Cauchy noise loss

for stochastic optimization of random matrix models

via free deterministic equivalents

Abstract.

For random matrix models, the parameter estimation based on the traditional likelihood functions is not straightforward in particular when we have only one sample matrix. We introduce a new parameter optimization method for random matrix models which works even in such a case. The method is based on the spectral distribution instead of the traditional likelihood. In the method, the Cauchy noise has an essential role because the free deterministic equivalent, which is a tool in free probability theory, allows us to approximate the spectral distribution perturbed by Cauchy noises by a smooth and accessible density function.

Moreover, we study an asymptotic property of determination gap, which has a similar role as generalization gap. Besides, we propose a new dimensionality recovery method for the signal-plus-noise model, and experimentally demonstrate that it recovers the rank of the signal part even if the true rank is not small. It is a simultaneous rank selection and parameter estimation procedure.

Key words and phrases:

Random Matrix Theory, Free Probability Theory, Stochastic Optimization, Rank Estimation, Dimensionality Recovery1. Introduction

Situations in many fields of research, such as digital communications and statistics, can be modeled with random matrices. The development of free probability theory (FPT for short) invented by Voiculescu [36] expands the scope of research of random matrices. The free probability theory is an invaluable tool for describing the asymptotic behavior of many random matrices when their size is large. For example, consider a fixed multivariate polynomial , independent random matrices , and the following;

-

(1)

deterministic matrices ,

-

(2)

the empirical spectral distribution of .

Then FPT answers how to infer (2) from (1) for a wide class of polynomials and random matrices. However, little is known about its opposite direction; that is, how to know (1) from (2). This direction is regarded as a statistical problem of how to estimate parameters of a random matrix model from observed empirical spectral distributions (ESD, for short). Now, estimating parameters of a system involving random matrices appears in several fields of engineering such as signal processing and machine learning. Therefore, we are interested in finding a common framework to treat several random matrix models using their algebraic structures.

Likelihood or Spectral Distribution

The maximal likelihood estimation, equivalently the minimizing empirical cross-entropy, is available in the case there are a large number of i.i.d. samples. For random matrix models, the parameter estimation based on the traditional likelihood is not straightforward in particular when we have only one sample matrix. For example, row vectors or column ones are not i.i.d family, then it is not clear that maximal likelihood estimation is applicable. We introduce a new parameter optimization method of random matrix models which works even in such a case not based on the traditional likelihood, instead of based on the spectral distribution. The so-called self-averaging property, which is an almost-sure convergence of ESD of random matrices, is a key to our method. In order to find a reasonable objective function to estimate parameters of random matrices, we focus on the fact that the ESD of a random matrix model is approximated by a deterministic measure such that its Cauchy transform is accessible; it is a fixed point of a holomorphic mapping. We choose the deterministic measure by replacing the random matrix model with its free deterministic equivalent (FDE for short, see Definition 5.5).

Based on the FDE, we introduce an objective function, which is an empirical cross-entropy defined as the following;

| (1.1) |

where is the spectral distribution of an observed sample matrix. In (1.1), the random variables and are independent, is distributed with the spectral distribution , and is distributed with the Cauchy distribution of scale . In addition, the probability measure is the deterministic one which approximates the ESD of the random matrix , and is its Cauchy transform. Note that the -slice of the Cauchy transform is a strictly positive density function on .

We choose this objective function because of the following reasons. The first one is, as mentioned above that the Cauchy transforms of the ESD becomes accessible by using iterative methods if we replace the random matrix model by its FDE. More precisely, we choose a family of deterministic probability measures , which approximates , and moreover we can compute by iterative methods. Note that the convergence of the iterative methods is rigorously proven (see Section 5.3). Besides, the gradient of each -slice is computable (see Section 5.4) by the chain rule and the implicit differentiation. The last reason is that -slice has enough information to distinguish original measures (see Lemma 3.9).

Compound Wishart and Signal-plus-Noise Models

Compound Wishart matrices and signal-plus-noise matrices are typical classes of random matrices. In this paper, we apply our methods to their families; compound Wishart models (CW model, for short) and signal-plus-noise models (SPN model). Compound Wishart matrices are introduced by Speicher [30], which also appear as sample covariance matrices of correlated samplings. Their modifications appear in the analysis of some statistical models [8, 6, 13, 15]. See [17] for more detail. The SPN model appears in the signal precessing [29, 11, 34]. The SPN model is also closely related with the probabilistic principal component analysis (see [33]), the matrix completion, the low-rank approximation, the reduced rank singular value decomposition, and the dimensionality recovery [21, 22, 23].

Dimensionality Recovery

Consider a rectangular random matrix model

| (1.2) |

where is a Ginibre matrix, , and . The parameter expresses the signal part of the , and does the noise power. Its likelihood is given by

| (1.3) |

Hence if is fixed, for a sample matrix , its maximal likelihood estimation is equivalent to the traditional trace norm minimization;

| (1.4) |

where is a parameter space which is a subset of . For a fixed and , its closed-form solution is given by a well-known truncated singular value decomposition of (note that the field can be replaced with ), that is, given by replacing smaller singular values of with . Now, if the assumption is removed, the solution is trivial; is estimated as the observed sample matrix itself. After all, for the low-rank approximation, we need to know the rank of the true parameter by another method beforehand if we use the likelihood function (1.3).

Instead of the likelihood (1.3), we apply our parameter estimation based on (1.1) to the low-rank approximation without the assumption on the true rank. Here we focus on the empirical singular values of the large dimensional , equivalently, the empirical spectral distribution of the signal-plus noise model defined as

We emphasize that we estimate not only the signal part but also the noise power from each single-shot sample matrix by our new method.

Free Deterministic Equivalents

Our work relies on the free deterministic equivalent (FDE for short) introduced by Speicher and Vargas [31, 35]. Roughly speaking, we can interpret independent random matrices as deterministic matrices of operators in an infinite-dimensional -probability space. The origin of FDE can be found in Neu-Speicher [25] as a mean-field approximation of an Anderson model in statistical physics. One can also consider FDE as one of the approximation methods to eliminate randomness for computing the expectation. Particularly, FDE is a “lift” of the deterministic equivalent introduced by [12]. More precisely, FDE is an approximation of a random matrix model at the level of operators, and on the other hand, the deterministic equivalent is that at the level of Cauchy transforms. Now the deterministic equivalent is known as an approximation method of Cauchy transforms of random matrices in several works of literature of wireless-network (see [12, 8]. Despite its rich background in FPT, the algorithm of FDE is not complicated. Roughly speaking, its primary step is to replace each Gaussian random variable in entries of a random matrix model by an “infinite size” Ginibre matrix, which is called a circular element in FPT.

Our Contribution

Here we summarize our contributions.

Our major contribution is to introduce a common framework for the parameter optimization of random matrix models, which is a combination of the Cauchy noise loss, FDE, iterative methods for computing Cauchy transforms, and a stochastic gradient descent method.

The second one is to give a brief, and general computing method of gradients of Cauchy transforms of FDE, in particular, give a norm estimation of derivations of implicit functions, which appear in the iterative method for computing Cauchy transforms.

The third one is to show the asymptotic properties of the gap between the Cauchy cross-entropy and the empirical one.

The fourth one is to show optimizations of the CW model and the SPN model via the Cauchy noise loss experimentally.

The last one is to propose a new dimensionality recovery method for the signal-plus-noise model, and experimentally demonstrate that it recovers the rank of the signal part even if the true rank is not small. It is a simultaneous rank selection and parameter estimation procedure.

2. Related Work

There are several applications of deterministic equivalents and FDE to the analysis of multi-input multi-output channels [8, 31].

Ryan [29] applied the free deconvolution to SPN models. Their method is based on evaluating the difference of moments, the mean square error of moments. Since it uses an only finite number of lower-order moments, the error has subtotal information of the empirical distribution. On the contrary, our method uses full information of the empirical distribution.

There are applications of the fluctuation of FDE to some autoregressive moving-average models [14, 15]. Their methods are based on the fluctuation of the CW model, and focus on the good-of-fit test of the parameter estimation, not for the parameter estimation itself.

Another direction to the low-rank approximation is the Bayesian matrix factorization. The matrix factorization model is defined as the following; fix with and factorize with ;

In addition, use the likelihood (1.3) and the Gaussian prior on , . The parameter is estimated as the integration of with the posterior distribution. The hyperparamers of the prior distributions are determined by minimizing the Bayesian free energy, which is called empirical Bayesian matrix factorization. See [21] for the theoretical analysis. Tipping-Bishop [33] treats the case is known.

The variational Bayesian method (see [5]), which approximates posterior distributions, is also called a mean-field approximation in the Bayesian framework. Recall that an origin of FDE is a mean-field approximation, but it is a deterministic approximation of the empirical spectral distribution, which is different from the variational Bayesian method.

Nakajima-Sugiyama-Babacan-Tomioka [22] and [23] gave the global analytic optimal solution of the empirical variational Bayesian matrix factorization (EVBMF, for short), and used it to a dimensionality recovery problem. Note that EVBMF almost surely recovers the true rank in the large scale limit under some assumptions [23, Theorem 13, Theorem 15], in particular, if the true rank is low. Their loss function is based on the likelihood. Recall that we use another loss function not based on the likelihood (1.3). Note that in our method, we need no assumption on the true rank.

3. Random Matrix Models

In this section, we introduce random matrix models and our main idea.

Basic Notation

In this paper, we fix a probability space . A random variable (resp. real random variable) is a -valued (resp. -valued) Borel measurable function on the probability space.

-

(1)

for any integrable or nonnegative real random variable .

-

(2)

for a square-integrable real random variable .

-

(3)

.

-

(4)

.

3.1. Gaussian Random Matrix models

Notation 3.1.

Let be or , and . Let us denote by the set of rectangular matrices over . We write . A random matrix is a map for a such that each entry is Borel measurable.

Definition 3.2.

-

(1)

A real Ginibre matrix of size is the matrix whose entries are independent and identically distributed with for a .

We denote by the set of real Ginibre matrices with .

-

(2)

A complex Ginibre matrix of size is the matrix whose entries are given by , where the family is independent and each element is distributed with for .

We denote by the set of complex Ginibre matrices with .

Notation 3.3.

We write .

Note that .

Definition 3.4.

Let be a self-adjoint polynomial (that is, it is stable under replacing by ) in non-commutative dummy variables and their adjoint . Let be a family of pairs of natural numbers and be corresponding evaluation of defined as

where products and sums satisfy dimension compatibility.

Then the real (resp. complex) polynomial Ginibre matrix model (PGM model, for short) of type on a subset with (resp. ) is the restriction of the following map to ;

where the family of ( ) is independent.

We introduce examples of Ginibre matrix models which are in the scope of our numerical experiments.

Definition 3.5.

-

(1)

A compound Wishart model (CW model for short) of type on , denoted by , is the PGM model of type on the subset , where . Note that

-

(2)

A signal-plus-noise model (SPN model for short) of type on a subset , denoted by , is the PGM model of type on , where is a polynomial of dummy variables given by Note that

Our estimation method is based on the spectral distribution of random matrices.

Definition 3.6.

(Spectral distribution and Moments)

-

(1)

For any self-adjoint matrix , let be the eigenvalues of . The spectral distribution of , denoted by , is defined as the discrete measure

-

(2)

For any self-adjoint random matrix , we write

-

(3)

Write and .

For any , we denote the -th moment of for by . For any random variable whose law is , we define its moment by . All moments of a probability measure (resp. a random variable ) are well-defined if (resp. ).

-

(4)

for , and .

-

(5)

We define the moment of as .

Note that for any and .

3.2. From Cauchy Transform to Cauchy Noise Loss

We use the Cauchy transform of ESD to define our loss function for parameter estimation of random matrix models. This is mainly because the Cauchy transform of ESD is accessible for specific random matrix models. More precisely, the Cauchy transform is approximated by the unique solution of a fixed point formula. Note that the fixed point formula depends on random matrix models. We discuss the fixed point formula in Section 5.3. Besides, the Cauchy transform is closely rated with the Cauchy noise.

Definition 3.7.

-

(1)

The Cauchy transform of is the holomorphic function on defined as

-

(2)

The Cauchy distribution with scale parameter is the probability measure over whose density function is given by the following Poisson kernel;

We call a random variable a Cauchy noise of scale , denoted by , if its density function is equal to .

The following is a key lemma of our algorithm.

Definition 3.8.

For and , we define their convolution as , .

Lemma 3.9.

Let . Fix . Then the following conditions are equivalent.

-

(1)

For any ,

(3.1) -

(1’)

.

-

(2)

.

Proof.

The equivalence of (1) and (1’) follows from the well-known fact that

| (3.2) |

Then we only need to show that (1’) induces (2). For any , let us denote its Fourier transform by . Similarly, we define the Fourier transform of any probability density function. Fix . Assume that . Since the Fourier transformation linearize the convolution, we have . Because , we have . Since the Fourier transformation is injective, we have . ∎

Let be a family of a self-adjoint random matrix. Then, for random matrix models such as CW and SPN, there is a family of deterministic measures which approximates (the proof is postponed to Section 5.1). We estimate parameters by comparing a deterministic measure and a random one instead of comparing two random measures; recall that there is only one single-shot observation.

Fix , pick and let . Then the right-hand side of (3.1) is equal to the density of the real random variable , where is a random variable distributed with the empirical spectral distribution, is a Cauchy noise of scale , and the pair is independent. On the other hand, each Cauchy transform approximates that of , and it is accessible; it is given by the solution of a fixed point formula and computed by an iterative method. Then Lemma 3.9 suggests a possibility of the parameter estimation by fitting parametric implicit density functions to an empirical distribution perturbed by Cauchy noises.

Definition 3.10.

Let . For , we call the strictly positive function the -slice of . If there is no confusion, we also call it the -slice of the Cauchy transform .

Now, in many kinds of research of statistics, the cross-entropy is used for fitting a density function to a reference distribution. To achieve optimization of random matrix models, we consider the following Cauchy cross-entropy.

Definition 3.11.

(Cauchy cross-entropy) Let and with . Then the Cauchy cross-entropy of against is defined as

| (3.3) |

where

| (3.4) |

Remark 3.12.

We prove that the Cauchy cross-entropy is well-defined and finite in Section 5.2. Note that

| (3.5) |

where is the cross-entropy of a probability density function against . We use both representations (3.3) and (3.5) of the Cauchy cross-entropy in the later sections.

Recall that the cross-entropy is possibly ill-defined, in particular, if and have disjoint compact supports. We emphasize that the ESD of random matrices are approximated by compactly supported probability measures, which can have singular parts. Hence it is difficult for the usual cross-entropy to treat ESD. However, the Cauchy cross-entropy is well-defined even if the measures have compact supports.

We have the principal of minimum Cauchy cross-entropy as follows.

Proposition 3.13.

Fix . For any , it holds that

According to the principal of minimal Cauchy cross-entropy, we consider the following minimizing problem for a fixed :

| (3.6) |

where is the family of deterministic probability measures mentioned above, which approximate . In our setting, we assume that is a single-shot observation of empirical distribution for an unknown parameter ; . That is, we consider

| (3.7) |

Furthermore we show in Section 5.2 that the gap between and is small uniformly on the parameter space, and almost surely on the probability space.

Definition 3.14.

(Empirical Cauchy cross-entropy) Let be a self-adjoint random matrix and . Fix . Then the empirical Cauchy cross-entropy of against is defined as the real random variable .

Next, there are two key points to minimize the empirical risk; is accessible, and the empirical Cauchy cross-entropy is written as the following expectation.

Lemma 3.15.

Under the setting of Definition 3.11, it holds that

| (3.8) |

where are independent real random variables such that and .

Proof.

This follows from the fact that the density of is . ∎

Lemma 3.15 is the key since there are many stochastic approaches to solve minimization problem of the form

under a given parametric function and a random variable . Robbins-Monro [28] is their origin. The online gradient descent iteratively updates parameters of the model based on the gradient at a sample randomly picked from the total one at each iteration: . There are several versions of the online gradient descent, see Algorithm 1 for the detail.

Here we introduce the Cauchy noise loss;

Definition 3.16.

(Cauchy Noise Loss) For and be a self-adjoint random matrix. Let and . Then the Cauchy noise loss is defined as the random variable

| (3.9) |

where is a uniform random variable on and is a Cauchy noise of scale which is independent from .

4. Algorithm

4.1. Loss Function and Its Gradient

Infinite-dimensional operators have theoretically critical roles in our methods. However, to implement our algorithm, infinite-dimensional operators are not needed; our method works only using finite-dimensional ones. For the reader’s convenience, we summarize the results needed for the algorithm.

Remark 4.1.

Let be a singular value decomposition of , where is a unitary matrix, is a unitary matrix, and is a rectangular diagonal matrix. Then . Hence , since the joint distribution of the entries of and that of is same. Similarly, it holds that , where is a diagonalization of . Hence in the parameter estimation of CW or SPN models from each empirical spectral distribution, we cannot know such unitary matrices. Therefore, we consider the following restricted domains of parameters.

Definition 4.2.

Let with . Let us define

| (4.1) | ||||

| (4.2) |

For , we define

| (4.3) | ||||

| (4.4) |

In addition, we define

| (4.5) | ||||

| (4.6) |

where for and . Let with . We denote by the diagonal embedding defined as

| (4.7) |

We write and . To abuse the notation, we write

| (4.8) | ||||

| (4.9) |

In Definition 4.2, note that maps into and maps into .

Notation 4.3.

-

(1)

, and .

-

(2)

, .

Theorem 4.4.

There exist probability measures which satisfy the following conditions.

-

(1)

Let , , , , , and . Then -almost surely

-

(2)

Let us define the maps and by

(4.10) Let and with . Then for any initial point , we have

(4.11) where

-

(3)

for any and any unitary matrix .

-

(4)

The function is of class C∞ for any , and . In addition, is invertible, where is the derivation, for any and .

Proof.

The proof is postponed to Section 5.5. ∎

Theorem 4.5.

There exist deterministic probability measures which satisfy the following conditions.

-

(1)

For any , , and such that with and , it holds that -almost surely

-

(2)

Let and be the vector of the singular values of . Let us define and for by

Then the following operator norm limit exists;

(4.12) where the limit does not depend on the choice of the initial point . In addition, for , let us define

(4.13) and , , where . Moreover let us define a map by

(4.14) and we write . Then the following limit in the operator norm topology exists;

(4.15) and it does not depend on the choice of the initial point . Lastly, the Cauchy transform is equal to the first entry of a vector in ;

(4.16) -

(3)

for any , and any pair of unitary matrices , .

-

(4)

The function is of class C∞ for any , and . In addition, and are invertible for any , and , where and are derivations at .

Proof.

The proof is postponed to Section 5.5. ∎

Remark 4.6.

The partial derivations are computed by the derivations of implicit functions , and the chain rule, since and are invertible. For SPN model, see Corollary 5.39 of the chain rule. Now,

| (4.17) |

4.2. Optimization

Our optimization algorithm is a modification of an online gradient descent (OGD, for short), which is a stochastic approximation of gradient descent.

Remark 4.7.

If a naive OGD is applied to a convex objective function , then , where is the updated parameter, becomes after the iteration [24]. If the OGD is applied to a non-convex smooth objective function, then its gradient converges to almost surely as under some additional assumptions (see [4] for more detail). An origin of OGD is the stochastic approximation by Robbins-Monro [28].

Algorithm 1 shows the OGD-based optimization algorithm using the gradient of Cauchy noise loss. Fix a self-adjoint random matrix model and write . The algorithm requires settings of the maximum number of iterations, an update rule of the parameters of the Cauchy noise loss, the initial parameter of the model, and the bounded convex parameter space for a .

In our method, the sample is assumed to be a single-shot observation of a self-adjoint square random matrix. Through the algorithm, the scale is fixed. We consider the collection of the eigenvalues of the sample matrix. Each iteration of the algorithm consists of the following steps. We continue the iteration while .

First, we generate an index from the uniform distribution on , and generate a Cauchy noise of scale . We generate them independently throughout all iterations.

Second, we compute by (4.17).

Third, we update parameters by using the gradient of the loss function. We use Adam [18] since it requires little tuning of hyperparameters. It is defined as follows. Assume that . Let and for , Adam uses the following recurrence formula;

| (4.18) | ||||

| (4.19) | ||||

| (4.20) | ||||

| (4.21) | ||||

| (4.22) |

where the product and the division of vectors are entrywise. In addition, are constants such that , which control the exponential moving average, and is a small value for preventing division by zero. Adam adaptively estimates the first and second moments of gradients. Note that our loss function is non-convex and the convergence of Adam is proven for convex loss functions [18].

Lastly, we project parameters onto a convex parameter space .

Remark 4.8.

Adam is a diagonal method based on the empirical Fisher matrix (see [18] and [19] for the detail). The vector approximates the diagonal part of the empirical version of the Fisher information matrix. Now, the natural gradient descent [1] is based on the information geometry, which updates parameters to the direction of the steepest direction in the Fisher information metric given by the Fisher information matrix.

Note that our loss function is given by the log of the new density instead of the log of the traditional likelihood (1.3).

5. Theory

5.1. Free Deterministic Equivalents

In this section, we reformulate free deterministic equivalents introduced by Speicher-Vargas [31]. To run our algorithm, we do not require infinite-dimensional operators, but only require using finite-dimensional ones. However, infinite-dimensional operators have theoretically critical roles.

First, we summarize some definitions from operator algebras and free probability theory. See [20] for the detail.

Definition 5.1.

-

(1)

A C∗-probability space is a pair satisfying followings.

-

(a)

The set is a unital -algebra, that is, a possibly non-commutative subalgebra of the algebra of bounded -linear operators on a Hilbert space over satisfying the following conditions:

-

(i)

it is stable under the adjoint ,

-

(ii)

it is closed under the topology of the operator norm of ,

-

(iii)

it contains the identity operator as the unit of .

-

(i)

-

(b)

The function on is a faithful tracial state, that, is a -valued linear functional with

-

(i)

for any , and the equality holds if and only if ,

-

(ii)

,

-

(iii)

for any .

-

(i)

-

(a)

-

(2)

A possibly non-commutative subalgebra of a C∗-algebra is called a -subalgebra if is stable under the adjoint operator . Moreover, it is called a unital C∗-subalgebra if the -subalgebra is closed under the operator norm topology and contains as its unit.

-

(3)

Two unital -algebras are called -isomorphic if there is a bijective linear map between them which preserves the -operation and the multiplication.

-

(4)

Let us denote by the set of self-adjoint elements, that is, of .

-

(5)

Write and for any .

-

(6)

The distribution of is the probability measure determined by

-

(7)

For , we define its Cauchy transform by , equivalently, .

Definition 5.2.

A family of -subalgebras of is said to be free if the following factorization rule holds: for any and indexes with , and with , it holds that

Let be a family of self-adjoint elements . For , let be the -subalgebra of polynomials of . Then is said to be free if is free.

We introduce special elements in a non-commutative probability space.

Definition 5.3.

Let be a C∗-probability space.

-

(1)

An element is called standard semicircular if its distribution is given by the standard semicircular law;

where is the indicator function for any subset .

-

(2)

Let . An element is called circular of variance if

where is a pair of free standard semicircular elements.

-

(3)

A -free circular family (resp. standard -free circular family) is a family of circular elements such that is free (resp. and each elements is of variance ).

A free deterministic equivalent (FDE, for short) of a PGM model is constructed by replacing Ginibre matrix by matrices of circular elements.

Remark 5.4.

Equivalently, FDE is obtained by taking the limit of amplified models which is constructed by (1) copying deterministic matrices by taking a tensor product with identity and (2) each is enlarged by simply increasing the number of entries. See [31] and [35, pp.19] for the detail.

Note that the original definition of FDE treats not only Ginibre matrices but also more general random matrices.

We reformulate FDE for random matrix models.

Definition 5.5 (Free Deterministic Equivalents).

Fix a C∗-probability space . Let be a Ginibre matrix model over or of type on a subset . Then its free deterministic equivalent (FDE for short) is the map defined as

where are rectangular matrices such that the collection of all rescaled entries

is a standard -free circular family in .

In addition, if and FDE is self-adjoint for any elements in , the Cauchy transform of FDE is called the deterministic equivalent.

Now, each coefficient is multiplied for the compatibility with the normalization of Gaussian random matrices. Besides, we note that the FDE model does not depend on the field or .

Definition 5.6.

Let .

-

(1)

The free deterministic equivalent signal-plus-noise model (FDESPN model, for short) of type is defined as the FDE of . Note that

where is a standard -free circular family.

-

(2)

The free deterministic equivalent compound Wishart model (FDECW model, for short) of type is defined as the FDE of . Note that

where is a standard -free circular family.

Remark 5.7.

We reformulate the convergence of the gap between FDE and the original random matrix model in the case parameters belong to bounded sets.

Proposition 5.8.

-

(1)

Let us consider following sequences;

-

(a)

such that with and ,

-

(b)

such that and .

Then for any , it holds that -almost surely,

-

(a)

-

(2)

Let us consider following sequences;

-

(a)

such that with and ,

-

(b)

such that and ,

-

(c)

such that and .

Then for any , it holds that -almost surely,

-

(a)

Proof.

This proposition is well known. For the reader’s convenience, we prove it. Firstly let us consider the case of CW model. By the genus expansion of Ginibre matrices (see [20] for both real and complex case) and the uniform boundedness of the sequences, there are constants such that for any ,

| (5.1) |

By the expansion of the fluctuation of Ginibre matrices (see [7] for the complex case, [27] for the real case) and the uniform boundedness of the sequences, there are constants such that for any ,

| (5.2) |

As the consequence, we have for any ,

| (5.3) |

Since , the almost-sure convergence holds.

The proof for SPN model is given by the same argument. ∎

5.2. Analysis of Determination Gap

In this section we prove the determination gap, which is defined as the following, converges to -almost surely and uniformly on a bounded parameter space as the matrix size becomes large. Note that the determination gap has the same role as the generalization gap in the empirical cross-entropy method.

Definition 5.9.

(Determination Gap) Let be a self-adjoint PGM model and be its FDE. Then the deterministic gap is the real random variable defined as

| (5.4) |

where .

Basic Properties

Let us recall on the entropy for strictly positive continuous probability density functions.

Definition 5.10.

-

(1)

Let us denote by the set .

-

(2)

For any , we denote by .

-

(3)

Let with . The cross-entropy of against the reference is defined by

-

(4)

For any such that , we denote by the entropy of .

-

(5)

The relative entropy (or Kullback-Leibler divergence) of against to is defined as .

We reformulate the principle of minimum cross-entropy for as the following.

Proposition 5.11.

Let with . Then

where for a -valued function on a set which has a minimum point.

Proof.

This is well-known. Let with . Then . Hence and the equality holds if and only if , which proves the assertion. ∎

We begin by proving the Cauchy cross-entropy is well-defined.

Lemma 5.12.

For any Cauchy random variable with , the random variable has every absolute moments;

| (5.5) |

In particular, the entropy of each Cauchy random variable is well-defined.

Proof.

This lemma is well-known; this follows from the facts and , for any . ∎

Lemma 5.13.

Write for . Fix . Then the following hold.

-

(1)

For any , it holds that

-

(2)

for any , where .

-

(3)

for any and with . Hence the Cauchy cross-entropy is well-defined.

Proof.

The inequality follows from the definition. Since for all and , we have

| (5.6) |

Hence we have (1).

In addition, , which proves (2).

Let us prove (3). Let satisfy . By Tonelli’s theorem for nonnegative measurable functions and (1), we have

∎

We prove the principle of minimum Cauchy cross-entropy.

proof of Proposition 3.13.

Notation 5.14.

Write .

Note that .

Lemma 5.15.

Fix . Then and are differentiable and the followings hold.

-

(1)

.

-

(2)

.

-

(3)

For any and ,

Proof.

For any , by the Cauchy-Schwarz inequality, it holds that

| (5.7) |

and implies that . In particular, is bounded. Thus , which implies (1).

In particular, . Therefore, is differentiable and for any ,

| (5.8) |

which proves (2).

By (2), . Hence

which proves (3).

∎

Determination Gap

Here we show an asymptotic property of the determination gap. It is known that the convergence in moments of a sequence of compact support probability measures implies its weak convergence (see [3, Theorem 30.2]). First, we prove its stronger version.

Lemma 5.16.

We denote by the set of -coefficient polynomials, and write . Consider arbitrary sequence of pairs with satisfying

-

(1)

,

-

(2)

there is such that .

Then for any and , we have

Proof.

Let such that . Then where . Hence without loss of generality, we may assume that . Next, for any , let us define as

| (5.9) |

Then

| (5.10) | ||||

| (5.11) | ||||

| (5.12) |

where we used for any . Hence the sequence satisfies the condition (1). It is clear that satisfies the condition (2). Hence without loss of generality, we only need to show the following; for any ,

| (5.13) |

To show (5.13), firstly consider arbitrary subsequence . By condition (2), the sequence is tight. Therefore, there exist a further subsequence and such that converges weakly to as . By the condition (2), it holds that and . Moreover, by cutting off out of , the condition (2) also implies that converges to in moments. By (1), also converges to in moments. Since has a compact support, the distribution of is determined by its moments. Hence by [3, Thoeorem 30.2], converges weakly to . This implies that

| (5.14) |

Hence by the sub-subsequence argument, (5.13) holds. ∎

Now we are ready to state the main theorem in a general setting, which implies an asymptotic property of the determination gap.

Theorem 5.17.

Let satisfy the assumptions in Lemma 5.16. Then for any and , we have

Proof.

Fix . By Lemma 5.15(2), there is such that

| (5.15) |

Hence such and any , it holds that

By Lemma 5.15(1), the family is uniform bounded and equicontinuous in . Hence by Ascoli-Arzela’s theorem (see [9]), is totally bounded in : for any , there are such that , where . Therefore for any , it holds that

By (5.15), we have

| (5.16) |

Since as by Lemma 5.15 (1), we can apply Lemma 5.16, and there is satisfying

Hence for any , which proves the assertion.

∎

We have the following almost-sure convergence of the determination gap.

Corollary 5.18.

Proof.

By the boundedness of each parameter space, we have , where is (resp. ) or (resp. ). Then gaps of moments converge to a.s. by Proposition 5.8. Let with such that the converges holds on . Then for any , the samples of empirical distributions at satisfy the assumption of Lemma 5.16. Then the assertion follows from Theorem 5.17. ∎

Remark 5.19.

Haargerup-Thorbjørnsen [10] shows bound of the variance of a function of random matrices. Unfortunately, since they consider a family of self-adjoint Gaussian random matrices, denoted by SGM in their paper, and because we treat a non-self-adjoint Gaussian random matrix , evaluating the variance of is out of the scope of their direct application.

5.3. Iterative Methods for Cauchy Transforms

In this section, we summarize iterative methods to compute possibly operator-valued Cauchy transforms of FDE.

-transform and Iterative Method I

The first method is based on the Voiculescu’s -transform. The Cauchy transform of FDE is controlled by the -transform. See [36] for the operator theoretic definition of scalar-valued -transform and [20] for the Speicher’s definition of scalar-valued and operator-valued -transform. Here we introduce the operator-valued Cauchy transform, which is useful to know the Cauchy transform of a matrix of circular elements.

Definition 5.20.

Let be a C∗-probability space and be a unital C∗-subalgebra of . Recall that they share the unit: .

-

(1)

Then a linear operator is called a conditional expectation onto if it satisfies following conditions;

-

(a)

for any ,

-

(b)

for any and ,

-

(c)

for any .

-

(a)

-

(2)

We write and .

-

(3)

Let be a conditional expectation. For , we define a -Cauchy transform as the map , where

If there is no confusion, we also call a -valued Cauchy transform.

Here we reformulate Helton-Far-Speicher [16], which is an iterative method to compute operator-valued Cauchy transforms.

Definition 5.21.

Let be a bounded domain (i.e. connected open subset) of a Banach space and . Then maps strictly into itself if there is such that

| (5.19) |

Proposition 5.22.

Let be a C∗-subalgebra of . Assume that

| (5.20) |

where for . For any fixed , let us define the map

Then

-

(1)

.

-

(2)

For any , it holds that .

-

(3)

For any , the map sends strictly into itself.

-

(4)

The equation has a unique solution . Moreover, for any we have

where the convergence is in the operator norm topology.

Proof.

Write , , , and . Then , and . Hence the assertion follows from [16, Theorem 2.1, Proposition 3.21]. ∎

Linearization Trick and Operator-valued Semicircular Elements

To apply the above iterative method to SPN model, we use a linearization trick. Firstly we embed the model into a square matrix. Then we use the operator-valued Cauchy transform defined as the following.

Notation 5.23.

We denote by the zero matrix for and write . We denote by the identity matrix for . Let with .

-

(1)

We denote by the map determined by

(5.21) -

(2)

We write

(5.22) -

(3)

We denote by (resp. ) the upper left corner (resp. the lower right corner) of .

Notation 5.24.

For any , we write . Note that is a conditional expectation with .

Proposition 5.25.

For any , we have , where the branch of is chosen as and .

Proof.

The proof is direct forward. ∎

Summarizing the above, the computation of the operator-valued Cauchy transform of is reduced to that of .

Definition 5.26.

Let us write . The linearized FDESPN model is the map , where

Let us review operator-valued semicircular elements. See [20] for the detail.

Definition 5.27.

Let be a conditional expectation. Let with . We define the corresponding covariance mapping by

Then is called -semicircular if

Proposition 5.28.

It holds that is -semicircular and the corresponding covariance mapping is given by

| (5.23) |

Since , it holds that

Proof.

This is a direct consequence of [20, Section 9.5]. ∎

The time complexity of computing through is at least if we compute in a naive way the inverse of matrix. To reduce it, we consider another method to compute based on the subordination.

Iterative method II: Subordination

Notation 5.29.

Let us write

| (5.24) |

We denote a conditional expectation by

Note that is -isomorphic to .

Definition 5.30.

(Operator-valued Freeness) Let be a C∗-probability space, and be a conditional expectation. Let be a family of -subalgebras of such that . Then is said to be -free if the following factorization rule holds: for any and indexes with , and with , it holds that

In addition, a family of elements is called -free if the family of -subalgebra of the -coefficient polynomials of is -free.

Here we summarize observations about -valued freeness. See [20, Section 9.2] for the definition of operator-valued free cumulants.

Proposition 5.31.

The operator is -semicircular. Its covariance mapping is given by

Moreover, the pair is -free for any .

Proof.

Since , and by [20, Section 9.4, Corollary 17], it holds that is -semicircular, with covariance mapping given by .

In addition, each -valued free cumulant of (see [20, Section 9.2] for the definition) is given by the restriction of its -valued free cumulants. On the other hand, all -valued free cumulants of vanish since and . Moreover, -valued mixed free cumulants of vanish because of -freeness. Summarizing above, the restriction to of each -valued cumulants of belong to . Hence by [26, Theorem 3.1], each -valued free cumulants of is equal to the restriction to of each -valued free cumulants. In particular, all mixed -valued free cumulants of vanish, which implies -freeness. ∎

By this proposition, for any , is given by

| (5.25) |

where

By the -valued freeness, we can use the following subordination method by Belinschi-Mai-Speicher [2, Theorem 2.3].

Proposition 5.32.

Let be a C∗-probability space, and be a unital C∗-subalgebra, and be a conditional expectation. We define the -transform of with respect to by the map with .

Assume that is a -free pair of self-adjoint elements in . Write

and . Then there is so that for all ,

-

(1)

for any ,

-

(2)

,

-

(3)

.

In addition, for any fixed and with , there is depending on and so that

In particular, .

Proof.

This is a direct consequence of [2, Theorem 2.3] and the claim in its proof. ∎

Now we have another representation of the scalar-valued Cauchy transform of as the following.

Corollary 5.33.

We have . Fix with . Let and . Write , , , , where . Moreover let us define a map by

| (5.26) |

We write . Then the limit

| (5.27) |

exists, and it is independent from the choice of the initial point . Moreover,

| (5.28) | ||||

| (5.29) |

Proof.

This follows immediately from Proposition 5.32. ∎

Remark 5.34.

Note that the method described in Corollary 5.33 is performed in under the -isomorphism . In addition, this method requires two nested loops of the computation of . We note that the time complexity of the computation of is ;

| (5.30) |

where , and .

5.4. Gradients of Cauchy Transforms

We discuss the gradients of operator-valued Cauchy transforms of FDE with respect to parameters.

Definition 5.35.

Let and be C∗-algebras and be domains. Then a map is called holomorphic if for each , there is a unique bounded linear map such that

In addition, we write and .

In this section, we fix a finite dimensional C∗-algebra and write .

The following lemma is pointed out by Genki Hosono.

Lemma 5.36.

Let be a bounded domain in the finite dimensional C∗-algebra and . Assume that has a unique fixed point and for any . Then . In particular, is invertible, where is the identity map.

Proof.

Without loss of generality, we may assume that , and in particular . Let be an eigenvector of and be the corresponding eigenvalue. Fix such that . Then by Cauchy’s integral formula it holds that

| (5.31) |

Since the sequence is uniform bounded and converges to as at every point, the right hand side of (5.31) converges to by the bounded convergence theorem. Since , the left hand side of (5.31) is equal to . Hence . Since is finite-dimensional, the spectral norm is equal to the maximum of the absolute value of eigenvalues, which proves the assertion. ∎

Theorem 5.37.

Let be a non-empty open subset, and . For , let us write . Assume that following conditions:

-

(1)

Fix . Then and bounded on bounded subsets; for any ,

-

(2)

the map is of class C1 for any .

We define a map by

where we denote by the canonical coordinate on . We write . Assume that is the solution in of the equation . Then and

| (5.32) |

Proof.

By the same lemma, we show that the following theorem about the gradient of the subordination.

Theorem 5.38.

Under the setting of Proposition 5.32 with the assumption that is finite dimensional, it holds that for any .

Proof.

Corollary 5.39.

Under the setting of Corollary 5.33, we have

| (5.33) | ||||

| (5.34) |

for any , , and , where is the -valued h-transform of .

5.5. Proof of Main Theorem

Proof of Theorem 4.4.

Define for and with . Then the assertion (1) follows from Corollary 5.18. The Cauchy transform is the solution of the equation in the variable by [35, Section 6.1].

Next we claim that defined in (2) satisfies the assumption (5.20). Fix . For any , write where with . Then

| (5.35) |

It holds that

| (5.36) |

Pick , with

| (5.37) |

Then

| (5.38) |

for any with . In addition, for any ,

| (5.39) |

Thus we have

| (5.40) |

Set

| (5.41) |

Then

| (5.42) |

Therefore, maps strictly into itself: set then

| (5.43) |

Hence the claim is proven and the assertion (2) follows from Proposition 5.22.

The assertion (3) directly follows from (2).

For any and , there is a domain such that the map is holomorphic on . In addition, by Theorem 5.37, (4) follows. ∎

Proof of Theorem 4.5.

Define . The assertion (1) follows from Corollary 5.18, and (2) follows from Corollary 5.33 and the identification by the -isomorphism . The assertion (3) directly follows from (2). For any , and with , there is a domain such that and the map is holomorphic on . In addition, by Theorem 5.37 and by Theorem 5.38, (4) follows. ∎

6. Experiments and Discussion

Implementation Detail

First, we discuss numerical considerations.

The first one is about the iterative method I (see Section 5.3). As proposed in [16], when we compute the Cauchy transform (or matrix-valued one) by the iteration described in Proposition 5.22, we replace the map by the averaged version . We observed the speed up of the convergence in our examples FDECW model and FDESPN model by using the averaging. We continue the iterates while the difference is not small ; , where the norm is Euclid norm and is a given threshold. We set . In our algorithm we have to use the iterative method I for many values and is the dimension of (operator-valued) Cauchy transform. For the speed-up, we use as the initial value to compute , and use the initial value to compute .

The second one is about the iterative method II (see Section 5.3), that is, the subordination method. We do not use the averaging for iterates of in the subordination method. We continue the iterates while the difference is not small, i.e., its Euclid norm is larger than . We set the initial value used for the map to be . In particular, for SPN model, we set it . Third, for Adam (see Section 4.2), we set , , , as suggested in [18].

6.1. Optimization without Regularization

In this section, we show numerical results of optimization of CW and SPN under some values of the scale parameter . Throughout experiments, each sample is a single-shot observation generated from a true model.

Assumption

We assume the following conditions.

-

(CW1)

.

-

(CW2)

Each true parameter of CW model is generated uniformly from .

-

(CW3)

We use the parameter space with .

-

(CW4)

The initial value of the parameter is generated uniformly from .

-

(SPN1)

.

-

(SPN2)

Each sample is generated from over , where and is drawn from such that

-

(a)

are drawn independently from the uniform distribution on the orthogonal matrices,

-

(b)

is a rectangular diagonal matrix given by the array which is uniformly generated from .

-

(a)

-

(SPN3)

We use the parameter space .

-

(SPN4)

As the initial values, we set , and set to the vector of eigenvalues of the sample matrix.

Validation Loss

To evaluate the optimized parameter, we use the validation loss defined as follows.

| (6.1) | ||||

| (6.2) |

where is the sorted vector of in ascending order, is the estimated parameter. Here we compare sorted vectors because eigenvalue distributions are stable under any permutations.

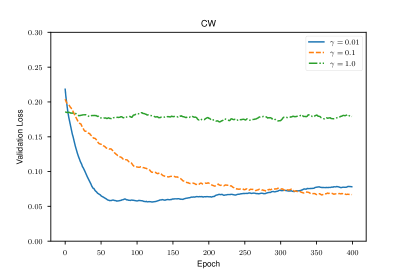

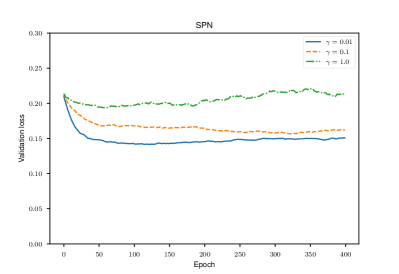

Figure 1 shows the optimization results of CW model and SPN model. The horizontal axis indicates the number of optimization epochs. We set the max iteration as for both models. The vertical axis indicates the validation loss and .

There was a difference between the scales; the smaller the scale became, the faster the validation loss decreased. For the large scale, the convergence speed became slow, or the validation loss did not converge. The significant finding is that the values of the validation loss at the stationary points did not become different so much between and . As a consequene, the parameter A does not need to be too small.

Now, Table 1 shows that the number of iterations for computing Cauchy transforms increased as the scale was set small. Besides, the number corresponding to the SPN model increased faster than that corresponding to the CW model. Therefore, it turned out that too small is not suited for the SPN model. However, the numbers for both CW and SPN models did not increase as the dimension increased. Further investigation is required to find the ideal way to choose the scale parameter .

Note that we compute the Cauchy noise loss for SPN and CW models by iterative mappings on one or two-dimensional complex vector space, and we compute their gradients by the implicit differentiation. Therefore, each step of the iterative methods and computing gradients require low time complexity concerning and .

6.2. Dimensionality Recovery

In this section, we show the dimensionality recovery method based on the optimization of SPN model by using the Cauchy noise loss with a regularization term. We assume the followings with (SPN3) and (SPN4).

-

(SPN1’)

or .

-

(SPN2’)

-

(a)

are drawn independently from the uniform distribution on the orthogonal matrices,

-

(b)

is a rectangular diagonal matrix given by the array

where are generated independently from the uniform distribution on , , and .

-

(a)

From a single-shot sample matrix, we estimate . The dimensionality recovery based on the Cauchy noise loss is as follows. To shrink small parameters to zero, we add the regularization term of , defined as the following, to the Cauchy noise loss.

| (6.3) |

In our experiments, we fixed . First, we optimize the parameters based on Algorithm 1 by using the Cauchy noise loss with the regularization term defined as

| (6.4) |

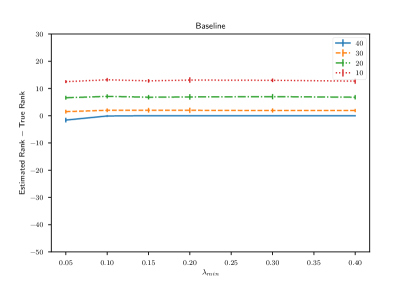

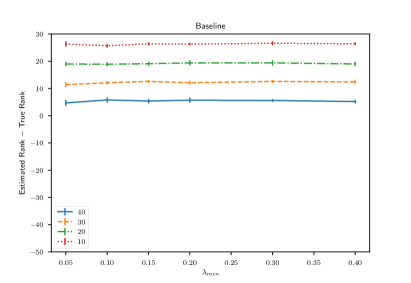

where , instead of by using the Cauchy nose loss itself. Lastly, the rank is estimated as .

We compare our method with a baseline method which consists of the following steps. First, fix . Second compute eigenvalues of an observed sample matrix. Lastly, estimate the rank of the signal part as . In our experiment, we chose a same value for all cases, based on the estimation results in the case and .

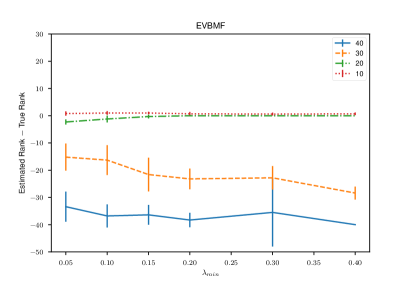

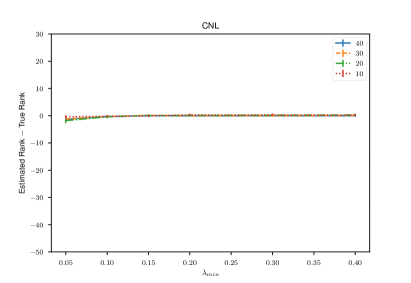

We also compare our method with the dimensionality recovery by the empirical variational Bayesian matrix factorization (EVBMF, for short) [22] [23] whose analytic solution is given by [23, Theorem 2]. We use this solution because it requires no tuning of hyperparameters, and it recovers the true rank asymptotically as the large scale limit under some assumptions [23, Theorem 13, Theorem 15].

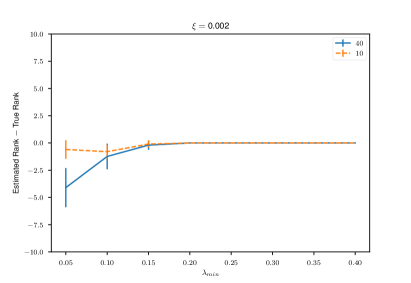

Figure 2 shows the dimensionality recovery experiments. The horizontal axis indicates . The vertical axis indicates the estimated rank minus the true rank . We observed that the baseline method did not work for all choices of under the similar setting of . However, our CNL based method recovered the true rank for all choices of and with the same . Lastly, the EVBMF recovered it if was low. We conclude that our method estimates the true rank well under a suitable setting of .

Validation Loss

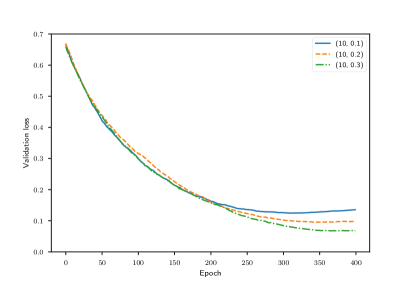

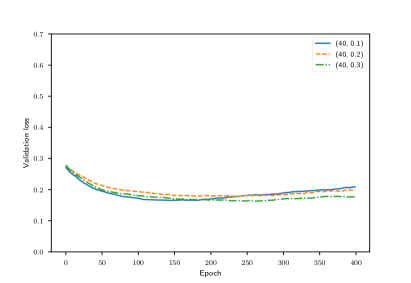

Figure 3 shows the validation loss curves under , and by the optimization via CNL. It simultaneously recovered true rank and decreased validation loss for larger . For smaller , it estimated smaller rank than and did not continue to decrease the validation loss.

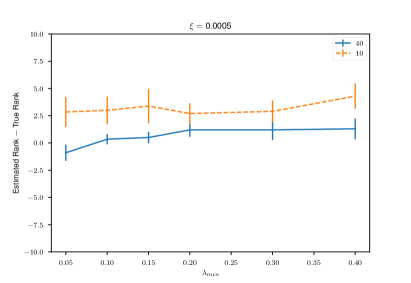

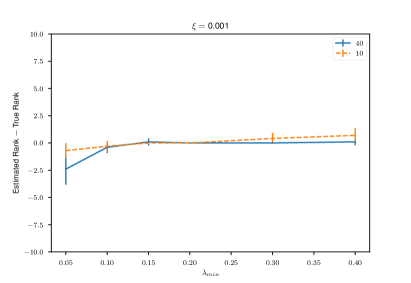

Robustness to the Change of

The regularization coefficient affects the rank estimation in the same way as that in Lasso [32]. Figure 4 shows that the dimensionality recovery for the different choices of . We set and . To see the effect of changing , in this experiment we use a consitent threshold and the number of iterations , then count and use it to estimate .

We observed that the small needed larger to recover the true rank, and a large gave unstable estimations for a small .

Then further research is also needed to determine whether the regularization term is necessary or not to the dimensionality recovery. More broadly, introducing cross-validation or a Bayesian framework of the Cauchy noise loss is also in the scope of future work.

7. Conclusion

This paper has introduced a new common framework of parameter estimation of random matrix models. The framework is a combination of the Cauchy noise loss, R-transform and the subordination, and online gradient descent.

Besides, we prove the determination gap converges uniformly to on each bounded parameter space. A vital point of the proof is that the integrand of the Cauchy cross-entropy has a bounded derivative. Based on the theoretical observation of the Cauchy cross-entropy, we introduce an optimization algorithm of random matrix models. In experiments, it turned out that too small scale parameter is deprecated. Moreover, in the application to the dimensionality recovery, our method surprisingly recovered the true rank even if the true rank was not low. However, it requires the setting of the weight of the regularization term.

This research has thrown up many questions in need of further investigation. First, we need to find an ideal way to choose the scale parameter . A possible approach is to evaluate the variance of the determination gap. Second, we need to prove the stability properties of Algorithm 1 because our loss function is non-convex. Lastly, further research is also needed to determine whether the regularization term is necessary or not the dimensionality recovery. More broadly, introducing cross-validation or an empirical Bayesian framework of Cauchy noise loss is also in the scope of future work.

Acknowledgement

The author is greatly indebted to Roland Speicher for valuable discussion and several helpful comments about free probability theory. The author wishes to express his thanks to Genki Hosono for proving a lemma about complex analysis. Kohei Chiba gives insightful comments and suggestions about probability theory. The author also wishes to express his gratitude to Hiroaki Yoshida and Noriyoshi Sakuma for fruitful discussion. The author is grateful for the travel support of Roland Speicher. Finally, the author gratefully appreciates the financial support of Benoit Collins that made it possible to complete this paper; our main idea was found during the workshop “Analysis in Quantum Information Theory”.

References

- [1] S. Amari. Natural gradient works efficiently in learning. Neural comput., 10(2):251–276, 1998.

- [2] S. T. Belinschi, T. Mai, and R. Speicher. Analytic subordination theory of operator-valued free additive convolution and the solution of a general random matrix problem. J. Reine Angew. Math., 2013.

- [3] P. Billingsley. Probability and measure. John Wiley & Sons, 2008.

- [4] L. Bottou. Online learning and stochastic approximations. pages 9–42. Cambridge Univ Pr, 1998.

- [5] M. B. Christopher. Pattern recognition and machine learning. Springer-Verlag New York, 2016.

- [6] B. Collins, D. McDonald, and N. Saad. Compound Wishart matrices and noisy covariance matrices: Risk underestimation. preprint, arXiv:1306.5510, 2013.

- [7] B. Collins, J. A. Mingo, P. Sniady, and R. Speicher. Second order freeness and fluctuations of random matrices. III. higher order freeness and free cumulants. Doc. Math, 12:1–70, 2007.

- [8] R. Couillet, M. Debbah, and J. W. Silverstein. A deterministic equivalent for the analysis of correlated mimo multiple access channels. IEEE Trans. on Inform. Theory, 57(6):3493–3514, 2011.

- [9] R. M. Dudley. Real analysis and probability, volume 74. Cambridge Univ. Press, 2002.

- [10] U. Haagerup and S. Thorbjørnsen. A new application of random matrices: Ext(C is not a group. Ann. Math., 162:711–775, 2005.

- [11] W. Hachem, P. Loubaton, X. Mestre, J. Najim, and P. Vallet. Large information plus noise random matrix models and consistent subspace estimation in large sensor networks. Random Matrices Theory Appl., 1(02):1150006, 2012.

- [12] W. Hachem, P. Loubaton, J. Najim, et al. Deterministic equivalents for certain functionals of large random matrices. Ann. Appl. Probab., 17(3):875–930, 2007.

- [13] A. Hasegawa, N. Sakuma, and H. Yoshida. Random matrices by MA models and compound free poisson laws. Probab. Math. Statist, 33(2):243–254, 2013.

- [14] A. Hasegawa, N. Sakuma, and H. Yoshida. Fluctuations of marchenko-pastur limit of random matrices with dependent entries. Statist. Probab. Lett, 127:85–96, 2017.

- [15] T. Hayase. Free deterministic equivalent z-scores of compound Wishart models: A goodness of fit test of 2DARMA models. preprint, arXiv:1710:09497, 2017.

- [16] J. W. Helton, R. R. Far, and R. Speicher. Operator-valued semicircular elements: solving a quadratic matrix equation with positivity constraints. Int. Math. Res. Not., 2007, 2007.

- [17] F. Hiai and D. Petz. The semicircle law, free random variables and entropy. Number 77. American Math. Soc., 2006.

- [18] D. P. Kingma and J. Ba. Adam: A method for stochastic optimization. in ICLR, 2015.

- [19] J. Martens. New insights and perspectives on the natural gradient method. preprint, arXiv:1412.1193, 2014.

- [20] J. A. Mingo and R. Speicher. Free probability and random matrices, volume 35. Springer, 2017.

- [21] S. Nakajima and M. Sugiyama. Theoretical analysis of Bayesian matrix factorization. J. of Mach. Learn. Res., 12:2583–2648, 2011.

- [22] S. Nakajima, M. Sugiyama, S. D. Babacan, and R. Tomioka. Global analytic solution of fully-observed variational Bayesian matrix factorization. J. Mach. Learn. Res., 14:1–37, 2013.

- [23] S. Nakajima, R. Tomioka, M. Sugiyama, and S. D. Babacan. Condition for perfect dimensionality recovery by variational Bayesian PCA. J. of Mach. Learn. Res., 16:3757–3811, 2015.

- [24] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM J. on optim., 19(4):1574–1609, 2009.

- [25] P. Neu and R. Speicher. Rigorous mean-field model for coherent-potential approximation: Anderson model with free random variables. J. Stat. Phys., 80(5):1279–1308, 1995.

- [26] A. Nica, D. Shlyakhtenko, and R. Speicher. Operator-valued distributions. I. characterizations of freeness. Int. Math. Res. Notices, 2002(29):1509–1538, 2002.

- [27] C. E. I. Redelmeier. Real second-order freeness and the asymptotic real second-order freeness of several real matrix models. Int. Math. Res. Not. IMRN., 2014(12):3353–3395, 2014.

- [28] H. Robbins and S. Monro. A stochastic approximation method. Ann. Math. Stat., 22(3):400–407, 1951.

- [29] O. Ryan and M. Debbah. Free deconvolution for signal processing applications. In IEEE Trans. Inform. Theory, pages 1846–1850. IEEE, 2007.

- [30] R. Speicher. Combinatorial theory of the free product with amalgamation and operator-valued free probability theory, volume 627. American Math. Soc., 1998.

- [31] R. Speicher and C. Vargas. Free deterministic equivalents, rectangular random matrix models, and operator-valued free probability theory. Random Matrices Theory Appl., 1(02):1150008, 2012.

- [32] R. Tibshirani. Regression shrinkage and selection via the lasso. J. Royal Stat. Series B, pages 267–288, 1996.

- [33] M. E. Tipping and C. M. Bishop. Probabilistic principal component analysis. J. Royal Stat. Soc.: Series B, 61(3):611–622, 1999.

- [34] P. Vallet, P. Loubaton, and X. Mestre. Improved subspace estimation for multivariate observations of high dimension: the deterministic signals case. IEEE Tran. Inf. Theory, 58(2):1043–1068, 2012.

- [35] C. Vargas. Free probability theory: deterministic equivalents and combinatorics. Doctoral thesis, 2015.

- [36] D. V. Voiculescu, K. J. Dykema, and A. Nica. Free random variables. Number 1. American Math. Soc., 1992.