Asymmetric linkages: maxmin vs. reflected maxmin copulas

Damjana Kokol Bukovšek

Damjana Kokol Bukovšek, School of Economics and Business, University of Ljubljana, and Institute of Mathematics, Physics and Mechanics, Ljubljana, Slovenia

damjana.kokol.bukovsek@ef.uni-lj.si, Tomaž Košir

Tomaž Košir, Faculty of Mathematics and Physics, University of Ljubljana, and Institute of Mathematics, Physics and Mechanics, Ljubljana, Slovenia

tomaz.kosir@fmf.uni-lj.si, Blaž Mojškerc

Blaž Mojškerc, School of Economics and Business, University of Ljubljana, and Institute of Mathematics, Physics and Mechanics, Ljubljana, Slovenia

blaz.mojskerc@ef.uni-lj.si and Matjaž Omladič

Matjaž Omladič, Institute of Mathematics, Physics and Mechanics, Ljubljana, Slovenia

matjaz@omladic.net

Abstract.

In this paper we introduce some new copulas emerging from shock models. It was shown in [21] that reflected maxmin copulas (RMM for short) are not just some specific singular copulas; they contain many important absolutely continuous copulas including the negative quadrant dependent “half” of the Eyraud-Farlie-Gumbel-Morgenstern class. The main goal of this paper is to develop the RMM copulas with dependent endogenous shocks and give evidence that RMM copulas may exhibit some characteristics better than the original maxmin copulas (MM for short): (1) An important evidence for that is the iteration procedure of the RMM transformation which we prove to be always convergent and we give many properties of it that are useful in applications. (2) Using this result we find also the limit of the iteration procedure of the MM transformation thus answering a question proposed in [10]. (3) We give the multivariate dependent RMM copula that compares to the MM version given in [10]. In all our copulas the idiosyncratic and systemic shocks are combined via asymmetric linking functions as opposed to Marshall copulas where symmetric linking functions are used.

Key words and phrases:

Copula; dependence concepts; maxmin copulas; transformations of distribution functions; PQD property; survival analysis; shock models

2010 Mathematics Subject Classification:

Primary: 60E05; Secondary: 60E15, 62N05

DKB&TK&BM&MO acknowledge financial support from the Slovenian Research Agency (research core funding No. P1-0222).

1. Introduction

Dependence concepts play a crucial role in multivariate statistical literature since it was recognized that the independence assumption cannot describe conveniently the behavior of a stochastic system. One of the main tools have eventually become copulas due to their theoretical omnipotence emerging from the Sklar’s theorem [30]. There has been a vast literature on the subject including [14, 19, 16, 17, 18]; for an excellent overview of these methods and the properties of copulas see [27] and a more recent monograph [11]. For an overview of probability background, see for instance [13].

In this paper we devote our study to the copulas emerging from shock models which are playing an important role in applications (cf. [15, 26, 22] and many more). This theory starts with Marshall and Olkin [24], although it is Marshall [23] who really introduces copulas into the picture of shock models. We believe that the third milestone on this path was set by Durante, Girard, and Mazo [6], cf. also more generally [2]. The paper [6] may have encouraged a vivid interest in the area [3, 26, 28, 10, 15, 21]. We want to point out the paper [28] where an asymmetric version of Marshall copulas was introduced, called maxmin copulas. The dependent version of these copulas together with the multivariate version were introduced in [10], while [21] brings into the picture the notion of reflected maxmin copulas, RMM for short; it is also shown there that these copulas are always bounded above by the product copula which means in particular that they are negatively quadrant dependent.

These views bring RMM copulas into the spotlight of some previously studied approaches and widen the range of their applications. The copulas of this type appeared in [7, Proposition 3.2]. Moreover, these copulas may be viewed as perturbations of the product copula . General perturbations of copulas were studied in [4] and [25], where a subclass of what we call reflected maxmin copulas were considered (cf. [25, §3]). The RMM copulas can also be related to the results presented in [9, Theorem 7.1] with the maximum replaced by the minimum; we believe that this similarity is more than just coincidental. The copulas introduced in [29] are not only very close to our RMM copulas, as it was said in [21], it turns out in our Example 3(a) that they basically belong to MM copulas. Let us also point out that the maxmin (and consequently reflected maxmin) copulas have some properties that are appealing in various contexts related to the fuzzy set theory and the multicriteria decision making. The class includes nonsymmetric copulas that are used, for instance, as more general fuzzy connectives [1, 8].

As an example consider two endogenous shocks and of a system, and one exogenous shock . Let the dependence of be governed by a copula , while is independent of it. The distribution of

as we know, is given by one of the two forms of the Marshall copula [23], while the other one is obtained from this one by replacing both linking functions with the linking functions . The point is that the systemic shock has either an effect on both components coherent with the two idiosyncratic shocks, or it is conflictive with the two shocks.

On the other hand, if we take asymmetric linking functions (terminology introduced in [6]) and , we get the maxmin copula as introduced in [28]. This may be viewed as if the shock has opposite effects on the two components and . So, it has a beneficial effect on one component (as seen through the linking function max) and detrimental effect on the other one (as seen through the linking function min), so that

We may think of and as r.v.’s representing the respective wealth of two groups of people, and the exogenous shock is interpreted as an event that is beneficial to one of the groups and detrimental to the other one. Analogously, and can be thought of as a short and a long investment, respectively, while is beneficial only to one of these types of investment. However, following [21] we argue that in this case there is a conceptual reason to replace one of the distribution functions corresponding to idiosyncratic shocks with the corresponding survival function. This way we get again the situation in which the systemic shock works in the same (or the opposite) direction as the idiosyncratic shock, but on both components in the same way.

The first among the important new results of this paper is the construction of the dependent version of the reflected maxmin copulas (RMM for short); the bivariate case is derived in Section 2, cf. especially Formula (4), the multivariate extension of these copulas in Section 6, cf. Theorem 14; the multivariate form of the original maxmin copulas was given in [10]. At the end of Section 2 we slightly extend the result of [21] by showing that every copula of Eyraud-Farlie-Gumbel-Morgenstern class belongs to either the MM or the RMM class (cf. Example 3(b)) and these are clearly only a very specific subclass of the MM and RMM copulas. There is some evidence for the claim that RMM copulas are conceptually a better and more natural approach to study MM copulas. An important result in this direction is the iteration procedure of the RMM transformation which we prove to be always convergent and give many properties of it that are useful in applications. Our main result in this direction is Theorem 8 which presents the limit copula depending on the starting copula (governing the dependence of the idiosyncratic shocks), and the two functions and (“generators” of the one step reflected maxmin transformation) together with the many dependence properties of the so constructed models presented in Section 4. Even more importantly, perhaps, we give as a consequence of these results the limit of the maxmin transformation in Theorem 10 thus answering the question proposed in [10].

In Section 2 we give an overview of the results on reflected maxmin copulas, extend them to the dependent case, give some properties and define the iterative RMM transformation. In Section 3 we actually perform the iteration procedure and prove that it is always convergent. This enables us to study in Section 4 how dependence properties are (dis)inherited when this transformation is applied to a copula. The multivariate case of an RMM copula is first given for 3-variate case for the benefit of the reader in Section 5 and finally for the general case in Section 6.

2. Reflected maxmin copulas for dependent shocks

In this section we introduce a dependent version of the bivariate reflected maxmin copulas presented in [21]. We start with two idiosyncratic shocks and and one systemic shock . We are seeking for the distribution of

Furthermore, we assume that the exogenous shock , having d.f. , is independent of endogenous shocks , while the joint d.f. of this vector can be expressed as , where is a given copula. The authors of [10], where a dependent version of maxmin copulas is presented, introduce functions that help express the dependence of via a maxmin copula (let us point out that notation we are using here is slightly different from the notation in [10])

(1)

Here we recall the sets of functions given in [10] that contain the generating functions and the corresponding auxiliary functions : (1) is the class of nondecreasing functions such that and the function is nondecreasing on ; and (2) is the class of nondecreasing functions such that and the function

is nondecreasing.

We want to develop the reflected maxmin copula from (1) using the ideas and notation of [21]. First we replace by the copula obtained from by one flip in the second variable. Following [21] we denote the so obtained copula by :

to get

By performing the flip on the result of this transformation we obtain

(2)

The authors of [10] were studying transformation (in our notation) and how the properties of copula are inherited when this transformation is applied to it. Our aim is to do that for transformation . Following [21] we replace the “generating functions” of the maxmin copula with the “generating functions” of the reflected maxmin copula and introduce the auxiliary functions :

This is our extension to the dependent case of the formula [21, (3)]. As a test, if we put into this formula , we first get , so that (4) is transformed to [21, (3)] back.

It turns out that the generating and auxiliary functions given in (3) satisfy conditions introduced in [21]

(G1):

, , ,

(G2):

the functions and are nondecreasing on .

(G3):

the functions and are nonincreasing on .

Actually, it was shown in [21, Lemma 1] and [21, Lemma 2] that these conditions are equivalent to the starting conditions (F1)–(F3) on functions studied in [28, 10].

Proposition 1.

If is an arbitrary copula, and and satisfy conditions (G1), (G2), and (G3), then defined by (4) is a copula.

Proof.

This follows immediately from [10, Theorem 2.7] by considerations above after taking into account the fact that flipping of one of the variables sends copula to a copula.

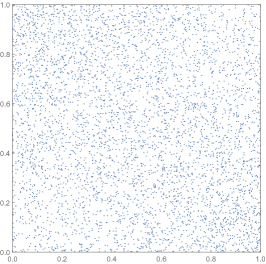

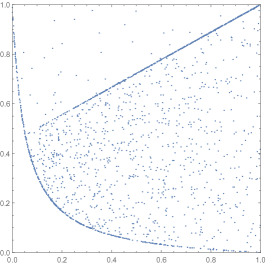

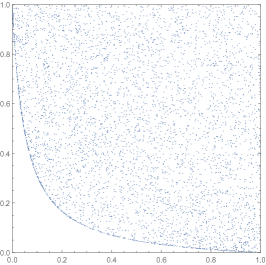

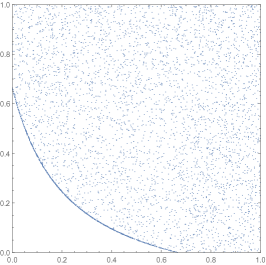

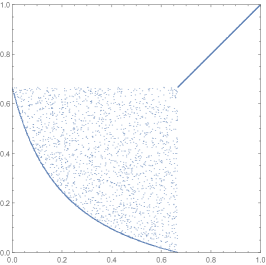

We present in Figure 1 the scatterplots of the copulas obtained when transformation is applied to three typical examples of copulas, , and in place of . The choice of generating functions in this example is and . Further remarks on Figure 1 will be given after Proposition 2.

Comment. All scatterplots in the paper are drawn using Mathematica software [31]. In the bivariate case we use the exact expressions for copulas and an algorithm to generate samples from a given copula presented in [27, Chapter 2.9], i.e. (i) generate two independent uniform variates and ; (ii) set , where denotes a quasi-inverse of the derivative ; (iii) the sample item is .

Figure 1. Transformation on copulas , and , respectively

It has been observed that the formulas for reflected maxmin copulas [21, (2)&(3)] are conceptually clearer to the ones for maxmin copulas [21, (1)] (rewritten from [28, (2)]) in the case that the shocks are independent. We have now seen that the same is obviously true for the case of dependent shocks when we compare formula (4) to formula (1) (rewritten from [10, (2.3)]).

At this point we want to present the first one of the properties that is being inherited by the transformation . Here we use the abbreviation PQD (respectively NQD) for the property that a random vector (or copula ) is positively quadrant dependent (respectively negatively quadrant dependent); this means that (respectively ) for all . For further explanation of the properties PQD/NQD we refer the reader to [27, Chapter 5] and [11, p. 64].

An elaboration of [10, Theorem 3.1(i)] is clearly obtained using a combination of that result and the obvious fact that reflection is exchanging PQD copulas and NQD copulas.

Proposition 2.

Let be a PQD copula, or equivalently let be an NQD copula, then is an NQD copula.

Remark. We can illustrate this result via Figure 1. Copula is NQD, so that is PQD and Proposition 2 gives no information on quadrant dependence in this case. This is in agreement with the third image of Figure 1 on which it is difficult to find any regularity. On the other hand, copula is PQD, so that is NQD and the second image shows a regularity in agreement with the proposition.

We conclude this section with two simple examples which we believe may help us emphasize the importance of the RMM and MM copulas. The first one deals with copulas introduced in [29]

(5)

the second one with the famous Eyraud-Farlie-Gumbel-Morgenstern copulas (cf. [11, p. 26]), i.e. for

(6)

Example 3.

(a):

Let functions and satisfy conditions (G1), (G2) and (G3), and let functions and satisfy conditions of [29, Theorem 2.3]. Then copula , defined by (5) is a maxmin copula.

(b):

If , then EFGM copula is a maxmin copula, if , then EFGM copula is a reflected maxmin copula.

Proof.

Consider to get (a). Claim (b) follows since and satisfy conditions (G1), (G2), and (G3).

.

3. Iterating reflected maxmin copulas

In this section we iterate the transformation introduced in the previous section as the authors of [10] iterated transformation (in our notation), i.e., we define . A straightforward application of the mathematical induction principle yields

(7)

where . Since are nondecreasing on by [21, Lemma 1, (G2)], their value is no greater than their value at 1 which is equal to 1, and no smaller than their value at 0 which is equal to 0. So, it follows that the iterates are well-defined. Before we go into showing that all these sequences are convergent, we start by a simple observation based on Proposition 2.

Corollary 4.

If is a PQD copula, then is an NQD copula for all .

The sequences of functions are pointwise convergent. Additionally, if respectively is any of their limit values, then it satisfies the equation , respectively .

Proof.

We recall the fact that are nondecreasing on by [21, Lemma 1, (G2)] implying that all the iterates are monotone nondecreasing. A simple observation implies that so that this sequence is monotone for all ; and similarly for . Choose an arbitrary and let be the limit of . Then, is the limit of , so that ; and similarly for .

Remark. It is an interesting question whether and perhaps when the mapping is a contraction on a compact metric space of all copulas. It is easy to see that for any copulas we have that

where is a product of and . Each of these factors is no greater than 1, however it tends to 1 when and tend to 1. So, we have that which proves that this mapping is non-expansive. Since it is not possible to find a constant upper bound for it is not a contraction. We omit the details not to overlengthen the paper any further. It is somewhat surprising that we are nevertheless able to prove the convergence of the iterates of this map and in the case of Corollary 9 below even the existence of a unique fixed point to which the iterates converge independently of the starting point.

By [10, Proposition 2.2.(ii)] is equal to the identity function on the interval , as soon as we can find an such that . (Actually, it is useful to write down the fact written there in the original form: if for some , then is identically equal to zero on the interval .) Let us denote by the smallest number with this property. So, we have that for all and is the smallest number of the kind. Observe that is equivalent to saying that is identically equal to zero on , and is equivalent to saying that has no zero on . The number corresponds to the function in the same way. So, in particular for all and is the smallest number with this property. This helps us computing the limits of sequences :

Lemma 6.

The limits of the above sequences exist and are given by

We are now in position to compute the limit copula of the sequence given by (7). We divide the unit square into four rectangles with respect to the lines and , called suggestively the NW, NE, SW, SE corner of the square. We will show the convergence in passing while computing the limits corner by corner. In order to simplify the notation we write

Lemma 7.

(a):

For and we have

(b):

For and we have

(c):

For and we have

(d):

In the remaining case it holds that

where the product in the first case is always convergent.

Proof.

(a)

Since and , it remains to see that the product in (7) equals to 1. Indeed, , so that for all , while and consequently , and the same kind of considerations apply to . So, it follows that the product on the right hand side of (7) is identically equal to one. The proof of (b) and (c) is based on similar ideas.

(d) We first assume that . If , the first factor of the product in (7) is zero and the desired conclusion follows. If , we only need to show convergence of the product, the rest is obvious from (7). Now, the first factor, and consequently all of them, are strictly positive and strictly smaller than . So, the sequence of partial products is positive and decreasing and always converges. However, an infinite product is convergent only if in addition its limit is nonzero. In case that we use the Fréchet-Hoeffding lower bound for our copula to see that this is indeed so and the desired result follows. It remains to treat the general case of which we will reduce to the previous one. We will use a well-known fact that (C) a product converges if and only if the series converges. This proves, in particular, that the series

(8)

converges for by the above. Next, if , then the sequences respectively are nondecreasing and converging to respectively . So, given big enough we have for all . So, if we denote and we get

so that the series on the left hand side must be convergent because it is a residual series of a convergent series and . It follows that the series on the right hand side is convergent and consequently the product is convergent by (C).

It remains to treat the case that either or . If we choose and , we get easily . Now, these iterates are copulas and so is the limit, yielding that it is continuous. So, for close to and close to , we still have, say, . Since the limit is positive, the rest of the proof goes as above.

Theorem 8.

The limit of the sequence (7) always exists and is equal to on the NE corner, to

on the NW, respectively the SE corner; while on the SW corner it equals to either

if (in this case the product always converges), or zero if .

Proof.

The form of the limit on the NW, NE, respectively SE corners is given by Lemma 7(a), (b) respectively (c). To get the desired result on the SW corner, write the right-hand side of (7) as

and the theorem follows by Lemma 6 and Lemma 7(d).

Corollary 9.

Assume that . Then

for any copula .

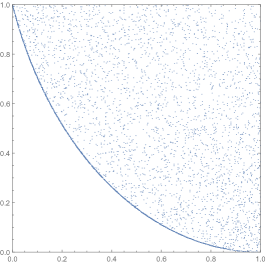

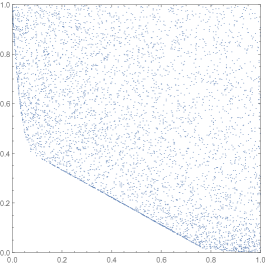

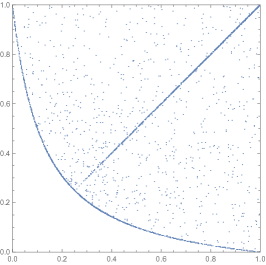

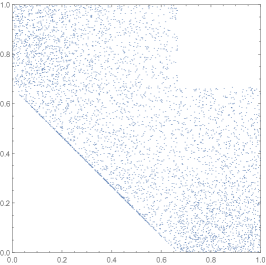

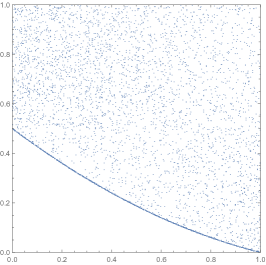

The scatterplots presented on Figure 2 are giving us some feeling of the convergence of the iteration we are studying in this section. Each image in the first row shows the scatterplot of the copula obtained when transformation is applied to a starting copula and the image below shows the one obtained when is applied to the same starting copula. The starting copulas are respectively , and . The choice of generating functions in all these examples are and . In all the cases the dots are scattered above a hyperbola. In the first column only the density of the dots varies with iteration. In the second column a singular line appeares that converges to the top of the square with iterations. In the third column a singular line appears that cuts out a piece of the area only on the plot of , while later the whole area above the hyperbola is dotted.

Figure 2. Transformation and on copulas , and , respectively.

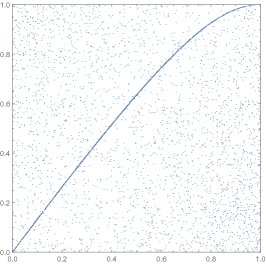

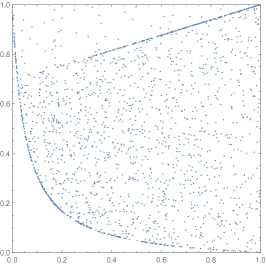

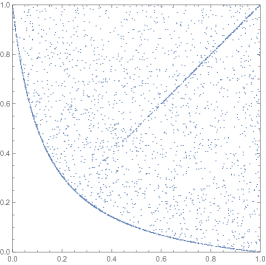

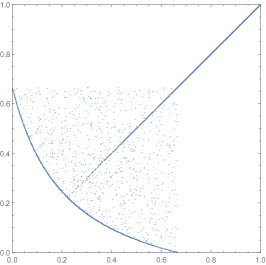

Figure 3. Various transformations on copulas , and as described in the text.

In Figure 3 we present some more interesting scatterplots. We give here the description of the images row by row going from the top to the bottom and within the row from the left to the right. Generating functions for the first three images are and , while the copula equals , and respectively , , . For the rest of the images the first generating function is and is as in the previous case. The first image in the second row corresponds to the copula and . For larger values of the image is very similar in this case. The next two images correspond to the case , and , respectively . The last two images correspond to , and , respectively .

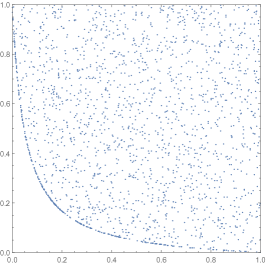

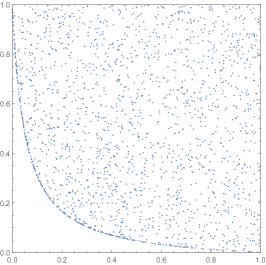

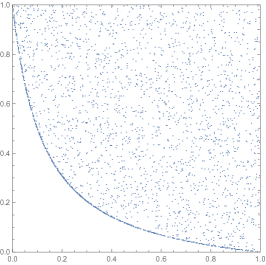

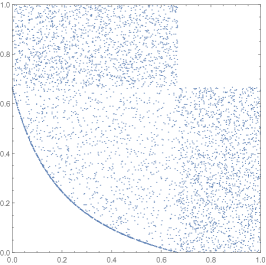

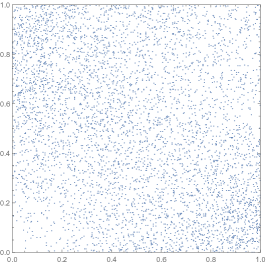

Figure 4. Evolution of the singular part.

On Figure 4 we consider evolution of the singular part for the example of an RMM copula given by , and . The resulting copulas for are shown on the first two scatterplots of Figure 4 and are clearly singular. When approaches infinity, the singularity is pushed to the lower edge of the square and in the limit it disappears. This is seen on the third scatterplot of this figure. The limiting copula is equal to as explained in Corollary 9.

Let us conclude this section by translating Theorem 8 in terms of maxmin copulas. The transformation is obtained from the transformation by applying the flip on either side of the transformation. Since the flip is an involutory operation (cf. [11, p. 33]), it follows inductively that the transformation is obtained from the transformation (here we adjust the notation of [10] in an obvious way) by applying the flip on both sides of the transformation. So, we can compute the formula for from the formula for by (a) applying the flip on both sides of and (b) replacing the generators and their auxiliary functions by the generators and their auxiliaries using relations (3). When replacing the iterates a simple inductive argument reveals

(9)

which implies

Here, is the smallest such that is equal to identity function on , and is the greatest such that is equal to identity function on (cf. [10, Proposition 2.2]). We divide again the square into four corners: The limit function in is equal to a constant for and to the identity otherwise; the limit function in is equal to the identity for and to a constant otherwise.

In order to transform equation (7), we need to replace functions using the functions introduced in [10, p. 156]. It is not hard to find the relation between and , and between and . We need formulas

so that

(10)

Using formulas (9) and (10) we can translate equation (7) into:

(11)

Theorem 10.

The limit of the sequence (11) always exists and equals

(a):

on the SE corner;

(b):

on the SW corner;

(c):

on the NE corner;

(d):

either

if (in this case the product always converges), or if , on the NW corner.

Proof.

Straightforward computation.

4. Inheritance of dependence properties via reflected maxmin transformation

Using Theorem 8 we upgrade the result presented in Corollary 4. Here and in the rest of this section we denote by the limit copula of the sequence .

Theorem 11.

(a):

If copula is PQD, or equivalently is NQD, then is NQD.

(b):

If either the function is nonzero for all or the function is nonzero for all , then is an NQD copula for any copula .

(c):

If copula is PQD, then is PQD.

(d):

If either for the function it holds that for all or for the function it holds that for all , then is a PQD copula for any copula .

We will omit the proof since it goes in an obvious way.

Table 1. Spearman’s rho for copulas , and Clayton copula

0.1

0.1

-0.0000

-0.0083

-0.0149

-0.0201

-0.0242

0.1

0.5

-0.0000

-0.0525

-0.0708

-0.0783

-0.0816

0.1

0.9

-0.0000

-0.1215

-0.1268

-0.1273

-0.1273

0.5

0.1

-0.0000

-0.0525

-0.0708

-0.0783

-0.0816

0.5

0.5

-0.0000

-0.2952

-0.3300

-0.3375

-0.3393

0.5

0.9

-0.0000

-0.5419

-0.5497

-0.5500

-0.5500

0.9

0.1

-0.0000

-0.1215

-0.1268

-0.1273

-0.1273

0.9

0.5

-0.0000

-0.5419

-0.5497

-0.5500

-0.5500

0.9

0.9

-0.0000

-0.8629

-0.8646

-0.8646

-0.8646

0.1

0.1

-1.0000

-0.8650

-0.7387

-0.6233

-0.5200

0.1

0.5

-1.0000

-0.5610

-0.2996

-0.1747

-0.1218

0.1

0.9

-1.0000

-0.2154

-0.1345

-0.1279

-0.1274

0.5

0.1

-1.0000

-0.5610

-0.2996

-0.1747

-0.1218

0.5

0.5

-1.0000

-0.4667

-0.3633

-0.3450

-0.3411

0.5

0.9

-1.0000

-0.5611

-0.5505

-0.5501

-0.5501

0.9

0.1

-1.0000

-0.2154

-0.1345

-0.1279

-0.1274

0.9

0.5

-1.0000

-0.5611

-0.5505

-0.5501

-0.5501

0.9

0.9

-1.0000

-0.8650

-0.8646

-0.8646

-0.8646

0.1

0.1

1.0000

0.8548

0.7350

0.6349

0.5502

0.1

0.5

1.0000

0.4891

0.2249

0.0794

0.0008

0.1

0.9

1.0000

0.0037

-0.1135

-0.1259

-0.1272

0.5

0.1

1.0000

0.4891

0.2249

0.0794

0.0008

0.5

0.5

1.0000

0.0167

-0.1859

-0.2677

-0.3049

0.5

0.9

1.0000

-0.4639

-0.5406

-0.5491

-0.5500

0.9

0.1

1.0000

0.0037

-0.1135

-0.1259

-0.1272

0.9

0.5

1.0000

-0.4637

-0.5406

-0.5491

-0.5500

0.9

0.9

1.0000

-0.8302

-0.8613

-0.8643

-0.8645

0.1

0.1

-0.6844

-0.5775

-0.4828

-0.4007

-0.3310

0.1

0.5

-0.6844

-0.3652

-0.2052

-0.1354

-0.1061

0.1

0.9

-0.6844

-0.1754

-0.1314

-0.1277

-0.1273

0.5

0.1

-0.6844

-0.3652

-0.2052

-0.1354

-0.1061

0.5

0.5

-0.6844

-0.3988

-0.3519

-0.3426

-0.3406

0.5

0.9

-0.6844

-0.5544

-0.5502

-0.5501

-0.5501

0.9

0.1

-0.6844

-0.1754

-0.1314

-0.1277

-0.1273

0.9

0.5

-0.6844

-0.5544

-0.5502

-0.5501

-0.5501

0.9

0.9

-0.6844

-0.8643

-0.8646

-0.8646

-0.8646

We want to observe how two important concordance measures (sometimes seen as coefficients) of copulas, Spearman’s rho and Kendall’s tau, change when transformation is applied to them. We refer the reader to [27, Chapter 5] and [11, Section 2.4] for definitions and explanation of these coefficients. Although formula (4) is simpler than [10, (2.3)] as we pointed out, computing the two coefficients is still a nontrivial task. In the paper [28], they were computed only for the case of independent shocks, of course. To go for dependent shocks we need to use the formulas given in [12]:

and

Here is the derivative of with respect to variable . We applied these formulas to generators and , for all combinations of parameters , and for copulas , and . We computed the integrals using the exact expression for copulas and by numerical integration using the Mathematica software [31]. The results are presented in Tables 1 and 2.

The presented experiment suggests that the convergence of the iteration studied in this section is substantially faster with parameters and big.

Table 2. Kendall’s tau for copulas , and Clayton copula

0.1

0.1

0.0000

-0.0055

-0.0099

-0.0134

-0.0162

0.1

0.5

0.0000

-0.0351

-0.0473

-0.0523

-0.0545

0.1

0.9

0.0000

-0.0837

-0.0871

-0.0874

-0.0874

0.5

0.1

0.0000

-0.0351

-0.0473

-0.0523

-0.0545

0.5

0.5

0.0000

-0.2111

-0.2338

-0.2387

-0.2399

0.5

0.9

0.0000

-0.4368

-0.4410

-0.4412

-0.4412

0.9

0.1

0.0000

-0.0837

-0.0871

-0.0874

-0.0874

0.9

0.5

0.0000

-0.4372

-0.4410

-0.4412

-0.4412

0.9

0.9

0.0000

-0.8063

-0.8064

-0.8064

-0.8064

0.1

0.1

-1.0000

-0.8065

-0.6457

-0.5139

-0.4073

0.1

0.5

-1.0000

-0.4475

-0.2118

-0.1184

-0.0817

0.1

0.9

-1.0000

-0.1495

-0.0923

-0.0879

-0.0875

0.5

0.1

-1.0000

-0.4475

-0.2118

-0.1184

-0.0817

0.5

0.5

-1.0000

-0.3333

-0.2561

-0.2437

-0.2411

0.5

0.9

-1.0000

-0.4474

-0.4415

-0.4412

-0.4412

0.9

0.1

-1.0000

-0.1495

-0.0923

-0.0879

-0.0875

0.9

0.5

-1.0000

-0.4474

-0.4415

-0.4412

-0.4412

0.9

0.9

-1.0000

-0.8065

-0.8064

-0.8064

-0.8064

0.1

0.1

1.0000

0.8000

0.6540

0.5428

0.4553

0.1

0.5

1.0000

0.4000

0.1692

0.0577

0.0015

0.1

0.9

1.0000

0.0001

-0.0810

-0.0875

-0.0875

0.5

0.1

1.0000

0.4000

0.1692

0.0577

0.0015

0.5

0.5

1.0000

0.0000

-0.1413

-0.1951

-0.2187

0.5

0.9

1.0000

-0.4000

-0.4368

-0.4412

-0.4412

0.9

0.1

1.0000

0.0001

-0.0810

-0.0875

-0.0875

0.9

0.5

1.0000

-0.4000

-0.4368

-0.4412

-0.4412

0.9

0.9

1.0000

-0.8000

-0.8058

-0.8064

-0.8064

0.1

0.1

-0.5385

-0.4368

-0.3532

-0.2854

-0.2308

0.1

0.5

-0.5385

-0.2569

-0.1390

-0.0909

-0.0710

0.1

0.9

-0.5385

-0.1202

-0.0902

-0.0877

-0.0875

0.5

0.1

-0.5385

-0.2569

-0.1390

-0.0909

-0.0710

0.5

0.5

-0.5385

-0.2810

-0.2483

-0.2421

-0.2407

0.5

0.9

-0.5385

-0.4436

-0.4413

-0.4412

-0.4412

0.9

0.1

-0.5385

-0.1202

-0.0902

-0.0877

-0.0875

0.9

0.5

-0.5385

-0.4436

-0.4413

-0.4412

-0.4412

0.9

0.9

-0.5385

-0.8064

-0.8064

-0.8064

-0.8064

Next we compute analytically the tail dependence coefficients for the limit reflected maxmin copula,

see [27, Section 5.4] and [11, Section 2.6.1]. One may find there an equivalent expression for each of the coefficients

Proposition 12.

(a):

If and , then , if not, then .

(b):

If and are both strictly smaller than 1, then , if not, then .

(c):

If either and or and then . If and then . In the remaining case and the value of depends on generators and .

(d):

If either and or and then . If and then . In the remaining case and the value of depends on generators and .

Proof.

Straightforward computation.

At this point it is appropriate to emphasize that in the situation of the semi-group action interpretation of the Durante-Girard-Mazo model presented in [6, Section 3] (cf. also [5]) some concrete stability results (cf. [6, Example 3.1]) show similar behavior to what we observed in the case of maxmin and reflected maxmin transformations given in Theorems 8 & 10. We think that these similarities are more than just coincidental and deserve to be studied further.

5. Multivariate reflected maxmin copulas:

It is now time to move to the second main result of the paper, the extension of the dependent reflected maxmin copulas to the multivariate case. In order to make our computations easier to understand, let us first compute one of the two possible cases for three variables. To get a perception of the possible improvement of reflected maxmin approach compared to the original maxmin techniques consider formula on [10, p. 166], where two minima and one maximum are taken

We will rewrite this formula into Equation (16) in the reflected maxmin setting. An interested reader may find the computations leading to this formula, although somewhat tedious, in the next lines. Our point is that it may be helpful to understand better the main steps of the computation in smaller dimension before we extend these steps to the general level in the next section. First, rewrite the above formula as

(12)

where

We want to perform the two flips on the copula respectively on terms . First transform the term by a flip in the second variable, i.e. :

Next, we perform a flip in the third variable, i.e. the transformation , on :

We now perform the two flips on , first a flip in the second variable, i.e. :

Here, we have used the fact that the second term in the first above is clearly greater than the first one and can therefore be neglected, and then we have used an obvious rule

(13)

to simplify the expression containing the two minima. Now, we apply a flip in the third variable, i.e. the transformation , on :

It is clear that can be obtained from by exchanging indices and , so after performing the two transformations and (in any order), we get by analogy with the result above:

It remains to transform the last term , first by flipping the second variable, i.e. :

In the considerations above, we have first neglected , clearly no smaller than the other two compared quantities of the first ; then we have used Rule (13) with and .

And finally we flip the third variable, i.e. in :

and use the above considerations. We have thus transformed maxmin copula of (12) into reflected maxmin copula

(14)

The second factor above reminds us of the reflected copula related to , but not quite yet. In order do get a better expression we need to replace the generating functions of the maxmin copula and their auxiliary functions with the according reflected maxmin generators and their auxiliaries. It is clear that when we follow (3) we have to use the transformation rule for the generator of index and transformation rule for the generators of indices :

(15)

Using these definitions, we transform the second factor of (14) into

and the first factor of (14) termwise. The first term equals

and similarly for the second term, where we replace index with . So, with the reflected maxmin generators we can write (14) in the form (16) as required:

(16)

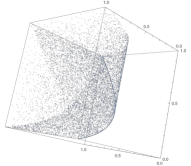

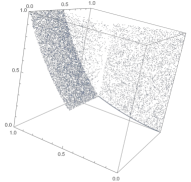

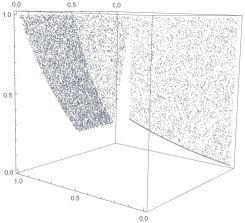

In Figures 5 to 8 we give examples of 3D scatterplots of reflected maxmin copulas. We explain how the samples of these plots have been generated in the Appendix. Generating functions for the scatterplot in Figure 5 are functions and is the product copula. In the figure there are three different views of the same scatterplot. The copula has 1-dimensional and 2-dimensional singular components. 1-dimensional singular component lies on the curve . 2-dimensional singular components lie on the surfaces , and . The zero set of the copula is the set On the complement of the union of the zero set and the singular components the third mixed derivative of the copula exists and is positive.

Figure 5. 3D-Scatterplots of reflected maxmin copulas

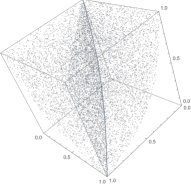

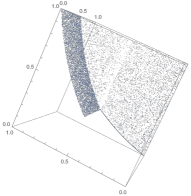

Generating functions for scatterplot in Figure 6 are functions and for and is the product copula. The copula has 1-dimensional and 2-dimensional singular components. 1-dimensional singular component lies on the curve for . 2-dimensional singular component lies on the surface for and . The third mixed derivative of the copula is zero where it exists.

Figure 6. Reflected maxmin copula with a 1-dimensional and 2-dimensional singular component

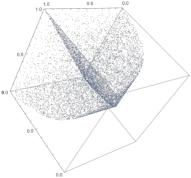

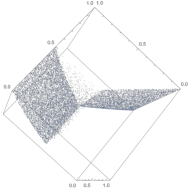

Generating functions for scatterplot in Figure 7 are functions , , and is the product copula. The copula has 1-dimensional and 2-dimensional singular components. 1-dimensional singular component lies on the curve , for . 2-dimensional singular components lie on the surfaces , for and for and . The third mixed derivative of the copula exists and is positive on the region . In the figure there are three different views of the same scatterplot.

Figure 7. Reflected maxmin copula with a 1-dimensional and two 2-dimensional singular components

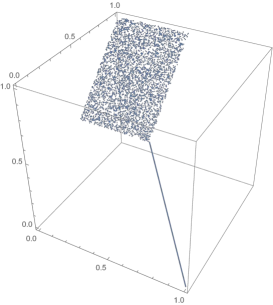

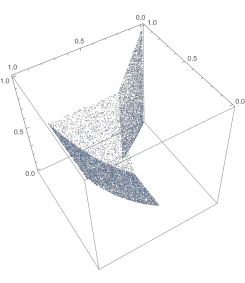

Generating functions for scatterplot in Figure 8 are functions , , and . The copula has 1-dimensional and 2-dimensional singular components. 1-dimensional singular component lies on the curve , for . The first 2-dimensional singular component lies on the surface , for , the second lies on , for , , and the third lies on for , . The third mixed derivative of the copula is zero where it exists. In the figure there are two different views of the same scatterplot.

Figure 8. Another example of reflected maxmin copula with more singular components

After we did all this for one important case of , we can go for general .

6. Multivariate reflected maxmin copulas: the general case

Recal the formula on [10, p. 166] that we transformed in Section 5 into (16). In order to do that for general , we first derive the general formula in the form of (14) of Section 5. We need to specify in what sense the inclusion-exclusion principle is made on the copula (note that we adjust here the notation of [10] in an obvious way)

Theorem 13.

Let be a maxmin -copula with maxima and minima. Then its reflected maxmin copula takes the form

where equals

Here, in the last displayed equation, we use one of the standard notations for the inclusion-exclusion principle formula. So, denotes a vector of zeros and ones whose entries are indexed by , and

The notation above means that we are taking into account all the possible vectors of the kind.

Take a single term of for some with , and denote it by . Without loss of generality we may assume that and To somewhat simplify the notation in what follows we introduce

and .

Then equals

We start by transforming the variables with indices in .

Apply transformation to term to get:

where the three inside minima are all taken over and . (Note that we have used Rule (13) here and will be doing so similarly in what follows.)

Next, apply transformation to term to get:

where the inside minima are taken over and .

We proceed inductively on the index of transformation variable up to to get the intermediate result

Now, we start performing the transformations of variables with indices in . So far, the factor corresponding to the copula has not been changing. From now on it will change, but only in indices from on. To somewhat simplify the notation we introduce:

First, apply transformation on the last term above:

where the two inside minima are to be taken over , , and . Note that , so that only the second term of the expression above stays. By applying the transformation to the expression under consideration, we get

where the inside minima are taken over , and . Similarly as above we see that only the second term stays. Again, we proceed inductively to get the final result for the transformed term:

The desired reflected maxmin copula is then the sum of all the terms of the kind. We first observe that the second factor of this term (i.e. the one that does not correspond to ), is independent of the choice of , so that we can take it out from the summation. The sum of the first factors, on the other hand, follows a certain well-known pattern called inclusion-exclusion principle. This factor of each term is of the form

where is any function , and means

The sign of this factor equals if we have an odd number of inclusions (i.e. 1’s in the row) and otherwise, so it equals to . This completes the proof.

It remains to translate the formula for the reflected maxmin copula in terms of the generators introduced in (15) of Section 5 to get the general case of Formula (16). We follow exactly the same computations as in Section 5 to get the following theorem, where denotes copula transformed with a flip in each of variables with indices .

Theorem 14.

The reflected maxmin -copula with maxima and minima, corresponding to generating functions and reflected copula , is of the form

Appendix

Let us give a rough explanation of how the three-dimensional scatterplot of a -copula is generated. It follows roughly the following process:

•

Determine all three marginal 2-copulas and their respective contourplots.

•

Check for existence of singularities of marginal 2-copulas and respective masses. If marginals are without singularities, copula doesn’t have a 1-dimensional singularity.

•

Split the sampling of 3-copula into regions where marginal is continuously distributed and where it is singular.

•

Calculate and determine maximal subregions of of continuity.

•

The most difficult part of the process is the calculation of pseudo-inverse of with respect to variable . Beside inverting function rules, it is also necessary to transform the boundary conditions where these rules apply.

•

At discontinuities of singular components occur. The size of the gap implies the amount of mass gathered on respective singular component.

•

When the calculation of pseudo-inverse of is complete, generate a sample set of say 5000 pairs distributed with respect to marginal 2-copula and an independent sample uniformly distributed on .

•

Merge sets and into 3-tuples .

•

For every 3-tuple determine the region that belongs to and apply corresponding pseudo-inverse function rule to .

•

The process is done manually with lots of careful considerations which doesn’t give rise to hope of automatization.

References

[1] L. Běhounek, U. Bodenhofer, P. Cintula, S. Saminger-Platz, P. Sarkoci, Graded dominance and related graded properties of fuzzy connectives, Fuzzy Sets and Systems, 262 (2015), 78–101.

[2] U. Cherubini, F. Durante, S. Mulinacci, (eds.), Marshall–Olkin Distributions – Advances in Theory and Applications, Springer Proceedings in Mathematics & Statistics, Springer International Publishing, 2015.

[3]U. Cherubini, S. Mulinacci, Systemic risk with exchangeable contagion: application to the European banking system, ArXiv e-prints, 2015.

[4] F. Durante, J. Fernández Sánchez, M. Úbeda Flores, Bivariate copulas generated by perturbarion, Fuzzy Sets and Systems, 228 (2013), 137–144.

[5] F. Durante, S. Girard, G. Mazo, Copulas Based on Marshall-Olkin Machinery, Chapter 2 in: U. Cherubini, F. Durante, S. Mulinacci (Eds.), Marshall-Olkin Distributions – Advances in Theory and Practice, in: Springer Proceedings in Mathematics & Statistics, Springer, 2015, pp. 15–31.

[6] F. Durante, S. Girard, G. Mazo, Marshall–Olkin type copulas generated by a global shock, J. Comput. Appl. Math., 296 (2016), 638–648.

[7] F. Durante, P. Jaworski, A new characterization of bivariate copulas, Comm. in Stats. Theory and Methods, 39 (2010), 2901–2912.

[8] F. Durante, A. Kolesarovà, R. Mesiar, C. Sempi, Semilinear copulas, Fuzzy Sets and Systems, 159 (2008), 63–76.

[9] F. Durante, R. Mesiar, P. L. Papini, C. Sempi, 2-Increasing binary aggregation operators, Information Sciences, 177 (2007), 111–129.

[10] F. Durante, M. Omladič, L. Oražem, N. Ružić, Shock models with dependence and asymmetric linkages, Fuzzy Sets and Systems, 323 (2017), 152–168.

[11] F. Durante, C. Sempi, Principles of Copula Theory, CRC/Chapman & Hall, Boca Raton (2015).

[12] G. A. Fredricks, R. B. Nelsen, On the relationship between Spearman’s rho and Kendall’s tau for pairs of continuous random variables, Journal of Statistical Planning and Inference 137 (2007), 2143–2150

[13] B. E. Fristedt, L. F. Gray, AModern Approach to Probability Theory, Probability and Its Applications, Birkhäuser, Boston, 2013.

[14] C. Genest, J. Nešlehová, Assessing and Modeling Asymmetry in Bivariate Continuous Data, In: P. Jaworski, F. Durante, W.K. Härdle, (eds.), Copulae in Mathematical and Quantitative Finance, Lecture Notes in Statistics, Springer Berlin Heidelberg, (2013), 152–16891–114.

[15] T. E. Huillet, Stochastic species abundance models involving special copulas, Phisica A, 490 (2018) 77–91

[16] T. Jwaid, B. De Baets, H. De Meyer, Ortholinear and paralinear semi-copulas, Fuzzy Sets and Systems, 252 (2014), 76–98.

[17] T. Jwaid, B. De Baets, H. De Meyer, Semiquadratic copulas based on horizontal and vertical interpolation, Fuzzy Sets and Systems, 264 (2015), 3–21.

[18] E. P. Klement, J. Li, R. Mesiar, E. Pap, Integrals based on monotone set functions, Fuzzy Sets and Systems, 281 (2015), 3–21.

[19] E. P. Klement, R. Mesiar, F. Spizzichino, A. Stupňanová, Universal integrals based on copulas, Fuzzy Optim. Decis. Mak., 13, No. 3, (2014), 273–286.

[20] D. Kokol Bukovšek, T. Košir, B. Mojškerc, and M. Omladič, Non-exchangeability of copulas arising from shock models, J. Comput. Appl. Math. 358 (2019), 61-83.

[21] T. Košir, M. Omladič, Reflected maxmin copulas and modelling quadrant subindependence, Fuzzy Sets and Systems, available online, in Press.

[22] F. Lindskog, A. J. McNeil, Common Poisson Shock Models: Applications to insurance and credit risk modelling, ASTIN Bulletin, 33, No. 2, (2003), 209–238.

[23] A. W. Marshall, Copulas, marginals, and joint distributions, in: L. Rüschendorf, B. Schweitzer, M. D. Taylor (eds.), Distributions with Fixed Marginals and Related Topics in LMS, Lecture Notes – Monograph Series, vol. 28, 1996, 213–222.

[24] A. W. Marshall, I. Olkin, A multivariate exzponential distributions, J. Amer. Stat. Assoc., 62, (1967), 30–44.

[25] R. Mesiar, M. Komorníková, J. Komorník, Perturbation of bivariate copulas, Fuzzy Sets and Systems, 268 (2015), 127–140.

[26] S. Mulinacci. Archimedean-based Marshall-Olkin distributions and related dependence structures, Methodol. Comput. Appl. Probab., 20 (2018), 205–236.

[27] R. B. Nelsen, An introduction to copulas, 2nd edition, Springer-Verlag, New York (2006).

[28] M. Omladič, N. Ružić, Shock models with recovery option via the maxmin copulas, Fuzzy Sets and Systems, 284 (2016), 113–128.

[29] J. A. Rodríguez-Lallena, M. Úbeda-Flores, A new class of bivariate copulas, Stat. & Probab. Lett., 66 (2004), 315–325.

[30] A. Sklar, Fonctions de répartition à dimensions et leurs marges, Publ. Inst. Stat. Univ. Paris 8 (1959) 229–231.

[31] Wolfram Research, Inc. Mathematica, Version 11, Champaign, IL, 2017.