Primal-dual stochastic gradient method for convex programs with many functional constraints††thanks: This work is partly supported by NSF grant DMS-1719549.

Abstract

Stochastic gradient method (SGM) has been popularly applied to solve optimization problems with objective that is stochastic or an average of many functions. Most existing works on SGMs assume that the underlying problem is unconstrained or has an easy-to-project constraint set. In this paper, we consider problems that have a stochastic objective and also many functional constraints. For such problems, it could be extremely expensive to project a point to the feasible set, or even compute subgradient and/or function value of all constraint functions. To find solutions of these problems, we propose a novel (adaptive) SGM based on the classical augmented Lagrangian function. Within every iteration, it inquires a stochastic subgradient of the objective, and a subgradient and the function value of one randomly sampled constraint function. Hence, the per-iteration complexity is low. We establish its convergence rate for convex problems and also problems with strongly convex objective. It can achieve the optimal convergence rate for convex case and nearly optimal rate for strongly convex case. Numerical experiments on a sample approximation problem of the robust portfolio selection and quadratically constrained quadratic programming are conducted to demonstrate its efficiency.

Keywords: stochastic gradient method (SGM), adaptive learning, augmented Lagrangian method (ALM), functional constraint, iteration complexity

Mathematics Subject Classification: 90C06, 90C25, 90C30, 68W40.

1 Introduction

In this paper, we consider the constrained stochastic program

| (1) |

where is a convex set in , is a random variable, and is a convex function for each . All nonlinear optimization problems in can be formulated in the form of (1). We are particularly interested in the case that is a large number.

To find a solution of (1), we aim at designing a novel primal-dual stochastic gradient method (SGM). We assume an oracle, which can return a stochastic approximation of a subgradient of , and also the function value and a deterministic subgradient of each at any inquired point . Since is big, it would be computationally very expensive if at every update, we inquire the objective value and/or subgradient of all ’s. Based on this observation, our algorithm, at every iteration, will simply call the oracle to return subgradients and function values of a few sampled constraint functions.

The algorithm is derived based on the classical augmented Lagrangian function (c.f. [19, 20]) of an equivalent rescaled variant of (1), i.e.,

Here, is the penalty parameter, is the Lagrangian multiplier or dual variable,

| (2) |

and

| (3) |

Note that is convex in and concave in . Given , the augmented dual function is defined as

| (4) |

At each iteration , we first sample one constraint function . Secondly we call the oracle to obtain a stochastic subgradient of , and a subgradient and the function value of at . Let

| (5) |

Then is a stochastic subgradient of with respect to . Thirdly we perform a projected stochastic subgradient update as in (6) to the primal variable , and finally we update dual variable .

| (6) |

| (7) |

The pseudocode of the proposed method is shown in Algorithm 1, which iteratively performs (adaptive) stochastic subgradient update to the primal variable and randomized coordinate update to the dual variable . In order to have an easy update, will be set to a diagonal matrix for each . We will consider two different settings of in our analysis.

Setting 1.

, where for all , and is the identity matrix.

Setting 2.

, where and with and for all . Here, and denote the componentwise square and square-root for a vector .

Note that in Setting 2, is adaptive to the primal stochastic subgradient. We scale the subgradient for technical reasons, and it is inspired by [29]. With such a setting, Algorithm 1 is an adaptive primal-dual stochastic gradient method, and it appears to be the first one under the primal-dual setting. Although the same order of convergence rate will be shown for both settings, the adaptive one can numerically perform significantly better.

We remark that if the potential application has any affine equality constraint , we can always write it into two affine inequality constraints and and thus formulate the problem in the form of (1), or we can use a technique similar to that in [27] to handle the equality and inequality constraints simultaneously. Furthermore, instead of sampling one constraint function every time, we can sample a small set of constraint functions, and let

in the update (6) and also update for all . All our convergence results can still be obtained.

1.1 Motivating examples

We give a few examples that can be written in the form of (1) with a very big , and our proposed algorithm can be applied.

Stochastic linear programming. A two-stage stochastic linear program (c.f. [22, Sec. 2.1]) can be formulated as

| (8) |

where and are respectively the data and the optimal value of the second stage linear program

As there are scenarios in the second stage, i.e., with and , then

Hence, (8) can be written as a single large-scale linear program:

| (9) |

Clearly, (9) is in the form of (1), and if there are many scenarios, i.e., is big, it could be extremely expensive to access all the data at every update to the variables.

Chance constrained problems by sampling and discarding. A nonlinear program with chance constraint is formulated as

| (10) |

where is a convex set, is an uncertain parameter on a support set , and is a user-specified risk level of constraint violation. Even though is convex for any , the chance constraint set in (10) may not be convex. Hence, exactly solving (10) is hard in general. To numerically solve (10), the work [4] introduces a sample-based approximation method, called sampling and discarding approach. This method makes independent samples of , then eliminates of them, and solves a deterministic problem with the remaining constraints, i.e.,

| (11) |

where contains the samples after discarding. It is shown that under certain assumptions, for any , if

| (12) |

the solution of (11) is feasible for (10) with probability at least .

Note that if no discarding is performed, the above method is similar to the scenario approximation approaches in [14, 10]. For high-dimensional problems, i.e., is big, it is required to set a significantly bigger and also to have (12). Therefore, the sample-based approximation problem (11) will have many functional constraints and be in the form of (1).

Robust optimization by sampling. Different from the chance constrained problem (10), robust optimization requires the constraint to be satisfied for any , i.e.,

| (13) |

Similar to the scenario approximation method for chance constrained problems, the sampling approach (e.g., [3]) has also been proposed to numerically solve (13). Let be independently extracted samples. It is shown in [3] that for any and any , if the number of samples satisfies then the solution to (11) will be a -level robustly feasible solution with probability at least . If is big, and high feasibility level and high probability are required, then would be a very big number, and thus (11) has an extremely big number of functional constraints.

1.2 Existing methods

In this subsection, we review a few existing methods that could potentially be applied to solve (1) and show how our method relates to them. Some of these methods are primal-dual type as our method, and others are purely primal methods.

Stochastic mirror-prox method. The proposed method is closely related to the stochastic mirror-prox method [7, 1] for saddle-point problems or more generally for variational inequality (VI) problems. By the augmented Lagrangian function, one can equivalently formulate (1) into the following saddle-point problem (c.f., [18]):

| (14) |

Assuming to be Lipschitz continuous and in a compact set , then we can apply the method in [1] to the above saddle-point problem and have the update:111Here, we use the Euclidean norm square as the proximal term, while [1] actually uses a more general Bregman distance function.

| (15a) | ||||

| (15b) | ||||

where and are stochastic approximation of at and . The above update performs two stochastic gradient (SG) projections. To have convergence, it seems to be required for VI problems. However, for saddle-point problems, [13] shows that one SG projection is sufficient for convergence guarantee, namely, simply set and then obtain by (15b).

The methods in [1] and [13] both require the dual variable to be in a compact set for convergence guarantee. Generally, it is difficult to estimate a valid bound on the dual variable, especially for a stochastic program. In addition, at each iteration, they use the same step size for both primal and dual variable update, which seems to be required in their analysis. On the contrary, we will not assume boundedness of but instead we can prove the boundedness of the sequence in expectation. Furthermore, we allow to use different step sizes, and this is crucial for the convergence analysis of our adaptive method.

The SGM for saddle-point problems is also studied in [15]. However, it requires strong convexity for both primal and dual variables. For bilinear convex-concave saddle-point problems, the authors of [5] give an optimal primal-dual SGM. Without assuming boundedness on either primal or dual variables, they show an convergence rate in terms of a perturbed primal-dual gap, c.f. [5, Corollary 3.4]. Applying their method, i.e., [5, Algorithm 3], to an affinely constrained convex problem, one can show that if the primal variable and the output dual iterate are bounded, then the convergence rate is in terms of both primal-dual objective gap and feasibility violation.

Cooperative stochastic approximation. The problem (1) can also be equivalently formulated as a stochastic program with a single finite-sum constraint:

| (16) |

and we can apply the cooperative stochastic approximation (CSA) method in [8] to find an approximate solution. At each iteration , CSA first samples one constraint function and check its value at the iterate . If , set , and otherwise, set to an unbiased estimate of , where is a parameter to control constraint violation. Then it updates the iterate by

| (17) |

where is a step size.

For convex problems, CSA is shown to enjoy convergence rate in terms of both objective and feasibility. The order can be improved to if both the objective and constraint functions in (16) are strongly convex. We will show that the proposed algorithm can enjoy the same order of convergence rate for convex problems. To have an improved rate of , we need strong convexity of the objective function but only convexity on the constraint functions. However, we need an additional assumption on the existence of a primal-dual solution. Hence, our method has better convergence rate for the problem with a strongly convex objective but only convex constraint functions, such as finding the projection onto the intersection of many polyhedral sets [16, 23].

Stochastic subgradient with random constraint projection. Let and

| (18) |

Then (1) can be written to

| (19) |

On solving the above problem, we can apply the method in [25, 24] and iteratively perform the update:

| (20) |

where is randomly chosen from , denotes the projection onto , and is a stochastic approximation of a subgradient of at . Various sampling schemes on are studied in [24]. Under the linear regularity assumption on the set collection , a sublinear convergence result is established. If is convex, the rate is in terms of objective error and in terms of constraint violation . In [25], the rate of constraint violation is improved to . Furthermore, if is strongly convex, [25] shows the convergence rate in terms of objective error and of constraint violation. To have efficient computation in the update (20), is required to be a simple set for each . Hence, if ’s are difficult to evaluate, such as the logistic loss function induced constraint set in the Neyman-pearson classification problem [17], the method in [25, 24] will be inefficient. By contrast, our update in (6) can be computed efficiently as long as is simple.

Stochastic proximal-proximal gradient method. Let and , where denotes the indicator function on , and ’s are defined in (18). Then (1) is equivalent to

| (21) |

When is differentiable, the stochastic proximal-proximal gradient (S-PPG) method [21] can be applied to find a solution of (21). It starts from and iteratively performs the update:

| (22) | ||||

where is chosen from uniformly at random. Since needs be evaluated, S-PPG has the same issue as the update in (20). However, it could be more suitable in a distributed system, for which communication cost is a main concern.

Stochastic subgradient with single projection. Let . Then (1) is equivalent to

| (23) |

For solving the above problem, we can apply the method in [11], which, at every iteration, inquires a stochastic subgradient of and also a subgradient of . Although the method in [11] only needs to perform a single projection to the feasible set at the last step, computing the subgradient of would generally require evaluating the function value of all ’s, and thus it is inefficient for the big- case. This issue is partly addressed in [6], which only checks a batch of randomly sampled constraint functions at every iteration. However, depending on the underlying problem and required accuracy, the batch size could be as large as .

Deterministic primal-dual first-order method. Other related methods are the deterministic primal-dual first-order algorithms in the author’s previous works [27, 28]. Although [27, 28] also use the classic augmented Lagrangian function, their algorithm design and targeted applications are fundamentally different from those in this paper. The methods in [27, 28] assumes differentiability of ’s, and it requires exact gradient of and uses all to update and . Hence, if exact gradient of is not available or very expensive to compute, or if is extremely big, the deterministic methods are either inapplicable or inefficient. In addition, the update to and in Algorithm 1 is Jacobi-type while [27, 28] and all existing works about deterministic augmented Lagrangian method update the primal and dual variables in a Gauss-Seidel manner. Furthermore, due to the stochasticity, the analysis of this paper is fundamentally different and more complicated than that in [27, 28]. Similarly, the deterministic first-order methods in [30, 31, 9] are also very expensive or do not apply for the stochastic program with many constraints.

Besides the above reviewed methods, in the literature there are also other methods that can be applied to (1) such as the penalty method with stochastic approximation [8]. Exhausting all the existing methods is impossible. We refer the interested readers to the papers above and the references therein.

1.3 Contributions

The main contributions are listed below.

-

•

We propose a novel (adaptive) primal-dual SGM for solving stochastic programs with many functional constraints. The method is derived based on the classical augmented Lagrangian function. Through a stochastic oracle, it alternatingly performs stochastic subgradient update to the primal variable and randomized coordinate update to the dual variable. At each iteration, it only needs to sample one out of many constraint functions and thus has low per-iteration complexity.

-

•

We establish convergence rate results of the proposed method for convex problems and also problems with strongly convex objective. Different from existing analysis of primal-dual SGM for saddle-point problems, we do not assume the boundedness of the dual variable , but instead we prove the boundedness of the dual iterate in expectation. For convex problems, we show that the algorithm can achieve the optimal convergence rate, and for problems with strongly convex objective, we show that it can achieve convergence rate, where is the number of subgradient inquiries. All convergence rate results are in terms of primal and/or dual objective value and also primal constraint violation. For the strongly convex case, the factor can be removed if the dual iterate sequence is assumed to be bounded; see Remark 3.4. To the best of our knowledge, no existing work has established convergence rate result for a primal-dual SGM by assuming strong convexity only on the primal objective function, even if the dual variable is restricted in a bounded set. The CSA method in [8] is a primal SGM, and it has convergence rate if both the objective and constraint functions are strongly convex.

-

•

We show the practical performance of the proposed algorithm by testing it on solving a sample approximation problem of the robust portfolio selection and convex quadratically constrained quadratic programs. The numerical results demonstrate that the proposed primal-dual SGM can be significantly better than the stochastic mirror-prox algorithm in [1] and the CSA method in [8].

1.4 Notation and outline

We use bold lower-case letters for vectors and for their -th components. The bold number and denote the all-zero and all-one vectors, respectively. is short for the set , and respectively denote the positive and negative parts of a real number . Given a symmetric positive semidefinite matrix , is defined as . We use to denote the Euclidean norm of a vector . For two vectors and of the same size, denotes their componentwise product. For a convex function , we denote by a subgradient of at , and the set of all subgradients of at is called the subdifferential of , denoted by . For a closed convex set , denotes the projection operator onto . We let contain the history of Algorithm 1 until , i.e., denotes the expectation of a random variable , and is for the expectation of conditional on . In addition, we denote

| (24) |

The rest of the paper is outlined as follows. In section 2, we give the technical assumptions required in our analysis, and in section 3, we analyze the algorithm with nonadaptive setting and show its convergence rate results. The convergence rate result of the algorithm with adaptive setting is given in section 4. Numerical results are provided in section 5, and finally section 6 concludes the paper.

2 Technical assumptions

Throughout our analysis, we make the following assumptions.

Assumption 1.

There exists a primal-dual solution satisfying the Karush-Kuhn-Tucker (KKT) conditions:

| (25a) | |||

| (25b) | |||

| (25c) | |||

where denotes the normal cone of at .

Assumption 2.

The SG approximation is unbiased and bounded, i.e., there is a constant such that

In addition, there exist constants and such that

Assumption 3.

For each , is a closed convex function on . In addition, is -strongly convex, i.e.,

| (26) |

Assumption 1 is satisfied if a certain constraint qualification holds such as the Slater’s condition [2]. In Assumption 2, the unbiasedness and boundedness assumption on is standard in the literature of SGM, and the boundedness of each and is satisfied if is bounded. In Assumption 3, if , then is simply a convex function.

As the KKT conditions in (25) hold, there are such that

Hence, from the convexity of and , it follows that

| (27) |

Since and is convex for each , we have

The above inequality together with (27) and the fact implies

| (28) |

Furthermore, note that for any , it holds , and thus (25a) exactly means . Hence, is a solution of , which indicates From the definitions of and in (2) and (3), and also (25b) and (25c), it is straightforward to have . Therefore,

| (29) |

i.e., the strong duality holds, and and are primal and dual optimal solutions.

3 Convergence analysis of the nonadaptive method

For ease of understanding, we first analyze the convergence of Algorithm 1 with the nonadaptive Setting 1. Under Assumptions 1 through 3, we show that for convex problems, our method can achieve the optimal convergence rate , and for problems with strongly convex objective, it can achieve a near-optimal rate , where is the number of iterations. While existing analysis [12, 1] for saddle-point problems assumes the boundedness of the dual variable, we do not require such an assumption. Instead we can bound all in expectation by choosing appropriate parameters. In addition, we do not find any existing work that has shown rate for a primal-dual SGM by assuming strong convexity on the primal objective.

3.1 Preliminary results

We first establish a few preliminary results. The lemma below can be directly verified from the definition of .

Lemma 1.

Let . Then for any such that and any , it holds .

The next lemma is important to establish the convergence rate of our algorithm. Similar ones in a deterministic form have appeared in [28, 27].

Lemma 2.

Let and be random vectors, and let and be scalars. If for any and that may depend on , it holds

| (30) |

then for any satisfying (25),

| (31) | |||

| (32) | |||

| (33) |

Since , we have from (28) that

| (35) |

We obtain the inequality in (32), by substituting the above inequality into (34) with given by if and otherwise for any .

Letting if and otherwise for each in (34) and adding (35) together gives

| (36) |

Hence, by the above inequality and (35), we obtain In addition, from (34) with , it follows . Since for any real number , we have

which gives (31).

Furthermore, in (30), let and take We have which together with (35), (36), and (29) gives the inequality in (33).

Remark 3.1.

The following two lemmas will be used to establish an important inequality for running one iteration of Algorithm 1. Their proofs are given in the appendix.

Lemma 3.

For any deterministic or stochastic , it holds

| (37) | ||||

| (38) | ||||

Lemma 4.

Under Assumption 2, for any and any , it holds

| (39) |

By the previous three lemmas, we establish an important result for running one iteration of Algorithm 1 and then use it to show the convergence rate results.

Theorem 5 (fundamental result).

Proof. From the update (6), it follows that for any ,

| (43) |

Next we estimate a lower bound about the left hand side of the above inequality. First, We write By the Young’s inequality, it holds

| (44) |

Also, we write where . Hence, from (44) and (26), it follows that

Taking conditional expectation, we have from the above inequality and Assumption 2 that

| (45) | ||||

| (46) | ||||

| (47) |

Similar to (45), we have

| (48) | ||||

| (49) | ||||

where . Since is chosen from uniformly at random, by (5), (39) and the Young’s inequality, we have

| (50) | ||||

| (51) |

In addition,

| (52) |

Taking expectation on both sides of (45) through (52), summing them up, substituting into (43), and noting gives

| (53) | ||||

Taking expectation on both sides of (37), adding it to (3.1), and rearranging terms yield the desired result.

By Theorem 5, we can bound the growth of as below. Its proof is given in the appendix.

3.2 Convergence rate for convex problems

In this subsection, we establish the convergence rate of Algorithm 1 for convex problems, i.e., . Different from existing analysis for saddle-point problems, we do not assume the boundedness of the dual variable but instead we can bound in expectation.

Using Proposition 6, we specify the parameters and bound . The proofs of both propositions below are given in the appendix.

Proposition 7 (pre-determined maximum number of iterations).

If the maximum number of iterations is not pre-determined, we set parameters adaptive to iteration numbers and can still bound .

Proposition 8 (varying maximum number of iterations).

To show the convergence rate results, we need the following lemma to handle the last three expectation terms in (5). Its proof is given in the appendix and follows the proof of [13, Lemma 3.1].

Lemma 9.

For any deterministic or stochastic vector with and , it holds for any positive number sequence that

| (62) | |||

| (65) | |||

| (68) |

Using Theorem 5 and also the boundedness of , we are now ready to show the convergence rate results for the case . First, we establish a result with constant step sizes, and the order is , where is the iteration number.

Theorem 10 (Convergence rate for convex case with constant step sizes).

Proof. When the parameters are set according to (56), we have (57). Hence, multiplying to (5), summing it up from through , using (62) through (68), and noting give

Since , by the convexity of ’s and also concavity of about , we have from the above inequality and the definition of in (69) that

| (71) |

Let in the above inequality. Then by Lemma 1 and the definition of in (24), we have

Hence, (70a) and (70b) follow from the proof of Lemma 2 and Remark 3.1.

Furthermore, as is bounded, the inequality (71) implies

Therefore, we obtain (70c) from Lemma 2 and complete the proof.

Below we make a few remarks about the results in Theorem 10. Similar remarks also apply to Theorems 11 and 14 established later.

Remark 3.2.

From the proof of Theorem 10, we see that the setting of is for bounding . If the dual variable is bounded, then can be taken as large as the augmented penalty parameter .

Remark 3.3.

By the Markov’s inequality for a nonnegative random variable , one can easily have a high-probability result from Theorem 10. One drawback of the result is that in (70b), the bound is on the average of all inequality constraint violation. Let Then (70b) implies If , then the maximum violation of the inequality constraint is similar to the avarage violation. However, in the worse case, could be as large as .

One may argue that since the averaged constraint violation is used as a measure in the convergence rate result, it could be more natural to work on the equivalent problem (16), for which only one dual variable is needed instead of the many more dual variables required in Algorithm 1. We point out two potential issues to pursue this direction. First, the augmented Lagrangian function of (16) has a term that is a composition of given in (3) with the finite-sum . For a stochastic program with such a nested structure, the convergence rate of SGM is much worse [26] due to the difficulty of obtaining an unbiased SG. Second, the Slater’s condition can never hold for (16). Hence, although one dual variable is needed, the existence of a KKT point is not guaranteed even if the Slater’s condition holds for the original problem (1), and this would affect the convergence analysis. Also, we point out that the use of dual variables does not cause an issue of memory or computational cost. Compared to the data involved in the constraint functions, the size of dual variables is smaller.

With varying step sizes, we can also show a sublinear convergence rate result of Algorithm 1 as follows. The order is worse with an additional logarithmic term.

Theorem 11 (Convergence rate for convex case with varying step sizes).

Proof. When the parameters are set according to (59), we have (60). Hence, multiplying to both sides of (5), summing it over , and using (62) through (68), we have

| (74) |

Note

Hence, dividing both sides of (3.2) by , we have from the convexity of ’s and the concavity of about , and also using from (A.3) and the definition of in (72) that

Now following the same arguments as those below (71) in the proof of Theorem 10, we obtain the desired results and complete the proof.

3.3 Convergence rate for strongly convex problems

In this subsection, we analyze the convergence rate of Algorithm 1 for strongly convex problems, i.e., in (26). Similar to the convex case, we first bound by choosing appropriate parameters. The proof is shown in the appendix.

Proposition 12.

Similar to Lemma 9, we have the following result bounding the expectation terms in (5). The proof is also given in the appendix.

Lemma 13.

Under the assumptions of Proposition 12, for any deterministic or stochastic vector , we have

| (78) | ||||

| (79) |

Using (5) and (76), we establish the convergence rate result of Algorithm 1 for the case of as follows.

Theorem 14 (convergence rate for strongly convex case).

Proof. Let . Since , it holds , i.e., . Hence, summing up (5) with from through , using Lemma 13, and noting and the choice of yield

| (83) |

where in the first inequality, we have used the fact and , and in the second inequality, we have used (76) and (98), Lemma 1, the setting , and also the definition of in (81). Let in the above inequality. Then by (28), we have that

which clearly implies (80) by the parameters given in (75) and also .

Furthermore, dropping the terms about and on the left hand side of (3.3), and using the convexity of ’s, we have for any that

Now using Lemma 2 and Remark 3.1, we obtain the desired results.

Remark 3.4.

The order of the established rate is worse than the optimal one obtained for a primal SGM by a factor. That term appears essentially because of the setting of to bound the dual iterate. If we assume to be bounded, then we can set and remove the logarithmic term. Furthermore, if the maximum number of iteration is not given, we can set

with . These parameters satisfy the conditions in Proposition 6, and thus we can still have a sublinear convergence result through first bounding . However, there will be an additional term in the obtained result, i.e., for any positive integer . The result can be shown by following the proofs of Proposition 12 and Theorem 14. We leave it to the interested readers.

4 Convergence analysis of the adaptive method

In this section, we analyze Algorithm 1 with the adaptive Setting 2 for ’s. For simplicity and also due to the page limitation, we only consider the convex case with pre-determined maximum number of iterations. For the convex case with varying maximum number of iterations and the strongly convex case, we can have similar results as those in section 3.

Similar to the analysis in the previous section, we first bound as follows. Its proof is given in the appendix.

Proposition 15.

Assume that is bounded and also Assumptions 1 through 3 hold. Given a positive integer , let and such that , and let

| (84) |

Suppose that is generated from Algorithm 1 with set according to Setting 2 and all other parameters specified in (84). Then for any , we have

| (85) |

In addition, for any , it holds that

| (86) |

Here and

| (87) |

By the above proposition, we have the convergence rate estimate of Algorithm 1 with the adaptive Setting 2 about ’s.

Theorem 16.

Proof. Multiply to (5), sum it up from through , use (62) through (68) and also (85), and note . Then we have from (86) that

Now the desired results can be obtained by following the same arguments as those in the proof of Theorem 10.

Remark 4.1.

From the proofs of Proposition 15 and Theorem 16, we see that the inequality (85) is important to bound and to have the convergence rate results. In addition, while proving (85), we use the bound . Since we scale the SGs in Setting 2, we automatically have such a bound. Without the scaling process, we may not have it unless we assume the dual variable to be bounded.

5 Numerical experiments

In this section, we test the proposed method (named PDSG) on solving a sample approximation problem of the robust portfolio selection (RPS) and also three quadratically constrained quadratic programs (QCQP). We compare to the stochastic mirror-prox method in [7] and the CSA method in [8]. The RPS test is performed in MATLAB 2016a installed on a Macbook Pro with 8 gigabyte memory, while the QCQP test is in MATLAB 2018a installed on a Dell workstation with 32 gigabyte memory.

5.1 Sample approximation of robust portfolio selection

Suppose that one investor has a unit of capital to invest on assets. Assume the return rate of the -th asset follows a uniform distribution on for each . The RPS aims to maximize the expected return subject to a minimum return for all possible return rate, i.e.,

| (90) |

where . It is easy to see that the above robust constraint is equivalent to , and thus (90) can be equivalently formulated as a linear program with only two linear constraints and also the nonnegativity constraint.

Now suppose that the distribution of the return rate is unknown but its samples are available. Let be samples of and be the empirical mean. Then we can solve a sample approximation of (90), i.e.,

| (91) |

The sample approximation problem is still a linear program, and one can apply any linear program solver. We use the proposed method in this test simply to see if it can numerically perform well. We set and . All entries of are generated independently following the uniform distribution on . For each , we set with generated by uniform distribution on . Then we let

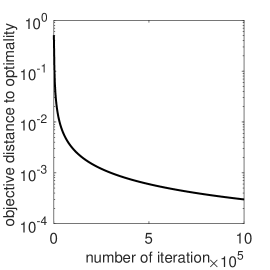

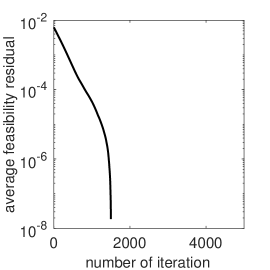

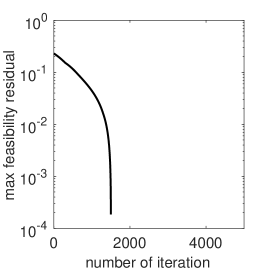

to ensure that (91) has a strict feasible solution. The parameters of our algorithm are set according to (56) with , and . The initial point is randomly generated. Figure 1 shows the distance of objective value to the optimal value, the averaged constraint violation, and also the maximum constraint violation, where the optimal objective value is obtained by MATLAB’s built-in function linprog. The feasibility curves only show the first 5,000 iterations, after which the points remain feasible. We also test the mirror-prox method [7] and the CSA method [8] and find that they perform almost the same as our method on this simple example.

5.2 Quadratically constrained quadratic program

In this subsection, we test the proposed method on a finite-sum structured quadratic program with many quadratic constraints, i.e.,

| (92) |

Here ; for each , and are randomly generated with components independently following standard Gaussian distribution; the entries of every also follow standard Gaussian distribution; ’s are randomly generated symmetric positive semidefinite matrices; each is generated according to uniform distribution on . Note that for the generated data, the Slater’s condition holds, and thus there must exist a KKT point for (92). Let be a random variable with uniform distribution on . Then the objective of (92) can be written to , and thus (92) is in the form of (1).

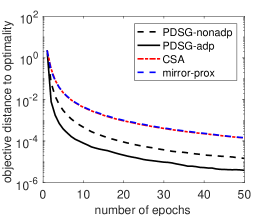

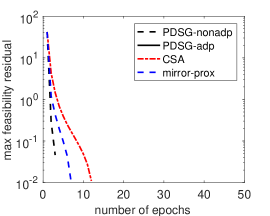

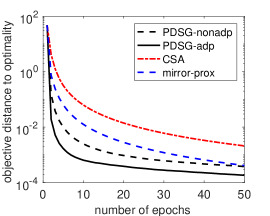

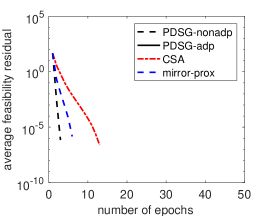

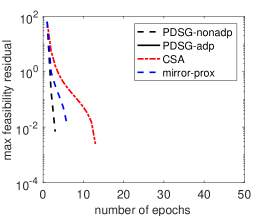

In the experiment, we test on three QCQP instances of different size. For all of them, we set in (92), and the dimension is set to , , and respectively for the three instances. We test the proposed algorithm with both nonadaptive and adaptive settings. For the nonadaptive one, we set algorithm parameters according to (56) with , , and , and it is named as PDSG-nonadp. For the adaptive method, i.e., given according to Setting 2, we set and the other parameters according to (84) with , , , and , and we name it as PDSG-adp. The stochastic mirror-prox method [7] with update given in (15) is applied on the equivalent saddle-point problem (14). Although the mirror-prox method requires a compact , we simply set , and the method still works well in this test. We use the same penalty parameter and the same step size as for our nonadaptive method. Also we apply the CSA method [8] with update given in (17). The same step size is used, and is set to for all . For all the tested methods, at each iteration, we sample 10 component functions in the objective and also 10 constraint functions to obtain an unbiased SG, i.e., mini-batch of size 10 is applied. Projecting onto the set does not generally admit an analytic solution and requires an iterative method. Hence, the methods in [24, 21] with updates (20) and (22) could be inefficient on solving the QCQP problem and are not compared.

Figure 2 shows the results for each method on the three QCQP instances, including the objective error, average constraint violation, and also maximum constraint violation with respect to epoch, where the “optimal” solution is computed by running PDSG-adp to 1,000 epochs for the smallest instance and 500 epochs for another two. Table 1 shows the running time (in second) of each method. Since all the tested methods have almost the same per-iteration complexity, their total running times are almost the same. The very long time for the largest instance is because the data size in this instance almost reaches the limit of machine memory. From the results, we see that the proposed algorithm performs significantly better than the stochastic mirror-prox and CSA methods. In addition, the adaptive PDSG is significantly better than the nonadaptive one. Note that we scale the SGs in the adaptive PDSG. Hence, with the parameters we set, the two PDSGs use roughly the same step size in this experiment. Therefore, the better performance of the adaptive method is mainly attributed to its different setting of .

| PDSG-nonadp | PDSG-adp | CSA | mirror-prox | |

| 20.20 | 20.69 | 20.56 | 20.32 | |

| 248.94 | 239.56 | 250.01 | 244.82 | |

| 20129.59 | 20044.41 | 20118.03 | 20161.85 |

6 Conclusions

We have proposed a primal-dual (adaptive) stochastic gradient method for stochastic programming with many functional constraints. Every iteration, the method only needs a stochastic subgradient of the objective, and a subgradient and the function value of one randomly sampled constraint function. Under standard assumptions, we have established its convergence rate for both convex and strongly convex problems. The order of rate is optimal for convex case and nearly optimal for strongly convex case. Numerical experiments on a sample approximation problem of the robust portfolio selection and quadratically constrained quadratic programming demonstrate its nice practical performance.

Acknowledgements

The author would like to thank the two anonymous referees for their constructive comments and suggestions, which greatly improve the paper. In particular, he very much appreciates the careful checking from one of them, who pointed out one technical mistake in the first submission. The author also would like to thank Professor Wotao Yin for his valuable discussions.

Appendix A Proofs of Propositions

A.1 Proof of Proposition 6

Let in (5). Then the last three expectation terms vanish. Since , we have by the definition of in (24) and Lemma 1 that

Multiplying to both sides of the above inequality gives

Summing the above inequality from through , we have by , noting from (28), and using the condition in (54) that

From the Young’s inequality, it follows that , which together with the above inequality gives the desired result.

A.2 Proof of Proposition 7

Let . It is easy to see that the parameters given in (56) satisfy the conditions in Proposition 6. Hence, for any , it follows from (55) that

| (93) |

Now we show the result in (57) by induction. Since , (57) holds trivially for . Assume it holds for . Then from (93), it follows that

which completes the proof.

A.3 Proof of Proposition 8

Let . It is easy to see that the parameters given in (59) satisfy the conditions in Proposition 6. Hence, plugging the specified parameters into (55) gives

| (94) |

By

| (95) |

we have from (A.3) that

| (96) |

Now we show the result in (60) by induction. When , it obviously holds. Assume the result holds for . Then from (A.3), it follows that

where the second inequality uses (A.3). This completes the proof.

A.4 Proof of Proposition 12

Let . If , then , i.e., . Hence, the parameters given in (75) satisfy the condition in Proposition 6, thus (55) holds and, with the specified parameters, becomes

| (97) | ||||

Note that for any ,

| (98) |

Hence, (97) implies

| (99) |

Now we show (76) by induction. When , it obviously holds since . Assume (76) holds for any . Then, from (98) and (99), it follows that

which completes the proof.

A.5 Proof of Proposition 15

We first prove (85). Since and , we have for any that

| (100) | ||||

| (101) | ||||

| (102) | ||||

| (103) |

where , and we have used the fact and for all and to have the last equality. By the Cauchy-Schwarz inequality and also noting due to the scaling in Setting 2, we have from (100) that

| (104) |

Hence, (85) holds.

Now let in (5) and sum it up from through . Note that the last three expectation terms in (5) vanish when . Then by (28) and Lemma 1, and also since , we have

which together with (104) by letting implies

Since and , multiplying to the above inequality and noting gives

Hence, by the Young’s inequality , we have from the above inequality that

Then following the same arguments as those in the end of the proof of Proposition 56, we can show the results in (86).

Appendix B Proofs of a few lemmas

B.1 Proof of Lemma 3

Note . Then the update of can be written in the compact form

| (105) |

where denotes componentwise product. Hence,

| (106) | ||||

Let

Note that for and any , it holds . Then from the definition of in (2), one can directly verify that

| (107) | ||||

| (108) | ||||

| (109) |

In addition, note

Hence, we have the desired result by adding (106) to (107) and using

B.2 Proof of Lemma 4

For any , we have for some that

From Assumption 2, note that and . Hence,

which implies the desired result.

B.3 Proof of Lemma 9

First note that . Hence, if is deterministic, the result in (62) trivially holds, and similarly if is deterministic, then the results in (65) and (68) hold. Next, we prove the results for the stochastic case.

B.4 Proof of Lemma 13

Denote . Let and for all . Then for any . Note . Hence,

where we have used . Since , we have (78) from the above inequality.

References

- [1] M. Baes, M. B rgisser, and A. Nemirovski. A randomized mirror-prox method for solving structured large-scale matrix saddle-point problems. SIAM Journal on Optimization, 23(2):934–962, 2013.

- [2] M. S. Bazaraa, H. D. Sherali, and C. M. Shetty. Nonlinear programming: theory and algorithms. John Wiley & Sons, 2013.

- [3] G. Calafiore and M. C. Campi. Uncertain convex programs: randomized solutions and confidence levels. Mathematical Programming, 102(1):25–46, 2005.

- [4] M. C. Campi and S. Garatti. A sampling-and-discarding approach to chance-constrained optimization: feasibility and optimality. Journal of Optimization Theory and Applications, 148(2):257–280, 2011.

- [5] Y. Chen, G. Lan, and Y. Ouyang. Optimal primal-dual methods for a class of saddle point problems. SIAM Journal on Optimization, 24(4):1779–1814, 2014.

- [6] A. Cotter, M. Gupta, and J. Pfeifer. A light touch for heavily constrained SGD. In Conference on Learning Theory, pages 729–771, 2016.

- [7] A. Juditsky, A. Nemirovski, and C. Tauvel. Solving variational inequalities with stochastic mirror-prox algorithm. Stochastic Systems, 1(1):17–58, 2011.

- [8] G. Lan and Z. Zhou. Algorithms for stochastic optimization with expectation constraints. arXiv preprint arXiv:1604.03887, 2016.

- [9] Q. Lin, S. Nadarajah, and N. Soheili. A level-set method for convex optimization with a feasible solution path. SIAM Journal on Optimization, 28(4):3290–3311, 2018.

- [10] J. Luedtke and S. Ahmed. A sample approximation approach for optimization with probabilistic constraints. SIAM Journal on Optimization, 19(2):674–699, 2008.

- [11] M. Mahdavi, T. Yang, R. Jin, S. Zhu, and J. Yi. Stochastic gradient descent with only one projection. In Advances in Neural Information Processing Systems, pages 494–502, 2012.

- [12] A. Nedić and A. Ozdaglar. Subgradient methods for saddle-point problems. Journal of optimization theory and applications, 142(1):205–228, 2009.

- [13] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4):1574–1609, 2009.

- [14] A. Nemirovski and A. Shapiro. Scenario approximations of chance constraints. In Probabilistic and randomized methods for design under uncertainty, pages 3–47. Springer, 2006.

- [15] B. Palaniappan and F. Bach. Stochastic variance reduction methods for saddle-point problems. In Advances in Neural Information Processing Systems, pages 1416–1424, 2016.

- [16] C. J. Pang. Set intersection problems: Supporting hyperplanes and quadratic programming. Mathematical Programming, 149(1-2):329–359, 2015.

- [17] P. Rigollet and X. Tong. Neyman-pearson classification, convexity and stochastic constraints. Journal of Machine Learning Research, 12(Oct):2831–2855, 2011.

- [18] R. T. Rockafellar. A dual approach to solving nonlinear programming problems by unconstrained optimization. Mathematical programming, 5(1):354–373, 1973.

- [19] R. T. Rockafellar. The multiplier method of hestenes and powell applied to convex programming. Journal of Optimization Theory and applications, 12(6):555–562, 1973.

- [20] R. T. Rockafellar. Augmented Lagrangians and applications of the proximal point algorithm in convex programming. Mathematics of operations research, 1(2):97–116, 1976.

- [21] E. K. Ryu and W. Yin. Proximal-proximal-gradient method. arXiv preprint arXiv:1708.06908, 2017.

- [22] A. Shapiro, D. Dentcheva, and A. Ruszczyński. Lectures on stochastic programming: modeling and theory. SIAM, 2009.

- [23] M. Stošić, J. Xavier, and M. Dodig. Projection on the intersection of convex sets. Linear Algebra and its Applications, 509:191–205, 2016.

- [24] M. Wang and D. P. Bertsekas. Stochastic first-order methods with random constraint projection. SIAM Journal on Optimization, 26(1):681–717, 2016.

- [25] M. Wang, Y. Chen, J. Liu, and Y. Gu. Random multi-constraint projection: Stochastic gradient methods for convex optimization with many constraints. arXiv preprint arXiv:1511.03760, 2015.

- [26] M. Wang, E. X. Fang, and H. Liu. Stochastic compositional gradient descent: algorithms for minimizing compositions of expected-value functions. Mathematical Programming, 161(1-2):419–449, 2017.

- [27] Y. Xu. First-order methods for constrained convex programming based on linearized augmented Lagrangian function. arXiv preprint arXiv:1711.08020, 2017.

- [28] Y. Xu. Iteration complexity of inexact augmented Lagrangian methods for constrained convex programming. arXiv preprint arXiv:1711.05812, 2017.

- [29] A. W. Yu, L. Huang, Q. Lin, R. Salakhutdinov, and J. Carbonell. Block-normalized gradient method: An empirical study for training deep neural network. arXiv preprint arXiv:1707.04822, 2017.

- [30] H. Yu and M. J. Neely. A primal-dual type algorithm with the convergence rate for large scale constrained convex programs. In Decision and Control (CDC), 2016 IEEE 55th Conference on, pages 1900–1905. IEEE, 2016.

- [31] H. Yu and M. J. Neely. A primal-dual parallel method with convergence for constrained composite convex programs. arXiv preprint arXiv:1708.00322, 2017.