Two-stage approaches to the analysis of occupancy data II. The heterogeneous model and conditional likelihood

Abstract

Occupancy models involve both the probability a site is occupied and the probability occupancy is detected. The homogeneous occupancy model, where the occupancy and detection probabilities are the same at each site, admits an orthogonal parameter transformation that yields a two-stage process to calculate the maximum likelihood estimates so that it is not necessary to simultaneously estimate the occupancy and detection probabilities. The two-stage approach is examined here for the heterogeneous occupancy model where the occupancy and detection probabilities now depend on covariates that may vary between sites and over time. There is no longer an orthogonal transformation but this approach effectively reduces the parameter space and allows fuller use of the R functionality. This permits use of existing vector generalised linear models methods to fit models for detection and allows the development of an iterative weighted least squares approach to fit models for occupancy. Efficiency is examined in a simulation study and the full maximum likelihood and two-stage approaches are compared on several data sets.111Software appears as annexes in the electronic version of this manuscript.

keywords:

Imperfect detection , Occupancy models, Covariates, Conditional likelihood.1 Introduction

Occupancy models were introduced in MacKenzie et al., (2002). They model the probability a site is occupied and the probability that occupancy is detected. We assume here that occupancy of a site is permanent over the observation period. Data are collected over repeated visits to a number of sites and consist of observations on whether occupancy is detected. It is common that both the occupancy and detection probabilities are modelled in terms of covariates, which can be time varying. Occupancy is related to time independent site covariates and detection can be related to both these site covariates and the time varying covariates. Thus modelling detection can be more complex than modelling occupancy.

Occupancy models are currently fitted to data using the full likelihood where the parameters associated with occupancy and detection are simultaneously estimated. The likelihood may be maximised numerically using the R Development Core Team, (2018) package unmarked (Fiske and Chandler,, 2015) for example. We have observed that the full likelihood can be numerically unstable. This is distinct from boundary solutions that occur in occupancy models, as noted in Wintle et al., (2004); Guillera-Arroita et al., (2010); Karavarsamis et al., (2013); Hutchinson et al., 2015b . Without constraints, the full likelihood may not converge, may give local maxima, or give estimates beyond the boundaries of the parameter space. Using the common logit transformation can still give estimated probabilities that are effectively zero or one. We examine this in simulations in Section 4 where it is seen that maximum likelihood can give extreme estimates of occupancy parameters when the two-stage approach does not.

Bayesian methods have been developed to estimate occupancy and detectability, for example Milne et al., (1989); Lunn et al., (2000); Wintle et al., (2003); MacKenzie et al., (2006); Gimenez et al., (2007); Royle and Dorazio, (2008); Gimenez et al., (2009); MacKenzie et al., (2009); Fiske and Chandler, (2011); Martin et al., (2011); Aing et al., (2011); Hui et al., (2011). An empirical Bayes method is known but this can underestimate the variance of the posterior distribution (Royle and Dorazio,, 2008; Fiske and Chandler,, 2011). Penalized likelihood methods for occupancy have also been developed to help overcome the numerical instability of the maximum likelihood estimators (Moreno and Lele,, 2010; Hutchinson et al., 2015b, ). These may be fitted using the occuPEN and occuPEN_CV functions in unmarked package. In our two-stage approach we address potential instability by considering detection and occupancy separately. This allows us to compute the estimates over two lower dimension parameter spaces. Moreover, the more complex modelling of the effect of time dependent covariates on the detection probabilities is relatively straightforward in the two-stage approach.

To help stabilise the numerical optimization algorithm the package unmarked (see p. 2 of the R vignette Fiske and Chandler, (2015)222cran.at.r-project.org/web/packages/unmarked/vignettes/unmarked.pdf) recommends that covariates be standardized. However, as observed in the documentation for the unmarked package, standardizing may cause problems with standard R functions, such as predict. The smartpred package may solve some issues but not in all instances of data dependent parameters. Moreover, there is no guarantee that users will standardise their data. In addition, the choice of algorithm for the numerical maximisation may be changed in optim, however this may be sensitive to the algorithm used.

Recently Karavarsamis and Huggins, (2017) showed that for the homogeneous occupancy model a simple transformation yielded orthogonal parameters resulting in a two-stage estimation procedure that simplified the computation of the estimates. We see in Section 3 that this no longer holds for heterogeneous models. Following the homogeneous case, a conditional likelihood is used to estimate detection probabilities which is the first stage of the analysis. This may be implemented using the vglm function in the VGAM package in R (Yee,, 2010, 2015; Yee et al.,, 2015). In the second stage, the remaining partial likelihood, evaluated at the estimated detection probabilities from the first stage, is used to estimate the occupancy probabilities. This effectively reduces the parameter space and allows the use of vector generalized linear model methods to fit models for detection. The partial likelihood for occupancy may be maximised using several numerical methods, here we implement this using an iterative weighted least squares (IWLS) approach.

Our notation is given and the full likelihood is examined in Section 2. In Section 3 we describe the two-stage approach. In the first stage in Section 3.1 we use conditional likelihood to estimate the detection probabilities, with time independent detection probabilities discussed in Section 3.1.1 and time dependent detection probabilities considered in Section 3.1.2. In the second stage in Section 3.2 we introduce a partial likelihood approach to estimate the occupancy probabilities using the detection probabilities estimated in the first stage. In Section 3.2.1 we give an IWLS algorithm to compute the occupancy estimates. A simulation study is conducted in Section 4 and the methods are applied to several data sets in Section 5. Some discussion is given in Section 6. Some technical derivations and the implementation of vglm in this setting are given in the appendices.

2 Notation and Full Likelihood

Consider sites labelled and occasions at each site where the presence of a species may be observed. We suppose that occupancy is constant over the observation period. Let be the probability that site is occupied and be the probability the species is observed at site on visit given it is present at site . Then is the probability of at least one detection at site given the site is occupied. If there is no dependence on the visit then and . Let take the value 1 if an individual was detected at site on occasion and zero otherwise. Let denote the number of occasions upon which the species was detected at site . We let be the indicator of no detections at site . Reorder the sites , where denote the sites at which at least one detection occurred and the remainder sites at which no sightings occurred.

It is common for covariates that may be related to detection or occupancy to be associated with each site. Suppose that where is a vector of covariates associated with site and is a vector of coefficients. Let be the probability of detection at site on occasion if site is occupied. We take where is a vector of covariates associated with site on occasion , and let , for site and time dependent detection. For time independent detection probabilities, we write , , for a possibly different vector of covariates to that above and with corresponding coefficient vector . In most applications will be the logistic function . Let in the time dependent case and otherwise.

The contribution to the full likelihood of site , can be written as

| (1) |

The full likelihood is based on maximising the product of (1) over all the sites. Let

be the contribution of site to the log-likelihood. Then, assuming sites are independent, the full log-likelihood is .

3 The Two-Stage Approach

Following the homogeneous case of Karavarsamis and Huggins, (2017) an alternate approach is to let () be the unconditional probability the species is detected at site . Then we may write the contribution of site to the full likelihood, (1), as

| (2) |

The partial likelihood component is a Bernoulli likelihood corresponding to the detection of the species at site and the partial component is the conditional likelihood of given at least one detection at the site. The contribution of site to the log-likelihood is then

| (3) | ||||

| (4) |

Our interest is in exploiting the decomposition (2) to simplify the calculations for complex models. To achieve this, we use (4) to estimate in the first stage of the estimation process. Let be the resulting conditional likelihood estimator of , and denote its large sample variance by . In the second stage, let be the fitted value of and the fitted value of . We then replace by in the log-partial likelihood (3) and maximise this to estimate .

From (4) the conditional likelihood estimator of arises from solving

| (5) |

Rather than solving (5) the maximum likelihood estimators of arise from solving

Thus unlike the simple homogeneous model considered in Karavarsamis and Huggins, (2017) the conditional likelihood estimators will not be the mle’s.

3.1 Stage 1: Estimating the Detection Probabilities

For the homogeneous model Karavarsamis and Huggins, (2017) included in their supplementary materials a plot of the estimated occupancy probability against values of the detection probability. This plot suggests that the occupancy probability is relatively insensitive to small changes in the detection probability. Thus modelling the detection probability may not be crucial. However, particularly if there are big changes in the detection probabilities between visits, correct modelling will be expected to improve the estimates and may be of interest independent to .

3.1.1 Time Independent Detection Probabilities

This is the simplest case, apart from constant detection probability. In this case and the conditional likelihood reduces to

which is a function of the number of detections at each site where there was at least one detection, i.e. , . This is the conditional likelihood of Huggins, (1989) which may be easily maximised using the VGAM package, with nomenclature similar to that used in generalised linear models (§17.2 Yee,, 2015; Yee et al.,, 2015). See A, A.1 and Section 5 for details and examples.

3.1.2 Time Dependent Detection Probabilities

Recall that in this case we have distinct probabilities , for different visits to site . A simple extension of the time independent model allows an effect of the th visit in the model for . That is, the covariate vector contains an indicator of the visit time. This is modelled by allowing the intercept to vary with the visit, and this is easily implemented in the VGAM package. See A.2 and Section 5. More generally environmental variables such as temperature or the time of day the visit was conducted may vary between visits. When we allow the detection probabilities to depend on time dependent covariates, the conditional likelihood corresponding to a site where occupancy was detected is now

That is, the detections form a sequence of independent Bernoulli trials but we only observe the outcome if there is at least one detection. Again this model can be fitted using the VGAM package. See A.2 for details.

3.2 Stage 2: Estimating Occupancy Probabilities

To estimate we maximise the partial likelihood where, as noted above, and hence has been replaced by its estimator from the first stage . The partial likelihood is . Let , then the log-partial likelihood is

| (6) |

This may be maximised numerically using the optim function in R (referred to as “Partial” in tables). However, there are two other possible approaches.

3.2.1 Iterative Weighted Least Squares

An alternative to this method that is commonly used to compute estimates from generalised linear models is the well known iterative weighted least squares (IWLS) approach. To define this estimator for a logistic model, let the matrix have th column . Let , , . Let be evaluated at . Set and . Let be the estimate at the th step and let . Then the estimate at the th is . The IWLS estimate is obtained by repeating this step until convergence. Details are given in B. An estimate of the expected Fisher information corresponding to the partial likelihood, , is given by .

3.2.2 Iterative Offset

As does not depend on , maximising (6) is equivalent to maximising

where . Let . Then under the logistic model

and has the appearance of an offset. However, it is a function of the linear predictor . This allows an alternative iterative approach.

3.3 Estimating the Standard Errors

We give the asymptotic variances of our occupancy estimators in the linear logistic case. Denote the partial score function by , and . Let be the estimator of arising from solving for a given . We show in C that under mild regularity conditions an estimator of the variance of is

| (7) | ||||

The estimated occupancy probability is , which is easily seen to have the estimated approximate variance .

To compute (7) note that in both the time homogeneous and inhomogeneous cases we have

| (8) |

However, is computed differently. In the time homogeneous case we have

| (9) |

whereas in the time heterogeneous case we have

| (10) |

Then in either case, the expression (7) holds (see C). Note that if and then (9) and (10) are the same. In computing we can replace by its expectation .

4 Simulations

To evaluate the two-stage approach (described in Section 3.2) we used one site covariate for occupancy, an independent site covariate for detection and a further independent single time varying covariate that also varied between sites. These were all taken to have standard normal distributions, reflecting that it is common to standardise the covariates. We took varying parameter values to reflect different mean occupancy and detection probabilities. For each value of and we simulated the covariates once then for varying parameter values simulated occupancy and detection. We first conducted simulations to determine which of the three methods of estimating occupancy performed best. Firstly we conducted simulations to determine which of the methods, IWLS, direct maximisation of the partial likelihood with optim (Partial) or iterative offset (Iterative) to use. Direct maximisation using optim allows different optimization methods, the option BFGS numerical maximisation method is adopted here. Comparison to CG and Nelder-Mead method displayed improved convergence for BFGS. We consider and , , and giving for our simulated covariates an average occupancy probability of 0.70 and an average probability of detection at least once at a site of 0.65. We took 1000 simulations. The results are in Table 1. Efficiencies are computed relative to the partial likelihood and are computed using the usual ratio of the variances (Efficiency) and the ratio of median absolute deviations squared (Efficiency (mad)). Median absolute deviations (mad) are given by mad median , where , is the third quartile of the inverse standard normal distribution, and is the median of . We used the function mad in R to calculate these. The medians showed little bias in any of the methods although when the means were computed, direct maximisation of the partial likelihood (Partial) exhibited considerable bias. The median absolute deviations of the IWLS and Partial methods were similar as is also evident in the efficiencies computed using the mad. With a smaller number of site visits, in Table 2 there is now some evidence of bias in all methods and the IWLS is clearly the most efficient. In this case the average probability of detection at least once at a site was 0.47.

| IWLS | Partial | Iterative | ||||

|---|---|---|---|---|---|---|

| Actual | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Median | 1.02 | 1.00 | 1.02 | 1.00 | 1.02 | 1.01 |

| mad | 0.25 | 0.25 | 0.25 | 0.26 | 0.32 | 0.31 |

| Mean | 1.03 | 1.02 | 1.97 | 1.47 | 1.15 | 1.15 |

| sd | 0.28 | 0.26 | 5.66 | 2.70 | 1.03 | 1.04 |

| Efficiency | 41656.85 | 10910.59 | 3014.89 | 677.40 | ||

| Efficiency(mad) | 100.00 | 107.35 | 61.96 | 67.59 | ||

| IWLS | Partial | Iterative | ||||

|---|---|---|---|---|---|---|

| Actual | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Median | 1.17 | 0.99 | 1.17 | 1.02 | 1.23 | 1.03 |

| mad | 0.57 | 0.24 | 0.62 | 0.31 | 0.68 | 0.54 |

| Mean | 1.17 | 1.05 | 1.34 | 1.15 | 1.81 | 1.67 |

| sd | 0.49 | 0.33 | 0.99 | 0.55 | 2.03 | 1.77 |

| Efficiency | 400.97 | 284.07 | 23.69 | 9.65 | ||

| Efficiency(mad) | 120.18 | 165.64 | 81.85 | 32.49 | ||

Next, we compare the IWLS method for the two-stage approach of estimation of occupancy to the full likelihood of MacKenzie et al., (2002). In Table 3 we consider and . We took 1000 simulations at each parameter combination. With a small number of standardised covariates the MacKenzie maximum likelihood estimators were expected to perform well. These were computed using the occu function in the R package unmarked (see D for a brief description). We report the median and mad of the estimates. With lower detection probabilities occasionally the IWLS algorithm did not converge in 200 iterations. In that case the partial likelihood could be directly maximised. The bias of both procedures was low. As expected the efficiencies of estimating the parameters associated with detection were low. The efficiencies of the two-stage estimator in estimating the occupancy probabilities was good and was generally around 100% for the covariate term, but less that 100% for the intercept. The large efficiencies for smaller occupancy and detection probabilities were due to several unusually large maximum likelihood estimates. Similarly the small efficiencies for smaller detection probabilities but larger occupancy probabilities were due to large values of the two-stage estimates.

| Occupancy | Detection | Occupancy | Detection | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Int | Int | time | Int | Int | time | |||||

| Mean Prob | 0.70 | 0.65 | 0.31 | 0.65 | ||||||

| Actual | 1.00 | 1.00 | -1.50 | -0.50 | -0.50 | -1.00 | 1.00 | -1.50 | -0.50 | -0.50 |

| med two-stage | 1.01 | 1.01 | -1.51 | -0.51 | -0.50 | -0.99 | 1.01 | -1.52 | -0.50 | -0.50 |

| mad two-stage | 0.26 | 0.23 | 0.11 | 0.10 | 0.07 | 0.19 | 0.18 | 0.16 | 0.15 | 0.11 |

| med mle | 1.01 | 1.01 | -1.51 | -0.50 | -0.49 | -0.99 | 1.01 | -1.52 | -0.51 | -0.50 |

| mad mle | 0.25 | 0.23 | 0.09 | 0.07 | 0.07 | 0.18 | 0.18 | 0.14 | 0.11 | 0.10 |

| Efficiency | 90.65 | 101.74 | 66.04 | 52.03 | 93.13 | 93.67 | 99.41 | 69.72 | 54.69 | 91.09 |

| Efficiency(mad) | 91.64 | 98.57 | 70.62 | 54.81 | 94.00 | 93.19 | 102.40 | 73.01 | 49.57 | 96.52 |

| Mean Prob | 0.70 | 0.37 | 0.31 | 0.37 | ||||||

| Actual | 1.00 | 1.00 | -2.50 | -0.50 | -0.50 | -1.00 | 1.00 | -2.50 | -0.50 | -0.50 |

| med two-stage | 1.01 | 0.99 | -2.53 | -0.50 | -0.50 | -0.97 | 1.03 | -2.55 | -0.52 | -0.50 |

| mad two-stage | 0.65 | 0.41 | 0.23 | 0.19 | 0.10 | 0.41 | 0.27 | 0.37 | 0.29 | 0.15 |

| med mle | 1.03 | 1.00 | -2.51 | -0.50 | -0.50 | -0.97 | 1.05 | -2.53 | -0.49 | -0.50 |

| mad mle | 0.57 | 0.39 | 0.16 | 0.09 | 0.09 | 0.36 | 0.28 | 0.28 | 0.16 | 0.14 |

| Efficiency | 0.15 | 0.22 | 43.13 | 23.13 | 81.39 | 371.60 | 3223.71 | 50.28 | 23.03 | 81.91 |

| Efficiency(mad) | 78.85 | 87.63 | 51.67 | 22.50 | 84.41 | 78.39 | 102.95 | 57.02 | 29.27 | 85.60 |

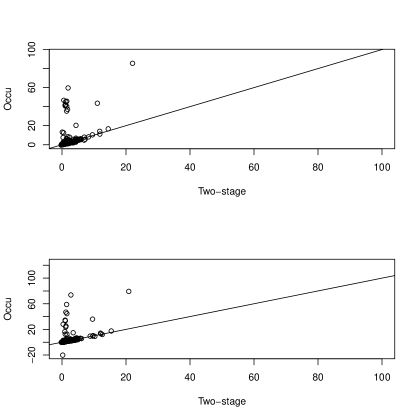

A plot of 1000 simulated occupancy estimates from our approach were compared to the full likelihood (see Figure 1). The model included time varying covariates using the two-stage approach for the IWLS method and the same was modelled with occu; , , and . Overall, the two-stage estimator gave estimates that were more accurate and more consistent and that occu may give extreme estimates of occupancy parameters when the two-stage approach does not. There was a single outlier that was omitted from the plot for clarity. Corresponding summary statistics are given in Table 4.

Table 5 shows that occu gives estimates that are large four times more often than our approach. We present agreement between our approach and occu to estimating occupancy. Agreement between the two methods is defined as the number of estimates that are either both or neither greater than three (), less than or equal to three (), or when these disagree. occu gives estimates that are greater than three (i.e ) four times more often than our IWLS method i.e. 36 to 12 (Table 5). The table clearly demonstrates there is no universal best method for finding estimates for occupancy. When IWLS fails i.e. does not converge, then we recommend using optim or occu.

| Occupancy | Detection | ||||

|---|---|---|---|---|---|

| Int | Int | time | |||

| Mean Prob | 0.72 | 0.63 | |||

| Actual | 1.00 | 1.00 | -1.50 | -0.50 | -0.50 |

| med two-stage | 0.98 | 1.03 | -1.53 | -0.52 | -0.51 |

| mad two-stage | 0.63 | 0.57 | 0.25 | 0.28 | 0.15 |

| sd two-stage | 7.82 | 9.94 | 0.28 | 0.28 | 0.16 |

| med mle | 1.10 | 1.16 | -1.52 | -0.53 | -0.51 |

| mad mle | 0.70 | 0.65 | 0.21 | 0.17 | 0.15 |

| Efficiency | 67.55 | 45.33 | 68.41 | 38.92 | 90.47 |

| Efficiency(mad) | 99.94 | 125.16 | 71.13 | 38.25 | 93.37 |

| occu method | ||

|---|---|---|

| Two-stage IWLS | ||

| 832 | 36 | |

| 12 | 37 | |

5 Applications

5.1 Data Set 1

Hutchinson et al., 2015b use a publicly available data set from Hutchinson et al., 2015a 333https://datadryad.org//resource/doi:10.5061/dryad.t40f2 to illustrate their penalized likelihood approach. The data set contains detections of 25 avian species over 3 visits to each of 656 sites from a field study in 2011 in southern Indiana, USA. We use the entire data set. There are six site-specific vegetation covariates available (labelled vegcov1, vegcov2, …vegcov6) and four time dependent survey covariates time, temp, cloud and julian measured for each visit to each site. These are included in the data data frame as time1, time2, …julian2, julian3. All the covariates have been standardised. We consider the entire data set for the first species. We considered four models for the detection probabilities. The first only involved the site covariates, the second the site covariates and time dependent intercepts, the third site and time dependent survey covariates and the last involved site and time dependent survey covariates and time dependent intercepts. The values of the AIC from the conditional likelihood are: Site only: AIC = 1517.4, Site + Time Varying Intercept: AIC = 1511.1, Site + Survey: AIC = 1488.3, Site + Survey + Time Varying Intercept: AIC = 1486.2. The best model of these includes the site covariates, time dependent survey covariates and time dependent intercepts. The resulting two-stage (Two-stage) estimates (with IWLS method) are displayed in Table 6 along with the full maximum likelihood estimates (Full likelihood) computed using the occu function in the R package unmarked (fitting the model with occu is briefly described in D). The maximum likelihood and two-stage estimates are very similar.

In the model for detection there are 6 site covariates and 4 survey covariates. This gives possible models (or if one allows time varying intercepts.) Whilst this is a large number of models, in the absence of variable selection methods in VGAM it is nevertheless feasible to compute the AIC for each model. We can then repeat this process for the model for occupancy after fixing the best detection model. The best fitting model for the detection probabilities using the AIC is indicated in Table 6. The function vglm allows more flexibility in the modelling. For example, by changing parallel.t=FALSE0 to parallel.t=TRUE0 the coefficients associated with each variable in the detection model may be time varying. We do not pursue this further here. Of course as occupancy is assumed constant over the visits we do not model the occupancy coefficients as time varying.

| Full Likelihood | Two-stage | |||||||

| Parameter | Estimate | se | Estimate | se | ||||

| Occupancy | ||||||||

| Intercept∗ | 2.27 | 0.15 | 14.98 | 0.00 | 2.26 | 0.15 | 14.91 | 0.00 |

| vegcov1∗ | 0.50 | 0.18 | 2.78 | 0.01 | 0.52 | 0.17 | 3.00 | 0.00 |

| vegcov2 | 0.03 | 0.17 | 0.15 | 0.88 | 0.01 | 0.17 | 0.04 | 0.97 |

| vegcov3 | 0.07 | 0.17 | 0.41 | 0.68 | 0.06 | 0.16 | 0.34 | 0.73 |

| vegcov4∗ | 0.37 | 0.13 | 2.89 | 0.00 | 0.37 | 0.12 | 3.03 | 0.00 |

| vegcov5 | 0.14 | 0.13 | 1.06 | 0.29 | 0.14 | 0.13 | 1.10 | 0.27 |

| vegcov6∗ | -0.29 | 0.16 | -1.85 | 0.06 | -0.29 | 0.15 | -1.88 | 0.06 |

| Detection | ||||||||

| Intercept:1∗ | 1.07 | 0.30 | 3.60 | 0.00 | 1.09 | 0.30 | 3.67 | 0.00 |

| Intercept:2∗ | 1.48 | 0.12 | 12.00 | 0.00 | 1.48 | 0.12 | 12.04 | 0.00 |

| Intercept:3∗ | 2.27 | 0.30 | 7.70 | 0.00 | 2.26 | 0.30 | 7.62 | 0.00 |

| vegcov1∗ | 0.56 | 0.09 | 6.06 | 0.00 | 0.55 | 0.09 | 6.02 | 0.00 |

| vegcov2∗ | -0.25 | 0.09 | -2.79 | 0.01 | -0.25 | 0.09 | -2.76 | 0.01 |

| vegcov3 | -0.10 | 0.09 | -1.16 | 0.24 | -0.09 | 0.09 | -1.05 | 0.30 |

| vegcov4∗ | 0.18 | 0.08 | 2.37 | 0.02 | 0.18 | 0.07 | 2.34 | 0.02 |

| vegcov5∗ | 0.10 | 0.08 | 1.34 | 0.18 | 0.11 | 0.07 | 1.46 | 0.14 |

| vegcov6∗ | -0.10 | 0.09 | -1.18 | 0.24 | -0.11 | 0.09 | -1.27 | 0.20 |

| time | -0.07 | 0.07 | -0.93 | 0.35 | -0.07 | 0.07 | -0.98 | 0.33 |

| temp∗ | -0.24 | 0.08 | -3.09 | 0.00 | -0.24 | 0.08 | -3.11 | 0.00 |

| cloud∗ | -0.13 | 0.07 | -1.90 | 0.06 | -0.13 | 0.07 | -1.93 | 0.05 |

| julian∗ | -0.74 | 0.23 | -3.23 | 0.00 | -0.73 | 0.23 | -3.18 | 0.00 |

5.2 Data II

A smaller data set is given on the website James Peterson 444http://people.oregonstate.edu/~peterjam/occupancy_workshop/hands_on.html that presents data on detections of brook trout collected via electrofishing in three 50 m sections of streams at 57 sites in the Upper Chattachochee 371 River basin, USA. These data contained a site covariate, Elevation (Ele) and a time dependent covariate stream mean cross-sectional area (CSA). These variables are on quite different scales. The average elevation was approximately 2861 and the mean cross-sectional area was less than 2. We considered four models, just the site covariates, site covariates and time varying intercepts, site and survey covariates and site and survey covariates with time varying intercepts. Using the default settings in occu the estimates did not converge. This was rectified by using the “Nelder-Mead” method set to a maximum of 2000 iterations. The two-stage estimator had no such problems. The estimates for the unstandardised data are in Table 7 (a). The estimates are generally similar. For the standardised data, occu with the default options did converge. The results are given in Table 7 (b). The estimates are again quite similar.

| Full Likelihood | Two-stage | |||||||

| Parameter | Estimate | se | Estimate | se | ||||

| (a) Unstandardised | ||||||||

| Occupancy | ||||||||

| Intercept | -3.9716 | 0.6858 | -5.7914 | 0.0000 | -4.0452 | 1.1218 | -3.6060 | 0.0003 |

| Ele | 0.0013 | 0.0003 | 4.5338 | 0.0000 | 0.0013 | 0.0004 | 3.6441 | 0.0003 |

| Detection | ||||||||

| Intercept | 0.0580 | 0.7352 | 0.0788 | 0.9372 | -0.1609 | 1.2397 | -0.1298 | 0.8968 |

| Ele | 0.0004 | 0.0002 | 1.9697 | 0.0489 | 0.0004 | 0.0003 | 1.2516 | 0.2107 |

| CSA | -0.8325 | 0.2822 | -2.9503 | 0.0032 | -0.7438 | 0.2873 | -2.5888 | 0.0096 |

| (b) Standardised | ||||||||

| Occupancy | ||||||||

| Intercept | -0.19 | 0.36 | -0.52 | 0.60 | -0.34 | 0.32 | -1.04 | 0.30 |

| Ele | 1.53 | 0.45 | 3.42 | 0.00 | 1.48 | 0.40 | 3.71 | 0.00 |

| Detection | ||||||||

| Intercept | -0.14 | 0.35 | -0.38 | 0.70 | -0.16 | 0.36 | -0.44 | 0.66 |

| Ele | 0.36 | 0.35 | 1.04 | 0.30 | 0.43 | 0.37 | 1.18 | 0.24 |

| CSA | -0.82 | 0.28 | -2.97 | 0.00 | -0.80 | 0.28 | -2.81 | 0.00 |

6 Discussion

In Karavarsamis and Huggins, (2017) we examined the two-stage approach for the homogeneous occupancy model. Here we examined the two-stage approach for the heterogeneous occupancy model where the occupancy and detection probabilities now depend on covariates that may vary between sites and over time.

In our applications here the two-stage estimator gave similar estimates to the full maximum likelihood with the occu function in package unmarked. For the large standardised data set first considered the estimates from the two methods were very similar. The two-stage method has advantages in model selection as the dimension of the space to be searched can be enormously reduced. By considering two smaller dimensional parameter spaces and using IWLS in both stages it is also numerically more stable so that standardisation is less important. It also gives access to the VGAM methodology in estimating detection. We defer further exploration elsewhere.

The default in the occu function in the unmarked package uses a vector of zeroes as starting values and if the algorithm does not converge suggests the user provides starting values. However, there is no guidance on how to find suitable values. A simulation study showed that occu may give extreme estimates of occupancy parameters when the two-stage does not.

If there are too few redetections the two-stage estimator can fail. This results from conditioning on at least one detection. However, when the main focus is on estimating occupancy, the occupancy probability appears to be relatively insensitive for small changes in detection probability (Karavarsamis and Huggins,, 2017).

References

References

- Aing et al., (2011) Aing, C., Halls, S., Oken, K., Dobrow, R., and Fieberg, J. (2011). A Bayesian hierarchical occupancy model for track surveys conducted in a series of linear, spatially correlated, sites. Journal of Applied Ecology, 48:1508–1517.

- Fiske and Chandler, (2011) Fiske, I. J. and Chandler, R. B. (2011). unmarked: An R package for fitting hierarchical models of wildlife occurrence and abundance. Journal of Statistical Software, 43(10):1–23.

- Fiske and Chandler, (2015) Fiske, I. J. and Chandler, R. B. (2015). Overview of Unmarked: An R Package for the Analysis of Data from Unmarked Animals. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Gimenez et al., (2009) Gimenez, O., Bonner, S., King, R., Parker, R., Brooks, S., Jamieson, L., Grosbois, V., Morgan, B., and Thomas, L. (2009). WinBUGS for population ecologists: Bayesian modeling using Markov chain Monte Carlo methods. In Thomson, D. L., Cooch, E. G., and Conroy, M. J., editors, Modeling Demographic Processes In Marked Populations, volume 3 of Environmental and Ecological Statistics, pages 883–915. Springer US.

- Gimenez et al., (2007) Gimenez, O., Rossi, V., Choquet, R., Dehais, C., Doris, B., Varella, H., Vila, J., and Pradel, R. (2007). State–space modelling of data on marked individuals. Ecological Modelling, 206(431–438).

- Guillera-Arroita et al., (2010) Guillera-Arroita, G., Ridout, M., and Morgan, B. (2010). Design of occupancy studies with imperfect detection. Methods in Ecology and Evolution, 1(2):131–139.

- Huggins, (1989) Huggins, R. M. (1989). On the Statistical Analysis of Capture Experiments. Biometrika, 76(1):133–140.

- Hui et al., (2011) Hui, C., Foxcroft, L. C., Richardson, D. M., and MacFadyen, S. (2011). Defining optimal sampling effort for large-scale monitoring of invasive alien plants: a Bayesian method for estimating abundance and distribution. Journal of Applied Ecology, 48(3):768–776.

- (9) Hutchinson, R., Valente, J., Emerson, S., Betts, M., and Dietterich, T. (2015a). Data from: Penalized likelihood methods improve parameter estimates in occupancy models.

- (10) Hutchinson, R. A., Valente, J. J., Emerson, S. C., Betts, M. G., and Dietterich, T. G. (2015b). Penalized likelihood methods improve parameter estimates in occupancy models. Methods in Ecology and Evolution. doi: 10.1111/2041-210X.12368.

- Karavarsamis and Huggins, (2017) Karavarsamis, N. and Huggins, R. M. (2017). Two-stage approaches to the analysis of occupancy data I: The homogeneous case. Submitted.

- Karavarsamis et al., (2013) Karavarsamis, N., Robinson, A. P., Hepworth, G., Hamilton, A., and Heard, G. (2013). Comparison of four bootstrap-based interval estimators of species occupancy and detection probabilities. Australian and New Zealand Journal of Statistics, 55(3):235–252.

- Lunn et al., (2000) Lunn, D., Thomas, A., Best, N., and Spiegelhalter, D. (2000). WinBUGS – a Bayesian modelling framework: concepts, structure, and extensibility. Statistics and Computing, 10:325–337.

- MacKenzie et al., (2006) MacKenzie, D. I., Nichols, J., Royle, J., Pollock, K., Bailey, L., and Hines, J. (2006). Occupancy Estimation and Modeling Inferring Patterns and Dynamics of Species Occurrence. Elsevier, San Diego, CA.

- MacKenzie et al., (2009) MacKenzie, D. I., Nichols, J., Seamans, M. E., and Gutiërrez, R. J. (2009). Modeling species occurrence dynamics with multiple states and imperfect detection. Ecology, 90(3):823–835.

- MacKenzie et al., (2002) MacKenzie, D. I., Nichols, J. D., Lachman, G. B., Droege, S., Royle, J., and Langtimm, C. A. (2002). Estimating site occupancy rates when detection probabilities are less than one. Ecology, 83(8):2248–2255.

- Martin et al., (2011) Martin, J., Royle, J., MacKenzie, D., Edwards, H., Kéry, M., and Gardner, B. (2011). Accounting for non-independent detection when estimating abundance of organisms with a Bayesian approach. Methods in Ecology and Evolution, 2(6):595–601.

- Milne et al., (1989) Milne, B., Johnston, K., and Forman, R. (1989). Scale-dependent proximity of wildlife habitat in a spatially-neutral Bayesian model. Landscape Ecology, 2:101–110.

- Moreno and Lele, (2010) Moreno, M. and Lele, S. R. (2010). Improved estimation of site occupancy using penalized likelihood. Ecology, 91(2):341–346.

- R Development Core Team, (2018) R Development Core Team (2018). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Royle and Dorazio, (2008) Royle, J. A. and Dorazio, R. (2008). Hierarchical Modeling and Inference in Ecology: The Analysis of Data from Populations, Metapopulations, and Communities. Academic Press, San Diego, CA.

- Wintle et al., (2004) Wintle, B., McCarthy, M., Parris, K., and Burgman, M. (2004). Precision and bias of methods for estimating point survey detection probabilities. Ecological Applications, 14:703–712.

- Wintle et al., (2003) Wintle, B., McCarthy, M., Volinsky, C., and Kavanagh, R. (2003). The use of Bayesian model averaging to better represent uncertainty in ecological models. Conservation Biology, 17(6):1579–1590.

- Yee, (2010) Yee, T. W. (2010). The VGAM package for categorical data analysis. Journal of Statistical Software, 32:1–34.

- Yee, (2015) Yee, T. W. (2015). Vector Generalized Linear and Additive Models: With an Implementation in R. Springer, New York, USA.

- Yee et al., (2015) Yee, T. W., Stoklosa, J., and Huggins, R. M. (2015). The VGAM package for capture–recapture data using the conditional likelihood. Journal of Statistical Software, 65:1–33.

Appendix A Conditional Likelihood using VGAM

The R package VGAM (Yee,, 2010) is a powerful and flexible package that fits models to vector responses. As such, at first glance it can be overwhelming. However, its handling of time dependent covariates makes it preferable to writing one’s own functions. Here we give a description of how it can be used to fit some common models to detections using conditional likelihood in the first stage of our approach.

A.1 Fitting Time Independent Covariates for Detection

In our two-stage approach the conditional likelihood fits the model for detection to data from the sites where there was at least one detection. This can be done the posbinomial family in the VGAM function vglm. Firstly the data is reduced to those sites where there was at least one detection. When there is no time dependence, computing the estimates using vglm is straightforward. We illustrate this for the data of Hutchinson et al., 2015b ; Hutchinson et al., 2015a as these data contain both site and visit (i.e. time dependent) covariates. For these data, the data frame data is a reduced data frame that contains data from the sites where occupancy was detected. The variable is the number of times the species was detected at each occupied site, is the number of visits to each site, and site covariates are vegcov1,vegcov2,…,vegcov6. See Figure 2 for selected output ( in this example). The parameter estimates may then be used in the second stage of the analysis.

> V.out=vglm(cbind(Y,3-Y)~vegcov1+vegcov2+vegcov3+vegcov4

+vegcov5+vegcov6,

family=posbinomial(omit.constant=TRUE),data=data)

> coef(V.out)

# (Intercept) vegcov1 vegcov2 vegcov3 vegcov4

# 1.5590909 0.5493825 -0.2512287 -0.1048756 0.1656597

# vegcov5 vegcov6

# 0.1186192 -0.1277806

With the univariate response , the implementation is very similar to glm. The term omit.constant=TRUE does not affect the fitting but removes the constant terms from the computation of the AIC. These estimates may then be input into the second stage procedure to estimate parameters associated with the occupancy model.

A.2 Fitting Time Dependent Covariates for Detection

Time dependent models for detection may be fitted to data using the posbernoulli.t family in the vglm function in VGAM. Fitting these models is more complex as many more models are available and the response consists of the detections on each visit to the site and is hence multivariate. We again use the data from Hutchinson et al., 2015b ; Hutchinson et al., 2015a . The time dependent covariates are time, temp, cloud and julian measured for each visit to each site. These are included in the data data frame as time1, time2, …julian2, julian3. With a vector valued response there is the possibility that the coefficient associated with a covariate may change with the visit, so the associated modelling and hence the functions to fit the models are more complex. See Yee, (2010, §6.3) for a worked example in a capture-recapture context. In Figure 3 we first fit a simple model with time dependent intercepts and the relationship with the site covariates remains independent of time. This was specified through the parallel.t argument to the posbernoulli.t family. Note that parallel.t=FALSE1 is the default for the posbernoulli.t family but for clarity we explicitly incorporate it in Figure 3.

> V.out=vglm(cbind(survey1,survey2,survey3)

~ vegcov1+vegcov2+vegcov3+vegcov4+vegcov5+vegcov6,

family=posbernoulli.t(parallel.t=FALSE~1), data=data)

> coef(V.out)

# (Intercept):1 (Intercept):2 (Intercept):3 vegcov1 vegcov2

# 1.8583766 1.5130892 1.3527893 0.5515551 -0.2522520

# vegcov3 vegcov4 vegcov5 vegcov6

# -0.1052631 0.1663444 0.1190595 -0.1282785

Incorporating time dependent covariates is a little more complex and requires use of the xij and form2 arguments in VGAM. The form2 argument is straightforward. It gives all the variables in the model and needs to be included if xij is used. The xij argument specifies that covariates have different values at different visits. To implement it is necessary to construct a new variable, for example time.tij, for each time dependent variable in the model and incorporate them in the data frame. In our case this gives four new variables, time.tij, temp.tij, cloud.tij and julian.tij in Figure 4.

> V.out=vglm(cbind(survey1,survey2,survey3)

~vegcov1+vegcov2+vegcov3+vegcov4

+vegcov5+vegcov6+time.tij+temp.tij+cloud.tij+julian.tij,

data=Data.all,

xij=list(time.tij~time1+time2+time3-1,temp.tij~temp1+temp2+temp3-1,

cloud.tij~cloud1+cloud2+cloud3-1,julian.tij~julian1+julian2

+julian3-1),

family=posbernoulli.t(parallel.t=FALSE~0),

form2=~vegcov1+vegcov2+vegcov3+vegcov4+vegcov5+vegcov6+time.tij

+temp.tij+cloud.tij+julian.tij+time1+time2+time3+temp1+temp2

+temp3+cloud1+cloud2+cloud3+julian1+julian2+julian3)

> coef(V.out)

# (Intercept) vegcov1 vegcov2 vegcov3 vegcov4

# 1.60651791 0.54525171 -0.24061702 -0.08727207 0.16955603

# vegcov5 vegcov6 time.tij temp.tij cloud.tij julian.tij

# 0.108527 -0.112085 -0.069456 -0.238605 -0.161028 -0.264658

Appendix B Iterative Weighted Least Squares

The potential instability of the maximum likelihood estimates when computed using numerical optimization, through the function optim in R motivated us to develop an iterative weighted least squares (IWLS) approach. This is quite straightforward for the logistic model in our two-stage approach.

Recall . Let , and the matrix has th column Then, as is not a function of , maximising the partial log-likelihood (6) is equivalent to maximising . Then, with we have . Let and . Now, and so that . That is, where or the partial score equations may be written as . The expected conditional Fisher information is then . Recall . Then

This gives the iterative procedure of Section 3.2.1.

Appendix C Derivation of the Standard Errors

We outline the proof of (7) for the linear model with logistic link. Let and denote the true values of and and let be a consistent estimator of . Here this will be the conditional likelihood estimator of but our results are more general than that. We suppose that for a matrix , and a matrix ,

and that the central limit theorem is applicable so that

| (11) |

We also suppose that the estimators arising from the first stage are consistent and satisfy for some matrix . That is, . Note that using vglm to estimate using conditional likelihood yields an estimate of . Then we approximate by . Finally, we suppose that the partial score functions for are uncorrelated with those for . We have noted in §3 that this holds for the likelihood conditional on at least one detection at a site.

The log-partial likelihood is

so that

The first order expansion of about yields

and that of about yields

which together give

The central limit theorem and recalling that the partial score functions are uncorrelated then gives

where

That is . To estimate the standard errors, recall yielding (8).

Next we determine in the time homogeneous case. As

| (12) |

and , the chain rule gives,

As we then see that

As where is the covariance matrix of and it is easily seen that reduces to (7).

Appendix D Fitting the Full Likelihood with occu

The use of occu is well documented. Here, we briefly describe its use as it handles time varying (or time dependent) covariates differently to vglm. To fit our full model using occu we first construct a matrix of factors, Visit, corresponding to the three visits. We then construct a list Obs that contains data frames of the time varying covariates. This is then converted into an unmarkedFrameOccu object, D. The model is then fitted to the data, as shown in Figure 5. Thus in either the vglm or occu approaches there is an initial data manipulation step requiring construction of an appropriately structured data frame, then the fitting to data. With vglm there is then a second step to estimate the occupancy model.

> Visit=matrix(as.factor(c(rep("a",656),rep("b",656),rep("c",656))),

ncol=3)

> Obs=list(time=as.data.frame(Model.out@T.ij[,c(1,5,9)]),

temp=as.data.frame(Model.out@T.ij[,c(2,6,10)]),

cloud=as.data.frame(Model.out@T.ij[,c(3,7,11)]),

julian=as.data.frame(Model.out@T.ij[,c(4,8,12)]),

Visit=as.data.frame(Visit))

> D=unmarkedFrameOccu(y=Model.out@Detect,

siteCovs=as.data.frame(Model.out@X[,-1]),obsCovs=Obs)

> O.5.out=occu(~Visit+vegcov1+vegcov2+vegcov3+vegcov4+vegcov5+vegcov6

+time+temp+cloud+julian-1~vegcov1+vegcov2+vegcov3+vegcov4+vegcov5

+vegcov6,data=D,engine=c("C"))

> O.5.out@estimates