∎

University of Queensland, Brisbane

22email: t.taimre@uq.edu.au 33institutetext: P. J. Laub 44institutetext: The University of Queensland, Brisbane &

Aarhus University, Aarhus

44email: p.laub@[uq.edu.aumath.au.dk]

Rare tail approximation using asymptotics and polar coordinates

Abstract

In this work, we propose a class of importance sampling (IS) estimators for estimating the right tail probability of a sum of continuous random variables based on a change of variables to polar coordinates in which the radial and angular components of the IS distribution are considered separately.

When the asymptotic behaviour of the sum is known we exploit it for the radial change of measure, and the resulting estimator has the appealing form of the (known) asymptotic multiplied by a random multiplicative correction factor. Given we assume knowledge of the asymptotic behaviour of the sum in this framework, traditional notions of efficiency that appear in the rare-event literature hold little practical meaning here. Instead, we focus on the practical behaviour of the proposed estimator in the pre-asymptotic regime for right tail probabilities between roughly and .

The proposed estimator and procedure are applicable in both the heavy- and light-tailed settings, as well as for independent and dependent summands. In the case of independent summands, we find that our estimator compares favourably with exponential tilting (iid light-tailed summands) and the Asmussen–Kroese method (independent subexponential summands).

However, for dependent subexponential summands using the same simple angular distribution as for the independent case, the performance of our estimator rapidly degenerates with increasing dimension, suggesting an open avenue for further research.

1 Introduction

A typical problem in the field of rare-event estimation is to determine the probability

| (1) |

where for a random vector with fixed having joint probability density function (pdf) and where the is large or increasing. In applications, we often wish to understand the behaviour of a combination of random factors, and hence the random variable (r.v.) is ubiquitous in real-world modeling problems. It can model, for example: aggregate risk or portfolio value for holding risky assets mcneil2015quantitative ; Rueschendorf2013 , the aggregate losses for insurance policy claims asmussen2010ruin ; klugman2012loss , or the combined signal interference from wireless transmission sources fischione2007approximation . Probabilities of the form (1) are used to understand how a system would behave under extreme scenarios such as a market crash, a power surge, or a natural disaster. One is typically interested not just in the quantity but also in the behaviour of the summands when the extreme event occurs.

This probability is available in closed-form for only a few basic cases, when the density of (which is a -fold convolution) has a known solution, c.f. nadarajah2008review . For example, when the summands are independent and identically distributed (iid) then it is sometimes simple to calculate (for example exponential, gamma, or normal summands, and in the discrete case binomial, geometric, or negative binomial summands) and sometimes it is still intractable (for example lognormal, Weibull, Laplace, or Beta summands). However, requiring the assumption of independence (let alone iid-ness) of the summands is a stifling restriction when modeling real-world events; a notorious example would be the partial blame of the 2008–9 global financial crisis on mathematicians’ inappropriate use of a simplistic dependence model (the Gaussian copula) salmon2009recipe .

When analytical solutions are unavailable, the next best option is numerical integration, and after that Monte Carlo integration (or quasi-Monte Carlo). Numerical integration algorithms applied to

where denotes the indicator of an event (taking value 1 if occurs and 0 otherwise), are typically slow, inaccurate, and misleading. This is because the indicator is rarely 1, floating-point errors accumulate, and the curse of dimensionality applies for larger than about 2 or 3. Some of these algorithms attempt to estimate the error in their result, but there are few (if any) theoretical guarantees that these estimates are reliable.

Rare-event problems also cause difficulties for the crude Monte Carlo (CMC) estimator. This is obvious as the CMC estimator’s relative error explodes for large — that is, the CMC estimator has

Intuitively, the problem is because the indicator is eventually always 0 when gets very large. In response, various variance reduction techniques have been applied so that there are now a large collection of estimators with better performance in this setting, c.f. ‘rare-event estimation’ in kroese2013handbook ; asmussen2007stochastic ; glasserman2003monte .

There is, of course, no silver bullet for the problem. Some estimators only apply to specific distributions (e.g. botev2017fast for sums of lognormals, yao2016estimating for sums of phase-type mixtures) or to certain classes of distributions (exponential tilting for light-tailed summands kroese2013handbook ; asmussen2007stochastic , hazard-rate twisting or the Asmussen–Kroese method asmussen2006improved for heavy-tailed summands). Other estimators are general but require specifying either some extra information (e.g. availability of conditional distributions for conditional Monte Carlo asmussen2017conditional , or an appropriate sampling distribution for use in importance sampling). The most general estimators — such as the generalised splitting method, cross-entropy method, or Markov Chain Monte Carlo (MCMC) methods such as chan2012improved — are usually computationally demanding, they often depend upon an intelligent selection of input parameters to perform efficiently, and are somewhat complicated.

Whilst one rarely has an exact expression for , it is somewhat common to know an asymptotic approximation to it, and this forms the basis for our proposed estimator. For example, if where and is positive definite (by which we mean that component-wise, where has a multivariate normal distribution with mean vector and covariance matrix ), then it has been shown that asmussen2008asymptotics

| (2) |

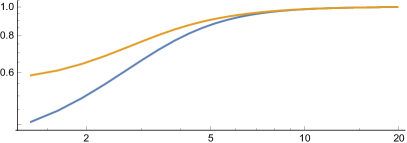

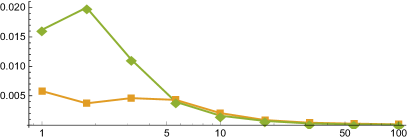

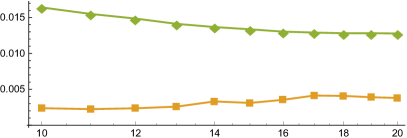

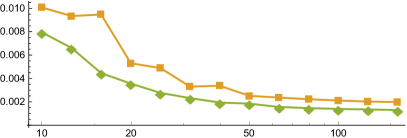

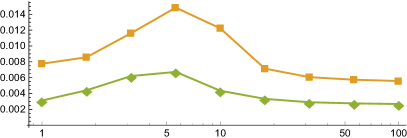

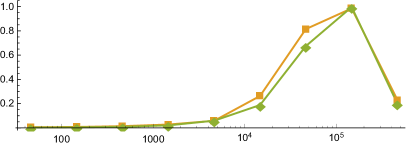

where denotes . Thus, one is tempted to label the right-hand side (RHS) of (2) as and use it as an approximation for . For certain values of this asymptotic approximation can be accurate, in others it can be wildly inaccurate, depending on how fast the asymptotic approximation converges to the true value; see Figure 1 for an illustration where it is only when that the asymptotic form begins to give accurate estimates (i.e., ). A discussion of this phenomenon is in botev2017fast .

We propose an importance sampling (IS) estimator which incorporates the asymptotic approximation and uses Monte Carlo sampling to estimate a correction to in order to construct an unbiased estimator of . The main drawback to IS is likelihood degeneration, where one can face numerical errors if or is extremely large. The degeneration caused by a large is only partially compensated by our approach, so we take . To mitigate degeneration for large , we focus our attention of values of which are moderately large but not unrealistically so. Our goal is to provide an estimator which is practically useful when is between roughly and .

The range of probabilities that we consider are unusual as they are less rare than much of the standard rare-event literature. The orthodox approach is to construct an estimator and analyse the limit

if the limit is small (i.e., zero, bounded, or at least grows only at a polynomial rate) then the estimator is branded as a success (it has ‘vanishing relative error’, ‘bounded relative error’, or is ‘logarithmically efficient’ respectively) regardless of its behaviour in the finite situation. It can happen that these desirable limiting properties are only discernible in cases when the probabilities are truly minuscule (e.g. of order or smaller); in a situation such as this, the model error would surely dominate any estimation error.

2 The polar estimator

2.1 The general form

We construct an estimator of the quantity , where for large by applying IS. Standard IS theory says to construct an estimator which samples from a distribution close to (that is, the distribution of conditioned on ), rather than the original . To do this, we perform a change of variables to Pickand’s coordinates FalkReiss2005 so

The new density is available (if is known), and is

Consider IS in this new form. Imagine that we have a density which is in some way similar to , for which we also know the marginal density and the conditional density . If we truncate so that a.s., and use this as the IS distribution, we obtain

| (3) |

for , , where we define and .

We investigate estimators of the general form of (3) which we call () polar estimators. These are accurate when closely resembles . This is carried out in two steps: (i) by finding a radial approximation which approximates , and (ii) an angular approximation similar to , which we discuss in the following sections.

2.2 The radial approximation

As mentioned in the introduction, we consider utilising an asymptotic form of the sum in our estimator — they form our radial approximation. To clarify the notation, we precisely define the relevant asymptotic forms:

Definition 1 (Asymptotic form)

If for some function , with tail , and constant , we have that

| (4) |

then we say is an asymptotic form of .

Thus, in the general form (3) we will use when it is available and is a proper pdf. There are some technicalities for the cases when does not form a proper pdf which we defer from discussing in this work. The estimator resulting from this radial approximation is

| (5) |

for and .

Remark 1

Define a “correction factor” to the asymptotic form, , by ; note that . We can see that has a nice interpretation, because

where is an unbiased Monte Carlo estimate of the factor .

The recent applied probability literature has found the for a staggering array of distributions of . Perhaps the simplest case is when the are iid subexponential random variables. By definition (cf. foss2011introduction ), they satisfy

| (6) |

For sums of independent non-identically distributed (ind) subexponential variables (or for sums containing some subexponential and some lighter-tailed variables) we have

| (7) |

where is the set of indices of slowest tail decay. The asymptotics in (7) also hold in many regimes where dependence has been introduced, cf. foss2010sums ; wuthrich2003asymptotic ; alink2004diversification ; alink2007diversification .

A distribution can satisfy a stronger property called regular variation which implies subexponentiality and hence the asymptotics above. Examples of regularly varying distributions are Cauchy, Fréchet, and Pareto distributions bingham1989regular . The lognormal and heavy-tailed Weibull distributions are subexponential but not regularly varying.

The Weibull distribution is interesting as it is a family which can be heavy-tailed, light-tailed (the Rayleigh distribution is a special case), or on the boundary between these (i.e. the exponential distribution). The asymptotic form for the heavy-tailed Weibull sum is covered by (6) and (7) as the summands are subexponential. The difficulty in finding the asymptotics for the light-tailed case led the authors to investigate it in detail, leading to the paper asmussen2017tail which uses results originally from balkema1993densities .

Proposition 1

Assume that are iid light-tailed where , , . Then

for .

The exposition in asmussen2017tail details this and more general asymptotics (i.e. the independent but non-identically distributed case, and when the variables are not exactly Weibull but are ‘Weibull-like’).

By its very construction, one would expect the estimator utilising an asymptotic form for the right-tail, (5), to enjoy good efficiency properties as . As mentioned in the introduction, our goal is to provide a practically useful estimator for ‘moderately’ rare problems, in the range of before the asymptotic regime takes hold. As such, it is our view that the orthodox notions of efficiency have little meaning in our setting. Nevertheless, we note that it is straightforward to verify that if the ratio remains bounded by some finite constant for all as , then the estimator (5) enjoys bounded relative error, and if then the estimator enjoys vanishing relative error.

2.3 The angular approximation

The choice of angular approximation is not as obvious as was the choice of radial approximation. Finding a conditional density which is similar to has little precedent in the literature.

Instead of taking an which is larger than and asking ‘what is the distribution of given this ?’, we can instead ask ‘what is the distribution of given ?’. This is the same situation that is studied in multivariate extreme value theory, where the spectral density characterises the behaviour of in the limit as deHaanResnick1977 . This second conditional distribution will resemble the first in cases that converges quickly to zero when becomes large. Moreover, we have a computation benefit to finding a which is similar to as this distribution will be constant across all Monte Carlo iterates, in contrast to and .

Nevertheless, when it is possible, we follow the same approach as the radial approximation and utilise some asymptotic information. However, we note that if one simply re-uses the previous asymptotic form, that is

which may appear natural, then the estimator (5) degenerates to the deterministic

Moreover, if it is known that degenerates in the limit [e.g. to a point mass at in each coordinate (perfect extremal dependence) or is degenerate on axes (independence in the extreme)], this does not tell us what we should do for finite .

Indeed, when the summands are iid subexponentials, then the distribution of as degenerates to a discrete distribution over the -dimensional unit vectors , …, (with having a single 1 in the -th coordinate and zeros in all other coordinates). This is just a re-casting of the principle of the single big jump (cf. foss2011introduction ). Unfortunately, for finite we cannot use this directly as in this case the likelihood ratio appearing in (3) is not well defined. One density, which we call the optimistic density (see the algorithm below), that is not degenerate (and therefore will have well-defined likelihood ratio) but is asymptotically equivalent to for the case of ind subexponential summands is

| (8) |

where and denote the -dimensional vectors obtained from and by removing the elements in -th coordinates ( and , respectively), and the functions are defined by

| (9) |

Algorithm 1 shows a method for sampling from this , and Proposition 2 shows that it has limiting distribution consistent with (7) as .

When the subexponential summands are only independent in the extreme, a simple generalisation of Algorithm 1 is to replace Lines 3 to 5 with taking a random sample from .

Proposition 2

Proof

Remark 2

The polar estimator for ind subexponential summands with the optimistic angular approximation (8) simplifies to

where , , and is the harmonic mean of the inputs.

The conditional angular asymptotic distribution is more challenging to obtain in the case of light-tailed summands. The following example shows these distributions differ qualitatively when different copulas are considered.

Example 1

Consider and to be Exp(1) variables which are: i) independent, ii) Clayton(1) dependent, or iii) Ali-Mikhail-Haq(-1) dependent. The sum densities can be calculated explicitly and are given by

respectively. Hence, for and , we have angular densities

respectively. It is interesting to note that the asymptotic independence of the Clayton copula would indicate that as which is indeed the case. In contrast, degenerates to a pair of atoms at 0 and 1 as .

One (light-tailed) case where we can determine an asymptotic angular distribution is for light-tailed Weibull sums. The angular asymptotic can be extracted from the results in asmussen2017tail , and appears as follows.

Proposition 3

Say are iid and are distributed as light-tailed with survival function where , . Define the vector function component-wise by

where . Then as we have

where .

Note that the -dimensional multivariate normal distribution appearing in Proposition 3 is supported on a -dimensional subspace.

When the asymptotic angular approximation is unavailable, there are several conceivable alternatives. One can select a from some family of distributions which has the appropriate support. For instance, if has non-negative components, then the support of is the simplex . To the authors’ knowledge, the only commonly known distribution over is the Dirichlet distribution, and appears to be a natural candidate.

In some experiments carried out while writing this paper, we sampled using MCMC, then used the maximum likelihood Dirichlet fit to the samples as an angular approximation in the polar estimator. Unfortunately the results were disappointing and are omitted — the Dirichlet distribution struggles to fit the multimodal angular distributions which are characteristic of subexponential sums conditioned on taking large values. We also attempted the MCMC flavour of the cross-entropy method as outlined by Chan and Kroese chan2012improved , though the multimodality led to extremely high variance estimates (relative to the much simpler Asmussen–Kroese method).

We also performed an approximation of the angular density using Bernstein polynomials. The angular density , so it is easy to calculate quantities which are proportional to the desired conditional density. Using Bernstein polynomials effectively constructed an approximation which was a mixture of Dirichlet distributions using these unnormalised angular density values. The results for these experiments are also omitted, since the number of mixture components required to create an accurate approximation easily becomes prohibitively large (then, the computation time for evaluating the pdf of the mixture becomes a bottleneck).

3 Results

In this section we give illustrative results of numerical experiments. For subexponential summands, we compare to the most competitive alternative, the Asmussen–Kroese estimator, and for light-tailed summands we compare to the standard IS approach of exponential tilting. In what follows, we adopt Mathematica’s parameterisations for the lognormal, Pareto, and Weibull distributions. The code we used is available online PolarCode .

3.1 Subexponential Summands

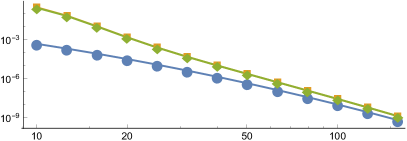

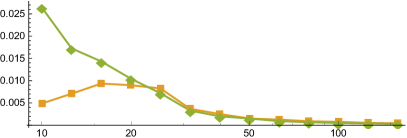

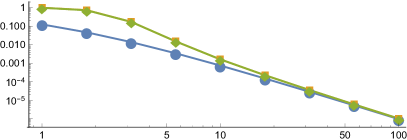

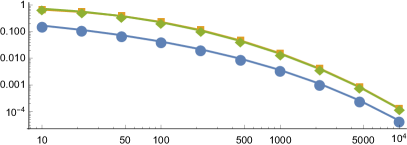

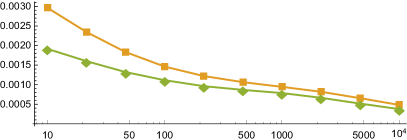

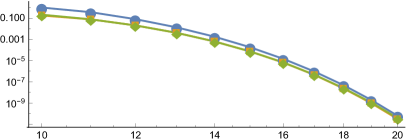

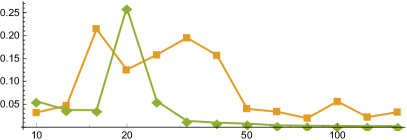

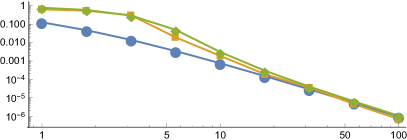

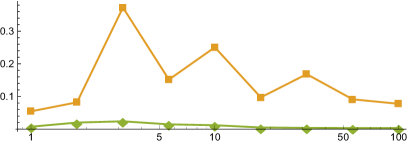

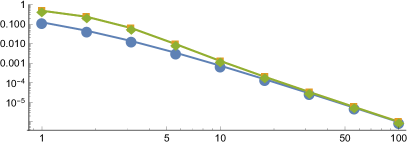

Below we present the estimates and the estimated relative errors for the polar estimator and the Asmussen–Kroese estimator for various distributions of . Each estimator is given iid samples of .

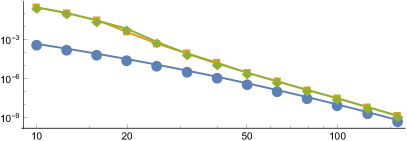

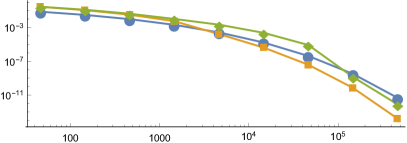

The first test (Figs. 2 and 3) takes the sum of independent lognormal random variables, with marginal distributions . Here, the sum behaves asymptotically as the dominant term , and the optimistic angular distribution is used.

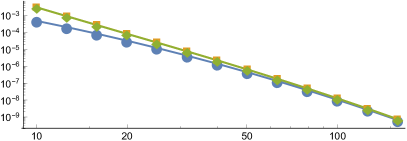

The second test (Figs. 4 and 5) considers the sum of independent Pareto random variables, where . The sum behaves asymptotically as the dominant term , and the optimistic angular distribution is used.

The third test (Figs. 6 and 7) considers the sum of independent heavy-tailed Weibull variables. The marginal distributions are . The sum behaves asymptotically as the last summand , and the optimistic angular distribution is used.

3.2 Light-tailed Weibull Summands

This fourth test (Figs. 8 and 9) takes the sum of iid light-tailed Weibulls, where . An asymptotic survival function for the sum is given by Proposition 1, and the optimistic angular distribution used is from Proposition 3. Instead of the Asmussen–Kroese method, which is designed for subexponential summands, we have compared the polar estimator against exponential tilting. The exponential tilting method is usually easy to implement but it takes some effort in this situation. Simulating each exponentially tilted Weibull variable is done via acceptance–rejection; the proposals come from the gamma distribution which is moment-matched to the asymptotic normal approximation for the exponentially tilted Weibull distribution, cf. Section 6 of asmussen2017tail .

3.3 Dependent Summands

Next we reproduce the three subexponential tests above with dependence added by Archimedean copulas. We use the Asmussen–Kroese estimator as outlined in Section 3.2.2.2 of nandayapa2008risk as the traditional form of this estimator needs to be adapted for the case of dependent summands.

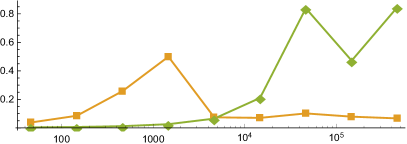

The fifth test (Figs. 10 and 11) recreates the first test, with lognormal variables and marginals , except dependence is added via a copula.

We see immediately that introducing even a mild level of dependence gives rise to substantially more variability in the polar estimator in the pre-asymptotic regime as a result of using the optimistic angular distribution — an illustration of likelihood ratio degeneracy in . To illustrate this point, we carry out the same test with in Figs. 12 and 13.

The seventh test (Figs. 14 and 15) is similar to the second test above, considering Pareto random variables where , except that the summands exhibit dependence via a copula.

Once again, we observe significant likelihood ratio degeneracy in the polar estimator, and for comparison we repeat the experiment with in Figs. 16 and 17.

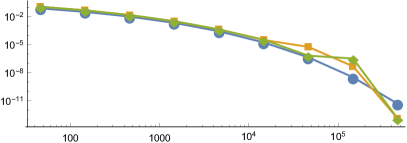

Test nine (Figs. 18 and 19) is similar to the third test, with heavy-tailed Weibull variables with marginal distributions , except with a copula (which is dependent in the extreme).

As one would expect, as increases, both estimators behave increasingly poorly due to the upper-tail dependence of this copula. We repeat the experiment in Figs. 20 and 21 with to more clearly illustrate this phenomenon.

4 Conclusion

On the tests carried out in this work, our estimator appears to perform on par with the Asmussen–Kroese method for independent subexponential summands, and outperforms all the other methods compared against (i.e. the improved cross-entropy method, fitting mixtures of Dirichlet variables, and Bernstein polynomial approximation).

Moreover, for the comparison of iid light-tailed Weibull summands, our estimator outperforms exponential tilting.

However, with the introduction of dependence for subexponential summands (even with upper-tail independence of the copula) the performance of our estimator degrades rapidly as dimension increases (likelihood ratio degeneracy) as a consequence of utilising the optimistic angular distribution, and unsurprisingly performs poorly when the copula has upper-tail dependence. Thus there remains the opportunity for further research into suitable choice of the angular distribution in the case of dependent summands.

Acknowledgements.

This work was supported under the Australian Research Council’s Discovery Projects funding scheme (DP180101602). Also, PJL was supported by an Australian Government Research Training Program Scholarship and by the Australian Research Council Centre of Excellence for Mathematical & Statistical Frontiers (ACEMS), under grant number CE140100049.References

- (1) Alink, S., Löwe, M., Wüthrich, M.V.: Diversification of aggregate dependent risks. Insurance: Mathematics and Economics 35(1), 77–95 (2004)

- (2) Alink, S., Löwe, M., Wüthrich, M.V.: Diversification for general copula dependence. Statistica Neerlandica 61(4), 446–465 (2007)

- (3) Asmussen, S.: Conditional Monte Carlo for sums, with applications to insurance and finance. Annals of Actuarial Science (2017). Submitted, available from thiele.au.dk/publications

- (4) Asmussen, S., Albrecher, H.: Ruin probabilities, Advanced Series on Statistical Science and Applied Probability, vol. 14, 2 edn. World Scientific Publishing Co Pte Ltd, River Edge, NJ (2010). DOI 10.1142/9789814282536. URL http://dx.doi.org/10.1142/9789814282536. Advanced series on statistical science & applied probability; v. 14

- (5) Asmussen, S., Glynn, P.W.: Stochastic Simulation: Algorithms and Analysis, Stochastic Modelling and Applied Probability series, vol. 57. Springer (2007)

- (6) Asmussen, S., Hashorva, E., Laub, P.J., Taimre, T.: Tail asymptotics for light-tailed Weibull-like sums. Probability and Mathematical Statistics 37(2) (2017)

- (7) Asmussen, S., Kroese, D.P.: Improved algorithms for rare event simulation with heavy tails. Advances in Applied Probability 38(2), 545–558 (2006)

- (8) Asmussen, S., Rojas-Nandayapa, L.: Asymptotics of sums of lognormal random variables with Gaussian copula. Statistics & Probability Letters 78(16), 2709–2714 (2008)

- (9) Balkema, A.A., Klüppelberg, C., Resnick, S.I.: Densities with Gaussian tails. Proceedings of the London Mathematical Society 3(3), 568–588 (1993)

- (10) Bingham, N.H., Goldie, C.M., Teugels, J.L.: Regular Variation, Encyclopedia of Mathematics and its Applications, vol. 27. Cambridge university press, Cambridge (1989)

- (11) Botev, Z., Salomone, R., MacKinlay, D.: Fast and accurate computation of the distribution of sums of dependent log-normals. arXiv preprint arXiv:1705.03196 (2017)

- (12) Chan, J.C., Kroese, D.P.: Improved cross-entropy method for estimation. Statistics and Computing 22(5), 1031–1040 (2012)

- (13) De Haan, L., Resnick, S.I.: Limit theory for multivariate sample extremes. Zeitschrift für Wahrschein-lichkeitstheorie und verwandte Gebiete 40, 317–377 (1977)

- (14) Falk, M., Reiss, R.D.: On Pickands coordinates in arbitrary dimensions. Journal of Multivariate Analysis 92(2), 426–453 (2005)

- (15) Fischione, C., Graziosi, F., Santucci, F.: Approximation for a sum of on-off lognormal processes with wireless applications. IEEE Transactions on Communications 55(10), 1984–1993 (2007)

- (16) Foss, S., Korshunov, D., Zachary, S.: An Introduction to Heavy-tailed and Subexponential Distributions, vol. 6, 2 edn. Springer (2013)

- (17) Foss, S., Richards, A.: On sums of conditionally independent subexponential random variables. Mathematics of Operations Research 35(1), 102–119 (2010)

- (18) Glasserman, P.: Monte Carlo Methods in Financial Engineering, Stochastic Modelling and Applied Probability series, vol. 53. Springer (2003)

- (19) Klugman, S.A., Panjer, H.H., Willmot, G.E.: Loss models: from data to decisions, vol. 715. John Wiley & Sons (2012)

- (20) Kroese, D.P., Taimre, T., Botev, Z.I.: Handbook of Monte Carlo Methods, vol. 706. John Wiley & Sons (2013)

- (21) McNeil, A.J., Frey, R., Embrechts, P.: Quantitative Risk Management: Concepts, Techniques and Tools, 2nd edn. Princeton University Press (2015)

- (22) Nadarajah, S.: A review of results on sums of random variables. Acta Applicandae Mathematicae 103(2), 131–140 (2008)

- (23) Nandayapa, L.R.: Risk probabilities: asymptotics and simulation. Ph.D. thesis, University of Aarhus, Department of Mathematical Sciences (2008)

- (24) Rüschendorf, L.: Mathematical Risk Analysis. Springer (2013)

- (25) Salmon, F.: Recipe for disaster: The formula that killed Wall Street (2009). Online 23/02/2009

- (26) Taimre, T., Laub, P.J.: Online accompaniment for “Rare tail approximation using asymptotics and polar coordinates” (2018). Available at https://github.com/Pat-Laub/PolarRareTailApproximation

- (27) Wüthrich, M.V.: Asymptotic value-at-risk estimates for sums of dependent random variables. Astin Bulletin 33(01), 75–92 (2003)

- (28) Yao, H., Rojas-Nandayapa, L., Taimre, T.: Estimating tail probabilities of random sums of infinite mixtures of phase-type distributions. In: Proceedings of the 2016 Winter Simulation Conference, pp. 347–358. IEEE Press (2016)