Centralized Volatility Reduction for Electricity Markets

To appear in the International Journal of Electrical Power and Energy Systems

Abstract

Increased penetration of wind energy will make electricity market prices more volatile. As a result, market participants will bear increased financial risks, which impact investment decisions and in turn, makes it harder to achieve sustainable energy goals. As a remedy, in this paper, we propose an insurance market that complements any wholesale market design. Our mechanism can be run by any suitable financial entity such as an independent system operator, with the aim of reducing the financial impacts of volatile prices. We provide theoretical guarantees, analytically characterize the outcomes over a copperplate power system example, and numerically explore the same for a modified IEEE 14-bus test system.

1 Introduction

Wind energy is uncertain (difficult to forecast), intermittent (shows large ramps), and largely uncontrollable (output largely cannot be altered on command). It fundamentally differs from dispatchable generation that “can be controlled by the system operator and can be turned on and off based primarily on their economic attractiveness at every point in time” [1]. It has been a widely recognized fact that escalated penetration of wind will dampen electricity prices. Wind is a (near) zero marginal cost resource, and hence, alters the merit-order at the base of the stack. “Free” wind shifts the market supply curve to the right, leading to price reduction. Empirical evidence corroborates that hypothesis, such as the analyses by Ketterer in [2] for the German market, Munksgaard and Morthorst in [3] for the Danish market, de Miera et al. in [4] for the Spanish electricity market, among others. Green’s model-oriented analysis [5] for the British market resonates the same sentiments.

A perhaps less studied effect of large-scale wind integration is its contribution to price volatility. Dispatchable (and often marginal) generators need to compensate for variations in wind availability, leading to variations in energy prices. Data from various markets support that conclusion, such as the studies by Woo et al. in [6] for ERCOT, Martinez-Anido in [7] for New England, Jónsson et al. in [8] for the Danish market, and Ketterer in [2] for the German one.111Price variations differ considerably across a day; they are positively correlated with demand, as [5] concludes from the British market. They also exhibit seasonal variations; these variations are greater in the summer, as the Australian market analysis in [9] reveals. Gerasimova [10], studying the Nord pool (Finland, Sweden, Norway, Denmark), shows that intraday price variations in parts of Finland and Sweden – measured in terms of the expected difference in daily on-peak and off-peak prices – have roughly doubled during the period 2008-2016 from that in 2000-2007. Such trends are likely to persist and perhaps grow, given the rapid growth in wind penetration.

How can market participants hedge against financial risks from these price variations? Financial instruments, such as forwards, futures, swaps, and options, can help mitigate such risks; see [11, 12, 13, 14, 15, 16] for their use in electricity markets. In addition to hedging, options have been shown to mitigate the effects of market power in electricity markets [17, 18, 19]. The focus of the current paper is on the design of an insurance market that complements any wholesale market design. Our design is inspired by cash-settled call options that are bilateral financial instruments to hedge volatility.

In this paper, we propose a centralized market mechanism for insurance contracts, where a market maker facilitates the trade of insurance contracts by ‘matching’ buyers and sellers. Our market design is different from a traditional exchange such as the European Energy Exchange and the Chicago Board Options Exchange. Here, we allocate the collection of contracts bought among sellers with the goal to reduce the aggregate volatilities in the profits received by electricity market participants. Such a mechanism will aid electricity markets with high penetration of wind by allowing the market participants to mitigate their financial risks. The market we propose is an add-on to run in parallel with any electricity market design, and hence, does not advocate any alteration to existing dispatch and pricing of electricity markets. Our contribution complements the financial risk exchange between wind power producers proposed in [20], but it is more general in the sense that we allow any electricity market participant to buy or sell the contracts we study.

We propose our centralized insurance clearing mechanism in Section 2 that is run by a market maker. For our mechanism, we prove that the aggregate volatilities cannot increase, and the expected merchandising surplus remains zero even if the market maker is profit-motivated. Next, in Section 3, we present a dispatch and pricing model for a two-period electricity market that we apply our insurance market to, provide conditions to guarantee strict volatility reduction for market participants. Then, Section 4 analytically illustrates volatility reductions through a stylized copperplate power system example and demonstrates how our mechanism generalizes bilateral trading of call options. We conduct numerical experiments on the IEEE 14-bus test system [21] in Section 5 to further explain the properties of our mechanism. The paper concludes in Section 6. All proofs are included in the Appendix.

Notation

We let denote the set of real numbers, and (resp. ) denote the set of nonnegative (resp. positive) numbers. For , we let . For a random variable , we denote its expectation by , its variance by , and its cross-covariance with another random variable by ; note that . For an event , we denote its probability by for a suitably defined probability measure . The indicator function for an event is given by . In any optimization problem, a decision variable at optimality is denoted by .

2 Centralized clearing of insurance contracts

Consider a wholesale electricity market with multiple consumers and producers. The consumers are utility companies or retail aggregators who represent a collection of retail customers. In this model, we consider two types of producers – dispatchable generators and variable renewable wind power producers. Dispatchable generators can alter their power output within their capabilities on command, e.g., nuclear, coal, natural gas, biomass or hydro power based power plants. In contrast, the available production capacity of variable producers rely on an intermittent resource like wind energy. The SO implements a centralized market mechanism to balance demand and supply of power within the network constraints.

To motivate the design of our insurance market, consider a two-stage electricity market model. Identify as the forward stage, prior to the uncertainty being realized, and , the real-time stage. Let denote the probability space describing the uncertainty. Here, is the collection of possible scenarios at , is a suitable -algebra over , and is a probability distribution over . We assume that is compact, and that all market participants know .

An insurance contract in our context allows its buyer the right to claim a monetary reward equal to the positive difference between the real-time price and the strike price of an underlying commodity for an upfront fee. Adopting a game-theoretic framework, consider the case where player is the buyer and another player is the seller. The contract costs a fee of , where is the upfront price and is the quantity. Once they agree on the trade triple , their profits in scenario are respectively given by

| (1) |

In each expression, the first term is the profit from the electricity market, and the other two terms capture the aggregate return from the insurance contract. Such contracts allow market participants to reduce their profit volatilies, which are measured here in terms of their variances. That is, with a well-designed contract, one would expect for market participant .

Peaker power plants are not always asked to produce in real time, but they are critical for resource adequacy in wholesale markets [22]. The California Independent System Operator (CAISO) and the Midcontinent ISO (MISO) have proposed flexible ramping products and buy capacities from peaker power plants to provide them incentives to remain online. The above contracts can provide financial incentives for peaker power plants to stay in the market, without requiring the system operator to purchase such capacities. For example, a peaker power plant can participate as a seller, and receive profit of in the forward stage. On the other hand, wind power producers face the risks of not being able to produce much power in real time, and hence, they can become buyers and guarantee a reward in such events. This leads to incentives for both wind producers and peaker plants to engage in such trades.

Contracts of the form in (1) are often traded bilaterally between market participants in the form of cash-settled call options, but in a wholesale market with a collection of dispatchable generators and variable generators , one can conceive of bilateral trades. It is difficult to convene and settle a large number of bilateral trades on a regular basis. Financial exchanges provide an alternative that typically seek to maximize the surplus from trading (options and other financial derivatives) with a collection of market participants, without explicit consideration of aggregate volatilities. In this paper, we take an alternate view, and propose a centralized clearing mechanism for both buyers and sellers of insurance contracts with the goal to reduce profit volatilities in electricity markets. Such an approach leads to critical outcomes: it makes volatility reduction accessible to any market participant, does not alter dispatch and pricing of the wholesale market, and is therefore compatible with any existing electricity market design.

Consider a market maker who acts as an aggregate buyer for a collection of sellers , and acts as a seller for the buyers . The SO or a suitable financial institution can fulfill the role of such an intermediary. In this paper, we primarily focus on the case where is social (e.g., is the SO). We later discuss how the problem would change if is profit-motivated. We now describe the step-by-step procedure for clearing the insurance market by a social . Forward stage:

-

•

broadcasts a set of allowable trades , given by

to all market participants .

-

•

Each submits an acceptable (compact) set of trades, denoted by .222 can fix a parametric description of ’s, and market participants report their parameter choices.

-

•

correctly conjectures the real-time prices in each scenario . Also, knows the profit functions ’s of all market participants for each scenario . 333One can consider revenues instead of profits in the design of this market. If is the SO, then the revenues are known exactly, while the profits are only known approximately. We sidestep such nuances and focus on the profit-based market throughout. Let the merchandising surplus (sum of profits) for be denoted by in scenario . As an aggregate buyer and seller, it is given by

The market maker solves the following stochastic optimization problem to clear the insurance market.

(2) over for each , and the -measurable square-integrable maps for each . Here, denotes the market price faced by . We define the same for , accordingly.

The constraints in (2) dictate that the volume of insurance contracts bought equals the amount that is sold, all trades are acceptable to market participants, and real-time payments cashable in each scenario can be allocated to the sellers. Imposing ensures that the market maker maintains zero balance from insurance contracts, and purely facilitates the trade among the market participants, i.e., we adopt the viewpoint of a social . The objective is to reduce profit volatilities in aggregate among acceptable trades.

-

•

Buyer pays to .

-

•

pays to seller .

Real-time stage:

-

•

Scenario is realized, and the real-time electricity prices become known.

-

•

pays to buyer .

-

•

Seller pays to .

Our mechanism is guaranteed not to increase (and possibly decrease) the aggregate volatility of profits, i.e., problem (2) admits an optimal solution that satisfies

| (3) |

The above inequality follows from the properties of problem (2). The constraint set is compact and the objective function is continuous, and hence, Weierstrass Theorem (see [23]) guarantees the existence of an optimum. Note that ’s being zero is always a feasible choice at which (3) is met with an equality. Thus, at the optimal solution, aggregate volatility can only be lower than that at the feasible point with no trades.

We remark that electricity market-specific considerations can be incorporated in our design if is the SO. For example, the strike prices and fees for buying/selling our contracts can be deemed to be nodally uniform, i.e., they are required to satisfy and for all market participants at a particular bus in the power system.

2.1 How participant decides

Consider a seller who expects a profit in scenario . From the electricity and insurance market, she receives a payoff of

in scenario with the trade triple , if allocates . Having no control over , assume that conjectures the worst case outcome that minimizes her payoff, given by

Evidence from electricity markets suggests that participants are often risk averse, e.g., see [24, 11]. To illustrate how the acceptability sets can be defined for risk-averse players, assume that a market participant perceives risk via the conditional value at risk functional (see [25, 26]), and finds a trade triple acceptable, if

| (4) |

where and describe her profits from the energy market and the energy-cum-insurance market, respectively, in scenario . The CVaR risk measure is given by

for an -measurable map . Parameter encodes the extent of risk-aversion. If is the monetary loss in scenario with a smooth distribution, then equals the expected loss over the fraction of the scenarios that result in the highest losses.

If all market participants pick , it follows that

which is equivalent to the expected merchandising surplus being nonpositive (). The constraints in (2), however, impose , and hence it follows that

for each . Our insurance market design is not limited to the above description of risk-preferences. Market participants can freely choose the trades they find acceptable via ’s and ’s. We illustrate the effects of risk-aversion later in Section 4. Our mechanism is centralized with complete information, i.e., the market maker needs to know profit functions, risk-preferences, and correct price conjectures. While this might be challenging to implement in practice as is, our theoretical guarantees, stylized examples, and numerical experiments demonstrate that it can achieve significant volatility reductions, and hence, it may serve as an optimal benchmark that can be used to derive insightful policy recommendations for the development of new insurance markets.

2.2 Electricity markets with multiple ex-post stages

The proposed insurance market can run in parallel with wholesale electricity markets that have multiple ex-post stages. For example, consider an electricity market with a forward stage at (think day-ahead market), and multiple ex-post stages with (e.g., the multiple real-time markets). Here, is the collection of possible scenarios at ,

Denote the price for electricity faced by at by , where encodes a random trajectory of available renewable supply. The insurance market can proceed as described, where the price signal is computed as the average electricity price over periods as

The profit to each market participant in the objective of (2) becomes the total profit over periods. That is, for a market participant , denoting her profit from the electricity market at stage by , her total profit becomes

The insurance market is then defined with the parameters and for each .

2.3 When the market maker is a profit-maximizer

The insurance market mechanism in (2) assumes a social intermediary. Next, consider a selfish market maker who aims at maximizing its expected merchandising surplus, and solves

| (5) |

Although the market maker here is motivated to maximize profit, our next result says that a selfish intermediary does not make profits on the average! However, volatility reduction such as that in (3) remains challenging to derive when is a profit-maximizer.

Proposition 1.

If each player picks , then, at an optimal solution of (5).

3 Application: A Stylized Two-Stage Electricity Market Model

In this section, we apply our mechanism to a simple, yet illustrative electricity market model to demonstrate its properties.

3.1 Modeling the market participants

Consider a power network for which denotes the set of buses, and let denote the aggregate real-time demand in scenario at node . Let and denote the collection of dispatchable generators and variable renewable wind power producers, respectively. We denote the collection of generators at node by . We similarly define . We model their individual capabilities as follows. Let each dispatchable generator produce in scenario in real time. We model its ramping capability by letting where is a generator set point at the stage prior to the real-time stage, and is the ramping limit. Let the installed capacity of generator be , and hence . Its cost of production is given by the smooth convex increasing map . Each variable renewable wind power producer produces in scenario in real time. It has no ramping limitations, but its available production capacity is random, and we have That is, denotes the random available capacity of production, and denotes the installed capacity for . The cost of production for is generally linear [27] and hence, we consider it to be a smooth convex increasing map . We call a vector comprised of for each and for each a dispatch. The SO decides the dispatch decisions and the compensations of all market participants. We adopt the dispatch and pricing model described below, which serves as a caricature of real electricity markets [28, 29, 30, 31]. We also adopt the commonly used DC approximation of the power flow [32]. That is, if the supply vector is denoted by , and the demand vector is denoted by , then the injection , where is the injection polytope defined as

where is the shift factor matrix and denotes the vector of capacities of the transmission lines.

3.2 The dispatch and the pricing model

Assume that SO knows for each and for each , and we have the following two stages.444In practice, the cost functions are derived from supply offers.

3.2.1 The forward stage

The SO computes a forward dispatch against a point forecast of all uncertain parameters. In particular, the SO replaces the random available capacity by a certainty surrogate for each . A popular surrogate555See [31] for an alternate certainty surrogate. is given by . Denote the forward dispatch by , and . This dispatch is the solution of the following optimization problem, in which the system operator minimizes the aggregate cost of production needed to meet the demand, given the forecasts of all random variables, and subject to the network constraints.

| minimize | |||||

| subject to | |||||

The forward price at node is given by the optimal Lagrange multiplier of the energy balance constraint. Denoting this price by , generator is paid , while producer is paid . Aggregate consumer pays .

3.2.2 At real time

Scenario is realized. Denote the real-time dispatch by , and . This dispatch is the solution of the following optimization problem, in which the system operator minimizes the aggregate real-time cost of production, subject to supply-demand balance and generation and network constraints.

| minimize | |||||

| subject to | |||||

The real-time (or spot) price is again defined by the optimal Lagrange multiplier of the energy balance constraint, and is denoted by , for each . Note that computed at defines the generator set-points for each generator . Generator is paid , while producer is paid . The aggregate consumer pays . Demand forecasts in practice are typically quite accurate and hence, we assume for each for all . The payments in realtime correspond to balancing energy needs in real time; the forward stage compensates for the bulk energy transactions.

The total payments to each participant is the sum of her forward and real time payments. We denote the profits corresponding to these payments for each and for each in scenario . The above benchmark dispatch model generally defines a suboptimal forward dispatch in that the generator set-points are not optimized to minimize the expected aggregate costs of production [33]. Several authors have advocated a so-called stochastic economic dispatch model, wherein the forward set-points are optimized against the expected real-time cost of balancing (cf. [34, 35, 36, 37]). Our insurance market design can operate in parallel to such an electricity market, and this model only serves to illustrate the properties of our mechanism.

3.3 Strict volatility reduction for each participant

Our mechanism reduces volatility of market participants in aggregate, but it does not guarantee that each participant reduces her volatility. Here, we provide conditions under which strict reduction in volatility is guaranteed for each participant.

Proposition 2.

When the centralized insurance market mechanism in (2) is applied to the two-stage electricity market model, variance in profits of participant reduces if and only if , where

for each and .

Proposition 2 reveals that there is reduction in the volatility of a participant when the total profits in real time (from energy and insurance markets) are anti-correlated with the profits from the insurance market alone. It aligns with the intuition that variance will decrease when the insurance market supplements the profits from the energy market.

4 Copperplate Power System Example

We present here a stylized single-bus power system example (adopted from [33]) and illustrate how a bilateral trade can reduce the volatility in payments of market participants, and even mitigate the risks of financial losses for some.

Consider a power system with two dispatchable generators and a single variable renewable wind power producer serving a demand . In this example, , where is a base-load generator, is a peaker power plant, and is a wind power producer.

Let Therefore, and have unlimited generation capacities. does not have the flexibility to alter its output in real time from its forward set-point. In contrast, has no ramping limitations. For simplicity, let and have linear costs of production. has a true marginal cost , and offers a unit marginal cost. has a true unit marginal cost, and offers a higher cost , where , i.e., generators offer higher prices than their true costs, which is an observed phenomenon in electricity markets [38]. Encode the uncertainty in available wind in the set

and take to be the uniform distribution over . That is, available wind is uniform with mean and variance . Scenario defines an available wind capacity of . Further, assume that produces power at zero cost, and fixed demand .

This stylized example is a caricature of electricity markets with deepening penetration of variable renewable wind supply. Base-load generators, specifically nuclear power plants, have limited ramping capabilities. Natural gas based peakers can quickly ramp their power outputs. Utilizing them to balance variability can be costly. Finally, (aggregated) demand is largely inflexible but predictable. In the remainder of this section, we analyze the effect of a bilateral contract on the market outcomes for this example.

The benchmark dispatch model yields the following forward and real-time dispatch decisions , , and the forward and real-time prices , respectively. See [33] for the calculations.

The above dispatch and the prices yield the following profits for market participants in scenario :

A keen reader would recognize that the payment to market participants from our mechanism in (2) shares parallels to that from cash-settled call options. Through the copperplate power system example, we illustrate that our market mechanism is indeed a generalization of a bilateral call option trade between and . In fact, we show that our centralized mechanism is able to achieve the maximum aggregate volatility reduction among all possible bilateral call option trades between and .

4.1 Bilateral insurance contract between and

We model a bilateral contract between and as a robust Stackelberg game (see [39]) as follows. Right after the day ahead market is settled at , announces a premium and a strike price . Then, responds by purchasing . Note that we impose an upper bound equivalent to the maximum possible shortfall, which allows for ease of exposition. We say constitutes a Stackelberg equilibrium, if

where is the best response of . Given , the best response satisfies

This two-player Stackelberg game has one leader and one follower, where the leader acts first and then the follower responds. chooses , anticipating the best response by to the prices offered by . Note that the response function might not be unique, and in this case, might consider the worst-case scenario , and hence, it is a robust Stackelberg game [39]. We have the following result.

Proposition 3.

The Stackelberg equilibria of are given by and that satisfy one of the following two conditions:

-

(i)

, and ,

-

(ii)

, and .

Over all equilibria with ,

The first kind of equilibria describes the degenerate case, where . and engage in trading at the second kind of equilibria, where . For , note that the bilateral trade always guarantees volatility reduction for the wind producer . For , reductions are only guaranteed for the equilibria that satisfy . Furthermore, in expectation, profits are unchanged. Similar conclusions can be drawn for any . This stylized example illustrates how insurance contracts can help with volatility reductions, but also shows that further improvements can be attained, which can be done by applying our centralized mechanism, which yields the largest volatility reductions.

4.2 Outcomes of the centralized mechanism

Consider an insurance market with buyer and seller and intermediary . Let the price cap be given by the maximum real-time price , and the trade volume be capped at , the maximum energy shortfall in available wind from its forward contract. Said otherwise, restricts trade triples to the set .

Letting , the set of acceptable trades for and are given by

| (6) | ||||

From the above sets, it is straightforward to infer the feasible set of the insurance contracts in (2), given by that satisfies

The above trades coincide with the set of all (non-degenerate) Stackelberg equilibria of the bilateral trade between and in Proposition 3. Given the objective of the central clearing problem (2), we conclude that the trade mediated by the market maker finds an equilibrium with the highest aggregate variance reduction. We characterize that reduction in the following result.

Proposition 4.

The optimal solutions of (2) for the copperplate power system example are given by , where

Moreover, we have

| (7) |

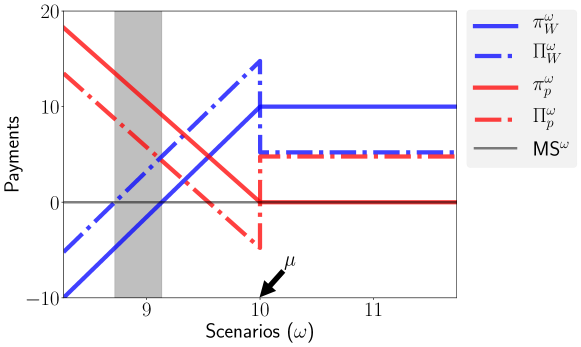

Proposition 4 (specifically (7)) reveals that aggregate volatilities of and strictly decrease as a result of the centralized insurance market. Contrast this result to that in Proposition 3, strict volatility reduction was only attained for . Propositions 3 and 4 reveal that the centralized mechanism picks the subset of Stackelberg equilibria that attain the largest aggregate volatility reduction, while preserving the same expected profits for and . Larger implies higher wind uncertainty, leading to largeer variance reduction via our centralized mechanism. We plot the profits of and across the scenarios with the parameters in Figure 1. Besides decreasing each player’s volatility (at no cost to the intermediary), the diagram reveals how is less exposed to negative profits than without the insurance contract. On the other hand, is now exposed to negative profits in some scenarios. We will show later in the paper that if is more risk-averse, she hedges against such losses by requiring higher premium in the forward stage.

4.2.1 The effect of risk-aversion

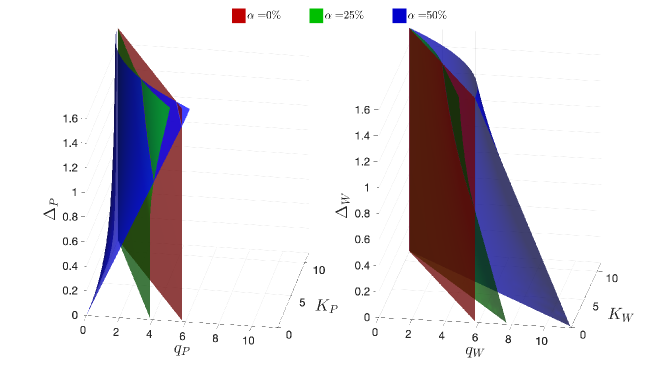

By varying the risk-aversion parameter, we plot the boundaries of and – the sets of acceptable trades for the wind power producer and the peaker power plant in our copperplate power system example, respectively – for various values of in Figure 2.666The current diagram stands as a correction to [41, Figure 2]. Acceptable trades at each for lie to the left of the corresponding surface. For , they lie to the right of it. When , linearity of expectation allows one to deduce that the acceptability of a trade is independent of . This no longer holds when , which is intuitive, as more risk-averse players do not prefer a large . As grows, requires higher forward premium for a given volume . Similar conclusions hold for . She becomes less willing to accept trades with a higher forward premium, the more risk-averse she gets.

5 Numerical Experiments on the IEEE 14-bus test system

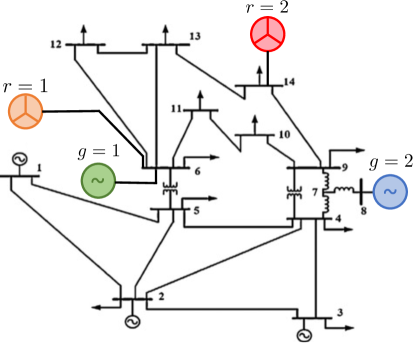

We now explore the outcomes from the electricity and insurance markets on a modified IEEE 14-bus test system shown in Figure 3. Relevant data is adopted from MATPOWER [42]. All transmission lines are assumed to have a capacity of MW, except that between buses 1 and 2 ( MW) and another one between buses 2 and 4 ( MW). 777The line capacity constraints are added to vary the real-time prices between different buses, which makes the simulation more realistic. Two wind power producers are added to the network at buses 6 and 14. We encode the uncertainty in available wind in MW and take to be a uniform distribution, i.e., the mean MW. We assume zero production costs for the wind generators. We have the following marginal costs, reflecting offers by producers

| (8) |

We further assume that the true marginal production costs for each generator is 20 $/MWh.888 We can also assume that the true cost is (8), which implies truthful bidding. However, in reality, power plants were observed to bid higher costs [38]. Nevertheless, if true costs are considered, our mechanism remains applicable, as our stylized examples in [41] suggest. Furthermore, we have three real-time prices of interest (one for each bus at which there is a buyer/seller), , and . Each seller/buyer preferences and insurance contract payments are related only to her corresponding bus’s day-ahead and real-time prices. Consider an insurance market with the wind power producers at buses and as buyers, and the dispatchable generators at buses and as sellers. The sellers are generators with higher production costs compared to others in the power system. To deal with uncertainty, we discretize the set and consider a finite set of scenarios in MWs.

5.1 Clearing Procedure and Solution Method

With our stylized two-stage electricity market described in Section 3, we have the following profits for each scenario :

where denotes the day-ahead price, is the day-ahead dispatch for participant , and is the real-time dispatch. Recalling the structure of the profit functions after participating in the centralized mechanism, we have:

Equipped with the electricity market outcomes for each from MATPOWER, and adopting with risk-aversion parameters ’s for all participants, the social market maker solves

| subject to | |||

The decision variables are for each market participant , and for each scenario . The centralized clearing problem is non-smooth and non-convex. We tackle non-smooth functions through smooth surrogates. Precisely, we replace and by and , respectively, with a large . These smooth surrogates slightly relax the problem but they allow us to utilize powerful numerical optimization techniques. Non-convexity makes it challenging to claim convergence of optimization techniques to a global optimum. As evident in the sequel, our simulations demonstrate that solving it using sequential least-squares quadratic programming (SLSQP) returns meaningful results. This is not surprising, given that SLSQP is widely known to work well in practice in solving nonlinear constrained optimization problems [43]. The market clearing procedure is implemented as a Jupyter notebook at [44] that utilizes the SLSQP implementation outlined in [45]. In our experiments, we use the following values for the set of allowable trades described in Section 2:

For the social market maker , if for each participant , then, in view of the constraint , the constraint can be replaced with for each . Instead, if is profit-maximizing, he would solve the following problem (over the same decision variables).

| subject to | |||

5.2 Experimental Results

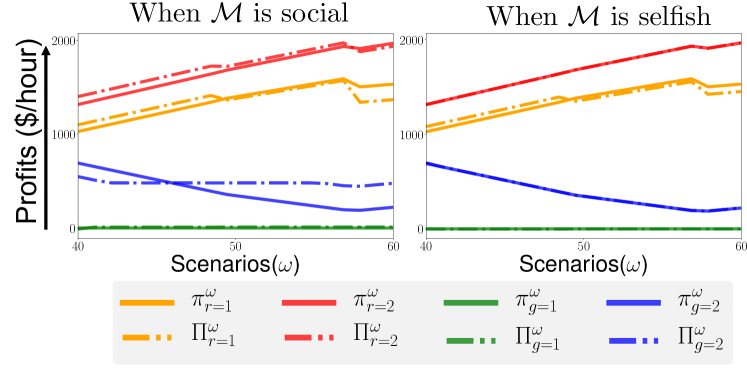

Figure 4 plots the profits of the market participants with and without the insurance market. With both social and profit-maximizing , seller at bus 6 is never dispatched, and hence, receives no profit in the electricity market. Thus, the variance of his profit is zero; it is also kept almost zero after the insurance contract. On the contrary, the insurance market reduces the variance for seller drastically (he receives almost the same profit for all scenarios). When is a profit-maximizer, there are no guarantees on volatility reduction. Although the market maker here is motivated by maximization of profit, our result in Proposition 1 showed that a selfish intermediary does not make profits on the average. For the remainder of this section, we focus on the interesting case for which is social and report the corresponding optimal numerical insurance values in Table 1. We also report the results when players are risk-averse with . When participants are more risk-averse, the quantities cleared are less. For example, does not buy insurance contracts when . For ’s, we report a sample of the numerical values because of the large number of scenarios.999For some , instead of , due to the smooth approximation of the indicator function. Our results remain largely unaffected as other non-relaxed constraints preserve participants’ preferences and consistency. A key feature of our mechanism compared to bilateral contracts is that insurance quantity bought by buyer can be matched with multiple sellers through the real-time variables ’s via the market maker’s clearing procedure.

| Participant | ||||||

|---|---|---|---|---|---|---|

| 0 | 0 | 0 | 0.5 | 0.5 | 0.5 | |

| 21.96 | 7.88 | 10 | 23.52 | 7.8 | 0 | |

| 17.86 | 16.13 | 10 | 0 | 20.23 | 10 | |

| 0.28 | 36.36 | 10 | 6.78 | 3.64 | 0 | |

| 28.68 | 0 | 10 | 21.73 | 0 | 10 |

| 40 | 45 | 50 | 55 | 60 | 40 | 45 | 50 | 55 | 60 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 0 | 0 | 0 | 0.5 | 0.5 | 0.5 | 0.5 | 0.5 | |

| 10 | 0.22 | 0.22 | 3.6 | 3.6 | 0 | 0 | 0 | 0 | 0 | |

| 10 | 7.94 | 4.2 | 1.5 | 0 | 10 | 7.5 | 4 | 0 | 0 |

5.3 On Complementing Existing Financial Instruments

Recall that in our mechanism, profit for market participant is not limited to the profit from the electricity market alone, but in fact, can represent the payoff from the electricity market in addition to other traditional financial instruments. Next, we demonstrate that our centralized mechanism naturally complements such instruments, leading to significant further volatility reductions while being consistent with participants’ preferences. With a slight abuse of notation, assume that buyer is also a buyer in the bilateral contract described by . Then, he receives a total profit of

Similarly, we can define . Next, consider the case when there is an existing bilateral cash-settled call option (or insurance contract) between the wind power producer at bus 6 and peaker power plant at bus 7. For illustration, we use the optimal values found for the case when there was no bilateral contract, and assume following bilateral contract values:

Note that when , the bilateral contract has no effect on the payoffs and we only have the effects of the centralized mechanism’s outcomes. In Table 2, we report the percentage change in terms of payoff variances for different values of for all market participants. Our mechanism complements bilaterally traded call options, leading to further volatility reductions. Also, the bilateral contract did not affect other market participants.

| Participant | ||||

|---|---|---|---|---|

| -47.7% | -50.3% | -56.1% | -68% | |

| -28.5% | -28.5% | -28.5% | -28.5% | |

| 0% | 0% | 0% | 0% | |

| -98.5% | -99% | -99.7% | -100% |

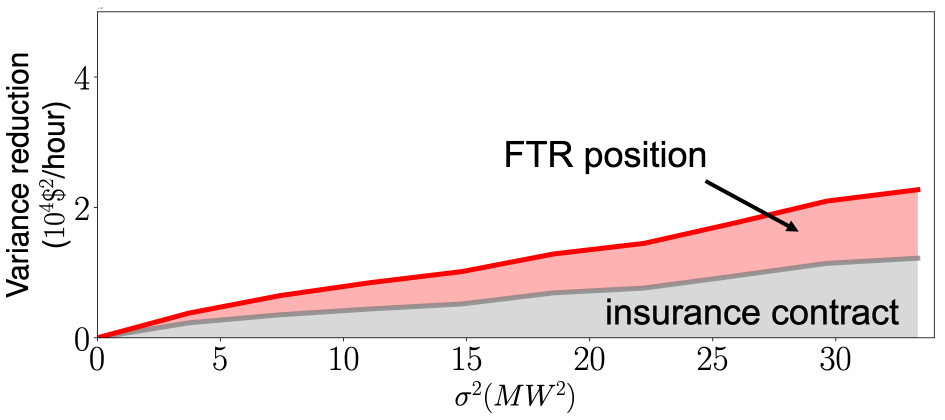

Finally, we also remark that our mechanism does not have any conflicts with other kinds of price variations. For example, a market participant might also hedge against spatial price variations using instruments such as financial transmission rights (FTRs) [46]. Holding FTRs between buses and entitles a market participant to receive a payment of

in scenario . Thus, an insurance buyer located at bus holding an between buses and receives a total profit of

Figure 5 illustrates how can reduce its volatility by holding MW worth of FTR’s between buses and , in addition to the reduction it attains from the insurance contract.

6 Concluding remarks

Price volatility in electricity markets is an inevitable consequence of integrating large scale wind energy. In this paper, we have proposed a centralized market for insurance contracts for market participants to tackle the attending financial risks. The centralized mechanism (mediated by a market maker) generalizes bilateral trading of such contracts. On a stylized copperplate power system example, this market provably reduces the profit volatilities of market participants. Numerical experiments on an IEEE 14-bus test system also appear encouraging. For adoption in practice, one needs to estimate the trade volume with real market data from regions with high wind penetration (e.g., Germany, Texas, Denmark). Also, operating such an insurance market in conjunction with current electricity markets will require a carefully designed legal and regulatory framework. Further, our centralized mechanism remains purely financial, but it might motivate market participants to alter their offers/bids in forward electricity markets, such as the day-ahead market. This might change real dispatch schedules, and it would be interesting to formally analyze such effects, which we leave as future research.

References

- [1] P. L. Joskow, “Comparing the costs of intermittent and dispatchable electricity generating technologies,” American Economic Review, vol. 101, no. 3, pp. 238–41, 2011.

- [2] J. C. Ketterer, “The impact of wind power generation on the electricity price in germany,” Energy Economics, vol. 44, pp. 270–280, 2014.

- [3] J. Munksgaard and P. E. Morthorst, “Wind power in the danish liberalised power market– Policy measures, price impact and investor incentives,” Energy Policy, vol. 36, no. 10, pp. 3940–3947, 2008.

- [4] G. S. de Miera, P. del Río González, and I. Vizcaíno, “Analysing the impact of renewable electricity support schemes on power prices: The case of wind electricity in spain,” Energy Policy, vol. 36, no. 9, pp. 3345–3359, 2008.

- [5] R. Green and N. Vasilakos, “Market behaviour with large amounts of intermittent generation,” Energy Policy, vol. 38, no. 7, pp. 3211–3220, 2010.

- [6] C.-K. Woo, I. Horowitz, J. Moore, and A. Pacheco, “The impact of wind generation on the electricity spot-market price level and variance: The texas experience,” Energy Policy, vol. 39, no. 7, pp. 3939–3944, 2011.

- [7] C. B. Martinez-Anido, G. Brinkman, and B.-M. Hodge, “The impact of wind power on electricity prices,” Renewable Energy, vol. 94, pp. 474–487, 2016.

- [8] T. Jónsson, P. Pinson, and H. Madsen, “On the market impact of wind energy forecasts,” Energy Economics, vol. 32, no. 2, pp. 313–320, 2010.

- [9] H. Higgs, G. Lien, and A. C. Worthington, “Australian evidence on the role of interregional flows, production capacity, and generation mix in wholesale electricity prices and price volatility,” Economic Analysis and Policy, vol. 48, pp. 172–181, 2015.

- [10] K. Gerasimova, “Electricity price volatility: its evolution and drivers,” Master’s thesis, Aalto University School of Business, 2017.

- [11] S. Deng and S. S. Oren, “Electricity derivatives and risk management,” Energy, vol. 31, 2006.

- [12] R. M. Kovacevic and G. C. Pflug, “Electricity swing option pricing by stochastic bilevel optimization: a survey and new approaches,” European J. of Operational Research, 2014.

- [13] T. Kluge, “Pricing swing options and other electricity derivatives,” Ph.D. dissertation, University of Oxford, 2006.

- [14] D. R. Biggar and M. R. Hesamzadeh, The Economics of Electricity Markets. Wiley-IEEE Press, 2014.

- [15] H.-P. Chao and R. Wilson, “Resource adequacy and market power mitigation via option contracts,” EPRI, Tech. Rep., 2004.

- [16] N. Aguiar, V. Gupta, and P. P. Khargonekar, “A real options market-based approach to increase penetration of renewables,” IEEE Transactions on Smart Grid, vol. 11, no. 2, pp. 1691–1701, 2019.

- [17] B. Allaz and J.-L. Vila, “Cournot competition, forward markets and efficiency,” Journal of Economic Theory, vol. 59, no. 1, pp. 1–16, 1993.

- [18] E. J. Anderson and H. Xu, “Optimal supply functions in electricity markets with option contracts and non-smooth costs,” Mathematical Methods of Operations Research, vol. 63, no. 3, pp. 387–441, 2006.

- [19] P. Holmberg and B. Willems, “Relaxing competition through speculation: Committing to a negative supply slope,” Journal of Economic Theory, vol. 159, pp. 236–266, 2015.

- [20] H. Shin and R. Baldick, “Mitigating market risk for wind power providers via financial risk exchange,” Energy Economics, vol. 71, pp. 344–358, 2018.

- [21] Power systems test case archive. [Online]. Available: https://www2.ee.washington.edu/research

- [22] Q. Wang and B.-M. Hodge, “Enhancing power system operational flexibility with flexible ramping products: A review,” IEEE Trans. Industrial Informatics, vol. 13, no. 4, pp. 1652–1664, August 2017.

- [23] D. G. Luenberger, Optimization by Vector Space Methods. John Wiley and Sons, Inc, 1969.

- [24] R. Bjorgan, C.-C. Liu, and J. Lawarree, “Financial risk management in a competitive electricity market,” IEEE Trans. Power Systems, vol. 14, no. 4, pp. 1285–1291, 1999.

- [25] R. T. Rockafellar and S. Uryasev, “Conditional value-at-risk for general loss distributions,” Journal of Banking & Finance, vol. 26, no. 7, pp. 1443–1471, 2002.

- [26] H. Föllmer and A. Schied, “Convex and coherent risk measures,” Encyclopedia of Quantitative Finance, pp. 1200–1204, 2010.

- [27] A. K. Zadeh, M. Abdel-Akher, M. Wang, and T. Senjyu, “Optimized day-ahead hydrothermal wind energy systems scheduling using parallel PSO,” International Conference on Renewable Energy Research and Applications (ICRERA), 2012.

- [28] S. Stoft, Power System Economics: Designing Markets for Electricity. Wiley-IEEE Press, 2002.

- [29] D. S. Kirschen and G. Strbac, Fundamentals of Power System Economics. Wiley, 2004.

- [30] J. M. Morales, M. Zugno, S. Pineda, and P. Pinson, “Electricity market clearing with improved scheduling of stochastic production,,” European J. of Operational Research, vol. 235, no. 3, pp. 765–774, 2014.

- [31] J. M. Morales, A. J. Conejo, K. Liu, and J. Zhong, “Pricing electricity in pools with wind producers,” IEEE Trans. Power Systems, vol. 27, no. 3, pp. 1366–1376, 2012.

- [32] J. J. Grainger and W. D. Stevenson, Power System Analysis. New York McGraw-Hill, 1994.

- [33] S. Bose, “On the design of wholesale electricity markets under uncertainty,” Proc. Fifty-third Annual Allerton Conference on Communication, Control, and Computing, Allerton House, UIUC, Illinois, USA, 2015.

- [34] S. Wong and J. D. Fuller, “Pricing energy and reserves using stochastic optimization in an alternative electricity market,” IEEE Trans. Power Systems, vol. 22, no. 2, pp. 631–638, 2007.

- [35] G. Pritchard, G. Zakeri, and A. Philpott, “A single-settlement, energy-only electric power market for unpredictable and intermittent participants,” Operations Research, vol. 58, pp. 1210–1219, April 2010.

- [36] F. Bouffard, F. D. Galiana, and A. J. Conejo, “Market-clearing with stochastic security-part I: formulation,” IEEE Trans. Power Systems, vol. 20, no. 4, pp. 1818–1826, 2005.

- [37] ——, “Market-clearing with stochastic security-part II: case studies,” IEEE Trans. Power Systems, vol. 20, no. 4, pp. 1827–1835, 2005.

- [38] R. J. Green and D. M. Newbery, “Competition in the british electricity spot market,” Journal of Political Economy, vol. 100, no. 5, pp. 929–953, 1992.

- [39] T. Başar and G. J. Olsder, Dynamic Noncooperative Game Theory. SIAM, 1999.

- [40] L. J. Hong and G. Liu, “Monte Carlo estimation of value-at-risk, conditional value-at-risk and their sensitivities,” Proc. of the 2011 Winter Simulation Conference, 2011.

- [41] K. Alshehri, S. Bose, and T. Başar, “Cash-settled options for wholesale electricity markets,” Proc. 20th IFAC World Congress (IFAC WC 2017), Toulouse, France, pp. 14 147–14 153, 2017.

- [42] R. D. Zimmerman, C. E. Murillo-Sánchez, and R. J. Thomas, “Matpower: Steady-state operations, planning and analysis tools for power systems research and education,” IEEE Trans. Power Systems, vol. 26, no. 1, pp. 12–19, Feb. 2011.

- [43] P. T. Boggs and J. W. Tolle, “Sequential quadratic programming for large-scale nonlinear optimization,” Journal of Computational and Applied Mathematics, vol. 124, 2000.

- [44] K. Alshehri, “Centralized options respiratory,” GitHub repository. [Online]. Available: https://github.com/kalsheh2/CentralizedOptions

- [45] D. Kraft, “A software package for sequential quadratic programming.” Tech. Rep. DFVLR-FB 88-28, DLR German Aerospace Center – Institute for Flight Mechanics, Koln, Germany., 1988.

- [46] J. Rosellón and T. Kristiansen, Financial Transmission Rights. Springer, 2013.

Appendix A Proofs

Proof of Proposition 1

The definitions of and yield

for each and . Summing the above inequalities over all and yields . Furthermore, is achieved at a feasible point with all ’s being identically zero. This completes the proof.

Proof of Proposition 2

Define . Then, for each , we have

The argument for is similar and omitted for brevity.

Proof of Proposition 3

Let choose . Then, ’s payoff from the insurance contract alone is given by which, upon utilizing (1), yields

We now describe ’s best response to ’s action.

-

•

If , then responds by playing .

-

•

If , then is agnostic to in .

-

•

If , then chooses .

Define as the payoff of from the insurance contract. Then, the relation in (1) yields

| (9) |

Given ’s choices, we have the following cases.

-

•

If , then . Therefore, will avoid playing such a .

-

•

If , then , and is agnostic to ’s choice of in .

-

•

If , then responds with . And, receives zero income from the contract.

Combining them yields the equilibria of . Now, the difference in variances for with and without insurance is equal to

| (10) |

When , we have

Utilizing and from the above relation in (10), we conclude

| (11) |

The last expression is nonpositive because . For , we have and . Therefore, similarly, we get

| (12) |

Proof of Proposition 4

The feasible set of (2) for the copperplate power system example coincides with the set of nontrivial equilibria of the bilateral trade. We conclude from (11)-(12) in the proof of Proposition 3 that (2) amounts to solving

| minimize | (13) | |||||

| subject to | ||||||

Substituting for , the objective function of the above problem simplifies to . Being convex quadratic in , it is minimized at for each . Split the analysis into two cases:

-

•

Case : Then, , and the objective function of (13) simplifies to . That function is minimized at , taking the value .

-

•

Case : Then, we have for each , for which the objective function of (13) further simplifies to a constant .

Combining the above two cases and computing the variance reduction at the outcome yields the stated result.