A particle model for the herding phenomena induced by dynamic market signals

Abstract.

In this paper, we study the herding phenomena in financial markets arising from the combined effect of (1) non-coordinated collective interactions between the market players and (2) concurrent reactions of market players to dynamic market signals. By interpreting the expected rate of return of an asset and the favorability on that asset as position and velocity in phase space, we construct an agent-based particle model for herding behavior in finance. We then define two types of herding functionals using this model, and show that they satisfy a Gronwall type estimate and a LaSalle type invariance property respectively, leading to the herding behavior of the market players. Various numerical tests are presented to numerically verify these results.

1. introduction

Collective behaviors such as aggregation, fads, fashion, flocking and herding are frequently observed in nature [7, 8, 14, 16, 35] and society [5, 9, 19, 25]. Among these various types of collective behaviors, the flocking phenomena, in which alignment of the velocity occurs through the process of adjusting the velocity according to the particles around it, has seen tremendous progress recently. Several models have been suggested such as the Cucker-Smale model [16, 17] or Viseck model [34], and many successful mathematical theories have been developed to understand those models [13, 15, 21, 22, 23, 24, 30].

In this paper, we study the herding behavior arising in financial markets using a particle model. The term herding is used in several different contexts. The most basic meaning underlying them is the gathering behavior of individuals to form a group and move as a group. Therefore, unlike the flocking phenomena, the adjustment occurs also between position variables and, therefore, the interactions between position and velocity may play important roles in the dynamics. In finance and economy, herding is often used to describe the phenomena in which the market players tend more and more to follow the market trend even though one’s own opinion, information, favorability or instinct are against it [5]. The expression “information cascade” is also frequently used.

In traditional economics and finance, it is assumed that all agents are rational, and all the information is already reflected on the price (efficient markets hypothesis), which implies the absence of bubbles [4, 29, 31, 32]. However, as we can see in the examples of Tulip mania in 1637, the South Sea Bubble in 1711-1720, the stock market boom in 2000, and the financial crisis in US housing market in 2007, there have been many irrational events like bubbles and crashes. It is not clear whether these phenomena are caused solely by herding behavior of the market players, but herding definitely plays a crucial role in the formulation of such phenomena.

Previous works on herding behavior in finance were largely based on sequential analysis [4, 5, 6, 9, 10, 26, 27], in which the effect of the decision of the first player on the behavior of subsequent players was analyzed. (See Section 2.) In this paper, we study the herding phenomena arising from concurrent reaction to other players and dynamic market signals. By the word “dynamic”, we mean either (1) the signal changes with time, or (2) the signal is determined by the dynamics of market players.

For this, we introduce two variables: : the rate of return of assets over time expected by th market player, and : the favorability that th market player has on those assets at time . These two variables play the role of position and velocity of a self-propelled particle in the phase space, and enable one to derive a particle model giving dynamical relations between the rate of return, favorability and the market signal. (See Section 2.) We then analyze the herding properties of the system by deriving two Lyapunov type herding functionals satisfying a Gronwall type inequality and LaSalle type invariance conditions respectively. (See Section 3, 4, 5.)

In flocking models, the occupation of the same place by several particles is considered to be undesirable [2, 12, 16, 17]. In contrast, we allow “particles” to occupy the same and . Such overlap corresponds to the emergence of consensus on the expected rate of return and the favorability on specific assets, which is exactly what we try to model.

The outline of this paper is as follows: In Section 2, we derive a particle model describing herding phenomena induced by dynamic market signals. A motivation of our model from the perspective of a pricing model in finance is also given. In Section 3, our main herding theorems are presented. Section 4 and Section 5 are then devoted to the proof of the main results. In Section 6, we provide some relevant numerical simulations. The conclusion and possible future projects are discussed in Section 7.

2. Particle model for herding behavior in finance

Suppose there are market players and assets, such as stocks or real estimates. For simplicity we assume that no new players or assets enter or leave the market. We then define and , in the following way:

-

•

: the rate of return of the assets expected by market player over time .

-

•

: the favorability that market player has on those assets at time .

We denote and .

It is natural to assume that the market players may consider the value of the asset in a more favorable way if the expectation on the rate of return rises, and the opposite when the rate of return decreases. In this regard, we relate and by

To describe the dynamics of , we assume that the market players are very sensitive to market trend and imitative strategy prevails in the market, which is believed to be true by both economists and market participants up to certain level. We formulate this assumption by postulating that the favorability is affected by other player’s assessment in the following three ways:

-

(1)

Other players’ evaluation on the expected rate of return for the assets:

-

(2)

Other players’ favorability on the assets:

In (1) and (2), is the communication rate between player and player , whose precise form will be given below.

-

(3)

Various types of signals from the market also influence players’ opinion and decision. Such an influence can be observed more clearly when the market is experiencing a rapid transition or turmoil such as the 1997 Asian financial crisis and the subprime mortgage crisis in 2008, to name a few. To systematically formulate such signals, we introduce a function , which we call the “dynamic market signal”, and assume that the favorability on the asset is affected by how big the difference is between the expected return and the signal:

Explicit examples of will be considered below.

By combining the above three effects, we derive our main model:

| (2.1) | ||||

where , and are interaction strength.

Several choices can be made for the communication rate , which determine how strongly a player’s expected rate of return and favorability are influenced by those of other players in the market. Throughout this paper, we use

for We remark that the effect of noise should be considered for this model to be more realistic:

where is the volatility and is -dimensional Brownian motion. Throughout this paper, however, we neglect the effect of noise and consider only for simplicity and clarity. We leave it as a future project.

Examples of the dynamic market signal : We can choose various types of mathematical expressions for the dynamic market signal depending on the market situation. Some of the financially interesting examples are:

-

(a)

A sweeping trend of the market that the market players cannot handle. (Ex: abrupt upheaval in the market such as economic crisis or the rise and fall of foreign currency exchange rate) In this case, we set

to be a given function of time.

-

(b)

Asymmetric information or signal from an informed influential market player like Warren Buffett. Without loss of generality, we fix to be such influential player so that we can set

That is, the rate of return expected by an influential player is a strong affecting factor in the market

-

(c)

Average market expectation, market atmosphere or some average index such as Dow Johns index, which is believed to reflect such average market expectation, in which case we can define

We will show that the herding behavior induced by these signals can be explained in a unified manner. (See Section 3.)

Financial motivation of the model: We now provide a financial motivation of our model (2.1). For that, we recall the geometric Brownian motion for an asset price :

where is the instantaneous expected rate of return, the volatility and the one-dimensional Brownian motion. We then apply Ito’s formula:

and take expectation to to get

or equivalently,

| (2.2) |

According to [28], the expected rate of return is generated by the following stochastic differential equation

| (2.3) |

where the first term represents a long-run regressive adjustment of the expected rate of return toward a normal rate of return with the adjustment speed , and the second term is a short-run extrapolative adjustment of the expected rate of return of the error-learning type with the adjustment speed . Coupling (2.3) with (2.2), we get the following system:

This can be generically extended to multi-variable system:

Rewriting by and taking , we may express this as a particle model:

Now, if we make the following choice:

we recover our herding model (2.1) with and .

Brief review of the studies in Finance on Herding: Herding behavior in finance has been extensively studied in the literature including [4, 5, 6, 9, 10, 27]. Herding behavior is associated with people blindly following the decisions of others [10]. Imitating somebody’s action can be rational if the predecessor’s action affects one’s (1) payoff structure such that imitation leads to a higher payoff (payoff externality) and/or (2) his probability assessment of the state of the world such that it dominates the private signal (informational externality). Herding due to informational externalities occurs if an agent imitates the decision of his predecessor even though his own signal might advise him to take a different action. This herding can also lead to informational cascades. In [5], the concepts of investor herding and informational cascade are defined:

-

•

An informational cascade occurs in a period when

-

•

A trader with private information engages in herd behavior at time if he buys when or if he sells when ; and buying (or selling) is strictly preferred to other actions.

Here, means the conditional probability, denotes the value of the new information, is the history of actions until time , and is the action (buy or sell) taken by the trader (market player) who arrives in period , is the private information of trader , is the market maker’s expected value for the asset given public information, which we sometimes refer to as the price, and is the expected value of an informed trader .

In an informational cascade, new information on the asset does not affect the decision of the market players. The above technical definition in [5] of the buying herding behavior can be expressed in the following three steps: (1) Initially a trader’s evaluation is less than the market value of the asset, so that he is inclined to sell. (2) The market value of the asset is, nevertheless, increasing. (3) The trader must want to buy the asset ignoring his own evalution. Also in [5], it is shown that whether or not herd behavior affects asset prices, asset prices can certainly affect herd behavior.

Even though it can make a large difference whether the market players decide sequentially or simultaneously, most herding models are studied sequentially. Up to the best knowledge of authors, particle model interpreting it as a dynamical system that reacts concurrently to other players and the market signal has not been proposed. A related study can be found in [1, 3], where the flocking behavior of volatility is considered using Cucker-Smale type models.

As related works, we mention [18, 20], where Boltzmann type kinetic equations were suggested to model the dynamics of a market and understand the formation of bubbles and crashes through the combined effect of public information and herding (See also [33].), and [11] in which a macroscopic herding model of Keller-Siegel type was introduced to simulate herding behaviours of human crowds.

3. Main results

In this section, we present our main results. We start with some simplification of our model for the convenience of proof.

3.1. Centralized herding model:

We first record a simple result on the averaged motion and . Let , denote the average expected rate of return and the average favorability respectively:

These averaged quantities evolve according to the following simple system:

Lemma 3.1.

and satisfy

Proof.

Since for all , we have from symmetry argument

| (3.1) |

Using these identity with , we get the desired result by summing (2.1) over . ∎

We will show that the large time behavior of is governed by . In view of this, we replace

in our model (2.1) to get

| (3.2) | ||||

where . Note that

| (3.3) |

From now on, we study only this centralized version for clarity and simplicity.

3.2. Two herding functionals:

We define two kinds of herding energies and and prove their decay property. is defined on a rather stringent assumptions on the parameters and initial configuration, but an explicit exponential herding rate can be derived (Theorem 3.3). For , such explicit herding rate is not available, but restrictions on the parameters and initial configuration can be relaxed a lot (Theorem 3.6). To state our main theorem, we first need to define some notations to be kept throughout this paper.

-

•

deviation and covariance functionals:

and

-

•

Weighted deviation and weighted covariance functionals:

and

We define the herding behavior of market:

Definition 3.2.

Let be the solution to (3.2). Then, we say that the herding phenomena occurs if

We now state our main theorem.

3.3. Main result I - Exponential herding:

Define the herding energy of the market by

Theorem 3.3.

Let . Suppose the interaction strength , and satisfy

| (3.4) |

Assume that the initial configuration satisfies

| (3.5) |

and

| (3.6) |

where denotes

| (3.7) |

Then the herding functional decays exponentially fast:

where the decay rate is explicitly given by

and is a constant to be chosen in the proof. Moreover, we have

| (3.8) |

for all .

Remark 3.4.

An immediate corollary is that the market shows an exponentially fast herding phenomena.

3.4. Main result II - Herding without decaying rate:

We define another market energy that eventually vanishes even without any restrictions on and initial configurations. First, we define

| (3.9) |

Note that for all . Now, for any , we define the herding energy of the market by

where is

Theorem 3.6.

For any positive constants , and with initial data , goes to as tends to .

Remark 3.7.

This leads to the following general herding phenomena, which holds unconditionally.

Corollary 3.8.

Under the assumptions in Theorem 3.6, the herding phenomena occurs in the market:

4. Proof of Theorem 3.3: Exponentially fast herding

Before we delve into the proof of the main theorem, we establish several technical lemmas.

Lemma 4.1.

We have

Proof.

The first identity is immediate:

For the second one, we compute

Then, clearly,

In view of (3.1), we have

Similarly,

Therefore,

∎

We also need to consider the time evolution of :

Lemma 4.2.

For any

Proof.

See

Computation for is direct:

For , we consider

We then compute each term. clearly is

From (3.1) and a simple symmetry argument, we get

and

so that

∎

4.1. Proof of Theorem 3.3:

We divide the proof into the following two steps:

Step 1: Step 1 is devoted to the proof of the following claim:

Proof.

Recall the definition of in Corollary 3.5:

Then, by Lemma 4.1 and Lemma 4.2, we have

| (4.1) | ||||

Now, using

we obtain

Therefore, we have from (4.1)

We set for simplicity, and compute

| (4.2) | ||||

Since we are assuming

we have

for defined in (3.7). Therefore,

which gives from (4.2)

Finally, we go back to (4.1) with these computations to derive

| (4.3) | ||||

Next, we need to show that there exists such that

| (4.4) |

which is equivalent to find such that

This holds if

Recalling the definition of , it can be rewritten as

which holds true for sufficiently small . Now, with this choice of , we can combine (4.3) and (4.4) to close the desired Gronwall inequality:

∎

Step 2: We now prove that prolongs to infinity:

Claim: , that is,

for all .

Proof.

We first rewrite (3.5) as

and use the positivity of and to get

or, equivalently

With this and the fact that , which follows from the definition of , we see that

| (4.5) | ||||

Therefore, combining this with the result of Claim 1, we get,

| (4.6) |

Now, contrary to the claim, suppose that there are and such that

| (4.7) |

for some . Then, for any , we have from (4.6)

Therefore, applying the result of Step I, we deduce for

The last inequality is from (3.6):

In conclusion, we have

for all , which is contradictory to (4.7). Therefore, . This completes the proof. ∎

4.2. Proof of Corollary 3.5:

4.3. Proof of Remark 3.4

(1) It was shown in (4.5) that is positive under our assumptions in Theorem 3.3.

(2) We only consider the case where there are at least two players in the market, that is . For this, we define by

where the positivity of comes from (3.4). With this , we choose and as

and set all the remaining and to be zero. Since and , we can say and . Then, we have

Moreover, implies and does . Therefore,

In the last line, we used

and

5. Proof of Theorem 3.6: Herding without explicit decay rate

We start with establishing technical lemmas.

Lemma 5.1.

For any , we have

| (5.1) |

where is given by

Proof.

When , we have

For , we similarly compute

∎

Lemma 5.2.

For , we have

-

(1)

First derivative:

-

(2)

Second derivative:

-

(3)

Third derivative:

Proof.

(1) We differentiate and use Lemma 5.1 to get

Identities in (2) and (3) follow directly from differentiating in the r.h.s. ∎

Lemma 5.3.

Fix . Assume are all identical, but are not. That is,

Then the first, second derivatives of vanish at :

and the third derivative of is strictly negative at :

Proof.

is clear from Lemma 5.2 (1) and (2). For , recall from Lemma 5.2 (3) that, when are all identical, all but the third term in the r.h.s vanishes, yielding

| (5.2) |

Therefore, our goal is reduced to showing that the right hand side is not zero. For this, we note from (3.2) that

which, under our assumption of identical favorability, reduces to

Now, for a vector , let denote the th element of . That is, . Then from our assumption, we can find and such that

For such choice of and , we have

We now turn back to (5.2) with this observation to obtain the desired result:

∎

5.1. Proof of Theorem 3.6:

We first recall the following invariance principle by LaSalle [36]:

Definition 5.4.

[36] A set is said to be invariant if each solution starting in remains in for all . That is,

Theorem 5.5.

[36] Consider the system of differential equations

| (5.3) |

where and is a vector field. Let be a scalar function with continuous first partials for all . Assume that

Let be the set of all points where , and let be the largest invariant set contained in E. Then every solution of (5.3) bounded for all approaches as .

We now start the proof of Theorem 3.6. First, recall that the herding functional is non-negative:

and vanishes only when . We also have

| (5.4) |

The equality holds only when are all identical. (5.4) also implies the boundness of the solutions. Therefore, satisfies the conditions of Theorem 5.5. Now, define to be the null-space of :

Since we are considering the centralized model, and , actually is

Let be the largest invariance set in . In view of the above invariance theorem, our goal is to verify that is trivial:

| (5.5) |

For this, suppose contrarily that there exists an open interval and a solution to (3.2) in such that

Since by definition, we have

and by Lemma 5.3, the first and second derivative of vanishes while the third derivative remains strictly negative on :

Therefore, for any , we have from the Taylor’s theorem

which is a contradiction. This proves (5.5). The desired result then follows from Theorem 5.5.

6. Numerical Simulation

In this section, we present three numerical tests demonstrating the herding behavior in the market. In Test 1, we numerically verify Theorem 3.3 and Theorem 3.6 in the case (, ) with different choices of parameters and initial data. In Test 2, we present trajectories of the numerical solution to (3.2) for two dimensional problem () to visualize the herding phenomenon in multi-d case. In Test 3, we give two dimensional histograms for each variable and with for the simulation of large number of players. We employ a fourth-order Runge-Kutta method for the time evolution with fixed time steps in all simulations.

6.1. Numerical test 1

We recall three scenarios of the dynamic market signals presented in Section 2 and fix throughout test 1 as

For simplicity, we consider five market players and one asset .

In the numerical Test 1-1 and 1-2 below, the initial data have been chosen randomly, and the only difference is the choice of :

The choice means that initially market player has viewed the market positively, and choice means the opposite. This is to compare the influence of the assessment of the influential player on the market.

In Test 1-3, we consider the dynamics of solutions corresponding to an initial configuration that doesn’t satisfy the conditions of Theorem 3.3. We observe that essential features of Theorem 3.3 break down but the result of Theorem 3.6 still holds. It demonstrates that the conditions in Theorem 3.3 are essential. (See Remark 3.7.) Throughout Test 1-1 to 1-3, we consider numerical solutions to the non-centralized model (2.1) to clearly manifest the influence of on the herding dynamics.

6.1.1. Numerical test 1-1:

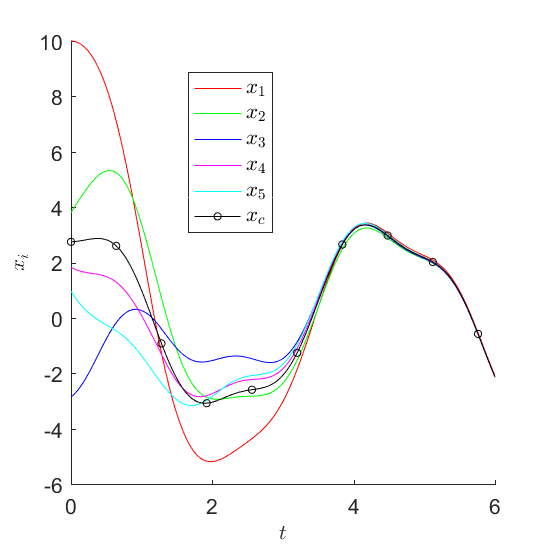

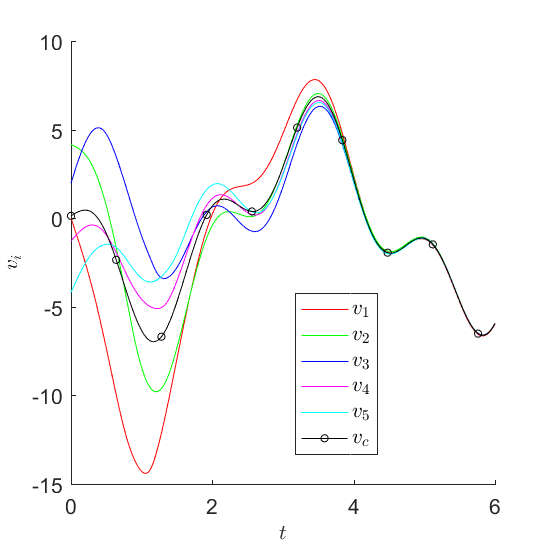

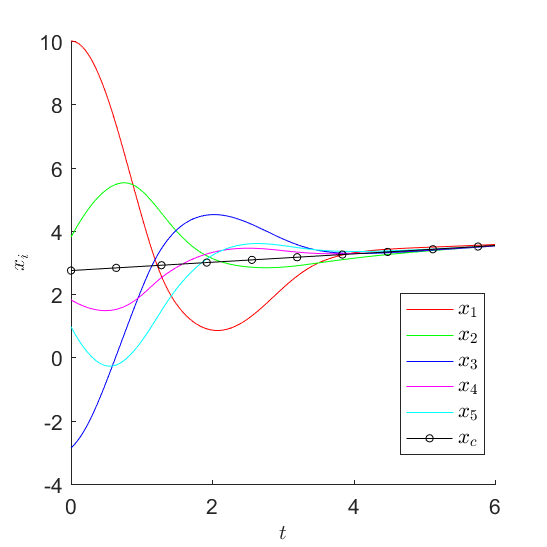

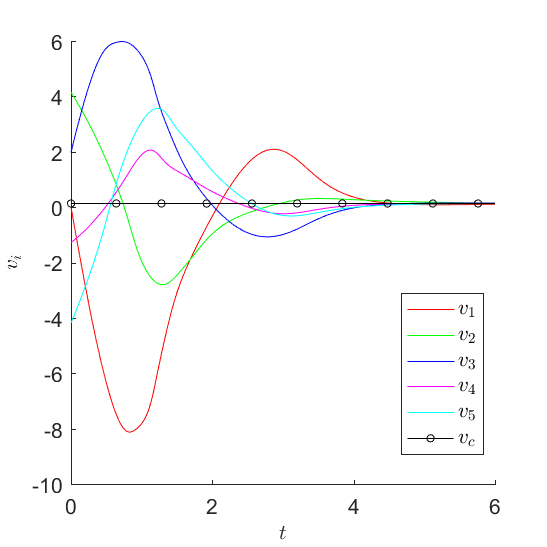

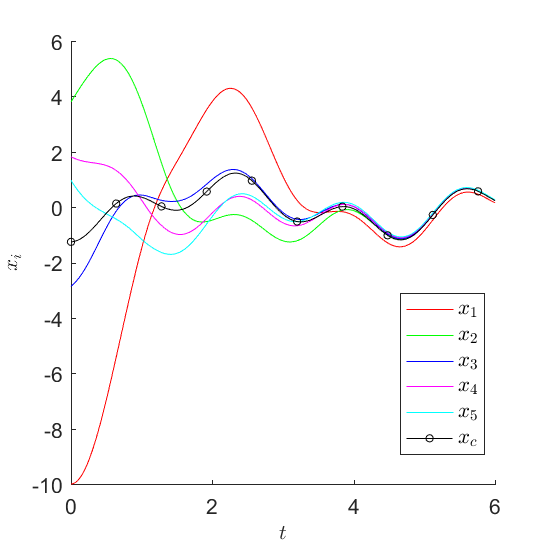

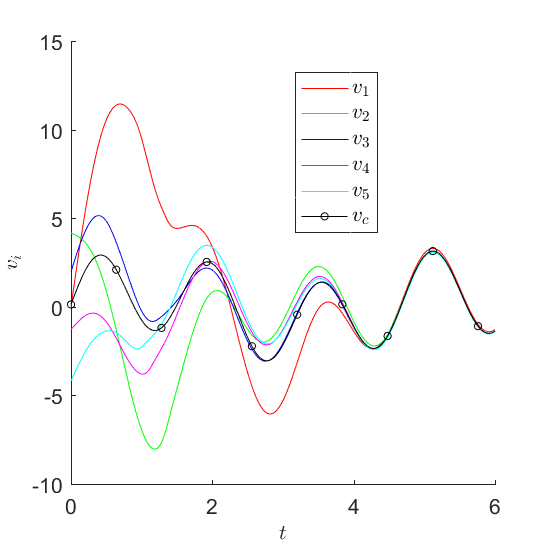

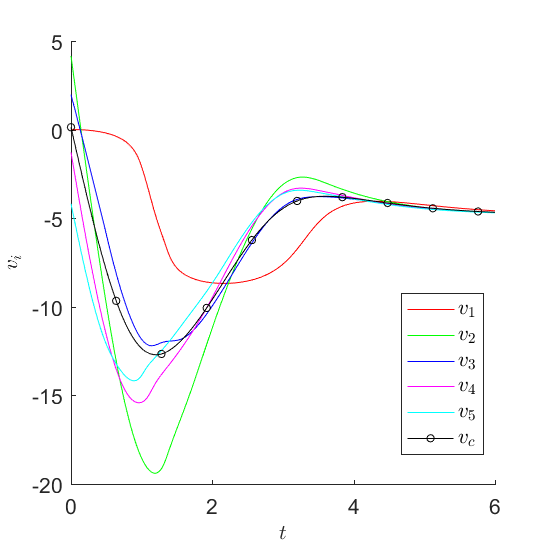

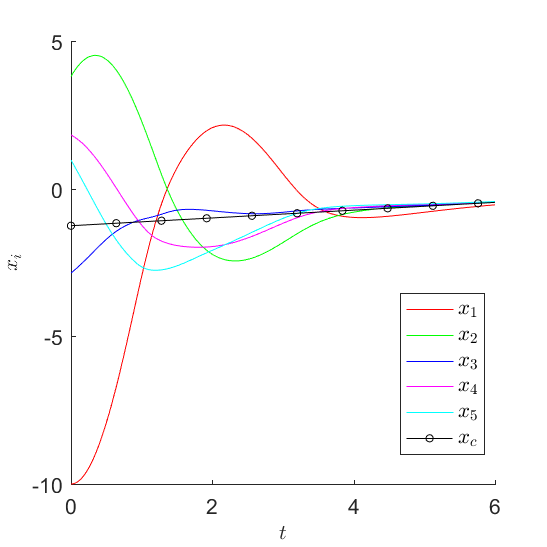

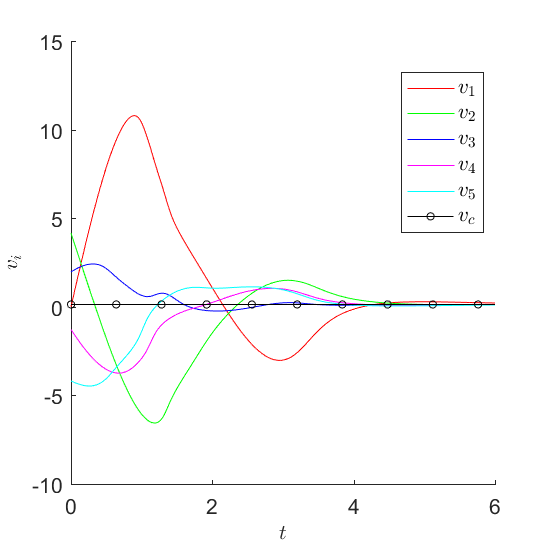

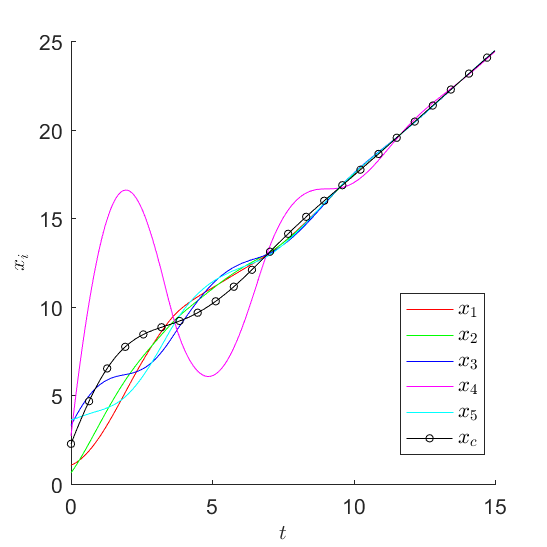

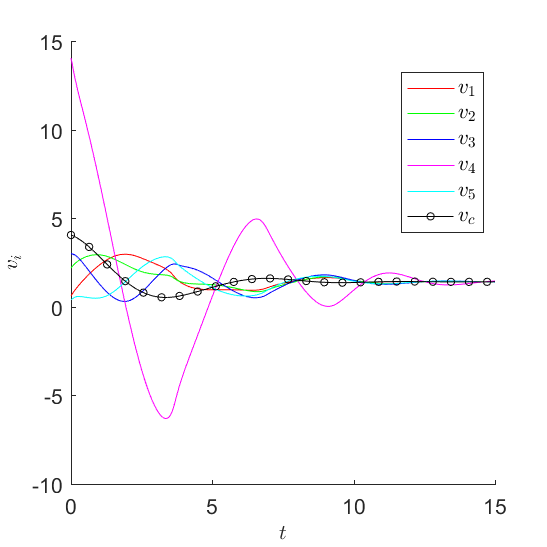

(The case of ) In this test, we choose , , and , which satisfy the parameter assumption (3.4). Initial data is randomly chosen in to satisfy (3.5) and (3.6) in Theorem 3.3. We obtain numerical solutions to the original non-centralized herding model (2.1) corresponding to each of the three scenarios and plot them in Figure 1,2 and 3, respectively. The final time is taken as .

In Figure 1, we plost and in the case of . We observe that tend to show similar patterns after . We also see that the average favorability moves up and down. Since the market signal has a oscillating pattern, it is natural to observe such situation in which the market players tend to change their minds frequently.

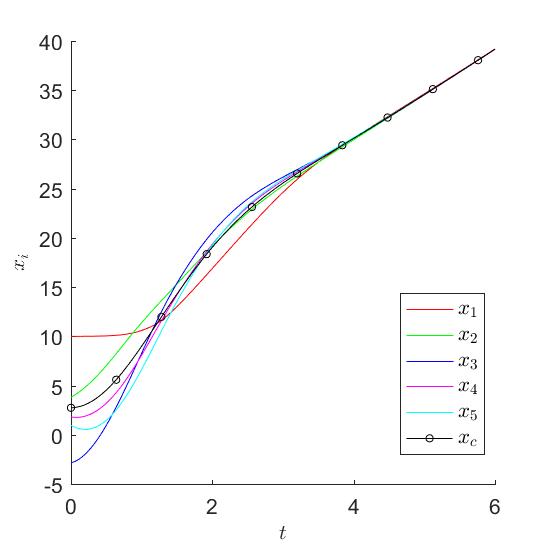

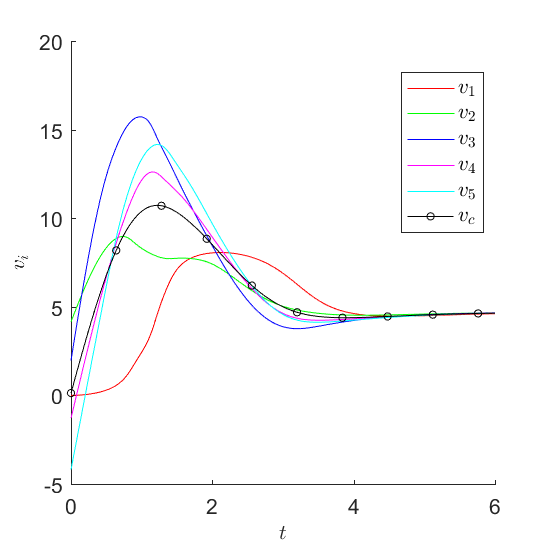

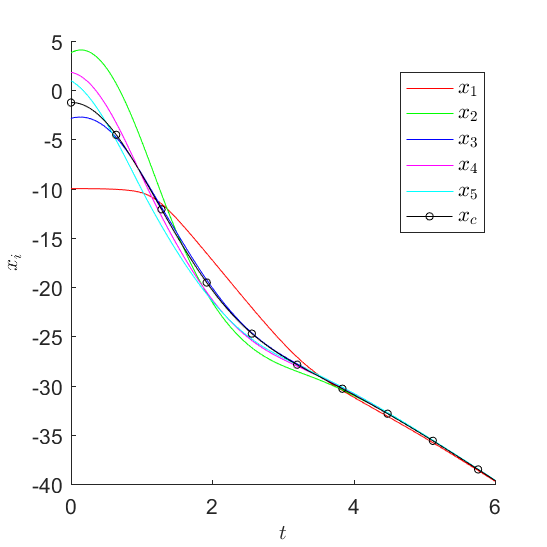

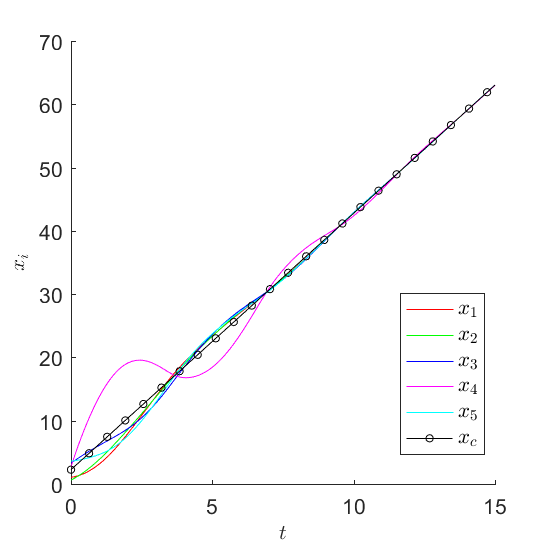

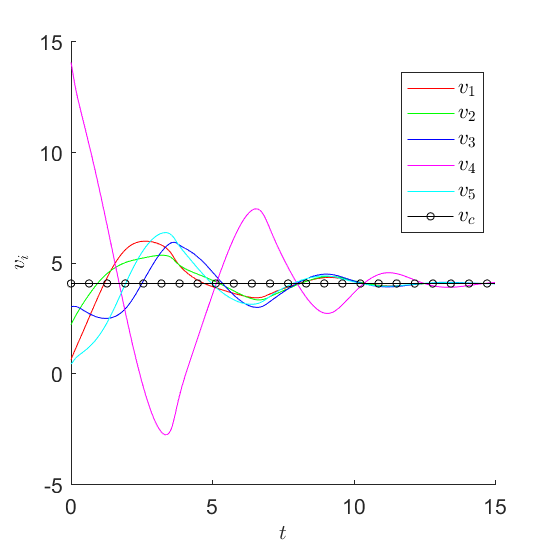

In Figure 2, the behaviors of and are provided when . We see that the numerical solution to the second scenario shows very different phase compared to those presented in Figure 1 even though they start with the same initial random data. After , each seems to converge to a fixed constant about , which leads to linear increase in .

In Figure 3, behaviors of are shown for . We observe that remains unchanged. Recalling Lemma 3.1 implies in this case, it is natural to have such a fixed constant . We can observe that it also shows the collective behaviors after .

6.1.2. Numerical test 1-2:

(The case of In this test, we replace as

with all the other initial configuration and parameters fixed. Note that the new initial condition also satisfies conditions of Theorem 3.3.

In Figure 5, 6 and 7, we plot the numerical solutions to (2.1) for each scenario upto , respectively. In all these figures, we observe the herding phenomenon in the expected rate of returns and favorabilities.

The main difference compared to the Test 1-1 is observed in Figure 6, where we clearly see the influence of negative evaluation on the asset by player in that, in contrast to Figure 2, the negative assessment of the influential market player on the rate of return of the asset leads to the ever-decreasing expected rate of returns, and emergence of negative value of even if we initially have .

6.1.3. Numerical test 1-3

(Removal of restrictions on parameters) In this test, we provide a numerical example which shows that the herding behavior still occurs even when the restrictions on the paramenters and initial configurations imposed on Theorem 3.3 are not satisfied, as was guranteed by Theorem 3.6.

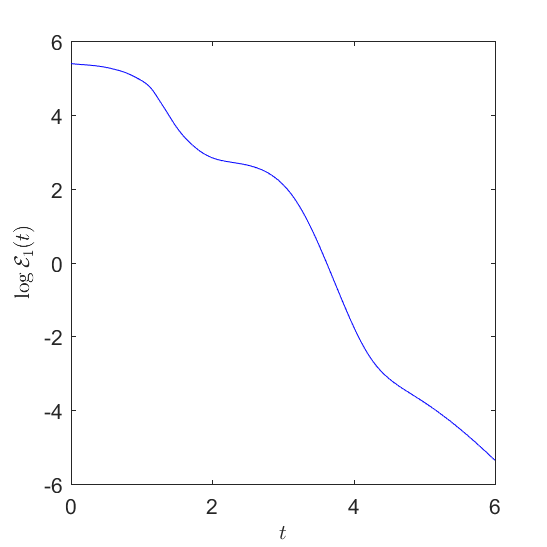

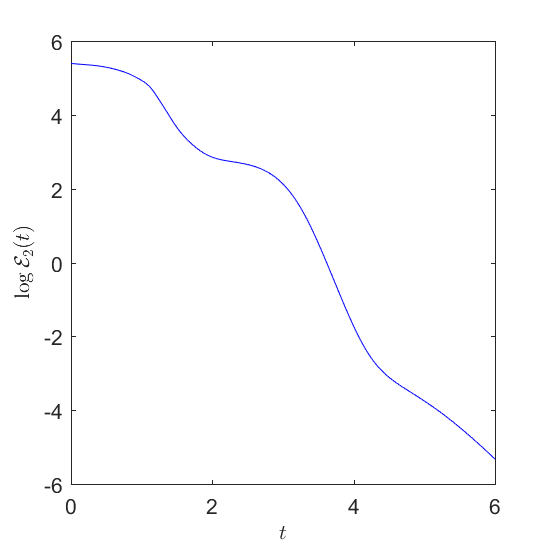

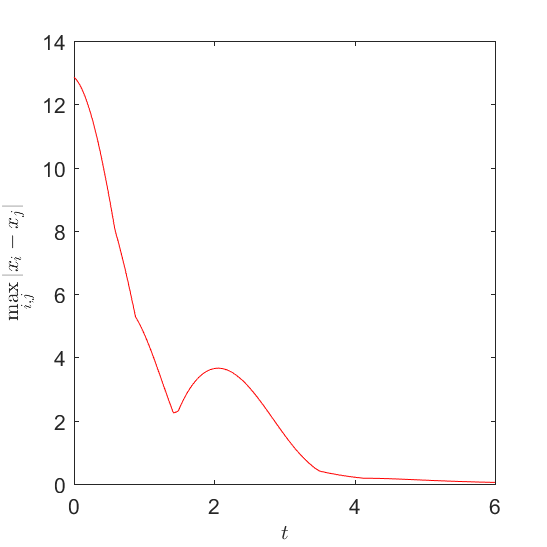

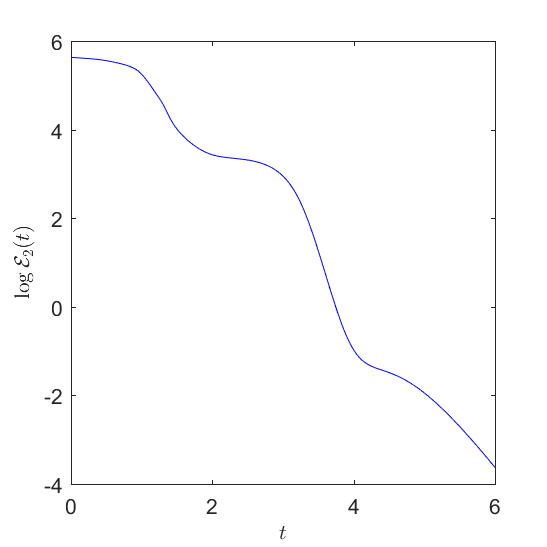

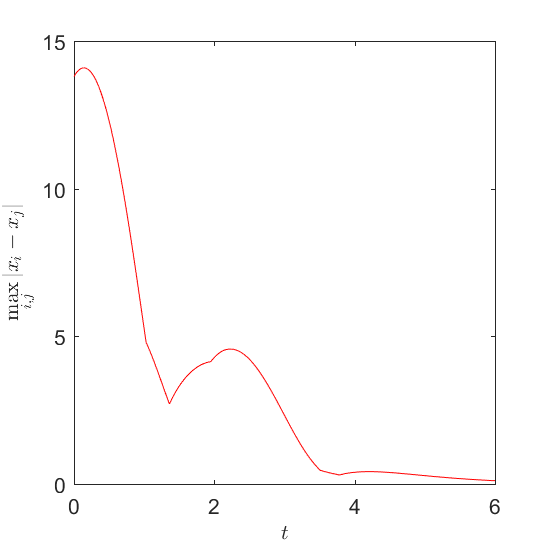

For this, we choose , , and . Since there is no restriction on initial data in Theorem 3.6, we choose them randomly in . In Figure 9 - 11, we plot the numerical solutions to (2.1) upto . These figures show that the desired herding phenomena occurs.

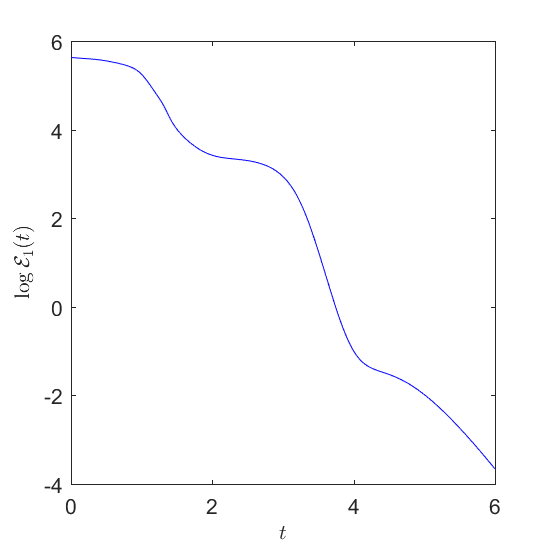

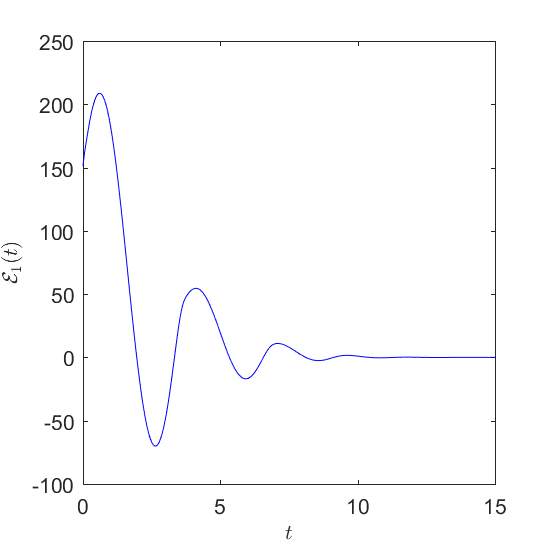

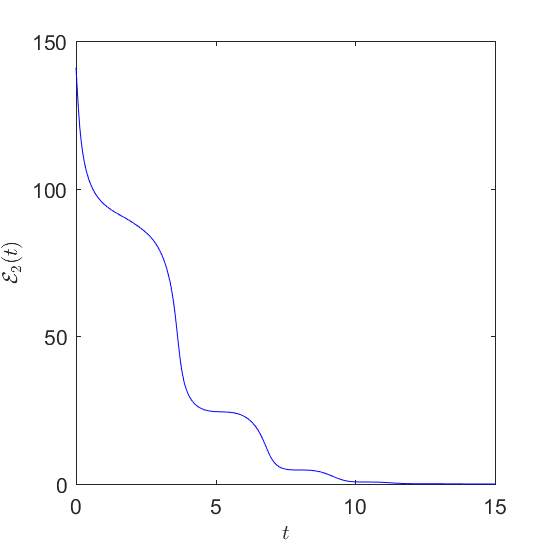

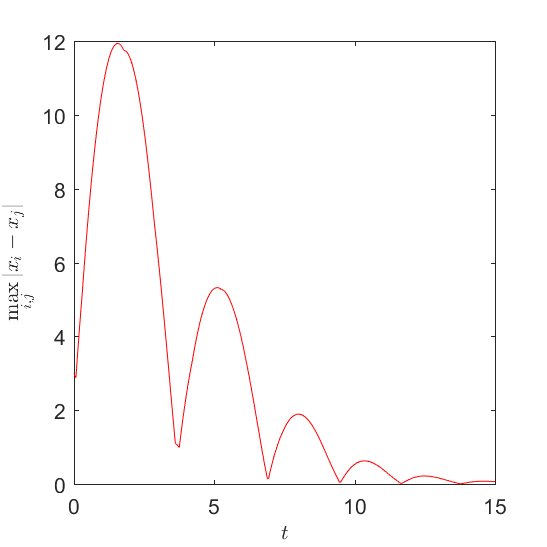

We, however, observe that various important features of Theorem 3.3 do not hold. Figure 12(a) shows that does not decrease monotonically anymore, and even may exceed . We observe that can take negative values. In Figure 12(c), we also see that can exceed in this case, which implies that the proof of Theorem 3.3 in Section 4 breaks down. Meanwhile, in Figure 12(b), decreases monotonically toward even with same initial data.

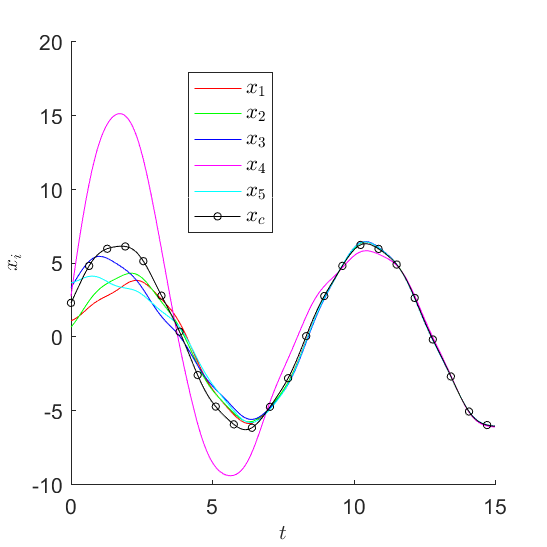

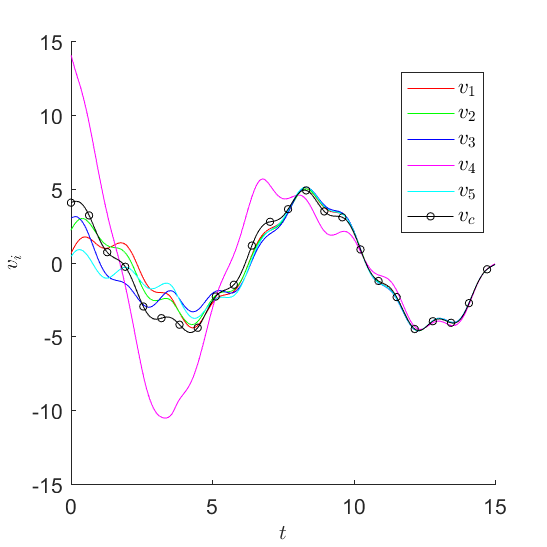

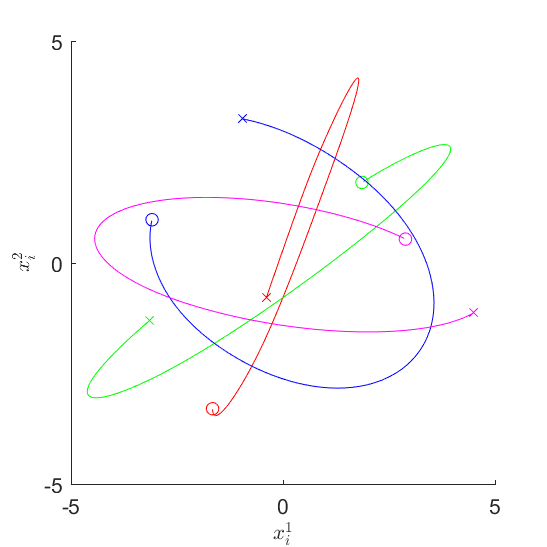

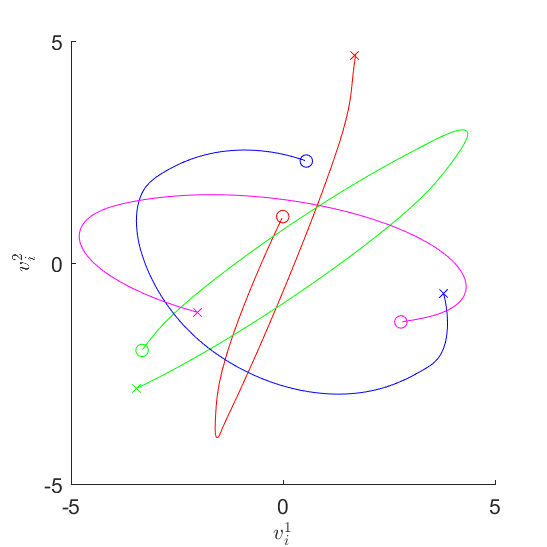

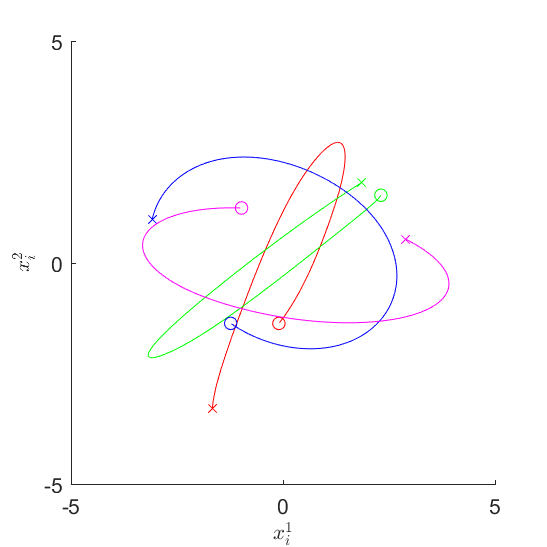

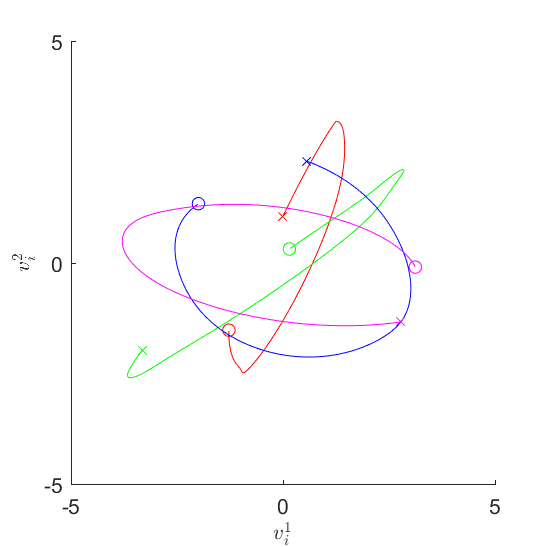

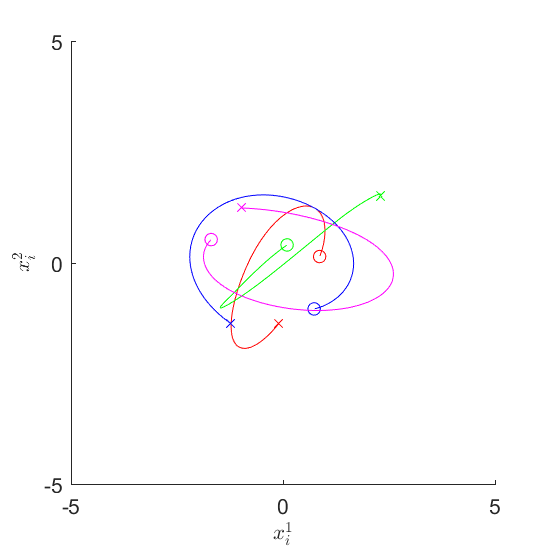

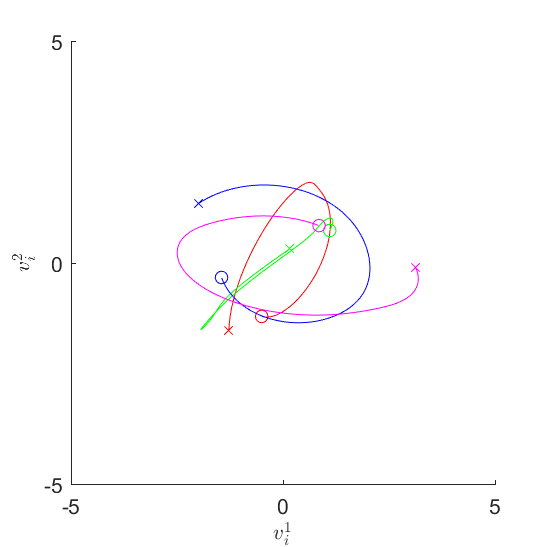

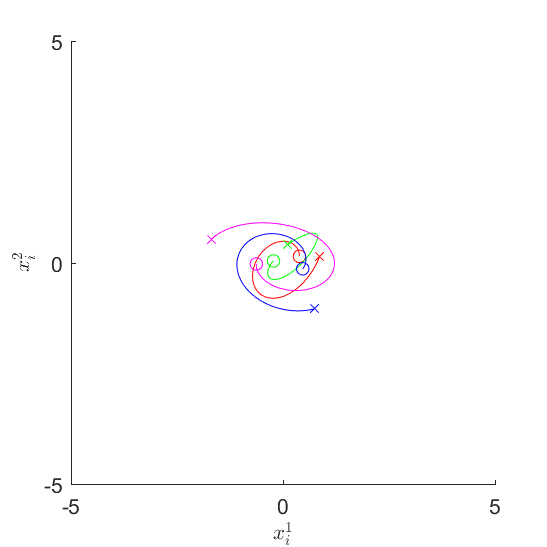

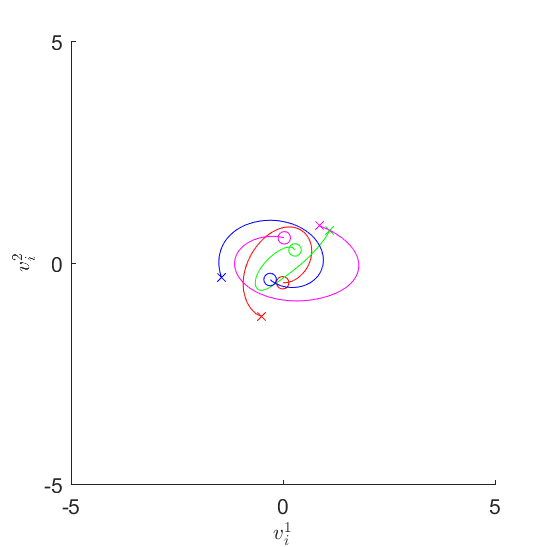

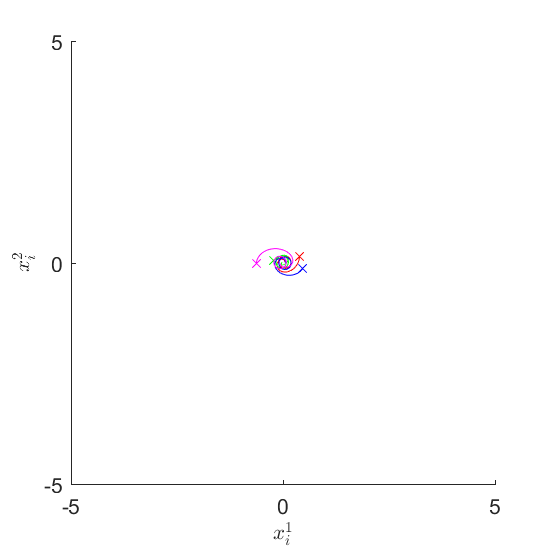

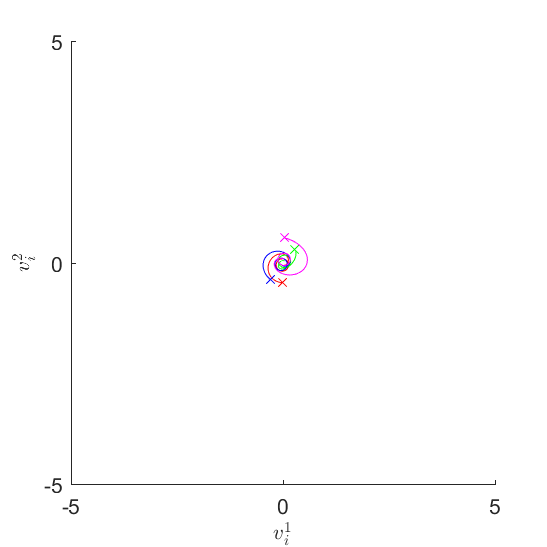

6.2. Numerical test 2:

In this test, we consider the trajectory of numerical solutions to the centralized herding model (3.2) to visualize the dynamics of solutions. We choose , , and , which do not fit into the condition of Theorem 3.3. The herding phenomena is still guaranteed by Theorem 3.6. For the clarity of simulation, we take the number of assets and the number of players as , and pick initial data from such that

Figure 15 - 17 present the trajectory of each and upto final time . In each figure, ‘o’ and ‘x’ stand for the endpoint and the starting point of each trajectory respectively. These figures show how the configurations of and evolve as time passes. Even though their movement seems to be very tangle, all fluctuations are getting smaller in each step, eventually leading to herding phenomena.

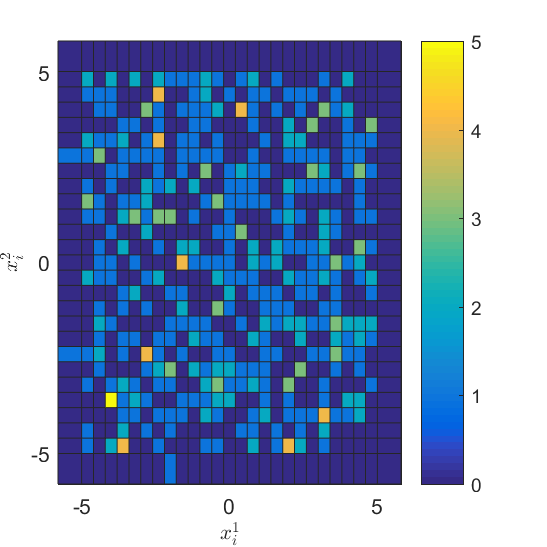

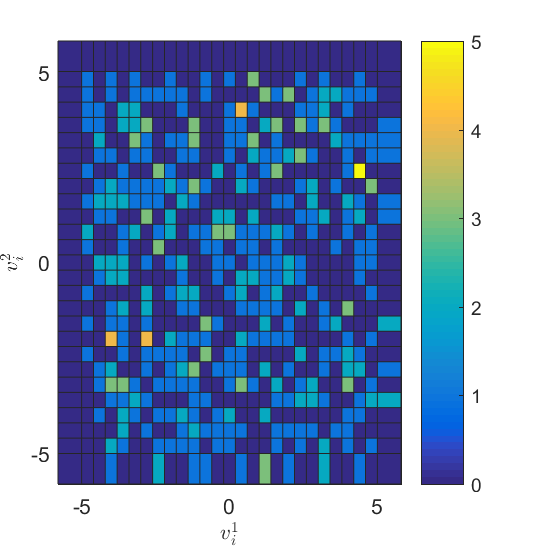

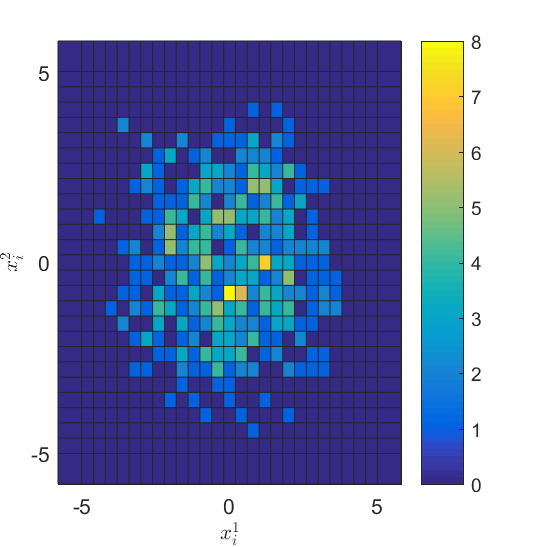

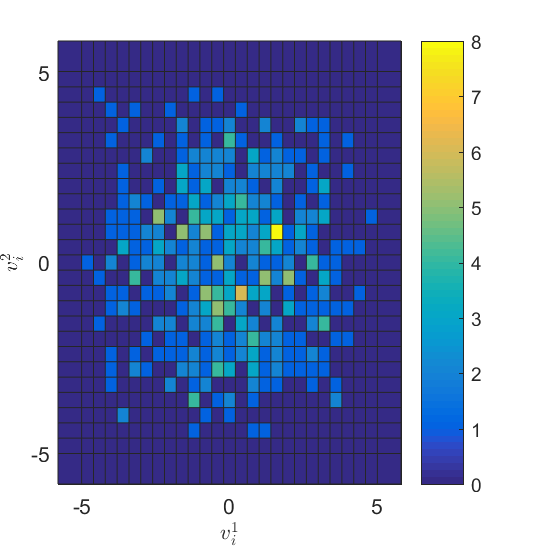

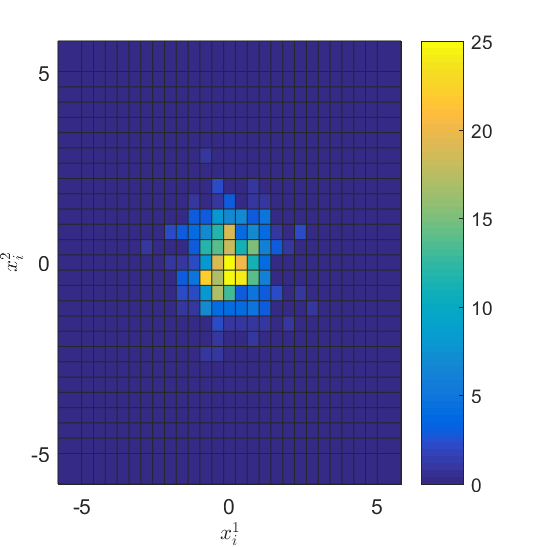

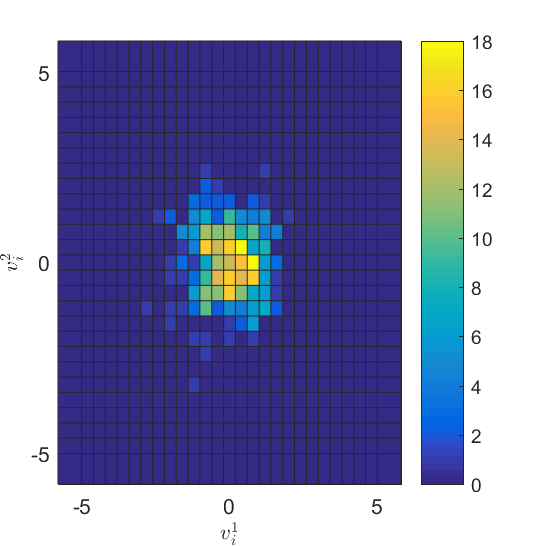

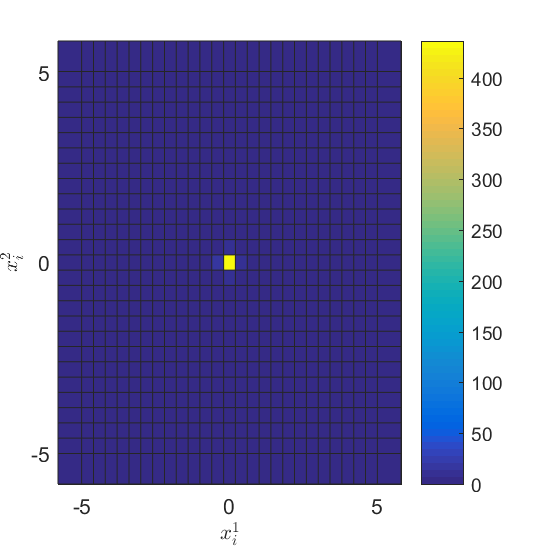

6.3. Numerical test 3:

In this test, we simulate the behavior of large number of players dealing with two assets . We set , , and and choose initial data from to be

We take final time as . As in test 2, we consider the numerical solution to the centralized model (3.2).

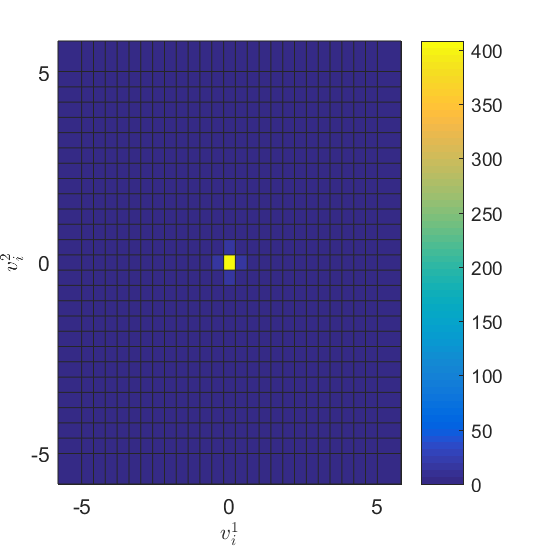

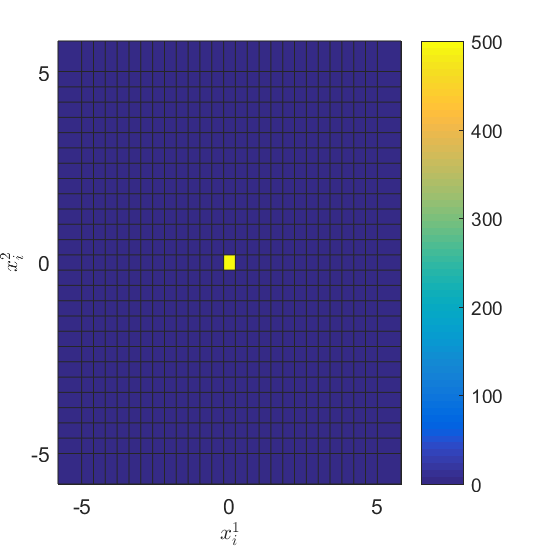

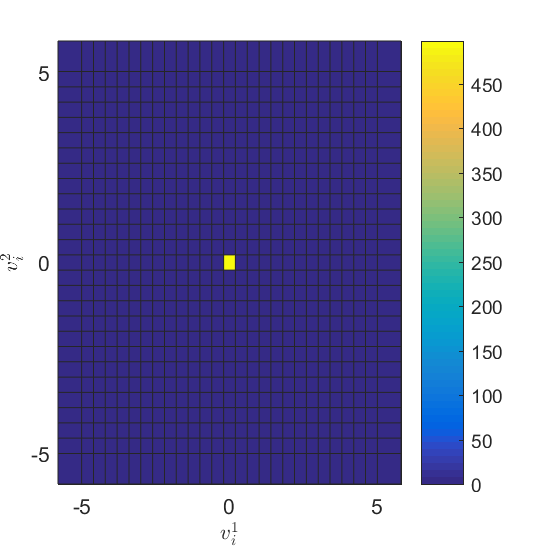

In Figure 20 - 22, we plot histograms of and at and , respectively. In each histogram, each boundary cell count the number of outliers in its designated region. For example, the top left cell counts the number of market players in . We see that, except for Figure 20, there is no outlier at and . As time flows, and are concentrated to centers and , respectively. In Figure 22, we observe that all market players have similar expected rate of returns and favorabilies enough to be contained in one pixel.

7. Conclusion and future work

In this paper, we reinterpreted the rate of return and the favorability as phase point on phase space, and derive an agent based particle model for herding phenomena. We then use this model to prove the herding behavior induced by various dynamic market signals. We also provided various numerical simulations to verify and visualize these results. This work can be developed or extended in several direction. First, particle model with noise is definitely on the first place in the next-to-do list. We restricted ourselves to noiseless situation for clarity in this paper. Secondly, upon incorporating collision avoidance mechanism, our model can be naturally modified to model herding or swarming behavior of particles, animals, bacteria, individuals, unmanned vehicles and so on. Thirdly, we didn’t consider the case where the players can enter or leave the market based on the asset prices. This also seems to be interesting possible future work. Finally, kinetic and hydrodynamic limit of this model and verifying herding phenomena at those levels will be be treated in future works.

Acknowledgement. The authors thank Jane Yoo for serious discussion and helpful comments.

References

- [1] S. Ahn, H.-O. Bae, S.-Y. Ha, Y. Kim and H. Lim, Application of flocking mechanism to the modeling of stochastic volatility, Math. Models Methods Appl. Sci. 23 (2013) 1603–1628.

- [2] S. Ahn, H. Choi, S.-Y. Ha, H. Lee, On collision-avoiding initial configurations to Cucker-Smale type flocking models, Commun. Math. Sci. 10 (2012) 625–643.

- [3] H.-O. Bae, S.-Y. Ha, Y. Kim, S.-H. Lee, H. Lim, and J. Yoo, A mathematical model for volatility flocking with a regime switching mechanism in a stock market, Math. Models Methods Appl. Sci. 25 (2015) 1299–1335.

- [4] D. Abreu and M. K. Brunnermeier, Bubbles and Crashes, Econometrica 71 (2003) 173–204.

- [5] C. Avery and P. Zemsky, Multidimensional uncertainty and herd behavior in financial markets, Amer. Eco. rev. (1998) 724–748.

- [6] A. V. Banerjee, A simple model of herd behavior, Quar. J. Eco. 107 (1992) 797–818.

- [7] A. B. T. Barbaro, K. Taylor, P. F. Trethewey, L. Youseff and B. Birnir, Discrete and continuous models of the dynamics of pelagic fish, Math. Comput. Simulat. 79 (2009) 3397–3414.

- [8] N. Bellomo, A. Bellouquid, J. Nieto and J. Soler, Multiscale biological tissue models and flux-limited chemotaxis for multicellular growing systems, Math. Models Methods Appl. Sci. 20 (2010) 1179–-1207.

- [9] S. Bikhchandani, D. Hirshleifer and I. Welch, A theory of fads, fashion, custom and cultural change as informational cascades, J. Poli. Eco. 100 (1992) 992–1027.

- [10] M. K. Brunnermeier, Asset Pricing under Asymmetric Information, Bubbles, Crashes, Technical Analysis and Herding (Oxford University Press on Demand, 2001).

- [11] M. Burger, P. Markowich, and J.-F. Pietschmann. Continuous limit of a crowd motion and herding model: analysis and numerical simulations, Kinet. Relat. Models 4 (2011) 1025–1047.

- [12] J. A. Carrillo, Y.-P. Choi, P. B. Mucha, J. Peszek, Sharp conditions to avoid collisions in singular Cucker-Smale interactions, Nonlinear Anal. Real World Appl. 37 (2017) 317–-328.

- [13] J. A. Carrillo, M. Fornasier, J. Rosado and G. Toscani, Asymptotic flocking dynamics for the kinetic Cucker-Smale model, SIAM J. Math. Anal. 42 (2010) 218–236.

- [14] A. Cavagna, A. Cimarelli, I. Giardina, G. Parisi, R. Santagati, F. Stefanini and R. Tavarone, From empirical data to inter-individual interactions: Unveiling the rules of collective animal behavior, Math. Models Methods Appl. Sci. 20 (2010) 1491-–1510.

- [15] Y.-P. Choi, S.-Y. Ha and Z. Li, Emergent dynamics of the Cucker-Smale flocking model and its variants. Active particles. Vol. 1. Advances in theory, models, and applications, 299–331, Model. Simul. Sci. Eng. Technol. (Birkhäuser/Springer, Cham, 2017).

- [16] F. Cucker and S. Smale, Emergent behavior in flocks, IEEE Trans. Automat. Control 52 (2007) 852–-862.

- [17] F. Cucker and S. Smale, On the mathematics of emergence, Japan. J. Math. 2 (2007) 197-–227.

- [18] M. Delitala and T. Lorenzi, A mathematical model for value estimation with public information and herding, Kinet. Relat. Models 7 (2014) 29–44.

- [19] A. Devenow and I. Welch, Rational herding in financial economics, Europ. Econ. Rev. 40 (1996) 603–615.

- [20] B. During, A. Jungel and L. Trussardi, A kinetic equation for economic value estimate with irrationality and herding, Kinet. Relat. Models 10 (2017) 239–261.

- [21] P. Degond and S. Motsch, Continuum limit of self-driven particles with orientation interaction, Math. Models Methods Appl. Sci. 18 (2008) 1193–-1215.

- [22] S.-Y. Ha, K. Lee and D. Levy, Emergence of time-asymptotic flocking in a stochastic Cucker-Smale system, Commun. Math. Sci. 7 (2009) 453–-469.

- [23] S.-Y. Ha, J. G. Liu, A simple proof of the Cucker-Smale flocking dynamics and mean-field limit, Commun. Math. Sci. 7 (2009) 297–-325.

- [24] S.-Y. Ha and E. Tadmor : From particle to kinetic and hydrodynamic descriptions of flocking, Kinet. Relat. Models 1 (2008) 415–-435.

- [25] C. S. Hemphill, J. Suk, The law, culture, and economics of fashion, Stan. L. Rev. 61 (2009) 1147–1200.

- [26] S. Hwang and M. Salmon, Market stress and herding, J. Empir. Finan. 11 (2004) 585–616.

- [27] I. H. Lee, Market crashes and informational avalance, The Rev. Econ. Stud. 65 (1995).

- [28] R. C. Merton and P. A. Samuelson, Continuous-Time Finance (Blackwell Publishing, 1992).

- [29] P. R. Milgrom and N. Stokey, Information, Trade and Common Knowledge, J. Econ. Theory 26 (1982) 17–27.

- [30] S. Motsch and E. Tadmor, A new model for self-organized dynamics and its flocking behavior, J. Stat. Phys. 144 (2011) 923-–947.

- [31] M. S. Santos and M. Woodford, Rational asset pricing bubbles, Econometrica 65 (1997) 19–57.

- [32] J. Tirole, On the possibility of speculation under rational expectations, Econometrica 50 (1982) 1163–1182.

- [33] G. Toscani, Kinetic models of opinion formation. Commun. Math. Sci. 4 (2006), 481–496.

- [34] T. Vicsek, ; A. Czirók, ; E. Ben-Jacob, I. Cohen and O. Shochet, Novel type of phase transition in a system of self-driven particles, Phys. Rev. Lett. 75 (1995) 1226–-1229.

- [35] J. Toner and Y. Tu, Flocks, herds, and schools: a quantitative theory of flocking, Phys. Rev. E58 (1998) 4828–-4858.

- [36] J. P. LaSalle, Some extensions of Liapunov’s second method, IRE Trans. 7 (1960) 520–527.