Bayesian estimation of a decreasing density

Abstract

Suppose is a random sample from a bounded and decreasing density on . We are interested in estimating such , with special interest in . This problem is encountered in various statistical applications and has gained quite some attention in the statistical literature. It is well known that the maximum likelihood estimator is inconsistent at zero. This has led several authors to propose alternative estimators which are consistent. As any decreasing density can be represented as a scale mixture of uniform densities, a Bayesian estimator is obtained by endowing the mixture distribution with the Dirichlet process prior. Assuming this prior, we derive contraction rates of the posterior density at zero by carefully revising arguments presented in Salomond (2014). Several choices of base measure are numerically evaluated and compared. In a simulation various frequentist methods and a Bayesian estimator are compared. Finally, the Bayesian procedure is applied to current durations data described in Keiding et al. (2012).

keywords:

[class=MSC]keywords:

, and

a]Institute of Applied Mathematics, Delft University of Technology

1 Introduction

1.1 Setting

Consider an independent and identically distributed sample from a bounded decreasing density on . The problem of estimating based on the sample, only using the information that it is decreasing, has attracted quite some attention in the literature. One of the reasons for this is that the estimation problem arises naturally in several applications.

To set the stage, we discuss a simple idealized example related to the waiting time paradox. Suppose buses arrive at a bus stop at random times, with independent interarrival times sampled from a distribution with distribution function . At some randomly selected time, somebody arrives and has to wait for a certain amount of time until the next bus arrives. A natural question then is: ‘what is the distribution of the remaining waiting time until the next bus arrives?’ In order to derive this distribution, two observations are important.

The first is, that the time of arrival of the traveller is more likely contained in a long interarrival interval than a short interarrival interval. Under mild assumptions, one can show that actually the length of the whole interarrival interval (so between arrival of the previous and the next bus) containing the time the traveller arrives, can be viewed as a draw from the length biased distribution associated to distribution function . This is the distribution with distribution function

| (1.1) |

It is assumed that .

The second observation is that the remaining waiting time for the traveller is a uniformly distributed fraction of the interarrival time. A residual waiting time is therefore interpreted as

where is uniformly distributed on and, independently of , according to distribution function defined in (1.1).

These observations imply that on , has survival function

using integration by parts in the last step. Differentiating with respect to , yields the following relation between the sampling density and distribution function :

| (1.2) |

In words: the sampling density is proportional to a survival function of the interarrival distribution, which is by definition decreasing. Note that in the classical waiting time paradox, the underlying arrival process is taken to be a homogeneous Poisson process, with exponential interarrival times. In view of (1.2), this leads to the ‘paradox’ that the distribution of the residual waiting time equals the distribution of the interarrival time itself.

More examples where exactly this model comes into play can for instance be found in the introductory section of Kulikov & Lopuhaä (2006), in Vardi (1989), Watson (1971), Keiding et al. (2012) and references therein. In those examples, the challenge is to estimate the interarrival distribution function based on a sample from density . To do this, the ‘inverse relation’ of (1.2), expressing in terms of can be employed:

| (1.3) |

Here it is used that .

From (1.3) it is clear that in order to estimate at some specific point , estimating the decreasing sampling density at zero is of special interest. This value occurs at the right hand side for any choice of .

1.2 Literature overview

The most commonly used estimator for is the maximum likelihood estimator derived in Grenander (1956). This estimator is defined as the maximizer of the log likelihood over all decreasing density functions on . The solution of this maximization problem can be graphically constructed. Starting from the empirical distribution based on , the least concave majorant of can be constructed. This is a concave distribution function. The left-continuous derivative of this piecewise linear concave function yields the maximum likelihood (or Grenander) estimator for . For more details on the derivation of this estimate, see Section 2.2 in Groeneboom & Jongbloed (2014). As can immediately be inferred from the characterization of the Grenander estimator,

where denotes the -th order statistic of the sample. Denoting convergence in distribution by ,

where has the standard exponential distribution. It is clear that does not converge in probability to . This inconsistency of was first studied in Woodroofe & Sun (1993). There it is also shown that

where is a standard Poisson process on and is a standard uniform random variable.

It is clear from (1.3) that this inconsistency is undesirable, as estimating the distribution function of interest, , at any point , requires estimation of . Various approaches have been taken to obtain a consistent estimator of . The idea in Kulikov & Lopuhaä (2006) is to estimate by evaluated at a small positive (but vanishing) number: for some . There it is shown that the estimator is -consistent, assuming and .

A likelihood related approach was taken in Woodroofe & Sun (1993). There a penalized log likelihood function is introduced, where the estimator is defined as maximizer of

For fixed , this estimator can be computed explicitly by first transforming the data using a data dependent affine transformation and then applying the basic concave majorant algorithm to the empirical distribution function based these transformations data. It is shown (again, assuming and ) that the optimal rate to choose is . Then, the maximum penalized estimator is -consistent.

Groeneboom & Jongbloed (2014) proposed to estimate by the histogram estimator , where is a sequence of positive numbers with if . The bin widths can e.g. be chosen by estimating the asymptotically Mean Squared Error-optimal choice. Also this estimator is - consistent assuming and .

1.3 Approach

In this paper we take a Bayesian nonparametric approach to the problem. An advantage of the Bayesian setup is the ease of constructing credible regions. To construct frequentist analogues of these, confidence regions, can be quite cumbersome, relying on either bootstrap simulations or asymptotic arguments.

To formulate a Bayesian approach for estimating a decreasing density, note that any decreasing density on can be represented as a scale mixture of uniform densities (see e.g. Williamson (1956)):

| (1.4) |

where is a distribution function concentrated on the positive half line. Therefore, by endowing the mixing measure with a prior distribution we obtain the posterior distribution of the decreasing density, and in particular of . A convenient and well studied prior for distribution functions on the real line is the Dirichlet process (DP) prior (see for instance Ferguson (1973) and Van der Vaart and Ghosal (2017)). This prior contains two parameters: the concentration parameter, usually denoted by , and the base probability distribution, which we will denote by . The approach where a prior is obtained by putting a Dirichlet process prior on in (1.4) was previously considered in Salomond (2014). In that paper, the asymptotic properties of the posterior in a frequentist setup are studied. More specifically, contraction rates are derived to quantify the performance of the Bayesian procedure. This is a rate for which we can shrink balls around the true parameter value, while maintaining most of the posterior mass. More formally, if is a semimetric on the space of density functions, a contraction rate is a sequence of positive numbers for which the posterior mass of the balls converges in probability to as , when assuming are independent and identically distributed with density . A general discussion on contraction rates is given in Chapter 8 of Van der Vaart and Ghosal (2017).

1.4 Contributions

In Theorem 4 in Salomond (2014) the rate is derived for pointwise loss at any . For , only posterior consistency is derived, essentially under the assumption that the base measure admits a density for which there exists such that when is sufficiently small (theorem 4). These are interesting results, though one would hope to prove the rate for all . Under specific conditions on the underlying density, this rate is attained by estimators to be discussed in section 4. We explain why the techniques in the proof of Salomond (2014) cannot be used to obtain rates at zero and present an alternative proof (using different arguments). This proof not only reveals consistency, but also yields a contraction rate equal to (up to log factors) that coincides with the case . We argue that with the present method of proof a better rate is not easily obtained. Many results from Salomond (2014) are important ingredients to the proof we present. The first key contribution of this paper is to derive the claimed contraction rate, combining some of Salomond’s results with new arguments.

We also address computational aspects of the problem and show how draws from the posterior can be obtained using the algorithm presented in Neal (2000). Using this algorithm we conduct four studies.

-

•

For a fixed dataset, we compare the performance of the posterior mean under various choices of base measure for the Dirichlet process.

-

•

We investigate empirically the rate of convergence of the Bayesian procedure for estimating the density at zero when or for . The simulation results suggest that for both choices of base measure the rate is . If this implies that the derived rate (up to log factors) is indeed suboptimal, as anticipated by Salomond (2014). If the rate is interesting, as it contradicts the belief that “due to the similarity to the maximum likelihood estimator, the posterior distribution is in this case not consistent“ (page 1386 in Salomond (2014)).

-

•

We compare the behaviour of various proposed frequentist methods and the Bayesian method for estimating . Here we vary the sample sizes and consider both the Exponential and half-Normal distribution as true data generating distributions.

-

•

Pointwise credible sets can be approximated in a direct way from MCMC-output, which is much more straightforward than the construction of frequentist confidence intervals based on large-sample limiting results.

1.5 Outline

In section 2 we derive pointwise contraction rates for the density evaluated at , for any . In section 3 a Markov Chain Monte Carlo method for obtaining draws from the posterior is given, based on the results of Neal (2000). This is followed by a review of some existing methods to consistently estimate at zero. Section 5 contains numerical illustrations. The appendix contains some technical results.

1.6 Frequently used notation

For two sequences and of positive real numbers, the notation (or ) means that there exists a constant that is independent of and such that We write if both and hold. We denote by and the cumulative distribution functions corresponding to the probability densities and respectively. We denote the -distance between two density functions and by , i.e. . The Kullback-Leibler divergence ‘from to ’ is denoted by .

2 Pointwise posterior contraction rates

Let denote the collection of all bounded decreasing densities on and recall that are i.i.d. with density . Denote the distribution of under by and expectation under by . In this section we are interested in the asymptotic behaviour of the posterior distribution of in a frequentist setup. This entails that we study the behaviour of the posterior distribution on while assuming a true underlying density . Set and . Denote the prior measure on by and the posterior measure by .

Given a loss function on , we say that the posterior is consistent with respect to if for any , when . If is a sequence that tends to zero, then we say that the posterior contracts at rate (with respect to ) if when . The rate is called a contraction rate.

Salomond (2014) derived contraction rates based on the Dirichlet process prior for the , Hellinger- and pointwise loss function.

In the following theorem we derive sufficient conditions for posterior contraction in terms of the behaviour of the density of the base measure near zero. In that, we closely follow the line of proof in Salomond (2014). Although the argument in Salomond (2014) for proving posterior contraction rate for with is correct, we prove the theorem below for rather than only for . The reason for this is twofold: (i) many steps in the proof for are also used in the proof for ; (ii) we obtain one theorem covering pointwise contraction rates for all . For the base measure we have the following assumption.

Assumption 2.1.

The base distribution function of prior, , has a strictly positive Lebesgue density on . There exists positive numbers such that

| (2.1) |

For the data generating density we assume

Assumption 2.2.

The data generating density and

-

•

there exists an such that ;

-

•

the exist positive constants and such that for sufficiently large.

Theorem 2 in Salomond (2014) asserts the existence of a positive constant such that

. This result will be used in the proof for deriving an upper bound on the pointwise contraction rate of the posterior at zero.

Define a sequence of subsets of by

where and .

Theorem 2.3.

In the proof we will use the following lemma (see appendix B and lemma 8 of Salomond (2014)).

Lemma 2.4.

Let and satisfy assumption 2.2. Define

| (2.2) |

There exist strictly positive constants and such that

| (2.3) |

We now give the proof of Theorem 2.3.

Proof of Theorem 2.3.

The posterior measure of a measurable set is given by

where is as defined in (2.2). By lemma 2.4 there exist positive constants and such that , where . Let . Define , and consider (test-) functions . We bound

| (2.4) |

To construct the specific test functions , we distinguish between and . For case , it follows from the proofs of theorems 3 and 5 in Salomond (2014) that there exists a sequence test functions such that

for some constant . Substituting these bounds into (2) and choosing shows that as . This finishes the proof for .

We now consider the case . Define subsets

As , . For bounding , use the same test function defined in Salomond (2014). Then it follows from the inequalities in (2), applied with instead of , that as .

For bounding , we also use the inequalities in (2), applied with instead of . However, we also intersect with the event

to obtain

This holds true since theorem 2 in Salomond (2014) gives , -almost surely.

Here we bound the second moment of under by and use that .

It remains to bound

Since both and are nonincreasing we have

Hence

the final inequality being a consequence of . Since for we have we get

Using the derived bound we see that

where

| (2.6) |

Note that , by choice of . Taking big enough such that we have is positive (recall that is defined in (2.5)). Using that is nonincreasing and that we get

Bernstein’s inequality gives

If we take , then

This tends to infinity faster than whenever , i.e. when . ∎

Remark 2.5.

The derived rate is not the optimal but cannot be easily improved upon with the present type of proof. At first sight, one may wonder whether the tests can be improved upon by choosing different sequences and . Unfortunately, the choice of and cannot be much improved upon. To see this, for bounding with Bernstein’s inequality we need that in (2.6) is positive. Assume and (up to factors), we must have . Hence this restriction leads to .

Define . Then , we can bound by

We have two cases according to sequence .

-

1.

, implies . We have should tend to infinity faster than , hence . By combine all restrictions, we derive that necessarily has to satisfy .

-

2.

, implies . Then gives . Hence .

Therefore, can not go to zero faster than .

Remark 2.6.

As pointwise consistency is proved in Theorem 2.3, Theorem 4 in Salomond (2014) implies that the posterior median is a consistent estimator at any fixed point. Moreover, the posterior median has the same converge rate . The consistency of the posterior mean is not clear now. However, the posterior mean of is a decreasing density function, which provides a convenient way for estimation. We use either mean or median estimator according to different purpose in the simulation study.

2.1 A difficulty in the proof of theorem 4 in Salomond (2014)

The construction of the tests in the proof of theorem 2.3 is new. In Salomond (2014) a different argument is used, which we now shortly review (it is given in section 3.3 of that paper). First we give a lemma for the following discussion.

Lemma 2.7.

Let be the prior distribution on that is obtained via (1.4), where and satisfies there exists positive numbers such that

Then for any (possibly sequence) in ,

Proof.

Let be a sequence of positive numbers. Trivially, we have

Since both and are nonincreasing, and , for all . Hence,

This implies

Using this bound and define a new sequence , we get

| (2.7) |

Choose and such that . Theorem 1 in Salomond (2014) implies that the second term on the right-hand-side tends to zero. We aim to choose such that the first term on the right-hand-side in (2.7) also tends to zero. This term can be dealt with using lemma 2.4:

Using lemma 2.7, the second term on the right-hand-side can be bounded by

Since , the right-hand-side in the preceding display tends to zero () upon choosing and . This yields

which unfortunately does not tend to zero. Hence, we do not see how the presented argument can yield pointwise consistency of the posterior at zero.

2.2 Attempt to fix the proof by adjusting the condition on the base measure

A natural attempt to fix the argument consists of changing the condition on the base measure. If the assumption on would be replaced with

| (2.8) |

then lemma 2.7 would give the bound

Now we can repeat the argument and check whether it is possible to choose and such that both and

| (2.9) |

hold true simultaneously. The requirement leads to taking , with . With this choice for , equation (2.9) can only be satisfied if . Now if we assume (2.8) with , then we need to check whether lemma 2.4 is still valid. This is a delicate issue as we need to trace back in which steps of its proof the assumption on the base measure is used. In appendix B of Salomond (2014) it is shown that the result in lemma 2.4 follows upon proving that

| (2.10) |

with (as in the statement of the lemma). Here, the set is defined as

where

In lemma 8 of Salomond (2014) it is proved that for some constant , which implies the specific rate . The proof of this lemma is rather complicated, the key being to establish the existence of a set for which . Next, upon tracking down at which place the prior mass condition is used for that result (see appendix A), we find that it needs to be such that

| (2.11) |

where and (see in particular inequality (A.1) in the appendix). Now assume (2.8), then

Hence

if (which we need to assume for (2.9) to hold). From this inequality we see that (2.11) can only be satisfied if . We conclude that with the line of proof in Salomond (2014) the outlined problem in the proof of consistency near zero cannot be fixed by adjusting the prior to (2.8): one inequality requires , while another inequality requires and these inequalities need to hold true jointly.

3 Gibbs Sampling in the DPM model

Since a decreasing density can be represented as a scale mixture of uniform densities (see (1.4)) and the mixing measure is chosen according to a Dirichlet process, the model is a special instance of a so-called Dirichlet Process Mixture (DPM) Model. Algorithms for drawing from the posterior in such models have been studied in many papers over the past two decades, a key reference being Neal (2000). Here we shortly discuss the algorithm coined “algorithm 2” in that paper. We assume has a density with respect to Lebesgue measure.

Let denote the number of distinct values in the vector and let denote the vector obtained by removing the -th element of . Denote by and the maximum and minimum of all elements in the vector respectively.

The starting point for the algorithm is a construction to sample from the DPM model:

| (3.1) |

Here CRP denotes the “Chinese Restaurant Process” prior, which is a distribution on the set of partitions of the integers . This distribution is most easily described in a recursive way. Initialize by setting . Next, given , let and set

where varies over and is the number of current ’s equal to . In principle this process can be continued indefinitely, but for our purposes it ends after steps. One can interpret the vector as a partitioning of the index set (and hence the data ) into disjoint sets (sometimes called “clusters”). For ease of notation, write .

An algorithm for drawing from the posterior of is obtained by successive substitution sampling (also known as Gibbs sampling), where the following two steps are iterated:

-

1.

sample ;

-

2.

sample .

The first step entails sampling from the posterior within each cluster. For the th component of , , this means sampling from

| (3.2) |

Sampling is done by cycling over all () iteratively. For and we have

| (3.3) |

The right-hand-side of this display equals

| (3.4) |

where . The expression for follows since in that case sampling from boils down to sampling from the marginal distribution of . Summarising, we have the following algorithm:

It may happen that over subsequent iterations of the Gibbs sampler certain clusters disappear. Then and will not be the same. If this happens, the corresponding to the disappearing cluster is understood to be removed from the vector (because the cluster becomes “empty”, the prior and posterior distribution of such a are equal). The precise labels do not have a specific meaning and are only used to specify the partitioning into clusters.

4 Review of existing methods for estimating the decreasing density at zero

In this section we review some consistent estimators for a decreasing density at zero that have appeared in the literature. These will be compared with the Bayesian method of this paper using a simulation study in section 5.

4.1 Maximum penalised likelihood

In Woodroofe & Sun (1993), the maximum penalised likelihood estimator is defined as the maximiser of the following penalised log likelihood function:

Here is a (small) penalty parameter. This estimator has the same form as the maximum likelihood estimator (MLE), being piecewise constant with at most discontinuities. For fixed , for ease of notation here let denote the ordered observed values and

where is the unique solution of the equation

Denote by the penalized estimator with penalty parameter . Taking , is a step function with

At zero it is defined by right continuity and for as . Here

Geometrically, for , is the left derivative of the least concave majorant of the empirical distribution function of the transformed data evaluated at . Note that an alternative expression for is which can be easily calculated.

4.2 Simple and ‘adaptive’ estimators

In Kulikov & Lopuhaä (2006), is estimated by the maximum likelihood estimator evaluated at a small positive (but vanishing) number: for some . Of course, the estimator depends on the choice of the parameter .

In Kulikov & Lopuhaä (2006), Theorem 3.1, it is shown that

converges in distribution to when . Here is the right derivative of the least concave majorant on of the process , evaluated at . Furthermore, and .

Based on this asymptotic result, two estimators are proposed, denoted as and (‘S’ for simple, ‘A’ for adaptive). The first is a simple one with , then . The second is , where is taken such that the the second moment of the limiting distribution is minimized. Of course, to really turn this into an estimator, has to be estimated. Details on this are presented in section 5.5.

4.3 Histogram estimator

In chapter 2 of Groeneboom & Jongbloed (2014) a natural and simple histogram-type estimator for is proposed. Let be a vanishing sequence of positive numbers and consider the estimator , where is the empirical distribution of . It can be shown that behaves like and the variance of behaves like as . Then the asymptotic mean square error (aMSE) optimal choice for is , where is as defined in the Section 4.2.

5 Numerical illlustrations

In this section we use the algorithm described in Section 3 to sample from the posterior distribution. We consider two data generating settings for the true density function: the standard Exponential distribution and the half-Normal distribution. Both densities are bounded, decreasing and satisfy assumption 2.2. Suppose in the -th iteration of the Gibbs sampler (possibly after discarding “burn in” samples) we have obtained At iteration , if the stationary region of the mcmc sampler has been reached, a sample from the posterior distribution is given by

| (5.1) |

Two natural derived Bayesian point estimators are the posterior mean and the median. Assuming iterations, a Rao-Blackwellized estimator for the posterior mean is obtained by computing and an estimator for the posterior median at is the median value in . We implemented our procedures in Julia, see Bezanson et al. (2017). The computer code and datasets for replication of our examples forms part of the BayesianDecreasingDensity repository (https://github.com/fmeulen/BayesianDecreasingDensity). For plotting we used functionalities of the ggplot2 package (see Wickham (2016)) in R. The computations were performed on a MacBook Pro, with a 2.7GHz Intel Core i5 with 8 GB RAM.

5.1 Base measures

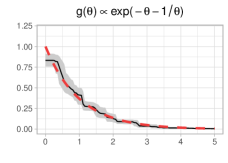

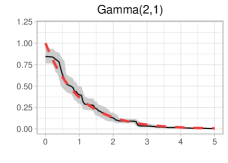

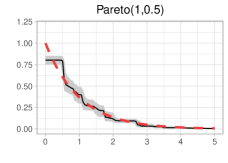

To assess the influence of the base measure in the Dirichlet-process prior, we consider the following choices for the base measure:

-

(A)

The density of the base measure vanishes exponentially fast near zero, as the lower bound of Assumption 2.1 requires:

(5.2) -

(B)

The density of the distribution

-

(C)

The density of the distribution. That is

Here, we consider various choices for the threshold parameter .

-

(D)

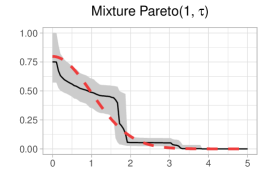

The density is obtained as a mixture of the density, where the mixing measure on has the distribution. This implies that for . The parameter is fixed here, but could be equipped with with a “hyper” prior without adding much additional computational complexity.

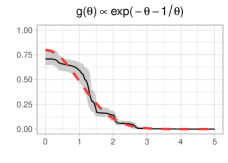

Note that cases (A), (B), (D)(when ) satisfy Assumption 2.1 and case (C) does not. In cases (A) and (B) the update on the “cluster centra” does not boil down to sampling from a “standard” distribution. In this case either rejection sampling or a Metropolis-Hastings step can be used, the details of which are given in section B in the appendix. In case (C) we have partial conjugacy, which in this case means that the ’s can be sampled from a Pareto distribution. Finally, case (D) can be dealt with by Gibbs sampling. More precisely, conditional on the current value of , the ’s can be sampled from the Pareto distribution just as in case (C). Next, is sampled conditional on from the density

(where we use “Bayesian notation”, to simplify the expressions). Hence, this boils down to sampling from a truncated Gamma distribution.

5.2 Estimates of the density for two simulated datasets

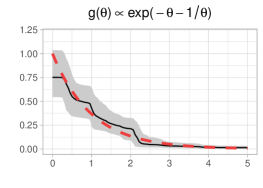

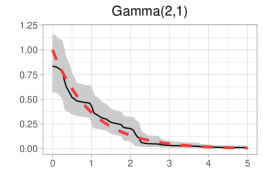

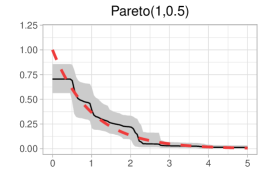

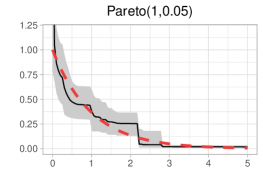

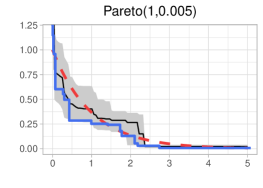

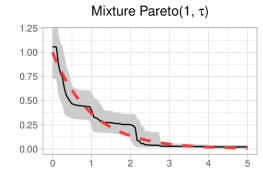

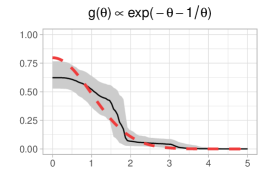

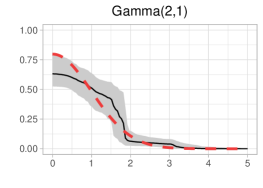

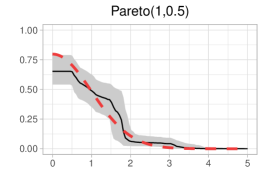

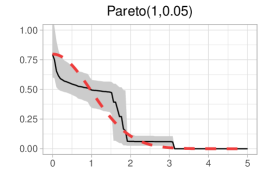

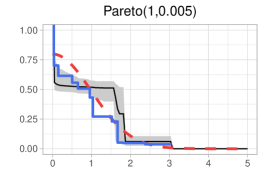

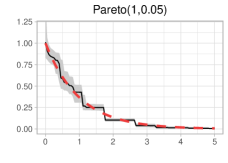

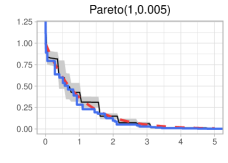

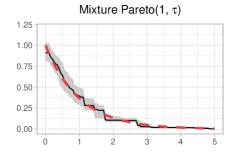

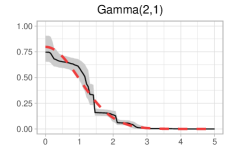

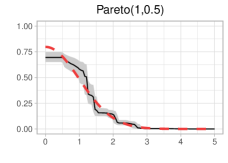

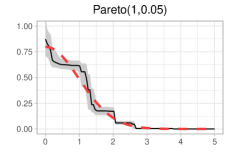

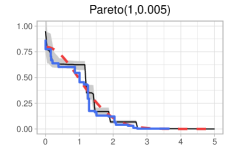

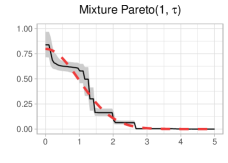

We obtained datasets of size by sampling independently from both the standard Exponential distribution and the halfNormal distribution. In the prior specification, the concentration parameter was fixed to in all simulations, while the base measure was varied over cases (A), (B), (C) with , and (D) with , and . The algorithm was run for iterations and the first half of the iterates were discarded as burn in. The computing time was approximately 2 minutes. In case Metropolis-Hastings steps were used for updating ’s, the acceptance rates of the random-walk updates was approximately , both in case (A) and (B). The results are displayed in figures 1 and 2. From the top figures we see that the posterior mean and pointwise credible bands visually look similar for the choices of base-measure under (A) and (B). If the base measure is chosen according to (C), the middle and bottom-left figures show the effect of the parameter . Choosing too small (here: ) the posterior mean appears inconsistent at zero, similar as the Grenander estimator which is added to the figure for comparison. For somewhat larger values of (middle-left figure), the estimate near zero is like a histogram estimator. Finally, the bottom-right figure shows the posterior mean under the base measure specification (D). Here, the posterior mean looks comparable as obtained under (A) and (B), suggesting that we are able to learn the parameter from the data. In fact, whereas the prior mean of equals , the average of the non burn in samples of equals . We have repeated the whole experiment with sample size . The results are in Appendix C.

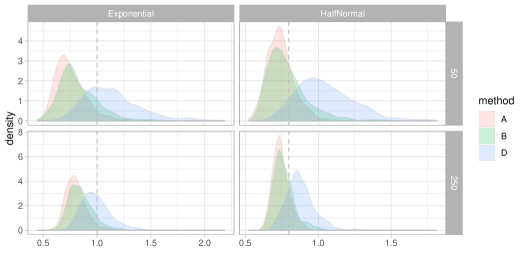

5.3 Distribution of the posterior mean for under various bases measures.

In this section we compare base measures (A), (B) and (D) for estimating at zero. In the experiment, we considered samples of sizes either or . We computed the posterior mean for for each sample based on MCMC-iterations, discarding the first half as burnin. The Monte-Carlo sample size was taken equal to . Figure 3 summarises the results. While the density for base measure (D) is slightly more spread, contrary to base measures (A) and (B), it concentrates on correct values for both the Exponential and HalfNormal distribution.

5.4 Empirical assessment of the rate of contraction

We also performed a large scale experiment to empirically assess the rate of contraction of the posterior median at zero, under either choices (A), (B) or (D) for the base measure. Our proof for deriving the contraction rate really requires a base-measure as under (A) and now the underlying idea is to see in a simulation study whether for near is suitable or not. In the experiment, we first fixed a sample size and generated independent realisations from the standard Exponential distribution. We then ran the MCMC sampler for iterations, and kept the final iterate for initialisation of all chains ran for that particular sample size. Next, we repeated times

-

1.

sample a dataset of size from the standard Exponential distribution;

-

2.

run the MCMC algorithm for iterations;

-

3.

compute the median value at zero obtained in those samples.

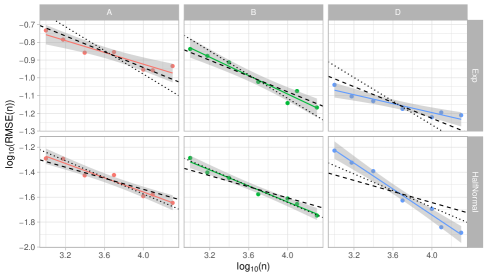

The Metropolis-Hastings proposals for updating the ’s were tuned such that the acceptance rate was about in all cases. If the averages are denoted by , we finally computed the Root Mean Squared Error, defined by . By repeating this experiment for all three choices of base measure and various values of , we obtained figure 4. The contraction rate is an asymptotic property, and hence there is definitely uncertainty on which values of correspond to that. The computed slopes do not give a conclusive answer to the actual rate of contraction. For the halfNormal distribution, it is conceivable that methods (A) and (B) yield rate , whereas method (D) gives a rate almost . The latter can intuitively be explained by the fact that the slope of the density of the halfNormal is zero at zero which coincides with realisations from the prior. For the Exponential distribution, methods (A) and (B) support rate , whereas method (D) has worse rates. For completeness, we tabulated the computed slopes in Table 1. The difficulty with rate-assessment by finite samples for Dirichlet mixture priors has been noted recently in Wehrhahn, Jara & Barrientos (2019) as well.

| Method | |||

|---|---|---|---|

| A | B | D | |

| Exp | |||

| halfNormal | |||

5.5 Comparing between Bayesian and various frequentist methods for estimating at 0

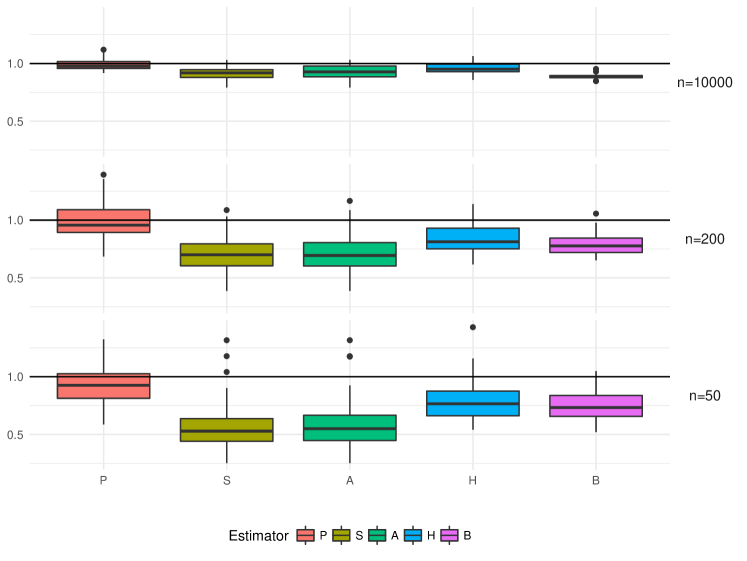

In this section we present a simulation study comparing our Bayesian estimator (posterior median) with various frequentist estimators available for discussed in section 4. We simulated 50 samples of sizes from the standard exponential distribution and halfNormal distribution. For each sample, the following estimators are calculated: the posterior median estimator , the penalized NPMLE , the two estimators and and the histogram type estimator . All these estimators require choosing some input parameters.

- 1.

-

2.

For the penalized estimator the parameter was taken with

Here is the second point of jump of and for (listed in Woodroofe & Sun (1993)).

-

3.

For no tuning is needed. For the other estimator we take , where

(5.3) a consistent estimator of where

-

4.

For the histogram estimator , was chosen with as in (5.3).

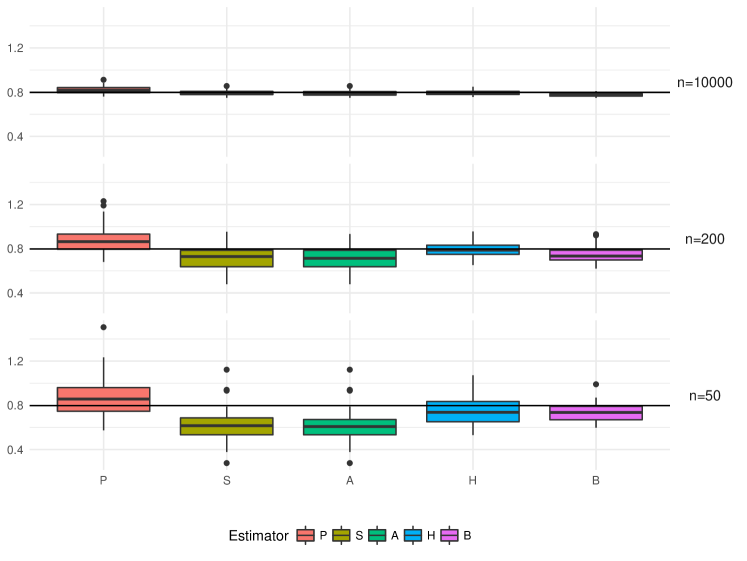

Figure 5 shows, for each combination of sample size and estimation method described, the boxplots of the 50 realized values based on samples from the standard exponential distribution. Figure 6 shows these boxplots for the samples from the halfNormal distribution.

In table 2 we compare the bias, variance and mean squared error of these consistent estimators based on data from the standard exponential distribution. For the standard exponential data, the penalized estimator performs best in the MSE sense. The Bayesian estimator has smallest variance, but big bias when the sample size is large (). This might be explained by the small contraction rate at zero, but also by the fact that the Bayesian method is not specifically aimed at only estimating the density at zero, but instead the full density.

| 50 | Bias | -0.067 | -0.423 | -0.402 | -0.214 | -0.266 |

|---|---|---|---|---|---|---|

| Var | 0.033 | 0.042 | 0.049 | 0.030 | 0.013 | |

| MSE | 0.037 | 0.222 | 0.210 | 0.076 | 0.084 | |

| 200 | Bias | -0.001 | -0.286 | -0.271 | -0.158 | -0.221 |

| Var | 0.029 | 0.020 | 0.027 | 0.015 | 0.007 | |

| MSE | 0.029 | 0.101 | 0.100 | 0.040 | 0.056 | |

| 10000 | Bias | -0.011 | -0.084 | -0.072 | -0.041 | -0.112 |

| Var | 0.002 | 0.002 | 0.003 | 0.002 | 0.0004 | |

| MSE | 0.002 | 0.010 | 0.009 | 0.004 | 0.013 |

Table 3 lists the bias, variance and MSE values of the estimators with observations sampled from the halfNormal distribution. For the halfNormal data, the histogram estimator behaves best in the bias and MSE sense. This can probably be explained by the behaviour of near zero, note that in the halfNormal case. The estimator for , , probably quite unstable which leads to big value for resulting in a big bandwidth . As the behaviour of the underlying density is “flat” near zero, the MSE-optimal choice of bandwidth is of the slower order . The posterior mean again has smallest variance.

| 50 | Bias | 0.063 | -0.182 | -0.185 | -0.043 | -0.073 |

|---|---|---|---|---|---|---|

| Var | 0.029 | 0.022 | 0.022 | 0.016 | 0.007 | |

| MSE | 0.033 | 0.055 | 0.056 | 0.018 | 0.012 | |

| 200 | Bias | 0.080 | -0.086 | -0.088 | -0.011 | -0.051 |

| Var | 0.014 | 0.012 | 0.012 | 0.004 | 0.005 | |

| MSE | 0.020 | 0.019 | 0.020 | 0.004 | 0.008 | |

| 10000 | Bias | 0.0216 | -0.0022 | -0.0060 | -0.0019 | -0.0239 |

| Var | 0.0010 | 0.0005 | 0.0006 | 0.0005 | 0.0002 | |

| MSE | 0.0015 | 0.0005 | 0.0006 | 0.0005 | 0.0008 |

5.6 Application to fertility data

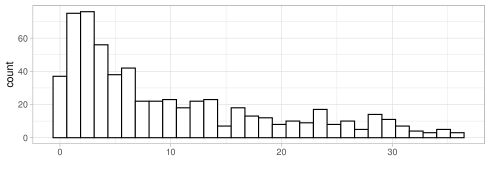

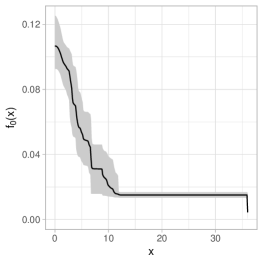

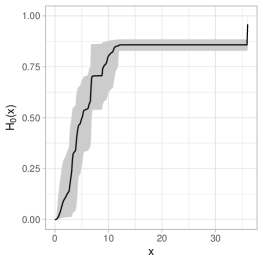

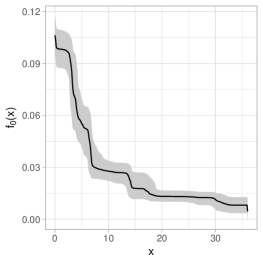

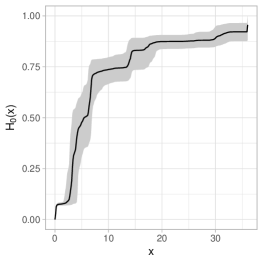

In Keiding et al. (2012) data concerning the fertility of a population are analysed. The aim is to estimate the distribution of the duration for women to become pregnant from when they start attempting, based on data from so-called current durations. These current durations can be modeled as described in the introduction. Indeed, the true durations are modeled as sample from an unknown distribution function . According to length-biased sampling, individuals are selected and then the time since the start of attempting to become pregnant is administered. This is called the current duration, and can be seen as a uniform random fraction of the true duration of the selected individual. This current duration then has bounded decreasing probability density as given in (1.2). The distribution function of the durations , can be expressed in terms of as in Equation(1.3). For more information on the design of this study we refer to Keiding et al. (2012). For illustration purpose we only used the measured current durations that do not exceed months. Figure 7 shows the histogram of 618 raw data, modeled as sample from the decreasing density .

In this section we estimate the density using base measure choice (A) which satisfies assumption 2.1 and (D) which does not satisfy assumption 2.1 with concentration parameter . Then each MCMC iterate of the posterior mean can be converted to an iterate for using the relation (1.3). In Groeneboom & Jongbloed (2015) chapter 9, pointwise confidence bands for and are constructed based on the smoothed maximum likelihood estimator. Having derived the estimators, producing such confidence bands needs quite some fine tuning. In this section, we construct the Bayesian counterpart of the confidence bands, credible regions for . Contrary to the frequentist approach, having the machinery available for computing the posterior mean, the pointwise credible sets can be obtained directly from the MCMC output. The results for the fertility data are shown in Figures 8 using base measures (A) and (D) respectively.

6 Discussion

In this paper we have used Bayesian analysis to nonparametrically estimate a decreasing density based on a random sample. Particular emphasis is given to estimation of the density at zero and sufficient criteria on the base measure of the prior are derived to obtain contraction rate . Besides a base measure attaining this rate, we have investigated the relative performance of other base measures by means of a Monte Carlo study. This study was extended to compare multiple frequentist estimators for estimating the density at zero to a Bayesian derived point estimator.

It remains an open question whether for a given density function there exists a base measure such that the contraction rate for estimation of is . From the simulation study it appears that taking a mixture of Pareto densities as base measure empirically yields satisfactory performance and henceforth we recommend taking base measure (D) from Section 5.1.

Appendix A Review and supplementary proof of inequality (2.10)

In this section we point out a technical issue arising in the proof of inequality (2.10). As mentioned in section 2.2, it suffices to lower bound the prior mass of a certain subset of , for which lower bounding is tractable. To construct this set, we first need some approximation results.

Lemma A.1.

For any there exists a discrete measure , with , , and such that

Moreover, the sequence can be taken such that for all .

Proof.

Without the claimed separation property, existence of the discrete measure follows from lemma 11 in Salomond (2014). Denote this measure by and note that . The set is obtained from by removing points from the latter set which are not -separated. Clearly, . The mass of any removed point is subsequently added to the point () that is closest to . Denote the mass of , obtained in this way, by . Hence, we can written , where if assigned to . Furthermore,

Since for any ,

This implies that

The claimed result now follows from the triangle inequality and that the squared Hellinger distance is bounded by the -distance. ∎

Lemma A.2.

Assume satisfies assumption 2.2. There exists a discrete probability measure , supported on , with such that

Proof.

Corollary A.3.

Assume satisfies assumption 2.2. There exists a discrete probability measure , supported on , with , and such that

Moreover, the sequence can be taken such that for all .

For easy reference, we redefine the weights of the measure from this corollary so that we can write .

Next, we use the support points and masses of the constructed measure . To this end, define

such that is a partition of . Now define the following set of decreasing densities

To prove that is a subset of a key property is that the measure is constructed such that (see the proof of lemma 8 in Salomond (2014)). Moreover, the prior mass of is tractable because is a partition of .

Remark A.4.

If the set is defined with the masses from lemma A.1 (as is done in Salomond (2014), then the resulting sets do not form a partition. This results in intractable expressions for . For that reason, we defined another discrete measure such that the support points are separated thereby fixing the issue.

The arguments for lower bounding can now be finished as outlined in Salomond (2014). Without loss of generality, for sufficiently large we can assume , for . Similar to Lemma 6.1 in Ghosal et al. (2000), we have

Here we use . As we have

Substituting this bound into the lower bound on , combined with the inequalities for and , we obtain

When it is trivial that and therefore

For bounding when , we use the property of in (2.1): . In this case we have

Implying

Since , we therefore have

| (A.1) |

Therefore, we obtain

for some . This is exactly as is required.

Appendix B Some details on the simulation in section 5

In this section we provide some computational details for updating the -values in the MCMC-sampler. Given the initialisation of , we numerically evaluate for . If is not conjugate to the uniform distribution, we use the random walk type Metropolis-Hastings method sampling from using the normal distribution. For update each , if , we first remove . If we draw a new ”cluster” for , , then we also draw a new sample for according to (3.2). In this case, the product only has one item, that is . Sampling a value for is done as follows:

-

1.

If the base density is as in (5.2), then we use rejection sampling. To that end, if we set , then

where is a constant such that . For reject sampling, we choose the proposal density to be uniform on . Since for any , an upper bound for is given by . Hence, we sample from as follows:

-

(a)

sample , ;

-

(b)

if

then accept and set ; else return to step (a).

-

(a)

-

2.

If the base density is , then

where . Hence the cumulative distribution function satisfies , when . By the inverse cdf method, can be sampled by first sampling and next computing .

Appendix C Results for the simulation experiment of Section 5.2 with sample size

References

- Balabdaoui et al. (2011) Balabdaoui, F., Jankowski, H., Pavlides, M., Seregin, A. and Wellner, J.A. (2011). On the Grenander estimator at zero. Statist. Sinica 21, p. 873–899.

- Bertoin (1998) Bertoin J. (1998). Lévy Processes. Cambridge University Press.

- Bezanson et al. (2017) Bezanson, J. and Edelman, A. and Karpinski, S. and Shah, V. (2017). Julia: A Fresh Approach to Numerical Computing. SIAM Review 59, p. 65-98.

- Blackwell and MacQueen (1973) Blackwell, D. and MacQueen J.B. (1973). Ferguson distributions via Polya urn schemes. Ann. Statist. 1, p. 353-355.

- Doss & Sellke (1982) Doss, H. and Sellke T. (1982). The Tails of Probabilities Chosen From A Dirichlet Prior. Ann. Statist. 10, p. 1302–1355.

- Ferguson (1973) Ferguson, T.S. (1973). A Bayesian Analysis of Some Nonparametric Problem. Ann. Statist. 1, p. 209–230.

- Ghosal et al. (2000) Ghosal, S., Ghosh, J.K. and Van der Vaart, A.W. (2000). Convergence rates of posterior distributions. Ann. Statist. 28, p. 500-531.

- Grenander (1956) Grenander, U. (1956). On the theory of mortality measurement. II. Skand. Aktuarietidskr., 39, p. 125–-153.

- Groeneboom & Jongbloed (2014) Groeneboom, P. and Jongbloed, G. (2014). Nonparametric estimation under shape constraints. Cambridge University Press.

- Groeneboom & Jongbloed (2015) Groeneboom, P. and Jongbloed, G. (2015). Nonparametric confidence intervals for monotone functions. Ann. Statist. 43, p.2019-2054.

- Groeneboom et al. (2001) Groeneboom, P., Jongbloed, G. and Wellner, J.A. (2001). Estimation of a convex function: characterizations and asymptotic theory. Ann. Statist. 29, p. 1653-1698.

- Hoffmann (2015) Hoffmann, M., Rousseau, J., and Schmidt-Hieber, J. (2015). On adaptive posterior concentration rates. Ann. Statist. 43, p. 2259–-2295.

- Kulikov & Lopuhaä (2006) Kulikov, V.N. and Lopuhaä, H.P. (2006). The behavior of the NPMLE of a decreasing density near the boundaries of the support. Ann. Statist. 34, p. 742–-768.

- MacEachern and Müller (1998) MacEachern, S.N. and Müller, P. (1998). Estimating Mixture of Dirichlet Process Models. J. Comput. Graph. Statist. 7(2), 223–238.

- Meyer & Woodroofe (2004) Meyer, M.C. and Woodroofe, M. (2004). Consistent maximum likelihood estimation of a unimodal density using shape restrictions. Can. J. Statist. 32, p. 55–-100.

- Neal (2000) Neal, R.M. (2000). Markov Chain Sampling Methods for Dirichlet Process Mixture Models. Journal of Comp. and Graph. Statist. 9, p. 249-265.

- Orbanz (2014) Orbanz, P. (2014). Lecture Notes on Bayesian Nonparametrics. Version: May 16, 2014.

- Salomond (2014) Salomond, JB. (2014). Concentration rate and Consistency of the posterior distribution for selected priors under monotonicity constraints. Electron. J. Statist. 8, p. 1380-1404.

- Sethuraman (1994) Sethuraman, J. (1994) A constructive definition of Dirichlet priors. Statist. Sinica, 4(2), 639–650.

- Keiding et al. (2012) Slama, R. and Højbjerg Hansen, O.K. and Ducot, B. and Bohet, A. and Sorensen, D. and Allemand, L. and Eijkemans, M.J. and Rosetta, L. and Thalabard, J.C. and Keiding, N. and others. (2012). Estimation of the frequency of involuntary infertility on a nation-wide basis. Human Reproduction 27, p. 1489–1498.

- Van der Vaart and Ghosal (2017) Van der Vaart, A.W. and Ghosal, S. (2017) Fundamentals of Nonparametric Bayesian Inference. Cambridge Series in Statistical and Probabilistic Mathematics.

- Van der Vaart (1998) Van der Vaart, A.W. (1998). Asymptotic Statistics. Cambridge University Press.

- Vardi (1989) Vardi, Y. (1989). Multiplicative censoring, renewal processes, deconvolution and decreasing density: nonparametric estimation. Biometrika 76, p.751–761.

- Watson (1971) Watson, G.S. (1971). Estimating functionals of particle size distributions. Biometrika 58, p. 483–490.

- Wehrhahn, Jara & Barrientos (2019) Wehrhahn, C., Jara, A., and Barrientos A.F. (2019). On the small sample behavior of dirichlet process mixture models for data supported on compact intervals.Communications in Statistics-Simulation and Computation. p. 1–25.

- Wickham (2016) Wickham, H. (2016). ggplot2: Elegant graphics for data analysis, 2nd ediition, Springer-Verlag, New York.

- Williamson (1956) Williamson, R. E. (1956). Multiply monotone functions and their Laplace transforms. Duke Math. J. 23, p. 189–207.

- Woodroofe & Sun (1993) Woodroofe, M. and Sun, J. (1993). A penalized maximum likelihood estimate of when is non-increasing. Statist. Sinica 3, p. 501–515.