mylongform \excludeversionmyscribbles \includeversionmysolution

Bandwidth selection for kernel density estimators of multivariate level sets and highest density regions

Abstract

We consider bandwidth matrix selection for kernel density estimators (KDEs) of density level sets in , . We also consider estimation of highest density regions, which differs from estimating level sets in that one specifies the probability content of the set rather than specifying the level directly. This complicates the problem. Bandwidth selection for KDEs is well studied, but the goal of most methods is to minimize a global loss function for the density or its derivatives. The loss we consider here is instead the measure of the symmetric difference of the true set and estimated set. We derive an asymptotic approximation to the corresponding risk. The approximation depends on unknown quantities which can be estimated, and the approximation can then be minimized to yield a choice of bandwidth, which we show in simulations performs well. We provide an R package lsbs for implementing our procedure.

1 Introduction

As computing power has become greater and as data sets have become simultaneously larger and more complicated, demand for statistical methods that are increasingly flexible and data driven has increased. Two related methods for capturing the complex structure of a data set from a true density are to estimate either the density’s level sets (LS’s) or the density’s highest-density regions (HDR’s). (We will explain the difference between estimating LS’s and estimating HDR’s shortly.) For a density function defined on and a given constant , the -level set (sometimes known as a density contour) of is and the corresponding super-level set is

| (1) |

Under some basic regularity conditions, the density super-level set is a set of minimum volume having -probability at least (Garcia et al., 2003). For this reason, perhaps the most common use for HDR estimation occurs in Bayesian statistics. An HDR of a posterior density is a so-called (minimum volume) credible region, which is one of the most fundamental tools in Bayesian statistics. There are quite a wide range of other applications for estimation of density LS’s or density HDR’s and these estimation problems have received increasing attention in the statistics and machine learning literatures in recent years. (We consider estimation of density level sets and estimation of density super-level sets to be equivalent tasks.) The applications of LS or HDR estimation include outlier/novelty detection (Lichman and Smyth, 2014; Park et al., 2010), discriminant analysis (Mammen and Tsybakov, 1999) and clustering analysis (Hartigan, 1975; Rinaldo and Wasserman, 2010; Cuevas et al., 2001). LS estimation is one of the fundamental tools in estimation of cluster trees and persistence diagrams, used in topological data analysis (Chen (2017), Wasserman (2016)).

A common way to estimate the density super-level set based on independent and identically distributed (i.i.d.) is to replace the density function in (1) with a kernel density estimator (KDE)

| (2) |

where is a symmetric positive definite bandwidth matrix and is a kernel function. This gives us the so-called plug-in estimator

| (3) |

We now explain the difference between “LS estimation” and “HDR estimation.” Often the level of interest is only specified indirectly through a given probability which yields a level . Then the corresponding super-level set is

| (4) |

and the corresponding plug-in estimators are

and

| (5) |

Estimating (4) based on specifying is known as the HDR estimation problem; this has extra complication over the LS estimation problem because has to be estimated rather than being fixed in advance. Thus we use the phrase LS estimation to mean estimation of (1) with fixed in advance (equivalently, estimation of (4) with fixed). When we use the phrase HDR estimation we mean estimation of (4) with (but not ) fixed in advance. Thus, LS’s and HDR’s are mathematically equivalent, but estimating LS’s and estimating HDR’s are statistically different tasks.

Early work on LS or HDR estimation includes Hartigan (1987), Müller and Sawitzki (1991), Polonik (1995), Tsybakov (1997), and Walther (1997). Some recent work has focused on asymptotic properties of KDE plug-in estimators, including results about consistency, limit distribution theory, and statistical inference. Baíllo et al. (2001) show that the probability content of the plug-in estimator converges to the probability of the true super-level set as the sample size tends to infinity. Baíllo (2003) proves the strong consistency of the plug-in estimator under an integrated symmetric difference metric. Cadre (2006) further obtains the rate of convergence of the plug-in estimator when the loss is given by the generalized symmetric difference of sets. Mason and Polonik (2009) give the asymptotic normality of estimated super-level sets under the same metric as Cadre (2006). Chen et al. (2017) find a more practically usable limiting distribution of the plug-in estimator for LS’s by using Hausdorff distance as the metric for set difference and provide methods for constructing confidence regions for LS’s based on this limiting distribution. Jankowski and Stanberry (2012) and Mammen and Polonik (2013) also investigate the formation of confidence regions for LS’s.

It is well known that KDE’s are sensitive to the choice of the bandwidth (matrix). The optimal bandwidth (matrix) depends on the objective of estimation. There are many tools that have been developed for selecting the bandwidth when or the bandwidth matrix when ; these include minimizing an asymptotic approximation to an appropriate risk function, as well as computational methods such as the bootstrap or cross-validation, and are largely focused on globally estimating the density or its derivatives well. A good summary of those methods can be found in Wand and Jones (1995), Sain et al. (1994b), or Jones et al. (1996).

However, Duong et al. (2009, page 505) state that, “a number of practical issues in highest density region estimation, such as good data-driven rules for choosing smoothing parameters, are yet to be resolved.” Samworth and Wand (2010) is the only published work we know of that investigates the problem of selecting bandwidths for HDR estimation (and we know of no published works that directly investigate bandwidth selection for LS estimation). Samworth and Wand (2010) study the KDE plug-in estimator when , and show by simulation that the kernel density estimator aiming for HDR estimation can be very different from the one aiming for global density estimation. They also propose an asymptotic approximation to a risk function that is suitable for HDR estimation and a corresponding bandwidth selection procedure based on the approximation, all when .

In this paper, we consider the multivariate setting, where . In this case, we are estimating a level set manifold, which involves some added technical difficulties over the case (in which case the level set is a finite point set), but we believe that LS or HDR estimation when is of great practical interest because of the large variety of complicated structures that multivariate level sets can reveal. We derive asymptotic approximations to a risk function for LS estimation and to a risk function for HDR estimation. We believe that our approximations and derivations will be very valuable for any future procedures that do (either) LS or HDR bandwidth selection. Our calculations shed light on the important quantities relating to LS or HDR estimation. Furthermore, we develop a “plug-in” bandwidth selector method based on minimizing an estimate of the LS or the HDR risk approximation. This approach can be used to optimize over all positive definite bandwidth matrices or over restricted classes of matrices (e.g., diagonal ones). Our theory applies for all . We have developed code to implement our bandwidth selector when . It is straightforward to implement a numeric approximation to Hausdorff integrals that appear in our approximations (see Subsection 2.1 for discussion of the Hausdorff measure) when . It is less immediately obvious how to implement such approximations when , although we indeed believe that implementation is feasible for such approximations. In fact, we believe that computational feasibility is an important benefit of using a closed-form approximation to the risk, particularly in the multivariate setting that we consider in this paper. As will be discussed later in the paper, many simple problems in the univariate setting are more complicated in the multivariate setting and must be solved by Monte Carlo. Thus performing bootstrap or cross-validation, which involves nested Monte Carlo computations, quickly becomes infeasible.

During the development of the present paper we became aware of the recent related work, Qiao (2018). Qiao (2018) also considers problems about bandwidth selection for KDE’s in settings related to level set estimation. However, the main focus of Qiao (2018) is somewhat different than the one here. In fact, Qiao (2018) states that bandwidth selection for multivariate HDR estimation is “far from trivial” and does not consider this problem. We will discuss the approach taken by Qiao (2018) again in the Discussion section.

The structure of the paper is as follows. We present our two asymptotic risk approximation theorems, as well as corollaries about the risk approximation minimizers, in Section 2. We present methodology to select bandwidth matrices in Section 3. In Section 4 we study the performance of our bandwidth selector in simulation experiments as well as in analysis of two real data sets, the Wisconsin Breast Cancer Diagnostic data and the Banknote Authentication data. We give concluding discussion in Section 5. Proofs of the main results are given in Appendix A, and further details, technical results, and intermediate lemmas are given in Appendix B and Appendix C. Some notation and assumptions are presented in Subsections 2.1 and 2.2.

2 Asymptotic risk results

2.1 Notation

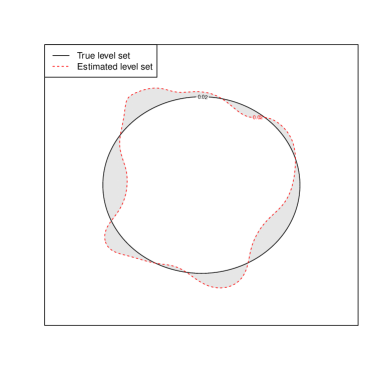

We use the following notation throughout. For a density function on and a Borel measurable set , define the measure . For a function on , a measure , and , we let if this quantity is finite. If is Lebesgue measure we abbreviate , . Let , and for a function with vector or matrix values, that is, , let . We let for . Let be the gradient (column) vector of and let be the Hessian matrix . Let be dimensional Hausdorff measure (Evans and Gariepy, 2015). The Hausdorff measure is useful for measuring the volume of lower dimensional sets, like manifolds, embedded in a higher dimensional ambient space. Let denote Lebesgue measure. Recall that and , we let and . We generally use bold to denote vectors. We use “” to denote notational equivalences and “” or “” for definitions. Any integral whose domain is not specified explicitly is taken over all of . We will occasionally omit the integrating variable when there’s no confusion in doing so. We use to denote the set of all symmetric positive definite matrices. For a symmetric matrix , we use and to denote the largest and the smallest eigenvalues of respectively. In this paper, we will use the -probability volume of the symmetric difference as the distance between the true set and its estimator. We use to denote the symmetric difference operation between two sets: for two sets and , where “” is set difference. Figure 1 shows the symmetric difference between the super-level set of standard bivariate normal distribution and an “estimated” super-level set. We let be the complement of a set . For and , let , and for a set , let .

2.2 Assumptions

To derive our asymptotic expansion, we make the following basic assumptions on the underlying density, kernel function and bandwidth matrix.

Assumption D1a.

-

1.

Let be i.i.d. from a bounded density on , .

-

2.

Fix . There exists a constant such that (a) has two bounded continuous partial derivatives over , (b) , and (c) is contained in for some .

Assumption D1b.

-

1.

Let be i.i.d. from a bounded density on , .

-

2.

The density has two bounded continuous partial derivatives for all .

-

3.

There exists a constant such that satisfies (a) , and (b) is contained in for some . {mylongform}

-

4.

For any , , where is the Lebesgue measure in . (indicated by 3, see NunezGarcia:2003ci)

Assumption Assumption D1a will be used for LS estimation and Assumption Assumption D1b for HDR estimation. We need the stronger global twice differentiability assumption in HDR estimation because of the need to estimate (which involves estimating the -probability content of ). The global twice differentiability assumption in Assumption Assumption D1b could be weakened to an assumption of twice differentiability either on or on .

Assumptions Assumption D1a and Assumption D1b entail that the gradient of is nonzero on (a neighborhood of) the level set of interest. This implies by the preimage theorem that the level set , taken to be either or , is a -dimensional (boundaryless) manifold (Guillemin and Pollack, 1974). The only additional assumption we need is one of compactness, which rules out only very pathological cases, where has “spikes” of increasingly small width going out towards infinity.

Assumption D2.

Let or be as in Assumptions Assumption D1a and Assumption D1b. Assume that or is compact.

Our assumption on the kernel will come in the form of a so-called Vapnik-Chervonenkis (VC) (Dudley, 1999) type of assumption. For a metric space and , the covering number is the smallest number of balls of radius (and centers which may or may not be in ) needed to cover . If a class of functions is a VC class, we have that

| (6) |

for some positive , where the sup is over all probability measures , and where is the envelope of meaning (Chapter 2.6, van der Vaart and Wellner (1996)). We will simply directly assume that the needed classes satisfy (6). Thus our assumptions are as follows.

Assumption K.

-

1.

The kernel is an everywhere continuously differentiable bounded density on with bounded partial derivatives. Both and are finite or have finite entries, respectively. Assume , , where is the identity matrix and is independent of .

-

2.

Assume that (6) is satisfied with taken to be

(7) (8)

Let and let be the largest eigenvalue of .

Assumption H.

-

1.

Let , such that for some , , , , as , and .

-

2.

Assume that and and as . {mylongform} ,

Here, means that decreases monotonically to . {mylongform} From the above assumption, we know and are of the same order. So we make further assumptions on through . Let , and then we know and . We list out the assumptions we need for during the proof.

-

1.

. This is equivalent to .

-

2.

For the proof of Lemma LABEL:lem:hdr-step2, we require . So this requires .

-

3.

In the proof of Lemma A.2, we need while .

- 4.

We can see the above requirement are satisfied by our assumption on . Since for any and , we can always let

then by our assumption on , and are satisfied. We need to verify that , which can be shown by

by our assumption of . Assumptios Assumption D1a and Assumption D1b are standard in the KDE literature (see, e.g., page 95 of Wand and Jones (1995)). Note that Assumption 3 of Assumption Assumption D1b implies that there exists a constant such that for small enough that ; this is a standard type of assumption that appears in the level set estimation literature (Polonik, 1995). Assumption Assumption D2 is not very limiting and only rules out pathological cases.

Our Assumption Assumption K on the kernel function is not restrictive and all of the conditions imposed are fairly standard. For Assumption 1 see, e.g., page 95 of Wand and Jones (1995) where similar conditions are imposed. Assumption 2 is also fairly standard in the KDE literature (e.g., Chen et al. (2017) uses similar conditions in the context of inference for level sets). This assumption is needed to apply the results of Giné and Guillou (2002) to get almost sure convergence rates of and . Assumption of Giné and Guillou (2002) (or Assumption K, page 2572, of Giné et al. (2004)) is an easy-to-verify condition that implies Assumption 2 holds, and shows that Assumption 2 holds for Gaussian kernels and for many compactly supported kernels.

The expansions given in our Theorem 2.1 and 2.2 hold for the range of bandwidths given in Assumption Assumption H. This is sufficient to develop a practical bandwidth selector, since larger or smaller bandwidths can be easily ruled out. See Corollaries 2.1 and 2.2.

2.3 Asymptotic risk expansions

Our main results are stated in the following two theorems. The first gives the asymptotic risk expansion for level set estimation. Let and denote the standard normal distribution function and density function, respectively.

Theorem 2.1.

For given constant with , let Assumptions Assumption K, Assumption H, Assumption D1a and Assumption D2 hold. Moreover, the kernel function has bounded support. Then

as , where

| (9) |

with .

Note that the first summand (including the factor ) in the integral defining is of the order of magnitude of a variance term in a mean-squared error decomposition, and the second two summands are of the same order of magnitude of a squared bias term. The next theorem gives the HDR asymptotic risk expansion.

Theorem 2.2.

Let Assumptions Assumption D1b,Assumption D2,Assumption K and Assumption H hold. Then

as , where

and are defined in the same way as in Theorem 2.1 with replaced by . And

with and

We defer the proofs to the appendix. Next, we would like to study the theoretical behavior of the minimizers of and . Note that the minimizers of or of are not practically usable bandwidth matrices, since and depend on the true, unknown density . We will discuss estimation of and of and practical bandwidth selectors in the next section. Presently, we consider the minimizers of and , which serve as oracle bandwidth selectors.

Unfortunately, and are quite complicated functions so studying their minimizers in general is not at all straightforward. Thus we will make some simplifying assumptions. We will consider that is unimodal and spherically symmetric about some point (taken to be the origin in Corollary 2.1 and 2.2). We will consider optimizing over the subclass of bandwidth matrices, where is the identity matrix. These assumptions are made largely for simplicity and ease of presentation of the following two corollaries, and are far from necessary for the conclusions to hold. We discuss these assumptions again after the corollaries. By a slight abuse of notation, we let and

Corollary 2.1.

Let the assumptions of Theorem 2.1 hold. Assume further that and that the function defined for is strictly decreasing on . Then there exists a constant depending on and (but not on ) such that there is a unique positive number satisfying

where is any minimizer of .

Corollary 2.2.

Let the assumptions of Theorem 2.2 hold. Assume further that and that the function defined for is strictly decreasing on . Then there exists a constant depending on and (but not on ) such that there is a unique positive number satisfying

where is any minimizer of .

The proof of the two corollaries follows exactly the same way, so we provide the proof for HDR estimation and omit that for LS estimation. The corollaries tell us the order of magnitude of the true optimal bandwidths and of the oracle bandwidths. We used the assumptions of unimodality and spherical symmetry because these assumptions imply that , , and are constant on and . We believe that (an analogous form of) the conclusions of Corollary 2.1 and 2.2 hold for and for , and for much more general densities . Our simulations show that our practical bandwidth selector (studied in the next section) does not require such extreme assumptions.

3 Bandwidth selection methodology

In the previous section, we provided asymptotic expansions of symmetric risks for HDR estimation and LS estimation, which could be used as guidance for bandwidth selection in those two scenarios. Minimizers of and are natural bandwidth selectors for HDR estimation and LS estimation, respectively. The theoretical performance of the bandwidth selector using “oracle” knowledge of the functionals of the true density is studied in Corollary 2.1 and 2.2. Of course, in practice, one does not have this oracle knowledge. In the present section, we develop an effective practical bandwidth selection procedure for HDR estimation (a procedure for level set estimation is simpler and can be derived in a similar way). We will also study the theoretical performance of our bandwidth selector restricted to a simplified class .

Since there are unknown quantities that depends on, a natural “plug-in” approach is to estimate those quantities using different kernel density estimators and plug the estimates in. Moreover, the unknown functionals depend on the truth through , so we will use three pilot kernel density estimators. To be specific, we use to estimate and ; we use to estimate , and combined with the pilot estimator of ; we use to estimate , where , and are corresponding pilot bandwidth matrices for the three kernel density estimators. (One could also use three different kernels for , , but we will use the same kernel for all three.) For our theoretical results to hold, we require just the bandwidth matrix to be of the optimal order for estimating the th derivatives of (see Corollary 3.2 and Assumption Assumption H2, below). We use two-stage direct plug-in estimators for the pilot bandwidths in our algorithm below, which converge at the correct rate. A detailed description about plug-in estimators could be found in Wand and Jones (1995, Chapter 3) and Chacón and Duong (2010).

Once we have those estimated functionals, we can plug them into to obtain an estimated loss function . Note appears in the integrand of a Hausdorff integral and cannot be factored out of the integral; thus minimizing directly is infeasible. Instead, we minimize a discretized approximation to . To illustrate this idea, we use the minimization of as an example. Let be a partition of such that is sufficiently small for . Then can be approximated by , where is an arbitrary point belonging to . Note for , is well approximated by the length of the line segment connecting the boundary points of . and can be computed approximately in similar ways. Replacing , , with corresponding discretized approximations in gives us an approximation for each . Then

| (10) |

The last line above provides a computable, optimizable and close approximation to as long as is small enough for each . We use throughout the algorithm.

The full algorithm for the HDR bandwidth selector is as follows:

-

1.

With given i.i.d random sample , estimate , , using two-stage direct plug-in strategies.

-

2.

Obtain the pilot estimator of , , based on the kernel density estimators , , .

-

3.

Let be the pilot estimator of , be the pilot estimator of and be the pilot estimator of .

-

4.

Substitute the estimators from Step 2 and 3 into the expressions for and to obtain and . Then

-

5.

Minimize the discretized approximation of described in the previous paragraph with Newton’s method to obtain the estimated optimal HDR bandwidth.

Note for the above procedure, in step 3, unlike the pilot estimator for , the pilot estimator for is obtained using with as the level. The reason we use instead of is because the error bound for estimating depends on the difference between the gradient of true density and that of the kernel density estimator and using yields a better error bound (See Lemma B.5 and proof of Corollary 3.1, 3.2 for details).

Newton’s method does not guarantee the optimum will be a positive definite bandwidth matrix. Luckily, in practice the global minimum appears to always be positive definite. The objective function appear to be locally convex although not globally convex (see Figures 2 and 3 for some plots of and ), so one has to be slightly careful about starting values for Newton’s algorithm.

Notice also that in Step 3 of the above algorithm we need to calculate the level having -probability . Hyndman (1996) suggests two similar methods for calculating . One is to use an appropriate empirical quantile of the values (“Approach H1”). An approach of this type is studied by Cadre et al. (2013) (and by Chen (2016) in calculating his ). However, this estimator is not equal to , and we have not yet quantified the difference, so we choose not to use this approach. Alternatively, Hyndman (1996) suggests resampling , and then using the appropriate empirical quantile of (“Approach H2”). Any desired accuracy can be attained by taking large enough. Another method is to simply use numeric integration: one can do a binary search over , computing the integral (numerically) at each level until one arrives at within desired accuracy. When , we found the numeric integration and binary search to be the fastest method for calculating . We suspect for higher dimensions, Approach H2 will be faster than numeric integration. Of course, Approach H1 is faster than the other two, and so it would be helpful to study how the Approach H1 estimator compares to .

In our pilot estimation process when , we use numerical interpolation to generate points on and to calculate . In more detail: we generate dense grid points along both the -axis and the -axis, and we estimate the density values at those grid points. Then we perform interpolation between grid points to get points such that the estimated density values at those points are (approximately) , and those points induce a partition of . Then for any in the partition, is defined by two end points, and can be approximated by the length of the line segment connecting those two end points. By generating enough dense and equally spaced grid points, we expect those line segments will approximate the true partition well and thus the Hausdorff integral will also be well approximated. However, this method is hard to implement in dimension larger than because there is no simple approximation for the volumes of corresponding partition sets of . One approach that may be fruitful for solving this problem is to use Quasi-Monte Carlo integration to calculate the Hausdorff integral (see De Marchi and Elefante, 2018). The idea is to generate a set of points on the manifold such that those points are approximately uniformly distributed and then we can approximate by . Analysis and numerical simulation for the method has been done for special Hausdorff integrals over special manifolds (cone, cylinder, sphere and torus). There is further work needed to extend the method to the more general manifolds that arise in our problem, which we believe is non-trivial and beyond the scope of this paper.

Note that the method just described for computing the approximation (10) can be implemented as a so-called midpoint method of numerical integration, for which classical analysis shows an error rate of ( is the number of equi-sized partitioning sets of the interval), provided that the function being integrated has bounded second derivative and the domain being integrated is a compact interval in (Hämmerlin and Hoffmann, 1991). The same error applies for using the midpoint method to numerically compute Hausdorff integrals over one dimensional compact manifolds embedded in , by the change of variables Theorem 2 (page 99) of Evans and Gariepy (2015). Thus the errors for our selected bandwidths in the corollaries below will also have an error dependent on , but in our experience can be chosen large enough that this is negligible (when ), so we do not include it in the analysis.

To give the asymptotic performance of our bandwidth selector, we need the following additional assumptions.

Assumption D3.

The true density function has four continuous bounded and square integrable derivatives.

Assumption K2.

is symmetric, i.e., for . And all the first and second partial derivatives of are square integrable.

Assumption H2.

For , the bandwidth matrix is symmetric, positive definite, such that elementwise, and as , where stands for Kronecker product.

This assumption and notation is as in Chacón et al. (2011). Here for a matrix , and . Now, recall that

and with . And

and , where

By letting , we see that minimizing is equivalent to minimizing

and minimizing is equivalent to minimizing

he following corollaries show the convergence rate of the estimated optimal bandwidth for .

Corollary 3.1.

Let Assumptions Assumption D1a, Assumption D2, Assumption D3, Assumption K, Assumption K2 and Assumption H2 hold. Assume further that is a unique minimizer of for and . Then

as , where is the minimizer of , is the minimizer of and is any minimizer of over the class .

Corollary 3.2.

Let Assumptions Assumption D1b, Assumption D3, Assumption K, Assumption K2 and Assumption H2 hold. Assume further that is a unique minimizer of for and . Then

as , where is the minimizer of and is the minimizer of .

Corollaries 3.1 and 3.2 both assume existence of a point . Corollary 2.1 and 2.2 show the existence of under one set of assumptions, although (as discussed after those corollaries) this conclusion holds in many other scenarios.

Remark 3.1.

In Corollary 3.1, we provide the rates of convergence for both the estimated optimal bandwidth to the oracle bandwidth selector and the estimated optimal bandwidth to the true minimizer of , while in Corollary 3.2, we only provide the rate of convergence for the estimated optimal bandwidth to the oracle bandwidth selector. The main difficulty for proving the convergence rate of the estimated optimal bandwidth to the true minimizer of , as we can see from the proof of Theorem 2.2, is understanding the term. At present, we can only show that is , but do not have a more explicit expression. Thus (even with higher order derivative assumptions) we cannot say anything stronger about , which is different than when is a discrete point set, in the case.

Remark 3.2.

The rates of convergence given in Corollaries 3.1 and 3.2 are known as relative rates of convergence since they are of the form for some (which is itself converging to ) (Wand and Jones, 1995). One can compare the relative rates from Corollaries 3.1 and 3.2 to the relative rates of other KDE bandwidth selectors. If we plug into the rate we recover the rate that arose in Theorem 3 of Samworth and Wand (2010). We can also make comparisons to bandwidth selector relative rates based on global loss functions. {mylongform} We consider the case where , where the most results are available for comparison, even though we focus on the case for our results in Corollaries 3.1 and 3.2. Scott and Terrell (1987) show that when has four derivatives that satisfy some further integrability conditions, then where is either the bandwidth based on a “least squares (unbiased) cross validation” procedure or on a “biased cross validation” procedure. (This requires also some assumptions on the kernel.) This slow rate of can be sped up; under various differentiability assumptions on , where is the bandwidth based on a “two-stage direct plug-in” procedure, a two-stage “solve the equation” procedure, or a “smoothed cross validation” procedure (Wand and Jones, 1995; Sheather and Jones, 1991; Hall et al., 1992). To achieve this rate, certain pilot bandwidths and kernels must be chosen correctly, in addition to having appropriate smoothness of . (In fact, somewhat more complicated versions of these procedures can achieve root- rates of relative convergence, again with appropriate smoothness of ; but simulations show that very large sample sizes are needed for these more complicated procedures to perform well, see e.g. (Wand and Jones, 1995, Section 3.8).) The rate exponent of is faster than but slower than . Duong and Hazelton (2005) study relative rates of convergence for various bandwidth selectors to the bandwidth matrix that minimizes mean integrated squared error, . (An alternative benchmark is the bandwidth that minimizes integrated squared error, , for which e.g., LSCV performs well (Hall and Marron, 1987), but the relative rates for that problem behave quite differently than the ones we study in Corollaries 3.1 and 3.2, so we do not mention them here.) Table 1 of Duong and Hazelton (2005) presents the convergence rates for plug-in, unbiased cross validation, biased cross validation, and smoothed cross validation bandwidth matrix estimators. (See also Sain et al. (1994a); Wand and Jones (1994); Duong and Hazelton (2003); Scott and Terrell (1987); Sheather and Jones (1991); Hall et al. (1992).) Consider . The unbiased and biased cross validation methods have relative convergence rates of . The smoothed cross validation method and the plug-in method of Duong and Hazelton (2003) both have rates of . The plug-in method of Wand and Jones (1994) has a rate of which is the fastest rate for all . The rate presented in our corollaries is faster than but slower than . This suggests that more careful development of our plug-in procedure, perhaps involving more careful pilot bandwidth selection procedures, could potentially improve the asymptotic rate. However the analysis (in particular understanding how behaves) may not be trivial. Also, procedures with better asymptotics may be inferior until the sample size is unrealistically large (this is somewhat common in bandwidth selection settings (Wand and Jones, 1995, Section 3.8)).

4 Simulations and data analysis

In Section 3, we used LS and HDR to develop a bandwidth selection procedure for level set and HDR estimation. We have implemented our procedure in an R (R Core Team, 2018) package lsbs. In this section, we assess the accuracy of and at approximating the true risks. We also use simulation to compare our procedure with the least square cross validation procedure (LSCV), An established ISE-based bandwidth selector (See Rudemo, 1982; Bowman, 1984). We simulate from the 12 bivariate normal mixture densities constructed by Wand and Jones (1993). These densities have a variety of shapes and have between 1 and 4 modes. In addition to those 12 density functions, we also simulate from

| (11) |

which is constructed to play a bivariate analogy to the sharp mode density 4 in Marron and Wand (1992) (see also Figure 1 of Samworth and Wand (2010)). The specific form in (11) is chosen to match that used by Qiao (2018).

We will close this section with a real data analysis in which we apply HDR estimation to novelty detection for the Wisconsin Diagnostic Breast Cancer dataset and Banknote Authentication dataset, which are available on the UCI Machine Learning Repository (http://archive.ics.uci.edu/ml/).

4.1 Assessment of approximation and estimation comparison

Since it is infeasible to exactly evaluate the true symmetric risk , we approximate the true risk through Monte Carlo. For given , for a large Monte Carlo sample size , where are independent realizations of . In a multivariate KDE the bandwidth matrix contains parameters. For the purpose of visualization, we restrict so that it can be parametrized by a single parameter .

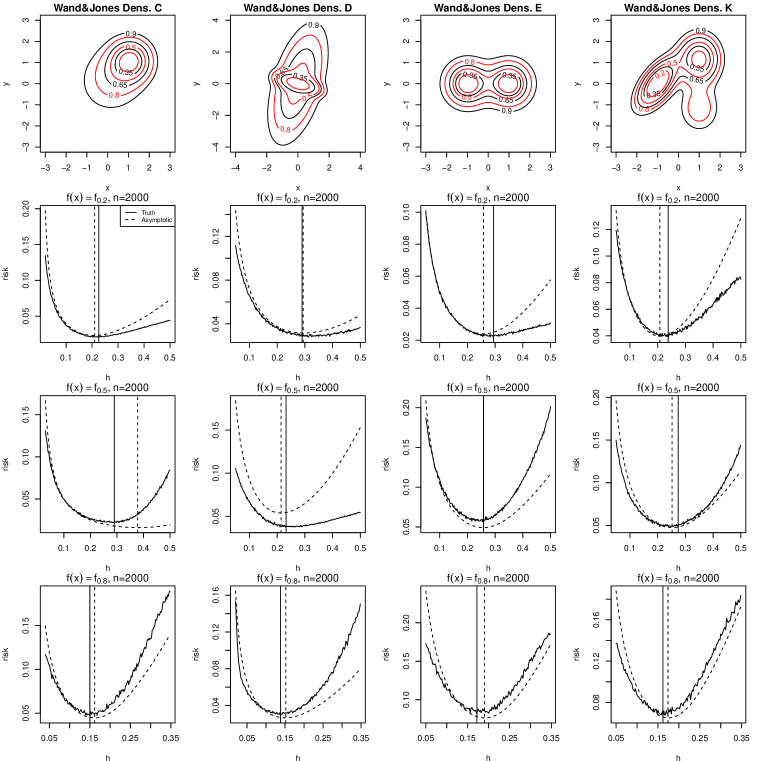

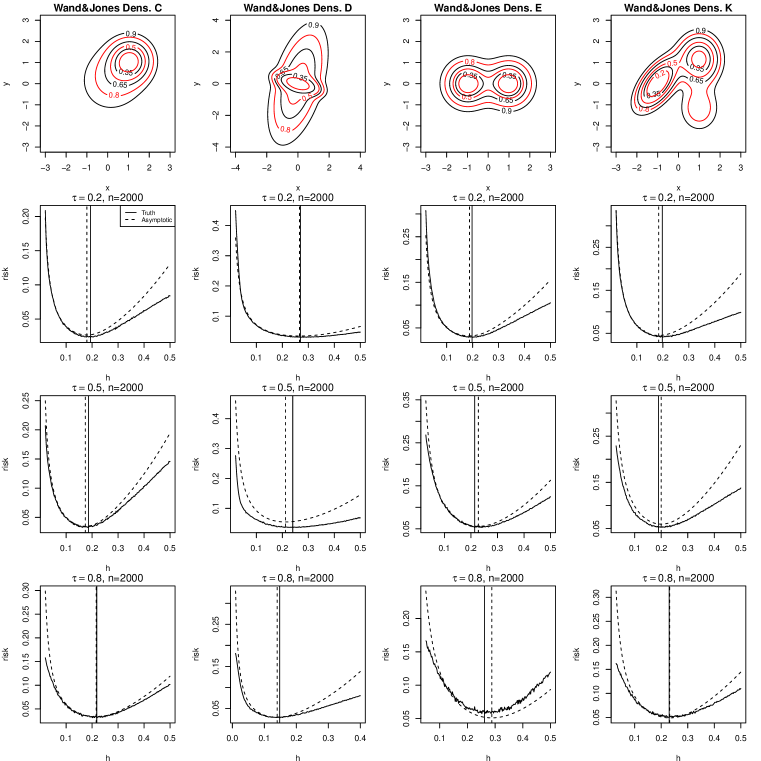

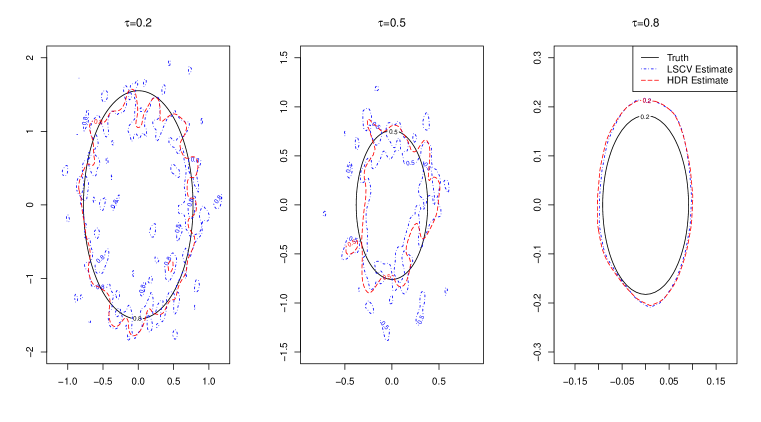

Figures 2 and 3 compare the asymptotic risk approximation with the simulated true risk for HDR estimation and LS estimation, respectively, for densities corresponding to Densities C, D, E and K of Wand and Jones (1993). Contour plots of the densities are given in the top row of the figures. In Figure 3, we choose to be 0.2, 0.5 and 0.8 while in Figure 2, we use the same levels but with true level values computed from the underlying true density functions. For both scenarios, the sample size is chosen to be 2000 and the kernel is set to be the Gaussian kernel throughout the simulation (Theorem 2.1 requires to be compactly supported, but nonetheless, the simulation results are not sensitive to the choice of Guassian kernel). We can see from Figures 2 and 3, in both scenarios, our asymptotic expansions provide a good approximation to the truth. The approximation works fairly well for the small values of bandwidth but the discrepancy becomes obvious when is larger, which is unlike what was observed from the simulation in univariate cases (see Samworth and Wand, 2010). This is consistent with our Assumption Assumption H which imposes an upper bound on the largest eigenvalue of the bandwidth matrix, restricting it not to converge too slowly. One more thing to notice from these two figures is that the optimal bandwidth chosen from the asymptotic expansion serves as a good approximation to the true optimal bandwidth, as we can see they are quite close in most cases in simulation.

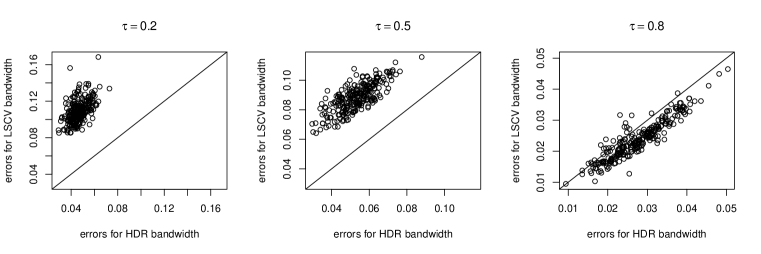

We ran a simulation study to compare the performance of our bandwidth selection method with LSCV for all the 12 densities in Wand and Jones (1993) and for density (11). For each density function, 250 Monte Carlo samples with 2000 observations were generated. For each sample, we estimated the 0.2, 0.5, 0.8 HDR with bandwidth matrices chosen by our method and LSCV respectively. The HDR error was calculated for each method in each replication. Figure 4 shows the plot of the estimation errors generated by the two methods for density (11). Figure 5 shows the boundaries of the estimated HDR by HDR bandwidth and by the LSCV bandwidth selector from one of the simulated samples. We can see for , the performance of HDR bandwidth selector outperformed LSCV bandwidth selector greatly for each simulated instance. For , the HDR bandwidth performed slightly less well than the LSCV bandwidth on average. One hypothesis for why our method suffers when is that Assumption Assumption D1b requires that in a neighborhood of the HDR. However, when , is close to having gradient zero on the true HDR which is close to the density mode.

It is worth noticing in Figure 5 that the HDR estimated by our method discovers the true underlying topological structure of the density, while the HDR estimated by LSCV does a very poor job of revealing the topological structure when or (the LSCV estimates have many spurious separate connected components rather than a single one).

Applying the Wilcoxon signed rank test to the simulated paired errors genererated by our HDR bandwidth and LSCV bandwidth showed that for , our method outperformed LSCV for 12 out of 13 density functions; for , our method did better for 8 out of 13 density functions; for , our method did better in 8 out of 13 density functions.

Note that for any given fixed density, it is likely to be the case for some HDR that the MISE-optimal bandwidth and the HDR-optimal bandwidth will approximately coincide. Thus we may not expect our method to be better than LSCV for all densities and levels simultaneously. Of course, in practice one does not know whether LSCV will work well for the value one is interested in. Our HDR method appears to work well for lower values, which are the useful values in many applications of HDR estimation. For example in novelty detection, the value of equals the probability of type-I error which is often set to be or ; in clustering analysis, corresponds to fraction of the data that will be discarded during analysis and is also set to be a value close to . As mentioned in the previous paragraph, this may be related to the assumption that on the HDR boundary. Relaxing this assumption is an important direction for future work, but seems likely to involve somewhat different approximations than the ones used in this paper. {mylongform}

| Density | Test statistic | p-value | Test statistic | p-value | Test statistic | p-value |

|---|---|---|---|---|---|---|

| Density A | 27743 | ¡2.2e-16 | 25356 | 1.816e-14 | 26608 | ¡2.2e-16 |

| Density B | 27743 | ¡2.2e-16 | 25297 | ¡2.2e-16 | 26361 | ¡2.2e-16 |

| Density C | 23200 | ¡2.2e-16 | 25419 | ¡2.2e-16 | 20725 | 5.388e-06 |

| Density D | 31349 | ¡2.2e-16 | 29159 | ¡2.2e-16 | 799 | 1 |

| Density E | 28630 | ¡2.2.e-16 | 22430 | 1.923e-09 | 24220 | 4.503e-14 |

| Density F | 24756 | 1.159e-15 | 3223 | 1 | 6433 | 1 |

| Density G | 29997 | ¡2.2e-16 | 14861 | 0.765 | 16265 | 0.3071 |

| Density H | 25968 | ¡2.2e-16 | 11889 | 0.9996 | 10535 | 1 |

| Density I | 8419 | 1 | 3713 | 1 | 3643 | 1 |

| Density J | 29488 | ¡2.2e-16 | 18411 | 0.008676 | 28905 | ¡2.2e-16 |

| Density K | 24555 | 4.689e-15 | 21411 | 2.861e-07 | 19746 | 0.0001958 |

| Density L | 24658 | 2.3e-15 | 15659 | 0.5101 | 18997 | 0.001919 |

| Density | Test statistic | p-value | Test statistic | p-value | Test statistic | p-value |

|---|---|---|---|---|---|---|

| Density A | 25385 | ¡2.2e-16 | 29238 | ¡2.2e-16 | 26520 | ¡2.2e-16 |

| Density B | 25690 | ¡2.2e-16 | 29290 | ¡2.2e-16 | 23990 | 2.027e-13 |

| Density C | 27574 | ¡2.2e-16 | 24585 | 3.814e-15 | 21568 | 1.392e-07 |

| Density D | 29298 | ¡2.2e-16 | 31363 | ¡2.2e-16 | 1486 | 1 |

| Density E | 21824 | 4.133e-08 | 29934 | 2.2e-16 | 22241 | 5.154e-09 |

| Density F | 5344 | 1 | 25023 | ¡2.2e-16 | 9866 | 1 |

| Density G | 15348 | 0.6168 | 28737 | ¡2.2e-16 | 17723 | 0.0377 |

| Density H | 16244 | 0.3136 | 25987 | ¡2.2e-16 | 11732 | 1 |

| Density I | 4573 | 1 | 9796 | 1 | 4485 | 1 |

| Density J | 20982 | ¡1.868e-06 | 29863 | ¡2.2e-16 | 29830 | ¡2.2e-16 |

| Density K | 21595 | 1.227e-07 | 21842 | 3.788e-08 | 22701 | 4.463e-10 |

| Density L | 16854 | 0.1542 | 24077 | 1.153e-13 | 20861 | 3.094e-06 |

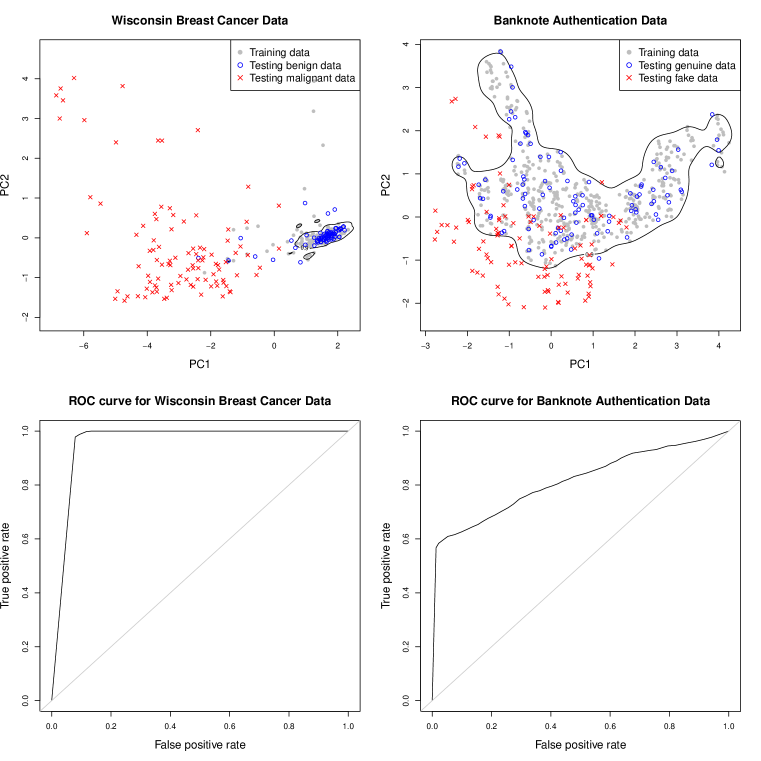

4.2 Real data analysis

We now discuss two real datasets. The Wisconsin Diagnostic Breast Cancer data contains 699 instances of breast cancer cases with 458 of them being benign instances and 241 being malignant instances. Nine cancer-related features were measured for each instance. For the Banknote Authentication data, images were taken of 1372 banknotes, some fake and some genuine. Wavelet transformation tools were used to extract four descriptive features of the images. For both datasets, we reduced the original features to the first two principal components. We apply our method to perform novelty detection for the two data sets. Novelty detection is like a classification problem where only the “normal” class is observed in the training data. Then, for a new data point , we want to test the null hypothesis (or, alternatively, to classify as “normal” or “anomalous”). For level set (HDR) based novelty detection, we can consider an oracle decision rule, or acceptance region, (based on knowing ); if , we accept the null hypothesis, and we reject otherwise. For the breast cancer data, “normal” means healthy, and for the banknote data, “normal” means genuine. If we take , then the oracle decision rule will have type-I error, or False Positive Rate (FPR), of (under a regularity condition). Additionally, under regularity conditions, has the minimum volume of any acceptance rule with FPR of , since HDR’s are minimum volume sets (Garcia et al., 2003). This property is beneficial for controlling the type-II error rate, or False Negative Rate (although the actual False Negative Rate depends on the unknown “anomaly” distribution).

In this section, for each of the two data sets we use a KDE with our bandwidth selection procedure to estimate an HDR based on the “normal” class data and use the estimated HDR to perform classification. We delete the observations with missing values for any covariates and randomly split the data set into two parts, training data and testing data. For the Wisconsin Breast Cancer data, 345 benign instances are contained in the training data and 200 (with half being benign and another half being malignant) are contained in the testing data. For the Banknote Authentication data, 400 genuine instances are contained in the training data and again, 200 (with half being genuine and another half being fake) are contained in the testing data. We estimate the HDR using our method based on the training data. The first row of Figure 6 shows the plot of the data and the boundaries of the HDR which are the decision boundaries for the two classification problems. The asymptotic FPR in these two classification problems is . For the Wisconsin Breast Cancer data, on the test data, the observed FPR is and the True Positive Rate (TPR) is . For the Banknote Authentication data, the observed FPR is , and the observed TPR is . We also generated full ROC curves for the two datasets which are shown in the second row of Figure 6. The ROC curves are based on different splits of the data into training and test sets (with the reported FPR and TPR given by the averages over the 30 test sets). The ROC curve clearly shows that the Wisconsin Breast Cancer data is an example where HDR-based anomaly detection is highly effective. The Banknote data is not as easy for our method; it may be the case that using an HDR based on all four variables improves the classification performance. We leave the very interesting question of how best to combine HDR-based classification with dimension reduction for future work.

5 Discussion

In this paper, we derive asymptotic expansions of the symmetric risk for LS estimation and HDR estimation based on kernel density estimators. We provide an efficient bandwidth selection procedure using a plug-in strategy. We also study by theory and by simulation the performance of our bandwidth selector. Simulation studies show that both our asymptotic expansion and our bandwidth selector are effective tools. The two asymptotic risk approximations we provide may also be useful in the analysis of other procedures, developed in future work, for doing LS or HDR bandwidth selection.

As discussed in the Introduction, the interesting paper Qiao (2018) also considers problems of bandwidth selection for KDE’s via minimizing asymptotic expansions of risk functions that are based on loss functions related to level sets. Qiao (2018) does not consider HDR estimation. Qiao (2018) does consider the LS estimation problem. Our Theorem 2.1 is similar to Qiao (2018)’s Corollary 3.1; both results consider the LS estimation setting, and give risk expansions based on loss functions that are given by integrating the symmetric set differences against (or against something similar). Our theorem requires only that have two continuous derivatives in a neighborhood of (which we believe to be approximately the weakest possible conditions), whereas Qiao (2018) requires four continuous derivatives. On the other hand, Qiao (2018) allows for using higher order kernels if one has higher order smoothness of . While Qiao (2018)’s Corollary 3.1 studies the same risk function approximation, , that we study in our Theorem 2.1, Qiao (2018) does not present any algorithm for minimizing and thus presents no simulations related to . Rather, Qiao (2018) focuses more attention on a different risk function (the “excess risk”) approximation that allows for an analytic solution, at least when .

There are many interesting avenues for extending the work done in the present paper. We describe a few here.

-

(A).

(Regression and classification) In the present paper we have considered only the density estimation context, but estimation of level sets of regression functions estimated by kernel-based methods is also interesting, as is consideration of classification problems.

Regression level set estimation has received less attention than density level set estimation, although it has been studied in some settings; Cavalier (1997) studies multivariate nonparametric regression level set minimax rates of convergence.

One method for classification is to estimate densities for different classes and then classify a point by the class density having highest value at the point. In that case, rather than estimating a level set of one density, one is estimating the level set of a difference of two densities. Mason and Polonik (2009, page 1110) discuss this approach to classification. In the context of an application in flow cytometry, Duong et al. (2009) also study estimation of HDR’s of density differences (without specifically focusing on classification). We believe the methods of this paper can be extended to those contexts.

-

(B).

(Topological data analysis and critical points) Another important avenue of research is to consider modifications of the assumptions under which our approximations hold. Level set estimation is one of the main tools in topological data analysis (TDA). Estimation of LS’s which have zero gradient (at some points) on the boundary (which is ruled out by our assumptions) is of great interest in TDA, because the topology of level sets can change as the level crosses critical points (points having zero gradient). In fact, in the context of using tools based on level set estimates, Wasserman (2016, Section 5) states that “the problem of choosing tuning parameters is one of the biggest open challenges in TDA”. Thus, developing tools for bandwidth selection when the gradient is zero would be very useful for TDA. Unfortunately, at points where the gradient is zero we cannot apply the inverse function theorem which is used in Lemma A.1 (implicitly) and by several results in Appendix B, so a very different analysis than the one we completed here may be necessary in such cases. In general, there are very few theoretical works on level set estimation at levels that contain critical values (points where is ). In fact, the only one we know of is Chen (2016), in which a rate of convergence of (where is Lebesgue measure) is derived.

-

(C).

(MCMC level sets) The work in this paper is restricted to the case where are independent. An important extension is to allow the to be samples from a Markov chain. It is well known that KDE’s often work similarly when the data exhibit weak dependence as when they are independent (Wand and Jones, 1995). This would allow our tools for HDR estimation to be used to form credible regions based on Markov chain Monte Carlo output in Bayesian statistical analyses. At present, ad-hoc methods are often used for forming credible regions based on Markov chain Monte Carlo output.

Appendix A Proof of main results

A.1 Proof of Theorem 2.2

First, we observe that

Then by Tonelli’s Theorem (Folland, 1999, Theorem 2.37), we have

| (12) |

For a density function on , let . By this definition, . The following lemma bounds the modulus of continuity of when the difference between two density functions is sufficiently small.

Lemma A.1.

Let the assumptions of Theorem 2.2 hold. Let be another uniformly continuous density function on and . Then there exists a constant such that for all sufficiently small, whenever .

It is intuitively believable that when the sample size is sufficiently large, the values of the two integrals on the right of (12) are mostly governed by the integrals over a small neighborhood of . To shrink the region of integration, for , and for a given level , we let , and . We also let

Then we can shrink the integral region using the following lemma.

Lemma A.2.

Let the assumptions of Theorem 2.2 hold. Then for a sequence converging to 0 such that , we will have

| (13) |

is as .

The definition of is simple and straightforward, however there is no explicit form for this quantity. So we want to seek an asymptotic expansion for . For a uniformly continuous density on and , we define

First, we observe for sufficiently small,

| (14) | ||||

as , where the last line comes from a similar argument of (71) and (72). A similar argument shows the same result when . Next, we look at

| (15) | ||||

where . For the first integral on the last line, since indicates that or , we have . Combining (16) with our result in Lemma A.1 yields

| (16) |

for . Next we need the following lemmas.

Lemma A.3.

Let the assumptions of Theorem 2.2 hold and the notation be as defined above. As , we have

| (17) |

Lemma A.4.

Let the assumptions of Theorem 2.2 hold and the notation be as defined above. As , we have

Now with Lemma A.3, A.4 and (16), we see that (15) equals . {mylongform} Because

Note that if , then . Combining this with (14) and the order of (15), we have

| (18) |

as . We want to apply (18) with , so that . To do this, note by Theorem B.1 {mylongform} (and so Assumptions Assumption H (as well as Assumptions LABEL:assm:DA and Assumption K)) that , , by (75), . We also have . {mylongform} Because,

where and . So

By Taylor Expansion, , depends on . Now we have

By assumption LABEL:assm:DA is bounded, there exists , such that

Then applying the above results, we have

| (19) |

Note from (2) and (19), for fixed , can be expressed as the average of i.i.d. random variables with a negligible stochastic error term. This motivates us to use the Berry-Essen Theorem (Ferguson, 1996) to approximate the two probabilities appearing on the right of (13). In order to do so, we will need to approximate the mean and variance of , which we do in the next lemmas.

Lemma A.5.

Let the assumptions of Theorem 2.2 hold and the notation be as defined above. Then we have

| (20) |

as .

Recall and are defined in Theorem 2.2. The next lemma shows is negligible compared with other terms in the expansion.

Lemma A.6.

Let the assumptions of Theorem 2.2 hold and the notation be as defined above. Then .

Now according to Lemma A.2 and (12), we have

Then by Lemma B.4 when is small enough, the dominating term on the last line above is equal to

| (21) | ||||

where is the unit outer normal vector of at . Now for a fixed , let for , we see (21) equals

| (22) | ||||

| (23) |

By Taylor Expansion, we have

for some . Since by Assumption Assumption D1b, has bounded first derivatives, we see the dominating term in (22) equals

| (24) | ||||

as . {mylongform} Because

We can further shrink the region of interest by the following lemma.

Lemma A.7.

Let the assumptions of Theorem 2.2 hold and the notation be as defined above. Then for sufficiently large, is a strictly monotone function of , with a unique zero . For a sequence diverging to infinity and , let

We have

| (25) |

as .

To complete the proof of Theorem 2.2, by (24) and Lemma A.7 it suffices to show that there exists a sequence diverging to infinity slowly such that

For , let and , where

Then by (18) and (19), we can write , where . {mylongform} Because by (18) we have

and from Lemma A.6 we know , and , so . Then for any ,

which suggests . By Lemma A.6, we know is uniformly in and . Let diverge slowly such that for fixed ,

-

•

uniformly for . {mylongform} Because we can let diverge slowly such that .

-

•

, uniformly for and , by Assumption Assumption D1b part 3. {mylongform}

uniformly in and . By Taylor Expansion we know

uniformly in and because by Assumption Assumption D1b we have bounded third derivative around . And uniformly in and . Then

uniformly in and .

-

•

uniformly for and . {mylongform} Since is uniformly in and , and , uniformly for and . Besides, we have

uniformly. So .

Then

Applying the Berry-Esseen theorem (Ferguson, 1996) to the last two terms on the last line yields

Now since uniformly, . And it can be shown that , so we further have

and then

uniformly in and . A similar argument shows a lower bound of the same order. {mylongform}

Now we look at the integrated error

Since

uniformly in and , and

We can see that

uniformly in . From (C) we know is uniformly , then

and similarly

So we have

It remains to see from Lemma B.3 that

A.2 Proof of Theorem 2.1

We also provide a brief proof for Theorem 2.1, which is a simpler and shares the same idea as that of Theorem 2.2. First, we have

| (26) |

Like Lemma A.2, we can shrink the region of interest. We show that for each sufficiently small, we have

as .

Observe that under Assumption Assumption D1a if is sufficiently small, then there exists s.t for and for . By reducing if necessary, for ,

Similarly we can show the same bound for . Then

where for large enough. So with the same argument in proof Lemma A.2, the above quantity is . Further, we have that for a sequence converging to 0 such that ,

| (27) |

and we also prove this by showing that which is defined as

is as . Note that there exits a constant small s.t if we take , then we have when .Then for ,

We can derive the same bound for . Then

is when is large enough.

Now the risk function can be expressed as

Then according to Lemma B.4, when is small enough

where is the unit normal outer vector at . And by simple transformation,

To further shrink the intervals of interest, we also argue that when is large enough, is a strictly monotone function of with a unique zero . Now we claim for a sequence diverging to infinity,

as , where . For detail of proof, please refer to the proof of Theorem 2.2.

Now by previous steps, we know

To complete the proof, it suffices to show the dominating term above is equal to . Let and . Then . Now let diverge slowly such that

| (28) |

by Assumption Assumption D1b part 3, and

| (29) |

uniformly for and . Then

applying the Berry-Esseen theorem (Ferguson, 1996, Page 31) to the first term above yields

and

uniformly for and . A similar argument shows a lower bound of the same order. Next, with a similar argument as we had in the last step of proof for Theorem 2.2, we can show the integrated error

So we have

By Lemma B.3,

This completes the proof.

A.3 Proof of Corollary 3.1

Let . If is of order then by Assumption Assumption D3,

uniformly in . From the proof of Theorem 2.1, if we pick , and , we can further quantify the error in equations (28) and (29) as

and further

With a similar argument as Corollary 2.2, we see .

Now we study . Let , , . Let

and with slight abuse of notation, we let be defined similarly where we substitute with , with and with . We look at the difference

| (30) | ||||

where . By Lemma B.5, when and as , the second term on the last line above is . For first term on the last line above, by Jensen’s inequality we know . So for any (large) we have

which is bounded above by

by Markov’s inequality. And by Tonelli’s Theorem, we have .

Extension of classical results on the stochastic errors of kernel density estimator and derivative estimator using unconstrained (full) bandwidth matrix can be found in Chacón et al. (2011). Since we assume the true density function has 4 continuous bounded derivatives, by Theorem 4 in Chacón et al. (2011) with slight modification, it can be easily seen , , is . Thus , and . And we can also see

Thus, we can check that is , and the first term on the last line of (30) is . We can conclude that for any , we have uniformly for . Then we have , where and is bounded from 0 as . This gives us , and recall that , , we conclude

Combining this result with gives us .

A.4 Proof of Corollary 3.2

Similar to the proof of Corollary 3.1, let , , , and let . Since we assume the true density function has 4 continuous bounded derivatives, again by Theorem 4 in Chacón et al. (2011), it can be easily seen , , , . And by Lemma A.1, . We first look at the difference

| (31) | ||||

Since by Chacón et al. (2011), it is easy to see the first term on the last line above is . Recalling , we can bound the second term as

By Lemma B.5, the first term is of order when and as . Then, by Taylor expansion, we have

where . Then we have

| (32) | ||||

From the proof of Lemma B.5, we can see when is sufficiently large, the derivative on the last line of (32) is uniformly bounded. Moreover, by Lemma A.1, , so we have

Then

and thus . Using exactly the same trick, we can show

Next, we provide the bound for . Similarly, we have

| (33) | ||||

and since we assume has bounded second derivatives, the difference on the second line above . Now we show . It can be seen that

and then

Further by Proposition A.1 of Cadre (2006),

and

and thus

when .

Now for the last term of (33), by Jensen’s inequality we have

and then for any (large) ,

where we applied Markov’s inequality to obtain the upper bound. Applying Tonelli’s Theorem yields

So .

Now from Chacón et al. (2011), we know that , . And using a similar trick as for , we have

And we can conclude that for any , we have uniformly for . Then we have , where and is bounded from 0 as . This gives us , and recalling that , , we conclude

Appendix B Additional theorems and proofs

The following theorem is a slight extension of Theorem 2.3 of Giné and Guillou (2002) to allow general bandwidth matrices and to apply to gradient estimation. Its proof is essentially the same as that of their Theorem 2.3, so is omitted.

Theorem B.1.

Let be i.i.d. from a bounded density on , and let Assumptions Assumption K, and Assumption H hold. We have

| (34) |

and

| (35) |

Here and depend on and

Here , for a constant depending only on the kernel (and dimension ).

See GineGuillou-notes.tex for details.

The proof of Theorem B.1 also yields the following probability bound which we need in particular. {mylongform} In the corollary we consider a single value, rather than the range , simplifying the argument.

Corollary B.1.

Let be i.i.d. from a bounded density on , and let Assumptions Assumption K, and Assumption H hold. Then for some constant and for , we have

| (36) |

where depends on , , and . Similarly, for small enough (with bound depending on and ),

| (37) |

where depends on , , and , and where is the smallest eigenvalue of .

Proof.

We let

(which is a VC class by Assumption Assumption K). We have that for

| (38) |

Thus we set

which satisfy the conditions of Corollary 2.2 of Giné and Guillou (2002) so we have and (depending on and ) from the corollary, so we set , and so that (7) in Giné and Guillou (2002) is satisfied (using that for the lower bound). We conclude that (38) is bounded above by

where , completing the proof.

A similar proof shows that (37) holds. Let . Then , so {mylongform} equals {mylongform}

which is bounded above by

where is a row of , and the previous display is bounded above by {mylongform} (rather than equal to)

by the Cauchy-Schwarz inequality where is a row of (and, recall, is just Euclidean norm). Since where is the largest eigenvalue of , the previous display is bounded above by {mylongform}

which equals

where

is a VC class by Assumption Assumption K. We thus take and and apply Corollary 2.2 of Giné and Guillou (2002). Here is the largest eigenvalue of . We take and . Then (7) of Giné and Guillou (2002) is satisfied since . {mylongform} That is, the lower bound in our (LABEL:eq:t-range) ((7) of Giné and Guillou (2002)) is

which holds if and only if . This yields (37). ∎

The following is referred to as the -Neighborhood Theorem by Guillemin and Pollack (1974). It states that for certain manifolds, so-called Tubular Neighborhoods exist.

Theorem B.2 (page 69, Guillemin and Pollack (1974)).

For a compact boundaryless manifold in and , let be the open set of points in with distance less than from . If is small enough, then each point possesses a unique closest point in , denoted . Moreover, the map is a submersion.

A map between manifolds is a submersion if, at all points, the Jacobian map between corresponding tangent spaces is of full rank; see page 20 of Guillemin and Pollack (1974).

The following is referred to as the -Neighborhood Theorem by Guillemin and Pollack (1974). It states that for certain manifolds, so-called Tubular Neighborhoods exist.

Theorem B.3 (page 69, Guillemin and Pollack (1974)).

For a compact boundaryless manifold in and , let be the open set of points in with distance less than from . If is small enough, then each point possesses a unique closest point in , denoted . Moreover, the map is a submersion.

A map between manifolds is a submersion if, at all points, the Jacobian map between corresponding tangent spaces is of full rank; see page 20 of Guillemin and Pollack (1974).

Theorem B.4 (Taylor’s Theorem in Several Variables).

Suppose is of class on an open convex set . If and , then

| (39) |

where the remainder is given in Lagrange’s form by

| (40) |

for some .

Lemma B.1.

Let be a -dimensional vector and be a matrix. Then , where .

Proof.

We have

∎

Lemma B.2.

Let Assumption Assumption D1b and Assumption D2 hold, the for small enough, there exists constant and another sequence such that and when .

Proof.

The existence of such can be proved by Theorem B.3, which says for all sufficiently small, then for each there exist a unique and such that , where

is outer unit normal vector of at . And here we pick sufficiently small such that not only the Tubular Neighborhood Theorem (Theorem B.3) but also the following hold: When , , for some .

Note these two conditions are both feasible because under Assumption Assumption D1b, has two continuous bounded derivatives, which indicates both and are Lipschitz. Then for ,

where for some , . So

Note that

Let , so by Assumption Assumption D1b, . Then by Cauchy-Schwarz inequality

We can choose sufficiently small such that . Then since is bounded, . Now for , , so

.

∎

Lemma B.3.

Let and be two constants, then

Proof.

Note

And

which equals

Also,

which equals

Thus

∎

Recall that and that we let be the unit outer normal vector to the manifold at . The following lemma gives a very useful approximate change of variables type of theorem. {mylongform} It holds for any such that Lebesgue integrable on (with and defined below). We only use it for bounded .

Lemma B.4.

Let either Assumption Assumption D1a or Assumption Assumption D1b hold, and let Assumption D2 hold for the density . Let either in the LS setting or let in the HDR setting. Let be such that the conclusion of Theorem B.3 holds for . Let be a bounded Lebesgue measurable function on and let . Then

| (41) |

where is a constant depending on .

Proof.

Since is compact (Assumption Assumption D1b), it admits a finite “atlas”, , meaning is an open cover of , that is a diffeomorphism, and that is open in . Let . Let be defined by

Thus is the unit outer normal to at . By the change of variables Theorem 2 (page 99) of Evans and Gariepy (2015) (see also the example on page 101),

| (42) |

By the change of variables Theorem 2 (page 99) of Evans and Gariepy (2015) (see also the example on page 101), for any with ,

| (43) |

Note that in Evans and Gariepy (2015), a function is -integrable if the integral is well-defined, although possibly . Then is -summable if it is integrable and the integral is finite. This is defined on page 18. The formula for is

| (44) |

Here,

| (45) |

by Theorem 3 (page 88) of Evans and Gariepy (2015). {mylongform} is defined on page 91. (The above formula is then given as Theorem 3 on page 88 for “[[ ]]”.) Similarly,

| (46) |

where and . {mylongform} This is from

| (47) |

We can see that

| (48) |

Thus, because is perpendicular to the tangent space of at , and this tangent space is equal to the span of the columns of for , letting , we have

| (49) |

where

| (50) |

In particular,

| (51) |

Note that from (49) we have

| (52) |

Now

| (53) |

as (Magnus and Neudecker, 1999) for any square matrices and of the same dimension. Thus

which equals

which equals

| (54) |

by differentiability of away from , since is uniformly bounded away from . {mylongform} (Need add/state the conditions from the last few lines giving uniform-in-?) The term is uniform in . Thus, by (52), (42), and (46),

| (55) |

where where is the constant from the term in (54). This proves the lemma if is parameterizable by a single open set; for the general case, we use a partition of unity. Let be a finite (smooth) partition of unity subordinate to (Spivak, 1965, page 63). Define for (which thus forms a partition of unity of subordinate to ). Then replacing in (55) by , since each is bounded, smooth, and zero outside one of the ,

since and where . ∎

The equality (and the similar one for the integral over ) is just by definition of the integral, which is defined via a partition of unity. See spivak. I don’t know if evans and gariepy explicitly do this or not.

Lemma B.5.

Let Assumption Assumption D1a hold.

-

1.

Assume that is a continuously differentiable function on an open neighborhood of in . For near , let and assume is compact for all in a neighborhood of . Then is continuously differentiable in a neighborhood of .

-

2.

Let be the KDE (defined in (2)), where satisfies Assumptions Assumption K and Assumption K2, and satisfies and as . Let . Let Assume is potentially random but satisfies and , for some . Then

as .

Proof.

Proof of Part 1: Fix . By Assumption Assumption D1a, we may assume without loss of generality that . Define

and note that . Since is twice continuously differentiable at (Assumption Assumption D1a), is twice continuously differentiable at . By the inverse function theorem (pages 67–68, Bredon (1993)), exists and is twice continuously differentiable in a neighborhood of . Clearly equals for some that is twice continuously differentiable and satisfies

Thus

is a twice-continuously differentiable invertible parameterization (is a “ diffeomorphism”) from an open set to where is open in . {mylongform} (Open in the subspace topology.) Each has such a diffeomorphism onto an open neighborhood ; since is compact, we can pick a finite number of them that cover and construct a partition of unity (Spivak, 1965, page 63) on the cover. We will continue considering our fixed and the above-constructed parameterization on a neighborhood of . At the end of the proof, our local result can be made global by using the partition of unity.

Now, where is Lebesgue measure (Evans and Gariepy, 2015). Here is continuously differentiable in (in a neighborhood of ) since is twice continuously differentiable and since . {mylongform} Since is a diffeomorphism, so is of full rank . We also know that is continuously differentiable in since is assumed continuously differentiable. {mylongform} (Note we need to be differentiable; the setup is quite different than that of the Fundamental Theorem of Calculus.) Since is continuous so is bounded on , some , we can apply the Leibniz rule (Billingsley, 2012) to see that

(Note that to say that is defined on requires an explicit construction such as the one we made above.) Thus, the derivative on the left side of the previous display exists, meaning that is indeed differentiable for near , as desired. This is true on the neighborhood ; it extends to the case where is replaced by by using the partition of unity we constructed above.

Proof of Part 2: We write , suppressing dependence on . For , let , and let . We will explicitly construct , for some open and , by the inverse function theorem, and then check that is and that is . Then the proof can be finished as the proof of the previous part was finished.

Fix . Define . As in the proof of the previous part, note that (when is small), so by the inverse function theorem exists, is twice continuously differentiable in a neighborhood of , and clearly satisfies . Let and note by definition

| (56) |

From this we will derive formulas for the first and second derivatives of . In this proof, for a function we use the notation for and for . Taking of (56) for , we see that

| (57) |

Applying to (56), we get that

| (58) |

and applying to (56), we get

| (59) |

Applying to (57) yields

| (60) |

and, letting , since and , this implies that {mylongform}

so

| (61) |

To understand the expression in (61) we need to control , , and . Applying to (58) we see that

so

| (62) |

We will next verify that and are (which is under our assumption on (Chacón et al., 2011)). Then by (61) and (62), we will see, uniformly for , that

| (63) |

Note that by (58), and (since by assumption and ).

Now applying to (58), we see

| (64) |

so . Applying to (the left expression in) (58) yields

| (65) |

Thus by (64) we see , so (63) holds. {mylongform} To show the three terms are , possibly could just do this in one or two steps from Id and differentiating twice and making a more abstract argument about how the second derivatives of are algebraic expressions in the zeroth, first, second derivatives of ? Still may need to bound denominators away from zero conceivably so maybe necessary to see what those expressions are.

Now we let

which we have shown is a parameterization from an open set to where is open in . We can check that is continuously differentiable in for by (63), and, by three Taylor expansions,

| (66) |

where , since is uniformly for , since uniformly for (by (59)), and since is continuously differentiable in a neighborhood of . In fact, we can see that for a constant . By the Fubini-Tonelli theorem, , so we can see

| (67) |

by Markov’s inequality. Combining (66), (67), and we get

Then the proof can be finished as in the proof of Part 1, including using a partition of unity to extend to and to to conclude from the previous display that ∎

B.1 Proof of Corollary 2.2

By our assumptions of unimodality and spherical symmetry of , we have that and are constant on , and we denote these two quantities as and . Then for we can write

and where

Some additional computations and substitutions are as follows. Note that

Since

we get the formula for and above. Then

where . Note that . Let , We will thus minimize

| (68) |

over . By the change of variables

| (69) |

minimizing (68) is equivalent to minimizing

Note that as and as , so attains its minimum on . Now, has a unique minimum if has a unique , and by calculation,

has a unique if and only if

| (70) |

has a unique . We can compute the derivative of (70) to be

for . Thus (70) is strictly increasing on , is negative at , and approaches as , and so (70) has a unique zero. {mylongform} See mathematica notebook for derivative computations. We can compute the first and second derivatives of (70) to be

(We do not actually need the second derivative it seems.) Let be the unique minimum of , and let . By (69), minimizes (68), and so minimizes . By Theorem 2.2, we conclude that for any that minimizes , .

Appendix C Proof of intermediate results

Proof of Lemma A.1.

From the proof, we shall see only depends on . Let . Then when is sufficiently small,

On the second line of the above inequalities, when by continuity of measure. So when is sufficiently small. By Proposition A.1 of Cadre (2006),

| (71) |

So we can express as

| (72) |

by Lemma B.5, and thus see that

when is sufficiently small. So . For the upper bound, with a similar argument, {mylongform}

when is sufficiently small, we get . So we proved for sufficiently small. ∎

Proof of Lemma A.2.

We first prove an intermediate result that

| (73) |

is as for fixed sufficiently small. Observe that under Assumption Assumption D1b if is sufficiently small, then there exists such that for and for . By reducing if necessary, for ,

where is the constant we defined in Lemma A.1 ; by that lemma, we have

so

| (74) |

A similar argument yields the same upper bound for when . {mylongform}

Now, since is uniformly continuous,

here is the modulus of uniform continuity of and thus the above quantity converges to 0 as by Lebesgue Dominated Convergence Theorem. Now by Assumption Assumption D1b,

as . Together with the inequality (74) together, this yields that for sufficiently large,

which is bounded above by

where the last inequality comes from Corollary B.1.

Now it suffices to show that , where is defined as {mylongform}

Using Taylor expansion, we have {mylongform} (See Theorem B.4 in Appendix or folland2002advanced, Page 91, Theorem 2.68) yields

where for some . Under Assumption Assumption D1b, has bounded second derivatives and let be such that . Then {mylongform}

| (75) | ||||

as . Now by Lemma B.2, there exists a constant small enough that if we take , then we have when . Moreover, by our assumption, so for sufficiently large, by (75), . Then for large enough,

| (76) | ||||

as . ∎

Lemma C.1.

Let be another uniformly continuous density function satisfying Assumption LABEL:assm:DA and such that for some sufficiently small. Then if Assumption LABEL:assm:DA holds for , we will have for every where , it is within of , i.e., there exists some such that .

Proof.

Let be such that . If , let be the inner outer unit normal vector to at . And we let . Then by Taylor expansion,

where . Since has bounded second derivatives. Let be such that . Then by Lemma B.1, the second order term

This ensures that we can take small enough such that .

This can be achieved by letting be such that , that is, . This choice of upper bound for depends on . However, we can also choose an upper bound not depending on . Note in our assumption, is bounded away from 0 for and by the result of step 1, if is sufficiently small, we can have . Then we can make small enough such that and apparently in this case the upper bound for does not depend on .

So we have

and we also know

Since we can regard as a continuous function in , we conclude for some , we can have . Then

which gives us

To bound the second term of the last line, note