A path integral based model

for stocks and order dynamics

Abstract

We introduce a model for the short-term dynamics of financial assets based on an application to finance of quantum gauge theory, developing ideas of Ilinski. We present a numerical algorithm for the computation of the probability distribution of prices and compare the results with APPLE stocks prices and the S&P500 index.

Dipartimento di Matematica

Politecnico di Milano

piazza Leonardo da Vinci 32, 20133 Milano, Italy

giovanni.paolinelli@polimi.it, gianni.arioli@polimi.it

Keywords: Stock prices, econophysics, path integral, gauge theory, financial markets.

1 Introduction

In [2] Ilinski introduced a model for the short-term dynamics of stocks and orders based on a gauge interpretation of classical finance. A similar approach has been developed in [10, 11, 12], where a model based on quantum field theory has been developed. The approach to the financial mathematical problems with the quantum mechanics is called quantum finance. In the last 20 years, the path integral approach to quantum mechanics introduced by Feynman [15] has turned out to be particularly suitable for financial applications, see also [4, 5, 6, 7, 8, 9]. We further analyse and extend these ideas and develop a model that provides results in good agreement with real market data.

Ilinski’s model describes the amount of cash and share in the portfolio and all possible trading configurations, and in particular the impact of the orders in the stocks dynamics. Quantum mechanics plays a fundamental role in providing a robust mathematical background to describe the fundamental ideas of this theory. In particular, the discrete nature of the portfolio, characterized by an integer number of stock and cash is modelled by the coherent-state path-integral. We generalize this model and introduce an algorithm to compute the coherent-state path-integral proposed by Ilinski.

The model is tested against data of APPLE stocks and the S&P500 index with a time step of one minute; the agreement between real data and the model covers four orders of magnitude. In particular we get a good fit also of the fat-tails.

It is interesting to observe that the fat tails phenomenon can be seen as an effect of the orders. We point out that the shape of the tails has a significant impact on the risk-free rate. More precisely, in [13] it is shown that the rate of return of an investment with no risk of financial loss and the term premium, i.e. the compensation that investors require for bearing the risk that short-term Treasury yields do not evolve as they expected, are miscomputed if the fat tails are ignored.

We show a direct relationship between the kurtosis of the PDF and the strength of the perturbation caused by the orders; in fact, the model without orders provides results equivalent to the Geometric Brownian Motion.

2 A simpler model

We present in this section the basic concepts of Ilinski’s theory; the reader interested in a detailed explanation should refer to [1] and [2].

Ilinski’s starting point is the basic idea that it is not possible to earn money without risk; if this were the case, then we would have an arbitrage opportunity. Consider an elementary market model where it is possible to buy a non-risky asset and a risky asset with the same initial value. If we assume temporarily that is not a risky asset, then after a time the final values of and must to be equal. Otherwise it would be possible to perform an arbitrage operation; that is, we could borrow and sell the under-performing asset, and then use the capital obtained to buy the over-performing one. When we sell the over-performing asset we have enough money to buy back the under-performing asset and also have some money left, the arbitrage revenue. This situation does not occur in the reality since we cannot know the value at a future time of , i.e., we do not know in advance whether is the under- or the over-performing asset. This implies that a revenue from the previous situation can only be achieved with some amount of risk.

In [2] Ilinski shows a strategy involving stocks and cash which generates a positive revenue independently of the final value of the risky asset . Such strategy is called arbitrage. In classical finance such amount is assumed to be zero. Ilinski proposes a weaker assumption, which entails a minimization of the arbitrage.

Denote by the gain of the arbitrage described above; in Ilinski’s model this quantity is treated as the action in a Lagrangian description of the dynamics of the system. We assume that the probability associated to is given by

| (1) |

This assumption represents the main link with the quantum mechanics and with path integrals in particular. The core idea in the path integral representation of quantum mechanics consists in the fact that all trajectories are considered, but those achieving a lower action are more probable. In Ilinski’s financial model the least action ( in quantum mechanics) corresponds to zero arbitrage. Trajectories with small arbitrage (quantum fluctuations) are considered, but their probability decreases when they get farther apart from the zero arbitrage trajectory. The role of Plank’s constant is played by the variance of the financial asset.

We also assume that the stock dynamics is invariant under the change of the currency. This concept is well known in physics as gauge-invariance. We require our theory not to depend of the choice of the numeraire for any asset at any moment of the time. Agents do not start to behave in a different way because they are dealing with 100 pence instead of 1 or the equivalent amount of money in . This invariance must be encoded in all quantities described in this theory. We assume that the probability of a certain amount of arbitrage does not change if the assets are expressed in a different currency.

In physics, the equations that describe the system in a gauge theory are invariant under the transformation induced by the action of a group, either local or global. If we want to denote 10 in , i.e, perform a change of gauge, we have to multiply the capital by a positive number which is the conversion ratio; the previous number is an element of the gauge group. This is true for all possible currency conversions, therefore the gauge group in this context is the multiplicative .

Ilinski uses the previous framework to obtain the conditional probability for the stock price. He considers a discrete time model, where time takes the values for some , and then the price of an asset is denoted by , . Denote by the price at time and the final price at time ; Ilinski proves that:

| (2) |

where

is the revenue at time of the double arbitrage and the constants and represent the interest rates respectively of the cash and of the risky asset. The exponential is the probability described in , whereas is the variance of the prices of the risky asset. Note that the values are gauge invariant.

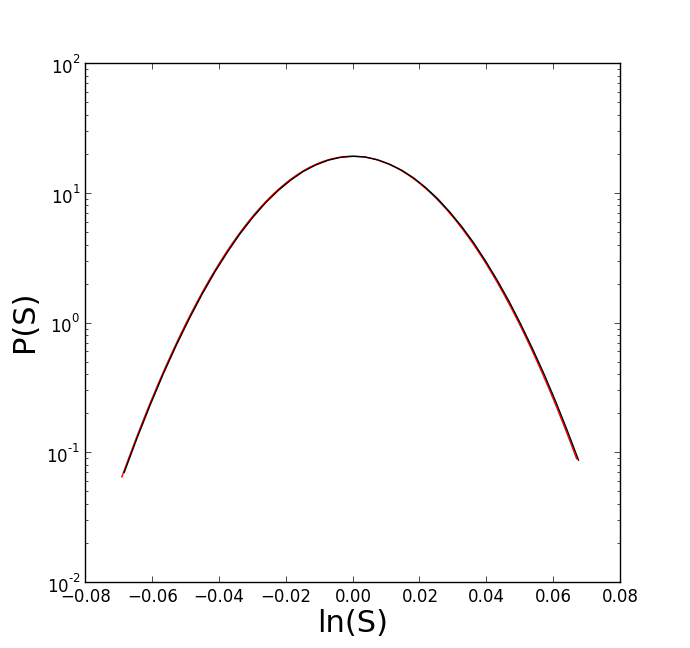

The product of differentials is the path space differential used to sum all over the possible trajectories from to ; details about this concept can be found in [16]. The measure is the gauge invariant expression . In [2], Ilinski proves that (2) results in a normal PDF. Figure 1 shows the result of a numerical simulation that corroborates such result.

3 The model with orders

In [2] Ilinski also introduces a generalization of the previous model consisting in the addition of a perturbation which takes into account the effect of the orders in the stocks dynamics. In this paper we show that a modified perturbation generates a leptokurtic probability distribution of the returns.

Ilinski adds to the action a term which describes the dynamics of the orders, so that the price goes up (down) when somebody buys (sells) the stock. The action is given by

| (3) |

The derivation can be found in [2].

The terms represent the net amount of the orders at time , its value is positive if the net amount is a buy order, negative otherwise, while represents the share liquidity.

The initial allocation of the portfolio is described by the pair which represents the amounts of cash and share at the initial time; the final allocation is denoted by . Because of the gauge invariance, we can express the share and money values in the same unit, so that a unit of cash can be traded for a share.

We assume the closed environment hypothesis, which implies a constant amount of lots at all times; denoting by the total number of traded lots (both money and shares) we have . In this context the initial configuration of the system is the capital allocation ; at each time step , the system evolves to the capital allocation up to time , where it achieves the final allocation . In order to consider the effect of the orders on the price dynamics, it is necessary to compute all the possible paths in the capital allocation space and add the effect of each path.

This computation is achieved with the Coherent State Path Integral (CSPI), see [2, 16, 17]. The numbers are integers, and in the context of the CSPI they are described as

where are complex numbers, corresponding to the creation/annihilation operators.

We denote an order via the operators. Buying stocks we lose units of cash, and vice versa. We have:

Where the symbol stands for the forward different quotient, i.e.,

with equal to the minimal time frame.

The dynamics of the variables is described by a Hamiltonian

which links to . The following expression is derived in [2]:

| (4) |

Here is the relative cost of the transaction; is the time step of the model in the Hamiltonian dynamics and denotes the amplitude of the price variations.

In our simulations we assume and . Given the Hamiltonian, we compute the propagator:

| (5) | ||||

The quantity inside the first square bracket corresponds to

| (6) |

Substituting and in we obtain:

| (7) |

We introduce the hydrodynamical variables

| (8) |

where and . Note that, because of the close environment assumption, and then .

We write in the hydrodynamical variables. Starting from

| (9) |

if we assume

then (9) becomes:

recalling the definition of the forward difference quotient, we obtain:

recalling that

we get

| (10) |

where the conservation law has been used.

We also have

| (11) |

Using the equation and in we obtain the formula for the propagator:

The previous propagator depends on all possible paths in the portfolio space; in order to obtain the conditional probability we need to link it with the price dynamics using . We can write as:

| (12) |

so that equation becomes

We consider now the propagator above together with the stock price action , and we obtain the new propagator which takes into account both the trajectories in the spaces of portfolio allocation and the stock prices.

with:

We note that the coherent states at initial and final times are not integrated in the previous formula.

By the quantum mechanics formalism, the conditional probability is given by

where:

With some computations explained in [2]111 pg.s. 136, 166 and 277-281, we obtain the formula

| (13) | ||||

where:

The previous integral is expressed in the coherent state variables, which means that in order to compute it, we need to transform the whole expression in the hydrodynamical variables; Note that, as in quantum mechanics, the result of the integral is a complex number, while the probability is its module squared. We keep Ilinski’s notation to simplify the comparison with his theory.

The previous formula allows us to compute the probability density function of the final price with a final portfolio allocation , given the initial price and the portfolio allocation . Due to gauge-invariance, we can choose . This is the choice we make in all simulations.

4 The numerical integration

The numerical simulation requires the computation of the approximate value of an integral in high dimension. We provide here a brief description of the strategy for the numerical integration. We first note that the integral involves four variables for each time step:

The first three variables describe the orders dynamics; we denote the space of these variables the hydrodynamical space. The last variable is the stock price.

The algorithm first selects a particular configuration in the hydrodynamical space, which corresponds to a particular trading pattern, then it samples the associated stock price variables with the Metropolis-Hastings algorithm, which is a Markov chain Monte Carlo method, using the potential

The sampled values are then used to compute the integral . Details about the Metropolis-Hastings algorithm can be found in [18]. We recall that the following assumption have been introduced:

-

•

,

-

•

tc=0

-

•

=2.5,

-

•

M=====100.

The first assumption is not restrictive, and makes the results more transparent. The second one consists in neglecting transaction costs, but we point out that these could be easily introduced in the model. We choose as in [2], observing that a different value of does not change the qualitative behaviour of the model. Indeed, the Hamiltonian is invariant under the transformation

and such invariance can be used to eliminate .

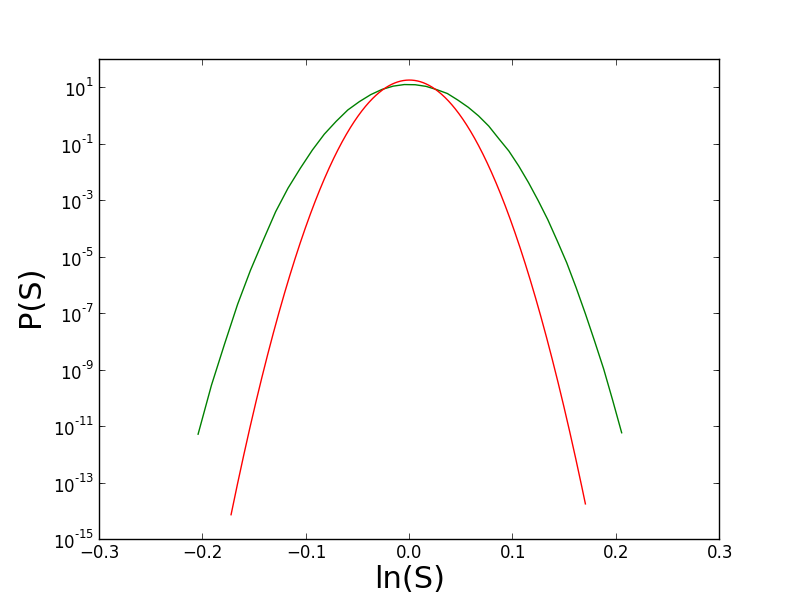

The final assumption is chosen as a compromise between the computational complexity and the accuracy; simulations performed with higher values of show similar results. The dynamics of the model is a perturbed Geometric Brownian Motion, the perturbation being proportional to the parameter . The parameters of the Brownian Motion are the same of the simulation discussed above. The results of simulations are shown in logarithmic scale in Figures 2 and 3.

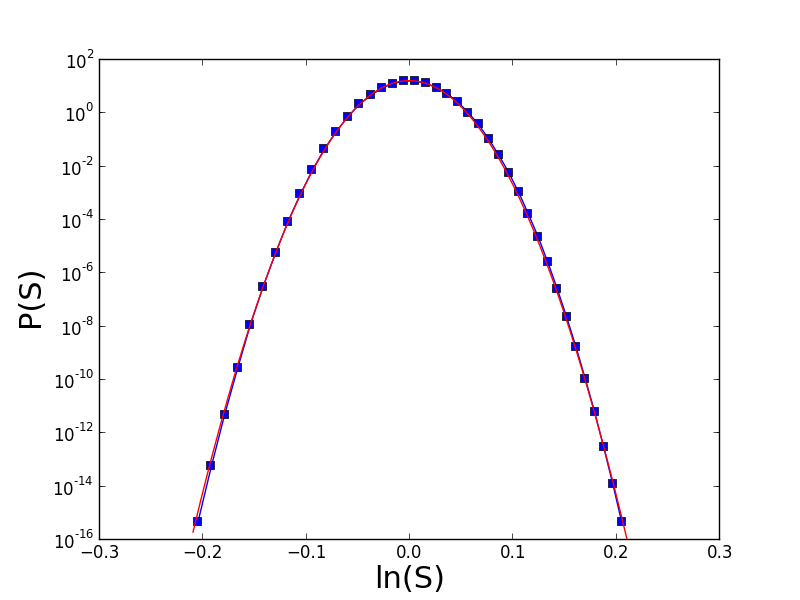

It turns out that this perturbation only causes an increase of the variance . This can be observed in Figure 4, where the PDF of the model without orders, with and (red continuous line), and a normal distribution with variance (blue line with squares) are shown.

The numerical computation of the mean, variance and kurtosis of the simulated probability density function shows that the previous values are equal to those corresponding to the Geometric Brownian Motion with , within of 0.001%.

This poor match with financial data is also confirmed by Ilinski in [2], where he writes that “this strategy is far from optimal”.

5 The generalized model

Ilinski suggests a second kind of perturbation

and he computes the probability distribution of with the saddle point method and other approximations in the case . The probability distribution displayed in [2, p. 148, Fig. 6.15] is very accurate in the central part, but it behaves badly in the deep tails. If we analyse the probability density function derived by Ilinski’s model, we note that its wings exhibit a linear relationship between and .

This behaviour is not in good agreement with the stocks dynamics. The overlap between the computed and observed probability density functions is not very accurate in the wings region. In particular we can see that the relation between and showed in the PDF is of polynomial type; i.e,

We propose a different perturbation: Ilinski’s action

depends linearly on the differences . We introduce the action

where and are integers.

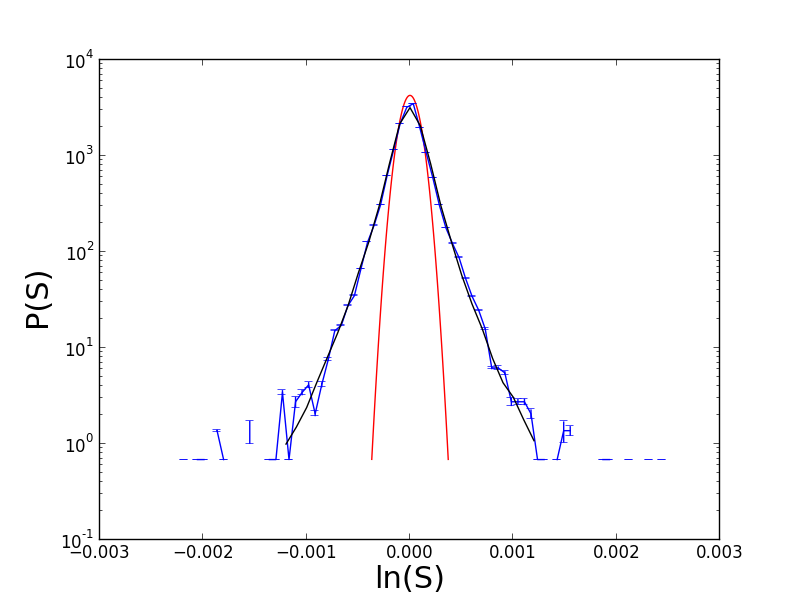

We keep small to avoid to overfit the data; it turns out that this perturbation with provides results in good agreement with all the real data that we analysed. Still, at first we present a result with and i.e.

The result of the numerical simulation is displayed in Figure 5, which shows the leptokurtic behaviour

We present some comparisons between real data and our model. The source of the real data consists in 3 months price-sheets of the S&P500 index and APPLE stocks from 01/05/2017 to 26/07/2017. The sampling frequency is ; each dataset consists of about 25000 prices. In order to obtain the probability density function associated to the index and the stock, we follow the method introduced in reference [14], i.e. we consider a set of historical data as instances of a stochastic variable. We first compute by

then we build a histogram of the values with bins. The histograms shown in Figure and 9 display the number of counts in each histogram bin, divided by the bin width . The result is then normalized in order to approximate a probability density function.

The error bars for the real data are estimated as ; where is the width of the histogram -bars. In order to compare the simulations with the results obtained in [2, 3, 10], we plot the probability density functions in logarithmic scale.

We plot the results of some simulations performed with the intent to reproduce real data. Here we did not plot the simulation errors in order to keep the pictures as clear as possible; such errors have been estimated and they are within .

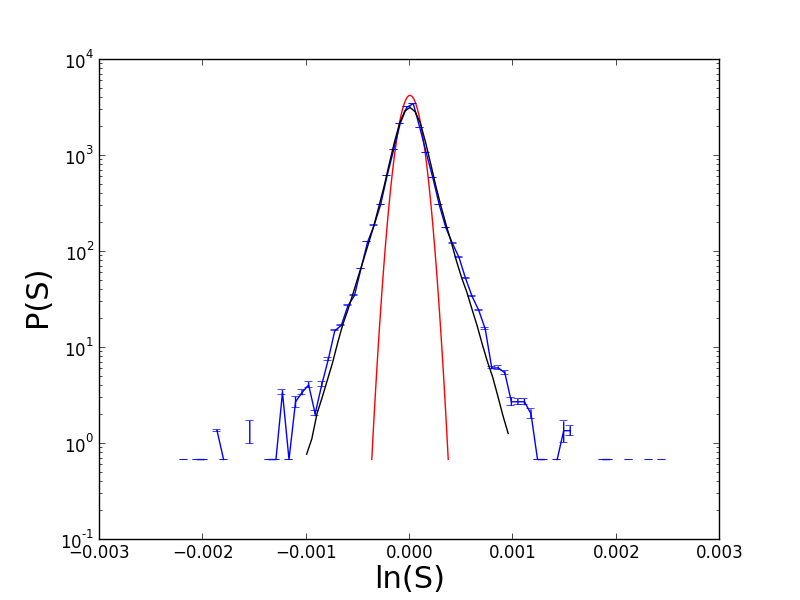

The picture show in blue the empirical distributions of SP500 index; the black curves represent the results of the simulations with the generalized model.

The red curves represent the normal distribution with the same and ;

The agreement is quite good in a very wide region near the central price 222.; yet in the tails, the model underestimates the value of the probability density function. This behaviour concerns the simulations of both the indices and the Apple stock.

, , , and .

This can be explained by the absence of large jumps in the simulation, i.e., our model produces a smaller amount of big price variations than the real market. The agreement between simulations and real data can be improved with an extra term. Heuristically, we observe that the addition of a higher degree term creates a more intense perturbation when . For the APPLE share and S&P500 index two different kinds of perturbations are used:

The numerical simulations associated with the previous perturbations give the following results:

, , , , and .

, , and , and .

The measure that we used to quantify the agreement between real data and the simulations is the overlap amplitude between the numerical and real data probability density functions in the y-axes. For example if the overlap spans from the point up to the point on the y-axis, we claim that the agreement is of one and half order of magnitude. We choose this particular measure because it has been used in the references we use as benchmarks.

One of the first attempt to reproduce the probability density function of a real asset with a stochastic process is [3]. The authors prove that it is possible to obtain an agreement of almost three orders of magnitude with a Lévy flight for the S&P index with = 1 min. Better results have been achieved in [10] by Dupoyet and Fiebig using a quantum lattice model which reproduces the probability density function of NSDAQ index with an agreement about four orders of magnitude with the same . Albeit [10] is a considerable improvement over [3], it suffers of the same problem of Ilinski’s, that is, it underestimates the probabilities of large market corrections.

Our model fits the APPLE stock and S&P index probability density functions with an agreement of almost four order of magnitude, and in particular, when compared with the other models mentioned above, it provides a good fit or the distributions in the deep tails region.

6 Tables and statistical analysis

We provide a quantitative relationship between the statistical properties of the simulations and the parameters values. Two tables are presented with different values of and ; in the first line we write the parameters associated to a GBM with the same and of the generalized model. From the tables it is possible to infer a direct relationship between the strength of the perturbation and the value of . The greatest differences between the two models can be seen in the last lines of the table, where , i.e., where the perturbation generated by is stronger. The estimate of the parameters is obtained by the classical formula

where stands for the probability density function of the variable and is its mean.

The error in the variance, kurtosis and the other moments is estimated computing times the probability density function and then evaluating for each result the parameters. The values written are the mean and standard deviation computed over the previous results.

![[Uncaptioned image]](/html/1803.07904/assets/FirstTable1.png)

| Variance | Kurtosis | 6th-Moment | 8th-Moment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GBM | 3.93 e-8 | 3.00 | 9.19 e-22 | 2.53 e-28 | ||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

![[Uncaptioned image]](/html/1803.07904/assets/SecondTable1.png)

| Variance | Kurtosis | 6th-Moment | 8th-Moment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GBM | 3.93 e-8 | 3.00 | 9.19 e-22 | 2.53 e-28 | ||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

It is also important to note that the values are proportional to . In the first generalized model simulation , which is equal to the real data cases . This is clear if we observe the whole action

In the Metropolis-Hastings algorithm, in order to obtain a mixing ratio of , the fluctuations are proportional to , while is always distributed in , i.e.,

In order to perturb in a proper way the price variation we need

therefore a change in the order of magnitude of must correspond to a similar change in the parameters and .

7 Interpretation of the generalized model

The terms introduced above allow us to obtain a good agreement between the simulated and the real PDF. In this section we provide a financial interpretation of such quantities. Given the perturbation

we observe that

-

•

affects the jumps size,

-

•

affects the probability of the jumps.

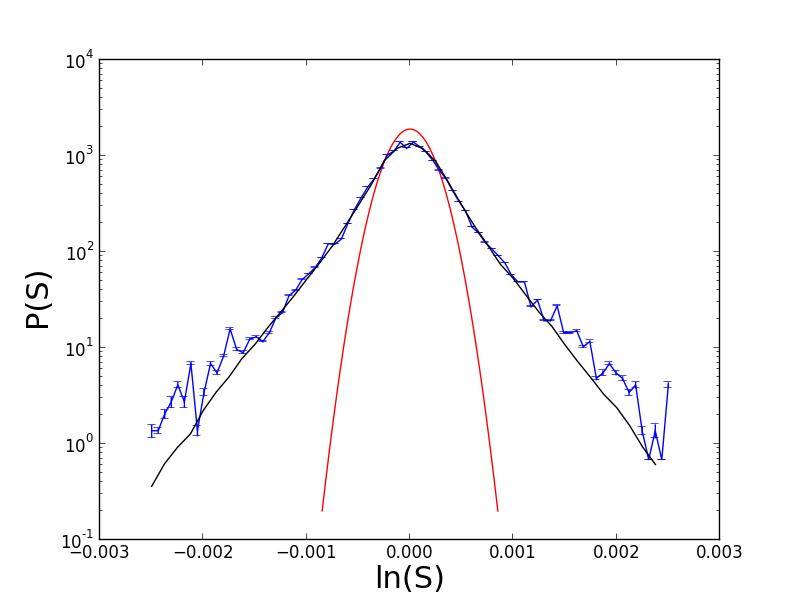

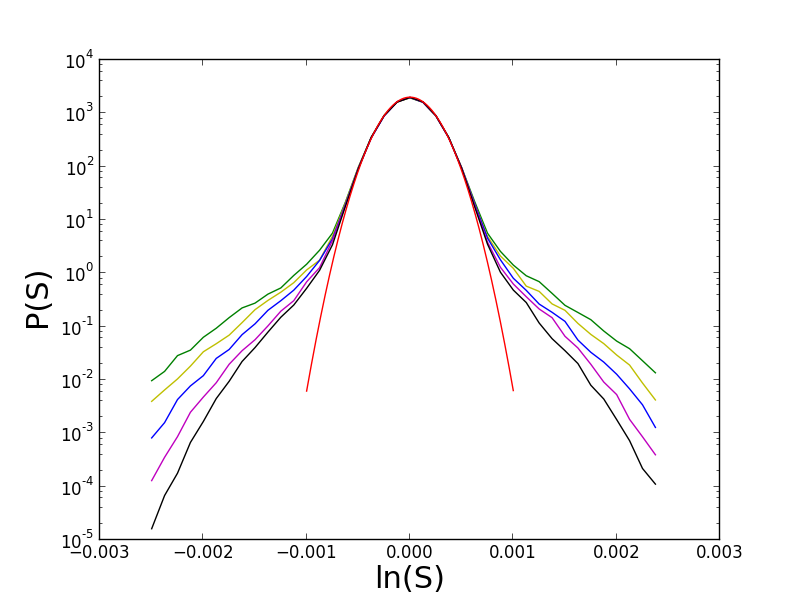

We consider first. Figure 10 shows the result of a single perturbed model with different values of and fixed .

=5 -blue-, 7 -green-, 9 -yellow-, 11 -purple- and 13 -black-.

The red curve represents the normal distribution with the same .

The Geometric Brownian Motion yields a mesokurtic probability density function and all the trajectories simulated with this model have a continuous path. However, it is possible to obtain big fluctuations between the initial price and the final price by setting a large variance . Increasing does not affect the trajectory continuity, since the model remains a GBM. The price fluctuations are directly linked with the variance ; but the continuity is not affected by the value of this parameter. These facts suggest an interpretation of as the frequency of the orders with small spread . A larger value of corresponds to a larger number of orders per unit time, yielding a larger price fluctuation. Since we are considering small variations, continuity is preserved.

This model is too simple for a real market description; in particular some massive price corrections may happen in a unit time frame. This events are called jumps.

In the real financial context, massive price corrections appear when there is an external change in the macroeconomic scenario; when this happens, the original price may be greatly underestimated or overestimated. In the previous situation the orders given immediately after the macroeconomic change will have a large spread .

Within this framework, large price corrections are more likely; which implies that the tails of the PDF are fatter. Given a model which allows only jumps with , the probability of a price change where , it is equal to the case without jumps. Instead, if the probability will be much higher with respect the jumps-less case.

Denoting as the price where the wings start to exhibit their presence, we can observe that it is proportional to . In fact we note that the overlap between the normal distribution and the black line, with , is longer with respect to the overlap of the blue line, with ; moreover all the price variations y are more likely to happen with respect to the Geometric Brownian Motion model. This is in agreement with our interpretation on .

We also recall that the perturbation with is equal to a Geometric Brownian Motion with increased ; suggesting again that is related with jumps size present in the model.

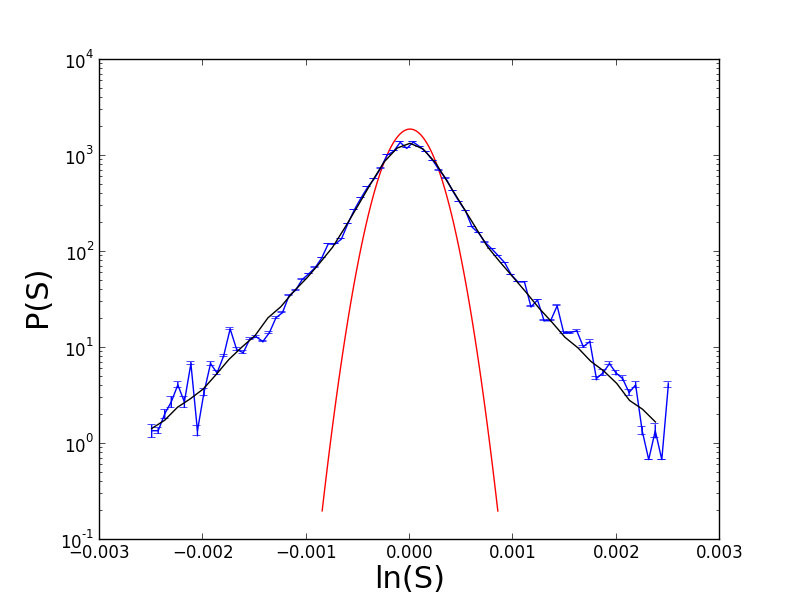

To consider the effect of , we show the results of a simulation with the perturbation and different values of in Figure 11.

0.00181 -green-, 0.00158 -yellow-, 0.00140 -blue-, 0.00126 -purple- and 0.00114 -black-.

The previous simulation, along with the previous tables, shows that the kurtosis and higher even moments of the distribution are directly linked with the value of .

The mass under the tails quantify the presence of massive price variation, occurring in presence of jumps; which means that the probability associated to this variations is directly related with the jumps probability. This shows the relation between jumps and the shape of the tails.

References

- [1] K. Ilinski, Physics of Finance, http://lanl.arxiv.org/abs/hep-th/9710148

- [2] K. Ilinski, Physics of Finance: Gauge Modelling in Non-equilibrium Pricing, Wiley 2001

- [3] R. N. Mantegna and H. E. Stanley, Scaling Behaviour in the Dynamics of Economic Index, Letters to Nature 06/07/1995, 376, 46-49

- [4] B.E. Baaquie, Quantum Finance Path Integrals and Hamiltonians for Options and Interest rates, Cambridge University Press, 2004.

- [5] B.E. Baaquie, Interest Rates and Coupon Bonds in Quantum Finance, Cambridge University Press, 2009.

- [6] G. Montagna, O. Nicrosini, N. Moreni, A path integral way to option pricing, Physica A 310 (2002) 450-466

- [7] G. Montagna, M. Morelli, O. Nicrosini, P. Amato, M. Farina Pricing derivatives by path integral and neural networks, Physica A 324, 189-195, (2003)

- [8] G Bormetti, G Montagna, N Moreni, O Nicrosini, Pricing Exotic Options in a Path Integral Approach, Quantitative Finance 6, 1, 55-66 (2006)

- [9] J.P.A. Devreese, D. Lemmens, J. Tempere, Path integral approach to Asian options in the Black-Scholes model, Physica A 389, 780-788 (2010)

- [10] B. Dupoyet, H.R. Fiebig, D.P. Musgrove, Gauge invariant lattice quantum field theory: Implications for statistical properties of high frequency financial markets, Physica A 389 (2010) 107-116.

- [11] B. Dupoyet, H.R. Fiebig, D.P. Musgrove, Replicating financial market dynamics with a simple self-organized critical lattice model, Physica A 390 (2011) 3120-3135.

- [12] B. Dupoyet, H.R. Fiebig, D.P. Musgrove, Arbitrage-free self-organizing markets with GARCH properties: Generating them in the lab with a lattice model, Physica A 391 (2012) 4350-4363.

- [13] P. Bidarkota, B. Dupoyet, The impact of fat tails on equilibrium rates of return and term premia , Journal of Economic Dynamics and Control 31 (2007) 887-905

- [14] L.Bachelier, Théorie de la Spéculation, Annales Scientifiques de l’École Normale Supérieure 3 (17) (1900) 21-86.

- [15] R. P. Feynman, Space-time approach to non-relativistic quantum mechanics, Rev. Mod. Phys. 20, 367-387 (1948)

- [16] R. P. Feynman, Quantum Mechanics and Path Integrals, Dover, 2010.

- [17] E. Fradkin, Field Theories of Condensed Matter, Cambridge University Press, 2013.

- [18] N.Metropolis, A. Rosenbluth, M. Rosenbluth, A. Teller, E. Teller, Equation of state calculation by fast computing machine, Journal of Chemical Physics 21 (6) 1087-1092 (1953)