The Structure of Equilibria in Trading Networks with Frictions

Abstract

Several structural results for the set of competitive equilibria in trading networks with frictions are established: The lattice theorem, the rural hospitals theorem, the existence of side-optimal equilibria, and a group-incentive-compatibility result hold with imperfectly transferable utility and in the presence of frictions. While our results are developed in a trading network model, they also imply analogous (and new) results for exchange economies with combinatorial demand and for two-sided matching markets with transfers.

JEL-classification:C78, D47, D52, L14

Keywords: Trading Networks; Full Substitutability; Imperfectly Transferable Utility; Competitive Equilibrium; Indivisible Goods; Frictions; Lattice; Rural Hospitals

1 Introduction

The assumption of quasi-linear utility in transfers is pervasive in models of matching markets, exchange economies with indivisible goods, trading networks, and in mechanism design. Quasi-linearity can simplify the analysis considerably since it allows us to exploit the duality between optimal allocations and supporting equilibrium prices. While the assumption of quasi-linearity simplifies the analysis, it is often empirically problematic. Wealth effects are present in marriage and labor markets so that matching models with transferable utility are unrealistic for these applications. Even if wealth effects are absent, transaction frictions such as those induced by taxation, subsidies, or transaction costs, make a transferable utility model inapplicable. This has motivated researchers to explore how results for matching markets with transfers Demange and Gale (1985); Legros and Newman (2007); Nöldeke and Samuelson (2018); Galichon et al. (2019) and for trading networks Fleiner et al. (2019); Hatfield et al. (2020) can be generalized beyond quasi-linear utility.

In this paper, we contribute to this discussion and study imperfectly transferable utility and frictions222In the following, we distinguish language-wise between the case of pure imperfectly transferable utility where utility is not necessarily linear in transfers, but a function of the sum of transfers received, and the case of frictions where utility is not necessarily a function of the sum of transfers received, but a function of the entire vector of transfers. If frictions are present, it thus not only matters how much a firm receives in total transfers, but also through which trades it receives the transfers. This can e.g. be the case if different trades involve different transaction costs. The results in our paper apply to both pure imperfectly transferable utility and frictions. in the context of trading networks Hatfield et al. (2013). Trading networks with bilateral contracts model complex supply chains in an industry where firms are engaged in upstream as well as downstream contracts. They generalize two-sided matching markets, in the sense that they replace a bipartite graph of potential relations, by an arbitrary graph where each edge represents a potential trade. We show that important structural results for trading networks do not depend on the assumption of quasi-linear utility, and establish several results about the set of competitive equilibria under minimal assumptions on utility functions. Our results apply even in the case of imperfectly transferable utility, in the presence of frictions, and if constraints make the execution of certain combinations of trades infeasible.

Our results can be summarized as follow: For a model of trading networks with frictions Fleiner et al. (2019) and under the assumptions of full substitutability Sun and Yang (2006); Ostrovsky (2008); Hatfield et al. (2013) and the laws of aggregate demand and supply Ostrovsky (2008); Hatfield et al. (2020), we show that

-

-

the set of competitive equilibria is a sublattice of the price space (first part of Theorem 1),

-

-

a generalized ”rural hospitals theorem” holds: the difference between the number of signed downstream and the number of signed upstream contracts is the same for each firm in each equilibrium (second part of Theorem 1),

- -

-

-

a mechanism that selects buyer-optimal equilibria is group-strategy-proof for terminal buyers on the domain of unit-demand utility functions and similarly a mechanism that selects seller-optimal equilibria is group-strategy-proof for terminal sellers on the domain of unit-supply utility functions (Theorem 3).

While our results are established for trading networks, the results are already new for many-to-one matching markets and for exchange economies with combinatorial demand which are special cases of our model. For matching markets, similar results were so far only known (a) under quasi-linear utility, (b) for models without transfers and with strict preferences, or (c) for one-to-one matching markets with imperfectly transferable utility. For exchange economies with indivisible goods, analogous results were so far only known for (a) quasi-linear utility, or for the case of (b) unit demand.

Working with imperfectly-transferable utility and frictions requires us to develop fundamentally new techniques: Similar results for the case of imperfectly transferable utility were so far only known for one-to-one matching markets Demange and Gale (1985) and the proof techniques developed in this context (in particular the ”decomposition lemma”) do not adapt to more general settings. On the other hand, techniques from transferable utility models do not generalize to our model: Hatfield et al. (2013) use the efficiency of competitive equilibria and the submodularity of the indirect utility function to establish the lattice property. For our model with frictions, competitive equilibria can fail to be efficient. Moreover, full substitutability implies only the weaker notion of quasi-submodularity Fleiner et al. (2019). More subtly, as we will discuss below, without quasi-linearity there are several non-equivalent definitions of full substitutability and these definitions are not distinguishable through conditions on the indirect utility function alone. Thus, an approach as in Hatfield et al. (2013) that characterizes competitive equilibria through the indirect utility function and uses properties of that function under full substitutability does not generalize. Likewise, the network flow approach to trading networks Candogan et al. (2016) obtains structural results on the set of equilibria through the duality between optimal allocations and supporting prices. Since efficiency fails in our setting this duality approach does not generalize. Finally, techniques from trading networks without transfers Ostrovsky (2008) that rely on Tarski’s fixpoint theorem do not apply to the our model. With transfers, the issue of tie-breaking arises that is not present in models without transfers and with strict preferences. While versions of Tarski’s fixpoint theorem for correspondences are known Zhou (1994), none of them work under sufficiently weak assumptions to be useful in our environment.

Since existing techniques do not work for our setting, we introduce a new approach to establish structural results for the set of competitive equilibria. The approach can be characterized as a tie-breaking approach: we show that for each finite set of (equilibrium) price vectors and each firm a single-valued selection from the demand correspondence can be made such that the properties of full substitutability and the laws of aggregate demand and supply are satisfied by the selection, and moreover, relevant trades that are demanded in the supporting equilibrium allocations are demanded in the selection. The assumption of the Laws of Aggregate Demand and Supply is necessary for our tie-breaking argument, and our result does not hold under Full Substitutability alone (see Example 2).

We also make a more technical contributions to the literature on trading networks with imperfectly transferable utility nad frictions and clarify issues related to the definition of Full Substitutability: For the quasi-linear model, there are various equivalent definitions of Full Substitutability Hatfield et al. (2019). The equivalence, however, breaks down if we go beyond quasi-linear utility, and, for our results, it matters which of the full substitutability notions is used. More specifically, it matters how full substitutability restricts the demand at price vectors at which the demand is multi-valued. We introduce weak notions of Full Substitutability and the Laws of Aggregate Demand and Supply that only restrict the demand at price vectors where the demand is single-valued and stronger versions that also restrict it at prices where the demand is multi-valued. The notions are equivalent under quasi-linear utility, but not in general. The set of competitive equilibria is a lattice only under the strong versions of Full Substitutability (see Example 1) and the rural hospitals theorem requires the strong versions of the law of aggregate demand and supply (see Example 4). Our group-strategy-proofness result, however, holds also under the weaker notions (Corollary 1). Thus, the exact definition of Full Substitutability matters in the model with frictions.333Related issues occur in Hatfield et al. (2020) where the stronger Monotone Substitutability property is needed that restricts the choice in circumstances where the choice correspondence is multi-valued. See our discussion in Appendix A.

We proceed as follows: In Section 2, we introduce the model and discuss different versions of the Full Substitutability conditions and their relation to each other. We provide a more detailed discussion of different Full Substitutability conditions in Appendix A. In Section 3, we prove our main results: the lattice structure of the set of competitive equilibria, the generalized rural hospitals theorem, the existence of extremal equilibria, and group-incentive compatibility for terminal buyers. In Section 4, we apply our main results to two-sided matching markets, and to exchange economies with indivisible goods.

1.1 Related Literature

The literature on trading networks has its origins in the literature on matching markets with transfers. In a seminal paper, Kelso and Crawford (1982) show that, under the assumption of gross substitutability, competitive equilibria with personalized prices exist and are equivalent to core allocations in a many-to-one labor market matching model. The construction is by an approximation argument where the existence in the continuum is obtained from the existence of an equilibrium in a discrete markets with smaller and smaller price increments. Different versions of a strategy-proofness result for a many-to-one matching model with continuous transfers were established by Hatfield et al. (2014); Schlegel (2018); Jagadeesan et al. (2018). Subsequent to Kelso and Crawford (1982), the question of existence of equilibria has been studied in the context of exchange economies with indivisibilities. See for example Gul and Stacchetti (1999) and the recent contribution of Baldwin and Klemperer (2019).

Trading networks with bilateral contracts and continuous transfers were introduced by Hatfield et al. (2013). Under the assumption of quasi-linear utility and full substitutability they establish many results that we generalize to the case of general utility functions. The notion of full substitutability has been studied in detail by Hatfield et al. (2019) who show the equivalence of various different definitions of full substitutability. The existence result of Hatfield et al. (2013) is proved via a reduction to the existence result of Kelso and Crawford (1982). An alternative approach is via a submodular version of a network flow problem Candogan et al. (2016).

The work of Hatfield et al. (2013) builds on the work of Ostrovsky (2008) on trading networks without transfers that generalizes matching models with contracts Hatfield and Milgrom (2005); Fleiner (2003); Roth (1984) beyond two-sided markets. The matching model with contracts in turn originates in the discrete version of the model of Kelso and Crawford (1982). Hatfield and Kominers (2012) and Fleiner et al. (2016) provide additional results for the discrete trading networks model, which in many ways are parallel to the results we obtain in the continuous model. Importantly, results for the model without continuous transfers rely on the assumption of strict preferences.

All the above mentioned work for the continuous models make the assumption of quasi-linear utility.444Note however that the existence proof of Kelso and Crawford (1982) is actually more general and also applies to non-quasi-linear preferences, provided they are continuous, monotonic and unbounded in transfers for each bundle. There are few papers that deal with non-quasi-linear utility functions, frictions or constraints and that are particularly close to our work: In a classical paper, Demange and Gale (1985) establish several structural results about the core (or equivalently the set of competitive equilibria) for a one-to-one matching model with continuous transfers. In particular, they show that the core has a lattice structure and an agent that is unmatched in one core allocation receives his reservation utility in each core allocation (the result is often called the rural hospitals theorem in the literature on discrete matching markets). Moreover, they show that the mechanism that selects an extreme point of the bounded lattice is strategy-proof for one side of the market. Importantly, these results are established without assuming quasi-linearity in transfers. They only require that utility is increasing, continuous in transfers and satisfies a full range assumption. We generalize this work to trading networks and to situations in which utility does not satisfy the full range assumption.

In recent work, Fleiner et al. (2019) study trading networks with imperfectly transferable utility and frictions. Their work is in many regards complementary to our work. In particular, Fleiner et al. (2019) establish the existence of a competitive equilibrium under the assumption of Full Substitutability and mild regularity conditions. Moreover, they study the efficiency of competitive equilibria and provide conditions under which equilibria correspond to allocations satisfying different related cooperative solution concepts. We derive our results for competitive equilibria. However, by the equivalence result of Fleiner et al. (2019) analogous results also would hold for ”trail-stable” allocations. All results of Hatfield et al. (2013), except for the maximal domain result (Theorem 7) are generalized to general utility functions with frictions, either in our work or by Fleiner et al. (2019). Table 1 in Appendix E summarizes known results for trading networks with frictions.

Kojima et al. (2020b) introduce constraints in the job matching model of Kelso and Crawford (1982) and characterize constraints that leave the gross substitutes condition invariant. The model with constraints is a special case of the model in the current paper so that we obtain as a corollary of our results a version of a lattice and of the rural hospital theorems for their model of job matching under constraints. In a spin-off paper, Kojima et al. (2020a) study comparative statics for their model and also proof versions of the lattice result and the rural hospitals theorem. These results have been obtained independently and contemporaneously with the results in the current paper.555Weaker versions of these results were obtained prior to that in Schlegel (2018).

2 Model

The model is based on Hatfield et al. (2013), and the extensions of Fleiner et al. (2019) and Hatfield et al. (2020). We consider a finite set of firms and a finite set of trades . Each trade is associated with a buyer and a seller with . For a set of trades and firm we define the set of downstream trades for by and the set of upstream trades by . Moreover, we let . A firm such that is called a terminal buyer and a firm such that is called a terminal buyer. Note that terminal buyers and/or terminal buyers do not need to exist. A contract is a pair , where is the price attached to the trade .

An allocation is a pair consisting of a set of trades and a price vector . We denote the set of allocations by and we let . An arrangement is a pair . In contrast to an allocation the price vector also contains prices for unrealized trades.

Each firm has a utility function . For notational convenience we extend to by defining for and , the utility We allow the utility function to take on a value of to model technical or institutional constraints faced by a firm that make the execution of the combination of trades infeasible. We require that

-

•

if a bundle is infeasible under some prices, then it is infeasible under all prices: if for then for each ,

-

•

at least one bundle of trades is feasible: there is a such that .666In contrast to Fleiner et al. (2019) where it is always feasible to refuse all trades, we allow for the possibility that . This does not really make our model more general, since we could alternatively apply a continuous and monotonic utility transformation to guarantee that utility for all feasible bundles is positive and assign zero utility to .

Moreover, we make the following assumptions on utility functions:

-

•

Continuity: For with the function is continuous on .

-

•

Monotonicity: For with and with :

-

1.

If for and for , then .

-

2.

If for and for , then .

-

1.

Thus, utility is continuous in prices and firms strictly prefer higher sell prices to lower sell prices and lower buy prices to higher buy prices.

Remark 1.

Note that we allow utility for a set of trades to be different for prices , even if the transfers received are the same for both price vectors, i.e. even if This can e.g. be the case if different trades involve different transaction costs.

If utility only depends on the set of trades and the transfers received, we have a special case of our model: We say that satisfies no frictions Fleiner et al. (2019) if there is a function such that

Quasi-linear utility corresponds to the case without frictions where is linear in transfers. In this case there is a valuation function such that

∎

A utility function induces an indirect utility function by

and a demand correspondence by:

Continuity of the utility function implies (e.g. by Berge’s maximum theorem) that the demand correspondence is upper hemi-continuous. Monotonicity of the utility function implies that price vectors where the demand is single-valued are dense in price space. We will repeatedly use these facts to generate a single-valued selection from the demand-correspondence by perturbing the price vector such that it becomes single-valued. The proof is straightforward and hence omitted.

Lemma 1.

For a continuous and monotonic utility function ,

-

1.

the induced demand is upper hemi-continuous, i.e. for each there is an such for any with (where denotes the Euclidean norm) we have ,

-

2.

the set of price vectors such that the induced demand is single-valued is dense in , i.e. for each and there is a with such that .

2.1 Full Substitutability

Our results rely on a full substitutability assumption on utility functions. Informally, the condition requires that a firm sees upstream (downstream) trades as substitutes to each other, and upstream and downstream trades as complements to each other. Hatfield et al. (2019) show that for quasi-linear utility various ways of defining full substitutability are equivalent, and hence one can work with either of the definitions discussed in their paper. Going beyond quasi-linear utility makes issues more subtle: Not all equivalence results of Hatfield et al. (2019) generalize to non-quasi-linear utility and it matters which of the full substitutability conditions are used. More specifically, it matters how the full substitutes condition is defined in instances where indifferences matter, i.e. when the demand is multi-valued.

We will proceed as follows: First, we introduce our main definition of full substitutability which restrict the demand both at price vectors where the demand is single-valued and where it is multi-valued. Second, we introduce the weak version of full substitutability that only restricts the demand at price vectors where the demand is single-valued. We provide an example that shows that the single-valued version of full substitutability is strictly weaker than the multi-valued version. We later show, using this example, that the single-valued full substitutability condition is not sufficient for establishing the lattice and the rural hospitals theorem. Importantly, the difference between the single-valued and multi-valued version of full substitutability only matters for the ”cross-side conditions” on firms’ demand functions. In particular, the notions are equivalent for a two-sided market and the results for two-sided markets (see Section 4.1) hold under the single-valued notion of full substitutability. Third, we show that the multi-valued and the single-valued versions are, however, closely related in the sense that for each demand correspondence satisfying weak full substitutability, a selection from the demand correspondence exists that satisfies (multi-valued) full substitutability and can be rationalized by a utility function inducing the same indirect utility. In particular, this will allow us, later on (Corollary 1), to obtain a group-strategy-proofness result using only the weak full substitutability notion.

In Appendix A we discuss in more detail the logical relation between different notions of full substitutability. In particular, we show (Corollary A.1) that under the assumption of continuity and monotonicity, monotone substitutability as defined in Hatfield et al. (2020), is equivalent to the combination of (the multi-valued versions of) full substitutability, the laws of aggregate demand and supply. Thus, the main results in our paper hold under (the demand language version of) the substitutability notion used by Hatfield et al. (2020) for their main result.

2.1.1 Multi-Valued Full Substitutability

The following notion of full substitutability is due to Hatfield et al. (2019).777Hatfield et al., 2019 call this version of full substitutability the ”demand-language expansion” version of full

substitutability (cf. Definition A.3 in Hatfield et al., 2019). There are alternative multi-valued definitions of full substitutability which we discuss in Appendix A. Throughout the paper, we use “demand language” definitions of full substitubility that restrict the demand correspondence induced by the utility function. The demand language definitions are generally weaker than the

corresponding “choice language” definitions that restrict the choice correspondence induced by the utility function. Consequently, all of our result would also hold under the corresponding “choice language” notions of full substitutability. Precursors of the full substitutability notion were introduced for exchange economies Sun and Yang (2006) and for trading networks without transfers Ostrovsky (2008). Full substitutability can be further decomposed in a same-side substitutability and a cross-side complementarity notion.

(Expansion) Same-Side Substitutability (SSS): For

and each there

exists a such that if for

and

for , then

and if for and for , then

(Expansion) Cross-Side Complementarity (CSC): For and each there exists a such if for and for , then

and if for and for , then

The combination of the two properties is called full substitutability.

(Expansion) Full Substitutability (FS): The demand of firm satisfies Expansion Full Substitutability if it satisfies Expansion Same-Side Substitutability and Expansion Cross-Side Complementarity.

Next we introduce monotonicity properties called the Law of Aggregate Demand respectively the Law of Aggregate Supply. Under quasi-linear utility, the two properties are implied by full substitutability. However, in general they are independent of full substitutability.

Law of Aggregate Demand (LAD): For and each there exists a such that if for and for , then

Law of Aggregate Supply (LAS): For and each there exists a such that if for and for , then

2.1.2 Single-Valued Full Substitutability

Next we introduce the weaker notion of full substitutability where the condition only needs to hold at price vectors where the demand is single-valued.

Weak Full Substitutability (weak FS):

For such that and , if for and for , then

and if for and for , then

Remark 2.

Similarly, we can define weak versions of the laws of aggregate demand and supply.

Weak Law of Aggregate Demand (Weak LAD): For such that and , if for and for , then

Weak Law of Aggregate Supply (Weak LAS): For such that and , if for and for , then

The following example shows that the two notions of full substitutability that we have defined can differ for non-quasi-linear utility. In Section 3, we will use the example to show that under weak FS the lattice result in our paper does not necessarily hold. Similar examples show that weak LAD/weak LAS is strictly weaker than LAD/LAS, see Example 4 in Appendix A.

Example 1.

Consider four trades with . We let

We let for any other . Observe that

but

As , FS would require that there is a with . Hence FS is not satisfied. As the demand at and is multi-valued, Weak FS does not impose any structure here. More generally, note that the bundle is only demanded at prices so that if we replace by the utility function such that

only the demand at prices changes. One readily checks that satisfies FS. Hence satisfies Weak FS. Note, moreover, that satisfied LAD and LAS. ∎

Remark 3.

In the example, the bundle is only demanded at prices , but not at any price vector in the neighborhood. One can show (see Proposition A.3 in Appendix A) that if there are no such ”isolated” bundles, i.e. bundles that are demanded at a price vector but nowhere in the neighborhood of it, then weak FS and FS are equivalent. Formally this requirement is the following:

No Isolated Bundles (NIB): For each , and there is a with and

It is not generally true that, conversely, FS implies NIB (see Example 4 in Appendix A). However, CSC (SSS is not necessary here), LAD and LAS together imply NIB (see Proposition A.4 in Appendix A). This observation will be important for the proof of our main result, Theorem 1.∎

Next we show that for each utility function satisfying weak FS, weak LAD and weak LAS, we can construct a demand correspondence that satisfies FS, LAD and LAS by removing isolated bundles from the original demand. The resulting demand can be rationalized by a continuous and monotonic utility function. Put differently, we show that the two notions of Full Substitutability are almost equivalent in the following sense: for each utility function for which the induced demand satisfies weak FS, weak LAD, and weak LAS, there is a corresponding utility function for which the induced demand satisfies FS, LAD, and LAS, and such that selects from . The utility function can be chosen such that the induced indirect utility is the same. The result is proved in Appendix B.

Proposition 1.

Let satisfy weak FS, weak LAD, and weak LAS. Then there is a utility function that satisfies FS, LAD, and LAS such that the induced indirect utility functions are the same

and the induced demand is a selection from the original demand,

3 Results

3.1 The Lattice Theorem and the Rural Hospitals Theorem

As our first main result we establish that equilibrium prices in trading networks form a lattice and that (modulo indifferences) for each firm the difference between the number of signed upstream and downstream contracts is the same in each equilibrium. The join and meet are the coordinate-wise maximum and minimum of the two price vectors under consideration, i.e. the lattice is a sublattice of with the usual partial order. These results extend results established by Hatfield et al. (2013) for the case of quasi-linear utility functions.

In the following, a competitive equilibrium for utility profile is an arrangement such that for each and the demand induced by we have . We call the equilibrium allocation induced by We denote the set of equilibrium price vectors for by and define for each price vector the (possibly empty) set of sets of trades that support as a competitive equilibrium under .

Theorem 1.

Let be a utility profile such that for each firm the induced demand satisfies FS, LAD and LAS.

-

1.

Lattice Theorem: Let be equilibrium prices. Then defined by

are equilibrium prices.

-

2.

Rural Hospitals Theorem: Let be equilibrium prices. For each there exists a such that for each we have .

The proof and all subsequent proofs of this section are in Appendix C. However, for the moment we give a sketch of the proof strategy and comment on the challenges when generalizing from quasi-linear to more general preferences. Let be two equilibrium price vectors and consider the pairwise maximum (a dual argument works for the pairwise minimum ). Suppose for the moment that the demand for each firm is single-valued at and at , i.e. each firm has unique optimal bundles of trades and at the equilibrium prices and . For each firm let be a bundle demanded at . Full Substitutability for individual firms implies full substitutability for the aggregate demand so that we obtain

The equation states that there is no excess supply of trades at The laws of aggregate demand and supply, can be used to show that

Combining these two observations shows that the market clears, i.e.

and thus

Suppose now that we want to generalize the argument to the case of multi-valued demand at the equilibrium prices. A natural idea is to use a perturbation argument: Continuity and monotonicity of utility in transfers allows us (see Lemma 1) to perturb price vectors to obtain a single-valued selection from the demand correspondence at prices and .

Lemma 2.

Let be a utility function inducing a demand correspondence satisfying weak FS, weak LAD and weak LAS. Let be finite. Then there is a (single-valued) demand function that selects from , i.e. for and satisfies FS, LAD and LAS.

Once perturbed, the argument above could be applied to the perturbed price vectors. However, this line of argument has a flaw: There is no guarantee that the trades demanded at the perturbed prices support an equilibrium, since not every collection of demanded trades at an equilibrium price vector support these prices as an equilibrium. This problem would not occur under quasi-linear utility: for quasi-linear utility it is easy to show that the set of competitive equilibrium price vectors is convex. Thus, for quasi-linear utility either there is a unique equilibrium price vector, in which case the lattice result trivially holds, or there is in the neighborhood of each equilibrium price vector another equilibrium price vector at which demand is single-valued for each firm (since price vectors where demand is single-valued are dense in price space). For general utility functions, convexity and more generally connectedness of the set of equilibria can fail888This is already true for one-to-one matching with transfers which is a special case of our model. See the example in Roth and Sotomayor (1988). so that a perturbation argument might fail.

While a naive perturbation argument fails to work, we can use a more intricate perturbation argument. We perturb prices for each firm individually. Importantly, we can rely on the observation (recall Remark 3) that for each firm there are prices (in general different for different firms) close to where the equilibrium set of trades is the unique demanded bundle of trades. The following lemma is the main ingredient in the proof of the theorem.

Lemma 3.

Let be a utility function inducing a demand correspondence satisfying FS, LAD and LAS. Let and define by

Let and .

-

1.

There is a with

-

2.

There is a with

-

3.

and can be chosen such that

With the lemma the theorem follows straightforwardly. The lemma and the first part of the theorem fail to hold if we replace FS by weak FS, as the following example shows. A similar example shows that the second part of the theorem fails if LAD (LAS) is replaced by weak LAD (weak LAS), see Example 4 in Appendix C.

Example 1 (cont.).

Consider the set of trades and firm with the utility function as defined in Example 1. The induced demand satisfies weak FS as previously shown. Moreover, for each and we have . Thus satisfies LAD and LAS. Consider four additional firms with and . Define utility functions for the additional firms as follows: For define

Observe that the equilibria for are and for . In particular, the vector is not an equilibrium price vector, since and but . ∎

It is well-known that the theorem fails to hold without FS, even for quasi-linear utility functions. The following example shows that the first part of the theorem fails without LAD. More generally, the example shows that without LAD the set of equilibria can even fail to be a lattice with respect to the (weaker) partial ordering induced by terminal sellers’ preferences.

Example 2.

Let . Let for and for . We let for and . We define by

and else.

Consider the price vectors and . Note that and . Moreover, we have , and . Thus and are equilibrium price vectors. Suppose there is a that each terminal seller weakly prefers to and , i.e. , , and . Thus and . But then . Moreover, Thus, there is no such equilibrium price vector .

To check that satisfies FS, first note that for each , we have . Thus, at each we have and the only possible FS violation could occur for with and . However, if , then, as is increasing in and in for each , we have Thus, FS holds. ∎

3.2 Extremal equilibria

So far we have not considered whether competitive equilibria exist in our model and, in principle, the lattice in Theorem 1 could be empty. Next we show that under the additional assumption of bounded compensating variations, as introduced by Fleiner et al. (2019), side-optimal equilibria exist, i.e. there exist an equilibrium that is a most preferred equilibrium for all terminal buyers and an equilibrium that is a most preferred equilibrium for all terminal sellers.

Bounded compensating variations: The utility function of firm satisfies bounded compensating variations if for each we have

The condition rules out for example the case that for a trade the seller would never sell under any price and the buyer would buy under any price, by guaranteeing that utility for individually rational allocations is bounded for all agents. Fleiner et al. (2019) show that under the assumption of BCV, (weak) FS equilibria exist. We generalize the result by proving the existence of side-optimal equilibria:

Theorem 2 (Existence of Extremal Equilibria).

Under the assumption of BCV, FS, LAD, LAS, there exists a seller-optimal equilibrium, i.e. a such that for each terminal seller :

and a buyer-optimal equilibrium, i.e. a such that for each terminal buyer :

Remark 4.

Fleiner et al. (2019) also introduce a stronger regularity condition, called bounded willigness to pay (BWP), which guarantees that prices in individually rational allocations are bounded for all agents.

Bounded willingness to pay (BWP): The utility function satisfies bounded willingness to pay if there exists a such that for all and

if then and

if then .

The previous result also holds if BCV is replaced by BWP, and more generally one can show that in this case the set of equilibrium prices for realized trades is compact (see Proposition C.1 and its proof in the appendix).

Under the assumptions of (weak) FS and BWP, Fleiner et al. (2019) establish that equilibrium allocations are equivalent to trail-stable allocations. Thus, under BWP, FS, LAD, LAS there is a seller-optimal trail-stable allocation and a buyer-optimal trail-stable allocation. In the case of no frictions, BWP is implied by requiring, that and utility functions have full range: for each , , is a surjective function onto .

∎

3.3 Strategic Considerations

The existence of buyer-optimal equilibria established in Theorem 2, allows us to obtain a group-incentive compatibility result.999In the following we talk about incentives for terminal buyers. A completely analogous result also holds for terminal sellers. In the following, a domain of utility profiles is a set where is a set of (continuous and monotonic) utility functions for firm . A mechanism is a function . A mechanism is (weakly) group-strategy-proof for a set of workers on the domain if for each with , there exist a with

Theorem 2 allows us to define a class of focal mechanisms on the domain of utility profiles satisfying BCV, FS, LAD and LAS: a buyer-optimal mechanism maps to each utility profile a buyer-optimal equilibrium allocation.

To obtain a group-strategy-proofness results for terminal buyers for buyer-optimal mechanisms, we have to restrict the domain. In the following a unit demand utility function is a such that for the induced demand at each and we have .

Theorem 3 (Group-Strategy-Proofness).

Each buyer-optimal mechanism is group-strategy-proof for terminal buyers on the domain of utility profiles such that terminal buyers’ utility functions satisfy Unit Demand and BCV and all other firms’ utility functions satisfy BCV, FS, LAD and LAS.

In view of Proposition 1, we can extend the construction to profiles satisfying BCV, weak (!) FS, weak LAD and weak LAS. For each such profile there exists a corresponding profile satisfying BCV, FS, LAD and LAS such that the indirect utility functions are the same for both profiles. The mechanism that assigns to each profile a buyer-optimal equilibrium allocation under a corresponding profile is group-strategy-proof for terminal buyers (since for terminal buyers (and terminal sellers) the weak FS and the FS condition coincide), and the assigned allocations are equilibrium allocations under as well.

Corollary 1 (Group-Strategy-Proofness under weak FS).

On the domain of utility profiles such that terminal buyers’ utility functions satisfy Unit Demand and BCV and all other firms’ utility functions satisfy BCV, weak FS, weak LAD and weak LAS, there exists a group-strategy-proof mechanisms for terminal buyers that implements a competitive equilibrium.

4 Applications

4.1 Two-sided Matching Markets

The results in the previous sections immediately apply to two-sided matching markets. In this case, the results generalize previously known results for two-sided matching markets in two directions: we provide a lattice result, a rural hospitals theorem and a group-strategy-proofness result for markets with a) possibly non-quasi-linear preferences for both sides of the market b) the possibility that it is infeasible for a hospital to hire certain groups of doctors. As remarked in Section 2.1, the weak version of Full Substitutability is sufficient to obtain the results for two-sided markets.

Instead of a set of firms, the economy now consists of a finite set of hospitals and a finite set of doctors . Each hospital has a utility function that assigns to each and price vector a utility level. We extend to by letting . We allow the utility function to take on a value of to indicate that it is infeasible for the hospital to hire a particular group of doctors. This allows us for example to incorporate institutional constraints such as the “generalized interval constraints” characterized by Kojima et al. (2020b) which specify a lower and an upper bound on the number of doctors a hospital can hire. We assume that implies for each . We assume that there is at least one group of doctors that is feasible to hire, i.e. such that Moreover, we require that for , the utility function is continuous and strictly decreasing in prices. The utility function induces a demand correspondence by We assume that doctors are gross substitutes for hospitals. We only need to require the condition for price vectors where the demand is single-valued.

Weak Gross Substitutability:

For with and we have .

Moreover, we require the law of aggregate demand.

Law of Aggregate Demand:

For with and each there is a with .

Each doctor has a utility function that is strictly increasing and continuous in its second argument. We extend to by letting and .

A matching is a function with for each and for each such that if and only if A competitive equilibrium is a pair consisting of a matching , and a price vector such that for each and we have and for each and we have The following is an immediate consequence of Theorems 1, 2 and 3.

Corollary 2.

For each matching market such that doctors are weak gross substitutes for hospitals and the law of aggregate demand holds the following is true:

-

1.

Let be equilibrium prices. Then defined by

are equilibrium prices.

-

2.

Let be equilibrium prices. For each matching supporting as an equilibrium there is a matching supporting as an equilibrium such that

-

(a)

a doctor is unemployed in if and only if he is unemployed in , i.e. for each ,

-

(b)

each hospital hires the same number of doctors in and , i.e. for each

-

(a)

-

3.

If utility functions satisfy, moreover, BCV, then there exists a worker-optimal equilibrium allocation and a hospital-optimal equilibrium allocation.

-

4.

The worker-optimal mechanism is group-strategy-proof for workers on the domain of utility profiles such that workers’ utility functions satisfy Unit Supply and BCV and hospitals’ utility functions satisfy BCV, weak GS, and LAD.

Proof.

We can construct a corresponding trading network with and for and and if with . The weak gross substitutes condition then corresponds to the weak SSS condition (see Appendix A) which by Proposition A.1 in Appendix A is equivalent to the SSS condition. Since the market is two-sided, SSS and FS are equivalent. The corollary follows from Theorems 1, 2 and 3. ∎

4.2 Exchange economies with uniform pricing

Next, we apply the model to the exchange of indivisible objects. The result extend results of Gul and Stacchetti (1999) and Hatfield et al. (2013) (see the discussion in their Section IV.B) to imperfectly transferable utility. As in Gul and Stacchetti (1999), we maintain the assumption that the market is cleared through transfers of a perfectly divisible good and there is no constraint on the amount of the divisible good an agent can consume. Moreover, negative quantities of the divisible good can be consumed. However, we do not assume that utility in the divisible good is quasi-linear. Similar assumption are standard in the object allocation literature with general preferences, see for example Morimoto and Serizawa (2015).

In the following, we let be a finite set of heterogeneous indivisible objects. From now on, we use the term agents in lieu of firms. Agents have utility functions over bundles of objects and transfers, such that for each , is continuous, strictly increasing and has full range,101010This assumption is only necessary for the existence of side-optimal allocations and otherwise redundant. and for each and , we have . Each agent is endowed with a bundle of objects such that for and . An exchange economy is a pair of utility functions and endowments for each agent. We define for each a demand correspondence by

Remark 5.

In contrast to quasi-linear utility, the demand can differ with the endowment, i.e. in general for .∎

We assume that objects are gross substitutes for agents.

Gross Substitutability:

For with , if for , then for each there exists a such that , and if for , then for each there exists a , such that .

Moreover, we assume the law of aggregate demand:

Law of Aggregate Demand:

For with , if for , then for each there exists a , and if for , then for each there exists a , such that .

Remark 6.

We assume that there is only one copy of each object. Our results also hold true with multiple copies provided each agent can supply at most one unit of each indivisible object and wants to consume at most one unit of each indivisible object. We can deal with multi-unit supply of the same good by a seller and multi-unit demand of the same good by a buyer in our model, by creating identical copies of objects and price units individually. However, in this case, we will generally have non-linear pricing. For the case of multi-unit demand and supply with linear pricing, we would have to modify our model and the gross substitutability condition. For the quasi-linear case with multiple units of the same good, see Baldwin and Klemperer (2019) and in particular their ordinary substitutability condition.∎

An allocation of objects is a partition with and for . A competitive equilibrium of the exchange economy is a pair where is an allocation of objects and such that for each we have

For each exchange economy , a corresponding trading network can be defined as follows: The set of trades is

where for we have . We write for the object involved in trade . For and define

Utility functions are induced by utility functions over bundles of objects and transfers; for and we let

To apply the results from the previous sections, we also extend the utility functions to negative prices; for and we let

Remark 7.

Extending utility for negative prices in this way implies (see the proof of Lemma 4) that the induced demand satisfies FS on whenever it satisfies FS on . Moreover, is easy to see that for each with , is continuous (as is continuous on , and and are continuous) and monotonic on . This will allow us to apply the results from previous sections.

Equilibrium prices in the trading network are non-negative by our assumption that for and : Let and define . First note that for we have : Define by for and else. Note that . Thus, by monotonicity

As , all inequalities hold with equality, in particular, and therefore, by monotonicity, By a similar argument, if and , then . Thus, for there is excess demand and for each , we have for each . ∎

The gross substitutes condition for corresponds to the full substitutability condition for and the law of aggregate demand for implies the laws of aggregate demand and supply for .

Lemma 4.

If objects are gross substitutes under , then trades are full substitutes under . If the law of aggregate demand holds under , then the laws of aggregate demand and supply hold under .

In general, different trades involving the same object can be priced differently. In the following, we call a competitive equilibrium of the trading network with uniform pricing, if for , with we have . Trades in the same object are perfect substitutes to each other for the seller of the object, and he will sell the object to a buyer who is offering the highest price. Thus, we can always construct an equilibrium with uniform pricing from an equilibrium with non-uniform pricing by setting the price of the non-realized trades to the highest price for the involved object over all trades in the trading network. Similarly, a competitive equilibrium in the exchange economy, induces a competitive equilibrium with uniform pricing in the trading network. The following theorem can be interpreted as a generalization of Theorem 10 of Hatfield et al. (2013).

Proposition 2.

-

1.

If are equilibrium prices in the trading network induced by an exchange economy, then are equilibrium prices in the exchange economy.

-

2.

If are equilibrium prices in an exchange economy, then are equilibrium prices in the trading network induced by the exchange economy.

Proof.

Let be an equilibrium in the induced trading network. Let and consider the allocation in the exchange economy. By construction, we have for each and for . Thus

and is an equilibrium of the exchange economy.

For the second part, let be an equilibrium of the exchange economy. Define and consider the set of trades defined by

By construction, we have

Therefore is an equilibrium of the induced trading network. ∎

Proposition 2 and the previous results for trading networks imply the following:

Corollary 3.

Let be an exchange economy such that objects are gross substitutes for agents and the law of aggregate demand holds.

-

1.

Lattice Theorem: Let be equilibrium prices. Then the price vectors defined by

are equilibrium equilibrium prices.

-

2.

Rural Hospitals Theorem: Let be equilibrium prices. For each equilibrium there exists an assignment such that for each , i.e. consumes the same number of objects in and .

-

3.

Existence of Extremal equilibria: There exist equilibrium price vectors , such that for each equilibrium price vector and we have

Remark 8.

Throughout this section, we have made the assumption that utility depends on the total amount of the divisible good, but not on how transfers of the divisible good are obtained through different trades. For the induced trading network this means that utility satisfies the no frictions assumption. Frictions for individual trades in the trading network can lead to non-uniform pricing. Suppose for example that an agent is endowed with an object and faces different transactions costs depending on whom he is selling the object to. In this case, he might have an incentive to sell the object to a buyer who is offering a lower price, if transaction costs with this buyer are lower than with other buyers who offer a higher price. Thus, Proposition 2 can fail to hold in the presence of frictions. A slightly more general version of the theorem can be obtained, where it is assumed that utility is symmetric in transfers from different trades with the same objects, but transfers from trades with different objects can enter the utility asymmetrically. In this case, trades in different objects can contain different frictions, however, trades of the same objects are perfect substitutes for each other.∎

5 Conclusion

In this paper, we have established several structural results for the set of equilibria in trading networks with frictions, making only minimal assumption on utility functions. Quasi-linearity can be replaced by the assumption of monotonicity and continuity to establish the lattice structure for the set of equilibria, the rural hospitals theorems, the existence of buyer-optimal and seller-optimal equilibria, and a group-incentive-compatibility result. Our results are applicable to a wide range of situations where the assumption of quasi-linearity is unrealistic because of imperfectly transferable utility or the presence of frictions.

To prove the results we used a novel tie-breaking approach where for prices where demand is multi-valued we show that a well-behaved selection from the demand correspondence can be made. After ties are broken standard techniques can be applied to obtain the lattice theorem and the rural hospitals theorem. This motivates us to pose two open questions for future research: First, can results for the trading networks model without transfers as in Fleiner et al. (2016), generalize from strict preferences to preferences with ties?111111For marriage markets, the lattice result extends to the case with ties for strongly stable matchings Manlove (2002). A recent result by Hatfield et al. (2020) is very much in this spirit. The authors show that chain-stable and stable outcomes are equivalent for trading networks without making assumptions of monotonicity or continuity on utility functions. Hence their result applies to both trading networks with and without transfers.

Second, in the case of quasi-linear utility, corresponding results to ours can be obtained through solving a generalized network flow problem Candogan et al. (2016). The optimal solutions to the flow problem correspond to a competitive equilibrium outcome and its dual yields supporting prices. This generalizes the linear programming approach from one-to-one matching markets with quasi-linear utility Shapley and Shubik (1971). Recently, Nöldeke and Samuelson (2018) have shown that a more general non-linear duality theory can be used to obtain versions of the results of Demange and Gale (1985) that generalize Shapley and Shubik (1971) beyond quasi-linear utility. It seems unlikely that the approach generalizes to our full model with frictions. However, for the case of no frictions (in which case utility only depends on the sum of transfers and competitive equilibria are efficient), it is a natural question whether the duality approach to equilibria in trading networks generalizes beyond quasi-linear utility to obtain similar results as in the present paper through different techniques.

References

- Baldwin and Klemperer (2019) Baldwin, E. and Klemperer, P. (2019): “Understanding Preferences: “Demand Types”, and the Existence of Equilibrium With Indivisibilities.” Econometrica, 87(3): 867–932.

- Candogan et al. (2016) Candogan, O., Epitropou, M., and Vohra, R. V. (2016): “Competitive equilibrium and trading networks: A network flow approach.” In Proceedings of the 2016 ACM Conference on Economics and Computation, pages 701–702. ACM.

- Demange and Gale (1985) Demange, G. and Gale, D. (1985): “The Strategy Structure of Two-Sided Matching Markets.” Econometrica, 53: 873–888.

- Dupuy et al. (2017) Dupuy, A., Galichon, A., Jaffe, S., and Kominers, S. D. (2017): “Taxation in Matching Markets.”

- Fleiner (2003) Fleiner, T. (2003): “A Fixed-Point Approach to Stable Matchings and some Applications.” Mathematics of Operations Research, 28(1): 103–126.

- Fleiner et al. (2019) Fleiner, T., Jagadeesan, R., Jankó, Z., and Teytelboym, A. (2019): “Trading networks with frictions.” Econometrica, 87(5): 1633–1661.

- Fleiner et al. (2016) Fleiner, T., Jankó, Z., Tamura, A., and Teytelboym, A. (2016): “Trading Networks with Bilateral Contracts.”

- Galichon et al. (2019) Galichon, A., Kominers, S. D., and Weber, S. (2019): “Costly Concessions: An Empirical Framework for Matching with Imperfectly Transferable Utility.” Journal of Political Economy, 127(6): 2875–2925.

- Gul and Stacchetti (1999) Gul, F. and Stacchetti, E. (1999): “Walrasian Equilibrium with Gross Substitutes.” Journal of Economic Theory, 87(1): 95–124.

- Hatfield et al. (2014) Hatfield, J. W., Kojima, F., and Kominers, S. D. (2014): “Investment Incentives in Labor Market Matching.” American Economic Review, 104(5): 436–41.

- Hatfield and Kominers (2012) Hatfield, J. W. and Kominers, S. D. (2012): “Matching in networks with bilateral contracts.” American Economic Journal: Microeconomics, 4(1): 176––208.

- Hatfield et al. (2013) Hatfield, J. W., Kominers, S. D., Nichifor, A., Ostrovsky, M., and Westkamp, A. (2013): “Stability and competitive equilibrium in trading networks.” Journal of Political Economy, 121(5): 966–1005.

- Hatfield et al. (2019) Hatfield, J. W., Kominers, S. D., Nichifor, A., Ostrovsky, M., and Westkamp, A. (2019): “Full Substitutability.” Theoretical Economics, 14(4): 1535–1590.

- Hatfield et al. (2020) Hatfield, J. W., Kominers, S. D., Nichifor, A., Ostrovsky, M., and Westkamp, A. (2020): “Chain Stability in Trading Networks.” Theoretical Economics, forthcoming.

- Hatfield and Milgrom (2005) Hatfield, J. W. and Milgrom, P. R. (2005): “Matching with Contracts.” American Economic Review, 95(4): 913–935.

- Jagadeesan et al. (2018) Jagadeesan, R., Kominers, S. D., and Rheingans-Yoo, R. (2018): “Strategy-proofness of worker-optimal matching with continuously transferable utility.” Games and Economic Behavior, 108: 287 – 294.

- Kelso and Crawford (1982) Kelso, A. and Crawford, V. P. (1982): “Job Matching, Coalition Formation, and Gross Substitutes.” Econometrica, 50(6): 1483–1504.

- Kojima et al. (2020a) Kojima, F., Sun, N., and Yu, N. N. (2020a): “Job Market Interventions.”

- Kojima et al. (2020b) Kojima, F., Sun, N., and Yu, N. N. (2020b): “Job Matching under Constraints.” American Economic Review, forthcoming.

- Legros and Newman (2007) Legros, P. and Newman, A. F. (2007): “Beauty is a beast, frog is a prince: Assortative matching with nontransferabilities.” Econometrica, 75(4): 1073–1102.

- Manlove (2002) Manlove, D. F. (2002): “The structure of stable marriage with indifference.” Discrete Applied Mathematics, 122(1-3): 167–181.

- Morimoto and Serizawa (2015) Morimoto, S. and Serizawa, S. (2015): “Strategy-proofness and efficiency with non-quasi-linear preferences: A characterization of minimum price Walrasian rule.” Theoretical Economics, 10(2): 445–487.

- Nöldeke and Samuelson (2018) Nöldeke, G. and Samuelson, L. (2018): “The Implementation Duality.” Econometrica, 86(4): 1283–1324.

- Ostrovsky (2008) Ostrovsky, M. (2008): “Stability in supply chain networks.” American Economic Review, 98(3): 897––923.

- Roth (1984) Roth, A. E. (1984): “Stability and Polarization of Interests in Job Matching.” Econometrica, 52(1): 47–57.

- Roth and Sotomayor (1988) Roth, A. E. and Sotomayor, M. (1988): “Interior Points in the Core of Two-Sided Matching Markets.” Journal of Economic Theory, 45(1): 85–101.

- Schlegel (2018) Schlegel, J. C. (2018): “Group-Strategy-Proof and Stable Mechanisms for Matching Markets with Continuous Transfers.”

- Shapley and Shubik (1971) Shapley, L. S. and Shubik, M. (1971): “The Assignment Game I: The Core.” International Journal of Game Theory, 1(1): 111–130.

- Sun and Yang (2006) Sun, N. and Yang, Z. (2006): “Equilibria and Indivisibilities: Gross Substitutes and Complements.” Econometrica, 74(5): 1385–1402.

- Vohra (2011) Vohra, R. V. (2011): Mechanism design: a linear programming approach, volume 47. Cambridge University Press.

- Zhou (1994) Zhou, L. (1994): “The Set of Nash Equilibria of a Supermodular Game is a Complete Lattice.” Games and Economic Behavior, 7(2): 295–300.

Appendix A Different Versions of Full Substitutability

Contraction Full Substitutability

In Appendix A of Hatfield et al. (2019), the authors introduce the contraction and expansion version of full substitutability that differ in regard to how they are defined at price vectors where the demand is multi-valued. Note that full substitutability relates the demand at two price vectors and . If for and for respectively if for and and , then the choice set expands from to , and it contracts from to . The contraction version of full substitutability requires that “for all there is a such that…” whereas the expansion version inverts the order of quantification and requires that “for all there is a such that…” We further split full substituability into same-side substitutability (SSS) and cross-side complementarity (CSC) and the laws of aggregate demand and supply, all of which are implied by all versions of full substitutability in the quasi-linear case. We use the expansion version of SSS as our main definition. Alternatively, we can consider the contraction version.

Contraction Same-Side Substitutability: For and each there exists a such that if for and for , then

and if for and for , then

We have previously introduced weak FS that can be further decomposed into weak SSS and weak CSC.

Weak Same-Side Substitutability: For such that and if for and for , then

and if for and for , then

All three notions of SSS, the weak, the contraction version, as well as the expansion version that we use as our main definition are equivalent under quasi-linear utility Hatfield et al. (2019). For general utility functions, the weak version and the expansion version of SSS remain equivalent (by a result of Fleiner et al., 2019 in their Appendix A121212More precisely, Contraction SSS is the conjunction of the two properties that Fleiner et al. (2019) denote by “decreasing-price full substitutability for sales (in demand language)” and “increasing-price full substitutability for purchases in (demand language)”.) but the contraction version of SSS is strictly stronger than the expansion version. See Example 3 after the following proposition.

Proposition A.1 (Hatfield et al., 2019; Fleiner et al., 2019).

Let be a monotonic and continuous utility function with induced demand .

-

1.

satisfies weak SSS if and only if it satisfies (Expansion) SSS.

-

2.

If satisfies Contraction SSS then it satisfies weak SSS.

-

3.

If is quasi-linear and satisfies weak SSS, then satisfies Contraction SSS.

Example 3.

Consider three trades with . We let , for , for and

Observe that

but

As , Contraction SSS would require that there is a with . Hence Contraction SSS is not satisfied. As the demand at and is multi-valued, Weak SSS does not impose any structure here. More generally, note that if we replace by the quasi-linear utility functions such that for all and remains otherwise unchanged, only the demand at prices changes. One readily checks that satisfies (Weak) SSS. Hence satisfies Weak SSS. ∎

Similarly as for Same-Side Substitutabilty, we can define an alternative version of Cross-Side Complementarity.

Contraction Cross-Side Complementarity: For each there exists a such if for and for , then

and if for and for , then

As before, we also define a weak version of CSC that together with Weak SSS defines Weak FS.

Weak Cross-Side Complementarity: For each with and such if for and for , then

and if for and for , then

Similarly as for SSS, the weak, the contraction version as well as the expansion version of CSC that we use as our main definition are equivalent under quasi-linear utility Hatfield et al. (2019). For general utility functions, the weak version and the contraction version of CSC remain equivalent (by a result of Fleiner et al., 2019 in their Appendix A131313More precisely, Contraction SSS is the conjunction of the two properties that Fleiner et al. (2019) denote “increasing-price full substitutability for sales (in demand language)” and “decreasing-price full substitutability for purchases (in demand language)”.) but the contraction version of SSS is strictly stronger than the expansion version (see Example 1 in the main text).

Proposition A.2 (Hatfield et al., 2019; Fleiner et al., 2019).

Let be a monotonic and continuous utility function with induced demand .

-

1.

satisfies weak CSC if and only if it satisfies Contraction CSC.

-

2.

If satisfies (Expansion) CSC then it satisfies Weak CSC.

-

3.

If is quasi-linear and satisfies Weak CSC, then satisfies (Expansion) CSC.

Monotone Substitutability, No Isolated Bundles, and Single Improvements

Following the terminology of Hatfield et al. (2020), we denote by monotone substitutability, the property that the FS, LAD, and LAS hold jointly for the same bundles of trades.141414Note that we use the (weaker) demand-language version rather than the choice-language definition of the property used by Hatfield et al. (2020).

Monotone Substitutability: For and each there exists a such that if for and for , then

and if for and for , then

If there are no isolated bundles, weak FS and FS are equivalent, and the combination of weak FS, weak LAD and weak LAS is equivalent to Monotonone Substitutability.

Proposition A.3.

Let be a continuous and monotonic utility function inducing a demand .

-

1.

If satisfies NIB and weak FS then it satisfies FS.

-

2.

If satisfies NIB, weak FS, weak LAD and weak LAS, then it satisfies Monotone Substitutability.

Proof.

Let such that for and for . Let . By upper hemi-continuity there exists an such that for we have . By NIB, there is a with and . Let . By construction and therefore By upper hemi-continuity there exists an such that for with we have . We may choose . By the second part of Lemma 1, there exists a with such that demand is single-valued, for a . As, , we have . Let . As , we have . By construction, we have and . Since for and for , this implies for and for . By weak FS applied to the vectors and and the fact that demand at both price vectors is single-valued with and we obtain

If, moreover, weak LAD holds, then

A completely analogous argument shows the second part of the FS, resp. of the Monotone Substitutability property. ∎

The converse of the first part of the proposition is not true, as the following example shows.

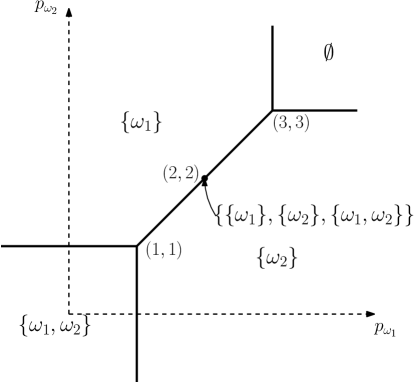

Example 4.

Consider two trades with . We let , for , and

See Figure 1 for a geometric representation of the demand in the example.

The induced demand violates NIB, since but for with Moreover, it violates LAD at and, e.g., since but . One readily checks that satisfies FS and weak LAD. ∎

The converse of the second part of Proposition A.3 is true, and more generally the following holds:

Proposition A.4.

Let be a continuous and monotonic utility function inducing a demand satisfying CSC, LAD and LAS. Then satisfies NIB.

Proof.

Let and . We show that for each there is a with such that . Let First, consider a vector with such that for , for , and for By monotonicity of , for each with we have , and we have . Thus, and . By upper hemi-continuity, there is a such that for with we have We may choose By the second part of Lemma 1, there is a with such that demand is single-valued, , and we may choose it such that for and for We show that for the unique with we have . An analogous argument shows that .

Let with for and for . By the first part of the CSC condition applied to vectors (in the role of ) and (in the role of ), there is a such that . Since , we have . Thus, and, by the previous observation that , we have By LAS applied to prices (in the role of ) and (in the role of ) we have

| (1) |

Since , we have . Thus, and, by the previous observation that , we have Together with Inequality (1) this implies . By the second part of the CSC condition applied to prices (in the role of ) and (in the role of ) we have Together with the previous inequality this implies Furthermore, together with Inequality (1), this implies and, as , we have As observed previously, . Together with the previous inequality this implies

∎

Hatfield et al. (2020) do not assume continuity of utility functions for their main result, and in that case, monotone substitutability is generally a stronger property than the combination of FS, LAD and LAS. With continuity, however, it follows as a corollary from the previous propositions that the conditions are equivalent.

Corollary A.1.

Let be a continuous and monotonic utility function inducing a demand satisfying FS, LAD and LAS. Then satisfies FS, LAD, and LAS if and only if satisfies Monotone Substitutability.

Proof.

In the context of object allocation with quasi-linear preferences, Gul and Stacchetti (1999) show that gross substitutability is equivalent to a ”single improvement property”: If the price of an object increases, and previously a bundle of objects has been demanded, while now a bundle of objects is demanded, then and , i.e. at most one new object is added to the demand and at most one object is no longer demanded. We can prove a (partial) generalization of the result to general utility functions. The proof uses the following lemma which will also be useful subsequently.

Lemma A.1.

Let be a continuous and monotonic utility function inducing a demand correspondence . For each and with for , for , for and for .

-

1.

If satisfies weak FS, weak LAD and weak LAS, then implies .

-

2.

If satisfies FS, LAD and LAS, then implies .

Proof.

We first prove the first part. Let satisfy weak FS, weak LAD and weak LAS and . By monotonicity of it is without loss of generality to assume that for . By upper hemi-continuity of , it suffices to show that for each there is a with such that By upper hemi-continuity of there is a such that for with we have . Define such that

By the second part of Lemma 1, there is a with and a such that . By upper hemi-continuity of there is a such that for we have We may choose . By the second part of Lemma 1, there is a with and a such that . Let and . By construction we have . Thus . By construction, we have and therefore Applying the weak FS, condition to vector and (note that by construction we have for ) we have and . Applying the weak LAD this implies . Applying the weak FS, condition to vector and (note that by construction we have for ) we have and . Applying the weak LAS this implies . Thus as desired.

The second part of the lemma follows from the first as follows: By Proposition A.4, there is for each a with such that . By the first part of the lemma applied to vectors and we have . Thus for each there is a with and . Thus, by upper hemi-continuity,

∎

Proposition A.5 (Single Improvement Property).

Let be a continuous and monotonic utility function inducing a demand satisfying FS, LAD and LAS. Let such that there is a with and , or a with and . Then for each there exists a such that

Proof.

We show the result for and . A dual argument establishes the result for and . Let . If , then by Lemma A.1 we may choose . If , then by monotone substitutability (which holds by Corollary A.1), there is a such that , , and . The inequality can be rearranged to The condition that implies , whereas the condition implies . Thus

Since , if , then , and if , then or for . Since , if , then for an , and if , then . In conclusion, if , then for an , if , then , and if , then or for . In either case, we have

∎

Appendix B Proof of Proposition 1

Proof.

We first define the demand and show that it is a selection from . Then we rationalize it by a continuous and monotonic utility function that induces the same indirect utility. Afterwards we show that it satisfies FS, LAD and LAS.

For each , consider the (possibly empty) set of price vectors such that is the unique demanded bundle at :

Let be the (topological) closure of . We let

By upper hemi-continuity of , for each and we have . Thus for each .

Claim 1.

For each , let be the projection of to and its (topological) closure. Then there is a continuous and monotonic utility function such that

| (2) | ||||

| (3) |

Proof of Claim 1.

Denote for each by the distance from to . We define

Suppose . The function is continuous since is continuous and the distance to a set in is continuous. Moreover, with equality if and only if Thus and hold. It remain to show that is monotonic. Let with such that for and for (an analogous argument works for downstream trades). For each there is such that . Let such that . Let and define by for and for . Since we have and thus, by the first part of Lemma A.1, we have . More generally, by upper hemi-continuity of there is a such that for each with we have . Thus, by the first part of Lemma A.1, for each with we have . By the second part of Lemma 1, this implies that for each there is a with . Therefore . Thus, . Since this holds for any we have . Thus,

∎

Claim 2 implies that can be rationalized by a continuous and monotonic utility function that induces the same indirect utility: By the second part of Lemma 1, for each there is a with . Since we have and therefore . Next we show that rationalizes by showing that for and for . Let . If , then and . Since we have and thus . If and , then . If , then we show and thus : By definition of we have . Thus, there is a such that for each with we have . Let such that and for , for and for . Since and is monotonic, we have . By Lemma 1, we can find a such that for we have . Now suppose for the sake of contradiction that . Then, there is a such that . Since , we have and thus, in particular, for each . Now define by for and for By construction, we have . Thus . Moreover, for each . Thus and . However, and therefore , a contradiction.

Next we show that that satisfies FS, LAD and LAS. By Proposition A.3 it suffices to show that satisfies NIB, weak FS, weak LAD and weak LAS. Let . Since is the closure of there is for each and a with . By definition of and we have . Thus satisfies NIB. For the other properties, recall that satisfies weak FS, weak LAD and weak LAS. Thus, it suffices to show that for each we have if and only if Let with . If , then . If , i.e. if is on the boundary of , then for each there is a with . By the second part of Lemma 1, we may choose such that . Since is finite, this implies that there is a such that for each there is a with and . Thus for . Hence . Thus, if and only if as desired.

∎

Appendix C Proofs for Section 3

Proof of Lemma 2

Proof.

By Lemma 1, there exists an such that for each and every with we have . Let . By Lemma 1, there is a with such that and for the unique . Consider . For each we have . By Lemma 1, there exists an such that for each and every with we have . By Lemma 1, there is a with such that and for the unique . Next consider . For each we have and so on. Iterating in this way, we obtain such that for each , we have and for the unique . We define . By construction . Moreover, as all price vectors are translated by the same vector , FS, LAD and LAS follow from weak FS, weak LAD and weak LAS for . ∎

Proof of Lemma 3

Proof.

By Lemma 1, there exists an such that for each and every with we have . Let such that and Define by

Note that by construction we have and thus . First we prove the following claim.

Claim 2.

For each we have and .

Proof.

First we show that for each we have . Suppose not, and there is a and a . Let with and for . By the second part of Lemma A.1, we have . Thus, by monotonicity, we have contradicting the assumption that .

Next we show that for each we have . Suppose not, and there is a and a . Let with and for . By the second part of Lemma A.1, we have . Thus, by monotonicity, we have contradicting the assumption that .∎

By Lemma 1, there exists such that for every with we have . We may choose . By Proposition A.4, there is a with such that Define Define as the pairwise maximum of and , i.e. , and as the pairwise minimum of and , i.e. .

By construction, we have , we have and thus , and we have and thus . Moreover, by construction, if and only if , if and only if , and if and only if .

Let . By Lemma 2, there is a single-valued selection from satisfying FS, LAD and LAS. Let and . As , we have . Moreover, by Claim 2 and as , we have and . By FS of and since , we have

Next we show that

Let . We consider two cases. Either or . In the first case, consider with for and for . Let By SSS of , we have . By CSC, we have and hence .

Similarly, if , consider with for and for . Let By SSS of we have . By CSC, we have and hence . Since and this implies . A completely analogous proof shows that has the desired properties. Finally, by LAD and LAS for , we have

∎

Proof of Theorem 1

Proof.

Let and . Define

We show that and . Let . By Lemma 3, with and there is a and a such that , , and and

Note that this implies

Summing the inequalities over all firms, we obtain

Thus

Therefore for each . Moreover,

Therefore for each .

Next we show that the above construction implies the rural hospital theorem: As and , for each we have

Summing the inequalities over all , we obtain

Thus, for each we have

Next define the set of trades

Since and , the same argument as before with in the role of , and in the role of establishes (note that the pairwise minimum of and is again ) that is an equilibrium. Moreover, with the same argument as before for each we have

Since

this concludes the proof. ∎

Example for the Failure of the Rural Hospitals Theorem without LAD

Example 4 (cont.).

Consider the set of trades and firm with the utility function as defined in Example 4. As observed before, satisfies FS, weak LAD, (and, trivially, LAS), but not LAD. Consider a second firm with with utility function defined by

The induced demand satisfies FS and LAS (and, trivially, LAD). The set of equilibrium vectors is . Each is supported by and by . The equilibrium prices are supported by . An analogous example can be constructed to show that LAS and not just weak LAS is necessary for the Rural Hospitals Theorem. ∎

Proof of Theorem 2

We first show that the result holds for utility functions satisfying BWP.

Proposition C.1.

Under the assumption of BWP, FS, LAD, LAS, there exists a seller-optimal equilibrium, i.e. a such that for each terminal seller :

and a buyer-optimal equilibrium, i.e. a such that for each terminal buyer :

Proof.

Following an idea of Kelso and Crawford (1982), we can characterize competitive equilibria by a zero-surplus condition. Define a surplus function by

By definition, for each , we have Thus for each arrangement , we have with equality if and only if . Thus if and only if The surplus function is continuous, as is continuous in and the maximum resp. minimum of finitely many continuous functions is continuous. Thus is a closed set, as it is the pre-image of the closed set under the continuous function .

By BWP, there is a such that for all , and if then and if then . Let . By BWP, for each , the vector defined by for , for , and for is an equilibrium price vector with for each . By Corollary 2 in Fleiner et al. (2019), is non-empty and hence is non-empty. As is closed, is compact. From Theorem 1, and observing that the pairwise maximum (minimum) of two vectors in is an element of , we conclude that is a non-empty, compact sublattice of . This implies that has a maximal element and a minimal element By monotonicity and the previous observation that for each there is a with for each , for each terminal seller and we have . Thus is a terminal seller optimal equilibrium. Similarly, is a terminal buyer optimal equilibrium under . ∎