On the Increasing Tritronquée Solutions of the Painlevé-II Equation

On the Increasing Tritronquée Solutions

of the Painlevé-II Equation††This paper is a contribution to the Special Issue on Painlevé Equations and Applications in Memory of Andrei Kapaev. The full collection is available at https://www.emis.de/journals/SIGMA/Kapaev.html

Peter D. MILLER

P.D. Miller

Department of Mathematics, University of Michigan,

East Hall, 530 Church St., Ann Arbor, MI 48109, USA

\Emailmillerpd@umich.edu

\URLaddresshttp://www.math.lsa.umich.edu/~millerpd/

Received April 11, 2018, in final form November 12, 2018; Published online November 15, 2018

The increasing tritronquée solutions of the Painlevé-II equation with parameter exhibit square-root asymptotics in the maximally-large sector and have recently appeared in applications where it is necessary to understand the behavior of these solutions for complex values of . Here these solutions are investigated from the point of view of a Riemann–Hilbert representation related to the Lax pair of Jimbo and Miwa, which naturally arises in the analysis of rogue waves of infinite order. We show that for generic complex , all such solutions are asymptotically pole-free along the bisecting ray of the complementary sector that contains the poles far from the origin. This allows the definition of a total integral of the solution along the axis containing the bisecting ray, in which certain algebraic terms are subtracted at infinity and the poles are dealt with in the principal-value sense. We compute the value of this integral for all such solutions. We also prove that if the Painlevé-II parameter is of the form , , one of the increasing tritronquée solutions has no poles or zeros whatsoever along the bisecting axis.

Painlevé-II equation; tronquée solutions

33E17; 34M40; 34M55; 35Q15

1 Introduction

The Painlevé-II equation with parameter

| (1.1) |

has been the object of intense study ever since it was identified by Painlevé more than a century ago as one of only 6 formerly unknown second-order ordinary differential equations of the form with rational in and meromorphic in having what is now called the Painlevé property: the only singularities of a solution whose location in the -plane depends on initial conditions are poles. In fact, it is now known that every solution of (1.1) is a meromorphic function of all of whose poles are simple and of residue . Since its original discovery in the context of the solution of an abstract classification problem for differential equations, the equation (1.1) and its particular solutions have become very important in numerous applications. For instance, similarity solutions of the modified Korteweg–de Vries equation satisfy (1.1) [16]. The oscillations appearing near the leading edge of the dispersive shock wave generated from a wide class of initial data in the weakly-dispersive Korteweg–de Vries equation have a universal profile corresponding to the Hastings–McLeod solution of (1.1) with [12]. The real graphs of the rational solutions of (1.1) for integer values of determine the locations of kinks in space-time near a point where generic initial data for the semiclassical sine-Gordon equation crosses the separatrix in the phase portrait of the simple pendulum in a transversal manner [9]. In mathematical physics there are also many applications of solutions of (1.1). Perhaps the most famous one concerns the distribution functions for the largest eigenvalue of random matrices from certain ensembles, which in the scaling limit can in some cases can be written in terms of again the Hastings–McLeod solution [28].

The Hastings–McLeod solution of (1.1) is especially important in applications because it is a global solution for real values of , i.e., it has no singularities for . It is an example of a so-called tronquée solution, namely one having no poles near in one or more sectors of opening angle of the complex plane. In fact, the Hastings–McLeod solution has no poles near infinity in two disjoint sectors: and . The intervening sectors symmetric about the imaginary axis are filled with poles for large , and the poles form a locally regular lattice. In general, there are two distinct types of tronquée solutions of the Painlevé-II equation (1.1). The increasing tronquée solutions satisfy as with (arising from a dominant balance between the terms and in (1.1)), and the decreasing tronquée solutions satisfy as with (arising from a dominant balance between the terms and in (1.1)). The Hastings–McLeod solution is uniquely determined as being both an increasing and a decreasing tronquée solution. Otherwise, the tronquée solutions are not generally determined by their leading asymptotics. However, for each choice of sign there is a unique solution of (1.1) for which holds as with and another unique solution for which the same asymptotic holds for . These solutions are related by the rotation symmetry of the Painlevé-II equation in which whenever is a solution, then so is . Thus there is also for each choice of sign a unique solution for which as with . These six solutions are called the increasing tritronquée solutions of (1.1) in the nomenclature of [17, Chapter 11] that can be traced back to the terminology introduced by Boutroux [7, 8].

The Painlevé-I equation also has tritronquée solutions, and these have been conjectured and/or shown to describe critical phenomena in several different situations [2, 11, 15, 24]. The tritronquée solutions of other Painlevé equations seem to not arise as frequently; however the increasing tritronquée solutions of (1.1) have recently appeared in two quite different applications. The first application is the asymptotic description of rational solutions , , , of the Painlevé-III equation

| (1.2) |

in the limit of large integer parameter . Given such , the rational solution is uniquely determined by the rationality condition and the asymptotic property as . As , the poles and zeros of accumulate within a dilation of a fixed eye-shaped domain centered at the origin and with corners at the points . In the interior of the eye-shaped domain there are accurate asymptotic formulæ for in terms of modulated elliptic functions [5]. If one examines the function near the corner point , it turns out to be natural to zoom in on the corner point by centering and rescaling the independent variable as and also to introduce a new dependent variable by . Substituting these scalings into the Painlevé-III equation (1.2) and formally considering large one finds that is a solution of an perturbation of the Painlevé-II equation (1.1) with parameter . Noting that the interior angle of the eye-shaped domain at its corners is exactly and comparing with the known asymptotic behavior of in the exterior of , in [6] the following conjecture is formulated.

Conjecture 1.1 (Bothner, Miller, and Sheng).

Let be fixed. Then

where is the unique increasing tritronquée solution of (1.1) with parameter and determined by the asymptotic behavior as with .

Thus the complementary sector in which the poles of the tritronquée solution reside for large corresponds to the interior of the eye-shaped domain in an overlap region where the Painlevé-II asymptotics and the modulated elliptic function asymptotics are simultaneously valid. Now the elliptic function asymptotics valid within are associated with an elliptic curve associated to each point of , and in [5] it is shown that the elliptic curve degenerates along the vertical segment of the imaginary axis connecting the two corner points. This degeneration makes one of the periods of the elliptic function blow up and results in a local dilution of the pole/zero distribution of when is near the vertical segment. In the overlap domain this vertical segment corresponds to the negative real axis in the variable of the Painlevé-II increasing tritronquée solution. Of course the negative real axis is precisely the ray that bisects the asymptotic pole sector for the tritronquée solution. This is one of the critical rays111This is terminology used in [25]. In other references the same rays are also called canonical rays [17, Chapters 9–10] or Stokes rays [17, Remark 7.1]. for the Painlevé-II equation (1.1), and it is well known in the case that solutions behave differently for large near such rays than elsewhere in the complex plane. See [17, Chapters 9–10], where the large- asymptotics are worked out in detail for a class of solutions for that includes the tritronquées as a particular case. However, since is an arbitrary parameter in the sequence of rational Painlevé-III solutions , to fully explain the matching between the corner asymptotics suggested by Conjecture 1.1 and the large- asymptotics of along the central axis of the eye domain , it is desirable to generalize known asymptotic results for the tritronquée solutions of (1.1) with to the setting of arbitrary . This is the aim of Theorem 1.2 below.

The second application concerns a new solution of the focusing nonlinear Schrödinger equation

| (1.3) |

which was recently identified [3] as a scaling limit of a sequence of particular solutions of the same equation modeling so-called rogue waves of increasingly higher amplitude. The special solution , the rogue wave of infinite order, has many remarkable additional properties. In particular, the function is related to a special transcendental solution of the Painlevé-III equation (1.2) with for which all Stokes multipliers of the direct monodromy problem for (1.2) vanish. In the regime of large variables , it turns out that exhibits transitional asymptotic behavior when is in the neighborhood of the critical value . In [3] it is proved that as with , the rogue wave of infinite order can be expressed explicitly in terms of a function extracted from a certain model Riemann–Hilbert problem, namely Riemann–Hilbert Problem 2.1 in Section 2 below in the case of parameters and . It is then of some practical interest to obtain some alternative and possibly more effective characterization of , and to determine its essential properties. One of the goals of this paper is to relate to the Painlevé-II equation (1.1), and to identify the particular solution needed to construct as the increasing tritronquée222We stress that the subscript in the notation is mnemonic for “tritronquée” and has nothing to do with the independent variable in (1.3). for . It is known [17, p. 297] that when , is well-defined for all real , however for to be a meaningful asymptotic description of the rogue wave of infinite order , it would be necessary that be a global solution of (1.1) also for the complex value . The global nature of tritronquée solutions of (1.1) for certain complex including this particular value is the subject of Theorem 1.4 below.

One of the earliest and most important scientific contributions of Andrei Kapaev was a systematic description of the large- asymptotics of general solutions of the Painlevé-II equation (1.1); see for example [21, 22]. These works were based on the isomonodromy method in the setting of the Flaschka–Newell Lax pair representation [16] of (1.1). Kapaev’s results were made fully rigorous for with the development by Deift and Zhou [14] of a suitable analogue of the steepest descent method adapted to matrix Riemann–Hilbert problems such as that arising in the inverse monodromy theory for (1.1). The more general results of Kapaev were later also put on rigorous footing by this method; in particular the asymptotic analysis of the increasing tronquée solutions for general is described fully for general avoiding the critical rays in [17, Chapter 11, Section 5]. Tritronquée solutions of higher-order equations in the Painlevé-II hierarchy have also been studied by Joshi and Mazzocco [20].

Despite these developments, the results needed for the applications described above do not appear to be in the literature. In this note, we try to fill this gap by proving the following results, in which we assume that , and let denote the corresponding increasing tritronquée solution of the Painlevé-II equation (1.1) characterized uniquely by the asymptotics

| (1.4) |

The uniqueness of given (1.4) combines with elementary Schwarz and odd-reflection symmetries of (1.1) to imply the following identities:

| (1.5) |

The remaining four increasing tritronquée solutions are obtained from via the cyclic symmetry group generated by .

The first result concerns the behavior of increasing tritronquée solutions as along the critical bisecting ray of the complementary sector containing the poles near infinity. Given , let and be defined as follows. Firstly, set

| (1.6) |

where to be precise the principal branch of the logarithm is meant, with imaginary part in . Then denoting by the nearest integer to with half-integers rounded down, i.e., for ,

| (1.7) |

Note that .

Theorem 1.2.

Suppose that . Then is pole free for sufficiently large negative , and the following asymptotic formulæ hold:

and

| (1.8) |

Corresponding formulæ for can be obtained from Theorem 1.2 using the symmetries (1.5) provided that or . In fact, the proof of Theorem 1.2 will show that it is also possible to obtain an asymptotic description of when , but it may be necessary to exclude certain neighborhoods of infinitely many values of where poles may exist, and the resulting formula must include more terms.

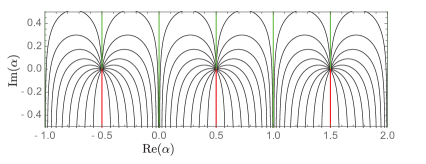

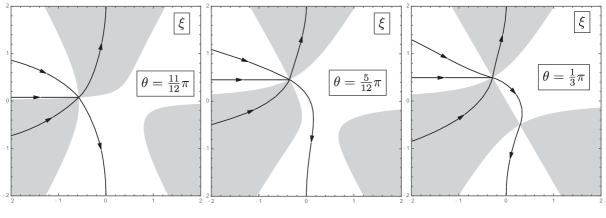

The only values of that are not covered by Theorem 1.2 are those for which . This means that , i.e., has the form where and are arbitrary parameters. No information is therefore lost by exponentiating, which leads to . It is then straightforward to determine that the excluded values of have the form for and . Similarly, the values of for which (so the asymptotics are oscillatory) correspond to , i.e., has the form where and . Therefore . The case then corresponds to while corresponds instead to for and . See Fig. 1.

Specific examples that are especially relevant include:

and, for applications to rogue waves of infinite order,

In both cases, the relevant asymptotic formula for in the limit is (1.8). In particular, we have

| (1.9) |

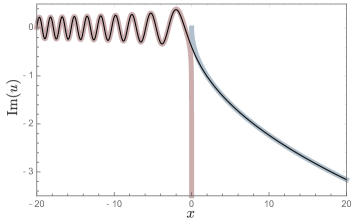

a connection formula that is well-known in the literature, cf. [17, Theorem 9.1] and [25]. In the Flaschka–Newell theory [16], the solution is associated with Stokes multipliers ; see [25]. It is striking to compare the (purely imaginary) exact solution with its asymptotic approximations for large positive and negative (see (1.4) and (1.9), respectively). To do this, we used the Mathematica package RHPackage of Olver [27] with the command PainleveII[{I,I,I},x] to obtain the numerical approximation of the solution, which we compare with the two asymptotic formulæ in Fig. 2.

The fact that the solution has simple asymptotics as suggests that, after subtracting off certain explicit terms, may be integrable over in a suitable sense. To make the definition of such an integral precise, we may recall that the only possible singularities of each solution of (1.1) are simple poles of residue , which may in principle occur along the real axis. Hence they may be taken into account by a suitable regularization of the integral. We choose the Hadamard principal value, and then we can establish the following result.

Theorem 1.3.

Suppose that , and let be such that all real poles of lie in the interval . Then the total integral formula

| (1.10) |

holds, where denotes the number of real poles of of residue , and in which the integral over is a convergent improper integral while that over is absolutely convergent.

Again, a corresponding formula for can be obtained from (1.10) using the symmetries (1.5) provided that or . Similar results have been obtained for other well-known solutions of the Painlevé-II equation such as the Hastings–McLeod and Ablowitz-Segur solutions for , see, e.g., [1], although usually such integration formulæ have been considered only for global (i.e., pole-free on the integration axis) solutions.

Next, we recall that in the setting of the rogue wave solution of infinite order, we need to consider the special complex value of and know that the solution has no poles at all on the real line. In fact, we can show more.

Theorem 1.4.

Suppose that . Then , , , and are global solutions for , i.e., they are analytic for . Moreover, they have no real zeros.

The reader may observe that, in the cases covered by Theorem 1.4, the relevant solution always has oscillatory asymptotics as according to (1.8) in Theorem 1.2, and that the leading term has infinitely many zeros in the limit. Indeed, for the indicated values of in Theorem 1.4 lie on the green half-lines emerging vertically from in Fig. 1. But whereas the solutions are purely imaginary and hence the zeros of the leading term are perturbations of actual real zeros of the solution, the tritronquée solutions that are the subject of Theorem 1.4 are essentially complex-valued. Thus, the fact that they have no real zeros simply means that the error term in (1.8) is nonzero and has a phase with a component orthogonal to that of in neighborhoods of -values satisfying for large.

The reason for excluding the half-integral values of in the above results is that the Riemann–Hilbert representation of the increasing tritronquée solution that we study below fails to yield a determinate expression for the solution in such cases333As will be seen early in Section 2, if then Riemann–Hilbert Problem 2.1 below has no solution at all, while if it has a trivial solution through which is represented as an indeterminate fraction: .. On the other hand, it was discovered by Gambier [18] and is now well-known that for , the Painlevé-II equation (1.1) is solvable via Bäcklund transformations and the general solution of the Airy equation (see [17, Chapter 11, Section 4]); the tronquée solutions of these special cases were recently studied in detail by Clarkson [13]. However, it is clear from Theorem 1.2 and Fig. 1 that the asymptotic behavior of is very sensitive to the value of near half-integers . This raises the interesting question of double-scaling asymptotics, i.e., consideration of the limits and simultaneously at appropriate related rates, a problem for the future. A different double-scaling limit related to solutions of (1.1) has been recently addressed by Bothner [4], and the joint asymptotic behavior of when and are both large has also been studied [10, 11, 23].

Finally, we formulate a corollary of the above results and their connection with Riemann–Hilbert Problem 2.1 formulated in Section 2 below that is needed in the application to rogue waves of infinite order [3].

Corollary 1.5.

The rest of this paper is organized as follows. In Section 2 we present a Riemann–Hilbert problem connected with the Jimbo–Miwa theory of the Painlevé-II equation (1.1) and use the Deift-Zhou steepest descent method to study its asymptotic behavior and therefore establish precisely which solution of the latter equation it encodes, namely the increasing tritronquée solution . Then in Sections 3, 4, and 5 we use the Riemann–Hilbert representation to prove Theorems 1.2, 1.3, and 1.4, respectively. A certain parabolic cylinder parametrix needed in Sections 2 and 3 is described in Appendix Appendix A. Parabolic cylinder function parametrix.

Notation

We use subscripts and to denote the boundary values taken by a sectionally analytic function on an oriented jump contour from the left and right sides respectively. We also make frequent use of the Pauli matrices

2 A Jimbo–Miwa representation of

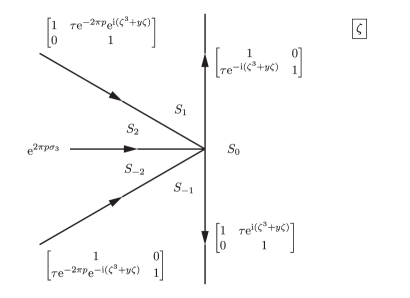

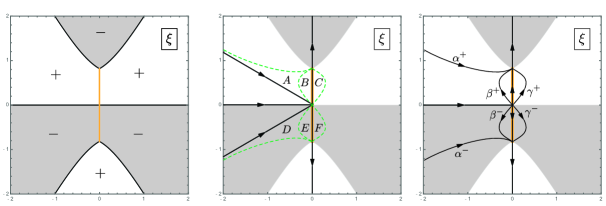

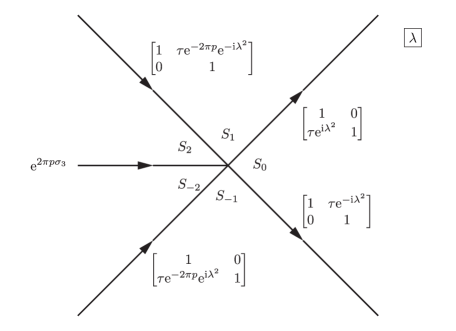

In [3], the analysis of the rogue wave of infinite order in the transitional regime where leads to consideration of a certain local model Riemann–Hilbert problem which coincides with the following in the special case of parameters and . Consider the jump contour and jump matrix shown in Fig. 3.

Riemann–Hilbert Problem 2.1 (Jimbo–Miwa Painlevé-II problem).

Let be related by . Seek a matrix-valued function with the following properties.

-

Analyticity: is analytic for in the five sectors : , : , : , : , and : . It takes continuous boundary values on the excluded rays and at the origin from each sector.

-

Jump conditions: , where is the matrix defined on the jump contour shown in Fig. 3.

-

Normalization: as uniformly in all directions.

Note that the condition ensures that the cyclic product of the jump matrices at the origin is the identity, which is a necessary condition for the continuity of the boundary values from each sector at . Noting also that all jump matrices have unit determinant, it is therefore a simple consequence of Liouville’s theorem that this problem has at most one solution, and if it exists it must have unit determinant. If then all jump matrices become the identity so given the continuity of the boundary values at the origin from each sector the solution would need to be entire; but this yields a contradiction with the normalization condition unless also . Hence there is no solution for . If it is easy to check that is the unique solution. For all other values of , the solution will exist for generic values of that avoid certain poles.

2.1 Differential equations

Given parameters and with , and assuming solvability of Riemann–Hilbert Problem 2.1 in the neighborhood of some value of , we can derive from the solution certain differential equations via the dressing construction. It is a consequence of the exponential decay to the identity of the jump matrix as that the normalization condition on holds in the stronger sense that:

| (2.1) | |||

It is easy to see that the “undressed” matrix is analytic in the same domain that is, and satisfies analogous jump conditions except that the factors in the jump matrix have been replaced in all cases by . It follows easily that and are both entire functions of whose asymptotic expansions as are easily computed from (2.1). Applying Liouville’s theorem shows that these entire functions are polynomials:

| (2.2) | |||

and from the necessarily vanishing coefficient of in the expansion of one finds that

| (2.3) |

while setting to zero the coefficient of in the expansion of gives

| (2.4) |

The latter allows (2.2) to be rewritten in terms of the matrix coefficient alone:

| (2.5) |

It is convenient to use the representation (2.2) for the diagonal terms and (2.5) for the off-diagonal terms. Thus, if

| (2.6) |

then is a simultaneous fundamental solution matrix of the two Lax pair equations:

and

These equations constitute the Lax pair for Painlevé-II found by Jimbo and Miwa [19]. The existence of a simultaneous fundamental solution matrix of both differential equations implies compatibility of the Lax pair, i.e., the coefficient matrices and necessarily satisfy the zero-curvature condition , which by direct computation is equivalent to the following coupled system for the functions and :

| (2.7) |

Combining the diagonal part of (2.3) with the off-diagonal part of (2.4) and using the identity following from yields

| (2.8) |

Since the left-hand side is independent of , so must be the right-hand side, and indeed it is straightforward to check that is a constant of motion for the system (2.7). It follows immediately that the logarithmic derivatives

| (2.9) |

satisfy uncoupled inhomogeneous Painlevé-II equations:

| (2.10) |

These two equations are simply rescaled forms of the standard Painlevé-II equation (1.1). Indeed, the function is a solution of (1.1) with parameter . Likewise, the function satisfies (1.1) with .

Remark 2.2.

Let denote the solution of Riemann–Hilbert Problem 2.1 with parameters related by . Observing that also satisfies the same relation, it is a direct matter to check that . At the level of the functions , , , and , this symmetry implies that , , , and . The latter two identities indicate that, for the purposes of studying the solutions of (2.10), or equivalently of (1.1) for , the sign of the second parameter in Riemann–Hilbert Problem 2.1 is arbitrary and can be chosen for convenience.

2.2 Asymptotic behavior for large and solution identification

When , Riemann–Hilbert Problem 2.1 determines a specific solution of each of the two Painlevé-II equations (2.10) as well as specific corresponding logarithmic “potentials” and (which would involve additional integration constants to determine from and ). The monograph [17] contains an exhaustive description of all solutions of the standard form Painlevé-II equation (1.1) in which their properties are associated with the monodromy data of a different Riemann–Hilbert problem, namely that corresponding to the alternate Lax pair discovered by Flaschka and Newell [16]. Since to our knowledge the literature does not yet contain a complete description of the relation between the monodromy data for the Lax pairs of Flaschka–Newell and Jimbo–Miwa, in order to identify the specific solutions arising we need to compute the large- asymptotic behavior directly from Riemann–Hilbert Problem 2.1 and then compare with known asymptotics of solutions catalogued in [17].

Let us write , , uniquely in the form , . Letting and setting

the conditions of Riemann–Hilbert Problem 2.1 imply an equivalent rescaled Riemann–Hilbert problem for :

Riemann–Hilbert Problem 2.3 (rescaled Painlevé-II parametrix).

Let and be given parameters. Given also a number on the unit circle and , seek a matrix-valued function with the following properties.

-

Analyticity: is analytic for in the five sectors shown in Fig. 3, now interpreted in the -plane. It takes continuous boundary values on the excluded rays and at the origin from each sector.

-

Jump conditions: , where is the same jump matrix as shown in Fig. 3 except that the exponent is everywhere replaced with , .

-

Normalization: as uniformly in all directions.

2.2.1 The case . Asymptotic behavior as

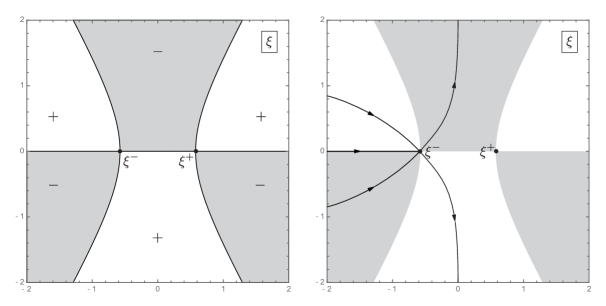

Note that has critical points . We observe that the sign table for has the structure plotted in the left-hand panel of Fig. 4.

We take the jump contour for to be deformed as shown in the right-hand panel of Fig. 4, so that in particular the self-intersection point now coincides with the left-most critical point . As an outer parametrix for we take the matrix function

| (2.11) |

which satisfies exactly the jump condition of on the ray , as well as the normalization condition on . Let denote a disk centered at of radius less than (so that it excludes the other critical point ). For , we introduce a conformal mapping that satisfies the equation

| (2.12) |

which has a unique analytic solution for which and . Assuming that when the jump contour for is taken to consist of five straight-line segments joined at the origin in the -plane with , , and , we observe that the matrix , where is the solution of the parabolic cylinder Riemann–Hilbert problem solved in the appendix, is an exact local solution of Riemann–Hilbert Problem 2.3 near . Writing the outer parametrix in the form

where we note that is analytic within and is independent of , we define the inner parametrix by the formula

We combine the outer and inner parametrices into a global parametrix defined by

Consider the error matrix defined by

| (2.13) |

Because and its parametrix satisfy exactly the same jump conditions both on the real axis to the left of and also on all jump contour arcs within the disk , it can be shown that admits analytic continuation to these contours and hence can be regarded as a function analytic in the complex -plane except on the four non-real jump contours shown in the right-hand panel of Fig. 4 restricted to the exterior of the disk, and the disk boundary where the inner and outer parametrices fail to match exactly. The jump matrix for on the resulting jump contour just described is an exponentially small perturbation of the identity matrix except when due to the placement of the contour relative to the sign chart of as shown in Fig. 4. Taking the circle to have clockwise orientation, the jump condition for expresses the mismatch between outer and inner parametrices in the form , where

| (2.14) |

where . Since the conjugating factors are bounded as while is bounded below by a multiple of when , it follows that differs from the identity uniformly on the jump contour for by . The boundary value necessarily satisfies the integral equation

| (2.15) |

which is to be solved for . Here, for a contour , denotes the right boundary value Cauchy operator defined by

where the subscript “” indicates that a nontangential limit is taken toward from the right side of by local orientation. It is well-known to be a bounded operator on for contours such as , with a norm depending only on geometrical details of the contour. Now due to the exponential decay of as along the four unbounded rays of , it is easy to see that not only (uniform estimate on ) but also ( estimate on ). It follows easily that the integral equation is uniquely solvable in with solution satisfying as . From the integral representation

the exponential decay of as in guarantees that

| (2.16) |

where

Since is also in with norm proportional to , it follows by Cauchy–Schwarz that

| (2.17) |

The contribution to the first term from integration over is exponentially small as , and therefore we may take the integration over just with no change in the order of the error estimate. Combining (2.16) with (2.13) and the identity holding for sufficiently large , recalling the definition (2.11) together with the relation and the first expansion in (2.1), we see that for sufficiently large negative ,

where for . In the case of the formula for we also used (2.4) to eliminate . To calculate , we therefore substitute (2.14) into (2.17) for , replacing the integration contour by with clockwise orientation, and use also the expansion (A.9) from the appendix to obtain:

where is given by (A.8). Since the integrand is analytic within the circle of integration aside from a simple pole at , we compute it by residues and obtain

| (2.18) |

Note that and taking two derivatives of (2.12) with and gives . Therefore, also using (A.8) to eliminate , we arrive at the asymptotic formula (1.11), which is valid for all .

Now the dominant contribution to is as . On the other hand, the dominant contribution to is calculated exactly as above, by residues. Since the integrand now has an additional factor of , it is easy to see that . We therefore conclude that

2.2.2 Generalization to complex

As soon as , the two critical points of are in general no longer on the same level of . We denote by the critical point that agrees with when . The level set undergoes a bifurcation in the neighborhood of the other critical point , when and then again when . The bifurcation at is harmless from the point of view of placing the jump contour so as to achieve exponential decay of the jump matrix to the identity relative to the neighborhood of the point . However, the bifurcations at are genuine obstructions to the basic approach valid for . The development of the problematic bifurcation as ranges over the upper (lower) half semicircle from toward (toward ) is illustrated in Fig. 5 (in Fig. 6).

These figures show that the same basic method as applies to the special case of also applies over the whole range . Mutatis mutandis, the construction of the parametrix explained in Section 2.2.1 is the same, as is the analysis of the error , and we arrive again at the asymptotic formula (2.18) for now valid for , except that has to be replaced with in the exponent and that the conformal mapping has a generalized interpretation. In general, is the conformal mapping defined near by that is chosen to depend continuously on . Therefore, , and also , so we see that (1.11) holds true as with . Similarly,

| (2.19) |

In both cases, we use the principal branch to interpret the power functions: with .

2.2.3 Solution identification

Recall that the function is a solution of the Painlevé-II equation in standard form (1.1) with parameter . From (2.19), we therefore have shown that matches the asymptotic description of the solution given in (1.4), and covering the sector . According to the analysis of the Riemann–Hilbert problem arising from the Flaschka–Newell Lax pair of Painlevé-II described in [17, Chapter 11], for each there is exactly one solution of (1.1) consistent with the asymptotic formula (1.4) (for each choice of the sign ). Thus . Having square-root asymptotics in such a large sector of the complex -plane, the solutions are two of the six increasing tritronquée solutions of (1.1) (four others are obtained by rotation symmetry in the complex -plane). Each of these six is determined by its leading asymptotic behavior in a sector of maximal opening angle . It is shown in [17] that the leading asymptotic (1.4) admits correction in the form of a full asymptotic series in decreasing powers of differing by in consecutive terms, the coefficients of which can be determined by formal substitution into the differential equation (1.1). Thus in particular it holds that

Using , this implies also that (2.19) can be improved to

| (2.20) |

The solution characterized by the asymptotic behavior (1.4) is globally meromorphic and has poles near in the complementary sector ; equivalently has poles near for . Indeed, for typical values of with , the procedure of asymptotic analysis of Riemann–Hilbert Problem 2.3 requires the introduction of a two-cut -function with one cut shrinking while approaching each of the two critical points of as (see the right-hand panels of Figs. 5 and 6). Thus the asymptotic behavior is given in terms of a certain elliptic function of with modulus depending on . Another degeneration occurs precisely when as the two cuts merge at the origin and thus become a single cut. This observation implies that the elliptic asymptotics give way to algebraic/trigonometric asymptotics in the limit , and it forms the basis for the proof of Theorem 1.2 which we turn to next.

3 Proof of Theorem 1.2

To study and in the opposite limit , we return to the consideration of as , now in the case . In this situation there is no distinction between and its modulus , so we just replace with in this section.

3.1 Introduction of -function

The critical points of form a conjugate pair, and to deal with this it turns out to be necessary to introduce a so-called -function. Define

| (3.1) |

let denote the straight line segment connecting the points , and then set

| (3.2) |

where is the function analytic for determined from the conditions while as . It is easy to confirm directly that as so is well defined by the integral

where the path of integration is arbitrary in the domain of analyticity of the integrand. It is easy to obtain the asymptotic formula

| (3.3) |

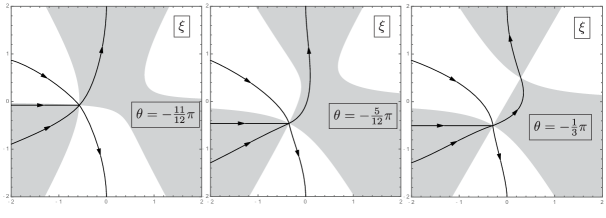

Consider the function . The left-hand panel of Fig. 7 shows the sign chart for , a function that is continuous across the branch cut , which in turn is part of the zero level set .

Moreover, it is clear from the definition of that the sum of the boundary values taken by on is . Therefore, , , is a real constant. Evaluating this constant for using the fact that is an odd function of shows that holds identically for . Since is continuous at , this implies that . However, the limiting values taken at are opposite and nonzero:

| (3.4) |

Remark 3.1.

The formula (3.2) can be motivated by the desire to enforce the condition that or equivalently that holds on . Indeed, the latter equation can be re-arranged to read , so should have no jump across and hence can be sought as an entire function. Imposing the integrability condition that as determines this entire function up to a constant as the polynomial . The formula (3.2) then corresponds to the choice . This is the only choice of for which the polynomial has two simple roots and one double root.

The central panel of Fig. 7 shows the original jump contour for together with six regions denoted , , , , , and . We use the function to give a piecewise-analytic definition of a new matrix unknown as follows:

and for we set . The resulting jump contour for is illustrated in the right-hand panel of Fig. 7. is analytic for , and across the arcs of the jump condition holds, where the jump matrix is defined as follows:

| (3.5) | |||

| (3.6) | |||

| (3.7) | |||

| (3.8) | |||

| (3.9) | |||

| (3.10) |

Due to the placement of the jump contour relative to the sign chart for illustrated in Fig. 7, the jump matrix converges exponentially fast to the identity pointwise on as , with the exception of the two halves of and the negative real line, see (3.7), (3.8), and (3.9).

3.2 Parametrix construction

3.2.1 Outer parametrix

We construct an outer parametrix to satisfy the latter jump conditions as follows. Since satisfies exactly the normalization condition as , as well as the jump condition for across the negative real axis, we seek the outer parametrix in the form and we require that as and that be analytic except on , where

| (3.11) |

and

| (3.12) |

These choices guarantee that exactly satisfies the jump conditions of described by the jump matrix in (3.7), (3.8), and (3.9). Given , observe that there exists a unique number such that solves the equation and such that the following inequalities hold:

| (3.13) |

Indeed, the relation determines modulo , and hence a unique definite value of can be chosen so that and the inequalities (3.13) hold. We are thus breaking the symmetry mentioned in the remark at the end of Section 2.1 in order to facilitate subsequent asymptotic analysis. We note that in the application of Riemann–Hilbert Problem 2.1 to rogue waves in [3], it is necessary to have for ; this amounts to choosing which is consistent with the inequalities (3.13), so we can be assured that the analysis that follows applies to that special case.

Now, given and as above, let be defined by

where the constant is defined by

Here, refers to the principal branch, and refers to the boundary value from the left by orientation of the integration contour (the direction of which is irrelevant for making and well-defined given the factor in the integrand). Thus, taking the integration in the upward direction, and parametrizing by , we have , and hence

| (3.14) |

The function is analytic for and the value of the constant is determined so that as . In fact, it is not difficult to establish that

| (3.15) |

The boundary values taken on and are continuous except at the origin, but including the other endpoints . Since changes sign across , the sum of the boundary values is easy to compute directly:

Let denote a disk of sufficiently small radius (less than will do) centered at the origin. It is straightforward to show that

| (3.16) |

where again denotes the principal branch, and where is a function analytic in the full disk . Letting denote the analytic continuation of from the right half of to all of , a formula for that admits direct evaluation for any reads

where is any sufficiently large constant, and where the contour integrals on the first two lines are taken over straight line segments. It is an exercise to show from this formula that

| (3.17) |

Now set . Then as implies that also as , and analytic in implies that the same is true for . According to (3.11), satisfies the jump condition

We take for the following solution:

| (3.18) |

This function takes continuous boundary values along except at the endpoints, where it exhibits negative fourth-root singularities. Moreover, its boundary values from the left and right half-planes admit analytic continuation into the full neighborhood . The outer parametrix is thus defined by the formula

| (3.19) |

3.2.2 Inner parametrices near

Let denote a disk of sufficiently small radius (less than ) centered at . We define a conformal mapping of onto a neighborhood of the origin by the equation

in which we understand that both sides of this equation are positive real for on the imaginary axis above . To define the conformal map, we choose the solution that is also positive for such before analytically continuing the resulting solution to . That this procedure succeeds is a consequence of the formula and the fact that since holds identically on and is continuous at .

Suppose that within the disk , the contour arcs and are merged into a single arc carrying the product of their (commuting) jump matrices (see (3.5)–(3.6)), and that this arc lies along the ray . Likewise, we take to lie within along the ray , while automatically maps the imaginary axis near to the real axis so that lies along and the imaginary axis above is taken to the positive real axis. Then, the identity implies that the jump conditions satisfied by the product (here denotes any fixed square root of ) read as follows for , where :

| (3.20) | |||

and

| (3.21) |

To properly interpret these jump conditions, note that all contours carry the orientation induced from that shown in the right-hand panel of Fig. 7 by the conformal mapping , which means that the rays in the -plane are oriented in the direction of increasing real part.

From the definition (3.19) of the outer parametrix that there exists a matrix-valued function analytic in and having unit determinant, such that

where denotes the same eigenvector matrix defined in (3.18). Because we would like to build an inner parametrix that matches well onto the outer parametrix when , we take guidance from the final two factors and define a matrix as the solution of the following Riemann–Hilbert Problem.

Riemann–Hilbert Problem 3.2 (Airy parametrix).

Seek a matrix function defined for and with the following properties:

-

Analyticity: is analytic in the four sectors indicated above, and takes continuous boundary values from each sector including at the origin.

-

Normalization: as .

This problem is well-known to have a unique solution constructed from Airy functions. The solution has the additional property that the normalization condition is strengthened to

| (3.22) |

We then define an inner parametrix for as follows:

Since is bounded away from zero and hence is proportional to when , we then get from (3.22) that

| (3.23) |

where the estimate on the last line holds in the uniform sense on the circle in the limit .

A very similar construction gives an explicit parametrix defined in a small disk centered at in terms of Airy functions, satisfying exactly the jump conditions of within the disk and for which the estimate holds uniformly on . We will require no further details of these inner parametrices.

3.2.3 Inner parametrix near

Recall the disk of sufficiently small radius centered at the origin. We define a conformal mapping in terms of within as follows. Here a slightly different approach is required because is locally two opposite analytic functions in the left and right half-disks, each of which has a simple critical point at the origin. Thus, we will define a mapping on by two different conditions:

| (3.24) |

Here, denotes the limiting value of at from the domain ; see (3.4). These conditions determine up to an overall sign as a conformal mapping of the disk with the property that . We fix the sign by insisting that . In fact, by taking two derivatives in (3.24) and setting we see that

| (3.25) |

We deform the jump contour within to ensure both that and that . The conformal mapping is real, and therefore it automatically holds that corresponds to .

Consider the matrix explicitly related to for as follows:

| (3.26) |

From this definition, it follows that

| (3.27) |

so that may be considered to be analytic on . The remaining jump conditions satisfied by are easily expressed in terms of the rescaled conformal mapping with a new independent variable . They read as follows:

| (3.28) | |||

and finally,

| (3.29) |

where all contours are oriented in the direction of increasing real part (so have been re-oriented). To confirm these jump conditions, it is necessary to use the fact that .

The jump conditions (3.27)–(3.29) match those of the parabolic cylinder function parametrix described in the appendix, provided we replace the parameters with , where (recall that is a specific number for which )

| (3.30) |

It is easy to check that the condition guarantees that also . It then follows from the definition (3.19) of the outer parametrix and from (3.16) that there exists a matrix function , independent of and having unit determinant, that is analytic in such that

Note that, in particular,

| (3.31) |

Similarly (comparing with (3.26)),

Taking into account the final factor of to obtain a good match on the boundary , we are led to construct an inner parametrix near the origin by the following formulæ

Here is the solution of Riemann–Hilbert Problem A.1 given in the appendix. We emphasize that is an exact local solution of the jump conditions for within the disk . It satisfies the mismatch condition

| (3.32) |

where .

3.3 Error analysis

The global parametrix for is defined as

In a preliminary attempt to gauge the accuracy of the approximation of by , we define the error matrix as wherever both factors are defined (note that by definition holds everywhere). Because the inner parametrices are in each case exact local solutions of the jump conditions for , it is easy to apply Morera’s theorem to deduce that can be viewed as a function analytic within all three disks: and . Similarly, because the outer parametrix exactly satisfies the jump condition for on the part of the negative real axis outside of and the parts of lying outside of all three disks, may be considered to be analytic in a neighborhood of these. Therefore, the only points of non-analyticity for correspond to jump discontinuities (i) across the portions of , , and lying outside all three disks (where is discontinuous while is analytic) and (ii) across the boundaries of the three disks (where the parametrix is discontinuous while is analytic).

For jumps of type (i), we directly compute that , where is defined on the relevant arcs by (3.5)–(3.10). The placement of the jump contour relative to the sign chart for as shown in Fig. 7, the fact that for jumps of type (i), is bounded away from the points , and the fact that the conjugating factors are uniformly bounded for such and independent of , show that .

For jumps of type (ii), if we take the disk boundaries to be oriented in the clockwise direction, it is easy to see that holds when , for all three cases . For we have from (3.23) and its analogue on that holds uniformly on . For , we combine (3.32) with formulæ (A.7)–(A.9) from the appendix and the fact that is bounded away from zero on to conclude that

| (3.33) | |||

where we have used (following from (3.4)) and where

| (3.34) |

Now the inequalities (3.13) and the definition (3.30) of show that , which implies that all matrix elements in the error term on the second line of (3.33) are as . However, the terms on the first line are larger; indeed, does not decay to zero at all as if . So it will be necessary to take that term into account explicitly in order to arrive at a small-norm problem, and it will also be convenient to remove the effect of , since for it can decay arbitrarily slowly as for near the lower end of the allowed range.

3.3.1 First parametrix for the error

Since does not decay when , to cover the whole range we must construct a parametrix for itself, which we will denote by . We want it to have the following properties. It should be analytic for , taking continuous boundary values on from the interior and exterior. It should converge to the identity as . Finally, it should satisfy the jump condition

in which the circle is taken with clockwise orientation. Given that has a simple pole at the origin, a reasonable ansatz for is that its exterior boundary value is a function with a simple pole at and that satisfies the normalization condition at infinity:

| (3.35) |

We then attempt to determine the residue by insisting that the corresponding boundary value obtained from the jump condition admit analytic continuation to the full interior of the disk . Thus,

needs to be analytic at , where we have used and (3.35) to obtain the second line. Noting that , the Laurent expansion of about is therefore

To remove the coefficient of , we will again use to express in the rank- form

| (3.36) |

and is a vector unknown yet to be determined. Using this form, two terms in the coefficient of are automatically cancelled, and the condition that this coefficient also vanish becomes

The first column is an identity, and after multiplying on the left by , the second column reads

Since is a scalar, the solution is explicitly given by

| (3.37) |

provided the denominator of the coefficient is nonzero. Since and are independent of , while as , it is clear that will be well-defined and will also satisfy if . This is a decaying estimate as . Only in the case is it even possible for to fail to exist for sufficiently large positive . In the latter case, by excluding neighborhoods of certain points, we may still assume that as . Thus it is certainly true that as with the above caveat if . Since the same holds for the inverse matrix.

3.3.2 Second parametrix for the error

We now compare the initial error matrix with its parametrix by setting . Clearly, is analytic in the same domain as is , and takes its boundary values on the jump contour in the same continuous fashion. Moreover, since we require as , we also have the corresponding condition on because as . For all points on the jump contour for omitting the circle , we use the uniform estimate on and its inverse to conclude that the previously obtained estimates of the deviation of the jump matrix for from the identity persist. Hence

| (3.39) |

where the estimate is in the sense, but the error term also decays exponentially to zero in both and along unbounded portions of . On the circle where and , we have , where

Now, using along with and the fact that over the whole range we have as , we get

where . Therefore, using (3.38) and defining ,

where again we used and took into account that and that . Therefore conjugating again by ,

| (3.40) |

This form suggests that we might finally arrive at a small-norm target problem with jump matrices uniformly deviating from the identity by if we choose to remove the term proportional to by a second parametrix for the error, which we denote by . Technically, since which is as over the whole range of values , already satisfies the conditions of a small-norm problem, but it is convenient to first construct and then compare to before obtaining estimates from small-norm theory.

Therefore, we define as the matrix analytic for , normalized to the identity as , and whose continuous boundary values on are related by the jump condition

| (3.41) |

Of course, the solution of this problem is very similar to that for , and we obtain the result that

| (3.42) |

and one can check directly that , obtained from evaluating the above expression on as and applying the jump condition (3.41), admits analytic continuation to the interior of . Unlike for which existence may require conditions on arbitrarily large if , always exists as long as is sufficiently large and .

3.3.3 Improved error analysis

We finally set

Carrying forward the conditions on sufficient to guarantee that as (no conditions needed unless in which case it may be necessary to exclude certain intervals), we can show that satisfies the conditions of a small-norm Riemann–Hilbert problem. Clearly, is analytic in the domain , where , and as as this normalization holds for both factors in the definition. It remains to estimate the difference of the jump matrix for from the identity. First note that since and are bounded uniformly for sufficiently large, it is easy to see that the estimate (3.39) implies a similar estimate for :

| (3.43) |

again with the estimate holding uniformly and also exhibiting exponential decay in both and on unbounded arcs of . Because the jump condition (3.41) for on takes into account everything except the error term in the jump matrix (3.40) for , it is easy to show that the estimate (3.43) extends also to . Through standard analysis of a system of singular integral equations equivalent to the Riemann–Hilbert conditions for (completely analogous to (2.15)) it follows that exists for sufficiently large (again with possible exclusions if ) and satisfies

| (3.44) |

where the limit may be taken in any direction, and in which the moments , , satisfy the estimate as .

Now . Provided that is sufficiently large, we may take the rational forms (3.38) and (3.42) for and respectively, and also we will have . Therefore, for such , we have the exact formula

This expression admits an asymptotic expansion in descending non-negative powers of as , i.e., of the form of the expansion in parentheses on the first line of (2.1). It is straightforward but tedious to calculate explicitly the first two coefficients and by combining (3.44), the rational expressions (3.38) and (3.42), the large- expansion of (see (3.18)):

and the expansion (see (3.3) and (3.15))

In substituting from the formulæ (3.38) and (3.42), we use the fact

which follows from (3.31) with the help of (3.14), (3.17), and (3.25), recalling also (3.1). This leads to the following exact formulæ for and :

| (3.45) |

and

where

| (3.46) |

Suppose now that , so we are excluding only the endpoint case . Then from (3.34) we see that and both decay algebraically as , so from (3.37) and (3.42) we get (also using (3.25)) that

| (3.47) |

Furthermore, this condition on guarantees that we are in the small-norm setting for , so holds for . Then, using (3.34) again we see that (3.45) becomes simply

| (3.48) |

This becomes (1.12) when , which means . Similarly, all but the terms on the first line of (3.46) are , so using (3.34) and (3.47),

The two terms in square brackets are only of equal size in the limit if . Thus, keeping only the leading term(s), there are three different asymptotic formulæ for in the limit assuming that :

and, using the identity [26, equation (5.4.3)] and the relations and ,

It is straightforward to translate these formulæ into corresponding the asymptotic formulæ for given in the statement of Theorem 1.2, where . In doing so, one must express and explicitly in terms of , or equivalently, , which results in the definitions (1.6)–(1.7). This concludes the proof of Theorem 1.2.

4 Proof of Theorem 1.3

The computation of total integrals of Painlevé-II solutions is fairly straightforward when such solutions are extracted from a Riemann–Hilbert problem associated with the Jimbo–Miwa Lax pair because the “fundamental” potentials in this setting are the quantities and (see (2.6)) whose asymptotics are easiest to compute for large and whose logarithmic derivatives yield solutions of Painlevé-II.

Since and since (2.20) gives asymptotics for as up to an error term that it absolutely integrable in this limit, it is easy to see that

holds for sufficiently negative , where is an integration constant, and where the integral in the exponent is absolutely convergent. The integration constant is easily determined from the asymptotic formula (1.11) valid for as . Therefore we have the representation

| (4.1) |

which is valid for of sufficiently large magnitude that it lies to the left of all real poles of .

Pick and so that all real poles of lie in the interval . This is possible under the hypothesis according to the defining asymptotic formula (1.4) and Theorem 1.2. Then using the formula (4.1) for and again the relation , we get the following formula, now valid for :

| (4.2) |

Here, is any contour in the complex plane from to that avoids all poles of . Now rewriting (3.48) for in the form

we compare with (4.2) and eliminate to find

| (4.3) |

Taking the limit in (4.3) yields the total integral identity

in which the integral over the interval is not generally absolutely convergent, but it necessarily makes sense as an improper integral. Suppose that we take for a real path with infinitesimal semicircular indentations in the lower half-plane centered at each real pole of . It is well-known that all poles of are simple and have residue . Therefore,

where “P.V.” denotes the Hadamard principal value and is the number of real poles of of residue .

5 Proof of Theorem 1.4

When , which also implies that , Riemann–Hilbert Problem 2.1 has a unique solution for every as a consequence of Zhou’s vanishing lemma [29]. Indeed, let us define a modified unknown as for and for . This transformation removes the jump from the negative real axis for , modifies the remaining jump matrices for by conjugation, and introduces a new diagonal jump across the unit circle. For the latter, it is convenient in the setting of [29] to take the upper and lower semicircles both to be oriented from left to right. The jump conditions for are illustrated in Fig. 8.

Now satisfies the conditions of an identity-normalized (as ) Riemann–Hilbert problem whose jump matrix is easily checked to satisfy the cyclic condition at each self-intersection point that is necessary for consistency. Moreover, when and , the jump matrix satisfies for all non-real and that is positive-definite for all real in the jump contour. The vanishing lemma [29] therefore guarantees the existence of , which also yields by inverting the substitution made for . Uniqueness of the solution is standard, as is the fact that the solution satisfies .

The existence of a solution of Riemann–Hilbert Problem 2.1 for every real when actually implies via analytic Fredholm theory that the functions and defined by (2.6) are analytic for . Moreover, these functions are Schwarz reflections of each other: . The relation (2.8) then implies that and cannot have any real zeros unless (in which case they vanish identically because ), because and would have to vanish simultaneously. The same argument shows that and cannot have any real critical points for positive real . Therefore, when , and defined by (2.9) are nonvanishing analytic functions for , and they are related by the symmetry . This implies that when , the increasing tritronquée solution of (1.1) for is globally analytic and nonvanishing for real . Applying the symmetries (1.5) for then shows that , , and are global nonvanishing solutions for whenever . This completes the proof of Theorem 1.4.

Appendix A. Parabolic cylinder function parametrix

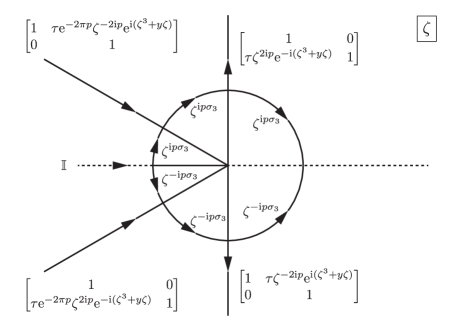

Consider the contour shown in Fig. 9 and the indicated jump matrix defined thereon.

Riemann–Hilbert Problem A.1 (parabolic cylinder parametrix).

Let be related by . Seek a matrix-valued function with the following properties.

-

Analyticity: is analytic for in the five sectors , , , , and . It takes continuous boundary values on the excluded rays and at the origin from each sector.

-

Jump conditions: , where is the matrix function defined on the jump contour shown in Fig. 9.

-

Normalization: as uniformly in all directions.

To solve Riemann–Hilbert Problem A.1, first note that there can be at most one solution, and if it exists it must have unit determinant. This problem has no solution if for the same reason as in the case of Riemann–Hilbert Problem 2.1, and its solution is if .

Therefore we now assume that , and consider the matrix . This change of variables removes the exponentials from the jump conditions, from which it follows that and satisfy exactly the same jump conditions. Appealing to invertibility and the specified regular behavior of near we see that is an entire function of . If has an asymptotic expansion as consistent with the normalization condition and hence of the form , the additional assumption that the series is differentiable term-by-term with respect to shows by a Liouville argument that ; therefore is a matrix solution of the first-order system

| (A.1) |

Eliminating the second row of and rescaling by shows that the first row elements of satisfy Weber’s equation for parabolic cylinder functions [26, equation (12.2.2)]

This differential equation has particular solutions and , and the special function is described in detail in [26, Section 12]. In each of the five sectors, the general solution can be written as a linear combination of a suitable “numerically satisfactory” fundamental pair:

The first row of the matrix differential equation (A.1) then gives the elements of the second row explicitly in terms of those of the first and their derivatives; however the derivatives can be eliminated using [26, equations (12.8.2)–(12.8.3)], and we therefore obtain

In each sector, the asymptotic expansion [26, equation (12.9.1)]:

| (A.2) |

can be used to obtain the asymptotic behavior of the matrix elements of . Since the normalization condition on forbids exponential growth, it is necessary that and for all sector indices . From the jump conditions it follows that the second column of must match between sectors and , as well as between sectors and . This implies that and that . Similarly, the first column of must match between sectors and , as well as between sectors and . This implies that and that . Lastly, the jump condition between sectors and implies that and that . Therefore, if denotes the restriction of to , we have so far found that

| (A.3) | |||

| (A.4) |

Now taking in each sector we find that the matrix satisfies the required normalization condition provided that

| (A.5) |

and that the remaining unknown coefficients are subject to the following:

| (A.6) |

Only the values of the constants and remain undetermined. It is interesting to observe that if one tries to use the definitions in (A.1) to find and from the formulæ (A.3)–(A.4) after substituting from (A.5) and (A.6) and using the asymptotic expansion (A.2) for the off-diagonal entries, one finds simply the truisms and . These constants must therefore be determined from the only other information we have not yet used: the nontrivial jumps captured by the first (resp. second) column of the jump matrix for (resp. for ). In particular, the jump condition for requires that

which given all available information is equivalent to the condition

But it is easy to check that this matches the connection formula [26, equation (12.2.18)] for the parabolic cylinder function provided that

| (A.7) |

Using (A.5) one then deduces that

| (A.8) |

At last all free parameters have been determined, and it is straightforward to verify with the use of connection formulæ for that the other jump conditions that we have not yet enforced are automatically satisfied.

Remark A.2.

In fact, the unenforced jump conditions cannot contain any further information, because the cyclic product of the jump matrices for is the identity (as must be the case for consistency at the origin). This matrix identity modulo unit determinant amounts to three conditions, which determine all of the off-diagonal entries of given any one of them.

This completes the solution of Riemann–Hilbert Problem A.1. We pause to point out that the normalization condition on indeed holds in every sense we assumed at the start in order to derive the differential equation (A.1), and therefore in particular from the asymptotic expansion (A.2),

| (A.9) |

In fact, (A.2) shows that the diagonal (resp. off-diagonal) elements have explicit asymptotic expansions in descending even (resp. odd) powers of . The full expansion of as is the same in all five sectors.

In the special case that , which also implies that , we may use the identity for the modulus of the gamma function on the imaginary axis (see [26, equation (5.4.3)]) to deduce that .

Acknowledgements

The author’s work was supported by the National Science Foundation under grants DMS-1513054 and DMS-1812625. The author thanks Thomas Bothner, Deniz Bilman, and Liming Ling for useful discussions.

References

- [1] Baik J., Buckingham R., DiFranco J., Its A., Total integrals of global solutions to Painlevé II, Nonlinearity 22 (2009), 1021–1061, arXiv:0810.2586.

- [2] Bertola M., Tovbis A., Universality for the focusing nonlinear Schrödinger equation at the gradient catastrophe point: rational breathers and poles of the tritronquée solution to Painlevé I, Comm. Pure Appl. Math. 66 (2013), 678–752, arXiv:1004.1828.

- [3] Bilman D., Ling L., Miller P.D., Extreme superposition: rogue waves of infinite order and the Painlevé-III hierarchy, arXiv:1806.00545.

- [4] Bothner T., Transition asymptotics for the Painlevé II transcendent, Duke Math. J. 166 (2017), 205–324, arXiv:1502.03402.

- [5] Bothner T., Miller P.D., Rational solutions of the Painlevé-III equation: large parameter asymptotics, arXiv:1808.01421.

- [6] Bothner T., Miller P.D., Sheng Y., Rational solutions of the Painlevé-III equation, Stud. Appl. Math. 141 (2018), 626–679, arXiv:1801.04360.

- [7] Boutroux P., Recherches sur les transcendantes de M. Painlevé et l’étude asymptotique des équations différentielles du second ordre, Ann. Sci. École Norm. Sup. 30 (1913), 255–375.

- [8] Boutroux P., Recherches sur les transcendantes de M. Painlevé et l’étude asymptotique des équations différentielles du second ordre (suite), Ann. Sci. École Norm. Sup. 31 (1914), 99–159.

- [9] Buckingham R.J., Miller P.D., The sine-Gordon equation in the semiclassical limit: critical behavior near a separatrix, J. Anal. Math. 118 (2012), 397–492, Corrigenda, J. Anal. Math. 119 (2013), 403–405, arXiv:1106.5716.

- [10] Buckingham R.J., Miller P.D., Large-degree asymptotics of rational Painlevé-II functions: noncritical behaviour, Nonlinearity 27 (2014), 2489–2578, arXiv:1310.2276.

- [11] Buckingham R.J., Miller P.D., Large-degree asymptotics of rational Painlevé-II functions: critical behaviour, Nonlinearity 28 (2015), 1539–1596, arXiv:1406.0826.

- [12] Claeys T., Grava T., Painlevé II asymptotics near the leading edge of the oscillatory zone for the Korteweg–de Vries equation in the small-dispersion limit, Comm. Pure Appl. Math. 63 (2010), 203–232, arXiv:0812.4142.

- [13] Clarkson P.A., On Airy solutions of the second Painlevé equation, Stud. Appl. Math. 137 (2016), 93–109, arXiv:1510.08326.

- [14] Deift P.A., Zhou X., Asymptotics for the Painlevé II equation, Comm. Pure Appl. Math. 48 (1995), 277–337.

- [15] Dubrovin B., Grava T., Klein C., On universality of critical behavior in the focusing nonlinear Schrödinger equation, elliptic umbilic catastrophe and the tritronquée solution to the Painlevé-I equation, J. Nonlinear Sci. 19 (2009), 57–94, arXiv:0704.0501.

- [16] Flaschka H., Newell A.C., Monodromy- and spectrum-preserving deformations. I, Comm. Math. Phys. 76 (1980), 65–116.

- [17] Fokas A.S., Its A.R., Kapaev A.A., Novokshenov V.Yu., Painlevé transcendents: the Riemann–Hilbert approach, Mathematical Surveys and Monographs, Vol. 128, Amer. Math. Soc., Providence, RI, 2006.

- [18] Gambier B., Sur les équations différentielles du second ordre et du premier degré dont l’intégrale générale est a points critiques fixes, Acta Math. 33 (1910), 1–55.

- [19] Jimbo M., Miwa T., Monodromy preserving deformation of linear ordinary differential equations with rational coefficients. II, Phys. D 2 (1981), 407–448.

- [20] Joshi N., Mazzocco M., Existence and uniqueness of tri-tronquée solutions of the second Painlevé hierarchy, Nonlinearity 16 (2003), 427–439, math.CA/0212117.

- [21] Kapaev A.A., Asymptotic expressions for the second Painlevé functions, Theoret. and Math. Phys. 77 (1988), 1227–1234.

- [22] Kapaev A.A., Global asymptotics of the second Painlevé transcendent, Phys. Lett. A 167 (1992), 356–362.

- [23] Kapaev A.A., Scaling limits in the second Painlevé transcendent, J. Math. Sci. 83 (1997), 38–61.

- [24] Lu B.-Y., Miller P.D., Universality near the gradient catastrophe point in the semiclassical sine-Gordon equation, in preparation.

- [25] Novokshenov V.Yu., Tronquée solutions of the Painlevé II equation, Theoret. and Math. Phys. 172 (2012), 1136–1146.

- [26] Olver F.W.J., Olde Daalhuis A.B., Lozier D.W., Schneider B.I., Boisvert R.F., Clark C.W., Miller B.R., Saunders B.V. (Editors), NIST digital library of mathematical functions, Release 1.0.17, 2017, available at http://dlmf.nist.gov/.

- [27] Olver S., RHPackage, Version 0.4, 2011, available at https://github.com/dlfivefifty/RHPackage.

- [28] Tracy C.A., Widom H., Level-spacing distributions and the Airy kernel, Comm. Math. Phys. 159 (1994), 151–174, hep-th/9211141.

- [29] Zhou X., The Riemann–Hilbert problem and inverse scattering, SIAM J. Math. Anal. 20 (1989), 966–986.