The goal of a recommendation system is to predict the interest of a user in a given item by exploiting the existing set of ratings as well as certain user/item features. A standard approach to modeling this problem is Inductive Matrix Completion where the predicted rating is modeled as an inner product of the user and the item features projected onto a latent space. In order to learn the parameters effectively from a small number of observed ratings, the latent space is constrained to be low-dimensional which implies that the parameter matrix is constrained to be low-rank.

However, such bilinear modeling of the ratings can be limiting in practice and non-linear prediction functions can lead to significant improvements. A natural approach to introducing non-linearity in the prediction function is to apply a non-linear activation function on top of the projected user/item features.

Imposition of non-linearities further complicates an already challenging problem that has two sources of non-convexity: a) low-rank structure of the parameter matrix, and b) non-linear activation function. We show that one can still solve the non-linear Inductive Matrix Completion problem using gradient descent type methods as long as the solution is initialized well. That is, close to the optima, the optimization function is strongly convex and hence admits standard optimization techniques, at least for certain activation functions, such as Sigmoid and tanh. We also highlight the importance of the activation function and show how ReLU can behave significantly differently than say a sigmoid function. Finally, we apply our proposed technique to recommendation systems and semi-supervised clustering, and show that our method can lead to much better performance than standard linear Inductive Matrix Completion methods.

1 Introduction

Matrix Completion (MC) or Collaborative filtering [CR09, GUH16] is by now a standard technique to model recommendation systems problems where a few user-item ratings are available and the goal is to predict ratings for any user-item pair. However, standard collaborative filtering suffers from two drawbacks: 1) Cold-start problem: MC can’t give prediction for new users or items, 2) Missing side-information: MC cannot leverage side-information that is typically present in recommendation systems such as features for users/items. Consequently, several methods [ABEV06, Ren10, XJZ13, JD13] have been proposed to leverage the side information together with the ratings. Inductive matrix completion (IMC) [ABEV06, JD13] is one of the most popular methods in this class.

IMC models the ratings as the inner product between certain linear mapping of the user/items’ features, i.e., , where is the predicted rating of user for item , are the feature vectors. Parameters () can typically be learned using a small number of observed ratings [JD13].

However, the bilinear structure of IMC is fairly simplistic and limiting in practice and might lead to fairly poor accuracy on real-world recommendation problems. For example, consider the Youtube recommendation system [CAS16] that requires predictions over videos. Naturally, a linear function over the pixels of videos will lead to fairly inaccurate predictions and hence one needs to model the videos using non-linear networks. The survey paper by [ZYS17] presents many more such examples, where we need to design a non-linear ratings prediction function for the input features, including [LLL+16] for image recommendation, [WW14] for music recommendation and [ZYL+16] for recommendation systems with multiple types of inputs.

We can introduce non-linearity in the prediction function using several standard techniques, however, if our parameterization admits too many free parameters then learning them might be challenging as the number of available user-item ratings tend to be fairly small. Instead, we use a simple non-linear extension of IMC that can control the number of parameters to be estimated. Note that IMC based prediction function can be viewed as an inner product between certain latent user-item features where the latent features are a linear map of the raw user-item features. To introduce non-linearity, we can use a non-linear mapping of the raw user-item features rather than the linear mapping used by IMC. This leads to the following general framework that we call non-linear inductive matrix completion (NIMC),

|

|

|

(1) |

where are the feature vectors, is their rating and are non-linear mappings from the raw feature space to the latent space.

The above general framework reduces to standard inductive matrix completion when are linear mappings and further reduces to matrix completion when are unit vectors for -th item and -th user respectively. When is used as the feature vector and is restricted to be a two-block (one for and the other for ) diagonal matrix, then the above framework reduces to the dirtyIMC model [CHD15]. Similarly, can also be neural networks (NNs),

such as feedforward NNs [SCH+16, CAS16], convolutional NNs for images and recurrent NNs for speech/text.

In this paper, we focus on a simple nonlinear activation based mapping for the user-item features. That is, we set and where is a nonlinear activation function . Note that if is ReLU then the latent space is guaranteed to be in non-negative orthant which in itself can be a desirable property for certain recommendation problems.

Note that parameter estimation in both IMC and NIMC models is hard due to non-convexity of the corresponding optimization problem. However, for "nice" data, several strong results are known for the linear models, such as [CR09, JNS13, GJZ17] for MC and [JD13, XJZ13, CHD15] for IMC. However, non-linearity in NIMC models adds to the complexity of an already challenging problem and has not been studied extensively, despite its popularity in practice.

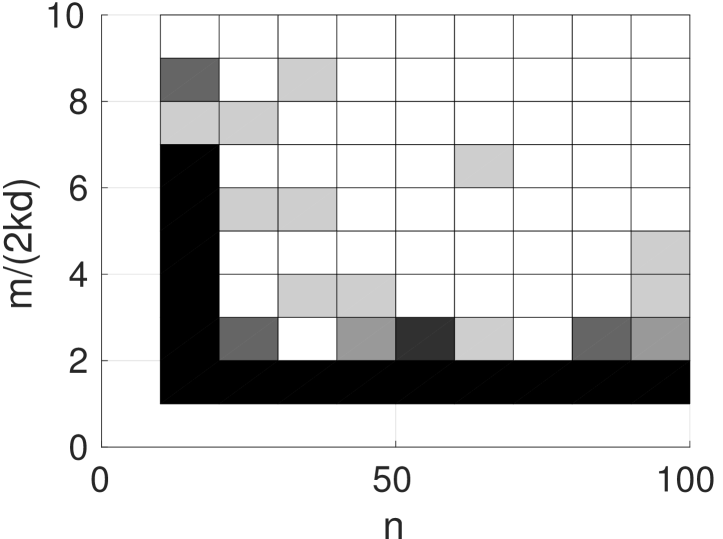

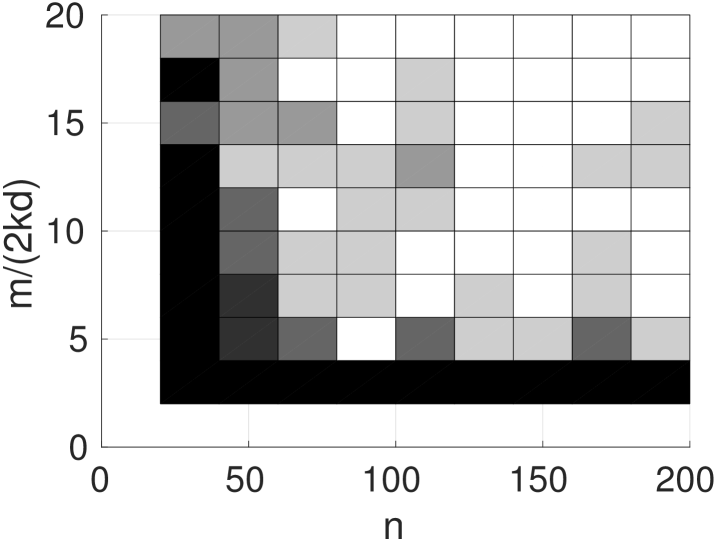

In this paper, we study a simple one-layer neural network style NIMC model mentioned above. In particular, we formulate a squared-loss based optimization problem for estimating parameters and . We show that under a realizable model and Gaussian input assumption, the objective function is locally strongly convex within a "reasonably large" neighborhood of the ground truth. Moreover, we show that the above strong convexity claim holds even if the number of observed ratings is nearly-linear in dimension and polynomial in the conditioning of the weight matrices. In particular, for well-conditioned matrices, we can recover the underlying parameters using only user-item ratings, which is critical for practical recommendation systems as they tend to have very few ratings available per user. Our analysis covers popular activation functions, e.g., sigmoid and ReLU, and discuss various subtleties that arise due to the activation function. Finally we discuss how we can leverage standard tensor decomposition techniques to initialize our parameters well. We would like to stress that practitioners typically use random initialization itself, and hence results studying random initialization for NIMC model would be of significant interest.

As mentioned above, due to non-linearity of activation function along with non-convexity of the parameter space, the existing proof techniques do not apply directly to the problem. Moreover, we have to carefully argue about both the optimization landscape as well as the sample complexity of the algorithm which is not carefully studied for neural networks. Our proof establishes some new techniques that might be of independent interest, e.g., how to handle the redundancy in the parameters for ReLU activation. To the best of our knowledge, this is one of the first theoretically rigorous study of neural-network based recommendation systems and will hopefully be a stepping stone for similar analysis for "deeper" neural networks based recommendation systems. We would also like to highlight that our model can be viewed as a strict generalization of a one-hidden layer neural network, hence our result represents one of the few rigorous guarantees for models that are more powerful than one-hidden layer neural networks [LY17, BGMSS18, ZSJ+17].

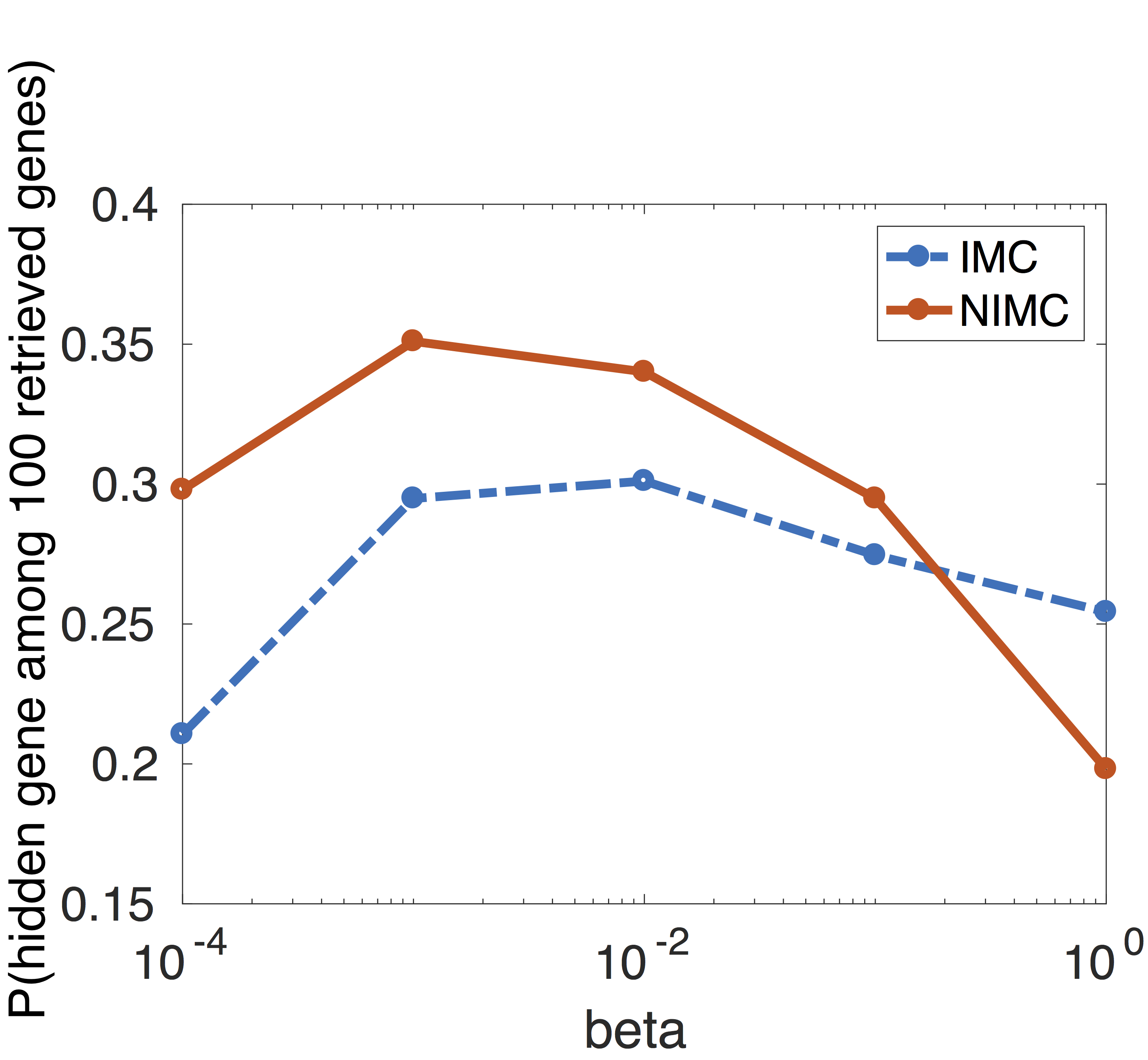

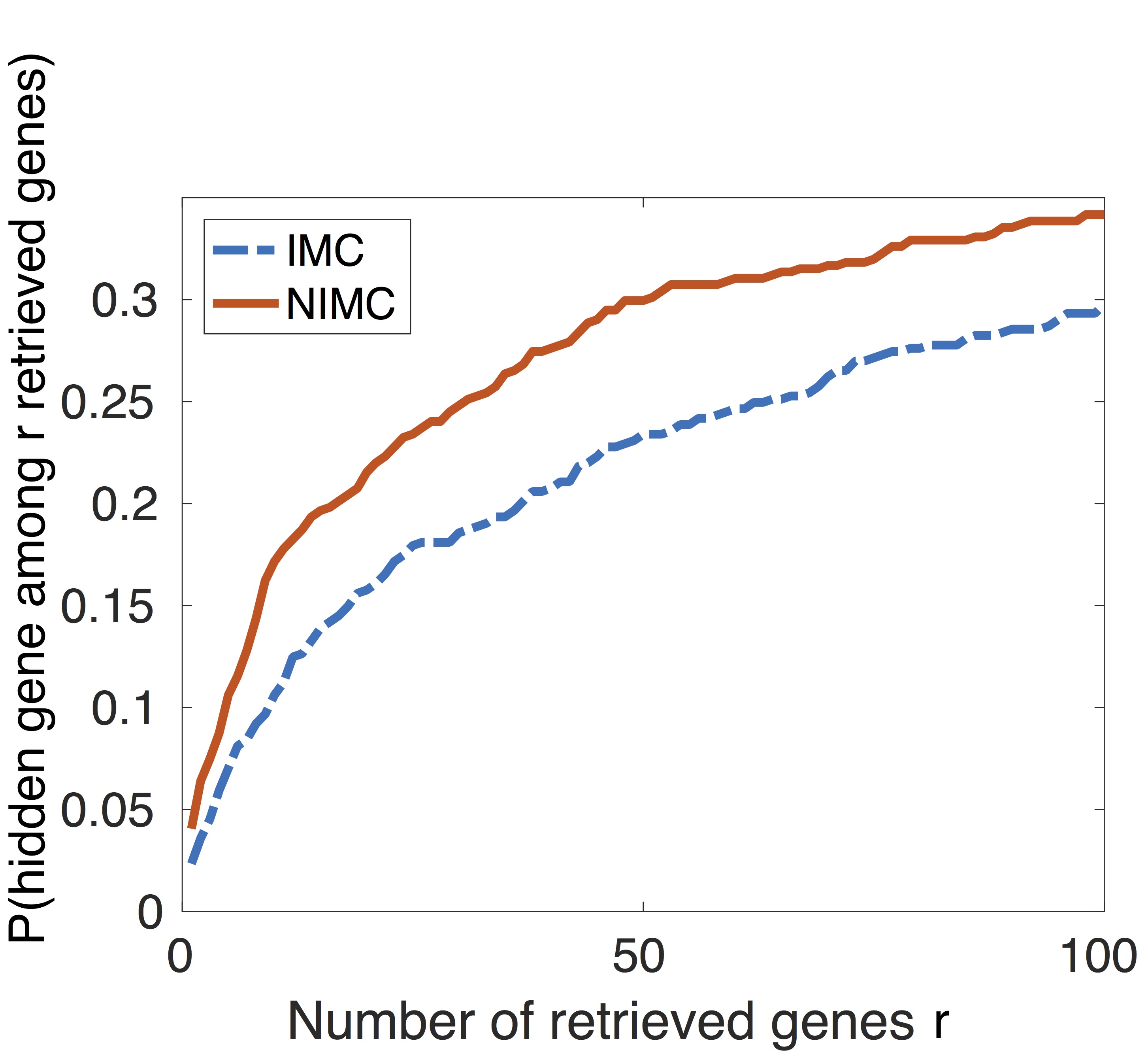

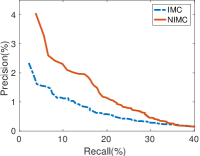

Finally, we apply our model on synthetic datasets and verify our theoretical analysis. Further, we compare our NIMC model with standard linear IMC on several real-world recommendation-type problems, including user-movie rating prediction, gene-disease association prediction and semi-supervised clustering. NIMC demonstrates significantly superior performance over IMC.

1.1 Related work

Collaborative filtering:

Our model is a non-linear version of the standard inductive matrix completion model [JD13]. Practically, IMC has been applied to gene-disease prediction [ND14], matrix sensing [ZJD15], multi-label classification[YJKD14], blog recommender system [SCLD15], link prediction [CHD15] and semi-supervised clustering [CHD15, SCH+16]. However, IMC restricts the latent space of users/items to be a linear transformation of the user/item’s feature space. [SCH+16] extended the model to a three-layer neural network and showed significantly better empirical performance for multi-label/multi-class classification problem and semi-supervised problems.

Although standard IMC has linear mappings, it is still a non-convex problem due to the bilinearity . To deal with this non-convex problem, [JD13, Har14] provided recovery guarantees using alternating minimization with sample complexity linear in dimension. [XJZ13] relaxed this problem to a nuclear-norm problem and also provided recovery guarantees. More general norms have been studied [RSW16, SWZ17a, SWZ17b, SWZ18], e.g. weighted Frobenius norm, entry-wise norm. More recently, [ZDG18] uses gradient-based non-convex optimization and proves a better sample complexity. [CHD15] studied dirtyIMC models and showed that the sample complexity can be improved if the features are informative when compared to matrix completion. Several low-rank matrix sensing problems [ZJD15, GJZ17] are also closely related to IMC models where the observations are sampled only from the diagonal elements of the rating matrix. [Ren10, LY16] introduced and studied an alternate framework for ratings prediction with side-information but the prediction function is linear in their case as well.

Neural networks: Nonlinear activation functions play an important role in neural networks. Recently, several powerful results have been discovered for learning one-hidden-layer feedforward neural networks [Tia17, ZSJ+17, JSA15, LY17, BGMSS18, GKKT17], convolutional neural networks [BG17, ZSD17, DLT18a, DLT+18b, GKM18]. However, our problem is a strict generalization of the one-hidden layer neural network and is not covered by the above mentioned results.

Notations.

For any function , we define to be .

For two functions , we use the shorthand (resp. ) to indicate that (resp. ) for an absolute constant . We use to mean for constants . We use to denote .

Roadmap. We first present the formal model and the corresponding optimization problem in Section 2. We then present the local strong convexity and local linear convergence results in Section 3. Finally, we demonstrate the empirical superiority of NIMC when compared to linear IMC (Section 4).

2 Problem Formulation

Consider a user-item recommender system, where we have users with feature vectors , items with feature vectors and a collection of partially-observed user-item ratings, . That is is the rating that user gave for item .

For simplicity, we assume ’s and ’s are sampled i.i.d. from distribution and , respectively. Each element of the index set is also sampled independently and uniformly with replacement from .

In this paper, our goal is to predict the rating for any user-item pair with feature vectors and , respectively.

We model the user-item ratings as:

|

|

|

(2) |

where , and is a non-linear activation function.

Under this realizable model, our goal is to recover from a collection of observed entries, . Without loss of generality, we set . Also we treat as a constant throughout the paper. Our analysis requires to be full column rank, so we require . And w.l.o.g., we assume , i.e., the smallest singular value of both and is .

Note that this model is similar to one-hidden layer feed-forward network popular in standard classification/regression tasks. However, as there is an inner product between the output of two non-linear layers, and , it cannot be modeled by a single hidden layer neural network (with same number of nodes). Also, for linear activation function, the problem reduces to inductive matrix completion [ABEV06, JD13].

Now, to solve for , , we optimize a simple squared-loss based optimization problem, i.e.,

|

|

|

(3) |

Naturally, the above problem is a challenging non-convex optimization problem that is strictly harder than two non-convex optimization problems which are challenging in their own right: a) the linear inductive matrix completion where non-convexity arises due to bilinearity of , and b) the standard one-hidden layer neural network (NN). In fact, recently a lot of research has focused on understanding various properties of both the linear inductive matrix completion problem [GJZ17, JD13] as well as one-hidden layer NN [GLM18, ZSJ+17].

In this paper, we show that despite the non-convexity of Problem (3), it behaves as a convex optimization problem close to the optima if the data is sampled stochastically from a Gaussian distribution. This result combined with standard tensor decomposition based initialization [ZSJ+17, KCL15, JSA15] leads to a polynomial time algorithm for solving (3) optimally if the data satisfies certain sampling assumptions in Theorem 2.1. Moreover, we also discuss the effect of various activation functions, especially the difference between a sigmoid activation function vs RELU activation (see Theorem 3.2 and Theorem 3.4).

Informally, our recovery guarantee can be stated as follows,

Theorem 2.1 (Informal Recovery Guarantee).

Consider a recommender system with a realizable model Eq. (2) with sigmoid activation,

Assume the features and are sampled i.i.d. from the normal distribution and the observed pairs are i.i.d. sampled from uniformly at random. Then there exists an algorithm such that can be recovered to any precision with time complexity and sample complexity (refers to ) polynomial in the dimension and the condition number of , and logarithmic in .

Appendix A Notation

For any positive integer , we use to denote the set .

For random variable , let denote the expectation of (if this quantity exists).

For any vector , we use to denote its norm.

We provide several definitions related to matrix .

Let denote the determinant of a square matrix . Let denote the transpose of . Let denote the Moore-Penrose pseudoinverse of . Let denote the inverse of a full rank square matrix. Let denote the Frobenius norm of matrix . Let denote the spectral norm of matrix . Let to denote the -th largest singular value of .

We use to denote the indicator function, which is if

holds and otherwise. Let

denote the identity matrix. We use to denote an activation

function.

We use to denote a Gaussian distribution .

For integer , we use to denote .

For any function , we define to be . In addition to notation, for two functions , we use the shorthand (resp. ) to indicate that (resp. ) for an absolute constant . We use to mean for constants .

Appendix C Proof Sketch

At high level the proofs for Theorem 3.2 and Theorem 3.4 include the following steps. 1) Show that the population Hessian at the ground truth is positive definite. 2) Show that population Hessians near the ground truth are also positive definite. 3) Employ matrix Bernstein inequality to bound the population Hessian and the empirical Hessian.

We now formulate the Hessian. The Hessian of Eq. (3), , can be decomposed into two types of blocks, (),

|

|

|

where (, resp.) is the -th column of (-th column of , resp.). Note that each of the above second-order derivatives is a matrix.

The first type of blocks are given by:

|

|

|

where , , and

|

|

|

For sigmoid/tanh activation function, the second type of blocks are given by:

|

|

|

(6) |

For ReLU/leaky ReLU activation function, the second type of blocks are given by:

|

|

|

Note that the second term of Eq. (6) is missing here as are fixed, the number of samples is finite and almost everywhere.

In this section, we will discuss important lemmas/theorems for Step 1 in Appendix C.1 and Step 2,3 in Appendix C.3.

C.1 Positive definiteness of the population hessian

The corresponding population risk for Eq. (3) is given by:

|

|

|

(7) |

where .

For simplicity, we also assume and are normal distributions.

Now we study the Hessian of the population risk at the ground truth.

Let the Hessian of at the ground-truth be , which can be decomposed into the following two types of blocks (),

|

|

|

|

|

|

|

|

To study the positive definiteness of , we characterize the minimal eigenvalue of by a constrained optimization problem,

|

|

|

(8) |

where denotes that .

Obviously, due to the squared loss and the realizable assumption. However, this is not sufficient for the local convexity around the ground truth, which requires the positive (semi-)definiteness for the neighborhood around the ground truth. In other words, we need to show that is strictly greater than , so that we can characterize an area in which the Hessian still preserves positive definiteness (PD) despite the deviation from the ground truth.

Challenges. As we mentioned previously there are activation functions that lead to redundancy in parameters. Hence one challenge is to distill properties of the activation functions that preserve the PD. Another challenge is the correlation introduced by when it is non-orthogonal. So we first study the minimal eigenvalue for orthogonal and orthogonal and then link the non-orthogonal case to the orthogonal case.

C.2 Warm up: orthogonal case

In this section, we consider the case when are unitary matrices, i.e., . (). This case is easier to analyze because the dependency between different elements of or can be disentangled. And we are able to provide lower bound for the Hessian. Before we introduce the lower bound, let’s first define the following quantities for an activation function .

|

|

|

|

(9) |

|

|

|

|

|

|

|

|

|

|

|

|

We now present a lower bound for general activation functions including sigmoid and tanh.

Lemma C.1.

Let denote that .

Assume and are unitary matrices, i.e., , then the minimal eigenvalue of the population Hessian in Eq. (8) can be simplified as,

|

|

|

Let be defined as in Eq. (9). If the activation function satisfies , then

Since sigmoid and tanh have symmetric derivatives w.r.t. , they satisfy . Specifically, we have for sigmoid and for tanh. Also for ReLU, , so ReLU does not fit in this lemma. The full proof of Lemma C.1, the lower bound of the population Hessian for ReLU and the extension to non-orthogonal cases can be found in Appendix D.

C.3 Error bound for the empirical Hessian near the ground truth

In the previous section, we have shown PD for the population Hessian at the ground truth for the orthogonal cases. Based on that, we can characterize the landscape around the ground truth for the empirical risk. In particular, we bound the difference between the empirical Hessian near the ground truth and the population Hessian at the ground truth. The theorem below provides the error bound w.r.t. the number of samples and the number of observations for both sigmoid and ReLU activation functions.

Theorem C.2.

For any , if

|

|

|

then with probability at least ,

for sigmoid/tanh,

|

|

|

for ReLU,

|

|

|

The key idea to prove this theorem is to use the population Hessian at as a bridge.

On one side, we bound the population Hessian at the ground truth and the population Hessian at . This would be easy if the second derivative of the activation function is Lipschitz, which is the case of sigmoid and tanh. But ReLU doesn’t have this property. However, we can utilize the condition that the parameters are close enough to the ground truth and the piece-wise linearity of ReLU to bound this term.

On the other side, we bound the empirical Hessian and the population Hessian. A natural idea is to apply matrix Bernstein inequality. However, there are two obstacles. First the Gaussian variables are not uniformly bounded. Therefore, we instead use Lemma B.7 in [ZSJ+17], which is a loosely-bounded version of matrix Bernstein inequality. The second obstacle is that each individual Hessian calculated from one observation is not independent from another observation , since they may share the same feature or . The analyses for vanilla IMC and MC assume all the items(users) are given and the observed entries are independently sampled from the whole matrix. However, our observations are sampled from the joint distribution of and .

To handle the dependency, our model assumes the following two-stage sampling rule. First, the items/users are sampled from their distributions independently, then given the items and users, the observations are sampled uniformly with replacement. The key question here is how to combine the error bounds from these two stages.

Fortunately, we found special structures in the blocks of Hessian which enables us to separate for each block, and bound the errors in stage separately. See Appendix E for details.

Appendix E Positive Definiteness of the Empirical Hessian

For any , the population Hessian can be decomposed into the following blocks (),

|

|

|

|

(16) |

|

|

|

|

|

|

|

|

|

|

|

|

where if , otherwise . Similarly we can write the formula for and .

Replacing by in the above formula, we can obtain the formula for the corresponding empirical Hessian, .

We now bound the difference between and .

Theorem E.1 (Restatement of Theorem C.2).

For any , if

|

|

|

then with probability ,

for sigmoid/tanh,

|

|

|

for ReLU,

|

|

|

Proof.

Define as a symmetric matrix, whose blocks are represented as

|

|

|

|

(17) |

|

|

|

|

where correspond to respectively.

We decompose the difference into

|

|

|

|

Combining Lemma E.2, E.14, we complete the proof.

∎

Lemma E.2.

For any , if

|

|

|

then with probability ,

for sigmoid/tanh,

|

|

|

for ReLU,

|

|

|

Proof.

We can bound if we bound each block.

We can show that if

|

|

|

then with probability ,

|

|

|

|

|

|

|

Lemma E.3 |

|

|

|

|

|

|

|

|

Lemma E.6 |

|

|

|

|

|

|

|

|

Lemma E.7 |

|

|

|

|

|

|

|

|

Lemma E.9 |

|

where if is ReLU, if is sigmoid/tanh.

Note that for ReLU activation, for any given , the second term is because almost everywhere.

∎

Lemma E.3.

If

|

|

|

then with probability at least ,

|

|

|

where if is , if is sigmoid/tanh.

Proof.

Let . By applying Lemma E.11 and Property in Lemma E.4 and Lemma E.5, we have for any if

|

|

|

then with probability at least ,

|

|

|

(18) |

By applying Lemma E.12 and Property in Lemma E.4 and Lemma E.5, we have for any if

|

|

|

then

|

|

|

and

|

|

|

Therefore,

|

|

|

(19) |

We can apply Lemma E.13 and use Eq. (19) and Property in Lemma E.4 and Lemma E.5 to obtain the following result.

If

|

|

|

then with probability at least ,

|

|

|

(20) |

Combining Eq. (18) and (20), we finish the proof.

∎

Lemma E.4.

Define . If , and is ReLU or sigmoid/tanh, the following holds for and any ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proof.

Note that , therefore can be proved by Proposition 1 of [HKZ12].

can be proved by Hölder’s inequality.

∎

Lemma E.5.

Define . If , and is ReLU or sigmoid/tanh, the following holds for and any ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where if is ReLU, if is sigmoid/tanh.

Proof.

Note that , therefore can be proved by Proposition 1 of [HKZ12].

can be proved by Hölder’s inequality

∎

Lemma E.6.

If

|

|

|

then with probability at least ,

|

|

|

|

|

|

|

|

Proof.

We consider the following formula first,

|

|

|

|

|

|

|

|

Similar to Lemma E.3, we are able to show

|

|

|

|

|

|

|

|

Note that by Hölder’s inequality, we have,

|

|

|

So we complete the proof.

∎

Lemma E.7.

If

|

|

|

then with probability at least ,

|

|

|

Proof.

Let , where and . By applying Lemma E.11 and Property in Lemma E.8 , we have for any if

|

|

|

then with probability at least ,

|

|

|

(21) |

By applying Lemma E.12 and Property in Lemma E.8, we have for any if

|

|

|

then

|

|

|

By applying Lemma E.12 and Property in Lemma E.8, we have for any if

|

|

|

then

|

|

|

Therefore,

|

|

|

(22) |

We can apply Lemma E.13 and Eq. (22) and Property in Lemma E.8 to obtain the following result.

If

|

|

|

then with probability at least ,

|

|

|

(23) |

Combining Eq. (21) and (23), we finish the proof.

∎

Lemma E.8.

Define . If , and is ReLU or sigmoid/tanh, the following holds for and any ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proof.

Note that ,, therefore can be proved by Proposition 1 of [HKZ12].

can be proved by Hölder’s inequality.

∎

Lemma E.9.

If

|

|

|

then with probability at least ,

|

|

|

|

|

|

|

|

Proof.

We consider the following formula first,

|

|

|

Set and and follow the proof for Lemma E.7. Also note that is Lipschitz, i.e., . We can show the following. If

|

|

|

then with probability at least ,

|

|

|

Note that by Hölder’s inequality, we have,

|

|

|

So we complete the proof.

We provide a variation of Lemma B.7 in [ZSJ+17]. Note that the Lemma B.7 [ZSJ+17] requires four properties, we simplify it into three properties.

Lemma E.10 (Matrix Bernstein for unbounded case (A modified version of bounded case, Theorem 6.1 in [Tro12], A variation of Lemma B.7 in [ZSJ+17])).

Let denote a distribution over . Let . Let be i.i.d. random matrices sampled from . Let and . For parameters , if the distribution satisfies the following four properties,

|

|

|

|

|

|

|

|

|

|

|

|

Then we have for any and , if

|

|

|

with probability at least ,

|

|

|

Proof.

Define the event

|

|

|

Define . Let and . By triangle inequality, we have

|

|

|

(24) |

In the next a few paragraphs, we will upper bound the above three terms.

The first term in Eq. (24). For each , let denote the complementary set of , i.e. . Thus .

By a union bound over , with probability , for all . Thus .

The second term in Eq. (24). For a matrix sampled from , we use to denote the event that . Then, we can upper bound in the following way,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by Hölder’s inequality |

|

|

|

|

by Property (\@slowromancapiv@) |

|

|

|

|

|

|

|

|

|

|

|

which is

|

|

|

Therefore, .

The third term in Eq. (24). We can bound by Matrix Bernstein’s inequality [Tro12].

We define . Thus we have , , and

|

|

|

Similarly, we have .

Using matrix Bernstein’s inequality, for any ,

|

|

|

By choosing

|

|

|

for , we have with probability at least ,

|

|

|

Putting it all together, we have for , if

|

|

|

with probability at least ,

|

|

|

Lemma E.11 (Tail Bound for fully-observed rating matrix).

Let be independent samples from distribution and be independent samples from distribution . Denote as the collection of all the pairs. Let be a random matrix of , which can be represented as the product of two matrices , i.e., . Let and . Let be the sum of the two dimensions of and be the sum of the two dimensions of . Suppose both and satisfy the following properties ( is a representative for , and is a representative for ),

|

|

|

|

|

|

|

|

|

|

|

|

Then for any if

|

|

|

|

|

|

with probability at least ,

|

|

|

(25) |

Proof.

First we note that,

|

|

|

and

|

|

|

Therefore, if we can bound and the corresponding term for , we are able to prove this lemma.

By the conditions of , the three conditions in Lemma E.10 are satisfied, which completes the proof.

Lemma E.12 (Upper bound for the second-order moment).

Let be independent samples from distribution . Let be a matrix of .

Let be the sum of the two dimensions of and . Suppose satisfies the following properties.

|

|

|

|

|

|

|

|

|

|

|

|

Then for any , if

|

|

|

we have with probability at least ,

|

|

|

Proof.

The proof directly follows by applying Lemma E.10.

∎

Lemma E.13 (Tail Bound for partially-observed rating matrix).

Given and , let’s denote as the collection of all the pairs. Let also be a collection of pairs, where each pair is sampled from independently and uniformly. Let be a matrix of . Let be the sum of the two dimensions of . Define . Assume the following,

|

|

|

|

|

|

|

|

Then we have for any and , if

|

|

|

with probability at least ,

|

|

|

Proof.

Since each entry in is sampled from uniformly and independently, we have

|

|

|

Applying the matrix Bernstein inequality Theorem 6.1 in [Tro12], we prove this lemma.

∎

Lemma E.14.

For sigmoid/tanh activation function,

|

|

|

where is defined as in Eq. (17).

For ReLU activation function,

|

|

|

Proof.

We can bound each block, i.e.,

|

|

|

|

(26) |

|

|

|

(27) |

For smooth activations, the bound for Eq. (26) follows by combining Lemma E.15 and Lemma E.16 and the bound for Eq. (27) follows

Lemma E.18 and Lemma E.20.

For ReLU activation, the bound for Eq. (26) follows by combining Lemma E.15, Lemma E.17 and the bound for Eq. (27) follows

Lemma E.18 and Lemma E.19.

∎

Lemma E.15.

|

|

|

Proof.

The proof follows the property of the activation function () and Hölder’s inequality.

∎

Lemma E.16.

When the activation function is smooth, we have

|

|

|

Proof.

The proof directly follows Eq. (12) in Lemma D.10 in [ZSJ+17].

∎

Lemma E.17.

When the activation function is piece-wise linear with turning points, we have

|

|

|

Proof.

|

|

|

Let be the orthogonal basis of . Without loss of generality, we assume are independent, so is -by-3. Let . Let , where is the complementary matrix of .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(28) |

where the first step follows by , the last step follows by .

We have exceptional points which have . Let these points be . Note that if and are not separated by any of these exceptional points, i.e., there exists no such that or , then we have since are zeros except for . So we consider the probability that are separated by any exception point. We use to denote the event that are separated by an exceptional point . By union bound, is the probability that are not separated by any exceptional point.

The first term of Equation (E) can be bounded as,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where the first step follows by if are not separated by any exceptional point then and the last step follows by Hölder’s inequality.

It remains to upper bound . First note that if are separated by an exceptional point, , then . Therefore,

|

|

|

Note that follows Beta(1,1) distribution which is uniform distribution on .

|

|

|

where the first step is because we can view and as two independent random variables: the former is about the direction of and the later is related to the magnitude of .

Thus, we have

|

|

|

(29) |

Similarly we have

|

|

|

(30) |

Finally combining Eq. (29) and Eq. (30) completes the proof.

Lemma E.18.

|

|

|

Proof.

First, we can use the Lipschitz continuity of the activation function,

|

|

|

|

|

|

|

where is the Lipschitz constant of .

Then the proof follows Hölder’s inequality.

∎

Lemma E.19.

When the activation function is ReLU,

|

|

|

Proof.

|

|

|

Similar to Lemma E.17, we can show that

|

|

|

∎

Lemma E.20.

When the activation function is sigmoid/tanh,

|

|

|

Proof.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

E.1 Local Linear Convergence

Given Theorem 3.2, we are now able to show local linear convergence of gradient descent for sigmoid and tanh activation function.

Theorem E.21 (Restatement of Theorem 3.3).

Let be the parameters in the -th iteration. Assuming ,

then given a fresh sample set, , that is independent of and satisfies the conditions in Theorem 3.2, the next iterate using one step of gradient descent, i.e.,

satisfies

|

|

|

with probability , where is the step size and is the lower bound on the eigenvalues of the Hessian and is the upper bound on the eigenvalues of the Hessian.

Proof.

In order to show the linear convergence of gradient descent, we first show that the Hessian along the line between and are positive definite w.h.p..

The idea is essentially building a -net for the line between the current iterate and the optimal. In particular, we set points that are equally distributed between and . Therefore,

Using Lemma E.22, we can show that for any , if there exists a value of such that , then

|

|

|

Therefore, for every point in the line between and , we can find a fixed point in , such that . Now applying union bound for all , we have that w.p.

, for every point in the line between and ,

|

|

|

where and . Note that the upper bound of the Hessian is due to the fact that and are bounded.

Given the positive definiteness of the Hessian along the line between the current iterate and the optimal, we are ready to show the linear convergence. First we set the stepsize for the gradient descent update as and use notation to simplify the writing.

|

|

|

|

|

|

|

|

|

|

|

|

Note that

|

|

|

Define ,

|

|

|

By the result provided above, we have

|

|

|

(31) |

Now we upper bound the norm of the gradient,

|

|

|

Therefore,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

Lemma E.22.

Let the activation function be tan/sigmoid. For given and , if

|

|

|

then with probability ,

|

|

|

Proof.

We consider each block of the Hessian as defined in Eq (16).

In particular, we show that if

|

|

|

then with probability ,

|

|

|

|

|

|

|

|

|

|

by Lemma E.23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by Lemma E.24 |

|

|

|

|

|

|

|

|

|

|

|

by Lemma E.25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by Lemma E.26 |

|

∎

Lemma E.23.

If

|

|

|

then with probability at least ,

|

|

|

|

|

|

|

|

Proof.

Note that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(32) |

Let’s consider the first term in the above formula. The other terms are similar.

|

|

|

|

|

|

|

|

which is because both and are bounded and Lipschitz continuous.

Applying the unbounded matrix Bernstein Inequality Lemma E.10, we can bound

|

|

|

Since both and are bounded and Lipschitz continuous, we can easily extend the above inequality to other cases and finish the proof.

∎

Lemma E.24.

If

|

|

|

then with probability at least ,

|

|

|

|

|

|

|

|

|

|

|

|

Proof.

Since for sigmoid/tanh, are all Lipschitz continuous and bounded, the proof of this lemma resembles the proof for Lemma E.23.

∎

Lemma E.25.

If

|

|

|

then with probability at least ,

|

|

|

|

|

|

|

|

Proof.

Do the similar splits as Eq. (32) and let’s consider the following case,

|

|

|

Setting , and using the fact that , we can follow the proof of Lemma E.7 to show if

|

|

|

then with probability at least ,

|

|

|

∎

Lemma E.26.

If

|

|

|

then with probability at least ,

|

|

|

|

|

|

|

|

|

|

|

|

Proof.

Since for sigmoid/tanh, are all Lipschitz continuous and bounded, the proof of this lemma resembles the proof for Lemma E.25.

∎