Quantile Regression with Interval Data

Abstract

This paper investigates the identification of quantiles and quantile regression parameters when observations are set valued.

We define the identification set of quantiles of random sets in a way that extends the definition of quantiles for regular random variables.

We then give sharp characterization of this set by extending concepts from random set theory.

Applying the identification set of quantiles and its sharpness to parametric quantile regression models yields the identification set of the parameters and its sharpness.

We apply our methods to data on localized environmental benefits and their impact on house values.

Keywords: Partial Identification, Random Sets, Quantile Regression, Quantile Sets.

JEL Code: C21.

1 Introduction

Interval valued observations are common in data based on surveys. One type of interval valued data is generated by a response to a questioner that offers a distinct set of intervals to choose from. Another type of interval data is generated by respondents choosing the minimum and/or maximum amount. Willingness to pay surveys often fall in this type. Simple econometric tools, such as to apply the OLS using the midpoint of willingness-to-pay interval as a dependent variable, have long been known to suffer from substantial biases – see Cameron and Huppert (1989).

Set identification and set inference approaches are proposed to solve this issue under a number of econometric contexts – see our discussion of the literature ahead near the end of this section. To the best of our knowledge, however, no preceding paper in this literature has discussed quantile regression models with general quantile ranks and general set valued data. Some empirical papers (e.g., O’Garra and Mourato, 2007; Gamper-Rabindran and Timmins, 2013), on the other hand, use quantiles and quantile regressions where outcome data are interval-valued by taking the midpoint of the interval as the representative value. In this light, this paper investigates the identification of quantiles and of quantile regressions when the outcome variable is set valued.

We first identify the unconditional and conditional quantiles of a random set in Section 2. The concept of the quantile set of a random set is introduced. The quantile set is shown to be identified by the containment and capacity quantiles which we define in Section 2. The identification argument for unconditional quantiles extends to that for conditional quantiles in Section 3.1. Further, the identification argument for conditional quantiles is extended to set identification of quantile regression functions depending on a finite number of parameters in Section 3.2. We show that this identification set is defined by a system of conditional moment inequalities. These inequalities involve the cumulative containment and cumulative capacity functionals, which characterize the identification set for the quantile regression parameters. We also show that the sharp identification set is convex if the quantile regression is linear in parameters. We use simulation studies to demonstrate the validity of the sharp characterization of the identified sets in Section 4.

Literature: This paper is related to two broad literatures. One is the literature on partial identification with interval data and the other is the literature on quantile regressions. For the former branch of the literature, binary choice models with interval regressors are discussed in Manski and Tamer (2002). Mean regressions when the outcome variables are interval valued are discussed in Beresteanu and Molinari (2008). The models of Manski and Tamer (2002) and Beresteanu and Molinari (2008) are generalized in Beresteanu, Molchanov, and Molinari (2011).

Quantile regressions are introduced and studied extensively in the literature (e.g., Koenker and Bassett, 1978; Koenker, 2005). A number of notable papers in the literature discuss identification of quantiles and/or quantile regressions under set-valued observed outcomes. One of the most common causes of set-valued outcomes is censoring. Powell (1984) provides an estimator for the linear median regression model where the outcome variable is censored. Manski (1985) discusses identification of the linear median regression model where econometricians only observe the sign of an outcome variable. Hong and Tamer (2003) discuss inference on the linear median regression model where the outcome variable is censored and regressors are endogenous. Khan and Tamer (2009) discuss inference on the linear median regression model where the outcome variable is endogenously censored. The model considered in this paper includes the case of censored outcome variables as special cases of set-valued outcome variables. Furthermore, compared with these preceding papers, we consider generalized quantile ranks in addition to the median .

More recently, Li and Oka (2015) consider linear quantile regressions with a censored outcome variable in the framework of Rosen (2012). We do not deal with panel data, but the model considered in this paper includes the case of censored outcome variables as argued above. While the source of partial identification is not interval-valued outcomes, partial identification of nonseparable models are also investigated by Chesher (2005, 2010) and generalized by Chesher and Rosen (2015).

Notations and definitions: We introduce basic notations and definitions partly following those of Molchanov (2005). Let be a complete probability space on which all random variables and sets are defined. Let denote the collection of all closed sets in . For an -valued random variable , let define the cumulative distribution function of . When it exists, the probability density function is denoted by . For , let denote the -th quantile of . A random variable is a measurable selection of if -a.s. The set of selections of is denoted by . The containment functional and capacity functional of are defined by and , respectively.

2 Quantiles of Random Sets

We start by discussing identification of quantiles. In the current section, we focus on unconditional quantiles. Section 3 extends this baseline result to conditional quantiles by considering the corresponding conditional probabilities given covariates, where the responses are allowed to arbitrarily depend on the covariates.

Assumption 2.1 (Data)

Let be such that is unobserved, is observed, is non-empty -a.s., and -a.s.

At this point, we do not assume that is interval-valued. We later show that sharp identification requires to be interval-valued – see Theorem 2.2 ahead.

We would like to learn about . Define the -th quantile set of by

This is, by definition, the identification set for . In other words, with no further information the only thing we can say about is that .

For any , define

to be the cumulative containment and cumulative capacity functionals, respectively. Note that and are monotone increasing and right continuous. For , define

to be the containment and capacity quantiles of , respectively. Since is -valued, and are equivalent to and , respectively.

Theorem 2.1 (Partial Identification)

Suppose that Assumption 2.1 holds. For every , .

Proof.

The statement trivially holds if is an empty set. Suppose that is not empty. Let . Thus, there exists such that . By the definitions of and , implies for all .111This implication corresponds to the necessity part of Artstein’s Lemma, which does not restrict to compact sets. See discussion in Beresteanu, Molchanov, and Molinari (2012). Therefore, . This proves the theorem. ∎

When for a random variable , . Molchanov (1990) defines a quantile of a random set in a different way. His definition does not provide the same generalization of a quantile function in case of a -valued random set that we need in this paper.

The other direction of set inclusion for Theorem 2.1 need not hold. To see this, consider a simple random set such that -a.s. Then, we have , but . This example illustrates why a ‘hole’ in the set fails to establish the other direction of set inclusion. This observation in fact can be generalized. The following theorem shows that the identification set equality holds without such holes (i.e., for interval-valued random sets).

Theorem 2.2 (Sharpness)

Suppose that Assumption 2.1 holds. If is a convex valued random set in with , then for all . Furthermore, if in addition -a.s., then for all . Similarly, if in addition -a.s., then for all .

Proof.

If is empty, then the first claim in the theorem is trivially satisfied. Now, suppose that it is non-empty. Fix and take . Let , , and . By definition, and . By , we choose . Let

Since is convex, for all , and thus the random variable defined above is a selection of . By construction, and thus .

Suppose that -a.s. Then, since is closed, the random variable defined by is a selection of . It also satisfies Therefore, .

Finally, suppose that -a.s. Then, since is closed, the random variable defined by is a selection of . It also satisfies Therefore, . ∎

Theorems 2.1 and 2.2 together show that for all , if has a selection and is a compact interval -a.s. In other words, is a sharp characterization of the identification set . There are sufficient conditions that guarantees that . One such condition is that is closed-valued and non-empty a.s., as stated in the Fundamental Selection Theorem (Molchanov, 2005, Theorem 2.13).

Outcome variables which are reported as convex valued sets include several important cases that an empirical researcher may encounter. First is the case where is generated by a response to a questioner that offers a distinct set of intervals to choose from. The conditions in Theorems 2.1 and 2.2 are general enough to allows these intervals to be distinct, intersect or even be included in each other. A second type of data which is covered by these conditions is willingness to pay surveys. Contingent valuation surveys which employ the collapsing interval method are a prominent example for this case. Sometimes in these surveys, the interval is indeed for some real , and quantiles can be estimated while expectations cannot.

Estimation of the sharp identified set can be implemented simply by taking the sample -th quantiles and of and , respectively. Inference can also be implemented by applying Beresteanu and Molinari (2008) to the standard limit joint distribution of the empirical quantiles .

3 Covariates

Suppose that in addition to we observe a vector of covariates, denoted by .

Assumption 3.1 (Data with Covariates)

Let be such that is unobserved, is observed, is non-empty -a.s., -a.s., and the regular conditional probability measures of and given exist.

The true response can arbitrarily depend on the covariates as long as the regular conditional probability measures exist. Since is allowed to arbitrarily depend on and is contained in , the random set generally depends on the covariates as well.

To account for the observed covariates, we use the following extended notations. Let denote the conditional cumulative distribution function of given . Let denote the conditional quantile function of given . In light of the regular conditional probability measures, the conditional containment functional and conditional capacity functional of given are defined by

respectively.

3.1 Conditional Quantiles

Theorems 2.1 and 2.2 presented in Section 2 naturally extend to conditional quantile counterparts. Define the -th conditional quantile set of gien by

The following two corollaries are the extended counterparts of Theorems 2.1 and 2.2.

Corollary 3.1 (Partial Identification)

Suppose that Assumption 3.1 holds. We have for every .

Corollary 3.2 (Sharpness)

Suppose that Assumption 3.1 holds. If is a convex valued random set in with , then for all . Furthermore, if in addition for -a.s. then for all . Similarly, if in addition for -a.s. , then for all .

Estimation of the sharp identified set can be implemented by local polynomial estimators and for the -th quantiles of and , respectively, given . Inference can be also implemented by applying Beresteanu and Molinari (2008) to the limit joint distribution of based on a version of Bahadur representations (e.g., Chaudhuri, 1991; Guerre and Sabbah, 2012; Qu and Yoon, 2015, 2018).

3.2 Parametric Quantile Regression Models

We now turn to parametric quantile regression models. We define a parametrized -th quantile regression function by

for all . With the covariates allowed to include a constant, a special case is the linear quantile regression function given by . We would like to identify for each . The identification set is defined by

| (3.1) |

for each .

Theorem 3.3 (Partial Identification)

Suppose that Assumption 3.1 holds. For every ,

| (3.2) |

Proof.

As in the proof of Theorem 2.1, implies for all . Therefore, implies -a.s. Thus,

Writing the last expression in terms of conditional moments yields the expression in the statement of the theorem. ∎

This theorem provides conditional moment inequality restrictions to characterize a superset of the identification set . Like Theorem 2.1 for quantiles, the other direction of set inclusion is not generally guaranteed. However, like Theorem 2.2 for quantiles, the following theorem provides an important case where the reverse inclusion is true.

Theorem 3.4 (Sharpness)

Suppose that Assumption 3.1 holds. If and is a convex valued random set in (i.e. is interval valued), then

for all . Furthermore, if in addition -a.s., then

for all . Similarly, if in addition -a.s., then

for all .

Proof.

If is empty, then the first claim in the theorem is satisfied. Now, suppose that this set is non-empty. Take Let , , and . Then, and , -a.s. By , we choose . Let

Since is convex, for all , and thus the random variable defined above is a selection of . Therefore, . By construction, , -a.s., and thus . This shows

Writing the expression on the left-hand side in terms of conditional moments yields the expression in the statement of the theorem.

Suppose that -a.s. Then, since is closed, the random variable defined by is a selection of . Therefore, . If we take , then -a.s., and thus . This shows

Writing the expression on the left-hand side in terms of conditional moments yields the expression in the statement of the theorem.

Suppose that -a.s. Then, since is closed, the random variable defined by is a selection of . Therefore, . If we take , then -a.s., and thus . This shows

Writing the expression on the left-hand side in terms of conditional moments yields the expression in the statement of the theorem. ∎

Theorems 3.3 and 3.4 together show that the conditional moment inequality restrictions in (3.2) provide a sharp characterization of the identification set for all if has a selection and is a compact interval -a.s. One sufficient condition for the condition, , of Theorem 3.4 is that is closed-valued and non-empty, as stated in the Fundamental Selection Theorem (Molchanov, 2005, Theorem 2.13). The conditional moment inequalities can be rewritten more simply as

| (3.3) |

where is an -dimensional random vector generated by through the transformation for each .

For the quantile set, the sharp identification set is guaranteed to be an interval (see Section 2). For the current setting where the sharp identification set is only implicitly characterized by a system of conditional moment inequalities, it is not clear if the identification set has nice geometric properties such as convexity. Suppose that the quantile regression is specified in the linear-in-parameters form . In this case, the identification set can be shown to be convex. Consequently, projections of the identification set on each coordinate is an interval.

Theorem 3.5 (Convexity)

Suppose that Assumption 3.1 holds. Suppose that for all . If is a closed convex valued random set in , then the identification set is convex for all .

Proof.

This geometric information is useful in practice. For example, it provides a guidance about the direction of computational search for a grid representation of set estimates. Furthermore, this result guarantees that a projection of the identification set is an interval, which will be useful when methods of inference becomes available in the future for projections of identified sets under conditional moment inequalities.222See for example Belloni, Bugni, and Chernozhukov (2018) and Bugni and Shi (2018). Also see Kaido, Molinari and Stoye (2016).

The conditional moment inequality restrictions in (3.3) to characterize the identification set can be rewritten as

where the moment functions, and , are defined by

for . This model fits in the framework for which the existing literature provides methods of inference via moment selection, e.g., Andrews and Shi (2013). For convenience of the readers, we describe the procedure of inference based on this existing literature in Appendix A. Furthermore, Appendix B provides a practical procedure to supplement this inference procedure in the context of linear quantile regressions.

4 Simulation Studies

In this section, we use simulation studies to evaluate the proposed method. We consider the identified set of quantile regression parameters defined in (3.1), and conduct inference for the true parameters based on the moment inequalities (3.3) that sharply characterize this identified set. The method of inference outlined in Appendix A is applied to these moment inequalities (3.3). With this method of inference and our characterization of the identified set, we use Monte Carlo simulations to check the size control at the true parameter value contained in the identified set.

In order to generate analytically tractable parametric quantile regressions, we use the following model.

| (4.1) | |||||

For example, if and , then and . This individual is at the () 0.573-th quantile, and the corresponding quantile regression function is given by . In fact, model (4.1) yields the linear model for each quantile with intercept and slope . Hence, the true quantile regression parameter vector is . Our identification theory shows that the moment inequalities (3.3) give the sharp characterization of the identified set containing this true parameter vector, and an application of the existing inference method outlined in Appendix A thus allows for inference about this true parameter vector.

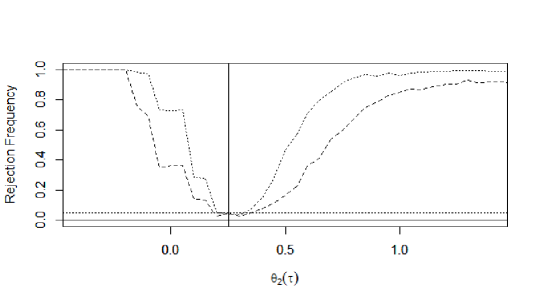

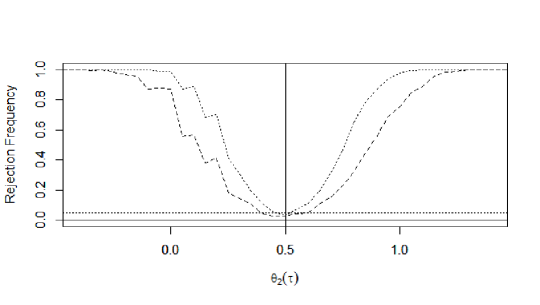

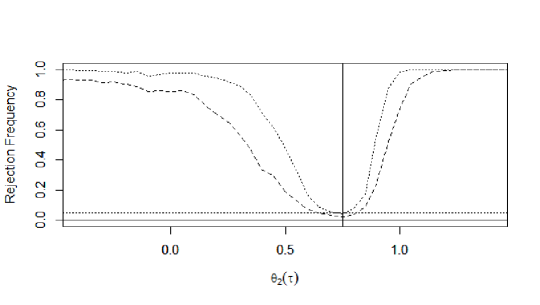

For Monte Carlo experiments, 1,000 small samples are drawn of sizes 100 and 200 observations. Based on the methods presented in Section 3.2, we conduct tests of versus for various parameter vectors for each quantile . The critical value is estimated using the procedure outlined in Appendix A with 1,000 bootstrap replications for the size .333We used , , and .

Figure 1 shows graphs of rejection frequencies for the test described above. Parts (I), (II), and (III) of the figure focus on quantiles 0.25, 0.50, and 0.75, respectively. For ease of presentation, we focus on the one-dimensional slice of the two-dimensional parameter space running through the true parameter point at each quantile . Specifically, for the -th quantile, the results are displayed on the set , and the horizontal axes in Figure 1 represent this set indexed by . The true point is indicated in the figure by a solid vertical line. The rejection frequencies are a indicated by dashed and dotted curves for sample sizes and 200, respectively. The uniform asymptotic theory of Andrews and Shi (2013, Section 5) together with our identification theory predicts that the implied size control entails the rejection probabilities asymptotically at or below the nominal rejection probability in the identified set. The curves displayed in the figure running at or below the nominal rejection probabilities are thus consistent with the theory.

5 Empirical Application

To assess the effects of localized environmental benefits on housing values through an extended hedonic regression model, (Gamper-Rabindran and Timmins, 2013, henceforth GRT) use within-tract quantiles of housing values as outcome variables. Controlling for tract fixed effects through first differencing as well as controlling for various observed tract attributes, they find that localized cleanup of hazardous waste sites leads to larger appreciation in house prices at lower quantiles. The Decennial Census provides house prices only in terms of intervals. GRT used these intervals to compute quantile points of house prices – see Table A.1 of their online appendix.

In this paper, we re-examine the empirical analysis of GRT by treating the housing prices as interval-valued data as in the original data, rather than adding assumptions to obtain point-valued housing prices. Our econometric procedure consists of three steps. First, we obtain within-tract quantile sets for each tract for each year by using the methods proposed in Appendix C. Due to the discrete nature of the house price intervals, we can rely on the super-consistency property presented in Appendix C – see Theorem C.1. In the second step, we take the set difference and take first differences of all the observed covariates as in GRT. This second step is used to difference out tract fixed effects. Finally, we use (Beresteanu and Molinari, 2008, Sec. 4) and the constructed data to obtain set-valued best linear predictors of on . In the asymptotic setting where the number of within-tract houses increases as the number of tracts increases, the effects of the first-step quantile set estimation on the subsequent set estimation can be ignored due to the super-consistency result for the quantile set estimation under discrete categories (see Theorem C.1 in Appendix C.1).

We use the same set of observed controls as in GRT. In Table 1, we report the estimates for the coefficient of cleanup of hazardous waste sites. The table consists of nine rows showing estimation results across the nine quantiles . Column (I) shows point estimates of GRT as a reference.444We remark that the sample used by GRT and the sample used by us are slightly different likely due to different data selection procedures. Furthermore, they use sampling weights, while we do not. In column (II), we assume that equals the lower bound of interval categories , and obtained point estimates. Similarly, in column (III) we assume that equals the upper bound of interval categories , and obtained point estimates. Column (IV) shows the set estimates according to the three-step procedure outlined in the previous paragraph. Column (V) in addition shows the 95% confidence region to account for the sampling variations.

For most quantiles , the numbers in column (I) are located around the middle between the numbers shown in columns (II) and (III). Furthermore, those numbers in column (I) are also located around the middle of the set estimates shown in column (IV) and the 95% confidence regions shown in column (V). Column (I) indicates that GRT obtain significant effects across all the quantiles. Column (II) implies that the significant positivity may disappear, depending on which selection of the interval-valued outcomes we take. Column (III) implies that we may get even larger and more significant effects than those reported by GRT, depending on which selection of the interval-valued outcomes we take. Columns (IV) and (V) show that the range of effects that we could get out of all the potential selections in the interval-valued outcome is large, and of course contains those numbers reported in columns (II) and (III) in particular. Previous results depend on the assumptions made on the selection mechanism (e.g., taking the middle point). Our analysis shows that different assumptions on the selection can lead to quite different results.

6 Summary

This paper investigates the identification of quantiles and of quantile regressions when the outcome variable is interval valued. We first identify the quantiles of a random set. The quantile set is shown to be identified by the containment and capacity quantiles. The sharpness of the identification set was shown when the set-valued outcomes are interval-valued. The identification argument for quantiles then is extended to set identification of quantile regression parameters. We show that a system of conditional moment inequalities, involving the cumulative containment and cumulative capacity functionals, characterize the identification set for quantile regression parameters. The sharpness of the identification set was shown when the set-valued outcomes are interval-valued.

Appendix

Appendix A Procedure of Inference for Quantile Regression Parameters

This appendix section provides the procedure of inference for quantile regression parameters based on the conditional moment inequality restrictions derived in Section 3.2 via the method of Andrews and Shi (2013). Recall that, if is a closed convex value random set, then identification set of the quantile regression parameters is characterized by the conditional moment inequalities

where the moment functions, and , are defined by

for . Recall also that this set is convex if the quantile regression function is linear in parameters .

Normalize the vector of covariates into , and define the sample moment functions and the sample variances by

for a function to be defined below. To bound the sample variance away from zero, we use

With , an approximated test statistic at is computed by

for some truncation number , where if and if .

Lemma 1 of Andrews and Shi (2013) guarantees that our definition of satisfies Assumptions S1–S4 in their paper. Likewise, Lemma 3 of Andrews and Shi (2013) guarantees that the choice of defined above satisfies Assumptions CI and M in their paper. In order to assure that we can use the method of Andrews and Shi (2013), it remains to check their condition (2.3). The following conditions suffice: is i.i.d.; ; ; ; and ; where , , and .

To compute the critical value for , generate bootstrap samples for . For each bootstrap sample , compute and for . For each bootstrap sample, compute the bootstrap test statistic

where is given by

Andrews and Shi (2013) recommend , , and . The critical value is set to be the sample quantile of the bootstrap test statistics. Thus, a nominal level confidence set is approximated by

Because finding the approximate region for this set is computationally burdensome when the dimension of the parameter set is large, we provide in Appendix B an efficient algorithm to compute the estimate of the identification set.

Appendix B Set of Best Linear Predictors

In this section, we present a novel set programming method for ease of implementation of obtaining set estimate for linear quantile regressions, as motivated for practical ease fo finding the approximate region at the end of Appendix A. We focus on the linear quantile regression model, . We define the identification region for the best linear predictors (BLP) by extending Koenker and Bassett (1978) for the case of interval valued . In addition, we show in Theorem B.1 that the identification region for the BLP model is a superset of the identification region defined in (3.3) for linear models. This result is important since finding the identification defined in (3.3) is challenging relatively to finding the identification region for the BLP model. Therefore, one can start by finding the identification region for the BLP model and use this superset as a starting region where we should look for the identification region of Section 3.2.

For a given selection , we can estimate the associated parameters by minimizing the risk

| (B.1) |

where . (See Koenker and Bassett (1978) and Koenker (2005)). We propose that the identification set be approximated by

In appendix B.3, we provide some useful geometric properties of this set of best linear predictors. More importantly, we show in the theorem below that it is useful to locate the identification set .

Theorem B.1

If , then .

Proof.

Suppose that . In other words, -a.s. for a selection . Taking the gradient of with respect to , we have

where the last equality follows from our choice of satisfying -a.s. Therefore, we obtain . Since is convex, this implies . ∎

The other direction of set inclusion does not hold. While the identification set contains only those parameter vectors that correctly specify the quantile regression for some , the approximate set contains many other parameter vectors which only allow to be a best linear predictor for some . By Theorems B.1, the approximation set does not miss any element of the identification set . Therefore, we propose to first compute this set of best linear predictors, and conduct the test of conditional moment inequalities on and around this set. If the identification set is empty, then the parametric quantile regression model is misspecified, and trivially contains . In this case of misspecification, the set of best linear predictors itself may be of use for best linear prediction and for causal inference – see Angrist, Chernozhukov, and Fernández-Val (2006) and Kato and Sasaki (2017). The remainder of this section is devoted to a computational algorithm to obtain the approximation set .

B.1 Linear Programming

Since a random set can be viewed as a collection of regular random variables, we start by reviewing the regular random variable case. It seems logical that what we define for random sets should yield a regular quantile regression for singleton random sets.

The canonical LP problem is written as the following constrained minimization problem,

where is a matrix, is a vector of coefficients, is a vector of right-hand side constraints, and is a vector of unknowns. It is assumed that .

Consider a finite random sample of observations. Let be the vector of outcomes, be the matrix of covariates (which includes a column of ones). We can solve the least absolute deviation problem corresponding to the -quantile regression by using the following linear programming problem,

| (B.3) | |||

The vector consists of the coefficients of the linear -quantile regression, while and are slack parameters (variables). The LP problem in (B.3) is labeled . The simplex algorithm provides a solution to the above problem. The first stage is to transform the linear programming problem in (B.3) into the canonical form. Note that (B.1) requires that all variables over which we minimize be positive while the coefficients in (B.3) are unrestricted. The first step requires the user to transform the problem into the form in (B.1). So at first, we can write (B.3) as

where , , , , and . The first coordinates of are unrestricted while the last coordinates are restricted to be non-negative. Some software packages handle this kind of almost canonical form (e.g. Matlab) but some more traditional code may not. Assume w.l.o.g. that the first rows of the matrix form a full rank (and thus invertible) matrix. Denote this matrix by and similarly denote by , and the first lines of the the corresponding column vectors , and . Denote by , , and the remaining rows of these matrices and vectors. The first equations in as well as the unconstrained variable can be eliminated by writing and substituting into these first equations in . The remaining equations then can be written as

Therefore, the problem in (B.1) can be written as

where , , , and . Notice that the LP problem in (B.3) has variables and equality constraints and the LP problem in (B.1) has variables and equality constraints. Out of the solution for and in (B.1) we can of course recover the vector of interest by using .

For any ordered set , let denote the -th element of . For any ordered set of cardinality and for any -dimensional vector , we define the -dimensional vector whose -th coordinate is given by

for each . The simplex algorithm yields a solution with an ordered set of basic indices. Also let denote an ordered set of non-basic indices. It is required that , , , and . Using these notations, the solution is explicitly written as the -dimensional vector . Optimality requires and feasibility requires that . The simplex algorithm prescribes an efficient computational procedure to find such an index set satisfying these requirements.

B.2 Set Linear Programming

A simple brute force approach to set estimation of is to obtain the solution to the optimization problem (B.1) for each , and to take the union where . However, this exhaustive approach (even with a lattice approximation) is computationally intensive. In this light, we use some convenient properties of linear programming to propose a faster algorithm to compute the set estimate for .

Pick . The simplex algorithm yields a solution with an ordered set of basic indices. Also let denote an ordered set of non-basic indices. The solution is explicitly written as the -dimensional vector . The next proposition shows that there is a set containing such that the set of basic indices for (B.1) remains unchanged for all . Therefore, once we solve (B.1) for , we do not need to solve (B.1) again for any other , and we thus tremendously save our computational resources.

Proposition B.2

A solution to (B.1) is given by for all where . In particular, .

Proof.

We have by the definition of and as the sets of basic and non-basic indices, respectively, at the solution to (B.1) with . Notice that does not depend on in (B.1). Hence, any feasible vertex of the constraint set having non-zero elements only for those indices in is optimal for (B.1). Consider (B.1) with . A vertex having non-zero elements only for those indices in is written as . It is feasible if , which is true if and only if . Therefore, a solution to (B.1) is given by for all such that . ∎

In light of this proposition, we propose the following procedure. For any , let

be two -dimensional subvectors of the solution . We can then directly compute the estimate of corresponding to this by . Thus, we construct the subset estimate

Since this subset estimate is an image of through a simple linear transformation, it conveniently circumvents the need to solve the optimization problem for each . Once this subset estimate has been computed, pick , use the simplex algorithm to get the set of basic indices under , and obtain the resultant subset estimate . This is followed by the third step where produces the subset estimate , and so on. Repeat this process to obtain the set estimate for steps until we exhaust .

B.3 Geometric Properties of the Set of Best Linear Predictors

In this section, we provide some geometric properties of the set of best linear predictors proposed in Section B. It is shown that the set of connected, and therefore a projection of the set to each coordinate is interval-valued. To show this property, we go through several auxiliary lemmas. For the sake of rigorous proofs, we now formally define categorical sets and interval-valued sets below.

Definition B.1

A random set is categorical if we have either or for all pairs

Definition B.2

A random set is interval-valued if is an interval for all .

For a random set , define the restricted set of selections

We first state the following auxiliary lemma of CDF equivalence for interval-valued categorical random sets.

Lemma B.1

Proof.

Define the set . Let . By the strict increase of for , we can write where by the definition of . Since and is an interval-valued categorical random set, we the obtain by the monotone property of probability measures.

Assume by way of contradition that . Since is increasing and is interval-valued, this implies either for all or for all . Without loss of generality, we consider the former case, which can be rewritten as for all , where for a short-hand notation. Consider a decreasing sequence such that . Since , we have where the last set has a zero probability measure by the continuity of . Apply the continuity theorem of probability measures to the decreasing sequence , we obtain Combining this result with the conclusion from the last paragraph, we obtain a contradiction. Similarly, the case of for all leads to a contradiction. Therefore, holds.

A symmetric argument by interchanging the roles of and shows that implies . Therefore, follows. ∎

Lemma B.2

Proof.

Define by . First, we show that is measurable. is continuous and strictly increasing on its support because . Therefore, has a strictly increasing inverse by Pfeiffer (1990, pp. 266), and it follows that . Since and are continuous and is measurable, it follows that is measurable.

Second, we show that is a selection of . Let . Because , we have . Thus, we obtain , where the first equality is due to the definition of and the last equality is due to Lemma B.1. Taking a convex combination yields . Therefore, it follows that , showing that is a selection of .

Finally, we show that . This claim follows from the following chain of equalities: where the first equality is by the definition of the cdf , the second equality is due to the definition of , the third equality is by the short-hand notation for , and the last equality uses by the probability integral transform. Therefore, we have . ∎

We now consider the joint random set and extend the restricted set of selections to

Similar lines of a proof to those of Lemma B.2 yield the following extension to Lemma B.2.

Lemma B.3

Proof.

For each , let . Consider the restrictions , and of , and , respectively, to the domain . Because is a measurable subset of due to the measurability of , the restrictions and are also measurable functions. Furthermore, and are selection of because they are restricted to the identical domain . Therefore, by Lemma B.2, there exists a selection of such that .

Define the function by the rule of assignment . Further, define the function by the rule of assignment . We have because the previous paragraph concluded that is a selection of for each . Because is a measurable function for each from the previous paragraph and is countable, this is a measurable function. But then, is also a measurable function. It also follows from the conclusion of the previous paragraph that . These arguments together show that the desired conclusion holds. ∎

The condition that the support of is countable is restrictive, but is needed in our proof. This condition guarantees that is a measurable function. Without this condition, it is not clear if the same conclusion remains due to the fact that a sigma field is closed only under countable unions.

Now, for a random vector , we consider the best linear predictor defined by

where and is a convex and compact set.

Lemma B.4

Proof.

Lemma B.3 shows that there exists such that . Furthermore, and the strict convexity of and in imply that is strictly convex. ∎

Lemma B.5

Suppose that has a countable support. If is compactly supported and admits a conditional density for each , then is twice continuously differentiable in with

Proof.

We first modify the check function by

With this modification, we have due to the compactness of and . We can write the BLP objective as

where and ‘’ denotes the convolution operator. Since is clearly twice continuously differentiable with respect to with its first and second derivatives given by and , respectively, it suffices to show that is twice continuously differentiable with its first and second derivatives given by and , respectively. But this desired property follows from the fact that and implies with for each , , and our condition that admits for each . ∎

We now define the set of best linear predictors by

for

where the condition is given below.

Condition 1

(i) is continuous and strictly increasing on for each .

(ii) is compactly supported.

(iii) admits a conditional density function for each .

(iv) are strictly convex in .

Proposition B.3

Proof.

Let . By Lemma B.3, for any , there exists such that . Condition 1 (ii) and (iii) are satisfied by such a selection due to . Furthermore, Lemma B.4 shows that such a selection also satisfies Condition 1 (iv). Therefore, .

Let be an open subset of , , and be an open subset of . Define the function by , which is guaranteed to exist by Lemma B.5. Note also that , and Lemma B.5 show that for each .

First, observe that for each there is exactly one satisfying due to Lemma B.4. Second, the local solvability (i.e., the existence of a continuous explicit function at each ) follows from the implicit function theorem with Lemmas B.4 and B.5. Third, for each compact subset of , implies that holds for some by the condition of the proposition. Therefore, by Theorem 1 of Sandberg (1981), the map from into is continuous. Also, this continuity extends to the domain by the definition of and Lemma B.5.

Therefore, is path-connected, and is therefore connected. ∎

Appendix C Estimation and Inference under Discrete Intervals

This appendix section provides additional estimation and inference results that are relevant to a part of the procedure used in the empirical application in Section 5. Assume that are independently and identically distributed. Let and let and be the order statistics of and , respectively. For , let denote the biggest integer smaller than . Then, for , define

to be our estimators of the lower bound and upper bound of , respectively. Specifically, we define as our estimator for .

In many surveys, the respondent is given a list of brackets to choose from. In this case both and are discrete random variables. Assume , and hence by Theorems 2.1 and 2.2, where and vary discretely. In the current appendix section, we define the set estimator by , where denotes the smallest integer greater than .

C.1 Super-Consistency

By Theorem 2 of Ramachandramurty and Rao (1973), we have

as , if as . Note that can diverge at an arbitrary rate as a function of – even faster than . Thus, we obtain the following result by the continuous mapping theorem.

Theorem C.1

Suppose the random set takes the form -a.s. where and are discretely distributed. If , are independently and identically distributed, then for

for as , where and denote the Hausdorff distance and the directed Hausdorff distance, respectively.555 For two sets, and , in a finite dimensional Euclidean space , the directed Hausdorff distance from to is and the Hausdorff distance between and is

Theorem C.1 suggests that the estimator for the identification region when is a discrete random set is super-consistent. Super-consistency is useful in cases where estimating a discrete quantile set is just a first step in a two-step estimation procedure. On the other hand, a drawback to this result is that we do not obtain a root- non-degenerate asymptotic normal distribution. The next subsection provides a modified estimator with a root- non-degenerate distribution.

C.2 Non-Degenerate Asymptotic Distribution

The lack of the ability to conduct inference with the naive quantile estimators is unfortunate. However, in the special case where the discrete boundaries, and , of the random set are given as a count data, we can allow for inference even in the discrete case by using the idea of Machado and Silva (2005). Suppose that and are supported in the set of cardinality . Construct the random variables and where and is independent of . Let denote the joint cumulative distribution function of , which is identified from the two-dimensional convolution of the distributions of and . As a result of the convolution, the distribution of is differentiable infinitely many times on . Furthermore, the above construction of the mixture distribution yields the marginal quantiles relations

See Machado and Silva (2005). As such, we can define a new set estimator by

where and denote the empirical mass for each . Note that, in this estimator, we distinguish the -consistent estimator and the aforementioned super-consistent estimator -consistent estimator on purpose

To analyze the asymptotic distribution of this estimator , we first need the joint asymptotic distribution of the -dimensional vector which consists stochastic element of the boundaries of the set estimator. For any such that ,

| (C.1) |

where is a matrix which is completely expressed in (C.6) in Appendix C.3. If and , then we therefore obtain

| (C.2) |

where is a matrix, where the first row takes the form

and the second row takes the form

From this asymptotic joint normal distribution, we obtain the following theorem that can be used for inference on random sets where the boundaries are counts.

Theorem C.2

Suppose the random set takes the form -a.s. where both and are discretely distributed with support contained in . Construct the random variables and where and is independent of . For any such that , , and ,

| (C.3) | |||

| (C.4) | |||

| (C.5) |

where the random vector is distributed according to (C.2).

C.3 The variance matrix

In this section, we give a complete expression for the matrix, which is a component of the asymptotic normal distribution for the -dimensional vector . See (C.1).

is a matrix

| (C.6) |

is a matrix of the form

and is a are matrices of the forms

and are a matrices of the forms

and are matrices of the forms

and is a matrix of the form

References

- Andrews and Shi (2013) Andrews, D. W., and X. Shi (2013): “Inference Based on Conditional Moment Inequalities,” Econometrica, 81(2), 609–666.

- Angrist, Chernozhukov, and Fernández-Val (2006) Angrist, J., V. Chernozhukov, and I. Fernández-Val (2006): “Quantile Regression under Misspecification, with an Application to the U.S. Wage Structure,” Econometrica, 74(2), 539–563.

- Beresteanu, Molchanov, and Molinari (2011) Beresteanu, A., I. Molchanov, and F. Molinari (2011): “Sharp Identification Regions in Models with Convex Moment Predictions,” mimeo.

- Beresteanu, Molchanov, and Molinari (2012) Beresteanu, A., I. Molchanov, and F. Molinari (2012): “Partial Identification Using Random Set Theory,” Journal of Econometrics, 166(1), 17–32.

- Beresteanu and Molinari (2008) Beresteanu, A., and F. Molinari (2008): “Asymptotic Properties for a Class of Partially Identified Models,” Econometrica, 76(4), 763–814.

- Belloni, Bugni, and Chernozhukov (2018) Belloni, A., F. Bugni, and V. Chernozhukov (2018) “Subvector Inference in Partially Identified Models with Many Moment Inequalities,” mimeo.

- Bugni and Shi (2018) Bugni, F., and X. Shi (2018) “Inference for Functions of Partially Identified Parameters in Conditional Moment Inequality Models,” mimeo.

- Cameron and Huppert (1989) Cameron, T. A., and D. D. Huppert (1989): “OLS Versus ML Estimation of Non-Market Resource Values with Payment Card Interval Data,” Journal of Environmental Economics and Management, 17(3), 230–246.

- Chaudhuri (1991) Chaudhuri, P. (1991): “Nonparametric Estimates of Regression Quantiles and Their Local Bahadur Representation,” Annals of Statistics, 19(2), 760–777.

- Chesher (2005) Chesher, A. (2005): “Nonparametric Identification under Discrete Variation,” Econometrica, 73(5), 1525–1550.

- Chesher (2010) Chesher, A. (2010): “Instrumental Variable Models for Discrete Outcomes,” Econometrica, 78(2), 575–601.

- Chesher and Rosen (2015) Chesher, A., and A. M. Rosen (2015): “Characterizations of Identified Sets delivered by Structural Econometric Models,” CeMMAP Working Paper CWP63/15.

- Gamper-Rabindran and Timmins (2013) Gamper-Rabindran, S., and C. Timmins (2013): “Does Cleanup of Hazardous Waste Sites Raise Housing Values? Evidence of Spatially Localized Benefits,” Journal of Environmental Economics and Management, 65(3), 345–360.

- Guerre and Sabbah (2012) Guerre, E. and C. Sabbah (2012): “Uniform Bias Study and Bahadur Representation for Local polynomial Estimators of the Conditional Quantile Function,” Econometric Theory, 26 (5), 1529–1564.

- Hong and Tamer (2003) Hong, H., and E. Tamer (2003): “Inference in Censored Models with Endogenous Regressors,” Econometrica, 71(3), 905–932.

- Kaido, Molinari and Stoye (2016) Kaido, H., F. Molinari, and J. Stoye (2016): “Confidence Intervals for Projections of Partially Identified Parameters,” arXiv:1601.00934.

- Kato and Sasaki (2017) Kato, R., and Y. Sasaki (2017): “On Using Linear Quantile Regressions for Causal Inference,” Econometric Theory, 33(3), 664–690.

- Khan and Tamer (2009) Khan, S., and E. Tamer (2009): “Inference on Endogenously Censored Regression Models Using Conditional Moment Inequalities,” Journal of Econometrics, 152(2), 104–119.

- Koenker (2005) Koenker, R. (2005): Quantile Regression, Vol. 38 of Econometric Society Monographs. Cambridge University Press.

- Koenker and Bassett (1978) Koenker, R., and G. Bassett (1978): “Regression Quantiles,” Econometrica, 46(1), 33–50.

- Li and Oka (2015) Li, T., and T. Oka (2015): “Set Identification of the Censored Quantile Regression Model for Short Panels with Fixed Effects,” Journal of Econometrics, 188(2), 363–377.

- Machado and Silva (2005) Machado, J. A., and J. S. Silva (2005): “Quantiles for Counts,” Journal of the American Statistical Association, 100(472), 1226–1237.

- Manski (1985) Manski, C. F. (1985): “Semiparametric Analysis of Discrete Response: Asymptotic Properties of the Maximum Score Estimator,” Journal of Econometrics, 27(3), 313–333.

- Manski and Tamer (2002) Manski, C. F., and E. Tamer (2002): “Inference on Regressions with Interval Data on a Regressor or Outcome,” Econometrica, 70(2), 519–546.

- Molchanov (2005) Molchanov, I. (2005): Theory of Random Sets. Springer Verlag, London.

- Molchanov (1990) Molchanov, I. S. (1990): “Empirical Estimation of Distribution Quantiles of Random Sets,” Theory of Probability and its Applications, 35(3), 594–600.

- O’Garra and Mourato (2007) O’Garra, T., and S. Mourato (2007): “Public Preferences for Hydrogen Buses: Comparing Interval Data, OLS and Quantile Regression Approaches,” Environmental and Resource Economics, 36(4), 389–411.

- Pfeiffer (1990) Pfeiffer, P. E. (1990): Probability for Applications. Springer.

- Powell (1984) Powell, J. (1984): “Least Absolute Deviations Estimation for the Censored Regression Model,” Journal of Econometrics, 53(3), 303–325.

- Qu and Yoon (2015) Qu, Z. and J. Yoon (2015): “Nonparametric Estimation and Inference on Conditional Quantile Processes,” Journal of Econometrics, 185 (1), 1–19.

- Qu and Yoon (2018) Qu, Z. and J. Yoon (2018): “Uniform Inference on Quantile Effects under Sharp Regression Discontinuity Designs,” Journal of Business and Economic Statistics, forthcoming.

- Ramachandramurty and Rao (1973) Ramachandramurty, P., and M. S. Rao (1973): “Some Comments on Quantiles and Order Statistics,” Canadian Mathematical Bulletin, 16(2), 289–293.

- Rosen (2012) Rosen, A. M. (2012): “Set identification via Quantile Restrictions in Short Panels,” Journal of Econometrics, 166(1), 127–137.

- Sandberg (1981) Sandberg, I. W. (1981): “Global Implicit Function Theorems,” IEEE Transactions on Circuits and Systems, 28(2), 145–149.

(I)

(II)

(III)

| (I) | (II) | (III) | (IV) | (V) | |||

|---|---|---|---|---|---|---|---|

| GT (2013) | Set Estimate | 95% CR | |||||

| 0.10 | 0.244 (0.086) | -0.709 (0.196) | 1.260 (0.196) | [-10.780 | 11.331] | [-11.877 | 12.473] |

| 0.20 | 0.214 (0.085) | -0.506 (0.123) | 0.945 (0.123) | [-5.390 | 5.829] | [-6.185 | 6.626] |

| 0.30 | 0.211 (0.084) | -0.201 (0.076) | 0.868 (0.076) | [-3.093 | 3.760] | [-3.727 | 4.408] |

| 0.40 | 0.210 (0.083) | -0.019 (0.040) | 0.534 (0.040) | [-2.047 | 2.563] | [-2.421 | 3.013] |

| 0.50 | 0.208 (0.083) | -0.013 (0.038) | 0.484 (0.038) | [-1.635 | 2.106] | [-2.052 | 2.541] |

| 0.60 | 0.205 (0.084) | 0.046 (0.017) | 0.402 (0.017) | [-1.366 | 1.814] | [-1.637 | 2.127] |

| 0.70 | 0.198 (0.085) | 0.062 (0.018) | 0.343 (0.018) | [-1.271 | 1.677] | [-1.496 | 1.970] |

| 0.80 | 0.187 (0.081) | 0.057 (0.017) | 0.180 (0.017) | [-1.212 | 1.449] | [-1.360 | 1.635] |

| 0.90 | 0.187 (0.077) | 0.054 (0.018) | 0.072 (0.018) | [-1.214 | 1.341] | [-1.329 | 1.461] |