From a monotone probabilistic scheme to a probabilistic max-plus algorithm for solving Hamilton-Jacobi-Bellman equations

Abstract.

In a previous work (Akian, Fodjo, 2016), we introduced a lower complexity probabilistic max-plus numerical method for solving fully nonlinear Hamilton-Jacobi-Bellman equations associated to diffusion control problems involving a finite set-valued (or switching) control and possibly a continuum-valued control. This method was based on the idempotent expansion properties obtained by McEneaney, Kaise and Han (2011) and on the numerical probabilistic method proposed by Fahim, Touzi and Warin (2011) for solving some fully nonlinear parabolic partial differential equations. A difficulty of the algorithm of Fahim, Touzi and Warin is in the critical constraints imposed on the Hamiltonian to ensure the monotonicity of the scheme, hence the convergence of the algorithm. Here, we propose a new “probabilistic scheme” which is monotone under rather weak assumptions, including the case of strongly elliptic PDE with bounded coefficients. This allows us to apply our probabilistic max-plus method in more general situations. We illustrate this on the evaluation of the superhedging price of an option under uncertain correlation model with several underlying stocks and changing sign cross gamma, and consider in particular the case of 5 stocks leading to a PDE in dimension 5.

Key words and phrases:

Stochastic control, Hamilton-Jacobi-Bellman equations, Max-plus numerical methods, Tropical methods, Probabilistic schemes.2010 Mathematics Subject Classification:

93E20, 49L20, 49M25, 65M751. Introduction

We consider a finite horizon diffusion control problem on involving at the same time a “discrete” control taking its values in a finite set , and a “continuum” control taking its values in some subset of a finite dimensional space (for instance a convex set with nonempty interior), which we next describe.

Let be the horizon. The state at time satisfies the stochastic differential equation

| (1) |

where is a -dimensional Brownian motion on a filtered probability space . The control processes and take their values in the sets and respectively and they are admissible if they are progressively measurable with respect to the filtration . We assume that, for all , the maps and are continuous and satisfy properties implying the existence of the process for any admissible control processes and .

Given an initial time , the control problem consists in maximizing the following payoff:

where, for all , , , and are given continuous maps. We then define the value function of the problem as the optimal payoff:

where the maximization holds over all admissible control processes and .

Let denotes the set of symmetric matrices and let us denote by the Loewner order on ( if is nonnegative). The Hamiltonian of the above control problem is defined as:

| (2a) | ||||

| with | ||||

| (2b) | ||||

| (2c) | ||||

Under suitable assumptions, the value function is the unique (continuous) viscosity solution of the following Hamilton-Jacobi-Bellman equation

| (3a) | |||

| (3b) | |||

satisfying also some growth condition at infinity (in space).

In [6], Fahim, Touzi and Warin proposed a probabilistic numerical method to solve such fully nonlinear partial differential equations (3), inspired by their backward stochastic differential equation interpretation given by Cheridito, Soner, Touzi and Victoir in [5]. In [6], the convergence of the resulting algorithm follows from the theorem of Barles and Souganidis [3], which requires the monotonicity of the scheme. Moreover, for this monotonicity to hold, critical constraints are imposed on the Hamiltonian: the diffusion matrices need at the same time to be bounded from below (with respect to the Loewner order) by a symmetric positive definite matrix and bounded from above by . Such a constraint can be restrictive, in particular it may not hold even when the matrices do not depend on and but take different values for . In [7], Guo, Zhang and Zhuo proposed a monotone scheme exploiting the diagonal part of the diffusion matrices and combining a usual finite difference scheme to the scheme of [6]. This new scheme can be applied in more general situations than the one of [6], but still does not work for general control problems.

McEneaney, Kaise and Han proposed in [8, 11] an idempotent numerical method which works at least when the Hamiltonians with fixed discrete control, , correspond to linear quadratic control problems. This method is based on the distributivity of the (usual) addition operation over the supremum (or infimum) operation, and on a property of invariance of the set of quadratic forms. It computes in a backward manner the value function at time as a supremum of quadratic forms. However, as decreases, the number of quadratic forms generated by the method increases exponentially (and even become infinite if the Brownian is not discretized in space) and some pruning is necessary to reduce the complexity of the algorithm.

In [1], we introduced an algorithm combining the two above methods which uses in particular the simulation of as many uncontrolled stochastic processes as discrete controls. Moreover, we shown that even without pruning, the complexity of the algorithm is bounded polynomially in the number of discretization time steps and the sampling size.

However, due to the above critical constraints imposed in [6], the algorithm of [1] is difficult to apply in practical situations. One way to avoid these critical constraints, is as suggested in [1], to introduce a large number of Hamiltonians such that each of them satisfy the constraints. Since one need to simulate a stochastic process for each Hamiltonian, this technique may increase the complexity unnecessarily.

Here, we propose a different probabilistic discretization of the Hessian of the value function, which ensures the monotonicity of the scheme in rather general situations, including the case of strongly elliptic PDE with bounded coefficients and we show how the algorithm of [1] associated to the new scheme can be applied in these situations and high dimension.

The paper is organized as follows. In Section 2, we recall the scheme of [6]. Then, the new monotone probabilistic discretization is presented in Section 3. In Section 4, we recall the algorithm of [1] and show how it can be combined with the scheme of Section 3. In Section 5, we illustrate this algorithm numerically. There, we consider the evaluation of the superhedging price of an option under uncertain correlation model with several underlying stocks and changing sign cross gamma. We consider in particular the case of 5 stocks leading to a PDE in dimension 5.

2. The probabilistic method of Fahim, Touzi and Warin

In the present section we recall the probabilistic numerical method of Fahim, Touzi and Warin proposed in [6]. We begin with the general description and continue with an example in order to illustrate the critical constraint.

2.1. General description

Let be a time discretization step such that is an integer. We denote by the set of discretization times of . Let be any Hamiltonian of the form (2). Let us decompose as the sum of the (linear) generator of a given diffusion (with no control) and of a nonlinear elliptic Hamiltonian . This means that

with , for some drift map and standard deviation (volatility) map . This also means that the Hamiltonian satisfies the ellipticity condition, that is is positive semidefinite, for all . We shall also assume that is positive definite (which implies that is invertible). A typical example is obtained when is uniformly strongly elliptic and with small enough, which corresponds to the generator . Denote by the Euler discretization of the diffusion with generator :

| (4) |

The time discretization of (3) proposed in [6] has the following form:

| (5) |

with

| (6) |

In (6), , , denotes the following approximation of the th differential of :

| (7a) | ||||

| where denotes the th differential operator. Moreover, it is computed using the following scheme: | ||||

| (7b) | ||||

where, for all , is the polynomial of degree in the variable given by:

| (8a) | ||||

| (8b) | ||||

| (8c) | ||||

where is the identity matrix. Note that the equality between the two formulations in (7) holds for all with exponential growth [6, Lemma 2.1].

In addition to the formal expression in (6-8), which can be compared to a standard numerical approximation (or more precisely to a time discretization), the method of [6] includes the approximation of the conditional expectations in (7) by any probabilistic method such as a regression estimator: after a simulation of the processes and , one apply at each time a regression estimation to find the value of at the points by using the values of and . Hence, although in our setting the operator does not depend on , since both the law of and the Hamiltonian do not depend on , we shall keep the index in the above expressions to allow further approximations as above.

In [6], the convergence of the time discretization scheme (5) is proved by using the theorem of Barles and Souganidis of [3], under the above assumptions together with the critical assumption that is lower bounded by some positive definite matrix (for all ) and that . Indeed, the latter conditions together with the boundedness of are used to show (in Lemma 3.12 and 3.14) that the operator is a -almost monotone operator over the set of Lipschitz continuous functions from to , where we shall say that an operator between any partially ordered sets and of real valued functions (for instance , or the set of bounded functions from some set to ) is -almost monotone, for some constant , if

| (9) |

and that it is monotone, when this holds for .

Note that some other technical assumptions are used in [6], such as the uniform Lipschitz continuity of the Hamiltonian , and the boundedness of the value function of the corresponding control problem, which are less crucial, since they can be replaced by more usual stochastic control assumptions (like boundedness and Lipschitz continuity of the coefficients of the controlled diffusion itself).

In [1], we proposed to bypass the critical constraint, by assuming that the Hamiltonians (but not necessarily ) satisfy the critical constraint, and applying the above scheme to the Hamiltonians . Another way is to replace the part of the operator (6) by any approximation of it in , for instance by using or combining the probabilistic scheme with a finite difference scheme, as is done in [7]. Indeed, the operator (6) is already an approximation of the semigroup of the HJB equation in time which is at best in , therefore one can replace, with no loss of order of approximation, the inside by (which is an approximation in ) or any approximation of order of it. Note however that the first in (6) can only be replaced by an approximation in or at least in . In Section 3, we shall propose an approximation of or which is expressed as a conditional expectation as in (7b), and leads to a monotone operator without assuming the critical constraint. The advantage with respect to finite difference methods or with the method of [7] is that it can still be used with simulations. Before describing the new scheme, we shall compare on some examples the method of [6] with finite difference schemes.

2.2. Examples and comparison with finite difference schemes constraints

Let us first show on examples the behavior of the discretization of [6]. This should help to understand the advantage of the new discretization that we propose in next section. For this, we shall show what happen when the increments of the Brownian motion are replaced by any finite valued independent random variables with same law. This allows one in particular to compare the discretization of [6] with finite difference schemes. Similar comparisons were done in [6] but here we shall discuss in addition the meaning of the critical constraint in this situation.

To simplify the comparison, consider the case where is linear and depends only on , that is

where is a -dimensional symmetric positive definite matrix. We assume that and choose , that is and . Hence, .

Then, denoting by any -dimensional normal random variable, we get that the operator of (6) satisfies:

| (10) |

This operator is linear, and it is thus monotone if and only if for almost all values of the coefficient of inside the expectation, that is , is nonnegative. The critical constraint is equivalent here to . This corresponds exactly to the condition that the coefficient of inside the expectation is nonnegative. Thus, if is replaced by any random variable taking a finite number of values including , the critical constraint is necessary.

Consider the dimension and a simple discretization of by the random variable taking the values with probability and the value with probability , where . Then, we obtain

| (11) |

with . This scheme is equivalent to an explicit finite difference discretization of (3) with a space step . However it is consistent with the Hamilton-Jacobi-Bellman equation (3) if and only if and so if and only if . In that case, the critical condition is necessary for the scheme to be monotone and it is equivalent to the CFL condition .

For finite difference schemes, the CFL condition can be satisfied by increasing . However, here is strongly connected to the possible values of and since the probability of large is small, one cannot avoid the critical constraint if we keep the discretization (7b) of .

Let us consider now the same example in dimension . In that case, the usual difficulty of finite difference schemes is in the monotone discretization of mixed derivatives. This can be solved for instance when the matrix is diagonally dominant by using only close points to the initial point of the grid, that is using the 9-points stencil, see [10], or in general by using points of the grid which are far from the initial point (see for instance [4, 12]). Here, we shall see that this difficulty is hidden by the critical constraint , which implies in particular that the matrix is diagonally dominant.

Indeed, consider the simple discretization of where each entry of is replaced by a random variable as above, taking the values with probability and the value with probability . In that case, the critical constraint is necessary and sufficient for the discretization to be monotone. We have

where is the canonical basis of . This discretization can be rewritten as

where , is the standard -point stencil discretization of the partial derivative on the grid with space step (as above), and is the discretization of using the external vertices of the -point stencil (that is the points ). Note also that the critical constraint implies . Moreover, since is positive semidefinite, then and , so for . The latter condition means that the matrix is diagonally dominant. So, in dimension , the critical constraint implies automatically that the equation can be discretized using a 9-points stencil finite difference monotone scheme.

Hence, the difficulty of the probabilistic scheme does not come only or necessarily from mixed derivatives as for finite difference schemes. It essentially comes from the weights of the possible values of , which link strongly the possible space discretization and time discretization steps. The new approximation of that we propose in next section will allows one to change these weights, while keeping the probabilistic interpretation.

3. A monotone probabilistic scheme for fully nonlinear PDEs

We denote by the set of functions from to with continuous partial derivatives up to order in and , and by the subset of functions with bounded such derivatives.

Theorem 3.1.

Let , as in (4), for some and denote . Let be a one dimensional normal random variable. For a nonnegative integer , consider the polynomial of degree in the variable defined by:

| (12a) | |||

| where, for any real vector and , denotes the th coordinate of , for any matrix and , denotes the th column of , and | |||

| (12b) | |||

We have, for :

| (13) | |||

| (14) |

where the error is uniform in and .

Sketch of proof.

Since , it is sufficient to show (14) when for each . In that case, with fixed, using a unitary matrix with th column equal to , we obtain that (13-14) are equivalent to the same equations for . Since is a unitary matrix, is a -dimensional normal random vector, and in particular its th coordinate is a normal random variable. This implies in particular (13). Applying a Taylor expansion of around up to order and using the values of the moments of any -dimensional normal random vector, we deduce (14). ∎

Since the above approximation depends on the matrix to which the second derivative is multiplied, we cannot apply it directly as an argument of as in (6), but need instead to use the expression of as a supremum of Hamiltonians which are affine with respect to and apply (14) to each of these Hamiltonians. In what follows, we shall present a scheme which combine at the same time this idea and the one of [1]. Note that the decomposition of the matrix involved in the expression of the second order terms of the Hamiltonians as the product is used in a similar way to obtain general monotone finite difference discretizations (see for instance [12]).

Let us decompose the Hamiltonian of (2c) as with

and , and denote by the Euler discretization of the diffusion with generator . Note that, we can also choose a linear operator depending on , but this would increase too much the number of simulations. We can also choose the same linear operator for different values of , which is the case in Algorithm 4.4 below. Assume that is positive definite (so that is invertible) and that , for all , and denote by any matrix such that

| (15) |

Such a matrix exists under the above assumptions since is invertible, and is a symmetric nonnegative matrix. Indeed, one can choose as the square root of the latter matrix. One may also use its Cholesky factorization in which zero columns are eliminated: this leads to a rectangular and triangular matrix of size , where is the rank of the factorized matrix. This is what we use in the practical implementation of Algorithm 4.4 below.

Define

| (16) |

so that

Corollary 3.2.

Let , , be given by (7-8), with and instead of and respectively. Let be defined as:

with as in (12).

Consider the operator:

Assume that the maps , and are bounded with respect to . Then, for , , and , we have

This result shows the consistency of the scheme (5) in the sense of [3]. This implies easily that if the solution of (3) is smooth enough, then the solution of (5) converges to when goes to zero. In the general case, when is only Lipschitz continuous for instance, the convergence is obtained by the theorem of Barles and Souganidis [3]. For this, one need to satisfy also the other assumptions of the theorem, that we shall now show.

Note that when , and does not depend on , the above operator coincides with the operator (6) proposed in [6], since . In [6, Lemma 3.12], the monotonicity of the scheme is proved under the critical constraint that . This constraint is equivalent to the condition that for all and all useful controls and that are optimal in the expression of , which means that the constant in Theorem 3.1 is for . By increasing , we can obtain that this constant is in more general situations, which implies the following monotonicity result.

Theorem 3.3.

Let be as in Corollary 3.2. Assume that the map is upper bounded in and and let be an upper bound. Assume also that is upper bounded, and that there exists a bounded map (in and ) such that . Then, for such that , there exists such that is monotone for over the set of bounded continuous functions , and there exists such that is -almost monotone for all .

Proof.

Let be bounded and let . We can write as the supremum over and of the operators

where

If is such that is a lower bound of for all , we obtain that the operators satisfy (9), and taking the supremum, we get that also satisfies (9) on the set of bounded continuous functions . Let be an upper bound of all the and with (which is a finite set). We get that

For any matrix , , and , we have

with as in (12). Taking such that and using that , we obtain

Since is a multiple of , there exists a constant depending on , such that

for all . Let us choose such that . We get that the lower bound of is nonnegative for for some , which implies from the above remark that satisfies (9) with . Then, for , for some constant , which implies that for all . This shows that satisfies (9) with . ∎

Note that the boundedness of holds if is bounded and is uniformly lower bounded by a positive matrix. Also, the continuity of the maps to which is applied is not necessary, Borel measurability is clearly sufficient. The Lebesgue measurability is also sufficient since and is positive definite, so that if is negligible, then a.e. In the latter case the inequalities and suprema in (9) are for the a.s. partial order.

Remark 3.4.

As explained in Section 2.2, the critical constraint that is necessary even in dimension , and comes from the weak weights of large values of the increments of the Brownian motion in the expression of the derivatives as conditional expectations in (7b). Let us see what happens when increasing by considering the simple example of Section 2.2 in dimension . So consider the same linear Hamiltonian and same operator . Then, the operator of Corollary (3.2) satisfies in any dimension:

| (17) |

with as in (12), such that and a -dimensional normal random variable. If and , we can rewrite as:

If we replace in the two above expressions (for consistency) by the random variable taking the values with probability and the value with probability , where , we obtain the same expression as in (11) but with . As in Section 2.2, (11) is equivalent to an explicit finite difference discretization of (3) with a space step , which is consistent with the Hamilton-Jacobi-Bellman equation (3) if and only if and so if and only if . The condition in Theorem 3.3 is equivalent here to , which is equivalent to the strict CFL condition . The difference with the scheme of [6] is that we can increase , thus the ratio between and , by increasing .

In the sequel, we shall also need the following property which is standard. We shall say that an operator between any sets and of partially ordered sets of real valued functions, which are stable by the addition of a constant function (identified to a real number), is additively -subhomogeneous if

| (18) |

Lemma 3.5.

Let be as in Corollary 3.2. Assume that is lower bounded in and . Then, is additively -subhomogeneous over the set of bounded continuous functions , for some constant with .

Proof.

Take for a nonnegative upper bound of . ∎

With the monotonicity, the -subhomogeneity implies the -Lipschitz continuity of the operator, which allows one to show easily the stability as follows.

Corollary 3.6.

Proof.

The boundedness of implies that is bounded. Applying Corollary 3.2 to the zero function, we deduce that the function is bounded by the constant function , for some constant . From the conclusion of Theorem 3.3, one can choose such that (9) holds with on the set of bounded functions . Let also be as in Lemma 3.5. Applying (9) and Lemma 3.5 we obtain that if is a positive constant such that , then

By symmetry, we obtain that is an upper bound of . By induction, we get that is bounded by which is bounded independently of . This implies the stability of the scheme. ∎

Applying the theorem of Barles and Souganidis [3], we obtain the convergence of the scheme.

Corollary 3.7.

Let the assumptions and notations of Corollary 3.6 hold. Assume also that (3) has a strong uniqueness property for viscosity solutions and let be its unique viscosity solution. Let us extend on as a continuous and piecewise linear function with respect to . Then, when , converges to locally uniformly in and .

Similar results can be proved, under different assumptions on the Hamiltonian, for value functions that have a given growth such as a quadratic growth (functions that are bounded above and below by a multiple of the quadratic function ). We shall not discuss this here although this is the type of results that are needed for the Hamilton-Jacobi-Bellman equations involved in the next section, see Theorem 4.2. Indeed, there are few such results in the literature for unbounded value functions which make more difficult to show all the steps of the convergence proof. For instance one need to extend the theorem of Barles and Souganidis [3] in the context of functions with a given growth. Let us mention that in [2], Assellaou, Bokanowski and Zidani show convergence and estimation results for semilagrangian schemes for quadratic growth value functions. Unfortunately, nor the results nor the steps of the proof can be used in our context due to the special assumptions made there.

4. The probabilistic max-plus method

The algorithm of [1] was based on the scheme (5), with as in Corollary 3.2, and . Here, we shall construct it similarly but with as in Theorem 3.3. The originality of the algorithm of [1] is that instead of applying a regression estimation to compute by projecting the functions inside the conditional expectation into a (large) finite dimensional linear space of functions, we approximate by a max-plus linear combination of basic functions (namely quadratic forms) and use the following distributivity property which generalizes Theorem 3.1 of McEneaney, Kaise and Han [11].

In the sequel, we denote and the set of measurable functions from to with at most some given growth or growth rate (for instance with at most exponential growth rate), assuming that it contains the constant functions.

Theorem 4.1 ([1, Theorem 4]).

Let be a monotone additively -subhomogeneous operator from to , for some constant . Let be a measurable space, and let be endowed with its Borel -algebra. Let be a measurable map such that for all , is continuous and belongs to . Let be such that . Assume that is continuous and bounded. Then,

where , and

To explain the algorithm, assume that the final reward of the control problem can be written as the supremum of a finite number of quadratic forms. Denote (recall that is the set of symmetric matrices) and let

| (19) |

be the quadratic form with parameter applied to the vector . Then for , we have

where is a finite subset of .

The application of the operator of Corollary 3.2 to a (continuous) function can be written, for each , as

| (20a) | |||||

| where | |||||

| (20b) | |||||

| (20c) | |||||

| and is the operator from to given by | |||||

| (20d) | |||||

with

and as in Section 3, and as in (12). Indeed, the Euler discretization of the diffusion with generator satisfies

| (21) |

Using the same arguments as for Theorem 3.3 and Lemma 3.5, one can obtain the stronger property that for , all the operators belong to the class of monotone additively -subhomogeneous operators from to . This allows us to apply Theorem 4.1 and thus the following result.

Theorem 4.2 ([1, Theorem 2], compare with [11, Theorem 5.1]).

Consider the control problem of Section 1. Assume that and that for each , and are constant, is nonsingular, is affine with respect to , is quadratic with respect to and strictly concave with respect to , and that is the supremum of a finite number of quadratic forms. Consider the scheme (5), with and as in (20), constant and nonsingular, constant and nonsingular and affine. Assume that the operators belong to the class of monotone additively -subhomogeneous operators from to , for some constant with . Assume also that the value function of (5) belongs to and is locally Lipschitz continuous with respect to . Then, for all , there exists a set and a map such that for all , is a quadratic form and

| (22) |

Moreover, the sets satisfy .

Theorem 4.2 uses the following property which was stated in [1, Lemma 3] without proof, and without the upper bound assumption. Since counter examples exist when the upper bound assumption is not satisfied, we are giving here the proof of the lemma.

Lemma 4.3 (Compare with [1, Lemma 3]).

Let us consider the notations and assumptions of Theorem 4.2. Let be a measurable function from to and let denotes the measurable map , with as in (19). Assume that there exists such that for all , and almost all , and that belongs to , for all . Then, the function is a quadratic function, that is it can be written as for some .

Proof.

Since is linear with respect to , is a quadratic function of the coefficients of which depend on . Then, due to the assumptions that and are constant and nonsingular, we get that with , and are quadratic functions of . Let denotes the expression in (20d) without the maximization in . We get that is of the form , where is a quadratic function of , strictly concave with respect to and and are matrices. This also holds if we replace by , that is if we replace by , where is the quadratic function . However in that case, since is deterministic, which is an affine function of , since is affine. Therefore is a quadratic function of , strictly concave with respect to , so its maximum over is a quadratic function of , that we shall denote by .

Since is assumed to be monotone from to , we get that . Therefore for all and , we obtain that . So is a polynomial of degree at most in the variables upper bounded by a polynomial of degree at most . Taking the limit when the and go to , we deduce that all the monomials of degree have zero coefficients, so that is a quadratic function of . Hence, is a quadratic function of , strictly concave with respect to , which implies that its maximum over , , is a quadratic function of . ∎

Sketch of proof of Theorem 4.2.

Lemma 4.3 shows in particular (and indeed uses) the property that each operator such that with as in (20d), sends a deterministic quadratic form into a quadratic form. Since for any finite number of quadratic forms, there exists a quadratic form which dominates them, the assumptions of Theorem 4.2 imply that and then all the functions are upper bounded by a quadratic form (recall that is a finite set). Then, applying Theorem 4.1 to the maps and using Lemma 4.3, we get the representation formula (22). ∎

In Theorem 4.2, as in [11, Theorem 5.1], the sets are infinite for . If the Brownian process is discretized in space, the set can be replaced by a finite subset, and the sets become finite. Nevertheless, their cardinality increases at each time step as where is the cardinality of the discretization of . Then, if all the quadratic functions generated in this way were different, we would obtain that is doubly exponential with respect to the number of time discretization points and more than exponential with respect to . Since the Brownian process is -dimensional, one may need to discretize it with a number of values which is exponential in the dimension . Hence, the computational time of the resulting method would be worst than the one of a usual grid discretization. In [11], McEneaney, Kaise and Han proposed to apply a pruning method at each time step to reduce the cardinality of . For this, they assume already that the function is represented as the supremum of the quadratic functions parameterized by a finite set of . They show that pruning (that is eliminating elements of ) is optimal if one looks for a subset of with given size representing as the supremum of the corresponding quadratic functions with a minimal measure of the error. There, the measure of the error is the maximum of the integral of the difference of functions with respect to any probabilistic measure on . Then, restricting the set of probabilistic measures to the set of normal distributions, they propose to use LMI techniques to find the elements of that can be eliminated. However, whatever the number of quadratic functions used at the end to represent at each time step is, the computational time of the pruning method is at least in the order of the cardinal of the initial set . Hence, if is computed as above using a discretization of the Brownian process and the representation of at time already uses quadratic forms, then , so that it is exponential with respect to and can then be doubly exponential with respect to the dimension .

In [1], we proposed to compute the expression of the maps as a maximum of quadratic forms by using simulations of the processes . These simulations are not only used for regression estimations of conditional expectations, which are computed there only in the case of random quadratic forms, leading to quadratic forms, but they are also used to fix the “discretization points” at which the optimal quadratic forms in the expression (22) are computed. We present below a particular case of the algorithm (in [1], different samplings were tested for the regression). However, we add the possibility of having the same operator for different , in which case we choose to simulate the process only one time for each possible , then the number of simulations and quadratic forms decreases. To formalize this, we consider in the algorithm the projection map which sends an element of to a particular element of its equivalence class for the equivalence relation “ if ”.

Algorithm 4.4 (Compare with [1, Algorithm1]).

Input: A constant giving the precision, a time step and a horizon time such that is an integer, a -uple of integers giving the numbers of samples, such that , a subset and a projection map . A finite subset of such that , for all , and . The operators , and as in (20) for and , with (and thus ) depending only on .

Output: The subsets of , for , and the approximate value function .

Initialization: Let , for all , where is random and independent of the Brownian process. Consider a sample of of size indexed by , and denote, for each , , and , the value of induced by this sample satisfying (21). Define , for , with as in (19).

For apply the following 3 steps:

(1) Choose a random sampling among the elements of and independently a random sampling among the elements of , then take the product of samplings, that is consider and for all and , leading to for .

Induce the sample (resp. ) for of with (resp. ). Denote by the set of for .

(2) For each and , denote and construct depending on and as follows:

(a) Choose such that, for all , we have

Extend as a measurable map from to . Let be the element of given by .

(b) For each such that , compute an approximation of by a linear regression estimation on the set of quadratic forms using the sample , with , and denote by the parameter of the resulting quadratic form.

(c) Choose optimal among the at the point , that is such that .

(3) Denote by the set of all the obtained in this way, and define

Note that no computation is done at Step (3), which gives only a formula (or procedure) to be able to compute the value function at each time step and point as a function of the sets . This is what is done for instance to obtain plots. In particular, the algorithm only stores the elements of which are elements of . Since satisfy for all , and has dimension , the memory space to store the value function at a time step is in the order of , so the maximum space complexity of the algorithm is . Before computing the value function, one need to store the values of all the processes, with a memory space in . Moreover, the total number of computations at each time step is in the order of , where the first term corresponds to step (a) and the second one to step (b). Note also that can be chosen to be in the order of a polynomial in since the regression is done on the set of quadratic forms, so in general the second term is negligible, and it is also worth to take small.

As recalled above, the map is a quadratic form, hence there is no loss in choosing to do a regression estimation over the set of quadratic forms. Hence, as stated in [1, Proposition 5], under suitable assumptions, we have the convergence .

5. Numerical tests

To illustrate our algorithm, we consider the problem of

evaluating the superhedging price of an option under uncertain

correlation model

with several underlying stocks (the number

of which determines the dimension of the problem),

and changing sign cross gamma.

The case with two underlying stocks

was studied first as an example in Section 3.2

of [9], where the method proposed is based on a regression on

a process involving not only the state but also the (discrete) control.

In [1], we tested our algorithm with

on the same -dimensional example. Here we shall consider the same example

with reduced to one element and then consider a similar one

with 5 stocks (so in dimension ).

Illustrations are obtained from a C++ implementation

of Algorithm 4.4, which can easily be adapted to any model.

With the notations of the introduction, the problem has no continuum control, so is omitted, and for all , and . So it reduces to maximize

The dynamics is given by where the are Brownians with uncertain correlations: with , a subset of the set of positive symmetric matrices with on the diagonal. This is equivalent to the condition that

Here we assume that is the convex hull of a finite set . Since the Hamiltonian of the problem is linear with respect to , the maximum over is the same as the maximum over , so we can assume that the correlations satisfy . We consider the following final payoff:

Since is nondecreasing, we have , for all odd and even. Then, we can lower bound the value function in dimension by the application of the value function of dimension and volatilities to .

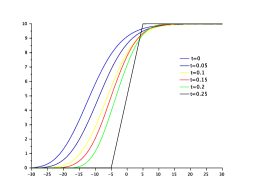

Note that all the coordinates of the controlled process stay in , the set of positive real numbers. To be in the conditions of Theorem 4.2, we approximate the function with a supremum of a finite number of quadratic forms on a large subset of , typically on , so that is approximated with a supremum of a finite number of quadratic forms on the such that . Note that since the second derivative of is in some points, it is not -semiconvex for any and bounded domain, so the approximation need to use some quadratic forms with a large negative curvature, and so we are not under the conditions of [11]. Moreover, since the state space is unbounded, one cannot approximate as a supremum of a finite number of quadratic forms on all the state space as assumed in Algorithm 4.4. However, due to stability considerations, the simulated process stays with almost one probability in a ball around the initial point, so that one may expect the value function to be well approximated in a bounded subset of . The maps for are not constant but they are linear, and one can choose such that is constant and , and get that the result of Theorem 4.2 still holds.

In the illustration below, we choose , the time step , the volatilities and the following correlations sets:

and

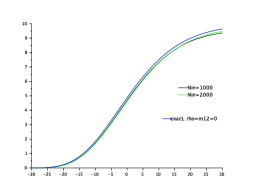

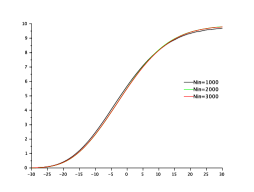

In dimension , we choose , and test several values of simulation size , and compare our results with the true solutions that can be computed analytically when is a singleton, see Figures 1 and 2. For or , is sufficient in Theorem 3.3 (indeed for , so there is no second derivative to discretize), whereas for , one need to take to obtain the monotonicity of the scheme. This may explain why a greater sampling size is needed to obtain the convergence for .

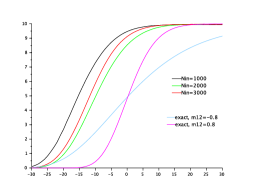

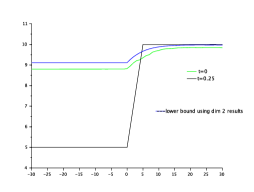

In dimension , we choose , and , and compare our results with a lower bound obtained from the results in dimension , as explained above, see Figure 3. Although, the lower bound appears to be above the value function computed from the Hamilton-Jacobi-Bellman equation in dimension 5, the difference between the value function and the lower bound is small and of the same amount as the difference observed in Figure 2 between the value functions computed in dimension 2 with the simulation sizes and . This indicates that the size of the simulations is not enough to attain the convergence of the approximation, although the results give already the correct shape of the value function. Such a result would be difficult to obtain with finite difference schemes, and at least will take much more memory space. For instance, the computing time for one time step of a finite difference scheme on a regular grid over with steps by coordinate is in and is thus comparable with the computing time of Algorithm 4.4, , with the above parameters, whereas the memory space needed for the finite difference scheme at each time step is similar to the computing time and is thus much larger than the one needed in Algorithm 4.4 (in ).

The computation of the value function in dimension took h

with the C++ program compiled with “OpenMP”

on a core Intel(R) Xeon(R) CPU - GHz

with Go of RAM (each time iteration taking s).

The main part of the computation time is taken by the

optimization part (a) of Algorithm 4.4, with a

time in .

The bottleneck here is in the computation, for each given state at time

, of the quadratic form which is maximal in the

expression of .

Therefore, a better understanding of this maximization problem is necessary

in order to decrease the total computing time.

This would allow us to

obtain better approximations in dimension 5 in particular,

and increase the dimension with a small cost.

Such an improvement is left for further work.

References

- [1] Marianne Akian and Eric Fodjo. A probabilistic max-plus numerical method for solving stochastic control problems. In 55th Conference on Decision and Control (CDC 2016), Las Vegas, United States, December 2016. Also arXiv:1605.02816.

- [2] Mohamed Assellaou, Olivier Bokanowski, and Hasnaa Zidani. Error estimates for second order Hamilton-Jacobi-Bellman equations. Approximation of probabilistic reachable sets. Discrete Contin. Dyn. Syst., 35(9):3933–3964, 2015.

- [3] G. Barles and P. E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Anal., 4(3):271–283, 1991.

- [4] J. Frédéric Bonnans and Housnaa Zidani. Consistency of generalized finite difference schemes for the stochastic HJB equation. SIAM J. Numer. Anal., 41(3):1008–1021, 2003.

- [5] Patrick Cheridito, H. Mete Soner, Nizar Touzi, and Nicolas Victoir. Second-order backward stochastic differential equations and fully nonlinear parabolic PDEs. Comm. Pure Appl. Math., 60(7):1081–1110, 2007.

- [6] Arash Fahim, Nizar Touzi, and Xavier Warin. A probabilistic numerical method for fully nonlinear parabolic PDEs. Ann. Appl. Probab., 21(4):1322–1364, 2011.

- [7] Wenjie Guo, Jianfeng Zhang, and Jia Zhuo. A monotone scheme for high-dimensional fully nonlinear PDEs. Ann. Appl. Probab., 25(3):1540–1580, 2015.

- [8] Hidehiro Kaise and William M. McEneaney. Idempotent expansions for continuous-time stochastic control: compact control space. In Proceedings of the 49th IEEE Conference on Decision and Control, Atlanta, Dec. 2010.

- [9] Idris Kharroubi, Nicolas Langrené, and Huyên Pham. A numerical algorithm for fully nonlinear HJB equations: an approach by control randomization. Monte Carlo Methods Appl., 20(2):145–165, 2014.

- [10] Harold J. Kushner. Probability methods for approximations in stochastic control and for elliptic equations. Academic Press [Harcourt Brace Jovanovich, Publishers], New York-London, 1977. Mathematics in Science and Engineering, Vol. 129.

- [11] William M. McEneaney, Hidehiro Kaise, and Seung Hak Han. Idempotent method for continuous-time stochastic control and complexity attenuation. In Proceedings of the 18th IFAC World Congress, 2011, pages 3216–3221, Milano, Italie, 2011.

- [12] J.-M. Mirebeau. Minimal stencils for discretizations of anisotropic PDEs preserving causality or the maximum principle, 2016. Accepted in SIAM Journal on Numerical Analysis (SINUM).