separable, then is the unique NMF of up to permutation and scaling.

2.2 Identifiability with side information

The NMF with linear row features, , is said to be unique, if for all matrix pairs that verifies

we have up to permutation of columns and scaling.

For a given full-rank matrix , consider the following two sets of matrices:

Theorem 3.

If , and , and is separable, then the factorization is unique.

Proof.

Notice that for , the nonnegative matrix is strongly boundary close. The factorization is therefore unique. The model identifiability follows immediately, since is of full rank. ∎

Example of that verifies

For this theorem to have practical consequences, one needs to find appropriate row features so that .

Here we provide a family of matrices so that .

With a fixed , suppose that has columns, and at least rows, with the first rows defined as the following:

-

•

the first row and column have 0 on the first entry and positive entries elsewhere;

-

•

for , has strictly positive entries on the first columns, from Row to Row , and zero entries everywhere else. These rows are linearly independent.

Then we have , because the following -by- matrix is in this set:

-

•

for , has consecutive strictly positive entries on the -th column, between Row and Row .

The following matrices instantiate the case of :

If , for any invertible matrix , .

3 HALSX algorithm

In this section, we propose Hierarchical Alternating Least Squares with eXogeneous variables (HALSX), a general algorithm to estimate the nonnegative matrix factorization problem with side information, from linear measurement, by solving (3). It is an extension to a popular NMF algorithm: Hierarchical Alternating Least Squares (HALS) (see [26, 27]).

Before discussing HALSX, we will first present a result on the local convergence of Gauss-Seidel algorithms. This result guarantees that any legitimate limiting points generated by HALSX are critical points of (3).

While presenting specific methods to estimate link functions, we will only discuss row features, as a generalization to column features is immediate.

3.1 Relaxation of convexity assumption for the convergence of Gauss-Seidel algorithm

To show the local convergence of HALSX algorithm, we first extend a classical result concerning block nonlinear Gauss-Seidel algorithm [28, Proposition 4].

Consider the minimization problem,

| (10) | ||||

| s.t. |

where is a continuously differentiable real-valued function, and the feasible set is the Cartesian product of closed, nonempty and convex subsets , for , with . Suppose that the global minimum is reached at a point in . The -block Gauss-Seidel algorithm is defined as Algorithm 1.

Define formally the notion of component-wise quasi-convexity.

Definition 3.

Let . The function is quasi-convex with respect to the -th component on if for every and , we have

for all . is said to be strictly quasi-convex with respect to the -th component, if with the additional assumption that , we have

for all .

It has been shown that if is strictly quasi-convex with respect to the first blocks of components on , then a limiting point produced by a Gauss-Seidel algorithm is a critical point [28].

This result is not directly applicable for the HALS algorithm. Typically, if , the column of , is identically zero, the loss function is completely flat respect to , the -th column of . Therefore the loss function is not strictly quasi-convex. In order to avoid this scenario, [27] suggests thresholding at a small positive number instead of at 0, when updating each column of the factor matrices.

In fact the convexity assumption of [28] can be slightly relaxed to directly apply to HALS, as demonstrated by the following proposition.

Theorem 4.

Suppose that the function is quasi-convex with respect to on , for . Suppose that some limit points of the sequence verify that is strictly quasi-convex with respect to on the product set , for . Then every such limiting point is a critical point of Problem (1).

Compared to the result of [28], this shows that the strict convexity with respect to one block does not have to hold universally for feasible regions of other blocks. It only needs to hold at the limiting point.

This theorem can be established following the proof of Proposition 5 of [28], using the following lemma.

Lemma 5.

Suppose that the function is quasi-convex with respect to on , for some . Suppose that some limit points of verify that is strictly quasi-convex with respect to on . Let be a sequence of vectors defined as follows:

Then, if , we have . That is .

Proof.

(The proof of the lemma is based on [29].)

Suppose on the contrary that does not converge to 0. Define . Restricting to a subsequence, we can obtain that Define . Notice that is of unit norm, and . Since is on the unit sphere, it has a converging subsequence. By restricting to a subsequence again, we could suppose that converges to .

For all , we have , which implies is on the segment . This segment has strictly positive dimension in the subspace corresponding to .

By the definition of , , for all , and for all . In particular,

By quasi-convexity of on ,

Taking the limit when converges to on both equalities, we obtain

In other words, , , which contradicts the strict quasi-convexity of on . ∎

3.2 HALSX algorithm

To solve (3), we propose HALSX (Algorithm 2). When complete observations are available, the feature matrices are identity matrices, and when only linear functions are allowed as link functions, Algorithm 2 is equivalent to HALS [26].

From Theorem 4, one deduces that every full-rank limiting point produced by the popular HALS algorithm is a critical point.

In this algorithm, at each elementary update step, we first look for a link function which minimizes the quadratic error, without concerning ourselves with its nonnegativity. The obtained evaluation of the minimizer function is then thresholded at to update the factors.

To show the convergence of HALSX algorithm, we need to assure that for some functional spaces and , such an update solves a corresponding subproblem of (3). To do this, we will use the following proposition:

Proposition 6.

Suppose that , are not identically equal to zero, and , with , is a convex differentiable function. Suppose

If , the Jacobian matrix of at , is of rank , then is also a solution to

| (11) |

Proof.

Take , not identically equal to zero. We will note by the loss function, so that for all . The function is convex.

Problem (11), which can be rewritten as

is also convex. The subgradient of the composition function at is simply obtained by multiplying , the Jacobian matrix of at , to each element of , or . Therefore , is a minimizer of (11), if and only if .

Since

is a minimizer of a smooth convex problem,

This means , because is of full rank. Consequently

It has been shown in NMF literature (for example [27, Theorem 2]) that,

This is equivalent to

or

We therefore conclude with . ∎

In many regression methods, even when a non-linear transformation is applied to the data, the regression function is linear in its parameters. A non-exhaustive list of methods include linear regression , spline regression , or support vector regression (SVR) . In this case, has a constant Jacobian matrix. In the case of linear and spline regression, the Jacobian matrix is of rank if there are no less features than examples. For SVR, this is true for any positive definite kernels. This allows us to apply the previous lemma to each column update step of Algorithm 2. By calculating at Step for Column in , we actually have

This shows that at each iteration, we solve the subproblems of (3).

In these cases, by rewriting the functional space and in a parametric form, the search space is actually and , for some and .

Proposition 7.

Remark.

In order to extend this convergence result for Problem (6), one would need to ensure the obtained functions have non-negative values on the features. This could be done by alternating projection.

3.3 Designs and HALSX

At each iteration of Algorithm 2, we need to project the working matrix into the convex polytope defined by the measurements and nonnegativity:

| (12) |

In general, the polytope projection can be obtained by alternating projection. Namely, we can alternate between:

-

•

;

-

•

,

where is the right pseudo-inverse of , viewed as an -by- matrix.

3.4 Linear HALSX

In this section, we consider HALSX with numeric row features and linear row link functions. That is, given and , we need to solve

| (13) | ||||

| s.t. |

Following Algorithm 2, we need to update the columns of at each iteration. At the -th step, for , we solve the subproblem

where This minimization problem has a closed-form solution:

In order to accelerate the numerical algorithm, a QR decomposition of is done before the iterations, where is an orthogonal matrix, and is a square upper triangular matrix. When is of full rank, is invertible. We compute one time before the iterations, and use the result at each iteration.

Stopping criterion

As in classical NMF algorithms, we will use the Karush–Kuhn–Tucker conditions (KKT) to provide a stopping criterion. The KKT conditions of (13) are,

where is the entry-wise product (Hadamard product) for of the same dimension, and is the subgradient of the function at point , with respect to the variable . Note that and are always satisfied at the end of an iteration.

As and are respectively in the subgradient with respect to and , we will stop the algorithm when the norm of following vector

is smaller than times its initial value, with a small . For the algorithms presented in the next sections, this stopping criterion is generalized quite easily.

3.5 HALSX with smoothing splines

The computation considered above can estimate an NMF with linear features fairly efficiently. However, in real applications, linear link functions are too restrictive. In the following, we will estimate non-linear link functions that are Generalized Additive Models (GAM, [30]).

A Generalized Additive Model is a generalization to Generalized Linear Model (GLM) which includes additive non-linear components. Consider observations , for , where is the vector of features, and is an observation of a random variable . Suppose that , where are independent identically distributed zero-mean Gaussian variables, and has the following relationship to the features:

where is the vector of parametric model components, is a known, monotonic, twice-differentiable function, , , …, are the non-linear functions to be estimated.

We note by the matrix grouping the features of all observations. We use penalized regression spline to fit the GAMs. For , define a spline basis in which , the -th component of the GAM, is to be estimated. Practically, we search for is the -dimensional vector space

Noting by the design matrix, for , an element of the functional space, we have

The whole model of , can then be represented linearly:

The dimension of , , controls the the smoothness of the functions to be estimated. As little information is available on the degree of smoothness of the functions, we use a rather large , and add a penalty on the wiggliness, , as in [30]. The least squares estimator of this model is therefore

where is the penalization parameter of the -th non-linear component, and is a positive definite matrix depending on and . The penalization parameter, , is chosen by a generalized cross validation criterion.

HALSX-GAM

At each iteration of the algorithm, for , we re-estimate the link function of the -th column of as a GAM.

The subproblem for is the following

| (14) | ||||

With fixed penalization parameters …, the optimization above can be solved by

In practice, we use the GAM estimation routines implemented in the R package mgcv [30] to choose the penalization parameter and estimate the model at the same time.

3.6 HALSX with other regression models

We can replicate the strategy above to work with other regression models. As mentioned before, the convergence to critical point is guaranteed, as long as the regression model estimation can be re-parameterized to verify the conditions of Proposition 6. Using this strategy, many off-the-shelf algorithms for regression model training can be plugged in. In the experiments described in the next section, we use the predictive model API provided in the R package caret [31].

Meta-parameters in regression models

As in HALSX-GAM, we build the estimation of meta-parameters using cross validation as a part of the link function estimation step, can treat them indifferently as regular parameters.

3.7 An HALS-like algorithm for (8)

Before detailing Algorithm 3 which aims to solve (8), we will first develop the elemental HALS iteration in the context of (8) where no supplemental information is supplied for the factorization model, namely . Indeed, when updating one column of , the sub-problem becomes: how to solve ?

We will use the fact that for all ,

and for all , , the transpose of is defined by

Since

the first order optimality condition is therefore equivalent to

The left-hand side of the equation can be written as

which leads to the following symmetric -by- system on :

or

This computation generalizes to linear exogenous variables, with the optimality condition:

When the matrices to be inversed in the these equations are not invertible, we will use the generalized inverse instead.

Using these elementary steps, we propose Algorithm 3 to solve Problem (8). Compared to Algorithm 2, Algorithm 3

-

•

has one less block (the slack variable is not present);

-

•

checks the deviation with data more frequently;

-

•

each subproblem is more costly because of the presence of in the subproblem. As we will see in the detailed development of the computation, when , the sample size (the dimension of image of ) is large, each update involves rather costly computations.

Complexity

At each sub-iteration Algorithm 3, we need to calculate -by- or -by- matrices (), then inverse the sum of the these matrices. While the computation of the sum is map-reducible, on a single-threaded machine, this can be computationally expensive when is large. Each iteration of Algorithm 3 has a multiplicative complexity of , while each iteration of Algorithm 2 has a complexity of with general linear measurement operator. This difference in complexity can be very important when or is large.

4 Experiments

We use one synthetic dataset and three real datasets to evaluate the proposed methods.

-

•

Synthetic data: a rank-20 150-by-180 nonnegative matrix simulated following the generative model (Section 1.1), with and matrices with independent Gaussian entries, () is a function formed with a dimension-33 (44 for ) spline basis with random weights, truncated at 0 ().

-

•

French electricity consumption (proprietary dataset): daily consumption of 473 medium-voltage feeders gathering each around 1,500 consumers based near Lyon in France from 2010 to 2012. The first two years are used as training data ().

-

•

Portuguese electricity consumption [32] daily consumption of 370 Portuguese clients from 2010 to 2014 ().

-

•

MovieLens 100k [33] an anonymized public dataset with 100,000 movie scores for 1682 movies from 943 users (). Note that the data matrix is not complete. Error rates are calculated on the vector of available scores.

The following matrix recovery/completion methods are compared:

-

•

interpolation For temporal aggregates only: to recover the target matrix, temporal aggregates are distributed equally over the covered periods.

-

•

HALS, NeNMF, softImpute Matrix recovery/completion methods without side information.

The following regression methods are compared:

-

•

individual_gam Estimating separate GAMs on each individual or period, on the matrix obtained from interpolation or on the whole data matrix when it is available.

-

•

factor_gam Estimating GAMs on the factors obtained by HALS or NeNMF.

-

•

rrr [34] Applying reduced-rank regression on the matrix obtained from interpolation or on the whole data matrix when it is available.

-

•

grmf [2] A matrix completion algorithm using graph-based side information to enhance collaborative filtering performance.

-

•

trmf [35] A matrix completion algorithm tailored to time series, by adding three penalization terms to the matrix factorization quadratic error. When only temporal aggregate measurements are available, we apply this method on the matrix obtained from interpolation.

-

•

HALSX_model Algorithm 2.

For all matrix factorization methods (HALS, NeNMF, rrr, factor_gam, grmf, trmf, HALSX_model), we use the method with several ranks, then choose the best rank ( for synthetic and Portuguese data, for French and MovieLens data). For trmf, we do a grid search on the three penalization parameters, and choose the best combination. For HALSX_model, we use four different regression models: linear model, GAM, support vector regression with linear kernel, and Gaussian process regression with radial basis kernel (lm, gam, svmLinear, gaussprRadial). We use the implementation of lm in standard R, and svmLinear and gaussprRadial of the R package kernlab[36], through the caret API. As of gam, we use the mgcv implementation directly.

For each data matrix, we apply a linear measurement operator on an upper-left submatrix to obtain the measures (of dimension 100-by-130 for synthetic data, 730-by-270 for French data, 731-by-369 for Portuguese data, and 666-by-1189 for MovieLens data). On these measurements of the submatrix, we use each method to estimate a matrix factorization model, with or without side information. We then report the matrix recovery error on this sampled submatrix for all methods, and the prediction errors on the rest of the data matrix for the methods can produce predictions for new columns and/or rows. We distinguish row prediction error, column prediction error, and row-column prediction error, as the error calculated on the lower-left, upper-right and lower-right submatrix.

We report the relative root-mean-squared error as error metric in this section:

-

•

for electricity datasets, ,

-

•

for MovieLens, we calculate the -norm version on the vector of all available movie scores.

Other error metrics do not seem to be qualitatively different in our experiments.

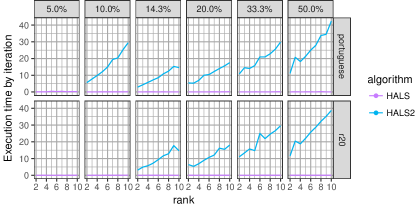

4.1 Execution time and precision between HALS and HALS2

To show-case the complexity difference discussed in Section 3.7, we run HALS (Algorithm 2) and HALS2 (Algorithm 3) on a random temporal aggregate mask, with no side information. In HALS, we treated the mask as a general mask, without using the acceleration specific to temporal aggregate masks. The per iteration execution time is shown in Figure 1. The difference in complexity discussed in Section 3.7 is fairly clear here. In HALS2, the execution time per iteration increases both with the rank and the number of samples in the data, at least for sampling rate from 14.3% on. For low sampling rates, HALS2 often diverges.

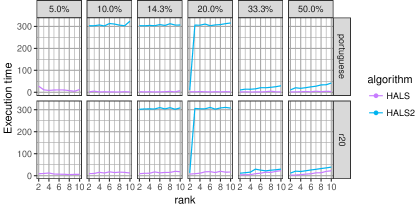

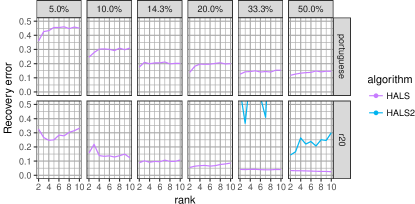

As discussed in Section 3.7, although the execution time per iteration is greater, HALS2 could be more efficient if it does much less iterations than HALS. In Figure 2, we can see that this is not the case: for problems with high sampling rates, HALS2 indeed does less iterations to converge. However, the total execution time is still larger than HALS. For lower sampling rates, HALS2 has troubles converging, and only stops when the maximal execution time allowed (300 seconds) is reached. This is also confirmed in Figure 3, where HALS2 has much worse recovery error than HALS.

4.2 Performance on temporal aggregate measurements

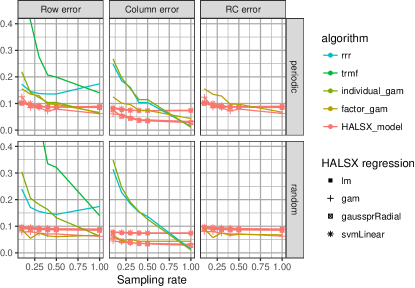

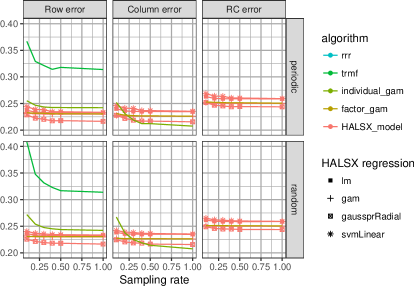

On the synthetic and the two real electricity consumption datasets, we use Algorithm 2 to perform matrix recovery and prediction on temporal aggregate measurements. Every method except for grmf is used in this setting.

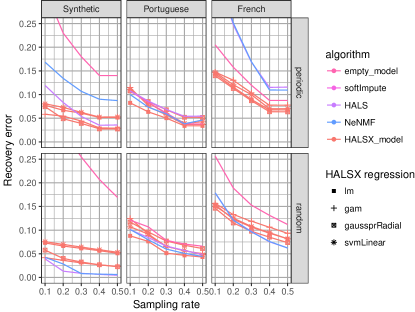

We use two types of temporal aggregate measurements: periodic and random. In periodic measurements, each scalar measure covers a fixed number of periods of one individual. In random measurements, the number of periods covered by a measure is random (see [5] for more details). In electricity consumption data, periodic measurements are closer to the actual meter reading schedules of utility companies, while matrix recovery with random measurements is an easier problem. For both sampling types, we sample 10%, 20%, …, 50% of the data to show-case the matrix recovery performance of the proposed method.

For the synthetic data, we use the true row and column features used to produce the simulations. For the French electricity data, the row features are variables known to have an influence on electricity consumption: the temperature, the day type (weekday, weekend, or holiday), the position of the year. The column features are the percentage of residential, professional, or industrial usages in the group of users for each column. For the Portuguese electricity data, as no individual features are available, we only use the same row features as for the French dataset (temperature, day type, position of the year).

Figure 4 shows the matrix recovery error. For most of the scenario, HALSX_models (red lines with symbols) are comparable or better than the other methods without side information. The only case where an HALSX_model is a little worse is when compared with HALS and NeNMF (two NMF methods) in synthetic data with random measurements, which is the least close to the real application. The softImpute [37] method is not well adapted to temporal aggregate measurements, and has much higher error (higher than the maximal value in these graphics.

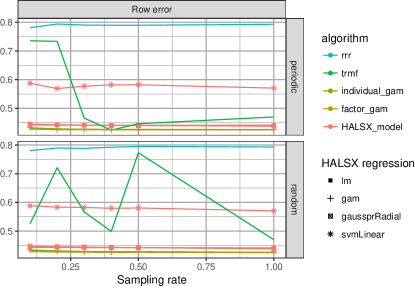

Figures 5, 6, and 7 show the prediction error on the three datasets. We can see that trmf [35] and rrr [34] not very adapted to temporal aggregate measurements. When they are applicable (trmf is only applicable to row prediction, rrr only applicable to row or column predictions, not RC predictions), they have much worse performance than the other methods, except in Synthetic data with complete observations.

In most cases, HALSX_models are comparable to or better than factor_gam and individual_gam, which shows that using side information while estimating the factorization model produces factors more adapted for prediction. It is interesting to note that in some cases, using HALSX_models with incomplete data (sampling rate less than 100%) is actually better than using individual_gam with complete data. This means that compared to traditional regression methods, the proposed method achieves better prediction models using much less data, by exploiting the low-rank structure of the problem.

Moreover, the performance HALSX_models is the least sensitive to sampling rates: it is mostly constant from 30% of data. This shows that using side information is supplementary to observing more data.

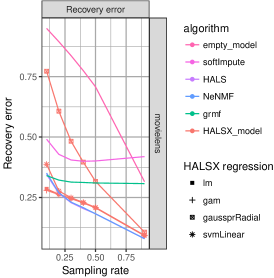

4.3 Performance on matrix completion mask

On the MovieLens dataset, we use Algorithm 2 to perform matrix recovery and prediction with uniformly sampled matrix entries. The sampling rates are .

As is the case for temporal aggregate measurements, we use samples from the upper-left submatrix to estimate the model, evaluate matrix recovery on that submatrix, and evaluate row and/or column prediction errors.

Every method except for trmf is used in this setting. As side information, we use the gender, the age, and the occupation of the users and the genre (a dimension-19 binary variable) of the movies. For grmf [2], we produce a graph where each individual is connected to its ten nearest neighbors with euclidean distance with the features. As the parameters estimated in grmf is per user/movie, it can not be used to predict new individuals, even though it uses side information.

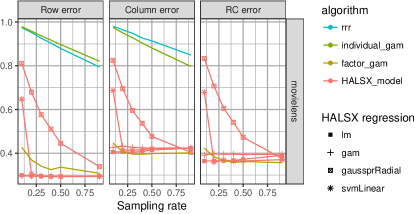

Figure 8 shows the recovery error on MovieLens data. We can see that in the low sampling rate case (10%), HALSX_model with lm works the best. In higher sampling rate cases, the NMF methods without side information (HALS and NeNMF) work the best, with HALSX_model with lm, gam or svmLinear are second to best. HALSX_model with gaussprRadial does not work very in this case, as is the case with the other comparison methods.

Figure 8 shows the prediction error on MovieLens data for new users and/or new movies. The order of the variants of the HALSX_models is conserved: gam and lm are the best, svmLinear is not very good for 10%, but better with higher sampling rates, and gaussprRadial does not work well in this problem. Otherwise, the factor_gam method is slightly better for column predictions (new movies) in higher sampling rate cases, but worse in other cases. Both individual_gam and rrr are much worse than the proposed methods.

5 Conclusion

We established a general approach for including side information on the columns and row in nonnegative matrix factorization methods, with general linear measurements. On the theoretical front, we established a sufficient condition on the features for the factorization to be unique. We deduced a general algorithm to solve the problem, and showed that the algorithm converges to a critical point in rather general conditions. The proposed algorithm is compared in synthetic and real datasets in various sampling rates, and showed comparable or better empirical performance than the referenced methods.

The authors would like to thank Enedis for their help with the proprietary datasets.

References

- [1] P. Jain and I. S. Dhillon, “Provable inductive matrix completion,” arXiv preprint arXiv:1306.0626, 2013.

- [2] N. Rao, H.-F. Yu, P. K. Ravikumar, and I. S. Dhillon, “Collaborative Filtering with Graph Information: Consistency and Scalable Methods,” in Advances in Neural Information Processing Systems 28, C. Cortes, N. D. Lawrence, D. D. Lee, M. Sugiyama, and R. Garnett, Eds. Curran Associates, Inc., 2015, pp. 2107–2115.

- [3] S. Si, K.-Y. Chiang, C.-J. Hsieh, N. Rao, and I. S. Dhillon, “Goal-Directed Inductive Matrix Completion,” in ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (KDD), Aug. 2016.

- [4] D. Donoho and V. Stodden, “When does non-negative matrix factorization give a correct decomposition into parts?” in Advances in Neural Information Processing Systems, 2003, p. None.

- [5] J. Mei, Y. De Castro, Y. Goude, and G. Hébrail, “Nonnegative matrix factorization for time series recovery from a few temporal aggregates,” in Proceedings of the 34th International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, D. Precup and Y. W. Teh, Eds., vol. 70. PMLR, pp. 2382–2390. [Online]. Available: http://proceedings.mlr.press/v70/mei17a.html

- [6] B. Recht, M. Fazel, and P. A. Parrilo, “Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization,” SIAM review, vol. 52, no. 3, pp. 471–501, 2010.

- [7] T. T. Cai, A. Zhang, and others, “ROP: Matrix recovery via rank-one projections,” The Annals of Statistics, vol. 43, no. 1, pp. 102–138, 2015.

- [8] O. Zuk and A. Wagner, “Low-Rank Matrix Recovery from Row-and-Column Affine Measurements,” in Proceedings of The 32nd International Conference on Machine Learning, 2015, pp. 2012–2020.

- [9] R. Velu and G. C. Reinsel, Multivariate Reduced-Rank Regression: Theory and Applications. Springer Science & Business Media, Apr. 2013, google-Books-ID: dsfSBwAAQBAJ.

- [10] F. Bunea, Y. She, and M. H. Wegkamp, “Joint variable and rank selection for parsimonious estimation of high-dimensional matrices,” The Annals of Statistics, vol. 40, no. 5, pp. 2359–2388, Oct. 2012.

- [11] L. Chen and J. Z. Huang, “Sparse reduced-rank regression for simultaneous dimension reduction and variable selection,” Journal of the American Statistical Association, vol. 107, no. 500, pp. 1533–1545, 2012.

- [12] V. Kekatos, Y. Zhang, and G. B. Giannakis, “Electricity Market Forecasting via Low-Rank Multi-Kernel Learning,” IEEE Journal of Selected Topics in Signal Processing, vol. 8, no. 6, pp. 1182–1193, Dec. 2014.

- [13] R. Foygel, M. Horrell, M. Drton, and J. D. Lafferty, “Nonparametric reduced rank regression,” in Advances in Neural Information Processing Systems, 2012, pp. 1628–1636.

- [14] E. J. Candès and B. Recht, “Exact Matrix Completion via Convex Optimization,” Foundations of Computational Mathematics, vol. 9, no. 6, pp. 717–772, 2009.

- [15] D. Agarwal and B.-C. Chen, “Regression-based latent factor models,” in Proceedings of the 15th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM, 2009, pp. 19–28.

- [16] M. Xu, R. Jin, and Z.-H. Zhou, “Speedup Matrix Completion with Side Information: Application to Multi-Label Learning,” in Advances in Neural Information Processing Systems 26, C. J. C. Burges, L. Bottou, M. Welling, Z. Ghahramani, and K. Q. Weinberger, Eds. Curran Associates, Inc., 2013, pp. 2301–2309.

- [17] K.-Y. Chiang, C.-J. Hsieh, and I. S. Dhillon, “Matrix Completion with Noisy Side Information,” in Advances in Neural Information Processing Systems 28, C. Cortes, N. D. Lawrence, D. D. Lee, M. Sugiyama, and R. Garnett, Eds. Curran Associates, Inc., 2015, pp. 3447–3455.

- [18] J. Abernethy, F. Bach, T. Evgeniou, and J.-P. Vert, “A new approach to collaborative filtering: Operator estimation with spectral regularization,” The Journal of Machine Learning Research, vol. 10, pp. 803–826, 2009.

- [19] E. J. Candès and Y. Plan, “Tight Oracle Inequalities for Low-Rank Matrix Recovery From a Minimal Number of Noisy Random Measurements,” IEEE Transactions on Information Theory, vol. 57, no. 4, pp. 2342–2359, 2011.

- [20] M. Roughan, Y. Zhang, W. Willinger, and L. Qiu, “Spatio-Temporal Compressive Sensing and Internet Traffic Matrices (Extended Version),” IEEE/ACM Transactions on Networking, vol. 20, no. 3, pp. 662–676, Jun. 2012.

- [21] A. Rohde and A. B. Tsybakov, “Estimation of high-dimensional low-rank matrices,” The Annals of Statistics, vol. 39, no. 2, pp. 887–930, 2011.

- [22] S. Bhojanapalli, B. Neyshabur, and N. Srebro, “Global Optimality of Local Search for Low Rank Matrix Recovery,” arXiv:1605.07221 [cs, math, stat], May 2016.

- [23] E. A. Pnevmatikakis and L. Paninski, “Sparse nonnegative deconvolution for compressive calcium imaging: Algorithms and phase transitions,” in Advances in Neural Information Processing Systems, 2013, pp. 1250–1258.

- [24] K. Chen, H. Dong, and K.-S. Chan, “Reduced rank regression via adaptive nuclear norm penalization,” Biometrika, vol. 100, no. 4, pp. 901–920, Dec. 2013.

- [25] H. Laurberg, M. G. Christensen, M. D. Plumbley, L. K. Hansen, and S. H. Jensen, “Theorems on Positive Data: On the Uniqueness of NMF,” Computational Intelligence and Neuroscience, vol. 2008, pp. 1–9, 2008.

- [26] A. Cichocki, R. Zdunek, and S.-i. Amari, “Hierarchical ALS algorithms for nonnegative matrix and 3D tensor factorization,” in Independent Component Analysis and Signal Separation. Springer, 2007, pp. 169–176.

- [27] J. Kim, Y. He, and H. Park, “Algorithms for nonnegative matrix and tensor factorizations: A unified view based on block coordinate descent framework,” Journal of Global Optimization, vol. 58, no. 2, pp. 285–319, 2014.

- [28] L. Grippo and M. Sciandrone, “On the convergence of the block nonlinear Gauss–Seidel method under convex constraints,” Operations Research Letters, vol. 26, no. 3, pp. 127–136, 2000.

- [29] D. P. Bertsekas and J. N. Tsitsiklis, Parallel and Distributed Computation: Numerical Methods. Prentice hall Englewood Cliffs, NJ, 1989, vol. 23.

- [30] S. Wood, Generalized Additive Models: An Introduction with R. CRC press, 2006.

- [31] M. Kuhn, “Building predictive models in R using the caret package,” Journal of Statistical Software, vol. 28, no. 5, pp. 1–26, 2008.

- [32] A. Trindade, “UCI Maching Learning Repository - ElectricityLoadDiagrams20112014 Data Set,” 2016.

- [33] “MovieLens 100K Dataset,” https://grouplens.org/datasets/movielens/100k/, 2015-09-23T15:02:16+00:00.

- [34] C. Addy, “Reduced-Rank Regression [R package rrr version 1.0.0].”

- [35] H.-F. Yu, N. Rao, and I. S. Dhillon, “High-dimensional Time Series Prediction with Missing Values,” arXiv preprint arXiv:1509.08333, 2015.

- [36] A. Karatzoglou, A. Smola, K. Hornik, and A. Zeileis, “Kernlab-an S4 package for kernel methods in R,” 2004.

- [37] R. Mazumder, T. Hastie, and R. Tibshirani, “Spectral regularization algorithms for learning large incomplete matrices,” Journal of machine learning research, vol. 11, no. Aug, pp. 2287–2322, 2010.