Serve the shortest queue and Walsh Brownian motion††thanks: This is the final version of the paper. To appear in The Annals of Applied Probability.

Abstract

We study a single-server Markovian queueing model with customer classes in which priority is given to the shortest queue. Under a critical load condition, we establish the diffusion limit of the nominal workload and queue length processes in the form of a Walsh Brownian motion (WBM) living in the union of the nonnegative coordinate axes in and a linear transformation thereof. This reveals the following asymptotic behavior. Each time that queues begin to build starting from an empty system, one of them becomes dominant in the sense that it contains nearly all the workload in the system, and it remains so until the system becomes (nearly) empty again. The radial part of the WBM, given as a reflected Brownian motion (RBM) on the half-line, captures the total workload asymptotics, whereas its angular distribution expresses how likely it is for each class to become dominant on excursions.

As a heavy traffic result it is nonstandard in three ways: (i) In the terminology of Harrison [12] it is unconventional, in that the limit is not an RBM. (ii) It does not constitute an invariance principle, in that the limit law (specifically, the angular distribution) is not determined solely by the first two moments of the data, and is sensitive even to tie breaking rules. (iii) The proof method does not fully characterize the limit law (specifically, it gives no information on the angular distribution).

AMS subject classification: 60F05, 93E03, 60K25, 60J65, 60J70

Keywords: Serve the shortest queue, heavy traffic, diffusion limits, Walsh Brownian motion

1 Introduction

We consider a multiclass single-server queueing system operating under serve the shortest queue (SSQ) (also referred to in the literature as shortest queue first) regime, where service is offered to the customer class in which the queue is shortest. The practical significance of this policy has been recognized [19, 20, 6, 5, 3, 8, 9, 10], and analytic results have been obtained [8, 9, 10, 6]. Briefly, our probabilistic assumptions are that both arrival and potential service processes are Poisson, which makes the model Markovian, and that arrival and service rates are class-dependent. The diffusion scale behavior of the model in heavy traffic has not been studied before. The main result of this paper addresses the -dimensional nominal workload (a term adopted from [21], expressing conditional expectation of workload given the state) and queue length processes, where denotes the number of classes. It asserts that, under a critical load condition, the diffusion scale versions of both these processes converge to processes living in the set , which consists of the union of the coordinate axes in . Specifically, the rescaled nominal workload converges to a Walsh Brownian motion (WBM) on , and the rescaled queue length converges to a certain diagonal transformation of the same process.

WBM was introduced by Walsh in [27] as a planar diffusion that has a singular behavior at the origin. Away from the origin it evolves as a one-dimensional Brownian motion (BM) along a ray connecting its position to the origin, and its excursions into rays emanating from the origin follow a fixed angular distribution. Some early results on this process, including its special case referred to as skew BM, where the state space consists of exactly two rays, are [13, 23, 2, 26, 24, 1]. Intriguing aspects related to the natural filtration of this process were addressed in [25]. Recently, vast extensions of this model have been proposed and thoroughly studied. The reader is referred to [16] and the references therein for this development.

In the terminology of Harrison [12], an unconventional limit theorem for a queueing system in heavy traffic is one for which the limit process is not given as a reflected Brownian motion (RBM). Our result thus belongs to a family of unconventional heavy traffic limits, starting from [14] and including the more recent [17] as well as several other results surveyed in [29] and [17]. Moreover, our heavy traffic result is nonstandard in that it does not constitute an invariance principle. That is, it is observed in simulations that the limit law (specifically, the angular distribution of the limit WBM) is not determined solely by the first two moments of the data. The simulations also indicate that it is sensitive even to tie breaking rules. A third nonstandard aspect of the result is that the proof method does not provide an explicit expression or a characterization of the limit law. Whereas the modulus is given as an RBM with specified drift and diffusion coefficients, no information on the angular distribution is available from the proof. In fact, it appears unlikely to the authors that an explicit expression can be attained except under some special symmetry.

Some further details on the policy are as follows. In the literature, there are two variants, distinguished by the interpretation given to the selection of jobs from the shortest queue: that may refer to the one having least nominal workload or the one having least number of jobs. We adopt here the convention of [8, 9, 10] and work with the former. However, for all other purposes, the term queue length refers in this paper to job count. Next, the service rule is assumed to follow a preemptive priority. Finally, the tie breaking rule is a part of the model description. We allow for a rather general choice, by assuming that when the collection, , of classes having shortest queue consists of more than one class, the server’s effort is split according to a specified probability measure supported on the set .

Under static priority it is well known since Whitt’s result [28] that in heavy traffic, the queue which has least priority is always dominant, where this term means that nearly all the workload in the system is contained in this queue. Under SSQ, heuristically, one may imagine that very soon after each time the system (nearly) empties, a competition takes place among the queues, where the one that loses ends up with most workload and consequently least priority. Thus it is reasonable, in view of the aforementioned result on static priority, to expect that the losing class actually becomes dominant and remains so until again the system becomes empty (or nearly empty). This heuristic suggests, moreover, that the choice of the class to become dominant during an excursion (the outcome of the competition, one may say) is random, and is highly sensitive to the dynamics of the Markov process as the queues just start to build. The result of this paper reveals an asymptotic behavior with exactly these elements. One of the most significant and least obvious aspects of it is that the probabilities of each class becoming dominant starting from an empty system do converge in the scaling limit. Indeed, their limit is given by the WBM’s angular distribution.

An important feature of SSQ is that when two streams of arrivals have similar first order characteristics but one is more variable than the other, or has greater tendency to exhibit bursts, the policy tends to prioritize the former over the latter. This is due to the fact that a burst of traffic is likely to cause a long queue, resulting in lower priority. For this reason, SSQ has been referred to in the literature as ‘implicit service differentiation’ [20, 5, 6] and ‘self prioritization’ [5]. Quoting from [9], “…priority is thus implicitly given to smooth flows over data traffic… sending packets in bursts”. The policy has gained interest in technological uses, specifically in the context of packet scheduling [20, 6, 5, 3, 8, 9, 10]. For example, in [20, 5, 3] SSQ (referred to there as shortest queue first) is compared with first in first out and stochastic fairness queueing, via experimental tests, and is argued to be the best candidate solution for quality of service on ADSL internet access in various tests (web browsing, file download, peer-to-peer file sharing, VoIP and video calls, audio streaming, and video streaming). It is also found experimentally that the policy prioritizes TCP acknowledgment and delay- and loss-sensitive applications (voice, audio and video streaming), which leads to lower loss counts and delays. For further advantages and additional uses of this policy see [6] and the references therein, as well as [19].

The policy has been theoretically analyzed in several papers. Guillemin and Simonian [9] study the case of two buffers with Poisson arrivals and general service time distributions, establishing functional equations for the Laplace transform of the workload processes at stationarity. They also specialize to the symmetric, exponential service time case, where they are able to derive empty queue probabilities and tail behavior for the distribution of the workload. In [10] the authors study the same features in the asymmetric case, again for at stationarity, where service times are exponentially distributed. The paper [6] studies instantaneous throughput and buffer occupancy of long-lived TCP sources, using a deterministic fluid model, under three per-flow scheduling disciplines: fair queuing, longest queue first, and shortest queue first, assuming longest queue drop buffer management. They obtain closed form expressions for the stationary throughput and the buffer occupancy.

We now make some comments about the proof. To this end we introduce , , that are -valued processes indexed by the scaling parameter . The component represents the nominal workload in buffer at time , rescaled diffusively; the precise definition appears in §2. We start by treating the rescaled total nominal workload, , and recall the well-known fact that it converges to an RBM under any work conserving policy, to which SSQ is no exception. This result is required in a slightly extended form, stated in Lemma 3.1, which asserts that convergence holds uniformly with respect to initial conditions. The remainder of the proof has three main ingredients. The first is concerned with showing that resides close to as gets large. The aforementioned term ‘dominant queue’ is treated mathematically by considering tubes of width about each of the positive coordinate axes. In terms of these tubes, queue is dominant at time if resides in an -tube about axis , for arbitrarily small and large . Thus the first main ingredient of the proof is to show that the probability of exiting the collection of tubes tends to zero as . This is the content of Lemma 3.2(i). Note that this element, along with the weak convergence of the total nominal workload to an RBM, immediately provides the convergence of the modulus process to the same RBM.

The second main ingredient is concerned with the angular behavior. It is to show that the entrance law into tubes converges in the scaling limit. We consider first a special case of the model, that we call the homogeneous case, in which the transition intensities of the underlying Markov process corresponding to are rescaled version of those for . This trick buys us the ability to transform the double limit problem of entrance law into -tubes (involving and ) to a single limit (involving only). The existence of a limit of the entrance law is shown by arguing that, starting at the origin, the probabilities of entering -tubes form a Cauchy sequence, where is a suitable constant. The tools used to establish this argument are the martingale property of the total nominal workload (that also owes to homogeneity), and a strengthening of Lemma 3.2(i) which improves the exit probability estimates to polynomial estimates. Relying on the homogeneous case, the general case is then treated by means of a change of measure. The homogeneous case is stated in Lemma 3.5. The double limit assertion is stated as Proposition 3.3, and the reduced version in the form of a single limit is given in (3.43). The polynomial exit probability measure is proved by means of construction of a Lyapunov function for the distance of the state from , that may be interpreted as the nominal workload included in all but the dominant class. This tool is stated in Lemma 3.4. Finally, the change of measure argument is provided within the proof of Proposition 3.3 in §3.5.

The third main ingredient is the asymptotic independence of modulus and angle. This relies, first and foremost, on the second ingredient alluded to above, as well as on strong Markovity of the prelimit process and some estimates on the heat kernel associated with RBM on the half-line. This asymptotic independence property is stated in (3.14). These ingredients are finally combined in the proof of the main result, building on the characterization of WBM via its semigroup [1], and using crucially strong Markovity of the prelimit.

Some earlier results on the convergence of discrete processes to WBM appear in [13] and [11]. The paper [13] studies the case of a skew BM. The convergence result included within this paper addresses a suitably defined random walk on the integers observed at the diffusion scale, and establishes its weak convergence to a skew BM. The focus of [11] is the stochastic flow associated to WBM, and for this model, discrete approximations to the flow are obtained. In both these references, the pre-limit processes already live in a collection of rays ( in the former, , finite, in the latter), forming a symmetric random walk everywhere on the state space except at the origin. Consequently, the three main issues alluded to above in the description of our proof (estimates on exiting tubes, existence of a limit for the entrance probability into tubes, asymptotic independence) are all trivial in the cases studied in [13] and [11].

A general method was introduced in [18] for obtaining convergence of regenerative processes from a certain notion of convergence of their excursions. The regenerative processes we treat do fall into the category of those addressed in [18]. However, in the setting considered here, proving the convergence of excursions amounts, roughly speaking, to establishing the three ingredients alluded to above, and so it seems that as far as our result is concerned, this method does not provide a significant shortcut.

The paper is organized as follows. §2 presents the model and the main result. §3 is devoted to the proof. First, in §3.1, the result is proved based on Lemma 3.1, Lemma 3.2 and Proposition 3.3, stated in the beginning of the section. The convergence of the total nominal workload to an RBM is proved in §3.2. §3.3 provides estimates on probabilities to exit the tubes. §3.4 and §3.5 establish the limit result regarding the angular distribution, dealing with the homogeneous case and the general case, respectively. Finally, some concluding remarks are included in §4.

Notation

For ( a positive integer), let and denote the usual scalar product and norm, respectively. Denote and let denote the standard basis in . Let denote the -dimensional vector whose all entries equal 1. For and , let . Let denote the closed ball. Denote . For and , let , and, for , . For a Polish space , let and denote the set of continuous and, respectively, càdlàg functions . Let and denote the respective sets of functions . Endow with the Skorohod topology. A sequence of processes with sample paths in is said to be -tight if it is tight and every subsequential limit has, with probability 1, sample paths in . Write for convergence in law. Let denote the set of continuous, compactly supported functions on . For and , a -BM starting from is a -dimensional BM having drift , infinitesimal covariance and initial condition . A -RBM starting from is an RBM in with reflection at zero, with the corresponding parameters and initial condition . Denote by the collection of -dimensional probability vectors, namely . Throughout, we use the letter to denote a positive deterministic constant whose value may change from one appearance to another.

2 Setting and result

2.1 Serve-the-shortest-queue in heavy traffic

Consider a sequence of queueing models indexed by , defined on a probability space . A server operates to serve customers of classes. Each customer class has a dedicated buffer with infinite room. Upon arrival, a class- customer is queued in buffer . The process representing the number of customers in buffer is called the th queue length and is denoted by . The -valued random variable (RV) is referred to as the initial queue length. The arrivals are Poissonian and the service times are exponential. To model these, let be a collection of mutually independent Poisson processes, with right-continuous sample paths, independent of the initial queue length, where (resp., ) has rate (resp., ). The processes and represent the arrival and potential service processes for class , respectively. More precisely, is the number of class- customers to arrive (to buffer ) until time , and gives the number of class- service completions by the time the server has dedicated units of time to class- customers.

The process defined by

| (2.1) |

is referred to as the nominal workload process. This term, borrowed from [21], expresses the fact that represents the conditional expectation of the time it takes to serve the customers present in buffer at time , conditioned on (assuming that the server works exclusively on this class).

Within each class, only one customer may be served at a time (and for concreteness, we may assume it is the oldest one present in the system), although service effort is sometimes split among classes (see below). The priority rule among classes is to always serve the shortest queue as measured in terms of nominal workload. To make this statement precise some additional notation is required. We say that buffer contains the shortest queue at time , if

When there is exactly one buffer containing the shortest queue, the server serves it at full capacity (thus, service is preemptive). When there is more than one such buffer, the server’s effort is split among the buffers containing the shortest queue according to predetermined fractions in a head-of-the-line form. To model these fractions, it is assumed that for any we are given a vector , such that . When the collection of shortest queues is , the fraction of effort dedicated to class is given by . If we denote by the total effort dedicated to class by time (measured in units of time), then it is given by

| (2.2) |

where, for , we denote

| (2.3) |

The departure process consists of counting processes, where for each , gives the number of class- job completions. It thus satisfies

| (2.4) |

Clearly, satisfies the balance equation

| (2.5) |

This completes the description of the model. Note that according to this description, the queue length process is a Markov process on , whereas is a Markov process on

| (2.6) |

(where ‘u’ is mnemonic for unscaled). Thus an alternative, concise description of the model is via the generator of the process , denoted by . It is given by

| (2.7) |

for any bounded . Note that and that, by the assumptions on , whenever consists of the singleton , .

The parameters and are assumed to scale like . The precise assumption is that there exist constants and , such that for , as ,

| (2.8) | ||||

The system is assumed to be critically loaded in the sense that the overall traffic intensity equals 1. This is expressed as a condition on the first order parameters as follows,

| (2.9) |

Our main result regards rescaled versions of the nominal workload and queue length processes, defined as

| (2.10) |

Both these processes are obtained from via invertible transformations, and are therefore Markov processes on discrete spaces. The one to which most of the analysis is devoted in this paper is . Recalling (2.1), it follows that is a Markov process with state space

| (2.11) |

Specifically, the jump rates of both and are of order and their jump sizes are of order , confirming that (2.10) gives the usual heavy traffic scaling.

2.2 Walsh Brownian motion

In [27], Walsh introduced a diffusion process in the plane that can informally be described as follows. Let , , be the representation of the process in polar coordinates. Then the radial part is an RBM, and on each excursion of away from the origin, the angular part remains fixed. Moreover, the constant value which takes on each such excursion has a fixed distribution, independent for the different excursions. The precise definition that we shall work with is the one given by Barlow, Pitman and Yor [1], via its semigroup. However, rather than working with a planar diffusion we work with what is more natural for our purposes, namely a process in . Also, it is not necessary for our purposes to consider general angular measures, and so the presentation below is restricted to angular measures supported on the vectors .

Let , , and be given. Let , and , denote the semigroups of a -RBM and a -BM killed at 0, respectively. That is, for ,

where is a -RBM and denotes its hitting time at zero, and, throughout the paper, (resp., ) denotes the law of with (resp., the corresponding expectation). Let denote the -sphere. Use polar coordinates to denote members by setting and when , when . The semigroup of a -WBM is defined as follows. For , acts on as

| (2.12) |

where we denote

| (2.13) |

It is shown in [1] that is a Feller semigroup on and that there exists a strong Markov process with state space and semigroup , that has a.s.-continuous sample paths. Moreover, this process has the properties alluded to above. More precisely, when written in polar coordinates as , the radial part is a -RBM and the values that the angular part takes are constant on the interval (where the constant is determined by the initial condition ) as well as on each excursion away from zero. These constant values on the excursions away from zero are mutually independent with common distribution , where is the Dirac measure at . In this paper we are interested in the case where the initial condition is supported on . Note that in this case, takes values in for all .

Throughout, let and denote the law of for , and respective expectation. Then relations (2.12) can be expressed, for , as

| (2.14) |

2.3 Main result

The linear relation between and , the convergence that follows from (2.8), and the rescaling defined in (2.10) imply an asymptotic relation between and which one can express in terms of the matrix . For example, the statement is equivalent to the statement , as , where, throughout, the symbol denotes convergence in law under . Denote

Theorem 2.1

There exists such that, if is a -WBM with initial distribution supported on and then and , as .

Remark 2.2

(a) Whereas the coefficients and of the process

are given explicitly, our approach does not provide

a construction or any explicit information of the angular distribution .

However, this much can be said: does not depend on the second order

parameters

(where we use standard terminology by which and are called

first and second order parameters, respectively, due to the fact that in most conventional queueing models,

LLN limits depend only on the former, whereas CLT limits are also affected by the latter).

This statement is a direct consequence of our results of §3.5.

(b) Initial conditions which are not asymptotically concentrated

on are excluded from our treatment.

For such initial conditions the asymptotic behavior

is expected to follow a jump to at time zero,

and then proceed as a WBM.

However, the position to which the process jumps is dictated by

properties finer than the limiting initial distribution,

to the extent that the limit does not exist in general.

For example, for ,

a sequence of initial conditions may converge to a point

on the diagonal in such a way that .

It is not hard to see that,

due to even a small advantage to ,

the limiting process will initially jump to a point on the axis,

provided that tends to zero sufficiently slowly.

Interchanging the roles of and

will result in a jump to the axis.

3 Proof of the main result

Below we present two central lemmas and one central proposition required to prove our main result. The proof of the main result is presented next, in §3.1. The proofs of the lemmas and the proposition are then provided in §3.2–3.5.

Some notation used throughout this section is as follows. We use as shorthand notation for . For , let be defined by

| (3.1) |

The Skorohod map just introduced transforms a -BM starting from , say, , into a -RBM starting from the same point, via . The process given by gives the corresponding boundary term.

Let , , and let be a -RBM. In addition to the notation and introduced above, for each and , we use and for the law of the Markov process with , and the respective expectation. Moreover, for each and , we use and for the law of the tuple with , and the respective expectation.

Let . Finally, denote , and for ,

| (3.2) |

Both and are easily seen to be a.s. finite.

Lemma 3.1

i. The process is given as , where decomposes as . For each , (resp., ) is measurable w.r.t. (resp., ) and , where is a -BM starting from zero, whereas

| (3.3) |

As a consequence, if , then .

ii. For any ,

Throughout, let denote the class of functions for which as .

Lemma 3.2

The processes are -tight under .

Moreover, let denote the distribution of .

Then there exists such that

for every one has the following.

i.

as .

ii.

as ,

where the infimum extends over , and is a given

compact set.

iii. For , , , and ,

where we recall that .

Proposition 3.3

There exist and such that

| (3.4) |

3.1 Proof of Theorem 2.1

Given , define a sequence of hitting times as

| (3.5) | ||||

Let . When we need to emphasize the dependence on we write these RVs as and .

Let be a -WBM and assume, without loss of generality, that . For this process we define an analogous sequence of hitting times by

and set .

The weak convergence stated in Lemma 3.1(i) does not directly imply that of the hitting times of (3.2) to when both and start at zero. However, this convergence is clearly valid, as can be seen by using in addition the property of RBM that in probability as . Moreover, under , it is assumed in Theorem 2.1 that converges to in distribution. An inductive use of this fact yields a similar statement for the stopping times . More precisely, for any fixed , as , we have, the following uniform convergence: for any compact set and a function ,

| (3.6) |

The proof of the main result is based on finite-dimensional convergence and -tightness. The key ingredient is showing that for any compact set , , and a function ,

| (3.7) |

Before proving this statement we show, adapting the proof of Theorem 4.2.5 of [7], that it implies the convergence of to for finite-dimensional marginals. That is, for every , , that converges to , , , and functions , one has

| (3.8) |

We argue by induction over . The base case follows from (3.7). Next, assume that (3.8) holds for . Denote by the semigroup corresponding to . Then by Lemma 3.2(i), there exists , such that

where here denotes a generic function of that vanishes as . From (3.7) and the Feller property of proved in [1], it follows that for , as . It follows that the expression in the above display equals

| (3.9) |

By the induction hypothesis, the above expression converges to

This establishes (3.8). In view of the -tightness of stated in Lemma 3.2, this gives the main result .

The rest of the proof is devoted to showing that (3.7) holds. Fix . It suffices to prove the result for . Moreover, arguing by approximation, we may, and will assume that is constant on a ball about the origin. Thus, there exists for which vanishes for all with . We fix such , and let , and similarly let , and be defined in terms of the same value of .

Fix and a compact set . For , we will be concerned with and such that . We call such a pair a -admissible pair. In what follows we denote . Since and are arbitrary, to prove (3.7), it suffices to show that uniformly over -admissible pairs , for an arbitrary . Fix such a function . Notice that the assertions in Lemma 3.2(i), (ii), and Proposition 3.3 are all monotone in in the sense that if they hold for some then they also hold for a function that dominates and vanishes at infinity. Hence, without loss of generality, we may and will assume that Lemma 3.2(i), (ii), and Proposition 3.3 hold for the function that we have fixed.

On the intervals one has . As a consequence,

where

The above goal will be achieved once we show that, uniformly over -admissible pairs,

| (3.10) |

where we recall the definition of from (2.13), that for and for . Note that the first convergence is stated in Lemma 3.2(iii). Thus in what follows we focus on the term . Denote

Recall that the jumps of the (unscaled) queue length process are of size 1. By the way the scaled nominal workload process is defined, it follows that all the jumps of this process are bounded by , for some positive constant . As a consequence, one always has . Denote . It follows from Lemma 3.2(ii) that

uniformly over -admissible pairs. As a result,

where here and in what follows, is a generic function of and , that converges to zero as , uniformly over -admissible pairs .

Next we truncate the sum over . The tail can be estimated by . For a fixed initial condition , the -tightness of gives the tightness of the RVs . For arbitrary initial conditions , the strong Markovity reduces the same question to that of tightness of when starting at . Thus

| (3.11) |

where here and in what follows, refers to any function of satisfying .

Our next step is to use the condition included in the -th term in (3.11), to approximate the expression therein by . Note carefully that it is possible for the process to move from to , , without exiting or hitting the origin. Thus we must argue that, given any distinct and ,

| (3.12) |

The proof of this statement, which we now give, is based on the fact that in order for the process to behave as indicated in (3.1) while remaining within , it must reach close to the origin. Since we consider only finitely many ’s, it is sufficient to show that for every fixed , and ,

| (3.13) |

For every , , and define

The probability from (3.13) is bounded above by . Under this event, if the process does not leave between times and , then after time , it must reach close to the origin and not hit the origin prior to reaching a small neighborhood of . Therefore, the LHS of (3.13) is bounded by

where From Lemma 3.2(ii), the first term is . For every , let denote the filtration induced by . Then for the second term, using the strong Markov property,

where and . It remains to show that , for a constant. Now, , where . The last term goes to zero, uniformly in . This shows (3.1).

Equipped with (3.1), we have from (3.11)

Thus, using the uniform continuity of and denoting , ,

again using Lemma 3.2. The -th term can be written as

By strong Markovity, the conditional expectation above can be written as , where

This gives

Define . Then by Lemma 3.2(iii) one has for . Hence

It will be shown below that, for fixed , and are asymptotically independent, in the sense that

| (3.14) |

Hence

Using (3.6), and a similar argument based on strong Markovity,

Thus sending , then gives the second statement in (3.10).

It remains to prove (3.14). Since is continuous on and the law of has no atoms, it suffices to prove that for every and ,

| (3.15) |

uniformly over -admissible pairs . Toward showing (3.15), we argue that it suffices to establish this assertion for and . Indeed,

where we used the fact that , and , and denoted

Similarly, , . Thus if then we obtain

and since uniformly over -admissible pairs , (3.15) follows.

To prove (3.15) for and , note that under , and so is a.s. equal to (see (3.2)). Moreover, that has been defined as is a.s. equal to . Hence we aim now at showing

| (3.16) |

Without loss of generality, we take . In addition to the parameter , that has been fixed, we introduce a new parameter, , that will play the role of the parameter in Proposition 3.3. We introduce several pieces of notation associated with in a way analogous to those defined in terms of . Namely, , and . In addition, we let denote the probability measures supported on , given by .

Let

We analyze by studying its relation to . First,

| (3.17) |

where

Hence

| (3.18) |

where

We denote by (resp., ) any function of the tuple satisfying (resp., ). We argue that . To this end, note that

Now, as , uniformly for in . Moreover, for RBM, denoting the density by (where, as before, ), a uniform bound holds in the form

| (3.19) |

Indeed, an explicit eigenfunction expansion of the density is given in [15]. Using equations (3.15)–(3.19) of [15] one can directly obtain the bound for any constant . This gives (3.19). Using (3.19) for and the trivial bound for gives

for some constant (which may depend on ), for all . In view of this, , where the last inequality is standard, and follows by Brownian scaling.

Going back to (3.18) and noting that , we have . Therefore, it follows from Lemma 3.2(ii) that the probability of having is , hence

| (3.20) |

where by Proposition 3.3, (note that agrees with the ball from Proposition 3.3).

Next consider initial condition , for which we can write

where and . Now,

and for every that satisfies ,

Hence

| (3.21) |

where

and we used again the bound (3.1). To further bound , note that the argument provided earlier for can be used also for , and gives . On the indicated event, is bounded by the exit time of from the interval , the expectation of which is . Hence .

Next, for the RBM denote analogously . Denote

Then for all . Moreover, . Hence from (3.1) and (3.1) we obtain

Solving this system of equations gives

Denote

In order to show that it suffices to show that . Since it is known for RBM (equivalently, for a 1-dimensional BM) that for some constant and all small , it suffices to show that as . To this end, use strong Markovity to write

for . Now, , and therefore

Hence

where . If we show that then as , and the proof is established.

To show that , let denote the generator of the process , and for . Then is given by , with the Neumann boundary condition at and the Dirichlet boundary condition at , and is a smooth function satisfying

In particular, it is a smooth function satisfying , and therefore , for fixed and . This shows that .

3.2 The total nominal workload process

In this section we prove Lemma 3.1. Roughly stated, this lemma asserts that the total nominal workload process converges at diffusion scale to an RBM. This is a well-understood fact for an arbitrary non-idling policy. However, for completeness and since the statement of the lemma involves uniform convergence, which is perhaps less standard, we provide a proof.

Proof of Lemma 3.1. i. We start the proof with some notation aimed at describing the scaled nominal workload process in terms of scaled arrival and service processes. Let , and

for . Then by (2.5),

| (3.22) |

Note by (2.1) and (2.10) that . If we denote

then we have the identity . Moreover, by its definition, takes values in . Furthermore, by the non-idling property, the right derivative of at assumes the value 1 if and only if the system is non-empty at this time, that is, (it otherwise assumes the value 0). Consequently, . These three properties imply

| (3.23) |

It follows from the expression (3.1) for that for

| (3.24) |

Now, the bound for all gives . The quantities as well as converge in view of (2.8). Hence . Therefore,

By the functional central limit theorem for renewal processes (see Theorem 14.6 of [4]), converge to a BM with drift zero and diffusion matrix , where

This implies that is a tight sequence of RVs (for each fixed ), and in view of the above bound, so is .

By the discussion preceding Theorem 2.1, and are asymptotically related via the matrix . Appealing to (3.22) again and recalling that , we have , and we get the tightness of (uniformly in the initial state). In view of the definition of , we obtain that for every ,

| (3.25) |

Set

Notice that is measurable w.r.t. . Now,

where . The -tightness of along with (3.25) give (3.3). Finally, the convergence in law of gives , where is a -BM.

ii. Fix . For every with , one has by the representation , noting that is measurable w.r.t. ,

By part (i) of the lemma, specifically, the convergence of to (indep of ) and the uniform estimate (3.3) on , it follows that for every and all sufficiently large and with , the RHS of the above display is bounded below by . The last expression does not depend on and, as is a BM starting at the origin, converges to as . Therefore

Taking gives the result.

3.3 Estimates on exiting the tubes

In this section we develop an estimate on the displacement of the prelimit process away from . The main use of this estimate is in the argument provided in §3.4. In addition, the statement constitutes a strong form of that of Lemma 3.2(i). Thus at the end of the section we provide a proof of Lemma 3.2 based on this estimate.

The proof is based on a Lyapunov function technique. This function is constructed so that it expresses the total nominal workload in all buffers save the one where queue length is greatest. For a precise definition we need some notation. Recall from (2.3) the sets , and note that gives the set of shortest nonempty queues at time . For , let

Then gives the set of longest queues. Let be given by

| (3.26) |

Note that is nonnegative and vanishes on the set and only there.

Lemma 3.4

Given , and , there exist constants such that for every and every initial state that satisfies ,

| (3.27) |

Lemma 3.4 and the first item of Lemma 3.2 are similar, where the former is concerned with long time intervals as well as rates of convergence. However, the latter is not an immediate consequence of the former. We present their proofs together.

Proof of Lemma 3.4 and Lemma 3.2(i). For the proof of Lemma 3.4, fix , , and as in the statement of the lemma. Using the expression (2.7) for the generator of write the one for (see (2.10)), as

| (3.28) |

for bounded .

Recall that denotes a generic positive constant that does not depend on . We begin by showing that there exists a constant such that for all sufficiently large,

| (3.29) |

To this end, note that the first term on the RHS of (3.28), upon substituting for , equals

The inequality above is valid since for the -th term in the sum is zero, and for ,

The second term on the RHS of (3.28) (with ) can be expressed as

| (3.30) |

We argue that for ,

If for some then . Therefore, if then either or and contains more than one element. In both cases, for every there is , different from , such that both maxima above equal . This shows that the expression in (3.30) equals . Combining this with the bound on the first term, and recalling that is asymptotic to , and that the latter fractions sum to 1, shows (3.29).

We analyze the event under for such that . Recall that the jump sizes of are at the scale of ; as a result, the same is true for the process . Since , is at a larger scale than these jumps. Hence there exist random times such that -a.s. on ,

| (3.31) |

The process

| (3.32) |

is a local martingale. From (3.29) and (3.31), denoting , one has

| (3.33) |

Fix a constant and consider the events

Then . We argue separately for the two events.

The event . Let intervals be defined by for , where . On there must exist and an interval such that

where here and throughout, . As a result, . Therefore, using the Burkholder-Davis-Gundy (BDG) inequality [22, Theorem 48] and denoting by the quadratic variation of over an interval ,

| (3.34) |

where is any number in . The quadratic variation process has piecewise-constant samples paths with jumps taking values in the set . The number of its jumps in an interval is stochastically dominated by a Poisson RV with parameter . Since and scale like , is stochastically dominated by , where is a Poisson RV with parameter . Consequently,

Therefore the r.h.s. of (3.34) is bounded above by (where may depend on ). Taking gives the bound , provided that is sufficiently large.

The event . Clearly,

Using again the BDG inequality (with ) followed by a domination of the number of jumps in terms of a Poisson RV with parameter , and the sizes of the jumps by , gives

This completes the proof of Lemma 3.4.

In order to establish the proof of Lemma 3.2(i) we prove below the following stronger result that also serves us in the proof of Lemma 3.2(iii): for every satisfying , one has

| (3.35) |

This statement implies Lemma 3.2(i), since by the assumption on , there exists , such that ; without loss of generality we may assume that .

We next show how the details of the above proof are modified in order to prove (3.35). Fix an arbitrary that satisfies . We claim that

Unlike in (3.27), we consider here a fixed horizon , we do not provide a convergence rate, and the polynomial tube widths are replaced by .

Recall (3.28), (3.29), and (3.32). We analyze the event under . Since and the jump sizes of the process are at the scale of , there must exist random times such that -a.s. on ,

| (3.36) |

From (3.29) and (3.36), one has

| (3.37) |

Set and consider the events

Then . We argue separately for the two events.

The event . Let intervals be defined by

for . The same arguments given before with the choice of in BDG inequality lead to the following sequence of inequalities and the uniform limit over

| (3.38) | ||||

The event . Arguing as before, we obtain,

By our choice of the function , the last expression converges to as , uniformly for .

Proof of Lemma 3.2 (continued). First, the assertion regarding -tightness follows directly from Lemma 3.1(i) and Lemma 3.2(i).

ii. The statement of this part follows from part (i) with initial condition and strong Markovity.

iii. It is sufficient to show that for every satisfying , one has

| (3.39) |

We first show that for every such and every ,

Indeed, in order for the process , starting inside the -tube around axis , to exit the -tube around the same axis by time and reach away from the origin, it must either escape before or pass through a -neighborhood of the origin without hitting the origin and then move through a different tube and away from the origin. The probabilities of these two events converge to zero uniformly in the initial conditions; the first convergence follows by (3.35). The second event can be expressed in terms of an atypical behavior of , as a sequence of processes converging in law to an RBM.

3.4 The small ball exit measure

This section and the next are devoted to the proof of Proposition 3.3. By assumption, the parameters and scale like , as expressed in equation (2.8). The special case where, for all , and is referred to as the homogeneous case. Our strategy is to first prove the lemma in the homogeneous case, where the processes can all be expressed as scaled versions of a single process. This is the content of this section. In §3.5, the general case is considered, and by appealing to a change of measure argument, Proposition 3.3 is proved.

Lemma 3.5

The statement of Proposition 3.3 holds in the homogeneous case, with , for any .

Proof. Let mutually independent Poisson processes , be given, with intensities and , respectively. Since by assumption and , the tuple is equal in law, for each , to , and without loss of generality we may, and will, assume that and for all , and . Let now , , and be defined as the processes , , and respectively (that is, where one sets ). Then in particular, equations (2.1), (2.2) and (2.5) are satisfied by , , and , and is a Markov process on (see (2.6)).

Since for each we have the aforementioned relation between and , one can also express as certain path transformations of , for each . The most significant aspect of this in the proof is that the rescaled processes and can be written as rescaled versions of a single process. Denote . Then by (2.1), , whereas . Hence , and thus by (2.10),

| (3.40) |

The state space for the Markov process is given in the case under consideration as .

For , set

| (3.41) |

Clearly we have the identity (see (3.2)). Let be as in the statement of the lemma, that is, , and set . Denote

and , where

where (with the corresponding expectation ) stands for the law of with . Then

| (3.42) | ||||

Using the fact that the balls are disjoint for each and sufficiently large , (3.4) will follow once we show that

| (3.43) |

Note that Proposition 3.3 asserts, moreover, that does not depend on the choice of . To address this point, consider for which and, respectively , satisfy (3.43). Then the fact that the LHS of (3.42) is monotone decreasing in gives for all , and since and are members of , this shows that . Hence the proof will be complete once we show (3.43) for fixed .

To this end, note that it suffices to show that there exist and such that for every , , one has

| (3.44) |

and

| (3.45) |

Indeed, if and are both within then (3.44) gives . As a result, for arbitrary , denoting ,

This shows that, for fixed , any sequence is a Cauchy sequence as . Along with (3.45), we obtain that (3.43) holds.

In what follows, we prove (3.44) and (3.45). We let and , where is arbitrary, but fixed. Without loss of generality, the proof of (3.44) considers only .

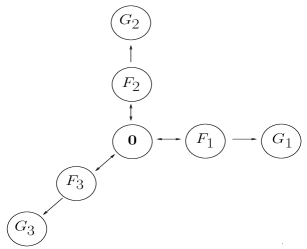

To help explain the main idea and motivate a couple of technical tools, we first consider a highly simplified model, illustrated in Figure 1. Consider a discrete time Markov process on a finite set that is star shaped. That is, consists of states, denoted by , , , . For each , communicates only with and . The state communicates only with the states , while are absorbing. Denoting transition probabilities by , we have , , , and , while all other transition probabilities are zero. For , let denote the probability to get absorbed at starting from . Then

From this one obtains

If the transition probabilities starting at depend weakly on , in the sense that for some one has for all , and if in addition for some constant , it follows that

where depends on but not on . The relevance to our problem is as follows. Roughly speaking, the states and represent the collections of states within and , respectively, and represents the origin. The calculation above suggests that if the probability of reaching before reaching starting anywhere in depends weakly on then the difference is small.

We now consider the process and the stopping times , and in addition let

We aim at showing there exist such that for every , one has

| (3.46) |

| (3.47) |

| (3.48) |

| (3.49) |

For estimate (3.46), note that it follows from the identity , the expression (2.7) for the generator of (with and substituted for and ), and condition (2.9), that the stopped process is a martingale. By this martingale property and the fact that lives on the grid , there is a constant such that

Estimate (3.46) follows, using the fact that .

For inequality (3.47), the relation gives . By Lemma 3.1, converges in law to an RBM , and so . Thus there exists such that for all sufficiently large, . For other initial conditions the probability of this event under is even smaller, and therefore is still bounded by . Markovity thus gives (3.47).

For estimate (3.48), fix to be a constant that satisfies (3.47). Recall the definition of from (3.26). Since takes values in , must take a value within , for some constant . We claim that if , and then . To this end, assume, without loss of generality, that . Since , we have . Therefore, if , we have that and hence . If on the other hand , then using , we obtain again .

As a result of the above claim, for all large ,

| (3.50) |

By (3.47), the first term above is bounded by . Since , we have by Lemma 3.4, relation (3.40), and the relation , that the second term is bounded by .

For estimate (3.49), define

Fix and consider . Denote . Then a use of Strong Markovity gives

| (3.51) |

To bound the first term consider the event . If then holds, whereas if , then by the argument provided in the previous paragraph we have . This implies that the first term in (3.51) is bounded by

This expression can be handled as the RHS of (3.50). Since , . Thus Lemma 3.4 is applicable with . This gives the bound on the first term on the RHS of (3.51).

To bound the second term in (3.51) we again use the martingale property of . It gives

Since , we obtain that for sufficiently large , the last term in (3.51) is bounded above by . This completes the proof of (3.46)–(3.49).

We now deduce (3.44) and (3.45) from (3.46)–(3.49). Identity (3.45) follows immediately from (3.48). For (see (2.6)) denote

and . Then

| (3.52) | ||||

It follows from (3.48) that . Next, consider the term . Let and . Then

The first term above is equal to . By (3.49), the second term bounded by . Combining this with (3.46),

where here and in the remainder of this proof, denotes a generic function of which staisfies for all large .

3.5 Relaxation of the homogeneity assumption

In this section we prove Proposition 3.3 based on Lemma 3.5, by means of a change of measure. Thus the general setting, where and satisfy the hypotheses of Theorem 2.1, is in force. Since the statement of Proposition 3.3 refers to , we may and will assume in this section that the initial condition is identically. Thus the only stochastic primitives in the model are the processes . In particular, as follows from equations (2.1), (2.2), (2.4), (2.5) and (2.10), the processes , and , are determined by , for . In addition to the measure , we introduce below a reference probability measure on under which, for all , the Poisson processes and have intensities and , respectively, where we denote and . Denote by the corresponding expectation. The laws of the driving Poisson processes as well as that of the queue length process under can then be obtained from those under by a change of measure (as shown below). However, this does not apply to the nominal workload process , for which the parameters and determine not only the jump intensities but also the scaling factors in the definition (2.1) of in terms of . This is reflected also in the formula for the generator (see (2.7)) where these parameters enter in both the jump rates and the jump sizes. An intermediate transformation is required.

To this end we define analogously to (2.1) and (2.10), a process and its scaled version by

Similarly, we let and .

The starting point of this section is to notice that Lemma 3.5, proved in the previous section, implies that there exists such that for ,

| (3.53) |

The proof proceeds in two steps. First, it is shown that a version of (3.53), that refers to in place of , is valid, and then that the same statement remains true under (equivalently, under ).

Proof of Proposition 3.3. We first prove that, for as in (3.53), there exists such that

| (3.54) |

Based on (3.53), the statement (3.54) is almost an immediate consequence of convergence of to an RBM under and the closeness of and . Indeed, the relation between and is where . We have by (2.8). Thus for , for all . Hence (3.54) will follow from (3.53) if we show that, as , in probability. Since are -tight by Lemma 3.2 and are dominated by , that form a tight sequence of RVs, it suffices to prove that

| (3.55) |

The convergence of to RBM implies that for any and ,

It follows that for any and ,

Using again the tightness of the RVs , (3.55) follows, hence also (3.54).

The second and final step is to prove that in (3.54), may be replaced by . Denote the events of interest by . Since , using the fact that for any and all sufficiently large , are disjoint, it suffices to prove for each the lower bound

| (3.56) |

Given any , we clearly have . Hence by (3.54), denoting , we have

| (3.57) |

A change of measure is formulated in terms of the exponential martingale

Let . Let also . For each and , let a probability measure on be defined by for . Then, for each and , the law of under is the same as that under . Moreover, note that for each , the event is measurable on . Hence to establish (3.56), it suffices to prove that for each ,

| (3.58) |

For , denote . Suppose we show that for any ,

| (3.59) |

Then we may argue as follows,

Taking then , then using (3.57), and finally taking , gives

Since is arbitrary, this gives (3.58) and consequently (3.56).

Thus the proof will be complete once (3.59) is shown. To this end, let

These processes, defined analogously to and , converge under to BMs. Denote and and recall by (2.8) that these sequences converge. Write in terms of and as

where , . Denoting and using for all , we have for all large ,

The aforementioned convergence to BM clearly implies that, for any ,

We thus obtain (3.59) and complete the proof.

4 Concluding remarks

-

1.

It is desirable to extend the main result of this paper beyond the Markovian setting, to general service time distributions and renewal arrival distributions, under second moment conditions. Whereas the behavior of the modulus according to an RBM certainly holds in vast generality, and the attraction to the collection of axes can likely be extended, the existence of limiting entrance laws appears to require different machinery. Indeed, the proof presented here makes crucial use of the strong Markovity of the prelimit processes.

-

2.

The proof presented in this paper sheds no light on the angular distribution (except that it does not depend on the second order parameters , ). A characterization of that would be useful and lead to further information about it is desirable.

-

3.

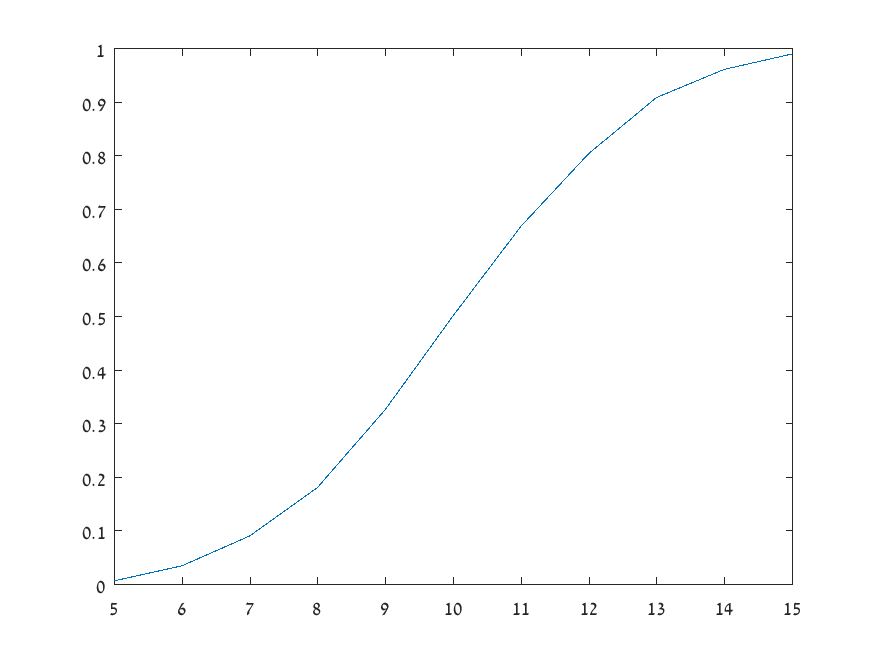

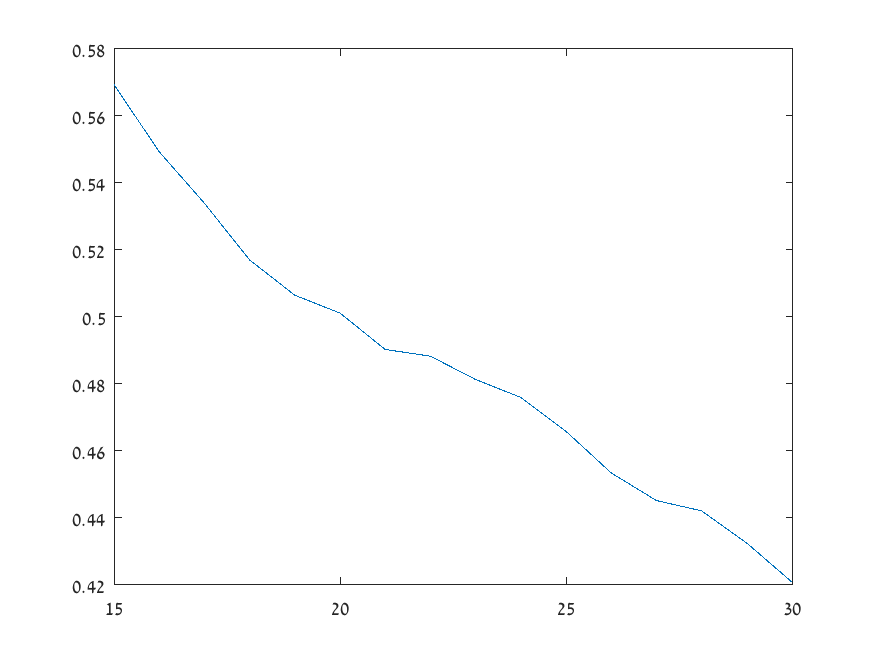

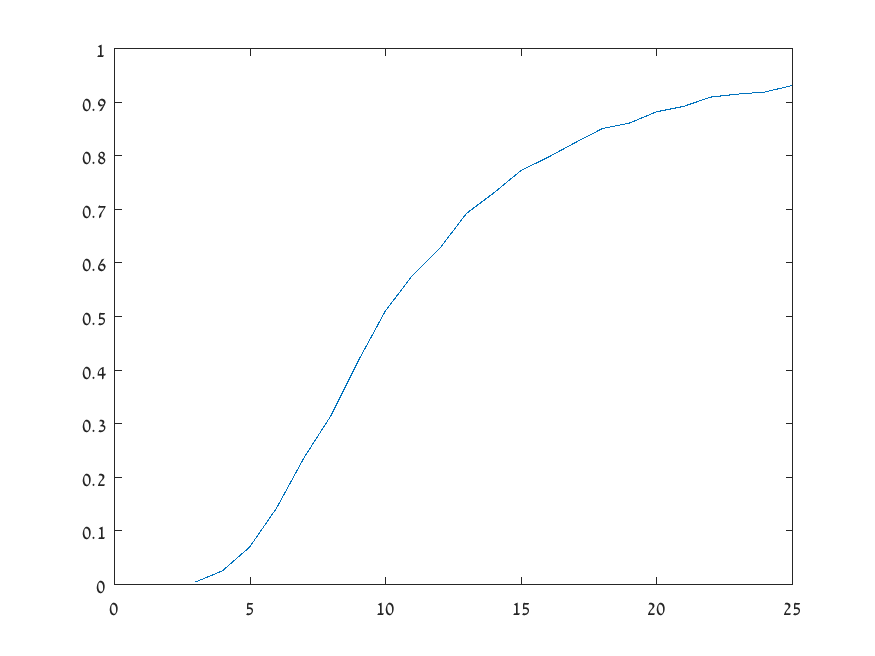

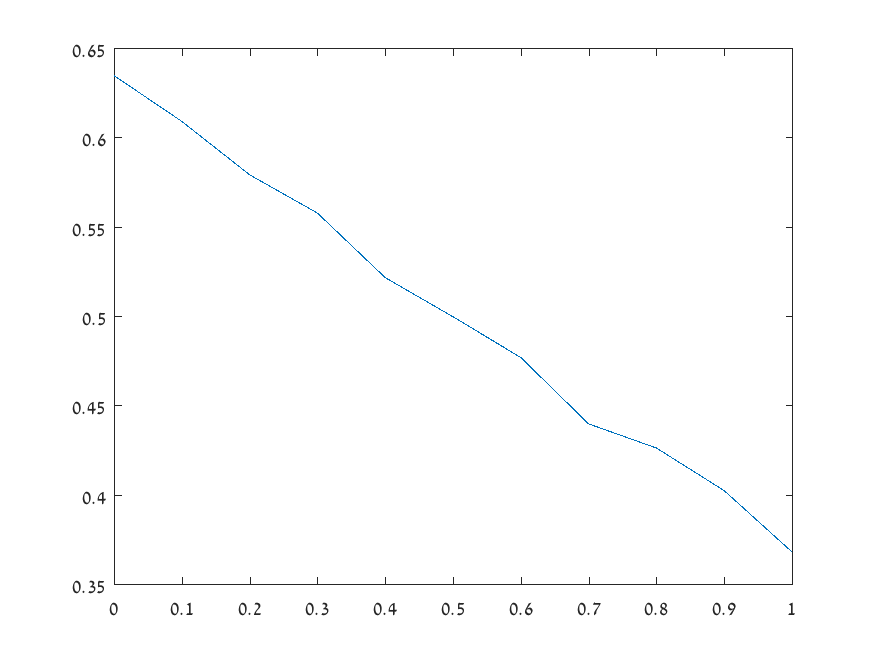

Figure 2 depicts results of Monte Carlo simulations for an SSQ model with at criticality, aimed at estimating . It shows the behavior of as several parameters vary. They all suggest monotone dependence, that one would wish to substantiate mathematically.

-

(a)

The graph shown at Figure 2(c) is, in particular, relevant to the heuristic mentioned in the introduction, according to which more variable traffic attains lower priority. In this example, the traffic intensities are kept fixed. As increases, the inter-arrival variance increases, which, according to the graph, increases , indicating lower priority for this class.

-

(b)

Figure 2(d) shows the dependence on the tie breaking parameter, . It exhibits that the tie breaking rule affects the limiting angular distribution. However, we have not aimed at providing a proof of this claim.

-

(a)

(a) (b)

(c) (d)

(a) as a function of , fixed ’s: , .

(b) as a function of , fixed ’s: , .

(c) as a function of , fixed ratio , and : , , .

(d) as a function of , fixed ’s and ’s: , , .

Acknowledgement. The authors are grateful to Ross Pinsky for useful discussions about heat equation estimates, to Bert Zwart for bringing reference [18] to their attention, and to the referee for careful reading and valuable comments.

References

- [1] M. Barlow, J. Pitman, and M. Yor. On Walsh’s Brownian motions. In Séminaire de Probabilités, XXIII, volume 1372 of Lecture Notes in Math., pages 275–293. Springer, Berlin, 1989.

- [2] J. R. Baxter and R. V. Chacon. The equivalence of diffusions on networks to Brownian motion. Contemp. Math, 26:33–47, 1984.

- [3] N. Benameur, F. Guillemin, and L. Muscariello. Latency reduction in home access gateways with shortest queue first. In Proc. ISOC Workshop on Reducing Internet Latency, 2013.

- [4] P. Billingsley. Convergence of Probability Measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition, 1999.

- [5] T. Bonald, L. Muscariello, and N. Ostallo. Self-prioritization of audio and video traffic. In IEEE International Conference on Communications (ICC), pages 1–6. IEEE, 2011.

- [6] G. Carofiglio and L. Muscariello. On the impact of TCP and per-flow scheduling on internet performance. In INFOCOM, 2010 Proceedings IEEE, pages 1–9. IEEE, 2010.

- [7] S. N. Ethier and T. G. Kurtz. Markov Processes. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons Inc., New York, 1986.

- [8] F. Guillemin and A. Simonian. Analysis of the shortest queue first service discipline with two classes. In Proceedings of the 7th International Conference on Performance Evaluation Methodologies and Tools, pages 1–10. ICST (Institute for Computer Sciences, Social-Informatics and Telecommunications Engineering), 2013.

- [9] F. Guillemin and A. Simonian. Stationary analysis of the shortest queue first service policy. Queueing Syst., 77(4):393–426, 2014.

- [10] F. Guillemin and A. Simonian. Stationary analysis of the “shortest queue first” service policy: the asymmetric case. Stoch. Models, 33(2):256–296, 2017.

- [11] H. Hajri. Discrete approximations to solution flows of Tanaka’s SDE related to Walsh Brownian motion. In Séminaire de Probabilités XLIV, volume 2046 of Lecture Notes in Math., pages 167–190. Springer, Heidelberg, 2012.

- [12] J. M. Harrison. Balanced fluid models of multiclass queueing networks: a heavy traffic conjecture. In Stochastic networks, volume 71 of IMA Vol. Math. Appl., pages 1–20. Springer, New York, 1995.

- [13] J. M. Harrison and L. A. Shepp. On skew Brownian motion. Ann. Probab., 9(2):309–313, 1981.

- [14] J. M. Harrison and R. J. Williams. A multiclass closed queueing network with unconventional heavy traffic behavior. Ann. Appl. Probab., 6(1):1–47, 1996.

- [15] Q. Hu, Y. Wang, and X. Yang. The hitting time density for a reflected Brownian motion. Computational Economics, 40(1):1–18, 2012.

- [16] T. Ichiba, I. Karatzas, V. Prokaj, and M. Yan. Stochastic integral equations for Walsh semimartingales. arXiv preprint arXiv:1505.02504, 2015.

- [17] L. Kruk. An open queueing network with asymptotically stable fluid model and unconventional heavy traffic behavior. Math. Oper. Res., 36(3):538–551, 2011.

- [18] A. Lambert and F. Simatos. The weak convergence of regenerative processes using some excursion path decompositions. Ann. Inst. H. Poincaré Probab. Statist., 50(2):492–511, 05 2014.

- [19] N. Nasser, B. Al-Manthari, and H. Hassanein. A performance comparison of class-based scheduling algorithms in future UMTS access. In Performance, Computing, and Communications Conference, 2005. IPCCC 2005. 24th IEEE International, pages 437–441. IEEE, 2005.

- [20] N. Ostallo. Service differentiation by means of packet scheduling. Master’s thesis, Institut Eurècom Sophia Antipolis, Biot, France, 2008.

- [21] E. Plambeck, S. Kumar, and J. M. Harrison. A multiclass queue in heavy traffic with throughput time constraints: asymptotically optimal dynamic controls. Queueing Syst., 39(1):23–54, 2001.

- [22] P. E. Protter. Stochastic Integration and Differential Equations, volume 21 of Applications of Mathematics (New York). Springer-Verlag, Berlin, second edition, 2004.

- [23] L. C. G. Rogers. Itô excursion theory via resolvents. Probability Theory and Related Fields, 63(2):237–255, 1983.

- [24] T. S. Salisbury. Construction of right processes from excursions. Probability theory and related fields, 73(3):351–367, 1986.

- [25] B. Tsirelson. Triple points: from non-Brownian filtrations to harmonic measures. Geom. Funct. Anal., 7(6):1096–1142, 1997.

- [26] N. Varopoulos. Long range estimates for markov chains. Bulletin des sciences mathématiques, 109(3):225–252, 1985.

- [27] J. B. Walsh. A diffusion with a discontinuous local time. Astérisque, 52(53):37–45, 1978.

- [28] W. Whitt. Weak convergence theorems for priority queues: Preemptive-resume discipline. J. Appl. Probability, 8:74–94, 1971.

- [29] R. J. Williams. On the approximation of queueing networks in heavy traffic. Stochastic Networks: Theory and Applications, (4):35–56, 1996.