On Drawdown-Modulated Feedback

Control in Stock Trading

Abstract

Control of drawdown, that is, the control of the drops in wealth over time from peaks to subsequent lows, is of great concern from a risk management perspective. With this motivation in mind, the focal point of this paper is to address the drawdown issue in a stock trading context. Although our analysis can be carried out without reference to control theory, to make the work accessible to this community, we use the language of feedback systems. The takeoff point for the results to follow, which we call the Drawdown Modulation Lemma, characterizes any investment which guarantees that the percentage drawdown is no greater than a prespecified level with probability one. With the aid of this lemma, we introduce a new scheme which we call the drawdown-modulated feedback control. To illustrate the power of the theory, we consider a drawdown-constrained version of the well-known Kelly Optimization Problem which involves maximizing the expected logarithmic growth of the trader’s account value. As the drawdown parameter in our new formulation tends to one, we recover existing results as a special case. This new theory leads to an optimal investment strategy whose application is illustrated via an example with historical stock-price data.

keywords:

Financial Engineering, Stochastic Systems, Robustness1 Introduction

Control of drawdown, that is, the control of the drops in wealth over time from peaks to subsequent lows, is of great concern from a risk management perspective. Suffice it to say, the issue of drawdown control has received a considerable attention in the finance literature. More specifically, to properly control drawdown in a stock trading context, one standard approach is to incorporate this consideration into a constrained optimization framework which typically includes other performance criteria; e.g., see Grossman_Zhou_1993 and Klass_Nowicki_2005 which focus on a single-stock scenario. There are also some papers dealing with modifications and extensions of these results for the single-stock case to address an entire portfolio under various stochastic modeling assumptions; e.g., see Zhou_Shang_2015 -Cherney_2015 . Finally, the literature also includes various methodologies to address different types of drawdown. For example, absolute drawdown is studied in Hayes and other drawdown-based metrics are considered in Barmish_Hsieh_2015 , Rockafellar_2006 and Goldberg_Mahmoud_2016 .

In this paper, we focus on the notion of percentage drawdown whose technical definition is given in the next section. We provide a new result which enables a trader to guarantee that a prescribed maximum level for this quantity will not be exceeded. To provide further context for this paper, we mention a sampling of some other papers in the existing literature using different risk measures rather than drawdown. Examples of such measures include Value at Risk (VaR), Conditional Value at Risk, Expected Shortfall and the celebrated mean-variance criterion; e.g., see Jorion_2006 -Luenberger_2011 and Markowitz_1959 . In addition to the analysis of risk, some papers in the literature consider portfolio optimization involving a maximization of expected logarithmic growth. This is the so-called Kelly Optimization Problem which will be used to demonstrate our theory; e.g., see Maclean_1992 -MacLean_Thorp_Ziemba_2011 . Related to this, the literature also includes a well-known method called the Fractional Kelly Strategy. This is aimed at scaling down the size of investment for the purpose of mitigating the risk; e.g., see Thorp_2006 and Maclean_Thorp_Ziemba_2010 .

The takeoff point for this paper, which we call the Drawdown Modulation Lemma, characterizes investments which guarantee that the percentage drawdown is no greater than a prespecified level with probability one. To make our exposition appealing to this community, this investment scheme which we derive from the lemma, is expressed in a classical feedback control setting. We call it drawdown-modulated feedback control. As the drawdown parameter , we recover existing results as a special case. To further illustrate its use, as previously mentioned, we consider a drawdown-constrained version of the Kelly Optimization Problem which involves maximizing the expected logarithmic growth. Then, a numerical example with historical data is carried out and a further generalization of the lemma for portfolio case is discussed in this paper.

2 Drawdown Definitions

For , we let denote the account value at stage . Then as evolves, the percentage drawdown (to-date) is defined as

where

This leads to overall percentage drawdown

Note that the percentage drawdown satisfies Although not considered here, there is another well-known measure, called the maximum absolute drawdown, which we denote by and is given by

The reader is referred to Ismail_2004 and Malekpour_Barmish_2013 for work on this topic.

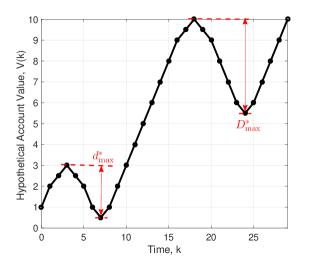

To further elaborate on these two notions of drawdown, we consider an example with a hypothetical account value shown in Figure 2. From the plot, we obtain the overall percentage drawdown, occurs at stage On the other hand, the maximum absolute drawdown, , occurs at stage This toy example shows that the two types of drawdown described above can be quite different. In this paper, we concentrate on the percentage drawdown. This is the version of drawdown which is better suited to deal with different “scales” for . That is both small and large investors can identify with this concept.

3 Feedback Control Point of View

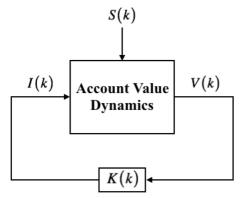

In the sequel, as previously mentioned, we emphasize the control-theoretic point of view. Our formulation here is consistent with a growing body of the literature addressing finance problems but originating from the control community; e.g., see Barmish_2011 -Barmish_Primbs_2015 . Although our analysis to follow can be carried out without reference to control theory, to make the work accessible to this audience, we use the language of feedback systems. Specifically, we view the stock prices as exogenous inputs to a feedback system. In this setting, we use a linear feedback controller which modifies the investment using a time-varying gain applied to the account value . That is, for each stage , we consider the controller having the form

Typically, when selecting this feedback gain, we include a constraint which we express as . For instance, suppose we restrict attention to a so-called cash-financed investment. Then we impose a constraint which guarantees . That is, the investment level is limited to the value of one’s account. This in turn forces . The feedback control configuration which describes this scheme is depicted in Figure 3 for a single stock. Such a configuration can be generalized to deal with a portfolio case of stocks; e.g., see Barmish_Hsieh_2015 . To link back to finance concepts, the special case of buy-and-hold is obtained when

4 Stock-Trading Formulation

For , we let denote the stock price. The associated returns up to stage are given by

In the sequel, we assume that the returns are bounded; i.e.,

with and being points in the support, denoted by , and satisfying

In the sections to follow, when necessary, we assume the random variables are independent and identically distributed (i.i.d.).

Account Value and Drawdown: Now letting be the investment at stage and note that stands for short selling. Beginning at some initial account value , the evolution to terminal state is described sequentially by the recursion

Now, given a maximum acceptable drawdown level satisfying , we focus on conditions on under which satisfaction of the constraint

is assured along all sample pathes with probability one.

Idealized Market: In the sequel, we further assume that our stock-trading occurs within “idealized market.” That is, we assume zero transaction costs, zero interest rates and perfect liquidity conditions. For more details about idealized market assumption, the reader is referred to reference Barmish_Primbs_2015 .

5 The Drawdown Modulation Lemma

In this section, the stepping stone in this paper, which we call it The Drawdown Modulation Lemma, is given. This lemma provides a necessary and sufficient condition on the investment which guarantees that the percentage drawdown is no greater than a given level with probability one.

The Drawdown Modulation Lemma: An investment function guarantees maximum acceptable drawdown level or less with probability one if and only if for all , the condition

is satisfied along all sample pathes.

Proof: To prove necessity, assuming that for all with probability one, we must show the required condition on holds along all sample pathes. Indeed, letting be given, since both and with probability one, we claim this forces the required inequalities on . Without loss of generality, we provide a proof of the rightmost inequality for the case and note that a nearly identical proof is used for . Indeed, using the fact that is in the support , there exists a suitably small neighborhood of , call it , such that

Thus, given any arbitrarily small , there exists some point such that and leading to associated realizable loss . Noting that and

we now substitute

into the inequality above and noting that as , we obtain

To prove sufficiency, we assume that the condition on holds along all sample pathes. We must show for all with probability one. Proceeding by induction, for , we trivially have with probability one. To complete the inductive argument, we assume that with probability one, and must show with probability one. Without loss of generality, we again provide a proof for the case and note that a nearly identical proof is used for . Now, by noting that

and with probability one, we split the argument into two cases: If , then Thus, we have On the other hand, if , with the aid of the dynamics of account value, we have

Using the rightmost inequality condition on , we obtain which completes the proof.

Remarks: First, it is worth to mentioning that since , any investment satisfying the inequality condition in the lemma assures survival. That is, along all sample pathes, for . This is an easy consequence of the fact that at each stage , drawdown of from some previous maximum for never occurs. Second, the satisfactions of the drawdown condition along sample pathes opens a door to solution of new drawdown-constrained optimization problems which involve parameters entering into an investment satisfying the inequality in the lemma; e.g., see Section 6 to follow. Finally, note that the i.i.d. assumption on the returns is not required in the proof of the lemma. What is needed is an explicit bound on the returns which is realizable with non-zero probability.

Feedback Control Realization: With the aid of the Drawdown Modulation Lemma, we can readily obtain a class of investment functions expressed as a linear feedback control parameterized by a gain and leading to satisfaction of the drawdown specification. To be more specific, for each stage , we define

which we call modulator function. Now, using , we express in the feedback form

with constraint

Note that the feedback gain can be selected without regard for the modulator . This idea has a similar flavor to that of the celebrated Separation Theorem in linear control theory; e.g., see Chen_1995 . Henceforth, we call the investment described above a drawdown-modulated feedback controller and the constraint on above is denoted by writing

We note that this is not the only feedback-control realization which is possible. A more general class of feedback controls, to be pursued in our future work, can be formulated with a time varying gain . That is, one can equally well take with and still satisfy the drawdown requirement; see the conclusion of this paper for further discussion of promising research along these lines.

6 Drawdown-Modulated Kelly Optimization

In this section, we consider one of many possible ways to incorporate the Drawdown Modulation Lemma into an optimization problem. To this end, we formulate a drawdown-constrained version of the so-called Kelly Optimization Problem. To be more specific, for , assuming that the returns are i.i.d. random variables with probability density function (PDF) denoted by , we work with the drawdown-modulated feedback controller

with feedback gain treated as an optimization parameter. Now letting be the account value at stage induced by feedback gain , the associated recursion is described by

and we seek to find which achieves

Moreover, in the sequel, a corresponding maximizer is then denoted by

Remarks: The limiting case obtained by letting leads to which brings us back into the world of classical Kelly optimization; e.g., see Thorp_2006 and Kelly_1956 . Thus, the classical Kelly problem can be viewed as a special case of our theory. In the next section, we consider a numerical example, based on historical data, to compare the trading performance obtained via drawdown-modulated feedback control with that obtained via a classical Kelly solution. Given that this solution is often deemed to be too risky, some existing papers introduce the so-called Fractional Kelly strategy which was discussed in the introduction. One disadvantage of a fractional Kelly strategy is that it is often designed in an ad-hoc manner. In contrast, the drawdown-modulated feedback control provides a systematic way to obtain a time-varying problem solution.

7 Numerical Example

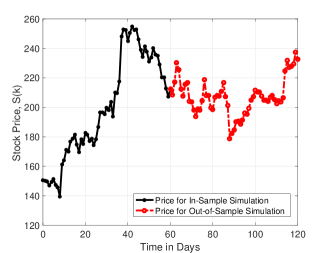

In this section, we provide a numerical example involving real stock data to illustrate how the drawdown modulation is used in practice. We consider the Kelly Optimization Problem described in the last section and use historical price data for Tesla Motors (ticker TSLA) covering the period December 31, 2013 to March 28, 2014; see Figure 7 where these underlying stock prices are plotted. The figure also shows an additional sixty-one days within the period from March 28, 2014 to June 24, 2014 of stock prices which will be used in an out-of-sample test described below.

Our goal is to first use the price data to estimate a probability mass function (PMF) model then calculate the optimal feedback gain which maximizes the objective function

with generated using the cash-financing constraint imposed. We use this to study the out-of-sample trading performance for the resulting controller. In this example we use

as the maximum acceptable drawdown level. To be more specific, using the stock prices, we first calculate the corresponding returns

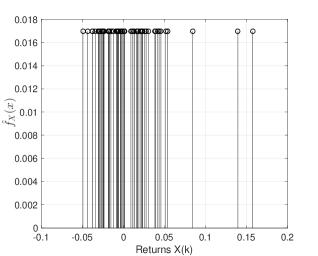

Now letting denote the -th calculated return for , we obtain the estimated PMF of the returns as the sum of impulses

which is used as input to the optimization to be carried out. This PMF, plotted in Figure 7, has and . Hence, the constraint set is described by

for the Kelly Optimization Problem to be solved.

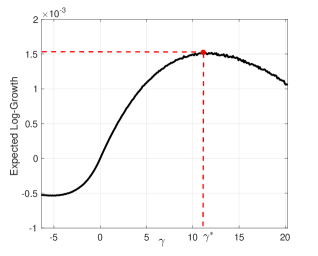

Next, to evaluate for each fixed , we perform Monte Carlo simulation to generate sample pathes for from the PMF. Then we use these to estimate which is needed for the function evaluation. We note that use of the modulator automatically assures that the drawdown requirement is satisfied. Using the plot of the expected logarithmic growth in Figure 7, we obtain a maximizer for given by

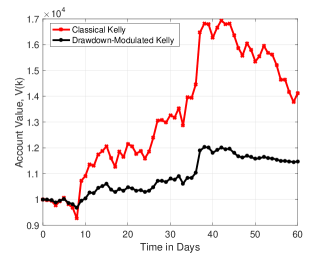

In-Sample Trading Performance: Now, to examine the in-sample trading performance, we take the initial account value and then compare the trading performance obtained via drawdown-modulated feedback control with that obtained via the classical Kelly solution. Figure 7 depicts the sixty-one days in-sample simulation result. In particular, we see that the drawdown-modulated feedback control with

leads to account value given by with the overall percentage drawdown

which is within the allowed upper limit of . For comparison purposes, we also computed the classical Kelly solution which is obtained as a special case of our formulation as . In this case, the optimum turned out to be with the account value and the overall percentage drawdown which is much higher than the drawdown we obtained using modulation.

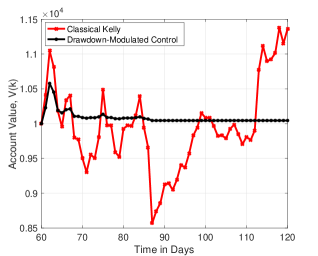

Out-of-Sample Trading Analysis: Next, we evaluate the out-of-sample performance for the second segment of stock prices given in Figure 7. That is, we use the optimal feedback gain obtained previously to carry out sixty new trades. Again, we begin with the same initial account value; i.e., . The associated trading performance is depicted in Figure 7. We see that the the drawdown-modulated control leads to the terminal account value with the overall percentage drawdown as required. In contrast, the classical Kelly strategy without a drawdown constraint leads to the terminal account value and the overall percentage drawdown which corresponds to . While this level is much higher than the specification , the terminal account value is considerably higher. This higher return is to be expected since the drawdown risk was neglected. There is one interesting observation can be made from Figure 7. That is, when the maximum drawdown acceptable level is hit, then the investment becomes zero. Thus, we see that the drawdown-modulated feedback control yields a “stop-loss” type of behavior.

8 Generalized Drawdown Modulation

The Drawdown Modulation Lemma in Section 5 can be generalized to address a portfolio of stocks as follows: With being the -th stock price, we form the returns

for and vectorize it as

As in the scalar case, we assume known bounds

with

for and . We let denote the vertices of the hypercube defined by and above and assume that every point is in the support of . Henceforth, for simplicity of notation, we take and to be vectors with -th components and , respectively and we let denote the vector with -th component by . Now letting be the -th component of the investment vector , the associated account value is updated as

Now denoting the positive and negative parts of component-wise by and respectively, we are now prepared to provide a result for the general case of an -stock portfolio. The proof which proceeds along similar lines to that of the lemma in Section 5 is included for the sake of completeness.

Generalized Drawdown Modulation Lemma: An investment function guarantees that the maximum acceptable drawdown level or less with probability one if and only if for all , the condition

is satisfied along all sample pathes.

Proof: To prove necessity, assuming that for all with probability one, we must show the required condition on holds along all sample pathes. Indeed, letting be given, since both and with probability one, we claim this forces the required inequalities on . Indeed, with the -th component being either or , there exists a vertex such that

Using the fact that is in the support , it follows that there exists a neighborhood of , call it , such that

Hence, given any arbitrarily small , there exists some point such that , and leading to the realizable loss Noting that we have Thus, it follows that

Now, substituting

into the inequality above and noting that as , we obtain

To prove sufficiency, we assume the condition on holds along all sample pathes. We must show for all with probability one. Proceeding by induction, for , we trivially have with probability one. To complete the inductive argument, we assume that with probability one, and must show with probability one. Now, by noting that

and , we split the argument into two cases: If , then Thus, we have On the other hand, if , with the aid of the dynamics of account value, we have

Using the given inequality condition on , we obtain which completes the proof.

Remarks: The drawdown-modulated feedback realization described for the single-stock case is generalized to this multi-stock case as follows: For the -th stock, we use feedback gain and take the investment to be

Then, the condition in the Generalized Drawdown Modulation Lemma above leads to the constraint on as follows:

where and have -th component

9 Conclusion and Future Research

In this paper we introduced a new scheme, which we called drawdown-modulated feedback control. It enables us to express the investment as a linear feedback realization with a gain which leads to satisfaction of a given percentage drawdown specification with probability one. We also provided an illustration of our theory in the context of the Kelly Optimization Problem. The resulting drawdown-modulated feedback control which we obtain provides a systematic way to obtain a time-varying fractional Kelly strategy which takes care of the drawdown requirements.

To further pursue this research, one obvious problem to consider would be the portfolio optimization version of the expected logarithmic growth maximization described in Section 6 with consideration of drawdown along the lines of Section 8. To find an associated optimal solution vector in the portfolio scenario, some efficient algorithm aimed at dealing with potential computational complexity issue might need to be used.

Further to the optimization aspects of the work in this paper, we draw attention to the fact that the solution we obtained is simply a pure gain. However, it can be argued that such a pure gain is not necessarily the true optimum for many problems. Recalling the discussion in Section 5, it may prove to be the case that a time-varying feedback gain may lead to superior performance.

References

- (1) S. J. Grossman and Z. Zhou, “Optimal Investment Strategies for Controlling Drawdowns,” Mathematical Finance, vol. 3, pp. 241-276, 1993.

- (2) M. J. Klass and K. Nowicki, “The Grossman and Zhou Investment Strategy is Not Always Optimal,” Statistics and Probability Letters, vol. 74, pp. 245-252, 2005.

- (3) J. Zhou and J. Shang. “Drawdown Control With a Risk Floor,” The Journal of Alternative Investments, vol 17, pp. 79-94, 2015.

- (4) C. H. Hsieh and B. R. Barmish, “On Kelly Betting: Some Limitations,” Proceedings of Annual Allerton Conference on Communication, Control, and Computing, Monticello, pp. 165-172, 2015.

- (5) J. Cvitanic and I. Karatzas, “On Portfolio Optimization Under Drawdown Constraints,” IMA Lecture Notes in Mathematics and Applications, vol. 65, pp. 77-88, 1994.

- (6) A. Chekhlov, S. Uryasev and M. Zabarankin, “Portfolio Optimization with Drawdown Constraints,” Asset and Liability Management Tools, pp. 263-278, 2003.

- (7) A. Chekhlov, S. Uryasev and M. Zabarankin. “Drawdown Measure in Portfolio Optimization,” International Journal of Theoretical and Applied Finance vol 8, pp.13-58, 2005.

- (8) V. Cherney and J. Obloj, “Portfolio Optimization Under Non-linear Drawdown Constraints in a Semimartingale Financial Model,” Finance and Stochastics, vol. 17, pp. 771-800, 2013.

- (9) R. T. Rockafellar, S. P. Uryasev, and M. Zabarankin, “Generalized Deviations in Risk Analysis,” Fiance and Stochastics, vol 10, pp. 51-74, 2002

- (10) M. Ismail, A. Atiya, A. Pratap and Y. Abu-Mostafa, “On the Maximum Drawdown of a Brownian Motion,” Journal of Applied Probability, vol. 41, pp. 147-161, 2004.

- (11) B. T. Hayes, “Maximum Drawdowns of Hedge Funds with Serial Correlation,” Journal of Alternative Investments, vol. 8, pp. 26-38, 2006.

- (12) E. O. Thorp, “The Kelly Criterion in Blackjack Sports Betting and The Stock Market,” Handbook of Asset and Liability Management: Theory and Methodology, vol. 1, pp. 385-428, Elsevier Science, 2006.

- (13) L. C. Maclean, W. T. Ziemba and G. Blazenko “Growth Versus Security in Dynamic Investment Analysis,” Management Science, vol. 38, pp. 1562-1585, 1992.

- (14) L. C. Maclean and W. T. Ziemba “Growth Versus Security Tradeoffs in Dynamic Investment Analysis,” Annals of Operations Research, vol. 85, pp. 193-227, 1999.

- (15) L. C. MacLean, E. O. Thorp, and W. T. Ziemba, The Kelly Capital Growth Investment Criterion: Theory and Practice, World Scientific Publishing Company, 2011.

- (16) L. C. Maclean, E. O. Thorp, and W. T. Ziemba “Long-term Capital Growth: The Good and Bad Properties of The Kelly and Fractional Kelly Capital Growth Criteria,” Quantitative Finance, vol. 10, pp. 681-687, 2010.

- (17) J. L. Kelly, “A New Interpretation of Information Rate,” Bell System Technical Journal, pp. 917-926, 1956.

- (18) P. Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, McGraw-Hill, 2006.

- (19) Z. Bodie, A. Kane, A. Marcus, Investments, McGraw-Hill, 2010.

- (20) D. G. Luenberger, Investment Science, Oxford University Press, New York, 2011.

- (21) C. T. Chen, Linear System Theory and Design, Oxford University Press, 1995.

- (22) B. R. Barmish, “On Performance Limits of Feedback Control-Based Stock Trading Strategies”, Proceedings of American Control Conference, pp. 3874-3879, 2011

- (23) S. Malekpour and B. R. Barmish, “A Drawdown Formula for Stock Trading Via Linear Feedback in a Market Governed by Brownian Motion,” Proceedings of the European Control Conference, Zurich, Switzerland, pp. 87-92, 2013.

- (24) C. H. Hsieh, B. R. Barmish and J. A. Gubner, “Kelly Betting Can be Too Conservative,” Proceedings of IEEE Conference on Decision and Control, pp. 3695-3701, Las Vegas, 2016.

- (25) B. R. Barmish and J. A. Primbs, “On a New Paradigm for Stock Trading Via a Model-Free Feedback Controller,” IEEE Transactions on Automatic Control, AC-61, pp. 662-676, 2016.

- (26) L. R. Goldberg and O. Mahmoud, “Drawdown: From Practice to Theory and Back Again,” Mathematics and Financial Economics, pp. 1-23, 2016.

- (27) H. Markowitz, Portfolio Selection, Yale University Press, 1959.