Efficient Pricing of Barrier Options on High Volatility Assets using Subset Simulation111The authors would like to thank Siu-Kui (Ivan) Au, James Beck, Damiano Brigo, Gianluca Fusai, Steven Kou, Ioannis Kyriakou, Zili Zhu, and the participants at Caltech, University of Liverpool, and Monash University seminars for helpful comments. Any remaining errors are ours.

Abstract

Barrier options are one of the most widely traded exotic options on stock exchanges. In this paper, we develop a new stochastic simulation method for pricing barrier options and estimating the corresponding execution probabilities. We show that the proposed method always outperforms the standard Monte Carlo approach and becomes substantially more efficient when the underlying asset has high volatility, while it performs better than multilevel Monte Carlo for special cases of barrier options and underlying assets. These theoretical findings are confirmed by numerous simulation results.

JEL classification: G13, C15

Keywords:

Simulation; Barrier Options Pricing; Path–Dependent Derivatives; Monte Carlo; Discretely Monitored

1 Introduction

A barrier option is among the most actively-traded path–dependent financial derivatives whose payoff depends on whether the underlying asset has reached or exceeded a predetermined price during the option’s contract term (Hull, 2009; Dadachanji, 2015). A barrier option is typically classified as either knock -in or -out depending on whether it is activated or expires worthless when the price of the underlying asset crosses a certain level (the barrier) (Derman and Kani, 1996, 1997; Guardasoni and Sanfelici, 2016). Then, the payoff at maturity is identical to that of a plain–vanilla European option, in case the price of the underlying asset has remained above the barrier (for a knock-out barrier option) or zero otherwise. Barrier options tend to be cheaper than the corresponding plain vanilla ones because they expire more easily and are less likely to be executed (Jewitt, 2015). It was estimated that they accounted for approximately half the volume of all traded exotic options (Luenberger and Luenberger, 1999). Despite the 2007–08 credit crunch and the subsequent drop in the demand for path–dependent instruments, barrier options can still be a useful investment or hedging vehicle when the structure and the risks of the product are comprehensible.

In the financial industry, barrier options can be traded for a number of reasons, using mostly foreign exchanges, commodities and interest rates as the underlying asset(s). First, barrier options more accurately represent investor’s beliefs than the corresponding plain–vanilla options, as a down-and-out barrier call option can serve the same purpose as a plain–vanilla option but at a lower cost, given one has a strong indication that the price of the underlying asset will increase. Second, barrier options offer a more attractive risk–reward relation than plain–vanilla options, and their advantage stems from their lower price that reflects the additional risk that the spot price might never reach (knock–in) or cross (knock–out) the barrier throughout its life (further discussion about ins and outs of barriers options can be found in Derman and Kani, 1996, 1997). In specific, barrier options on high volatility underlying assets can be used in a similar way as cheap deep out–of–the–money options, serving as a hedge to provide insurance in a financial turmoil, given their volatility–dependence (Carr and Chou, 2002). Hence, the development of a framework able to deal efficiently with barrier options on high volatility underlying assets tackles an actual problem in computational finance, which to our knowledge has not been explicitly studied in past. According to Andersen et al. (2001), the mean annualized volatility of the thirty stocks in the Dow Jones Industrial Average (DJIA) is approximately equal to 28% (ranging between 22% and 42%) while it is not uncommon to record stocks with volatility levels between 33% and 40%.

Therefore, the pricing of barrier options is a challenging problem due to the need to monitor the price of the underlying asset and compare it against the barriers at multiple discrete points during the contract life (Kou, 2007). In fact, barrier options pricing provides particular challenges to practitioners in all areas of the financial industry, and across all asset classes. Particularly, the Foreign Exchange options industry has always shown great innovation in this class of products and has committed enormous resources to studying them (Dadachanji, 2015). However, pricing discretely monitored barrier options is not a trivial task as in essence we have to solve a multi–dimensional integral of normal distribution functionals, where the dimension of the integral is defined by the number of discrete monitoring points (Fusai and Recchioni, 2007).

Computationally, certain barrier options such as down-and-out options, can be priced via the standard Black–Scholes–Merton (BSM) (Merton, 1973)’s paper. This idea can be further extended to more complicated barrier options which can be priced using replicating portfolios of vanilla options in a BSM framework (Carr and Chou, 2002). All these approaches, however, suffer from the BSM model’s dependence on a number of assumptionswhich are not met in real–world trading (Hull, 2009). As a result, the estimates we obtain for option’s price under the equivalent martingale measure (EMM) are often inaccurate. While there are other models for barrier options with analytical solutions, such as jump-diffusion models (Kou, 2002; Kou and Wang, 2004), the constant elasticity of variance (CEV) model (Boyle and Tian, 1999; Davydov and Linetsky, 2001), exact analytical approaches (Fusai et al., 2006), the Hilbert transform-based (Feng and Linetsky, 2008), the Laplace transform method built on Lévy processes (Jeannin and Pistorius, 2010) or the Fourier-cosine-based semi-analytical methods (Lian et al., 2017), all of them depend on assumptions similar to the ones of the BSM pricing equation. Another set of methods for pricing barrier options based on solving partial differential equations (PDEs) was proposed in Boyle and Tian (1998), Zvan et al. (2000), Zhu and De Hoog (2010) and Golbabai et al. (2014). Although these methods are generally powerful, they depend on being able to accurately model the option with PDEs and cannot be used in all circumstances (other approaches used in the pricing of exotic derivatives include the method of lines (Chiarella et al., 2012), where the Greeks are also estimated, robust optimization techniques (Bandi and Bertsimas, 2014), applicable also to American options, finite–difference based approaches (Wade et al., 2007), where a Crank–Nicolson smoothing strategy to treat discontinuities in barrier options is presented, and regime–switching models (Elliott et al., 2014; Rambeerich and Pantelous, 2016)). As a result, Monte Carlo simulation (MCS) is often used for option pricing (Schoutens and Symens, 2003) and particularly for barrier options (Glasserman and Staum, 2001).

The main advantage of MCS over other pricing methods is its model–free property and its non–dependence on the dimension of the approximated equation. The latter is an important property since as (), the price of a discretely monitored barrier option converges to that of a continuously monitored one (Broadie et al., 1997). On the other hand, MCS has a serious drawback: it is inefficient in estimating prices of barrier options on high volatility assets. Indeed, high volatility makes it difficult for the asset to remain within barriers, which, in turn, makes a positive payoff a rare event (Glasserman et al., 1999). As a result, any standard MCS method will be inaccurate and highly unstable (Geman and Yor, 1996). This motivates the development of more advanced stochastic simulation methods which inherit the robustness of MCS, and yet are more efficient in estimating barrier option prices. A range of stochastic simulation techniques for speeding up the convergence have been proposed, such as the MCS approximation correction for constant single barrier options (Beaglehole et al., 1997), the simulation method based on the Large Deviations Theory (Baldi et al., 1999), and more recently the sequential MCS method (Shevchenko and Del Moral, 2017).

The main results of this study can be summarized as follows. First, we develop a novel stochastic simulation method for pricing barrier options which is based on the Subset Simulation (SubSim) method, a Markon chain Monte Carlo (MCMC) –based algorithm originally introduced in Au and Beck (2001) to deal with complex engineered systems and later extended by Zuev et al. (2015) to complex networks (for more details, the reader is referred to Au and Wang, 2014). MCMC provides us with a more efficient way to simulate the quantity of interest, compared to naive MCS methods, by sampling from a target distribution and has been widely used in statistical modelling in finance (see Eraker, 2001; Philipov and Glickman, 2006; Gerlach et al., 2011; Stroud and Johannes, 2014, amongst others for finance–related applications of MCMC). Here, we apply and further extend this idea to compute both the execution probabilities and prices of barrier options.

Second, we calculate the fair price for double barrier options on high volatility assets and barriers set near the starting price of the underlying asset. In our framework, the “failure” probability corresponds to the probability of the barrier option to be executed at maturity (i.e., the price of the underlying asset to remain withing the barriers). This setting in a simple MCS setup results – with an extremely large probability – in asset price trajectories which cross the barriers, rendering the barrier option invalid before maturity.

Third, we show by measuring the coefficient of variation (CV), and the mean squared error (MSE) that the proposed SubSim–based algorithm is an efficient technique for the pricing of such derivatives. In particular, the SubSim estimator has a CV which is , where is the execution probability and is a constant. Comparing this against the MCS estimator whose CV is and for very small values of , we can easily see that the latter increases at a dramatically faster pace compared to the SubSim estimator. Moreover, the MSE of the created SubSim estimator is – where is a constant –, which decreases for increasing .

Finally, we compare our results against the Multi–level Monte Carlo (MLMC) (Giles, 2008b, a) approach and show that for very small values of the option’s survival probability the SubSim estimator outperforms the MLMC estimator in terms of the observed CV. Thus our method can be seen as an alternative to price path–dependent options which also complements MLMC for special cases of underlying assets.

This paper begins with the introduction of the problem of barrier option pricing and the modification of the SubSim method in order to be able to accommodate it. In section 3, we show how SubSim can be used specifically for the estimation of the execution probability and the option payoff at maturity. Section 4 subsequently presents the main theorem and its proof. This establishes the limiting behaviour of the MSE and the computational complexity for a broad category of applications. Finally, numerical results and comparisons with the standard MCS and the MLMC methods are presented to provide support for the theoretical analysis followed by some concluding remarks.

2 Barrier Option Pricing with SubSim

2.1 Geometric Brownian Motion (GBM)

The starting point in option pricing is modeling the price of the underlying asset. Given the focus of this paper which is more on the simulation and statistical aspects of the method, and less on the modeling of the underlying price process, we use a standard GBM instead of a more complex jump process or a model with stochastic volatility which is frequently used in pricing exotic derivatives (see Kou, 2002; Kou and Wang, 2004; Chiarella et al., 2012, amongst others). Assume that follows the stochastic differential equation (SDE)

| (1) |

a risk–neutral proces, where is the drift, is volatility, and is the standard Brownian motion defined on a common probability space . The discretized solution of (1) can then be written as follows

| (2) |

where are i.i.d. standard normal random variables.

2.2 SubSim for Barrier Options

We first consider how SubSim can be used specifically for pricing barrier options and why it is especially efficient for options on assets with high volatility. The goal is to estimate the barrier option price , which is given by the following discounted expectation under the risk–neutral measure :

| (3) |

where is the payoff at the contract maturity (), , is the strike price, and stands for the indicator function: if , where and are the upper and lower barriers respectively, and zero otherwise.

In order to use the SubSim method we need to bring the problem in (3) in a form suitable to be used as input by the method. Suppose that the time–evolution of the dynamic system under study (e.g. evolution of the asset price ) is modeled by the following discrete model:

| (4) |

where is the price of the underlying asset at time , is the trajectory of the underlying asset, is a random input at time , and is a certain function that governs the evolution of S (i.e., the GBM (1) in our case). Let be the performance function – a function related to the quantity of interest S – (e.g. the maximum value of the asset price ). We say that a target event occurs if exceeds a critical threshold :

| (5) |

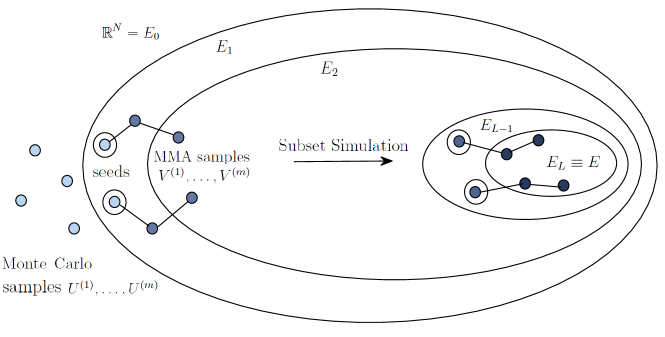

The central idea behind SubSim is to break down the rare event of interest into a series of “less rare” events that have easier-to-compute probabilities. This idea is implemented by considering a collection of nested subsets starting from the entire input space and finishing at the target rare event,

| (6) |

The intermediate events can be defined by simply repeatedly relaxing the value of the critical threshold in (5),

| (7) |

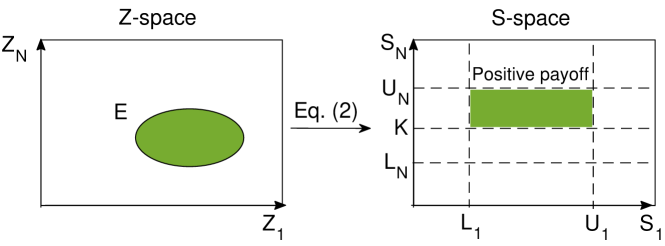

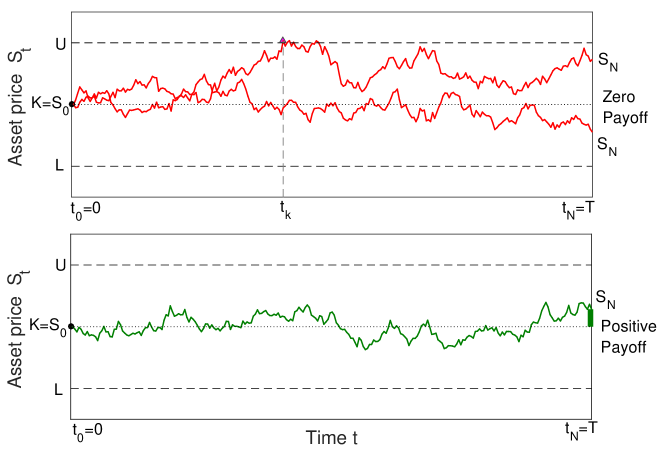

To make SubSim directly applicable, we need to specify suitable functions for the underlying asset price trajectory and the expected payoff at maturity. Let be a set of vectors that lead to a positive payoff. In other words, represents the target event for our problem and consists of all vectors that result into those asset price trajectories that remain within barriers and end up above the strike price. This is schematically illustrated in Figure 1.

Let be the payoff function,

| (8) |

equal to the payoff of a plain vanilla call in case the asset price trajectory remains within the barriers and ends up above the strike price or zero otherwise.

As for the performance function, in the case of option pricing, this quantifies how far the asset price trajectory lies from the positive payoff, or equivalently, how far is from . We define it as follows:

| (9) |

where terms quantify how far the asset prices is from the barriers and strike ,

| (10) |

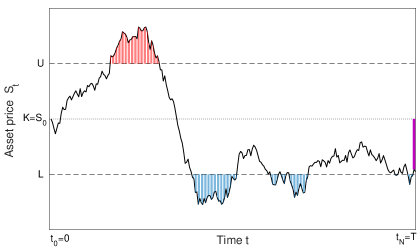

The difference between for and stems from the fact that at maturity , the role of the lower barrier is played by the strike price . The performance function is schematically shown in Figure 2. In terms of , the positive-payoff event can be written, according to the definition of the performance function in eq. 10, as follows:

| (11) |

where is now replaced by zero and the defined performance function brings the problem of estimating the probability of positive payoff into the general SubSim framework developed in Au and Beck (2001).

Then, combining equations (8) and (10), the option price, which in our case is the expected payoff of the contract at maturity, can be rewritten as follows:

| (12) |

Now, the problem boils down to estimating the execution probability and the expectation of the payoff at maturity, given by the second term in the product of eq. 12.

3 Probability of contract execution and option payoff via SubSim

We start with the calculation of to notice that given the sequence (6), the small probability of rare event can be written as a product of conditional probabilities:

| (13) |

By choosing the intermediate thresholds appropriately (in the actual implementation of SubSim described below, are chosen adaptively on the fly), we can make all conditional probabilities sufficiently large, and estimate them efficiently by MC-like simulation methods. In fact, the first factor in the right-hand side of (13), , can be directly estimated by MCS:

| (14) |

Estimating the remaining factors for is more difficult since this requires sampling from the conditional distribution , which is a nontrivial task, especially at later levels, where becomes a rare event. In SubSim, this is achieved by using the so-called modified Metropolis algorithm (MMA) (Au and Beck, 2001; Zuev and Katafygiotis, 2011), which belongs to a large family of MCMC algorithms (Liu, 2001; Robert and Casella, 2004) for sampling from complex probability distributions. The MMA algorithm is a component-wise modification of the original Metropolis algorithm (Metropolis et al., 1953), which is specifically tailored for sampling in high dimensions, where the original algorithm is known to perform poorly (Katafygiotis and Zuev, 2008).

To sample from , MMA generates a Markov chain whose stationary distribution is . The key difference between MMA and the original Metropolis algorithm is how the “candidate” state of a Markov chain is generated (in appendix A, the MMA algorithm used for the sampling is presented). Then, using the detailed balance equation, it can be shown (see Au and Beck, 2001, for details) that if is distributed according to the target distribution, , then so is , and is thus indeed the stationary distribution of the Markov chain generated by MMA. Now, to estimate the small probability of execution the method starts by generating MCS samples and computing the corresponding system trajectories via (4) and performance values . Without loss of generality, we can assume that

| (15) |

Indeed, to achieve this ordering, we can simply renumber the samples accordingly. Since is a rare event, all with large probability. The ordering (15) means however that, in the metric induced by the performance function, is the closest sample to , is the second closest, etc. Let’s define the first intermediate threshold as the average between the performance values of the and system trajectories, where with :

| (16) |

Setting to this value has two important corollaries: (1) the MCS estimate of given by (14) is exactly , and (2) samples are i.i.d. random vectors distributed according to the conditional distribution .

In the next step, SubSim generates Markov chains by MMA starting from most closest to samples as “seeds”:

| (17) |

Since by construction, all seeds are in the stationary state, , so are all Markov chains states . The length of each chain is , which makes the total number of states . To simplify the notation, let’s denote samples by simply . Next, the second intermediate threshold is similarly defined as follows:

| (18) |

where are the ordered performance values corresponding to samples . Again, by construction, and . The SubSim method, schematically illustrated in Figure 3, proceeds in this way by directing Markov chains towards the rare event until it is reached and sufficiently sampled. Specifically, it stops when the number of samples in , which a priori , is . All but the last factor in the right-hand side of (13) are then approximated by and . This results into the following estimate:

| (19) |

where is the number of subsets in (13) required to reach . The total number of samples used by SubSim is then

| (20) |

The first factor, the probability of positive payoff , can be readily estimated by SubSim,

| (21) |

Moreover, the conditional expectation in (12) for the terminal asset price can be estimated using the samples generated by SubSim at the last level. Namely, let be the last batch of MMA samples generated by SubSim before it stops,

| (22) |

where denotes the standard multivariate normal distribution conditioned on . By construction (this is the SubSim stopping criterion), at least of these samples are in . Let

| (23) |

denote those samples. The conditional expectation can then be estimated as follows:

| (24) |

where is the final value of the asset price obtained from (2). The expression in (24) in essence gives the expected terminal price of the underlying asset under the risk–neutral measure as the average of all the generated asset price paths. Combining (21) and (24), we obtain the SubSim estimate of the option price:

| (25) |

SubSim as described above, yields an estimator for the execution probability which scales like a power of the logarithm of (Au and Beck, 2001):

| (26) |

where is a constant that depends on the correlation of the Markov chain states and . Comparing (26) against the CV of a standard MCS method (Liu, 2001; Robert and Casella, 2004)

| (27) |

reveals a serious drawback of MCS: it is inefficient in estimating small probabilities of rare events. Indeed, as , then . This means that the number of samples needed to achieve an acceptable level of accuracy is inversely proportional to , and therefore very large, . Therefore, for rare events, where probabilities are small , the CV of SubSim is significantly lower than that of MCS, . This property guaranties that SubSim produces more accurate (on average) estimates of small probabilities of rare events.

In case the asset price has high volatility, then discrete asset price trajectories will have large variability and with large probability will either cross the barriers and expire or end up bellow the strike. This means that having a positive payoff will be a rare event. This suggests – and we confirm this by simulation in Section 5 – that SubSim should be substantially more efficient in estimating prices of barrier options on high volatility assets than MC-based methods.

4 Complexity Theorem

The complexity theorem relates the execution probability with the mean squared error (MSE) and the computational complexity/cost of the SubSim estimator for the option price at , by examining their limiting behavior. The theorem does not make any assumptions regarding the underlying SDE or the functional of the solution used.

Theorem 1.

The SubSim estimator for a functional of the solution to a given SDE has

-

(i)

a MSE bounded from above by ,

-

(ii)

with computational cost which has an upper bound of ,

where are constants, is the CV of , is the probability of positive payoff at maturity and a parameter dependent on the correlation between the intermediate execution probabilities.

Proof. Using result (26) we have that the squared CV of the execution probability is equal to

| (28) |

where is a constant related to the correlation between the states of the Markov chains used for the sampling at different levels, is the level probability, is the total number of subsets and represents the number of samples per subset (the product approximates the total number of samples in (26)). By (25) we see that the option price estimate given by SubSim is a function of the execution probability , the number of MMA samples that lead to a non-zero payoff and the payoff at maturity . As a result, the CV of the SubSim estimator for the option price P is equal to the CV of times a scaling factor (the payoff at ) and the CV in (28) can be used. Now, the complexity of given by the product of the samples per level times the number of simulation levels used is equal to

| (29) |

by noting that the number of simulation levels is chosen as . Fixing and treating as a known constant we have that

| (30) |

which yields the upper bound of the computational complexity, given that is for fixed . Moreover, considering the definition for the coefficient of variation for we have

| (31) |

Squaring both sides of (31) gives

| (32) |

which equivalently can be written as

| (33) |

Now, we use Propositions 1 and 2 (Au and Beck, 2001) which prove that both the bias and the squared CV of are bounded above by . As a result, the first term of the is while the second term is which gives an bounded above by as for large values of it dominates the term.

By (28) we also notice that is from which we obtain . Setting and fixing , the number of samples becomes where is a new constant. Consequently, we end up with an MSE bounded from above by

| (34) |

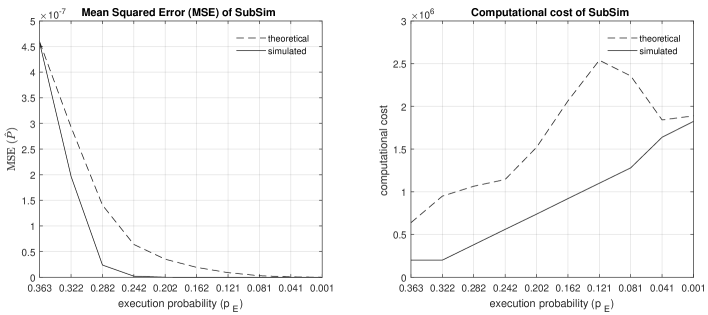

The result in is very important as it shows that by decreasing the probability of contract execution (i.e., generating a more rare event) results in a smaller MSE while at the same time, the corresponding CV grows (see also results in Table 1). Moreover, in we show that the computational complexity of SubSim is inversely proportional to the square of the target CV and the natural logarithm of the execution probability . On one hand, as the target CV becomes smaller (i.e., we demand a more accurate output), the cost increases as the method uses more subsets and subsequently a larger number of samples. On the other hand, as the execution probability decreases, the absolute value of its logarithm increases, resulting in a higher computational cost as the lower the execution probability the more demanding the estimation of becomes. Figure 4 shows the results of a simulation run (repeated 100 times) to compare how the MSE and the computational complexity scale with respect to according to the SubSim theory and the experimental outputs.

5 Simulation Study

5.1 Barrier Options

Our numerical experiments focus on pricing double knock-out barrier call options, but it is straightforward to extend the proposed methodology to other types of barrier options. Suppose that barriers are monitored during time period at equally spaced times with frequency , and the option expires if the asset hits either the upper or the lower barrier. Let us denote the corresponding asset prices by , the drift by and the volatility by .

The quantity of interest is the barrier option price at the beginning of the contract (), given by (3), which takes a non–zero value only in case the asset price trajectory remains within the two barriers. For illustrative purposes, Figure 5 shows several asset trajectories that lead to both option expiration and positive payoff.

5.2 Simulation results for SubSim vs standard MCS

In the first of our numerical experiments, we consider a double knock-out barrier call option with a starting price (spot) , strike , and constant lower and upper barriers and . A double knock–out option expires worthless in case either the upper or the lower barrier is crossed by the asset price trajectory over the life of the option (). In any other case, the payoff at maturity is calculated as a plain vanilla European call option (i.e., , where is the terminal asset price). The option is discretely monitored during time period at equally spaced times with frequency , where (approximate number of trading days in a financial year). We further assume that the drift of the underlying asset is constant . To observe the effect of high volatility, we vary the value of over ten different values logarithmically spaced between and .

The quantity of interest, the fair option price at the beginning of the contract () is given by

| (35) |

where is the value of the option at the end of time period given by (3) and estimated by (25), is the discounting factor from maturity to , and is the interest rate, which is assumed to be constant in this example, .

First, we use SubSim with samples per subset to estimate both the probability of having a positive payoff at the end of the period, , and the option price,

| (36) |

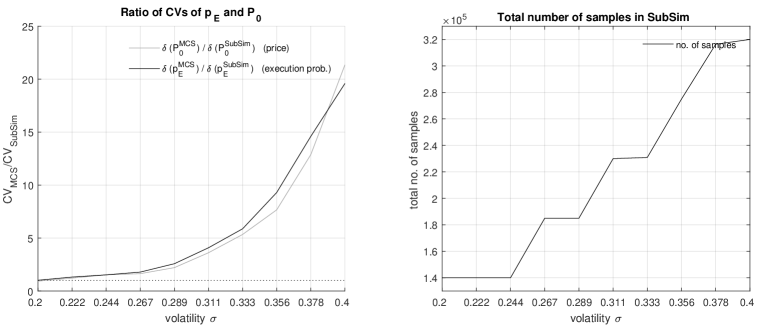

The mean values of estimates and their CVs computed from 100 independent runs of the SubSim algorithm are presented in Table 1. As expected, as the asset volatility increases, the event of having a positive payoff becomes increasingly rare (e.g. if , then ) and, as a result, the option becomes cheaper. The right plot in Figure 6 shows the average (based on 100 runs) total number of samples used by SubSim versus the volatility . The obtained trend is again expected: as increases, the probability becomes smaller, and, therefore, the number of subsets in (19) increases, which leads to the increase in the total number of samples (20).

| 0.200 | / | / | 0.030 / 0.0281 | 0.034 / 0.0347 |

| 0.216 | / | / | 0.032 / 0.0391 | 0.036 / 0.0476 |

| 0.233 | / | / | 0.039 / 0.0596 | 0.044 / 0.0673 |

| 0.252 | / | / | 0.048 / 0.0788 | 0.055 / 0.0985 |

| 0.272 | / | / | 0.057 / 0.126 | 0.062 / 0.160 |

| 0.294 | / | / | 0.060 / 0.217 | 0.069 / 0.282 |

| 0.317 | / | / | 0.076 / 0.406 | 0.081 / 0.476 |

| 0.343 | / | / | 0.099 / 0.759 | 0.109 / 1.014 |

| 0.370 | / | / | 0.153 / 1.971 | 0.160 / 2.337 |

| 0.400 | / | / | 0.180 / 3.844 | 0.205 / 4.017 |

Next, we use MCS to estimate and . To ensure fair comparison of the two methods, for each value of , MCS is implemented with the same total number of samples as in SubSim. The mean values of Monte Carlo estimates for the execution probability and the option price , with their CVs are presented in Table 1. The mean values of and are approximately the same as those of and , which confirms that SubSim estimates are approximately unbiased. The CVs, however, differ drastically. Namely, and are substantially smaller than and , respectively. This effect is more pronounced the larger the volatility. For example, if , then SubSim is approximately 20 times more efficient than MCS, i.e., on average, SubSim produces 20 times more accurate estimates, where the accuracy is measured by the CV. As explained at the end of Section 3, this result stems from the fact that SubSim is more efficient than MCS in estimating small probabilities of rare events, and if volatility is large, then the event of having a positive payoff is rare.

To visualize how SubSim outperforms MCS as the volatility increases, in the left plot of Figure 6 we plot the ratios of CVs and versus . Since the mean values of SubSim and MCS estimates are approximately the same, the ratios of CVs are approximately the ratios of the corresponding standard errors. Graphically, the cases where SubSim outperforms MCS for the estimation of the execution probability and the option price are those for which the corresponding value of or lies above the horizontal line (dotted line in Figure 6). At that level, both methods would exhibit the same level of accuracy measured by the CV, since would equal . We notice that SubSim outperforms MCS in every examined case as both lines (for and ) lie above the level.

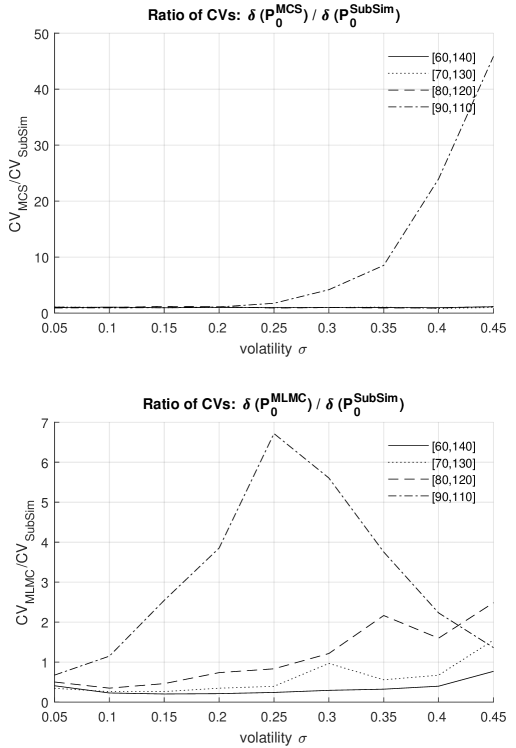

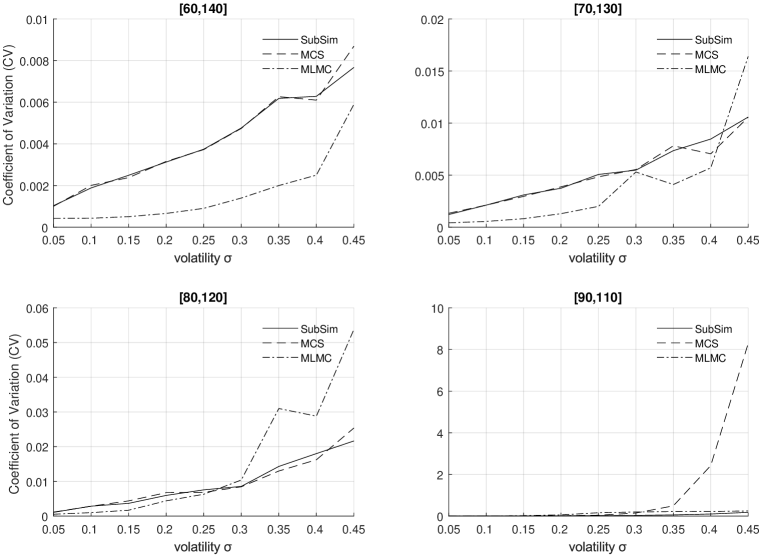

In the second of our simulation tests we increase the number of samples to using also different levels for the lower and the upper barrier. The reason we consider more samples is to compare SubSim against not only MCS but also multilevel Monte–Carlo (see subsection 5.3), where is considered in the original barrier option numerical experiments. To maintain a fair comparison we perform our MCS tests with the same number of samples as in SubSim. The top graph of Figure 7 plots the ratio of CV between SubSim and standard MCS with respect to the volatility of the underlying asset for four levels of the upper and lower barrier. It is immediately noticeable that for volatility values up to the two methods have comparable CVs (SubSim outperforms standard MCS as reported in Table 3 but not significantly), providing evidence that for low–volatility assets the two methods produce sufficiently accurate results. This result is not surprising as SubSim is designed by construction to deal with problems with extremely small execution probabilities.

However, as volatility increases, SubSim outperforms naive MCS in all barrier levels, while especially in the case of and (barriers close to ) and (a high–volatility asset), SubSim is up to 50 times more efficient than standard MC; for lower levels of , SubSim still outperforms MCS.

5.3 Simulation results for SubSim vs MLMC

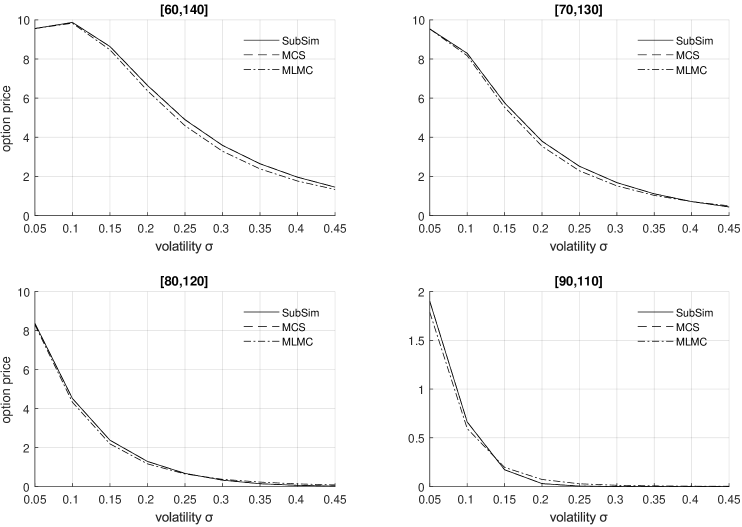

In this section we compare the performance of SubSim against the multilevel Monte Carlo method (Giles, 2008b, a), when both used to price a double knock–out barrier call option with two fixed barriers set at four different levels, while all the other parameters remain the same as in subsection 5.2. The original multilevel MCS method was developed to price single knock–out barrier options, amongst other exotic derivatives, and thus we add a component for the second barrier in order to accommodate double barrier options as well (see appendices B and C).

The price at of the asset is , the strike price is and the time–increment is where represents the number of discrete monitoring points of the barrier option. In the case of MLMC, varies between levels as it is a function of a constant and level , where . The barriers take four different values in increments of ten between and (lower) and and (upper). The drift of the diffusion equation is equal to , while the volatility (diffusion coefficient) varies between and taking nine discrete values linearly spaced in this interval. Finally, the risk–free rate at which we discount the terminal payoffs is known and fixed at .

The bottom graph of Figure 7 plots the ratio of CV between SubSim and MLMC for four levels of barriers against asset’s volatility. For barriers which lie far from the price of the asset at (i.e., and represented by the solid and the dotted line respectively), MLMC produces more accurate results than SubSim. Nevertheless, we notice that as asset volatility increases the performance of SubSim improves, approaching that of MLMC without surpassing it. SubSim outperforms MLMC when and (dashed/dotted line) and when and (dashed line) and the volatility of the underlying asset is higher than 0.25. In both cases, the probability of a non–zero payoff at is extremely small (Table 1), and hence the use of SubSim provides more accurate results compared either to standard MCS or MLMC. The evidence we obtain here further supports the findings in Section 5.2 that SubSim is an efficient technique to price barrier options on high volatility assets, especially when the barriers are close to the initial price of the underlying asset.

6 Conclusion

In this paper, we develop a new stochastic simulation method for pricing barrier options. The method is based on Subset Simulation (SubSim), a very efficient algorithm for estimating small probabilities of rare events. The key observation allowing to exploit the efficiency of SubSim is that the barrier option price can be written as a function of the probability of option execution and a certain conditional expectation, which can both be estimated efficiently by SubSim. In the case of barrier options on high–volatility assets, SubSim is especially advantageous because of the very small probability of the contract to remain valid until maturity. We first compare the proposed SubSim method against the standard Monte Carlo simulation (MCS) to show that SubSim always outperforms MCS, confirming this with a series of numerical examples. Moreover, we show that the higher the volatility of the underlying asset (i.e. the smaller the probability of option execution), the larger the advantage of SubSim over MCS. Next, we compare our proposed method with the multilevel Monte–Carlo (MLMC) simulation introduced in Giles (2008b). Although MLMC outperforms SubSim in general, we find that SubSim can still be more efficient than MLMC, – where efficiency is measured by the coefficient of variation (CV) – in cases where the volatility of the underlying asset is high and the barriers are set close to the starting price of the asset. As a result, the method we propose here complements MLMC, handling special cases of barrier option settings more efficiently.

References

- Andersen et al. (2001) T. G. Andersen, T. Bollerslev, F. X. Diebold, and H. Ebens. The distribution of realized stock return volatility. Journal of Financial Economics, 61(1):43–76, 2001.

- Au and Beck (2001) I. Au and J. Beck. Estimation of small failure probabilities in high dimensions by subset simulation. Probabilistic Engineering Mechanics, 16:193–207, 2001.

- Au and Wang (2014) S.K. Au and Y. Wang. Engineering Risk Assessment and Design with Subset Simulation. John Wiley and Sons, 2014.

- Baldi et al. (1999) P. Baldi, L. Caramellino, and M.G. Iovino. Pricing general barrier options: a numerical approach using sharp large deviations. Mathematical Finance, 9(4):293–321, 1999.

- Bandi and Bertsimas (2014) C. Bandi and D. Bertsimas. Robust option pricing. European Journal of Operational Research, 239(3):842–853, 2014.

- Beaglehole et al. (1997) D. R. Beaglehole, P. H. Dybvig, and G. Zhou. Going to extremes: Correcting simulation bias in exotic option valuation. Financial Analysts Journal, 53(1):62–68, 1997.

- Boyle and Tian (1998) P. P. Boyle and Y. Tian. An explicit finite difference approach to the pricing of barrier options. Applied Mathematical Finance, 5(1):17–43, 1998.

- Boyle and Tian (1999) P. P. Boyle and Y. Tian. Pricing lookback and barrier options under the CEV process. Journal of Financial and Quantitative Analysis, 34(2):241–264, 1999.

- Broadie et al. (1997) M. Broadie, P. Glasserman, and S. Kou. A continuity correction for discrete barrier options. Mathematical Finance, 7(4):325–349, 1997.

- Carr and Chou (2002) P. Carr and A. Chou. Hedging complex barrier options. 2002.

- Chiarella et al. (2012) C. Chiarella, B. Kang, and G. H. Meyer. The evaluation of barrier option prices under stochastic volatility. Computers & Mathematics with Applications, 64(6):2034–2048, 2012.

- Dadachanji (2015) Z. Dadachanji. FX Barrier Options: A comprehensive guide for industry quants. Springer, 2015.

- Davydov and Linetsky (2001) D. Davydov and V. Linetsky. Pricing and hedging path-dependent options under the CEV process. Management Science, 47(7):949–965, 2001.

- Derman and Kani (1996) E. Derman and I. Kani. The ins and outs of barrier options: Part 1. Derivatives Quarterly, 2:55–67, 1996.

- Derman and Kani (1997) E. Derman and I. Kani. The ins and outs of barrier options: Part 2. Derivatives Quarterly, 3:73–80, 1997.

- Elliott et al. (2014) R. J Elliott, T. K. Siu, and L. Chan. On pricing barrier options with regime switching. Journal of Computational and Applied Mathematics, 256:196–210, 2014.

- Eraker (2001) B Eraker. Mcmc analysis of diffusion models with application to finance. Journal of Business & Economic Statistics, 19(2):177–191, 2001.

- Feng and Linetsky (2008) L. Feng and V. Linetsky. Pricing discretely monitored barrier options and defaultable bonds in Lévy process models: a fast Hilbert transform approach. Mathematical Finance, 18(3):337–384, 2008.

- Fusai and Recchioni (2007) G. Fusai and M. C. Recchioni. Analysis of quadrature methods for pricing discrete barrier options. Journal of Economic Dynamics and Control, 31(3):826–860, 2007.

- Fusai et al. (2006) G. Fusai, D. I. Abrahams, and C. Sgarra. An exact analytical solution for discrete barrier options. Finance and Stochastics, 10(1):1–26, 2006.

- Geman and Yor (1996) H. Geman and M. Yor. Pricing and hedging double-barrier options: a probabilistic approach. Mathematical Finance, 6(4):365–378, 1996.

- Gerlach et al. (2011) R H Gerlach, C WS Chen, and N YC Chan. Bayesian time-varying quantile forecasting for value-at-risk in financial markets. Journal of Business & Economic Statistics, 29(4):481–492, 2011.

- Giles (2008a) M. Giles. Improved multilevel Monte Carlo convergence using the Milstein scheme. Springer, 2008a.

- Giles (2008b) M. B. Giles. Multilevel Monte Carlo path simulation. Operations Research, 56(3):607–617, 2008b.

- Glasserman (2013) P. Glasserman. Monte Carlo methods in financial engineering, volume 53. Springer Science & Business Media, 2013.

- Glasserman and Staum (2001) P Glasserman and J Staum. Conditioning on one-step survival for barrier option simulations. Operations Research, 49(6):923–937, 2001.

- Glasserman et al. (1999) P Glasserman, P Heidelberger, P Shahabuddin, and T Zajic. Multilevel splitting for estimating rare event probabilities. Operations Research, 47(4):585–600, 1999.

- Golbabai et al. (2014) A. Golbabai, L. V. Ballestra, and D. Ahmadian. A highly accurate finite element method to price discrete double barrier options. Computational Economics, 44(2):153–173, 2014.

- Guardasoni and Sanfelici (2016) C. Guardasoni and S. Sanfelici. Fast numerical pricing of barrier options under stochastic volatility and jumps. SIAM Journal on Applied Mathematics, 76(1), 2016.

- Hull (2009) J. C. Hull. Options, futures, and other derivatives. Pearson, USA, 2009.

- Jeannin and Pistorius (2010) M. Jeannin and M. Pistorius. A transform approach to compute prices and Greeks of barrier options driven by a class of Lévy processes. Quantitative Finance, 10(6):629–644, 2010.

- Jewitt (2015) G. Jewitt. FX derivatives trader school. John Wiley & Sons, 2015.

- Katafygiotis and Zuev (2008) L. S. Katafygiotis and K. M. Zuev. Geometric insight into the challenges of solving high-dimensional reliability problems. Probabilistic Engineering Mechanics, 23:208–218, 2008.

- Kou (2002) S. G. Kou. A jump-diffusion model for option pricing. Management Science, 48(8):1086–1101, 2002.

- Kou (2007) S. G. Kou. Discrete barrier and lookback options. Handbooks in Operations Research and Management Science, 15:343–373, 2007.

- Kou and Wang (2004) S. G. Kou and H. Wang. Option pricing under a double exponential jump diffusion model. Management Science, 50(9):1178–1192, 2004.

- Lian et al. (2017) G. Lian, S.-P. Zhu, R. J. Elliott, and Z. Cui. Semi-analytical valuation for discrete barrier options under time-dependent Lévy processes. Journal of Banking & Finance, 75:167–183, 2017.

- Liu (2001) J. S. Liu. Monte Carlo strategies in scientific computing. Springer Verlag, New York, 2001.

- Luenberger and Luenberger (1999) D. Luenberger and R. Luenberger. Pricing and hedging barrier options. Investment Practice, Stanford University, EES-OR, 1999.

- Merton (1973) R. C. Merton. Theory of rational option pricing. The Bell Journal of Economics and Management Science, 4(1):141–183, 1973.

- Metropolis et al. (1953) N. Metropolis, A.W. Rosenbluth, M.N. Rosenbluth, A.H. Teller, and E. Teller. Equation of state calculations by fast computing machines. The Journal of Chemical Physics, 21:1087–1092, 1953.

- Philipov and Glickman (2006) A Philipov and M E Glickman. Multivariate stochastic volatility via wishart processes. Journal of Business & Economic Statistics, 24(3):313–328, 2006.

- Rambeerich and Pantelous (2016) N. Rambeerich and A. A. Pantelous. A high order finite element scheme for pricing options under regime switching jump diffusion processes. Journal of Computational and Applied Mathematics, 300:83–96, 2016.

- Robert and Casella (2004) C. P. Robert and G. Casella. Monte Carlo statistical methods. Springer Verlag, New York, 2004.

- Schoutens and Symens (2003) W. Schoutens and S. Symens. The pricing of exotic options by Monte–Carlo simulations in a Lévy market with stochastic volatility. International Journal of Theoretical and Applied Finance, 6(8):839–864, 2003.

- Shevchenko and Del Moral (2017) P. V. Shevchenko and P. Del Moral. Valuation of barrier options using sequential Monte Carlo. Journal of Computational Finance, 20(4):107–135, 2017.

- Stroud and Johannes (2014) J R Stroud and M S Johannes. Bayesian modeling and forecasting of 24-hour high-frequency volatility. Journal of the American Statistical Association, 109(508):1368–1384, 2014.

- Wade et al. (2007) B. A. Wade, A. Q. M. Khaliq, M. Yousuf, J. Vigo-Aguiar, and R. Deininger. On smoothing of the Crank–Nicolson scheme and higher order schemes for pricing barrier options. Journal of Computational and Applied Mathematics, 204(1):144–158, 2007.

- Zhu and De Hoog (2010) Z. Zhu and F. De Hoog. A fully coupled solution algorithm for pricing options with complex barrier structures. The Journal of Derivatives, 18(1):9–17, 2010.

- Zuev and Katafygiotis (2011) K. M. Zuev and L. S. Katafygiotis. Modified Metropolis-Hastings algorithm with delayed rejection. Probabilistic Engineering Mechanics, 26:405–412, 2011.

- Zuev et al. (2015) K.M. Zuev, S. Wu, and J.L. Beck. General network reliability problem and its efficient solution by subset simulation. Probabilistic Engineering Mechanics, 40:25–35, 2015.

- Zvan et al. (2000) R. Zvan, K. R. Vetzal, and P. A. Forsyth. Pde methods for pricing barrier options. Journal of Economic Dynamics and Control, 24(11–12):1563–1590, 2000.

Appendix A MMA sampling from the target distribution

To sample from the target distribution , the MMA generates a Markov chain with stationary distribution . Namely, if we let be the current state, then the next state is generated as follows:

-

1.

Generate a candidate state :

-

(a)

For each , generate , where is a symmetric, , univariate proposal distribution, e.g. Gaussian distribution centered at , the component of .

-

(b)

Compute the acceptance probability:

(37) where is the marginal PDF of , , and are assumed to be independent.

-

(c)

Set

(38)

-

(a)

-

2.

Accept or reject the candidate state:

(39)

Appendix B Probability of survival of a barrier option

The pricing of barrier options is a first passage time problem in which we are interested in the first time that the price trajectory of the underlying asset crosses a prespecified barrier. Now, assuming that and are the upper and lower barriers respectively, the survival indicator function of the barrier option in (3) can be approximated via its discrete form

| (40) |

where and are the maximum and minimum, respectively, of (2) in and or is the size of the timestep on a discrete grid. Equation (40) takes the value one if and only if the conditions for and are met at every time–step of the discretized problem, otherwise the product (40) becomes zero and the option expires worthless. Following Glasserman (2013) (see particularly section 6.4 and example 2.2.3) we sample the minimum and the maximum of by formulating the following problem:

| (41) |

with

| (42) |

the maximum of the approximation of S on , and

| (43) |

with

| (44) |

the minimum of a discrete time approximation of S on .

In the sampling of the maximum, conditioning on the endpoints and , the process becomes a Brownian bridge, and thus we sample from the distribution of the maximum of a Brownian bridge, a Rayleigh distribution, which results in

| (45) |

where is a uniformly distributed random variable in . Now, let be a discrete time approximation of the solution of in (1), where , . To obtain a good estimation for (i.e. the maximum of the interpolating Brownian bridge) and decrease the error induced by the discretization (i.e., the case where crosses or between two grid points), we interpolate over , which given the end points and results in

| (46) |

with .

Given a barrier , the probability of survival for the option (the maximum price of the underlying asset to remain below ) in the fine–path estimation is given by

| (47) |

where is the fixed standard deviation of the underlying asset price and is the time–step in the discretization process. The corresponding estimation for a coarse–path is equal to

| (48) |

Appendix C Minimum of Brownian bridge

We now derive analytically the probability of survival for a double barrier option in a fine path estimation, by calculating also the probability of the minimum of to cross the lower barrier . Conditioning on endpoints and , the distribution of the minimum of the Brownian bridge (interpolated over ) is given by

| (49) |

where . Subsequently, the probability of the minimum of to cross the lower barrier is equal to

| (50) |

The probability in (50) refers to the case of the running minimum crossing the lower barrier. The probability to remain above the lower barrier is thus equal to its complement

| (51) |

and the probability of the asset price to remain within the barriers on is equal to

| (52) |

The calculation of the probability of survival for the coarse path estimation follows trivially from (52) by adjusting it using (48). Then, the option remains alive until time when the asset price is bounded between and , which in the case of a coarse path estimation, using a midpoint equal to , equals

| (53) | ||||

| (54) |

Appendix D Simulation study results

| Barriers | |||||

| [60,140] | [70,130] | [80,120] | [90,110] | ||

| Volatility () | Method | ||||

| 0.05 | Standard MCS | 9.5559 | 9.5345 | 8.3761 | 1.9009 |

| MLMC | 9.5549 | 9.5339 | 8.3008 | 1.7882 | |

| SubSim | 9.5573 | 9.5351 | 8.3728 | 1.8997 | |

| 0.10 | Standard MCS | 9.8679 | 8.2903 | 4.5155 | 0.6617 |

| MLMC | 9.8271 | 8.1682 | 4.3242 | 0.5941 | |

| SubSim | 9.8656 | 8.2862 | 4.5137 | 0.6615 | |

| 0.15 | Standard MCS | 8.6454 | 5.7592 | 2.3743 | 0.1712 |

| MLMC | 8.4688 | 5.5283 | 2.1859 | 0.1956 | |

| SubSim | 8.6413 | 5.7570 | 2.3734 | 0.1711 | |

| 0.20 | Standard MCS | 6.6578 | 3.8014 | 1.2839 | 0.0290 |

| MLMC | 6.3772 | 3.5392 | 1.1595 | 0.0716 | |

| SubSim | 6.6477 | 3.7958 | 1.2839 | 0.0292 | |

| 0.25 | Standard MCS | 4.8993 | 2.5194 | 0.6712 | 0.0033 |

| MLMC | 4.5896 | 2.2841 | 0.6406 | 0.0273 | |

| SubSim | 4.8970 | 2.5148 | 0.6707 | 0.0033 | |

| 0.30 | Standard MCS | 3.5877 | 1.6833 | 0.3226 | 0.0003 |

| MLMC | 3.2844 | 1.5152 | 0.3668 | 0.0120 | |

| SubSim | 3.5840 | 1.6792 | 0.3223 | 0.0003 | |

| 0.35 | Standard MCS | 2.6423 | 1.1106 | 0.1406 | 1.33E-05 |

| MLMC | 2.3811 | 1.0275 | 0.2233 | 5.70E-03 | |

| SubSim | 2.6414 | 1.1096 | 0.1403 | 1.61E-05 | |

| 0.40 | Standard MCS | 1.9638 | 0.7114 | 0.0554 | 1.84E-06 |

| MLMC | 1.7620 | 0.7101 | 0.1306 | 3.00E-03 | |

| SubSim | 1.9604 | 0.7107 | 0.0554 | 7.19E-07 | |

| 0.45 | Standard MCS | 1.4525 | 0.4387 | 0.0199 | 5.79E-08 |

| MLMC | 1.3312 | 0.4956 | 0.0776 | 1.70E-03 | |

| SubSim | 1.4501 | 0.4371 | 0.0198 | 2.49E-08 | |

| Barriers | |||||

| [60,140] | [70,130] | [80,120] | [90,110] | ||

| Volatility () | Method | ||||

| 0.05 | Standard MCS | 0.0018 | 0.0016 | 0.0019 | 0.0045 |

| MLMC | 0.0004 | 0.0004 | 0.0005 | 0.0024 | |

| SubSim | 0.0011 | 0.0013 | 0.0013 | 0.0031 | |

| 0.10 | Standard MCS | 0.0027 | 0.0026 | 0.0038 | 0.0080 |

| MLMC | 0.0004 | 0.0006 | 0.0010 | 0.0077 | |

| SubSim | 0.0018 | 0.0019 | 0.0025 | 0.0059 | |

| 0.15 | Standard MCS | 0.0037 | 0.0040 | 0.0054 | 0.0177 |

| MLMC | 0.0005 | 0.0008 | 0.0017 | 0.0229 | |

| SubSim | 0.0027 | 0.0026 | 0.0037 | 0.0092 | |

| 0.20 | Standard MCS | 0.0041 | 0.0053 | 0.0084 | 0.0444 |

| MLMC | 0.0007 | 0.0013 | 0.0044 | 0.0598 | |

| SubSim | 0.0032 | 0.0039 | 0.0055 | 0.0156 | |

| 0.25 | Standard MCS | 0.0054 | 0.0066 | 0.0095 | 0.1122 |

| MLMC | 0.0009 | 0.0020 | 0.0063 | 0.1623 | |

| SubSim | 0.0042 | 0.0053 | 0.0068 | 0.0219 | |

| 0.30 | Standard MCS | 0.0069 | 0.0089 | 0.0180 | 0.4069 |

| MLMC | 0.0014 | 0.0053 | 0.0104 | 0.1992 | |

| SubSim | 0.0043 | 0.0061 | 0.0093 | 0.0347 | |

| 0.35 | Standard MCS | 0.0075 | 0.0099 | 0.0301 | 1.9758 |

| MLMC | 0.0020 | 0.0041 | 0.0310 | 0.2169 | |

| SubSim | 0.0061 | 0.0072 | 0.0129 | 0.0652 | |

| 0.40 | Standard MCS | 0.0098 | 0.0126 | 0.0373 | 5.6981 |

| MLMC | 0.0025 | 0.0057 | 0.0288 | 0.2257 | |

| SubSim | 0.0067 | 0.0088 | 0.0166 | 0.1047 | |

| 0.45 | Standard MCS | 0.0087 | 0.0106 | 0.0254 | 8.2893 |

| MLMC | 0.0059 | 0.0164 | 0.0538 | 0.2465 | |

| SubSim | 0.0077 | 0.0128 | 0.0217 | 0.1808 | |