Abstract

We develop algorithms for computing expectations

with respect to the laws of

models associated to

stochastic differential equations (SDEs) driven by pure Lévy processes. We consider filtering such processes and well as

pricing of path dependent options.

We propose a multilevel particle filter (MLPF) to address the computational issues involved in solving these continuum problems.

We show via numerical simulations and theoretical results that under suitable assumptions regarding the discretization

of the underlying driving Lévy proccess, our proposed method achieves optimal convergence rates:

the cost to obtain MSE scales like

for our method, as compared with the standard particle filter .

Keywords: Lévy-driven SDE; Lévy processes; Particle Filters; Multilevel Particle Filters; Barrier options.

Multilevel Particle Filters for Lévy-driven stochastic differential equations

BY AJAY JASRA 1, KODY J. H. LAW 2 & PRINCE PEPRAH OSEI 1

1 Department of Statistics & Applied Probability,

National University of Singapore, Singapore, 117546, SG.

E-Mail: op.peprah@u.nus.edu, staja@nus.edu.sg

2 School of Mathematics, University of Manchester, UK, AND Computer Science and Mathematics Division, Oak Ridge National Laboratory Oak Ridge, TN, 37831, USA.

E-Mail: kodylaw@gmail.com

1 Introduction

Lévy processes have become very useful recently in several scientific disciplines. A non-exhaustive list includes physics, in the study of turbulence and quantum field theory; economics, for continuous time-series models; insurance mathematics, for computation of insurance and risk, and mathematical finance, for pricing path dependent options. Earlier application of Lévy processes in modeling financial instruments dates back in [23] where a variance gamma process is used to model market returns.

A typical computational problem in mathematical finance is the computation of the quantity , where is the time solution of a stochastic differential equation driven by a Lévy process and , a bounded Borel measurable function on . For instance can be a payoff function. Typically one uses the Black-Scholes model, in which the underlying price process is lognormal. However, often the asset price exhibits big jumps over the time horizon. The inconsistency of the assumptions of the Black-Scholes model for market data has lead to the development of more realistic models for these data in the literature. General Lévy processes offer a promising alternative to describe the observed reality of financial market data, as compared to models that are based on standard Brownian motions.

In the application of standard and multilevel particle filter methods to SDEs driven by general Lévy processes, in addition to pricing path dependent options, we will consider filtering of partially-observed Lévy process with discrete-time observations. In the latter context, we will assume that the partially-observed data are regularly spaced observations , where is a realization of and ) has density given by , where is the time scale. Real S&P stock price data will be used to illustrate our proposed methods as well as the standard particle filter. We will show how both of these problems can be formulated as general Feynman-Kac type problems [5], with time-dependent potential functions modifying the Lévy path measure.

The multilevel Monte Carlo (MLMC) methodology was introduced in [13] and first applied to the simulation of SDE driven by Brownian motion in [10]. Recently, [7] provided a detailed analysis of the application of MLMC to a Lévy-driven SDE. This first work was extended in [6] to a method with a Gaussian correction term which can substantially improve the rate for pure jump processes [2]. The authors in [9] use the MLMC method for general Lévy processes based on Wiener-Hopf decomposition. We extend the methodology described in [7] to a particle filtering framework. This is challenging due to the following reasons. First, one must choose a suitable weighting function to prevent the weights in the particle filter being zero (or infinite). Next, one must control the jump part of the underlying Lévy process such that the path of the filter does not blow up as the time parameter increases. In pricing path dependent options, for example knock out barrier options, we adopt the same strategy described in [16, 17] for the computation of the expectation of the functionals of the SDE driven by general Lévy processes.

The rest of the paper is organised as follows. In Section 2, we briefly review the construction of general Lévy processes, the numerical approximation of Lévy-driven SDEs, the MLMC method, and finally the construction of a coupled kernel for Lévy-driven SDEs which will allow MLMC to be used. Section 3 introduces both the standard and multilevel particle filter methods and their application to Lévy-driven SDEs. Section 4 features numerical examples of pricing barrier options and filtering of partially observed Lévy processes. The computational savings of the multilevel particle filter over the standard particle filter is illustrated in this section.

2 Approximating SDE driven by Lévy Processes

In this section, we briefly describe the construction and approximation of a general -dimensional Lévy process , and the solution of a -dimensional SDE driven by . Consider a stochastic differential equation given by

| (1) |

where , and the initial value is (assumed known). In particular, in the present work we are interested in computing the expectation of bounded and measurable functions , that is .

2.1 Lévy Processes

For a general detailed description of the Lévy processes and analysis of SDEs driven by Lévy processes, we shall refer the reader to the monographs of [3, 27] and [1, 24]. Lévy processes are stochastic processes with stationary and independent increments, which begin almost surely from the origin and are stochastically continuous. Two important fundamental tools available to study the richness of the class of Lévy processes are the Lévy-Khintchine formula and the Lévy-Itô decomposition. They respectively characterize the distributional properties and the structure of sample paths of the Lévy process. Important examples of Lévy processes include Poisson processes, compound Poisson processes and Brownian motions.

There is a strong interplay between Lévy processes and infinitely divisible distributions such that, for any the distribution of is infinitely divisible. Conversely, if is an infinitely divisible distribution then there exists a Lévy process such that the distribution of is given by . This conclusion is the result of Lévy-Khintchine formula for Lévy processes we describe below. Let be a Lévy process with a triplet , , where is a measure satisfying and , such that

with the probability law of , where

| (2) |

The measure is called the Lévy measure of . The triplet of Lévy characteristics is simply called Lévy triplet. Note that in general, the Lévy measure can be finite or infinite. If , then almost all paths of the Lévy process have a finite number of jumps on every compact interval and it can be represented as a compensated compound Poisson process. On the other hand, if , then the process has an infinite number of jumps on every compact interval almost surely. Even in this case the third term in the integrand ensures that the integral is finite, and hence so is the characteristic exponent.

2.2 Simulation of Lévy Processes

The law of increments of many Lévy processes is not known explicitly. This makes it more difficult to simulate a path of a general Lévy process than for instance standard Brownian motion. For a few Lévy processes where the distribution of the process is known explicitly, [4, 28] provided methods for exact simulation of such processes, which are applicable in financial modelling. For our purposes, the simulation of the path of a general Lévy process will be based on the Lévy-Itô decomposition and we briefly describe the construction below. An alternative construction is based on Wiener-Hopf decomposition. This is used in [9].

The Lévy-Itô decomposition reveals much about the structure of the paths of a Lévy process. We can split the Lévy exponent, or the characteristic exponent of in , into three parts

where

The first term corresponds to a deterministic drift process with parameter , the second term to a Wiener process with covariance , where denotes the symmetric square-root, and the last part corresponds to a Lévy process which is a square integrable martingale. This term may either be a compensated compound Poisson process or the limit of such processes, and it is the hardest to handle when it arises from such a limit.

Thus, any Lévy process can be decomposed into three independent Lévy processes thanks to the Lévy-Itô decomposition theorem. In particular, let denote a Wiener process independent of the process . A Lévy process can be constructed as follows

| (3) |

The Lévy-Itô decomposition guarantees that every square integrable Lévy process has a representation as . We will assume that one cannot sample from the law of , hence of , and rather we must numerically approximate the process with finite resolution. Such numerical methods have been studied extensively, for example in [15, 25].

It will be assumed that the Lévy process (2), and the Lévy-driven process in (1), satisfy the following conditions. Let denote the standard Euclidean norm, for vectors, and induced operator norm for matrices.

Assumption 2.1.

There exists a such that

-

(i)

, and for all ;

-

(ii)

;

-

(iii)

and .

Item (i) provides continuity of the forward map, while (ii) controls the variance of the jumps, and (iii) controls the diffusion and drift components and is trivially satisfied. These assumptions are the same as in the paper [7], with the exception of the second part of (i), which was not required there. As in that paper we refer to the following general references on Lévy processes for further details[1, 3].

2.3 Numerical Approximation of a Lévy Process and Lévy-driven SDE

Recall and . Consider the evolution of discretized Lévy process and hence the Lévy-driven SDE over the time interval .

In order to describe the Euler discretization of the two processes for a given accuracy parameter , we need some definitions. The meaning of the subscript will become clear in the next section. Let denote a jump threshold parameter in the sense that jumps which are smaller than will be ignored. Let . Define , that is the Lévy measure outside of the ball of radius . We assume that the Lévy component of the process is nontrivial so that . First will be chosen and then the parameter will be chosen such that the step-size of the time-stepping method is . The jump time increments are exponentially distributed with parameter so that the number of jumps before time is a Poisson process with intensity . The jump times will be denoted by . The jump heights are distributed according to

Define

| (4) |

The expected number of jumps on an interval of length is , and the compensated compound Poisson process defined by

is an martingale which converges in to the Lévy process as [1, 7].

The Euler discretization of the Lévy process and the Lévy driven SDE is given by Algorithm 1. Appropriate refinement of the original jump times to new jump times is necessary to control the discretization error arising from the Brownian motion component, the original drift process, and the drift component of the compound Poisson process. Note that the is non-zero only when corresponds with for some , as a consequence of the construction presented above.

-

(A)

Generate jump times: , ;

If ; Go to (B);

Otherwise ; Go to start of (A).

-

(B)

Generate jump heights:

For , ;

and ;

Set , .

-

(C)

Refinement of original jump times:

;

If for some , then ; otherwise ;

If ; Go to (D);

Otherwise ; Go to start of (C).

-

(D)

Recursion of the process:

For , ;

(5)

The numerical approximation of the Lévy process described in Algorithm 1 gives rise to an approximation of the Lévy-driven SDE as follows. Given , for

| (6) |

where is given by (5). In particular the recursion in (6) gives rise to a transition kernel, denoted by , between observation times . This kernel is the measure of given initial condition . Observe that the initial condition for is irrelevant for simulation of , since only the increments are required, which are simulated independently by adding a realization of to .

Remark 2.1.

2.4 Multilevel Monte Carlo Method

Suppose one aims to approximate the expectation of functionals of the solution of the Lévy-driven SDE in at time , that is , where is a bounded and measurable function. Typically, one is interested in the expectation w.r.t. the law of exact solution of SDE , but this is not always possible in practice. Suppose that the law associated with with no discretization is . Since we cannot sample from , we use a biased version associated with a given level of discretization of SDE at time . Given , define , the expectation with respect to the density associated with the Euler discretization at level . The standard Monte Carlo (MC) approximation at time consists in obtaining i.i.d. samples from the density and approximating by its empirical average

The mean square error of the estimator is

Since the MC estimator is an unbiased estimator for , this can further be decomposed into

| (7) |

The first term in the right hand side of the decomposition is the variance of MC simulation and the second term is the bias arising from discretization. If we want (7) to be , then it is clearly necessary to choose , and then the total cost is , where it is assumed that for some is the cost to ensure the bias is .

Now, in the multilevel Monte Carlo (MLMC) settings, one can observe that the expectation of the finest approximation can be written as a telescopic sum starting from a coarser approximation , and the intermediate ones:

| (8) |

Now it is our hope that the variance of the increments decays with , which is reasonable in the present scenario where they are finite resolution approximations of a limiting process. The idea of the MLMC method is to approximate the multilevel (ML) identity by independently computing each of the expectations in the telescopic sum by a standard MC method. This is possible by obtaining i.i.d. pairs of samples for each , from a suitably coupled joint measure with the appropriate marginals and , for example generated from a coupled simulation the Euler discretization of SDE at successive refinements. The construction of such a coupled kernel is detailed in Section 2.5. Suppose it is possible to obtain such coupled samples at time . Then for , one has independent MC estimates. Let

| (9) |

where . Analogously to the single level Monte Carlo method, the mean square error for the multilevel estimator can be expanded to obtain

| (10) |

with the convention that . It is observed that the bias term remains the same; that is we have not introduced any additional bias. However, by an optimal choice of , one can possibly reduce the computational cost for any pre-selected tolerance of the variance of the estimator, or conversely reduce the variance of the estimator for a given computational effort.

In particular, for a given user specified error tolerance measured in the root mean square error, the highest level and the replication numbers are derived as follows. We make the following assumptions about the bias, variance and computational cost based on the observation that there is an exponential decay of bias and variance as increases.

Suppose that there exist some constants and an accuracy parameter associated with the discretization of SDE at level such that

-

,

-

,

-

,

where are related to the particular choice of the discretization method and cost is the computational effort to obtain one sample . For example, the Euler-Maruyama discretization method for the solution of SDEs driven by Brownian motion gives orders . The accuracy parameter typically takes the form for some integer . Such estimates can be obtained for Lévy driven SDE and this point will be revisited in detail below. For the time being we take this as an assumption.

The key observation from the mean-square error of the multilevel estimator is that the bias is given by the finest level, while the variance is decomposed into a sum of variances of the increments. Thus the total variance is of the form and by condition above, the variance of the increment is of the form . The total computational cost takes the form . In order to minimize the effort to obtain a given mean square error (MSE), one must balance the terms in . Based on the condition above, a bias error proportional to will require the highest level

| (11) |

In order to obtain optimal allocation of resources , one needs to solve a constrained optimization problem: minimize the total cost for a given fixed total variance or vice versa. Based on the conditions and above, one obtains via the Lagrange multiplier method the optimal allocation .

Now targetting an error of size , one sets , where is chosen to control the total error for increasing . Thus, for the multilevel estimator we obtained:

| variance | |||

One then sets in order to have variance of . We can identify three distinct cases

-

(i).

If , which corresponds to the Euler-Maruyama scheme, then . One can clearly see from the expression in that . Then the total cost is compared with single level .

-

(ii).

If , which correspond to the Milstein scheme, then , and hence the optimal computational cost is .

-

(iii).

If , which is the worst case scenario, then it is sufficient to choose . In this scenario, one can easily deduce that the total cost is , where , using the fact that .

One of the defining features of the multilevel method is that the realizations for a given increment must be sufficiently coupled in order to obtain decaying variances . It is clear how to accomplish this in the context of stochastic differential equations driven by Brownian motion introduced in [10] (see also [18]), where coarse icrements are obtained by summing the fine increments, but it is non-trivial how to proceed in the context of SDEs purely driven by general Lévy processes. A technique based on Poisson thinning has been suggested by [11] for pure-jump diffusion and by [9] for general Lévy processes. In the next section, we explain an alternative construction of a coupled kernel based on the Lévy-Ito decomposition, in the same spirit as in [7].

2.5 Coupled Sampling for Levy-driven SDEs

The ML methodology described in Section 2.4 works by obtaining samples from some coupled-kernel associated with discretization of . We now describe how one can construct such a kernel associated with the discretization of the Lévy-driven SDE. Let . Define a kernel, , where denotes the -algebra of measurable subsets, such that for

| (12) | |||||

| (13) |

The coupled kernel can be constructed using the following strategy. Using the same definitions in Section 2.3, let and be user specified jump-thresholds for the fine and coarse approximation, respectively. Define

| (14) |

The objective is to generate a coupled pair given , with . The parameter will be chosen such that , and these determine the value of in (14), for . We now describe the construction of the coupled kernel and thus obtain the coupled pair in Algorithm 2, which is the same as the one presented in [7].

-

Generate fine process: Use parts (A) to (C) of Algorithm 1 to generate fine process yielding and

-

Generate coarse jump times and heights: for ,

If , then and ; ;

-

Refine jump times: Set and ,

(i) .

If , set ; else and Go to (i).

(ii) .

If , set , and redefine for ;

Else and Go to (ii).

-

Recursion of the process: sample (noting );

Let , , , and ;

| (15) | |||||

| (16) |

The construction of the coupled kernel outlined in Algorithm 2 ensures that the paths of fine and coarse processes are correlated enough to ensure that the optimal convergence rate of the multilevel algorithm is achieved.

3 Multilevel Particle Filter for Lévy-driven SDEs

In this section, the multilevel particle filter will be discussed for sampling from certain types of measures which have a density with respect to a Lévy process. We will begin by briefly reviewing the general framework and standard particle filter, and then we will extend these ideas into the multilevel particle filtering framework.

3.1 Filtering and Normalizing Constant Estimation for Lévy-driven SDEs

Recall the Lévy-driven SDE (1). We will use the following notation here . It will be assumed that the general probability density of interest is of the form for , for some given

| (17) |

where is the transition density of the process as a function of , i.e. the density of solution at observational time point given initial condition . It is assumed that is the conditional density (given ) of an observation at discrete time , so observations (which are omitted from our notations) are regularly observed at times . Note that the formulation discussed here, that is for , also allows one to consider general Feynman-Kac models (of the form (17)), rather than just the filters that are focussed upon in this section. The following assumptions will be made on the likelihood functions . Note these assumptions are needed for our later mathematical results and do not preclude the application of the algorithm to be described.

Assumption 3.1.

There are and , such that for all , and , satisfies

-

(i)

;

-

(ii)

.

In practice, as discussed earlier on is typically analytically intractable (and we further suppose is not currently known up-to a non-negative unbiased estimate). As a result, we will focus upon targets associated to a discretization, i.e. of the type

| (18) |

for , where is defined by iterates of the recursion in (6). Note that we will use as the notation for measure and density, with the use clear from the context, where .

The objective is to compute the expectation of functionals with respect to this measure, particularly at the last co-ordinate. For any bounded and measurable function , , we will use the notation

| (19) |

Often of interest is the computation of the un-normalized measure. That is, for any bounded and measurable function define, for

| (20) |

In the context of the model under study, is the marginal likelihood.

Henceforth will be used to denote a draw from . The vanilla case described earlier can be viewed as the special example in which for all . Following standard practice, realizations of random variables will be denoted with small letters. So, after drawing , then the notation will be used for later references to the realized value. The randomness of the samples will be recalled again for MSE calculations, over potential realizations.

3.2 Particle Filtering

We will describe the particle filter that is capable of exactly approximating, that is as the Monte Carlo samples go to infinity, terms of the form (19) and (20), for any fixed . The particle filter has been studied and used extensively (see for example [5, 8]) in many practical applications of interest.

For a given level , algorithm 5 gives the standard particle filter. The weights are defined as for

| (21) |

with the convention that . Note that the abbreviation stands for effective sample size which measures the variability of weights at time of the algorithm (other more efficient procedures are also possible, but not considered). In the analysis to follow in algorithm 5 (or rather it’s extension in the next section), but this is not the case in our numerical implementations.

[5] (along with many other authors) have shown that for upper-bounded, non-negative, , bounded measurable (these conditions can be relaxed), at step 3 of algorithm 5, the estimate

will converge almost surely to (19). In addition, if in algorithm 5,

will converge almost surely to (20).

-

0.

Set ; for , draw

-

1.

Compute weights using

-

2.

Compute .

If (for some threshold ), resample the particles and set all weights to . Denote the resampled particles .

Else set

-

3.

Set ; if stop;

for , draw ;

compute weights by using . Go to 2.

3.3 Multilevel Particle Filter

We now describe the multilevel particle filter of [18] for the context considered here. The basic idea is to run independent algorithms, the first a particle filter as in the previous section and the remaining, coupled particle filters. The particle filter will sequentially (in time) approximate and the coupled filters will sequentially approximate the couples . Each (coupled) particle filter will be run with particles.

The most important step in the MLPF is the coupled resampling step, which maximizes the probability of resampled indices being the same at the coarse and fine levels. Denote the coarse and fine particles at level and step as , for . Equation (21) is replaced by the following, for

| (22) | ||||

| (23) |

with the convention that .

-

(i)

Sample with probability proportional to for , where the weights are computed according to (22).

-

(ii)

Set .

-

(i)

Sample with probability proportional to for ,

-

(ii)

Sample with probability proportional to for ,

-

(iii)

Set , and .

In the below description, we set (as in algorithm 5), but it need not be the case. Recall that the case

is just a particle filter. For each the following procedure is run independently.

The samples generated by the particle filter for at time are denoted , (we are assuming ).

To estimate the quantities (19) and (20) (with ) [18, 19] show that in the case of discretized diffusion processes

and

| (24) |

converge almost surely to and respectively, as min. Furthermore, both can significantly improve over the particle filter, for and appropriately chosen to depend upon a target mean square error (MSE). By improve, we mean that the work is less than the particle filter to achieve a given MSE with respect to the continuous time limit, under appropriate assumptions on the diffusion. We show how the can be chosen in Section 3.3.1. Note that for positive the estimator above can take negative values with positive probability.

We remark that the coupled resampling method can be improved as in [29]. We also remark that the approaches of [14, 20] could potentially be used here. However, none of these articles has sufficient supporting theory to verify a reduction in cost of the ML procedure.

3.3.1 Theoretical Result

We conclude this section with a technical theorem. We consider only , but this can be extended to , similarly to [19] . The proofs are given in Appendix A.

Define as the bounded, measurable and real-valued functions on and as the globally Lipschitz real-valued functions on . Define the space with the norm .

The following assumptions will be required.

Assumption 3.2.

For all , there exists a solution to the equation , and some such that .

Denote by the coupling of the Markov transitions and , as in Algorithm 2.

Assumption 3.3.

There is a such that

-

•

,

where is the cost to simulate one sample from the kernel .

Below denotes expectation w.r.t. the law of the particle system.

4 Numerical Examples

In this section, we compare our proposed multilevel particle filter method with the vanilla particle filter method. A target accuracy parameter will be specified and the cost to achieve an error below this target accuracy will be estimated. The performance of the two algorithms will be compared in two applications of SDEs driven by general Lévy process: filtering of a partially observed Lévy process (S&P stock price data) and pricing of a path dependent option. In each of these two applications, we let denote a symmetric stable Lévy process, i.e. is a -Lévy process, and Lebesgue density of the Lévy measure given by

| (25) |

with , (the truncation threshold) and index . The parameters and are both for all the examples considered. The Lévy-driven SDE considered here has the form

| (26) |

with assumed known, and satisfies Assumption 2.1(i). Notice Assumption 2.1(ii-iii) are also satisfied by the Lévy process defined above. In the examples illustrated below, we take , and .

Remark 4.1 (Symmetric Stable Lévy process of index ).

In approximating the Lévy-driven SDE , Theorem of [7] provided asymptotic error bounds for the strong approximation by the Euler scheme. If the driving Lévy process has no Brownian component, that is , then the -error, denoted , is bounded by

and for ,

for a fixed constant (that is the Lipschitz constant), where . Recall that is chosen such that . One obtains the analytical expression

| (27) |

for some constant . One can also analytically compute

Now, setting , one obtains

| (28) |

so that the Lévy measure , hence verifying assumption 3.2 for this example. Then, one can easily bound by

for some constant . So . Using - and the error bounds for , one can straightforwardly obtain strong error rates for the approximation of SDE driven by stable Lévy process in terms of the single accuracy parameter . This is given by

Thus, if , the strong error rate of Assumption 3.3(ii) associated with a particular discretization level is given by

| (29) |

Otherwise it is just given by .

In the examples considered below, the original Lévy process has no drift and Brownian motion components, that is . Due to the linear drift correction in the compensated compound Poisson process, the random jump times are refined such that the time differences between successive jumps are bounded by the accuracy parameter associated with the Euler discretization approximation methods in and -. However, since here, due to symmetry, this does not affect the rate, as described in Remark 4.1.

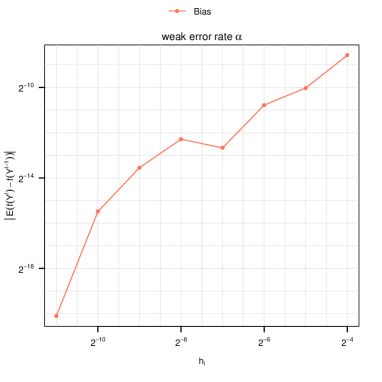

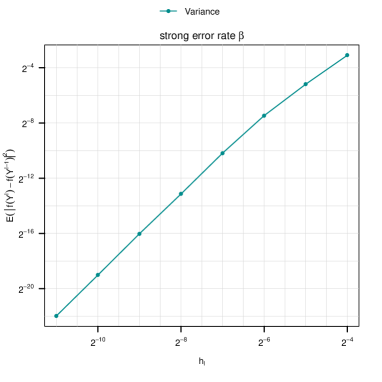

We start with verification of the weak and strong error convergence rates, and for the forward model. To this end the quantities and are computed over increasing levels . Figure 1 shows these computed values plotted against on base- logarithmic scales. A fit of a linear model gives rate , and similar simulation experiment gives . This is consistent with the rate and from Remark 4.1 .

We begin our comparison of the MLPF and PF algorithms starting with the filtering of a partially observed Lévy-driven SDE and then consider the knock out barrier call option pricing problem.

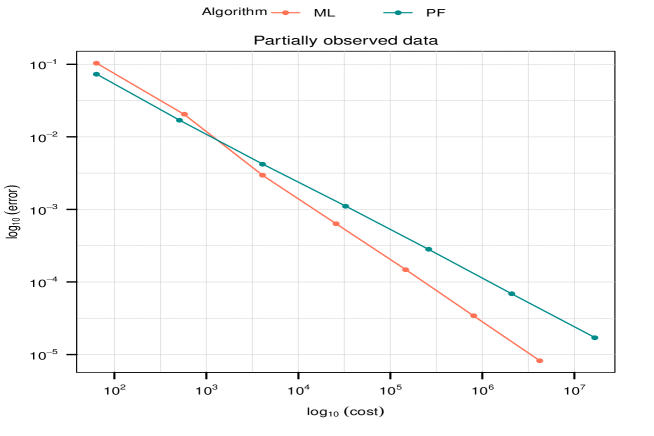

4.1 Partially observed data

In this section we consider filtering a partially observed Lévy process. Recall that the Lévy-driven SDE takes the form . In addition, partial observations are available with obtained at time and has a density function (with observation is omitted from the notation and appearing only as subscript ). The observation density is Gaussian with mean and variance 1. We aim to estimate for some test function . In this application, we consider the real daily S&P return data (from August , to July , , normalized to unity variance). We shall take the test function for the example considered below, which we note does not satisfy the assumptions of Theorem 3.1, and hence challenges the theory. In fact the results are roughly equivalent to the case , where is the indicator function on the set , which was also considered and does satisfy the required assumptions.

The error-versus-cost plots on base logarithmic scales for PF and MLPF are shown in Figure 2. The fitted linear model of MSE against Cost has a slope of and for PF and MLPF respectively. These results again verify numerically the expected theoretical asymptotic behaviour of computational cost as a function of MSE for both standard cost and ML cost.

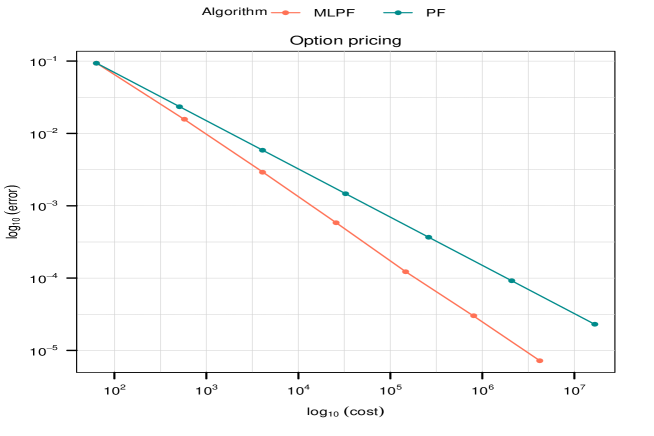

4.2 Barrier Option

Here we consider computing the value of a discretley monitored knock out barrier option (see e.g. [12] and the references therein). Let for some known and let be the transition density of the process as in (26). Then the value of the barrier option (up-to a known constant) is

for given. As seen in [16] the calculation of the barrier option is non-trivial, in the sense that even importance sampling may not work well. We consider the (time) discretized version

Define a sequence of probability densities,

| (30) |

for some non-negative collection of functions , to be specified. Recall that denotes the un-normalized density associated to . Then the value of the time discretized barrier option is exactly

| (31) |

where . Thus, we can apply the MLPF targetting the sequence and use our normalizing constant estimator (24) to estimate (31). If , then we have an optimal importance distribution, in the sense that we are estimating the integral of the constant function and the variance is minimal [26]. However, noting the form of the effective potential above (30), this can result in infinite weights (with adaptive resampling as done here), and so some regularization is necessary. We bypass this issue by choosing , where is an annealing parameter with and . We make no claim that this is the best option, but it guides us to something reminiscent of the optimal thing, and with well-behaved weights, in practice. We tried also , with , and the results are almost identical.

For this example we choose . The are chosen as in the previous example. The error-versus-cost plots for PF and MLPF are shown in Figure 3. Note that the bullets in the graph correspond to different choices of (for both PF and MLPF, ). The fitted linear model of MSE against cost has a slope of and for PF and MLPF respectively. These numerical results are consistent with the expected theoretical asymptotic behaviour of MSECost-1 for the multilevel method. The single level particle filter achieves the asymptotic behaviour of the standard Monte Carlo method with MSECost-2/3.

Acknowledgements

AJ was supported by Singapore ministry of education AcRF tier 2 grant R-155-00-161-112 and he is affiliated with the CQF, RMI and ORA cluster at NUS. He was also supported by a King Abdullah University of Science and Technology Competitive Research Grant round 4, Ref:2584. KJHL was sponsored by the Laboratory Directed Research and Development Program of Oak Ridge National Laboratory, managed by UT-Battelle, LLC, for the U. S. Department of Energy.

Appendix A Theoretical results

Our proof consists of following the proof of [18]. To that end all the proofs of [18, Appendices A-C] are the same for the approach in this article (note that one needs Lemma A.2 of this article along the way). One must verify the analogous results of [18, Appendix D], which is what is done in this appendix.

The predictor at time , level , is denoted as . Denote the total variation norm as . For , is the Lipschitz constant. For ease (in abuse) of notation, defined by iterates of the recursion in (6) is used as a Markov kernel below. We set for ,

Recall, for , is the coupling of the kernels and as in Algorithm 2. For we use the notation for :

and note that for

where denotes the tensor product of functions, e.g. denotes in the integrand associated to .

Let , and let , where is the natural continuation of the discretized Lévy process (5). Define the continuation of the discretized driven process by

Let and independently . We denote expectations w.r.t. these random variables as .

Lemma A.1.

Assume (2.1). Then there exists a such that for any , and

Proof.

Let . We have

Let be the number of time-steps before time , and denote , where and are generated by Algorithm 1. The sigma algebra generated by these random variables is denoted .

Following from the independence of and conditioned on , we have

| (32) |

The inequality is a result of the last term which uses the definition of the matrix 2 norm. Note that , so that . In addition, (4), Jensen’s inequality and the fact that , together imply that

| (33) |

We have

| (34) |

The inequality follows from Cauchy-Schwarz, definition of the matrix 2 norm, Assumption 2.1(i), (iii), and (ii) in connection with (33) and the definition of the construction of in Algorithm 1, so that .

Lemma A.2.

Assume (2.1). Then there exists a such that for any , , and

Proof.

We have

where Jensen has been applied to go to the second line and that to the third. The proof is concluded via Lemma A.1. ∎

Proof.

We have

Using Jensen’s inequality yields

Recall for there exists such that . By [7, Theorem 2], there exists such that for any ,

| (37) |

The proof is then easily concluded. ∎

Remark A.1.

Lemma A.4.

Proof.

Proposition A.1.

Proof.

References

- [1] Applebaum, D. (2004). Lévy Processes and Stochastic Calculus. Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge.

- [2] Asmussen, S. & Rosiński, J. (2001). Approximations of small jumps of Lévy processes with a view towards simulation. J. Appl. Prob. 38(2), 482–493.

- [3] Bertoin, J. (1996). Lévy Processes. Cambridge Tracts in Mathematics 121. Cambridge University Press, Cambridge.

- [4] Cont, R., & Tankov, P. (2004). Financial Modelling with Jump Processes. Chapman & Hall/CRC, Boca Raton, Financial Mathematics Series.

- [5] Del Moral, P. (2004). Feyman-Kac Formulae: Genealogical and Interacting Particle Systems with Applications. Springer: New York.

- [6] Dereich, S. (2011). Multilevel Monte Carlo Algorithms for Lévy-driven SDEs with Gaussian correction. Ann. Appl. Probab., 21(1), 283–311.

- [7] Dereich, S., & Heidenreich, F. (2011). A multilevel Monte Carlo algorithm for Lévy- driven stochastic differential equations. Stoc. Proc. Appl., 121(7), 1565–1587.

- [8] Doucet, A., De Freitas, N., & Gordon, N. J. (2001). Sequential Monte Carlo Methods in Practice. Springer: New York.

- [9] Ferreiro-Castilla, A., Kyprianou, A. E., Scheichl, & Suryanarayana, G. (2014). Multilevel Monte Carlo simulation for Lévy processes based on the Wiener-Hopf factorisation. Stoch. Proc. Appl., 124(2), 985–1010.

- [10] Giles, M. B. (2008). Multilevel Monte Carlo Path Simulation. Oper. Res 56(3), 607–617.

- [11] Giles, M. B., & Xia, Y. (2012). Multilevel path simulation for jump-diffusion SDEs. In Monte Carlo and Quasi-Monte Carlo Methods 2010 (L. Plaskota, H. Woźniakowski, Eds.), Springer, Berlin.

- [12] Glasserman, P. (2004). Monte Carlo Methods in Financial Engineering. Springer: New York.

- [13] Heinrich, S. (2001). Multilevel monte carlo methods. In Large-Scale Scientific Computing, (eds. S. Margenov, J. Wasniewski & P. Yalamov), Springer: Berlin.

- [14] Houssineau, J., Jasra, A., & Singh, SS. (2018). Multilevel Monte Carlo for smoothing via transport methods. SIAM J. Sci. Comp. (to appear).

- [15] Jacod, J., Kurtz, T. G., Méléard, S., & Protter, P. (2005). The approximate Euler method for Lévy driven stochastic differential equations. Ann. Inst. Henri Poincaré Probab. Stat. 41(3), 523–558.

- [16] Jasra, A. & Del Moral P. (2011). Sequential Monte Carlo methods for option pricing. Stoch. Anal. Appl., 29, 292–316.

- [17] Jasra, A. & Doucet A. (2009). Sequential Monte Carlo methods for diffusion processes. Proc. Roy. Soc. A, 465, 3709–3727.

- [18] Jasra, A., Kamatani, K., Law, K. J. H., & Zhou Y. (2017). Multilevel particle filters. SIAM J. Numer. Anal. 55, 3068-3096.

- [19] Jasra, A., Kamatani, K., Osei, P. P., & Zhou Y. (2018). Multilevel particle filters: Normalizing Constant Estimation. Statist. Comp. 28, 47-60.

- [20] Jacob, P. E., Lindsten, F., Schön, T. B. Coupling of Particle Filters. arXiv:1606.01156.

- [21] Kloeden, P. E. & Platen E. (1992). Numerical Solution of Stochastic Differential Equations. Springer: Berlin.

- [22] Kyprianou, A. E. (2006). Introductory Lectures on Fluctuations of Lévy processes with Applications. Springer, Berlin.

- [23] Madan, D., & Seneta, E. (1990). The variance gamma (V.G.) model for share market returns. Journal of Business, 63(4), 511–524.

- [24] Protter, P. (2004). Stochastic Integration and Differential Equations. Second Edition. Stochastic Modelling and Applied Probability 21. Springer-Verlag, Berlin.

- [25] Rubenthaler, S. (2003). Numerical simulation of the solution of a stochastic differential equation driven by a Lévy process. Stochastic Process. Appl. 103(2), 311–349.

- [26] Rubinstein, R.Y. and Kroese, D.P. (2016). Simulation and the Monte Carlo method (Vol. 10). John Wiley & Sons.

- [27] Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge studies in Advanced Mathematics 68. Cambridge University Press, Cambridge.

- [28] Schoutens, W. (2003). Lévy Processes in Finance: Pricing Financial Derivatives. Wiley, Chichester.

- [29] Sen, D., Thiery, A., & Jasra A. (2018). On coupling particle filter trajectories. Statist. Comp. (to appear).