Distributionally Robust Co-Optimization of Power Dispatch and Do-Not-Exceed Limits

Abstract

To address the challenge of the renewable energy uncertainty, the ISO New England (ISO-NE) has proposed to apply do-not-exceed (DNE) limits, which represent the maximum nodal injection of renewable energy the grid can accommodate. Unfortunately, it appears challenging to compute DNE limits that simultaneously maintain the system flexibility and incorporate a large portion of the available renewable energy at the minimum cost. In addition, it is often challenging to accurately estimate the joint probability distribution of the renewable energy. In this paper, we propose a two-stage distributionally robust optimization model that co-optimizes the power dispatch and the DNE limits, by adopting an affinely adjustable power re-dispatch and an adjustable joint chance constraint that measures the renewable utilization. Notably, this model admits a second-order conic reformulation that can be efficiently solved by the commercial solvers (e.g., MOSEK). We conduct case studies based on modified IEEE test instances to demonstrate the effectiveness of the proposed approach and analyze the trade-off among the system flexibility, the renewable utilization, and the dispatch cost.

Index Terms:

Power dispatch, renewable energy uncertainty, robust optimization, do-not-exceed limit, affine policy.Nomenclature

- Indices and Sets

-

Index for time period, thermal unit, renewable resource, node, and transmission line, respectively.

-

Numbers of time periods, thermal units, renewable resources, nodes, and transmission lines, respectively.

-

Sets of thermal units and renewable resources at node , respectively.

-

for positive integer .

- Parameters

-

Fuel cost function of thermal unit .

-

Unit cost of overestimating and underestimating the output of renewable resource during time period , respectively.

-

Forecasted output of renewable resource during time period .

-

Load of node during time period .

-

Transmission capacity limit of line .

-

Shift distribution factor of node to line .

-

Minimum and Maximum generation capacity of thermal unit , respectively.

-

Upward and downward ramp-rate of thermal unit (MW/min), respectively.

-

Dispatch interval (min) and response time window (min), respectively.

-

Minimum and maximum generation capacity of renewable resource , respectively.

-

Empirical mean and empirical variance of the prediction error of renewable output during time period , respectively.

-

Weight coefficient between power dispatch and renewable utilization.

-

Random variable representing the output deviation of renewable resource from its forecast value during time period .

-

Lower bound on renewable utilization.

- Decision Variables

-

Scheduled generation amount of thermal unit during time period .

-

Actual generation amount of thermal unit at time .

-

Lower and upper do-not-exceed limits of , respectively.

-

Renewable utilization probability.

-

Coefficients of the affine decision rule.

-

Auxiliary dual variables in the reformulation of the adjustable joint chance constraint.

I Introduction

The renewable energy (e.g., wind and solar power) leads to random nodal injections in the power grid and presents a significant challenge to the power system operation. Many methods have been proposed to hedge against the renewable energy uncertainty, including stochastic programming (see, e.g., [1, 2, 3]) and robust optimization approaches (see, e.g., [4, 5]). These approaches incorporate the uncertainty based on pre-specified models, e.g., probability distribution in stochastic programming (SP) approaches and uncertainty set in robust optimization (RO) approaches. Although SP and RO approaches are widely applied, we may still need to address the following two challenges:

- Challenge 1

- Challenge 2

To address Challenge 1, the ISO-NE proposes an inspiring concept of do-not-exceed (DNE) limits under a given power dispatch strategy [6]. The DNE limits assign an admissible range of renewable energy to each node of the transmission system. This provides a clear guideline for utilizing renewable energy: the system accommodates any nodal injection that lies within the admissible range, and otherwise emergency regulations (e.g., renewable energy curtailment, fast-starting units, and load shedding) may have to be used. In addition, the DNE limits also offer a convenient way of defining and measuring of the system flexibility [12].

Recently, the DNE limits have received increasing attention in the literature. [7, 13] show that the admissible range of a power grid is mathematically equivalent to a polytope. This generalizes the concept of the DNE limits, which take the form of a hypercube. In [6, 7, 13], the admissible range is obtained based on a given power dispatch strategy, which, however, may not be optimal for accommodating renewable generation. As a result, this might underestimate the dispatch capability of the power system in accommodating renewable energy. As an alternative, many studies propose to co-optimize the power dispatch and the DNE limits. [14] proposes a single-stage RO model that co-optimizes the power dispatch and the polytopic admissible range. To incorporate recourse actions (e.g., power re-dispatch), [15] proposes an adjustable RO model in which recourse actions follow an affine decision rule (ADR) with given coefficients. [16] studies an adjustable RO model with ADR and optimized coefficients. Additionally, the proposed model in [16] incorporates risk criteria based on the radius and the coverage probability of the admissible range. Without applying an ADR, [17] considers an adjustable RO model that co-optimizes power dispatch and DNE limits with full recourse. Later, [8] extends [17] by incorporating unit commitment (UC) into the co-optimization, and employs the column-and-constraint generation (CCG) algorithm [18] to solve the proposed model. [19] also considers an adjustable RO model with full recourse that incorporates UC and a polytopic admissible range. Furthermore, [20] considers the risk of the renewable energy being realized outside of the admissible region, which result in, e.g., curtailment of renewable energy. Differently, [21] models this risk by maximizing the probability that the renewable energy being realized within the DNE limits. Then, this model is solved by using the sample average approximation algorithm. [22] considers an adjustable RO model with both discrete and continuous recourse and proposes to solve this model with a nested CCG algorithm. [23] incorporates topology control into the co-optimization and considers zonal DNE limits. It is worth mentioning that solving the adjustable RO model with full recourse requires repeatedly solving mixed-integer programs with big-M coefficients (see, e.g., [13, 23, 20, 8]), which may be challenging when many nodes of the power grid incorporate renewable energy.

A natural way of mitigating Challenge 2 is to employ distributionally robust optimization (DRO). In contrast to SP that considers a single probability distribution, DRO considers a family of probability distributions that are plausible of modeling the renewable energy. We term the family of distributions as an ambiguity set. In the existing literature, ambiguity sets based on the moments of uncertainty (e.g., mean, variance, etc.) are commonly applied (see, e.g., [24, 25, 26, 27]). Other distributional information based on, e.g., the Wasserstein distance [28, 29], the -divergence [11, 30], and the unimodality [16, 31, 32], have also been proposed to characterize the ambiguity set. Accordingly, DRO formulates a robust counterpart of SP and hedges against the worst-case probability distribution within the ambiguity set.

In this paper, we consider a distributionally robust (DR) co-optimization model for the power dispatch and the DNE limits. Our model follows [20, 21] to incorporate the operational risks. Specifically, we consider the DR probability that the renewable energy being realized within the DNE limits. We further extend the model to incorporate the DR expected cost of overestimating/underestimating the renewable energy. By using ADR with optimized coefficients, we show that this model admits a conic programming reformulation that can be efficiently solved by the commercial solvers (e.g., MOSEK). The proposed model assumes a fixed UC and power grid topology. Nevertheless, these decisions can also be incorporated into this model with slight changes, leading to mixed 0-1 conic programming reformulations.

The remainder of this paper is organized as follows. Section II presents the mathematical formulation and Section III describes the solution methodology. Section IV extends the model and solution methodology to incorporate alternative operational risks. Section V reports the case studies that demonstrate the effectiveness of the proposed approach, before we draw conclusions in Section VI.

II Mathematical Formulation

We describe the co-optimization model of power dispatch and DNE limits in Section II-A and the adjustable DR chance constraint in Sections II-B.

II-A DNE Limits

Given the forecasted renewable energy outputs , the nominal economic dispatch (ED) model maintains the generation-load balance under operational restrictions. Mathematically, we formulate the constraints of a multi-period nominal ED model as follows:

| (1a) | |||

| (1b) | |||

| (1c) | |||

| (1d) | |||

where represents the pre-dispatch strategy based on the forecast renewable generation , constraints (1a) represent the generation-load balance, (1b) represent the transmission line capacity restrictions based on the dc approximation of the power flow equations, (1c) represent the capacity limits of the thermal units, and (1d) represent the ramp-rate limits of the thermal units. When taking the uncertainty of renewable energy and the DNE limits into account, the power system aims to accommodate any nodal injections of renewable energy through corrective power re-dispatch, as long as such injections lie within the DNE limits. We formulate this requirement as follows for all :

| (2a) | |||

| (2b) | |||

| (2c) | |||

| (2d) | |||

| (2e) | |||

| where constraints (2a)–(2d) are counterparts of (1a)–(1d) with regard to the power re-dispatch variables and constraints (2e) represent the ramping capacity limits within the response time window. In this paper, we assume that follows an ADR, i.e., is the following affine function of : | |||

| (2f) | |||

where and represent the response of to the forecast error and can be adjusted to optimize the objective function (to be specified in Section II-B). On the one hand, the ADR corresponds to the incremental output of the automatic generation control (AGC) units as an affine function of the renewable generation deviation. For the non-AGC units, we can set . On the other hand, the ADR restricts the search space of the recourse variables and so yields a conservative approximation of the constraints (2a)–(2e).

II-B Adjustable DR Joint Chance Constraints

We note that formulations (1a)–(1d) and (2a)–(2e) do not incorporate any distributional information of the forecast error . This may cause a mismatch between the DNE limits and renewable energy. For example, it may be unlikely that the renewable generation is realized within the DNE limits, and accordingly we may curtail a significant portion of the renewable generation. To address this challenge, we first designate that the DNE limits contain the forecasted output of renewable energy and lie within the capacity limits of the renewable generation:

| (3) |

Second, we consider an adjustable joint chance constraint to measure the utilization of renewable energy:

| (4a) | |||

| (4b) | |||

where estimates the probability of fully utilizing the renewable energy and represents a lower bound of . In this paper, we assume that (see Theorem 1). This assumption is not very restrictive because power system operators often desire high utilization of renewable energy (see, e.g., [33]). Additionally, we note that represents a decision variable in our model and can be adjusted to optimize the trade-off between the power dispatch cost and the renewable utilization. In addition, we consider an ambiguity set consisting of probability distributions that (i) match the empirical mean and empirical variance of each and (ii) is unimodal about , i.e.,

| (5) |

Unimodality about indicates that the probability density function of , if exists, is nondecreasing from to and is nonincreasing afterwards. In the literature, many probability distributions proposed for modeling the renewable energy forecast error are unimodal (see, e.g., [34, 35, 36]). It is worth mentioning that [16] consider the unimodality of the joint probability distribution of all . In contrast, the unimodality in is with respect to the marginal distribution of each , which is weaker than the joint unimodality assumed in [16] and easier to verify by the historical data. In addition, the ambiguity set leads to a polynomially solvable reformulation (see Section III).

We close this section by formulating the DR co-optimization (DRCO) model of power dispatch and DNE limits:

| (6a) | ||||

| s.t. | (6b) | |||

where represents the weight on the renewable utilization . The system operator can set based on her trade-off between the renewable utilization and the dispatch cost. If is close to zero then the dispatch cost and the renewable utilization are low. As increases, both dispatch cost and renewable utilization increase. By gradually increasing the value of and re-solving model (6a)–(6b), we obtain a cost-utilization frontier that can clearly indicate the trade-off between these two performance measures (see Section V for related case studies).

III Solution Methodology

We recast the DRCO model (6a)–(6b) as a second-order conic program that is polynomially solvable. For notation brevity, we derive based on abstract notation. First, we represent constraints (2a)–(2f) in the following abstract form:

| (7a) | |||

| (7b) | |||

| where denotes the power re-dispatch variables, matrices , , and denote the given parameters in constraints (2a)–(2e), and matrix and vector denote the variables in the ADR (2f). Letting , we represent the hypercube as , where denotes the vector of all ones. Then, we recast (7a)–(7b) as | |||

| (7c) | |||

| We claim that (7c) is equivalent to | |||

| (7d) | |||

| We now prove the equivalence . One the one hand, suppose that there exist and such that (7c) holds valid. Then, we let and to yield for all . Hence, (7c) implies (7d). On the other hand, suppose that there exist and such that (7d) holds valid. Then, we let and to yield for all . Hence, (7d) also implies (7c). Furthermore, we note that constraint (7d) holds valid if and only if , where the supremum operator is applied on each component of . Using the standard technique in robust optimization (see, e.g., [37]), we recast this constraint, and so constraints (2a)–(2f), as the following linear inequalities: | |||

| (7e) | |||

| (7f) | |||

Second, we recast the adjustable DR joint chance constraint (4a) as second-order conic constraints. We present this result in the following theorem and its proof in Appendix A.

Theorem 1

If , then, for all , chance constraint (4a) is equivalent to the following constraints:

| (8a) | |||

| (8b) | |||

| (8c) | |||

| (8d) | |||

| (8e) | |||

| (8f) | |||

IV Extension to Alternative Operational Risks

We extend the DRCO model (6a)–(6b) by considering alternative operational risks of the chance constraint (4a), which computes the expected costs incurred by overestimating/underestimating the renewable energy. We note that such operational risks are studied in [20]. In this paper, we study the DR counterpart of the risks based on the ambiguity set defined in (5). Specifically, the DR expected cost of overestimation/underestimation are defined as

where for . When , emergency regulations (e.g., renewable generation curtailment, fast-starting units, and load shedding) may be needed to recover the operational feasibility. Accordingly, the cost coefficients and should be estimated based on the corresponding regulations (e.g., the opportunity/penalty cost of curtailing renewable generation, the estimated real-time price of using fast-starting units, and the penalty cost of shedding load). Then, the DRCO model (6a)–(6b) can be extended by incorporating as follows:

| s.t. |

where and represent the weights on the expected costs of overestimation/underestimation, respectively.

We compute and by solving conic programs. We present this result in the following theorem and its proof in Appendix B. Accordingly, the extended DRCO model presented above can be recast as a conic program that can be efficiently solved by commercial solvers.

Theorem 2

Let represent the optimal value of the following conic program:

| (10a) | ||||

| s.t. | (10b) | |||

| (10c) | ||||

| (10d) | ||||

| (10e) | ||||

| (10f) | ||||

where represents the cone of all positive semidefinite matrices. Then, we have

Furthermore, can be conservatively approximated by piecewise linear functions of with arbitrary precision.

V Case Studies

We carry out numerical case studies on modified IEEE 14-bus and IEEE 118-bus systems. All programs are developed using MATLAB2014a and solved by MOSEK via YAlMIP 11.5 on a laptop with a 2.7GHz Intel Core i5 CPU and 8GB RAM.

V-A The Modified IEEE 14-bus System

In this system, there are 20 transmission lines and 5 generators (G1–G5) providing corrective power re-dispatch. The generators and network characteristics can be found in MATPOWER [38]. Two wind power farms with 80 MW (W1) and 100MW (W2) installed capacity are connected to the system at nodes 5 and 7, respectively. The load profile is from [19] and scaled by a factor of 0.1. We set , , , and for all .

V-B The Cost-Utilization Frontier and the DNE Limits

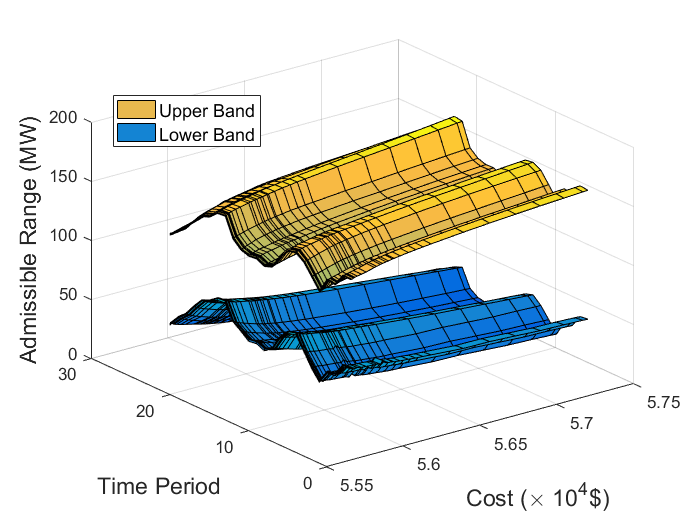

To demonstrate the trade-off between the dispatch cost and the utilization of renewable energy, we generate a cost-utilization frontier by gradually increasing the value of and re-solving the DRCO model (6a)–(6b) for each . To this end, we first obtain the wind power forecast of W1 and W2 from the NREL Eastern Wind Dataset [39]. We generate a set of wind power prediction error data by using Gaussian distribution, whose mean is set to be for all and variance increases from 10% of the installed capacity by 0.1% as increases from to . Second, we divide the data into two parts. We use the first part to calibrate the ambiguity set based on the empirical mean and variance. Then, for fixed , we solve the DRCO model to obtain the optimal DNE limits and the minimum power dispatch cost. We use the second part of the data to obtain an out-of-sample empirical estimate of the renewable utilization probability . Third, we repeat the second step by gradually increasing the value of from to . We set the step length as 100 when , when , when , and when . Accordingly, we obtain 33 groups of minimum power dispatch costs, optimal DNE limits, and the corresponding renewable utilization probabilities.

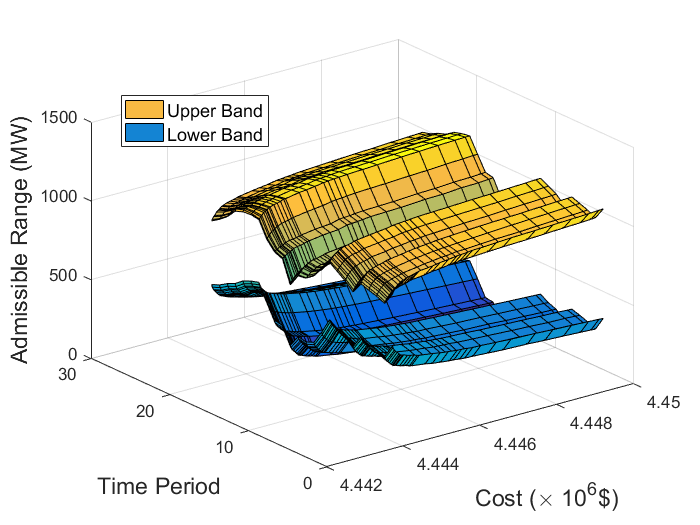

In Fig. 1, we display the minimum power dispatch cost and the optimal DNE limits under various values. For intuitive presentation, we shift the DNE limits to obtain the admissible ranges of wind power . The interpretation of each pair of points and is that, during time period , we need to spend at least on power dispatch in order to accommodate any total wind power output within the interval . From Fig. 1, we observe that the admissible range of wind power broadens as the minimum dispatch cost increases. This indicates that the power system can become more flexible as we invest more on power dispatch.

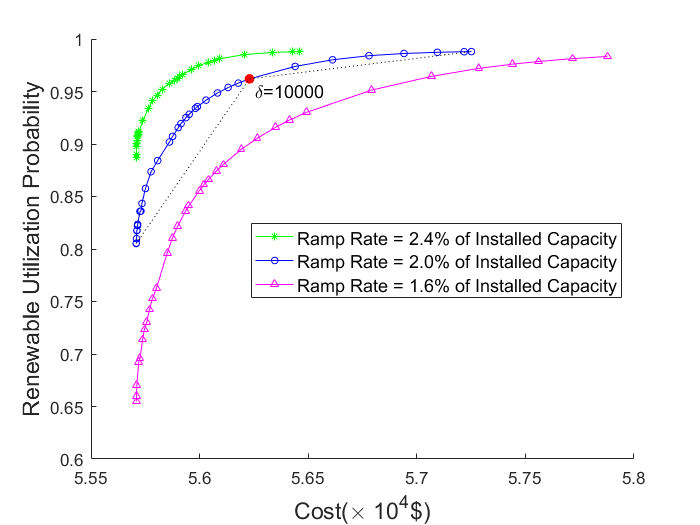

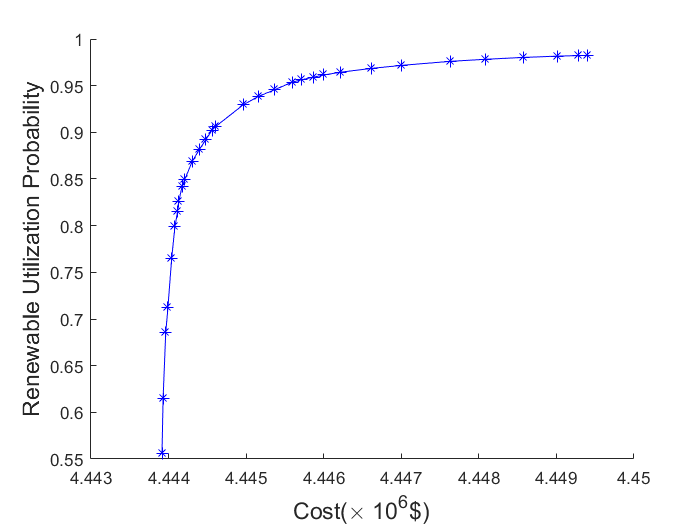

To take a closer look on the trade-off between the dispatch cost and the renewable utilization, we display the cost-utilization frontiers under various ramping capabilities in Fig. 2. Specifically, we consider three ramping capabilities in which and equal 1.6%, 2.0%, and 2.4% of for all , respectively. For each capability and for each value, we depict the minimum power dispatch cost versus the smallest renewable utilization probability in all time periods. From Fig. 2, we first observe that the renewable utilization increases as the dispatch cost increases, confirming our observation from Fig. 1. Second, the increasing trend of renewable utilization diminishes as the dispatch cost increases. Take the middle curve with 2% ramping capability for example. On this curve, we highlight two segments with and , respectively. The first segment reflects a 19.5% increase in renewable utilization with only an 0.9% increase in the power dispatch cost (i.e., increasing by $521). This translates into a 0.037%/$ increasing rate of the renewable utilization. On the contrary, the second segment reflects a 2.7% increase in renewable utilization with a 1.8% increase in the power dispatch cost (i.e., increasing by $1021). This translates into a 0.003%/$ increasing rate of the renewable utilization. This observation indicates that a small additional investment on power dispatch can quickly enhance the renewable utilization, but this investment becomes less efficient when the utilization is already high. Third, we observe from Fig. 2 that the frontier rises as the ramping capability increases. For example, to achieve a 95% renewable utilization, it costs when the ramping capability is 1.6%, when the ramping capability is 2.0%, and when the ramping capability is 2.4%. This observation indicates that a small enhancement on the ramping capability can significantly improve the cost-effectiveness of utilizing renewable energy.

V-C Comparisons with the Original DNE Limit Approach

We compare the proposed DRCO model (termed the IDNE approach) with the original DNE approach (termed ODNE) in [6], which computes the DNE limits based on a given dispatch strategy without explicitly modeling the renewable ambiguity. We randomly generate 5,000 out-of-sample scenarios of wind prediction errors from the hypothetical Gaussian distribution and compare (i) the optimal DNE limits, (ii) the renewable utilization probability, and (iii) the actual cost incurred in each scenario. The actual cost consists of the pre-dispatch cost, the corrective re-dispatch cost, and the penalty costs which are incurred (a) when , the load shedding takes place at a cost of 2,000$/MW and (b) when , the renewable energy is curtailed at a cost of 100$/MW. In all comparisons, we set and for all .

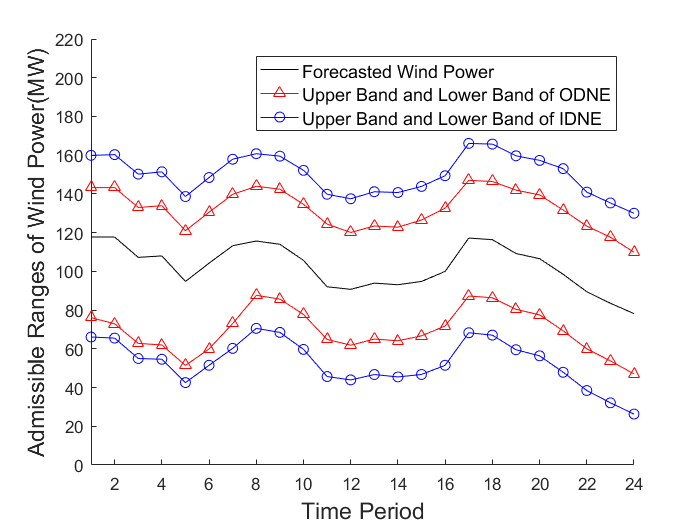

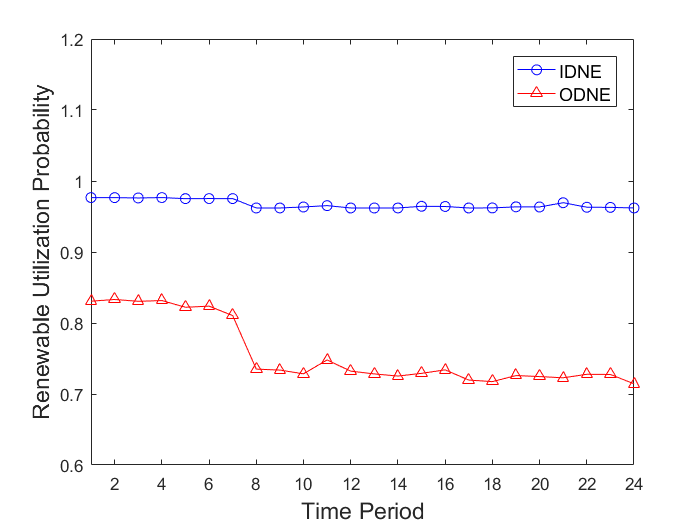

First, we compare the admissible ranges of wind power and the corresponding out-of-sample renewable utilization probabilities in Fig. 3. From this figure, we observe that the proposed IDNE approach yields wider admissible ranges, and so higher renewable utilization, than ODNE does. For example, IDNE can consistently accommodates more than 95% of the wind power throughout the 24 time periods, while ODNE accommodates less than 90% and shows a decreasing trend in renewable utilization as increases.

| Approach | AvgC ($) | MaxC ($) | AvgLS (MW) | AvgWC (MW) |

|---|---|---|---|---|

| IDNE | 56,004 | 98,333 | 0.0349 | 0.0276 |

| ODNE | 57,030 | 127,277 | 0.5686 | 0.2389 |

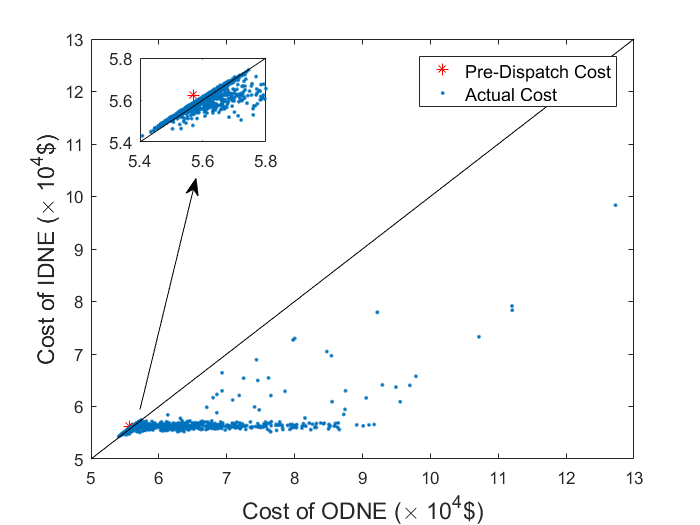

Second, we compare the actual cost in Fig. 4 and Table I. In Fig. 4, we plot the IDNE actual cost versus the ODNE actual cost for all 5,000 scenarios and the 45-degree reference line represents that the two costs agree. From this figure, we observe that most points distribute around or below the reference line, indicating that IDNE is likely to outperform ODNE in out-of-sample tests. In addition, most points line up along the horizontal line of , i.e., the IDNE pre-dispatch cost. This indicates that the IDNE yields stable actual costs with small variations. That is, the proposed DR approach provide stable and predictable out-of-sample performance. In Table I, we report the average actual cost (AvgC), the maximum actual cost (MaxC), the average load shedding (AvgLS), and the average wind curtailment (AvgWC) among the 5,000 scenarios. This table confirms the observations on the actual cost from Fig. 4, and further demonstrates that IDNE incurs one order of magnitude less load shedding as well as wind curtailment than ODNE does.

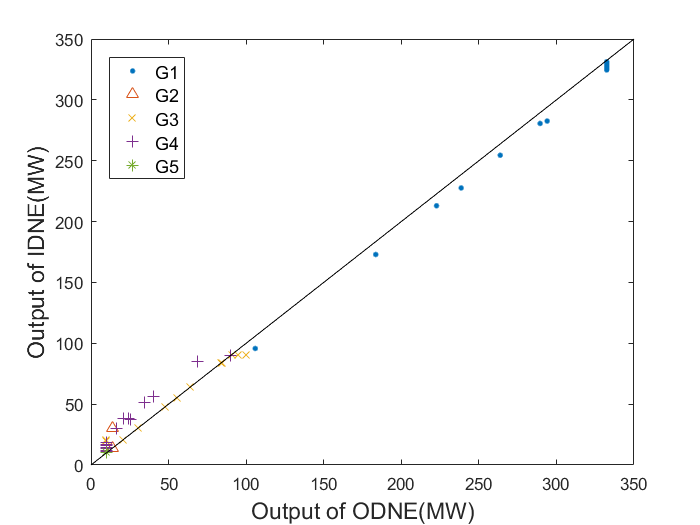

Third, we compare the optimal pre-dispatch strategies of IDNE and ODNE in Fig. 5, from which we observe that the pre-dispatch generation amounts of G1 and G3 under IDNE are lower than those under ODNE in most time periods. This strategy enhances the system flexibility under IDNE by preserving more ramping capability, especially when the load is high. Take the time period for example, in which the load is high and G1, G3 under ODNE reach their maximum generation capacities. In this case, the upward ramping capability of ODNE becomes scarce. On the contrary, IDNE sets a lower pre-dispatch generation amounts of G1 and G3, and so preserves more (upward) ramping capability. This demonstrates how the power dispatch and DNE limits can coordinate in the proposed DRCO model to enhance the system flexibility. Finally, it takes 30.80 CPU seconds on average and 33.42 CPU seconds at maximum to solve the DRCO model with various values of , which verifies the tractability of the proposed approach.

V-D The Modified IEEE 118-bus System

In the modified IEEE 118-bus system, there are 186 transmission lines and 54 generators providing corrective re-dispatch. Three wind farms with an identical 300 MW installed capacity are connected to the system at nodes 18, 32, and 88, respectively. The generator and network characteristics are from MATPOWER 5.1 [38] and the load profile is the same as in [19]. In addition, the wind forecasts are from the NREL Eastern Wind Dataset [39] and the mean and variance of the wind power prediction error are set as in the previous case study. We display the minimum power dispatch cost and the optimal DNE limits under various values in Fig. 6 and the cost-utilization frontier in Fig. 7. We make similar observations from these two figures on the trade-off between the power dispatch cost and the renewable utilization. Finally, it takes 296.38 CPU seconds on average and 307.51 CPU seconds at maximum to solve the DRCO model with various values of , which verifies the scalability of the proposed approach.

VI Conclusion and Future Research

We propose a DRCO model for power dispatch and DNE limits. Our model incorporates an adjustable DR joint chance constraint to explicitly measure the utilization of renewable energy. By using ADR, we derive a second order conic program that conservatively approximates the DRCO model. The case studies based on modified IEEE 14-bus and 118-bus systems demonstrate the effectiveness and computational tractability of the proposed approach. Future research includes alternative ambiguity sets and the corresponding DRCO models.

Appendix A Proof of Theorem 1

First, we observe that ambiguity set satisfies Assumption (A1) in [40]. Hence, by Theorem 3 in [40], the chance constraint (4a) is equivalent to its Bonferroni approximation:

| (11a) | |||

| (11b) | |||

| (11c) | |||

| where represents the (marginal) probability distribution of each and . | |||

Appendix B Proof of Theorem 2

First, for given , we compute the worst-case expectation with . To this end, by the unimodality of , there exists a random variable such that , where is uniform on and independent of (see [43]). It follows that , , and , where

We compute by formulating the following optimization problem:

| (12a) | ||||

| s.t. | (12b) | |||

| (12c) | ||||

| (12d) | ||||

| whose dual formulation is | ||||

| (12e) | ||||

| s.t. | (12f) | |||

| (12g) | ||||

| where dual variables , , and are associated with primal constraints (12b)–(12d), respectively. Dual constraint (12f) is equivalent to , which is further equivalent to | ||||

| (12h) | ||||

| In addition, dual constraint (12g) is equivalent to for all , which is further equivalent to | ||||

| (12i) | ||||

| (12j) | ||||

| (12k) | ||||

| by Proposition 3.1(b) in [44]. It follows that equals the optimal value of the following conic program: | ||||

| (12l) | ||||

| s.t. | (12m) | |||

Second, we have because is separable over indices and . But

because random variable has mean , variance , and is unimodal about . Hence,

Similarly, .

Third, is convex in because appears in the right-hand side of the formulation (12l)–(12m) with a minimization objective function that defines . It follows that admits a conservative piecewise linear approximation (CPLA, see Fig. 8). Specifically, suppose that is defined on the interval . Then, letting for and , we have , where

Hence, can be conservatively approximated by . Additionally, by construction, it is clear that . For all and , we have and by constraint (3). It follows that can be conservatively approximated by , where , , for all , and

Similarly, can be conservatively approximated by , where , , for all , and

Finally, we note that the values of can be efficiently obtained by solving the conic program (12l)–(12m) by setting . Hence, we can incorporate the conservative approximations of into the DRCO model by using a set of linear constraints.

References

- [1] L. Wu, M. Shahidehpour, and T. Li, “Stochastic security-constrained unit commitment,” IEEE Transactions on Power Systems, vol. 22, no. 2, pp. 800–811, 2007.

- [2] A. Papavasiliou, S. S. Oren, and R. P. O’Neill, “Reserve requirements for wind power integration: A scenario-based stochastic programming framework,” IEEE Transactions on Power Systems, vol. 26, no. 4, pp. 2197–2206, 2011.

- [3] Q. Wang, Y. Guan, and J. Wang, “A chance-constrained two-stage stochastic program for unit commitment with uncertain wind power output,” IEEE Transactions on Power Systems, vol. 27, no. 1, pp. 206–215, 2012.

- [4] R. Jiang, J. Wang, and Y. Guan, “Robust unit commitment with wind power and pumped storage hydro,” IEEE Transactions on Power Systems, vol. 27, no. 2, pp. 800–810, 2012.

- [5] D. Bertsimas, E. Litvinov, X. A. Sun, J. Zhao, and T. Zheng, “Adaptive robust optimization for the security constrained unit commitment problem,” IEEE Transactions on Power Systems, vol. 28, no. 1, pp. 52–63, 2013.

- [6] J. Zhao, T. Zheng, and E. Litvinov, “Variable resource dispatch through do-not-exceed limit,” IEEE Transactions on Power Systems, vol. 30, no. 2, pp. 820–828, 2015.

- [7] W. Wei, F. Liu, and S. Mei, “Dispatchable region of the variable wind generation,” IEEE Transactions on Power Systems, vol. 30, no. 5, pp. 2755–2765, 2015.

- [8] C. Shao, X. Wang, M. Shahidehpour, X. Wang, and B. Wang, “Security-constrained unit commitment with flexible uncertainty set for variable wind power,” IEEE Transactions on Sustainable Energy, vol. 8, no. 3, pp. 1237–1246, 2017.

- [9] S. Zymler, D. Kuhn, and B. Rustem, “Distributionally robust joint chance constraints with second-order moment information,” Mathematical Programming, vol. 137, no. 1-2, pp. 167–198, 2013.

- [10] W. Wiesemann, D. Kuhn, and M. Sim, “Distributionally robust convex optimization,” Operations Research, vol. 62, no. 6, pp. 1358–1376, 2014.

- [11] R. Jiang and Y. Guan, “Data-driven chance constrained stochastic program,” Mathematical Programming, vol. 158, no. 1-2, pp. 291–327, 2016.

- [12] J. Zhao, T. Zheng, and E. Litvinov, “A unified framework for defining and measuring flexibility in power system,” IEEE Transactions on Power Systems, vol. 31, no. 1, pp. 339–347, 2016.

- [13] W. Wei, F. Liu, and S. Mei, “Real-time dispatchability of bulk power systems with volatile renewable generations,” IEEE Transactions on Sustainable Energy, vol. 6, no. 3, pp. 738–747, 2015.

- [14] Z. Li, W. Wu, B. Zhang, and B. Wang, “Robust look-ahead power dispatch with adjustable conservativeness accommodating significant wind power integration,” IEEE Transactions on Sustainable Energy, vol. 6, no. 3, pp. 781–790, 2015.

- [15] ——, “Adjustable robust real-time power dispatch with large-scale wind power integration,” IEEE Transactions on Sustainable Energy, vol. 6, no. 2, pp. 357–368, 2015.

- [16] W. Wei, J. Wang, and S. Mei, “Dispatchability maximization for co-optimized energy and reserve dispatch with explicit reliability guarantee,” IEEE Transactions on Power Systems, vol. 31, no. 4, pp. 3276–3288, 2016.

- [17] C. Shao, X. Wang, M. Shahidehpour, X. Wang, and B. Wang, “Power system economic dispatch considering steady-state secure region for wind power,” IEEE Transactions on Sustainable Energy, vol. 8, no. 1, pp. 268–278, 2017.

- [18] B. Zeng and L. Zhao, “Solving two-stage robust optimization problems using a column-and-constraint generation method,” Operations Research Letters, vol. 41, no. 5, pp. 457–461, 2013.

- [19] C. Wang, F. Liu, J. Wang, F. Qiu, W. Wei, S. Mei, and S. Lei, “Robust risk-constrained unit commitment with large-scale wind generation: An adjustable uncertainty set approach,” IEEE Transactions on Power Systems, vol. 32, no. 1, pp. 723–733, 2017.

- [20] C. Wang, F. Liu, J. Wang, W. Wei, and S. Mei, “Risk-based admissibility assessment of wind generation integrated into a bulk power system,” IEEE Transactions on Sustainable Energy, vol. 7, no. 1, pp. 325–336, 2016.

- [21] F. Qiu, Z. Li, and J. Wang, “A data-driven approach to improve wind dispatchability,” IEEE Transactions on Power Systems, vol. 32, no. 1, pp. 421–429, 2017.

- [22] Z. Li, F. Qiu, and J. Wang, “Multi-period do-not-exceed limit for variable renewable generation dispatch considering discrete recourse controls,” arXiv preprint arXiv:1608.05273, 2016.

- [23] A. S. Korad and K. W. Hedman, “Zonal do-not-exceed limits with robust corrective topology control,” Electric Power Systems Research, vol. 129, pp. 235–242, 2015.

- [24] P. Xiong, P. Jirutitijaroen, and C. Singh, “A distributionally robust optimization model for unit commitment considering uncertain wind power generation,” IEEE Transactions on Power Systems, vol. 32, no. 1, pp. 39–49, 2017.

- [25] Y. Zhang, S. Shen, and J. L. Mathieu, “Distributionally robust chance-constrained optimal power flow with uncertain renewables and uncertain reserves provided by loads,” IEEE Transactions on Power Systems, vol. 32, no. 2, pp. 1378–1388, 2017.

- [26] W. Xie and S. Ahmed, “Distributionally robust chance constrained optimal power flow with renewables: A conic reformulation,” IEEE Transactions on Power Systems, vol. 33, no. 2, pp. 1860–1867, 2018.

- [27] C. Zhao and R. Jiang, “Distributionally robust contingency-constrained unit commitment,” IEEE Transactions on Power Systems, vol. 33, no. 1, pp. 94–102, 2018.

- [28] P. M. Esfahani and D. Kuhn, “Data-driven distributionally robust optimization using the wasserstein metric: Performance guarantees and tractable reformulations,” Mathematical Programming, Forthcoming, 2017.

- [29] C. Wang, R. Gao, F. Qiu, J. Wang, and L. Xin, “Risk-based distributionally robust optimal power flow with dynamic line rating,” arXiv preprint arXiv:1712.08015, 2017.

- [30] Y. Chen, Q. Guo, H. Sun, Z. Li, W. Wu, and Z. Li, “A distributionally robust optimization model for unit commitment based on kullback-leibler divergence,” IEEE Transactions on Power Systems, Forthcoming, 2018.

- [31] B. Li, R. Jiang, and J. L. Mathieu, “Distributionally robust risk-constrained optimal power flow using moment and unimodality information,” in Decision and Control (CDC), 2016 IEEE 55th Conference on. IEEE, 2016, pp. 2425–2430.

- [32] ——, “Ambiguous risk constraints with moment and unimodality information,” Mathematical Programming, pp. 1–42, 2017.

- [33] S. Fink, C. Mudd, K. Porter, and B. Morgenstern, “Wind energy curtailment case studies,” National Renewable Energy Laboratory Report, Tech. Rep., 2009, available at http://www.nrel.gov/docs/fy10osti/46716.pdf.

- [34] R. Doherty and M. O’malley, “A new approach to quantify reserve demand in systems with significant installed wind capacity,” IEEE Transactions on Power Systems, vol. 20, no. 2, pp. 587–595, 2005.

- [35] J. Wang, M. Shahidehpour, and Z. Li, “Security-constrained unit commitment with volatile wind power generation,” IEEE Transactions on Power Systems, vol. 23, no. 3, pp. 1319–1327, 2008.

- [36] B.-M. Hodge, D. Lew, M. Milligan, H. Holttinen, S. Sillanpää, E. Gómez-Lázaro, R. Scharff, L. Söder, X. G. Larsén, G. Giebel, D. Flynn, and J. Dobschinski, “Wind power forecasting error distributions: An international comparison,” in 11th Annual International Workshop on Large-Scale Integration of Wind Power into Power Systems as well as on Transmission Networks for Offshore Wind Power Plants Conference, 2012.

- [37] A. L. Soyster, “Convex programming with set-inclusive constraints and applications to inexact linear programming,” Operations Research, vol. 21, no. 5, pp. 1154–1157, 1973.

- [38] R. D. Zimmerman, C. E. Murillo-Sánchez, and R. J. Thomas, “Matpower: Steady-state operations, planning, and analysis tools for power systems research and education,” IEEE Transactions on power systems, vol. 26, no. 1, pp. 12–19, 2011.

- [39] “NREL Eastern Wind Dataset,” https://www.nrel.gov/grid/eastern-wind-data.html, accessed: 2018-07-30.

- [40] W. Xie, S. Ahmed, and R. Jiang, “Optimized bonferroni approximations of distributionally robust joint chance constraints,” Available at Optimization Online, 2017.

- [41] C.-F. Gauss, Theoria combinationis observationum erroribus minimis obnoxiae. Henricus Dieterich, 1823, vol. 1.

- [42] A. Ben-Tal and A. Nemirovski, Lectures on modern convex optimization: analysis, algorithms, and engineering applications. SIAM, 2001, vol. 2.

- [43] S. Dharmadhikari and K. Joag-Dev, Unimodality, Convexity, and Applications. Elsevier, 1988.

- [44] D. Bertsimas and I. Popescu, “Optimal inequalities in probability theory: A convex optimization approach,” SIAM Journal on Optimization, vol. 15, no. 3, pp. 780–804, 2005.