Explicit inverse of tridiagonal matrix with

applications in autoregressive modeling

Abstract

We present the explicit inverse of a class of symmetric tridiagonal matrices which is almost Toeplitz, except that the first and last diagonal elements are different from the rest. This class of tridiagonal matrices are of special interest in complex statistical models which uses the first order autoregression to induce dependence in the covariance structure, for instance, in econometrics or spatial modeling. They also arise in interpolation problems using the cubic spline. We show that the inverse can be expressed as a linear combination of Chebyshev polynomials of the second kind and present results on the properties of the inverse, such as bounds on the row sums, the trace of the inverse and its square, and their limits as the order of the matrix increases.

Keywords: tridiagonal matrix; explicit inverse; time series models; first order autoregression.

Mathematical sub classification numbers: 15A09, 65F50, 62M10, 91G70, 91B72

1 Introduction

Tridiagonal matrices occur in many areas of science, such as mathematics, econometrics and quantum mechanics. For instance, tridiagonal linear systems often arise in the solving of interpolation problems, boundary value problems and partial differential equations using finite difference methods (Pozrikidis, 2014). The inversion of both the general form as well as some special classes of tridiagonal matrices has thus been studied extensively (Schlegel, 1970; Lewis, 1982; Heinig and Rost, 1984). A comprehensive review is given in Meurant (1992). Various algorithms have also been proposed for efficient computation of the inverse (El-Mikkawy and Karawia, 2006; Hadj and Elouafi, 2008; Ran et al., 2009).

Formulas for the inverse of the general tridiagonal matrix have been derived by several authors based on different approaches (e.g. Yamamoto and Ikebe, 1979; Usmani, 1994; Huang and McColl, 1997), such as linear difference equation (Mallik, 2001) and backward continued fractions (Kılıç, 2008). These formulas usually involve recurrence relations and are not of explicit closed form, or they may reduce to closed form only for some special classes. Meurant (1992) presents an explicit inverse for the Toeplitz tridiagonal matrix by solving the recurrences in its Cholesky decomposition analytically. Extending these results, da Fonseca and Petronilho (2001, 2005) express the inverse of -Toeplitz tridiagonal matrices explicitly in terms of Chebyshev polynomials of the second kind. An order -Toeplitz tridiagonal matrix is of the form with for and if . That is, the diagonal, subdiagonal and superdiagonal entries are -periodic. A Toeplitz tridiagonal matrix is obtained when . Encinas and Jiménez (2018a) present the explicit inverse of a -Toeplitz tridiagonal matrix, in which each diagonal is a quasi-periodic sequence with period but multiplied by a real number . Such analytic formulas are important in studying the properties of the inverse, for instance, the rate of decay of elements along a row or column or for establishing bounds (Nabben, 1999a, b). In a closely related but independent work, Encinas and Jiménez (2018b) present the explicit inverse of tridiagonal matrices, and necessary and sufficient conditions for their invertibility, which are derived using the solution of Sturm-Liouville boundary value problems associated to second order linear difference equations expressed through a discrete Schrödinger operator. Our article focuses on the inverse of a more specialized form of the tridiagonal matrix and its properties, which has applications in econometric and statistical modeling problems.

In this article, we consider real symmetric tridiagonal matrices of the form

| (1) |

which is almost Toeplitz except that the first and last diagonal elements are different from the rest. We assume without loss of generality that or , and . Tridiagonal matrices of this form often arise in interpolation problems, as well as econometrics and spatial modeling when first order autoregression is used to induce dependence in the covariance structure. We note that Yueh (2006), Yueh and Cheng (2008) and Cheng and Yueh (2013) has derived the explicit inverse of complex tridiagonal matrices with constant diagonals and some perturbed elements using symbolic calculus, of which arises as a special case. However, here we focus on the real-valued case and present an alternative proof using difference equations (which may be more accessible to practitioners in statistics and econometrics) and show that the elements of can be viewed as a linear combination of Chebyshev polynomials of the second kind. While Yueh (2006) (Theorems 2 and 3) do consider simplified expressions for some special cases where the perturbed elements are of equal value and at the corners, these cases correspond only to in the context of . We first describe some motivating applications in Section 2 for which the results in this article are of special relevance, before deriving the explicit inverse. We also study some properties of . Bounds for the row (or column) sums are also presented and we provide expressions for the trace of and and their limiting behavior as the order of the matrix increases. Application of these results are illustrated in Section 7 using a first order autoregressive process with observational noise.

2 Applications

In this section, we discuss some applications where the tridiagonal matrix in (1) arises, and where the explicit inverse and its properties may be of interest.

In interpolation problems, the cubic spline is often used to avoid the Runge phenomenon (Knott, 2000). When equidistant knots and clamped (first derivative) boundary conditions are used, a tridiagonal matrix in the form of arises in the linear system for evaluating the coefficients of the piecewise cubic polynomials, where , and (see Revesz, 2014).

In econometrics, the stationary first order autoregression, AR(1), is defined as

where is a constant, and is a white noise process with zero mean and variance . If , the inverse covariance matrix of is , where , and . The covariance matrix of the AR(1) and hence the closed form of is well-known (Nerlove et al., 1979). However, the AR(1) is often used as building blocks in more complex models as a means of introducing dependence, and deriving the covariance structure in such models becomes a more challenging task.

Consider for instance the conditional autogressive (CAR) model, which is widely used in modeling spatial data (Besag, 1974; Cressie, 1993; Wall, 2004). Let denote the observation at site for and . The CAR model incorporates spatial dependence into the covariance structure by specifying a Gaussian distribution for

where is the mean of , is the conditional variance and is a covariance parameter. Let , and . Then , where

It is common to write , where is a spatial dependence parameter and represents the neighborhood structure of the sites. If the adjacency structure of a path graph is adopted and the rows of are restricted to sum to 1, then is a tridiagonal matrix with a zero diagonal, superdiagonal and subdiagonal . For the CAR model, must be symmetric, which implies that for some . In addition, for to be positive definite. If , where , and . Muenz (2017) notes that the elements of and hence are of interest for model calibration.

In Section 7, we discuss a reparametrization of the AR(1) plus noise model and use this setting demonstrate how the results derived in this article can be applied in econometrics and statistical modeling.

3 Inverse of tridiagonal matrix

First we introduce Chebyshev polynomials of the second kind, which are defined as solutions to the recurrence equation

| (2) |

with initial conditions and . The solution is of the form

The definition of Chebyshev polynomials of the second kind may be extended to negative indices via for negative , with .

In Lemma 1, we show that the solution of a second order difference equation, which differs from (2) in terms of initial conditions, can be expressed as a linear combination of . Then we present a closed form expression for in Theorem 1.

Definition 1.

If , then , , where is an integer and .

Note that , and . In addition, and are real if and purely imaginary if .

Lemma 1.

Consider the second order difference equation

| (3) |

with initial conditions and . Let . The solution is given by

| (4) |

If , then for .

Proof.

The characteristic equation of the second-order difference equation is and the roots are .

If , the characteristic equation has a single root and the general solution is . Applying the initial conditions, we obtain and . Thus for .

If , there are two distinct roots and the general solution is . Since , we have from the initial conditions,

Thus, for ,

If , the roots are real. Let . Then and so that

If , the roots are complex and where . Thus

Since and , it follows from the general solution that . ∎

The proof of the result in (4) can be simplified by noting that is a primary solution of (3), and hence (4) is also a solution of (3). See Theorem 3.1 of Aharonov et al. (2005) and Encinas and Jiménez (2018c). Thus it suffices to show that (4) satisfies the initial conditions and . However, we have presented a constructive proof based on the characteristic equation of the second order difference equation as we wanted to introduce the terms and , and to show that when . These results will be important in the rest of the article.

Theorem 1.

Suppose is a tridiagonal matrix of form (1) where or , and . Then exists if and only if . If exists, then it is symmetric and for , where

| (5) |

Proof.

We present below some corollaries of Theorem 2 and some properties of , , and which will be useful later.

Corollary 1.

If ,

Thus does not exist if or .

Proof.

From Lemma 1, if , for . and is undefined if the denominator is zero. ∎

Corollary 2.

If , for where

Corollary 3.

For , .

Property 1.

If and , the sequence is positive and strictly increasing. That is, . In addition, is positive.

Proof.

First we show that for . We have . If , then for . By induction, for . Since , we have for . Note that and . ∎

Property 2.

If , and ,

-

(i)

the sequence is positive and strictly increasing,

-

(ii)

the sequence is positive and strictly decreasing,

-

(iii)

all elements of are positive.

Proof.

If , and for . Thus the results (i) and (ii) follow from Property 1. For (iii), we also have for and is symmetric. ∎

Property 3.

If , then for . Thus,

Proof.

Using the recurrence relation for , we have

When , the above equality holds trivially. Hence, for .

4 Row sums of the inverse

In this section, we derive expressions for the row sums of .

Theorem 2.

Let denote the sum of the th row of .

Proof.

We have . If and ,

If and ,

Note that can be evaluated using the result:

| (7) |

Finally if ,

∎

5 Trace of the inverse

In this section, we derive the trace of and . We focus on the case where . These closed expressions are particularly useful as the order of increases. We also present some results on the limiting behavior of and as .

Definition 2.

Let .

Theorem 3.

If ,

Proof.

We have and

As , and . These two sums are equal as the powers in both cases form an arithmetic progression from to with a difference of 2. Finally,

Remark 1.

If , it is straightforward to show that

Corollary 4.

If , then .

Proof.

If , then are real and which implies since . Thus . From Theorem 3, equals

The left term approaches , while the right term goes to zero. ∎

Lemma 2.

Proof.

Since , and ,

∎

Theorem 4.

If , then , where

Proof.

By using the fact that , we have

We have

and

where

The result is then obtained by combining the terms together. ∎

Corollary 5.

If , .

Proof.

6 Bounds for row sums of the inverse

In this section, we focus on the AR(1) plus noise model which is discussed in Section 7 and derive bounds for row sums of . Suppose , and . Let , and . Note that . We first present Lemma 3 before deriving the bound in Theorem 5.

Lemma 3.

For , .

Proof.

First we show that for . Taking into account Corollary 2,

Thus the desired inequality holds for by direct substitution. Applying the inequality in Property 3 (repeatedly),

for . Thus for . By symmetry, this inequality holds for , since . It suffices to show that . Writing , applying the identity of Property 3 and using the fact that ,

∎

Theorem 5.

If ,

If ,

7 Application to AR(1) process with observational noise

Consider a univariate state space model where the observations are noisy and the latent states follow a stationary AR(1) process,

| (8) | ||||

The and sequences are distributed as standard normals, and they are independent of each other and of for all and . Let be the signal-to-noise ratio and be the vector of model parameters, where , , and . This model is called the AR(1) plus noise or ARMA(1,1) model. Pitt and Shephard (1999) and Frühwirth-Schnatter (2004) observe that the convergence rate of the Gibbs sampler, when applied to the AR(1) plus noise model, is dependent on the parametrization. In particular, (8) is known as the centered parametrization as the latent states are centered about and depend on . The noncentered parametrization is given by

| (9) | ||||

where the latent states are now independent of and . These two models are equivalent as the likelihood, , where , obtained upon integrating out the latent states, is the same regardless of the parametrization. As the optimal parametrization is data dependent, Tan (2017) introduced a partially noncentered parametrization,

| (10) | ||||

where . Let and , where is a vector of ones of length . This parametrization includes the centered (, ) and noncentered () parametrizations as special cases. Of interest are the values of the working parameters, and , which optimize the convergence rates of the Gibbs sampler or the expectation-maximization (EM) algorithm, used to fit the AR(1) plus noise model to a time series. Tan (2017) showed that the convergence rate of the EM algorithm is optimized by

| (11) |

if , , are known, and by

| (12) |

if , , are known. An alternating expectation conditional maximization algorithm, which uses these parametrizations in different cycles was then proposed for inferring . In (11), is a tridiagonal matrix, where is of the form in (1) if , with , , and . If , . In (12), and is a tridiagonal matrix with diagonal and off-diagonal elements equal to .

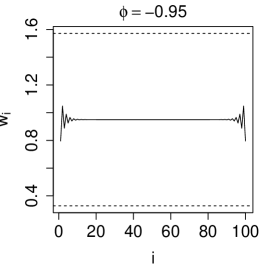

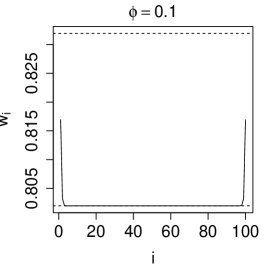

To investigate the behavior of and , such as their bounds, dependence on and and large-sample properties, we require the explicit inverse of and its properties. Suppose we are interested in understanding which parametrization is preferred when inferring given , , . The expression of in (11) involves which represents the row sums of . Hence we can use Theorem 2 to compute the elements in . If ,

From this expression, we observe that is a centrosymmetric vector and depends only on and the signal-to-noise ratio . From Theorem 5, we can easily obtain bounds for . If ,

Thus lies strictly in the interval if . Moreover, (centered parametrization is preferred) as or . If , then

In this case, is positive but not necessarily bounded above by 1. Figure 1 shows the values of and its bounds for some data simulated from the AR(1) plus noise model. We set , , , and . As noted above, is close to zero when , close to one when and it is not bounded above by one when . Note that the signal-to-noise ratio, .

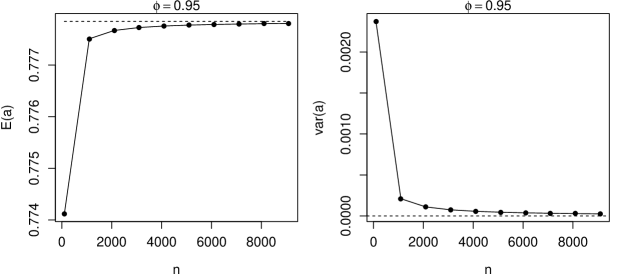

Now consider the value of in (12). The expression of is highly complex and it depends directly on the observations through . As it is difficult to infer the behavior of directly from (12), we attempt to study its large sample properties instead. Tan (2017) showed that the mean and variance of are given by

From Corollary (4),

From Corollary (5), . Hence, we may consider using the limit of as an estimate of when the sample size is large as this limit is more efficient to compute than . Figure 2 shows how the values of and approach their limits as increases when and . The values of and are computed using Theorems 3 and 4, which provide efficient ways to compute the trace of the inverse matrices when is large.

8 Conclusion

In this article, we have derived explicit expressions for the inverse of a class of tridiagonal matrices that often arise in interpolation problems and in statistical models which use first order autoregression to induce dependence in the covariance structure. Such analytic formulas will be important in model estimation and for studying the properties of estimators, such as their bounds or large-sample behavior as illustrated in the application to the AR(1) plus noise model.

9 Acknowledgments

Linda Tan is supported by the start-up grant (R-155-000-190-133). We thank the editor, associate editor and referees for their comments which have helped to improve the manuscript.

References

- Aharonov et al. (2005) Aharonov, D., A. Beardon, and K. Driver (2005). Fibonacci, chebyshev, and orthogonal polynomials. The American Mathematical Monthly 112, 612–630.

- Besag (1974) Besag, J. (1974). Spatial interaction and the statistical analysis of lattice systems. Journal of the Royal Statistical Society. Series B (Methodological) 36, 192–236.

- Cheng and Yueh (2013) Cheng, S. S. and W.-C. Yueh (2013). Inverses of tridiagonal matrices under simple perturbations. Southeast Asian Bulletin of Mathematics 37, 659–681.

- Cressie (1993) Cressie, N. A. C. (1993). Statistics for Spatial Datas. New York: John Wiley & Sons, Inc.

- da Fonseca and Petronilho (2001) da Fonseca, C. and J. Petronilho (2001). Explicit inverses of some tridiagonal matrices. Linear Algebra and its Applications 325, 7–21.

- da Fonseca and Petronilho (2005) da Fonseca, C. and J. Petronilho (2005). Explicit inverse of a tridiagonal k-toeplitz matrix. Numerische Mathematik 100, 457–482.

- El-Mikkawy and Karawia (2006) El-Mikkawy, M. and A. Karawia (2006). Inversion of general tridiagonal matrices. Applied Mathematics Letters 19, 712–720.

- Encinas and Jiménez (2018a) Encinas, A. and M. Jiménez (2018a). Explicit inverse of a tridiagonal (p,r)-toeplitz matrix. Linear Algebra and its Applications 542, 402–421.

- Encinas and Jiménez (2018b) Encinas, A. and M. Jiménez (2018b). Explicit inverse of nonsingular jacobi matrices. ArXiv: 1807.07642.

- Encinas and Jiménez (2018c) Encinas, A. and M. Jiménez (2018c). Second order linear difference equations. Journal of Difference Equations and Applications 24, 305–343.

- Frühwirth-Schnatter (2004) Frühwirth-Schnatter, S. (2004). Efficient Bayesian parameter estimation. In A. Harvey, S. J. Koopman, and N. Shephard (Eds.), State Space and Unobserved Component Models: Theory and Applications, pp. 123–151. Cambridge University Press.

- Hadj and Elouafi (2008) Hadj, A. D. A. and M. Elouafi (2008). A fast numerical algorithm for the inverse of a tridiagonal and pentadiagonal matrix. Applied Mathematics and Computation 202, 441–445.

- Heinig and Rost (1984) Heinig, G. and K. Rost (1984). Algebraic methods for Toeplitz-like matrices and operators. Birkhäuser Basel.

- Huang and McColl (1997) Huang, Y. and W. F. McColl (1997). Analytical inversion of general tridiagonal matrices. Journal of Physics A: Mathematical and General 30, 7919.

- Kılıç (2008) Kılıç, E. (2008). Explicit formula for the inverse of a tridiagonal matrix by backward continued fractions. Applied Mathematics and Computation 197, 345–357.

- Knott (2000) Knott, G. D. (2000). Interpolating Cubic Splines. Boston, MA: Birkhäuser.

- Lewis (1982) Lewis, J. W. (1982). Inversion of tridiagonal matrices. Numerische Mathematik 38, 333–345.

- Mallik (2001) Mallik, R. K. (2001). The inverse of a tridiagonal matrix. Linear Algebra and its Applications 325, 109–139.

- Meurant (1992) Meurant, G. (1992). A review on the inverse of symmetric tridiagonal and block tridiagonal matrices. SIAM Journal on Matrix Analysis and Applications 13, 707–728.

- Muenz (2017) Muenz, D. G. (2017). New Statistical Methods for Phase I Clinical Trials of a Single Agent. Ph. D. thesis, The University of Michigan.

- Nabben (1999a) Nabben, R. (1999a). Decay rates of the inverse of nonsymmetric tridiagonal and band matrices. SIAM Journal on Matrix Analysis and Applications 20, 820–837.

- Nabben (1999b) Nabben, R. (1999b). Two-sided bounds on the inverses of diagonally dominant tridiagonal matrices. Linear Algebra and its Applications 287, 289–305.

- Nerlove et al. (1979) Nerlove, M., D. M. Grether, and J. L. Carvalho (1979). Analysis of Economic Time Series A Synthesis. New York: Academic Press.

- Pitt and Shephard (1999) Pitt, M. K. and N. Shephard (1999). Analytic convergence rates and parameterization issues for the gibbs sampler applied to state space models. Journal of Time Series Analysis 20, 63–85.

- Pozrikidis (2014) Pozrikidis, C. (2014). An Introduction to Grids, Graphs, and Networks. New York: Oxford University Press.

- Ran et al. (2009) Ran, R.-s., T.-z. Huang, X.-p. Liu, and T.-x. Gu (2009). An inversion algorithm for general tridiagonal matrix. Applied Mathematics and Mechanics 30, 247–253.

- Revesz (2014) Revesz, P. Z. (2014). Cubic spline interpolation by solving a recurrence equation instead of a tridiagonal matrix. In N. Mastorakis, P. Revesz, P. M. Pardalos, C. A. Bulucea, and A. Fukasawa (Eds.), Mathematical methods in Science and Engineering (Proceedings of the 1st International Conference on Mathematical Methods & Computational Techniques in Science & Engineering), pp. 21–25.

- Schlegel (1970) Schlegel, P. (1970). The explicit inverse of a tridiagonal matrix. Applied Mathematics and Computation 24, 665.

- Tan (2017) Tan, L. S. L. (2017). Efficient data augmentation techniques for Gaussian state space models. ArXiv: 1712.08887.

- Usmani (1994) Usmani, R. A. (1994). Inversion of a tridiagonal jacobi matrix. Linear Algebra and its Applications 212, 413–414.

- Wall (2004) Wall, M. M. (2004). A close look at the spatial structure implied by the car and sar models. Journal of Statistical Planning and Inference 121, 311–324.

- Yamamoto and Ikebe (1979) Yamamoto, T. and Y. Ikebe (1979). Inversion of band matrices. Linear Algebra and its Applications 24, 105–111.

- Yueh (2006) Yueh, W.-C. (2006). Explicit inverses of several tridiagonal matrices. Applied Mathematics E-Notes 6, 74–83.

- Yueh and Cheng (2008) Yueh, W.-C. and S. S. Cheng (2008). Explicit eigenvalues and inverses of tridiagonal toeplitz matrices with four perturbed corners. The ANZIAM Journal 49, 361–387.